Cynthia Steer Chief Research Strategist Managing Director, Fixed Income Research Telephone: 203-656-6716 [email protected]State Association of County Retirement Systems Fall Conference November 13-16, 2007

Section II The Case for Emerging Market Debt in 2007

Section III Understanding Emerging Market Countries as the New, Powerful Institutional Investor

3

Section I

The Case for Emerging Markets in 2004

4

Cartography and Investment Topography

5

Cartography and Investment Topography

In 2004, two definitions were useful in dividing the world and setting investment strategies and asset allocation targets:

Developed Markets

Emerging Markets

6

What is a Developed Market?

The implication is:

A nation that is industrialized (e.g., a well-developed manufacturing sector), has substantive infrastructure, and a well-developed service sector

A nation that has a per capita income higher than $9,655

A nation that has universal education and significant health indicators on infant mortality, life expectancy, and literacy

7

What is an Emerging Market?

The official definition:

An economy with low-to-middle per capita income as defined by the World Bank (i.e., less than $9,656 minimum GNP per capita)

Investable market cap is low relative to its most recent Gross Domestic Product (GDP)

8

What is an Emerging Market?

The implication is:

It is a nation that is in rapid transition, increasing in size, activity, or level of sophistication

It is a nation that is making an effort to change and improve its economy, as well as provide an infrastructure in order to become a developed nation

9

Cartography and Investment Topography (2004)

Like nature, nations gradually or glacially evolve from emerging to developed

And a few move back

What contributes to a successful evolution is a complex question as tectonic plates shift slowly

Why does it matter from an investment perspective?

10

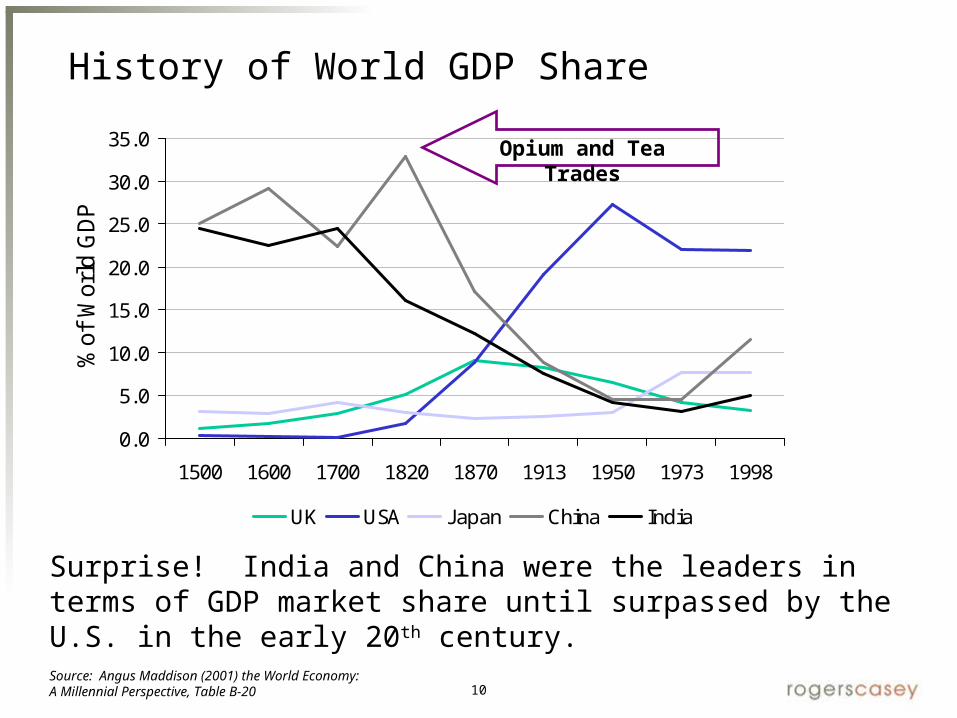

History of World GDP Share

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

1500 1600 1700 1820 1870 1913 1950 1973 1998

% o

f W

orld

GDP

UK USA J apan China India

Surprise! India and China were the leaders in terms of GDP market share until surpassed by the U.S. in the early 20th century. Source: Angus Maddison (2001) the World Economy:A Millennial Perspective, Table B-20

