© 2011 Beyond Philosophy 1

Customer Experience Management Management Implications Report

Global Customer Experience Management Survey 2011

Steven Walden Senior Head of Research and Consulting

Beyond Philosophy

180 Piccadilly London UK W1J 9HG T: +44 (0) 207 917 1717 F: +44 (0) 207 439 0262

1360 Center Drive, Suite 110 Atlanta, Georgia 30338 USA T: +1 (770) 206-5280 F: +1 (770) 206-5289

www.beyondphilosophy.com

© 2011 Beyond Philosophy 2

Abstract Between May and July 2011, Beyond Philosophy undertook a comprehensive review of

the state of the global market for customer experience management (CEM). This was

based on a sample of 8,000 customer experience (CE) executives from 239 countries

and regions of the world, as well as in-depth interviews of 53 leading authorities on

customer experience from all continents.

A webinar outlining the results can be found at:

http://www.beyondphilosophy.com/thought-leadership/webinars/customer-

experience-strategies-innovation-and-best-practices-around-worl

Management Implications report

CEM is standing at the crossroads of success and failure. It has succeeded in spreading

globally as a term, but has been inadequately adopted beyond a few verticals. Further,

in most cases, adoption means adoption of the term, not the application. Indeed CEM is

under threat of collapse due to software vendors’ use of CEM as a rebrand for CRM in

order to sell more software, on the top of an ‘everything is important now’ mentality. This

approach has unfortunately diluted the inherent value and message of customer

experience.

Yet drivers to its success remain particularly with increasing customer empowerment.

For instance, in the high growth BRICKS and Middle East region, expectations are rising

through engagement with the ‘developed’ world, social media and the growth of middle

class incomes, as well as the increasing demands of the wealthy elite for international

brands.

What is required now is a clear recognition that customer experience is different, that it’s

not just a rebrand, but in fact a transformational business strategy different from

marketing or customer service.

© 2011 Beyond Philosophy 3

It is essentially:

1. An organizing principle tying together silos such as marketing and customer

service that are failing to keep up with customer demand in an increasingly

complex multi-channel environment.

2. A cultural mind-set, keeping a customer focus in the organization when it is under

threat of being lost under a data deluge.

3. A means to focus and embed positive psychology into the customer journey (i.e.,

not just focus on the 4 Ps of marketing or physical interactions, but the

psychology of the consumer, their emotional as well as rational response).

This report summarizes the implications for management from the findings of the Global

Customer Experience Research 2011. Faced with the rebranding of CRM, marketing,

customer service and other initiatives as CEM, Beyond Philosophy calls for a

fundamental rethink of how customer experience management is being applied in firms;

in particular, whether CEM is an organizational effort to get closer to clients and

customers, and whether emotions are a fundamental part of ‘the experiences’ those

firms evoke.

© 2011 Beyond Philosophy 4

Contents Abstract 2

Executive Summary 6

1.0 Methodology 9

1.1 Quantitative 9

1.2 Qualitative 9

1.3 Sample 10

2.0 Five Major Risks 13

2.1 Use of the Term as a Rebrand for Current Operations 13

2.2 Risk 2: Misappropriation of the Term for Vendor Sales 16

2.3 Risk 3: Failure to Take Account of the Customer’s Emotional Viewpoint

(e.g. in ROI)

18

2.4 Risk 4: Limitations in its Adoption 20

2.5 Risk 5: Timeframe to Execute 22

3.0 A Strategy to Manage Risk 24

4.0 Five Major Drivers 28

4.1 Major Driver 1: Increasing Need to Respond to Customer Empowerment 29

4.1.1 10 Customer Empowerment Drivers 29

4.2 Major Driver 2: Increasing Need to Manage Organizational Complexity 32

4.3 Major Driver 3: Increased Awareness on the Importance of Emotion and how this

Translates into Loyalty Gains

35

4.3.1 Translation of Emotion into Loyalty 38

4.4 Major Driver 4: Move from Product-Based to Service-Based Organizations 40

4.5 Major Driver 5: Web Experience 41

5.0 A Final View 43

Contacts 47

© 2011 Beyond Philosophy 5

Figures and Tables

Table 1: Distribution of the 53 in-depth interviews including by title 10

Table 2: Summary distribution of the 53 in-depth interviews by regional percentage 11

Figure 1: Distribution of the 53 in-depth interviews by sector 12

Figure 2: Distribution of 53 expert interviews by industry 12

Table 3: What is the one question you would like answered about CEM? 13

Table 4: Examples of how CEM is being used badly 15

Table 5: How emotion is measured 19

Figure 3: Key areas of a CE implementation 24

Figure 4: Processes need emotional grounding 26

Figure 5: Culture and governance before process 27

Figure 6: The need to demonstrate proof of concept 27

Table 6: Resolution of risks 28

Figure 7: The path to enlightenment 43

Figure 8: First and second generation enlightenment 44

Figure 9: Rejuvenation or die 45

Figure 10: Make sure you are fit for purpose 46

© 2011 Beyond Philosophy 6

Executive Summary

What are the Five Major Risks?

I. Risk 1: Use of the term as a rebrand for current operations - Customer experience is

a well-used term as demonstrated by the global spread of executives with CE in their

titles. However, there is a disparity between use of the term and the actual

implementation of a CE program.

II. Risk 2: Misappropriation of the term for vendor sales - Another risk is the active

misappropriation of the term ‘customer experience’ by some vendors as a front for

rebranding CRM as CEM in order to sell more solutions.

III. Risk 3: Failure to take account of the customer’s emotional viewpoint e.g., in ROI -

Customer experience tends to follow a touch point definition. This is quite a

defensive position to take.

IV. Risk 4: Limitation in its adoption - Beyond Philosophy concludes that the term

customer experience has achieved global acceptance. However, this acceptance is

limited to a few key verticals: telecommunications, banking, retail and several of the

smaller sectors with increasing adoption in aviation, motor and insurance.

V. Risk 5: Timeframe to execute - One of the major problems with CE is that it depends

on the long-term. Its economic basis around loyalty is all about long-term return; its

advantages in terms of being more customer-centric also require levels of corporate

transformation that take years to realize.

What is the strategy to manage these risks?

VI. To avoid the risks companies have to realise that at its heart customer experience is

an organizational strategy based upon a holistic approach to the customer, using

emotion as a key differentiator. This means embedding from the very start the

message that this is a transformational approach, not just one based on tinkering

with the IT infrastructure, adapting call centers or measuring numerous touch points.

These may be part of a solution but they are not CE

What are the 5 Major Drivers?

VII. Major Driver 1: Increasing need to respond to customer empowerment - Customer

experience management used to be driven mainly by concerns over

© 2011 Beyond Philosophy 7

commoditization: CE, in effect, being used as a means for differentiation. However, a

new key driver - customer empowerment - has come to the fore globally. This makes

CE a necessity rather than an option:

a. The 10 customer empowerment drivers are: social media; fast society;

burgeoning middle class; development of high value segments; demand for

international brands; deregulation of markets; increased travel; regulation in

favor of the customer; cultural sensitivity and web aggregator sites.

VIII. Major Driver 2: Increasing need to manage organizational complexity - Customer

experience management is mainly, but not exclusively, a phenomenon of

multinational corporations. Faced with a proliferation of multiple channels, increasing

complexity in terms of IT infrastructure and expansion into new territories, the current

siloed structure of organizations is facing breakdown. With marketing focused on the

four Ps of marketing, customer service focused on service delivery and IT focused

on the web infrastructure, there is a problem of control and communication. This

failure leads to breakage points.

