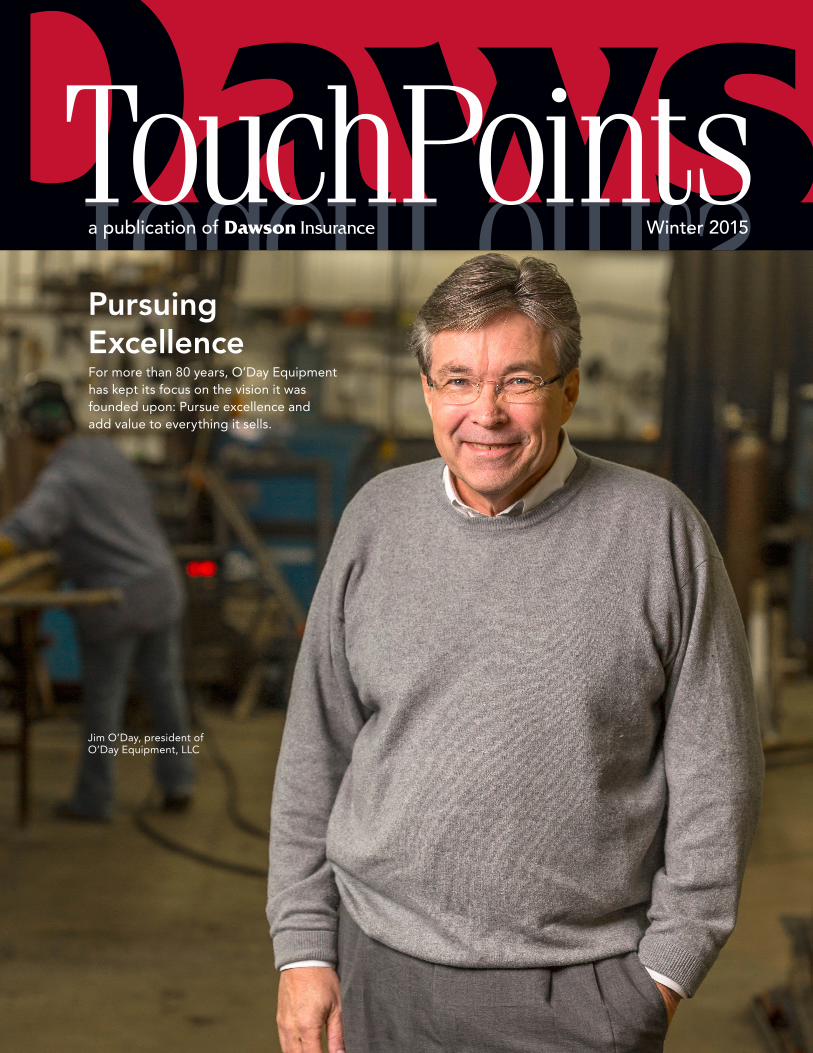

Daws Touch Points Touch Points Winter 2015 a publication of Dawson Insurance Pursuing Excellence For more than 80 years, O’Day Equipment has kept its focus on the vision it was founded upon: Pursue excellence and add value to everything it sells. Jim O’Day, president of O’Day Equipment, LLC

Transcript

DawsonTouch PointsTouch PointsWinter 2015a publication of Dawson Insurance

Pursuing ExcellenceFor more than 80 years, O’Day Equipment has kept its focus on the vision it was founded upon: Pursue excellence and add value to everything it sells.

Jim O’Day, president of O’Day Equipment, LLC

President’sMessage

TouchPoints • Winter 20152

From Gravel to GrowthBy Tom Dawson

It’s not all that long ago, as many of us will remember, that Veterans Boulevard in south Fargo was a

gravel road tucked between wheat, corn, and bean fields. Looking southward, it seemed that the road didn’t really lead to anything or anywhere; it simply just ended, presumably in another field.

With the installation of the Veterans Boulevard and I-94 interchange in 2010, things changed. Dramatically. Veterans Boulevard, which serves as the boundary between West Fargo and Fargo, is now a vibrant, booming corridor of growth. Retail, commercial, residential, hospitality – the area is home to it all, plus the new Sanford Fargo Medical Center, which is scheduled to open in 2017.

We are excited to be a part of that growth. As of this writing, we are putting the finishing touches on our second location at 5675 26th Avenue South (aka Veterans Boulevard) in Fargo. We’re located in the south end of the Galleria Plaza, just southeast of Costco. The dynamic development in this area of the metro is a wonderful complement to the revitalizing evolution taking place in downtown Fargo.

