Page 1 CMA BHAVAN CIRCUIT A News Magazine from the Hyderabad Chapter of The Institute of Cost Accountants of India Monthly Journal Regd. APENG/2012/49672, Volume No. 4, Issue No. 11, April, 2017 Posting under registration No. L II / RNP / HD / 1181 / 2016-18 Date of Publication on 14-04-2017 & Date of Posting on 17-04-2017 1 Web: cmahyderabadchapter.in E-mail: [email protected]Ph: 040-27635937 | Telefax: 040-27607893 A view of Dignitaries present on the occasion of International Women’s Day Celebrations on “Global Corporate Trends – Women Leadership” on 08th March, 2017 at Institute of Public Enterprise, Osmania University. A view of dignitaries seen on the dais at a joint programme with ICAI and ICSI with the support of Ministry of Corporate Affairs on “Corporate Social Responsibility” on 30th March, 2017 at ni-msme, Yousufguda, Hyderabad

I n t e r n a t i o n a l Wo m e n ’s D ay C e l e b ra t i o n s

on “Global Corporate Trends – Women Leadership”

on 08th March, 2017 at Institute of Public Enterprise,

Osmania University.

A view of dignitaries seen on the dais

at a joint programme with ICAI and ICSI

with the support of Ministry of Corporate

Affairs on “Corporate Social Responsibility”

on 30th March, 2017 at ni -msme,

Yousufguda, Hyderabad

HYDERABAD CIRCUIT - APRIL, 2017

Page 2

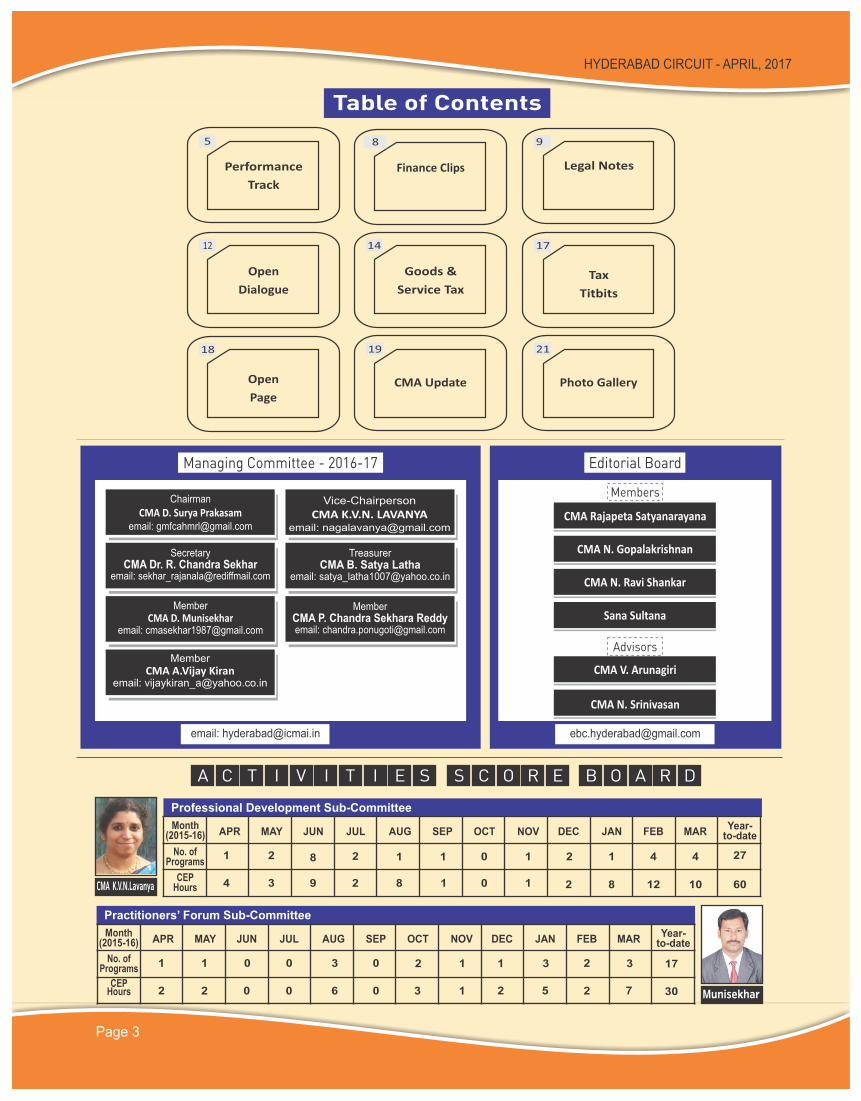

From the Edit Room...The Chairman writes to you

“Success is the result of perfection, hard work, learning from failure, loyalty, and persistence.”

- Colin Powell

Dear esteemed members,

I am delighted to inform you that as a first attempt of o u r C h a p t e r, w e c o n d u c t e d t w o w o m e n programmes on 08.03.2017 and 09.03.2017 to celebrate the International Women’s Day. Our President CMA Manas Kumar Thakur graced the occasion on 08.03.2017 held at IPE in the premises of Osmania University, a joint programme organised with IPE, ICSI, Institute of Directors and our Chapter. We have invited a panel of women speakers to deliberate on "Global Corporate Trends – Women Leadership". On 09.03.2017 we conducted another programme exclusively by our Chapter addressed by eminent speakers in different fields on topic "Women as Entrepreneurs and Directors".

We also conducted one programme on "Value Addition by CMA" addressed by our past president Sri M. Gopalakrishnan on 03.03.2017. He emphasised the need of the hour for our CMAs to create the requirement of our services to enhance their practice.

Our past central council member Sri.TCA Srinivasa Prasad addressed our members on 18.03.2017 on "Improving Productivity using Office Automation". He lucidly presented the techniques of using MS Office and Windows Explorer.

We had one programme on "Corporate Social Responsibility" on 30.03.2017 jointly organised by ICAI(CMA), ICAI and ICSI at the behest of ROC Hyderabad. Regional Director Sri S.B. Gautham, the chief guest for the programme, requested the three professional bodies to ensure the compliance of the CSR by the corporate sector as per the provisions of the Companies Act.

As mentioned in my previous communication, I am happy to inform you that the Chapter has conducted ten GST workshops for NMDC in different locations, one programme for BDL and another programme at HAL. The response from the corporate sector is encouraging and we are confident of doing more such programmes in the coming months.

GST implementation is inching towards reality after the consent obtained by the Central Government for the Central GST Bills by the both the houses of Parliament and it is waiting for President’s approval. In view of this development, we are planning to have one session in the second week of May to update our members on each topic in detail as mentioned in Central GST Acts. We are also planning to meet local commercial tax department officials for inclusion of Cost Accountants in line with Central GST acts to avoid any slippage.

On knowledge front I would like to bring to your notice that the Insolvency and Bankruptcy Board of India has issued regulations pertaining to the voluntary liquidation process for corporate persons. Corporate person for this purpose of regulation would include companies, limited liability partnerships and any other person incorporated with limited liability. The regulation came into effect from 01.04.2017, laid down the process from initiation of voluntary liquidation of corporate person till its dissolution.

Lastly, on behalf of our Managing committee members and myself, I wish all of you a good beginning to the new financial year 2017-18 with more opportunities in practice and advancement in career and best wishes for Sri Ram Navami, Hanuman Jayanti, Baisakhi and Good Friday.

CMAs to be more acceptable to the Industry needs to do constant study and observation in the place of work where employed. Further, constant professional updation to survive in the competitive scenario is also an essential requirement of CMAs are suggested by CMA M. Kameswara Rao the Past Chairman of our Chapter whose personal interview is published in this month’s Hyderabad Circuit.

Professionals to update on the new and changed regulations etc., relating to –Revised Trademark Rules , new IT Return Forms announced for the AY 2017-18,restrictions on cash transactions imposed by the IT wef 1st April, 2017, clarifications issued by CBDT on ICDs, simplified procedure for application of PAN & TAN, rules announced by the CBDT relating to online authentication of notices and documents, BSEs announcement of mandatory filing of Financial Reports in XBRL Mode only wef 1st April, 2017, partial withdrawal of exemptions under service tax to educational Institutions and the threshold limits notified by the Government for various Business combinations etc.,. Besides these, the other welcome features to be noted relate to renaming of CBEC as Central Board of Indirect Taxes & Customs (CBIC), accent of the President to Finance Bill 2017 received on 31.3.2017, Aadhaar prescribed as a must for pension s e t t l e m e n t , re d u c t i o n i n P F Administration charges & removal of administration charges on EDLI wef 1st Apri l , 2017, extension of maternity benefit to 26 weeks to women employees, increase in the Gratuity limit to Rs 20 lac and SEBI’s decision to adopt digital payments for all transactions with it.

