1 NEW YORK CITY BAR NEW YORK CITY BAR Securities Litigation Securities Litigation During the During the Financial Financial Crisis: Crisis: Current Developments & Strategies Current Developments & Strategies DAMAGES AND LOSS CAUSATION DAMAGES AND LOSS CAUSATION By Alex Sussman By Alex Sussman By Alex Sussman By Alex Sussman December December 8, 2009 8, 2009 Introduction Introduction Focus on the typical Rule 10b Focus on the typical Rule 10b-5 securities fraud class action, 5 securities fraud class action, governed by the Private Securities Litigation Reform Act of governed by the Private Securities Litigation Reform Act of 1995 (“PSLRA”) with special reference to the 1995 (“PSLRA”) with special reference to the financial financial crisis. crisis. Governing principles and methods of establishing: Governing principles and methods of establishing: Loss causation: Since 2005 Supreme Court decision in Loss causation: Since 2005 Supreme Court decision in Dura Dura, one of the most heavily litigated issues. , one of the most heavily litigated issues. Damages: Critical to the strategy and outcome Damages: Critical to the strategy and outcome. 1

Transcript

1

NEW YORK CITY BARNEW YORK CITY BARSecurities LitigationSecurities Litigation

During the During the Financial Financial Crisis: Crisis: Current Developments & StrategiesCurrent Developments & Strategiesp gp g

DAMAGES AND LOSS CAUSATIONDAMAGES AND LOSS CAUSATION

By Alex SussmanBy Alex SussmanBy Alex SussmanBy Alex Sussman

December December 8, 2009 8, 2009

IntroductionIntroduction

Focus on the typical Rule 10bFocus on the typical Rule 10b--5 securities fraud class action, 5 securities fraud class action, governed by the Private Securities Litigation Reform Act of governed by the Private Securities Litigation Reform Act of g y gg y g1995 (“PSLRA”) with special reference to the 1995 (“PSLRA”) with special reference to the financial financial crisis.crisis.Governing principles and methods of establishing:Governing principles and methods of establishing:

Loss causation: Since 2005 Supreme Court decision in Loss causation: Since 2005 Supreme Court decision in DuraDura, one of the most heavily litigated issues., one of the most heavily litigated issues.Damages: Critical to the strategy and outcomeDamages: Critical to the strategy and outcome..

1

2

Loss Causation Loss Causation ––PSLRA and PSLRA and Dura PharmaceuticalsDura Pharmaceuticals

Economic loss and loss causation are required elements of an Economic loss and loss causation are required elements of an SEC Rule 10bSEC Rule 10b--5 civil fraud claim. 5 civil fraud claim. Dura Dura PharmsPharms., ., Inc. v. Inc. v. Broudo,Broudo,544 544 U.S. 336 (2005).U.S. 336 (2005).“[T]he plaintiff shall have the burden of proving that the “[T]he plaintiff shall have the burden of proving that the [alleged 10b[alleged 10b--5 violation] caused the loss . . . .” 5 violation] caused the loss . . . .” 15 U.S.C. 15 U.S.C. §§ 78u78u--4(b)(4). 4(b)(4). Dura Dura held that the allegation that stock was purchased at an held that the allegation that stock was purchased at an allegedly inflated price due to a fraudulent misrepresentation allegedly inflated price due to a fraudulent misrepresentation

2

does not, in itself, adequately plead loss causation. does not, in itself, adequately plead loss causation.

Connecting Fraud to the LossConnecting Fraud to the Loss

“To prove loss causation, a plaintiff must demonstrate ‘that the “To prove loss causation, a plaintiff must demonstrate ‘that the misstatement or omission concealed something from the misstatement or omission concealed something from the ggmarket that, when disclosed, negatively affected the value of market that, when disclosed, negatively affected the value of the security.’” the security.’” In re Flag Telecom Holdings, Ltd. Sec. Litig.In re Flag Telecom Holdings, Ltd. Sec. Litig., , 574 F.3d 29 (2d Cir. 2009), quoting 574 F.3d 29 (2d Cir. 2009), quoting Lentell v. Merrill Lynch & Lentell v. Merrill Lynch & Co., Inc.Co., Inc., 396 F.3d 161 (2d Cir. 2005)., 396 F.3d 161 (2d Cir. 2005).Plaintiff must show that (1) “the market reacted negatively to a Plaintiff must show that (1) “the market reacted negatively to a corrective disclosure” or corrective disclosure” or ((2) defendants “misstated or omitted 2) defendants “misstated or omitted risks that did lead to the loss ”risks that did lead to the loss ” i ei e materialization of amaterialization of a

3

risks that did lead to the loss, risks that did lead to the loss, i.e. i.e. materialization of a materialization of a concealed risk. concealed risk. Lentell, Lentell, 396 396 F.3d F.3d at 173.at 173.

3

Loss Causation Complaint Loss Causation Complaint Allegations Allegations –– Does Rule 9(b) Apply?Does Rule 9(b) Apply?

Dura Dura assumed the Rule 8 notice pleading standard applies to assumed the Rule 8 notice pleading standard applies to allegations of loss allegations of loss causation. causation. ggHowever, the issue remains unsettled. However, the issue remains unsettled. In re Gilead Sciences In re Gilead Sciences Sec. Litig.Sec. Litig., , 536 F.3d 1049 536 F.3d 1049 (9th (9th Cir. Cir. 2008); 2008); seesee In re First In re First Union Sec. Litig.Union Sec. Litig., 2006 U.S. Dist. LEXIS 5083, *17, 2006 U.S. Dist. LEXIS 5083, *17--*18 *18 (W.D.N.C. Jan. 20, 2006) (citing cases applying Rule 9(b).(W.D.N.C. Jan. 20, 2006) (citing cases applying Rule 9(b).A Fifth Circuit panel applied Rule 8(a)(2) to A Fifth Circuit panel applied Rule 8(a)(2) to require the require the plaintiff to allege “a facially ‘plausible’ causal relationship plaintiff to allege “a facially ‘plausible’ causal relationship

4

between the fraudulent statements or omissions and plaintiff’s between the fraudulent statements or omissions and plaintiff’s economic loss.” economic loss.” LormandLormand v. US Unwired, Inc.v. US Unwired, Inc., 565 F.3d 228 , 565 F.3d 228 (5th Cir. 2009).(5th Cir. 2009).

