27

DCF Analysis Kelvin Xu Slides prepared by: Asthon Wu, Garrett Kuhlmann UofT Engineering Finance Association Finance 101

| Date post: | 01-Jan-2016 |

| Category: |

Documents |

| Upload: | vernon-wiggins |

| View: | 50 times |

| Download: | 2 times |

DCF Analysis

Kelvin Xu Slides prepared by: Asthon Wu, Garrett

Kuhlmann

UofT Engineering Finance AssociationFinance 101

2

Introduction

► Need to learn theory of DCF before learning how to use the spreadsheet

► The Forecasting Period & Forecasting Revenue Growth

► Forecasting Free Cash Flows► Calculating the Discount Rate► The Fair Value

UTEFA

3

Background UTEFA

► Projects how much money a company will make in the future

► Determines a fair price based on this projection

► “Time value of money”► Several approaches: free cash flow

to equity, dividend discount model, cash flow to firm

4

The Forecast Period

UTEFA

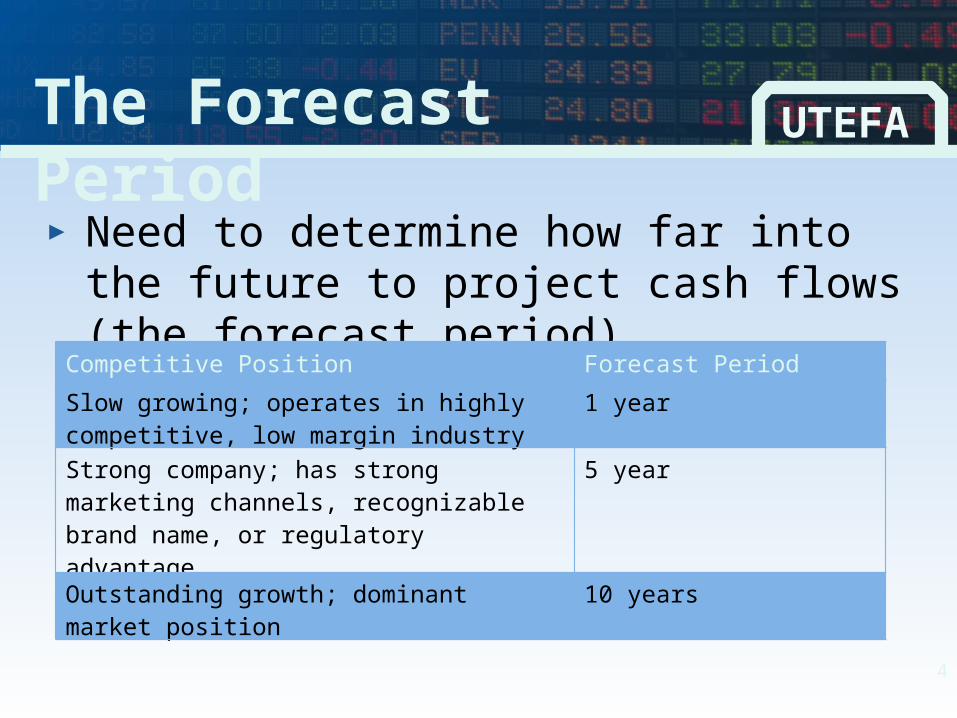

► Need to determine how far into the future to project cash flows (the forecast period)

Competitive Position Forecast Period

Slow growing; operates in highly competitive, low margin industry

1 year

Strong company; has strong marketing channels, recognizable brand name, or regulatory advantage

5 year

Outstanding growth; dominant market position 10 years

5

Revenue Growth Rate

UTEFA

► One of the most important assumptions one can make about the company’s future cash flows

► Consider future of company and market► What does the company predict?► Is the market expanding or

contracting?