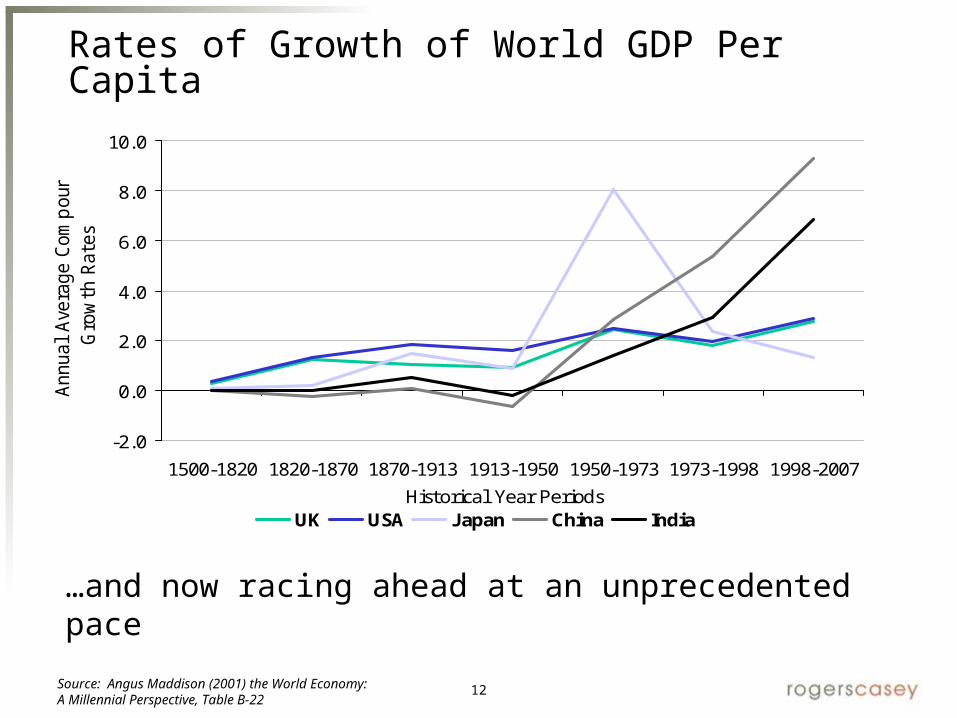

Source: Angus Maddison (2001) the World Economy:A Millennial Perspective, Table B-22

13

Developed, Emerging, or Hegemon?

Nation Time Period Source of Power or Wealth

Portugal 1494 – 1580 Dominance in navigation

Holland 1580 – 1688 Control of credit and money

Britain 1688 – 1792 Textiles and command of the sea

Britain 1815 – 1914 Industrial Supremacy and railroads

United States 1945 – 1971Petroleum and internal combustion engine

A highly evolved nation with overwhelming demographics does not always graduate to a developed nation

14

Cartography and Investment Topography (2004)

Economists and investors are always seeking to develop a set of metrics to identify a country’s future status

That is, which countries will move from:

Emerging to Developed to something else

However, there is no defined set of rules to determine who will and will not evolve

Are there catalysts?

15

Benchmarks as Investment Topography

Current industry practice is to construct portfolios using benchmarks as maps or guides

Are our current maps pre-Columbus, seismic sensors, or GPS?

16

A View of Our World in the Pre-Columbus Era

Fortunately, early investors did not use maps for guides or they might not have gotten there

17

A View of Our World from the English Colonies

Where would the U.S. be if our forefathers only focused on investing in the original 13 colonies and didn’t think about the frontier?

18

A View of Our World After the Louisiana Purchase

Or called it quits after Napoleon sold us the Louisiana Purchase?

19

So, What is the Lesson?

Historically, the most successful investors have sought future rather than past growth

Would you have invested in the Erie Canal?

If you are the typical institutional investor, probably not!

20

Cartography and Investment Topography

State of the art today…very Americentric

Very benchmark-aware

Average U.S. plan sponsor holds the following portfolio:

40 – 50% U.S. Equity

15 – 20% Non-U.S. Equity

15 – 30% Fixed Income

0 – 15% Alternatives

21

Market Capitalization Weights As Maps

10.1% 9.7%

52.6%

0.2% 0.4% 0.2%0%

10%

20%

30%

40%

50%

60%

UnitedKingdom

J apan USA India China Russia

Capi

taliz

atio

n W

eigh

ts w

ithi

n th

e M

SCI A

CWI F

ree

Source: RIMES Online

Constructing an investment map for tomorrow and today’s portfolio based on benchmarks is investing in the rearview mirror

Select Developed and Emerging Markets as of 2004

22

2004 Outlook

12.5%9.3% 9.7%

40.1%

46.7%

30.9%

0%

10%

20%

30%

40%

50%

UnitedKingdom

J apan USA India China Russia

5 Ye

ar C

umul

ativ

e Pr

ojec

ted

Real

GDP

Gro

wth

As an investor seeking to grow assets, wouldn’t you seek future rather than historical growth?