With easy access for many of our clients, our south Fargo office will be home to most of our personal lines agents and several account managers. The additional location enables our downtown office – which will continue to serve as our agency headquarters and remain home to our business lines agents and account managers – to accommodate our growing staff. Adding a second location enables us to serve our current and future clients even better. And for those personal lines clients who find our downtown location most convenient, they are welcome to continue to conduct business there.

And that – delivering exceptional customer service – is what it’s all about. Similar to O’Day Equipment, who is featured in our Client Spotlight this issue, Dawson Insurance was built on a vision of providing outstanding customer service, day in and day out.

Thank you for choosing Dawson Insurance and allowing us to serve you. We are grateful for your business and wish you a healthy and prosperous 2015. Watch for the grand opening at our new location, and in the meantime, stop in for a cup of coffee and check out our new digs! D

President’sMessage

Financial SerFinancial Services

Recent years have seen an explosion in wellness programs around the

country, and with good reason. A 2011 study published by the American Journal of Health Promotion indicated that successful wellness initiatives slowed the growth of health insurance premiums by more than 15 percent.

Even so, wellness programs – which usually fall into two distinct categories, participa-

tion based or outcome based – are oftentimes eventually discarded due to complexity, intrusiveness, or cost. Fortunately, there are several wellness ini-tiatives that are easy and cost-effective to implement.

Vaccination ClinicWith the passage of the Affordable Care Act, vaccinations and

immunizations are now free of charge to those enrolled in a compliant health plan. This can make scheduling a vaccination clinic at your business an easy piece of your wellness program. While many employees already schedule annual vaccinations on their own, having an employer-sponsored vaccination clinic can increase participation while easing employees into the mindset that their employer can play a positive role in their health management.

WorkstationsMany companies with a heavy office focus are also looking at stand-up

workstations as a way to alleviate back and neck strain for employees who spend long hours at their computer. “Height adjustable workstations are becoming increasingly popular as static posture from sitting can lead to strain, discomfort, and possible injury which can increase workers compensation claims,” said Barb Breuer, furniture account manager at Hannaher’s, Inc. of Fargo. While not often associated with a wellness program, the reduced risk of back and neck issues can have a real effect on healthcare costs, time spent out of the office, and productivity while in the office.

Stress Reduction ProgramsUnhealthy levels of stress can

have severe personal and finan-cial costs to your employees, and by extension, your busi-ness. Stress reduction programs can be an effective way of help-ing ensure that your employees are happy and healthy through: Employee assistance programs (EAPs), work/life balance pro-grams, concierge services (such as dry cleaning pick-up or on-site massages), and stress manage-ment resources.

There are many ways to effec-tively start or improve a wellness program in a simple, non-in-trusive, and affordable manner. To set up a free consultation to review options, give us a call at 701-237-3311. D

PERSONAL LINESKendra AhlquistConnie BertramGrant EllisStacey Frolek, CISRAshley KrumpRaeanna McCollumCrystal Rosen

Contract Surety BondsIn the United States, the

law requiring contract surety bonds on federal

construction projects is known as the Miller Act. Many states and local governments have adopted a similar law called the “Little Miller Act”.

The Miller Act payment bond covers subcontractors and suppliers of material who have direct contracts with the prime contractor. These firms are referred to as “first tier” claimants. Subcontractors and mate-rial suppliers who have con-tracts with these first tier subcontractors also have protection under the Miller Act as “second tier” claimants. Subcontractors and suppliers whose con-tract is with a first tier supplier have no protection under the Miller Act.

Why is all of this significant? Those second tier claimants, if not paid by the first tier subcontractors who hired them, can file a claim against the prime contractor’s payment bond, even though there is no direct relationship between the prime contractor and the second tier sub or supplier.

Case in point: A general contractor hires a subcontractor to furnish and install floor coverings in the new county courthouse. The subcontractor obtains the floor coverings and installs them. He is then paid by the prime contractor for material and labor. The subcontractor does not pay the supplier who provided the floor coverings; that supplier has recourse against the payment bond and the prime contractor.

Another case in point: A paving con-tractor hires a subcontractor to furnish and install new sewer and water lines be-fore the street is paved. The subcontractor

rents a backhoe to do the work. He in-stalls the new lines and is subsequently paid by the paving contractor. The sub fails to pay the rental company for the use of its backhoe to complete the work. The rental company is protected by the payment bond of the prime contractor.

In both of these cases, there is no direct relationship between the prime contractor and floor

covering supplier or the rental company. However, they both have protection under the prime contractor’s payment bond. The end result: The prime contractor could be required to pay twice for those materials and rental expense.