Loss Causation Complaint Loss Causation Complaint Allegations Allegations –– Does Rule 9(b) Apply? (cont’d)Does Rule 9(b) Apply? (cont’d)

In In McAdams v. McCord, McAdams v. McCord, 2009 U.S. App. LEXIS 22830, *4, *7 2009 U.S. App. LEXIS 22830, *4, *7 (8th Cir. Oct. 20, 2009), the court affirmed dismissal of a (8th Cir. Oct. 20, 2009), the court affirmed dismissal of a ( )( )PSLRA claim against an outside auditor on loss causation PSLRA claim against an outside auditor on loss causation grounds because a PSLRA “complaint must state with grounds because a PSLRA “complaint must state with particularity the circumstances of the alleged fraudulent particularity the circumstances of the alleged fraudulent statement” and this complaint did not “specify how two statement” and this complaint did not “specify how two statements by [the outside auditor) .statements by [the outside auditor) . .. . proximately caused the . proximately caused the investor’s losses.”investor’s losses.”InIn Teachers’ Ret Sys v HunterTeachers’ Ret Sys v Hunter 477 F 3d 162 186 (4th Cir477 F 3d 162 186 (4th Cir

5

In In Teachers Ret. Sys. v. HunterTeachers Ret. Sys. v. Hunter, 477 F.3d 162, 186 (4th Cir. , 477 F.3d 162, 186 (4th Cir. 2007), the court observed that there is a “strong case” for 2007), the court observed that there is a “strong case” for applying Rule 9(b) to loss causation allegations, but instead applying Rule 9(b) to loss causation allegations, but instead required “sufficient specificity to enable the court to evaluate required “sufficient specificity to enable the court to evaluate whether the necessary causal link existswhether the necessary causal link exists.”.”

4

Loss Causation Loss Causation ––A Necessary Element for Class Certification?A Necessary Element for Class Certification?

In In Oscar Private Equity Investments v. Allegiance Telecom, Oscar Private Equity Investments v. Allegiance Telecom, Inc.Inc., 487 F.3d 261 (5, 487 F.3d 261 (5thth Cir. 2007), the Cir. 2007), the Fifth Circuit Fifth Circuit ruled that ruled that (( ))plaintiffs must establish loss causation in order to obtain class plaintiffs must establish loss causation in order to obtain class certification.certification.

Plaintiffs bear the burden of establishing it by “a Plaintiffs bear the burden of establishing it by “a preponderance of the evidence.” preponderance of the evidence.” Alaska Elec. Pension Alaska Elec. Pension Fund v. Flowserve Corp.Fund v. Flowserve Corp., 572 F.3d 221 (5, 572 F.3d 221 (5thth Cir. 2009) Cir. 2009) (reversing district court’s dismissal of case).(reversing district court’s dismissal of case).

6

District courts in the Second Circuit District courts in the Second Circuit have generally not have generally not followed followed Oscar. See, e.g., Oscar. See, e.g., In re Flag Telecom, supra In re Flag Telecom, supra (noting (noting cases); cases); Lapin Lapin v. Goldman, Sachs & Co.v. Goldman, Sachs & Co., 2008 U.S. , 2008 U.S. Dist. Dist. LEXIS 69574 (S.D.N.Y. Sept. 15, 2008) (citing cases).LEXIS 69574 (S.D.N.Y. Sept. 15, 2008) (citing cases).

Loss Causation in Section 11 CasesLoss Causation in Section 11 Cases

Section 11(e) of the Securities Act of 1933, 15 U.S.C. Section 11(e) of the Securities Act of 1933, 15 U.S.C. §§ 77k(e), 77k(e), provides a “negative causation” affirmative defense to claims that a provides a “negative causation” affirmative defense to claims that a Registration Statement was materially misleading.Registration Statement was materially misleading.

In In Flowserve, supra, Flowserve, supra, the Ninth Circuit reversed a summary the Ninth Circuit reversed a summary judgment dismissal that found “negative causation.”judgment dismissal that found “negative causation.”Indiana District Council v. Alaska Elec. Pension FundIndiana District Council v. Alaska Elec. Pension Fund, 2009 , 2009 FED App. 0370P (6FED App. 0370P (6thth Cir. Oct. 21, 2009): Section 11 claim Cir. Oct. 21, 2009): Section 11 claim dismissal reversed because negative causation did not appear “on dismissal reversed because negative causation did not appear “on the face of the complaint.”the face of the complaint.”ppIn re Britannia Bulk Holdings Inc. Sec. Litig.In re Britannia Bulk Holdings Inc. Sec. Litig., 08 Civ. 9554 , 08 Civ. 9554 (DLC) (S.D.N.Y. Oct. 19, 2009): Claim dismissed based on (DLC) (S.D.N.Y. Oct. 19, 2009): Claim dismissed based on negative causation as misstatement was postnegative causation as misstatement was post--IPO and stock had IPO and stock had dropped 90% before corrective disclosure.dropped 90% before corrective disclosure.

7

5

Loss Loss Causation Causation –– Financial Crisis IssuesFinancial Crisis Issues

Was the investor’s loss caused by the misrepresentation or, rather, Was the investor’s loss caused by the misrepresentation or, rather, by “changed economic circumstances, new industryby “changed economic circumstances, new industry--specific or specific or firmfirm--specific facts, conditions, or other events,” which account for specific facts, conditions, or other events,” which account for the lower stock price? the lower stock price? DuraDura, 544 U.S. at 352, 544 U.S. at 352--5353..

Demonstrating loss causation is more difficult if “plaintiff’s loss Demonstrating loss causation is more difficult if “plaintiff’s loss coincides with a marketcoincides with a market--wide phenomenon.” wide phenomenon.” Lentell v. Merrill Lynch, Lentell v. Merrill Lynch, 396 F.3d at 174.396 F.3d at 174.

Was the stock price drop caused by unanticipated business losses Was the stock price drop caused by unanticipated business losses resulting from the resulting from the financial financial crisis?crisis?

8

Did a subDid a sub--prime finance company’s losses result from the decline in prime finance company’s losses result from the decline in home prices or from “corrective disclosure” or “materialization of home prices or from “corrective disclosure” or “materialization of risk” as to previously undisclosed mortgage problems?risk” as to previously undisclosed mortgage problems?

No Loss Causation No Loss Causation ––No Connection Between Fraud and LossNo Connection Between Fraud and Loss

Loss causation allegations fail if they are “conclusory and Loss causation allegations fail if they are “conclusory and involve unreasonable inferences.” involve unreasonable inferences.” In re Redback Networks, In re Redback Networks, Inc. Sec. Litig.Inc. Sec. Litig., 329 Fed. Appx. 715 (9, 329 Fed. Appx. 715 (9thth Cir. 2009).Cir. 2009).Plaintiffs failed to plead loss causation where they Plaintiffs failed to plead loss causation where they did not did not “allege that Deloitte’s misstatements concealed the risk of “allege that Deloitte’s misstatements concealed the risk of Warnaco’s bankruptcyWarnaco’s bankruptcy.” .” LattanzioLattanzio v. Deloitte & v. Deloitte & ToucheTouche LLPLLP, , 476 F.3d 147, 157 (2d Cir. 2007).476 F.3d 147, 157 (2d Cir. 2007).Rule 10bRule 10b--5 claim failed because fraudulent representation that 5 claim failed because fraudulent representation that

9

an investor was accredited did not cause any loss. an investor was accredited did not cause any loss. ATSI ATSI Commc’nsCommc’ns, Inc. v. The , Inc. v. The ShaarShaar Fund, Ltd.Fund, Ltd., 493 F.3d 87 2d (2d , 493 F.3d 87 2d (2d Cir. 2007).Cir. 2007).