Source: National Governments, Consensus Economics, Economist Intelligence Unit, Datastream

Five Year Projected Growth Rates of Select Developed and Emerging Markets

23

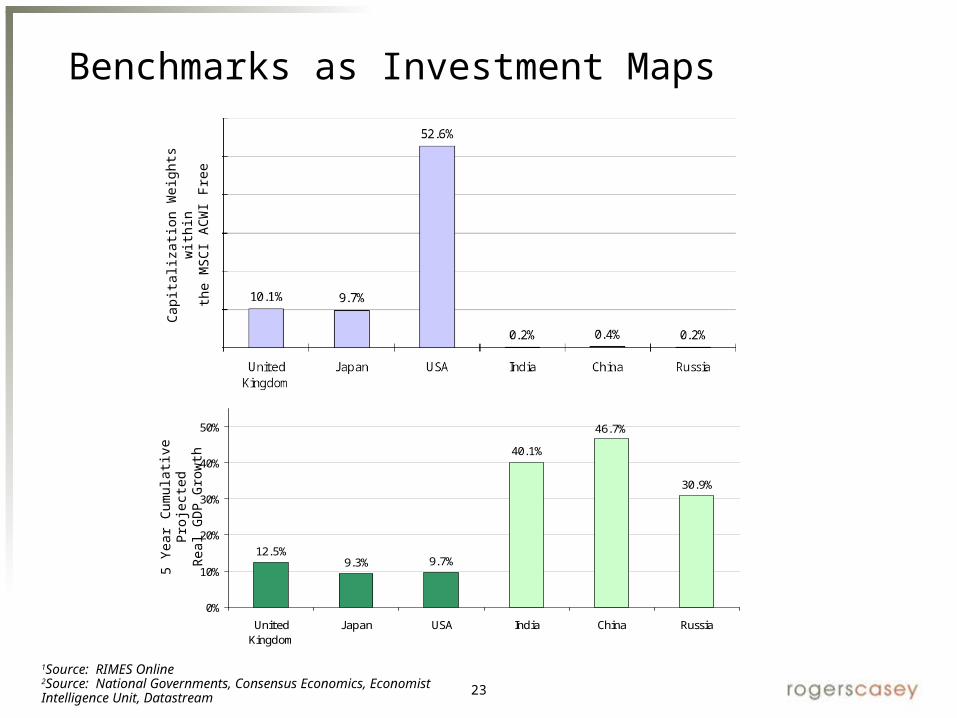

Benchmarks as Investment Maps

12.5%9.3% 9.7%

40.1%

30.9%

46.7%

0%

10%

20%

30%

40%

50%

UnitedKingdom

J apan USA India China Russia

1Source: RIMES Online2Source: National Governments, Consensus Economics, Economist Intelligence Unit, Datastream

Cap

italiz

ati

on

Weig

hts

wit

hin

the M

SC

I A

CW

I Fr

ee

5 Y

ear

Cu

mu

lati

ve

Pro

ject

ed

Real G

DP G

row

th

24

S&P 500 Index vs. Nominal GDP Growth

0

12

3

4

56

7

8

910

11

12De

c-48

Dec-

50

Dec-

52

Dec-

54

Dec-

56

Dec-

58

Dec-

60

Dec-

62

Dec-

64

Dec-

66

Dec-

68

Dec-

70

Dec-

72

Dec-

74

Dec-

76

Dec-

78

Dec-

80

Dec-

82

Dec-

84

Dec-

86

Dec-

88

Dec-

90

Dec-

92

Dec-

94

Dec-

96

Dec-

98

Dec-

00

Dec-

02

Cum

ulat

ive

Log-

Adju

sted

Ret

urn

S&P 500 Index Nominal GDP Growth

Developed markets are positively correlated with domestic GDP growth but emerging markets may not be

Source: Nominal GDP Growth data provided courtesy of Bureau of Economic Analysis (BEA)

