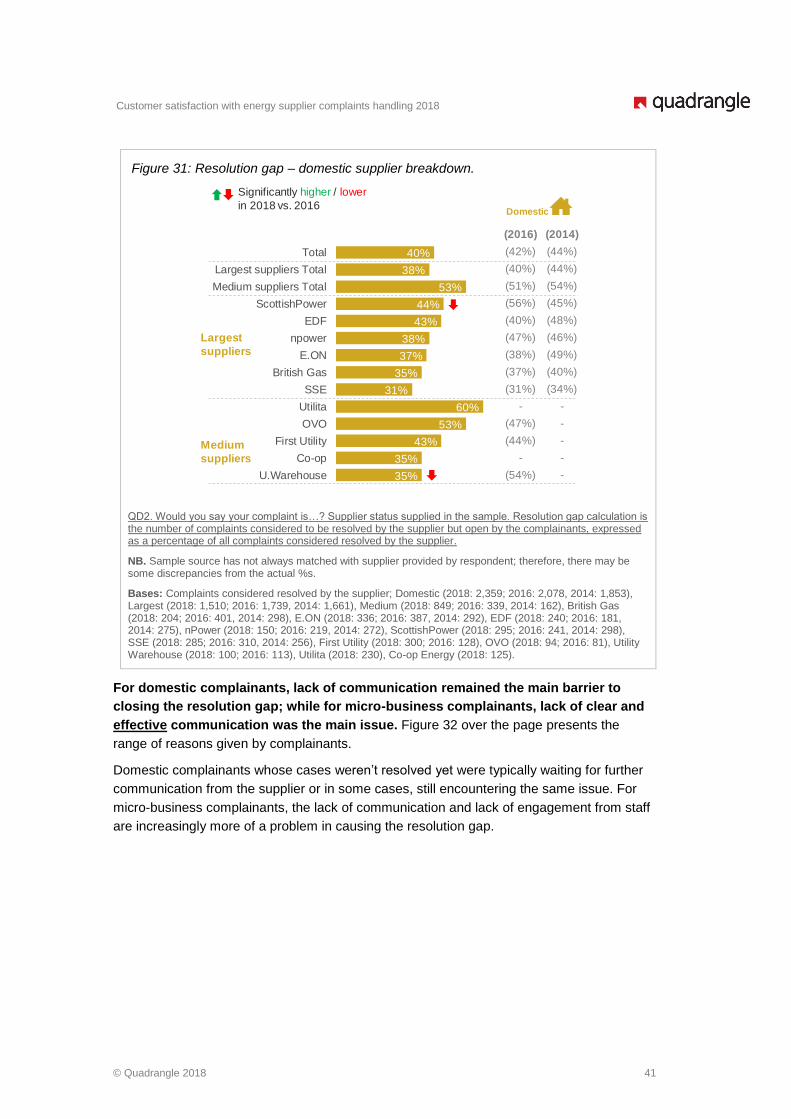

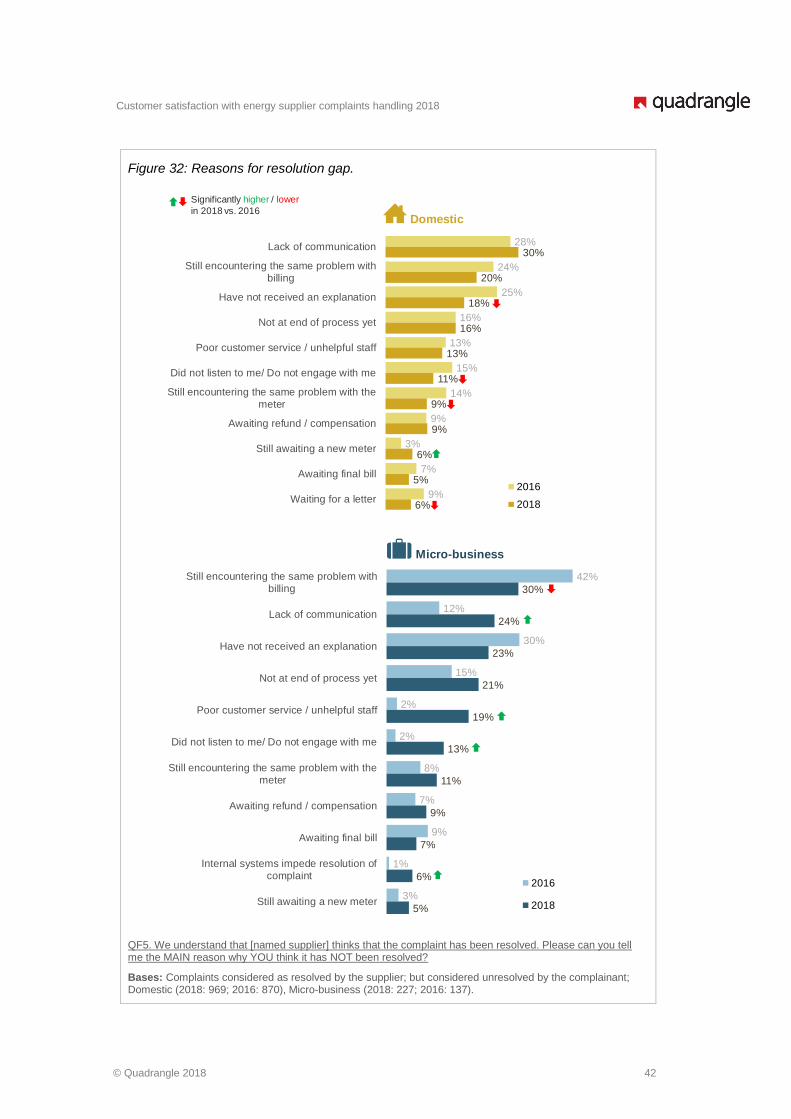

65

Customer satisfaction with energy supplier complaints handling 2018 Research Report Prepared for Ofgem June 2018

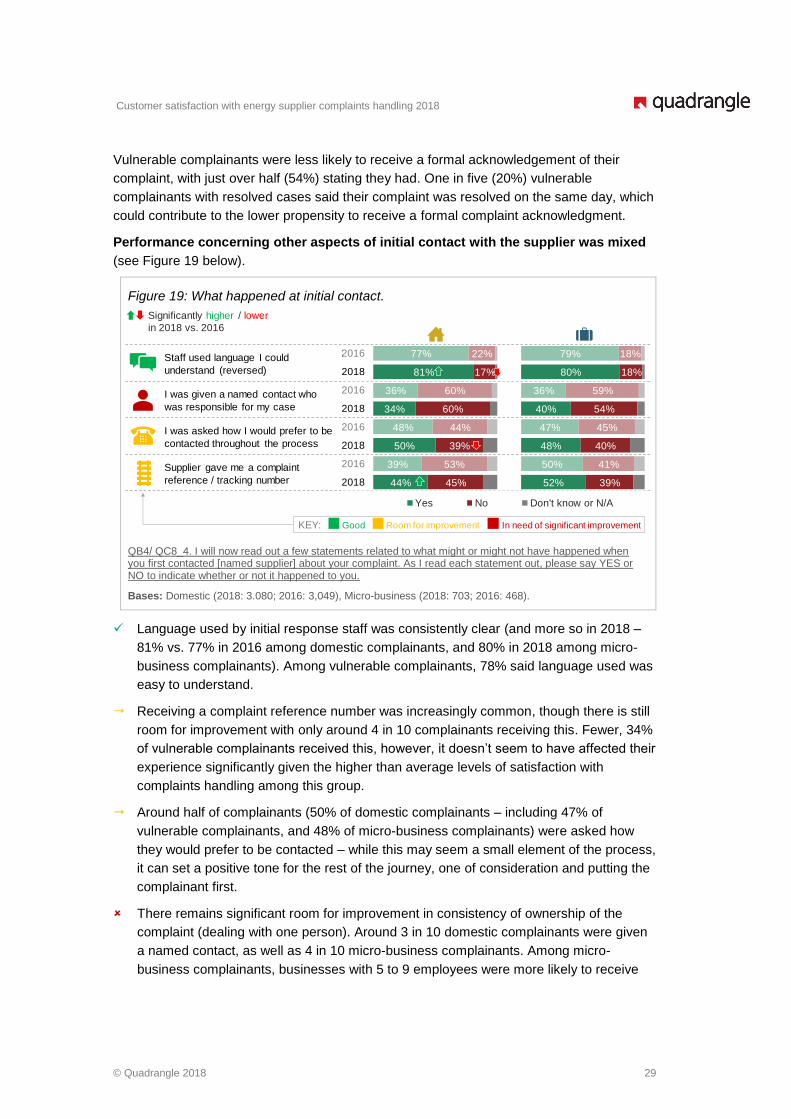

Customer satisfaction with energy supplier complaints handling 2018

Research Report

Prepared for Ofgem

June 2018

Customer satisfaction with energy supplier complaints handling 2018

1 © Quadrangle 2018

Contents

1 Executive summary .................................................................................................... 2

2 Introduction ................................................................................................................. 9

3 Complainant profiles ................................................................................................ 12

4 Satisfaction with complaints handling ................................................................... 19

5 The complaint journey .............................................................................................. 22

6 Impact of complaint handling .................................................................................. 50

7 Key drivers of satisfaction/dissatisfaction with complaints handling ................ 53

8 Conclusions and recommendations ....................................................................... 61

Customer satisfaction with energy supplier complaints handling 2018

© Quadrangle 2018 2

1 Executive summary

1.1 Context and approach

Research background

Ofgem is the independent gas and electricity markets regulator for Great Britain. Its principle

objective is to protect the interests of existing and future electricity and gas customers. In

2008, Ofgem set the Complaints Handling Standards1 (CHS) for all suppliers providing

energy to domestic (private households) and/or micro-business customers (defined as a

business with up to 9 employees with a turnover no greater than £2 million annually2). The

CHS are a set of regulations that suppliers must follow when responding to and dealing with

customer complaints; a complaint is defined as any expression of dissatisfaction with the

service received.

Ofgem has carried out research since the CHS were introduced to assess how well

suppliers have been meeting the standards. Research in 2016 found that satisfaction with

the way complaints had been handled had decreased and Ofgem asked suppliers to review

their processes and improve their services to generate positive change for complainants.

This research was commissioned to monitor any changes in complainants’ experiences.

Research aims and approach

The primary aim of this research is to measure domestic and micro-business complainants’

satisfaction with the way their complaints had been handled by their supplier. This includes

establishing the extent to which satisfaction levels have changed since 2016, identifying the

key drivers of satisfaction and dissatisfaction, and identifying evidence of good practice and

areas in need of improvement.

The research was carried out in February through to April 2018, with 3,080 domestic and

703 micro-business complainants who had lodged complaints with their supplier in late

20173. Interviews were carried out using a structured questionnaire, conducted by telephone

and lasted on average 18-21 minutes. Data were weighted to reflect the share of complaints

in the market. It is important to stress that research findings reflect the complainants’

experience of the complaints handling process.

Who are the complainants

Research participants were complainants of the following:

▪ The six largest domestic and micro-business suppliers: British Gas, SSE, EDF, E.ON,

ScottishPower and npower; and

1 https://www.ofgem.gov.uk/sites/default/files/docs/2008/07/complaint-handling-standards-decision-july-2008.pdf 2 Ofgem defines a non-domestic customer as a micro business if they meet one of the following criteria: 1) they

employ fewer than 10 employees and have an annual turnover or balance sheet no greater than €2 million, or 2) use no more than100,000 kWh of electricity per year or no more than 293,000 kWh of gas per year. For the purposes of this research, energy usage was not factored into the definition. 3 Note on Domestic complainants: Complainants to OVO raised complaints between 25 January and 2 March 2018

rather than in late 2017. Full details are available in the Technical Report.

Customer satisfaction with energy supplier complaints handling 2018

© Quadrangle 2018 3

▪ The largest of the medium-sized suppliers: First Utility, Utility Warehouse, OVO, Utilita

and Co-op Energy (domestic complainants only), as well as Opus (micro-business

complainants only).

The most common cause for complaint among both domestic and micro-business

complainants was billing, and the vast majority of complaints were made by telephone. Just

over half of all complainants stated that their complaint was resolved at the time of interview

(min. of 8 weeks after the complaint had been raised).

1.2 Key research findings

Overall levels of satisfaction and dissatisfaction

Satisfaction with complaints handling has improved significantly since 2016, both among

domestic and micro-business complainants. In the domestic market in 2016, just over a

quarter of complainants (27%) were satisfied with the way their complaint had been

handled, which rose significantly to a third (32%) in 2018. This was met with a significant

decline in the proportion of complainants who were dissatisfied, though more still remain

dissatisfied (57% in 2018) than satisfied.

▪ The greatest improvements in satisfaction were reported among those who complained

to npower and ScottishPower (the two worst performers among the largest suppliers in

2016) which shows the impact of the concentrated effort by those suppliers to improve

complainants experience following an intervention from Ofgem in 2016.

▪ Among the medium-sized suppliers, complainants to First Utility reported significantly

higher levels of satisfaction compared to previous years.

▪ However, there is still a long way to go as just under 2 in 3 complainants to those

suppliers were dissatisfied with how their complaint had been handled.

The improvement is similar in the micro-business market, where satisfaction rose from 21%

in 2016 to 28% in 2018 and was met with a similarly significant decline in the proportion of

micro-business complainants who were dissatisfied, though the majority (60%) remained

dissatisfied.

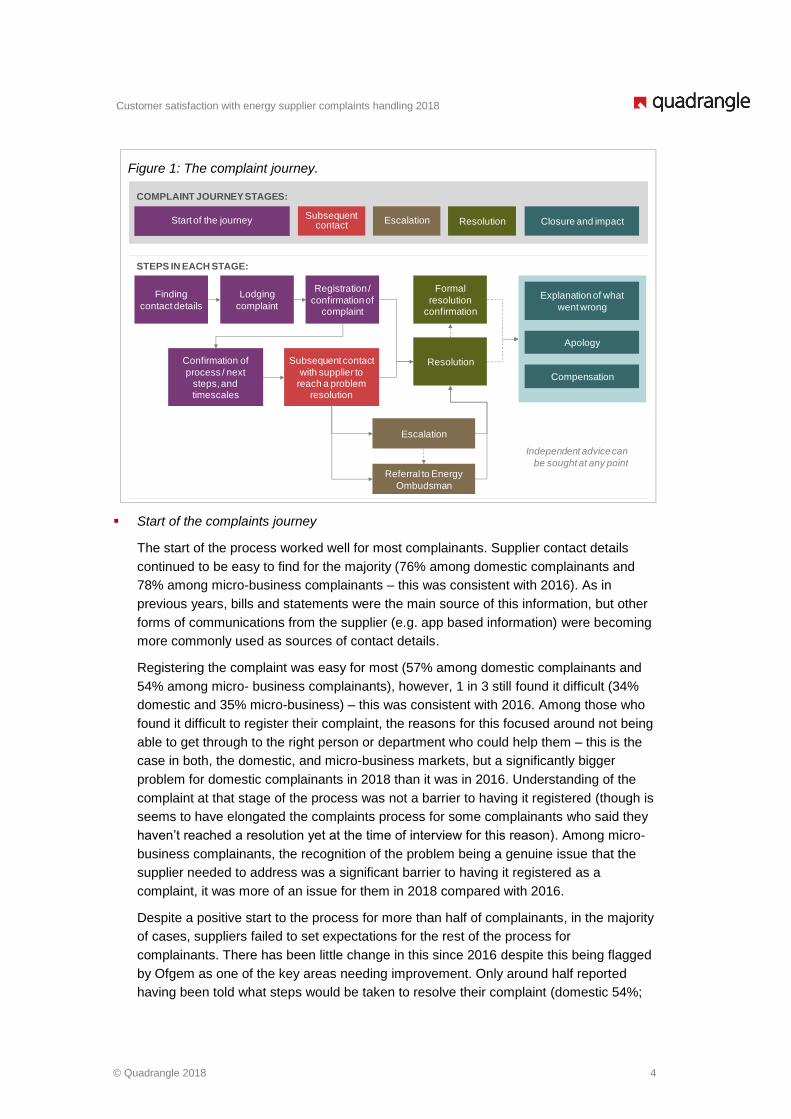

Experiences at different stages in the complaints handling journey

Each stage of the complaints process was investigated in detail to understand what the

process was like from the complainants’ perspective, and what impact each element had on

overall satisfaction with complaints handling. The questions asked within each stage

reflected the requirements of the Complaint Handling Standards (CHS). Figure 1 over the

page presents the complaints journey model used for the purposes of this study.