How does the prime contractor protect against this happening? He must do his due diligence when hiring the first tier subcontractor. If the prime contractor is unfamiliar with the sub, then requiring a subcontract performance and payment bond, which would be payable to the prime contractor, would provide protection. Another way for the prime contractor to gain protection would be to require information about the material supplier or rental company that the sub intends to use, and then issue joint checks, payable to both the sub and the supplier. At the least, the prime contractor should periodically check with suppliers during the term of the contract to confirm that they are being paid before issuing further progress payments to the first tier subcontractor.

For further discussions or information, contact Dawson Insurance’s Surety Department. D

Effective Now: New Flood Map

The new Fargo flood map became effective on January 16, 2015. If your property is affected and you have not already purchased a flood policy, we recommend that you purchase a policy now. The new flood map can

be found on the City of Fargo website (www.cityoffargo.com). If your property is impacted, or if you have questions regarding whether your property is impacted, please contact us at 701-237-3311. D

Company Overview: O’Day Management, Inc., serves as the holding entity for O’Day Equipment, LLC, O’Day Tank & Steel LLC, and Digital Surveillance Concepts LLC. Jim O’Day serves as president of the organization and focuses the majority of his time at O’Day Equipment.

Number of Employees: O’Day Management employs approximately 200 people.

(Note: Jim’s wife, Cindy, owns O’Day Caché in Fargo, and their daughters, Teresa and Ashlie, own Proper & Prim in Fargo and Minneapolis.)

As a fourth-generation family-owned business, O’Day Equipment has stayed true to the vision it was founded on

80 years ago: Add exceptional value to the products it sells.

For O’Day, that equipment focuses on the petroleum industry and includes service station and commercial pump equipment, underground and above-ground storage tanks, bulk petroleum pumps and meters, valves and fittings, rigid and flexible pipe, electronic point-of-sale terminals, card lock systems, tank gauging equipment, lubrication equipment, lighting, and farm fueling accessories.

In other words, O’Day provides equipment and service for everything in the fuel exchange process: The nozzle that dispenses fuel, the hoses, pumps, storage tanks, and the point of sale inside the store. Additionally, the company sells and services equipment for fleet fueling, fuel management systems, aviation fueling, and liquid storage tank maintenance. O’Day’s goal is to be the first choice for service, sales, and support of petroleum equipment in the Upper Midwest.

O’Day Equipment is headquartered in Fargo, North Dakota and has additional offices in Minot, North Dakota and Duluth and Minneapolis, Minnesota. The breadth of its offerings and its geographical coverage area make O’Day the perfect choice for reaching small single owners or servicing multi-location customers.

Jim O’Day serves as president of the company founded by his grandfather, Leo J. O’Day, in 1935. Jim’s son, Dan, works at O’Day’s Minneapolis office. For Jim, he’s been working in the family business for as long as he can remember.

Fueling Growth with Customer ServiceO’Day Equipment Built on Adding Value

800.220.4514 • DawsonIns.com 5

Client Spotlight Client Spotlight Client SpotlightFor 80 years, O’Day has provided equipment and service for everything in the fuel exchange process. The company also sells and services equipment for fleet fueling, fuel management systems, aviation fueling, and liquid storage tank maintenance. Day in and day out, the O’Day team is committed to the relentless pursuit of excellence.

“I started coming with my dad, (Dan), to his office on Saturdays when I was about 5 and did odd jobs as a kid and then as a teenager,” Jim recalls. “In college, I really didn’t know if I wanted to stay with the company or not.”

Upon his graduation from North Dakota State University in the mid-’70s, Dan told Jim that he needed help, and Jim went to work for O’Day doing special projects during the time that coal mines were being built in western North Dakota. It was the beginning of a lifelong career at O’Day.

That career has seen immense change in the industry. When Jim started at O’Day, very few gas stations were open late or on Sundays, and self-service and unleaded

gasoline did not exist. Now, stations are open 24/7/365, and the fueling systems are components controlled by point-of-sale systems. While such devices have brought consumers immense convenience, they’ve also brought challenges.

“Fueling systems used to be simple pumps and meters, all mechanical devices fixed with a wrench and hammer. Today these systems are for the most part electronic and fixed by highly trained technicians with a computer,” Jim says.

Other big changes in the industry have focused on regulations and environmental concerns, which created a new avenue of business for O’Day. “This is an entire line of equipment that wasn’t in existence

in 1980,” Jim says. “Now, storage tank systems are continuously monitored and often networked to smartphone apps. It is difficult to have a leak go undetected today.”

While the industry has changed immensely over the last 80 years, one thing hasn’t: O’Day’s commitment to customer service and its relentless pursuit of excellence.

