123

Data Collection guide March 2015 2015 Customer Service Benchmarking

| Date post: | 26-Dec-2015 |

| Category: |

Documents |

| Upload: | jeffry-wright |

| View: | 216 times |

| Download: | 2 times |

Data Collection guide

March 2015

2015 Customer Service Benchmarking

The organization of this Guide follows the questionnaire outline:

Data Collection Guide Outline

◼ ST. Statistics◼ KA. Key Accounts◼ FL. Financial◼ SF. Staffing◼ S. Safety◼ CS. Customer Satisfaction◼ IT. Customer Service I.T.◼ FR. First Contact Resolution

2

CT1. Contact Center CT2. Contact Volumes SS. Self-Service & Integration BL. Billing PP. Payment Processing FS. Field Service MR. Meter Reading CR. Credit & Collections RP. Revenue Protection

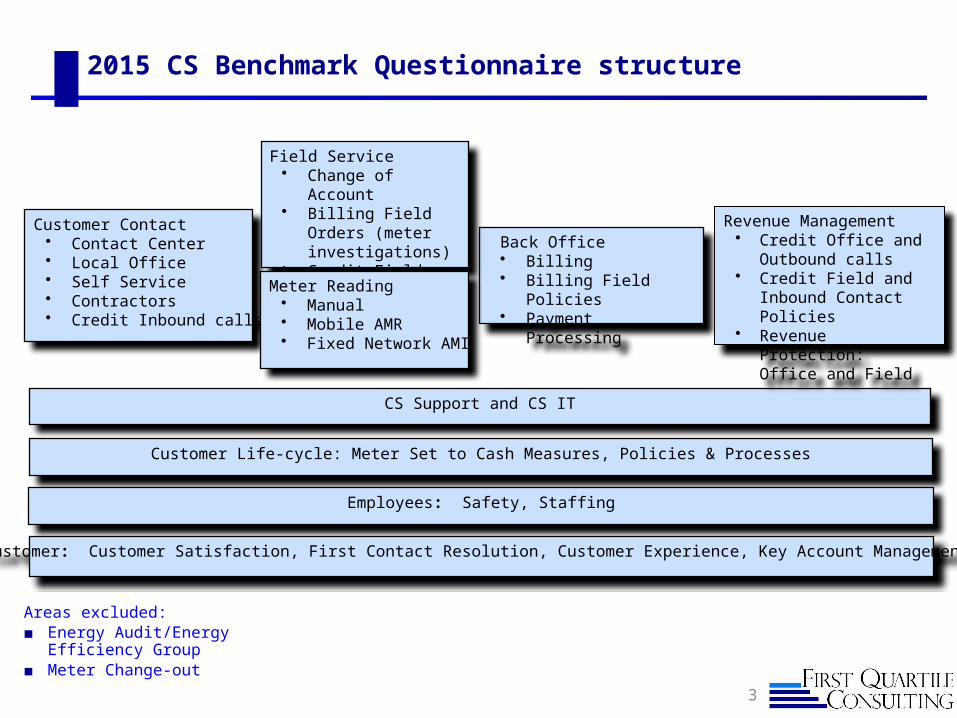

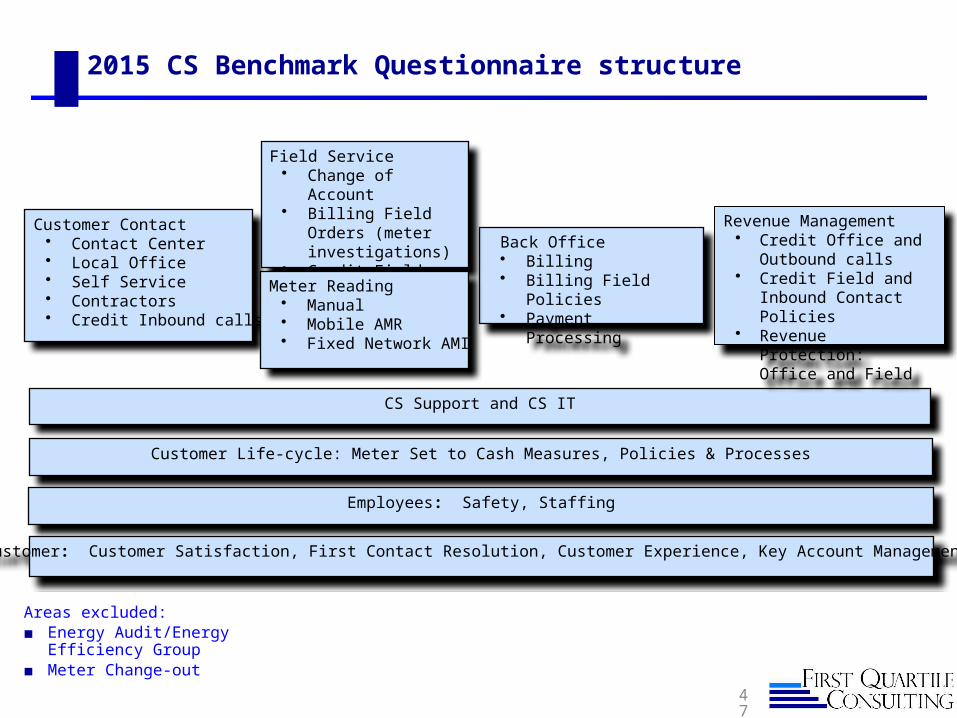

2015 CS Benchmark Questionnaire structure

3

CS Support and CS IT

Customer Contact• Contact Center• Local Office• Self Service• Contractors• Credit Inbound calls

Back Office• Billing• Billing Field Policies• Payment Processing

Field Service• Change of Account• Billing Field Orders

(meter investigations)

• Credit Field Orders• Order Management

Meter Reading• Manual• Mobile AMR• Fixed Network AMI

Revenue Management• Credit Office and

Outbound calls• Credit Field and Inbound

Contact Policies• Revenue Protection:

Office and Field

Customer Life-cycle: Meter Set to Cash Measures, Policies & Processes

Employees: Safety, Staffing

Customer: Customer Satisfaction, First Contact Resolution, Customer Experience, Key Account Management

Areas excluded:◼ Energy Audit/Energy

Efficiency Group◼ Meter Change-out

Introduction

Purpose of this document◼ The purpose of this Data Collection Guide is to provide guidance and

direction in how to complete the detailed questionnaire for the Customer Service benchmark study. It gives instructions regarding the types of answers expected, as well as errors to avoid. This Guide has been described as the “rules” for providing data.

◼ It provides the underlying process models around which the various sections of the questionnaire are organized, to help in understanding the purpose of some of the questions.

◼ The appropriate costs to include, and those to exclude, are highlighted, so that each member utility can provide accurate, comparable data for comparisons.

◼ A few key definitions are provided throughout the document. A comprehensive set of definitions is provided in a separate Glossary.

4

Collecting Financial, staffing & Volume data

It’s important to have everyone who is collecting financial, staffing and volume data communicating so that these items align. ◼ Be sure that labor costs include any staff reported◼ Be sure that activities/volumes match with the costs reported and vice

versa.

It’s helpful to have everyone collecting financial and staffing data review each of the sections functional sections so that they know what activities are included or excluded.

5

Initiatives vs. Practices

In many areas of the questionnaire, there are open-ended questions, in which we are looking for insights about how you operate. Answers should be:

◼ Brief and succinct – so that the reader doesn't't need to read through an extensive volume of material to understand the message; because the responses will be printed verbatim, don't mention your company name or individual names in your replies

◼ Complete enough to be understood in terms of the practice you are describing

◼ Practically speaking, this translates to 2-3 sentence answers to most of the text questions

For our purposes:

◼ Practices are current activities, programs or processes that have been around for a while. For these, sufficient time has passed in which to assess their success or failure. We mostly ask about practices that have proven successful in accomplishing a specific goal.

◼ Initiatives are new activities, programs or processes that have been enacted recently with the goal of improvement. These are so recent (1 to 2 years) that insufficient time has passed in which to assess their success.

6

Statistics

7

Purpose of the Section

The purpose of this section of the questionnaire is two-fold:

◼ To gather statistical information about the existing customer base, and then,

◼ To gather a bit of information about the organization of the Customer Service functions.

The Statistical Section gathers a variety of demographic information that describes each company's system in terms of size, customer density, etc. This information is used in doing analysis of the results, and understanding the inherent advantages and limitations of the circumstances facing each utility.

8

Statistical: Customer count

◼ Questionnaire: In the questionnaire we ask for meters and accounts. We ask for counts of both to be separated by commodity. Accounts Definition: Active accounts in your system. An account is typically used for

billing purposes. ◼ Reporting: In the report we will use both accounts and meters as denominators. In

some cases we'we will multiply the number of accounts by the number of commodities billed on that account. This will produce some adjusted numbers that get at the extra cost of serving an account that receives multiple commodities. Customer Count (accounts * commodity) = We add the number of accounts for

individual commodities to get the total. Roughly represents the number of meters. There are unmetered items and meters that are not counted (such as streetlights).

Customer Count (accounts) = Roughly represents the number of accounts. An account with electric and gas meters gets counted once.

Customer Count (internal) = The count you use internally to represent the number of customers you have. This is the one reported on annual reports and other documents.

9

Other Customers: Many utilities, especially municipals, provide other services beside electric, gas and water. Most of these we do not want, except for waste. If you also provide other services such as Waste pick-up, contact us and we'll help you to determine how to handle this.

Non-delivery customers can also be included.

We use one customer count as the denominator for all of the various costs. So you want to provide the customer count that best reflects your activity level in all of the

areas: meter reading, field service, billing, etc.

Customer Counts

10

This question allows us to track all the customers you have, by type (e.g. combination or single-commodity, etc.) These details are used as the denominators for many “cost per customer” calculations later.

If you can’t breakout C/I then enter into “Other”.

We do little analysis on the details.

Financial Section – Using the Cost Model

11

12

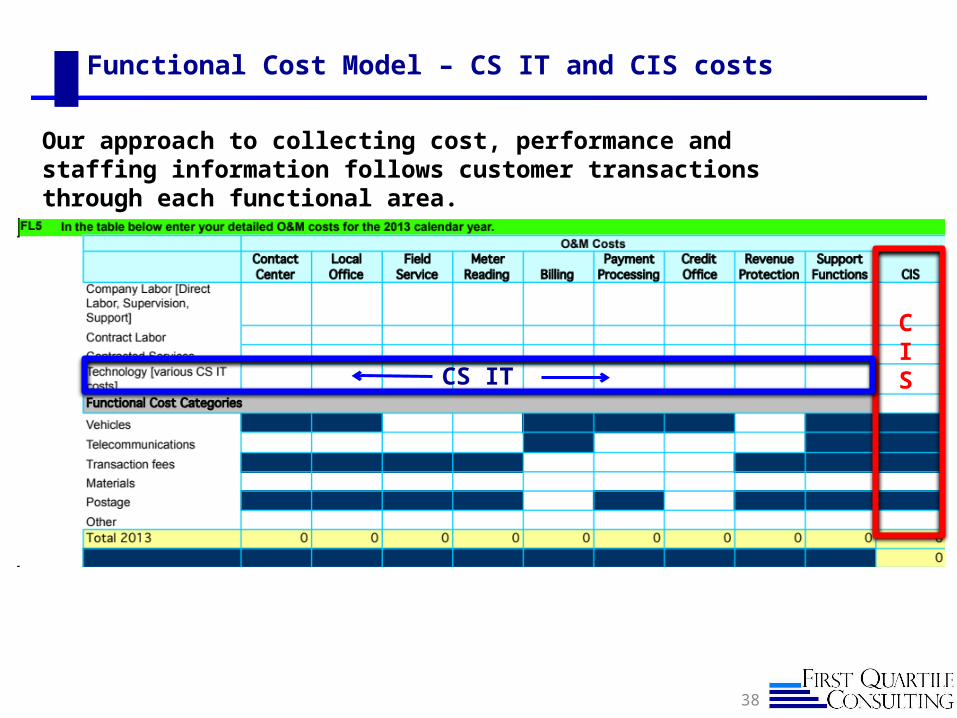

Functional Cost Model

Our approach to collecting cost, performance and staffing information follows customer transactions through each functional area.

If you have significant costs in one of the shaded categories, you can enter

your cost in the shaded box. No boxes are shaded on line.

Cost Categories Included

Costs can be broken down into basic categories◼ General:

Company Labor: direct, supervision, support Contract Labor (including temps, seasonal) Contracted Services Technology

(see page 17 for listing of technology to include and where)◼ Function-specific items:

Transaction fees Materials Postage Other

13

Cost definitions: General

14

Company Labor

Include Direct, Support, Supervision, Management. Cost of employees includes paid non-working time (e.g. vacation, sick, etc). Does not include labor overheads (e.g. payroll taxes, benefits) or other department's allocated charges. If a supervisor or manager spreads their time over multiple departments, then provide an allocated portion of their costs to the function. If someone works outside of CS and is applied as a corporate allocation charge, exclude them in labor costs. For support, include those people who are directly part of customer service but cannot be allocated to a specific function.50% rule: Include a person in an activity if they spend at least 50% of their time on that activity. If a person divides their time so that they don't spend at least 50% of their time on an activity they should be in the “Support” Group.

Contract Labor

Individuals contracted to perform a specific role

Contracted Services

Companies contracted to perform a specific function such as meter reading, overflow call centers, debt collection, etc.The cost of any contract or outsourcing services. Do not include any capitalized costs for IT services. Do include 3rd party back-up; disaster recovery. Include any collection agency or skip trace costs in contracted services.

Cost Definitions: functional

15

Materials Costs All cost associated with the function, including any warehouse/purchasing charges. A few items, such as postage are called out in a separate category. Includes cost of envelopes, paper, and ink. Should especially be included for Billing, Payment and Credit.

Postage Costs Cost of mailing bills and credit notices. Prepaid envelopes if used for payment processing. For postage for Credit & Collections, only include if a separate credit mailing, otherwise put in billing.

Transaction fees (fees paid by utility)

Fees for credit card transactions, bank charges, etc. Fees associated with payments (even if a call or a local office) still goes in payment. All third-party transaction costs associated with receiving and posting customer payments. This includes fees for lock box, credit card fees, payment gateways.

Cost Definitions: Functional

16

Vehicle Costs Costs associated with the operations & maintenance of vehicles for use solely by Customer service; usually charged out on a per mile or some other basis. Any payments for use of personal vehicles should also be included.

Other Costs Other miscellaneous costs not specifically broken out such as employee travel expenses; training; office supplies and any of the categories that are grayed out such as vehicles in the call center or postage in field service.

17

Technology Cost Within Function

NOTE: CIS is a separate category

Technology Any technology specifically used for a function such as meter reading devices, mobile data technology, telephone switch or call routing software, call monitoring software etc.

Contact Center:◼ IVR (Interactive Voice Response)◼ ACD (Automatic Call Distributor)◼ Scheduling Software◼ Workforce Management (WFM)◼ Multi-channel processing◼ Web, Social Media technology costs◼ VOIP (Voice Over Internet Protocol)◼ Web/email routers◼ Virtual Hold technology costs◼ 3rd party applications (OMS interface etc.)

Field:◼ Mobile data (software and hardware)◼ Scheduling◼ GPS (Global Positioning System)◼ Telecommunications◼ Routing software◼ Dispatching software

Revenue Protection◼ Tamper plug◼ Data mining software

Meter:◼ Handhelds◼ Routing software◼ Telecommunications◼ Remote disconnect◼ MV 90◼ GPS (Global Positioning System)

Bills:◼ Inserters◼ Web/email, bill presentment◼ C/I billing software

Payment:◼ Image processer◼ Slitter/sorter◼ Interface w/kiosks◼ Routing software for off-site payments◼ Payment Kiosks

Credit:◼ Behavioral scoring◼ Predictive dialer◼ Credit optimization software

Contact Center and CreditDetailed Cost Breakouts

In order to better understand costs we not only ask for them at the high level, but ask for some breakouts of cost by activity.

The diagram shows how the 2015 cost questions relate to one another.

These will be questions FL30-FL76 in the Financial Section

18

Meter ReadingDetailed Cost Breakouts

In order to better understand costs we not only ask for them at the high level, but ask for some breakouts of cost by activity.

The diagram shows how the 2015 cost questions relate to one another.