Customer satisfaction with energy supplier complaints handling 2018

© Quadrangle 2018 4

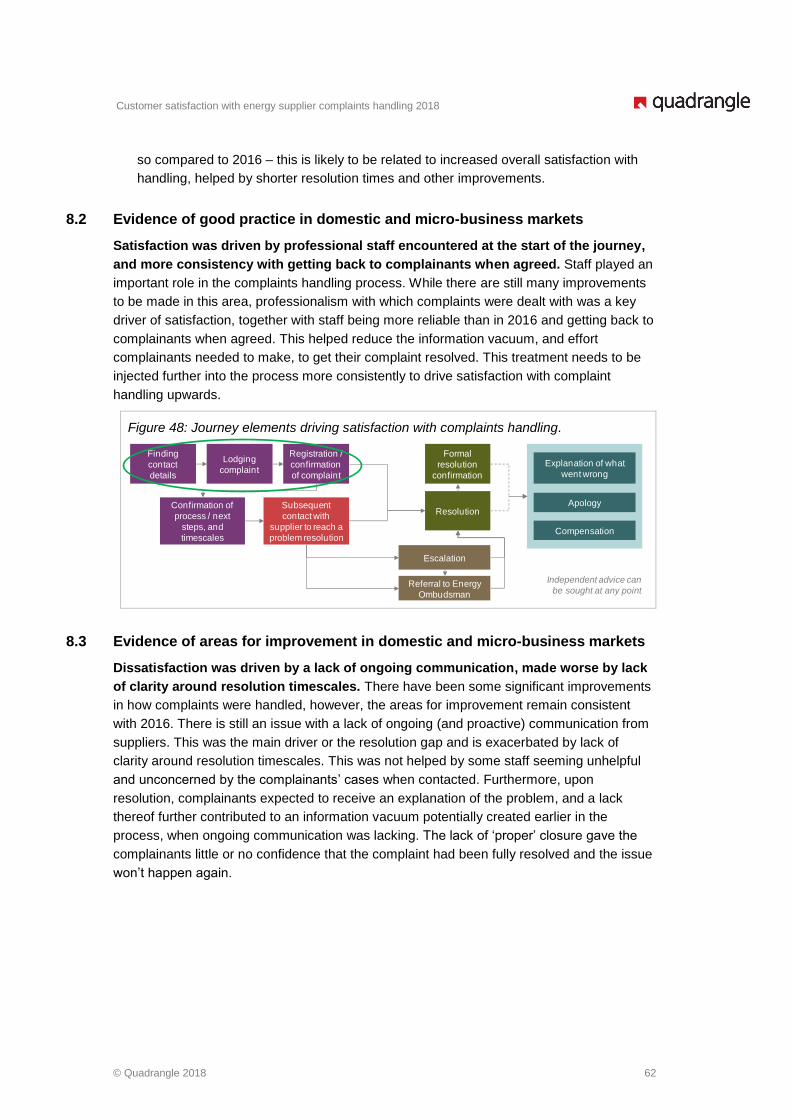

Figure 1: The complaint journey.

▪ Start of the complaints journey

The start of the process worked well for most complainants. Supplier contact details

continued to be easy to find for the majority (76% among domestic complainants and

78% among micro-business complainants – this was consistent with 2016). As in

previous years, bills and statements were the main source of this information, but other

forms of communications from the supplier (e.g. app based information) were becoming

more commonly used as sources of contact details.

Registering the complaint was easy for most (57% among domestic complainants and

54% among micro- business complainants), however, 1 in 3 still found it difficult (34%

domestic and 35% micro-business) – this was consistent with 2016. Among those who

found it difficult to register their complaint, the reasons for this focused around not being

able to get through to the right person or department who could help them – this is the

case in both, the domestic, and micro-business markets, but a significantly bigger

problem for domestic complainants in 2018 than it was in 2016. Understanding of the

complaint at that stage of the process was not a barrier to having it registered (though is

seems to have elongated the complaints process for some complainants who said they

haven’t reached a resolution yet at the time of interview for this reason). Among micro-

business complainants, the recognition of the problem being a genuine issue that the

supplier needed to address was a significant barrier to having it registered as a

complaint, it was more of an issue for them in 2018 compared with 2016.

Despite a positive start to the process for more than half of complainants, in the majority

of cases, suppliers failed to set expectations for the rest of the process for

complainants. There has been little change in this since 2016 despite this being flagged

by Ofgem as one of the key areas needing improvement. Only around half reported

having been told what steps would be taken to resolve their complaint (domestic 54%;

Independent advice can

be sought at any point

Finding

contact details

Lodging

complaint

Registration /

confirmation of complaint

Subsequent contact

with supplier to reach a problem

resolution

Referral to Energy

Ombudsman

Confirmation of

process / next steps, and timescales

Escalation

Formal

resolution confirmation

Resolution

Explanation of what

went wrong

Apology

Compensation

Start of the journeySubsequent

contactEscalation Resolution Closure and impact

COMPLAINT JOURNEY STAGES:

STEPS IN EACH STAGE:

Customer satisfaction with energy supplier complaints handling 2018

© Quadrangle 2018 5

micro-business 51%), and fewer, around a third, said they have been given a resolution

date (domestic 33%; micro-business 31%). absence of this information leaves

complainants to set their own expectation for what the process will look like and how

long it will take, which doesn’t always match the reality, and can lead to significant

disappointment among complainants when those expectations aren’t met.

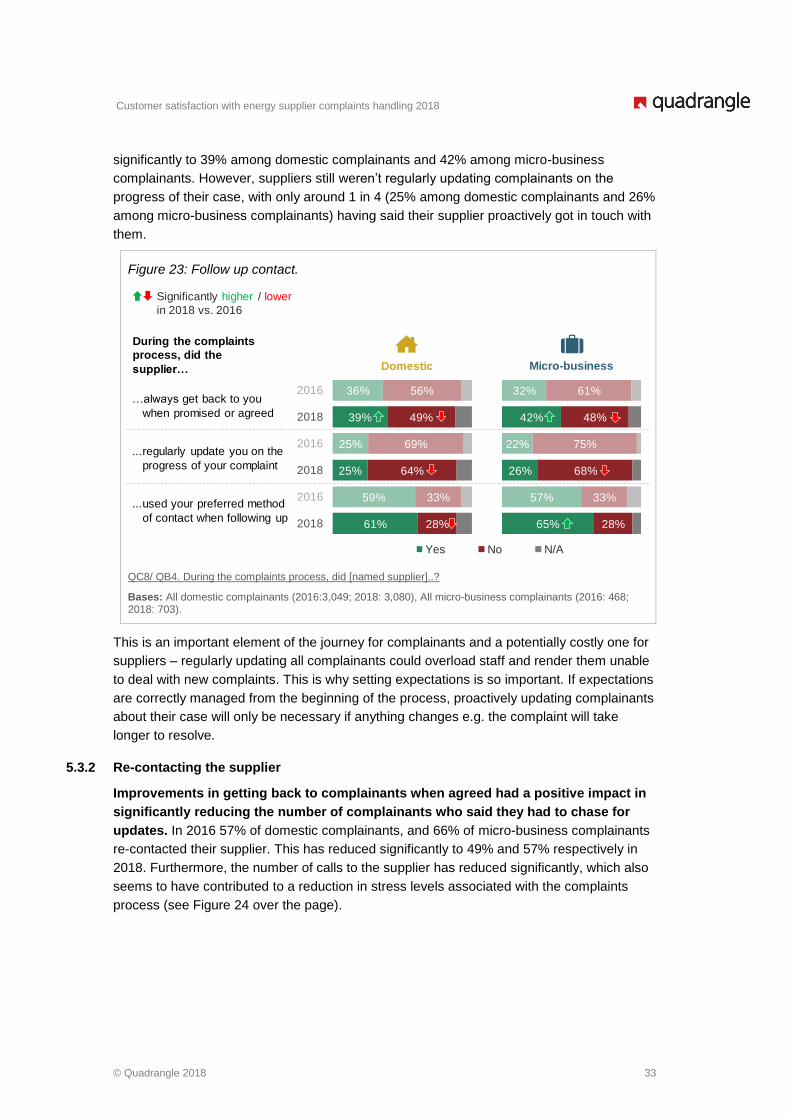

▪ Subsequent contact

Previous waves of the research have shown that ongoing communication is of

paramount importance to the complaint process as its presence ensured that

complainants are not in the dark about their situation and have confidence that their

case is being dealt with. There have been some improvements in this area, with

suppliers being significantly better at getting back to complainants when promised or

agreed compared to 2016 (domestic 36% in 2016 vs. 39% in 2018; micro-business 32%

in 2016 vs. 42% in 2018), however, consistently with 2016, only a quarter said that the

supplier kept them updated on the progress of their case without being prompted to do

so (domestic 25% in 2016 vs. 25% in 2018; micro-business 22% in 2016 vs. 26% in

2018).

Consequently, complainants chased suppliers for information, however, the proportion

who say they have done this has decreased significantly since 2016 (domestic 57% in

2016 vs. 49% in 2018; micro-business 66% in 2016 vs. 57% in 2018), which was

potentially connected to the suppliers being more reliable and getting back to

complainants when agreed.

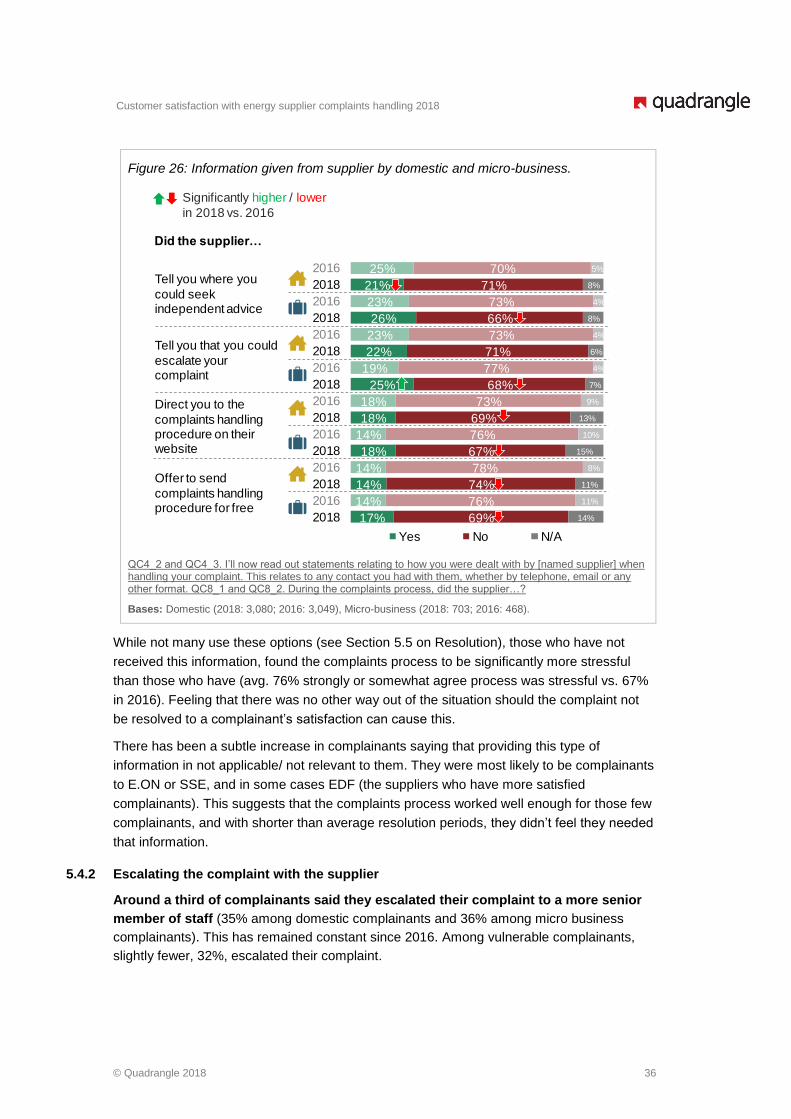

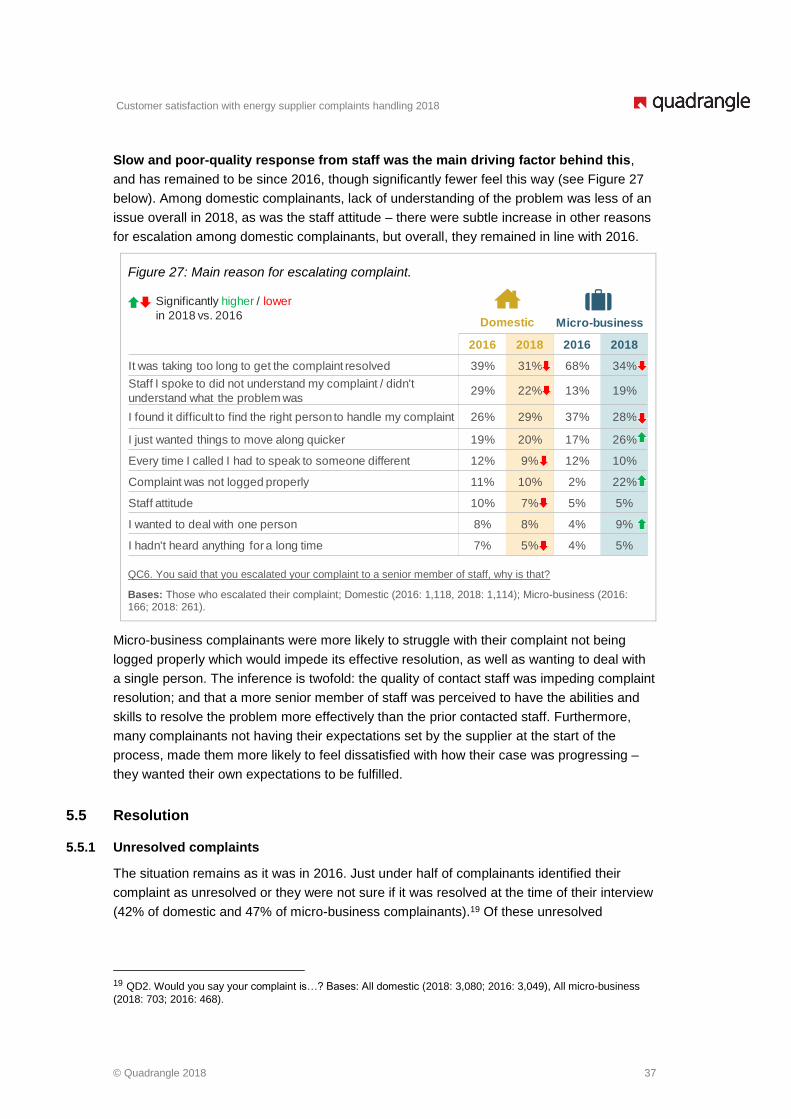

▪ Escalation and third party involvement

While there have been many improvements in how complaints were handled in 2018

compared to previous years, few complainants received information about alternative

resolution routes. Feeling like there is no other way to move the process along (should

this be necessary) could cause stress, so sharing information about alternative

resolution routes (or where to find it) with complainants is important to reducing levels of

stress associated with the complaints process.

Despite only around a quarter (domestic 22%; micro-business 25%) being told that they

could escalate their complaint to be dealt with by a more senior member of staff, around

a third of complainants had done so (domestic 35%; micro-business 36%). The main

reasons for this focused around slow and poor quality response from staff, and in some

cases, lack of understanding of the issue.