25

Section II

The Case for Emerging Market Debt in 2007

26

Cartography and Investment Topography

27

Asset Allocation with Possibly the Wrong Map

Public Plans Anticipating an Increase/ Decrease in Strategic Allocations

2%

9%

28%31%

22%

-15%

-28%

-2%0%0%

Equities Fixed Income Real Estate Private Equity Hedge Funds

Source: JPMorgan Asset Management

By Asset Class

% anticipating an increase in allocations

% anticipating a decrease in allocations

28

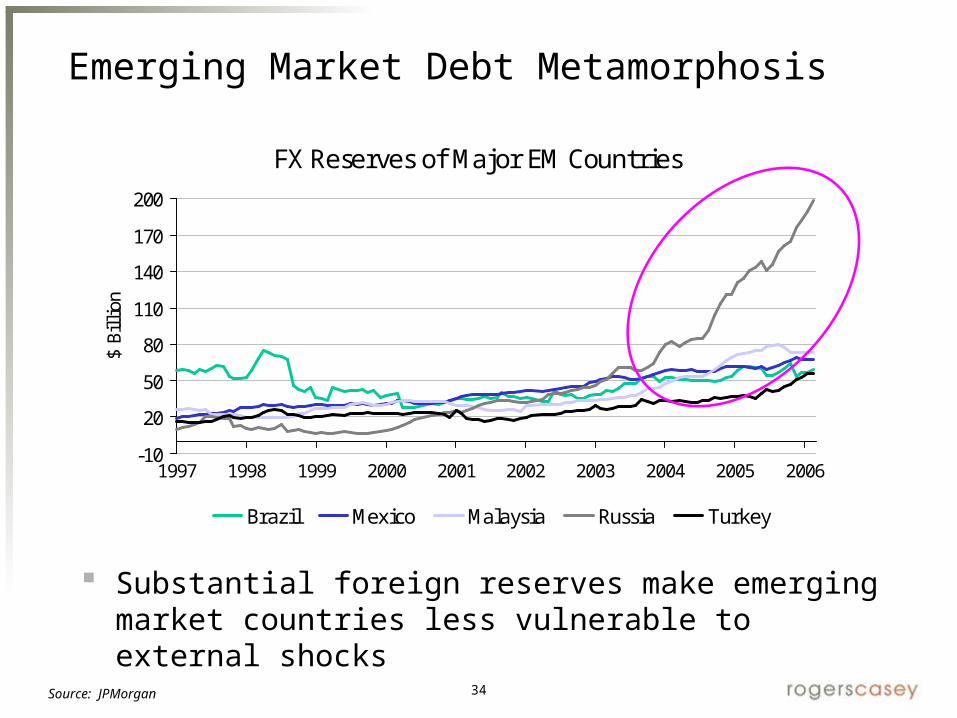

FX Reserves of Major EM Countries

-10

20

50

80

110

140

170

200

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006

$ Bi

llio

n

Brazil Mexico Malaysia Russia Turkey

Emerging Market Metamorphosis

We all read about global liquidity and its sources but generally don’t ponder its implications

Source: JPMorgan

29

Emerging or Developed?

FranceThailand

30

Emerging or Developed?

London Morocco

31

Trivia

Approximately 25% of the total number of world cranes is situated in one single city. Which city is it?

Up until 1998, the trophy for the tallest building has been in developed countries, mainly the United States. Currently how many of the top ten tallest buildings are in developed countries?

True or False. In 2005, more space missions have been launched by developed countries than emerging countries?

Of the top 40 countries by growth in manufacturing output, how many are emerging markets?

How many of the world’s top five billionaires are EM country nationals and who currently leads that list?