IX. Major Driver 3: Increasing awareness of the importance of emotion and how this

translates into loyalty gains - The way of operating marketing has changed from one

focused on the four Ps to one that increasingly looks at emotion as a platform for

differentiation. In part, this is driven by the commoditization challenge, but also by the

evidence from neuroscience and advanced research, that emotions drive behavior.

X. Major Driver 4: Move from product-based to service-based organizations - In

general, the focus of CE is on verticals with a high customer facing base. These are

industries that would have used the term customer service but now use customer

experience instead. Less apparent have been the B2B industries. However, as many

product based organizations face margin collapse with commoditization, so they will

look to CE as a means to target and develop new service-related propositions. Here,

the ability to manage relationships will be uppermost as the space for differentiation

along product lines declines. This is a trend focused on new wave customer

experience verticals in the B2B space (e.g. manufacturing, logistics, construction and

as current B2C providers integrate CE into their supply chains).

XI. Major Driver 5: Web Experience- The focus on Web enablement is allowing

companies in less mature regions to leapfrog a technology and play on a more even

playing field with the more mature countries. Indeed, in some cases the Web

experience is deemed of greater importance (e.g. Brazil).

© 2011 Beyond Philosophy 8

A Final View

XII. Growth in CE is intimately linked to organizational consciousness of the customer.

This is why some sectors such as telecoms ‘get it.’ There is nowhere to hide, while

others often in B2B are behind the curve. With increasing push from regulation and

pull from commoditization, Beyond Philosophy sees an increasing number of firms

becoming conscious of the need to organize themselves toward the customer.

XIII. In the current market, those sectors coming from a low base (such as

manufacturing); facing fast innovation (such as e-tail) and regulatory push (such as

healthcare) will experience the highest growth. However, there is a comprehensive

need even in the first generation to reconsider what customer experience is (i.e., are

you really doing it?).

XIV. It is no good taking a defensive position around measuring touch points or

rebranding service and research. Organizations need to ensure they ‘truly’ consider

the meaning of customer experience based on its founding notions of organizational

redesign and an emotional commitment to loyalty.

XV. It seems for now CE is standing at a crossroads between success and failure. The

message should be ‘rejuvenate or die.’

XVI. Companies that have emotions inside understand the customer experience far better

than those that assume customers are always rational. With an emotional

understanding, firms are better able to control complexity through customer action,

rather than more controlling measurements.

© 2011 Beyond Philosophy 9

1.0 Methodology

1.1 Quantitative

Beyond Philosophy undertook an analysis of 8,000 customer experience executives.

These executives were sourced from a country-by-country LinkedIn search; comprising

in-depth analysis of 239 countries and regions (i.e., the globe as defined by LinkedIn and

Google drop-down country/ region search list).

To qualify for inclusion, the LinkedIn respondents had to have ‘customer experience’ in

their ‘current’ job title: note that as a networking tool and to maximize coverage of

possible LinkedIn contacts, all main customer experience groups were joined. Likewise,

the search was conducted from a well-networked customer experience consulting group

(LinkedIn contacts were not used for marketing purposes, purely as a means of

research).

In addition, Beyond Philosophy conducted a Google search for firms that apply customer

experience across each of the 239 country and region web pages. In this search,

Beyond Philosophy set specific criteria for acceptance as a CE focused firm. Companies

had to have an active presence in customer experience ‘within the last year’ and ‘within

the country pages’. This was to avoid the presence of non-active firms that engaged in

customer experience over one year ago.

2,106 companies were identified as active in customer experience management

from around the world. This equates to an average of approximately 4 CE

executives per company.

1.2 Qualitative

From the quantitative database, Beyond Philosophy sourced 53 experts with whom to

conduct in-depth interviews on the topic of customer experience. Experts had to have

either overall line responsibility for managing customer experience on-the-ground (lead

PM) or be at CxO level (i.e., director or VP of customer experience). In addition, CE

experts were sourced (i.e., individuals who had deep regional or vertical understanding

of CE and were recognised experts in customer experience).

© 2011 Beyond Philosophy 10

All depth interviews were conducted by phone; excluding one interview that involved a

face-to-face meeting: Interviews typically lasted 20-25 minutes.

1.3 Sample Beyond Philosophy interviewed 53 experts from around the world. These were

distributed by job title (table 1) and by region (table 2).

Table 1: Distribution of the 53 in-depth interviews, including by title

Source: 53 CE professionals

Note: Experts can be general all round or by specific industry

Region Country Number Percent CE Expert CxO Lead PM

NAM USA 8 15% 1 7

NAM Canada 2 4% 1 1

CARIB Bahamas 1 2% 1

SAM Brazil 2 4% 2

SAM Peru 1 2% 1

EUW UK 9 17% 1 6 2

EUW Netherlands 1 2% 1

EUW France 1 2% 1

EUW Portugal 1 2% 1

EUW Switzerland 1 2% 1

EUW Belgium 1 2% 1

EUE Poland 1 2% 1

RUS Russia 3 6% 3

RUS Azerbaijan 1 2% 1

ME Saudi Arabia 3 6% 2 1

ME UEA 1 2% 1

ME Turkey 1 2% 1

AFR Nigeria 2 4% 1 1

AFR Kenya 1 2% 1

AFR South Africa 1 2% 1

IND India 3 6% 2 1

SEA Singapore 2 4% 1 1

SEA Indonesia 1 2% 1

CHI China 2 4% 1 1

AUST Australia 2 4% 1 1

AUST New Zealand 1 2% 1

Total 53 16 25 12

Total% 100% 30% 47% 23%

© 2011 Beyond Philosophy 11

Table 2: Summary distribution of the 53 in-depth interviews by regional percentage

Source: 53 CE professionals

Note: NAM (North America): CARIB (Caribbean); SAM (South America); EUW (Western Europe); EUE

(Eastern Europe); RUS (Russia); ME (Middle East); AFR (Africa); IND (India); SEA (South-East Asia); CHI

(China); AUS (Australia).

The two tables above demonstrate the broad spread of interviews geographically. All

continents were represented in the sample to ensure its global exposure. This dispersal

is disclosed in figure 1:

Region Total%

EUW 26%

NAM 19%

ME 9%

RUS 8%

AFR 8%

SAM 6%

IND 6%

SEA 6%

AUS 6%

CHI 4%

CARIB 2%

EUE 2%

Total 100%

© 2011 Beyond Philosophy 12

Figure 1: Distribution of the 53 in-depth interviews by sector

Source: 53 CE professionals

Figure 2: Distribution of 53 expert interviews by industry

Source: 53 CE professionals

Figure 2 shows the industrial distribution of interviewees: these are focused on banking

and telecommunications. However, a broad cross-section of other industries was chosen

alongside CE experts.