▪ Resolution

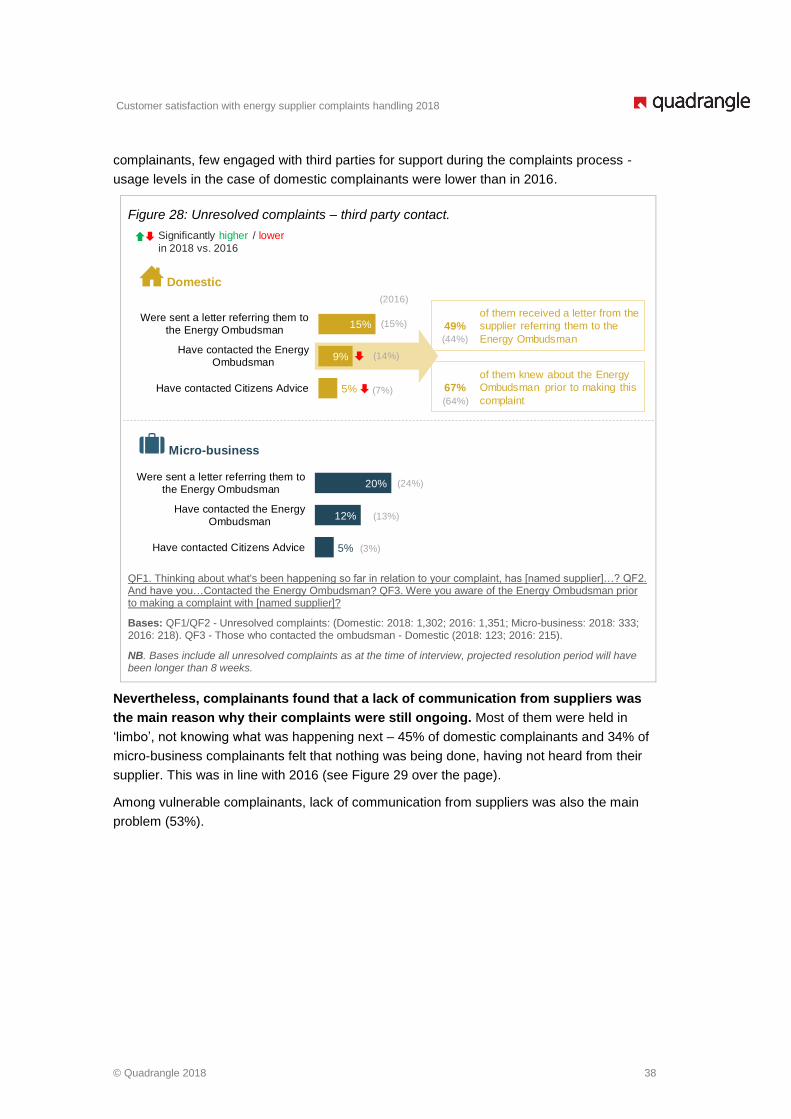

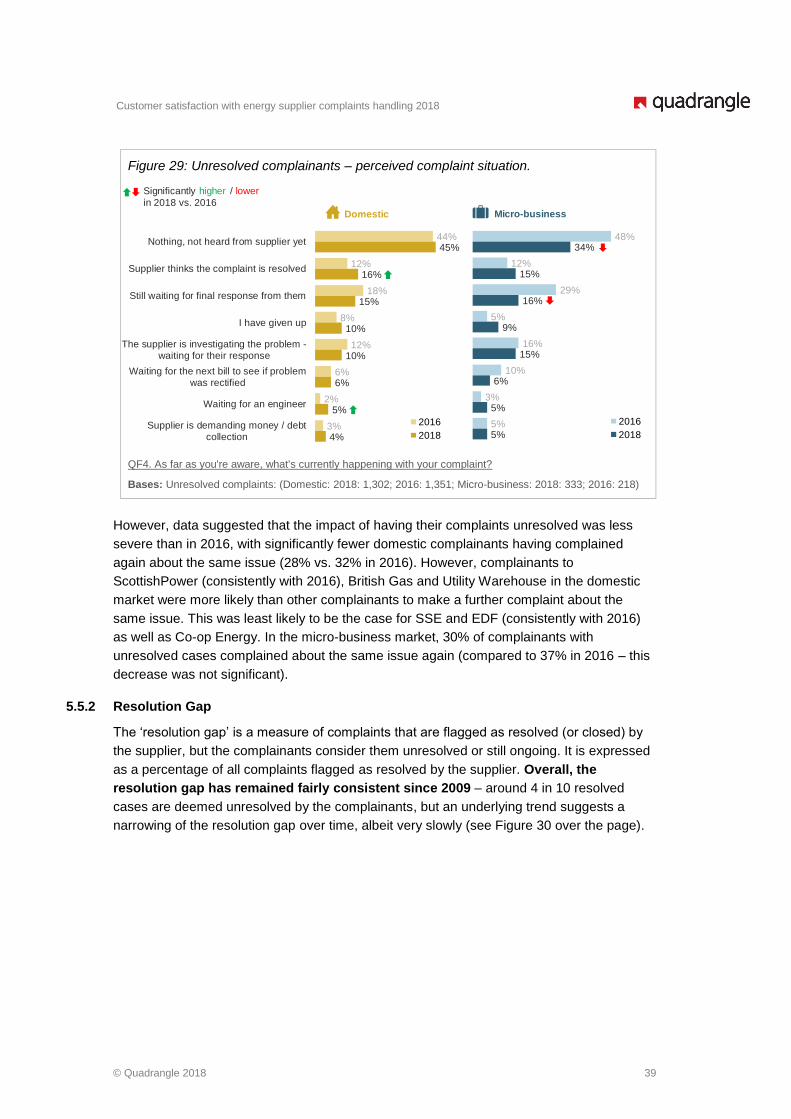

Just under half of complaints were considered unresolved by complainants (domestic

42%; micro-business 47%) and the main reason for this was the lack of communication

from suppliers confirming otherwise.

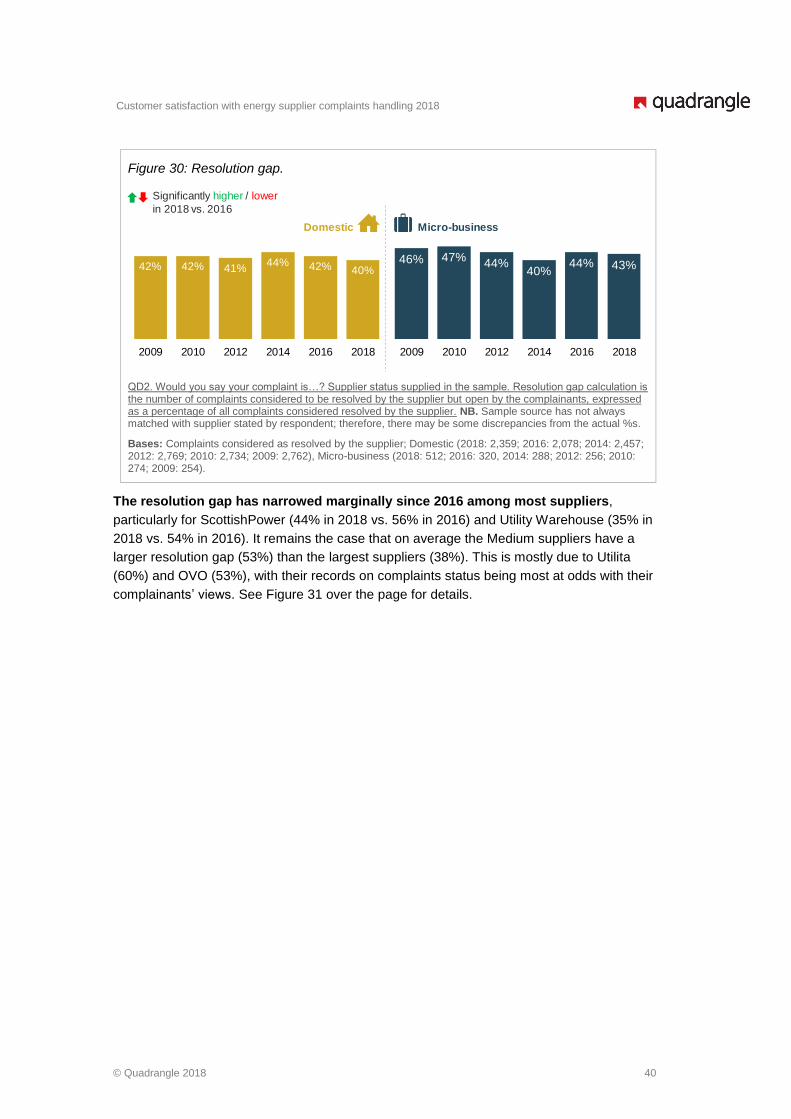

The resolution gap has remained relatively steady since 2009, with 40% of the domestic

complaints (and 43% of micro-business complaints) considered resolved by the

suppliers being considered as unresolved by the complainants themselves. Among

domestic complainants, the absence of communication is the main reason for this.

Micro-business complainants said they were still experiencing the same problem,

Customer satisfaction with energy supplier complaints handling 2018

© Quadrangle 2018 6

meaning that from their perspective, the issue hadn’t been fully addressed and dealt

with despite the supplier marking their case as resolved on their system.

▪ Closure and impact of the complaints process

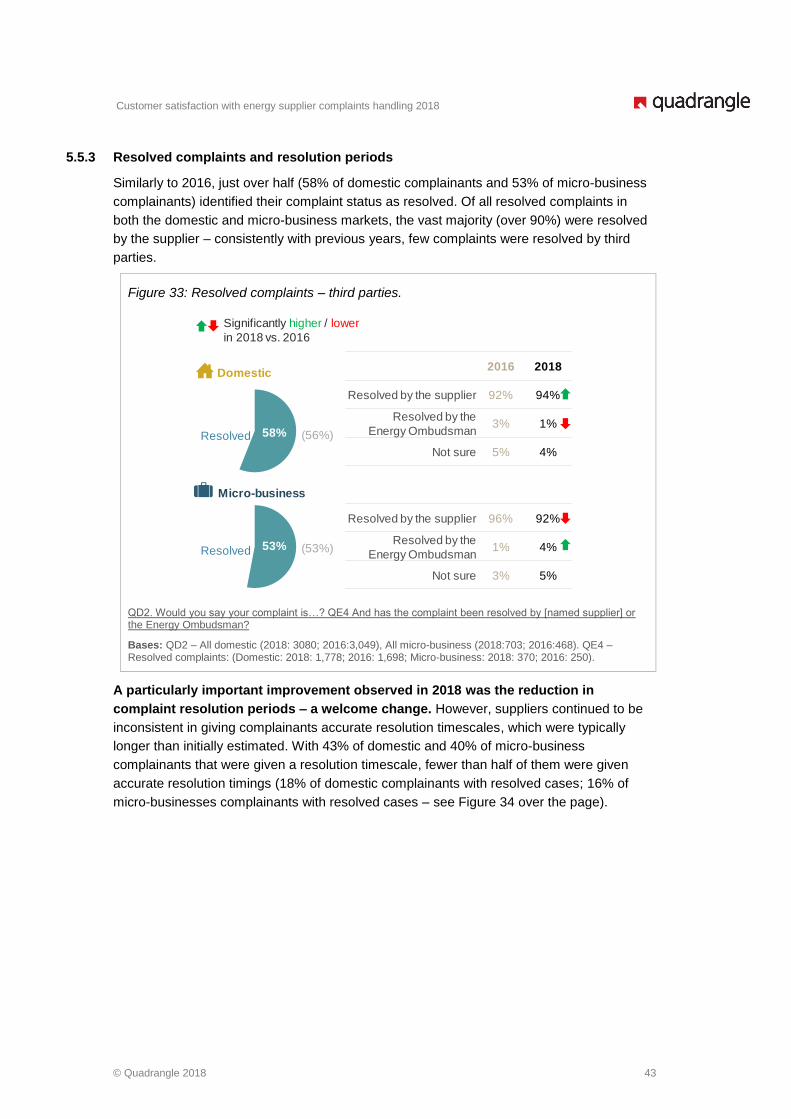

Just over half of complainants said their complaints had been resolved (domestic 58%;

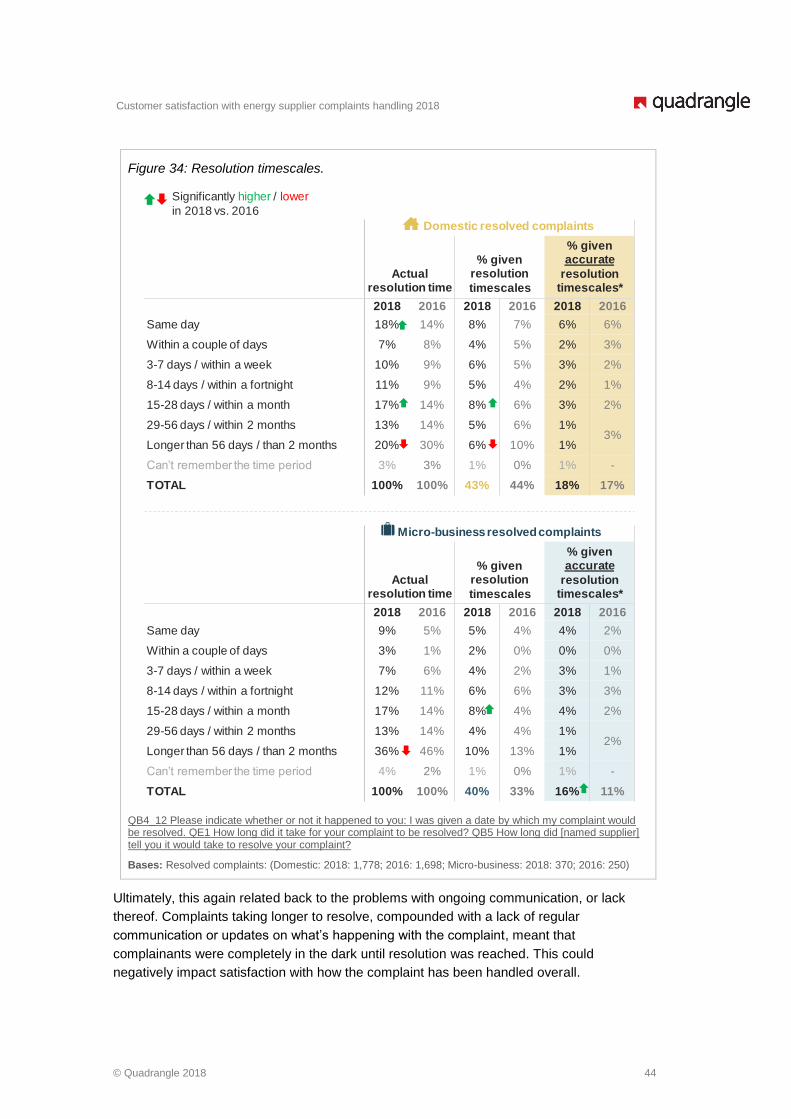

micro-business 53%) and reported resolution times have shortened compared to 2016.

However, fewer than 1 in 5 complainants (domestic 18%; micro-business 16%) reported

receiving resolutions timings at the start of the process which matched how long the

complaints ultimately took to resolve.

Expectations of what complainants would receive were largely met, with most

complainants with resolved cases saying they received at least a rectification of the

problem. However, fewer (around 1 in 3) received an explanation of the problem, which

was something most expected to receive. In fact, those who received an explanation of

the problem were more satisfied with the entire process than those who hadn’t received

it (consistently with drivers analysis which shows that not receiving an explanation

drives satisfaction with the process down), thus becoming an important step for the

suppliers to fulfil to ensure the complainants expectations and needs are met.

Experiences of vulnerable complainants (domestic market only)

Vulnerable complainants’ experience was comparable to that of other complainants,

however, they were significantly more satisfied with how their complaint had been handled

compared to the domestic market average (36% vs. 32% average). They were also

significantly less likely to be dissatisfied with their experience than the market average (52%

vs. 57% average). Nevertheless, it is important to point out that similarly to the market

average, vulnerable complainants were more likely to be dissatisfied than satisfied with how

their complaint had been handled.

Consistently with the market, they found the contact details to raise their complaint easily in

most cases (though they were more likely to use bills and account statements as the source

of that information than the rest of the market), and most found their complaint easy to

register with their supplier. Similarly to the other complainants, their expectations weren’t

correctly set at the start of the process, with around half being told what steps would be

taken to resolve their complaint (51%) and around a third (30%) being given a resolution

date.

Ongoing communication, and being kept updated on the progress of their case, are in need

of significant improvement, consistently with the market average. However, marginally fewer

vulnerable complainants compared to the market average (32% vs. 35% average) escalated

their complaint to a more senior member of staff. Reasons for escalation mirrored the

market average (taking too long, poor quality response).

The proportions of vulnerable complainants who report their complaint as resolved and

unresolved was consistent with the market average. Among those with unresolved cases,

lack of communication from suppliers to say otherwise was the main reason why (with 53%

of vulnerable complainants with unresolved cases having said this, vs. 45% average). For

those who said their complaint has been resolved, fewer than 1 in 5 reported having

received accurate resolution timescales, consistently with the market average.

