27

Commercial Real Estate Market Update presented to Dallas Bar Association

Commercial Real Estate Market Update

presented to

Dallas Bar Association

2

NATIONAL MARKET UPDATE

A G E N D ANATIONAL MARKET UPDATE

DFW MARKET UPDATE

VALUATION & ADVISORY

CAPITAL MARKETSCAPITAL MARKETS

NATIONAL MARKET UPDATE

4National Economic Overview

F th Q t 2010

■ Cautious consumers and businesses softened by yr end 2010.

New leases signed (leasing activity) up in the CBDs by 31 6 % in

Fourth Quarter 2010

New leases signed (leasing activity) up in the CBDs by 31.6 %, in suburbs by 20.2 % year over year.

■ Spending up = steady growth in real gross domestic product (2.9% for 2010).

■ By December, non-farm employment up by more than 1.1 million workers from one year ago - unemployment rate down one-half y g p ypercentage point to 9.4%.

Look for slow and steady improvement in 2011.

■ Asking office rents inching up slowly but most markets will not see significant increases until 2012 and 2013.

Source: Cushman & Wakefield Research

5

E l t V R t 1986 2010

U.S. Growth in OfficeEmployment vs. Vacancy Rates 1986 – 2010

1,500 25%4-qtr Change in Office-Using Employment CBD Vacancy Non-CBD Vacancy

1,000

(000

s)

20%

0

500

Empl

oym

ent

15%

-500

Offi

ce-U

sing

10%

-1,500

-1,000

Cha

nge

in

5%

-2,00086 87 88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10

0%

Data as of Fourth Quarter 2010

Source: Moody’s|Economy.com, Cushman & Wakefield Research

6

Y O Y N t J b G i

U.S. Employment GrowthYear-Over-Year Net Job Gains

February 2011

18.0 to 32.9

9.0 to 17.9

33.0 to 230.0

0.1 to 8.9

-10.5 to 0.0

Source: U.S. Bureau of Labor Statistics, Cushman & Wakefield Research

7

N L i A ti it

National Office MarketNew Leasing Activity

Square FeetCBD Suburban

(Forecast)

Square Feet(In Millions)

200.0

120 0

160.0

80.0

120.0

40.0

0.0

94 95 96 97 98 99 00 0302 04 05 070601 08 1009 11F 12F 13F 14F 15F

Data as of Fourth Quarter 2010

Source: Cushman & Wakefield Research

8

Hi h t CBD d N CBD N L i A ti it

National Office MarketHighest CBD and Non-CBD New Leasing Activity

Fourth Quarter 2010

CBD Non-CBD

1. Midtown NY 18,859,0002 Washington D C 5 822 502

1. Dallas, TX 11,392,6602 Los Angeles Metro 9 396 0542. Washington, D.C. 5,822,502

3. Chicago, IL 4,603,0534. Midtown South NY 4,082,887 5. Boston, MA 3,755,442

2. Los Angeles Metro 9,396,0543. Atlanta, GA 8,368,950 4. Boston, MA 7,906,5955. Denver, CO 7,553,135

6. San Francisco, CA 3,580,6847. Orange County CA 3,407,9888. Downtown NY 3,377,6809 Denver CO 2 730 124

6. Houston, TX 7,307,0287. Northern VA 7,023,4488. San Diego, CA 5,485,0869 Chicago IL 5 406 5259. Denver, CO 2,730,124

10. Houston, TX 1,553,652-- -- --

17. Dallas, TX 818,169

9. Chicago, IL 5,406,52510. Silicon Valley CA 4,460,213

Data as of Fourth Quarter 2010

Source: Cushman & Wakefield Research

9

O ll Ab ti

National Office MarketOverall Absorption

(Forecast)Square Feet80.0

CBD Suburban(Forecast)Square Feet

(In Millions)

60.0

80.0

40.0

20.0

-20.0

0.0

-40.094 95 96 97 98 99 00 0302 04 05 070601 08 1009 11F 12F 13F 14F 15F

Data as of Fourth Quarter 2010

Source: Cushman & Wakefield Research

10

O ll A ki R t

National Office Market

(Forecast)

Overall Asking Rents

CBD Suburban(Forecast)