6

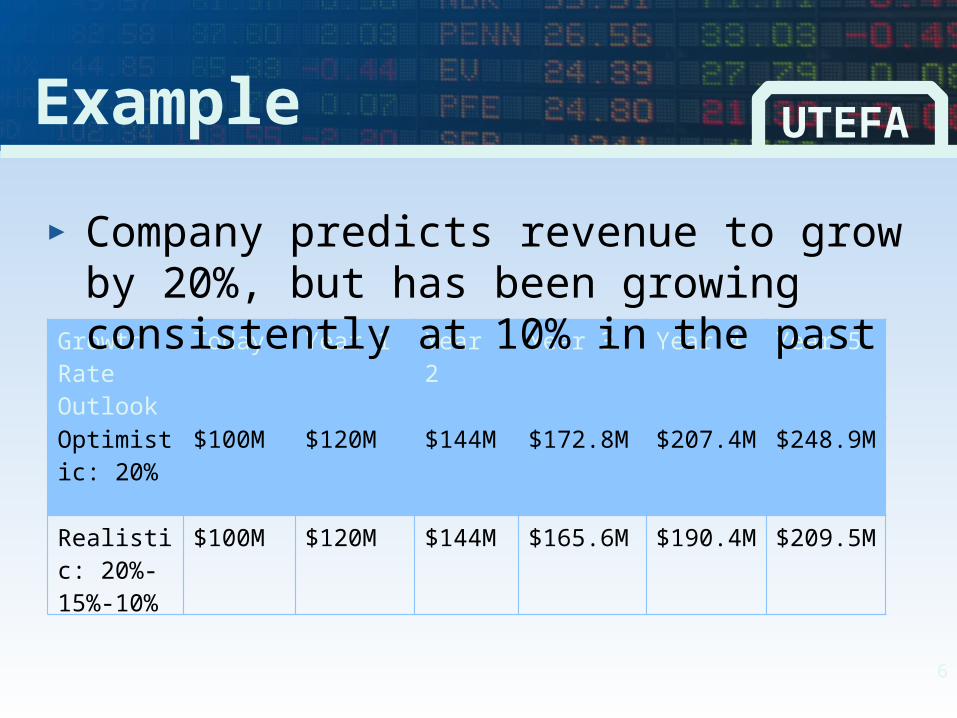

Example UTEFA

Growth Rate Outlook

Today Year 1 Year 2 Year 3 Year 4 Year 5

Optimistic: 20%

$100M $120M $144M $172.8M $207.4M $248.9M

Realistic: 20%-15%-10%

$100M $120M $144M $165.6M $190.4M $209.5M

► Company predicts revenue to grow by 20%, but has been growing consistently at 10% in the past

7

Free Cash Flow UTEFA

► The actual amount of cash a company has left from its operations to enhance shareholder value► Development of new products, or