We have covered our regular features and a special article on GST the most important Indirect tax legislation which may in all likelihood would be implemented from 1st July, 2017.

• 03rd March, a programme on “Value Addition by CMA” conducted at Hotel Vaishnaoi, Kachiguda Station Road, Hyderabad.

Speaker: CMA M. Gopalakrishnan, Past President, ICAI

CMA M. Gopalakrishnan elaborately discussed about the importance of performance appraisal report and how it carries the essence of a cost audit report. He explained that a CMA is bound to add value for the betterment of our profession. One may proceed to analysis by segregating sales into 80-20, going through the order to cash cycle and finding its significant processes, writing down the internal cost flow and finding out how it impacts the products etc. And also reiterated that the product cost cube has to be constructed such that it enables a slice and dice along the three axes. The program was attended by more than 40 CMAs.

• 04th March, a training programme on “Strategic Dimensions of Cost Accounting” held at Pendekanti Institute of Management, Ibrahimbagh, Gandipet, Hyderabad.

Speakers: CMA KVN. Lavanya, Vice Chairperson, CMA D. Zitendra Rao, Member, SIRC of ICAI and Smt. Sudha Murthy, Faculty.

After the inaugural, CMA Lavanya has explained with adequate examples the various pricing strategies and in the cost-competitive era, how firms like Walmart, KLM Airlines, the TATAs, Apple etc. have still retained their cost competitiveness. She had concluded with an Akbar and Birbal story on cutting costs in the manufacture of swords.

CMA Zitendra Rao has elaborated about the costing process, its impact on products and competition and how cost management may be used to stay ahead in the competitive world.

• GST Workshops - The Chapter has conducted workshops on GST at various locations as specified under. The Chapter has sourced eminent speakers for the workshops.

At Hindustan Aeronautics Limited (HAL) at Avionics Division, HAL Township, Balanagar on 04th March.

Speakers: CA M. Ramachandra Murthy, Practising Chartered Accountant, Sri S. Suresh Kumar, Superintendent, Central Excise, Customs & Service Tax.

At National Mineral Development Corporation (NMDC)

NMDC, with the help of the Institute of Cost Accountants of India – Hyderabad Chapter, has organized 2-day workshops on GST at different locations. They are conducted as under.

At Bharat Dynamics Limited (BDL) , Kanchanbagh , on 25th March.

Speakers: CA Bhupendra Agarwal, Tax head of Karvy Group and CA Radhika Verma, Partner, Indirect Taxes, Laxminivas & Co,.

• 08th March, International Women's Day celebration on "Global Corporate Trends - Women Leadership" in association with ICSI-Hyderabad Chapter, Institute of Directors and Institute of Public Enterprise at IPE, Osmania University.

A program titled "Global Corporate Trends - Women Leadership" was jointly held by ICAI - Hyderabad Chapter, ICSI-Hyderabad Chapter, Institute of Directors at the auditorium of the Institute of Public Enterprise on 8th March. This program witnessed CMA Manas Kumar Thakur, President ICAI, as the Chief Guest and CS Sheela, CS Rasheeda, CMA Manjula and Smt. Vinulata as the speakers. After the lamp lighting, the speakers have highlighted their points as to why there is dearth of women in leadership roles despite more number of women joining the middle management roles. The forum had aptly given the advantages for women in the top positions and how certain qualities of women are well-suited for them to achieve the corporate objectives.

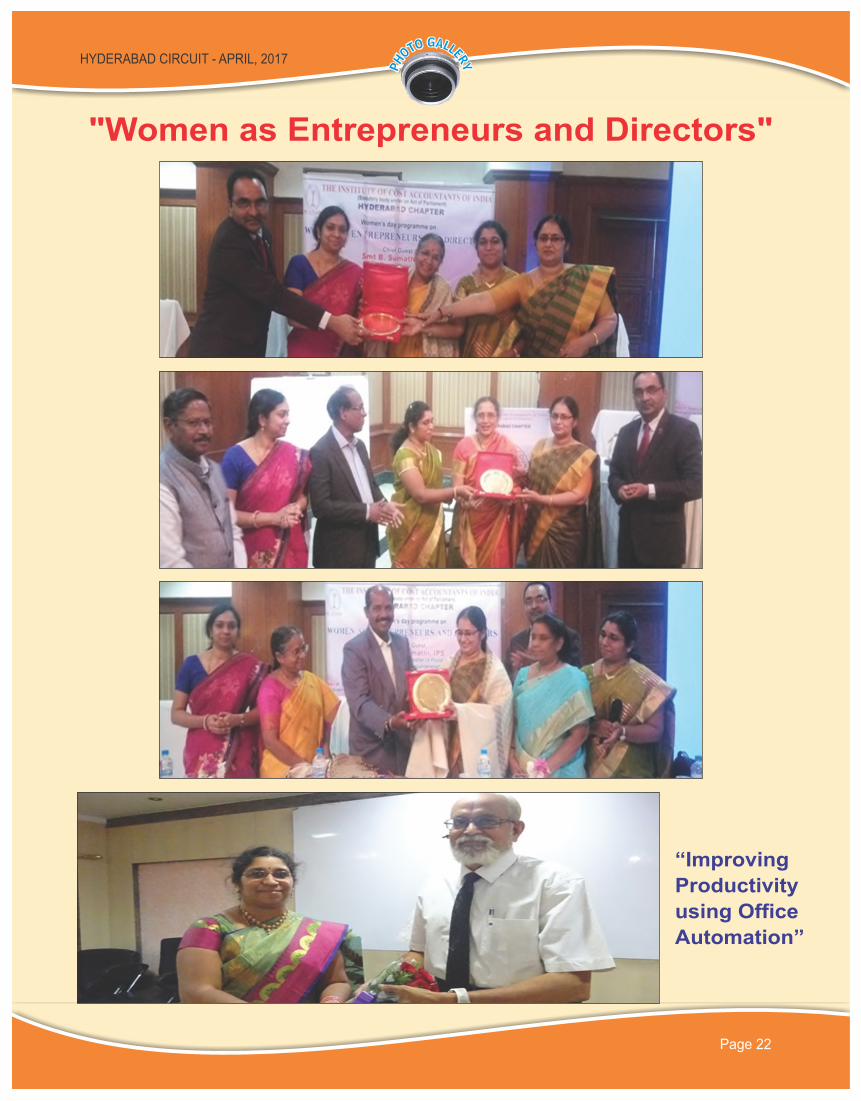

• 09th March, a Programme on "Women as Entrepreneurs and Directors" held at Hotel Katriya, Raj Bhavan Road, Hyderabad

Inviting the Deputy Commissioner of Police, North Zone, Smt. B. Sumathi as the Chief Guest and Smt. K. Ramadevi, President of ALEAP and Smt. Sujana Prabha, Vice-President of Vivekananda Seva Samithi of the Bharat Vikas Parishad, the Hyderabad Chapter celebrated its Women's day celebrations with the theme "Women as Entrepreneurs and Directors" on 9th March. This program has recognised and honoured the spouses of all the past Chairmen of the prestigious Chapter. The address of Smt. Ramadevi was very admiring and inspirational. She explained that the concepts of convincing nature, change, conviction, and commitment are very vital for a woman to be a successful entrepreneur. Smt. Sujana Prabha explained about the "Abhaya Bharathi" program that was started by the Bharat Vikas Parishad, and how a proper education of the general behaviour of girls and boys will prove quite beneficial to the society in eradicating the cases like "Nirbhaya". CMA Jyothi Satish, Treasurer, SIRC also added her inputs to the program. After the felicitation of the female partners of the past Chairmen and the guests, the program was concluded with a vote of thanks by CMA KVN Lavanya.

• 18th March, a programme on “Improving Productivity using Office Automation” held at CMA Bhavan, Himayatnagar, Hyderabad.

CMA Srinivasa Prasad has given certain tips for faster working with MS Office applications and the Windows explorer. These include setting the working directory, creating templates for documents like letters, using auto correcting options for replacing a repeated phrase with a small word (useful esp. in drafting contracts) etc. The program was well appreciated by the audience.

• 30th March, a joint programme with ICAI and ICSI with the support of Ministry of Corporate Affairs on “Corporate Social Responsibility”at ni-msme, Yousufguda, Hyderabad.

Speakers: Sri S.B. Gautham, Regional Director (Ser), MCA, CS S. Balachandra, Company Secretary in Practice, CA Ganesh Balakrishna and Sri N. Krishna Murthy, Registrar of Companies, AP & Telangana.

Speakers highlighted that the professional Insitutes, i.e CA, ICAI and ICSI shall prevail upon the corporate sector for compliance of CSR as per the provisions of the Companies Act.