6

No Loss Causation No Loss Causation ––Shares Sold Prior Shares Sold Prior to Corrective Disclosureto Corrective Disclosure

The Second Circuit excluded from a certified class inThe Second Circuit excluded from a certified class in andand outoutThe Second Circuit excluded from a certified class inThe Second Circuit excluded from a certified class in--andand--out out traders and others who sold their shares prior to the first traders and others who sold their shares prior to the first corrective disclosure. corrective disclosure. In re Flag TelecomIn re Flag Telecom, , supra.supra.Plaintiff Plaintiff sold shares before the corrective disclosure and, sold shares before the corrective disclosure and, therefore, suffered no loss and had no claim. therefore, suffered no loss and had no claim. Glaser v. Glaser v. EnzoEnzoBiochemBiochem, Inc., Inc., 474 F.3d 474 (4, 474 F.3d 474 (4thth Cir. 2006), Cir. 2006), cert. deniedcert. denied, 127 , 127 Sup. Ct. 1876 (2007).Sup. Ct. 1876 (2007).

10

No Loss Causation No Loss Causation ––Fraud Revealed After Unrelated Price DeclineFraud Revealed After Unrelated Price Decline

Courts find no loss causation where the disclosure of fraud Courts find no loss causation where the disclosure of fraud occurred after the stock price dropped for reasons unrelated to occurred after the stock price dropped for reasons unrelated to p ppp ppthe fraud. the fraud. McKowanMcKowan Lowe & Co.Lowe & Co. v. Jasmine Ltd.v. Jasmine Ltd., 231 Fed. , 231 Fed. AppxAppx. 216 (3d Cir. 2007).. 216 (3d Cir. 2007).In In light of 80% stock price drop during class period, loss light of 80% stock price drop during class period, loss causation for subsequent drop was not adequately alleged. causation for subsequent drop was not adequately alleged. The The 60223 Trust v. Goldman, Sachs & Co.60223 Trust v. Goldman, Sachs & Co., , 540 F.Supp. 2d 449 (S.D.N.Y. 2007).

11

No loss causation where price dropped after bankruptcy No loss causation where price dropped after bankruptcy announcement and plaintiff never alleged that “market’s announcement and plaintiff never alleged that “market’s acknowledgement of prior misrepresentations caused that acknowledgement of prior misrepresentations caused that drop.” drop.” D.E. & J. Ltd. D.E. & J. Ltd. P’shipP’ship v. Conawayv. Conaway, 133 F. , 133 F. App’xApp’x 994, 994, 1000 (61000 (6thth Cir. 2005).Cir. 2005).

7

No Loss CausationNo Loss CausationPrice Drops on Unrelated Bad NewsPrice Drops on Unrelated Bad News

Metzler Inv. GMBH v. Corinthian Colleges, Inc., Metzler Inv. GMBH v. Corinthian Colleges, Inc., 540 F.3d 540 F.3d 1049, 1064 (9th Cir. 2008): Revised forecast caused loss, not 1049, 1064 (9th Cir. 2008): Revised forecast caused loss, not ( )( )because of “revelation” of alleged fraud, but because “the because of “revelation” of alleged fraud, but because “the company failed to hit prior earnings estimates.”company failed to hit prior earnings estimates.”In re In re TelliumTellium, Inc. Sec. Litig., Inc. Sec. Litig., 2005 WL 2090254, at *3, 2005 WL 2090254, at *3--4 4 (D.N.J. Aug. 26, 2005): Announcement that revenues were (D.N.J. Aug. 26, 2005): Announcement that revenues were lower than expected was held not to be a corrective disclosure, lower than expected was held not to be a corrective disclosure, because the bad news did not disclose the fraud.because the bad news did not disclose the fraud.

12

Loss Causation Shown Loss Causation Shown ––Materialization of the Concealed RiskMaterialization of the Concealed Risk

Generally, if there is no corrective disclosure, the necessary Generally, if there is no corrective disclosure, the necessary materialization of risk is “sudden and caused the stock value to materialization of risk is “sudden and caused the stock value to plummet.” plummet.” In re In re RhodiaRhodia S.A. Sec. Litig.S.A. Sec. Litig., 2007 U.S. Dist. , 2007 U.S. Dist. LEXIS 72758 (S.D.N.Y. Sept. 26, 2007) (certain claims LEXIS 72758 (S.D.N.Y. Sept. 26, 2007) (certain claims dismissed).dismissed).For example, in For example, in In re In re ParmalatParmalat Securities Litigation,Securities Litigation,disclosure of a bond default was held to be the materialization disclosure of a bond default was held to be the materialization of the alleged fraudulent scheme. 375 F. Supp. 2d 278, 284 of the alleged fraudulent scheme. 375 F. Supp. 2d 278, 284 (S D N Y 2005)(S D N Y 2005)

13

(S.D.N.Y. 2005).(S.D.N.Y. 2005).

8

Loss Causation Shown Loss Causation Shown ––Materialization of the Concealed Risk Materialization of the Concealed Risk (cont’d)(cont’d)

Stock price decline following disclosure of accounting Stock price decline following disclosure of accounting problems was held to be the materialization of risk from problems was held to be the materialization of risk from ppconcealed internal control deficiencies. concealed internal control deficiencies. In re Scottish Re In re Scottish Re Group Sec. Litig.Group Sec. Litig., 2007 U.S. Dist. LEXIS 81565, *59, 2007 U.S. Dist. LEXIS 81565, *59--*62 *62 (S.D.N.Y. Nov. 2, 2007).(S.D.N.Y. Nov. 2, 2007).Plaintiffs adequately alleged that stock price decline resulted Plaintiffs adequately alleged that stock price decline resulted from concealed risks of various liabilities which became from concealed risks of various liabilities which became public, including in an analyst report. public, including in an analyst report. Schleicher v. WendtSchleicher v. Wendt, , 2007 U S Dist LEXIS 67924 *552007 U S Dist LEXIS 67924 *55 *57 (S D Ind Sept 12*57 (S D Ind Sept 12

No Loss Causation No Loss Causation ––No Concealed Risk Nor Corrective DisclosureNo Concealed Risk Nor Corrective Disclosure

Estimated $200 million jury verdict was overturned because Estimated $200 million jury verdict was overturned because the court found that analyst reports “did not provide any fraudthe court found that analyst reports “did not provide any fraud--y p p yy p p yrevealing analysis” and were therefore not “corrective.” revealing analysis” and were therefore not “corrective.” In re In re Apollo Group, Inc. Sec. Litig.Apollo Group, Inc. Sec. Litig., 2008 WL 3072731, at *3 ( D. , 2008 WL 3072731, at *3 ( D. Ariz. Aug. 4, 2008)Ariz. Aug. 4, 2008)Claims against accounting firm for allegedly false audit Claims against accounting firm for allegedly false audit opinions concerning AOL were dismissed to the extent they opinions concerning AOL were dismissed to the extent they neither concealed any undisclosed risk nor were ever neither concealed any undisclosed risk nor were ever correctedcorrected In re AOL Time Warner Inc Sec LitigIn re AOL Time Warner Inc Sec Litig 503 F503 F