Banking, 19%

Insurance, 9%

Telcommunications, 23%

Outsourcing, 2%Manufacturing, 6%

Retail, 6%

Car, 6%Utilities, 2%

Construction, 2%

Charity, 2%

Logistics, 2%

Healthcare, 2%

Oil, 2%

Experts , 19%

© 2011 Beyond Philosophy 13

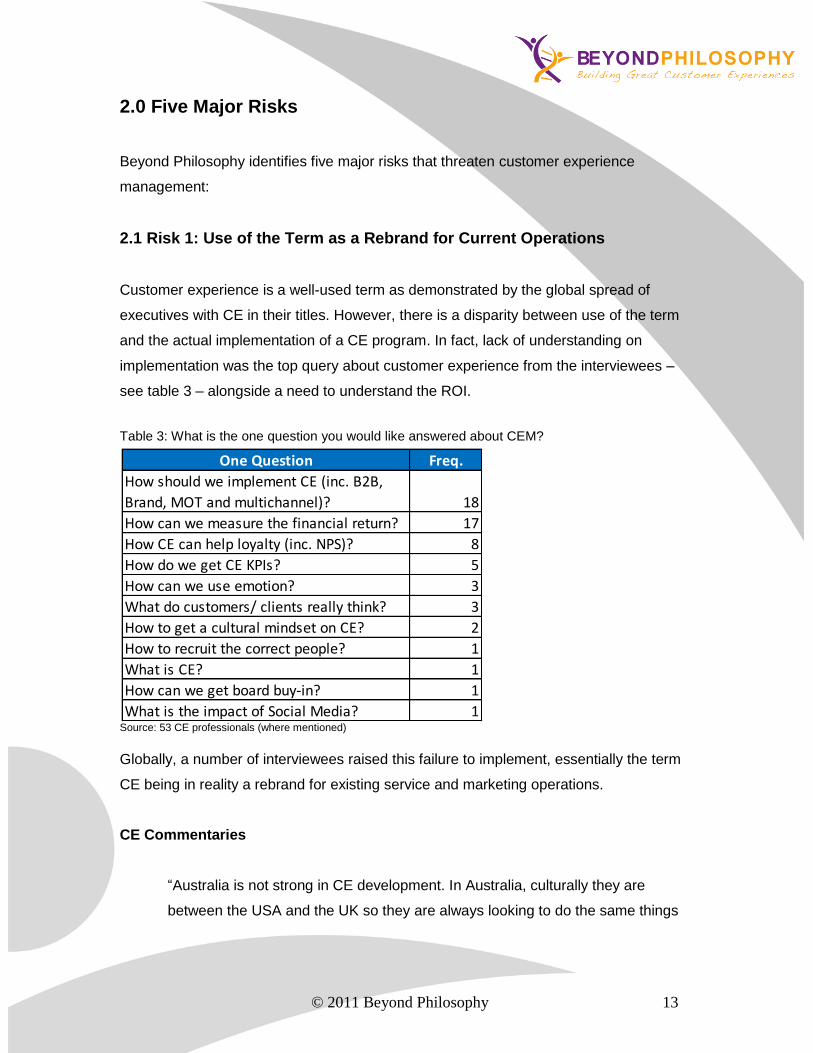

2.0 Five Major Risks

Beyond Philosophy identifies five major risks that threaten customer experience

management:

2.1 Risk 1: Use of the Term as a Rebrand for Current Operations

Customer experience is a well-used term as demonstrated by the global spread of

executives with CE in their titles. However, there is a disparity between use of the term

and the actual implementation of a CE program. In fact, lack of understanding on

implementation was the top query about customer experience from the interviewees –

see table 3 – alongside a need to understand the ROI.

Table 3: What is the one question you would like answered about CEM?

Source: 53 CE professionals (where mentioned)

Globally, a number of interviewees raised this failure to implement, essentially the term

CE being in reality a rebrand for existing service and marketing operations.

CE Commentaries

“Australia is not strong in CE development. In Australia, culturally they are

between the USA and the UK so they are always looking to do the same things

One Question Freq.

How should we implement CE (inc. B2B,

Brand, MOT and multichannel)? 18

How can we measure the financial return? 17

How CE can help loyalty (inc. NPS)? 8

How do we get CE KPIs? 5

How can we use emotion? 3

What do customers/ clients really think? 3

How to get a cultural mindset on CE? 2

How to recruit the correct people? 1

What is CE? 1

How can we get board buy-in? 1

What is the impact of Social Media? 1

© 2011 Beyond Philosophy 14

but that does not mean they do it; they get the title but still do standard marketing

things.” (Expert, Australia)

“In China it’s basically training, improving customer service, bringing a culture

and a philosophy to organizations. They have heard about Singapore and want

to embark on a strategy, then implementation. The type of work is not that

advanced in China, but would be quick to take off. A lot of people are speaking

the language.” (Expert, China)

“You can see increasingly job adverts with customer experience tutors, and the

term CX is mentioned more frequently in business and job descriptions. But there

is no common understanding of what it really is about.” (Banking Expert,

Switzerland)

“But here there is a degree of immaturity in thinking and understanding, so they

go for usability or marketing. We have a usability lab, a design agency and lots of

awareness: others think it is customer service.” (Banking CxO, Singapore)

“There is major confusion between customer service (i.e., bounded by customer

service departments) so CE=CS. The other one is confusion with user

experience, so things about web, user interface, design and uxp. Techies think

user experience, business professionals think customer service - here it

becomes survey tools, workforce automation, all stuff related to the contact

center use (as they worry about CSAT).” (Expert, UK)

“Scores only three out of seven, it is only key when it is seen to help our

business, the rest is just lip service.” (Financial Services CxO, USA)

Table 4 gives an example of the way in which the term is being used as a rebrand – in

this case for customer service. This has been taken from markets not core to CEM, but

demonstrates how it is being misinterpreted through vendor spread.

© 2011 Beyond Philosophy 15

Table 4: Examples of how CE is being used badly

Source: Company websites

Here, what is being spoken about is IT infrastructure enablement of contact center

operations. Likewise, contact center human enablements are described by Afghan

Global Insurance: "The claims team becomes active and acts efficiently and swiftly

toward its settlement. This is part of our endeavour to make the AGI customer

experience always a positive one."

Management advice: ensure that you have a clear plan for implementing CEM and

that it is understood as doing something different than what you do today. If you

find yourself without a roadmap and without an understanding of what CEM

means, then you are not doing CEM.

Company Vendor Area Solution Claim Fact

Bhutan Telecom Avaya

Business collaboration

systems, software and

services

Unified Communications,

Contact Centers, Desktop Level

Video Conferencing and Data

Networking solutons

"Enable Bhutan to have an end-to-

end customer experience

management approach"

Customer Contact

Centre solution with

help-desk support and

management

Enabling

infrastructure

Saudi Telecom Aegis Outsourcer

Aegis to manage entire call

customer care operations

including billing, directory

enquiry, collection and

verification

"We are confident Aegis would

provide a great level of satisfaction

given their vast experience in

managing customer experience

across multiple geographies"

Contact Center

management

Enabling

infrastructure

© 2011 Beyond Philosophy 16

2.2 Risk 2: Misappropriation of the Term for Vendor Sales

Another risk is the active misappropriation of the term ‘customer experience’ by some

vendors as a front for rebranding CRM as CEM in order to sell more solutions that

purportedly enable “complete visibility into customer interactions, span the entire

customer experience and provide sophisticated analytics.” (Source: CRM Review)

There is a link here to the popularity of the touchpoint definition of customer experience

in that if an experience is defined as everything, then a sales argument can be put

forward that all interactions need to be measured and ‘seen.’ Hence the trend to redefine

CRM along the lines of CEM in the hope of selling systems that latch onto the touchpoint

mapping concept through promoting end-to-end measurement, end-to-end visibility of all

interactions and increasing the sophistication of analytics.

“There is a lot of CRM being rebranded to CEM. Lots of vendors are doing this

and lots of buyers are thinking it.” (Expert, UK)

There is no doubt that vendor solutions in CRM are part of the enabling infrastructure of

a customer experience strategy, but that is a very different thing from saying that they

are the customer experience strategy (as seen in the call center examples in table 4). If

not managed carefully, a vendor sales fixation risks paralyzing CEM due to the following

risks:

An over-focus on measuring everything rather than measuring everything that is

important to customer experience.

An over-focus on management control rather than creating solutions – effectively,

vendor sales become a job creation scheme without adding any value.

An over-focus on an objective interaction view of the customer rather than trying

to understand their emotion and psychological response.

A lack of focus on how to interpret data, together with the application of poor

analytical understanding.

