Dealing With Financial Turmoil: The Fed’s Response David C. Wheelock* Federal Reserve Bank of St. Louis November 6, 2008 *Views expressed are not necessarily official positions of the Federal Reserve Bank of St. Louis or the Federal Reserve System.

Transcript

Dealing With Financial Turmoil: The Fed’s Response

David C. Wheelock*

Federal Reserve Bank

of St. Louis

November 6, 2008

*Views expressed are not necessarily official positions of the Federal Reserve Bank of St. Louis or the Federal Reserve System.

The Housing Slump: Root of the Crisis

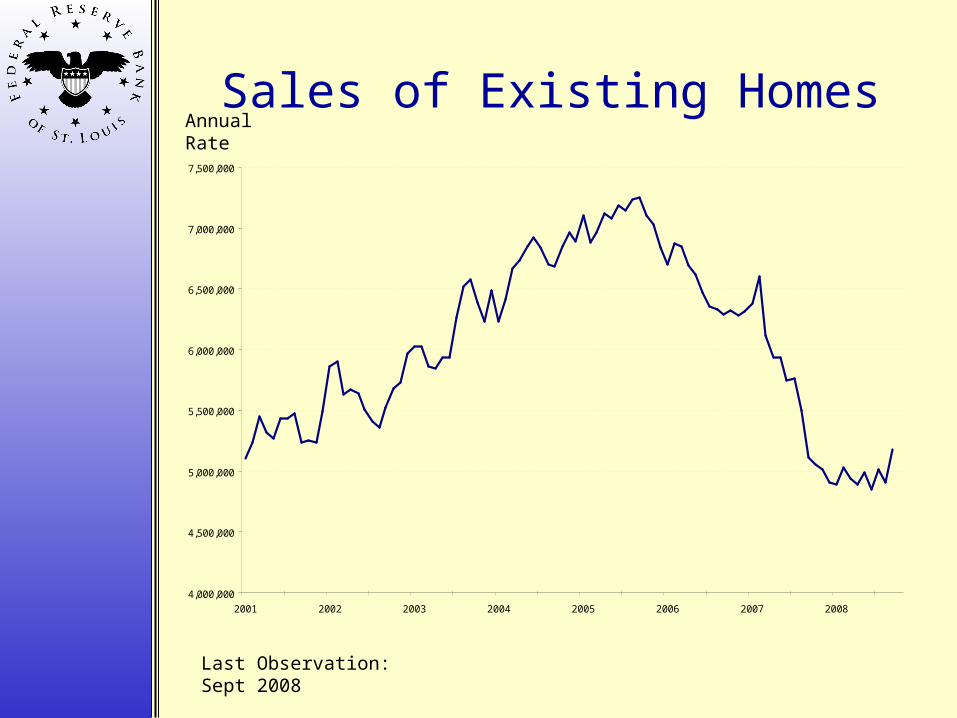

• Declining sales and rising vacancy rates• Less construction• Falling house prices• Rising foreclosure rates

– Cause mortgage-backed securities to decline in value, resulting in large financial losses and uncertainty about viability of counterparties.