$45.00

$40 00$40.00

$35 00

$30.00

$35.00

$25.00

06$20.00

01 02 03 04 05 11F06 0701 02 03 04 05 08 09 10 11F 12F 13F 14F 15F

Data as of Fourth Quarter 2010

Source: Cushman & Wakefield Research

DFW MARKET UPDATE

12Dallas Office Market

O iOverview

Economy

Jobs/Housing/Population

Office

Multi-family / Retail / Industrial

13Dallas Office Market

V t O i d S bl SVacant vs. Occupied Sublease Space

Vacant Occupied

Millions (SF)10

6

8

4

6

2

95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 1Q11

0

Data as of First Quarter 2011

Source: Cushman & Wakefield Research

14Dallas Office Market

S b k t Offi R t b Cl

Class A Class B

Submarket Office Rates by Class

$35Dollars/SF

$25

$30

$15

$20

$10

$15

*All rental rates are full service, including electricityData as of First Quarter 2011Source: Cushman & Wakefield Research

15Dallas Office Market

CBD Q t d G R t l R t b Cl *CBD - Quoted Gross Rental Rates by Class* vs. Occupancy in All Classes

Dallas CBD % Occupied Class A Class B

$25.00

$28.00 100%

$22.00

90%

$16.00

$19.00 80%

$13.00

$16.00

70%

$10.00 60%90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 1Q

11

*All rental rates are full service, including electricityData as of First Quarter 2011Source: Cushman & Wakefield Research

16Proposed Office Projects

TWO ARTS PLAZAHALL ARTS CENTER SPIRE DEVELOPMENT TWO ARTS PLAZAHALL ARTS CENTER SPIRE DEVELOPMENT

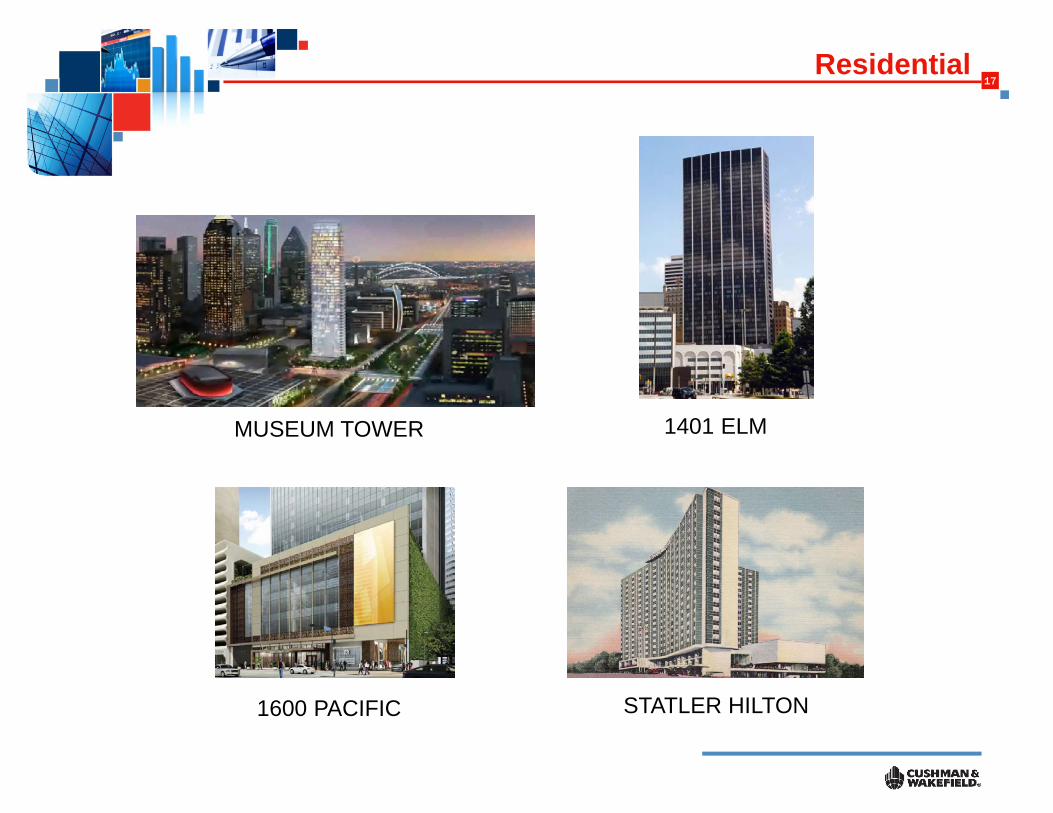

17Residential

1401 ELMMUSEUM TOWER

STATLER HILTON1600 PACIFIC STATLER HILTON1600 PACIFIC

VALUATION & ADVISORY

19Valuation & Advisory

In 2009, Valuation & Advisory (U.S.) completed over 18,500 appraisal assignments with an aggregate value in excess of $400 Billion.

