2016 turned out to be an eventful and surprising year for the steel industry after all. The biggest story is the strong recovery of steel prices over the course of the year, though not without some worrying pauses and dips in between. At the start of the year, few would have expected the steel industry to stage a rapid turnaround, not after steel prices fell to record lows in October 2015. As it turned out, steel prices started to rebound in March and although prices dipped again in May/June, the upward momentum in price movement has been generally well sustained over the course of the year. The recovery of global steel prices has been led by the spike in Chinese steel prices. The steel industry in China has benefited from the increase in infrastructure spending by the government, a resurging property market and an upturn in the automotive industry following the reduction of taxes on vehicle purchases. The strong rebound in commodity prices, in particular coking coal, which saw its prices trebled between July and November 2016, has also contributed to the higher prices of steel products. Due to the stronger domestic market demand, steel export offer prices from China have also gone up. While the higher export prices have not caused any significant dent in the volume of steel exports from China, with total volume for the period January to November 2016 dipping only 1% year-on-year to 100.68 million tonnes, the higher prices have at least brought some measure of relief to the steelmakers across the globe. Message from the Secretary General China’s economy is widely projected to expand at a comfortable 6.7% this year. However, its economic growth is expected to cool in 2017 as the government tightens monetary policy and imposes curbs to clamp down on asset price bubbles, especially in the property market. Thus, the general consensus is that China’s economic growth rate will slow down to 6.5% next year. The World Steel Association has projected China’s steel consumption to contract by 2% year-on-year in 2017 to 652.3 million tonnes while the China Iron and Steel Association (CISA) has indicated that China’s crude steel production will also decrease in the same year as a result of government measures aimed at reducing capacity. For steel raw materials, the popular consensus is that prices, especially for coking coal and iron ore, which have lost steam, might face further downward pressure. How the above developments will pan out for the global steel industry is anybody’s guess. But what is certain is that price volatility in the steel industry is here to stay. Let us hope for a smoother ride as we move into 2017. TAN AH YONG In ASEAN, the region continues to bear the brunt of the Chinese steel exports. During the period January to October 2016, a total of 30.45 million tonnes of steel products from China found their way into the ASEAN-6 market, representing a full one-third of China’s total steel export volume for the same period. While the influx of steel exports from China into ASEAN is still a matter of great concern to the steelmakers in the region, the regional steel players could at least breathe easier with the recovery of steel prices and many of the steel producers are seeing a gradual return to profit path. Besides the higher steel prices, another factor which has contributed to the improving perfor- mance of the steel companies in ASEAN is the continuing expansion in steel demand in the region. In the first six months of 2016, apparent steel consumption in ASEAN-6 expanded strongly by 19.3% year-on-year to 39.3 million tonnes. With this, steel producers in the region were able to step up their production resulting in output of hot rolled steel products surging 21.3% year-on-year to 16.5 million tonnes in the first half of 2016. The worst appears to be over for the global steel industry and the steel industry in ASEAN. However, the road ahead is still fraught with challenges and uncertainties. How this is going to play out will depend a lot on the develop- ments of the Chinese economy and its steel industry. SEAISI NEWSLETTER December 2016 South East Asia Iron and Steel Institute Publisher: SEAISI Editor: Pichsini Tepa-Apirak Contributing Editor: Josephine Fong Printer: Yeohprinco Sdn. Bhd. Email: [email protected]Tel: 603 55191102 Fax: 603 55191159 Website: www.seaisi.org ISSN 0166-9645

Transcript

2016 turned out to be an eventful and surprising year for the steel industry after all. The biggest story is the strong recovery of steel prices over the course of the year, though not without some worrying pauses and dips in between.

At the start of the year, few would have expected the steel industry to stage a rapid turnaround, not after steel prices fell to record lows in October 2015. As it turned out, steel prices started to rebound in March and although prices dipped again in May/June, the upward momentum in price movement has been generally well sustained over the course of the year.

The recovery of global steel prices has been led by the spike in Chinese steel prices. The steel industry in China has benefited from the increase in infrastructure spending by the government, a resurging property market and an upturn in the automotive industry following the reduction of taxes on vehicle purchases. The strong rebound in commodity prices, in particular coking coal, which saw its prices trebled between July and November 2016, has also contributed to the higher prices of steel products.

Due to the stronger domestic market demand, steel export offer prices from China have also gone up. While the higher export prices have not caused any significant dent in the volume of steel exports from China, with total volume for the period January to November 2016 dipping only 1% year-on-year to 100.68 million tonnes, the higher prices have at least brought some measure of relief to the steelmakers across the globe.

Message from the Secretary General China’s economy is widely projected to expand at a comfortable 6.7% this year. However, its economic growth is expected to cool in 2017 as the government tightens monetary policy and imposes curbs to clamp down on asset price bubbles, especially in the property market. Thus, the general consensus is that China’s economic growth rate will slow down to 6.5% next year.

The World Steel Association has projected China’s steel consumption to contract by 2% year-on-year in 2017 to 652.3 million tonnes while the China Iron and Steel Association (CISA) has indicated that China’s crude steel production will also decrease in the same year as a result of government measures aimed at reducing capacity.

For steel raw materials, the popular consensus is that prices, especially for coking coal and iron ore, which have lost steam, might face further downward pressure.

How the above developments will pan out for the global steel industry is anybody’s guess. But what is certain is that price volatility in the steel industry is here to stay. Let us hope for a smoother ride as we move into 2017.

TAN AH YONG

In ASEAN, the region continues to bear the brunt of the Chinese steel exports. During the period January to October 2016, a total of 30.45 million tonnes of steel products from China found their way into the ASEAN-6 market, representing a full one-third of China’s total steel export volume for the same period. While the influx of steel exports from China into ASEAN is still a matter of great concern to the steelmakers in the region, the regional steel players could at least breathe easier with the recovery of steel prices and many of the steel producers are seeing a gradual return to profit path.

Besides the higher steel prices, another factor which has contributed to the improving perfor-mance of the steel companies in ASEAN is the continuing expansion in steel demand in the region. In the first six months of 2016, apparent steel consumption in ASEAN-6 expanded strongly by 19.3% year-on-year to 39.3 million tonnes. With this, steel producers in the region were able to step up their production resulting in output of hot rolled steel products surging 21.3% year-on-year to 16.5 million tonnes in the first half of 2016.

The worst appears to be over for the global steel industry and the steel industry in ASEAN. However, the road ahead is still fraught with challenges and uncertainties. How this is going to play out will depend a lot on the develop-ments of the Chinese economy and its steel industry.

Ministry imposes safeguard duties on steel imports ..................... 10

Ha Tinh shuts down $79 million steel plant .................................... 11

Russia’s metal exports surge 9% in October on higher prices ........ 11

Brazil’s long steel imports double in November .............................. 11

India: Steel minister says not in favour of protectionist moves ..... 11

Indian demonetization slows automotive sheet demand .............. 12

India may turn net steel exporter .................................................... 12

China’s steel exports down 16% after new tariffs ........................... 13

Joint action can cut steel overcapacity ........................................... 13

China’s finished steel consumption set to drop in 2017 ................. 14

Steel could shine in 2017 as China expands capacity controls ...... 14

Intra-ASEAN Steel Trade: January – July 2016 .................................. 15

2017 SEAISI Conference & Exhibition: Call for Papers ..................... 16

A U S T R A L I A

I N D O N E S I A

Australia starts anti-dumping review of Dongbu flat steel imports

The Australian anti-dumping commission has initiated a reviewof its duties on zinc-coated and aluminium-zinc-coated flat steelproducts exported by South Korean steelmaker Dongbu Steel.

The review, announced on Wednesday December 7, will assessthe period between October 1, 2015, and September 30, 2016, todetermine whether or not the factors determining the anti-dumping duty have changed and the duties are still applicable.

The commission will submit a statement of essential facts to theAustralian parliamentary secretary, in anticipation of a finaldecision, by March 27, 2017.

Australia applied the original anti-dumping duties to a majorityof South Korean exporters in 2013. Dongbu was found to have adumping margin of 5.80% for aluminium-zinc coated steel and3.20% for zinc-coated steel.

Dongbu applied for a review of the duties in 2015, after whichthey were revised so that Dongbu’s products would not be taxedif sold at or above a confidential price determined by theAustralian government.

The aluminium-zinc-coated and zinc-coated flat steel productsin question are classified under Australian tariff codes7210.61.00 (statistical codes 60, 61 and 62), 7210.49.00(statistical codes 55, 56, 57 and 58) and 7212.30.00 (statisticalcode 61).

