58

DARWIN FENNER FUND HEALTHCARE & CONSUMER STAPLES FINAL REPORT S&P 600 SMALL-CAP Brandon Bujnowski, Yuan (Miya) Meng, Chao Wang, Yinuo (Perfeeno) Wang April 30th, 2015

DARWIN FENNER FUND HEALTHCARE &

CONSUMER STAPLES FINAL REPORT

S&P 600 SMALL-CAP

Brandon Bujnowski, Yuan (Miya) Meng, Chao Wang, Yinuo (Perfeeno) Wang

April 30th, 2015

Small-Cap Portfolio: Healthcare & Consumer Staples

Page 1 of 57

3

HEALTHCARE 3

STOCK LIST 4

RECOMMENDATIONS 6 HEALTHCARE SECTOR ANALYSIS 6

STOCK PERFORMANCE SNAPSHOT 6

OVERVIEW 7

RELATIVE PERFORMANCE AND RISK 7

GROWTH/VALUE SECTOR CLASSIFICATION 9

OVERWEIGHT AND UNDERWEIGHT DECISION 10

HEALTHCARE SECTOR PROCESS FLOWCHART 11

QUANTITATIVE SCREENINGS AND ANALYSIS 12

STEP 0: CAPITALIZING R&D 12

STEP 1: FUNDAMENTAL GROWTH 12

RISK ANALYSIS: STEP Z: BANKRUPTCY RISK 14

STEP 2: VALUE OR GROWTH 14

STEP 3: PROFITABILITY 15

QUALITATIVE SCREENS & ANALYSIS 16 MACROECONOMIC DRIVERS 17

FIRM OPERATIONS 17

CORPORATE GOVERNANCE AND MANAGEMENT 18

FINANCIAL QUALITY 18

FIRM-SPECIFIC QUALITATIVE ANALYSIS TABLES 19

NATUS MEDICAL INC. (BABY) 20

MERIDIAN BIOSCIENCES INC. (VIVO) 20

SURMODICS INC. (SRDX) 21

ANIKA THERAPEUTICS INC. (ANIK) 22

EMERGENT BIOSOLUTIONS INC (EBS) 22 CAMBREX CORP. (CBM) 23

ALMOST FAMILY INC. (AFAM) 24

PHARMERICA CORP (PMC) 24 INVESTMENT IDEA SUMMARY 25

NATUS MEDICAL INC. (NASDAQ: BABY)- STRONG BUY 25

MERIDIAN BIOSCIENCE, INC. (NASDAQ: VIVO)- BUY 25

SURMODICS, INC. (NASDAQ: SRDX)- BUY 26

ANIKA THERAPEUTICS INC. (NASDAQ: ANIK)- DELETE 26

EMERGENT BIOSOLUTIONS INC (NASDAQ: EBS)- HOLD 26

CAMBREX CORP. (NASDAQ: CBM)- HOLD 26 ALMOST FAMILY INC. (NASDAQ: AFAM)- SELL 27

PHARMERICA CORP (NASDAQ: PMC)- SELL 27

Table of Contents

Small-Cap Portfolio: Healthcare & Consumer Staples

Page 2 of 57

CONSUMER STAPLES 28

STOCK LIST 29

RECOMMENDATIONS 30 HEALTHCARE SECTOR ANALYSIS 30

STOCK PERFORMANCE SNAPSHOT 30

OVERVIEW 31

RELATIVE PERFORMANCE AND RISK 31

GROWTH/VALUE SECTOR CLASSIFICATION 33

OVERWEIGHT AND UNDERWEIGHT DECISION 34 HEALTHCARE SECTOR PROCESS FLOWCHART 35

QUANTITATIVE SCREENINGS AND ANALYSIS 36

STEP 1: FUNDAMENTAL GROWTH 36

RISK ANALYSIS: STEP Z: BANKRUPTCY RISK 38 STEP 2: VALUE OR GROWTH 38

STEP 3: PROFITABILITY 39

QUALITATIVE SCREENS & ANALYSIS 40 MACROECONOMIC DRIVERS 40

FIRM OPERATIONS 40

CORPORATE GOVERNANCE AND MANAGEMENT 40

FINANCIAL QUALITY 41 FIRM-SPECIFIC QUALITATIVE ANALYSIS TABLES 42

B&G FOODS INC. (BGS) 43

SPARTNASH CO. (SPTN) 44 MEDIFAST INC. (MED) 45

INVESTMENT IDEA SUMMARY 45

B&G FOODS (NYSE: BGS)- BUY 45 SPARTANNASH CO. (NASDAQ: SPTN)- HOLD 46

MEDIFAST INC. (NYSE: MED)-STRONG SELL 46

REFERENCES 47

APPENDIX 48

Small-Cap Portfolio: Healthcare & Consumer Staples

Page 3 of 57

Healthcare

Small-Cap Portfolio: Healthcare & Consumer Staples

Page 4 of 57

TICKER NAME SUB-SECTOR

RGEN Repligen Biotechnology

SPPI Spectrum Pharmaceuticals Biotechnology

EBS Emergent Biosolutions Biotechnology

LGND Ligand Pharmaceuticals Biotechnology

MNTA Momenta Pharmaceuticals Biotechnology

ACOR Acorda Therapeutics Biotechnology

ACET Aceto Health Care Distributors

PMC PharMerica Health Care Distributors

BABY Natus Medical Health Care Equipment

ANGO AngioDynamics Health Care Equipment

ALOG Analogic Health Care Equipment

GB Greatbatch Health Care Equipment

IVC Invacare Health Care Equipment

NUVA NuVasive Health Care Equipment

IART Integra LifeSciences Holdings Health Care Equipment

CYNO Cynosure Health Care Equipment

MASI Masimo Health Care Equipment

ABAX Abaxis Health Care Equipment

ABMD ABIOMED Health Care Equipment

SRDX SurModics Health Care Equipment

CNMD CONMED Health Care Equipment

CMN Cantel Medical Health Care Equipment

CYBX Cyberonics Health Care Equipment

CRY CryoLife Health Care Equipment

HGR Hanger Health Care Facilities

SEM Select Medical Holdings Health Care Facilities

KND Kindred Healthcare Health Care Facilities

ENSG Ensign Group/The Health Care Facilities

AMSG Amsurg Health Care Facilities

CHE Chemed Health Care Services

PRSC Providence Service/The Health Care Services

CCRN Cross Country Healthcare Health Care Services

LDR Landauer Health Care Services

Stock List

Healthcare (71 Stocks)

Small-Cap Portfolio: Healthcare & Consumer Staples

Page 5 of 57

TICKER NAME SUB-SECTOR

AHS AMN Healthcare Services Health Care Services

LHCG LHC Group Health Care Services

IPCM IPC Healthcare Health Care Services

HWAY Healthways Health Care Services

AIRM Air Methods Health Care Services

BRLI Bio-Reference Laboratories Health Care Services

AMED Amedisys Health Care Services

CRVL CorVel Health Care Services

AFAM Almost Family Health Care Services

EXAM ExamWorks Group Health Care Services

ICUI ICU Medical Health Care Supplies

VIVO Meridian Bioscience Health Care Supplies

HAE Haemonetics Health Care Supplies

MMSI Merit Medical Systems Health Care Supplies

NEOG Neogen Health Care Supplies

VASC Vascular Solutions Health Care Supplies

WST West Pharmaceutical Services Health Care Supplies

ANIK Anika Therapeutics Health Care Supplies

OMCL Omnicell Health Care Technology

CPSI Computer Programs & Systems Health Care Technology

QSII Quality Systems Health Care Technology

MDSO Medidata Solutions Health Care Technology

HSTM HealthStream Health Care Technology

MDAS MedAssets Health Care Technology

LMNX Luminex Life Sciences Tools & Services

AFFX Affymetrix Life Sciences Tools & Services

PRXL PAREXEL International Life Sciences Tools & Services

AMRI Albany Molecular Research Life Sciences Tools & Services

CBM Cambrex Life Sciences Tools & Services

MGLN Magellan Health Managed Health Care

MOH Molina Healthcare Managed Health Care

ANIP ANI Pharmaceuticals Pharmaceuticals

LCI Lannett Co Pharmaceuticals

SGNT Sagent Pharmaceuticals Pharmaceuticals

DEPO Depomed Pharmaceuticals

PBH Prestige Brands Holdings Pharmaceuticals

IPXL Impax Laboratories Pharmaceuticals

MDCO Medicines Co/The Pharmaceuticals

Small-Cap Portfolio: Healthcare & Consumer Staples

Page 6 of 57

Table 1 illustrates all Buy, Hold, and Sell recommendations for the S&P 600 Healthcare stocks

covered in the quantitative and qualitative screens and analyses described in this report.

Table 1: Healthcare Sector Recommendations

Ticker Name Sub-industry Recommendation

BABY Natus Medical Inc. Healthcare Equipment STRONG BUY

VIVO Meridian Bioscience Inc. Healthcare Supplies BUY

SRDX SurModics Inc. Healthcare Equipment BUY

EBS Emergent Biosolutions Inc. Biotechnology HOLD

CBM Cambrex Corp. Life Science Tools & Services HOLD

PMC PharMerica Corp. Healthcare Distributors SELL

AFAM Almost Family Inc. Health Care Services STRONG SELL

Sector Performance Snapshot (as of February 22, 2015)

Previous 36 Month Data S&P 600 Healthcare

Alpha - 0.70%

CAPM Beta 1 0.95

Downside CAPM Beta 1 0.61

CAR - 23.02%

BAH Return 51.63% 89.18%

Abnormal BAH Return - 37.55%

Cumulative Wealth 1.516 1.89

Sharpe Ratio .34 .46

B-M Ratio 0.449 0.301

CF-P Ratio 0.071 0.045

E-P Ratio 0.034 0.019

Avg. Sales Growth (past 5 years) 27.93% 25.13%

Recommendations

Healthcare Sector Analysis

Small-Cap Portfolio: Healthcare & Consumer Staples

Page 7 of 57

Overview

The Healthcare sector of the S&P 600 consists of 71 firms and, as of February 22, 2015, makes

up 11.96% of the S&P 600 market capitalization. All data in this sector analysis section is

recorded as of February 22, 2015. The two sub-industry groups include:

Pharmaceuticals, Biotechnology, and Life Sciences Tools and Services.

Healthcare Facilities, Healthcare Equipment and Supplies, Healthcare Providers and

Services, and Healthcare Technology.

Figure 1: Healthcare Sub-Industry Weights

Relative Performance and Risk

The healthcare sector outperformed the S&P 600 over the past 36 months. As shown in Figure 5,

the cumulative wealth of healthcare has been dominating the S&P 600 over the past 36 months.

The cumulative market adjusted abnormal return is 23.02%. The buy and hold (BAH) return is

89.18%, higher than that of the S&P 600 (refer to Figure 3).