After the inaugural session, CS Sunku Balachandra explained the need for CSR for a country like India and how actively corporates have to take in up for nation building. He gave an overview of the CSR provisions and rules as per the Companies Act, 2013.

HYDERABAD CIRCUIT - APRIL, 2017

Page 6

PRACTITIONERS' FORUM SUB-COMMITTEE

INVESTOR AWARENESS PROGRAMMES

• 30th March, interactive session on “Ind AS era-issues in Cost Audit” held at CMA Bhavan, Himayathnagar.

Moderator: CMA D. Zitendra Rao, Practising Cost Accountant

This is an initial discussion over the impact of IND AS, the new accounting standards for selected companies, on the cost audit report. A few areas identified include the standard for Employee Benefits, Provisions, etc. Further discussion sessions are planned so that any changes needed to the cost accounting standards may be suggested to the Institute.

• 24th March, Industrial visit to students to T.S Dairy Development Co-operative Federation Ltd., (Vijaya Dairy) at Tarnaka, Hyderabad.

The main purpose of industrial visit to this factory is to know the process of production, method of costing adapted, marketing structure, different types of products, etc. The factory officials clearly explained the production process and which has benefitted to the students with a practical perspective. This has provided a great experience for the students. This programme was attended by nearly 38 students from CMA inter and CMA Final students.

CMA Dr R. Chandra Sekhar, Secretary accompanied the students.

A press meet occurred on the occasion of the President, CMA Manas Kumar Thakur visiting Hyderabad. This was attended by both print media and electronic media. The President has detailed the need of CMAs to the society and how students will be benefitted by taking up the course. He has also highlighted that our Institute is committed to train more than 20 lakh assesses in the GST regime. He has also explained how a CMA can become an Insolvency Professional and be of help to the government and society as well. More than 10 regional newspapers have published about the press meet on 9th March.

F Unclaimed dividends: Government has prescribed revised Procedure for transferring shares against which dividend has not been paid or claimed for seven consecutive years. In cases where the period of seven years has been completed or being completed during the period from 7th September, 2016 to 31st May, 2017, the due date of transfer of such shares shall be deemed to be 31st May, 2017 and ford details refer to the Amendments made through Investor Education and Protection Fund Rules 2017 on sebi.gov.in

F Railway Accounts: ICAI Accounting Research Foundation (ICAI ARF) invites proposals from eligible Chartered Accountant Firms having preferably their Head Office at certain places to be associated for handling its upcoming project of Indian Railways for conversion of its books of accounts from hybrid to accrual accounting and for details refer to www.icai.org

F Revised General Financial Rules 2017: The Finance Minister Shri Arun Jaitley calls upon the Financial Advisers of different Ministries to ensure that expenditure on schemes and projects start from the beginning of the financial year to leverage the early passing of the Finance Bill this year; FM releases the Revised General Financial Rules (GFR) 2017 vide PIB dated 7th March, 2017.

F ICSI reaches 50000th membership: ICSI after 48 years of its coming into existence reached a Landmark of 50,000 members. Shri Arun Jaitley, Hon’ble Union Minister for Finance and Corporate Affairs in the presence of CS Shyam Agrawal, President, ICSI, awarded the ‘Certificate of CS Membership’ to the 50,000th member of ICSI and for details refer to www.icsi.org

F CISA: CS (Dr.) Shyam Agrawal, President The Institute of Company Secretaries of India (ICSI) has been elected as the Secretary of the Corporate Secretaries International Association (CSIA) during the Council Meeting of CSIA held on March 15-16, 2017

F Restrictions on cash transactions wef 1st April, 2017: With effect from 1st April, 2017 the revised limitations on cash transactions are -1any transaction (including transactions for capital assets) above Rs. 2,00,000/- shall be strictly done only through banking channels otherwise penalty on receiver equal to the cash amount received. 2. Donation above Rs. 2,000/- in cash will not be eligible for tax deduction under Sec 80G of the income tax act. 3. Any expense of above Rs. 10,000/- done in cash will be disallowed 4. Cash payments of above Rs. 10,000/- done for purchase of capital asset will be disallowed. I.e. they cannot be added in the cost of asset for Income Tax purposes hence, depreciation cannot be claimed on same.

F IND AS-102: MCA has notified amendments to Indian Accounting Standard Rules 2015 which reads -For cash-settled share-based payment transactions, the entity shall measure the goods or services acquired and the liability incurred at the fair value of the liability, subject to the requirements of paragraphs 31–33D. Until the liability is settled, the entity shall remeasure the fair value of the liability at the end of each reporting period and at the date of settlement, with any changes in fair value recognised in profit or loss for the period and for details refer to www.mca.gov.in

F ICDs: The CBDT has issued Circular No. 10 of 2017 dated 23.03.2017 by which it has provided important clarifications on the Income Computation and Disclosure Standards (ICDS) notified under section 145(2) of the Income-tax Act, 1961. The clarifications are in the form of FAQs. There are 25 FAQs dealing with all the important aspects of the ICDS and a must read for taxpayers and professionals. The ICDs are applicable from April, 2017.

F CBEC renamed: CBEC has been renamed as CBIC –Central Board of Indirect taxes and Customs vide PIB of Ministry of Finance dated 25th March, 2017 with 101 GST Commissionerates.

F ICSI guidelines for advertisement: ICSI has issued guidelines for advertisement by members of the Institute and for details refer to www.icsi.org

F Notices to companies for non compliance of Cost Audit: The Cost Audit Branch, Ministry of Corporate Affairs have taken a lead in ensuring cost audit compliance mechanism which will enable the different wings of the government to have a reliable data base at the HSN code level for GST decision making body. Moving a step ahead in tune with current business scenario and with the impending need for the useful data for government decision making and to implement the law regarding cost audit fully, the cost audit branch has started issuing notices to the defaulter companies which have not either appointed cost auditors or did not file the cost audit reports after appointment of cost auditors and for details refer to www.mca.gov.in

F IND AS Implementation group: The implementation of Ind AS converged with IFRS had begun in India from 1st April 2016. For Phase II companies, this will begin from 1st April 2017 onwards, and banks, NBFCs and insurance companies will be required to implement the Ind AS from 1st April, 2018 onwards. To provide guidance on the implementation of Ind AS in the required spirit, ICAI has launched an online Support-Desk for Implementation of Ind AS, where the preparers of financial statements, auditors and members at large can submit their implementation issues and get them resolved and for details refer to www.icai.org

F Applicability of GST for IPCC exam: The Council of ICAI has decided that Goods and Services Tax (GST) will be examined in both Part II: Indirect Taxes of Paper 4: Taxation of Intermediate (IPC) Course and Paper 8: Indirect Tax Laws of Final Course from May, 2018 examination onwards and for details refer to www.icai.org

F Disclosure of specified Bank notes: Govt. has notified the requirement of specified bank notes in Balance Sheet and Audit Report vide MCA Notification dated 30th March, 2017.

F Finance Bill Accented: The Finance Act 2017 received the assent of the President on the 31st March, 2017.

I. FOUR BILLS RELATED TO THE GOODS AND SERVICES TAX PASSED BY LOK SABHA

Four Bills related to Goods and Services Tax (GST) were passed by Lok Sabha. These Bills include the Central Goods and Service Tax (CGST) Bill, 2017, the Integrated Goods and Service Tax (IGST) Bill, 2017, the Union Territory Goods and Service Tax (UTGST) Bill, 2017, and the Goods and Service Tax (Compensation to States) Bill, 2017. The Bills levy the: (i) CGST on intra-state supply of goods and services, (ii) IGST on inter-state supply of goods and services, (iii) UTGST on supply of goods and services in union territories, and (iv) provide compensation to states for any loss of revenue, following the implementation of GST. Key features of the Bills include:

(a) Tax rates: The GST Council, constituted under the 101st Constitutional Amendment, will recommend the tax rates with respect to CGST, IGST and UTGST. The tax rates for CGST will not exceed 20%. The tax rate of IGST will not exceed 40%. In addition, a cess will be levied on certain goods and services to compensate states for revenue loss.

(b) Exemptions from GST: The centre may exempt certain goods and services from the purview of GST through a notification. This exemption will be based on the recommendations of the GST Council.

(c) Apportionment of IGST revenue: The IGST collected will be apportioned between the centre and the state where the goods or services are consumed. The revenue will be apportioned to the centre at the CGST rate, and the remaining amount will be apportioned to the consuming state.

(d) Registration of taxpayers: Every person with a turnover exceeding Rs 20 lakh will have to register in every state in which he conducts business. This

threshold will be Rs 10 lakh for special category states (i.e. Himalayan and North-Eastern states). A person may have multiple registrations for different business verticals in a state.