These will be questions FL30-FL76 in the Financial Section

19

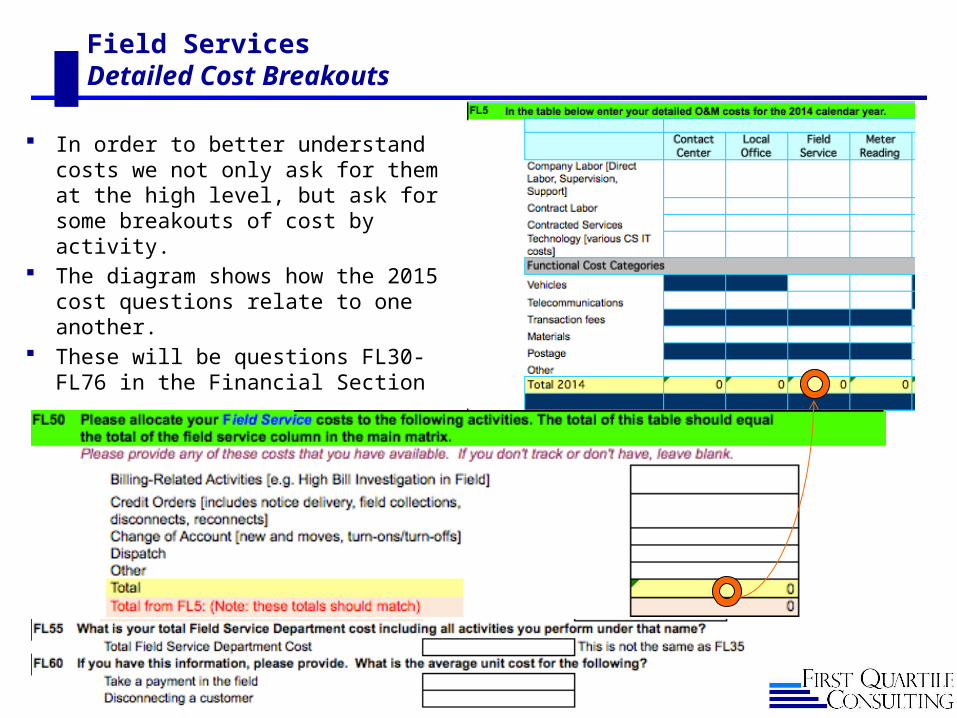

Field ServicesDetailed Cost Breakouts

In order to better understand costs we not only ask for them at the high level, but ask for some breakouts of cost by activity.

The diagram shows how the 2015 cost questions relate to one another.

These will be questions FL30-FL76 in the Financial Section

20

In order to better understand costs we not only ask for them at the high level, but ask for some breakouts of cost by activity.

The diagram shows how the 2015 cost questions relate to one another.

These will be questions FL30-FL76 in the Financial Section

21

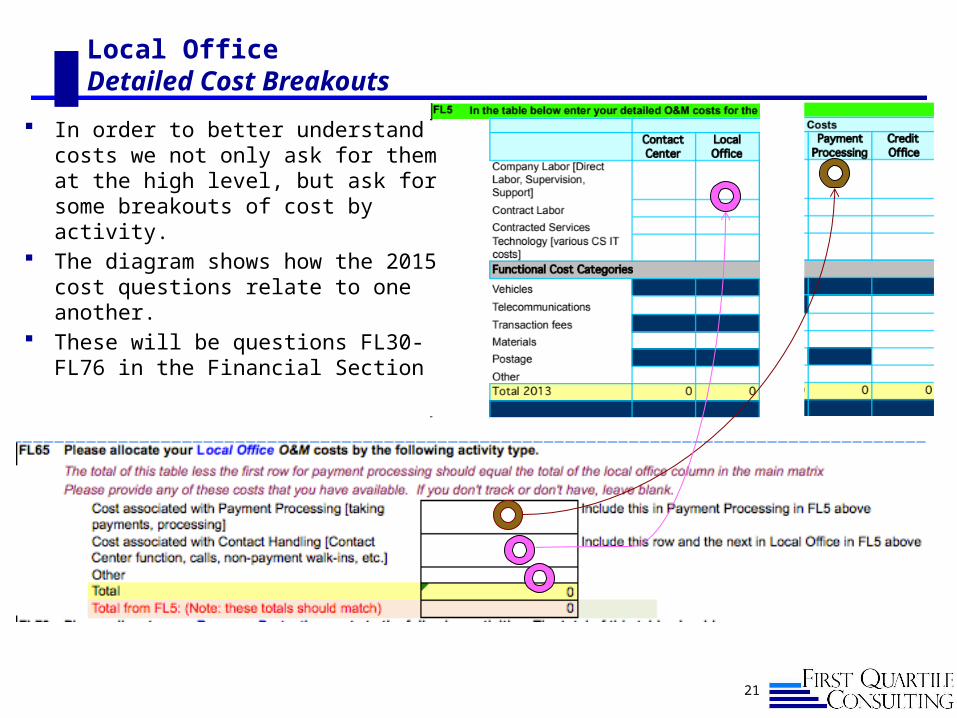

Local OfficeDetailed Cost Breakouts

In order to better understand costs we not only ask for them at the high level, but ask for some breakouts of cost by activity.

The diagram shows how the 2015 cost questions relate to one another.

These will be questions FL30-FL76 in the Financial Section

22

Revenue ProtectionDetailed Cost Breakouts

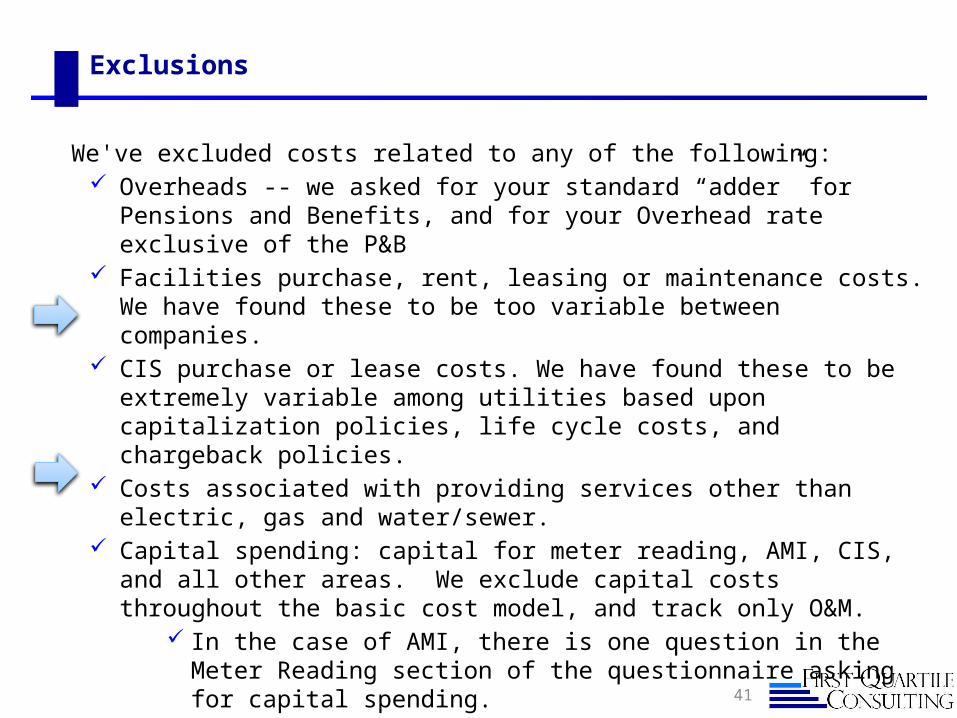

Exclusions

We've excluded costs related to any of the following:◼ Overheads -- we asked for your standard “adder” for Pensions and

Benefits, and for your Overhead rate exclusive of the P&B◼ Facilities purchase, rent, leasing or maintenance costs. We have found

these to be too variable between companies.◼ CIS purchase or lease costs. We have found these to be extremely

variable among utilities based upon capitalization policies, life cycle costs, and chargeback policies.

◼ Costs associated with providing services other than electric, gas and water/sewer.

◼ Meter purchase, installation, removal, retrofit, programmatic change out or maintenance costs.

◼ Capital spending: capital for meter reading, AMI, CIS, and all other areas. We exclude capital costs throughout the basic cost model, and track only O&M. In the case of AMI, there is one question in the Meter Reading section

of the questionnaire asking for capital spending.

23

This year we are seeking to understand capital investment in smart meters We are asking for the investment in each of the past 3 years- 2012, 2013, and 2014

24

AMI Capital Costs

25

Write-offs

This question captures Revenue and Write-off information. Note the most important fields are highlighted in red. If you do not answer these, you will not appear on the Write-offs per Revenue graph.

Write-offs Percent = Net percent of total revenue written off (e.g. less any recoveries). Goal is the actual dollar amount written off during the year. This is not necessarily the same as “uncollectibles”, which is in the FERC 904 account for the year, since that can be affected by changes in the provision for bad debt during the year (FERC 144 account). Write-offs are the annual “net” cost of bad debt. In other words any recoveries (less fees) should be subtracted from gross write-offs.

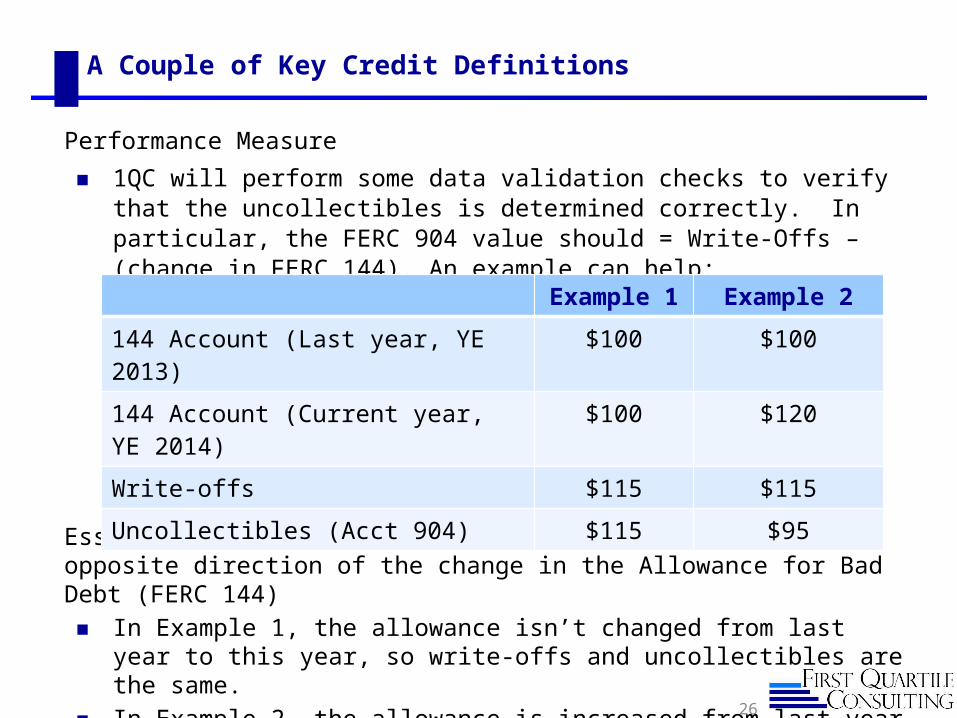

A Couple of Key Credit Definitions

Performance Measure

◼ 1QC will perform some data validation checks to verify that the uncollectibles is determined correctly. In particular, the FERC 904 value should = Write-Offs – (change in FERC 144). An example can help:

Essentially, the uncollectibles value varies in the opposite direction of the change in the Allowance for Bad Debt (FERC 144)◼ In Example 1, the allowance isn’t changed from last year to this year, so

write-offs and uncollectibles are the same.◼ In Example 2, the allowance is increased from last year to this one, which

has the effect of reducing the uncollectibles value for the year.

26

Example 1 Example 2

144 Account (Last year, YE 2013) $100 $100

144 Account (Current year, YE 2014) $100 $120

Write-offs $115 $115

Uncollectibles (Acct 904) $115 $95

Staffing & support

27

Staffing

Average or Year-end: We’re using FTEs so it’s really a full-year look. A person that was on payroll in January but left in July is 0.5 FTE. A person that started in Sept and worked through December is 0.3 FTE. If you’re using month end numbers to provide a response, use the average.

Staffing summary by◼ Direct Labor rule: a person having direct interactions with a customer or with a

customer account is considered direct labor. Everyone else is either supervision or support. Use the 50% rule if they divide their time.

◼ 50% rule: Include a person in an activity if they spend at least 50% of their time on that activity, you can indicate they are 0.5 FTEs. If a person divides their time so that they don't spend at least 50% of their time on an activity they probably should be in the “Support” Group.

◼ Employees assigned full time to a function. Include full-time supervisors and managers, or full-time employees who spend part time in different functions. Include part time supervisors and managers. Also include employees who spend less than 40 hours per week. When calculating FTE value use 2080 as the denominator.

◼ Outsourcing: If you outsource an entire function, do not attempt to turn that into FTEs.

28

Definitions: General

29

Direct Labor

A person having direct interactions with a customer or with a customer account is considered direct labor. A person whose task is directly in line with the mission of the process. Everyone else is either supervision or support. Use the 50% rule (see FTE definition in the Staffing Section) if they divide their time, if not 50% to a specific function, then charge to support.As a rule of thumb, when the work will affect a customer file or when it has an effect perceptible by a customer or a group of customers, this FTE will be classified as DirectTypes of direct labor (by function):

Contact center: taking calls, responding to correspondence, email, handling walk-in traffic

Meter reading: meter readers; mobile AMR van drivers Field service: representatives in the field collecting payments, disconnecting

customers, executing change-of-account orders, and billing investigations Billing: people handling exceptions, in-depth bill investigations, summary or

consolidated bill preparation Payment processing: people processing payments, handling payment exceptions,

lost or misapplied payments Credit and Collections: people making outbound calls regarding credit issues;

making payment arrangements with customers; issuing accounts for collections, and the Analysts who determine Credit policy and perform credit analysis.

Support Staff

Administrative support

Unlike technical support, administrative support refers to a task that is required in all processes. It is generic in nature and is (for the most part) interchangeable between functional areas. This category includes all secretarial /administrative FTEs as well as accounting and reporting activities that are decentralized in a specific activity, treatment of basic business information, scorecards, etc.

Technical support

Technical support includes people supporting work specific to that functional area. It refers to all tasks performed by an FTE in support of a Direct FTE. It is Mission oriented. It takes the form of a particular expertise or knowledge that can only be used for a particular activity or process. Trainers and schedulers are also part of this category. Technical support FTEs will not work directly on a particular case other than assisting direct FTEs resolve particular problems encountered. Their task may also be to analyze the process performance, produce new policies and design new business practices for direct FTEs in order to ensure the activity evolves towards greater performance.

30

CS Support area

Customer Service (CS) Support◼ Costs, FTE labor or activities associated with either the whole CS function that

cannot be allocated to another area of customer service or within a CS function that cannot be allocated to the activities described for that function.

◼ Only include people who don't spend at least 50% of their time in a specific functional area. This might include benchmarking/performance improvement; training; directors, vice president salaries.

◼ If training is for a specific functional area, then it belongs with that area. ◼ Do not include corporate allocations, or any HR activities. ◼ Inclusions (examples):

Training for Customer Service Overall centralized Quality function for Customer Service Benchmarking support for Customer Service Performance Management Group for Customer Service

◼ Exclusions (examples): Complaints handling Low income advocacy Regulatory, Human Resources, Corporate

31

Outsourcing- SF115

32

One question where we are looking for an outsourcing % for all functions…

Safety & Key Accounts

33

Safety

◼ For safety include Customer Service employees when calculating statistics.