Biotechnology6.20%

Life Sciences Tools & Services

7.65%

Parmaceuticals12.98%

Healthcare Technology

8.21%

Healthcare Products & Services27.65%

Healthcare Equipment &

Supplies37.31%

Small-Cap Portfolio: Healthcare & Consumer Staples

Page 8 of 57

Figure 2: Cumulative Wealth over the Past 36 Months (Healthcare vs S&P 600)

Figure 3: Buy and Hold Return over the Past 36 Months (Healthcare vs S&P 600)

Concerning risk, the healthcare sector has a CAPM beta of 0.95, showing that the sector has a

slightly lower systematic risk than S&P 600. One possible explanation is that people are in need

of medical care and pharmaceuticals even in downward market periods. Therefore, stocks in the

healthcare sector are defensive, and are less sensitive to systematic risks.

Figure 4: Systematic Risk of Healthcare over the Past 36 Months

0.8

1

1.2

1.4

1.6

1.8

2

S&P 600 Healthcare

89.18%

51.63%

Buy and Hold Return

Healthcare S&P 600

10.95

S&P 600 HC

Small-Cap Portfolio: Healthcare & Consumer Staples

Page 9 of 57

Additionally, the sector has a downside beta of 0.62 over the past 36 months, lower than S&P

600, showing that the healthcare sector did not lose as much as S&P 600 in market downturns.

As mentioned before, the economic drivers of healthcare are increasing, preserving the sector

performance in a downward market periods. The upside beta of the healthcare sector is 1.18,

higher than 1, showing that when market returns were positive, the healthcare sector earned more

than the market on average. The higher-than-market upside beta leads to a CAPM beta close to 1.

Figure 5: Upside and Downside Betas for Healthcare over the Past 36 Months

Growth/Value Sector Classification

Using the S&P 600 as the benchmark, we first calculated the weighted average B/M ratio of the

S&P 600 and Healthcare sector. Results shown in Table 2 indicate that, comparing to the

benchmark, Healthcare is classified as a growth sector. We further tested the CF/P ratio and E/P

ratio (weighted average) for S&P 600 and Healthcare sector and found similar evidence.

Table 2: B/M, CF/P, and E/P ratio for S&P 600 and Healthcare

S&P 600 Healthcare G/V

B/M Ratio 0.449 0.301 G

CF/P Ratio 0.071 0.045 G

E/P Ratio 0.034 0.019 G

*Data source: Bloomberg, 02/22/2015

The B/M ratio, CF/P ratio, and E/P ratio have a good consistency in classifying the Healthcare

sector. Therefore, the Healthcare sector is classified as a growth sector.

1

1

0.62

1.18S&P 600 HC

Small-Cap Portfolio: Healthcare & Consumer Staples

Page 10 of 57

Overweight and Underweight Decision

Previously stated performance evidence and industry trends suggest that the Darwin Fenner Fund

(DFF) portfolio should overweight the healthcare sector.

Currently, the DFF has four healthcare sector stocks: Almost Family Inc., Cambrex Corp.,

Emergent Biosolutions Inc., and PharMerica Corp., weighing at 11.25% of the portfolio.

Similarly, the healthcare sector weight in the S&P 600 is 11.96%.

Several reasons can be used to explain the decision to overweight. First, economic drivers for

healthcare remain strong. The drivers, such as NHE and government budget, will take time to

boost revenue and stock price growth as the sector realizes a delayed impact. Second, the

population of senior citizens continues to rise. After the ACA was enacted and executed, more

previously uninsured people became included into the U.S. healthcare system, which will

increase industry revenue. And third, both the systematic and downside beta of the healthcare

sector over the past 36 months was lower than the S&P 600 benchmark, all the while producing a

significant, outperforming BAH return. Therefore, the Darwin Fenner Fund portfolio should

overweight the S&P 600 Healthcare sector.

Small-Cap Portfolio: Healthcare & Consumer Staples

Page 11 of 57

Healthcare Sector Process Flow Chart

Small-Cap Portfolio: Healthcare & Consumer Staples

Page 12 of 57

The quantitative screens are based on a theory of isolating firms that are increasingly financially

healthy, undervalued, and currently profitable. To begin, all stocks with an initial public offering

(IPO) within the last three years are eliminated prior to the remaining screening steps. After this

initial step, Sagent Pharmaceuticals (SGNT) was eliminated before any screens (also due to

lack of data available). The healthcare sector is unique in the sense that the firms spend various

amounts on research and development (R&D), including none at all. To control for R&D

spending, all R&D amounts are capitalized to account for total assets and net income. The

stocks then enter the firm fundamental stage and, based on variables that measure the change in a

firm’s financial ability, all stocks are ranked into quintiles. Each stock receives a score of 1 – 5

for each variable based on how well the stock ranked relative to other healthcare sector stocks.

After receiving scores for each variables, they are then weighted equally and summed up to

receive an aggregate score for each step. Below are the variables and methods used in Step 0:

Capitalize R&D and Step 1: Fundamental Growth:

Step 0: Capitalizing R&D

The healthcare sector is composed of several companies which may or may not develop patents

and new technology. Therefore, adjusting R&D expense for all companies is a key step to start

the quantitative screens. According to Chan, Lakonishok and Sougiannis, without capitalizing

R&D the book-to-market (B/M) ratio is distorted. Additionally, without adding back R&D

expense into earnings the cash flow-to-price (CF/P) ratio will also be distorted. The two

equations below were used to control for R&D expenses to create a fair screening process for

different types of firms, and the results are shown in Appendix _.

Adjusted Assets:

Adjusted Earnings:

Step 1: Fundamental Growth

The following growth variables are used to measure the trend in a company’s profitability,

financial health, and fundamental growth. Therefore, all variables are calculated by determining

the ratio for each of the past four years, calculating the change in each variable year over year,

and averaging the change over the last four years. Asness, Frazzini, and Pedersen (2014) and

Piotroski and So (2012) find that firm’s performing strongly under these variables statistically

generate higher abnormal returns. Step 1 results are shown in Exhibit 1 of the Appendix.

Quantitative Screens & Analysis

Small-Cap Portfolio: Healthcare & Consumer Staples

Page 13 of 57

Δ Return on Assets (ROA)

The change in ROA indicator measures the trend of management’s effectiveness in its ability to

generate revenue relative to the firm’s total assets during past years. ROA is calculated by:

𝑅𝑂𝐴 = 𝐴𝑑𝑗𝑢𝑠𝑡𝑒𝑑 𝑁𝑒𝑡 𝐼𝑛𝑐𝑜𝑚𝑒𝑡/(𝐴𝑑𝑗𝑢𝑠𝑡𝑒𝑑 𝐴𝑠𝑠𝑒𝑡𝑠𝑡−1 + 𝐴𝑑𝑗𝑢𝑠𝑡𝑒𝑑 𝐴𝑠𝑠𝑒𝑡𝑠𝑡

2)

An increasing ROA ratio earns a higher score.

Δ Gross Margin

The gross margin indicator measures the trend of a firm’s percentage of sales after subtracting

the cost of goods sold (COGS). A firm’s gross margin is an easy variable to illustrate how cost

effective a company can be. An increasing gross margin earns a higher score.

Δ Gross Profit Over Assets (GPOA)

According to Novy-Marx’s paper “The Other Side of Value” (2013), this indicator has the same

power as the B/M ratio. This ratio illustrates the trend of a company’s profit efficiency and

financial health over past years. A higher Δ GPOA earns a higher score. GPOA is calculated

by:

𝐺𝑃𝑂𝐴 = 𝐺𝑟𝑜𝑠𝑠 𝑃𝑟𝑜𝑓𝑖𝑡𝑡/𝐴𝑑𝑗𝑢𝑠𝑡𝑒𝑑 𝐴𝑠𝑠𝑒𝑡𝑠𝑡

Δ Asset Turnover

This indicator measures the trend of how efficiently a company takes advantage of its assets. A

high Δ asset turnover earns a higher score. Asset turnover is calculated by:

𝐴𝑠𝑠𝑒𝑡 𝑇𝑢𝑟𝑛𝑜𝑣𝑒𝑟 = 𝑅𝑒𝑣𝑒𝑛𝑢𝑒𝑡/(𝐴𝑑𝑗𝑢𝑠𝑡𝑒𝑑 𝐴𝑠𝑠𝑒𝑡𝑠𝑡−1 + 𝐴𝑑𝑗𝑢𝑠𝑡𝑒𝑑 𝐴𝑠𝑠𝑒𝑡𝑠𝑡

2)

Δ Leverage

This indicator implies the trends company’s ability to payback long-term debt in future.

According to Piotroski, the increasing number of leverage show a negative signal because the

additional borrowing adds pressure to company’s financial flexibility. So we give the highest

score to the company with the lowest ΔLeverage ratio.

Small-Cap Portfolio: Healthcare & Consumer Staples

Page 14 of 57

Δ Accruals to Assets

This indicator measures the trend of company’s quality of total revenue. According to

Hirshleifer, Hou, Teoh, and Zhang’s paper “Do Investors Overvalue Firms with Bloated Balance

Sheets” (2004), increasing accruals can have negative effect on stock’s future price performance.

Stocks with higher Δ Accruals to Assets earn a lower score. Accruals to assets is calculated by:

𝐴𝑐𝑐𝑟𝑢𝑎𝑙𝑠 𝑡𝑜 𝐴𝑠𝑠𝑒𝑡𝑠= (𝐼𝑛𝑐𝑜𝑚𝑒 𝑏/𝑜 𝑋𝑂 𝑖𝑡𝑒𝑚𝑠𝑡

− 𝑂𝑝𝑒𝑟𝑎𝑡𝑖𝑛𝑔 𝑐𝑎𝑠ℎ 𝑓𝑙𝑜𝑤𝑡)/(𝐴𝑣𝑒𝑟𝑎𝑔𝑒 𝐴𝑑𝑗𝑢𝑠𝑡𝑒𝑑 𝐴𝑠𝑠𝑒𝑡𝑠𝑡,𝑡−1) )

Δ Liquidity

This indicator measures the trend of company’s ability to payback short-term debt, also known

as a firm’s current ratio. The higher a current ratio indicates the company has high ability to

meet short-term debt obligations and working capital obligations.