paying dividends

8

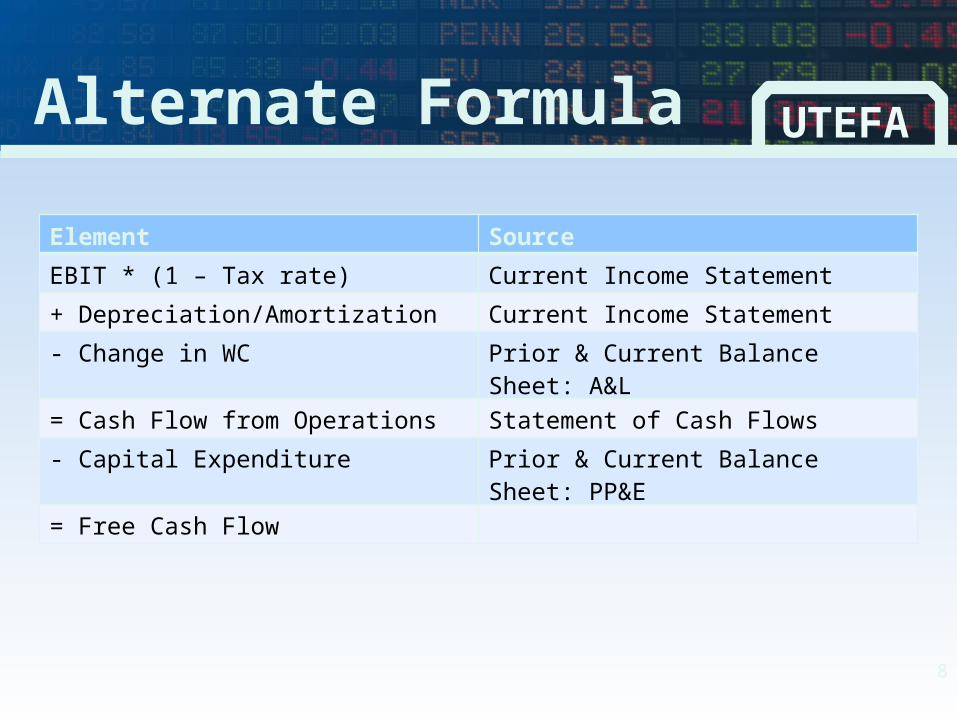

Alternate Formula UTEFA

Element Source

EBIT * (1 – Tax rate) Current Income Statement

+ Depreciation/Amortization Current Income Statement

- Change in WC Prior & Current Balance Sheet: A&L

= Cash Flow from Operations Statement of Cash Flows

- Capital Expenditure Prior & Current Balance Sheet: PP&E

= Free Cash Flow

9

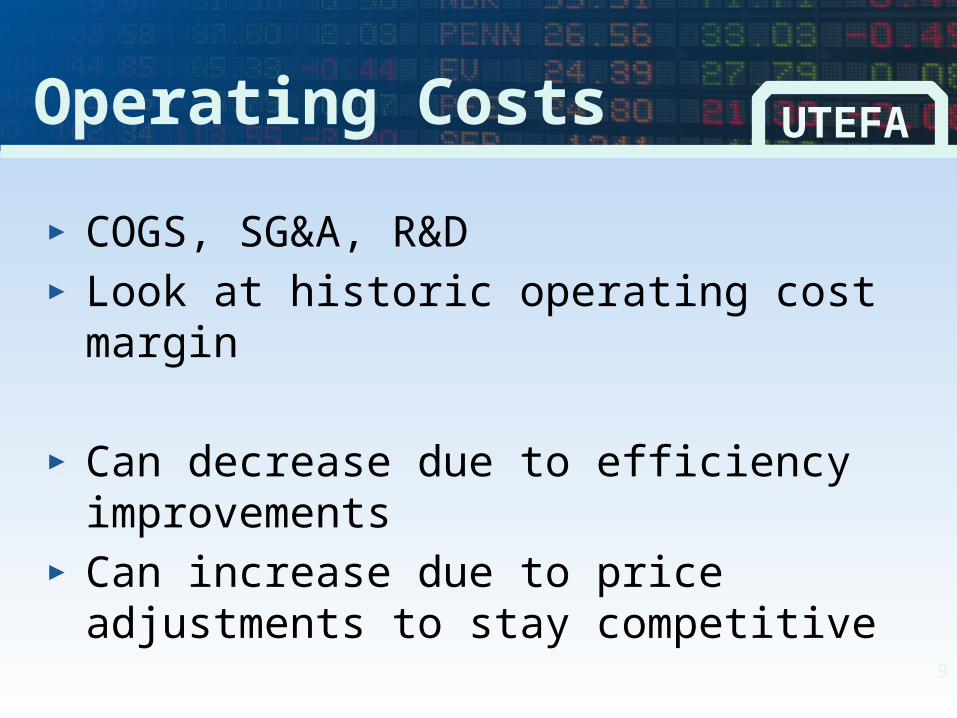

Operating Costs UTEFA

► COGS, SG&A, R&D► Look at historic operating cost margin

► Can decrease due to efficiency improvements

► Can increase due to price adjustments to stay competitive

10

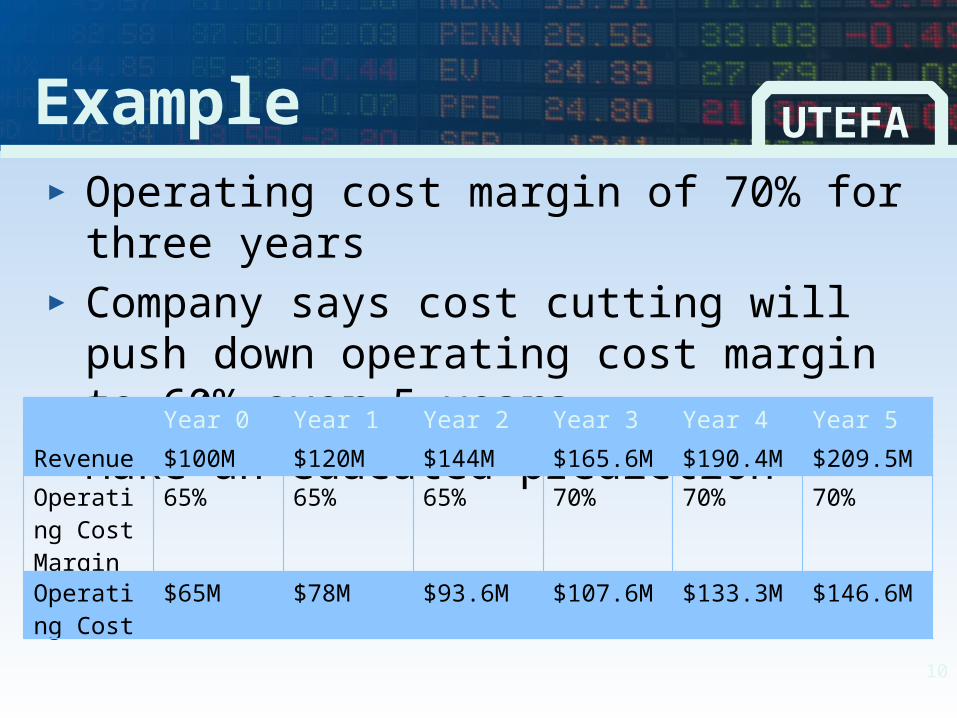

Example UTEFA

► Operating cost margin of 70% for three years

► Company says cost cutting will push down operating cost margin to 60% over 5 years