C d t P i YCompared to Prior Years:

2008 – 19,000 appraisal assignments. Values of $558 Billion.2007 21 000 appraisal assignments Values of $600 Billion2007 – 21,000 appraisal assignments. Values of $600 Billion.

C&W’s Appraisal Group is organized by Geographic Areas and Specialty Practices.

20Valuation & Advisory

S i lt P ti

U f A i l S i d d k l d d ti b th t f

Specialty Practices

Users of Appraisal Services demand knowledge and expertise by the type of practice and property type. Typical Specialty Practices on a national and global level:

■ Litigation Support ■ Portfolio Valuation ■ Mission Critical Facilities

■ Automobile Dealerships ■ Golf ■ Multi-Family/Office/Industrial

■ Agribusiness ■ Financial Advisory Services ■ Malls/Shopping Centers/Retail

■ Senior Housing ■ Hospitality ■ Residential Development

■ Appraisal Management ■ Property Tax Appeals ■ Self-Storage

■ Healthcare

21Valuation & Advisory

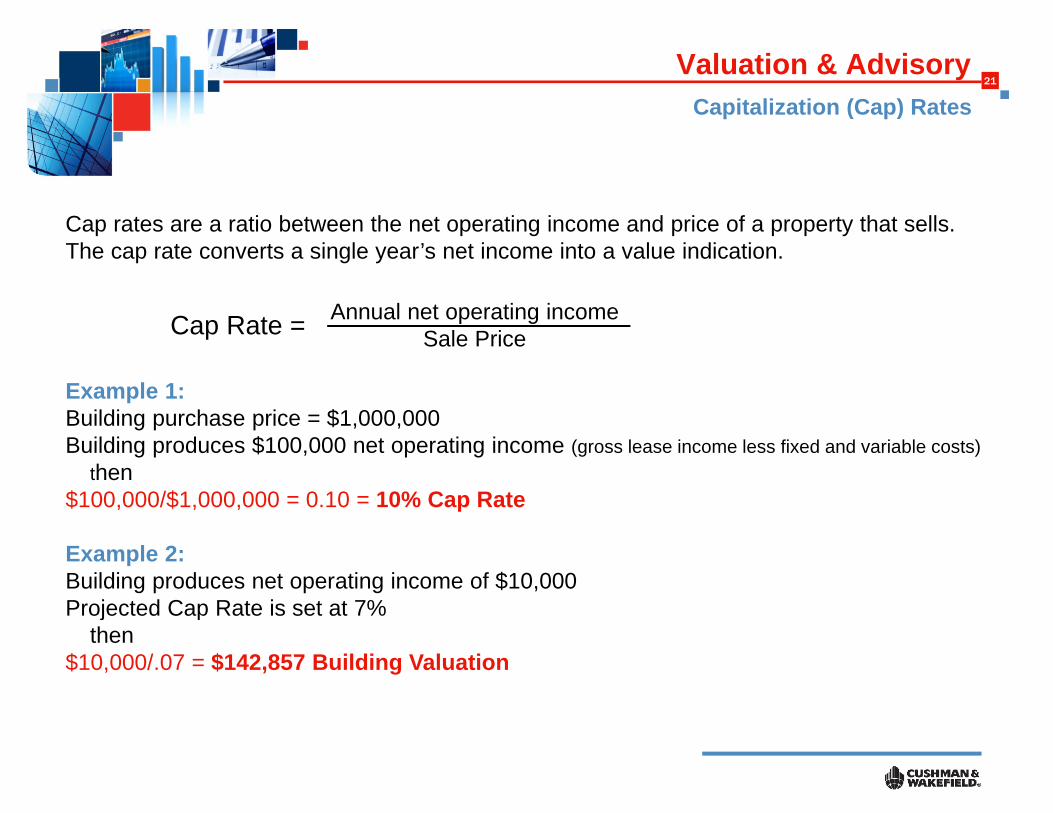

C it li ti (C ) R tCapitalization (Cap) Rates

A l t ti i

Cap rates are a ratio between the net operating income and price of a property that sells. The cap rate converts a single year’s net income into a value indication.