Δ Leverage

This indicator measures a company’s trend in its long term debt relative to its total assets. The

higher the Δ Leverage, the lower the score. Leverage is calculated as:

𝐿𝑒𝑣𝑒𝑟𝑎𝑔𝑒 = (𝐿𝑜𝑛𝑔 𝑇𝑒𝑟𝑚 𝐷𝑒𝑏𝑡)/(𝐴𝑑𝑗𝑢𝑠𝑡𝑒𝑑 𝐴𝑠𝑠𝑒𝑡𝑠)

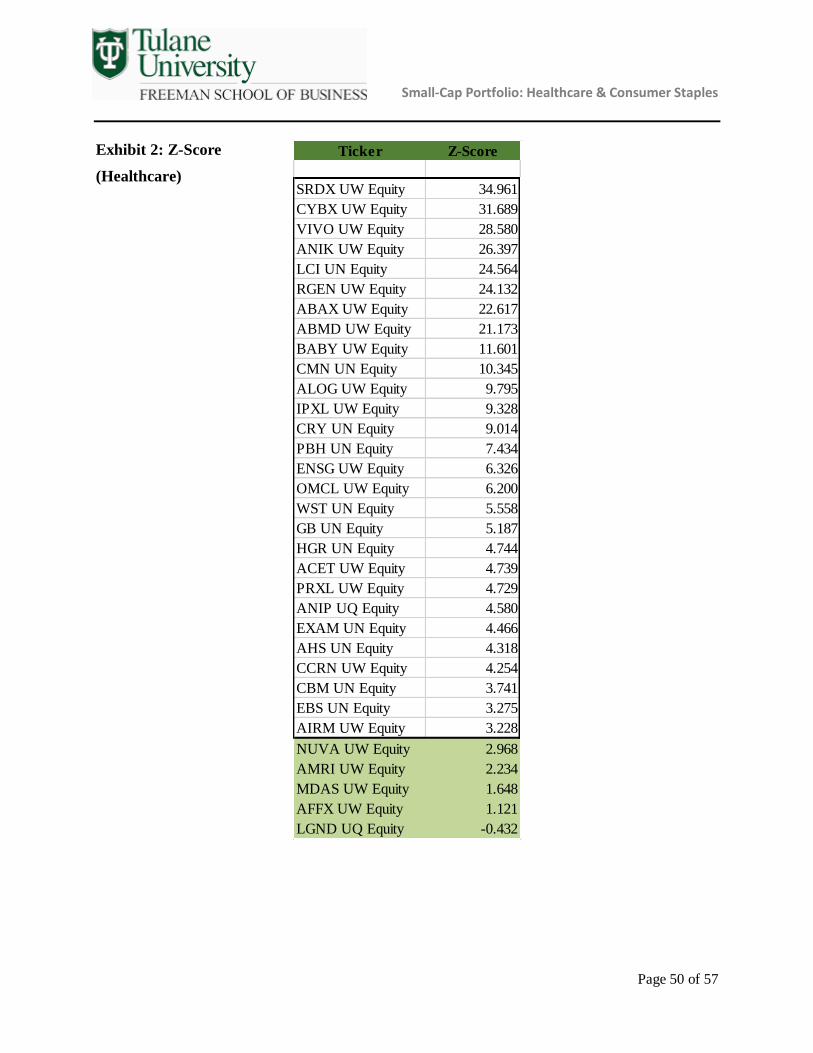

Risk Analysis: Step Z: Bankruptcy Risk

The small-capitalization companies tend to have high bankruptcy risk. Before moving to step 2

in the quantitative analysis, firms that have high probability of bankruptcy are eliminated using

Altman Z scores. Altman Z score is the criteria for risk because it reflects the financial condition

comprehensively in the following aspects: scale of capital, liquidity, profitability, financial

structure, debt payoff capacity, efficiency to use assets, etc. Firms with a Z score higher than

2.99 were eliminated, leaving healthy firms with low likelihood of bankruptcy to move to the

next quantitative step. Step Z results are shown in Exhibit 2 of the Appendix

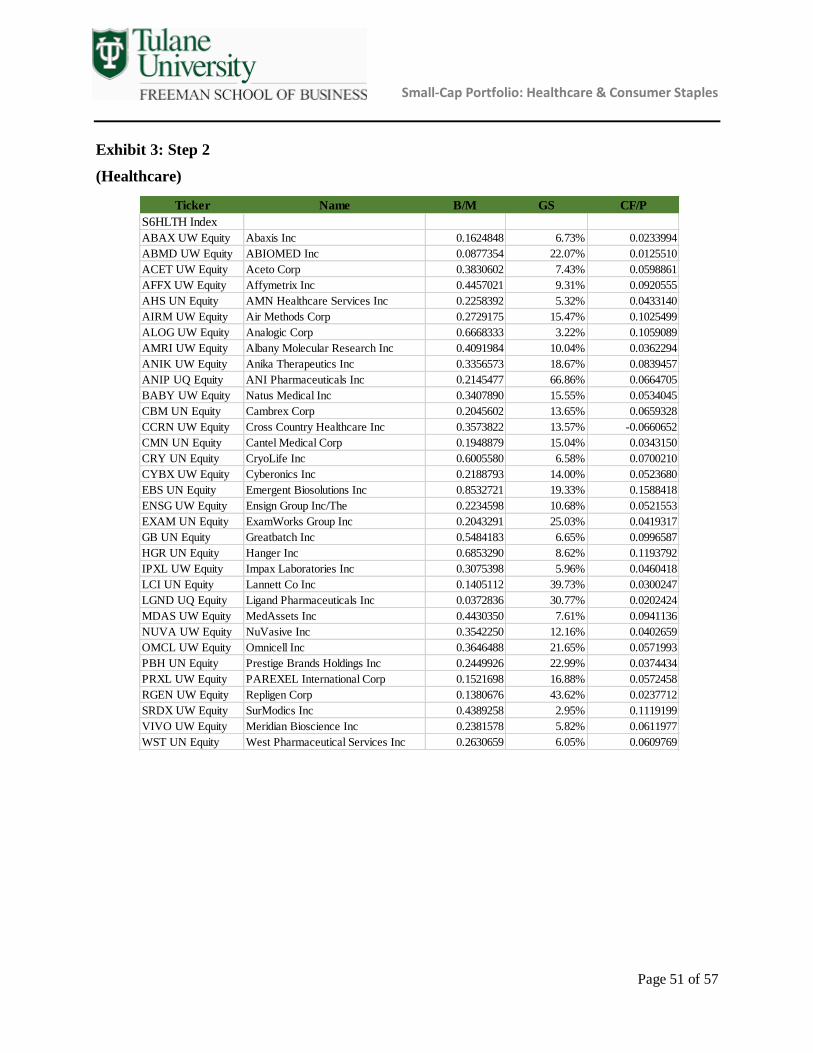

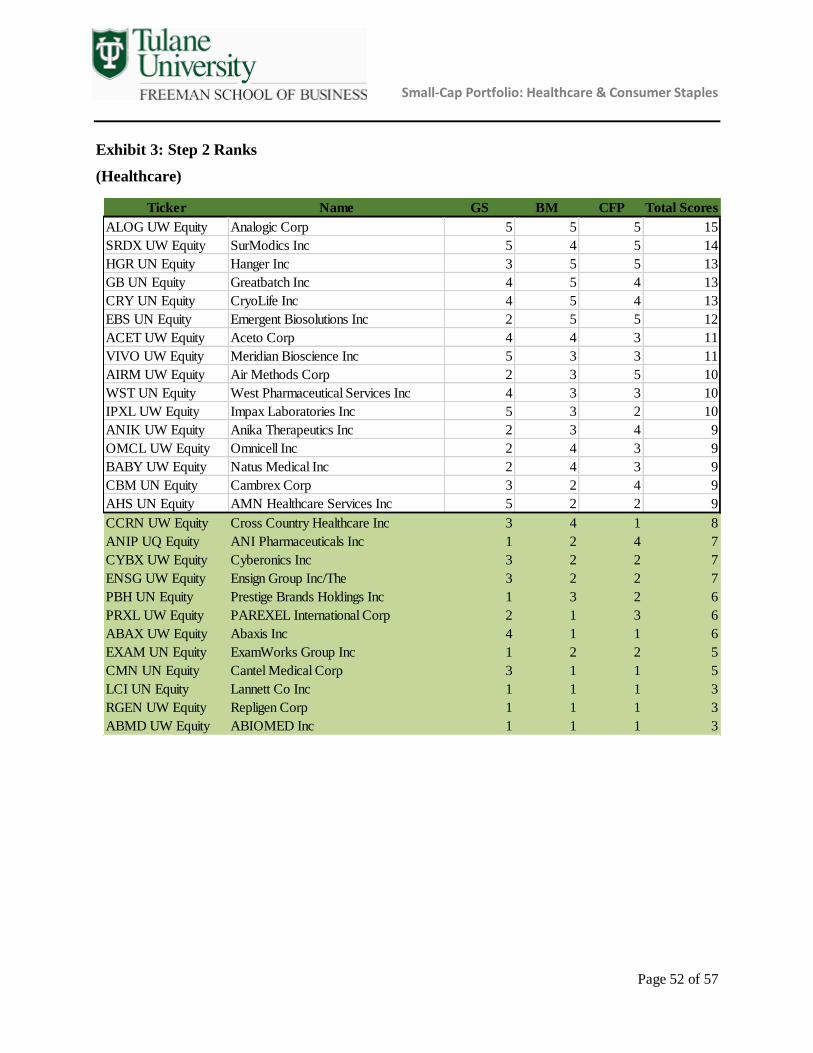

Step 2: Value or Growth

Step 2: Value or Growth uses variables related to a company’s value compared to its market

value to determine how relatively undervalued a firm’s stock price may be. In this step, three

current variables are used and weighted equally to determine the stock’s value. All stocks that

enter this step are sorted into quintiles for each variable, and receive a score based on which

quintile they fall into relative to other stocks. After receiving scores of 1 – 5, 5 ranking the best,

for each variable, they are then weighted equally and summed up to receive an aggregate score

for this step. Below are the variables used for Step 2: Value or Growth and the results for this

screen can be seen in Exhibit 3 of the Appendix.

Small-Cap Portfolio: Healthcare & Consumer Staples

Page 15 of 57

Book-to-Market (B/M) Ratio

This ratio compares the book value of the company to the market value of the company. In order

to find the relatively undervalued firms, stocks are sorted by B/M ratio from the highest to the

lowest. The most points are given to the companies which have high B/M ratios, because a high

B/M ratio means the company is undervalued by the market. The total equity amounts for each

firm are controlled for their R&D expenses.

Cash Flow-to-Price (CF/P) Ratio

According to Chan, Hamao, and Lakonishok, companies with high CF/P ratios statistically

generate higher returns than those with low CF/P ratios. In Health Care sector, we add R&D

expense in to the cash flow to get the CF/P ratio. After sorting the CF/P ratio from the highest to

the lowest, stocks with high CF/P ratios are ranked highest.

Growth in Sales (GS)

This indicator measures the percent change in sales year over year for four years. The changes

are then averaged to determine average sales growth over the past four years. Sorting GS ratio

from highest to lowest isolates the most undervalued firms which have good past sales

performance.

Step 3: Profitability

After the first two quantitative steps, all stocks that make it into Step 3: Profitability are screened

for levels of current profitability using variables measuring the most recent year’s financials.

Asness, Frazzini, and Pedersen (2014) find that firm’s with relatively stronger profitability ratios

have a greater ability to generate higher returns. Below are the variables used in Step 3:

Profitability and results for this screen can be seen in Exhbit 4 of the Appendix.

Return on Assets (ROA)

This indicator shows how efficiently a company use its assets to generate earnings. The higher

ROA a company has, the more profitable a company is. The highest scores go to the companies

which have the highest ROA.

*the equation for ROA can be seen under the ΔROA description

Gross Profits Over Assets (GPOA)

GPOA is a profitability measure. The higher the GPOA, the higher a firm will be scored.

*the equation for GPOA can be seen under the ΔGPOA description

Small-Cap Portfolio: Healthcare & Consumer Staples

Page 16 of 57

Gross Margin

By using this ratio, a stock’s profitably is measured by sales after subtracting COGS. The higher

the ratio is, the higher a company is ranked.