◼ This should include direct labor, support, management and supervision for: Call Center Meter Readers Field Service (this may only include part of your Field Service

employees or parts of other functions)• Includes: disconnect and reconnect activities, field notices and

collections, high bill investigations, energy audits, and change-of-account work

• Excludes: lineman, meter shop, meter technicians, gas leak repair Billing & Payment Processing Credit and Collections Office Revenue Protection

34

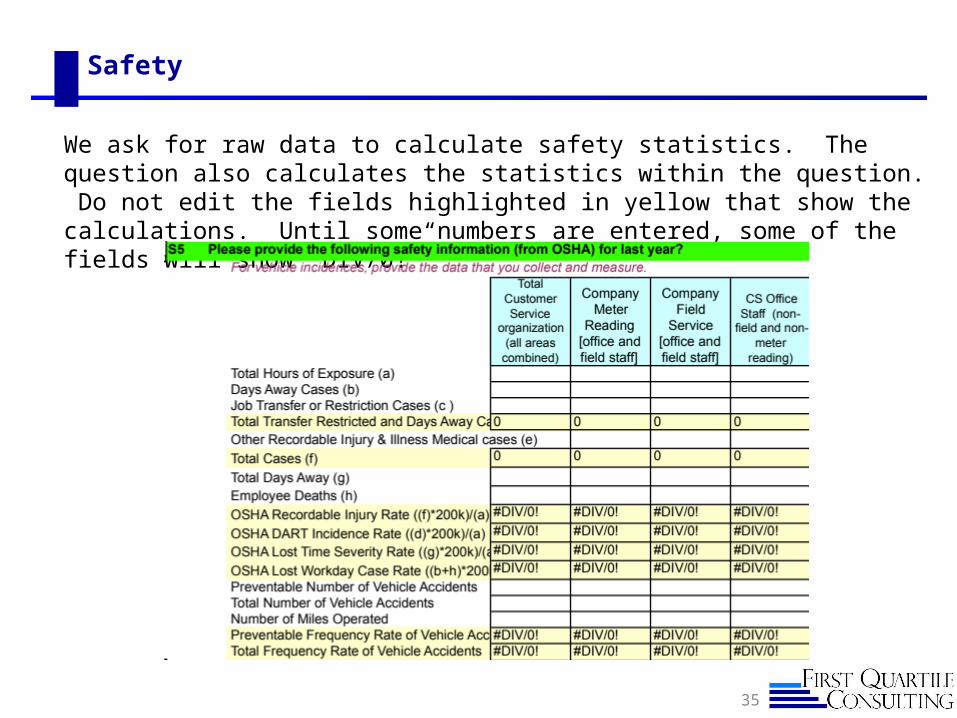

Safety

We ask for raw data to calculate safety statistics. The question also calculates the statistics within the question. Do not edit the fields highlighted in yellow that show the calculations. Until some numbers are entered, some of the fields will show “DIV/0!”

35

Key Account Management- New in 2015

In 2015, the survey asks about the elements and activities of key account management:

◼ Key accounts questions pertain to the organizations, practices and activities involved in interacting with and managing business customers who are receiving specific account management treatment from the utility. Typically, this is In the form of some type of dedicated and/or assigned account support/management

◼ We are seeking to understand how organizations have organized to support these customers, as well as the types of activities that are driving interaction and providing value

◼ This is section/tab KA in the 2015 survey

36

CIS and CS IT

37

38

Our approach to collecting cost, performance and staffing information follows customer transactions through each functional area.

CS IT

CIS

Functional Cost Model – CS IT and CIS costs

CIS vs. CS IT Costs

◼ CS IT (as part of “Technology” cost) is all the encompassing technology in a broad sense so it includes any non-CIS and may include some CIS, but is specific to a functional area

for example: ACD, IVR, Work Management, Mobile Data are part of CS IT and belong in their respective functional area (ACD to Contact Center etc.)

If there is a DIRECT allocation or charge to a function of CIS charges (such as usage or system utilization), then that goes into the CS IT, otherwise it is part of CIS

◼ CIS is the system used to to maintain customer information, generate bills, issue service requests, and help “manage” customer relationships by providing utility representatives data, information and insight about each customer's accounts, individual needs and preferences.

Examples of vendor's products include: Accenture's C/1 (Customer-1), Oracle Utilities Customer Care, SAP For Utilities.

CIS costs may be costs allocated to or associated with Customer Service but not to specific functions, such as usage charges, data transfer charges, and/or system maintenance charges. If such charges cannot be allocated to a specific function, they would go into the CIS cost column.

Everything else such as the Work Management, Mobile Data, Dispatch, ACD, IVR is Customer Service IT and should be specific to a function

39

40

Technology Cost Within Function

NOTE: CIS is a separate category

Technology Any technology specifically used for a function such as meter reading devices, mobile data technology, telephone switch or call routing software, call monitoring software etc.

Contact Center:◼ IVR (Interactive Voice Response)◼ ACD (Automatic Call Distributor)◼ Scheduling Software◼ Workforce Management (WFM)◼ Multi-channel processing◼ Web, Social Media technology costs◼ VOIP (Voice Over Internet Protocol)◼ Web/email routers◼ Virtual Hold technology costs◼ 3rd party applications (OMS interface etc.)

Field:◼ Mobile data (software and hardware)◼ Scheduling◼ GPS (Global Positioning System)◼ Telecommunications◼ Routing software◼ Dispatching software

Revenue Protection◼ Tamper plug◼ Data mining software

Meter:◼ Handhelds◼ Routing software◼ Telecommunications◼ Remote disconnect◼ MV 90◼ GPS (Global Positioning System)

Bills:◼ Inserters◼ Web/email, bill presentment◼ C/I billing software

Payment:◼ Image processer◼ Slitter/sorter◼ Interface w/kiosks◼ Routing software for off-site payments◼ Payment Kiosks

Credit:◼ Behavioral scoring◼ Predictive dialer◼ Credit optimization software

41

Exclusions

We've excluded costs related to any of the following: Overheads -- we asked for your standard “adder” for Pensions and Benefits,

and for your Overhead rate exclusive of the P&B Facilities purchase, rent, leasing or maintenance costs. We have found

these to be too variable between companies. CIS purchase or lease costs. We have found these to be extremely variable

among utilities based upon capitalization policies, life cycle costs, and chargeback policies.

Costs associated with providing services other than electric, gas and water/sewer.

Capital spending: capital for meter reading, AMI, CIS, and all other areas. We exclude capital costs throughout the basic cost model, and track only O&M.

In the case of AMI, there is one question in the Meter Reading section of the questionnaire asking for capital spending.

Customer Satisfaction, First Contact Resolution

42

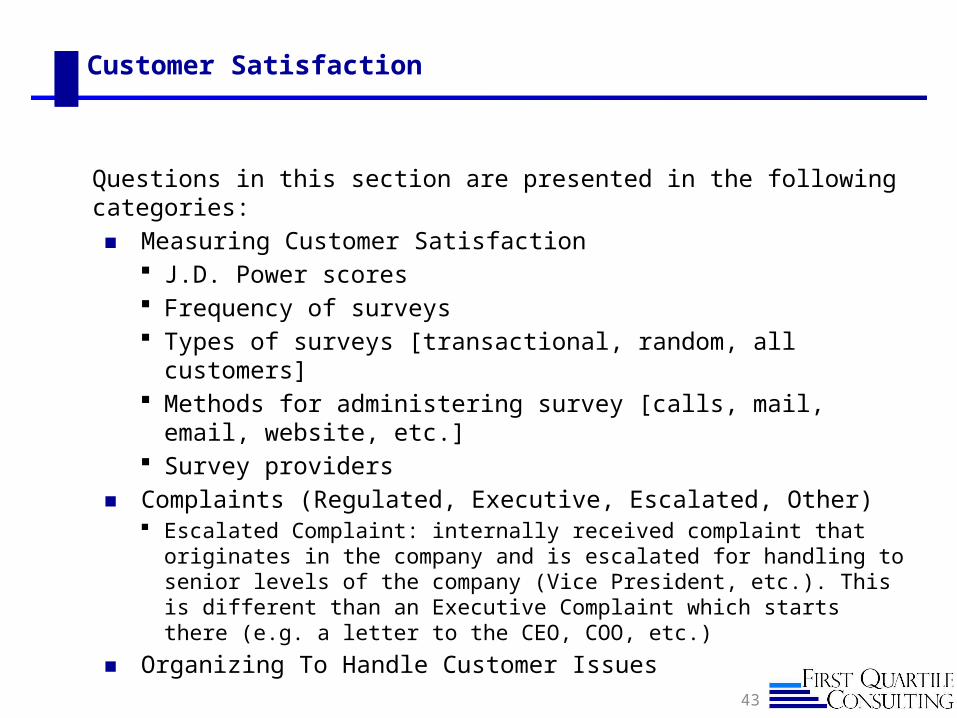

Customer Satisfaction

Questions in this section are presented in the following categories:◼ Measuring Customer Satisfaction

J.D. Power scores Frequency of surveys Types of surveys [transactional, random, all customers]

Methods for administering survey [calls, mail, email, website, etc.] Survey providers

◼ Complaints (Regulated, Executive, Escalated, Other) Escalated Complaint: internally received complaint that originates in the

company and is escalated for handling to senior levels of the company (Vice President, etc.). This is different than an Executive Complaint which starts there (e.g. a letter to the CEO, COO, etc.)

◼ Organizing To Handle Customer Issues

43

First Contact Resolution

◼ “First-Contact Resolution (FCR) is the percentage of initial contacts that do not require any further contact to address the customer reason for calling/contacting. The customer does not need to contact the company again to seek resolution, nor does anyone within the organization need to follow-up. Ideally, first-contact resolution should be defined from the customer perspective.”

(composite from multiple research sources)

44

Subject Areas in the FCR Section

The FCR section is relatively brief, although asking about a very important area of Customer Service. Key questions cover the following:

◼ Self-assessment◼ FCR definitions◼ Measurement approaches◼ Scope of FCR activities◼ Volume Reduction ◼ Customer Experience

45

Contact Center

46

2015 CS Benchmark Questionnaire structure

47

CS Support and CS IT

Customer Contact• Contact Center• Local Office• Self Service• Contractors• Credit Inbound calls

Back Office• Billing• Billing Field Policies• Payment Processing

Field Service• Change of Account• Billing Field Orders

(meter investigations)

• Credit Field Orders• Order Management

Meter Reading• Manual• Mobile AMR• Fixed Network AMI

Revenue Management• Credit Office and

Outbound calls• Credit Field and Inbound

Contact Policies• Revenue Protection:

Office and Field

Customer Life-cycle: Meter Set to Cash Measures, Policies & Processes

Employees: Safety, Staffing

Customer: Customer Satisfaction, First Contact Resolution, Customer Experience, Key Account Management

Areas excluded:◼ Energy Audit/Energy

Efficiency Group◼ Meter Change-out

48

Contact Center Introduction

◼ Contact Center covers the following areas of interest: Use of Call Center (internal and outsourced, including inbound

collections and small/mid-sized commercial and industrial account calls)

Use of Local Offices (there is a Local Office section for collecting costs separately from the Call Center)

Use of IVR (internal and outsourced) Use of Internet E-mail, fax, letter

◼ Enrollment and contract management for retailer (deregulated companies)

NOTE: Although payments by the above channels are included in Contact Center, do not include payment by check, at a kiosk or a payment center; these transactions are included in Payment Processing. Cashiers in Local Office who only take payments are part of Payment Processing.

Approach to Local Office Costs

49

Question FL65 follows from question FL5, in which the total costs for the Local Offices are provided. The goal is to understand how the costs are allocated across the services provided in the local offices.

As you’re preparing your data, your normal Local Office cost is likely to include costs that we want moved to Payment Processing per our guidelines. This question is a place to report your total Local Office cost but separated into the portions for Contact Center and Payment Processing.

Contact Center

What's not included:◼ Contact center covers every interaction with customers except:

Meter Reading Field Service Credit Outbound Calling Payment by mail, kiosk, or payment center

◼ Contacts related to regulatory, complaints, executive complaints, are not included here

◼ Contacts pertaining to large C&I customers (e.g. Account Managed) are not included here

◼ As per above, though payments that are made through contact center channels are included in Contact Center, they are also counted as payments in the Payment Processing section. Do not include payment by mail, at a kiosk or a payment center in contact center.

◼ Payments made to cashiers (who only take payments and perform no other functions) should be excluded from Contact Center.

50

51

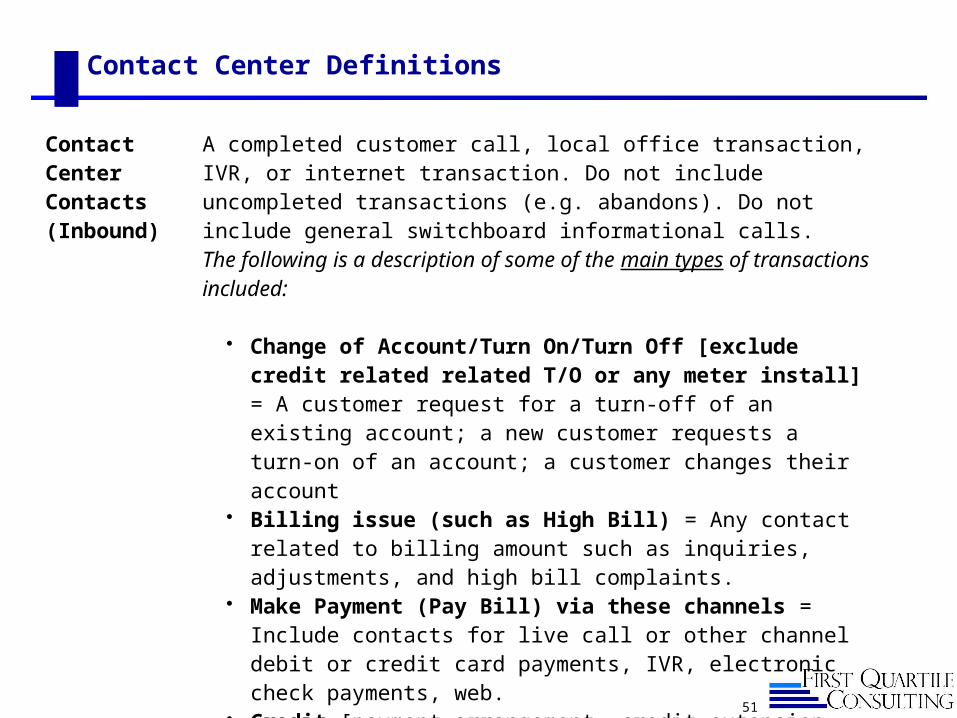

Contact Center Definitions

Contact Center Contacts (Inbound)

A completed customer call, local office transaction, IVR, or internet transaction. Do not include uncompleted transactions (e.g. abandons). Do not include general switchboard informational calls. The following is a description of some of the main types of transactions included:

• Change of Account/Turn On/Turn Off [exclude credit related related T/O or any meter install] = A customer request for a turn-off of an existing account; a new customer requests a turn-on of an account; a customer changes their account

• Billing issue (such as High Bill) = Any contact related to billing amount such as inquiries, adjustments, and high bill complaints.

• Make Payment (Pay Bill) via these channels = Include contacts for live call or other channel debit or credit card payments, IVR, electronic check payments, web.

• Credit [payment arrangement, credit extension, etc.] = Any contact related to a past due notice, including payment arrangements and reconnect of service

• Report Gas/Water Leak or Electric Interruption/Outage = A contact about an electrical outage, gas leak, water leak or other premise-related issue of this nature.

52

Contact Center Definitions (continued)

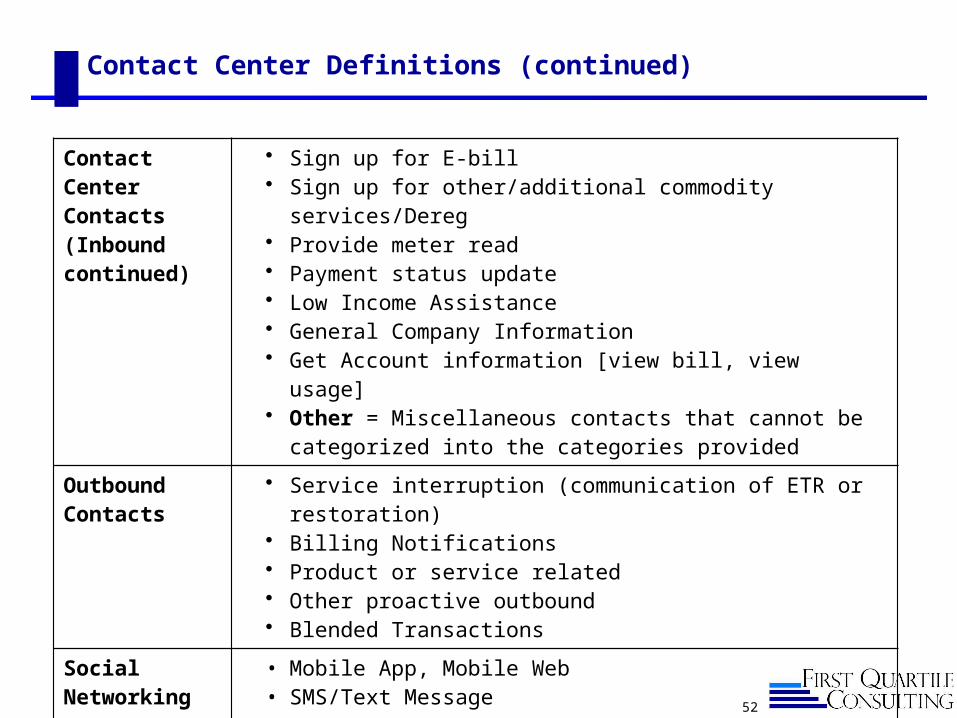

Contact Center Contacts (Inbound continued)

• Sign up for E-bill• Sign up for other/additional commodity services/Dereg• Provide meter read• Payment status update• Low Income Assistance• General Company Information• Get Account information [view bill, view usage]• Other = Miscellaneous contacts that cannot be categorized into

the categories provided

Outbound Contacts

• Service interruption (communication of ETR or restoration)• Billing Notifications• Product or service related• Other proactive outbound• Blended Transactions

Social Networking contacts

• Mobile App, Mobile Web• SMS/Text Message

Topics Covered in the Contact Center Section (CT1)

◼ Service Level and Measurements

◼ Demographics, Organization, and Scope of Services

◼ Measuring Shrinkage and Turnover

◼ Contact Volume Management Practices

◼ Initiatives

◼ Outsourcing

◼ Workforce Management

◼ Quality

◼ Understanding Contact Composition

◼ Estimated Time of Restoration

53

54

Technology- Contact Center

NOTE: CIS is a separate category

Technology Any technology specifically used for a function such as meter reading devices, mobile data technology, telephone switch or call routing software, call monitoring software etc.