The problem is akin to what happens with many founding definitions when they hit the

‘real world’ of sales and making a living. With Six Sigma/ Lean and other BPO initiatives

© 2011 Beyond Philosophy 17

the terms collapsed as the intent of improving the customer experience was changed to

cost cutting and efficiency. Likewise, CEM risks collapse, buried under a deluge of ‘let’s

sell everything we can.’

Management advice: Be careful that the infrastructure you put in place, both

measurement and IT, is supportive, not definitive of CE, and avoids corporate

paralysis.

© 2011 Beyond Philosophy 18

2.3 Risk 3: Failure to Take Account of the Customer’s Emotional Viewpoint

(e.g. in ROI)

Customer experience tends to follow a touch point definition. This is quite a defensive

position to take:

CE Commentaries

“Touch point is a solid way to look at it. It means you are looking at more than

one channel and how get all work together. Act like one organization, don't fall

down, but it is quite a defensive definition. Beware cocking it up; aspiration is

what is being caught here - get everything working together and act as one

organization, hand off works between departments.” (Expert, UK)

Theoretically, the start point belies a “moments of truth” approach – use of the word

experience to mean ‘all that is experienced’ rather than inclusion of a more “moments of

delight approach” as in ‘wow that was an experience.’ The risk here is that for some

organizations, this key point of difference between CE and ordinary service – emotional

engagement – is missed. Instead what is produced is an objective map of interactions

that fit well into measuring ‘things’ and implementing software, which fails to deliver a

return because (a) it is an objective view rather than taking into account how customers

perceive you through their feelings and (b) it becomes a theory of everything rather than

about something that gives a return based on the ‘true’ customer viewpoint, which

cannot exclusively be rational.

The emotional view is useful as it forces a subjective perspective, what it is like to be a

customer or client. Hence, it avoids a company-only perspective on customers.

Including the emotional view is also essential in quantitative research: understanding

emotions in resource allocation decisions, and in determining return on investment

(ROI). Unfortunately, among the interviewees (see table 5) there is a disconnect

between appreciating the importance of emotion and how it is actually measured and

understood. The majority of interviewees only undertook qualitative measurement

through focus group, sentiment analysis, verbatim analysis and journey mapping

© 2011 Beyond Philosophy 19

approaches or critical incident type techniques. The situation quantitatively is even

worse, respondents not adapting current measures and just using customer satisfaction

or loyalty indicators (NPS, TRIM) as proxies for emotion. Some avoided the issue as too

difficult or of importance only as an outcome of other measures.

Table 5: How emotion is measured

Source: 53 CE professionals (where mentioned)

CE Commentaries

“Most would not go to emotions. Most people come from an analytical service

management route rather than a brand emotional viewpoint. No more than a

handful use the language of emotion (e.g. by employing anthropologists to look

at user experience). US Bank is going down that path.” (Banking Expert, USA)

Yet, to be clear 88 percent of the interviewees accepted the importance of emotion to

customer experience. It is just that few know what to do about it!

Measurement Freq.

NPS 8

CSAT 8

Don’t measure 8

General qualitatives 6

Cannot measure 5

Journey Maps 4

Sentiment analysis 4

Verbatims 3

Focus Groups 2

Emotion Curves 1

TRIM index 1

Crisis moments 1

Customer immersion 1

Call recovery scripts 1

Quantitative 17

Qualitative 23

Don’t or Cannot 13

© 2011 Beyond Philosophy 20

Management advice: ensure that you have actively considered emotion in your

understanding of the term. Your research and mapping processes must have this

embedded in their procedures.

2.4 Risk 4: Limitations in its Adoption

Beyond Philosophy concludes that the term customer experience has achieved global

acceptance. However, this acceptance is limited to a few key verticals:

telecommunications, banking, retail and several of the smaller sectors outlined in table 9

with increasing adoption in aviation, motor and insurance.

However, beyond these sectors adoption is low: even in the most mature countries,

customer experience is still only used in a few sectors. In less mature markets again,

this is mostly through telecommunications entrance and a push from competitor entrants

in deregulated markets (e.g. Turkey, Nigeria, Saudi Arabia and UAE).

It is often considered that customer experience is approaching mass adoption. This is, in

part, due to the misappropriation of the term and over-branding, In fact, customer

experience as a business strategy that goes beyond a ‘rebrand’ and mind-set is far from

adoption in most markets. In some industries it is noteworthy that interest has actually

only arisen quite recently and that without the right culture in place customer experience

risks falling into a series of often IT-based projects:

CE Commentaries

“Some basics were not in place in the CE team. CE has only developed in

Canada in the last two years. It was noteworthy that people who joined from the

UK had been doing it for the last four years.” (Telecommunications CxO,

Canada)

“Most work in the USA today is in the top 100 banks (in the US there are 4,500

banks). It becomes more complex to manage - one third pay little attention to

experience/service (they only talk about it) but no execution (J.D. Power and

Associates, Satmetrix); one third are trying to do something so CE is a core

© 2011 Beyond Philosophy 21

strategy (e.g. TD Bank, Umpqua, Huntingdon); and one third are dabbling in the

middle - CE measurement. We are three to five years away from anything (at

least at the end of 2010). Now with the change in financial regulation and margin

pressure, momentum has been built to use service core to retain or use

experience to get more share of wallet – to avoid margin squeeze and

commoditization.” (Banking Expert, USA)

“It has some support from leadership now; one of the main risks is that senior

leadership is constantly raising variables to say it is not the most important thing.

IT systems say other priorities need investment. It is a barely conceived program

as yet, we need to establish. If not, it will drift down the list.” (Charity CxO, UK)

“This will increase in the next two years. Some areas are important, and

increasing in CE such as Indonesia and Malaysia. We are looking at demand

there.” (Banking CxO, Singapore)

Management advice: the problems with limited uptake will lead to a “so what?”

mentality. The way around this is to clearly espouse the competitive advantages

of CE (i.e., lack of adoption is an opportunity). To do this requires a clear

definition of its competitive advantages.

© 2011 Beyond Philosophy 22

2.5 Risk 5: Timeframe to Execute

One of the major problems with CE is that it depends on the long term. Its economic

basis around loyalty is all about long-term return, its advantages in terms of being more

customer-centric also require levels of corporate transformation that take years to

realize.

CE Commentaries

“The change occurred over a six- to seven-year time period. Driven by the

chairman, he appointed me customer relationship director to drive change, with a

focus on culture. It made a statement to the company.” (Motor CxO, UK)

“Also patience, Enterprise Rent-a-Car and Apple turned things around in the late

90s from pariah status, but each turn around takes five years. Sprint is currently

in a three- to four-year turn around period. It takes five years to go from awful to

okay, then another five years to go from good to great – the problem is

companies are usually hit by a recession in that time and scrap it, short-termism

does them in.” (Expert, UK)

Related to this is the need for a culture to support the necessary execution timeframes

as well as a supportive and visionary leadership.

CE Commentaries

“Top three to four percent, here CE is a cultural thing, connected to patience and

leadership. A lot can improve, but without changing the culture there can be no

transformation; down the line comes technology and process.“ (Expert, UK)

“Senior execs are the biggest driver, but they don’t know what they are talking

about. They are aware that it means a way to differentiate or they will decline.

Deloitte, in their IBM CE practice surveys, say that execs partly see brand

© 2011 Beyond Philosophy 23

agencies as weak and not grasping effectively with it from an operational

standpoint.” (Expert, UK)

Some organizations have set up an organic way of controlling expectations and

embedding customer experience. The focus of these action-orientated firms is more

ground-up, setting up cross-silo departments that are focused on a support role for

existing structures. For instance, undertaking the redesign of certain existing

experiences on behalf of a department – this could be about redesigning a form through

to creating a luxury experience.