15

corrected. corrected. In re AOL Time Warner, Inc. Sec. Litig.In re AOL Time Warner, Inc. Sec. Litig.,, 503 F. 503 F. Supp. 2d 666, 677Supp. 2d 666, 677--80 (S.D.N.Y. 2007)80 (S.D.N.Y. 2007)

In re Bradley In re Bradley PharmsPharms., Inc. Sec. Litig., ., Inc. Sec. Litig., 2006 WL 740793 2006 WL 740793 (D.N.J. Mar. 23, 2006): Court held that announcement of SEC (D.N.J. Mar. 23, 2006): Court held that announcement of SEC ( )( )investigation, resulting in stock drop, could be a partial investigation, resulting in stock drop, could be a partial corrective disclosure.corrective disclosure.Asher v. Baxter Int’l, Inc.Asher v. Baxter Int’l, Inc., 2006 WL 299068 (, 2006 WL 299068 (N.D.IllN.D.Ill. Feb. 7, . Feb. 7, 2006): Although a “close question,” court held disclosure of 2006): Although a “close question,” court held disclosure of disappointing quarterly results could be a corrective disclosure disappointing quarterly results could be a corrective disclosure of company’s prior allegedly fraudulent projections, in of company’s prior allegedly fraudulent projections, in apparent tension withapparent tension with TelliumTellium rulingruling suprasupra

16

apparent tension with apparent tension with TelliumTellium ruling, ruling, supra. supra.

Event Studies AssessingEvent Studies AssessingLoss Causation and DamagesLoss Causation and Damages

Event studies may be used to prove or disprove loss causation Event studies may be used to prove or disprove loss causation by providing a methodology for analyzing companyby providing a methodology for analyzing company--specific specific y p g gy y g p yy p g gy y g p y ppstock price movementsstock price movements“The tool most often used by experts to isolate the effect of a “The tool most often used by experts to isolate the effect of a corrective disclosure on the stock price is the ‘event study.’” corrective disclosure on the stock price is the ‘event study.’” Apollo, supra, Apollo, supra, at n. 1at n. 1..In the Fifth Circuit, in support of a motion for class In the Fifth Circuit, in support of a motion for class certification, “the testimony of an expertcertification, “the testimony of an expert----along with some along with some

17

kind of analytical research or event studykind of analytical research or event study----is required to show is required to show loss causation.” loss causation.” FenerFener v. Belo Corp.v. Belo Corp., 579 F.3d 401 (5, 579 F.3d 401 (5thth Cir. Cir. 2009)2009)

10

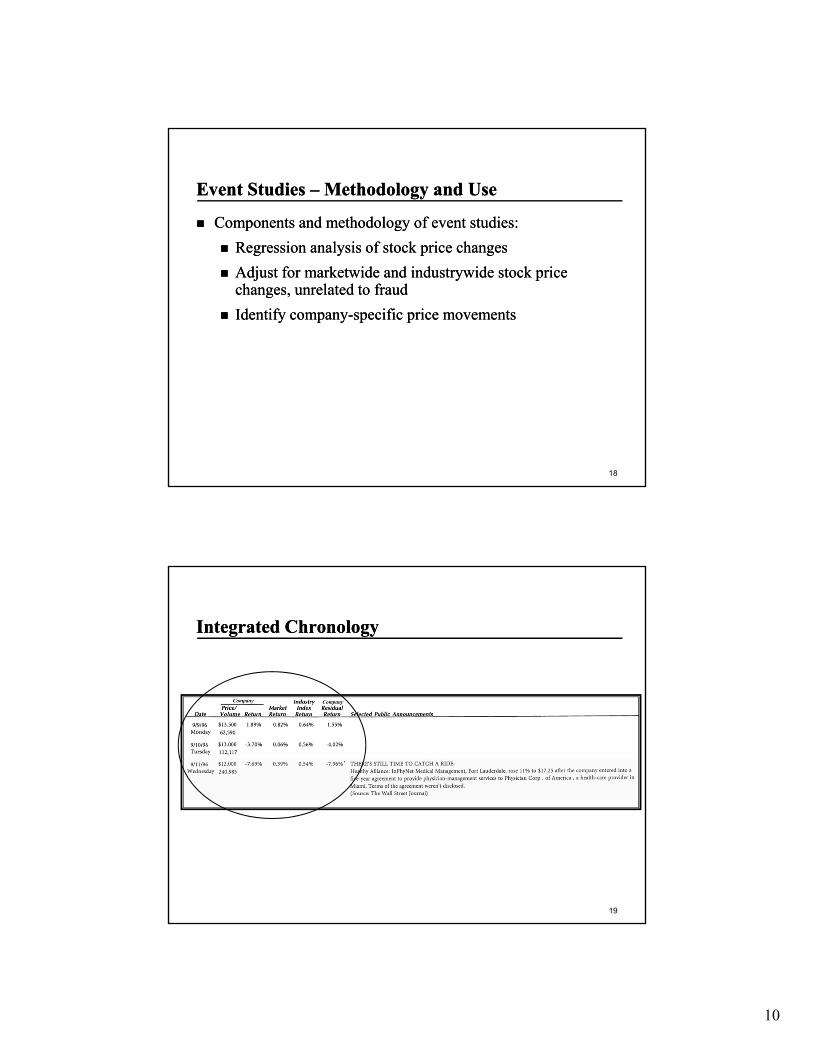

Event Studies Event Studies –– Methodology and UseMethodology and Use

Components and methodology of event studies:Components and methodology of event studies:Regression analysis of stock price changesRegression analysis of stock price changesRegression analysis of stock price changesRegression analysis of stock price changesAdjust for marketwide and industrywide stock price Adjust for marketwide and industrywide stock price changes, unrelated to fraud changes, unrelated to fraud Identify companyIdentify company--specific price movementsspecific price movements