Cap Rate = Annual net operating incomeSale Price

Example 1:Building purchase price = $1,000,000Building produces $100,000 net operating income (gross lease income less fixed and variable costs)

then$100,000/$1,000,000 = 0.10 = 10% Cap Rate$ , $ , , p

Example 2:Building produces net operating income of $10,000Projected Cap Rate is set at 7%Projected Cap Rate is set at 7%

then$10,000/.07 = $142,857 Building Valuation

22Valuation & Advisory

C R t D ll A 2010 2011

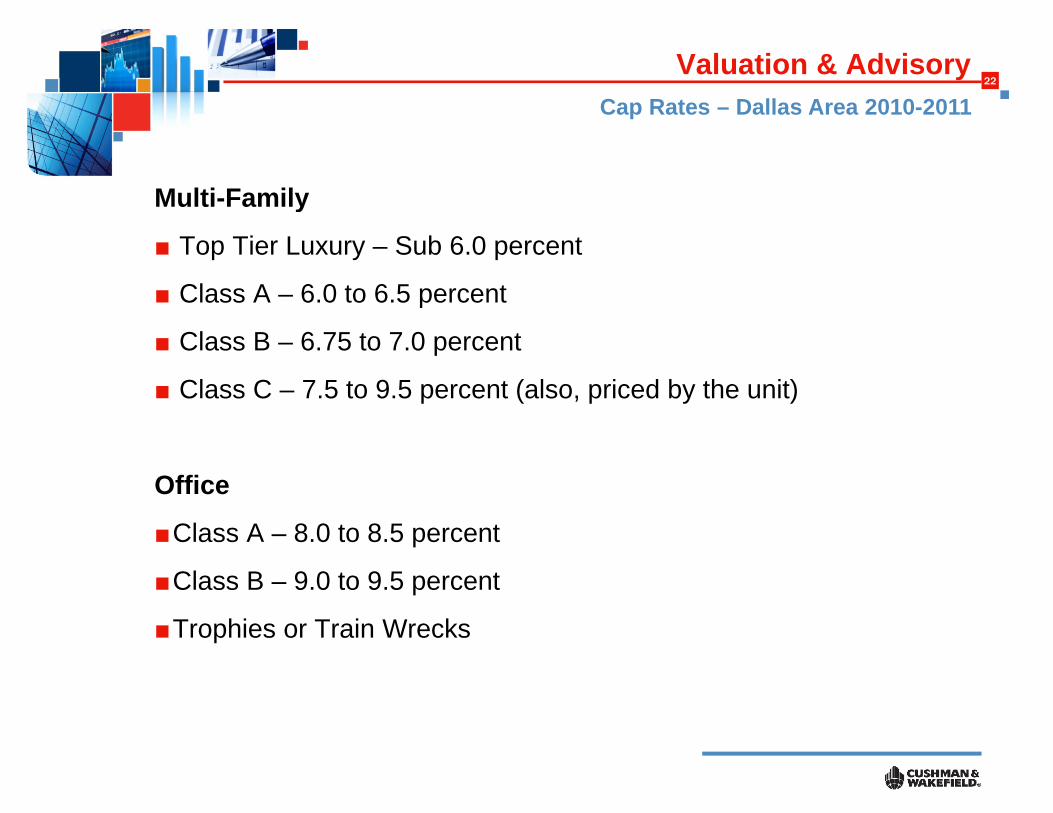

Multi-Family

Cap Rates – Dallas Area 2010-2011

Multi Family

■ Top Tier Luxury – Sub 6.0 percent

■ Class A – 6.0 to 6.5 percentp

■ Class B – 6.75 to 7.0 percent

■ Class C – 7.5 to 9.5 percent (also, priced by the unit)

Office

■Class A – 8.0 to 8.5 percent

■Class B – 9.0 to 9.5 percent

■Trophies or Train Wrecks

23Valuation & Advisory

C R t D ll A 2010 2011

Industrial

Cap Rates – Dallas Area 2010-2011

Industrial

■ Class A – Plus/Minus 7 percent

■ Class B – Plus/Minus 8 percentp

Shopping Centers/Retail

■ Class A Power Centers – 7.6 to 7.7 percent

■ Neighborhood Centers – 7.5 to 7.75 percent

■ Strip Centers – 9.0 to 10.0 percent

■ Top Tier Properties – 6.5 to 6.75 percent

(infill, with strong demographics)