► Make an educated predictionYear 0 Year 1 Year 2 Year 3 Year 4 Year 5

Revenue $100M $120M $144M $165.6M $190.4M $209.5M

Operating Cost Margin

65% 65% 65% 70% 70% 70%

Operating Cost

$65M $78M $93.6M $107.6M $133.3M $146.6M

11

Tax Rates

Introduction

Forecasting

Revenue

Forecasting FCF

Conclusion

UTEFA

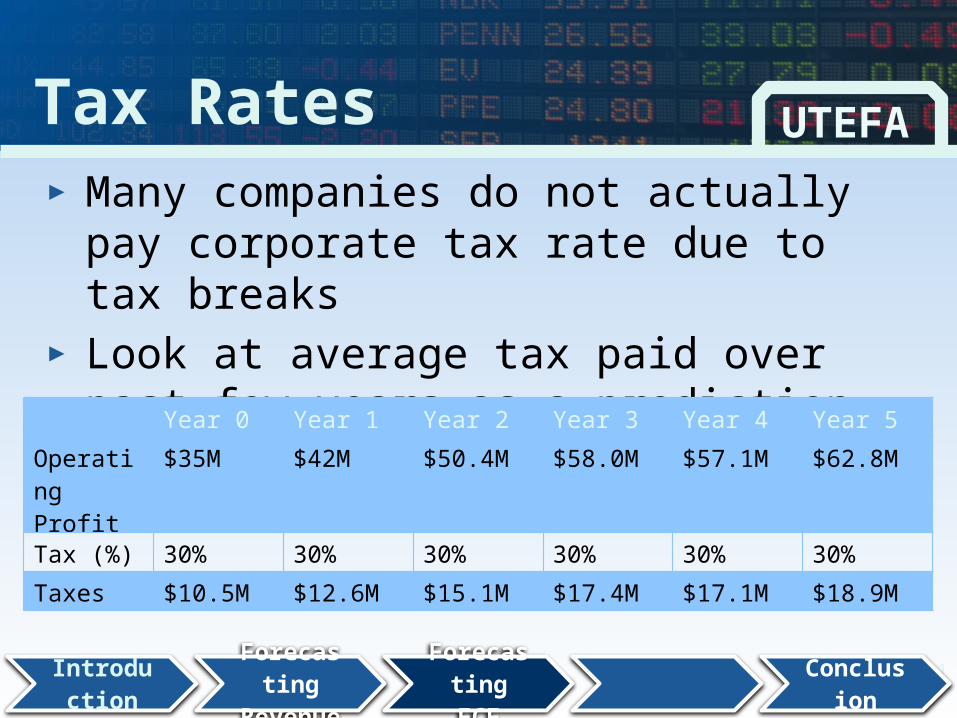

► Many companies do not actually pay corporate tax rate due to tax breaks

► Look at average tax paid over past few years as a prediction for future tax ratesYear 0 Year 1 Year 2 Year 3 Year 4 Year 5

Operating Profit

$35M $42M $50.4M $58.0M $57.1M $62.8M

Tax (%) 30% 30% 30% 30% 30% 30%

Taxes $10.5M $12.6M $15.1M $17.4M $17.1M $18.9M

12

Net Investment UTEFA

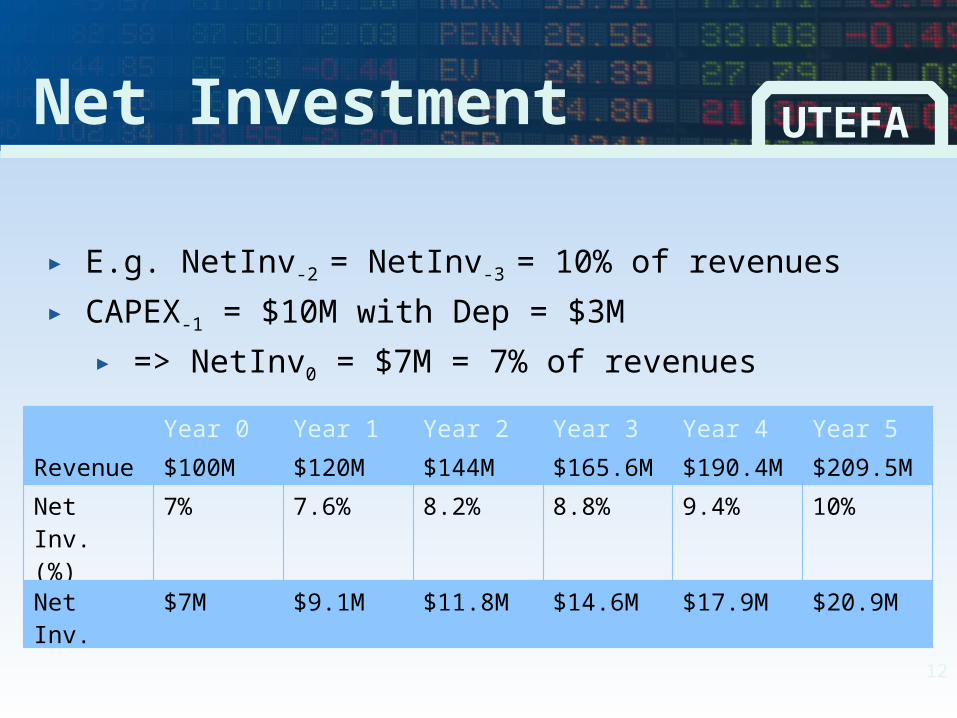

► E.g. NetInv-2 = NetInv-3 = 10% of revenues► CAPEX-1 = $10M with Dep = $3M

► => NetInv0 = $7M = 7% of revenues

Year 0 Year 1 Year 2 Year 3 Year 4 Year 5

Revenue $100M $120M $144M $165.6M $190.4M $209.5M

Net Inv. (%)