Metal Bulletin, December 7, 2016

Steel consumption in Indonesia rose in the first half of 2016

Steel consumption in Indonesia is expected to rise to 13-14 milliontons in 2016, from 11.3 million tons in the preceding year. Growthis supported by infrastructure development in Indonesia. Datafrom the Southeast Asia Iron and Steel Institute (SEAISI) showsthat steel consumption in Indonesia rose 11 percent year-on-year (y/y) to 6.4 million tons in the first half of 2016. In fact,many local companies are currently buying steel to fill theirwarehouses as the steel price tends to be highest in the January-February period.

Dadang Danusiri, Co Chairman II Flat Steel Indonesia Iron andSteel Industry Association (IISIA), informed that infrastructureprojects in Indonesia give rise to the nation’s higher steelconsumption. Projects, which are developed by private and state-owned enterprises, include toll roads and power stations.Secondly, steel demand in Indonesia’s automotive industry hasalso been strong, accounting for about 15 percent of totaldomestic steel sales.

He added that domestic steel consumption could rise furtherprovided the central government will force local infrastructuredevelopers to use domestically-manufactured steel. China, whichis plagued by steel overcapacity, has been exporting cheap steelinto Indonesia. This forms a major problem for the domestic

SEAISI Newsletter, December 2016 3

steel industry (which lacks competitiveness). In the first eightmonths of 2016 period China exported 3.8 million tons of steelto Indonesia. However, it is difficult to limit imports from Chinabecause both nations are members of the ASEAN China Free TradeAgreement.

Indonesia Investments, December 16, 2016

Krakatau Steel to acquire 500 hectares of land in Anyer

State-owned steel company PT Krakatau Steel (Persero) Tbk, willacquire 500 hectare of land in Anyer, Serang, Banten, as it plansto develop an industrial area.

Krakatau Steel president director Sukandar said that theacquisition will be carried out by the company’s subsidiary PTKrakatau Industrial Estate Cilegon (KIEC). “The acquisitionprocess is ongoing,” he said Tuesday in public expose, as quotedby Bisnis Indonesia.

Sukandar said that the company will need Rp700-750 billion tocomplete the acquisition, which will be disbursed from internalcash reserves. The company has completed the acquisition of350 hectares of land. It is aiming to complete development of100 hectares of land by 2017.

Moreover, KIEC is exploring opportunities to develop industrialareas in East Java’s Bojonegoro and West Java’s Subang. Thecompany plans to develop the areas together with subsidiariesof other SOEs. Sukandar declined to name them.

At present, Krakatau Steel owns 99.99 percent of KIEC, while theremaining 0.01 percent is owned by PT Krakatau Engineering.KIEC is engaged in industrial (industrial areas, warehousing,offices), commercial (hotels, golf courses and sport facilities)and residential sectors.

The KIEC industrial area takes up a surface area of 550 hectares(industrial area I) and 75 hectares (industrial area II). It is hometo Cigading Port, power plants, industrial water treatment plants,among others.

The KIEC owns The Royale Krakatau Hotel in Cilegon, West Java,situated next to Krakatau Pertama golf course, one of Indonesia’soldest.

Tempo.co, December 21, 2016

J A P A N

Construction of main Tokyo Olympics stadium starts at last

After considerable controversy and some delay, construction ofthe main stadium for the 2020 Tokyo Olympic Games has finallystarted, leading steel industry insiders to predict that steeldemand for Olympics-related projects will become more activesoon.

Initially, construction was to have commenced in October 2015,but the early design was scrapped over its massive Yen 252 billion($2.2 billion) price tag, which would have made the building themost costly sports venue in the world. The project, being managedby major contractor Taisei Corp, was formally launched Sundayto a new design and for a budget of Yen 149 billion. The work isscheduled to be completed by end-November 2019.

A Tokyo-based construction steel trader said that the constructionstart is 13 months delayed but the completion date is only fivemonths later than originally envisaged. As a result, the pace ofbuilding will have to be rapid and so too will be the uptick indemand for construction steel to build it.

“The general contractor has already booked most of the steelmaterials but deliveries will be quicker with the project actuallystarted,” he explained. “Also, work on other construction projectsfor the Olympics will follow so steel product shipments willbecome more active.”

Just last month Tokyo governor Yuriko Koike decided that a newaquatic center would be built but only with 15,000 seats, ratherthan the initial 20,000 seats to reduce costs. She has also decidedan existing canoeing facility was unsuitable and that a newcourse would be built. Piling work on the so-called Sea Forestsvenue officially started on December 8.

“The construction sizes for some facilities have been shrunkbecause of the cost and this may shrink the actual constructiondemand from what we expected,” another trader in Tokyo said.“But the formal launch of key Olympic projects will stimulate thebuilding market generally so we anticipate that market trendsfor construction steel will become active and support a rise inprices,” he told Platts.

Some industry groups estimated in late 2013 that the 2020 TokyoOlympics would boost steel demand by around 2-3 million mt,Platts notes.

Platts, December 12, 2016

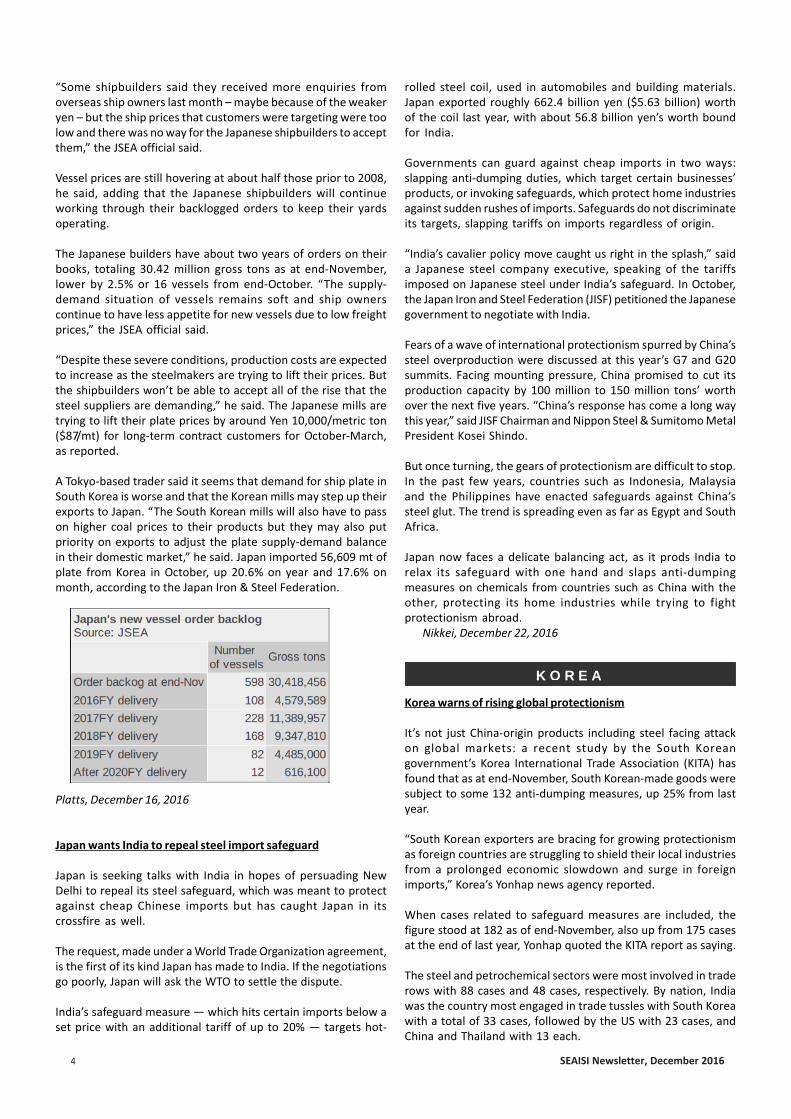

Japanese ship orders decrease again in November

New vessel orders for export booked by the Japanese shipbuildersin November plunged by 59.3% year-on-year to 336,300 grosstons in five vessels, according to new data from the Japan ShipExporters’ Association (JSEA).

The November orders in terms of gross tonnage were up by 169%from October, but a JSEA official downplayed the improvementsaying it was just the timing of the orders received and that therewere still no indications that vessel demand was increasing.

4 SEAISI Newsletter, December 2016

“Some shipbuilders said they received more enquiries fromoverseas ship owners last month – maybe because of the weakeryen – but the ship prices that customers were targeting were toolow and there was no way for the Japanese shipbuilders to acceptthem,” the JSEA official said.

Vessel prices are still hovering at about half those prior to 2008,he said, adding that the Japanese shipbuilders will continueworking through their backlogged orders to keep their yardsoperating.

The Japanese builders have about two years of orders on theirbooks, totaling 30.42 million gross tons as at end-November,lower by 2.5% or 16 vessels from end-October. “The supply-demand situation of vessels remains soft and ship ownerscontinue to have less appetite for new vessels due to low freightprices,” the JSEA official said.