Contact Center:◼ IVR (Interactive Voice Response)◼ ACD (Automatic Call Distributor)◼ Scheduling Software◼ Workforce Management (WFM)◼ Multi-channel processing◼ Web, Social Media technology costs◼ VOIP (Voice Over Internet Protocol)◼ Web/email routers◼ Virtual Hold technology costs◼ 3rd party applications (OMS interface etc.)

Field:◼ Mobile data (software and hardware)◼ Scheduling◼ GPS (Global Positioning System)◼ Telecommunications◼ Routing software◼ Dispatching software

Revenue Protection◼ Tamper plug◼ Data mining software

Meter:◼ Handhelds◼ Routing software◼ Telecommunications◼ Remote disconnect◼ MV 90◼ GPS (Global Positioning System)

Bills:◼ Inserters◼ Web/email, bill presentment◼ C/I billing software

Payment:◼ Image processer◼ Slitter/sorter◼ Interface w/kiosks◼ Routing software for off-site payments◼ Payment Kiosks

Credit:◼ Behavioral scoring◼ Predictive dialer◼ Credit optimization software

Contact Volumes

55

56

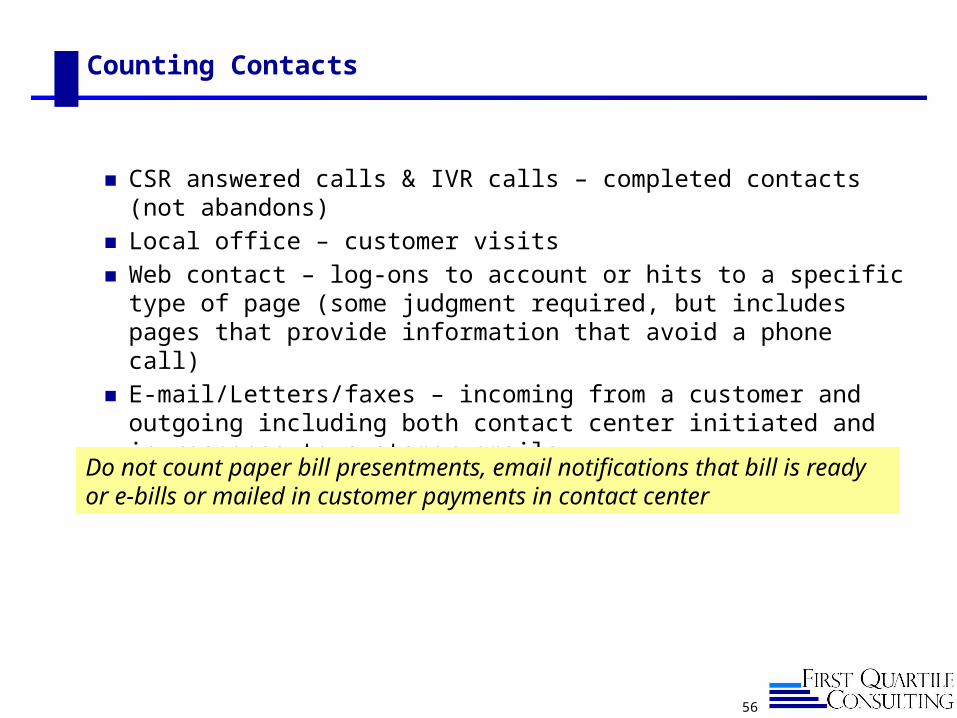

Counting Contacts

◼ CSR answered calls & IVR calls – completed contacts (not abandons)◼ Local office – customer visits◼ Web contact – log-ons to account or hits to a specific type of page (some

judgment required, but includes pages that provide information that avoid a phone call)

◼ E-mail/Letters/faxes – incoming from a customer and outgoing including both contact center initiated and in response to customer emails.

◼ Social networking – outbound

Do not count paper bill presentments, email notifications that bill is ready or e-bills or mailed in customer payments in contact center

Inbound Contact Volumes

57

T = Transactional activitiesL = Look-up activities

This matrix serves to provide the detailed information on how many contacts come into the company for each type of inquiry. Subsequent questions ask more detailed information about individual rows from this matrix.

Contact Volumes: Issues and Solutions

Identified Issues: ◼ There are 2 basic tables we ask to be completed in the Contact Volumes Section:

Inbound, Outbound, there are several related questions: Are the transaction types we are asking for used? Do they cover the types of

transactions your company is handling? (see CT305)◼ In the past several year, we have focused on how we define the “contact” for inbound.

Is it a completed transaction, is it just a contact? (Answer should be “completed”) Is it informational (e.g. view bill or “convenience transaction”) or does it have to be

specific business activity or event that is completed? Some companies report high volumes of “get information” or “general info”

(especially in web contacts).◼ There are at least 1/3 of the companies that CANNOT identify transactions (at all or

properly)—usually called “Other”. We need to work toward properly identifying these

58

59

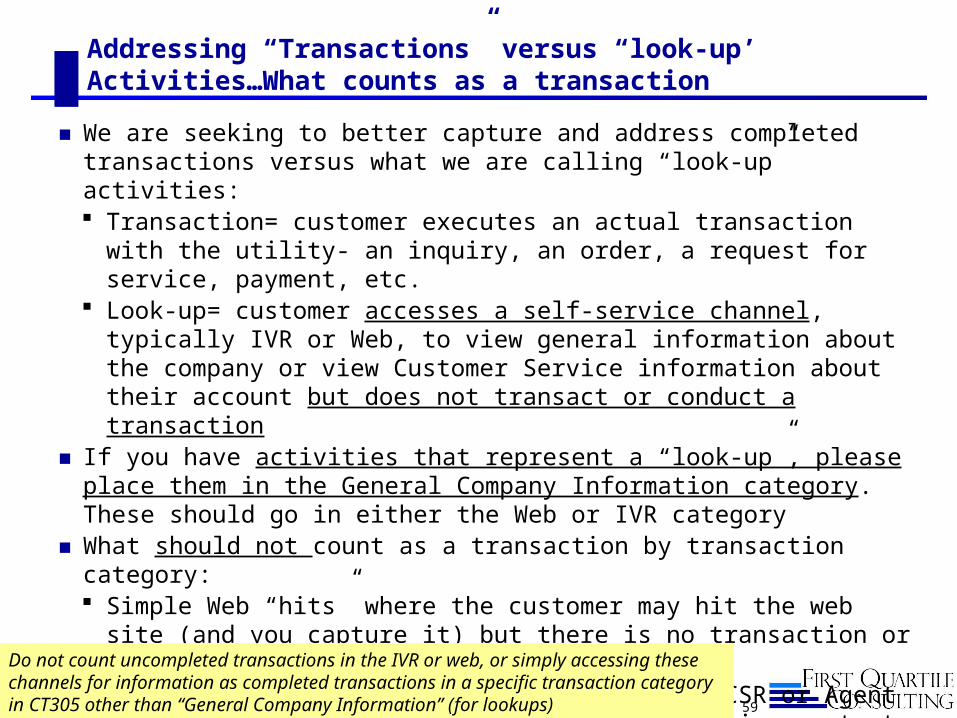

Addressing “Transactions” versus “look-up’ Activities…What counts as a transaction

◼ We are seeking to better capture and address completed transactions versus what we are calling “look-up” activities: Transaction= customer executes an actual transaction with the utility- an

inquiry, an order, a request for service, payment, etc. Look-up= customer accesses a self-service channel, typically IVR or Web,

to view general information about the company or view Customer Service information about their account but does not transact or conduct a transaction

◼ If you have activities that represent a “look-up”, please place them in the General Company Information category. These should go in either the Web or IVR category

◼ What should not count as a transaction by transaction category: Simple Web “hits” where the customer may hit the web site (and you capture

it) but there is no transaction or you don’t know the reason for the activity Accessing the IVR but then opting out to a CSR or Agent before completing

a transaction (the Agent live contact is a transaction, the initial IVR entry and opt out is not)

Do not count uncompleted transactions in the IVR or web, or simply accessing these channels for information as completed transactions in a specific transaction category in CT305 other than “General Company Information” (for lookups)

Outbound Contact Volumes

60

Self Service & Integration

61

Self-Service Background

◼ As part of the core questionnaire, we want to survey Self-Service Channels and innovative ways companies and customers are interacting with one-another.

◼ As companies evolve these solutions, greater levels of integration are required among and between key systems.

◼ We are interested in investigating and understanding the integration between the CIS (Customer Information System) and self-service mechanisms (including both company generated and customer generated communications) These include: IVR, Web and other self-service options or other newly expanding

means such as social networking. Areas covered include outage notifications, service appointments, and

collections

62

Self Service Integration with the CIS

63

Self-service interaction: much of what we ask about in self-service includes IVR, Web, E-mail, Fax, Kiosk etc., and we add “social networking” and outbound/ informational communications that allow for self-service and customer information

Outbound (proactive) contacts: build upon existing outbound data and information captured currently to understand:o What companies are doing to innovatively reach

customers using outbound (calling, text, email programs, appointment scheduling/confirmation etc.)

CIS Integration: Some focus on how Line of Business applications (trouble, credit, etc) above are integrated with the CIS for better (effective, efficient, responsive) service delivery

Social networking:o Which sites are being used for

what activitieso Plans for expansion or addition,

integration with other key systemso Impact on other channelso Costs associated (mainly in terms

of staffing, technology)o Success storieso “Social Media in the Contact

Center”

Topic Areas for Self-Service Channels

◼ Self-Assessment

◼ Self Service Tracking

◼ Transactions processing capability

◼ Social Media usage

◼ Customer self-service integration efforts (excluding social networking)

◼ Outbound service and communications (Credit, Outage, Appointment

◼ Mobile applications

64

Seeking to understand how your company measures self-service completion

65

Questions SS5 through SS13 seek to understand what your company counts as a “completed transaction” for self service.

We also would like to understand what information about these transactions and the customer’s experience in the self service channels is tracked

Billing

66

2015 CS Benchmark Questionnaire structure

67

CS Support and CS IT

Customer Contact• Contact Center• Local Office• Self Service• Contractors• Credit Inbound calls

Back Office• Billing• Billing Field Policies• Payment Processing

Field Service• Change of Account• Billing Field Orders

(meter investigations)

• Credit Field Orders• Order Management

Meter Reading• Manual• Mobile AMR• Fixed Network AMI

Revenue Management• Credit Office and

Outbound calls• Credit Field and Inbound

Contact Policies• Revenue Protection:

Office and Field

Customer Life-cycle: Meter Set to Cash Measures, Policies & Processes

Employees: Safety, Staffing

Customer: Customer Satisfaction, First Contact Resolution, Customer Experience, Key Account Management

Areas excluded:◼ Energy Audit/Energy

Efficiency Group◼ Meter Change-out

68

Technology- Billing

NOTE: CIS is a separate category

Technology Any technology specifically used for a function such as meter reading devices, mobile data technology, telephone switch or call routing software, call monitoring software etc.

Contact Center:◼ IVR (Interactive Voice Response)◼ ACD (Automatic Call Distributor)◼ Scheduling Software◼ Workforce Management (WFM)◼ Multi-channel processing◼ Web, Social Media technology costs◼ VOIP (Voice Over Internet Protocol)◼ Web/email routers◼ Virtual Hold technology costs◼ 3rd party applications (OMS interface etc.)

Field:◼ Mobile data (software and hardware)◼ Scheduling◼ GPS (Global Positioning System)◼ Telecommunications◼ Routing software◼ Dispatching software

Revenue Protection◼ Tamper plug◼ Data mining software

Meter:◼ Handhelds◼ Routing software◼ Telecommunications◼ Remote disconnect◼ MV 90◼ GPS (Global Positioning System)

Bills:◼ Inserters◼ Web/email, bill presentment◼ C/I billing software

Payment:◼ Image processer◼ Slitter/sorter◼ Interface w/kiosks◼ Routing software for off-site payments◼ Payment Kiosks

Credit:◼ Behavioral scoring◼ Predictive dialer◼ Credit optimization software

Subject Areas for Billing

◼ Bill Volumes and Types◼ Accuracy

Exceptions Errors Meter Reading Errors

◼ Billing Investigation◼ Estimating◼ Efficiency and Measurement◼ Outsourcing◼ Initiatives◼ Complexity/Deregulated Billing

69

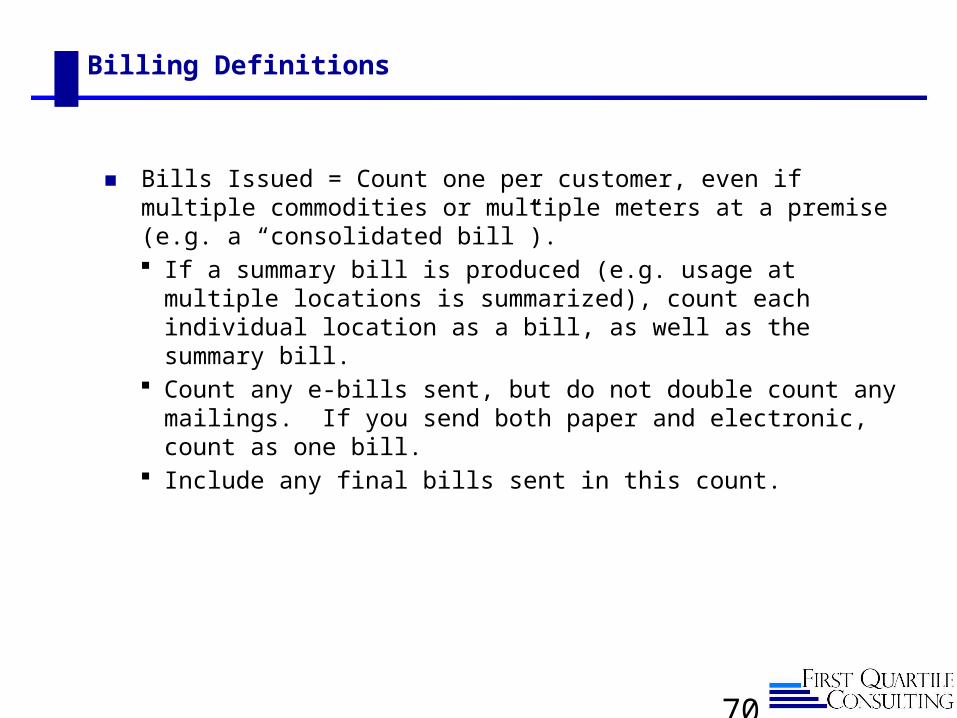

Billing Definitions

◼ Bills Issued = Count one per customer, even if multiple commodities or multiple meters at a premise (e.g. a “consolidated bill”). If a summary bill is produced (e.g. usage at multiple locations is

summarized), count each individual location as a bill, as well as the summary bill.

Count any e-bills sent, but do not double count any mailings. If you send both paper and electronic, count as one bill.

Include any final bills sent in this count.

70

When do “Billing Exceptions” and “billing Errors” Occur

◼ The general rule for Billing Exceptions that we are using is that:

Billing exceptions occur BEFORE the bill is sent to the customer.