7% 7.6% 8.2% 8.8% 9.4% 10%

Net Inv. $7M $9.1M $11.8M $14.6M $17.9M $20.9M

13

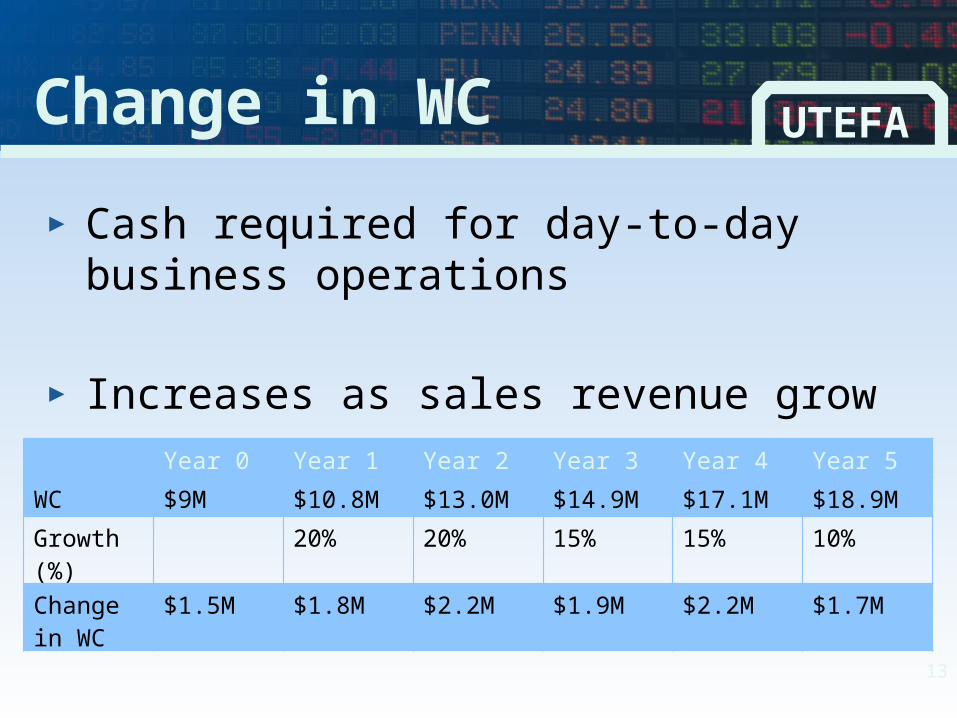

Change in WC UTEFA

► Cash required for day-to-day business operations

► Increases as sales revenue growYear 0 Year 1 Year 2 Year 3 Year 4 Year 5

WC $9M $10.8M $13.0M $14.9M $17.1M $18.9M

Growth (%)