“Despite these severe conditions, production costs are expectedto increase as the steelmakers are trying to lift their prices. Butthe shipbuilders won’t be able to accept all of the rise that thesteel suppliers are demanding,” he said. The Japanese mills aretrying to lift their plate prices by around Yen 10,000/metric ton($87/mt) for long-term contract customers for October-March,as reported.

A Tokyo-based trader said it seems that demand for ship plate inSouth Korea is worse and that the Korean mills may step up theirexports to Japan. “The South Korean mills will also have to passon higher coal prices to their products but they may also putpriority on exports to adjust the plate supply-demand balancein their domestic market,” he said. Japan imported 56,609 mt ofplate from Korea in October, up 20.6% on year and 17.6% onmonth, according to the Japan Iron & Steel Federation.

Platts, December 16, 2016

Japan wants India to repeal steel import safeguard

Japan is seeking talks with India in hopes of persuading NewDelhi to repeal its steel safeguard, which was meant to protectagainst cheap Chinese imports but has caught Japan in itscrossfire as well.

The request, made under a World Trade Organization agreement,is the first of its kind Japan has made to India. If the negotiationsgo poorly, Japan will ask the WTO to settle the dispute.

India’s safeguard measure — which hits certain imports below aset price with an additional tariff of up to 20% — targets hot-

rolled steel coil, used in automobiles and building materials.Japan exported roughly 662.4 billion yen ($5.63 billion) worthof the coil last year, with about 56.8 billion yen’s worth boundfor India.

Governments can guard against cheap imports in two ways:slapping anti-dumping duties, which target certain businesses’products, or invoking safeguards, which protect home industriesagainst sudden rushes of imports. Safeguards do not discriminateits targets, slapping tariffs on imports regardless of origin.

“India’s cavalier policy move caught us right in the splash,” saida Japanese steel company executive, speaking of the tariffsimposed on Japanese steel under India’s safeguard. In October,the Japan Iron and Steel Federation (JISF) petitioned the Japanesegovernment to negotiate with India.

Fears of a wave of international protectionism spurred by China’ssteel overproduction were discussed at this year’s G7 and G20summits. Facing mounting pressure, China promised to cut itsproduction capacity by 100 million to 150 million tons’ worthover the next five years. “China’s response has come a long waythis year,” said JISF Chairman and Nippon Steel & Sumitomo MetalPresident Kosei Shindo.

But once turning, the gears of protectionism are difficult to stop.In the past few years, countries such as Indonesia, Malaysiaand the Philippines have enacted safeguards against China’ssteel glut. The trend is spreading even as far as Egypt and SouthAfrica.

Japan now faces a delicate balancing act, as it prods India torelax its safeguard with one hand and slaps anti-dumpingmeasures on chemicals from countries such as China with theother, protecting its home industries while trying to fightprotectionism abroad.

Nikkei, December 22, 2016

Korea warns of rising global protectionism

It’s not just China-origin products including steel facing attackon global markets: a recent study by the South Koreangovernment’s Korea International Trade Association (KITA) hasfound that as at end-November, South Korean-made goods weresubject to some 132 anti-dumping measures, up 25% from lastyear.

“South Korean exporters are bracing for growing protectionismas foreign countries are struggling to shield their local industriesfrom a prolonged economic slowdown and surge in foreignimports,” Korea’s Yonhap news agency reported.

When cases related to safeguard measures are included, thefigure stood at 182 as of end-November, also up from 175 casesat the end of last year, Yonhap quoted the KITA report as saying.

The steel and petrochemical sectors were most involved in traderows with 88 cases and 48 cases, respectively. By nation, Indiawas the country most engaged in trade tussles with South Koreawith a total of 33 cases, followed by the US with 23 cases, andChina and Thailand with 13 each.

K O R E A

SEAISI Newsletter, December 2016 5

Only last month Thailand’s ministry of commerce imposedtemporary anti-dumping duties on certain imports of weldedpipe from China and South Korea, as Platts reported. Thoseshipped from leading Korean pipe makers SeAH Steel and HyundaiSteel were penalized at 17.22% and 32.62% respectively.

For its part the KITA had argued previously that Korea’s steelimport penetration rate is as much as 41% – far higher than theUS, Japan or China – and emphasized the importance ofmonitoring import trends of major exporting countries to Korea,especially China.

Platts, December 9, 2016

Korean mills target bar-in-coil to edge out rebar imports

South Korea’s major rebar makers Daehan Steel and DongkukSteel Mill are continuing to increase production of bar-in-coil(BIC), citing the product’s higher profitability and efficiency.Daehan was the first among South Korean steelmakers to offerBIC back in mid-2011 by commissioning a 450,000 metric tons/year capacity mill.

Five years later, in February this year, Dongkuk began making theproduct as well.

The officials from both steelmakers emphasized that their mainmotivation was the better profitability and enhanced efficiencyBIC offers. But they admitted too that BIC gives them a competitiveedge over China-origin imported rebars.

“Chinese mills don’t export BIC products to Korea,” the Dongkukofficial said. “Value-added Korean bar products includingearthquake resistant rebars and BIC have helped Korean rebarwin back some of the market share lost to Chinese imports.”During January-October, Korea’s rebar imports from Chinareached at 1.03 million mt, up 18.3% on year.

He added that rebar customers including the large constructionfirms have requested BIC products as they offer better efficiencybecause they can be cut to any length. “Regular rebars generatemuch wastage as their average length is around 8 meters, andanything shorter than 8m has to be cut and the remainder thrownaway as scrap,” the Daehan official said. BIC has lowered hismill’s processing costs, he added.

Both officials confirmed that the average price gap between BICand straight-length rebars is around Won 30,000/mt ($26/mt), amargin both steelmakers have exploited to lift their profitabilityas regular rebars barely generate any profits, they said.

Currently, Daehan is producing around 20,000-25,000 mt/monthof BIC, equivalent to around 240,000-300,000 mt/year, andDongkuk around 20,000 mt/month, equivalent to 240,000 mt/year.

Re-roller Jeil Steel Manufacturing, based in Ansan near Seoul,says it makes BIC by slicing up slabs – mostly bought from Poscobut also imported from China – into billets and then rolling BIC.During January-September Jeil produced a total of 36,792 mt,company data shows.

Platts, December 14, 2016

Mexico to increase import quota of South Korean cold-rolledsteel sheets

The Mexican government has decided to gradually expand itsimport quota on cold-rolled sheet steel from South Korea.Considering the fact that most of Mexico’s exports of cold-rolledsheet steel were materials used in the local plants, such as POSCOMexico, which produces galvanized steel sheets, and Hyundai-Kia Motors plant, the latest decision will help local investedplants to stabilize their business.

The Korea Iron & Steel Association announced on December 18that the Mexican government made a preliminary decision onDecember 16 to increase its import quota regarding cold-rolledsteel sheets imported from South Korea by 40,000 tons in 2017and by 60,000 tons in 2018. This measure is expected tocontribute to the stabilization of the operation of themanufacturing facilities of South Korean companies in Mexicosuch as POSCO Mexico, Hyundai Motor Company and Kia Motorsin that most of South Korea’s cold-rolled steel sheet exports toMexico are used in those facilities.

According to the association, South Korea’s cold-rolled steelsheet exports to Mexico are estimated to increase from 530,000tons to 565,500 tons between this year and next year and then to590,000 tons in 2018 once the preliminary decision is fixed. Thevalue of the exports is estimated to increase by US$22 millionand US$30 million as well, respectively.

South Korean steelmakers are planning to work closely with theSouth Korean government so that the amount of additionalimports can be further increased before the final determinationscheduled for July next year. The Mexican government hadlaunched an anti-dumping investigation on the item in July 2012and stopped the investigation in December 2013 by putting alimit on five-year imports instead of imposing an anti-dumpingtariff.

Business Korea, December 19, 2016

Malaysian Gov’t supports consolidation to create stronger steelplayers

The Malaysian government supports the consolidation of localsteel players to create stronger and more competitive entities tocompete in the global market, says International Trade andIndustry Minister II Datuk Seri Ong Ka Chuan.

“The consolidation among players is of course on a voluntarilybasis,” says the minister. “The ministry, through dedicated agencyMalaysia Steel Institute (MSI), is just undertaking the effort toprovide the platform for the sustainability of the sector.

“The consolidation efforts could include mergers andacquisitions, as well as joint ventures with international partners.

“What we want in the end is that the players are able to produceglobally competitive steel products both in terms of quality andpricing,” he told reporters after delivering his keynote address atthe Iron and Steel Conference: Sustainable Consolidation Effortfor Malaysia’s Iron and Steel Industry recently.