Sales of Existing HomesAnnual Rate

Last Observation: Sept 2008

4,000,000

4,500,000

5,000,000

5,500,000

6,000,000

6,500,000

7,000,000

7,500,000

2001 2002 2003 2004 2005 2006 2007 2008

Home Vacancy Rate

1.0

1.2

1.4

1.6

1.8

2.0

2.2

2.4

2.6

2.8

3.0

2000 2001 2002 2003 2004 2005 2006 2007 2008

Percent

Last Observation: Q3:2008

Months Supply of New and Existing Single Family Homes

Last Observation: Sept 2008

Months

0.0

2.0

4.0

6.0

8.0

10.0

12.0

2000 2001 2002 2003 2004 2005 2006 2007 2008

New Single Family Homes

Existing Single Family

Homes

U.S. Building Permits and Housing Starts

Last Observation: Sept 2008

Thousands

750

950

1150

1350

1550

1750

1950

2150

2350

2003 2004 2005 2006 2007 2008

Building Permits

Housing Starts

Median Sales Price of Existing Single Family Homes

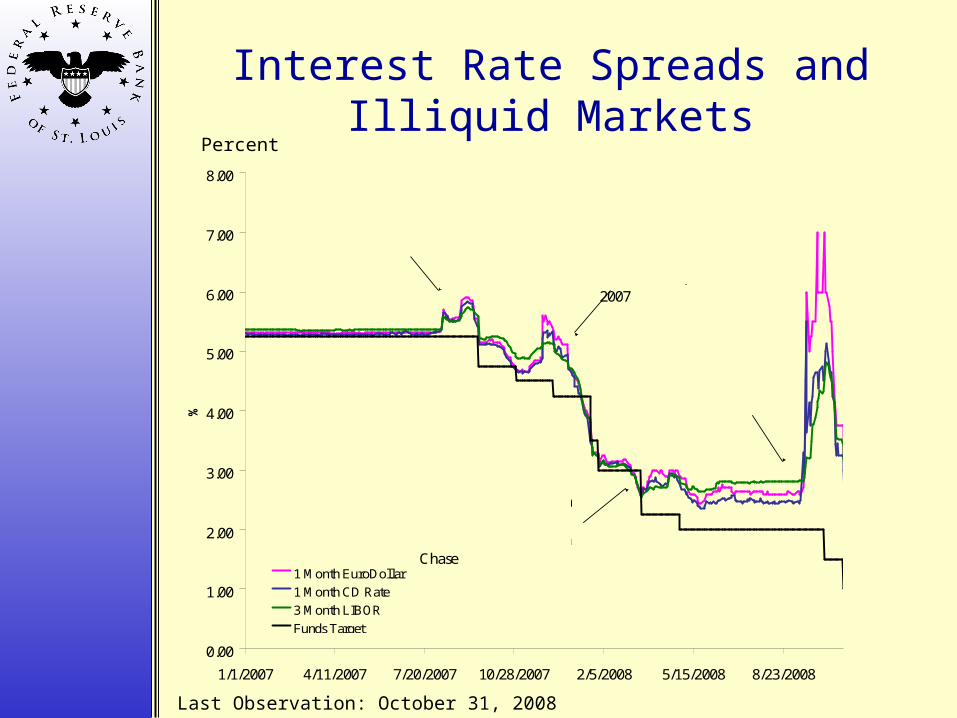

Lehman Brothers files for Bankruptcy, Sept 14, 2008

Term Auction Facility (TAF) Introduced, December 12, 2007

Fed lowers Primary Credit Rate 50 basis points to 5.75%

Fed approves $30 billion for Bear Stearns takeover by J.P. Morgan Chase

Commercial Paper OutstandingSeasonally Adjusted, Billions of Dollars

0.0

200.0

400.0

600.0

800.0

1000.0

1200.0

1400.0

2005 2006 2007 2008

0.0

50.0

100.0

150.0

200.0

250.0

Financial Asset Non Financial

Non FinancialFinancialAsset backed

Last Observation: October 22, 2008

The Fed’s Response

The TAF, TSLF, and PDCF

• Term Auction Facility (TAF): Fed auctions fixed amount of reserves to DIs; provides liquidity while avoiding the stigma of borrowing at the discount window.

• Term Securities Lending Facility (TSLF): Fed lends Treasury securities to DIs in exchange for other marketable assets.

• Primary Dealer Credit Facility (PDCF): Lending facility for all primary dealers, including non-DIs.

Bailouts and Non-Bailouts

• Bear Stearns (March ’08): Fed lent $30 billion to facilitate JPMorgan’s acquisition of Bear. Concern about systemic risk.

• Fannie/Freddie (Sept. ’08): Treasury places in conservatorship, replaces CEOs.

• Lehman (Sept. ’08): Allowed to fail.• AIG (Sept. ’08): Fed lends up to $85 billion

(increased later to $120); CEO replaced. Systemic risk – huge amount of credit default swaps outstanding.

The $700 Billion TARP

Troubled Asset Relief Program• Capital Purchase Program – Treasury will

purchase preferred stock in a qualifying financial firm.$125 billion in nine largest banks

$125 billion in other banks that apply and qualify

• Other program(s) may include purchases of MBSs and loans, insurance of troubled assets, and assistance to borrowers.

Commercial Paper, Money Market Funds

• Commercial Paper Funding Facility (CPFF): Fed will purchase highly-rated unsecured and asset-backed commercial paper.

• Money Market Mutual Fund Liquidity Facility (AMLF): Fed loans to banks to purchase asset-backed paper from MMMFs.

• Money Market Investor Funding Facility (MMIFF): Sets up special vehicles to buy money market instruments. Fed committed up to $540 billion.