Emerging Market Metamorphosis

32

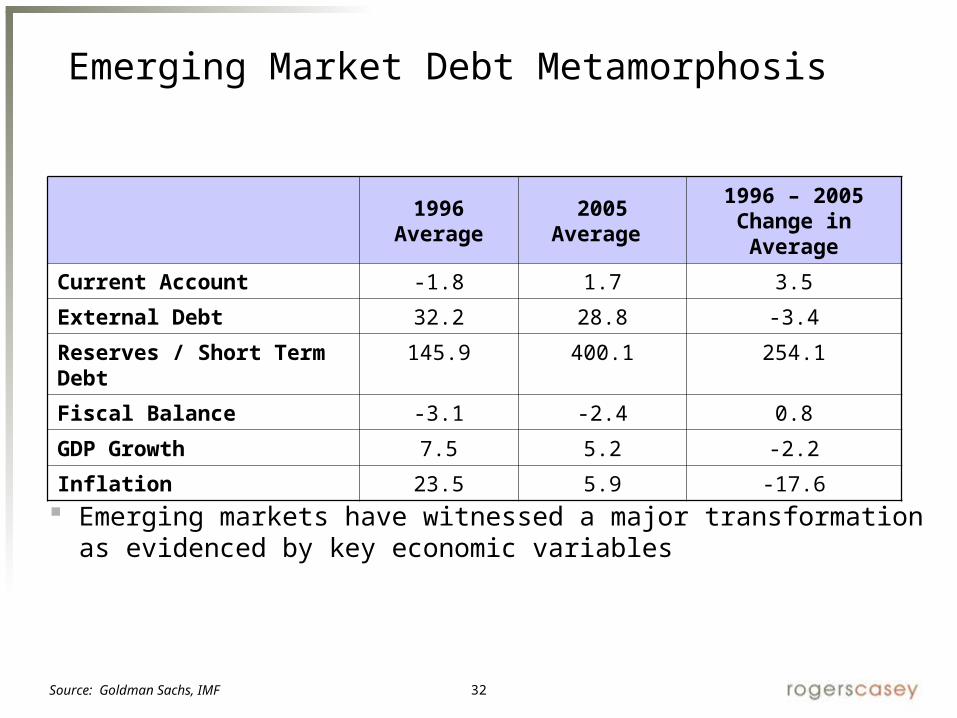

1996 Average

2005 Average

1996 – 2005Change in Average

Current Account -1.8 1.7 3.5

External Debt 32.2 28.8 -3.4

Reserves / Short Term Debt

145.9 400.1 254.1

Fiscal Balance -3.1 -2.4 0.8

GDP Growth 7.5 5.2 -2.2

Inflation 23.5 5.9 -17.6

Emerging markets have witnessed a major transformation as evidenced by key economic variables

Favorable rating trends have extended beyond sovereign debt

Source: S&P, JPMorgan Source: S&P, JPMorgan

39

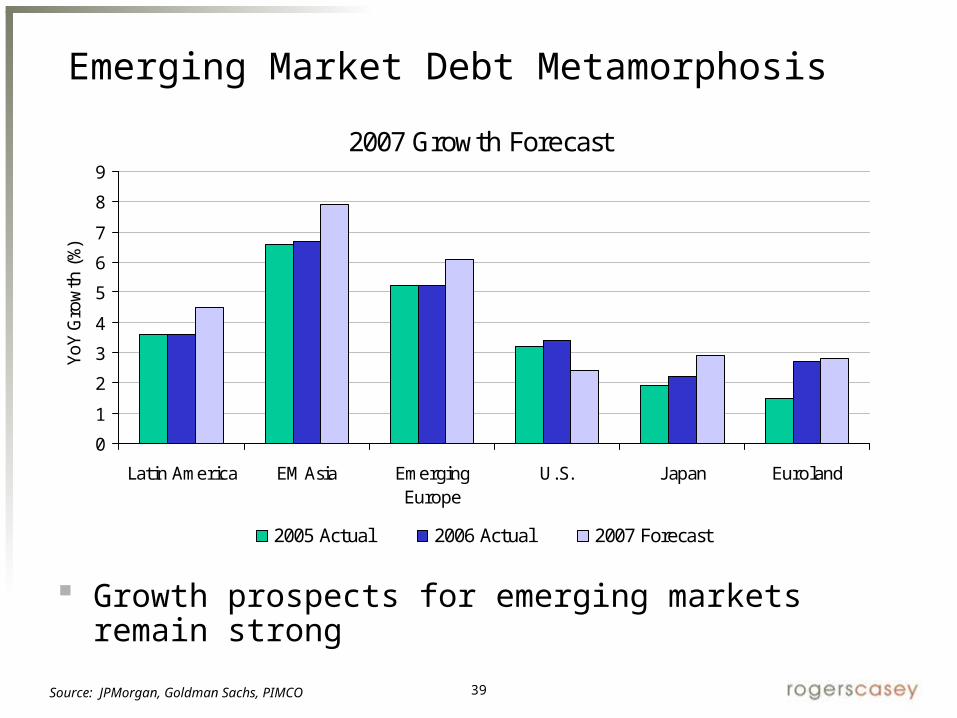

2007 Growth Forecast

0

1

2

3

4

5

6

7

8

9

Latin America EM Asia EmergingEurope

U.S. J apan Euroland

YoY

Gro

wth

(%)

2005 Actual 2006 Actual 2007 Forecast

Source: JPMorgan, Goldman Sachs, PIMCO

Growth prospects for emerging markets remain strong

Emerging Market Debt Metamorphosis

40

The correlation between economic activity in the large developed economies and total global growth has fallen, as emerging countries have become more important growth engines of the global economy

Relationship of G7 Growth to World Growth

-1

0

1

2

3

4

5

6

1980 1985 1990 1995 2000 2005

World Real GDP Growth G7 Real GDP Growth Correlation of G7 growth to World Growth

Source: IMF, PIMCO

Emerging Market Metamorphosis

41

Implications for the Investment Opportunity

Comparative Performance 2-Months as of August 31, 2007

-4

-3

-2

-1

0

1

2

3

J PM GBI-EM

(LC)

J PM EMBI

Global

Citigroup HY Credit Suisse

Leveraged

Loan

LB Aggregate

%

Is emerging market debt the new “safe haven” as opposed to U.S. credit? How much is too much in emerging markets? What is true growth?