Billing exceptions can be flagged during manual review or pre-bill edit or any other means of checking or auditing prior to sending the bill to the customer. Typically these are bills where the reading has failed some sort of hi-low parameter check or manual/automate billing review parameter

◼ The general rule for Billing Errors that we are using is that:

Billing errors occur AFTER the bill is sent to the customer

Billing errors can be identified by the customer or by the company

An error can result in an adjustment (e.g. cancel/rebill) or no adjustment/correction to a bill. A bill does not have to be adjusted to be a considered an erroneous bill.

71

ReviewPrinted

BillException

Report Review

Bill

Mai

led

Billing Exceptions Billing Errors

Billing Definitions

◼ “Meter reading error” is an incorrect actual meter read by a company representative or incorrect remote meter read (such as AMR or AMI)

◼ There are 3 places where a meter reading error can normally be found: Automated (software) check in the meter reading software (MV90 etc. when the

route is completed) Pre-bill review by Billing (after passing from meter reading) Post-bill identified by customer and upon review (field or office investigation)

determined to be a meter reading error.

72

Billing Volume

73

This question provides the key information to know how many bills of each type were issued. It is used in determining % of electronic bills, as well as billing costs per bill.

BL5 How many bills did you issue through each channel?

When sending both paper and e-bill, count paper bill only. Bills counted as being via Internet or E-mail should be "paperless".

Via paper only Via paper & posted on internet Via paper & sent through e-mail

paperless

Via internet only [customer must look up info, include here even if a reminder e-mail is sent] Via e-mail only [customer gets billing information via email, doesn’t have to visit web-site to view their bill] Via EDI, XML or other electronic billing source Total 0

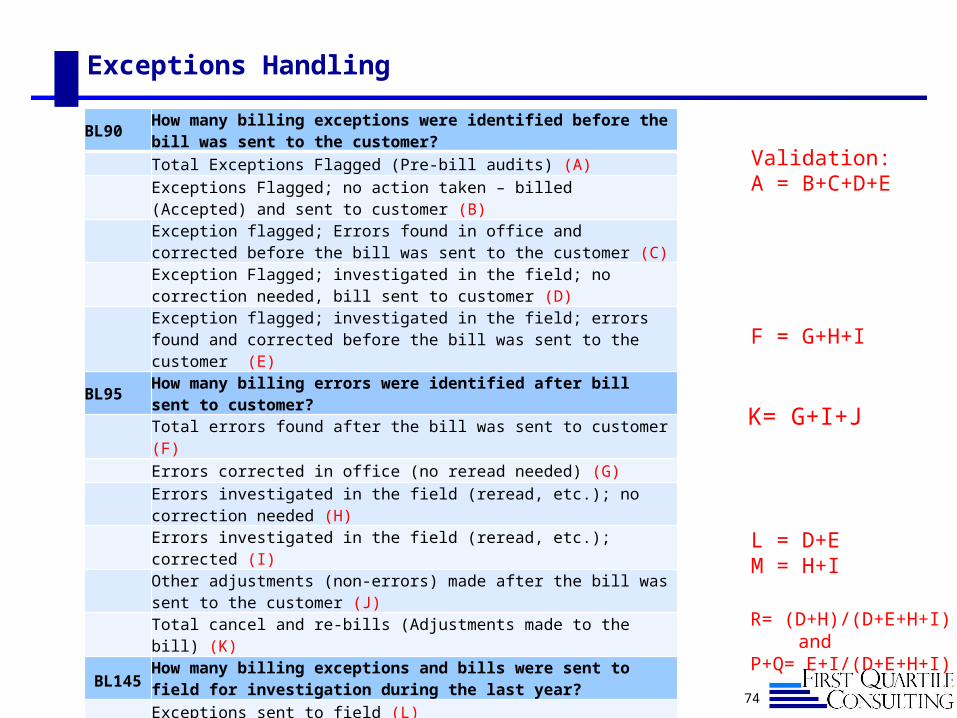

Exceptions Handling

BL90How many billing exceptions were identified before the bill was sent to the customer?Total Exceptions Flagged (Pre-bill audits) (A)Exceptions Flagged; no action taken – billed (Accepted) and sent to customer (B)Exception flagged; Errors found in office and corrected before the bill was sent to the customer (C)Exception Flagged; investigated in the field; no correction needed, bill sent to customer (D)Exception flagged; investigated in the field; errors found and corrected before the bill was sent to the customer (E)

BL95 How many billing errors were identified after bill sent to customer?

Total errors found after the bill was sent to customer (F)

Errors corrected in office (no reread needed) (G)

Errors investigated in the field (reread, etc.); no correction needed (H)

Errors investigated in the field (reread, etc.); corrected (I)Other adjustments (non-errors) made after the bill was sent to the customer (J)Total cancel and re-bills (Adjustments made to the bill) (K)

BL145

How many billing exceptions and bills were sent to field for investigation during the last year?

Exceptions sent to field (L)

Errors sent to field (M)

FS42What percentage of fielded billing exceptions and billing errors resulted in identification of … (N)Meter reading error (P)

Meter problem (Q)

No problem found (R) 74

Validation:A = B+C+D+E

F = G+H+I

L = D+EM = H+I

K= G+I+J

R= (D+H)/(D+E+H+I) andP+Q= E+I/(D+E+H+I)

Payment Processing

75

Subject Areas for Payment Processing

◼ Payment Volumes and Types Payment volumes and channels as delivered by the customer Payment volumes and channels as received

◼ Electronic Payments◼ Payment Agencies ◼ Accuracy/Timeliness

Efficiency Productivity Posting/timeliness

76

77

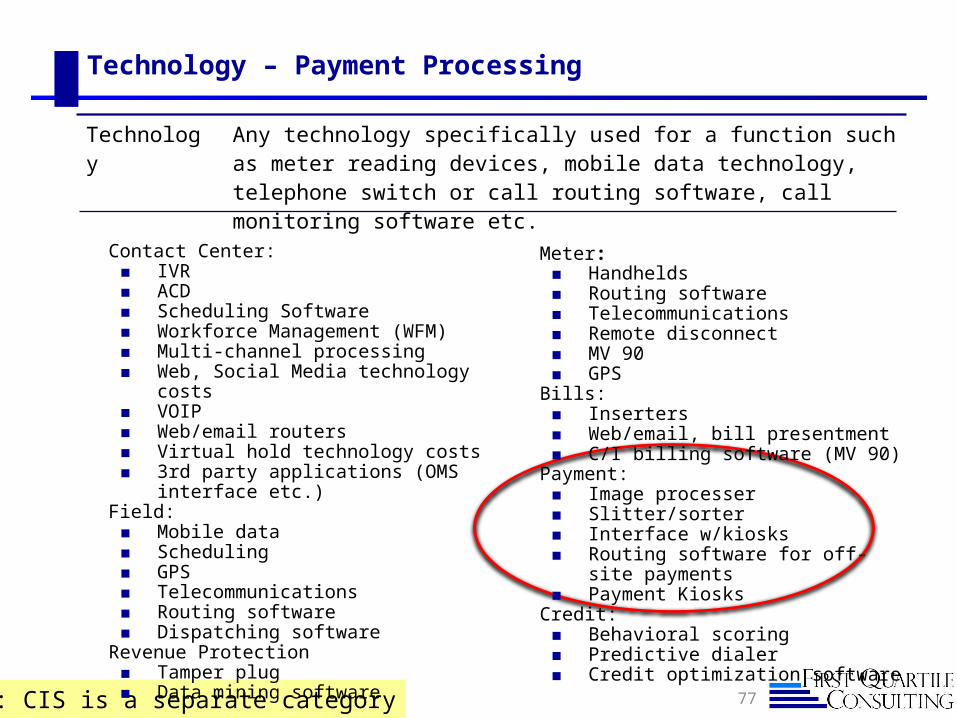

Technology – Payment Processing

NOTE: CIS is a separate category

Technology Any technology specifically used for a function such as meter reading devices, mobile data technology, telephone switch or call routing software, call monitoring software etc.

Contact Center:◼ IVR◼ ACD◼ Scheduling Software◼ Workforce Management (WFM)◼ Multi-channel processing◼ Web, Social Media technology costs◼ VOIP◼ Web/email routers◼ Virtual hold technology costs◼ 3rd party applications (OMS interface etc.)

Field:◼ Mobile data◼ Scheduling◼ GPS◼ Telecommunications◼ Routing software◼ Dispatching software

Revenue Protection◼ Tamper plug◼ Data mining software

Meter:◼ Handhelds◼ Routing software◼ Telecommunications◼ Remote disconnect◼ MV 90◼ GPS

Bills:◼ Inserters◼ Web/email, bill presentment◼ C/I billing software (MV 90)

Payment:◼ Image processer◼ Slitter/sorter◼ Interface w/kiosks◼ Routing software for off-site payments◼ Payment Kiosks

Credit:◼ Behavioral scoring◼ Predictive dialer◼ Credit optimization software

Payment Processing Definitions

Transactions◼ Payment = Payments processed should roughly equal bills issued. One

check for multiple bills counts as multiple payments. Multiple payments for one bill counts as multiple payments.

◼ Include all payments whether sent via mail, paid in local office, payment agency or pay station, paid on-line or through IVR or call center, or collected in the field.

Performance Measures◼ Payments that have been posted accurately to the right accounts as a

percent of all payments

Other◼ Payment locations = Payment agencies; local offices, pay stations ◼ Cashiers in local offices should be included with this function since their

primary function is to take payments. Other local office reps who handle activities in addition to taking payments are part of the contact center.

◼ Energy Assistance: payments might be processed by another agency or group. 3rd-party is paying on behalf of customer; agency accepts payment, uses other funds and processes it into the utility. Generally, put in "3rd Party"

78

Payment Processing Costs

◼ Transaction Fees (payment related – per payment fees) when paid by utility include: credit card transactions bank charges (checking account) Fees associated payment agencies Fees associated kiosk

◼ 3rd Party Contractor includes: Lockbox service Wholesale processing of payments

◼ Fees associated with payments (even if a call or a local office) still go in Payment.

79

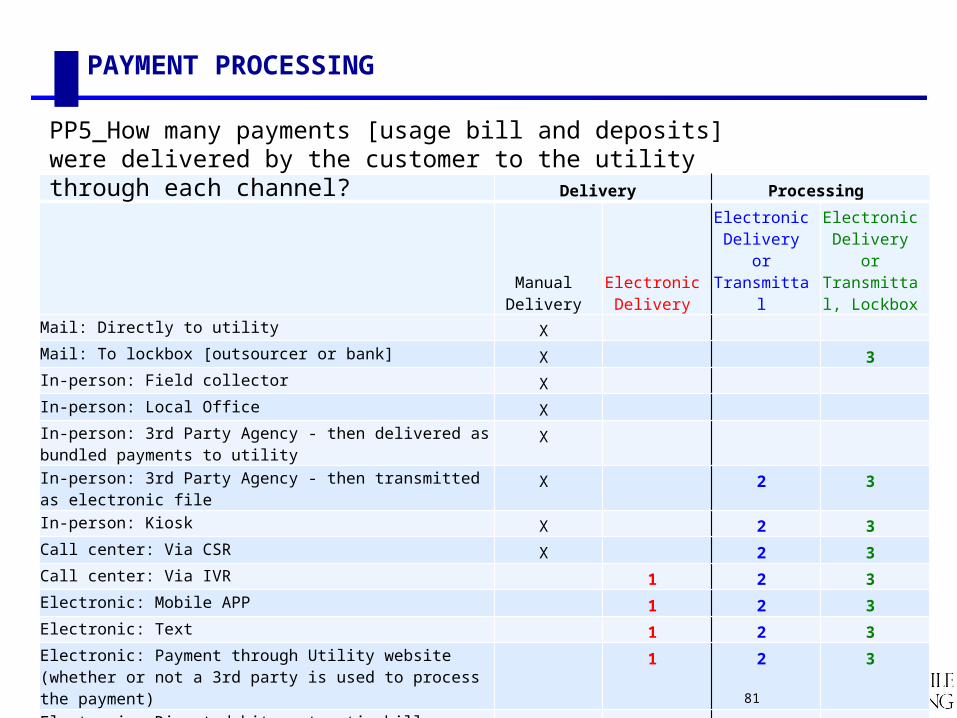

Payment Channels & Options

◼ We ask you to provide information on payments both by channel and option.

◼ We also capture information in both the Contact Center (CT305) and Payment (PP5) areas about payments received. Be sure that data is reported in all areas.

◼ If a customer is transferred to a third party to make their credit card payment, we still want to track where they started (CSR, IVR, Web) not where the ended (3rd party). We’re tracking how they intended to deliver the payment, not how you processed it.

80

In some cases, customers opt out of a transaction before it’s completed. So your call center considers it a payment call, but payment didn’t receive the payment. So numbers may not match.

PAYMENT PROCESSING

Delivery Processing

Manual Delivery

Electronic Delivery

Electronic Delivery or Transmittal

Electronic Delivery or Transmittal,

LockboxMail: Directly to utility XMail: To lockbox [outsourcer or bank] X 3In-person: Field collector XIn-person: Local Office XIn-person: 3rd Party Agency - then delivered as bundled payments to utility

X

In-person: 3rd Party Agency - then transmitted as electronic file X 2 3In-person: Kiosk X 2 3Call center: Via CSR X 2 3Call center: Via IVR 1 2 3Electronic: Mobile APP 1 2 3Electronic: Text 1 2 3Electronic: Payment through Utility website (whether or not a 3rd party is used to process the payment)

1 2 3

Electronic: Direct debit, automatic bill pay, pre-authorized payment (you go get the money)

1 2 3

Electronic: Customer sends you the money via LIHEAP, ACH, EDI, CheckFree, Customer pays through their bank)

1 2 3

PP5_How many payments [usage bill and deposits] were delivered by the customer to the utility through each channel?

81

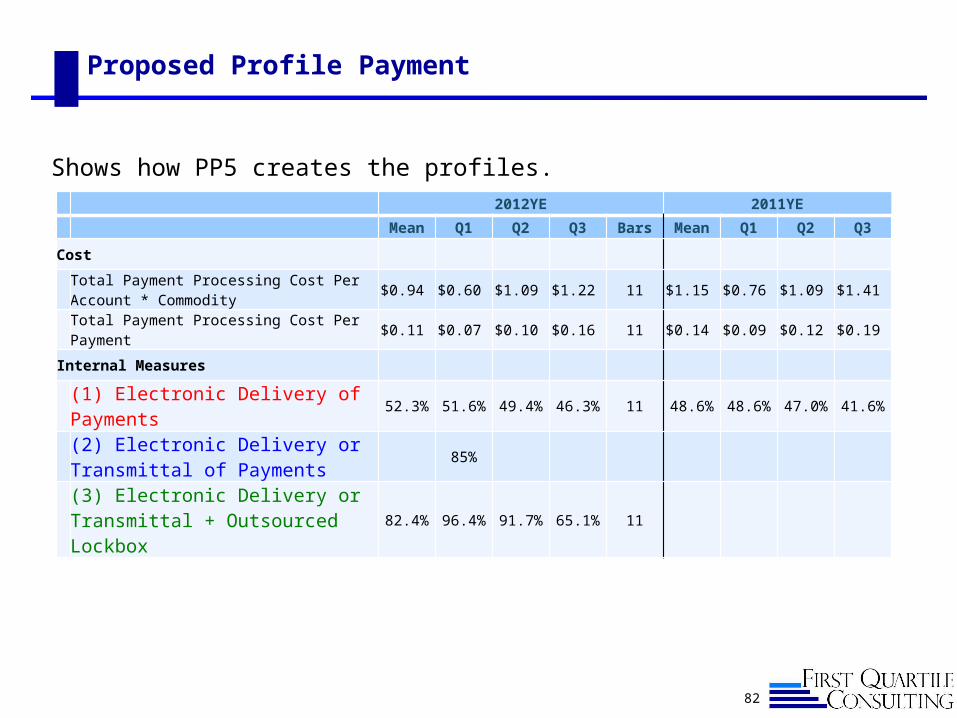

Proposed Profile Payment

82

2012YE 2011YE

Mean Q1 Q2 Q3 Bars Mean Q1 Q2 Q3

Cost

Total Payment Processing Cost Per Account * Commodity $0.94 $0.60 $1.09 $1.22 11 $1.15 $0.76 $1.09 $1.41

Total Payment Processing Cost Per Payment $0.11 $0.07 $0.10 $0.16 11 $0.14 $0.09 $0.12 $0.19

Internal Measures

(1) Electronic Delivery of Payments 52.3% 51.6% 49.4% 46.3% 11 48.6% 48.6% 47.0% 41.6%

(2) Electronic Delivery or Transmittal of Payments

85%

(3) Electronic Delivery or Transmittal + Outsourced Lockbox

82.4% 96.4% 91.7% 65.1% 11

Shows how PP5 creates the profiles.