The point is that this approach recognizes the 18-month time delay from set-up of a

department to potential closure (when patience runs out at board level). In this time,

some form of buy-in and return has to be demonstrated through design.

Management advice: Patience and leadership for the long-term are essential

requirements. To stay the course requires setting out up-front a clear vision.

Alternatively, and possible commensurately, a more design-led supportive role

should be considered (i.e., a demonstration of principle).

© 2011 Beyond Philosophy 24

3.0 A Strategy to Manage Risk

To avoid the risks companies have to realize that at its heart customer experience is an

organizational strategy based upon a holistic approach to the customer using emotion as

a key differentiator. This means embedding from the very start the message that this is a

transformational approach, not just one based on tinkering with the IT infrastructure,

adapting call centers or measuring numerous touch points. These may be part of a

solution, but they are not CE.

CE effectiveness requires looking across key areas (see figure 3), each one broadly

sequential to the next:

Figure 3: Key areas of a CE implementation

Understanding CE – get leadership buy-in and understanding as to what exactly

customer experience is.

Setting the Strategy – define (a) where your organization is in terms of the

customer experience, (b) your organization’s understanding of the customer

journey from an emotional perspective, and (c) the emotion drivers and

destroyers of value. Build out a case study based on ROI and how CE will reach

© 2011 Beyond Philosophy 25

your corporate objectives, usually toward competitive differentiation. Develop a

roadmap to change.

Engage the Organization – start to train the organization in the principles of

customer experience, and design in the organizational foundations to support it

long-term (e.g. governance).

Embed the CE Culture – focus on cultural alignment within the organization

through training, recruitment, embedding CE in the employee experience and

leadership buy-in and support.

Process Improvement - only after the company has started to ‘get it’ should you

move to process improvement. Clearly with time lags, some IT system can be

planned in, but the stage of cultural engagement should be in place prior to

delivery of a new CE process infrastructure, for without employee support no

system emplacement will succeed.

Redesign Experiences - finally, pilot implementations of specific customer

initiatives within the first 12 months to ensure proof of concept, and the

perception that change at the customer level is happening (i.e., we are starting to

see how we can get a return). Use emotion journey maps and emotional

measurement to assist in the redesign, but critically ensure creative execution.

If we take the example of a software implementation or other process improvement, this

can now be seen as only a part of the picture. Critically, if there is a failure to align

process improvement to the emotional understanding of customers, then any

implementation is risking failure (see figure 4). Likewise in figure 5, without a cultural and

a governance structure in place, any process improvement risks being piecemeal and

not transformational.

Finally in figure 6, it is no good just undertaking a process improvement without being

able to clearly plan for a pilot test to demonstrate the return; and not just for processes,

but for other areas identified as essentially for emotional engagement, either through

reducing the destruction of value or promoting a driver to value. It is important to note

© 2011 Beyond Philosophy 26

that this is not a theory of everything, as an implementation will depend on this value

impact, so only a few touch points will impact KPIs.

Within pilot implementations a metric should be included as a key CE indicator of

success. This varies from company to company, but usually includes a loyalty measure

and/or emotion/key touchpoint index measures.

Figure 4: Processes need emotional grounding

© 2011 Beyond Philosophy 27

Figure 5: Culture and governance before process

Figure 6: The need to demonstrate proof of concept

Table 6 indicates that the five major risks can be resolved through the use of a

transformational template:

© 2011 Beyond Philosophy 28

Table 6: Resolution of risks

4.0 Five Major Drivers

From the foregoing research, Beyond Philosophy has highlighted the major risks

inherent in how customer experience is currently operated and identified a five-step

process of managing these risks, wrapped around a redefinition of customer experience

toward a corporate transformation process founded upon emotional engagement.

Without this, current implementation approaches to CE that define it in terms of

rebranding current operations such as marketing and customer service, or as a means

to execute software sales, risk collapsing the market and open up the way for a

superseding paradigm.

The final part of this report highlights how, in the market as a whole, the research has

uncovered long-term drivers to customer experience management that mean it is

becoming increasingly important as a strategy.

Risk Assessment

Risk 1: Use of the term as an

over brand for current operations

Resolved – it is part of a corporate transformation

Risk 2: Misappropriation of the

term for vendor sales

Resolved – process change is grounded in emotional understanding

not in vendor pitches to measure rational touchpoints

Risk 3: Failure to take account of

the customer’s emotional

viewpoint e.g., in ROI

Resolved – the emotion view is the starting point and the end point for

implementation effectiveness and hence how ROI is calculated

Risk 4: Limitations in its adoption Resolved – Return on Experience (RoX) is the initial foundation (the

case study is financially grounded); there is no need to depend on in-

industry cases alone [see above]. Further Globalisation of the term

(CE) demonstrates opportunity

Risk 5: Timeframe to execute Resolved – embedding Experience in the leadership and the culture

keeps it alive for the long-term

© 2011 Beyond Philosophy 29

These five drivers are:

Major Driver 1: Increasing need to respond to customer empowerment.

Major Driver 2: Increasing need to manage organizational complexity.

Major Driver 3: Increased awareness on the importance of emotion and how this

translates into loyalty gains.

Major Driver 4: Move from product-based to service-based organizations.

Major Driver 5: Web experience.

Each of these drivers will be looked at in more detail based on the research findings and

evidence will be provided for business case-planning in support of the need to invest in a

customer experience strategy and design.

4.1 Major Driver 1: Increasing Need to Respond to Customer Empowerment

Using CE as a means to satisfy an increasing level of customer expectation

Customer experience management used to be driven mainly by concerns over

commoditization: CE, in effect, being used as a means to drive differentiation. However,

a new key driver - customer empowerment - has come to the fore globally. This makes

CE a necessity rather than an option:

4.1.1 10 Customer Empowerment Drivers:

1. Social media is increasing the spread of negative and positive word-of-mouth

and enabling communication between cultures. This leads to greater awareness

of customer standards.

2. The development of the ‘fast society’ has led to demands for more instantaneous

satisfaction – experiences from other industries and the use of technology (web

downloads for instance) has led to a change in intuitive expectations of service

delivery.

3. The burgeoning middle classes in countries such as India have raised service

expectations.

© 2011 Beyond Philosophy 30

4. The development of a high-value consumer segment in countries such as UAE

and China has raised demand for luxury experiences; requiring incumbent firms

to design new experiences and prompting new firms to enter the market.

5. Customer demand for international brands has encouraged the expansion of

western firms into new markets, and the development of the ‘branded

experience.’

6. Deregulation has opened demand from third-, fourth- or fifth-market players to

differentiate through CE.

7. With increased travel, customers are becoming more demanding in the

experiences they obtain at home.

8. Government regulation (e.g. treat customers fairly) is responding to increased

customer expectations and driving forward interest in reorganizing corporate

structures toward the customer.

9. Cultural sensitivity (e.g. some cultures are more open to the concept due to the

importance of service and hospitality): The middle-east region is noteworthy for

the cultural focus on CE.

10. Web aggregator sites for commentaries and sites that build combined purchasing

power both B2B and B2C are starting to shift the balance of power.

CE Commentaries

“Client expectations are driving it. We do a lot of B2B work, working on client-

based service loans. They want us to treat their customers well.” (Financial

Services CxO, USA)

“At the same time, I did a piece of work linking certain CE metrics to profit. I got

an overall score for the experience, and then compared this to outlets to show a

trend. With recession, demonstrated that if doing well with CE then a link to profit

– this has remained as social media and word-of-mouth keeps customers

informed of which outlets have a good reputation. You need to prove that this has

cash returns, otherwise who cares?” (Motor CxO, UK)

© 2011 Beyond Philosophy 31

“Secondly, it is built into the brand and marketing strategy (customer experience

is the current competitive landscape for most organizations).” (Hospital CxO,

USA)

“Social media plays a key role at least for companies that understand and get the

concept of social media. CE is not about social media, but social media is about

CE.” (Expert, Belgium)

“We are paying more attention to customer complaints. Social media is critical.