(e) Filing tax returns: Every taxpayer will have to self-assess and file tax returns on a monthly basis by submitting: (i) details of supplies provided, (ii) details of supplies received, and (iii) payment of tax. In addition to the monthly returns, an annual return will have to be filed by each taxpayer.

(f) Compensation to states on loss of revenue: The compensation amount will be calculated using revenue collections in 2015-16 as the base year. A compounded growth rate of 14% per annum over the base year will be assumed. A cess may be lev ied in order to prov ide the compensation.

(g) Prosecution and appeal: For offences such as mis-reporting of: (i) goods and services supplied, and (ii) details furnished in invoices, a person may be fined, imprisoned, or both, by the CGST Commissioner. Such orders can be appealed before the Goods and Services Tax Appellate Tribunal, and further before the High Court.

II. THE FINANCE BILL, 2017

The Finance Bill, 2017 was passed by Parliament with certain amendments. Key features of the Bill include:

(a) Income tax: The income tax rate for individuals with income between Rs 2.5 lakh to Rs 5 lakh will be reduced from 10% to 5%. An additional surcharge of 10% will be levied on individuals with income between Rs 50 lakh and Rs one crore.

(b) Limit on cash transactions: Cash transactions above Rs two lakh will not be permitted: (i) to a single person in one day, (ii) for a single transaction (irrespective of number of payments),

LEGAL

NOTES

and (iii) for any transactions relating to a single event.

(c) Political funding: Contributions to political parties may be made through a new mode called electoral bonds. These bonds will be issued by banks, for an amount paid through cheque or electronic means. Further, the 7.5% cap on percentage of profits that a company may give to parties has been removed. Companies would no longer be required to disclose the name of parties to which donations were made.

(d) Aadhaar mandatory for PAN and Income Tax: It will be mandatory for every person to quote his Aadhaar number after July 1, 2017 for: (i) applying for a Permanent Account Number (PAN), or (ii) filing Income Tax returns.

(e) Terms of service of Tribunal members: Currently, terms of service of Chairpersons and other members of Tribunals, Appellate Tribunals and other authorities are specified in their respective Acts. The Finance Bill permits the cent re to make ru les to determine the qualifications, and appointments, among other terms of service for members of 19 Tribunals.

(f) Replacing some Tribunals: Eight Tribunals have been replaced, and their functions transferred to existing Tribunals. For example, the functions of the Competition Appellate Tribunal will be carried out by the National Company Law Appellate Tribunal.

III. TAXATION LAWS AMENDMENT BILL, 2017

The Taxation Laws (Amendment) Bill, 2017 was introduced in Lok Sabha. It seeks to amend the Customs Act, 1962, the Customs Tariff Act, 1975, the Central Excise Act, 1944, the Finance Act, 2001, the Finance Act, 2005, and repeal provisions of few Acts.

IV. REGULATIONS FOR THE INFORMATION UTILITIES UNDER THE BANKRUPTCY CODE

The Insolvency and Bankruptcy Board of India (Information Utilities) Regulations, 2017 were notified. The regulations have been issued under the Insolvency and Bankruptcy Code, 2016. Key features of the regulations include:

(a) Eligibility and registration: An information utility (IU) will have to be a public company with a minimum net worth of Rs 50 crore. The Certificate

of Registration granted by the Insolvency and Bankruptcy Board to an IU will be valid for five years. The IU will be required to pay the Board Rs 50 lakh upon registration, and subsequently an annual fee of Rs 50 lakh.

(b) Governance: Independent directors wi l l constitute more than half of the IU’s Governing Board. An independent director will be the Chairperson of the Board.

(c) Grievance Redressal Policy: An IU will have a policy to address grievances from users or any person specified by the Governing Board. The policy will provide for: (i) constitution and functions of a grievance redressal committee, (ii) format and time to dispose applications, and (iii) a mediation mechanism, among others.

(d) Use of different IUs: Users may provide information to different IUs. A user may access this information from any IU.

(e) Fee: The IU will charge a fee for providing its service. The fee structure and any changes would be displayed on its website.

V. LAW COMMISSION SUBMITS REPORT ON INCOME TAX RELATED TO MINORS

The Law Commission submitted its report on the ‘Prospects of Exempting Income arising out of Maintenance Money of Minor’ to the Law Ministry. The Commission recommended that interest income of minors should be clubbed with their parents’ income.

Currently, interest on the amount of maintenance deposited in the name of minor children should be taxable with the parents’ income under the Income Tax Act, 1961. The Punjab and Haryana High Court is examining whether exceptions can be made to this provision based on special circumstances. The High Court referred the matter to the Law Commission for consideration. The Commission recommended that such interest income of the minors should be clubbed with the income of parents and should be taxed.

In addition, the Commission noted that any exceptions would open doors for tax evasion leading to loss and leakage of revenue.

VI. MATERNITY BENEFITS (AMENDMENT) BILL, 2016

The Maternity Benefits (Amendment) Bill, 2016 was passed by Parliament. It has also received the

HYDERABAD CIRCUIT - APRIL, 2017

Page 10

LEGAL

NOTES

President’s assent and was notified by the central government. The Bill amends the Maternity Benefits Act, 1961 in relation to the period of maternity leave for women, and certain other benefits. Key features of the Bill include:

(a) Duration of leave: The Act provides maternity leave up to 12 weeks for all women. The Bill extends this period to 26 weeks. However, a woman with two or more children will be entitled to 12 weeks of maternity leave.

(b) Leave for adoptive and commissioning mothers: The Bill introduces maternity leave up to 12 weeks for a woman who adopts a child below the age of three months, and for commissioning mothers. The period of leave will be calculated from the date the child is handed over to the adoptive or commissioning mother.

(c) Crèche facilities: The Bill requires every establishment with 50 or more employees to provide for crèche facilities within a prescribed distance. The woman will be allowed four visits to the crèche in a day.

(d) Work from home option: An employer may permit a woman to work from home, if the nature of work assigned permits her to do so. This may be mutually agreed upon by the employer and the woman.

VII. EMPLOYEE COMPENSATION (AMENDMENT) BILL

The Employee Compensation (Amendment) Bill, 2016 was passed by Parliament. The Bill amends the Employee’s Compensation Act, 1923. The Act provides payment of compensation to employees and their dependants in the case of injury by industrial accidents, including occupational diseases.

The Bill introduces a provision which requires an employer to inform the employee of his right to compensation under the Act. Such information must be given in writing (in English, Hindi or the relevant official language) at the time of employing him.

VIII. ENEMY PROPERTY (AMENDMENT) BILL, 2016

The Enemy Property (Amendment and Validation) Bill, 2016 was passed by Parliament. The Bill amends the Enemy Property Act, 1968. Previously, five similar Ordinances amending the 1968 Act had been promulgated in 2016. The last Ordinance was scheduled to lapse on March 14, 2017.

The central government had designated some properties belonging to nationals of Pakistan and China as ‘enemy property’ during the 1962, 1965 and 1971 wars. It vested these properties in the Custodian of Enemy Property, an office of the central government. The 1968 Act regulates these enemy properties.

IX. LAW COMMISSION SUBMITS REPORT ON HATE SPEECH

Law Commission of India submitted a report on ‘Hate Speech’, and made recommendations regarding amending the Indian Penal Code (IPC), 1860 and the Code of Criminal Procedure (CrPC), 1973.

In 2014, the Supreme Court in the case of Pravasi Bhalai Sangathan vs Union of India requested the Law Commission to define hate speech. It also asked the Law Commission to make recommendations regarding strengthening the Election Commission’s powers on curbing hate speech. In light of this, the Commission has recommended certain amendments.

X. SC REFERS ‘TRIPLE TALAQ’ CASE TO CONSTITUTION BENCH

Supreme Court of India on 30.03.2017 referred the ‘triple talaq’ and related matters to the Constitution Bench. The Bench headed by CJI Khehar said that a constitution bench will hear petitions challenging the constitution validity of triple talaq, polygamy and nikah halala from May 11.

XI. HC HAS NO JURISDICTION TO DECIDE ON SECOND APPEAL ON AN UNFRAMED QUESTION OF LAW

Setting aside a high court judgment, which suo moto applied a provision of law while deciding a second appeal, the Supreme Court reiterated that the high court has no jurisdiction to decide on a second appeal on a question which is not framed as required under Section 100(4) of the Code of Civil Procedure.

XII. ‘PUBLIC POLICY’ RULE CAN’T BE INVOKED TO FA C I L I TAT E L O A N E E AV O I D L E G A L OBLIGATION TO REPAY LOAN

The Supreme Court, in Himachal Pradesh Financial Corporation vs. Anil Garg, held that the concept of rule of ‘public policy’ cannot be invoked to facilitate a loanee to avoid legal obligation for repayment of a loan.