18

Integrated ChronologyIntegrated Chronology

19

11

20

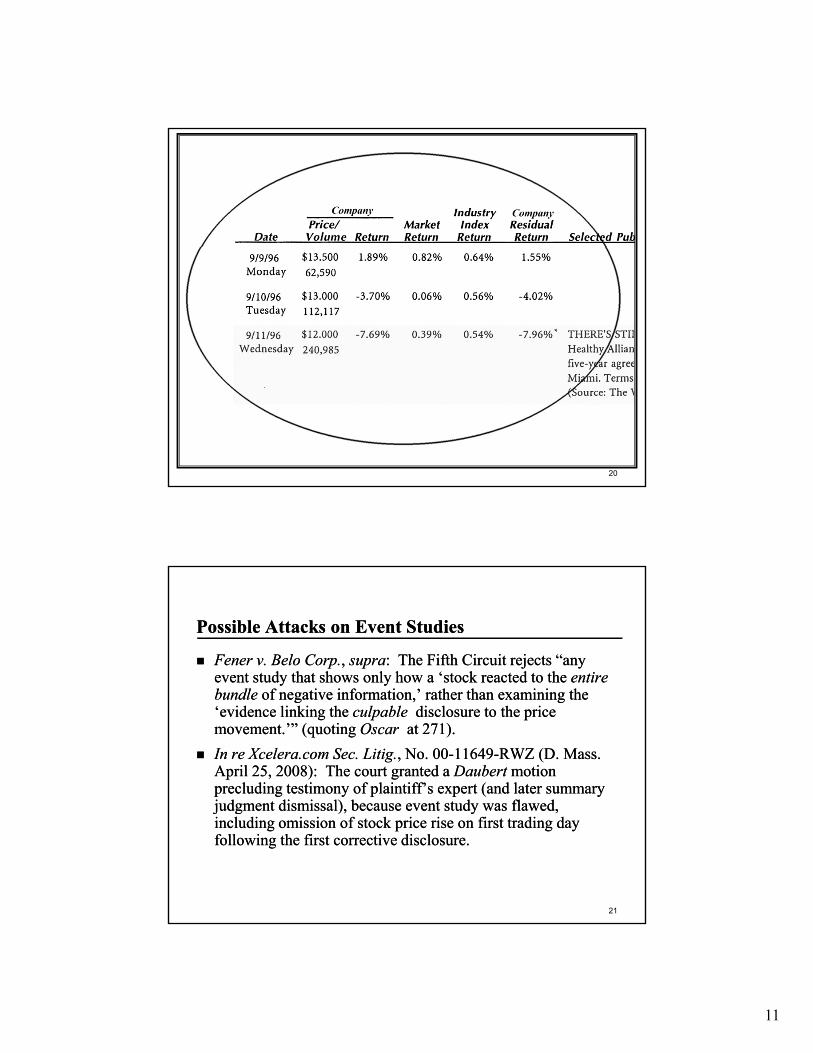

Possible Attacks on Event StudiesPossible Attacks on Event Studies

FenerFener v. Belo v. Belo Corp.Corp., , suprasupra: The Fifth Circuit rejects “any : The Fifth Circuit rejects “any event study that shows only how a ‘stock reacted to the event study that shows only how a ‘stock reacted to the entire entire y yy ybundlebundle of negative information,’ rather than examining the of negative information,’ rather than examining the ‘evidence linking the ‘evidence linking the culpableculpable disclosure to the price disclosure to the price movement.’” (quoting movement.’” (quoting Oscar Oscar at 271).at 271).In In re Xcelera.com Sec. Litig.re Xcelera.com Sec. Litig., No. 00, No. 00--1164911649--RWZ (D. Mass. RWZ (D. Mass. April 25, 2008): April 25, 2008): The court The court granted granted a a DaubertDaubert motion motion precluding testimony of plaintiff’s expert (and later summary precluding testimony of plaintiff’s expert (and later summary judgment dismissal) because event study was flawedjudgment dismissal) because event study was flawed

21

judgment dismissal), because event study was flawed, judgment dismissal), because event study was flawed, including omission of stock price rise on first trading day including omission of stock price rise on first trading day following the first corrective following the first corrective disclosure. disclosure.

12

Expert Opinions Showing Loss CausationExpert Opinions Showing Loss Causation

Court denied defendants’ summary judgment motion based on Court denied defendants’ summary judgment motion based on plaintiff expert’s opinion, but allowed possible later plaintiff expert’s opinion, but allowed possible later DaubertDaubertp p p pp p p pchallenge in challenge in In re BristolIn re Bristol--Myers Squibb Sec. Litig.Myers Squibb Sec. Litig., 2005 U.S. , 2005 U.S. Dist. LEXIS 18448, at *62Dist. LEXIS 18448, at *62--63 (D.N.J. Aug. 17, 2005)63 (D.N.J. Aug. 17, 2005)Plaintiffs’ expert showed loss causation that raised an issue for Plaintiffs’ expert showed loss causation that raised an issue for trial in trial in In re In re PharmaprintPharmaprint, Inc. Sec. Litig., Inc. Sec. Litig., 2002 U.S. Dist. , 2002 U.S. Dist. LEXIS 19845, at *26 (D.N.J. Apr.17, 2002)LEXIS 19845, at *26 (D.N.J. Apr.17, 2002)Plaintiffs won summary judgment using an event study Plaintiffs won summary judgment using an event study

22

showing loss causation in showing loss causation in Gaming Lottery Sec. Litig.Gaming Lottery Sec. Litig., 2001 , 2001 U.S. Dist. LEXIS 2034 (S.D.N.Y. Mar.U.S. Dist. LEXIS 2034 (S.D.N.Y. Mar. 1, 2001)1, 2001)

Failure of Expert to Show Loss CausationFailure of Expert to Show Loss Causation

Summary judgment dismissal affirmed where plaintiff’s Summary judgment dismissal affirmed where plaintiff’s expert’s methods did not “reliably link the class’s losses to the expert’s methods did not “reliably link the class’s losses to the p yp yrevelation of the alleged misrepresentations, as revelation of the alleged misrepresentations, as Dura Dura requires.” requires.” In re Williams Sec. Litig. In re Williams Sec. Litig. –– WCG SubclassWCG Subclass, 558 F.3d 1130, , 558 F.3d 1130, 1137 (101137 (10thth Cir. 2009).Cir. 2009).Plaintiffs Plaintiffs offered no expert testimony or other evidence to offered no expert testimony or other evidence to show loss causation, where the stock price had collapsed show loss causation, where the stock price had collapsed before alleged fraud was revealed. before alleged fraud was revealed. Ray v. Citigroup Global Ray v. Citigroup Global Markets IncMarkets Inc 2005 U S Dist LEXIS 24419 at *11 (N D Ill2005 U S Dist LEXIS 24419 at *11 (N D Ill

23

Markets, Inc., Markets, Inc., 2005 U.S. Dist. LEXIS 24419, at *11 (N.D. Ill. 2005 U.S. Dist. LEXIS 24419, at *11 (N.D. Ill. Oct. 18, 2005), Oct. 18, 2005), aff’daff’d, 482 F.3d 991 (7, 482 F.3d 991 (7thth Cir. 2007Cir. 2007).).

13

Defense Expert May Disprove Loss CausationDefense Expert May Disprove Loss Causation

“Defendants’ expert’s event study proved that none of the “Defendants’ expert’s event study proved that none of the alleged misstatements . . . had an effect on the stock price.” alleged misstatements . . . had an effect on the stock price.” g pg pNathenson v. Zonagen, Inc.Nathenson v. Zonagen, Inc., 322 F. Supp. 2d 764, 780 (S.D. , 322 F. Supp. 2d 764, 780 (S.D. Tex.), Tex.), aff'd in pertinent partaff'd in pertinent part, 267 F.3d 400 (5th Cir. 2001)., 267 F.3d 400 (5th Cir. 2001).