Customer satisfaction with energy supplier complaints handling 2018

© Quadrangle 2018 7

Based on the experiences in the process and perceptions of staff, both of which were

comparable with the market average, it is difficult to pin point what’s driving the higher levels

of satisfaction with complaint handling among vulnerable complainants – perhaps being

given additional support to help them with resolving their queries on an ongoing basis,

rather than specifically during the complaints process, contributes to a higher level of overall

satisfaction with interactions with their supplier.

1.3 Key drivers of satisfaction and dissatisfaction

Domestic complainants

▪ Satisfaction: The drivers of satisfaction this year were broadly consistent with 2016,

focusing primarily on the experiences early on in the process. Easily finding the right

contact details and being greeted by polite and professional staff who told them what

steps would be taken to get the complaint resolved (experienced by just over half of

domestic complainants) in clear and understandable language set the right tone for the

rest of the process. It was the smoothness of the early interactions that helped uplift

overall satisfaction with how the complaint has been handled.

Reducing effort the complainant has to make also contributes to increasing overall

satisfaction with complaint handling; this includes providing the complainants with

information about what is happening with their complaint on an ongoing basis, to help

reduce their need to chase for updates. There have been significant improvements in

suppliers getting back to complainants when agreed. However, further improvements

are recommended to ensure that complainants’ experience continues to improve, and

satisfaction levels continue to rise.

▪ Dissatisfaction: There were many more drivers of dissatisfaction than satisfaction. This

is expected given that complainants are more likely to be dissatisfied than satisfied

(despite the significant uplift in overall satisfaction levels).

The main contributors to high levels of dissatisfaction with complaint handling were long

resolution periods (though these have started to improve in 2018, but further

improvements are needed), and not being kept up to date with the progress of the case.

Furthermore, suppliers not providing complainants with a clear view of how long the

resolution will take continued to be a problem area in 2018. Lack of information on what

they should expect, and when, could cause anxiety and lead complainants to set their

own expectations, which doesn’t always reflect the reality of the situation, particularly if

the issue they have raised is complex.

Closure was also a problem area for many complainants. The main issue was a lack of

an explanation of the problem upon resolution, as well as a lack of an apology for the

issue occurring in the first place. Both help to reassure the complainant that the issue

has been dealt with and is unlikely to happen again. Lack of an explanation may leave

the complainant feeling that the problem could very easily come back as they have no

reassurance that it has been fully addressed.

Customer satisfaction with energy supplier complaints handling 2018

© Quadrangle 2018 8

Micro-business complainants

▪ Satisfaction: As with domestic complainants, being provided with information about the

steps that would be taken to resolve their complaint in clear language was one of the

key areas that need to be built on to improve complainants’ experience, and through

that, increase satisfaction with complaint handling. Receiving a resolution confirmation

at the end of the process had a similarly positive effect.

▪ Dissatisfaction: The key drivers of dissatisfaction among micro-business complainants

were similar to those within the domestic market. They focused around what

complainants considered to be unacceptably long resolution periods, and a lack of

ongoing communication or communication about likely timescales. This created an

information gap that micro-business complainants filled by repeatedly chasing suppliers

for information.

This became particularly problematic when they dealt with multiple members of staff,

who often appeared unhelpful and not taking the complaint seriously enough. The issue

with staff seemed to be permeating the entire journey for them – for example, micro-

business complainants were finding it more difficult to register their complaint because it

was not being acknowledged or understood when it is first raised.

1.4 Evidence of good practice and areas for improvement

Good practice

Satisfaction was driven by professional staff encountered at the start of the journey

and more consistency with getting back to complainants when agreed. Staff played an

important role in the complaints handling process. While there are still many improvements

to be made in this area, professionalism in how complaints were dealt with was a key driver

of satisfaction, together with staff being more reliable than in 2016 and getting back to

complainants when agreed. This helped reduce the information vacuum, and effort

complainants needed to make, to get their complaint resolved. This treatment needs to be

injected further into the process more consistently to drive satisfaction with complaint

handling upwards.

Areas for improvement

Dissatisfaction was driven by a lack of ongoing communication, made worse by lack

of clarity around resolution timescales. There have been some significant improvements

in how complaints are handled, however, the areas for improvement remain consistent with

2016. There is still an issue with a lack of ongoing (and proactive) communication from

suppliers. This was the main driver or the resolution gap and is exacerbated by lack of

clarity around resolution timescales. This was not helped by some staff seeming unhelpful

and unconcerned by the complainants’ cases when contacted.

Furthermore, upon resolution, complainants expected to receive an explanation of the

problem, and a lack thereof further contributed to an information vacuum potentially created

earlier in the process, when ongoing communication was lacking. The lack of ‘proper’

closure gave the complainants little or no confidence that the complaint had been fully

resolved and the issue won’t happen again.

Customer satisfaction with energy supplier complaints handling 2018

© Quadrangle 2018 9

2 Introduction

2.1 Research context

Ofgem is the independent gas and electricity markets regulator for Great Britain. It has a

principle objective to protect the interests of existing and future electricity and gas

customers. It has set key consumer outcomes that it requires energy suppliers to achieve.

These include standards prescribing better quality of service and fair treatment, as well as

listening to consumers to ensure that their experiences in the energy market are

understood. As part of that, Ofgem is committed to monitoring supplier performance against

the regulations it sets for handling complaints. By definition, complaints are ‘any expressions

of dissatisfaction with the service received’ made by consumers. These expressions of

dissatisfaction should be logged by the supplier as ‘a complaint’ and appropriately dealt with

thereafter as such.

Ofgem’s Complaints Handling Standards4 (CHS) for all suppliers providing energy to

domestic (private households) and/or micro-business customers (defined as a business with

up to 9 employees with a turnover no greater than £2 million annually) include requirements

on suppliers to use accessible language, offer a range of channels for lodging and

managing complaints, provide a clear pathway from complaint to resolution, and provide a

clear route for redress should the complaint not be resolved to the consumer’s satisfaction.

All complaint cases must be logged in written electronic form and the process of complaint

handling has to be readily available to consumers on the supplier website (and they must be

informed about the existence of the procedures). Suppliers are required to treat all

consumers fairly; the standards apply to domestic and micro-business5 complainants.

Research to measure how well suppliers have been meeting the standards has been

conducted since 2008, when they were introduced. Five waves of research have been

conducted prior to this survey, with this wave being the 6th.

In 2014 (4th wave) a number of issues contributed to a fall in satisfaction with complaint

handling, including speed of resolution, lack of ownership and staff’s inability to make

decisions at point of contact, as well as poor ongoing communication. Communications

were sent to suppliers to outline areas that needed improvement.

The 2016 wave (5th) identified a further decrease in satisfaction with the way suppliers were

handling complaints. This decrease was found among domestic and micro-business

complainants alike. The issues which affected this were largely similar to those in 2014:

Resolution periods were seen as unacceptably long, and the lack of ongoing communication

left complainants in the dark about their situation. They were left to set their own

expectations of what should happen, which was often far from reality and exacerbated the

already negative perception of the situation. Thus, many complainants chased suppliers for

information, which meant speaking to multiple staff who didn’t always have access to the full

complaint history – this was seen as unhelpful and was contributing to higher levels of

stress and consequently, complainants voting with their feet and switching suppliers. In

4 https://www.ofgem.gov.uk/sites/default/files/docs/2008/07/complaint-handling-standards-decision-july-2008.pdf 5 Micro-businesses are businesses with up to 9 employees.

Customer satisfaction with energy supplier complaints handling 2018

© Quadrangle 2018 10

response, Ofgem took a number of direct and indirect actions against suppliers to help

improve the situation for complainants and issued further guidance to suppliers to

encourage them to more effectively address the areas in need of improvement.

This wave of research was commissioned to assess how well suppliers responded to the

call for improvements, and to monitor any changes in complainants’ experiences.

2.2 Research aims and objectives

The primary aim of this research was to measure domestic and micro-business

complainants’ satisfaction with the way their complaints have been handled by their

energy supplier. Specifically, the research set out to:

1. Gauge complainants’ satisfaction with suppliers’ complaints handling at market (and

supplier) level, and understand the key drivers of satisfaction and dissatisfaction;

2. Identify areas of good practice in the application of the Complaints Handling Standards;

3. Identify areas of weakness in suppliers’ complaints handling process, and determine

priority areas that require action; and

4. Assess the extent to which suppliers’ handling of complaints and complainants’

satisfaction with this has changed since 2016, revealing areas where improvements

have been made or areas where they have remained steady or declined.

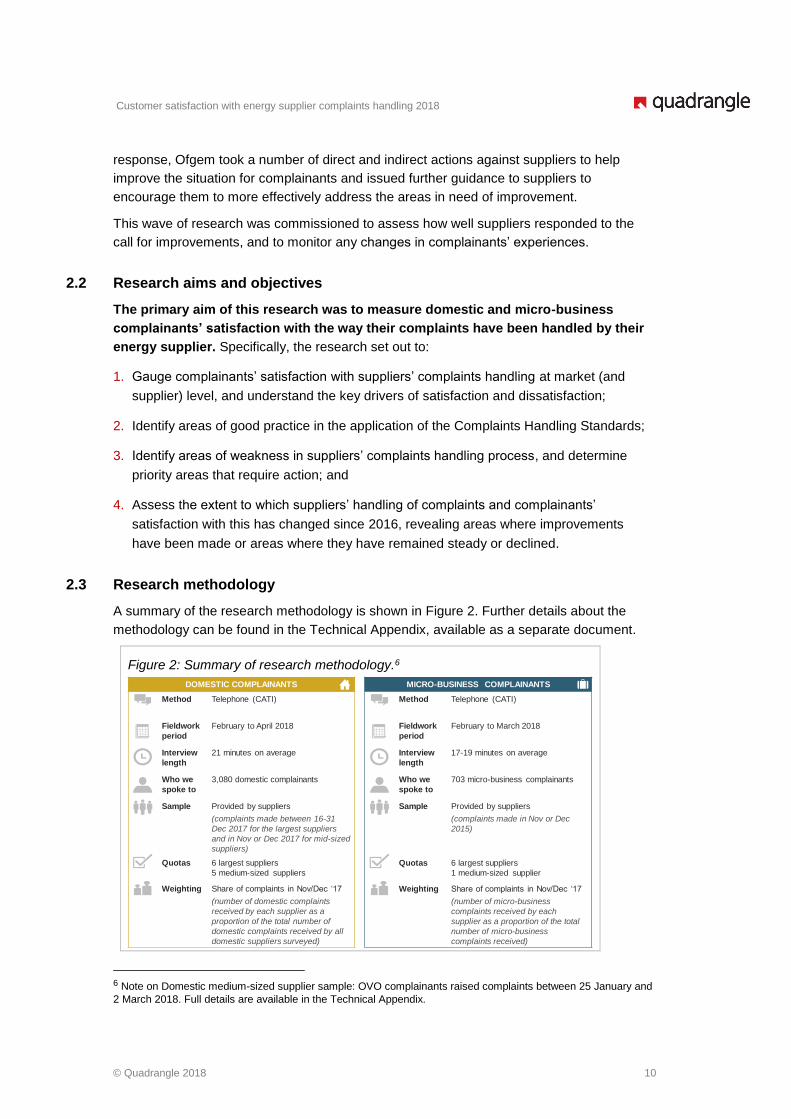

2.3 Research methodology

A summary of the research methodology is shown in Figure 2. Further details about the

methodology can be found in the Technical Appendix, available as a separate document.

Figure 2: Summary of research methodology.6

6 Note on Domestic medium-sized supplier sample: OVO complainants raised complaints between 25 January and

2 March 2018. Full details are available in the Technical Appendix.

MICRO-BUSINESS COMPLAINANTS

Method Telephone (CATI)

Fieldwork

period

February to March 2018

Interview

length

17-19 minutes on average

Who we

spoke to

703 micro-business complainants

Sample Provided by suppliers

(complaints made in Nov or Dec

2015)

Quotas 6 largest suppliers

1 medium-sized supplier

Weighting Share of complaints in Nov/Dec ‘17

(number of micro-business

complaints received by each

supplier as a proportion of the total

number of micro-business

complaints received)

DOMESTIC COMPLAINANTS

Method Telephone (CATI)

Fieldwork

period

February to April 2018

Interview

length

21 minutes on average

Who we

spoke to

3,080 domestic complainants

Sample Provided by suppliers

(complaints made between 16-31

Dec 2017 for the largest suppliers

and in Nov or Dec 2017 for mid-sized

suppliers)

Quotas 6 largest suppliers

5 medium-sized suppliers

Weighting Share of complaints in Nov/Dec ‘17

(number of domestic complaints

received by each supplier as a

proportion of the total number of

domestic complaints received by all

domestic suppliers surveyed)

Customer satisfaction with energy supplier complaints handling 2018

© Quadrangle 2018 11

2.4 Reporting conventions

When interpreting the data presented in this report, please note that:

• Results may not sum to 100% due to rounding and/or due to participants being able to

select more than one answer to a question.

• Data presented in this report is from a sample of complainants rather than the total

population. This means the results are subject to sampling error. Differences between

suppliers or other sub-groups, and between different waves of the research, are only

commented on if they are statistically significant at the 95 per cent confidence level.

This means there is no more than a 5 per cent chance that any reported differences are

not real but a consequence of chance/ sampling error.7

• Statistically significant differences are indicated on each figure with arrows, as

detailed below, and commented on where appropriate. Typically, the larger the base

size (the number of respondents answering the question), the more likely it is that any

differences observed are statistically significant. Results in each section of this report

are presented for the current wave of the survey in the first instance. Comparisons are

made with 2016 (and in some cases earlier years) to establish what has/ has not

changed over time.

• Results represent the experience from the complainants’ perspective; it is their

perception and recall of their experience that is reported.

7 Strictly speaking, calculations of statistical significance apply only to samples that have been selected using a

probability sampling design. However, in practice, it is reasonable to assume that these calculations provide a good indication of significant differences for quota sampling (as used for this research).

Significantly higher / lower

in 2018 vs. 2016

This indicates significant difference (at 95% level

of significance) between results reported in 2016 and 2018 (the most recent wave)

Customer satisfaction with energy supplier complaints handling 2018

© Quadrangle 2018 12

3 Complainant profiles

3.1 Demographic and firmographic profiles of complainants

The complainants are a representative sample of all consumers who had contacted their

supplier to ‘express dissatisfaction’ in late 2017.8 The profiles of the domestic and micro-

business complainants who participated in the survey are shown in Figures 3 and 4 below.

Figure 3: Domestic complainant profile.

Base: Domestic complainants (3,080).

Figure 4: Micro-business complainant profile (up to 9 employees).

Bases: Micro-business complainants (703).

8 To reiterate, complaints are ‘any expressions of dissatisfaction with the service received’ made by consumers

and for this research, the complaints were made between 16-31 December 2018 for the largest domestic suppliers and in November-December 2018 for all medium-sized suppliers (except for complainants to OVO who raised complaints between 25 January and 2 March 2018) and all micro-business suppliers.

No. of employees

35%16%

Sole Trader

1-4

5-9

Energy

management & procurement responsibility

Full

responsibility64%

Joint / some

responsibility27%

No responsibility 9%

6%

11%

52%

Refused /DK

Other

QuarterlyDD

On receiptof bill

Monthly DD

Gas 11%

Electricity 77%

Dual fuel 13%

Fuel type

Payment type

Sector

Annual turnover

10%

2%

7%

7%

8%

10%

11%

12%

14%

20%

Other

Public services& Government

Construction &Manufacturing

Not for profit

Farming

Leisure

Professional

Catering

Property

Retail

Role in the business

Owner / Partner / CEO 45%

Financial Director /

Director26%

Manager level employee 11%

Office manager 5%

Other employee 13%

(including garages)

28%

13%

34%

15%

11%

£0k-£25k

£25k-50k

£50k-250k

£250k-500k

£500k+

49%

19%

12%

3%

5%

3%

5%

9%

16%

59%

Refused /DK

Other

Paymentcard

QuarterlyDD

On receiptof bill

PPM

MonthlyDD

18-24 3%

25-34 12%

35-44 15%

45-54 18%

55-64 19%

65-74 19%

75+ 10%

Refused 3%

Gas 17%

Electricity 32%

Dual fuel 51%

Age

AB 21%

C1 24%

C2 15%

DE 28%

Refused 12%

SEG

Frequency of internet use

Ethnicity

White/White

British85%

Black/African/

Caribbean/ Black British

4%

Asian/Asian

British4%

Mixed 1%

Other 2%

Refused 4%

Fuel type

Payment type

Vulnerable groups

57% 21%5% 3% 11% 3%

Severaltimes a

day

Roughlyeveryday

At leastonce aweek

Once amonth or

less

Never Refused

Has a long term

disability25%

65 years old or older 28%

Has PPM or other

short-term or pre-payment scheme

19%

Socio-economic

group E20%

No access to internet 7%

English not spoken at

home4%

PSR * 30%

* The Priority Services Register

is available for consumers in

vulnerable situations. Being on

the register entitles consumers

to additional support services

such as quarterly meter reads,

accessible bills and priority in

case of a power cut

Customer satisfaction with energy supplier complaints handling 2018

© Quadrangle 2018 13

3.1.1 Complainants in vulnerable situations

Ofgem’s responsibility to protect the interests of energy consumers includes those who are

in vulnerable circumstances (this relates to domestic consumers only). Vulnerable

circumstances arise when a consumer’s personal circumstances and characteristics,

combined with aspects of the market, create situations where they are either:

▪ Significantly less able, than a typical consumer, to protect or represent their interests in

the energy market, and/ or

▪ Significantly more likely, than a typical consumer, to suffer detriment or that detriment is

likely to be more substantial.