HYDERABAD CIRCUIT - APRIL, 2017

Page 11

Interview with CMA M KAMESWARA RAO

HC: What made you to choose the CMA course?

MKR: Before I share my entry to this profession, I

should give you my background and how I reached here

BACKGROUND:

I was born in a remote village of Andhra Pradesh – 16 miles from Rajahmundry – Rangampeta in East Godavari Dist to Late M Venkata Rao and Late M. Suryakantam couple. My father was at the fag end of his aurvedic practice. People, after trying all routes of medication and who gave up their trials, used to be treated by my father and got their ailments cured. This was his USP. But no remuneration. Whatever gratification is paid is in kind like jaggery, paddy, vegetables etc.,

I am the third of the four sons my parents had and there was only basic education for my eldest brother which was only primary and higher secondary education only for my elder brother. My elder brother got a job in 1964 in Hyderabad as Postman and reached Hyderabad to take up that job with great conviction.

STUDIES:

After completing my SSLC (secondary school leaving certificate) in 1967, I was called by my elder brother and he decided that I should learn some technical skill to get employed in Hyderabad. During that period there was a great demand for Typists/Stenos and I was put to Typewriting Lower in a nearby Institute. After 6 months of training and examination, I failed in the exam and lost hope. This was my first failure. My brother consoled me that nothing is lost and encouraged me to try again.

This time I put out the best efforts and there was no relooking, I completed, Type Lower grade, Higher Grade, Shorthand Lower grade and Higher grade and High speed which is 180 wpm (words per minute). Also completed Pre University Certificate (PUC) and joined B.Com., degree in night college. All accomplished over a period of 1969 to 1971 and also worked in private companies making steel plates, Sirsilk/sirpur paper mills Limited, Nataraj Spg & Wvg. Mills Ltd.., Omar Khayyam wineries private limited before entering HMT Limited, Machine tools division as Steno in 1971.

My interest for further studies, did not stop at this stage though I secured a Job. I continued pursuing my Degree in Commerce under Osmania Univeristy (Badruka College of Commerce – as a Night College student) and completed in 1975. While I am yet to complete my degree, I got married to Ms Rama. While leaving the college after completing the degree my Lecturer in commerce suggested that I can pursue ICWAI as a private candidate while working in HMT. This has helped me to join the course as a postal student.

Build up of Career:

While in HMT Limited, having chosen to pursue ICWAI, I sought up change in my job from steno to Accountant and took transfer to Watch Division. I was posted as Accounts superintendent in One of the watch sales unit in Ernakulam, after on job training for two months.

While in Kerala I completed Intermediate examination of ICWAI, serving the Company and taking oral coaching in Cochin Chapter, leading life away from relatives, but with family and kids.

During the year 2007-2008 the chapter was headed by

CMA M. Kameswara Rao as Chairman. He has taken initiation in

the compilation of the members directory for Hyderabad Chapter,

which has become a reference book.

HYDERABAD CIRCUIT - APRIL, 2017

Page 12

I served HMT Limited (watch Division) for over 13 years in various capacities and reached Chennai in 1984 to complete the final examination. I had calamities of losing my father in 1985 and was not able to appear the final examination for almost one year. I took the final examination in 1987 June without any exemption and successfully come out with an All India Rank of 61 in that year.

I was then posted to the Head quarters of Watch Marketing Division for a short while of one year and taken to Internal Audit wing of HMT Limited (the holding company). After servicing for over two years in the capacity of Internal Auditor I sought a transfer back to Hyderabad in HMT Bearings Limited.

Here I served in Costing, Material Accounts, Pay Roll and MIS for a period of six years from 1992 to 1998. Then moved on to Ranibagh in Uttarakhand as In-charge of Finance – Asst. General Manager in the watch unit. All this was opportunity knocked at my door and I grabbed it without even blinking further.

I gained good experience as a Finance Chief in Ranibagh – a sick unit – due to its nature of location. It was away from both raw materials as well as market for its products. After serving Ranibagh for 5 years I was back in Hyderabad in 2002. I worked from 2002 to 2008 in Hyderabad in various capacities, as Dy.General Manager Finance HMT Bearings Limited (where I worked as Dy. Manager earlier), Chief Internal Auditor covering Machine Tools, Praga Unit, Tractor Division, and HMT Bearings

I had full satisfaction of servicing a Company for over 37 years from Junior grade Steno to Dy.General Manager and worked in Major divisions of the Company.

After leaving HMT in 2008 I joined a private company manufacturing Defence Electronics in Hyderabad as General Manager Finance and served for a limited period of just three years.

I started my practice as CMA in 2011 and continue to be in practice.

HC: Please share your experiences during the association with our Chapter?

MKR: I have been elected as Member of the

Hyderabad Chapter of Cost Accountants during 2004

HYDERABAD CIRCUIT - APRIL, 2017

Page 13

and continued till 2007 in various capacities as Treasurer, Secretary and Chairman of the Chapter. During my term I have organized compilation of members directory for Hyderabad Chapter which has become a reference for many of us to know members face to face.

I had to necessarily thank my lecturers in Badruka, family and particularly my wife for the development of my career.

HC: How did the Costing knowledge put you to advantage in your career?

MKR: I can say for sure the Profession of Cost

Accountancy has given me lot of insight in my career and helped me grasp the detailed working of factories, processes, and businesses. I had helped my Organization in

1. Proper valuation of work in progress, and finished goods which was done with costing principles and accepted by the management.

2. Undertook study and revamped the process of availing Cenvat Credit in the organization saving at least a crore of rupees in the first year of its implementation

3. Was a member of committee in the Unit and was able to guide the organization in buy/make decisions.

4. Pricing for outsourced components / jobs.

5. Gained experience in organizing meetings / conferences as a Office Bearer of the Chapter of Cost Accountants which helped me in organizing a COST CONSCIENCE meet in the organization. Chairman of the HMT Limited appreciated my initiative and was asked to conduct in all the units.

HC: Your advice to prospective CMAs

MKR: This profession needs consistent study and

observation in the place of working whatever it is. Combined with professional study and work experience make CMA more acceptable to the Industry.

Today I am proud to be a qualified and successful CMA and ready to help both Government and the Industry.

HYDERABAD CIRCUIT - APRIL, 2017

Page 14

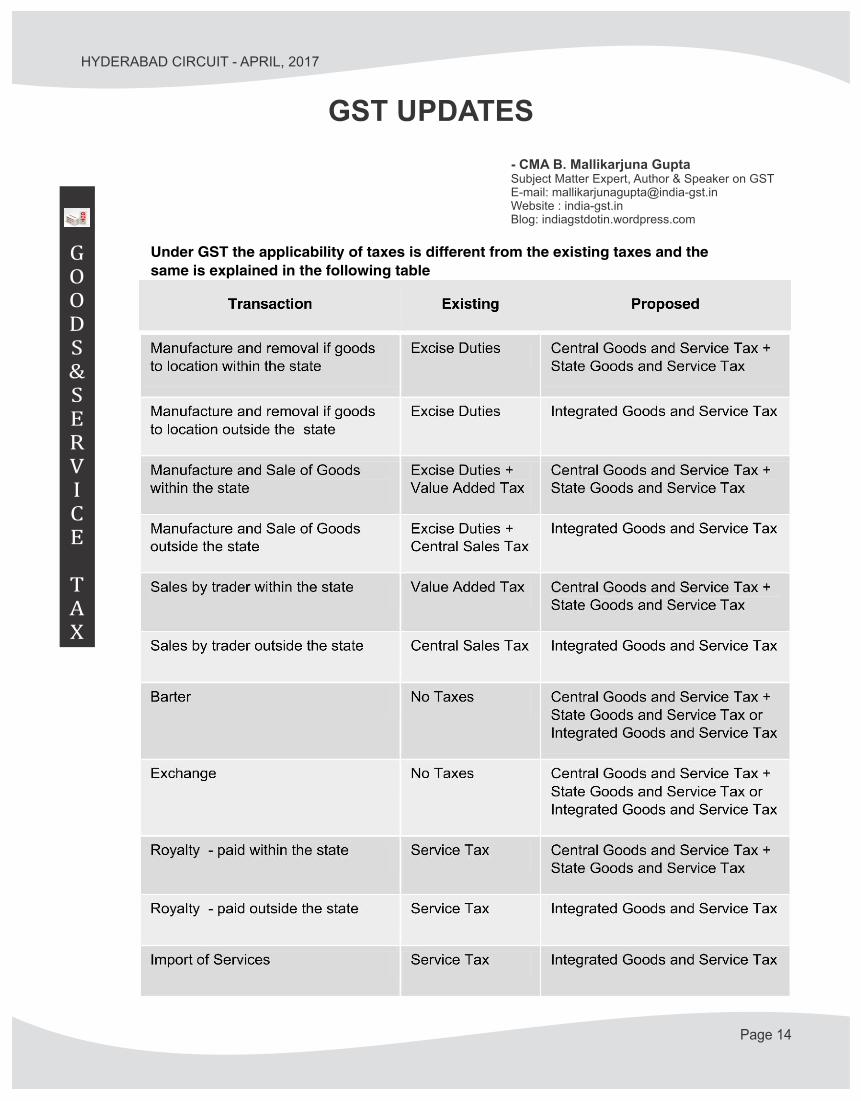

GOODS&SERVICE

TAX

- CMA B. Mallikarjuna GuptaSubject Matter Expert, Author & Speaker on GSTE-mail: [email protected] : india-gst.inBlog: indiagstdotin.wordpress.com

GST UPDATES

Cess will be levied on the sin and some luxury goods

and the same has to be added wherever applicable in

the above table.