Comparative Performance 1-Month as of August 31, 1998

-30

-25

-20

-15

-10

-5

0

5

J PM EMBI Global Citigroup HY Credit Suisse

Leveraged Loan

LB Aggregate

%

42

Section III

Understanding Emerging Market Countries as the New, Powerful Institutional Investor

43

Cartography and Investment Topography

44

Cartography and Investment Topography

Western financial markets create acronyms based on:

Economics

Liquidity and capital flows

Organizational structures

In era of vast change in size and influence of liquidity pools, important and instructional to reconsider basic assumptions

EMEA (Europe, Middle East and Africa) and MENA (Middle East, North Africa) are examples of this

Context of discussion centered on changing missions of World Bank, IMF, IFC (e.g., in North/South dialogues migrating to South/South investment)

45

Our Investment Topography Definition:

Europe, the Middle East, and Africa, usually abbreviated to EMEA, is a regional designation used for government, marketing, and business purposes. It is particularly common amongst North American based companies, who often divide their international operations into the following regions:

– The Americas, being North and South America (AMER)

– North America (NORAM)

– Europe, the Middle East, and Africa (EMEA)

– Asia Pacific and Japan (APAC or APJ)

– Brazil, Russia, India, and China (BRIC)

Increasingly, companies are separating their Eastern European business from the rest of Europe, and refer to the EEMEA (Emerging Europe, Middle East, and Africa) region as separate from the European region

46

New Investment Topography

Definition:

The term MENA, for Middle East and North Africa

– An acronym often used in academic and business writing

– Generally covers an extensive region, extending from Morocco in northwest Africa, to Iran in southwest Asia

– Generally includes all the Arab Middle East and North Africa countries, including Iran but not Turkey

47

Our Investment Topography

EMEA GDP (as % of world GDP) and Market Capitalization (as % of MSCI AC World Index Free)

1998 - 2007*

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007

(% )

GDP Market Cap

Source: MSCI and U.S. Department of Agriculture

* 2007 data is for the year to September.

48

EMEA Country GDP and Market Capitalization Growth (%)2003 - 2007

Source: MSCI and U.S. Department of Agriculture

Changing Investment Topography

CountryCumulative

GDPAnnualized

GDPCumulative Market Cap

Annualized Market Cap

Czech Republic 27.9 5.6 898 180

Hungary 20.0 4.0 430 86

Poland 28.0 5.6 895 179

Russia 39.4 7.9 1198 240

Turkey 38.3 7.7 924 185

Israel 23.2 4.6 337 67

Jordon 33.2 6.6 257 51

Egypt 28.3 5.7 2131 426

Morocco 23.1 4.6 658 132

South Africa 22.3 4.5 272 54

Total EMEA 30.9 6.2 552 110

49

Size and Shape of Capital Flows in Rapid Evolution

50

Changing Destination of Capital Flows

51

Changing Rapidly from EMEA to MENA

52

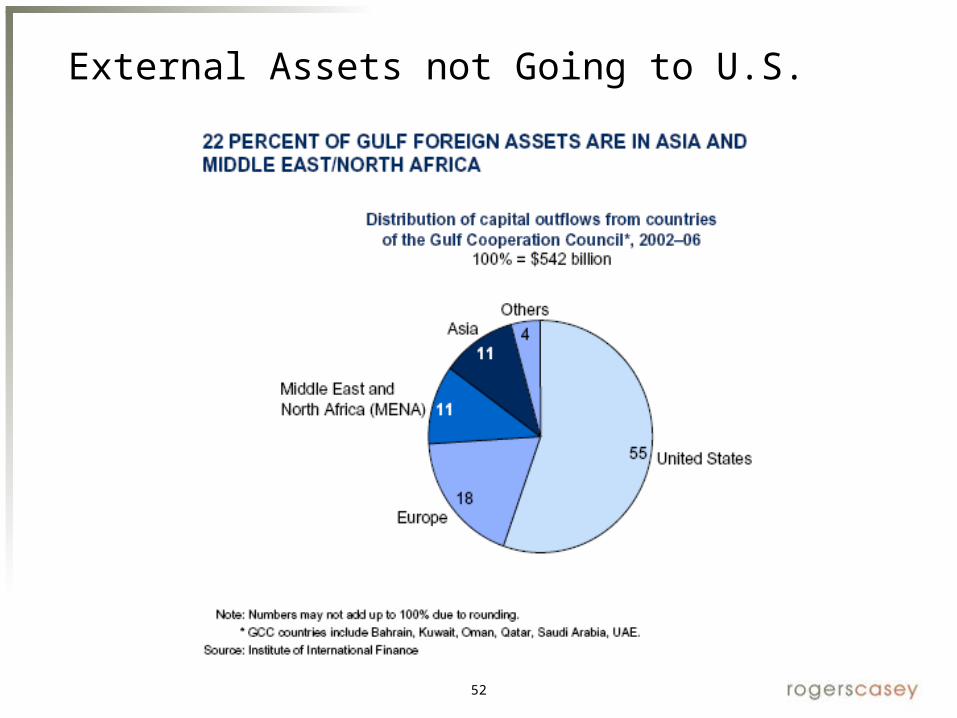

External Assets not Going to U.S.