M A L A Y S I A

6 SEAISI Newsletter, December 2016

Ong explained that in the past, steel players had requested theGovernment to increase the import duty on steel productsfollowing the influx of cheaper steel products into the country.

“But increasing the import duty would only solve their problemon a temporary basis, as expensive steel products will haveadverse effects on the construction industry especially, and itwill eventually trickle down to consumers who will have to bearthe brunt,” he said.

MSI estimates that there will be a 40% reduction in the numberof steel upstream and upper-middle-stream players to about 25from 40 companies.

Ong said consolidation is nothing new to the world’s iron andsteel industry. “We have seen it hitting the industry since themerger of steel giants Luxembourg-based Arcelor SA andNetherlands-based Mittal Steel Co in 2006.

“And presently, the merged entity, Arcelor-Mittal, controls 10% ofthe world’s steel production, making the company the numberone steel maker globally. Thus, I urge all industry players to fullyparticipate in this effort,” said Ong. He said this effort alsopromoted healthy competition and the standardizing of steelproduct prices.

“Realizing the challenges faced by the local iron and steelindustry, the Government will continue to support the industry,”he said. MSI intends to embark, as the facilitator, on thisconsolidation effort through three phases over a five-year period.

CFO Innovation Asia Online, December 5, 2016

Steel import permit recalled

The Trade Department recalled the import commodity clearancegranted earlier to Mannage Resources Trading Corp. to ensurethe quality of steel imports in the Philippines

The company earlier used the permit in shipping in 20,000 metrictons of imported Chinese steel bars to the Philippines.

Trade regional director Judith Angeles and Bureau of PhilippineStandards Assistant director and officer-in-charge MarimelPorciuncula informed Mannage president Lawrence Daniel Syon December 8, 2016 about the recall of the permit, documentsshowed.

The Trade Department said the withdrawal aimed to ensure thatshipment and further imports would meet the laws, rules andstandards required for traceability, quality and safety.

The Philippine Iron and Steel Institute, the umbrella organizationfor the local steel industry, was partly relieved by the decision ofthe Trade Department to recall the import certification.

Pisi president Roberto Cola said withdrawal was “in the interestof public safety” and in line with the government and industry’spolicy of strictly enforcing the mandatory standards for steelproducts.

P H I L I P P I N E S

The recall and stricter implementation of mandatory standardsis beneficial to the consuming public as it can lead to stoppingthe proliferation of uncertified or substandard steel bars in themarket.

PISI’s investigations on the October 2013 earthquake in Cebuand Bohol revealed that substandard and uncertified steel barswere used in the damaged buildings and infrastructure.

“The Philippines is located in an earthquake zone and typhoonarea, so the best disaster prevention is to prevent sub-standardmandatory steel products from being sold in the market” Colasaid.

Cola added the local industry “welcomes stricter implementationof standards to be applied to both locally manufactured andimported steel products for the benefit of the Filipino consumer.”

Mannage was also involved in a controversial shipment of 5,000tons of imported steel bars in May 2016, which were orderedheld by Subic customs officials for lack of permits and a legitimateimport clearance certificate.

Manila Standard, December 14, 2016

Singapore rebar market uncertain on two-year price high, Turkishpresence

Import prices for rebar in Singapore have reached levels lastseen over two years ago, but resistance from local buyers andcompetition faced by Chinese suppliers have blurred the near-term outlook for the market.

Metal Bulletin’s assessment for rebar import prices in SoutheastAsia – which mainly takes into account Chinese cargoes soldinto Singapore on a theoretical-weight basis – was $435-450 pertonne cfr for the week ended Monday December 20, wideningupwards by $10 per tonne from the preceding week’s $435-440per tonne cfr.

Prices are at their highest since early September 2014, when theassessment reached $445-455 per tonne cfr.

Major Chinese mills have been offering late January/Februaryshipments of rebar for prices as high as $460-465 per tonne cfrinto Singapore since early last week, when offer prices from Chinaspiked following gains in the domestic market.

Turkish suppliers, however, took advantage of the high pricespursued by Chinese mills and sold a number of cargoes intoSingapore and Hong Kong last week.

Traders and buyer sources in Singapore reported deals fromTurkey at prices ranging between $445 and $450 per tonne cfr.

“The Turkish sold at [as low as] $445 per tonne cfr, which forcedChinese traders to lower their offers,” one trader in China saidon Monday.

At least 30,000 tonnes for Turkey-origin rebar would have beenbooked in Singapore, sources estimated.

S I N G A P O R E

SEAISI Newsletter, December 2016 7

Information from one source about deals booked above $450per tonne cfr could not be verified by Metal Bulletin.

One official at a Chinese steelmaker confirmed his mill had beenunable to secure orders even at offer prices as low as $455 pertonne cfr into the Southeast Asian city-state.

“We had no orders last week, so our mill may consider to lowerits prices,” he said late on Monday.

Some Chinese traders were heard already offering positions atprices below $440 per tonne cfr, but still attracting limited interestfrom buyers.

“Domestic prices [in China] are dropping again,” one trader inSingapore said, noting he was expecting lower export offers fromChinese mills later this week.

China’s spot rebar prices dropped both on Monday and Tuesdaydue to poor demand amid weaker futures and billet prices.

Metal Bulletin, December 20, 2016

Taiwan’s steel scrap imports declined 4% in November

According to data published by Taiwan Customs Department, thecountry’s scrap imports totaled 220,000 tons during Novemberthis year. The imports declined by almost 4% when matched withthe imports of 228,000 tons during the previous month. The USaccounted for bulk of the monthly scrap imports. The importsfrom the US totaled nearly 90,000 tons, constituting over 40% ofTaiwanese scrap imports during the month. The second largestexporter was Japan.

The country’s scrap imports had totaled 228,000 tons in October.The monthly imports had increased by nearly 6% in comparisonwith the prior month. The primary source of import during themonth was the US. The US scrap exports to Taiwan totaled 128,475tons, accounting for nearly 57% of total imports. The secondlargest exporter of scrap to Taiwan during the month wasAustralia with 20,103 tons. The other key import sources wereRussia (12,313 tons) and the UK (7,800 tons).

Taiwan had imported 215,000 tons of scrap during the month ofSeptember this year. The imports dropped heavily by almost one-third when matched with the imports of 320,923 tons during themonth prior to that. The US accounted for more than half of themonthly scrap imports. The imports from the US totaled nearly120,000 tons. The other key sources of import were Japan (27,810tons) and Australia (16,525 tons).

It must be noted that the major Taiwanese long steel productmanufacturer-Feng Hsin Iron and Steel Co. had decided to increaseits scrap purchasing prices for the current week. The scrap buyingprices were increased by NT$300 per ton to range betweenNT$7,400 per ton and NT$7,900 per ton. Meantime, the companyhad also decided to keep the rebar base prices unchanged atNT$14,200 per ton for the current week.

The country’s billet imports too were down significantly duringNovember this year. The imports totaled nearly 100,000 tons,

T A I W A N

falling by almost 52% when compared with the previous month.The sharp cut in imports is on account of surge in internationalbillet prices, Customs Department noted. Russia accounted forhalf of the imports. The billet imports from Russia totaled nearly50,000 tons. The imports of billets from China dropped heavilyto total around 17,000 tons during the month.

The billet imports had totaled 158,000 tons in October, risingsharply by 285% over the previous month. The key exporter ofbillets to Taiwan was Russia. The billet imports from Russiatotaled 80,000 tons, followed by China. The country’s steel billetimports had dropped sharply by 58% month-on-month to 42,000tons in September, mainly on account of rising coke prices.

Meantime, the country’s H-section exports have increased by 5%month-on-month to 20,000 tons in November. The largest importerof Taiwanese H-section was the US. The imports by the US totalednearly 5,000 tons, accounting for almost a quarter of the totalexports by Taiwan. The second largest importer of Taiwanese H-section was South Korea. The Taiwanese rebar exports plungedby nearly 52% over the previous month to total 12,887 tons inNovember. The key importer was Australia with 12,198 tons(nearly 95% share of Taiwanese rebar exports in November).

Shanghai Metals Market, December 15, 2016

WTO rules largely in favour of Taiwan in steel row with Canada

A dispute panel of the World Trade Organisation (WTO) largelyruled in favour of Taiwan on Wednesday on its complaint overanti-dumping duties imposed by Canada on some of its steelgoods.

The ruling, related to certain carbon steel welded pipes andcertain provisions of Canada’s underlying legislation, found thatCanada had contravened the WTO’s Anti-Dumping Agreement butthat Taiwan had failed to establish some points.

Canada slapped duties on some imports of carbon steel weldedpipes from Taiwan in 2012 and Taiwan brought the complaint tothe WTO in Jan 2015.