Cash Flow Over Assets (CFOA)

This ratio is used to find how efficient a company uses its assets to generate cash flows. The

higher the variable, the more points the firm scores. This variable is calculated as:

𝐶𝐹𝑂𝐴 = 𝑁𝐼𝑡 + 𝐷𝑒𝑝𝑟&𝐴𝑚𝑜𝑟𝑡 − (𝑊𝑜𝑟𝑘𝑖𝑛𝑔 𝐶𝑎𝑝𝑖𝑡𝑎𝑙𝑡 − 𝑊𝑜𝑟𝑘𝑖𝑛𝑔 𝐶𝑎𝑝𝑖𝑡𝑎𝑙𝑡−1) − 𝐶𝐴𝑃𝐸𝑋𝑡

Accruals to Assets

This variable measures the quality of a firm’s revenue. The lower the ratio is relative to other

firms, the higher the stock is ranked.

*the equation for Assets to Accruals can be seen under the ΔAssets to Accruals description

The qualitative screening process delves into firm-specific details that measure several factors

considered either too subjective or difficult to quantify, or not powerful enough to remove stocks

prior to looking at them further. The qualitative screening process assesses all variables

collectively to determine each firm’s ability to generate high abnormal stock returns in the

future. Each variable is collected through numerical data and data supplied in each firm’s annual

reports as well as competing companies financial filings. Below is a table of firm specific

variables used in the qualitative screen.

Qualitative Screens & Analysis

Small-Cap Portfolio: Healthcare & Consumer Staples

Page 17 of 57

Category Variables

Macroeconomic Drivers

Regulations

Population

Technology Driver

Firm Operations

Products/ Patents Development or Moats

R&D Efficiency

Acquisition & Spin-off Quality

Corporate Governance &

Management

Stock Repurchases

Insider Trading

Management Stability

Financial Quality

Profitability Improvement

Earnings Surprise Performance

Downside Beta

Macroeconomic Drivers

Macroeconomic drivers are considered external variables impossible for firms to control, such as

demographics, regulations, available and/or competing technologies. If a firm is exposed to a

macroeconomic risk, it will be mentioned under this variable.

Firm Operations

R&D Efficiency

R&D Efficiency is measured by:

𝑅&𝐷 𝐸𝑓𝑓𝑖𝑐𝑖𝑒𝑛𝑐𝑦 = (𝑅&𝐷 𝐸𝑥𝑝𝑒𝑛𝑠𝑒)/(𝑀𝑎𝑟𝑘𝑒𝑡 𝑉𝑎𝑙𝑢𝑒 𝑜𝑓 𝐸𝑞𝑢𝑖𝑡𝑦)

According to Chan, Lakonishok and Sougiannis, stocks with high levels of R&D efficiency

generate higher abnormal returns. The firms R&D efficiency ratios are calculated and compared

to each other in this screen step.

Products/Patents Development or Moats

Many small-cap healthcare companies rely on certain niche products and patents developed in

R&D departments to keep the company alive and financially healthy/protected. This analysis

discusses which products these companies plan to produce, acquire, or continue to develop in the

future and how they affect the company’s financials.

Small-Cap Portfolio: Healthcare & Consumer Staples

Page 18 of 57

Acquisition and Spin-off Quality

Acquisitions play a large part in many companies’ growth strategies. This variable assesses each

company’s ability to generate revenue through acquisitions in both the past and the future

depending on the historical data and future plans of each firm.

Corporate Governance and Management

Stock Repurchases

This indicator represents a firm’s plans to repurchase stock from the public. Usually, a stock

repurchase is a positive signal because it shows the company’s confidence in its financial

condition and undervalued stock price. Here, any stock repurchases over the last two years are

reported in the variable.

Insider Trading

This information shows how many stocks the company executives bought and sold in the past 3

or 12 months. If the number of shares bought exceeds the number of shares sold, it shows a good

signal that the company is in good financial condition and the executives are confident about the

price of their own firm’s shares.

Management Stability

Management stability is measured using several factors including whether or not the founder has

recently left the company or if management has been restructured in a way that may benefit or

hurt the condition of the company. Any issues related to the strength of management or any

signals of a change in management can be found here.

Financial Quality

Profitability Improvement

Many of the quantitative factors used in the initial screening process may have been inflated or

deserve further investigation. This section reports any interesting findings regarding a

company’s improving financial condition upon further investigation of financial data.

Earnings Surprise Performance

This indicator shows how many times in the past 2 years the company earnings actually

exceeded consensus analyst estimates. The more times the company beats its earnings estimates,

the better signal it shows. Another variable used in this analysis is the earnings surprise ratio.

Doyle, Lindholm and Soliman (2006) explain that stocks with high earnings surprise ratios

statistically achieve higher future abnormal returns. The earnings surprise ratio is calculated as:

Small-Cap Portfolio: Healthcare & Consumer Staples

Page 19 of 57

𝐸𝑆 𝑅𝑎𝑡𝑖𝑜 = (𝐴𝑐𝑡𝑢𝑎𝑙 𝐸𝑃𝑆 − 𝐴𝑛𝑎𝑙𝑦𝑠𝑡 𝐶𝑜𝑛𝑠𝑒𝑛𝑠𝑢𝑠 𝐸𝑃𝑆)/(𝐴𝑐𝑡𝑢𝑎𝑙 𝑆𝑡𝑜𝑐𝑘 𝑃𝑟𝑖𝑐𝑒)

Downside Beta

The downside beta shows the systematic risk a company is exposed to during market downturns.

A downside beta lower than one shows the systematic risk of the company is lower than the

market. A downside beta higher than one shows there is a higher risk behind the company than

the risk of the market. While this variable is useful for consideration, the investment theory

behind this process does not support the theory that historical betas affect future systematic risk.

Firm-Specific Qualitative Analysis Tables

Table 3: Post-Screening Firm Overview

Ticker Name STEP 1 STEP 2 STEP 3

BABY Natus Medical 6th/70 14th/28 4th/16

VIVO Meridian Biosciences 11th/70 8th/28 2nd/16

SRDX SurModics 4th/70 2nd/28 1st/16

EBS Emergent Biosolutions 29th/70 6th/28 5th/16

CBM Cambrex Corp 7th/70 15th/28 12th/16

AFAM Almost Family 66th/70 N/A N/A

PMC PharMerica Corp 47th/70 N/A N/A

Small-Cap Portfolio: Healthcare & Consumer Staples

Page 20 of 57

Natus Medical Inc. (BABY)

Natus Medical Inc. (NYSE: BABY)

Natus Medical (BABY) has recently acquired and created several new products, captured a large

contract, and is on track to have double the exposure it had by year end 2014. This neurology and

newborn centered healthcare firm has a strong acquisition quality,

Firm

Operations

The firm’s growth strategy revolves around acquisitions, using newly acquired products in there research and development to create new patents and products.

BABY is on pace to be exposed in nearly double the amount of hospitals it was at

year end 2014, from being in 58 hospitals to aiming for 100 by year end 2015.

In April of 2015, Natus Medical was cleared to manufacture and sell the first 256-channel quantum amplifier used to measure brain activity related to epiliepsy and

sleep disorders. This new technology sensitive tool for measuring can be used in

many other products and services offered by BABY.

The R&D efficiency rate of BABY in 2014 was 2.46%, lower than the sector average

which is 3.32%.

BABY recently acquired two companies, GND and NicView, to expand its product

portfolio. GND supplies convenient EEG testing for brain activity and NicView offers hospitals a 24-hour monitoring system for newborns.

Corporate

Governance &

Management

Insider holdings over the past 12 months have shown that executives have sold shares

at a high rate

On June 9, 2014, BABY entered into a share repurchase program.

Financial

Quality

The firm has beat consensus estimate earnings in all past 8 quarters.

Downside beta is -0.65, much lower than the sector downside beta 0.61.

Recently awarded a 5-year, $32.5 million contract in the state of California.

Meridian Biosciences Inc. (VIVO)

Meridian Bioscience Inc. (NYSE: VIVO)

Meridian Bioscience mainly provides quick, cheap, and simple diagnostic test kits for niche markets and

diseases. The company is able to defend itself from market downturns with its leverage ratio at 0% and pays exceptional dividends to shareholders. While its major patented product will be unprotected soon,

VIVO will be releasing new testing kits for much more common diseases that can be used at home or

more efficiently in a physician’s office than other tests.

Firm Operations

VIVO has zero debt and utilizes an aggressive R&D expenditure strategy to outgrow its competition.

Meridian Bioscience is one of small-cap healthcare companies that pays dividends,

and has paid dividend for the past 21 years without decreasing its dividend amount.

The company maintains a large market share in specific medical areas and uses this strategy to offer leading products in niche markets..

VIVO develops a line of illumigene products: a patented technology used to test

more common diseases. In the next couple years, the company will be releasing its illumigene STD testing kits into the market, a test that may be widely used as STD

are amongst the most commonly feared and easily contractible diseases

Small-Cap Portfolio: Healthcare & Consumer Staples

Page 21 of 57

Its H. pylori testing kit will be losing its patent in 2016 and 2017, leaving its second

most revenue-generating technology unprotected

The R&D efficiency rate of VIVO in 2014 was 1.54%, lower than the sector average of 3.32%.

Increasing competition has kept market share at a flat rate year over year.

Corporate

Governance & Management

Insider holdings over the past 12 months have shown that executives bought more

shares than sold.

Financial Quality

The firm has missed consensus estimate earnings in 5 of 8 past quarters.

Downside beta is 1.53, higher than the sector downside beta of 0.61.

SurModics Inc. (SRDX)

SurModics Inc. (NYSE: SRDX)

SurModics is a medical device coating and in vitro diagnostic test producing company with strong R&D

efficiency, plans to offer ground-breaking products, and confidence amongst management that the stock

is undervalued.

Firm Operations

SurModics business strategy focuses highly on R&D and generating new patents

consistently to keep up with competition. They are able to do so by licensing out

most of its products/patents in order to generate passive revenue while focusing on

innovation.

SRDX recently sold all of its assets in an inefficient pharmaceutical subsidiary.

SRDX will continue its research and development project on a new drug coated

balloon product, SurVeil, which will enter human trails in November of 2015. Drug coated balloons have gained a wide acceptance in the medical community recently,

and only two competitors exist. They are useful for breaking down blockage and

clots in arteries and have a wide range of demand among other uses.

While SurModics will be losing one of its prominent medical device coating patents, PhotoLink, it has developed an improved coating, Serene, that the firm is attempting

to convert existing customers to use.

The R&D efficiency rate of SRDX in 2014 was 4.63%, higher than the sector average of 3.32%.

SRDX is increasing R&D expenditures by 5-7% in 2015 for its new SurVeil product.

Corporate

Governance & Management

Insider holdings over the past 12 months have shown that executives have bought more

shares than sold

On November 11, 2014, SRDX entered into an accelerated share repurchase program.

Financial Quality

The firm has beat consensus estimate earnings in 7 of 8 past quarters.

Downside beta is 1.34, much higher than the sector downside beta 0.61.

Small-Cap Portfolio: Healthcare & Consumer Staples

Page 22 of 57

Anika Therapeutics Inc. (ANIK)

Anika Therapeutics Inc. (NYSE: ANIK)

Anika Therapeutics embraces its long lived patented technology to supply its massive product line. The

company has proved to be very effective in creating value without straying from its core business.

