12

Czech Republic Czech Republic Eurostrategy, state of play VIII, 2007 Eurostrategy, state of play VIII, 2007 Sofia, September 2007 Ludek Niedermayer, CNB, Prague .cz

| Date post: | 30-Dec-2015 |

| Category: |

Documents |

| Upload: | cecil-stuart-hampton |

| View: | 214 times |

| Download: | 0 times |

Czech RepublicCzech RepublicEurostrategy, state of play VIII, 2007Eurostrategy, state of play VIII, 2007

Sofia, September 2007

Ludek Niedermayer, CNB, Prague

www. .cz

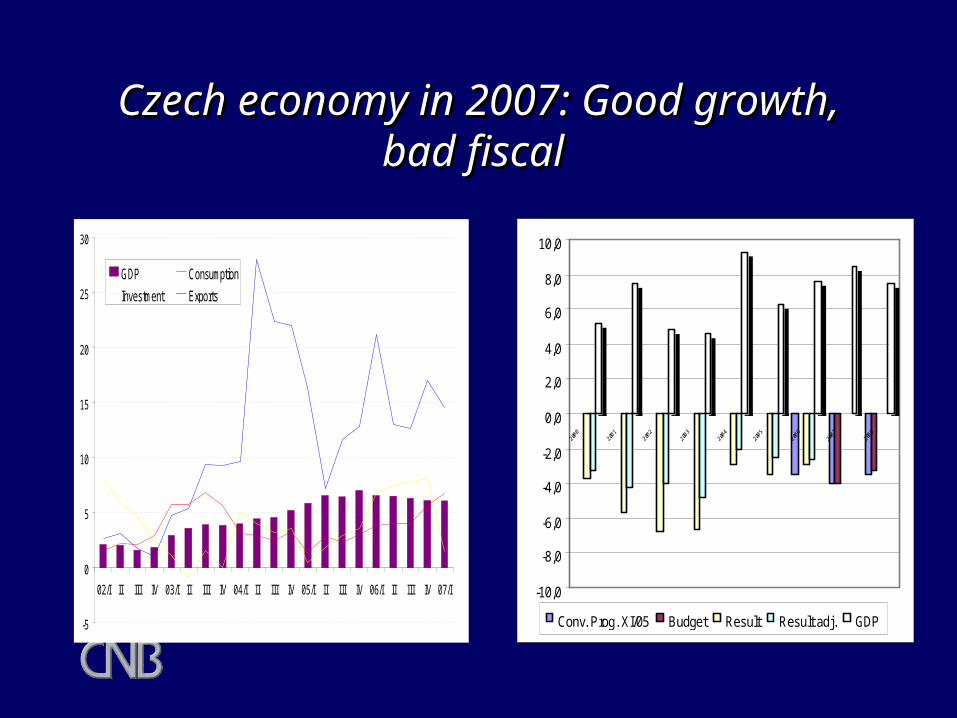

Czech economy in 2007: Good Czech economy in 2007: Good growth, bad fiscal growth, bad fiscal