53

And Increasingly Finding Local Homes

54

With Local Structures

55

The keystone to Islamic finance is the idea that investments must be made in a manner that is compliant with Shariah, a set of rules and laws, collectively governing economic, social, political, and cultural aspects of Islamic society.

Shariah prohibits riba, or the charging of interest, thus introducing a challenge to traditional investment mechanisms such as bonds or mortgages.

Most interpretations of Shariah state that in any investment arrangement, risks must be shared by all parties and equal risk-reward profiles must exist. Therefore, a predetermined interest rate is considered unacceptable (haram).

Sukuk – similar to an asset-backed bond, Sukuk pays investors over the life of the “bond” directly from leases, profits, or sales of tangible assets, such as property, infrastructure, equipment, or business ventures.

And Local Connotations

56

Sound Bytes About Islamic Finance

Up until this point, Islamic financial innovations have captured the attention of the clientele interested in Shariah compliant products. Going forward, these instruments will likely have a broader appeal.

In the near future, we will likely witness the creation of a much broader spectrum of Shariah compliant financial instruments, including structured products, hedging tools with features similar to the conventional derivatives markets, an increase in short-term liquidity products, and a wider variety of asset classes.

Shariah compliant securities will also attract attention from socially conscious investors across the globe. Shariah prohibits investment in any business that is deemed unethical, such as gambling, alcohol, and casinos.

Islamic finance offers a unique opportunity for bridging financial/cultural differences between Islamic and Western nations.

57

Implications for U.S. Pension Funds

Rapid redistribution of capital flows implies the following:

Mispricing of risk and return - old versus new thinking

Inappropriate weightings of region

Information inefficiency

Premium for early movers

BUT…old style analysis not as relevant

MENA investment dominated by real estate, infrastructure, plus hedge funds and private equity, not necessarily public equity

NECESSITY to consider new structures, including Shariah compliant bonds and investment vehicles

FEWER traditional managers (even hedge funds) able to take advantage, so finding regional capabilities will probably be important

IMPORTANT to know what you don’t know and to update frequently

58

Changing Investment Topography: Old Style Analyses Don’t Tell Story

EMEA GDP and Market Capitalization Annual Growth1998 - 2007*

MSCI Emerging Markets Index Regional BreakdownSeptember 2002

Market Cap: $475 Billion

EMEA

26%

Asia

58%

Latin America

16%

Changing Investment Topography

Source: MSCI

60

EMEA Country BreakdownSeptember 2007

Market Cap: $812 BillionHungary

4% Israel

9%

J ordan

0%

Poland

7%

Egypt

3%

South Africa

28%

Czech Republic

3%

Turkey

7%

Morocco

1%

Russia

37%

MSCI Emerging Markets Index Regional BreakdownSeptember 2007

Market Cap: $3,354 Billion

EMEA

24%

Asia

58%

Latin America

16%

Source: MSCI

Changing Investment Topography

61

EMEA Country Breakdown by GDP2002

Total GDP: $1,174 Billion

Hungary

4%

Israel

10%

J ordan

1%

Poland

15%

Egypt

9%

South Africa

12%

Czech Republic

5%

Turkey

17%

Morocco

3%

Russia

37%

Source: U.S. Department of Agriculture

Changing Investment Topography

EMEA Country Breakdown by GDP2007*

Total GDP: $1,538 Billion

Hungary

4%

Israel

9%

J ordan

1%

Poland

14%

Egypt

9%

South Africa

11%

Czech Republic

5%

Turkey

18%

Morocco

3%

Russia

37%

* 2007 data is for the year to September.

62

Old Versus New Topography

Growth in MENA lost in rapid growth in Asia and investor focus

Current index reflects public market capitalization but not true GDP growth and flows to private equity and new wealth

Country representation is limited

Plan sponsors lack time and focus to reposition portfolio

Alternatives include GDP/flow weighted indices and regional mandates for infrastructure, hedge funds, currency, and private equity as well as public equity

63

Old Versus New Topography

Facts:

0.3% of global equity markets but young demographics of 700 million

Resource provider to Europe and U.S.