Recently, they have significantly cut margins and captured major customers that produce well over the

majority of their revenue.

Firm Operating

ANIK creates a large line of products using its Hyaloric Acid (HA) based technology.

Two years ago, the company consolidated plant production from dual facilities into

one facility and reduced production in Italy, cutting costs and increasing gross margins dramatically.

ANIK has developed two significant revenue generating products within the last 12

months, MonoVisc and OrthoVisc, and plans to increase R&D spending by 15% in

the near future.

The R&D efficiency rate of ANIK in 2014 was 1.38%, lower than the sector average

of 3.32%.

Competition has increased dramatically, but Anika Therapeutics generates 72% of its

revenue from a Johnson & Johnson subsidiary. This has kept there revenue generating ability protected but also increases its risk in the ability to generate similar

revenue without the single client.

Corporate

Governance & Management

Insider holdings over the past 12 months have shown that executives have sold a

significantly more shares than they have bought.

Financial

Quality

The firm is covered by one analyst and has no data regarding earnings estimates.

Downside beta is 2.17, much higher than the sector downside beta of 0.61.

Emergent Biosolutions Inc. (EBS)

Emergent Biosolutions Inc. (NYSE: EBS)

Emergent Biosolutions Inc. performs well in the qualitative analysis with new patent licensed, high

probability to augment BioThrax manufacturing capacity, high R&D efficiency, good acquisition

quality, lower-than-average downside beta, and stable increases in revenue and net income. Though the leverage is increasing, we are still positive on the company.

Firm Operating

BioThrax contributes more 80% to EBS’ revenue. Building 55 will triple the

BioThrax manufacturing capacity. Biomedical Advanced Research and

Development Authority (BARDA) is funding the project. FDA’s might approve an sBLA in late 2015 or early 2016.

On April 22, EBS concluded its investigation in the particles sources of two

BioThrax production lots.

FDA approved Anthrasil™ (seven-year market exclusivity) on March 25, EBS now

enjoys five only-one patents licensed by FDA in its Biodefense division. BARDA

offers EBS $7 million for the achievement.

The R&D efficiency rate of EBS in 2014 is 13.45%, three times higher than sector average which is 3.32%.

Small-Cap Portfolio: Healthcare & Consumer Staples

Page 23 of 57

The acquisition of Cangene in February 2014 provides seven revenue-generating

products.

Corporate Governance &

Management

In the last three months, shares bought by insiders are more than three times the shares

sold.

Financial

Quality

In 2014, total revenue increased 43.9%, net income increased 18.0%, EPS increased

3.5%.

Total liabilities to total assets increased 86.4%, current ratio decreased 3.5%.

The firm has beat consensus estimate earnings in all past 8 quarters.

Downside beta is -0.65, much lower than the sector downside beta 0.61.

Cambrex Corp. (CBM)

Cambrex Corp. (NYSE: CBM)

Cambrex focuses on the manufacture of small molecule APIs and the current market trend benefits the business. The company performs well in its future product development, profitability, and downside

risk preservation. However, the depreciation of euros and competitions from low-cost suppliers would

be threats to Cambrex.

Macro Environment

The small molecule accounts for more than 80% of pharmaceutical spending. As the second largest US-based contract manufacturing organizations (CMO) and focuses

on manufacturing small molecule Active Pharmaceutical Ingredients (API), CBM

benefits from increasing categories of small molecule drugs, and increasing percentage of population taking drugs.

However, the European market accounts for more than 60% of CBM’s revenues in

2013 and 2014. CBM is not hedging to protect the foreign operations. The

depreciation of euros dramatically damaged the company’s profitability.

Firm Operations

In February 2015, Cambrex announced to expand its Iowa facility to support

increasing trends within the API market.

Cambrex expects to launch two new products which would generate roughly $10 million of annual revenue at peak sales.

The R&D efficiency in 2014 is only 0.92%, lower than 3.32%, the sector average.

Acquisition of Zenana in May 2014 provides additional producing capability.

The low-cost suppliers in developing markets are future competitors.

Gilead Sciences, Inc. accounted for more than 20% of Cambrex’s revenue, which is risky if the agreement was broken up.

Corporate

Governance & Management

Cambrex’s insiders kept selling stocks in the past 12 months.

The company missed estimated earnings 3 times out the last 8 quarters

Financial

Quality

The financial performance indicates a steady profitability and safety with liability.

Compared to FY2013, in FY2014, revenue increased 17.7%, gross margin

maintained, net income increased 37.1%, adjusted EPS increased 35.3%.

Total liabilities to total assets decreased 11.1%, current ratio went up 10.6%.

Small-Cap Portfolio: Healthcare & Consumer Staples

Page 24 of 57

Cambrex has a downside beta of -0.31, indicating that the firm generates abnormal

returns under bad market conditions.

Almost Family Inc. (AFAM)

Almost Family Inc. (NASDAQ: AFAM)

Though Almost Family Inc. is in a good market condition and it did well in 2014, the company’s business strategies cannot sustain its future growth and advantages for competition.

Macro

Environment

The increase of healthcare expenditures and the increase of aging population will

benefit healthcare services industry.

Firm Operating

The firm did three acquisitions in 2013 and one acquisition in 2014, and signed one acquisition contract in 2015. However, the firm’s operating efficiency did not

increase with the acquisitions. Besides, AFAM extends its business mainly by

referrals which are not sustainable. The competition of the industry is fierce.

Corporate Governance &

Management

Insiders kept buying AFAM in the past 12 months.

AFAM beats estimated earnings 6 times in the last 8 quarters.

Financial

Results

Compared to FY 2013, in FY 2014, net income increased 67.3%. Total liabilities to total assets went down 7.9%. However, gross margin maintained the same level.

PharMerica Corp. (PMC)

PharMerica Corp (NYSE: PMC)

PharMerica Corp benefits from its market position, acquisition strategies, and increasing healthcare

expenditures. However, the company becomes unfavorable because (1) it lost two major customers; (2) its genetic dispensing rate is increasing; (3) its failure to control cost; (4) its illegal issues in the past

years; and (5) bad profitability performance in FY 2014.

Macro

Environment

The increase in aging population and lifestyle changing results in the increase of

healthcare expenditure. The US government’s Center for Medicare and Medicaid Services (CMS) stated that healthcare expenditure in the country rose recently

6.8%. The increase in healthcare expenditures boosts the development of

pharmaceutical service companies.

Firm Operating

PharMerica Corp is the second largest institutional pharmacy service company in the US. The four acquisitions in 2014 enhances the company’s service offerings.

However, PMC lost two major customers last year, dramatically reduces its revenue

sources. The company’s generic drug dispensing rate kept increasing in the last three years, adversely affecting its profitability. Failure to control cost resulted in

increasing revenue but decreasing operating income. The illegal issues generated

extraordinary expenses. Besides, PMC failed to call back the receivables, its asset

turnover ratio kept decreasing in the past three years.

The President and CEO of PMC’s subsidiary will resign on July 3, 2015.

Small-Cap Portfolio: Healthcare & Consumer Staples

Page 25 of 57

Corporate

Governance &

Management

Insiders kept selling PMC in the last 12 months.

Financial

Results

PharMerica has a downside beta of 0.81, higher than the sector average.

Compared to FY 2013, in FY 2014, net profit decreased 64.0%, EPS decreased

65.1%. Total liabilities to total assets increased 12.2%, EBIT to total assets

decreased 60.5%.

Natus Medical Inc. (NASDAQ: BABY)- STRONG BUY

We strongly recommend a BUY rating for Natus Medical (BABY) for several reasons. First,

BABY performed exceptionally well in both profitability and fundamental growth screens.

While it is not the most relatively cheap stock amongst our step 2 stocks, we believe it to still be

and undervalued firm. Natus Medical has a strong acquisition history and recently acquired two

products that they plan to gain exposure in their existing hospitals that could make these products

mainstream. Additionally, they have developed a new one-of-a-kind technology that has

hundreds of uses. Natus Medical is not content at where they are, as they are aggressively trying

to gain more exposure in hospitals across the country, yet many of these updates are new and

may not be realized in the stock’s price yet. We see a lot of promise in BABY’s future stock

performance based on both quantitative and qualitative evidence and agree that this is the

healthcare sector best buy at the time.

Meridian Bioscience, Inc. (NASDAQ: VIVO)- BUY

We recommend a BUY rating for Meridian Bioscience. VIVO is a company with strong market share in

specific areas and is ready to release another testing kit for one of the most commonly feared diseas,

STDs. The company is essentially riskless as it holds zero debt and yet it still pays healthy dividends, a

quality not normally seen in healthcare small-cap stocks. VIVO is one of the most profitable companies

that passed all three quantitative screening tests. Although they have been facing increasing competition,

they have retained most market share and will certainly gain more through the sales of their illumigene

STD tests. Meridian Bioscience’s mission is one that follows a common trend in U.S. demand, quick,

easy, and cheap products. VIVO’s performance and future plans confirm our buy rating.

Investment Idea Summary

Small-Cap Portfolio: Healthcare & Consumer Staples

Page 26 of 57

SurModics, Inc. (NASDAQ: SRDX)- BUY

We recommend the Darwin Fenner Fund BUY SRDX stock for several reasons. To start, SRDX

passed all of our quantitative screens in flying colors, landing in the top 5 of every step and

ranking 2nd in our value screen and 1st in our profitability screen. SRDX is extremely close to

clearing their developing product, a drug coated balloon, which has already gain recent wide

acceptance in the medical field and has several types of uses. SRDX’s only issue to overcoe will

be transferring its current customers over to its new patent protected Serene products once their

PhotoLink patent expires soon. The stock has consistently beaten analyst estimates and SRDX is

currently in a share repurchase program, showing strong financial performance and even stronger

confidence within the company that reaffirms our buy rating.

Anika Therapeutics Inc. (NYSE: ANIK)- DELETE

Anike Therapeutics was DELETED during our firm specific qualitative screens. We realized

that the firm’s financial performance and strong quantitative screen results were due to a one

time consolidation of manufacturing resources and contract signing with a Johnson & Johnson

subsidiary. We are very put off by the fact that 72% of its revenue is in the hands of one

customer and we believe this stock is much too risky and overvalued to be considered for the

Darwin Fenner Fund.

Emergent Biosolutions Inc. (NYSE: EBS)- HOLD

We recommend to HOLD Emergent Biosolutions Inc. because it did well in our quantitative

screen and has favorable qualitative performance. EBS ranks 29th in step 1 screening, a middle

performer in fundamental growth trend. The company ranks 6th in step 2, indicating that EBS is

more undervalued than other companies in the sector. EBS got the 5th place in step 3, showing a

top current profitability. We confirm our hold recommendation because of the newly-licensed

patent, high probability to augment BioThrax manufacturing capacity, high R&D efficiency,

good acquisition quality, lower-than-average downside beta, and stable increases in revenue and

net income. After considering all the factors, we recommend to hold EBS.

Cambrex Corp. (NYSE: CBM)- HOLD

We recommend to HOLD Cambrex Corp. based on our quantitative and qualitative analysis.

CBM ranks the 7th in step 1, indicating that the firm has a strong trend of fundamental growth.