20% 20% 15% 15% 10%

Change in WC

$1.5M $1.8M $2.2M $1.9M $2.2M $1.7M

14

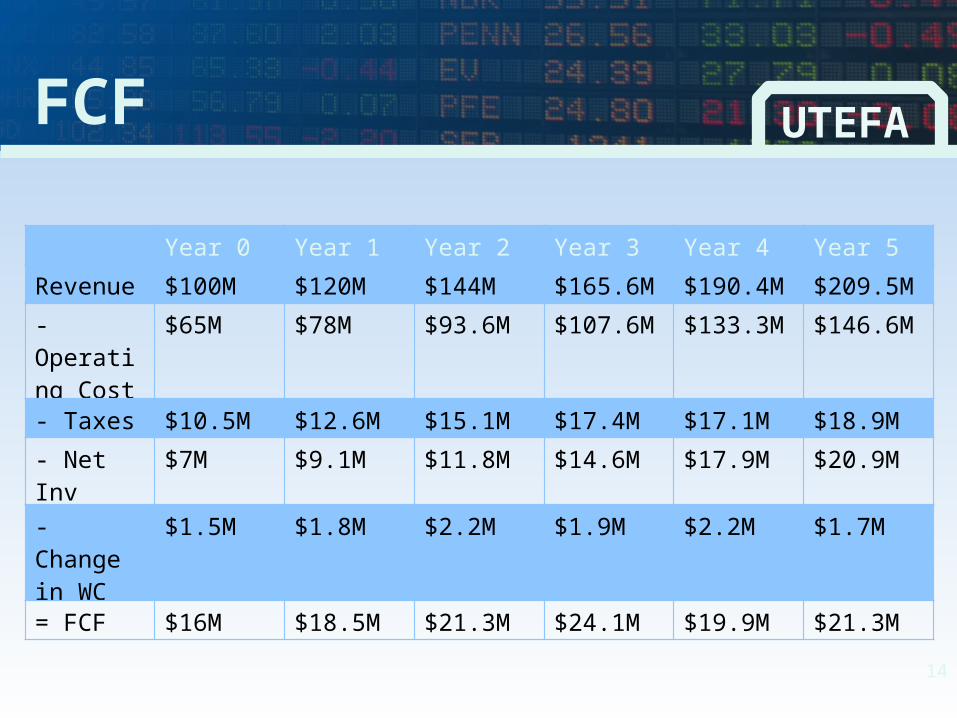

FCF UTEFA

Year 0 Year 1 Year 2 Year 3 Year 4 Year 5

Revenue $100M $120M $144M $165.6M $190.4M $209.5M

- Operating Cost

$65M $78M $93.6M $107.6M $133.3M $146.6M

- Taxes $10.5M $12.6M $15.1M $17.4M $17.1M $18.9M

- Net Inv $7M $9.1M $11.8M $14.6M $17.9M $20.9M

- Change in WC

$1.5M $1.8M $2.2M $1.9M $2.2M $1.7M

= FCF $16M $18.5M $21.3M $24.1M $19.9M $21.3M

15

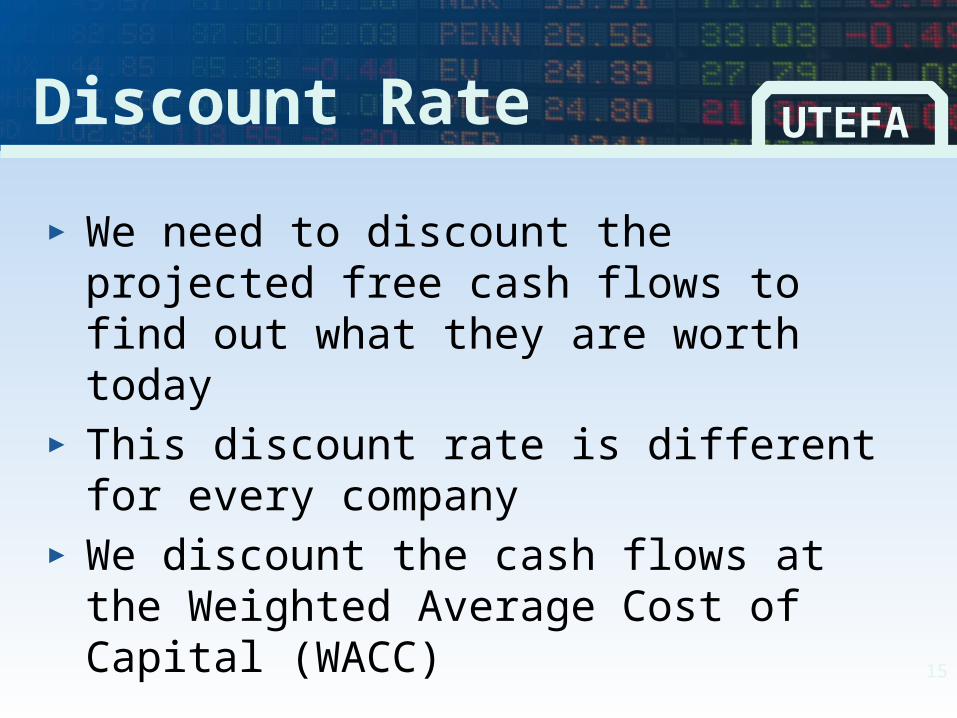

Discount Rate UTEFA

► We need to discount the projected free cash flows to find out what they are worth today

► This discount rate is different for every company

► We discount the cash flows at the Weighted Average Cost of Capital (WACC)

16

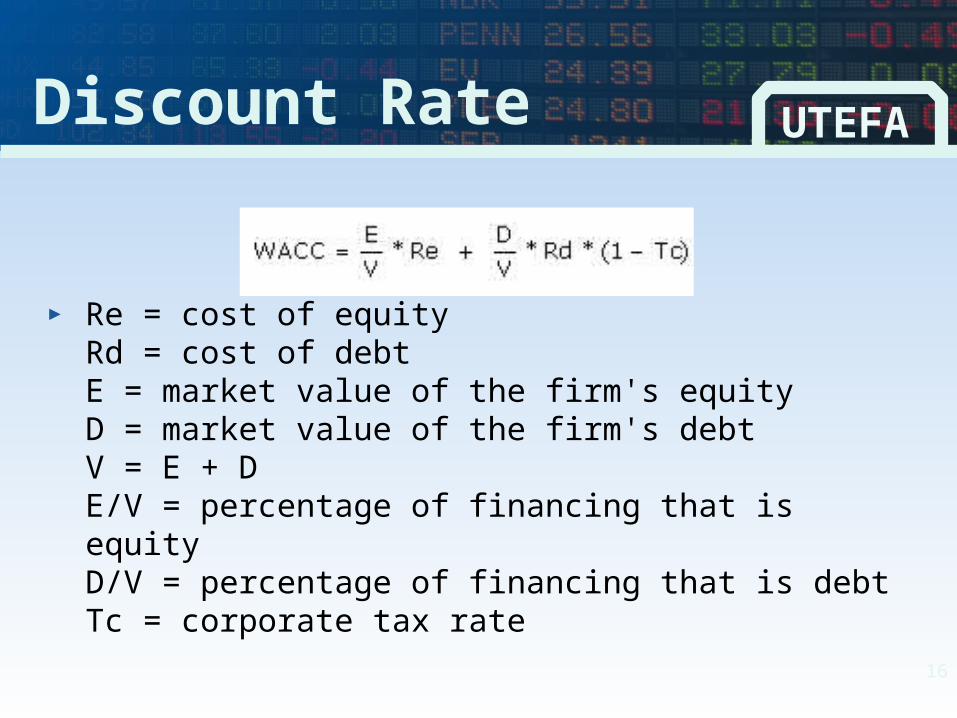

Discount Rate UTEFA

► Re = cost of equity Rd = cost of debt E = market value of the firm's equity D = market value of the firm's debt V = E + D E/V = percentage of financing that is equity D/V = percentage of financing that is debt Tc = corporate tax rate