-10,0

-8,0

-6,0

-4,0

-2,0

0,0

2,0

4,0

6,0

8,0

10,0

Conv. Prog. XI/05 Budget Result Result adj. GDP-5

0

5

10

15

20

25

30

02/I II III IV 03/I II III IV 04/I II III IV 05/I II III IV 06/I II III IV 07/I

GDP Consumption

Investment Exports

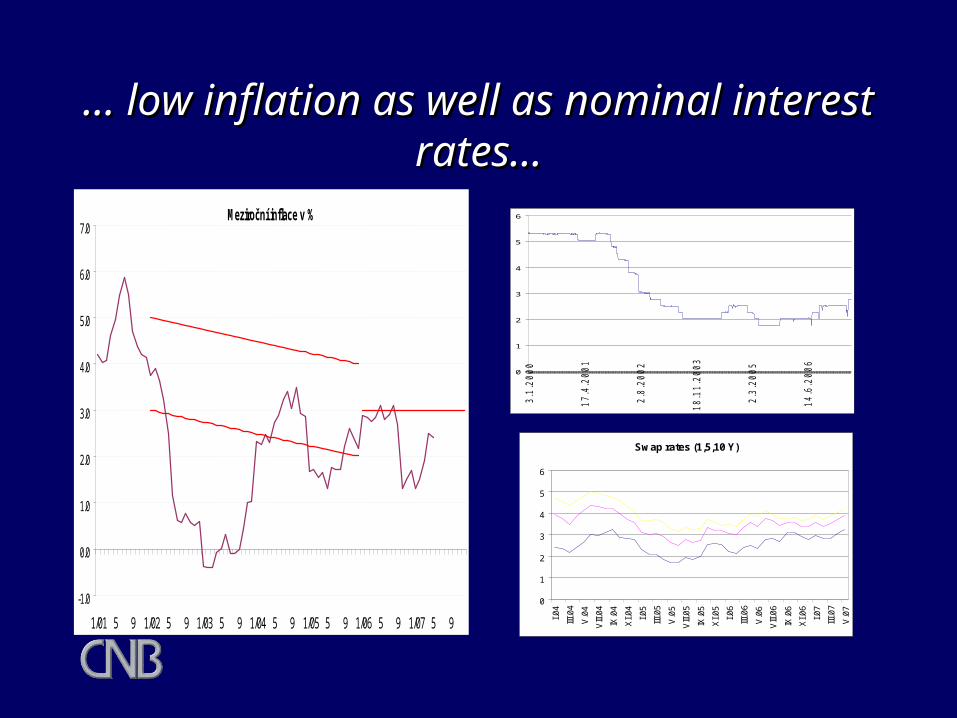

… … low inflation as well as nominal low inflation as well as nominal interest rates…interest rates…

0

1

2

3

4

5

6

3.1

.20

00

17

.4.2

00

1

2.8

.20

02

18

.11

.20

03

2.3

.20

05

14

.6.2

00

6

Swap rates (1,5,10 Y)

0

1

2

3

4

5

6

I.04

III.0

4

V.0

4

VII.

04

IX.0

4

XI.0

4

I.05

III.0

5

V.0

5

VII.

05

IX.0

5

XI.0

5

I.06

III.0

6

V.0

6

VII.

06

IX.0

6

XI.0

6

I.07

III.0

7

V.0

7

Meziroční inflace v %

-1.0

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

1/01 5 9 1/02 5 9 1/03 5 9 1/04 5 9 1/05 5 9 1/06 5 9 1/07 5 9

TTurnover in urnover in external external balancebalance despite despite appreciation of CZK...appreciation of CZK...

Current account and its components / GDP ratios (moving annual cumulations in %)

-12

-10

-8

-6

-4

-2

0

2

4

6

I/98 III I/99 III I/00 III I/01 III I/02 III I/03 III I/04 III I/05 III I/06 III I/07

%

trade balance balance of servicesincome balance current transferscurrent account

Euro Fx rate

25

27

29

31

33

35

37

Risks for EconomyRisks for Economy• Problems in the field of public finance are getting more urgent;• Problems in structural sphere are not solved so far:

Pension reform Changes in health care;

• Problems of too much regulation, limited flexibility of labour market. Non-solving of this problem, despite compensating openess of market, has adverse effects on future growth of economy.

• On the contrary, competitive environment in some spheres of economy could contribute more to low price growth and prosperity.