CBM ranks in the middle in step 2, showing that the firm is relatively a value firm. CBM does

not rank in the top in step 3, but the increase in net income and decrease in leverage in FY 2014

indicate a steady profitability and financial safety. The market concentration on small molecule

API benefits the firm’s business. However, CBM should be aware of the foreign currency

environment and low-cost competitors. After considering about all the factors, we recommend to

hold CBM.

Small-Cap Portfolio: Healthcare & Consumer Staples

Page 27 of 57

Almost Family Inc. (NASDAQ: AFAM)- Strong Sell

We recommend to STRONG SELL Almost Family Inc. based on our quantitative and

qualitative analysis. AFAM was deleted from step 1 with a ranking of 66th, indicating that the

company has a poor fundamental growth trend. Though Almost Family Inc. is in a good market

condition and it did well in 2014, the company’s business strategies cannot sustain its future

growth and advantages in a fierce competitive environment. After considering about all the

factors, we recommend to sell AFAM.

PharMerica Corp (NYSE: PMC)- Sell

We recommend to SELL PharMerica Corp based on our quantitative and qualitative analysis.

PMC ranks 47th in step 1 and failed to move into the next step. PharMrica Corp benefits from its

market position, acquisition strategies, and increasing healthcare expenditures. However, the

company lost two major customers in 2014, failed to control cost in the most recent years, and

bad profitability in 2014 confirmed our strong sell recommendation.

Small-Cap Portfolio: Healthcare & Consumer Staples

Page 28 of 57

Consumer

Staples

Small-Cap Portfolio: Healthcare & Consumer Staples

Page 29 of 57

TICKER NAME SUB-SECTOR

DAR Darling Ingredients Agricultural Products

ANDE Andersons/The Food Distributors

SPTN SpartanNash Co Food Distributors

CASY Casey's General Stores Food Retail

WDFC WD-40 Co Household Products

CENTA Central Garden & Pet Co Household Products

CALM Cal-Maine Foods Packaged Foods & Meats

JJSF J&J Snack Foods Packaged Foods & Meats

CVGW Calavo Growers Packaged Foods & Meats

BGS B&G Foods Packaged Foods & Meats

SAFM Sanderson Farms Packaged Foods & Meats

SENEA Seneca Foods Packaged Foods & Meats

DMND Diamond Foods Packaged Foods & Meats

LNCE Snyder's-Lance Packaged Foods & Meats

MED Medifast Personal Products

IPAR Inter Parfums Personal Products

UVV Universal/VA Tobacco

Stock List

Consumer Staples (17 Stocks)

Small-Cap Portfolio: Healthcare & Consumer Staples

Page 30 of 57

Table 4 illustrates all Buy, Hold, and Sell recommendations for the S&P 600 Consumer Staples

stocks covered in the quantitative and qualitative screens and analyses described in this report.

Table 4: Consumer Staples Sector Recommendations

Ticker Name Sub-industry Recommendation

BGS B&G Foods Inc Packaged Foods & Meats BUY

SPTN SpartanNash Co Food Distributors HOLD

MED Medifast Inc Personal Products STRONG SELL

Sector Performance Snapshot (as of February 22, 2015)

Previous 36 Month Data S&P 600 Consumer Staples

Alpha - 0.45%

CAPM Beta 1 0.81

Downside CAPM Beta 1 0.69

CAR - 8.13%

BAH Return 51.63% 64.33%

Abnormal BAH Return - 12.71%

Cumulative Wealth 1.516 1.643

Sharpe Ratio 0.34 0.40

B-M Ratio 0.449 0.442

CF-P Ratio 0.071 0.074

E-P Ratio 0.034 0.049

Avg. Sales Growth (past 5 years) 27.93% 11.63%

Recommendations

Consumer Staples Sector Analysis

Small-Cap Portfolio: Healthcare & Consumer Staples

Page 31 of 57

Sector Overview

The Consumer Staples sector of the S&P 600 consists of 17 stocks and, as of February 22, 2015,

makes up 3.09% of the S&P 600 market capitalization. All data in this sector analysis section is

recorded as of February 22, 2015. Consumer Staples generally refers to firms that produce

necessities and products under constant demand. Sub-industries in this sector are shown in

Figure 6.

Figure 6: Consumer Staples Sub-Industry Weights

Performance and Risk

The consumer staples sector outperforms the S&P 600 over the past 36 months. As shown in

Figure 7, the cumulative wealth of consumer staples has consistently larger than the S&P 600.

The cumulative market adjusted abnormal return is 8.13%. The BAH return is 64.33%, higher

than that of the S&P 600, 51.63% (refer to Figure 8).

Food & Beverages

56.40%

Tobacco5.22%

Household Products

7.25%

Personal Products

4%

Food Retailers16.63%

Food Distributors

10.50%

Small-Cap Portfolio: Healthcare & Consumer Staples

Page 32 of 57

Figure 7: Cumulative Wealth over the Past 36 Months (Consumer Staples vs S&P 600)

Figure 8: Buy and Hold Return over the Past 36 Months (Consumer Staples vs S&P 600)

Regarding risk, the consumer staples sector has a CAPM beta of 0.81, showing that the sector

has a lower systematic risk than the S&P 600. Consumer staples are products that the general

population are in need of constantly, no matter where a person’s financial condition. People

cannot or are unwilling to live without consumer staples. Thus, stocks of the consumer staples

sector are non-cyclical, tending to have lower systematic risks.

Figure 9: Systematic Risk of Consumer Staples

0.8

1

1.2

1.4

1.6

1.8

S&P 600 Consumer Staples

64.33%

51.63%

Buy and Hold Return

Consumer Staples SP600

1

0.81

S&P 600 CONS

Small-Cap Portfolio: Healthcare & Consumer Staples

Page 33 of 57

Additionally, the sector has a downside beta of 0.69 over the past 36 months, higher than that of

the S&P 600. The downside beta shows that the volatility of consumer staples stocks in market

downturns was lower than the volatility of the S&P 600 during the same period, returning a

lower loss than the market on average. As mentioned before, consumer staples stocks are

defensive in relation to the performance of the economy. Even if the market goes down, the

stocks are able to keep outperforming the market.

Figure 10: Upside and Downside Betas for Consumer Staples

Growth/Value Sector Classification

Using the S&P 600 as the benchmark, we first calculated the weighted average B/M ratio of the

S&P 600 and consumer staples sector. Results shown in Table 2 indicate that, compared to the

benchmark, the consumer staples sector is classified as a growth sector. However, the consumer

staples sector retain certain previously mentioned attributes, such as stability and necessity,

which reflect the constant demand of broad consumers. Furthermore, Consumer Staples has a

similar B/M ratio compared to S&P 600. After further analyzing the CF/P ratio and E/P ratio

(weighted average) for the S&P 600 and consumer staples sector, the sector maintains different

characteristics of growth/value throughout its separate ratios. Results are shown in Table 2.

1

1

.69

0.92

S&P 600 CONS

Small-Cap Portfolio: Healthcare & Consumer Staples

Page 34 of 57

Table 5: B/M, CF/P, and E/P ratio for S&P 600 and Consumer Staples

S&P 600 Consumer Staples G/V

B/M Ratio 0.449 0.442 G

CF/P Ratio 0.071 0.074 V

E/P Ratio 0.034 0.049 V

*Data source: Bloomberg, 02/22/2015

CF/P ratio and E/P ratio have a good consistency in Consumer Staples sector. And, as mentioned

before, investor sentiment of this sector has historically been conservative. While poor industry

performance may lead to weak CF/P and E/P ratios, active investors tend to believe this sector

has a high floor of performance which can lead to growth-style B?M ratios. Therefore, the

consumer staples sector is classified as a value sector.

Overweight and Underweight Decision

Taking into account past systematic risk and historical characteristics of the consumer staples

sector, the DFF portfolio should market-weight this sector of the S&P 600.

Currently, there are two consumer staples stocks in the fund, Medifast Inc. and Spartan Stores

Inc., which weigh at 7.25% of the DFF portfolio. Comparatively, the consumer staples sector

holds a market capitalization of 3.09% of the S&P 600.

Underweighting this sector would not be reasonable because the economy and consumer staples

market drivers are continuing to improve this year. Additionally, demand for consumer staples

products is elastic and people don’t purchase a significant amount more as disposable income

increases. Since the stock is generally conservative and the B/M ratio has remained lower than

that of the S&P 600 during market downturns, the DFF portfolio should market-weight the

consumer staples sector.

Small-Cap Portfolio: Healthcare & Consumer Staples

Page 35 of 57

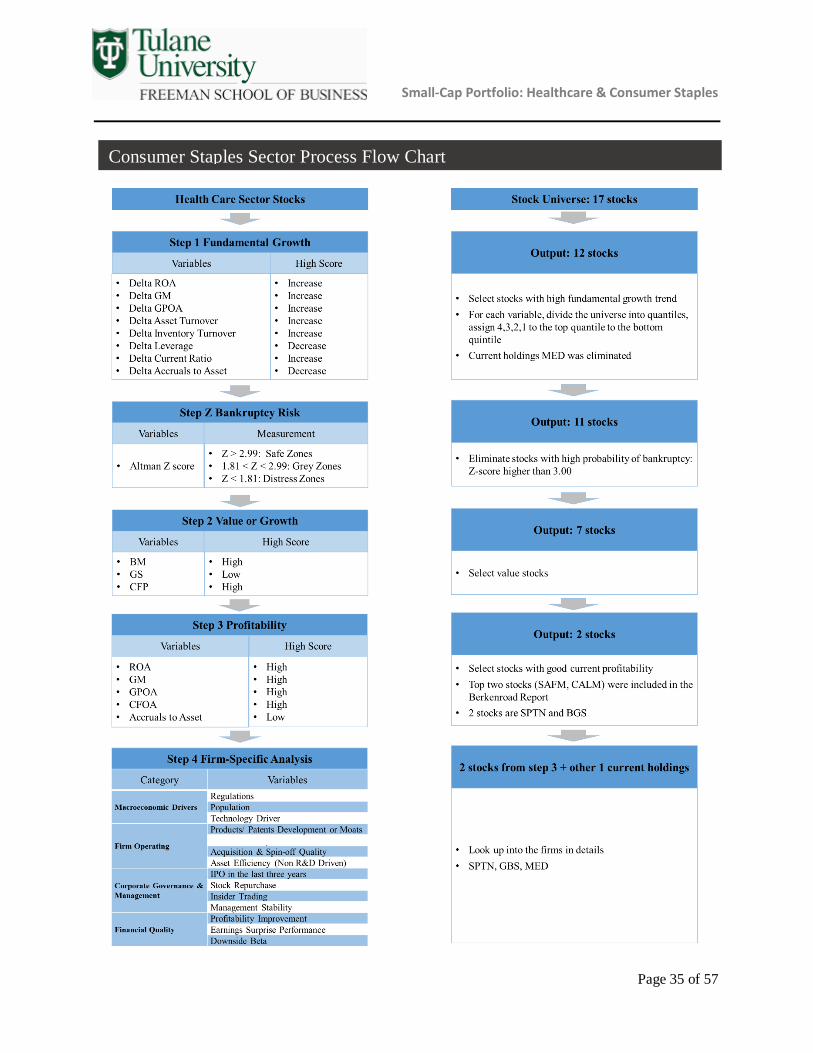

Consumer Staples Sector Process Flow Chart

Small-Cap Portfolio: Healthcare & Consumer Staples

Page 36 of 57

The quantitative screens are based on a theory of isolating firms that are increasingly financially

healthy, undervalued, and currently profitable. To begin, the stocks enter the firm fundamental

growth stage and, based on variables that measure the change in a firm’s financial ability, all

stocks are ranked into quartiles. Each stock receives a score of 1 – 4 for each variable based on

how well the stock ranked relative to other consumer staples sector stocks. After receiving

scores for each variables, they are then weighted equally and summed up to receive an aggregate

score for each step. Below are the variables and methods used in Step 1: Fundamental Growth:

Step 1: Fundamental Growth

The following growth variables are used to measure the trend in a company’s profitability,

financial health, and fundamental growth. Therefore, all variables are calculated by determining

the ratio for each of the past four years, calculating the change in each variable year over year,

and averaging the change over the last four years. Asness, Frazzini, and Pedersen (2014) and

Piotroski and So (2012) find that firm’s performing strongly under these variables statistically

generate higher abnormal returns. Step 1 results can be seen in Exhibit 5 of the Appendix.