CAPITAL MARKETS

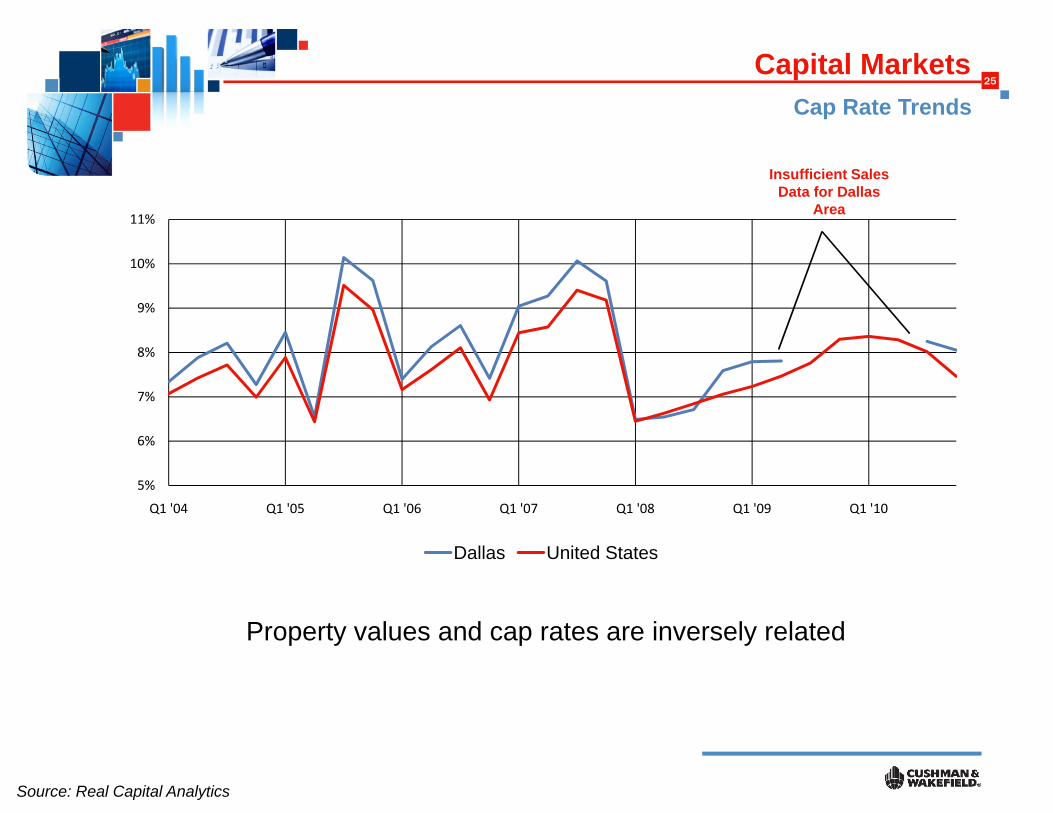

25Capital Markets

C R t T d

Insufficient Sales Data for Dallas

Cap Rate Trends

9%

10%

11%Area

7%

8%

9%

5%

6%

Q1 '04 Q1 '05 Q1 '06 Q1 '07 Q1 '08 Q1 '09 Q1 '10Q1 04 Q1 05 Q1 06 Q1 07 Q1 08 Q1 09 Q1 10

Dallas United States

Property values and cap rates are inversely related

Source: Real Capital Analytics

26

D ll M k t S l V l

Capital Markets

■ Office sales activity showed major signs of improvement in 2010

Dallas Market Sales Volume

y j g p

■ Strong momentum into 2011, as evidenced by several major sales that closed during the 1st Quarter 2011

6,000

7,000

3,000

4,000

5,000

1,000

2,000

,

0

Q1 '04 Q1 '05 Q1 '06 Q1 '07 Q1 '08 Q1 '09 Q1 '10

Rolling 12 mo Total Quarterly VolRolling 12-mo. Total Quarterly Vol.

Source: Real Capital Analytics

27Capital Markets

A ti B

Dallas Market U.S. Overall

Active Buyers

■ 2010 marked the return ofbuyers of all types to themarket after the downturnf 2008 09

0%0%19%

8%

32%

17%

29%of 2008-09■ Buyers are most actively

pursuing core assets anddi d i i h

5%

24%

1%

2%

0%

11%

32% 29%

Institutional

Cross-Border

distressed properties, withsignificantly less activity forother properties 54%

67% 14%

19%

Public Listed/REITs

Private

User/Other

50%

38%

36%

20%26%

2%

21%

5%

2008 2009 2010 2011 (YTD) 2011 (YTD)

Source: Real Capital Analytics