Czech Republic and EuroCzech Republic and Euro

Czech Republic X Euro

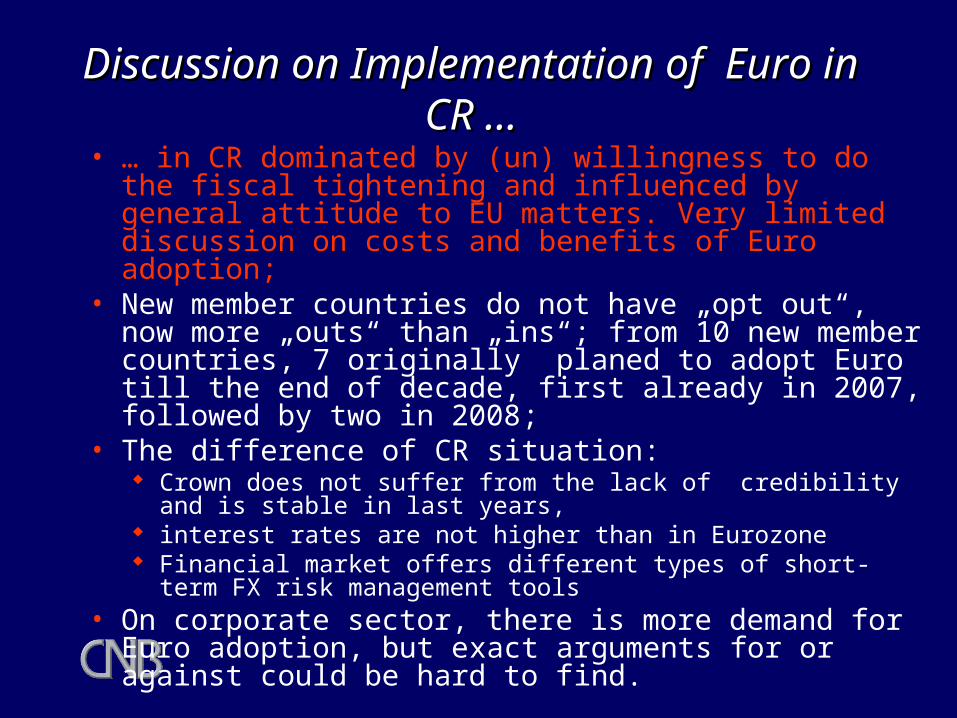

Discussion on Implementation of Discussion on Implementation of Euro in CR …Euro in CR …

• … in CR dominated by (un) willingness to do the fiscal tightening and influenced by general attitude to EU matters. Very limited discussion on costs and benefits of Euro adoption;

• New member countries do not have „opt out“, now more „outs“ than „ins“; from 10 new member countries, 7 originally planed to adopt Euro till the end of decade, first already in 2007, followed by two in 2008;

• The difference of CR situation: Crown does not suffer from the lack of credibility and is stable in last

years, interest rates are not higher than in Eurozone Financial market offers different types of short-term FX risk

management tools• On corporate sector, there is more demand for Euro adoption,

but exact arguments for or against could be hard to find.