Δ Return on Assets (ROA)

The change in ROA indicator measures the trend of management’s effectiveness in its ability to

generate revenue relative to the firm’s total assets during past years. ROA is calculated by:

𝑅𝑂𝐴 = 𝐴𝑑𝑗𝑢𝑠𝑡𝑒𝑑 𝑁𝑒𝑡 𝐼𝑛𝑐𝑜𝑚𝑒𝑡/(𝐴𝑠𝑠𝑒𝑡𝑠𝑡−1 + 𝐴𝑠𝑠𝑒𝑡𝑠𝑡

2)

An increasing ROA ratio earns a higher score.

Δ Gross Margin

The gross margin indicator measures the trend of a firm’s percentage of sales after subtracting

the cost of goods sold (COGS). A firm’s gross margin is an easy variable to illustrate how cost

effective a company can be. An increasing gross margin earns a higher score.

Δ Gross Profit Over Assets (GPOA)

According to Novy-Marx’s paper “The Other Side of Value” (2013), this indicator has the same

predictive power as the B/M ratio. This ratio illustrates the trend of a company’s profit efficiency

and financial health over past years. A higher Δ GPOA earns a higher score. GPOA is

calculated by:

𝐺𝑃𝑂𝐴 = 𝐺𝑟𝑜𝑠𝑠 𝑃𝑟𝑜𝑓𝑖𝑡𝑡/𝐴𝑠𝑠𝑒𝑡𝑠𝑡

Quantitative Screens & Analysis

Small-Cap Portfolio: Healthcare & Consumer Staples

Page 37 of 57

Δ Asset Turnover

This indicator measures the trend of how efficiently a company takes advantage of its assets. A

high Δ asset turnover earns a higher score. Asset turnover is calculated by:

𝐴𝑠𝑠𝑒𝑡 𝑇𝑢𝑟𝑛𝑜𝑣𝑒𝑟 = 𝑅𝑒𝑣𝑒𝑛𝑢𝑒𝑡/(𝐴𝑠𝑠𝑒𝑡𝑠𝑡−1 + 𝐴𝑠𝑠𝑒𝑡𝑠𝑡

2)

Δ Leverage

This indicator implies the trends company’s ability to payback long-term debt in future.

According to Piotroski, the increasing number of leverage show a negative signal because the

additional borrowing adds pressure to company’s financial flexibility. So we give the highest

score to the company with the lowest Δ Leverage ratio.

Δ Accruals to Assets

This indicator measures the trend of company’s quality of total revenue. According to

Hirshleifer, Hou, Teoh, and Zhang’s paper “Do Investors Overvalue Firms with Bloated Balance

Sheets” (2004), increasing accruals can have negative effect on stock’s future price performance.

Stocks with higher Δ Accruals to Assets earn a lower score. Accruals to assets is calculated by:

𝐴𝑐𝑐𝑟𝑢𝑎𝑙𝑠 𝑡𝑜 𝐴𝑠𝑠𝑒𝑡𝑠= (𝐼𝑛𝑐𝑜𝑚𝑒 𝑏/𝑜 𝑋𝑂 𝑖𝑡𝑒𝑚𝑠𝑡

− 𝑂𝑝𝑒𝑟𝑎𝑡𝑖𝑛𝑔 𝑐𝑎𝑠ℎ 𝑓𝑙𝑜𝑤𝑡)/(𝐴𝑣𝑒𝑟𝑎𝑔𝑒 𝐴𝑠𝑠𝑒𝑡𝑠𝑡,𝑡−1) )

Δ Liquidity

This indicator measures the trend of company’s ability to payback short-term debt, also known

as a firm’s current ratio. The higher a current ratio indicates the company has high ability to

meet short-term debt obligations and working capital obligations.

Δ Leverage

This indicator measures a company’s trend in its long term debt relative to its total assets. The

higher the Δ Leverage, the lower the score. Leverage is calculated as:

𝐿𝑒𝑣𝑒𝑟𝑎𝑔𝑒 = (𝐿𝑜𝑛𝑔 𝑇𝑒𝑟𝑚 𝐷𝑒𝑏𝑡)/(𝐴𝑠𝑠𝑒𝑡𝑠)

Δ Inventory Turnover (Consumer Staple sector only)

The Δ Inventory Turnover measures the trend over time of how many times a company sells and

replaces its products. This indicator is important to the Consumer Staple sector because the

Small-Cap Portfolio: Healthcare & Consumer Staples

Page 38 of 57

business strategy is simple and requires selling goods through inventory based operations. With a

strong Δ Inventory Turnover ratio, a company would be consistently paying less and less for

storage costs over time. Inventory Turnover is calculated as:

𝐼𝑛𝑣𝑒𝑛𝑡𝑜𝑟𝑦 𝑇𝑢𝑟𝑛𝑜𝑣𝑒𝑟 = 𝐶𝑜𝑠𝑡 𝑜𝑓 𝐺𝑜𝑜𝑑 𝑆𝑜𝑙𝑑/(𝐴𝑣𝑒𝑟𝑎𝑔𝑒 𝐴𝑠𝑠𝑒𝑡𝑠)

Risk Analysis: Step Z: Bankruptcy Risk

The small-capitalization companies tend to have high bankruptcy risk. Before moving to step 2

in the quantitative analysis, firms that have high probability of bankruptcy are eliminated using

Altman Z scores. Altman Z score is the criteria for risk because it reflects the financial condition

comprehensively in the following aspects: scale of capital, liquidity, profitability, financial

structure, debt payoff capacity, efficiency to use assets, etc. Firms with a Z score higher than

2.99 were eliminated, leaving healthy firms with low likelihood of bankruptcy to move to the

next quantitative step. Step Z results can be seen in Exhibit 6 of the Appendix.

Step 2: Value or Growth

Step 2: Value or Growth uses variables related to a company’s value compared to its market

value to determine how relatively undervalued a firm’s stock price may be. In this step, three

current variables are used and weighted equally to determine the stock’s value. All stocks that

enter this step are sorted into quintiles for each variable, and receive a score based on which

quintile they fall into relative to other stocks. After receiving scores of 1 – 5, 5 ranking the best,

for each variable, they are then weighted equally and summed up to receive an aggregate score

for this step. Below are the variables used for Step 2: Value or Growth and the results for this

screen can be seen in Exhibit 7 of the Appendix.

Book-to-Market (B/M) Ratio

This ratio compares the book value of the company to the market value of the company. In order

to find the relatively undervalued firms, stocks are sorted by B/M ratio from the highest to the

lowest. The most points are given to the companies which have high B/M ratios, because a high

B/M ratio means the company is undervalued by the market. The total equity amounts for each

firm are controlled for their R&D expenses.

Cash Flow-to-Price (CF/P) Ratio

According to Chan, Hamao, and Lakonishok, companies with high CF/P ratios statistically

generate higher returns than those with low CF/P ratios. In Health Care sector, we add R&D

expense in to the cash flow to get the CF/P ratio. After sorting the CF/P ratio from the highest to

the lowest, stocks with high CF/P ratios are ranked highest.

Small-Cap Portfolio: Healthcare & Consumer Staples

Page 39 of 57

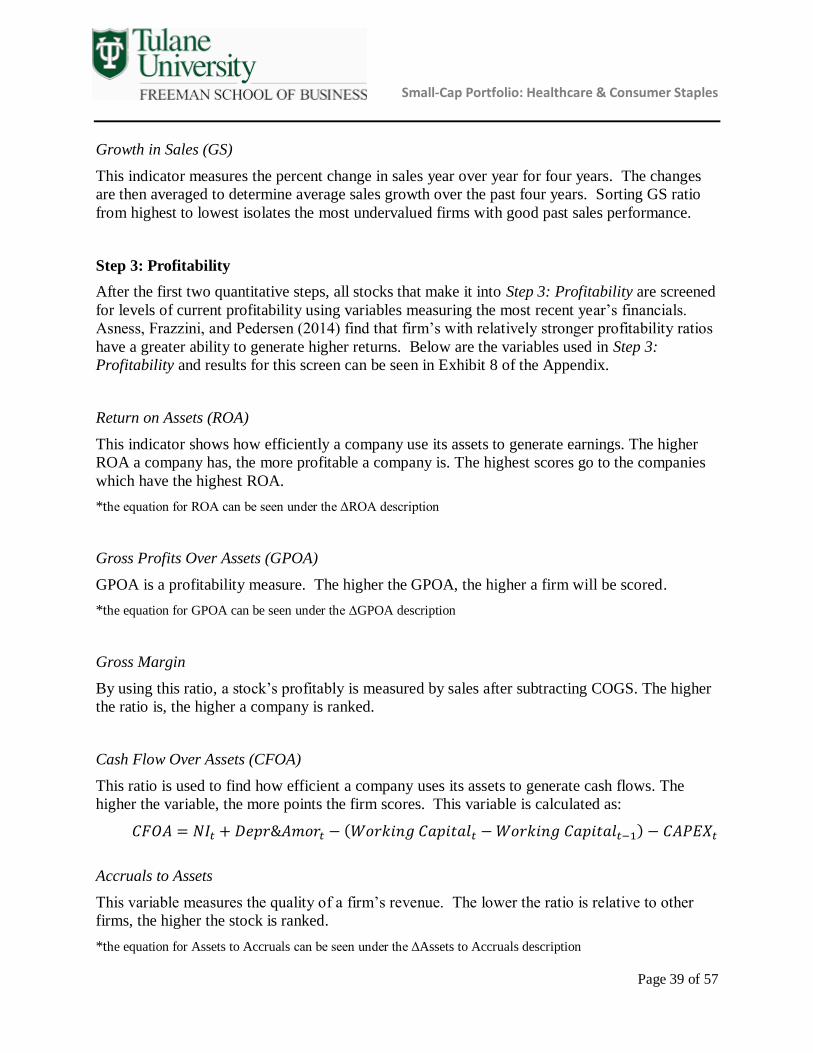

Growth in Sales (GS)

This indicator measures the percent change in sales year over year for four years. The changes

are then averaged to determine average sales growth over the past four years. Sorting GS ratio

from highest to lowest isolates the most undervalued firms with good past sales performance.