24

DamagesDamages

No express measure of damages under Section 10(b)No express measure of damages under Section 10(b)Section 28(a) provides that recovery shall not exceed aSection 28(a) provides that recovery shall not exceed aSection 28(a) provides that recovery shall not exceed a Section 28(a) provides that recovery shall not exceed a plaintiff’s “actual damages”plaintiff’s “actual damages”

25

14

Damages Measure in Section 10(b) Damages Measure in Section 10(b) “Fraud on the Market” Cases“Fraud on the Market” Cases

“Out“Out--ofof--pocket” measure of damages. pocket” measure of damages. Affiliated UteAffiliated Ute, 406 U.S. , 406 U.S. 128, 128, 155 (1972); 155 (1972); Gurary v. WinehouseGurary v. Winehouse, 235 F.3d 792 (2nd Cir. , 235 F.3d 792 (2nd Cir. ( )( ) yy ((2000)2000)

Amount overpaid by stock Amount overpaid by stock purchaserspurchasers because stock price because stock price was artificially inflated by alleged misrepresentation or was artificially inflated by alleged misrepresentation or omission; oromission; orAmount lost by stock Amount lost by stock sellerssellers because stock price was because stock price was artificially deflated by alleged misrepresentation or artificially deflated by alleged misrepresentation or

26

omissionomission

Aggregate Damages in Class ActionAggregate Damages in Class Action

Multiply: Per share damages (generally determined by event Multiply: Per share damages (generally determined by event studies)studies)))Times: Number of shares damaged (plaintiffs offer stock Times: Number of shares damaged (plaintiffs offer stock trading models/defendants may object)trading models/defendants may object)PSLRA provides “bouncePSLRA provides “bounce--back” rule back” rule which caps perwhich caps per--share share damages by the excess of purchase price over postdamages by the excess of purchase price over post--disclosure disclosure average price (to the earlier of sale or 90 days).average price (to the earlier of sale or 90 days). See See 15 U.S.C. 15 U.S.C. §§78u78u--4(e)4(e)

27

15

Determining PerDetermining Per--ShareShareDamages During Class PeriodDamages During Class Period

PerPer--share damages: The difference between “true value” of share damages: The difference between “true value” of stock and actual price paid by buyer stock and actual price paid by buyer p p y yp p y yGenerally, plaintiffs argue that stock price decline after Generally, plaintiffs argue that stock price decline after corrective disclosure reflects amount price was inflatedcorrective disclosure reflects amount price was inflatedProving damages can be a “daunting task”Proving damages can be a “daunting task”---- usually a “battle usually a “battle of experts,” of experts,” In re In re MicrostrategyMicrostrategy Sec. Litig.Sec. Litig., 150 , 150 F.SuppF.Supp. 2d . 2d 896 (E.D. Va. 2001)896 (E.D. Va. 2001)

28

Event Studies Necessary to Event Studies Necessary to Calculate Per Share DamagesCalculate Per Share Damages

Need to factor out extraneous factors and isolate effect of Need to factor out extraneous factors and isolate effect of fraud on stock pricefraud on stock priceppDamage calculations have been rejected for failure to conduct Damage calculations have been rejected for failure to conduct an event study, an event study, e.g., In re Imperial Credit Indus.; Executive e.g., In re Imperial Credit Indus.; Executive TelecardTelecard Sec. LitigSec. Litig., 979 F. Supp. 1021 (S.D.N.Y. 1997);., 979 F. Supp. 1021 (S.D.N.Y. 1997);Oracle SecOracle Sec. . Litig., Litig., 829 F. Supp. 1176 (N.D. Cal. 1993)829 F. Supp. 1176 (N.D. Cal. 1993)Where regression analysis was not feasible, event study was Where regression analysis was not feasible, event study was not required in not required in RMED Int’l v. Sloan’sRMED Int’l v. Sloan’s, 2000 U.S. Dist. LEXIS , 2000 U.S. Dist. LEXIS

29

3742 (S.D.N.Y. Mar. 24, 2000)3742 (S.D.N.Y. Mar. 24, 2000)

16

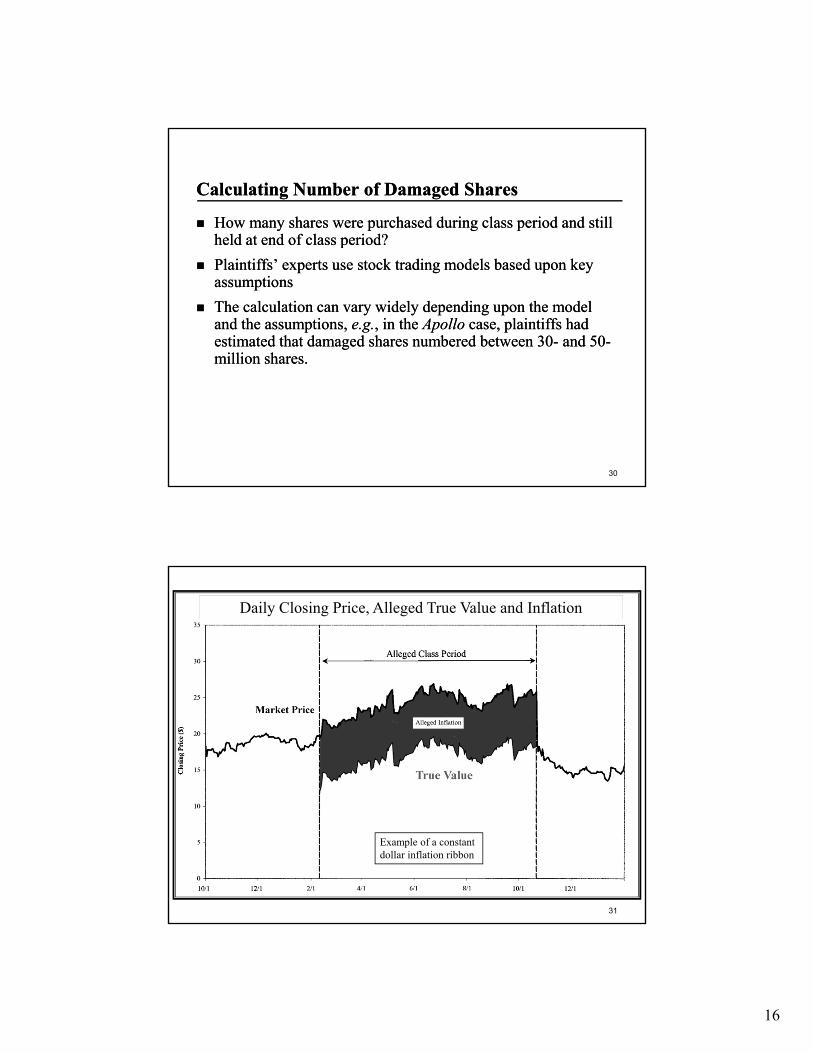

Calculating Number of Damaged SharesCalculating Number of Damaged Shares

How many shares were purchased during class period and still How many shares were purchased during class period and still held at end of class period?held at end of class period?ppPlaintiffs’ experts use stock trading models based upon key Plaintiffs’ experts use stock trading models based upon key assumptionsassumptionsThe calculation can vary widely depending upon the model The calculation can vary widely depending upon the model and the assumptions, and the assumptions, e.g.e.g., in the , in the ApolloApollo case, plaintiffs had case, plaintiffs had estimated that damaged shares numbered between 30estimated that damaged shares numbered between 30-- and 50and 50--million shares.million shares.