The annual value of Taiwan’s exports of carbon steel weldedpipes to Canada dropped from around US$19 million before theanti-dumping duties were imposed to around US$5 million,Taiwan officials said at the time of the filing.

A spokesman for Canadian Trade Minister Chrystia Freeland saidCanada will review the decision before deciding whether toappeal. Both sides have 60 days to decide whether to appeal anyof the panel’s findings.

“Canada takes its WTO trade obligations seriously and is alsocommitted to maintaining a strong trade remedy,” spokesmanAlex Lawrence said in an email.

The panel found that Canada acted inconsistently with certainobligations under the WTO and recommended that Canada bringits measures into conformity.

Taiwanese trade officials said that while they welcomed the rulingon Thursday, they also expect Canada will appeal the decision.

8 SEAISI Newsletter, December 2016

“In our filing, we requested the Canadian government to amendits laws,” said Jack Hsiao, an official in the trade negotiationoffice of Taiwan’s cabinet.

Hsiao added that Canadian regulations regarding dumpinginvestigations were problematic and if their appeal were rejectedCanada would need to revise its rules.

Joseph Galimberti, president of the Canadian Steel ProducersAssociation, said the group is “disappointed but not surprised”by the ruling.

Galimberti said the impact of the decision on Canada’s steelindustry is not hugely significant but declined to quantify theimpact. The group’s member companies produce about 13 milliontonnes of primary steel as well as over 1 million tonnes of steelpipe and tube products annually, for sales of about US$4 billion.

“We would not want to speculate on an amount of business onwhich Canadian companies could conceivably lose out or howmarket shares would shift as a result of the ruling,” Galimbertisaid in an email.

Reuters, December 23, 2016

Thai import duties for Japanese steel to be removed

Import duties Thailand has imposed on Japan-origin steel willbe removed from this coming January as per the terms of theJapan-Thailand Economic Partnership Agreement, Japan’sMinistry of Economy, Trade & Industry said Monday.

The Thai government confirmed the change in the steel industrydialogue the two countries held in Tokyo recently, the officialrevealed. “So we don’t need to argue about the import quota inour annual dialogues anymore,” he said. “From the next time wecan just focus on sharing information about the market andtrade conditions in both countries.”

In 2007, Japan and Thailand agreed a limited volume of Japaneseinterstitial-free (IF) steel, pickled coils and hot rolled coils forre-rolling could enter Thailand toll-free. As steel imported abovethe annually agreed volume attracted duties of about 5%, thisquota was a point of friction for both parties in the annualdialogues, as reported.

Those were the only items whose duties were not removed underthe terms of the Economic Partnership Agreement between Tokyoand Bangkok, Meti’s official explained. Their removal and theabolition of the quota scheme will be happy news for Japanesesteel end users in the country, mainly the auto-relatedtransplants, he said.

The final quota Bangkok set for calendar 2016 at 1.33 millionmetric tons was more than double the Thai side’s initialindication, so this year there was no grumble from the Japanesesteelmakers, Platts notes. Japan exported 1.52 million mt of hotrolled coils to Thailand during January-October, up 7.9% y-o-y,according to the Japan Iron & Steel Federation.

T H A I L A N D

The Meti official added that in exchange for introducing the quotascheme permitting duty-free entry of some Japanese steel,Thailand had received Japanese technical know-how in a fewlimited areas such as product inspections. With the terminationof the quota system this support will also end, he said.

Platts, December 6, 2016

Thailand puts safeguard duties on alloy beam imports

Thailand has announced plans to impose a definitive safeguardduty on imports of certain structural sections. In a filing to theWorld Trade Organisation it said the duty would be imposed forthree years from January 2017; the initial rate of 31.43% of theCIF price would decline to 31.05% in year two and to 30.68% inyear three.

The duty follows an investigation by the Ministry of Commercewhich began in February following a complaint by local producerSiam Yamato Steel.

Products affected are alloy-bearing H-beams classified underHS codes 7228.70.10000 and 7228.70.90000. In its WTO filing,the Thai government said imports of these products increased intonnage by 357% between 2011 and 2015, depressing prices andcausing the domestic industry to lose sales volume and revenue.

Thailand said interested parties will have an opportunity to makerepresentations before the duties are implemented, at meetingsarranged for 28 and 29 December. When the investigation wasopened, local sources told Platts they expected China to be theprincipal target, as its alloy-added exports typically contain aminimum content of alloys such as 0.3% chromium.

Platts, December 22, 2016

Thailand tables new standards for rebars

The Thai government has announced the new Thai IndustrialStandards Institute (TISI) standard for carbon steel rebars thatwill be enforced 180 days after December 20, the day the changewas notified in the Thai Royal Gazette.

As with the new standards published in September for hot rolledstructural sections such as angles, channels, I-beams and H-beams, the new standards stipulates the maximum permissiblelevels of elements such as 0.40% for copper and 0.3% chromiumand nickel, Platts understands.

A regional trading source noted the TISI’s new standards willindirectly affect billet imports into the country as these will needto comply with the new rebar chemistry.

TISI’s reviews on steel products are supported by the Thai steelindustry whose members have complained that Chinese suppliersare exporting mild-carbon steel products containing traceelements of alloy with the intent of declaring them as alloy oralloy-added steel in order to enjoy tax rebates.

Platts, December 22, 2016

SEAISI Newsletter, December 2016 9

V I E T N A M

CSC team to assess first Formosa Ha Tinh blast furnace in Vietnam

Taiwan’s China Steel Corp (CSC) has sent experts to Formosa HaTinh Steel in Vietnam this week to assess the condition of theplant’s blast furnace No1 in preparation for its commissioning,officials at CSC have told Metal Bulletin.

A team of 16 experts was sent to the Vietnamese steel plant tohelp Formosa Ha Tinh officials prepare to begin operations aswell as to take inventory of the manpower and equipment at theplant.

The CSC officials were unable to estimate a start-up date for theblast furnace, which was supposed to be commissioned inDecember 2016, but local news reports said that it should becommissioned in the first quarter of 2017.

The Ha Tinh plant is a $10.50 billion, three-staged, integratedsteelworks construction project comprising two blast furnacesand with planned crude steel capacity of 7.50 million tpy in itsfirst stage.

The plant will have a final production capacity of 22.50 milliontpy and will be able to manufacture slab, billet, hot rolled coil,wire rod and bars.

Formosa Ha Tinh is 25%-owned by CSC and 70%-owned byTaiwanese industrial conglomerate Formosa Plastics Group, withJapan’s JFE Steel owning the remaining 5%.

Metal Bulletin, December 6, 2016

Steel industry no longer governed by master plan, says VSA

The Vietnam Steel Association (VSA) has reminded the Ministryof Industry and Trade that the State would no longer manage thesteel industry with any master plan if the Planning Law wasvoted through and put into force in 2018. Regarding the currentpractices, a steel project cannot be approved if it is not named inthe master plan for the industry.

As per the draft Planning Law submitted to the National Assembly(NA), the steel industry and many others will no longer begoverned by planning but by other laws like the Enterprise Law,the Investment Law, the Law on Quality Standards and the Law onEnvironmental Protection, VSA said in a written comment on thedraft planning for the steel industry until 2025, with a vision to2035.

This planning, therefore, will only serve as a reference beforeinvestors make their decisions. Also, the issuance of investmentcertificates will be done according to the opinions of the relevantministries, not just the Ministry of Industry and Trade.

The draft Planning Law stipulates that only 21 industries neednational planning for their use of marine resources and large-scale infrastructure. For most of the other industries, includingsteel, the industry ministry is no longer responsible for doingthe planning.

This draft law has been widely discussed by the NA sinceSeptember, with most opinions against the planning for the steel

industry, yet the industry ministry has still drafted planning andgathered opinions.

Foreign investors should not be invited into the projects to producenormal steel products whose supply is redundant. Instead, theyshould be encouraged to invest in the production of alloy andhigh-quality steel, says VSA in the written comment signed byVice Chairman Nguyen Van Sua.

Currently, domestic investors are capable of developing large-scale steel complex projects. Foreign investors already accountfor a high proportion in the steel industry, so there is no need tocall for others, VSA states. The steel association also notes thatit is a major shortcoming of the industry ministry to adjust theplanning without setting an aim for the development of hot-rolledand high-quality steel, almost 100% of which Vietnam has toimport at the moment. Meanwhile, many projects of constructionsteel and steel billets are still conceived.

VSA also pointed out other faults in the ministry’s draft planning.Remarkably, in this draft planning, a mammoth project for“expansion of the second phase of Thai Nguyen Steel Factory”,which has made losses and remained inactive, is listed as “noinvestor”. This is incorrect since it is a project of Vietnam SteelCorporation and other shareholders.