Turkey is a top-five country in terms of Facebook and Twitter use. There is a

strong word-of-mouth in social media. One thing is that banking in Turkey is

different from UK and USA; it is like buying gum, and it is easy to move. Because

of competition it is easy to lose a customer.” (Banking PM, Turkey)

“Kenyans are becoming more knowledgeable, they travel more, and they want

customer service in exchange for what they pay. If I pay X, I demand X. They are

less accepting and more want their rights. In terms of development it is five out of

10 (with 10 being highest on the scale). Purely because of more and more

demand - although driven by the top 20% (control 80%). Banks are more and

more aware of service. Now they are shifting emphasis. Sales and service is like

a hand in a glove. We have our customer care center; before it was [open] 8:00

am -5:00 pm, now it is [open] to 8:00 pm. Some centers [operate] 24 hours. This

is a step in the right direction. Mobile phones also offer extended hours of

service. “(Banking CxO, Kenya)

“In India there is increasing awareness as customers travel to the west. This also

comes with an interest in international brands and services. It is a lifestyle and

culture thing. The brands we have are luxury brands.” (Retail Expert, India)

“The company is very similar to UAE. There are high-end Saudis who want the

best quick, fast and efficient. [It is a] money is no object culture. There are not

many expats. Then there are the six million labor class who want things as cheap

as possible. Then there are the Saudis in the middle, who use data on mobile

broadband. But infrastructure is not so good. So there are high expectations of

© 2011 Beyond Philosophy 32

30-40 percent and want it cheap 60 percent.”(Telecommunications CxO, Saudi

Arabia)

“With BI opening up we are seeing also more investment from the west and this

is driving retail.” (Retail CxO, India)

“The world is a global market; it is easier to see what Barclays in the UK: people

travel, get MBAs overseas and want to bring things to our country. However, 30

percent of banks are doing CE, most are not, but they all do customer service. A

push has also been, two and a half years ago we developed a financial

ombudsman that gives customers redress – so a regulatory push.” (Banking

CxO, Nigeria)

“The key measure now is CSAT, being in the annual KPMG survey.” (Banking

CxO, Nigeria)

4.2 Major Driver 2: Increasing Need to Manage Organizational Complexity

Using CE as an organizing principle to achieve customer closeness in complex

organizational structures

Customer experience management is mainly, but not exclusively, a phenomenon of

multinational corporations. Faced with a proliferation of multiple channels and increasing

complexity in terms of IT infrastructure and expansion into new territories, the current

siloed structure of organizations is facing breakdown. With marketing focused on the

four Ps, customer service focused on service delivery and IT focused on the web

infrastructure, there is a problem of control and communication. This failure leads to

breakage points.

Some other examples of difficulty are:

The difficulties of promoting brand and culture principles in an increasingly diverse

corporate environment.

© 2011 Beyond Philosophy 33

The difficulties of achieving ‘customer closeness’ in a complex organization that is

becoming increasingly distant from the customer.

The difficulties of managing the ‘data deluge’ from Web and other systems.

The difficulties of managing multiple channels, often under legacy infrastructure.

The difficulties of tying together a culturally diverse organization.

The difficulties of establishing control metrics when diverse channels are used.

The difficulties of establishing leadership across an increasingly diverse organization.

The result of these difficulties is that where once there was a close connection to

customers, and a clearer ownership structure (i.e., siloed customer service and

marketing departments), now there is a tendency toward ‘command and control

confusion.’

This trend is internally focused on how customer experience can be used as an

organizing principle to re-orientate the organization toward the customer. Some

examples of this re-orientation are:

1. Providing clear guidance as to customer ownership across the whole journey, not

just within marketing or service channels. The holistic approach effectively ties

the siloed organization together and delivers a means of seeing the customer’s

whole journey.

2. Support for the creation of moments of delight. A CE function offers a design lens

to bring to bear value-add moments of delight that would normally be considered

a cost by marketing or superfluous by service.

3. Support for journey redesign, bringing to the fore journey concepts that would be

lost in a siloed environment, yet are central to customers.

4. The implementation through the organization of a customer-centric culture.

5. Re-organizing customer research (e.g. emotional measurement and mapping),

embedding CE metrics, not just the traditional rational metrics.

6. Support for large multi-channel management (e.g. in joining up systems and

processes), promoting a drive to self-service and better web enablement.

7. Support for the branded experience.

CE Commentaries

© 2011 Beyond Philosophy 34

“Most work on customer experience in the USA is in the top 100 banks (in the US

there are 4,500 banks). As the customer becomes more complex to manage, one

third are trying to do something in customer experience as a core strategy (e.g.

TD Bank, Umpqua Bank, Huntingdon); one-third pay little attention to experience

and customer service (they just talk about it) and have no execution (e.g. J.D.

Power and Associates and Satmetrix); and one-third are dabbling with it (e.g. are

starting to look at customer experience measurement but are 3 to 5 years away

from doing anything [at least at the end of 2010]). (Banking CxO, USA)

“I am the first director of customer experience. With over 20 acquisitions in the

last two decades we have realized that there has been no focus on the end client

impact.” (Manufacturing CxO, USA)

“You need to have a founder who believes or gets the religion along the way.

Also, you need patience. With Enterprise Rent-a-Car and Apple, it took

[approximately five] years to turn them around. With Sprint, they are currently at

three to four years in their turnaround: it takes five years to go from awful to okay,

and then five years to go from okay to great. Often the problem is that you hit a

recession and scrap it all- ‘the short-term does them in.’ So success is connected

to leadership and patience. Culture is important, then down the line comes

technology and process.” (Expert, UK)

“With mergers you can create a Frankenstein even though you want to do good

service. Good branch model, but call center has the IVR from hell, outsourced

call centers are mismatched, which leads to frustration. Union Bank of California

tried to clean up their Frankenstein, but they could not. The leader Bank of

America in 2005 had four or five major platforms, now down due to aggressive

convergence of platforms.” (Banking Expert, USA)

“Choreography: at the front and back office: ING Direct gained full alignment

around service delivery especially as the CEO knows how to fire customers!

Zion’s Bank Utah had issues: it was a holding company with different banks.

Customers get different experiences across the bank.” (Banking Expert, USA)

© 2011 Beyond Philosophy 35

“Some form of business practice is not about technology. There is major

confusion between customer service (i.e., bounded by customer service

departments) so CE=CS. The other one is confusion with user experience, so

things about web, user interface, design and uxp. Techies think user experience,

business professionals think customer service - here it becomes, survey tools,

workforce automation, all stuff related to the contact center use (as they worry

about CSAT).”(Expert, UK)

“There are multiple big projects in the market across all industries, many of which

are technology-enabled. For example, banks are replacing core systems to

enable better, faster customer service while reducing costs, insurance

companies are transforming their claims operations enabled by new systems to

provide better service while reducing claims costs, Telco’s are trying to better

leverage their existing CRM and billing systems investments to reduce error

driven contact demand and increase customer service productivity.” (Expert,

Australia)

4.3 Major Driver 3: Increased Awareness on the Importance of Emotion and

how this Translates into Loyalty Gains

CE is the only platform for understanding and redesigning experiences for emotional

impact

The way of operating marketing has changed from one focused on the four Ps to one

that increasingly looks at emotion as a platform for differentiation. In part, this is driven

by the commoditization challenge, but also by the evidence from neuroscience and

advanced research, that emotions drive behavior.