Registration Number

Under the existing tax regime there are multiple tax

registration numbers like Excise Control Code (ECC)

under Central Excise at each factory level, Tax

Identification Number (TIN) under Value Added Tax at

each state level and, CST Number under CST, Service

Tax Registration Number under Service Tax at national

level or based on the region on assesses requirements.

Under the proposed all these registration numbers are

being replaced with a single registration number at

state level for all taxes called Goods and Service Tax

Identification Number (GSTIN).

The provisional registration for the existing tax payers

under Value Added Tax, Central Excise and Service Tax

has been initiated and a provisional ID has been issued.

On the rollout date the GST registration number will be

issued.

It is a fifteen-digit number based on PAN Number and

issued per state for the tax payer.

The first two digits, determine the state in which the

GSTIN in being obtained, the list of the states is based

on 2011 Indian Census. Under this each state will be

allocated a two-digit number.

Next 10 digits are PAN number of the entity issued by

the Income Tax Department.

Thirteenth digit is alpha numeric and it is based on the

user’s requirement to get registration based on the

business vertical. There can be 35 sequences

maximum for this 1-9 numbers and alphabets a - z. If the

tax payer is going for a single registration, then it will be

1 in the thirteenth field but if he goes for more than one

registration like one two business vertical say for

example one for consumer durables and another for

automobiles then the second one will be having 2 in the

thirteenth number and the third registration number will

be having 3 in the thirteenth field.

14th digit is a being reserved by the GSTN for the future

use and the 15th digit is check digit.

Time of Supply

Time of supply as per MGL refers to the event / point

during which the taxes will be applicable and tax liability

has to be accounted long with issue of the tax invoice.

The time of supply under GST is different for goods and

services.

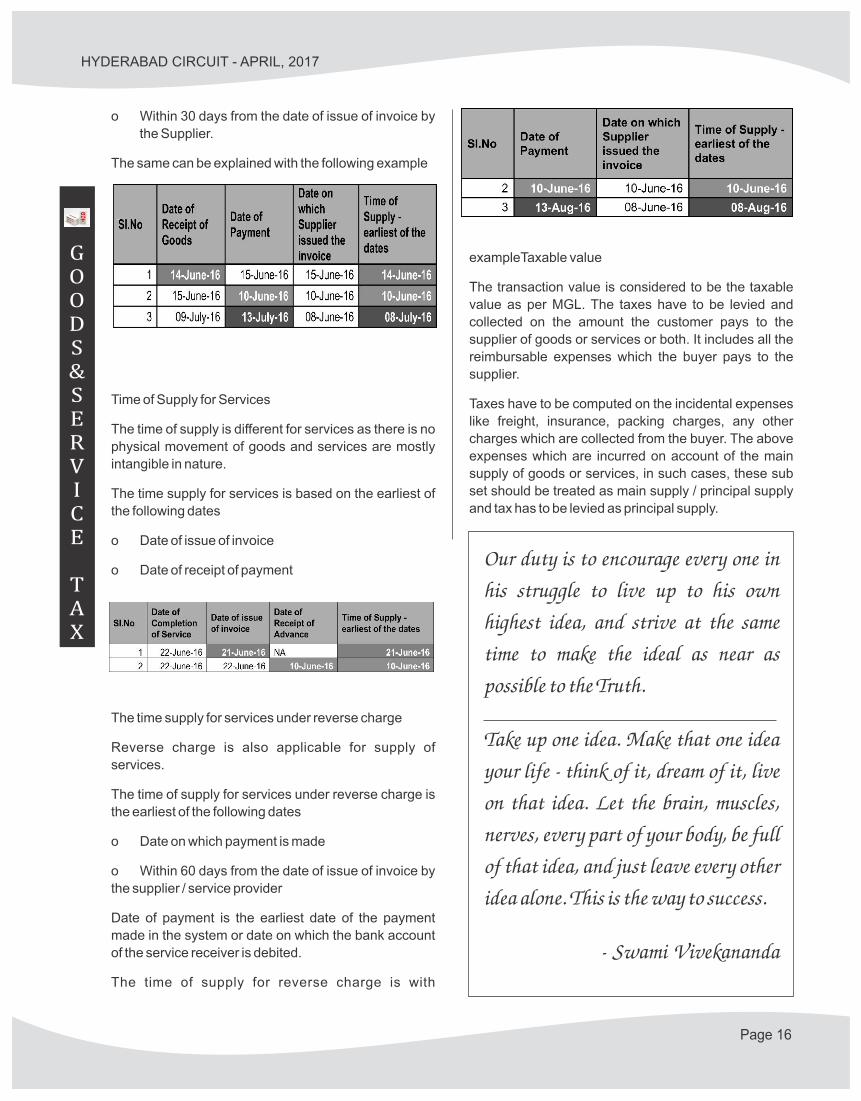

Time of Supply for Goods

The time of supply for supply of goods can be classified

broadly into three categories i.e forward charge,

reverse charge and miscellaneous.

The time of supply for goods under forward charge is

earliest of the following dates

o Date of issue of invoice

o Date of receipt of payment

The same can be explained with the following example

Time of supply for goods under reverse charge

In the normal course of trade, the sellers collect the

taxes from the buyer and remits the same to the tax

authorities. In the case of a reverse charge, the tax is

not collected by the seller, but the buyer pays the taxes

directly to the government on his purchases. To remit

the GST / SGST / IGST, the buyer has to be registered

for GST.

Under proposed GST, the reverse charge is also

applicable to the supply of goods and the applicable

taxes are CGST/ SGST/ IGST and Cess. The list of

goods for which reverse charge is applicable will be

issued through a notification on recommendations of

the GST Council.

The time of supply for goods under reverse charge is

the earliest of the following dates

o Date of receipt of goods

o Date on which payment is made

HYDERABAD CIRCUIT - APRIL, 2017

Page 15

GOODS&SERVICE

TAX

HYDERABAD CIRCUIT - APRIL, 2017

Page 16

o Within 30 days from the date of issue of invoice by

the Supplier.

The same can be explained with the following example

Time of Supply for Services

The time of supply is different for services as there is no

physical movement of goods and services are mostly

intangible in nature.

The time supply for services is based on the earliest of

the following dates

o Date of issue of invoice

o Date of receipt of payment

The time supply for services under reverse charge

Reverse charge is also applicable for supply of

services.

The time of supply for services under reverse charge is

the earliest of the following dates

o Date on which payment is made

o Within 60 days from the date of issue of invoice by

the supplier / service provider

Date of payment is the earliest date of the payment

made in the system or date on which the bank account

of the service receiver is debited.

The time of supply for reverse charge is with

exampleTaxable value

The transaction value is considered to be the taxable

value as per MGL. The taxes have to be levied and

collected on the amount the customer pays to the

supplier of goods or services or both. It includes all the

reimbursable expenses which the buyer pays to the

supplier.

Taxes have to be computed on the incidental expenses

like freight, insurance, packing charges, any other

charges which are collected from the buyer. The above

expenses which are incurred on account of the main

supply of goods or services, in such cases, these sub

set should be treated as main supply / principal supply

and tax has to be levied as principal supply.

Our duty is to encourage every one in

his struggle to live up to his own

highest idea, and strive at the same

time to make the ideal as near as

possible to the Truth.

Take up one idea. Make that one idea

your life - think of it, dream of it, live

on that idea. Let the brain, muscles,

nerves, every part of your body, be full

of that idea, and just leave every other

idea alone. This is the way to success.

- Swami Vivekananda

GOODS&SERVICE

TAX

TA

TITBITS

Page 17

HYDERABAD CIRCUIT - APRIL, 2017

Cleaning service and telephone services availed at branch offices- CENVAT Credit:

Facts of the Case: Assessee is manufacturer.It’s branchoffice received the cleaning and telephone services. The said branch is beyond the place of removal i.e. factory premises.