30

Daily Closing Price, Alleged True Value and Inflation

31

Example of a constant dollar inflation ribbon

17

Stock Trading ModelStock Trading Model

Estimate float available for trading by class members by Estimate float available for trading by class members by making adjustments to total outstanding sharesmaking adjustments to total outstanding sharesg j gg j gEstimate total shares traded by class members by making Estimate total shares traded by class members by making adjustments to reported trading volumeadjustments to reported trading volumeAssume trading pattern: Determine number of retained shares Assume trading pattern: Determine number of retained shares that are damagedthat are damaged

32

Stock Trading Models Stock Trading Models –– Typical Adjustments to Float Typical Adjustments to Float and Trading Volume Inputsand Trading Volume Inputs

Float adjustmentsFloat adjustmentsInstitutional investors that do not trade during the damage period (Institutional investors that do not trade during the damage period (--))g g p (g g p ( ))Insider holdings (Insider holdings (--))Company stock in 401(k) plan (Company stock in 401(k) plan (--))Short interest (+)Short interest (+)

Trading volume adjustments Trading volume adjustments Double counting in the reported volume due to market maker activity Double counting in the reported volume due to market maker activity ((--))

33

Short sellers covering positions (Short sellers covering positions (--))Changes in insiders holdings (Changes in insiders holdings (--))Stock buybacks (Stock buybacks (--))Lower float or trading volume results in fewer retained shares Lower float or trading volume results in fewer retained shares and lower damagesand lower damages

18

Types of Stock Trading Models Types of Stock Trading Models Proportional Trading Model (PTM)Proportional Trading Model (PTM)

Typical original plaintiffTypical original plaintiff--style modelstyle modelyp g pyp g p yyAssumes every share is equally likely to tradeAssumes every share is equally likely to trade

Accelerated Trading Model (ATM)Accelerated Trading Model (ATM)Generally lower damages than PTMGenerally lower damages than PTMAssumes shares traded since beginning of class period are more Assumes shares traded since beginning of class period are more likely to trade than shares that have not traded during class likely to trade than shares that have not traded during class periodperiod

T T d M d l (TTM)T T d M d l (TTM)

34

Two Trader Model (TTM)Two Trader Model (TTM)Modified plaintiffModified plaintiff--style modelstyle modelGenerally lower damages than PTMGenerally lower damages than PTMAssumes one class of shares (“Traders”) has a much higher Assumes one class of shares (“Traders”) has a much higher likelihood of trading than other class of shares (“Investors”)likelihood of trading than other class of shares (“Investors”)

Example of PTM Trading Damages AnalysisExample of PTM Trading Damages Analysis

35

19

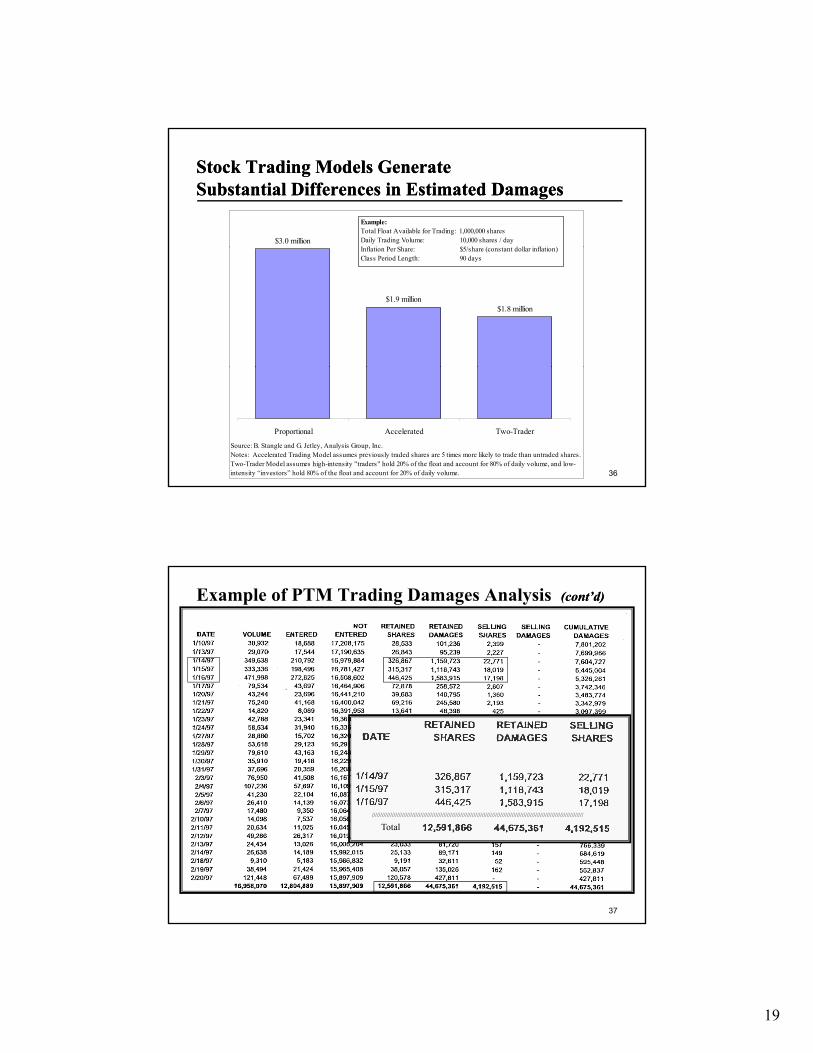

Stock Trading Models GenerateStock Trading Models GenerateSubstantial Differences in Estimated DamagesSubstantial Differences in Estimated Damages

$3.0 million

Example: Total Float Available for Trading: 1,000,000 sharesDaily Trading Volume: 10,000 shares / dayI fl ti P Sh $5/ h ( t t d ll i fl ti )

$1.8 million$1.9 million

Inflation Per Share: $5/share (constant dollar inflation)Class Period Length: 90 days

36

Proportional Accelerated Two-Trader

Source: B. Stangle and G. Jetley, Analysis Group, Inc.Notes: Accelerated Trading Model assumes previously traded shares are 5 times more likely to trade than untraded shares.Two-Trader Model assumes high-intensity "traders" hold 20% of the float and account for 80% of daily volume, and low-intensity “investors” hold 80% of the float and account for 20% of daily volume.