Customer experience management is built on this belief, focusing on the challenge of

providing emotionally differentiating experiences.

CE Commentaries

© 2011 Beyond Philosophy 36

“This is a key and underdeveloped area, not just in terms of how practiced in

business but in research and academics. When I talk about Apple, there is that

instant wow factor, how do we do that in banking, when all they do is open a

current account or provide a gateway for other products and services so it is very

important yet underdeveloped.” (Banking PM, UK)

Interestingly, when asked directly whether emotions were important, 88 percent of

interviewees stated that they were (average score 6.3 out of 7). Further in defining

customer experience there was a strong underpinning of emotional context (although not

in every case):

CE Commentaries

“Indians are very emotional, with a lot of emotional attachment. But it is not given

too much importance in designing the experience. As we are unable to put a line

into emotion, so this dictates the value proposition - quantification of value a

problem so we go to the rational side.” (India, Expert)

“At the moment we are not taking very much into account the emotional response

of our clients, but we want to improve that and increase it in the forthcoming

years.” (Telecommunications lead PM, Saudi Arabia)

“I try to, but very logical but emotions play a massive part (difference between

service and experience). But we are not there yet.” (Construction CxO, UK)

“We must treat patients as a whole - mind, body and spirit.” (Hospital CxO, USA)

“It is about the emotional side. How to engage from start to finish with our client:

creating a sense that people want to go there.” (Banking CxO, Kenya)

“Purposefully design an organization to achieve value by creating an emotional

connection.” (Financial Services CxO, Netherlands)

© 2011 Beyond Philosophy 37

“To experience is to “feel” how the outcome of a rational and emotional response

to a product or service generates happy or unhappy feelings.” (Outsourcing

Expert, India)

“Building a relationship every time you touch them and converting the non-

customer into a customer. This is not just about managing customers, but also

about looking at each moment of truth for all and creating a positive experience,

harnessing the relationship.” (Telecommunications lead PM, Australia)

“The relationship between the business and the customer. It is very important to

be a "family" with your customer, and to have a friend in their face, not just

business. You always have to put a heart in it.” (Banking lead PM, Nigeria)

“Designing, delivering, measuring and improving customers' rational and

emotional experiences of needs awareness, product/service purchase, usage

and renewal, along with all associated interactions.” (Expert, Australia)

“Customer experience: the experience that a company provides to their

customers, which has to be in critical points of contacts; experience when I

engage with a company, the emotions that are felt in that company.” (Expert,

Portugal)

“It’s how a customer feels and remembers a chain of interactions with and about

an organization.” (Expert, Belgium)

“The entire experience, but from the customers viewpoint. Did we follow the

process, to how does it feel, what is the experience, how emotionally

connected?” (Motor Cxo, UK)

CE Commentaries

“Emotions equal interactions. My start point is what is the definition of

experience? I found six definitions, one was around emotion, and one was

around interactions. When they talk about customer experience, what they mean

© 2011 Beyond Philosophy 38

is interactions and emotions. Largely, when you talk, they are talking about these

two. 95 percent is about interactions and emotions and the other five percent is

the other stuff lumped together. Those who ask about emotions are the five

percent who have if not mastered interactions, have minimised the damage of

those interactions.” (Expert, UK)

4.3.1 Translation of Emotion into Loyalty

Companies will increasingly embed loyalty metrics as de rigour over and

complimentary to customer satisfaction and look to CE to execute programs that

drive long-term return through emotional engagement/connection

Complimentary to an increased awareness on emotion is the emphasis on loyalty

returns and hence creating an emotional connection that lasts over the long term. This

has led to an increasing trend away from customer satisfaction toward loyalty metrics.

“There is a lot of interest in improving loyalty. Some companies offer a

comprehensive view of customer experience.” (Expert, Singapore)

“Our mission and values related to our brand as above. In other industries the

drivers are the same (e.g. in telecoms, banking, insurance). We do feed off the

developed world in terms of measurement (e.g. loyalty drivers to profit

measures).” (Banking PM, Caribbean)

“Other initiatives which are less technology focused are banks improving

segment based customer propositions for affluent customers, including loyalty

recognition and reward, wealth managers creating direct distribution offerings for

life insurance, and superannuation products.” (Expert, Australia)

This is best exemplified by the uptake of Net Promoter® (the “likelihood to recommend”

metric). In total, 65 percent of respondents have heard of NPS and know an organization

(whether their own or another in their country) that uses it. By contrast, 35 percent are

not aware of it or are aware of it but do not use it/believe it should be used.

© 2011 Beyond Philosophy 39

Interestingly, of those organizations that use it, there is some conflict starting to develop

in its application:

CE Commentaries

“There is a lot of hype around NPS. A number of organizations are using it.”

(Expert, India)

“In Singapore, there are two schools of thought on NPS: some think, yes, it is the

indicator; some see many other indicators.” (Expert, Singapore)

“I think it is a good method although we decided against it in the company. We

did so because we believe it is too complicated.” (Telecommunications CxO,

Saudi Arabia)

“We do it but it is not core.” (Banking CxO, Singapore)

“Not so much in China. I understand GE, Philips do this.” (Manufacturing CxO,

China)

“Many industries have heard of Net Promoter®, but only a few implement.”

(Expert, Indonesia)

“Not well-used but well-understood. Some variants such as J.D. Power and

Associates, Gallup. I think it is the best measure as it is a top-line relational

metric. Used for CE, but only a minimal amount look to drivers of CE here.”

(Banking CxO, USA)

“We use NPS, but it is not so common here. We had a head of marketing from

Chicago who brought NPS in last year. We used to have CSAT and a loyalty

index. I am not convinced we have done much better; yes the NPS score could

be improved, but it feels like is 'another flavor of the month.” (Banking CxO,

Caribbean)

© 2011 Beyond Philosophy 40

“Not support - too simplistic, it is a popularity measure (desire to be popular).”

(Telecommunications CxO, Canada)

“Yes - heard about it, but don't like it. It has been adopted in the business; I am

trying to un-adopt it. It depends on having the senior management's ear. I think

Reichheld ran out of things to say on customer satisfaction, so it invented Net

Promoter to sell more books.” (Telecommunications CxO, UK)

“In China: concept not as well recognized among marketing.” (Banking CxO,

China)

“It is being implemented in some organizations but has not yet replaced

satisfaction trackers as the de facto market measure.” (Expert, Australia)

“Yes it is used. It is driven by fashion from overseas and the ease to implement.

But don’t implement from it.” (Expert, South Africa)

“Yes we use it. I think that as a strategy tool it is useful, however it has some

slight challenges as it doesn't actually highlight customer issues.”

(Telecommunications CxO, UK)

4.4 Major Driver 4: Move from Product-Based to Service-Based

Organizations

CE is being looked at to move a product-based organization toward service.

In general, the focus of CE is on verticals with a high customer-facing base. These are

industries that would have used the term customer service but now use customer

experience instead. Less apparent has been the B2B industries. However, as many

product based organizations face margin collapse with commoditization, so they will look

to CE as a means to target and develop new service related propositions. Here, the

ability to manage relationships will be uppermost as the space for differentiation along

product lines declines. This is a trend focused on new wave customer experience

© 2011 Beyond Philosophy 41

verticals in the B2B space (e.g. manufacturing, logistics and construction) and as current

B2C providers integrate CE into their supply chain.

Although determinedly analytical in thinking, these organizations will be forced to

compete in the experience arena pulled along by the success of the forward-thinking

innovators.