“I work with extraordinary people, a truly wonderful group of people, and they’re really what drive this thing,” says Jim. “We want our customers to be amazed by our customer service, and the only way to deliver that is to have really great employees.” D

6 TouchPoints • Winter 2015

Claims CornerClient SaClaims Corner Client Safety

Important Changes to OSHA Injury and Illness Reporting Requirements

As of January 1, 2015, employers are required to report to the Occupational Safety and Health

Administration (OSHA) all work-related fatalities within eight hours as well as all in-patient hospitalizations, amputations, and losses of an eye within 24 hours of being informed of the incident.

Previously, employers were required to report 1) all workplace fatalities, and 2) when three or more workers were hospitalized in the same incident. While the updated reporting requirements have a life-saving purpose (to prevent future, possibly deadlier, incidents from occurring), it is also true that the total number of injuries reported directly to OSHA will rise dramatically by an estimated 25,000 more per year.

To place this in context, as of the end of 2013, the annual total number of federal inspections was 39,228, with state plans totaling 50,346. While this raises a question of whether or not OSHA has the capacity to process the increased caseload, some stakeholders are concerned that providing additional injury data will lead to more enforcement activity and increased citations. While OSHA leadership has suggested that the additional data will offer the opportunity to open a dialogue with employers, there is nothing in the new rule that would preclude mandated reported incidents from being treated differently than they were under the previous rule.

A second change, which is projected to have less impact, includes an update to the list of industries partially exempt from maintaining injury and illness logs. The change also replaces the Standard Industrial Classification system, currently used to determine exempt industries, with the new North American Industry Classification System. Impacted industries received notification by mail from OSHA in December of 2014.

If you have any questions regarding the changes and/or whether your business is covered or partially exempt from mandated reporting and recordkeeping, contact Matt Weis, client safety coordinator at Dawson Insurance, at 701-237-3311. D

A unit owner’s condo insurance policy, often referred to as an “HO-6,” is undoubtedly the most difficult

personal policy to set up correctly. Your policy must not only pick up coverage for your belongings and personal liability, but also protect the interior structural parts of your unit that are not covered by the association’s master policy.

To set adequate policy limits for your condo unit owners policy, it is important that you know where your condo association draws the line between what is the association’s responsibility and what is the unit owner’s responsibility. This will be outlined in the association’s bylaws. When determining your policy limits, you may need to take into consideration the cost to reconstruct the interior of your unit, including any improvements or alterations made to your unit from the original construction of the building. These five tips will help you correctly set up a unit owners policy:

• Determine from the association documents – usually the bylaws – exactly what part of the structural interior of your unit you are required to insure. It’s most common for the owner to have to insure everything beyond the bare walls and bare floor.

If the documents aren’t clear, assume you are responsible for everything structural inside your unit, including carpeting, hardwood flooring, any floor and wall tile, bathroom fixtures, kitchen cabinets, countertops, built-in appliances, lighting fixtures, etc.

• Inventory your personal property. You will want to schedule an appropriate limit for your personal property (the contents of your dwelling) that is not physically attached to your dwelling unit. The limit should be enough to allow you to replace your possessions at the current replacement cost.

• Purchase loss assessment coverage. In the event of a large loss to the condo building, the association may assess the condo association policy deductible to

the unit owners. In order to have proper limits for this coverage, you will need to know what the condo association policy deductible is. Also, be aware that your condo unit owner policy deductible will apply to this type of claim.

• Purchase loss of use coverage. If your unit becomes uninhabitable due to a covered loss, this coverage would provide for the additional expenses you incur while your unit is being repaired.

• Purchase personal liability coverage. This provides coverage for someone injured in your condo unit or if there is damage to the other units/common areas in the building due to your negligence. Dependent upon your personal wealth, you may want to consider extending your limits of personal liability through the purchase of an umbrella liability policy.

As always, work with your agent to customize an insurance program specific to your unique needs. D

Ashley joined the Dawson Insurance team in October of 2014, bringing customer service experience with her from previous jobs in childcare, food service, and insurance.

In her spare time, Ashley enjoys going to sporting events and the lakes as well as spending time with her niece and nephews.

Dexter began his career in the insurance industry in 2013 and joined the Dawson team in October of 2014. He has previous sales experience with Country Financial and Gateway Chevrolet, both in Fargo.

In his position at Dawson, Dexter specializes in personal lines, including home, auto, watercraft, motorcycle, umbrella, vacation home, and life insurance. He says he was drawn to

Dawson because of the expertise of its associates, noting that clients always receive professional, industry-leading service.