Step 3: Profitability

After the first two quantitative steps, all stocks that make it into Step 3: Profitability are screened

for levels of current profitability using variables measuring the most recent year’s financials.

Asness, Frazzini, and Pedersen (2014) find that firm’s with relatively stronger profitability ratios

have a greater ability to generate higher returns. Below are the variables used in Step 3:

Profitability and results for this screen can be seen in Exhibit 8 of the Appendix.

Return on Assets (ROA)

This indicator shows how efficiently a company use its assets to generate earnings. The higher

ROA a company has, the more profitable a company is. The highest scores go to the companies

which have the highest ROA.

*the equation for ROA can be seen under the ΔROA description

Gross Profits Over Assets (GPOA)

GPOA is a profitability measure. The higher the GPOA, the higher a firm will be scored.

*the equation for GPOA can be seen under the ΔGPOA description

Gross Margin

By using this ratio, a stock’s profitably is measured by sales after subtracting COGS. The higher

the ratio is, the higher a company is ranked.

Cash Flow Over Assets (CFOA)

This ratio is used to find how efficient a company uses its assets to generate cash flows. The

higher the variable, the more points the firm scores. This variable is calculated as:

𝐶𝐹𝑂𝐴 = 𝑁𝐼𝑡 + 𝐷𝑒𝑝𝑟&𝐴𝑚𝑜𝑟𝑡 − (𝑊𝑜𝑟𝑘𝑖𝑛𝑔 𝐶𝑎𝑝𝑖𝑡𝑎𝑙𝑡 − 𝑊𝑜𝑟𝑘𝑖𝑛𝑔 𝐶𝑎𝑝𝑖𝑡𝑎𝑙𝑡−1) − 𝐶𝐴𝑃𝐸𝑋𝑡

Accruals to Assets

This variable measures the quality of a firm’s revenue. The lower the ratio is relative to other

firms, the higher the stock is ranked.

*the equation for Assets to Accruals can be seen under the ΔAssets to Accruals description

Small-Cap Portfolio: Healthcare & Consumer Staples

Page 40 of 57

The qualitative screening process delves into firm-specific details that measure several factors

considered either too subjective or difficult to quantify, or not powerful enough to remove stocks

prior to looking at them further. The qualitative screening process assesses all variables

collectively to determine each firm’s ability to generate high abnormal stock returns in the

future. Each variable is collected through numerical data and data supplied in each firm’s annual

reports as well as competing companies financial filings. Below is a table of firm specific

variables used in the qualitative screen.

Category Variables

Macroeconomic Drivers

Regulations

Population

Technology Driver

Firm Operations Products/ Patents Development or Moats

Acquisition & Spin-off Quality

Corporate Governance &

Management

Stock Repurchases

Insider Trading

Management Stability

Financial Quality

Profitability Improvement

Earnings Surprise Performance

Downside Beta

Macroeconomic Drivers

Macroeconomic drivers are considered external variables impossible for firms to control, such as

demographics, regulations, available and/or competing technologies. If a firm is exposed to a

macroeconomic risk, it will be mentioned under this variable.

Firm Operations

Acquisition and Spin-off Quality

Acquisitions play a large part in many companies’ growth strategies. This variable assesses each

company’s ability to generate revenue through acquisitions in both the past and the future

depending on the historical data and future plans of each firm.

Corporate Governance and Management

Stock Repurchases

Qualitative Screens & Analysis

Small-Cap Portfolio: Healthcare & Consumer Staples

Page 41 of 57

This indicator represents a firm’s plans to repurchase stock from the public. Usually, a stock

repurchase is a positive signal because it shows the company’s confidence in its financial

condition and undervalued stock price. Here, any stock repurchases over the last two years are

reported in the variable.

Insider Trading

This information shows how many stocks the company executives bought and sold in the past 3

or 12 months. If the number of shares bought exceeds the number of shares sold, it shows a good

signal that the company is in good financial condition and the executives are confident about the

price of their own firm’s shares.

Management Stability

Management stability is measured using several factors including whether or not the founder has

recently left the company or if management has been restructured in a way that may benefit or

hurt the condition of the company. Any issues related to the strength of management or any

signals of a change in management can be found here.

Financial Quality

Profitability Improvement

Many of the quantitative factors used in the initial screening process may have been inflated or

deserve further investigation. This section reports any interesting findings regarding a

company’s improving financial condition upon further investigation of financial data.

Earnings Surprise Performance

This indicator shows how many times in the past 2 years the company earnings actually

exceeded consensus analyst estimates. The more times the company beats its earnings estimates,

the better signal it shows. Another variable used in this analysis is the earnings surprise ratio.

Doyle, Lindholm and Soliman (2006) explain that stocks with high earnings surprise ratios

statistically achieve higher future abnormal returns. The earnings surprise ratio is calculated as:

𝐸𝑆 𝑅𝑎𝑡𝑖𝑜 = (𝐴𝑐𝑡𝑢𝑎𝑙 𝐸𝑃𝑆 − 𝐴𝑛𝑎𝑙𝑦𝑠𝑡 𝐶𝑜𝑛𝑠𝑒𝑛𝑠𝑢𝑠 𝐸𝑃𝑆)/(𝐴𝑐𝑡𝑢𝑎𝑙 𝑆𝑡𝑜𝑐𝑘 𝑃𝑟𝑖𝑐𝑒)

Downside Beta

The downside beta shows the systematic risk a company is exposed to during market downturns.

A downside beta lower than one shows the systematic risk of the company is lower than the

market. A downside beta higher than one shows there is a higher risk behind the company than

the risk of the market. While this variable is useful for consideration, the investment theory

behind this process does not support the theory that historical betas affect future systematic risk.

Small-Cap Portfolio: Healthcare & Consumer Staples

Page 42 of 57

Firm-Specific Qualitative Analysis Tables

Table 6: Post-Screening Firm Overview

Ticker Name STEP 1 STEP 2 STEP 3

BGS B&G Foods Inc 6th/17 6th/11 5th/7

SPTN SpartanNash Co 7th/17 1st/11 3rd/7

MED Medifast Inc 14th/17 NA N/A

Small-Cap Portfolio: Healthcare & Consumer Staples

Page 43 of 57

B&G Foods Inc. (BGS)

B&G Foods Inc. (NYSE: BGS)

B&G Foods manufactures, sells and distributes a diverse portfolio of branded, high quality, shelf-stable

foods and household products in the United States, Canada, and Puerto Rico. The company offers its

products directly, as well as via a network of independent brokers and distributors to supermarket chains,

food service outlets, mass merchants, warehouse clubs, non-food outlets, and specialty distributors.

Macroeconomic

Drivers

The processed food industry is one of the United States' largest industries, which

characterized by relatively stable sales growth, based largely on price and population

increases.

B&G experiences margin pressure in certain markets as a result of competitors' pricing practices.

Firm Operations

The company has been built upon a successful track record of both organic and

acquisition-driven growth.

Net cash provided by operating activities decreased $15.8 million to $99.1 million in fiscal 2014 from $114.9 million in fiscal 2013 was primarily due to costs associated with the

Ortega and Las Palmas recall and other activities.

The company historically financed acquisitions with borrowings and cash flows from operating activities. On January 3, 2015, its total long-term debt of $1,025.9 million, net

of our cash and cash equivalents of $1.5 million, was $1,024.4 million. Stockholders'

equity as of that date was $338.0 million.

Unique multi-channel distribution strategy and unique multi-channel distribution strategy are primary differentiators that allow it to compete in this market.

Corporate

Governance & Management

The company just announced the primary equity offering on 04/28/2015 with an offer

size of 128.52 million.

B&G Food did not repurchase any shares of common stock during fiscal 2014, 2013 or

2012.

The number of shares bought exceeded the number of shares sold for the insider trading

in the past 3 months.

Financial

Quality

6 Analyst coverages

Downside beta is 0.41 comparing to the sector’s beta, which is 0.70.

Small-Cap Portfolio: Healthcare & Consumer Staples

Page 44 of 57

SpartanNash Co. (SPTN)

SpartanNash Co. (NYSE: SPTN)

SpartanNash is a good company with wide distribution range and continuously good acquisitions. The

company shows a financial health, an efficient management, low analyst coverages, and high frequency of

beating the market for earnings surprises. Stock repurchases showed the expectations of the future from the

firm’s prospective. The good financial results give us the confident that the company will continue well-performed in the future.

Macroeconomic

Drivers

Military, Food Distribution and Retail segments operate in highly competitive and low

profit margins markets. However, SpartanNash offers a full set of services, from value added service to the inclusion of fuel centers which helps it to compete with other peers.

Firm Operations

Several projects were planned for the fiscal year ending January 2, 2016 to further

integrate SpartanNash supply chain capabilities across distribution centers and thereby

increase the efficiency of both its inbound and outbound distribution operations.

The distribution facilities are strategically located to efficiently serve the company’s

current customers and have the available capacity to support future growth. the over-

arching focus on the consumer gives it competitive insight into purchasing and consumption behavior.

Corporate Governance &

Management

During fiscal years ended January 3, 2015 and March 30, 2013, the Company

repurchased 245,956 and 634,408 shares of common stock for approximately $5.0

million and $11.4 million, respectively.

The number of shares bought exceeded the number of shares sold for the insider trading in the past 3 months.

Financial Quality

Earnings surprise beat 5 of 6 in the last 6 periods.

4 Analyst coverages

Downside beta is 1.09, which is higher comparing to the consumer staples, 0.70.

Small-Cap Portfolio: Healthcare & Consumer Staples

Page 45 of 57

Medifast Inc (MED)

Medifast Inc. (NTSE: MED)

Midifast has its board of directors reconstituted and decreased from 12 to 9 independent directors. A franchise loan caused Midifast’s revenue and income from operations decreasing in 2014 from the 2013

level. With the development of consumer discretionary, Medifast faces uncertainties of its future profits.

Macroeconomic

Drivers

Consumer discretionary spending environment challenges the revenue of Medifast.

There are various weight loss products and programs within the highly competitive

weight-loss industry.

Firm Operations

Medifast expanded its product line in 2014 by introducing the most new products in the

Company’s history to meet consumer demand.

The Company experienced lower marketing efficiencies and new customer acquisition

during the year because of a default on a franchise loan guaranteed by Medifast and an

increase in legal expenses that caused $2.6 million in extraordinary expenses.

Income from operations decreased by $8.2 million, or 21%, versus 2013 with the percent of sales decreasing to 10.6% in 2014 as compared to 11.9% in 2013.

Medifast Direct Sales revenue decreased 24% to $57.2 million as compared with $75.5

million in 2013, a decrease of $18.3 million.

Corporate Governance &

Management

In the year ended December 31, 2014, Cash from financing activities was used to

purchase $33.9 million of treasury stock in the open market.

Medifast announced reconstitution of board of directors in 04/07/2015, which will eliminate its classified board and decrease the size of the board from 12 to 9.

The number of shares sold exceeded the number of shares bought for the insider trading

in the past 12 months.

Financial Quality

4 Analyst coverages