CE Commentaries

“It has become huge over the last six years. When I first joined it was a product

focused organization, now it’s moving to service.” (Motor CxO, UK)

“It is considered a fundamental. Part of our growth strategy. It is a means of

differentiating under conditions of commoditization (i.e., build in more than just

buying the product).” (Logistics CxO, USA)

“Because a company can never build a sustainable competitive strategy on the

basis of products, as products are rationally evaluated and hence not able to

build traction.” (Outsourcing Expert, India)

“The engine to drive from a product- to a service-based company. More and

more commercial companies start in China to talk about the practice on CEM, not

so much referenced to industrial companies yet.” (Manufacturing PM, China)

4.5 Major Driver 5: Web Experience

Web-based CE is an area of global interest whether through self-service and

efficiency or personalization and care

The focus on Web enablement is allowing companies in less mature regions to leapfrog

a technology and play on a more even playing field with the more mature countries.

Indeed, in some cases the Web experience is deemed of greater importance (e.g.

Brazil).

© 2011 Beyond Philosophy 42

There is a clear self-service trend in stated implementations – holding both cost and

experience advantages – as well as a focus on efficiency and customer service. The fact

that Amazon.com was the most admired firm for their customer experience among the

interviewees (table 19) is informative as to the direction of interest.

CE Commentaries

“Some of our big projects are about enabling customers to self-serve – the best

service after all is often quoted as no service. So we are thinking about pushing

and pulling web content: things like use of video. ” (Utilities PM, UK)

“We are updating the CRM system, standardizing and reviewing the metrics of

CE and developing website with self-service capabilities. Also reviewing our

wholesale strategy and CE design. (Telecommunications CxO, USA)

“Web care solution upgrade to provide great digital experience. Strategy and

processes in social media channel.” (Telecommunications CxO, Russia)

“We are starting to see some initiatives. Ipau is working on customer experience.

Generally though, a lot of talk but no action. Of the big projects we see the Web

experience being huge - in Brazil, companies are looking for a good web

experience. We love social media and the Internet. Ipau yesterday launched a

new website, to give you a new experience. It is a very different website. We are

less concerned about stores offering a differentiated experience. We do some

limited touch point mapping but the web is the main area.” (Manufacturing

Expert, Brazil)

“More website accessibility; making it friendly for users; getting people to spend

more time onsite.” (Telecommunications PM, Peru)

“Yes I see Lloyds doing a lot with their website. First Direct, although a little

different from us, is more customer centric, enabling world class service. HSBC

changed their login service.” (Banking PM, UK)

© 2011 Beyond Philosophy 43

“La redoute - catalog internet furniture company. A very good commercial

example, very efficient and effective web design fostering, first and foremost, the

capacity for customers to dream a house (ambiance) and then find details and

prices on the furniture.” (Retail Expert, France)

“www.Londontown.com. Web, hotel bookings, getting information from the site

for the last three to four years. They are very helpful, can contact anytime,

answer questions.” (Banking CxO, Russia)

“Amazon - because of friendly staff, easy website interface, excellent customer

service, they do all they can to please.” (Telecommunications PM, Peru)

5.0 A Final View

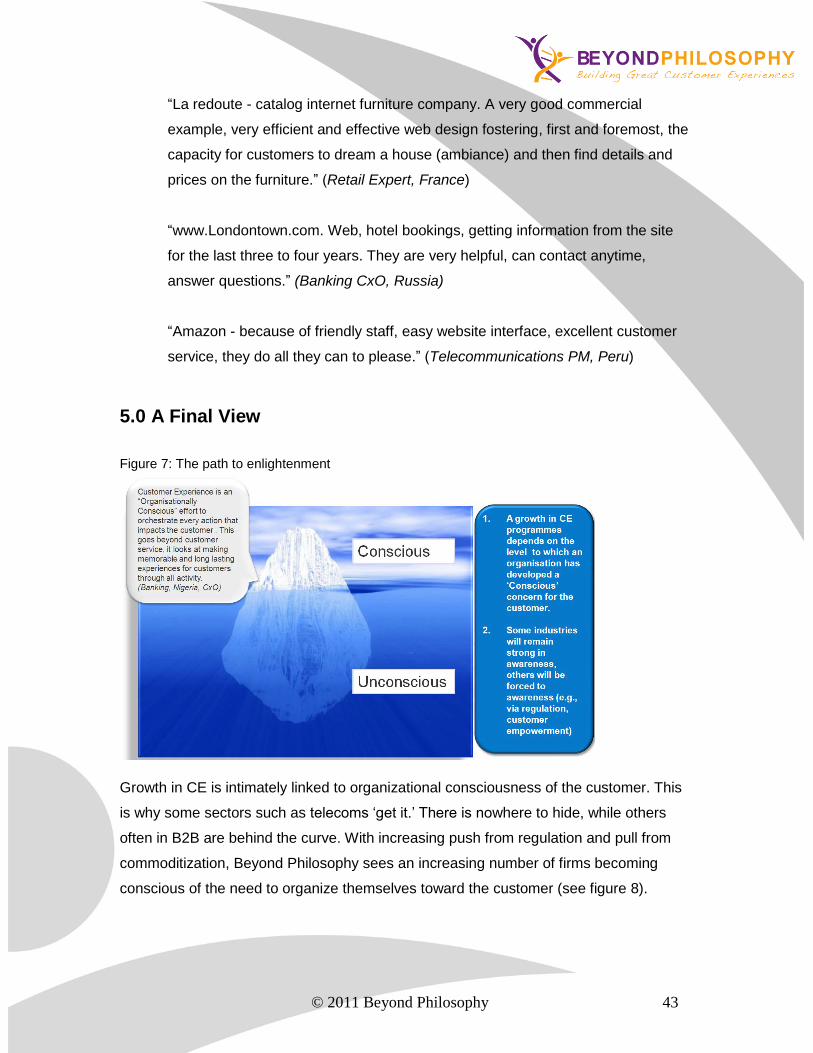

Figure 7: The path to enlightenment

Growth in CE is intimately linked to organizational consciousness of the customer. This

is why some sectors such as telecoms ‘get it.’ There is nowhere to hide, while others

often in B2B are behind the curve. With increasing push from regulation and pull from

commoditization, Beyond Philosophy sees an increasing number of firms becoming

conscious of the need to organize themselves toward the customer (see figure 8).

© 2011 Beyond Philosophy 44

Figure 8: First and second generation enlightenment

Figure 8 shows that in the current market those sectors coming from a low base (such

as manufacturing); facing fast innovation (such as e-tail) and regulatory push (such as

healthcare) will experience the highest growth. However, there is a comprehensive need

even in the first generation to reconsider what customer experience is (i.e., are you

really doing it?).

As figure 9 describes, it is no good taking a defensive position around measuring touch

points or rebranding service and research; organizations need to ensure they ‘truly’

consider the meaning of customer experience based on its founding notions of

organizational redesign and an emotional commitment to loyalty.

It seems for now CE is standing at a crossroads between success and failure. The

message should be ‘rejuvenate or die.’

© 2011 Beyond Philosophy 45

Figure 9: Rejuvenation or die

© 2011 Beyond Philosophy 46

Figure 10: Make sure you are fit for purpose

Companies that have emotions inside understand the customer experience far better

than those that assume customers are always rational. With an emotional understanding

firms are better able to control complexity through customer action, rather than more

controlling measurements.

© 2011 Beyond Philosophy 47

Contacts

For more information on this report or for information about customer experience

in general, please contact:

Steven Walden

Senior Head of Research and Consulting

Beyond Philosophy

Tel: 0207 917 1717

Mobile: 07809 836649

Email: [email protected]