VSA proposes this project should be thoroughly handled andsimilar projects that have yet to get going should be eliminated,including several other infeasible projects slated for 2017-2025.

VietnamNet Bridge, December 9, 2016

Steel masterplan drops 12 projects

The Ministry of Industry and Trade (MoIT) has removed 12“ineffective” projects from its latest master plan on steelproduction that charts a roadmap for the industry until 2025.

These projects, with a total capacity of 6,520 tonnes of steelingots and 1,350 tonnes of cast-iron and sponge iron, have beenremoved because of ineffective investments and incapableinvestors.

Included in the plan are two huge projects: the 1,000-tonne steelingot factory in Ninh Bình Province, invested in by Kyoei SteelVietnam Company Ltd.; and Phase 3 expansion of the Thái NguyênIron and Steel Corporation in the eponymous province, with anestimated annual capacity of 1,000 tonnes of cast-iron andsponge iron and 1,000 tonnes of steel ingots.

Two steel companies in Hu Giang Province, funded by VietnamSteel Corporation, and the HK and CLC steel factory, jointly fundedby Th Ðc and Biên Hòa steel companies, both designed toproduce 1,000 tonnes of steel ingots annually, are also included.

The list of ineffective projects include several proposed by localauthorities, like the Lào Cai Steel Ingot Factory, the Thiên Thanhcast-iron factory, the second phase of Vietnam-Italia steel plant;and the Qung Bình Cast-iron and Steel factory.

Two projects that don’t have investors are the Hà Giang SteelFactory and the Sõn La steel ingot and cast-iron factory innorthern Sõn La Province.

10 SEAISI Newsletter, December 2016

The new masterplan (with vision till 2035), estimates productionto increase to 21 million tonnes of cast-iron by 2020, 46 milliontonnes by 2025 and 55 million tonnes by 2035.

The country’s current production capacity is around 12.57 milliontonnes of cast-iron and sponge iron and 12.31 million tonnes ofvarious ingots.

Problem projectThe MoIT is looking for capable firms to assess Phase 2 of TháiNguyên Iron and Steel Corporation’s expansion project in TháiNguyên Province.

Based on the evaluation, the Ministry will submit a report to thePrime Minister, proposing feasible solutions for the project’sproblems.

The expansion project a Phase 2, with an estimated investmentcapital of VNÐ3.84 trillion (US$169.3 million), was approved in2005. Funding of 45 per cent each would come from the VietnamDevelopment Bank and Vietinbank and 10 per cent from theinvestor.

Due to price fluctuations and policy changes, the investorsadjusted the project’s investment capital, which was thenapproved at VNÐ8.1 trillion in 2013.

The project includes two main bidding packages. Engineering-procurement-construction (EPC) No. 1 will set up a metallurgyproduction line in Lýu Xá area with a designed capacity of 500,000tonnes of steel ingot per year.

EPC package No.2, which will exploit the Ti n B i ron mine to thetune of 300,000 tonnes a year, came into effect in May 2014.

Meanwhile, Package No1 has been unfinished and at a standstillsince 2012 after Chinese contractor Metallurgical GroupCorporation (MCC) left the project.

Phase II of the Thái Nguyên Steel Plant is a project that hasraised considerable public concern. It is one of the mega projectsof State corporations and groups that many National Assemblydeputies and voters recently raised questions about, relating toits sluggish progress, losses and wastefulness.

Answering these questions at the 14th NA last month, MinisterTran Tuan Anh said the Government had directed relevantministries to inspect these projects and suggest solutions,including revoking the State’s capital and reclaiming assets,clarifying the responsibilities of the organisation andindividuals, and strictly punishing violations.

Viet Nam News, December 12, 2016

Ministry imposes safeguard duties on steel imports

MoIT has worked with 20 steel manufacturers and importersregarding the sharp increase in the volume on steel imports codedHS7213.91.90 after imposing safeguard duties on steel importscoded HS7227.90.00 in April.

Mr. Nguyen Van Sua, Deputy Chairman of the Vietnam SteelAssociation (VSA), said that Vietnam’s steel industry hasn’t

focused on producing steel wire as domestic demand for theproducts is low. However, since duties were imposed on productscoded HS7227.90.00, domestic manufacturers have moved toproduce the products.

According to Mr. Nguyen Phuong Nam, Deputy Head of the VietnamCompetition Authority (VCA) under MoIT, trade defense measuresare an effective tool in protecting domestic manufacturers inany country. If they are not used in this case then the domesticindustry may go bankrupt and steel imported from China couldthen manipulate the market. He added that imposing trade defensemeasure must comply with procedures. “Trade defense is thelast tool to protect domestic industry, not just any individualcompany,” he said. The VCA will continue to collect opinionsfrom domestic steel enterprises until December 31 and will thensubmit a proposal to the Office of the Government.

The management agency also said that steel production inVietnam has recovered thanks to the imposition of temporarysafeguard measures. The volume of imports has fallen whilesteel production in the country has grown.

Volume of steel imports with two codes, 10M 2016

Source: VSA, October 2016

Earlier, 18 domestic steel manufacturers, including Hoa Phat,the Thai Nguyen Iron and Steel JSC, Pomina, Vina Kyoei, VSC-Posco, the Vietnam Germany Steel JSC, the Vietnam Italy SteelJSC, and Southern Steel Company, sent complaints and proposalsto MoIT on handling the importation of rolled steel into Vietnam.

MoIT decided to impose temporary safeguard measures on steelbillets and long steel bar imports, with rates of 23.3 per cent and15.4 per cent, respectively. Domestic enterprises then said thatsteel importers had declared another HS code for rolled steel toavoid being subject to the safeguard duties.

The importers declared rolled steel imports under code7227.90.00 to enjoy zero tariffs. After duties were imposed, importvolumes of the code fell 15.4 per cent. In the first ten months ofthis year, volumes were equal to 58 per cent of those in 2015 asa whole.

VietNamNet Bridge, December 22, 2016

SEAISI Newsletter, December 2016 11

Ha Tinh shuts down $79 million steel plant

The Van Loi Steel Mill, a VND1.8 trillion (US$ 79 million) steelplant in the central province of Ha Tinh, has been offically closeddown due to prolonged financial problems.

A member of Ha Tinh Economic Zone’s management board wasquoted by Lao Ðong (Labour) newspaper as saying on December20 that they have revoked the project’s investment certificate.

Van Loi Steel Mill occupies around 25 hectares of Vung Ang No.1Economic Zone. It received its investment certificate in 2007, butwork at the factory has been suspended for nearly six years now.The plant was supposed to specialise in refining steel and wasto have a capacity of 250,000 tonnes per year in the first phaseof the project and 500,000 tonnes per year in the second phase.It was scheduled to produce its first batch in August 2010, butbecause of financial problems, the project got stalled in 2010.

Ha Tinh Steel JSC, the investor, admitted that it cannot implementthe project as committed.

In 2015, Ha Tinh Steel JSC Director Ho Van Dung said the companyowed banks money to the tune of more than VND750 billion, andthat the machines and equipment imported a decade ago hadrusted and were damaged.

After Van Loi Steel Mill suspended operations, the VND158 billionVu Quang steel production factory, which was set up in 2008 toprovide iron ore to Van Loi Steel Mill, halted operations in 2012as the raw steel produced cannot be used. More than 100 workersof the factory lost their jobs then.

The Vu Quang factory had begun operations in 2009 and had thecapacity to produce 500,000 tonnes per year.

Another project in the province - to exploit Thach Khe ore mine,which has the largest reserves in Southeast Asia - has beensimilarly suspended since 2011 because of capital shortage.

The mining project, which kicked off in 2009 and required a totalinvestment of VND10 trillion, was managed by Thach Khe IronJSC. The mine, with an estimated total reserve of 544 milliontonnes of ore, was expected to become a sound supply source forthe country in the next five years, producing 10 million tonnes ayear. However, two years later, this project ground to a halt, too.

Ha Tinh province officials had held a meeting to discuss thematter and prepared documents to submit to the government.

VietNamNet Bridge, December 23, 2016

Russia’s metal exports surge 9% in October on higher prices

Russia’s ferrous metal product export volumes rose by 9.13%year-on-year in October, to 3.54 million tonnes, according toinformation released by the country’s Federal Customs Serviceon Thursday December 8.

The increase was driven by significant growth in pig iron andfinished flat steel shipments. Pig iron exports skyrocketed by64.37% to 475,700 tonnes, while the finished flat steel exportfigure rose by 20.24%, settling at 638.500 million tonnes.

Semi-finished goods exports went up by 5.57%, to 1.36 milliontonnes. Higher prices in August 2016 year-on-year, when productswere traded for September production and October shipment,were one of the reasons for the increaases.