Issue: Whether the respondent is eligible toavail credit of the service tax paid on cleaning services and telephone services received in branch?

Revenue’s Argument: Factory of the assessee is registered for the Central Excise purpose. Since the branch office is beyond the place of removal i.e. factory premises, assessee is not eligible for credit for the services availed at branch office.

Respondent’s argument: Place of availing the input services is not material for availing the credit.

Decision: Definition of input services does not state any such criteria as mentioned by the revenue for availing the credit on input service.Credit is allowed. Hence, appeal by revenue is dismissed.

Comments: Input service definition does not restrict the availment of credit by branch, as long as the credit is used in or in relation to manufacture of final product or provision of output service, CENVAT should be eligible, which gains the impact.

Value of the study material – to be included or not for service tax purpose?

Facts of the Case: Assessee is engaged in

SERVICE TAXCASE LAW UPDATES

commercial training and coaching services. Assessee claimed the cost of books sold from the quantification of the services provided. These books prices were decided by the publisher and printed by M/s. Bull Eye, Pune.

Issue: Challenging the order passed by tribunal in which tribunal has excluded the cost of the study material from the taxable quantum of services.

Revenue’s argument: Para 2.9.1 of the circular da ted 20 .06 .2003 i ssued by the CBEC contemplates that the exclusion of the cost of the books in terms of the notification no. 12/2003-ST dated 20.06.2003 shall apply only to the sale of value of standard text books, which are priced. Any study material or written text provided by the assessee is part of service, and will be subject to service tax.

Decision: The study material supplied by M/s.Bulls Eye is quantifiable separately. The condition in the circular relates to the services of reading material and text books provided by the assessee-institute and not whether the books purchased from another supplier. In this case such goods can be quantified by the price paid. Therefore, the amounts of such goods have been rightly excluded in terms of Notification no.12/2003-ST dated 20.06.2003.

Comments: The sale of goods in the provision of service should not be subjected to service tax. Whether the same is boughtout or otherwise has not difference, one as to also ensure, for the better transparency an invoice for sale of books and receipt for services can be given separately.

1. Transfer of right to use goods: Value added tax-Liability to tax-“Goods” and “Sale” –Definitions-Grant of non-exclusive license to franchisee for use of brand name for consideration for running school-Is transfer of right to use goods-Taxable –Uttar Pradesh Value Added Tax Act (5 of 2008), ss. 2(m), (ac), 28 (3) - Constitution of India, art. 366 (29A)

(2017) 99 VST 188, G.D. Goenka (P) Ltd. vs. State of U.P

2. Check post: Value added tax- Detention – Vehicle running upon fixed rails –Excluded from definition of “goods vehicle”-Goods transported in such vehicle –Cannot be detained –Punjab Value Added Tax Act (8 of 2005), ss. 2(1), 51.

(2017) 98 VST 21 (P & H) State of Punjab vs. Indo Arya Central Transport Ltd

3. Composition of offence: Value added tax –Compound tax –Dealer engaged in production of grantie metal and M-sand having primary and secondary crushers installed at its unit- Notice alleging that dealer paying tax on compounded basis not, in his application for compounding, declared auto sand machine used for producing M-sand –Dealer proposing for compounding of offence with request to reduce compounding fee to 60 per cent. On cone crushers with st ipulat ion compounding fee to be refunded with interest if Court decided in his favour in Writ Petition challenging demand of tax on vertical shaft impactor machines.

Kerala Value Added Tax Act, 2003 (30 of 2004), ss. 8, 74 (1) (a)

(2017) 98 VST 36 Cochin Blue Metal Industries (P) Ltd vs. Intelligence Officer

4. Detention: Value added tax- Detention of goods –Dealer in plastic carry bags – purchase of plastic carry bags from outside State –Detention at check post for mis-declaration of goods as packing material since dealer engaged in sale thereof –writ petition by dealer contending that it had been paying tax on bags at rate prescribed therefor and alleged mis-declaration because State from which goods imported did not have suitable entry in Schedule for plastic bags- Contentions to be considered in adjudication proceedings –Dealer having prima facie case-Goods to be released against simple bond- Kerala Value Added Tax Act, 2003 (30 of 2004), ss. 6(1) (a), 8F –

(2017) 98 VST 13 National Agencies vs. Commercial Tax Inspector.

On 23rd March 2017 - National Conference on sustainable infrastructure was organized by our Institute at Taj Mahal Hotel, New Delhi. The objective of this national conference was to create a platform of thought leadership and collaboration among industry and government with an objective of building sustainable infrastructure that strengthens India’s growth Mission. Hon'ble Union Minister of Railways Sri Suresh Prabhakar Prabhu , Hon'ble Union Minister of State for Finance & Corporate Affairs Sri Arjun Ram Meghwal graced the inaugural while Hon'ble Union Minister of state for Power, Coal, New and Renewable Energy and Mines (I/C) Sri Piyush Goyal participated in the final technical session and gave his message through Tele-conference mode. All this can give a feel that the GOI is viewing our profession as specialized one in Cost management in addition to other accounting and finance functions. With the explanation offered by our President CMA Manas Kumar Thakur - it is very clear that Costing is not restricted to just Cost Sheet and Cost Records but expects a CMA to talk about and connect to Outcome Budgeting, Resource mapping and Effective utilization of resources.

Diverse and dynamic group of speakers and panelists provided in-depth insight, as well as, actionable and practical tools of engagement models, methods and mechanisms (3Ms) and were able to share how Sustainable Infrastructure could be utilized to become more effective in the key Sectors such as: Railways, Power, Petroleum, Ports, Highways, and Civil Aviation.

In the session on Petroleum and Natural gas - Sri Arun Kumar Sharma , Director (Finance), Indian Oil Corporation and others presented their views. He has well connected the Value Added exercise (Recall our Para D3) to substantiate the role played by Oil and gas Companies in serving the varied stakeholders of the society including the Governments. In fact it is good that a person of reputed stature is quoting the VALUE ADDED concept in public forum. Taking a cue on this – one CMA opined that the Value Added Statement can be mandated to all the entities as a matter of disclosure in the financial statements.

Participating in the session on Ports & Highways - Dr.S.K.Gupta - CEO of Affordable Infrastructure & Housing Private Limited - emphasized upon 3 areas of expertise for CMAs viz., Project Cost Management System ( consisting of Planning the Project, Estimating the Project Cost, Determination of Budgets, Monitoring the project costs and Controlling the costs) , Creative thinking for new forms of Finances such as Green Bonds and lastly on Life Cycle Costing.

Our CMA Narsimha Murthy Garu gave a detailed insight of Power industry and brought into the lime light the actual problems of Power Industry on the imbalances between Inadequate capacities and the backed out capacities. Sri Surender Kumar from Delhi School of Economics gave a graphical analysis between Carbon Emissions and Generation of Power.

Finally, it was a good show in the Capital city by the Institute of Cost Accountants of India.

National Conference on Sustainable Infrastructure

CMA

UPDATE

GENERAL

F� �Revised Trade Mark Rules: Press Information Bureau Government of India Ministry of Commerce & Industry 06-March-2017 19:35 IST Trade Mark Rules 2017 The Trade Mark Rules, 2017 have been notified and have come into effect from 06th March, 2017. These Rules, which replace the erstwhile Trade Mark Rules 2002, will streamline and simplify the processing of Trade Mark applications. The New Trade Mark rules cut number of Forms from 74 to 8.

F� � After BHIM Govt. to Launch Aadhaar Pay: The government is gearing up to roll out Aadhaar Pay, a digital payment platform for merchants, with 20 banks expected to go live at launch on 14th April, 2017.

F� � Aadhaar compulsory: The Supreme Court today made it clear that Aadhaar cards cannot be made mandatory by the government for extending benefits of social welfare schemes. However it said the government cannot be barred from seeking these cards, which are issued by UIDAI, for "non-benefit" purposes like filing of IT returns and opening of accounts vide The Business Standard dated 28th March, 2017.

F� � IT Department notified IT Return Forms: IT Department has notified Sahaj (ITR-1), 2,3 and Sugam ITR 4,5,6,7 for AY 2017-18 and the same can be downloaded from www.incometaxindiaefiling.org GST

F� �Composition Scheme: A business entity with turnover upto Rs. 50 lakhs can avail the benefit of a composition scheme under which it has to pay a much lower rate of tax and has to fulfill very minimal compliance requirements. The Composition Scheme is available for all traders, select manufacturing sectors and for restaurants in the services sector as per draft GST Bills.