17

Cost of Equity (Re) UTEFA

► Investors generally wish to receive a premium for investing their money in the company

► Use Capital Asset Pricing Model to find this value

► Re = Rf + β(Rm – Rf)

18

Cost of Equity (Re) UTEFA

► Re = Rf + β(Rm – Rf)► Beta may be found on any finance

website and is a measure of how correlated the companies stock price is with the market

► Rf is the Risk Free Rate► Rm is the rate of return on the market

19

Cost of Debt (Rd) UTEFA

► Rd may usually be found on a companies financial statements

► Tells the investor what rate the company borrows at

► If it is not in the financial statements, it may be estimated from similar companies

20

WACC UTEFA

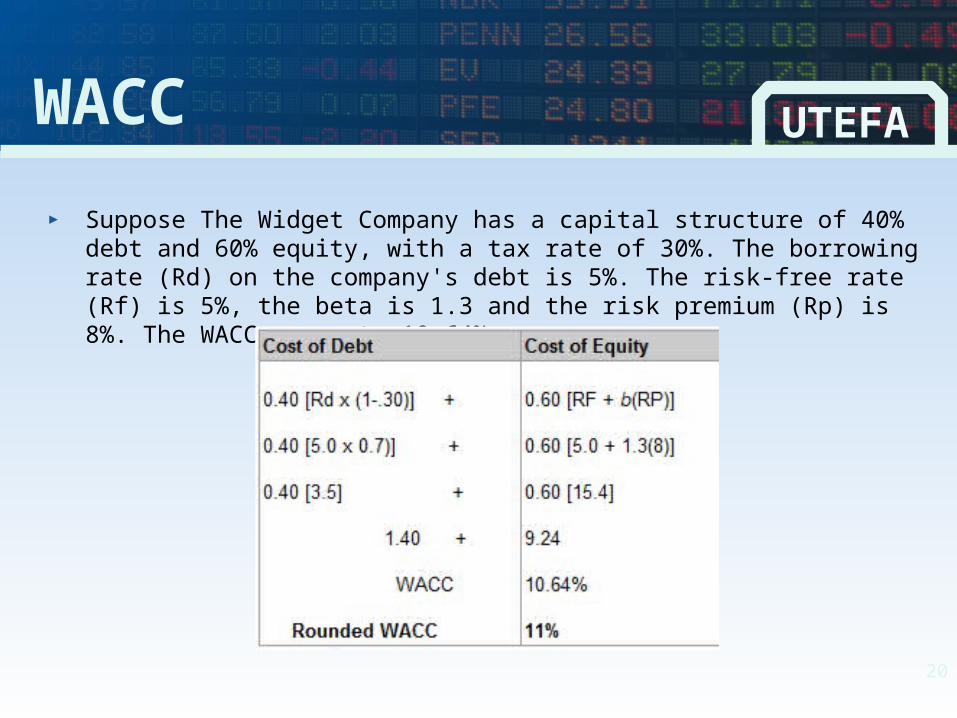

► Suppose The Widget Company has a capital structure of 40% debt and 60% equity, with a tax rate of 30%. The borrowing rate (Rd) on the company's debt is 5%. The risk-free rate (Rf) is 5%, the beta is 1.3 and the risk premium (Rp) is 8%. The WACC comes to 10.64%.

21

Terminal Value UTEFA

► To forecast the companies growth into the future, we use the Gordon Growth Method:

► Terminal Value = Final Projected Year Cash Flow X (1+Long-Term Cash Flow Growth Rate) (Discount Rate – Long-Term Cash Flow Growth Rate)

22

Terminal Value UTEFA

► Assume that the company's cash flows will grow in perpetuity by 4% per year. At first glance, 4% growth rate may seem low. But seen another way, 4% growth represents roughly double the 2% long-term rate of the U.S. economy into eternity.