Rapidly expanding and NEW infrastructure

Home to innovation in biotech and technology

Deep and liquid stock markets with over 200 global companies

Fast growing sovereign wealth funds (SWFs)

64

Aging Demographics but MENA is Young

Source: UN (2005)

65

With New Buildings and New Infrastructure…

Source: Factset, UBS

66

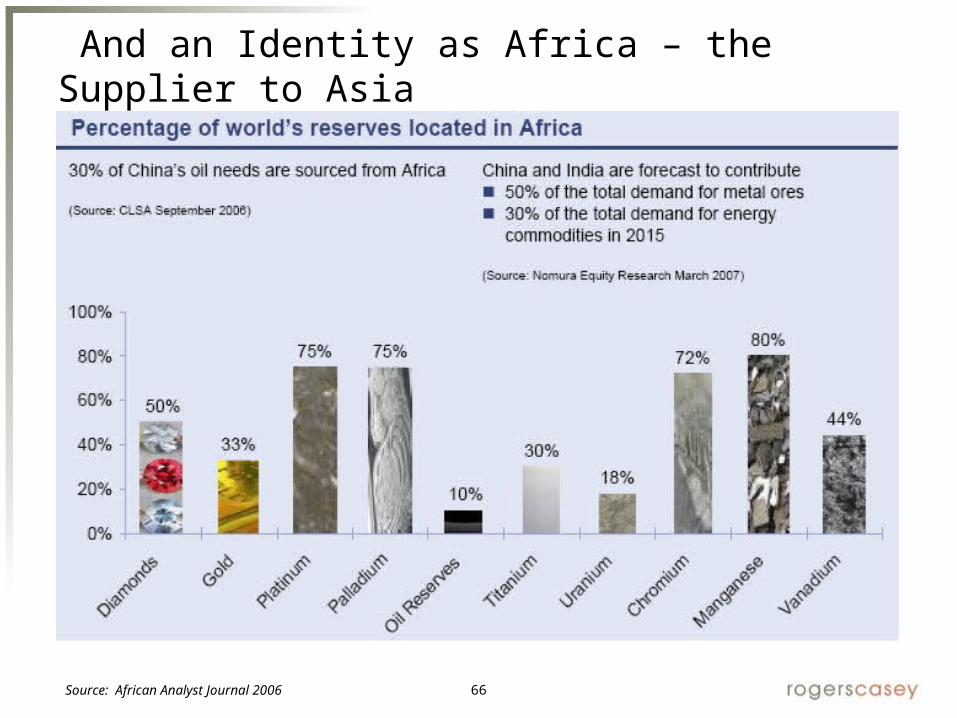

And an Identity as Africa – the Supplier to Asia

Source: African Analyst Journal 2006

67

So is this Risky?

Source: Factset

68

There is More to the Region than Just Oil…

Source: JPMorgan, Merrill Lynch estimates

69

Other Changing Topographies: Asia

70

Cartography and Investment Topography: Asia

Asia also growing rapidly

Surpluses are growing rapidly

Sovereign Wealth Funds have been created

Investment policy and governance are slowly being considered

Asian topography more centered on debt culture and ASEAN Plus 6

71

But Its Tectonic Plates Are Different

72

Investment Topography Changing but Slowly

73

Changing Investment Topography: Old Style Analyses Don’t Tell Story

ASEAN Plus 6 (Ex. U.S.) Plus New Zealand GDP and Market Capitalization Annual Growth

ASEAN Plus 6 (Ex. U.S.) Plus New ZealandCountry Breakdown, September 2007

Market Cap: $5,610 Billion

Hong Kong5%

South Korea9%

Malaysia1%

New Zeland0%

Phillipines0% Singapore

3%Thailand

1%

Indonesia1%

China10%

Japan52%

Australia17%

MSCI AC World Index (Ex. U.S.) Regional Breakdown, September 2007

Market Cap: $18,756 Billion

North America, 6%

Developed Europe

53%

ASEAN +6 (Ex. USA)

+ New Zealand

30%

EMEA

4%

Latin America

4%EM Asia Ex. Asean +6

3%

Source: MSCI

Changing Investment Topography

76

Implications for U.S. Pension Plans

Central bank reserves and sovereign wealth funds will be managed differently than petrodollar neighbors

Slow, cautious intra-region cooperation will be the norm

Asset allocation and SWF governance will evolve over time

ASEAN accords shed light on process (first steps, interlocking swap agreements to provide members liquidity relative to 1998 and purchases of regional sovereign debt)

ASEAN nations still engaging China, Japan, India, and Australasia

Policy focused on capital preservation and liquidity

Culture of debt and real estate rather than public and private equity

77

Summary

Surpluses of emerging markets are transforming to powerful investors

Risk/return appetites and perspectives differ from U.S. pension plans

Looking forward, it is imperative not to make assumptions viewing the world from our perspective…the consequences could be significant