More specifically, this would apply to some consumers of pensionable age, those who have

a disability, are chronically ill, have a mental health condition which impacts their ability to

e.g. understand their bill, if they live in rural areas, are on low incomes or in any other

vulnerable situation which means that they need additional support (on an ongoing basis or

for a limited time). Vulnerability can be transient as personal circumstances change.

Furthermore, a vulnerable consumer is not vulnerable because of who they are, but

because of the circumstances they are in, which is what may prevent them from being able

to fully protect or represent their interests in the energy market.9

Energy suppliers have the responsibility to ‘seek to identify’ each domestic customer in a

vulnerable situation, to be able to address their needs appropriately.10 This means

identifying where individual circumstances create barriers to accessing services in the

energy market and having a strategy to help consumers overcome those barriers.

Vulnerable customers are often included in the Priority Services Register (PSR) – it is a free

service provided by suppliers and network operators to customers in need. If eligible, and

the customer agrees to be registered, a customer will qualify for supplementary services

such as suppliers providing support to help the customer identify someone acting on behalf

of their supplier, e.g. a password or showing an agreed identification card if visiting the

customer’s home, among a number of other services.11 This level of support is particularly

important in relation to raising a complaint, which can have a financial and/ or emotional

impact on the complainants.

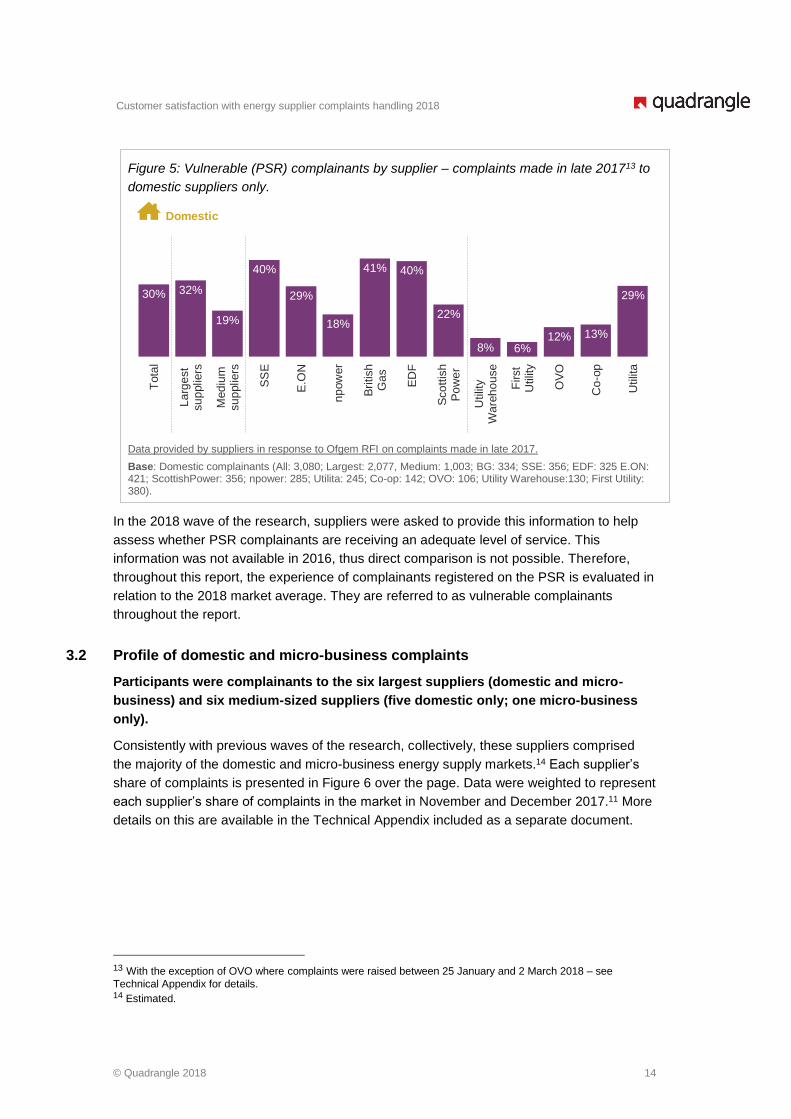

Figure 5 over the page presents the % of complainants registered on PSR among those

who raised complaints/ expressed dissatisfaction in late 201712 as identified by the

suppliers.

9 Ofgem Customer Vulnerability Strategy, published July 2013. 10 For more information on the Standards of Conduct, see Ofgem Licence guide: Standards of Conduct, published

October 2017. 11 https://www.ofgem.gov.uk/consumers/household-gas-and-electricity-guide/extra-help-energy-services/priority-

services-register-people-need 12 With the exception of OVO where complaints were raised between 25 January and 2 March 2018 – see

Technical Report for details.

Customer satisfaction with energy supplier complaints handling 2018

© Quadrangle 2018 14

Figure 5: Vulnerable (PSR) complainants by supplier – complaints made in late 201713 to

domestic suppliers only.

Data provided by suppliers in response to Ofgem RFI on complaints made in late 2017.

Base: Domestic complainants (All: 3,080; Largest: 2,077, Medium: 1,003; BG: 334; SSE: 356; EDF: 325 E.ON: 421; ScottishPower: 356; npower: 285; Utilita: 245; Co-op: 142; OVO: 106; Utility Warehouse:130; First Utility: 380).

In the 2018 wave of the research, suppliers were asked to provide this information to help

assess whether PSR complainants are receiving an adequate level of service. This

information was not available in 2016, thus direct comparison is not possible. Therefore,

throughout this report, the experience of complainants registered on the PSR is evaluated in

relation to the 2018 market average. They are referred to as vulnerable complainants

throughout the report.

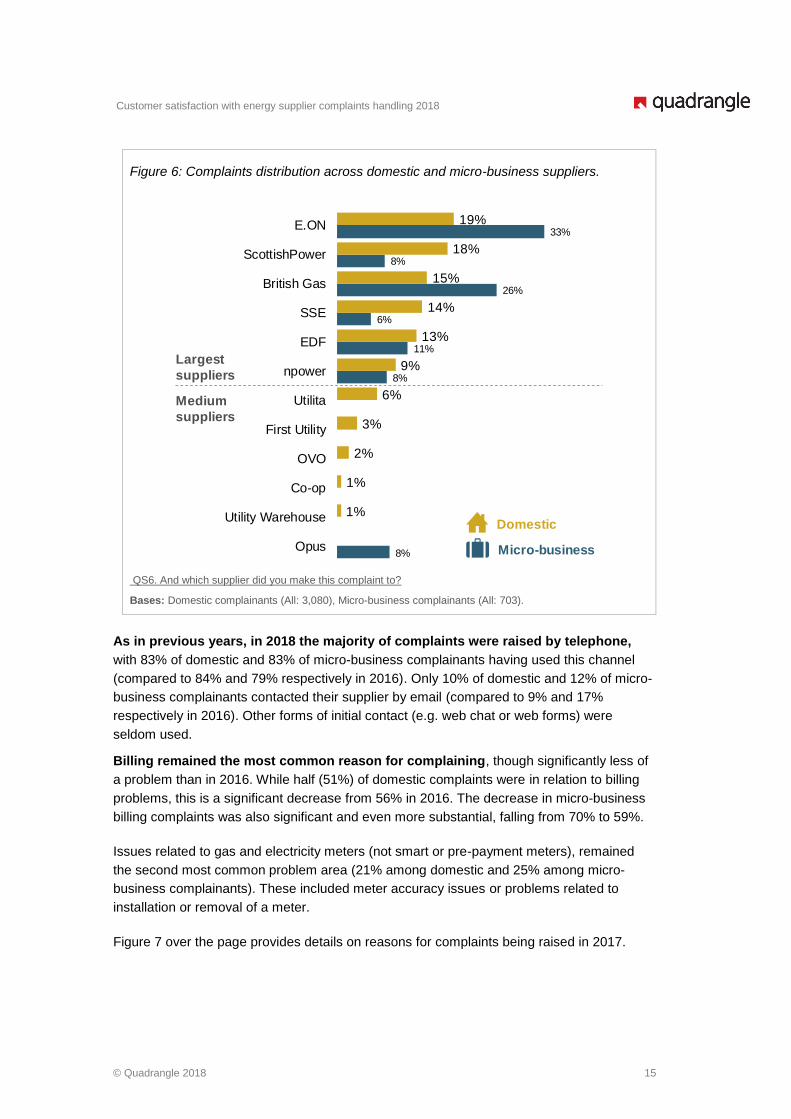

3.2 Profile of domestic and micro-business complaints

Participants were complainants to the six largest suppliers (domestic and micro-

business) and six medium-sized suppliers (five domestic only; one micro-business

only).

Consistently with previous waves of the research, collectively, these suppliers comprised

the majority of the domestic and micro-business energy supply markets.14 Each supplier’s

share of complaints is presented in Figure 6 over the page. Data were weighted to represent

each supplier’s share of complaints in the market in November and December 2017.11 More

details on this are available in the Technical Appendix included as a separate document.

13 With the exception of OVO where complaints were raised between 25 January and 2 March 2018 – see

Technical Appendix for details. 14 Estimated.

29%

13%12%6%8%

22%

40%41%

18%

29%

40%

19%

32%30%

Utilit

a

Co

-op

OV

O

First

Utilit

y

Utilit

yW

are

ho

use

Sco

ttis

hP

ow

er

ED

F

Bri

tish

Ga

s

np

ow

er

E.O

N

SS

E

Med

ium

su

pplie

rs

La

rge

st

su

pplie

rs

Tota

l

Domestic

Customer satisfaction with energy supplier complaints handling 2018

© Quadrangle 2018 15

Figure 6: Complaints distribution across domestic and micro-business suppliers.

QS6. And which supplier did you make this complaint to?

Bases: Domestic complainants (All: 3,080), Micro-business complainants (All: 703).

As in previous years, in 2018 the majority of complaints were raised by telephone,

with 83% of domestic and 83% of micro-business complainants having used this channel

(compared to 84% and 79% respectively in 2016). Only 10% of domestic and 12% of micro-

business complainants contacted their supplier by email (compared to 9% and 17%

respectively in 2016). Other forms of initial contact (e.g. web chat or web forms) were

seldom used.

Billing remained the most common reason for complaining, though significantly less of

a problem than in 2016. While half (51%) of domestic complaints were in relation to billing

problems, this is a significant decrease from 56% in 2016. The decrease in micro-business

billing complaints was also significant and even more substantial, falling from 70% to 59%.

Issues related to gas and electricity meters (not smart or pre-payment meters), remained

the second most common problem area (21% among domestic and 25% among micro-

business complainants). These included meter accuracy issues or problems related to

installation or removal of a meter.

Figure 7 over the page provides details on reasons for complaints being raised in 2017.

Domestic

Micro-business8%

8%

11%

6%

26%

8%

33%

1%

1%

2%

3%

6%

9%

13%

14%

15%

18%

19%

Opus

Utility Warehouse

Co-op

OVO

First Utility

Utilita

npower

EDF

SSE

British Gas

ScottishPower

E.ON

Largest

suppliers

Medium

suppliers

Customer satisfaction with energy supplier complaints handling 2018

© Quadrangle 2018 16

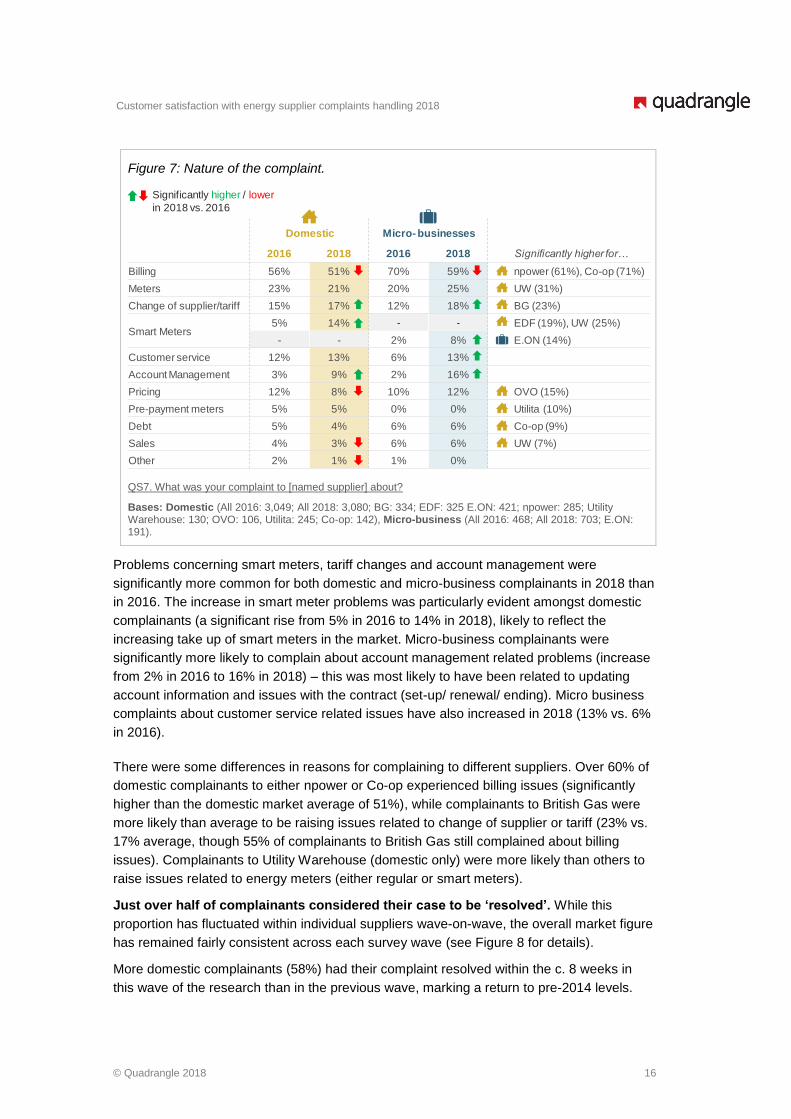

Figure 7: Nature of the complaint.

QS7. What was your complaint to [named supplier] about?

Bases: Domestic (All 2016: 3,049; All 2018: 3,080; BG: 334; EDF: 325 E.ON: 421; npower: 285; Utility Warehouse: 130; OVO: 106, Utilita: 245; Co-op: 142), Micro-business (All 2016: 468; All 2018: 703; E.ON: 191).

Problems concerning smart meters, tariff changes and account management were

significantly more common for both domestic and micro-business complainants in 2018 than

in 2016. The increase in smart meter problems was particularly evident amongst domestic

complainants (a significant rise from 5% in 2016 to 14% in 2018), likely to reflect the

increasing take up of smart meters in the market. Micro-business complainants were

significantly more likely to complain about account management related problems (increase

from 2% in 2016 to 16% in 2018) – this was most likely to have been related to updating

account information and issues with the contract (set-up/ renewal/ ending). Micro business

complaints about customer service related issues have also increased in 2018 (13% vs. 6%

in 2016).

There were some differences in reasons for complaining to different suppliers. Over 60% of

domestic complainants to either npower or Co-op experienced billing issues (significantly

higher than the domestic market average of 51%), while complainants to British Gas were

more likely than average to be raising issues related to change of supplier or tariff (23% vs.