Payment Delivery vs Processing

◼ Payment “delivered by the customer” How the customer makes the payment or delivers the payment, can be either 1)

manual or 2) electronic Any payment where there is an interaction with a person (In-Person 3rd party, CSR,

Field Collector, Agent, etc) regardless of how that payment is ultimately transmitted to the utility is considered manual.

Mailed payments are considered manual as are kiosk payments All other forms of delivery are considered electronic (e.g. IVR, Web, Direct Debit,

CheckFree, etc.)◼ Payment is “processed by the utility”

How the utility processes the payment it is receiving, can be either 1) manual or 2) electronic transmittal and delivery

Any payment where the processing has an associated manual activity–mailed, paid to a Collector, paid at the Local Office, bundled payment physically delivered to the utility, paid to a CSR over the phone– is considered manual

All other forms of processing are considered electronic transmittal and delivery (e.g. electronically transmitted 3rd party payment, IVR, Web, Direct Debit, CheckFree, etc.)

Lockbox payments are treated as a 3rd category and added to electronic as a separately reported measure

83

Field Service

84

2015 CS Benchmark Questionnaire structure

85

CS Support and CS IT

Customer Contact• Contact Center• Local Office• Self Service• Contractors• Credit Inbound calls

Back Office• Billing• Billing Field Policies• Payment Processing

Field Service• Change of Account• Billing Field Orders

(meter investigations)

• Credit Field Orders• Order Management

Meter Reading• Manual• Mobile AMR• Fixed Network AMI

Revenue Management• Credit Office and

Outbound calls• Credit Field and Inbound

Contact Policies• Revenue Protection:

Office and Field

Customer Life-cycle: Meter Set to Cash Measures, Policies & Processes

Employees: Safety, Staffing

Customer: Customer Satisfaction, First Contact Resolution, Customer Experience, Key Account Management

Areas excluded:◼ Energy Audit/Energy

Efficiency Group◼ Meter Change-out

86

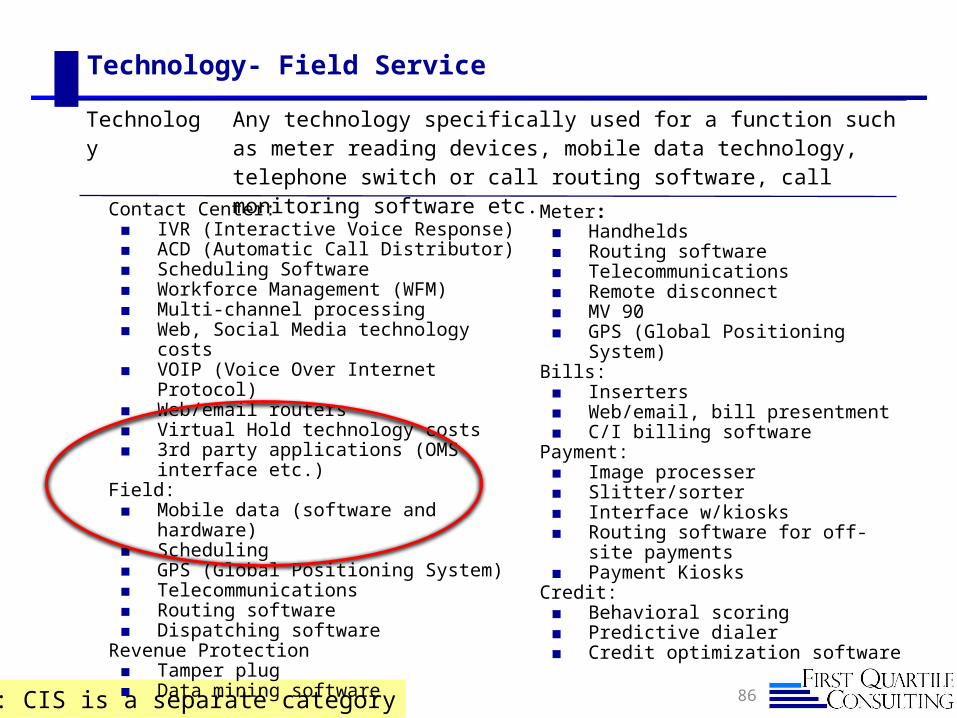

Technology- Field Service

NOTE: CIS is a separate category

Technology Any technology specifically used for a function such as meter reading devices, mobile data technology, telephone switch or call routing software, call monitoring software etc.

Contact Center:◼ IVR (Interactive Voice Response)◼ ACD (Automatic Call Distributor)◼ Scheduling Software◼ Workforce Management (WFM)◼ Multi-channel processing◼ Web, Social Media technology costs◼ VOIP (Voice Over Internet Protocol)◼ Web/email routers◼ Virtual Hold technology costs◼ 3rd party applications (OMS interface etc.)

Field:◼ Mobile data (software and hardware)◼ Scheduling◼ GPS (Global Positioning System)◼ Telecommunications◼ Routing software◼ Dispatching software

Revenue Protection◼ Tamper plug◼ Data mining software

Meter:◼ Handhelds◼ Routing software◼ Telecommunications◼ Remote disconnect◼ MV 90◼ GPS (Global Positioning System)

Bills:◼ Inserters◼ Web/email, bill presentment◼ C/I billing software

Payment:◼ Image processer◼ Slitter/sorter◼ Interface w/kiosks◼ Routing software for off-site payments◼ Payment Kiosks

Credit:◼ Behavioral scoring◼ Predictive dialer◼ Credit optimization software

Field Service Scope and Activities…2 parts

Field Service Orders◼ Field Service focuses on activity at the meter and includes (see detailed definitions

later): Billing-related activity Change of Account Field Credit activity

◼ Field Service policies have influence on activity costs Change of account estimating rules Hard vs. Soft Change of Account Credit policies AMI usage

◼ Even if these activities are performed in some other area of your company (e.g. meter electricians or line crews), we want them included in the Field Service section so that all companies are consistent.

Field Service Order Management ◼ Benchmark the process for getting short-cycle, customer-generated AND internally-

generated work to the field and completed

87

Field Service Definitions

◼ A completed field order is one where: the assigned activity has been performed. CGI or “Can't Get In” does not count as a completed order. A trip to a service location that involves multiple commodities (e.g. gas and electric change of

account) is considered as multiple trips. If multiple activities are performed at a location, count as only one trip.

Do not include orders that may have been received by the Field Services but not fielded. If an order is received but not undertaken in the field (e.g. a credit order that is allowed to expire or is “office-completed”), do not include this in the completed orders. We only want to include fielded orders in FS5.

◼ Types of orders: Billing-related activity – High bill investigation in the field, either customer or internally initiated,

check read, rereads, meter tests in conjunction with investigation, meter change out in conjunction with investigation, also includes a disconnection for meter that had been left on, has usage, but no customer.

Change of Account activity – new customer to service territory, customer moving within service territory; not greenfield site. Includes: Soft Connect/Disconnect (e.g. Read in or read out); Hard disconnect/reconnect (e.g. physically turn off service). Does not include a new meter set. Turn-on/turn-off for seasonal customers

Field Credit activity – Credit disconnections and reconnections, notice delivery, field collections

88

If you have an inactive meter that shows activity and you simply send a person to shut it off or

remove it – put that in Field ServiceDo not double count

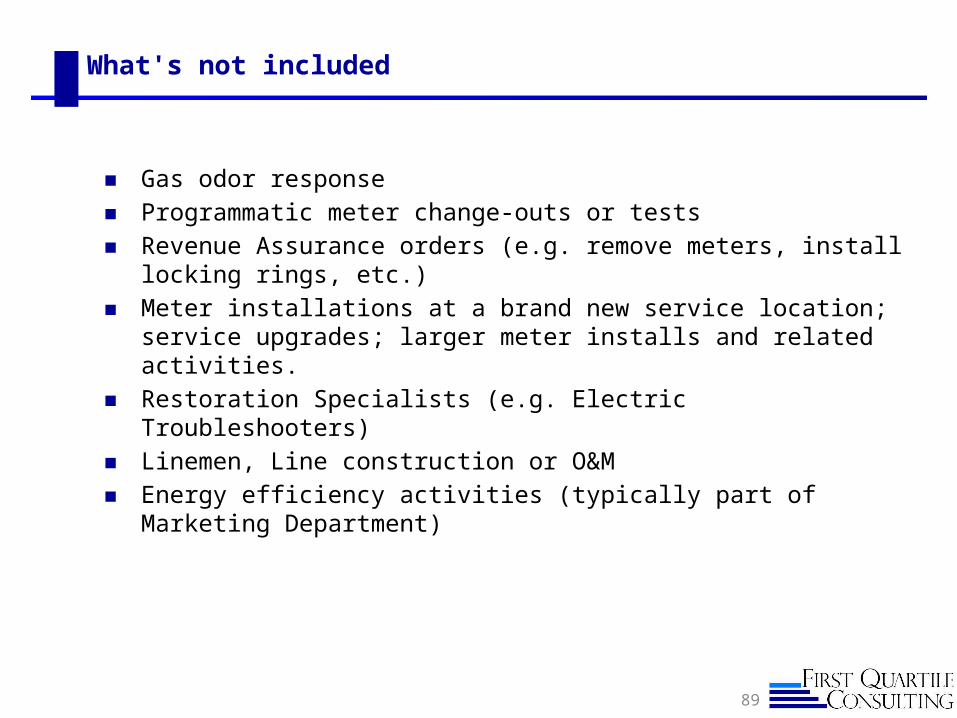

What's not included

◼ Gas odor response◼ Programmatic meter change-outs or tests◼ Revenue Assurance orders (e.g. remove meters, install locking rings,

etc.) ◼ Meter installations at a brand new service location; service upgrades;

larger meter installs and related activities.◼ Restoration Specialists (e.g. Electric Troubleshooters)◼ Linemen, Line construction or O&M◼ Energy efficiency activities (typically part of Marketing Department)

89

Field Service Order volumes

90

We ask for aggregate volumes, then some detail about each type of order, including handling approaches and policies

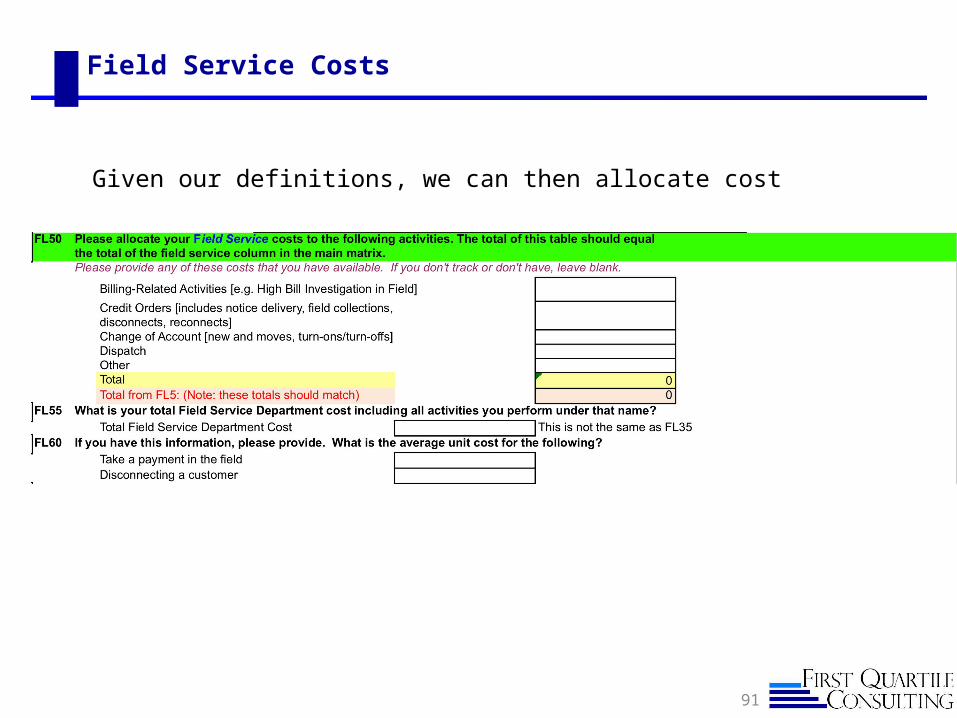

Field Service Costs

Given our definitions, we can then allocate cost

91

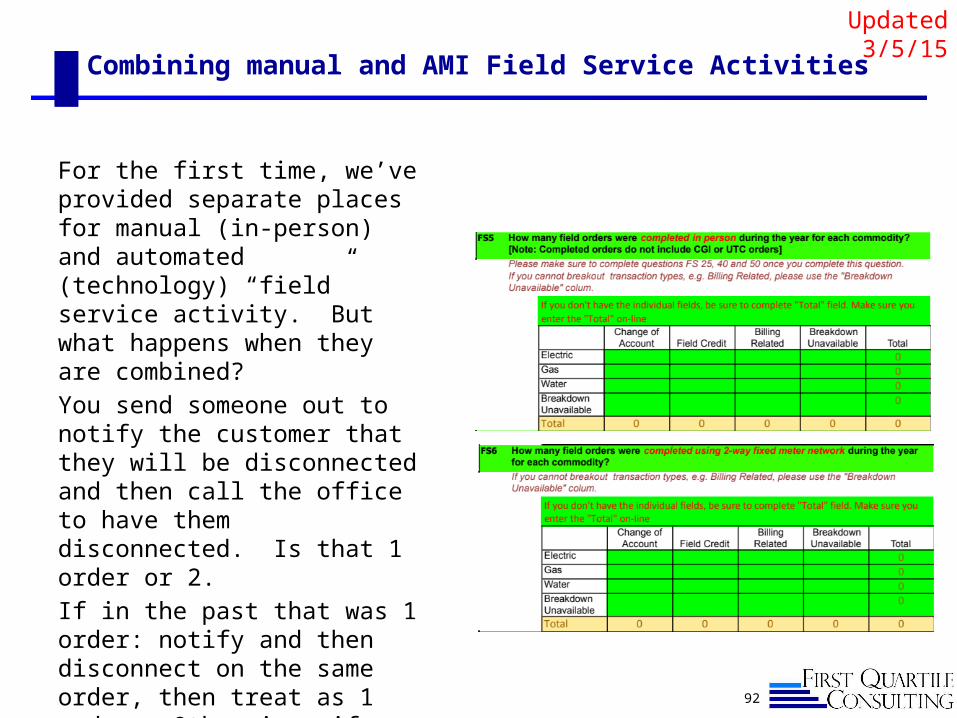

Combining manual and AMI Field Service Activities

For the first time, we’ve provided separate places for manual (in-person) and automated (technology) “field” service activity. But what happens when they are combined?

You send someone out to notify the customer that they will be disconnected and then call the office to have them disconnected. Is that 1 order or 2.

If in the past that was 1 order: notify and then disconnect on the same order, then treat as 1 order. Otherwise, if you’d notify one day and disconnect another day, that’s two orders.

92

Updated 3/5/15

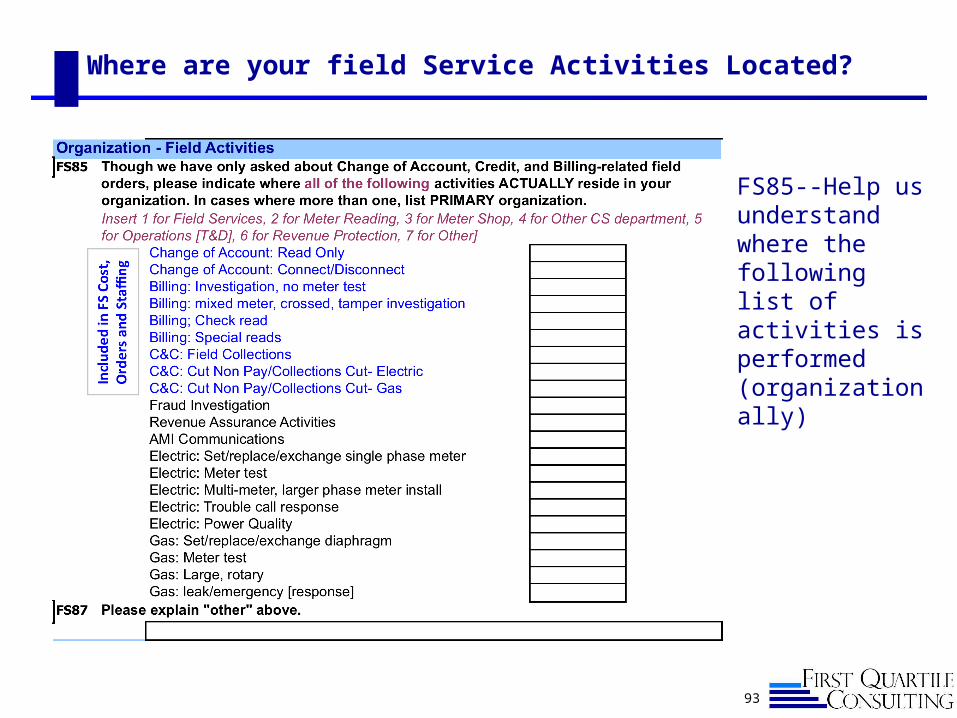

Where are your field Service Activities Located?