Metal Bulletin’s price assessment for CIS export pig iron averaged$231.87 per tonne fob Black Sea in August 2016, against $225per tonne fob a year earlier.

The assessment for CIS export hot rolled coil (HRC) averaged$368 per tonne fob Black Sea in August 2016, compared with$333.50 per tonne fob over the corresponding period of 2015.

Metal Bulletin, December 9, 2016

Brazil’s long steel imports double in November

Brazilian long steel import volumes more than doubled inNovember compared with the corresponding period last year.

Imports of non-alloy long steel goods reached 40,021 tonnes,compared with 19,929 tonnes a year earlier, according to figuresreleased by the country’s foreign trade ministry, MDIC, on MondayDecember 12.

This is the first monthly year-on-year rise since May, whenBrazilian long steel imports grew by 15.69% year-on-year.

Currently, Brazilian long steel prices are higher than importprices, which has encouraged the arrival of foreign goods in thecountry, mostly from China, according to local traders.

Long steel imports from China surged to 25,898 tonnes last month,up from 11,959 tonnes in November 2015.

Imports from Turkey came to 3,132 tonnes in November, comparedwith 1,408 tonnes a year earlier, according to MDIC.

Turkish rebar exports to Brazil have been kept at low levels sinceJanuary, when the government opened an anti-dumping probeinto Turkish rebar.

Metal Bulletin, December 13, 2016

India: Steel minister says not in favour of protectionist moves

India’s debt-laden steel industry should not take the government’sprotectionist measures for granted and need to raise theirefficiency to compete with foreign companies, the country’s steelminister told Reuters in an interview. The government has imposedvarious duties and quality controls on imports over the past twoyears to stop the inflow of cheap steel from countries such as

R U S S I A

B R A Z I L

I N D I A

12 SEAISI Newsletter, December 2016

China, the world’s biggest producer burdened with a massiveoversupply.“In my view (protectionist measures) should not be there evenfor a month, but I have to see the overall position of the industry,”minister Chaudhary Birender Singh said in his office.

“I’ve made it very clear to the industry that on one hand, we aregiving this much of protection but on the other hand, I want aroadmap where you can improve upon your efficiency … (to)narrow down the cost of production and sale price.”

Goutam Chakraborty, analyst at Emkay Global Financial Servicesin Mumbai, said Indian companies typically produce commodity-grade steel with lower returns and are less efficient than foreigncompanies producing high-end steel.

BAD DEBTSIndia’s steel sector still accounts for 28 percent of banks’ stressedloans, Singh said, but the government measures have helpedlocal companies including JSW Steel, Jindal Steel and Power,Tata Steel and state-run SAIL to raise prices and improve margins.

Lenders now want the government to help the steel sector withmore steps to expedite the recovery of their loans, including byasking state companies such as SAIL to buy some sick privatesteel assets or manage their operations.

Singh said loss-making SAIL or fellow state steel maker RINL werenot in a position to buy any assets of private companies strugglingto repay loans, but they could help with “expertise” or people.

“It’s very strange. When banks advanced loans to these companies,they never consulted me. (But the) responsibility (of sorting thebad loans) now rests with the steel ministry.”

The government expects India’s steel-making capacity to rise overa third to around 160 million tonnes by mid-2018, for which SAILwill need to speed up its capacity increase that Singh said hadnot been satisfactory.

The company recently signed a technical agreement with SouthKorean steel maker POSCO, which Singh hopes will help raiseoutput. The minister also said Japan and South Korea were keento invest in India’s steel sector and their officials have alreadymet with him.

Hellenic Shipping News Worldwide, December 12, 2016

Indian demonetization slows automotive sheet demand

The Indian government’s demonetization drive is likely to continueimpacting the country’s automotive steel sector as consumersput buying decisions on hold for now – a delay that is alreadycausing problems for steel sheet processors, Platts learnedMonday. “Automobile sales have been completely shattered,” saidan official with a Mumbai-based steel processing center.Consequently, orders for automotive steel processing halvedduring November from the previous month, he estimates.

During November, passenger car sales inched up by a mere 0.3%on-year to 173,606 units, according to the Society of IndianAutomobile Manufacturers, which said automotive sales hadbeen “temporarily disrupted due to demonetization.” Within the

total, sales of utility vehicles slumped by 7.5% y-o-y to 13,573vehicles.In India, passenger vehicle down-payments are typically madein cash, with the balance paid through bank financing, the coilcenter official said. “Demonetization has resulted in a lack ofdisposable cash, forcing consumers to postpone their purchases,”he explained.

“We expect December passenger vehicle volumes (to) also remainsubdued, though some recovery could be expected from Januaryonwards once the liquidity condition improves,” Mumbai-basedratings agency ICRA Ratings said in a recent report. After a robustquarter that ended in September, the domestic passenger vehicleindustry grew by a modest 4.5% during October and growthslowed further during November, ICRA reported.

However, the Mumbai service center official expressed concernthat the slowdown in automotive sheet sales may last throughthis quarter and next. Typically his company forecasts its salesone quarter ahead and the view for next quarter is looking dismal,he told Platts.

India’s overall steel sales during November plunged by 14.3%below October to 6.12 million metric tons, according to recentdata published by the Joint Plant Committee.

Platts, December 13, 2016

India may turn net steel exporter

India is likely to turn a net exporter of steel this year, on the backof an improvement in international prices, led by cost-push anda slump in retail sales, courtesy demonetisation.

During April-November, exports increased 53 per cent over thesame period last year to 4.24 million tonnes (mt). Imports, onthe other hand, dropped 39 per cent to 4.73 mt. Given that thereis still a quarter to go, the sector is expecting exports to surpassimports. The previous year saw a record level of imports at 12.7mt while exports were at 4.6-4.7 mt.

Cost-push has elevated prices in the international market. Lastyear was a bad cycle, said Jayant Acharya, director (commercial& marketing) at JSW Steel. Coking coal prices have been surgingfor a while now. International contract prices of premium hardcoking coal for the third quarter of FY17 have been settled at$200 a tonne, an increase of 116 per cent quarter-on-quarter.Moreover, spot prices have increased from $90 a tonne in July to$315 a tonne.

The increase in input cost is reflecting in steel prices. In the pastthree months, international steel prices have increased by morethan $100 a tonne. “Last year, the situation was volatile andexports had become unviable,” Acharya said.

Sushim Banerjee, director-general of Institute for SteelDevelopment & Growth, said major international markets hadimposed anti-dumping duty against China, which in turn, washelping India.

According to Vikram Amin, executive director (strategy andbusiness development) at Essar Steel, prices across the worldwere showing some buoyancy because domestic requirementshad risen.

SEAISI Newsletter, December 2016 13

“China’s consumption has improved, Europe is picking up, andNorth America had been doing well. So, overall, prices are steady,”said Amin.

Cheap imports from China, South Korea and Japan had put theindustry in dire straits, not only in India but globally. Thesituation prompted the Indian government to come out with aslew of trade measures – safeguard duty, minimum import priceand anti-dumping duty – to support the industry, towards theend of 2015.

The pick-up in international prices is also helping companies tobeat demonetisation. Since November 8, retail sales – that aremostly on account of small house builders, rural and suburban– have taken a massive hit.

“We did not want to sit and wait for things to improve. Wethought we should export more to take the pressure off thedomestic market,” said Amin. Products closer to the end-userand the construction sectors were affected. “Demand for whitegoods and consumer durables were affected and 60-70 per centof the project demand was down. Steel spends can bediscretionary,” a producer pointed out. However, Amin pointedout that some parts of retail sale were beginning to come backover the past week.

Business Standard, December 23, 2016

China’s steel exports down 16% after new tariffs

China’s steel exports plummeted for the fourth straight month inNovember, showing that supplies from the world’s largestproducer were wilting under a barrage of trade measures byother countries.

Its exports of steel products in November dropped 16% comparedwith a year ago to 8.12 million tons, according to Chinese tradedata released Thursday. Exports from January to November fell1% on year to 100.68 million tons.

China, which accounts for around half the world’s steel output,has been flooding markets overseas with cheap steel as domesticdemand has slowed. The U.S., Europe, India and other countrieshave imposed trade measures to stem inflows of Chinese steel toprotect local producers.

This year, the U.S. imposed new tariffs, as high as 266%, on Chinesesteel. China vigorously denies the dumping claims, but leadersof its steel industry pledged to cut back capacity last year amidthe outcry.

“These measures are still in place. It’s unlikely that othercountries are going to remove the measures anytime soon,” saidRajiv Biswas chief Asia-Pacific economist for IHS. “Chinese steelexports will continue to face pressure.”