17% average, though 55% of complainants to British Gas still complained about billing

issues). Complainants to Utility Warehouse (domestic only) were more likely than others to

raise issues related to energy meters (either regular or smart meters).

Just over half of complainants considered their case to be ‘resolved’. While this

proportion has fluctuated within individual suppliers wave-on-wave, the overall market figure

has remained fairly consistent across each survey wave (see Figure 8 for details).

More domestic complainants (58%) had their complaint resolved within the c. 8 weeks in

this wave of the research than in the previous wave, marking a return to pre-2014 levels.

2016 2018 2016 2018 Significantly higher for…

Billing 56% 51% 70% 59% npower (61%), Co-op (71%)

Meters 23% 21% 20% 25% UW (31%)

Change of supplier/tariff 15% 17% 12% 18% BG (23%)

Smart Meters5% 14% - - EDF (19%), UW (25%)

- - 2% 8% E.ON (14%)

Customer service 12% 13% 6% 13%

Account Management 3% 9% 2% 16%

Pricing 12% 8% 10% 12% OVO (15%)

Pre-payment meters 5% 5% 0% 0% Utilita (10%)

Debt 5% 4% 6% 6% Co-op (9%)

Sales 4% 3% 6% 6% UW (7%)

Other 2% 1% 1% 0%

Domestic Micro- businesses

Significantly higher / lower

in 2018 vs. 2016

Customer satisfaction with energy supplier complaints handling 2018

© Quadrangle 2018 17

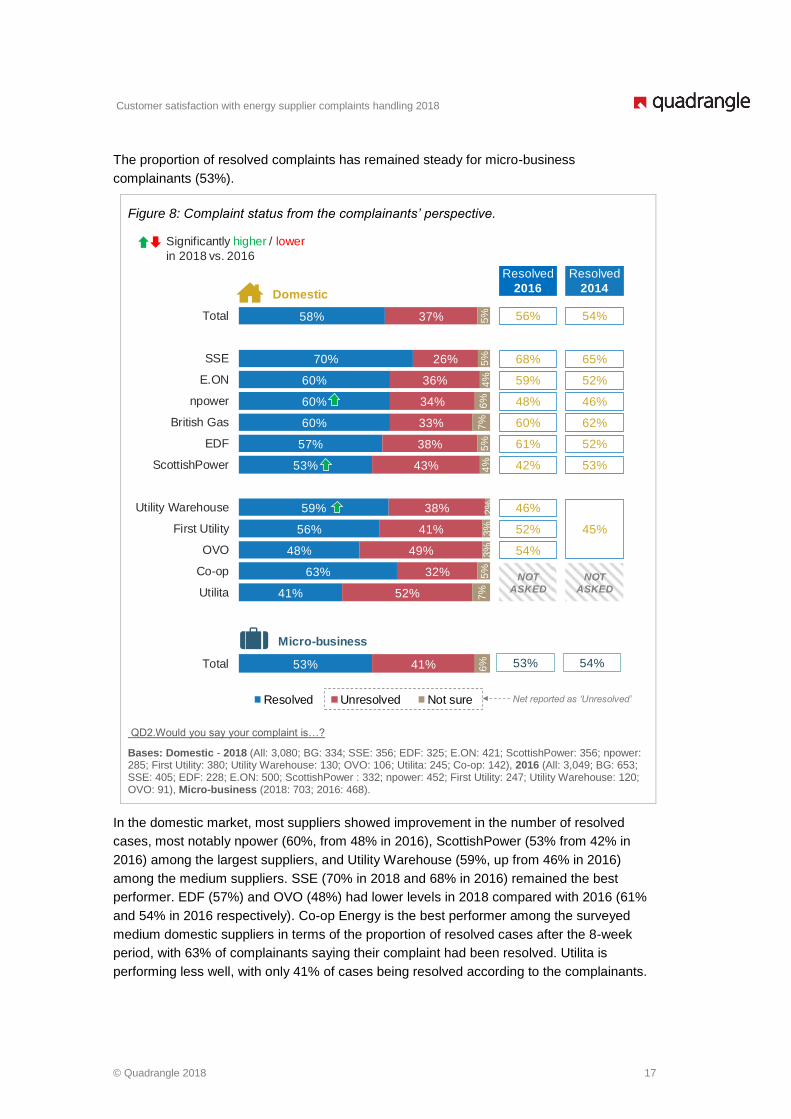

The proportion of resolved complaints has remained steady for micro-business

complainants (53%).

Figure 8: Complaint status from the complainants’ perspective.

QD2.Would you say your complaint is…?

Bases: Domestic - 2018 (All: 3,080; BG: 334; SSE: 356; EDF: 325; E.ON: 421; ScottishPower: 356; npower: 285; First Utility: 380; Utility Warehouse: 130; OVO: 106; Utilita: 245; Co-op: 142), 2016 (All: 3,049; BG: 653; SSE: 405; EDF: 228; E.ON: 500; ScottishPower : 332; npower: 452; First Utility: 247; Utility Warehouse: 120; OVO: 91), Micro-business (2018: 703; 2016: 468).

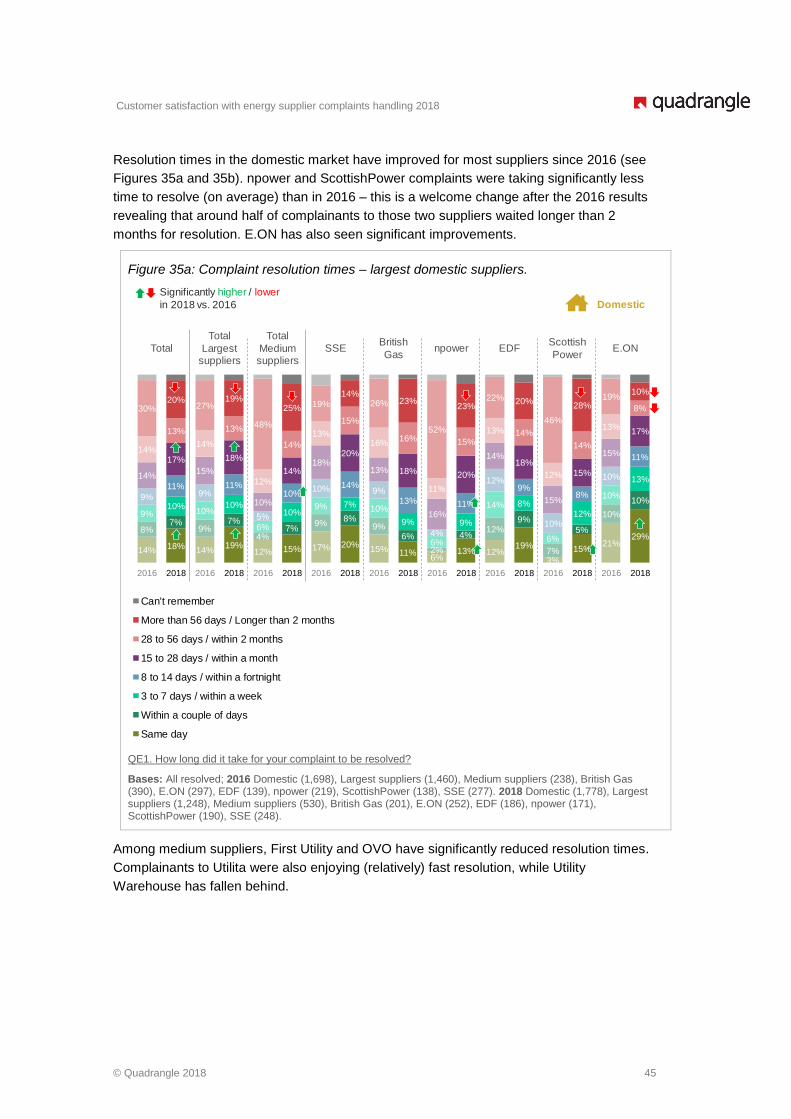

In the domestic market, most suppliers showed improvement in the number of resolved

cases, most notably npower (60%, from 48% in 2016), ScottishPower (53% from 42% in

2016) among the largest suppliers, and Utility Warehouse (59%, up from 46% in 2016)

among the medium suppliers. SSE (70% in 2018 and 68% in 2016) remained the best

performer. EDF (57%) and OVO (48%) had lower levels in 2018 compared with 2016 (61%

and 54% in 2016 respectively). Co-op Energy is the best performer among the surveyed

medium domestic suppliers in terms of the proportion of resolved cases after the 8-week

period, with 63% of complainants saying their complaint had been resolved. Utilita is

performing less well, with only 41% of cases being resolved according to the complainants.

41%

63%

48%

56%

59%

53%

57%

60%

60%

60%

70%

58%

52%

32%

49%

41%

38%

43%

38%

33%

34%

36%

26%

37%

7%

5%

3%

3%

2%

4%

5%

7%

6%

4%

5%

5%

Utilita

Co-op

OVO

First Utility

Utility Warehouse

ScottishPower

EDF

British Gas

npower

E.ON

SSE

Total

53% 41% 6%Total

Resolved

2016Domestic

Micro-business

53%

Resolved Unresolved Not sure

54%

65%

52%

46%

62%

52%

53%

45%

Resolved

2014

54%

56%

68%

59%

48%

60%

61%

42%

46%

52%

54%

NOT

ASKED

NOT

ASKED

Significantly higher / lower

in 2018 vs. 2016

Net reported as ‘Unresolved’

Customer satisfaction with energy supplier complaints handling 2018

© Quadrangle 2018 18

In the micro-business market, Opus, the only medium supplier included in the research, had

the highest number of resolved cases at the time of interview (around two-thirds of

complaints had been resolved at the time of interview). Most of the other micro-business

suppliers had lower numbers of resolved cases than in 2016, with a minor improvement for

EDF.

Note on unresolved cases: within this report, any reference to ‘unresolved’ cases refer to the

net figure of cases identified by complainants as unresolved plus those who were not sure if

their case had been resolved or not. This was consistent with the 2016 wave of the

research. Thus 42% of cases in the domestic market, and 47% of cases in the micro-

business market, were deemed unresolved.

Customer satisfaction with energy supplier complaints handling 2018

© Quadrangle 2018 19

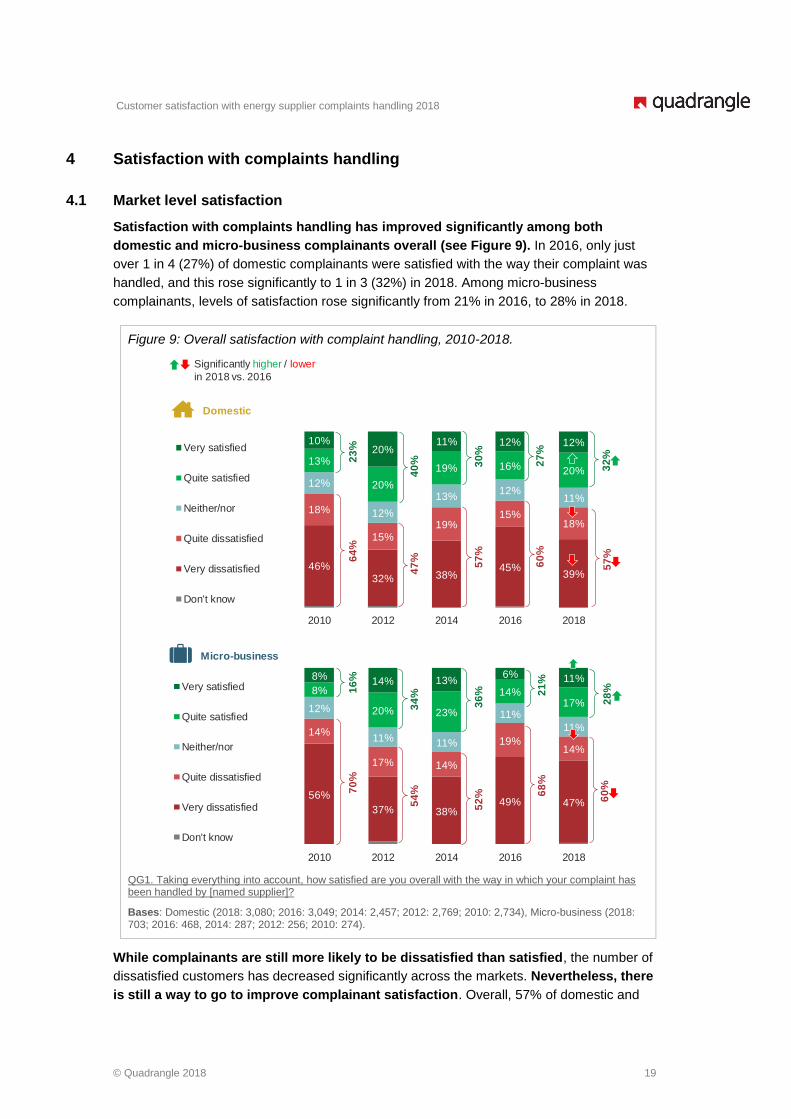

4 Satisfaction with complaints handling

4.1 Market level satisfaction

Satisfaction with complaints handling has improved significantly among both

domestic and micro-business complainants overall (see Figure 9). In 2016, only just

over 1 in 4 (27%) of domestic complainants were satisfied with the way their complaint was

handled, and this rose significantly to 1 in 3 (32%) in 2018. Among micro-business

complainants, levels of satisfaction rose significantly from 21% in 2016, to 28% in 2018.

Figure 9: Overall satisfaction with complaint handling, 2010-2018.

QG1. Taking everything into account, how satisfied are you overall with the way in which your complaint has been handled by [named supplier]?

Bases: Domestic (2018: 3,080; 2016: 3,049; 2014: 2,457; 2012: 2,769; 2010: 2,734), Micro-business (2018: 703; 2016: 468, 2014: 287; 2012: 256; 2010: 274).

While complainants are still more likely to be dissatisfied than satisfied, the number of

dissatisfied customers has decreased significantly across the markets. Nevertheless, there

is still a way to go to improve complainant satisfaction. Overall, 57% of domestic and

46%32% 38%

45%39%

18%

15%19%

15%18%

12%

12%

13%12%

11%

13%

20%

19% 16% 20%

10%20%

11% 12% 12%

2010 2012 2014 2016 2018

Very satisfied

Quite satisfied

Neither/nor

Quite dissatisfied

Very dissatisfied

Don't know

60

%2

7%

57

%3

0%

47

%4

0%

64

%2

3%

56%

37% 38%49% 47%

14%

17% 14%

19%14%

12%

11% 11%

11%

11%

8%

20% 23%

14%17%

8%14% 13%

6% 11%

2010 2012 2014 2016 2018

Very satisfied

Quite satisfied

Neither/nor

Quite dissatisfied

Very dissatisfied

Don't know

68

%2

1%

52

%3

6%

54

%3

4%

70

%1

6%

Domestic

Micro-business

57

%3

2%

60

%2

8%

Significantly higher / lower

in 2018 vs. 2016

Customer satisfaction with energy supplier complaints handling 2018

© Quadrangle 2018 20

60% of micro-business complainants were dissatisfied with their complaint handling

experience. Furthermore, the strength of complainants’ feelings of dissatisfaction is evident

given the high level of ‘very’ dissatisfied complainants: 39% domestic and 47% micro-

business.

4.2 Supplier level satisfaction

There were significant differences in levels of satisfaction and dissatisfaction with

how complaints were handled across suppliers in the domestic market since 2016.

Encouragingly, the worst domestic performers from 2016, npower and ScottishPower, have

shown significant uplifts in overall satisfaction, owing in part to the improvements in the

number of resolved cases. Clearly, their efforts to implement improvements after the

deterioration in satisfaction over the 2014-2016 period, have had a positive impact on the

experiences of their domestic complainants, though there is still a long way to go as the

majority, close to 2 in 3, were dissatisfied with how their complaint had been handled. Figure

10a below shows satisfaction levels among the largest suppliers in the domestic market.

Figure 10a: Overall satisfaction with complaint handling – largest domestic suppliers.

QG1. Taking everything into account, how satisfied are you overall with the way in which your complaint has been handled by [named supplier]?