Example of PTM Trading Damages Analysis (cont’d)(cont’d)

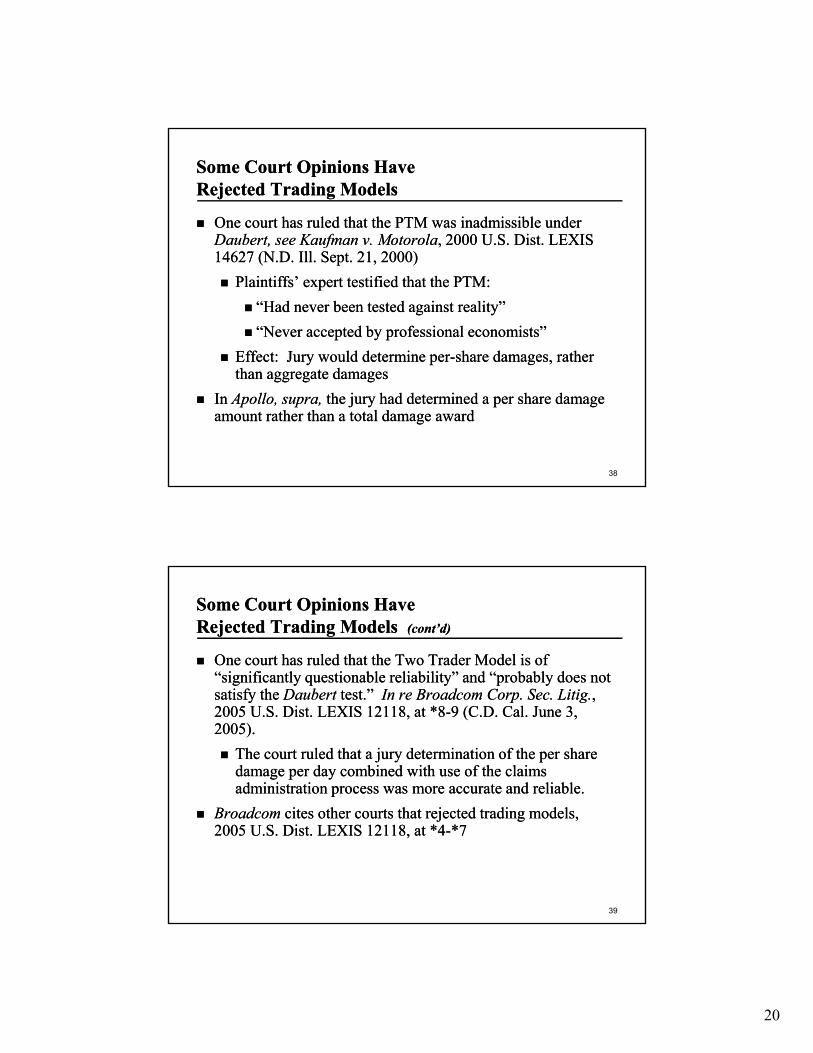

Some Court Opinions Have Some Court Opinions Have Rejected Trading ModelsRejected Trading Models

One court has ruled that the PTM was inadmissible under One court has ruled that the PTM was inadmissible under DaubertDaubert, see, see Kaufman v. MotorolaKaufman v. Motorola, 2000 U.S. Dist. LEXIS , 2000 U.S. Dist. LEXIS ff14627 (N.D. Ill. Sept.14627 (N.D. Ill. Sept. 21, 2000)21, 2000)

Plaintiffs’ expert testified that the PTM:Plaintiffs’ expert testified that the PTM:“Had never been tested against reality”“Had never been tested against reality”“Never accepted by professional economists”“Never accepted by professional economists”

Effect: Jury would determine perEffect: Jury would determine per--share damages, rather share damages, rather

38

than aggregate damagesthan aggregate damagesIn In Apollo, supra, Apollo, supra, the jury had determined a per share damage the jury had determined a per share damage amount rather than a total damage awardamount rather than a total damage award

One court has ruled that the Two Trader Model is of One court has ruled that the Two Trader Model is of “significantly questionable reliability” and “probably does not “significantly questionable reliability” and “probably does not g y q y p yg y q y p ysatisfy the satisfy the DaubertDaubert test.”test.” In re Broadcom Corp. Sec. Litig.In re Broadcom Corp. Sec. Litig., , 2005 U.S. Dist. LEXIS 12118, at *82005 U.S. Dist. LEXIS 12118, at *8--9 (C.D. Cal. June 3, 9 (C.D. Cal. June 3, 2005).2005).

The court ruled that a jury determination of the per share The court ruled that a jury determination of the per share damage per day combined with use of the claims damage per day combined with use of the claims administration process was more accurate and reliable.administration process was more accurate and reliable.

39

Broadcom Broadcom cites other courts that rejected trading models, cites other courts that rejected trading models, 2005 U.S. Dist. LEXIS 12118, at *42005 U.S. Dist. LEXIS 12118, at *4--*7*7

21

Other Courts Have Accepted Trading Other Courts Have Accepted Trading Models or Other Proof of Aggregate DamagesModels or Other Proof of Aggregate Damages

In In In re In re WorldcomWorldcom, Inc. Sec. Litig., , Inc. Sec. Litig., 2005 U.S. Dist. LEXIS 2005 U.S. Dist. LEXIS 3143 (S.D.N.Y. Mar. 3, 2005), evidence of aggregate damages 3143 (S.D.N.Y. Mar. 3, 2005), evidence of aggregate damages ( ) gg g g( ) gg g gwas allowed, but no stock trading model was at issuewas allowed, but no stock trading model was at issuePlaintiffs’ expert’s calculation of aggregate shares held Plaintiffs’ expert’s calculation of aggregate shares held admissible, without considering admissible, without considering Motorola Motorola criticisms, in criticisms, in BlechBlechSec. Litig., Sec. Litig., 2003 U.S. Dist. LEXIS 4650 (S.D.N.Y. Mar. 26, 2003 U.S. Dist. LEXIS 4650 (S.D.N.Y. Mar. 26, 2003)2003)Some courts view criticisms of PTM as going to weight and Some courts view criticisms of PTM as going to weight and

40

credibility, rather than admissibility, credibility, rather than admissibility, e.g., In re Cendant Corp. e.g., In re Cendant Corp. Sec. Litig.Sec. Litig., 109 F. Supp. 2d 235 (D.N.J. 2000), 109 F. Supp. 2d 235 (D.N.J. 2000)

ConclusionConclusion

Securities fraud cases present loss causation and damage Securities fraud cases present loss causation and damage issues that invite creative legal and economic analysis. issues that invite creative legal and economic analysis. g yg yExpert witnesses and studies play an important role in Expert witnesses and studies play an important role in analyzing and presenting arguments on those issues. analyzing and presenting arguments on those issues.