A boom in China’s housing sales this year has alleviated some ofthe demand pressures on its steel industry, but its sales arelikely to slow next year, with about 20 Chinese cities tighteningloans and sales to check speculative buyers. Around 15% ofChina’s steel demand comes from housing.

The combination of falling exports and slower housing demandis likely to lower steel prices in China and erode margins of itssteel mills, which had returned to profitability this year, Mr.Biswas said. China’s steel industry had a combined loss of 64.5billion yuan ($9.4 billion) in 2015.

Shanghai steel-rebar futures were trading nearly flat at 3,225yuan a ton in Thursday-afternoon trading, reversing sharp gainsthis week amid efforts by China to crack down on illegalproduction of low-quality steel from scrap in Hebei province,the country’s largest steel-producing province, Argonaut Researchsaid.

China has embarked on a program this year to cut back steeloutput capacity by up to 150 million tons by 2020. Nearly 25% ofChina’s steel-production capacity is excess. About 10% of theexcess capacity has been pared back.

Imports of iron-ore from January to November were up 9.2% onyear, while imports during November were up 12% on year,showing that demand for the critical steelmaking material wasstill robust among China’s steel mills.

MarketWatch, December 9, 2016

Joint action can cut steel overcapacity

Due to the feeble global economic recovery and dampened globaldemands, China’s steel industry (and those in other countries)faces overcapacity. During the US presidential campaign, rivalcandidates said that by “dumping its steel products”, China hascaused the American steel sector to lose its competitive edge.During his campaign trail, Donald Trump even threatened toimpose up to 45 percent punitive tariffs on Chinese imports if hewas elected president.

Such rhetoric and protectionist measures, however, will not helpresolve the global steel overproduction issue.

China has exported only about 10 percent of its total steel outputevery year over the past decade, which is far below the 40 percentof some developed steel-producing countries. However, the UnitedStates and some European Union member countries have blamedChina for the global steel overcapacity and launched anti-dumping investigations into Chinese steel products.

In May, the US International Trade Commission invoked Section337 of the Tariff Act of 1930 to formally launch an investigationagainst more than 40 Chinese steel manufacturers, alleging thecompetitive edge they enjoy is unfair.

Ironically, Chinese steel exports to the US and EU countries, involume and value both, account for only a small percentage oftheir steel imports. So, imposing punitive tariffs on Chinese steelproducts can only be a ploy to protect their backward steel sectors.

China has never shied away from accepting its surplus steelcapacity. Instead, it has taken measures to help localgovernments and enterprises to reduce overproduction. InFebruary, the State Council, China’s Cabinet, issued a guidelineto eliminate backward steel capacity, another 100 million to150 million tons of crude steel production will be cut in the nextfive years, with 45 million tons to be slashed this year alone.

C H I N A

14 SEAISI Newsletter, December 2016

Speaking at the opening ceremony of the G20 Hangzhou LeadersSummit on Sept 4, President Xi Jinping reiterated that China willkeep its promise of reducing its crude steel output during thenext five years. Starting late November, the central governmenthas sent several inspection teams to different regions to assessthe progress made in eliminating steel and coal overcapacity.And provinces such as Shanxi, Shandong, Jiangxi, Henan andGuangdong have already completed their tasks for 2016.

Steel overproduction is not an issue for just one country; goingby globalization rules, it’s the concern of all countries. In fact,G20 leaders at Hangzhou agreed steel overcapacity is a globalissue and called for the establishment of a global forum formembers of the G20 and the Organization for EconomicCooperation and Development to share information and worktogether to resolve the issue.

As the host of the Hangzhou summit, China has maintainedcommunication with the parties to help advance the preparatorywork for the establishment of the forum.

China is willing to work with the United States to resolve theglobal steel overcapacity issue. Trump has said he would pushfor $1 trillion spending on infrastructure construction in thenext 10 years that would include building and repairing highways,bridges, airports, schools and hospitals. Since the US cannotproduce enough steel to meet that sort of demand, it can buysome of the steel needed from China. This will not only ease theworld’s steel overproduction pressure, but also boost theeconomic recovery of the US and other countries.

Besides, the China-led Belt and Road Initiative (the Silk RoadEconomic Belt and 21st Century Maritime Silk Road) is expectedto strengthen connectivity and infrastructure construction amongcountries along the routes and thus boost global steel demands.

Hopefully, the US and other steel-producing countries willabandon their prejudices toward China and try to sincerelyresolve the global steel overproduction issue. Only when morecountries make coordinated decisions and strengthen their policycommunications can they eliminate steel overcapacity andachieve win-win results.

China Daily Asia Pacific, December 14, 2016

China’s finished steel consumption set to drop in 2017

China’s consumption of finished steel is set to drop in 2017 afterincreasing in 2016, according to a report released earlier thisweek.

The China Metallurgical Industry Planning & Research Institute,in its report, estimates that the country’s finished steelconsumption for this year would experience a 0.9% increase to670 million tonnes.

Next year, this number is expected to drop 1.5% to 660 milliontonnes, according to the report released on Monday December12. “The increase of consumption in 2016 is mainly attributed tothe big growth in the real estate and automotive sectors,” LiXinchuang, president of the institute, said.

The automakers are expected to increase their consumption by3.7% next year to 56 million tonnes. But various other downstreamindustries are expected to consume less steel.

The real estate sector is expected to consume 354 million tonnesof finished steel in 2017, down 1.7% from this year, while themachinery industry is set to experience a 1.9% drop inconsumption to 126 million tonnes.

The energy, shipbuilding and home appliances sectors too willsee their consumption drop by 0.3%, 4.2% and 0.9%, respectively,according to the report.

The institute estimates that China’s crude steel output will reach806 million tonnes in 2016, up 2 million tonnes from 2015. Thistoo is expected to fall next year by 2.2% to 788 million tonnes.

“Within the big picture of global overcapacity, the shutdown ofinduction furnaces which were used to produce substandardsteel will not lead to tighter supply,” Li said.

Metal Bulletin, December 15, 2016

Steel could shine in 2017 as China expands capacity controls

China has handed the resurgent global steel industry an earlyboost for next year, with a clampdown on illegal mills thatCitigroup Inc says could benefit the world’s biggest producers.

A campaign by China to shutter some induction furnaces, whichuse scrap as a raw material, may hit as much as 5% of thecountry’s output, bank analysts including Jack Shang and TracyLiao wrote in a note received yesterday.

That’s raising prices for Chinese steel, and is poised to prop upiron ore and coking coal markets when blast furnaces ramp upto fill the gap, they said. That will boost steelmakers includingArcelorMittal, the world’s biggest.

“China is the largest exporter of steel in the world and Chineseexport prices effectively put the floor under the global steel pricesin our view,” the analysts wrote. The crackdown is “changing theinvestment case for global steel stocks, iron ore and coking coal,”according to the note.

The closures in four provinces show China is using an expandingtoolbox of policies to restructure the world’s biggest steel industryafter decades of growth.

Stricter environmental rules, and this direct action against illegalsmall producers, add to measures to cut capacity. At the sametime, moves to stimulate growth in Asia’s biggest economy havebenefited global steelmakers, with China’s exports poised to fallin 2016 for the first time in seven years.

Steel in Europe and the US could rise US$50 to US$80 a tonne inthe next month if Chinese prices hold at current levels, Citigroupsaid. The price of benchmark hot rolled coil shipped from Chinahas already jumped to US$530, the highest since 2013, accordingto Beijing Antaike Information Development Co.

W O R L D

SEAISI Newsletter, December 2016 15

Industry data for November shed an early light on how tighterrestraints might play out next year, especially if this year’sresurgent demand is sustained. Run-rates at China’s steelmakersdidn’t budge in November from October, even though prices weresurging on a fresh bout of optimism for demand.

That’s a sign that environmental inspections which began in late-November were already having some impact, analyst Kevin Baiof CRU Group.

Citigroup singled the world’s No.1 producer ArcelorMittal asbenefiting from the furnace shutdowns, because it sells iron oreand coking coal to third parties, as well as shipping steel. Thefirm’s value has surged 135% this year. The swing from scrap tomined raw materials could generate as much as 5 million tons amonth of additional iron ore demand, and an extra 2 milliontonnes of coking coal consumption, helping to prop up prices,Citigroup said.

“China has focused this year on the so-called zombie plants, butnext year it’s going to target operational capacity,” Ren Zhuqian,chief analyst at consultancy Mysteel Research, said fromShanghai last week.

She said it’s possible that steel could follow the coal industrynext year, with more direct government intervention.

“Supply-side reform has effectively lifted coal market sentimentthis year and the market expects that to shift to the steel sector.”

Bloomberg, December 21, 2016

Intra-ASEAN Steel Trade: January – July 2016