Bases: 2016 – Domestic Total (3,049), Largest suppliers Total (2,570), Medium suppliers Total (479), British Gas (653), SSE (405), EDF (228), E.ON (500), ScottishPower (332), npower (452). 2018 – Domestic Total (3,080), Largest suppliers Total (2,077), Medium suppliers Total (1,003), British Gas (334), SSE (356), EDF (325), E.ON (421), ScottishPower (356), npower (285).

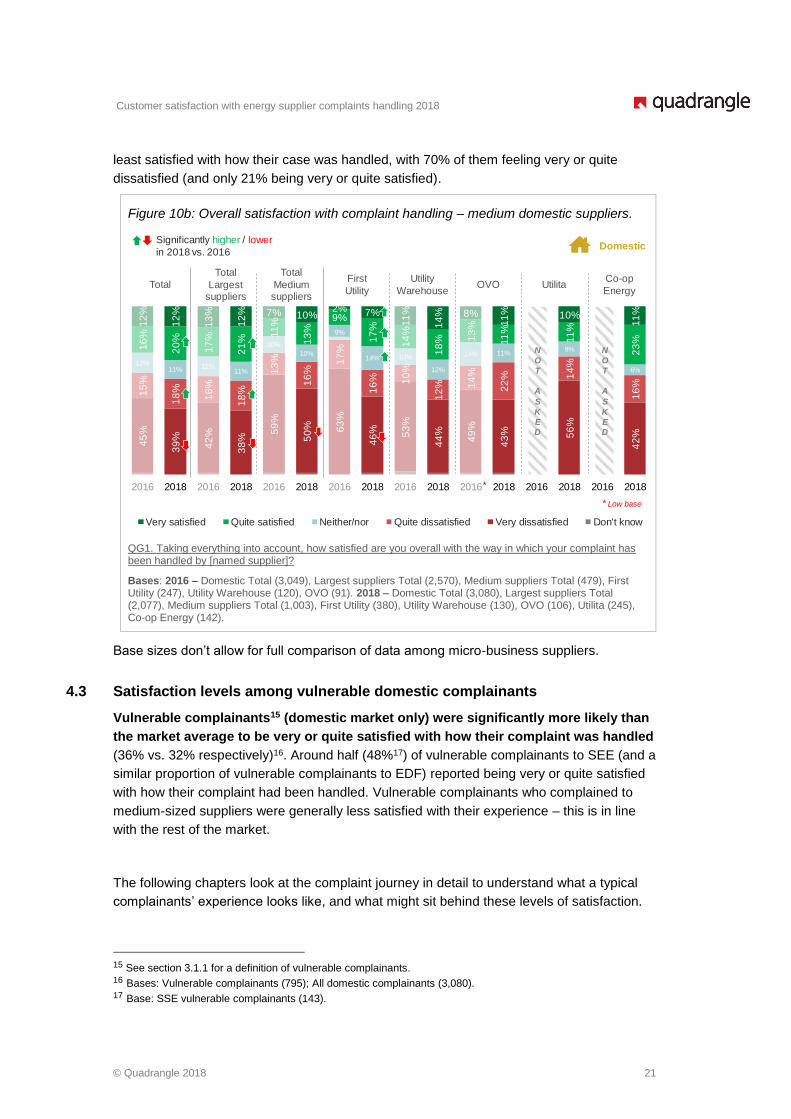

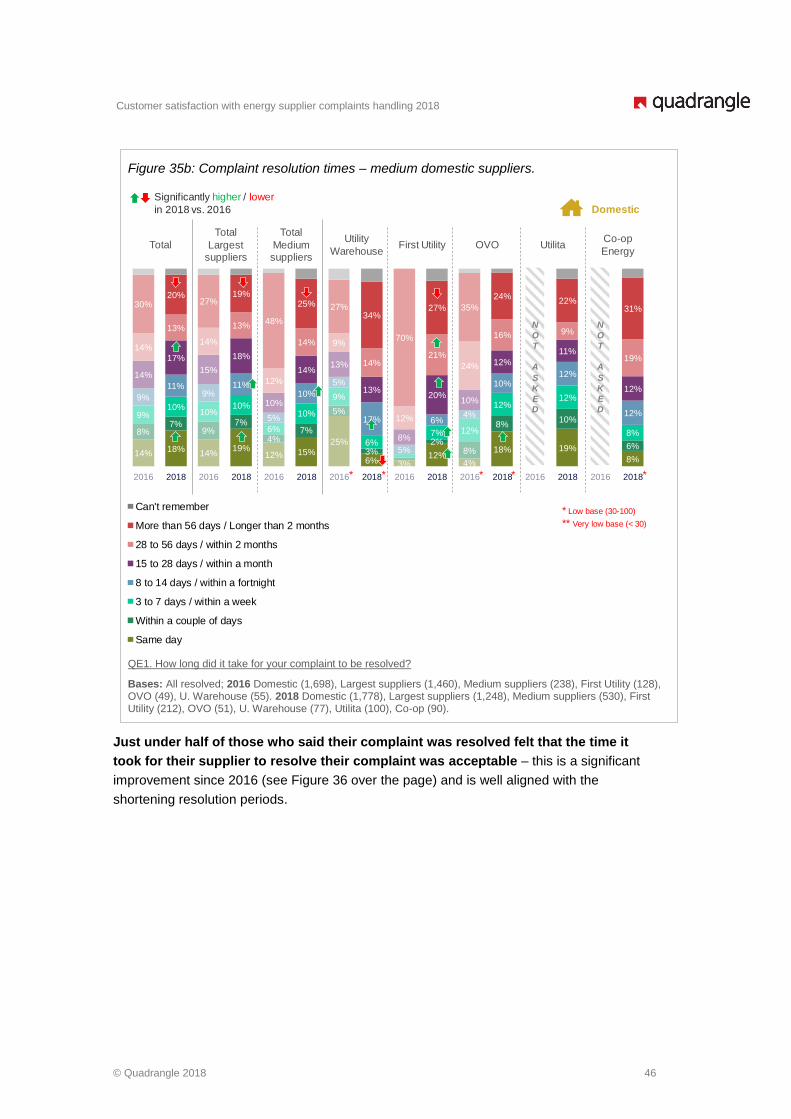

Among domestic medium suppliers (see Figure 10b below), First Utility has seen a

significant uplift in satisfaction with complaints handling, and others have seen marginal

improvements. It is also encouraging to see a decrease in levels of complainants who were

very dissatisfied with their experience (where comparisons with 2016 can be made). Co-op

is the top performer (34% satisfied, 58% dissatisfied), while complainants to Utilita were

45

%

39

%

42

%

38

%

59

%

50

%

26

%

27

%

34

%

35

%

35

%

30

% 41

%

45

%

67

%

41

%

64

%

47

%

15

%

18

%

16

%

18

%

13

%

16

%

14

%

16

% 16

%

19

%

16

%

22

% 17

%

17

%

16

%

21

%

13

%

16

%12%

11% 12%11%

10%

10%

16% 12%

14% 10% 15% 12%

12% 10%

6%

11%

9%

11%

16

%

20

%

17

%

21

%

11

%

13

%

23

%

26

% 19

%

21

%

15

%

22

% 18

%

19

%

8%2

0%

9%

19

%

12

%

12

%

13

%

12

% 7% 10%

20

%

18

%

16

%

15

%

17

%

14

%

11

% 10%3% 8% 4% 6%

2016 2018 2016 2018 2016 2018 2016 2018 2016 2018 2016 2018 2016 2018 2016 2018 2016 2018

Domestic

Total

Total

Largest suppliers

Total

Medium suppliers

SSE E.ON EDFBritish

Gasnpower

Scottish

Power

Very satisfied Quite satisfied Neither/nor Quite dissatisfied Very dissatisfied Don't know

Significantly higher / lower

in 2018 vs. 2016

Customer satisfaction with energy supplier complaints handling 2018

© Quadrangle 2018 21

least satisfied with how their case was handled, with 70% of them feeling very or quite

dissatisfied (and only 21% being very or quite satisfied).

Figure 10b: Overall satisfaction with complaint handling – medium domestic suppliers.

QG1. Taking everything into account, how satisfied are you overall with the way in which your complaint has been handled by [named supplier]?

Bases: 2016 – Domestic Total (3,049), Largest suppliers Total (2,570), Medium suppliers Total (479), First Utility (247), Utility Warehouse (120), OVO (91). 2018 – Domestic Total (3,080), Largest suppliers Total (2,077), Medium suppliers Total (1,003), First Utility (380), Utility Warehouse (130), OVO (106), Utilita (245), Co-op Energy (142).

Base sizes don’t allow for full comparison of data among micro-business suppliers.

4.3 Satisfaction levels among vulnerable domestic complainants

Vulnerable complainants15 (domestic market only) were significantly more likely than

the market average to be very or quite satisfied with how their complaint was handled

(36% vs. 32% respectively)16. Around half (48%17) of vulnerable complainants to SEE (and a

similar proportion of vulnerable complainants to EDF) reported being very or quite satisfied

with how their complaint had been handled. Vulnerable complainants who complained to

medium-sized suppliers were generally less satisfied with their experience – this is in line

with the rest of the market.

The following chapters look at the complaint journey in detail to understand what a typical

complainants’ experience looks like, and what might sit behind these levels of satisfaction.

15 See section 3.1.1 for a definition of vulnerable complainants. 16 Bases: Vulnerable complainants (795); All domestic complainants (3,080). 17 Base: SSE vulnerable complainants (143).

DomesticSignificantly higher / lower

in 2018 vs. 2016

*

45

%

39

%

42

%

38

%

59

%

50

% 63

%

46

% 53

%

44

%

49

%

43

%

0%

56

%

0

42

%

15

%

18

%

16

%

18

%

13

%

16

%

17

%

16

% 10

%

12

% 14

%

22

%

0%

14

%

0

16

%

12%11% 12%

11%

10%

10%

9%

14% 10%

12%

14% 11%

0%

9%

0

6%

16

%

20

%

17

%

21

%

11

%

13

%

9%

17

%

14

%

18

% 13

%

11

%

0%

11

%

0

23

%

12

%

12

%

13

%

12

% 7% 10%2% 7%

11

%

14

% 8%

11

%

0%

10%

0

11

%

2016 2018 2016 2018 2016 2018 2016 2018 2016 2018 2016 2018 2016 2018 2016 2018

Total

Total

Largest suppliers

Total

Medium suppliers

First

Utility

Utility

WarehouseOVO Utilita

Co-op

Energy

N

O

T

A

S

K

E

D

N

O

T

A

S

K

E

D

* Low base

Very satisfied Quite satisfied Neither/nor Quite dissatisfied Very dissatisfied Don't know

Customer satisfaction with energy supplier complaints handling 2018

© Quadrangle 2018 22

5 The complaint journey

5.1 Introducing the journey

The complaint ‘journey’ was explored by identifying the core stages in the complaints

process, also shown in Figure 11 below:

1. Start of the journey ▪ Finding contact details

▪ Registration and confirmation/ acknowledgement

▪ Next steps and timescales

2. Subsequent contact ▪ Communication following initial contact to reach problem

resolution

3. Escalation and third

party involvement

▪ Potential escalation to a more senior member of staff

and/or referral to the Energy Ombudsman

4. Resolution ▪ Including receiving confirmation/ acknowledgement of

resolution

5. Closure ▪ Receiving an explanation of what went wrong or an

apology

▪ Receiving compensation, if applicable

Each stage was investigated in detail to understand what the process was like from the

complainants’ perspective, and what impact each element had on overall satisfaction with

complaints handling. The questions asked about each stage of the complaint journey

reflected the requirements of Ofgem’s Complaint Handling Standards (CHS) which suppliers

must adhere to.

Figure 11: The complaint journey.

Independent advice can

be sought at any point

Finding

contact details

Lodging

complaint

Registration /

confirmation of complaint

Subsequent contact

with supplier to reach a problem

resolution

Referral to Energy

Ombudsman

Confirmation of

process / next steps, and timescales

Escalation

Formal

resolution confirmation

Resolution

Explanation of what

went wrong

Apology

Compensation

Start of the journeySubsequent

contactEscalation Resolution Closure and impact

COMPLAINT JOURNEY STAGES:

STEPS IN EACH STAGE:

Customer satisfaction with energy supplier complaints handling 2018

© Quadrangle 2018 23

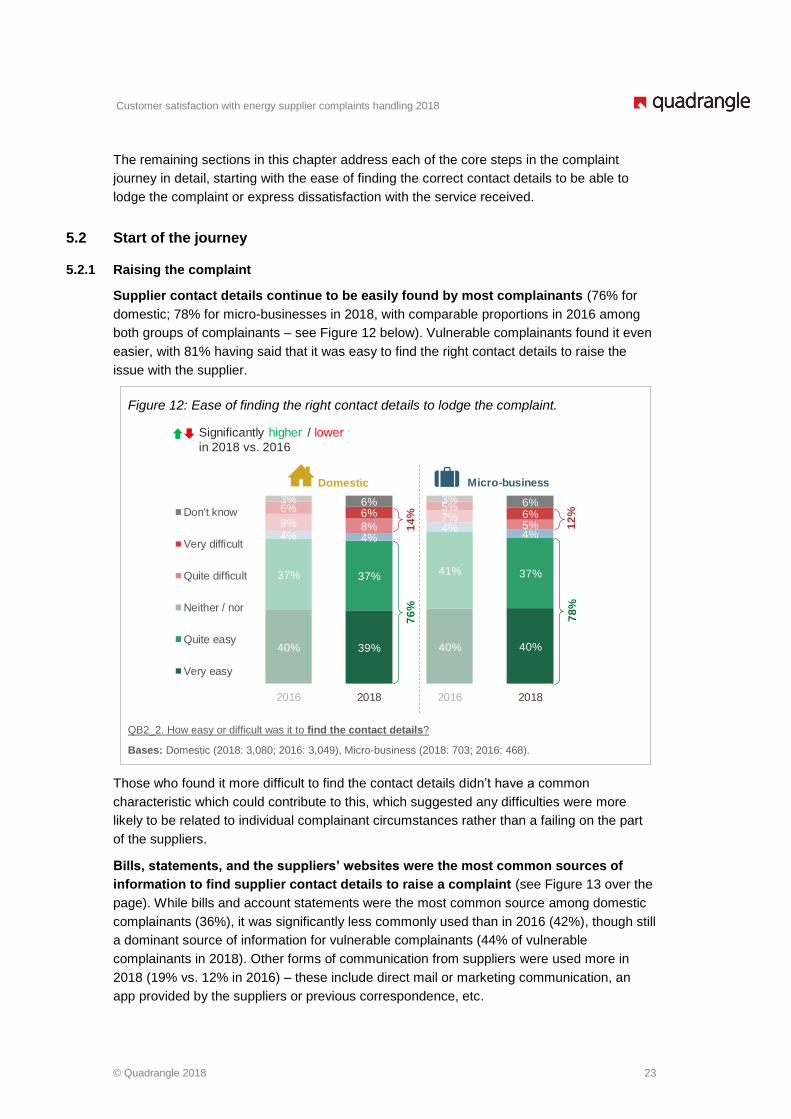

The remaining sections in this chapter address each of the core steps in the complaint

journey in detail, starting with the ease of finding the correct contact details to be able to

lodge the complaint or express dissatisfaction with the service received.

5.2 Start of the journey

5.2.1 Raising the complaint

Supplier contact details continue to be easily found by most complainants (76% for

domestic; 78% for micro-businesses in 2018, with comparable proportions in 2016 among

both groups of complainants – see Figure 12 below). Vulnerable complainants found it even

easier, with 81% having said that it was easy to find the right contact details to raise the

issue with the supplier.

Figure 12: Ease of finding the right contact details to lodge the complaint.

QB2_2. How easy or difficult was it to find the contact details?

Bases: Domestic (2018: 3,080; 2016: 3,049), Micro-business (2018: 703; 2016: 468).

Those who found it more difficult to find the contact details didn’t have a common

characteristic which could contribute to this, which suggested any difficulties were more

likely to be related to individual complainant circumstances rather than a failing on the part

of the suppliers.

Bills, statements, and the suppliers’ websites were the most common sources of

information to find supplier contact details to raise a complaint (see Figure 13 over the

page). While bills and account statements were the most common source among domestic

complainants (36%), it was significantly less commonly used than in 2016 (42%), though still

a dominant source of information for vulnerable complainants (44% of vulnerable

complainants in 2018). Other forms of communication from suppliers were used more in

2018 (19% vs. 12% in 2016) – these include direct mail or marketing communication, an

app provided by the suppliers or previous correspondence, etc.