93

FS85--Help us understand where the following list of activities is performed (organizationally)

Field service Order Planning and Scheduling, Execution and Measures

The purpose of this section is to understand your process for getting short-cycle, customer-generated AND internally-generated work to the field and completed.

This includes the three specific field service activities (credit, billing investigations, and change of account) specified in previous pages.

Because of the widespread adoption of mobile data solutions for many field activities, we are also interested in how the scheduling process for these activities interacts with other activities you do in the field.

The following topics are covered in this year’s survey:

Field Service Initiatives Planning and Scheduling Field Order Execution and Supervision Measures (Field) and Reporting

94

Process Model:Field Service Order Management Process

95

Order Scheduling

Order Assignment

Order Issuance/ Dispatch

Order Handling/

Completion

• First step in the order management process as defined by 1QC.

• Simply scheduling- when, what time etc.

• Does not include the assignment of the order or the issuance or dispatch of the order

• Orders can be scheduled for example as:

• same day,• current (with a specific

date) or• future (known to be

scheduled for future time period but with out a specific date)

• Second step in the order management process

• The assignment of a scheduled order to a worker (or work group), geographic territory and skill set

• It does not include the issuance of the order to a worker and the workers tasks for a day or shift.

• Third step in the order management process

• The issuance of a scheduled and assigned order to a specific worker or work crew in the field.

• The best example of an issued order would be an order that is in the hands of the worker (or on his/her mobile device) to be handled and completed.

• 1QC uses issued and dispatched synonymously

• Last steps in the order management process.

• The worker handles the issued order and either completes it or updates the status if unable to complete (UTC, CGI etc.).

• The completion process includes documenting all the appropriate work information required to complete the order for field purposes

Meter Reading

96

2015 CS Benchmark Questionnaire structure

97

CS Support and CS IT

Customer Contact• Contact Center• Local Office• Self Service• Contractors• Credit Inbound calls

Back Office• Billing• Billing Field Policies• Payment Processing

Field Service• Change of Account• Billing Field Orders

(meter investigations)

• Credit Field Orders• Order Management

Meter Reading• Manual• Mobile AMR• Fixed Network AMI

Revenue Management• Credit Office and

Outbound calls• Credit Field and Inbound

Contact Policies• Revenue Protection:

Office and Field

Customer Life-cycle: Meter Set to Cash Measures, Policies & Processes

Employees: Safety, Staffing

Customer: Customer Satisfaction, First Contact Resolution, Customer Experience, Key Account Management

Areas excluded:◼ Energy Audit/Energy

Efficiency Group◼ Meter Change-out

Subject Areas for Meter Reading

◼ Volumes

◼ Service Levels

◼ Missed Reads

◼ Outsourcing

◼ AMI/AMR

98

Meter Reading Introduction

Meter Reading covers regular monthly ◼ Manual reads◼ Demand (MV-90) ◼ AMR: mobile read and 1-way fixed network◼ AMI: 2-way fixed network reads used primarily for billing purposes

Does not include ◼ Check reads, re-reads, etc., which are included in Field Service.

99

100

Technology- Meter Reading

NOTE: CIS is a separate category

Technology Any technology specifically used for a function such as meter reading devices, mobile data technology, telephone switch or call routing software, call monitoring software etc.

Contact Center:◼ IVR (Interactive Voice Response)◼ ACD (Automatic Call Distributor)◼ Scheduling Software◼ Workforce Management (WFM)◼ Multi-channel processing◼ Web, Social Media technology costs◼ VOIP (Voice Over Internet Protocol)◼ Web/email routers◼ Virtual Hold technology costs◼ 3rd party applications (OMS interface etc.)

Field:◼ Mobile data (software and hardware)◼ Scheduling◼ GPS (Global Positioning System)◼ Telecommunications◼ Routing software◼ Dispatching software

Revenue Protection◼ Tamper plug◼ Data mining software

Meter:◼ Handhelds◼ Routing software◼ Telecommunications◼ Remote disconnect◼ MV 90◼ GPS (Global Positioning System)

Bills:◼ Inserters◼ Web/email, bill presentment◼ C/I billing software

Payment:◼ Image processer◼ Slitter/sorter◼ Interface w/kiosks◼ Routing software for off-site payments◼ Payment Kiosks

Credit:◼ Behavioral scoring◼ Predictive dialer◼ Credit optimization software

Cost Allocations: Meter Reading

Meter Reading O&M cost allocation, please break out total meter reading costs by technology (FL40). This year we are also asking about your Smart Meter Capital Investment (FL45 and FL46)

101

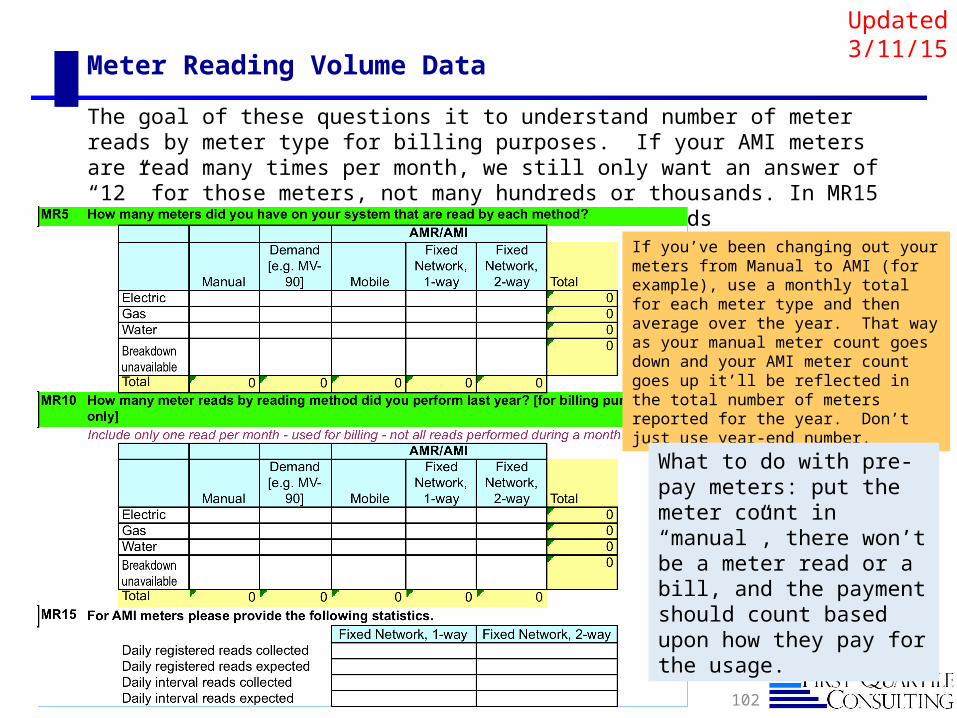

Meter Reading Volume Data

102

The goal of these questions it to understand number of meter reads by meter type for billing purposes. If your AMI meters are read many times per month, we still only want an answer of “12” for those meters, not many hundreds or thousands. In MR15 we do ask for daily registered and interval reads

If you’ve been changing out your meters from Manual to AMI (for example), use a monthly total for each meter type and then average over the year. That way as your manual meter count goes down and your AMI meter count goes up it’ll be reflected in the total number of meters reported for the year. Don’t just use year-end number.

Updated 3/11/15

What to do with pre-pay meters: put the meter count in “manual”, there won’t be a meter read or a bill, and the payment should count based upon how they pay for the usage.

Meter Reading Definitions

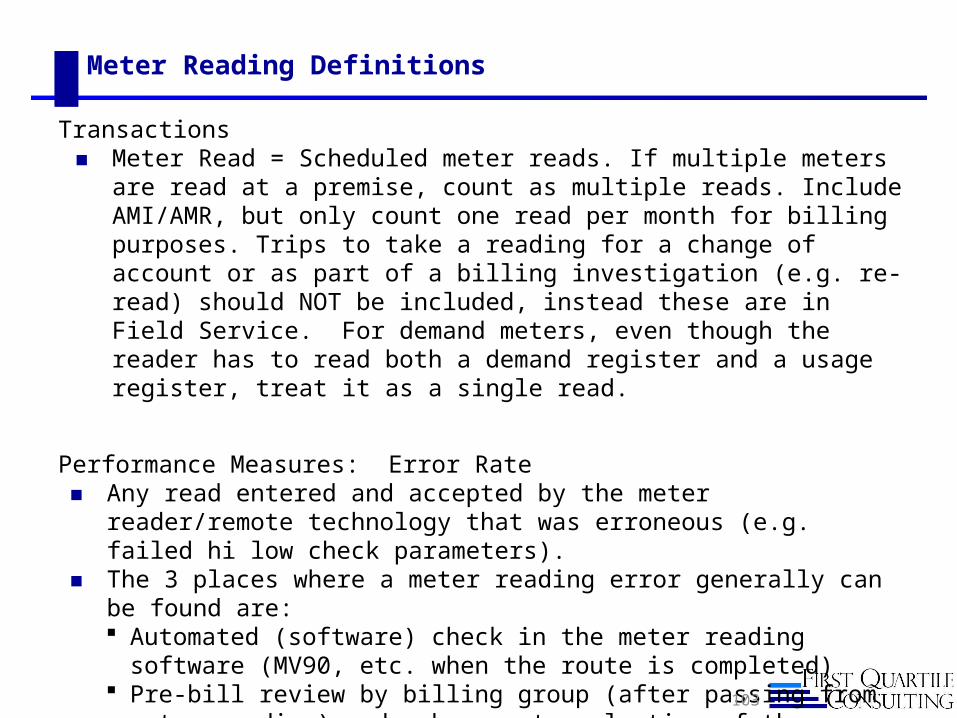

Transactions◼ Meter Read = Scheduled meter reads. If multiple meters are read at a

premise, count as multiple reads. Include AMI/AMR, but only count one read per month for billing purposes. Trips to take a reading for a change of account or as part of a billing investigation (e.g. re-read) should NOT be included, instead these are in Field Service. For demand meters, even though the reader has to read both a demand register and a usage register, treat it as a single read.

Performance Measures: Error Rate◼ Any read entered and accepted by the meter reader/remote technology that

was erroneous (e.g. failed hi low check parameters). ◼ The 3 places where a meter reading error generally can be found are:

Automated (software) check in the meter reading software (MV90, etc. when the route is completed)

Pre-bill review by billing group (after passing from meter reading) and subsequent evaluation of the exception

Post-bill identified by customer and upon review (field or office investigation) determine meter reading error

◼ Missed or skipped reads don’t count as errors.103

Credit & Collections

104

2015 CS Benchmark Questionnaire structure

105

CS Support and CS IT

Customer Contact• Contact Center• Local Office• Self Service• Contractors• Credit Inbound calls

Back Office• Billing• Billing Field Policies• Payment Processing

Field Service• Change of Account• Billing Field Orders

(meter investigations)

• Credit Field Orders• Order Management

Meter Reading• Manual• Mobile AMR• Fixed Network AMI

Revenue Management• Credit Office and

Outbound calls• Credit Field and Inbound

Contact Policies• Revenue Protection:

Office and Field

Customer Life-cycle: Meter Set to Cash Measures, Policies & Processes

Employees: Safety, Staffing

Customer: Customer Satisfaction, First Contact Resolution, Customer Experience, Key Account Management

Areas excluded:◼ Energy Audit/Energy

Efficiency Group◼ Meter Change-out

Sections in the Credit questionnaire

Overall Results – Delinquencies Transaction Volumes Process Management Regulatory Environment Process Steps

Account Initiation Active Account Management Collection Actions Final Account Management

Supplier Credit Technology

106

107

Process Model -- Key Areas of Credit & Collections

Note: Process includes Residential and C&I segments

Account Initiation

Active Account Management

Collection Actions

Final Account Management

Customer Assistance Programs

• Credit Scoring• Deposit

Requirements• Positive ID • Customer

Information Collection

• Fraud Prevention• Past due Amounts• Service Denial• C/I initiation

• Deposit Review• Behavioral Scoring• Contact Center

Policies• Customer

Segmentation• C/I Analysis• Late payment fees • Landlord

Agreements• Special Accounts• Record maintenance• Final Bills*• Vacant Properties

• Notices• Payment

Arrangements• Outbound calling• Field collections*• Field termination

(cut-out) *• Restoration of

service (cut-in) *• Sheriffs

Warrants/Legal• Bankruptcy/

Judgments• C/I Collections• Supplier Collections

• Final Billing*• Write-off• Skip-Tracing• Collection Agency

Operations• Reporting to Credit

Bureaus/ National Information Exchanges

• Low Income Assistance Programs

• Li-HEAP Programs• DSS/ State• Other Grants• Notification to DSS

of Pending Termination

• $ Minimums• Community

Outreach

Involved/Affected Organizations – Credit, Call Center, Accounts Processing, Field/Meter Services

Process Management – Performance measurement & reporting, organization structure, staffing & resources, effectiveness measurement of individual actions, write-off forecasting, optimization modeling

Regulatory Environment – RULES

* Not included in Credit Office Costs

Updated 3/11/15

Guidelines - Credit Office Activity

◼ Notices issued, determination of disconnections and reconnections, payment arrangements when handled in the credit area (separate from contact center), outbound calls, policy development and execution

◼ Include any collection agency, skip trace, positive ID, etc. in contracted services (basically a company that you pay monthly no matter the amount of activity)

◼ Include credit scoring transaction fees (when payment is based upon the amount of activity)

◼ Only include credit postage if a separate credit mailing, otherwise put in billing.

◼ Include outbound credit calls, which are calls made by the company (or contractors) to remind customers to pay their overdue bills, make payment arrangements, etc.

◼ Bankruptcy

◼ Customer Assistance

108

What's included:

Updated 3/5/15

Guidelines - Credit Office Activity

What's excluded:

◼ Field activities (connect/disconnect for non-pay, notices, collections) should be included in Field Service

◼ Inbound credit calls belong in contact center

109

Total Cost of Credit & Collections

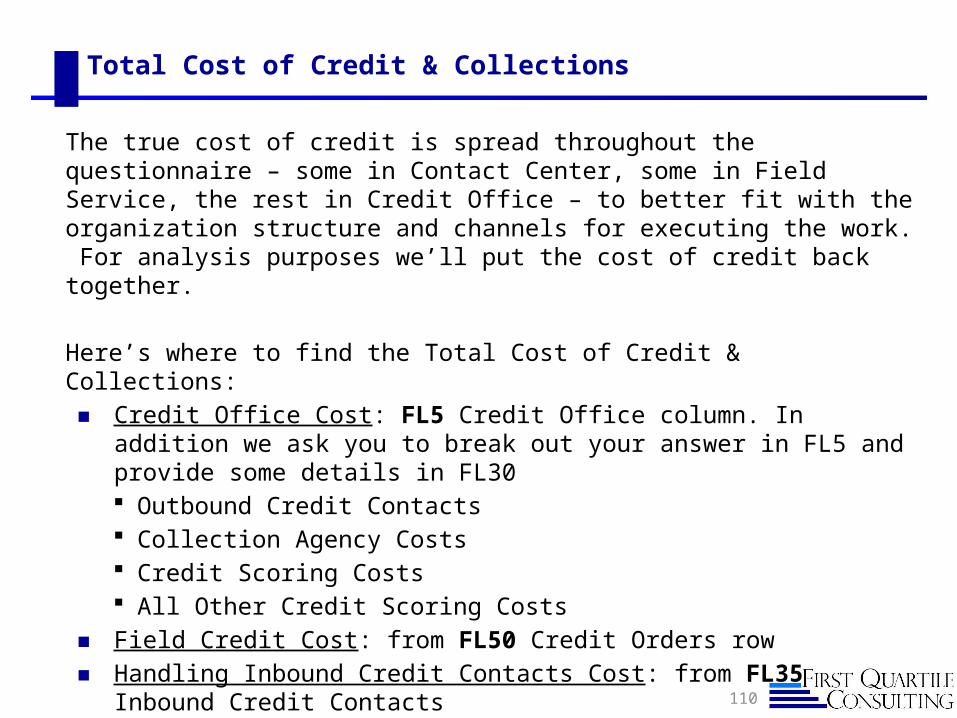

The true cost of credit is spread throughout the questionnaire – some in Contact Center, some in Field Service, the rest in Credit Office – to better fit with the organization structure and channels for executing the work. For analysis purposes we’ll put the cost of credit back together.