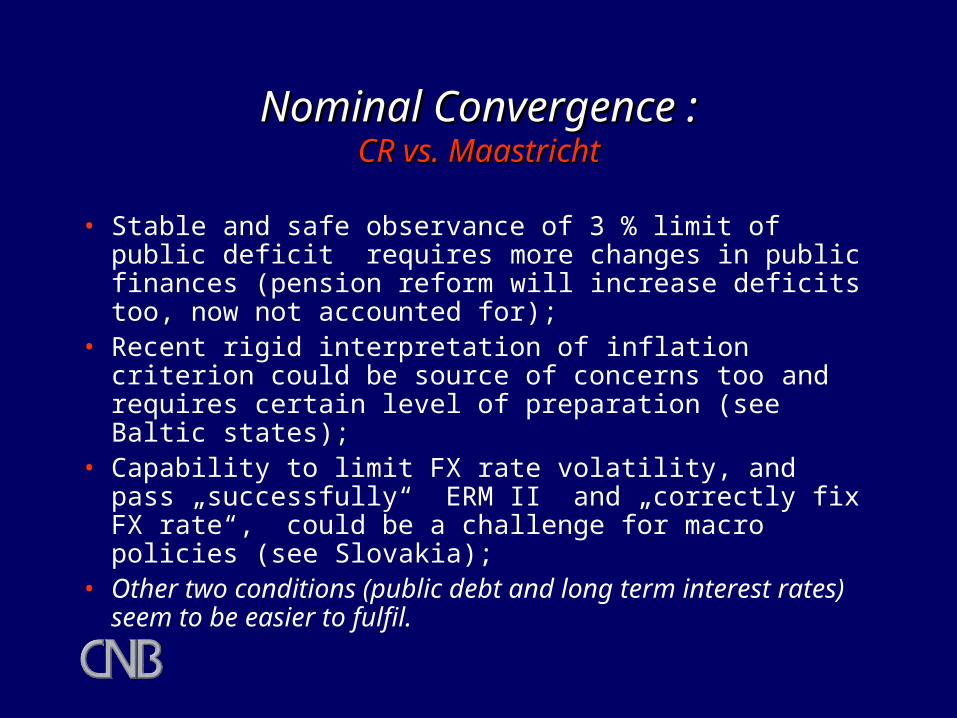

Nominal Convergence :Nominal Convergence :CRCR vs. Maastricht vs. Maastricht

• Stable and safe observance of 3 % limit of public deficit requires more changes in public finances (pension reform will increase deficits too, now not accounted for);

• Recent rigid interpretation of inflation criterion could be source of concerns too and requires certain level of preparation (see Baltic states);

• Capability to limit FX rate volatility, and pass „successfully“ ERM II and „correctly fix FX rate“, could be a challenge for macro policies (see Slovakia);

• Other two conditions (public debt and long term interest rates) seem to be easier to fulfil.

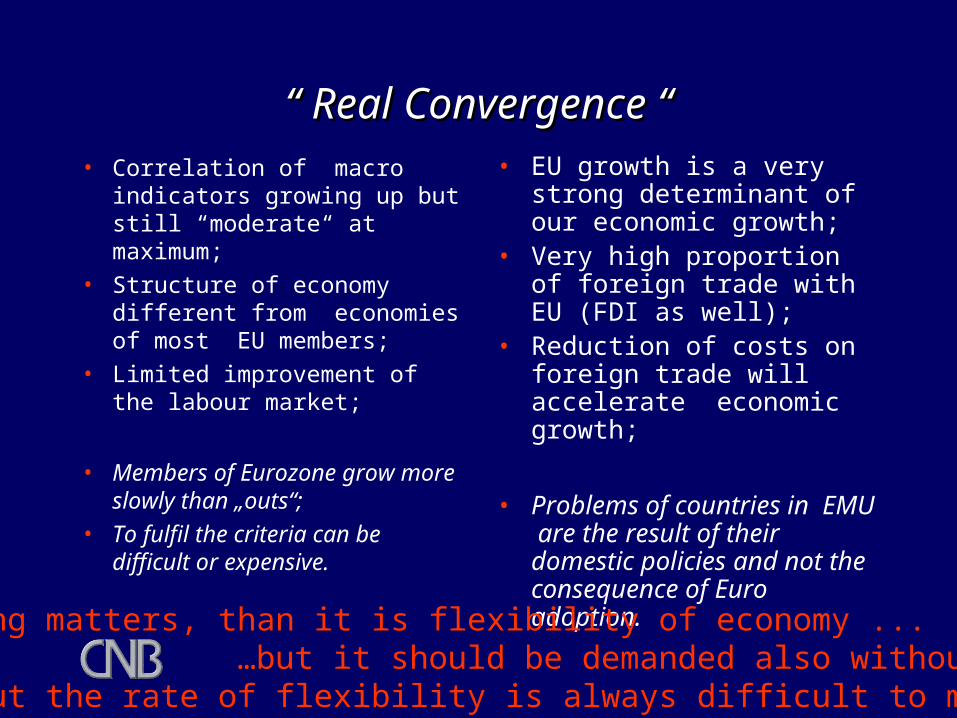

“ “ ReRealal CConvergenconvergencee “ “• Correlation of macro indicators

growing up but still “moderate“ at maximum;

• Structure of economy different from economies of most EU members;

• Limited improvement of the labour market;

• Members of Eurozone grow more slowly than „outs“;

• To fulfil the criteria can be difficult or expensive.