Domestic Micro-business

40% 39% 40% 40%

37% 37%41% 37%

4% 4%4%

4%9% 8%

7%5%

6% 6%5%

6%

3% 6% 3% 6%

2016 2018 2016 2018

Don't know

Very difficult

Quite difficult

Neither / nor

Quite easy

Very easy

14

%7

6%

12

%7

8%

Significantly higher / lower

in 2018 vs. 2016

Customer satisfaction with energy supplier complaints handling 2018

© Quadrangle 2018 24

Figure 13: Source of contact details.

QB1. Thinking about when you contacted [named supplier] in [Complaint month], where did you find the contact information you needed to make the complaint?

Bases: Domestic (2018: 3,080; 2016: 3,049), Micro-business (2018: 703; 2016: 468).

Micro-business complainants typically found the supplier’s contact details on their bills or

account statements (55% in 2018) – this is fairly consistent with 2016, when other sources

of information were used comparatively little.

While registering the complaint was easy for most, 1 in 3 still experienced difficulties

– this hasn’t changed since 2016 (see Figure 14). The experience of registering a

complaint among vulnerable complainants is comparable to the market average.

Figure 14: Ease of registering the complaint.

QB2_2. How easy or difficult was it to register your complaint with [named supplier]?

Bases: Domestic (2018: 3,080; 2016: 3,049), Micro-business (2018: 703; 2016: 468).

Domestic Micro-business

27% 27% 25% 26%

29% 30% 33% 28%

5% 5% 5%7%

15% 16% 14% 15%

21% 18% 19% 20%

3% 4% 3% 4%

2016 2018 2016 2018

Don't know

Very difficult

Quite difficult

Neither / nor

Quite easy

Very easy

34

%5

7%

35

%5

4%

Significantly higher / lower

in 2018 vs. 2016

Domestic Micro-business

Significantly higher / lower

in 2018 vs. 2016

62%

18%

14%

3%

0%

3%

2%

55%

15%

16%

6%

4%

2%

5%

2016

2018

42%

33%

12%

7%

1%

5%

2%

36%

33%

19%

8%

2%

3%

4%

Bill or account statement

Supplier website

Other form of communication with supplier

Other website

Referred from other department

Other

Can't remember2016

2018

Customer satisfaction with energy supplier complaints handling 2018

© Quadrangle 2018 25

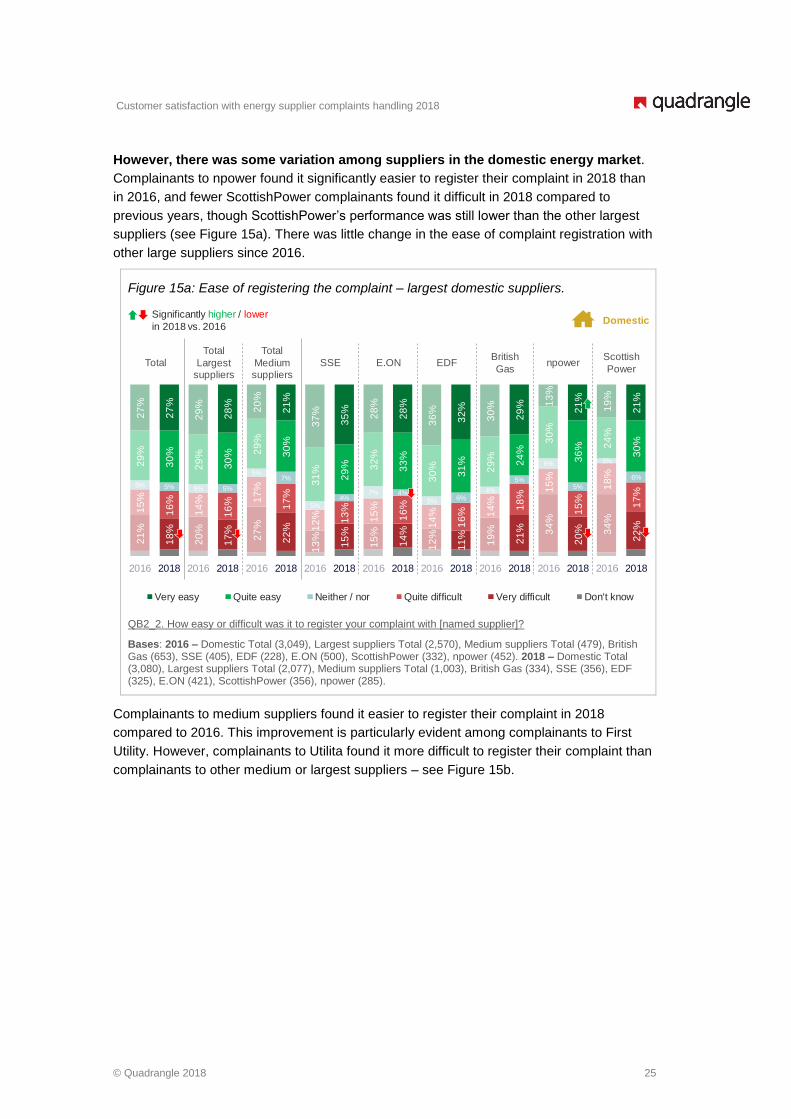

However, there was some variation among suppliers in the domestic energy market.

Complainants to npower found it significantly easier to register their complaint in 2018 than

in 2016, and fewer ScottishPower complainants found it difficult in 2018 compared to

previous years, though ScottishPower’s performance was still lower than the other largest

suppliers (see Figure 15a). There was little change in the ease of complaint registration with

other large suppliers since 2016.

Figure 15a: Ease of registering the complaint – largest domestic suppliers.

QB2_2. How easy or difficult was it to register your complaint with [named supplier]?

Bases: 2016 – Domestic Total (3,049), Largest suppliers Total (2,570), Medium suppliers Total (479), British Gas (653), SSE (405), EDF (228), E.ON (500), ScottishPower (332), npower (452). 2018 – Domestic Total (3,080), Largest suppliers Total (2,077), Medium suppliers Total (1,003), British Gas (334), SSE (356), EDF (325), E.ON (421), ScottishPower (356), npower (285).

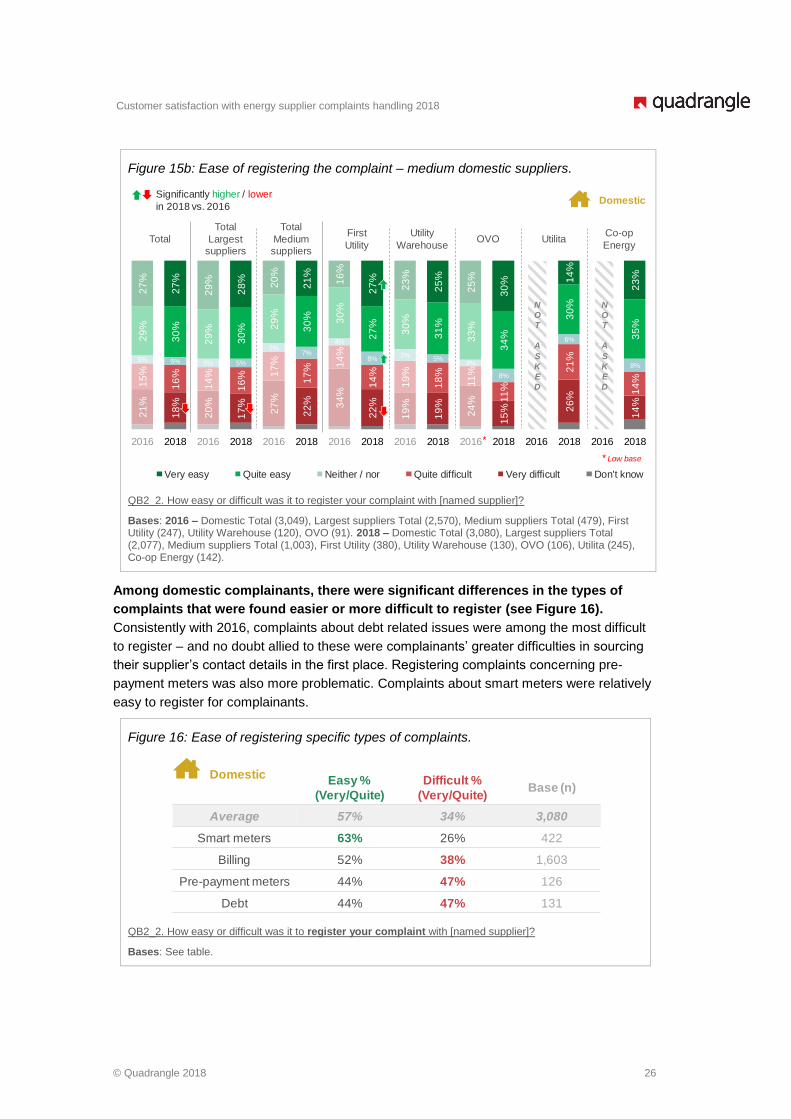

Complainants to medium suppliers found it easier to register their complaint in 2018

compared to 2016. This improvement is particularly evident among complainants to First

Utility. However, complainants to Utilita found it more difficult to register their complaint than

complainants to other medium or largest suppliers – see Figure 15b.

21

%

18

%

20

%

17

%

27

%

22

%

13

%

15

%

15

%

14

%

12

%

11

%

19

%

21

% 34

%

20

% 34

%

22

%

15

%

16

%

14

%

16

% 17

%

17

%

12

% 13

%

15

%

16

%

14

%

16

% 14

%

18

%

15

%

15

%

18

%

17

%

5% 5% 5% 5%

5%7%

5%4%

7% 4%

5% 6%4%

5%

6%

5%

3%

6%

29

%

30

%

29

%

30

% 29

%

30

%

31

%

29

% 32

%

33

%

30

%

31

%

29

%

24

%

30

%

36

% 24

%

30

%

27

%

27

%

29

%

28

%

20

%

21

%

37

%

35

%

28

%

28

%

36

%

32

%

30

%

29

% 13

%

21

%

19

%

21

%

2016 2018 2016 2018 2016 2018 2016 2018 2016 2018 2016 2018 2016 2018 2016 2018 2016 2018

Domestic

Total

Total

Largest suppliers

Total

Medium suppliers

SSE E.ON EDFBritish

Gasnpower

Scottish

Power

Very easy Quite easy Neither / nor Quite difficult Very difficult Don't know

Significantly higher / lower

in 2018 vs. 2016

Customer satisfaction with energy supplier complaints handling 2018

© Quadrangle 2018 26

Figure 15b: Ease of registering the complaint – medium domestic suppliers.

QB2_2. How easy or difficult was it to register your complaint with [named supplier]?

Bases: 2016 – Domestic Total (3,049), Largest suppliers Total (2,570), Medium suppliers Total (479), First Utility (247), Utility Warehouse (120), OVO (91). 2018 – Domestic Total (3,080), Largest suppliers Total (2,077), Medium suppliers Total (1,003), First Utility (380), Utility Warehouse (130), OVO (106), Utilita (245), Co-op Energy (142).

Among domestic complainants, there were significant differences in the types of

complaints that were found easier or more difficult to register (see Figure 16).

Consistently with 2016, complaints about debt related issues were among the most difficult

to register – and no doubt allied to these were complainants’ greater difficulties in sourcing

their supplier’s contact details in the first place. Registering complaints concerning pre-

payment meters was also more problematic. Complaints about smart meters were relatively

easy to register for complainants.

Figure 16: Ease of registering specific types of complaints.

QB2_2. How easy or difficult was it to register your complaint with [named supplier]?

Bases: See table.

DomesticEasy %

(Very/Quite)

Difficult %

(Very/Quite)Base (n)

Average 57% 34% 3,080

Smart meters 63% 26% 422

Billing 52% 38% 1,603

Pre-payment meters 44% 47% 126

Debt 44% 47% 131

Domestic

Very easy Quite easy Neither / nor Quite difficult Very difficult Don't know

Significantly higher / lower

in 2018 vs. 2016

*

21

%

18

%

20

%

17

%

27

%

22

% 34

%

22

%

19

%

19

%

24

%

15

%

0%

26

%

0%

14

%

15

%

16

%

14

%

16

% 17

%

17

% 14

%

14

%

19

%

18

%

11

%

11

%

0%

21

%

0%

14

%

5% 5% 5% 5%

5%7%

4%

8%7%

5%4%

8%

0%

6%

0%

8%

29

%

30

%

29

%

30

% 29

%

30

% 30

%

27

%

30

%

31

%

33

%

34

%

0%

30

%

0%

35

%

27

%

27

%

29

%

28

%

20

%

21

%

16

%

27

%

23

%

25

%

25

%

30

%

0%

14

%

0%

23

%

2016 2018 2016 2018 2016 2018 2016 2018 2016 2018 2016 2018 2016 2018 2016 2018

Total

Total

Largest suppliers

Total

Medium suppliers

First

Utility

Utility

WarehouseOVO Utilita

Co-op

Energy

N

O

T

A

S

K

E

D

N

O

T

A

S

K

E

D

* Low base

Customer satisfaction with energy supplier complaints handling 2018

© Quadrangle 2018 27

Among the c. third of complainants who found it difficult to have their complaint

registered, the most common reasons involved not being able to get through to the

right person or department and being passed around (see Figures 17a). Comparison

against 2016 showed this is a growing problem for domestic complainants (57% in 2016 vs.

66% in 2018). Problems related to the complaint not being properly acknowledged or

understood were less common in 2018 than in 2016. This suggests that once complainants

do get through, the level of service they receive is improving. However, domestic suppliers

need to address this emerging issue of complainants having difficulties accessing the right

staff to address their case. The experience of vulnerable complainants is consistent with

this.

Figure 17a: Main reasons it was difficult to register the complaint – domestic complaints.

QB3. What would you say was the MAIN reason why you found it difficult to have your complaint registered?

Bases: Domestic complainants who found it difficult to register their complaint (2018: 1,046; 2016: 1,131).

Micro-businesses were more likely to struggle in 2018 with having their complaint

acknowledged as a problem than in 2016 (33% in 2018 vs. 17% in 2016). In particular, they

found that the supplier claimed the complaint they were raising was not actually an issue

(see Figure 17b). From a complainant point of view this can be quite frustrating as it sets a

negative tone for the rest of the process.

33%

33%

15%

15%

9%

8%

3%

12%

5%

7%

43%

36%

12%

12%

6%

6%

1%

14%

3%

3%

I could not get through to the right person / department

I was passed around

I was put through to the wrong person / department

Supplier claimed there was no problem

Refused to put me through to complaints department

My written complaint was not acknowledged

Supplier never got back to me after I initially raised theissue

The phone was always engaged

No understanding of problem

Rude staff

2016

2018

NOT ABLE TO

GET THROUGH TOTHE RIGHT PERSON

LACK

OF RECOGNITION

GETTING THROUGH

STAFF RELATED

ISSUES

Domestic

2016 57%

2018 66%

2016 30%

2018 23%

Significantly higher / lower

in 2018 vs. 2016

2016 11%

2018 6%

Customer satisfaction with energy supplier complaints handling 2018

© Quadrangle 2018 28

Figure 17b: Main reasons it was difficult to register the complaint – micro-business complaints.

QB3. What would you say was the MAIN reason why you found it difficult to have your complaint registered?

Bases: Micro-business complainants who found it difficult to register their complaint (2018: 255; 2016: 163).

5.2.2 Confirmation of process and next steps

Around 6 in 10 complainants received a formal acknowledgement of their complaint,

consistently with 2016. Encouragingly, the proportion of complainants stating they have

not received a formal confirmation has decreased significantly among domestic

complainants – this may be a result of a higher number of complaints being resolved on the

same day (18% in 2018 vs.14% in 2016 among resolved cases, see Figure 34 in section

5.2.2), meaning that there is not a need to send out those types of communications.

Figure 18: Formal confirmation/ acknowledgment of the complaint.

QB4. I will now read out a few statements related to what might or might not have happened when you first contacted [named supplier] about your complaint. As I read each statement out, please say YES or NO to indicate whether or not it happened to you.

Bases: Domestic (2018: 3.080; 2016: 3,049), Micro-business (2018: 703; 2016: 468).

47%

42%

28%

9%

4%

4%

1%

2%

9%

2%

42%

38%

15%

23%

6%

7%

1%

5%

4%

3%

I could not get through to the right person / department

I was passed around

I was put through to the wrong person / department

Supplier claimed there was no problem

Refused to put me through to complaints department