Old Fashioned Monetary Policy

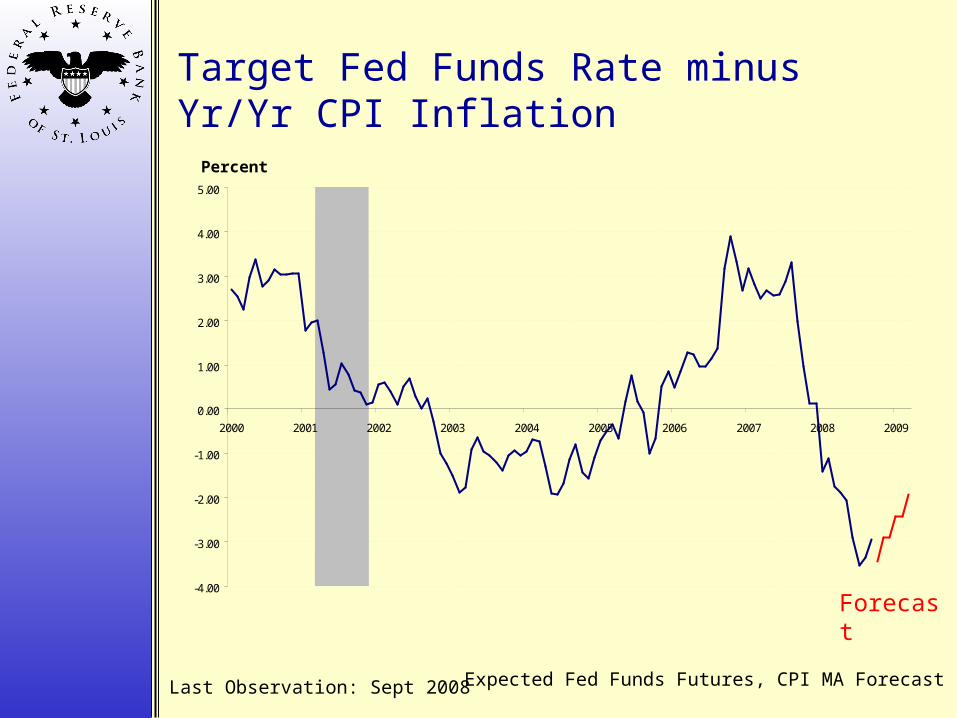

• The FOMC has sharply cut the fed funds rate target – negative real rate throughout 2008.

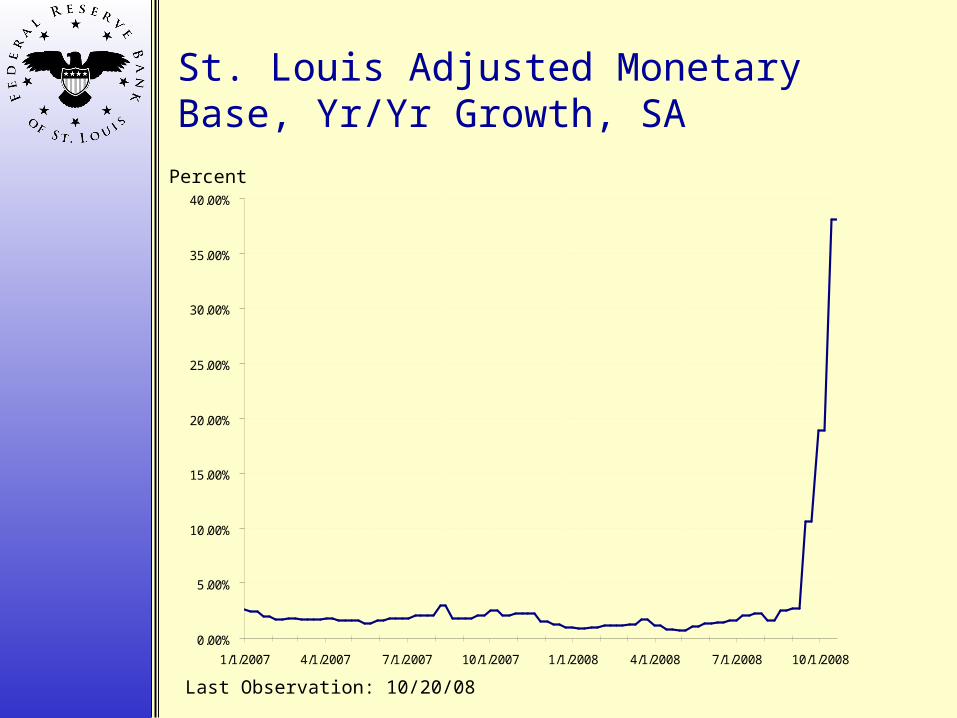

• Monetary base growth – up sharply since September (“quantitative easing”).

Target Fed Funds Rate minus Yr/Yr CPI Inflation

Last Observation: Sept 2008

-4.00

-3.00

-2.00

-1.00

0.00

1.00

2.00

3.00

4.00

5.00

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

Expected Fed Funds Futures, CPI MA Forecast

Forecast

Percent

St. Louis Adjusted Monetary Base, Yr/Yr Growth, SA

• The financial crisis was triggered when house prices began to decline and subprime mortgage defaults increased.

• Subprime accounts for about 10 percent of mortgage market. Subprime ARMs represent about 7 percent of loans, but 43 percent of foreclosures.

• Some $85 billion of losses on non-prime mortgage loans has mushroomed into some $1.4 trillion of losses world wide (IMF estimate).

Summary (2)

• Systemic failure centered in MBSs and other derivatives that have lost substantial market value.

• The Fed (and other agencies) have attempted to contain the crisis and re-start financial markets by providing liquidity and acting as lender of last resort.