• EU growth is a very strong determinant of our economic growth;

• Very high proportion of foreign trade with EU (FDI as well);

• Reduction of costs on foreign trade will accelerate economic growth;

• Problems of countries in EMU are the result of their domestic policies and not the consequence of Euro adoption.

If anything matters, than it is flexibility of economy ... …but it should be demanded also without EMU entry… … but the rate of flexibility is always difficult to measure …

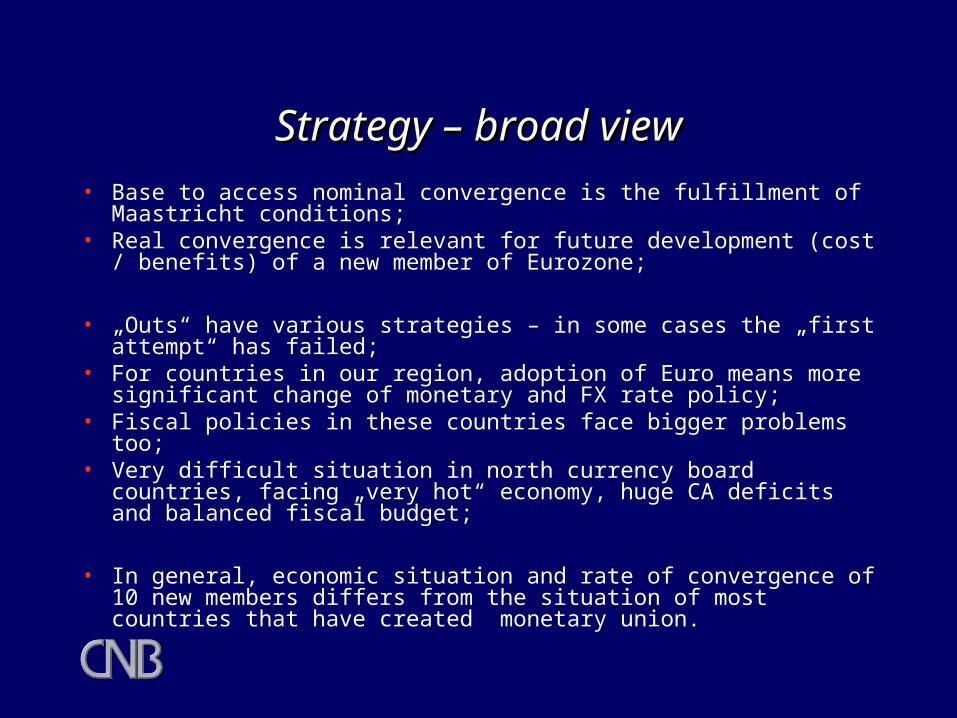

Strategy – broad viewStrategy – broad view• Base to access nominal convergence is the fulfillment of Maastricht

conditions;• Real convergence is relevant for future development (cost / benefits) of

a new member of Eurozone;

• „Outs“ have various strategies – in some cases the „first attempt“ has failed;

• For countries in our region, adoption of Euro means more significant change of monetary and FX rate policy;

• Fiscal policies in these countries face bigger problems too;• Very difficult situation in north currency board countries, facing „very

hot“ economy, huge CA deficits and balanced fiscal budget;

• In general, economic situation and rate of convergence of 10 new members differs from the situation of most countries that have created monetary union.

CCR R : : New Facts New Facts • „Rule book“ for Euro in CR set shortest possible „transition period“ (2

years in ERM II.) and minimum 3 years of preparation;• First strategy (adopted by previous government) of entering Eurozone

assumed implementation of Euro 01/01/2010 but failed on fiscal grounds;

• New strategy approved in VIII 2007, but no substancial new message there, date is not indicated, yearly evaluation continues (autumn);

• High economic growth caused cyclical decline of deficits (in practice close to 3% limit) in recent years and creates impression of „lower urgency of the action;

• Since 2008, some fiscal reform will be efective (VAT increase, direct tax cuts, partial reversal of large increase of social transfers from 2006). But it is not expected to bring large fiscal saving. Other large reforms, that will increase fiscal costs, are even scheduled so far;

www.cnb.czwww.cnb.cz