In his spare time, Dexter enjoys spending time outdoors with his wife and family hunting, fishing, skiing, and snowmobiling.

Laura joined Dawson Insurance in October of 2014 and brings several years of customer service experience to her position. Previously she worked as an account executive for broadcast and cable television.

When not in the office, Laura enjoys international travel and learning about new cultures. Although much of her

extended family still lives in Kentucky, she did bring her husband and dog to Fargo when she relocated.

Jill joined the Dawson Insurance team in December of 2014. Her customer service-centric career includes experience in student financial services, daycare curriculum and operations, and banking. Her primary responsibilities at Dawson include reviewing policies, issuing certificates and

providing overall support to her account manager.Jill says that the best part of her job is her co-workers, noting that everyone has

a great attitude and truly enjoys what they do. That shows in the customer service Dawson provides, Jill says, which is “above and beyond”, whether talking to a client in person or on the phone.

In her free time, Jill enjoys spending time with her husband and their daughter as well as shopping, reading, and going to the lake in the summer. D

New Employees Retirement

Congratulations, Todd!

After 21 years, our co-worker, mentor, and

friend Todd Anderson retired from Dawson Insurance at the end of 2014. A stockholder and member of the Dawson board of directors, Todd’s insurance industry career spanned 34 years.

He began working in the industry in 1980, including working a summer for his dad, Don, at Don’s agency in Grand Forks, North Dakota, Todd’s hometown. Dawson first worked with Todd while he was a field underwriter with Great American Insurance Company. He joined the Dawson team in May of 1994. As a commercial lines producer, Todd often said that the best part of his job was having the privilege to work with a great team. We feel the same way about him.

A true student of insurance, Todd was constantly studying, researching a difficult claim, or sorting out a tricky coverage issue. He conducted daily study classes for newer Dawson team members. He held the CPCU (Chartered Property Casualty Underwriter) and CIC (Certified Insurance Counselor) designations, and he was active in industry positions, including being past president of the Independent Insurance Agents of North Dakota and the North Dakota Roughrider Chapter of CPCU.

As an active community volunteer, Todd plans to spend even more time volunteering with Junior Achievement, the YMCA, and United Way of Cass-Clay. Retirement will also bring more time for taking in various sports activities (it is hard to find someone more knowledgeable than Todd in sports facts and trivia, especially that involving his beloved UND hockey), playing golf, and hunting pheasants and deer.

Todd had an unwavering dedication and commitment to his clients, many of whom became friends. He has been an extraordinary mentor, and all of us at Dawson are grateful for his leadership, guidance, friendship, and significant contributions to our success. We wish Todd nothing but the best in his well-deserved retirement. D

“The positive and upbeat atmosphere at Dawson help make every day a great day.”

“The best part of my job is interacting with clients and developing relationships with other business professionals.”

“I wanted to work for a local company that is recognized as an industry leader as well as one that gives back to the community.”

“Dawson Insurance has a great reputation in our community. I am excited to work for a growing company that cares so deeply about its clients and employees.”

800.220.4514 • DawsonIns.com 7

TouchPoints content is for illustration and informational purposes only. Dawson Insurance relies on the accuracy of information provided to us in developing this newsletter. For premium quotes, specific coverage options and other products and services, please contact us.

Dawson Insurance is proud to be a locally-owned, inde-pendent agency that provides a full line of property and casualty coverage, as well as life and health benefits, surety and financial services for individuals and businesses. For 98 years, we have been working hard to ensure our customers always come first, both in the services we offer and the protection we provide. Thank you for your business.

Trust EarnExtra Mile Trust Earned Daily Extra Mile

Downtown Veterans Boulevard 721 1st Ave N 5675 26th Ave S PO Box 1958 Suite 152 Fargo, ND 58107 Fargo, ND 58104

701-237-3311 | 800-220-4514 | 701-232-4442 (fax)

Bowling to Give BackIn November, Dawson Insurance participated in the annual Junior

Achievement bigBowl fundraising event. For the fourth consecutive year, Dawson was the top fundraising team, raising more than $1,200

for Junior Achievement. Plus, Dawson associate Dar Zimmerman was the second place individual fundraiser.

The Dawson team – Alex Dawson, Bridget Helm, Brooke Rogers, Dar Zimmerman, Jaclyn Hanson, and Steve Miller – was definitely in the Thanksgiv-ing spirit during the event as three Daw-son bowlers achieved “turkeys”!

Junior Achievement is a non-profit organization dedicated to educating young people about entrepreneurship, financial literacy, and workforce readi-ness skills. Last year Junior Achievement served more than 7,700 students in the Fargo-Moorhead area. D