Here’s where to find the Total Cost of Credit & Collections:◼ Credit Office Cost: FL5 Credit Office column. In addition we ask you to

break out your answer in FL5 and provide some details in FL30 Outbound Credit Contacts Collection Agency Costs Credit Scoring Costs All Other Credit Scoring Costs

◼ Field Credit Cost: from FL50 Credit Orders row◼ Handling Inbound Credit Contacts Cost: from FL35 Inbound Credit Contacts

110

111

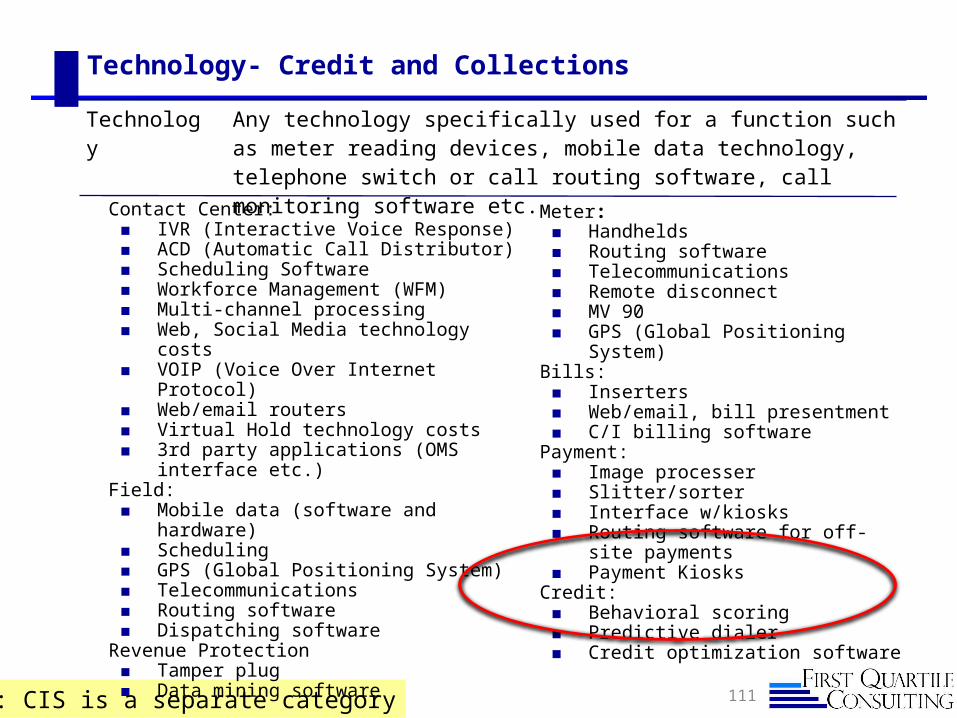

Technology- Credit and Collections

NOTE: CIS is a separate category

Technology Any technology specifically used for a function such as meter reading devices, mobile data technology, telephone switch or call routing software, call monitoring software etc.

Contact Center:◼ IVR (Interactive Voice Response)◼ ACD (Automatic Call Distributor)◼ Scheduling Software◼ Workforce Management (WFM)◼ Multi-channel processing◼ Web, Social Media technology costs◼ VOIP (Voice Over Internet Protocol)◼ Web/email routers◼ Virtual Hold technology costs◼ 3rd party applications (OMS interface etc.)

Field:◼ Mobile data (software and hardware)◼ Scheduling◼ GPS (Global Positioning System)◼ Telecommunications◼ Routing software◼ Dispatching software

Revenue Protection◼ Tamper plug◼ Data mining software

Meter:◼ Handhelds◼ Routing software◼ Telecommunications◼ Remote disconnect◼ MV 90◼ GPS (Global Positioning System)

Bills:◼ Inserters◼ Web/email, bill presentment◼ C/I billing software

Payment:◼ Image processer◼ Slitter/sorter◼ Interface w/kiosks◼ Routing software for off-site payments◼ Payment Kiosks

Credit:◼ Behavioral scoring◼ Predictive dialer◼ Credit optimization software

112

Write-offs

This question captures Revenue and Write-off information. Note the most important fields are highlighted in red. If you do not answer these, you will not appear on the Write-offs per Revenue graph.

Write-offs Percent = Net percent of total revenue written off (e.g. less any recoveries). Goal is the actual dollar amount written off during the year. This is not necessarily the same as “uncollectibles”, which is in the FERC 904 account for the year, since that can be affected by changes in the provision for bad debt during the year (FERC 144 account). Write-offs are the annual “net” cost of bad debt. In other words any recoveries (less fees) should be subtracted from gross write-offs.

A Couple of Key Credit Definitions

Performance Measure

◼ Write-offs Percent = Net percent of total revenue written off (e.g. less any recoveries). Goal is the actual dollar amount written off during the year. This is not necessarily the same as “uncollectibles”, which is in the FERC 904 account for the year, since that can be affected by changes in the provision for bad debt during the year (FERC 144 account). Write-offs are the annual “net” cost of bad debt. In other words any recoveries (less fees) should be subtracted from gross write-offs. **

◼ Percent Past Due 60 Days = Percent of accounts or receivables unpaid at 60 days. Note for most utilities this is balance due at second bill.

113

**Compare that to “Bad Debt” which is Uncollectable Expense plus the Year-On-Year Change in A/R Reserve

When does a customer/Bill become delinquent

We know that many companies count delinquencies differently. For some companies if a bill isn’t paid by day 31 (from when the bill is mailed) that bill will be 31 days past due. For another company, that bill will be 1 day past due. We want to try to get everyone to be consistent when reporting answers to questions CR5 and CR10.

114

Updated 3/11/15

Bill is mailed: Day 1

Bill is due: Day 15, Day

30

Bill is late: Day 16, 31

Bill is past due 30 days: day 46, 61

Bill is mailed: Day

1

Bill is late: day 31

Bill is past due 30 days:

day 61

CR10: % of customers

past due 30 days

What you track:

What we want:

=

Example: FERC 904 and 144 Validation

Performance Measure

◼ 1QC will perform some data validation checks to verify that the uncollectibles is determined correctly. In particular, the FERC 904 value should = Write-Offs – (change in FERC 144). An example can help:

Essentially, the uncollectibles value varies in the opposite direction of the change in the Allowance for Bad Debt (FERC 144)◼ In Example 1, the allowance isn’t changed from last year to this year, so

write-offs and uncollectibles are the same.◼ In Example 2, the allowance is increased from last year to this one, which

has the effect of reducing the uncollectibles value for the year.

115

Example 1 Example 2

144 Account (Last year, YE 2013) $100 $100

144 Account (Current year, YE 2014) $100 $120

Write-offs $115 $115

Uncollectibles (Acct 904) $115 $95

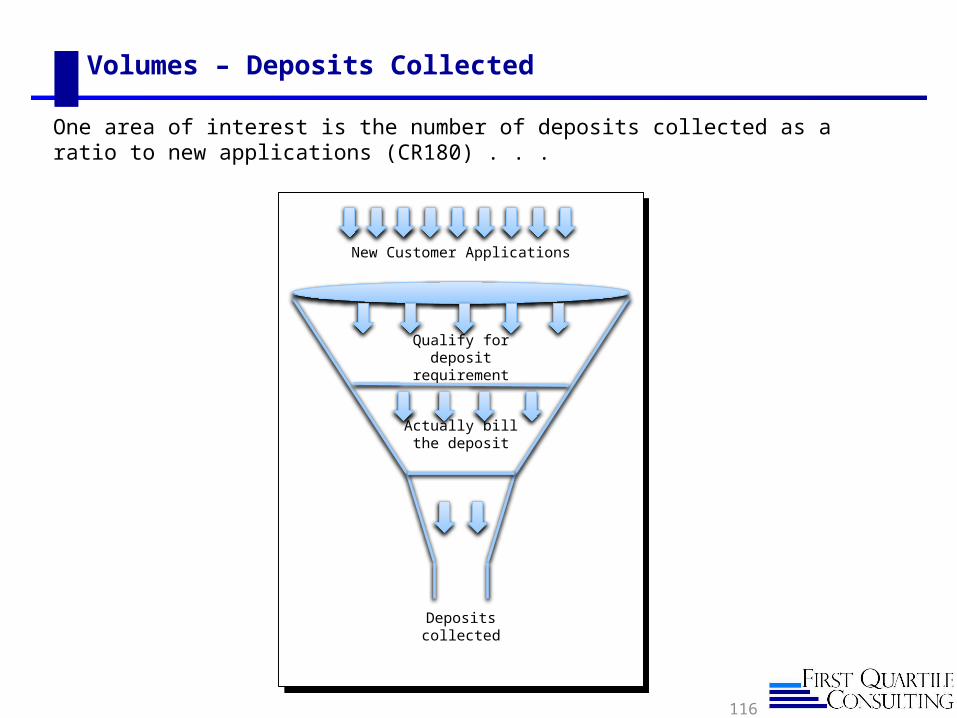

Volumes – Deposits Collected

One area of interest is the number of deposits collected as a ratio to new applications (CR180) . . .

116

New Customer Applications

Qualify for deposit requirement

Actually bill the deposit

Deposits collected

Revenue Protection

117

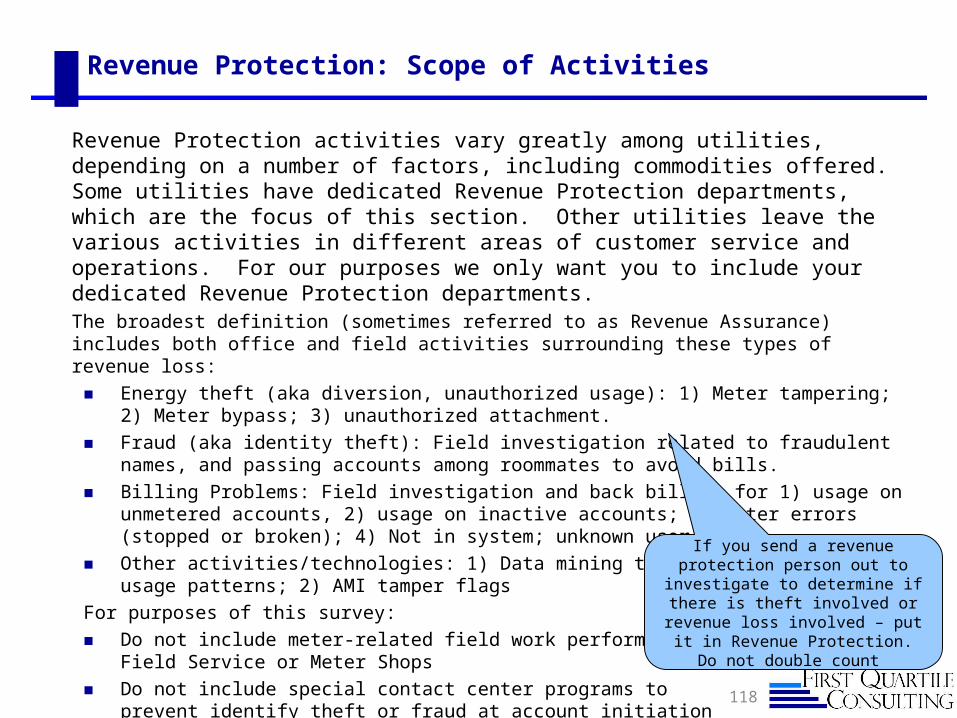

Revenue Protection: Scope of Activities

Revenue Protection activities vary greatly among utilities, depending on a number of factors, including commodities offered. Some utilities have dedicated Revenue Protection departments, which are the focus of this section. Other utilities leave the various activities in different areas of customer service and operations. For our purposes we only want you to include your dedicated Revenue Protection departments.The broadest definition (sometimes referred to as Revenue Assurance) includes both office and field activities surrounding these types of revenue loss: ◼ Energy theft (aka diversion, unauthorized usage): 1) Meter tampering; 2) Meter bypass; 3)

unauthorized attachment.◼ Fraud (aka identity theft): Field investigation related to fraudulent names, and passing accounts

among roommates to avoid bills.◼ Billing Problems: Field investigation and back billing for 1) usage on unmetered accounts, 2)

usage on inactive accounts; 3) Meter errors (stopped or broken); 4) Not in system; unknown user

◼ Other activities/technologies: 1) Data mining to identify suspicious usage patterns; 2) AMI tamper flags

For purposes of this survey: ◼ Do not include meter-related field work performed by

Field Service or Meter Shops◼ Do not include special contact center programs to

prevent identify theft or fraud at account initiation◼ Do not include routine billing investigations

118

If you send a revenue protection person out to investigate to

determine if there is theft involved or revenue loss involved – put it in

Revenue Protection.Do not double count

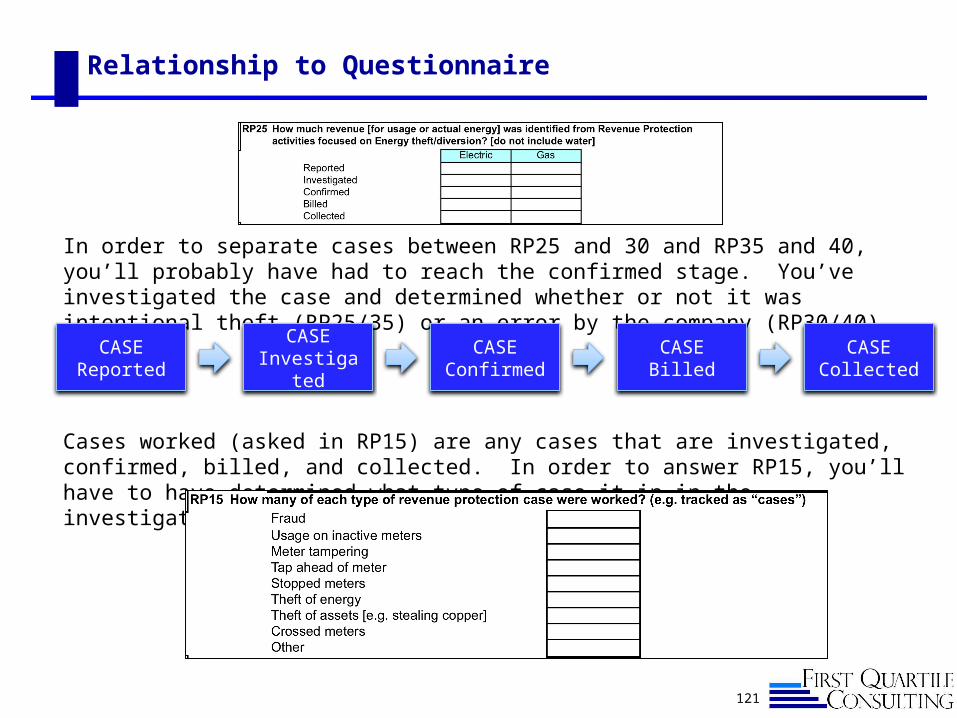

Revenue Protection: THE PROCESS Model

The process model is built on a series of individual steps through which each case must progress

◼ Reported: A reported issue (e.g. from Meter Reading, a hot line or data mining) is acknowledged and put in a backlog (perhaps identified as a “case”)

◼ Investigated: A revenue protection person reviews either in the office or in the field and identifies a course of action (probably identified as a “case”)

◼ Confirmed: The outcome of the investigation concludes there is usage that should have been paid for

◼ Billed: A bill is presented to the customer (almost always a “case”)◼ Collected: Customer pays (and the “case” is closed)

119

CASEInvestigated

CASEBilled

CASECollected

CASEReported

CASEConfirmed

Revenue Protection – the Iceberg Model

120

The amount of revenue collected only reflects the “tip of the iceberg” when it comes to energy theft and fraud.

Total Cases (unknown)

Cases Investigated