► Widget Company Terminal Value = $21.3M X 1.04/ (11% - 4%) = $316.9M

23

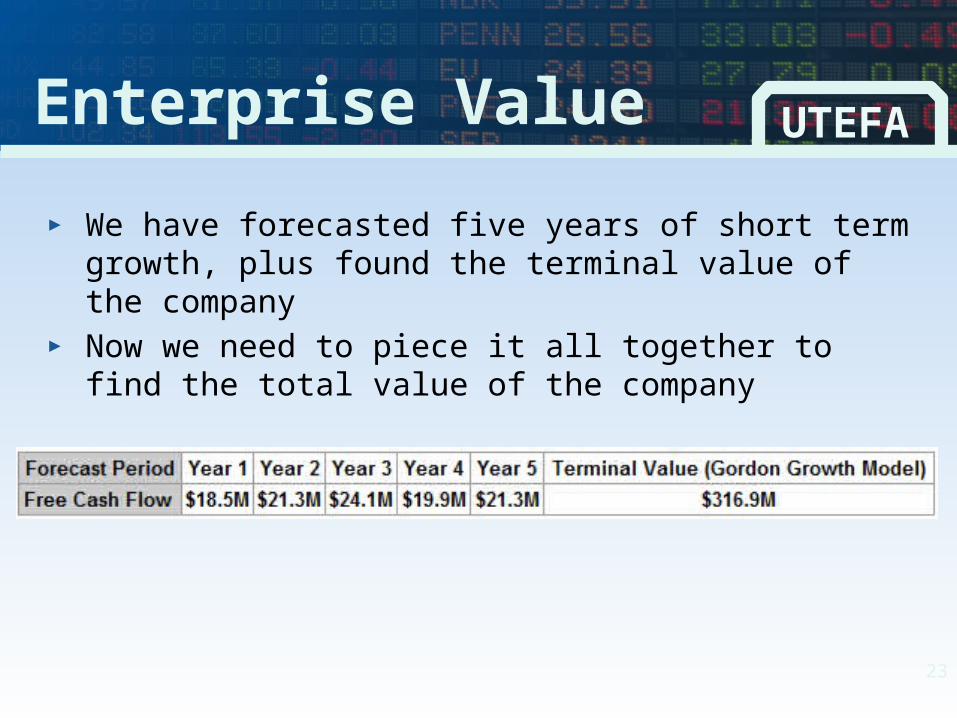

Enterprise Value UTEFA

► We have forecasted five years of short term growth, plus found the terminal value of the company

► Now we need to piece it all together to find the total value of the company

24

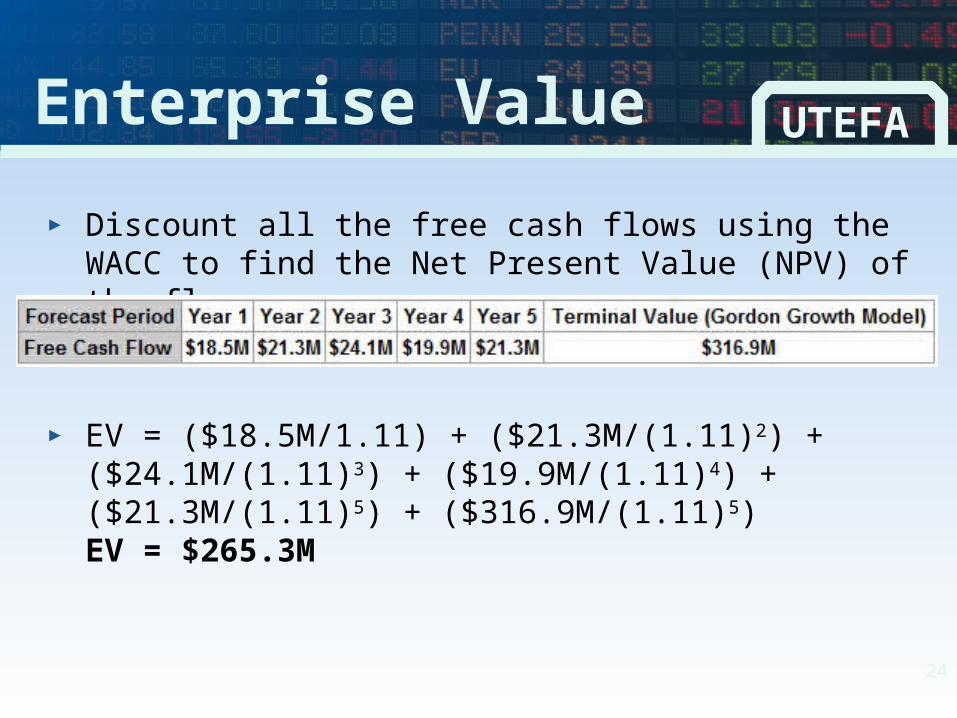

Enterprise Value UTEFA

► Discount all the free cash flows using the WACC to find the Net Present Value (NPV) of the flows

► EV = ($18.5M/1.11) + ($21.3M/(1.11)2) + ($24.1M/(1.11)3) + ($19.9M/(1.11)4) + ($21.3M/(1.11)5) + ($316.9M/(1.11)5) EV = $265.3M

25

Fair Value UTEFA

► Need to account for the debt that a company has► As investors, we are only purchasing equity of a

company so we subtract the debt that the company has on its balance sheet

► Fair Value of Widget Company Equity = Enterprise Value – Debt

26

Fair Value UTEFA

► After we find the fair value for the company, divide that number by the amount of shares outstanding to find the share price

► Say the Widget Company had no debt, and 2 million shares outstanding:

► 265.3 M/2 M = 132.65$ per share fair value

27

Any Questions or Comments?

![Valuation and Discounted Cash Flow (DCF) Analysis … and Discounted Cash Flow (DCF) Analysis Case Study: Jazz Pharmaceuticals [JAZZ] Detailed Stock Pitch Note that this is a lengthy](https://static.documents.pub/doc/80x56/5aea3a637f8b9a90318b5be8/valuation-and-discounted-cash-flow-dcf-analysis-and-discounted-cash-flow-dcf.jpg)