F� � Returns under GST: 27 Returns have been prescribed under GST to be furnished by a Registered Dealer under various circumstances.

F� Sale of Replenishment Licences or EXIM Scrips: The SC held that as and when the goods are presented, the replenishment licence or EXIM Scrip is cancelled and and ceases to be a marketable instruement. If a company gives it to an agent of RBI who did not hold or purchase any goods would not involve any sale or purchase, then no sales tax shall be payable vide decision given in the case of CTO Vs SBI & Anr 2016-TIOL-186-SC-CT.

F� � GST working groups: CBEC has constituted different Working Groups to address concerns of the Trade and Industry under the proposed GST implementation vide notification dated 24th March, 2017.

F� � Loksabha approves GST bills: The Central GST Bill, 2017; The Integrated GST Bill, 2017; The GST (Compensation to States) Bill, 2017; and The Union Territory GST Bill, 2017 were passed on 29th March, 2017 after negation of a host of amendments moved by the opposition parties vide ET dated 29th March, 2017.

F� Approval of Draft Rules: The all powerful GST council in its 13th meeting held on 31st March, 2017 has approved five sets of Draft GST Rules with some amendments though they were approved earlier. In this meeting the GST Council has given tentative not to another 4 sets of Draft rules relating to-Input Tax Credit, Valuation, Transitional Provisions and the Composition scheme and they are going to be taken up for approval in the next meeting vide ET dated 1st April, 2017.

LABOUR

F� Aadhaar a must for Pension settlement: The EPFO has clarified that obtaining of Aadhaar should be mandatory for the time being only for final settlement of Pension and not in withdrawal cases. The EPFO had extended the date of submission of Aadhaar Number authentication by the members of Employees’ Pension Scheme 1995 upto 31st March 2017.

HYDERABAD CIRCUIT - APRIL, 2017

CMA

UPDATE

F� PF administrative charges reduced: CG has reduced the PF administrative charges payable by Employers wef 1st April, 2017 from0.85% to 0.65% and this would be applicable only to organizations who are paying minimum of Rs 500 on this account. Further, the administration charges in respect EDLI totally stands withdrawn from April, 2017 vide EENADU dated 23rd March, 2017.

F� Foreign workers can withdraw retirement corpus: Providing significant relief to international employees of multinational firms working in India, the Employees’ Provident Fund Organization (EPFO) has issued guidelines that would allow lumpsum withdrawal of retirement savings once their employment in the country comes to an end vide The Hindu Business Line dated 28th March, 2017.

INCOME TAX

F� 100% Sops to NGOs to end: Donations made to hundreds of projects carried out by NGOs across the country will no longer be eligible for a 100% income tax (I-T) deduction in the hands of the donor from April 1. Section 35AC has a sunset clause which expires this March 2017 under which contributors to NGOs were getting the 100% Tax benefit vide ET dated 5th March, 2017.

F� Simplified procedure for application of TAN: Application for allotment of a tax deduction and collection account number (TAN) will be filed as a part of filing the SPICe (INC 32) form using Digital Signature of the applicant as specified by the Ministry of Corporate Affairs. After generation of Corporate Identity Number (CIN) MCA will forward data in Form 49B to prescribed Income Tax Authority through digital signature, Class 2/Class 3, of MCA and for details refer to Notification No. 3 of 2017 dated 21st of March, 2017

F� Online notices & documents: CBDT has notified rules for Authentication of online Notices & Documents and for details refer to Notification dated 23rd March, 2017.

F� Capital Employed: The Honourable Supreme Court held that the Share Premium Amount collected by the company on its subscribed issued share capital is not and cannot be said to be the part of “Capital employed in the business of the company” for the purpose of Section 35D (3)(b) of the IT Act vide decision given in the case of M/s Berger Paints India Ltd Vs CIT vide Civil Appeal No.2162 of 2007

RESERVE BANK OF INDIAF� Banks told to enable M-Banking for all: The

government has instructed banks to link all savings accounts with mobile and Aadhaar numbers by March 31, 2017 and enable mobile banking for such customers.

SEBI

F� SEBI goes digital of all payments: The Securities and Exchange Board of India (SEBI) has amended vzarious regulations to enable the market participants to make payments to it through digital mode as well, the regulator said in a notification dated March 6. However, certain receipts such as filing fees for IPOs, takeover fees and payment from mutual funds are still received through cheques and demand drafts. Further, option of online payment from market intermediaries was not available in the respective regulations vide the TOI dated 9th March, 2017.

F� Mandatory filing in XBRL Mode: The BSE Limited through its circular DCS/COMP/28/2016-17 dated March 30, 2017 has made mandatory filing of Financial Results through XBRL mode with effect from April 01, 2017 SERVICE TAX

F� Cesses and Surcharge: Central Cabinet approved Amendment of in the Customs and Excise Act, relating to abolition of cesses and surcharges on va r ious goods and se rv i ces to fac i l i t a te implementation of GST Regime vide decision announced on 23rd March, 2017. CUSTOMS RULES & ACT

F� eBRC: CBEC has decided that for exports with LEO dates 12.08.2012 onwards till 31.03.2014, DGFT’s e-BRC would be accepted, except in case of specific intelligence or information of misuse and for details refer to Noti f icat ion No.06/2017-cus dated 28.02.2017. COMPANIES ACT

F� Threshold limits for combinations notified: Ministry of Corporate Affairs issues fresh notifications wherein, the Central Government intends to provide clarity on the applicability of the threshold exemption limits to all forms of combinations; Clarity on the methodology to be adopted for calculating the relevant assets and turnover of the target when only a portion or segment or business of one enterprise is being combined with another and for details refer to www.mca.gov.in IRDA

F� eCommerce & Point of sale: IRDA has issued guidelines for insurance coverage of e-commerce & revised guidelines on point of sale for both life & non-life for details refer to www.irda.gov.in

Page 20

HYDERABAD CIRCUIT - APRIL, 2017

Page 21

“Investor

Awareness

Programme

at

Stuvartpuram”

“Corporate

Social

Responsibility”

“Training

programme

on GST

for HAL

employees”

“Industrial visit to T.S. Dairy DevelopmentCo-operative Federation Ltd”

“Ind AS era – issues in Cost Audit”

“Improving

Productivity

using Office

Automation”

"Women as Entrepreneurs and Directors"

Page 22

HYDERABAD CIRCUIT - APRIL, 2017

HYDERABAD CIRCUIT - APRIL, 2017

Page 23

A v

iew

of

Fe

lic

ita

tio

n o

f s

po

us

es

of

Pa

st

Ch

air

me

n,

ICA

I-H

yd

era

ba

d C

ha

pte

r

on

th

e o

cc

as

ion

of

Wo

me

n's

Da

y C

ele

bra

tio

ns

he

ld

on

09

th M

arc

h,

20

17

at

Ho

tel

Ka

triy

a,

So

ma

jig

ud

a,

Hy

de

rab

ad

.

Page 24

HYDERABAD CIRCUIT - APRIL, 2017

Views expressed by contributors are their own and The Institute of Cost Accountants of India - Hyderabad Chapter does not accept any responsibility.

To PRINTED MATTER - BOOK POST

If undelivered please return to:

HYDERABAD CHAPTER OF COST ACCOUNTANTSCMA BHAVAN, Street No. 5,Himayatnagar, Hyderabad - 500 029.Ph. 040-27635937, Telefax: 040-27607893Web: cmahyderabadchapter.inEmail: [email protected]

Editor: CMA D. SURYA PRAKASAM, The Institute of Cost Accountants of India – Hyderabad Chapter, 1-2-56/44A, 5th Street, Himayatnagar, Hyderabad - 500 029.

Posting under registration No. L II / RNP / HD / 1181 / 2016-18

Printed and Published by: Mrs. K. Kavitha, on behalf of Hyderabad Chapter of Cost Accountants, 1-2-56/44A, 5th Street, Himayatnagar, Hyderabad-500 029 and printed at Gayatri Printing Press, 5-18, Durganagar, Dilsukhnagar, Hyderabad – 60 and published at Hyderabad Chapter of Cost Accountants, 1-2-56/44A, 5th Street, Himayatnagar, Hyderabad-29. Phones : 27635937/27611912.

“National Conference on Sustainable Infrastructure”

![[XLS]services.iriskf.orgservices.iriskf.org/FCKeditor/_samples/asp/excel/Niraj... · Web viewrspl_hub@rediffmail.com vwdip.bandyopadhyay@rediffmail.com nhemdev@indiatimes.com bajaj@hotpop.com](https://static.documents.pub/doc/80x56/5ab070417f8b9a6b308e7f75/xls-viewrsplhubrediffmailcom-vwdipbandyopadhyayrediffmailcom-nhemdevindiatimescom.jpg)