17

December 3,2018 Peerless Master Picks- December, 2018 Edition

December 3,2018

Peerless Master Picks- December, 2018 Edition

Peerless Securities Master Picks

Stock Picks for December, 2018

December 3, 2018

COMPANY SECTOR CMP

(INR) RATING

MARKET

CAP(INR

CR)

POTENTIAL

TARGET POTENTIAL

UPSIDE

Axis Bank Banking 625 BUY 161,326 720 15.2%

Godrej Consumer

Products Consumer Staples 771 ACCUMULATE 77,452 880 14.14%

Infosys IT 670 ACCUMULATE 293,782 760 13.43%

Siemens Capital Goods 942 BUY 33,197 1120 18.90%

Godrej Properties Realty 698 ACCUMULATE 15,749 800 14.61%

(Current prices as on closing prices on December 3, 2018 in NSE)

Note: All price target for next 12 months.

Peerless Securities Master Picks

Market Outlook

Emerging Markets assets are seen valuation upgrade post fall in crude oil

prices and weaker US dollar:

� Recent fall in Crude oil prices and weak US dollar would be big macro positive for Indian economy. Key

to sustainable rally in Indian markets depends on sustainability of low crude oil prices going forward. � Valuations have fallen in Indian markets sufficiently to compensate for many key uncertainties. Asset

valuations have reverted from the “expensive” territory at start of 2018 to “now appears REASONABLE VALUATION.

� We see recovery in domestic cyclicals, credit growth in banking in CY 2019-2020. � FII flows in equities to remain volatile till June 2019, as major players are waiting for election outcome. � We remain equal-weight India from a structural perspective. Still now India puts up a brave face in

emerging markets equity sell-off due to macro recovery and resilient GDP growth. We see 12-15% earnings growth in India in FY19.

� RBI policy would be data dependant and we see very slow rate hike in 2019. US Fed expected to slow

down interest rate hikes in 2019 and it would be data dependent. � We are constructive on Indian Markets in 2019 based on current variables.

Key Risks to Markets: 1. Trade War and hike in tariff could hurt global growth. 2. Fading impacts of tax cuts in US could slow down corporate earning in US. 3. Change in US Fed’s current stance of slower rate hike policy. Faster than anticipated rate hike in US

could hurt equity market valuations in Emerging Markets. 4. Unfavourable election outcome in India could drag market valuation. 5. Any big rise in crude oil prices would be negative for India.

Peerless Securities Master Picks

How Benchmark Index- Nifty moved in November 2018

OPEN:10441 HIGH: 10922 CLOSE:10876

Peerless Securities Master Picks

BUY | PERIOD: 12 Months

CMP: Rs.625 | Target: Rs.720

Axis Bank Limited. Sector: Banking | NSECODE: AXISBANK

Axis Bank, headquartered in Mumbai,is the third largest of the private-sector banks in India offering a comprehensive suite of financial products. The Bank offers the entire spectrum of financial services to customer segments covering Large and Mid-Corporates, MSME, Agriculture and Retail Businesses.The Bank has strong and wide network distribution enabling it to reach out to a large cross-section of customers with an array of products and services.It services includes Retail Banking, Corporate Banking(credit, transaction banking, treasury,syndication, investment banking and trustee services,etc) and International Banking.

Investment Theme � Axis Bank posted a better-than-expected Q2FY19 result, boosted

by higher interest income,lower provisions and improvement in asset quality.The net profit rose by 82.6 % Y-o-Y to Rs.789.6 crore.The Net Interest Income(NIM) rose 15% to Rs.5,232 crore, backed by a 11 % growth in loans.The Bank saw a consistent compression in its Net Interest Margin(NIM) and stood at 3.36% this quarter.As per the management the NIM has already hit the bottom and from this level expects either a stability or further strengthening.Axis Bank’s total advances grew 11% Y-o-Y while domestic loans grew 15 % Y-o-Y, the overseas book shrank by 12% Y-o-Y. Its retail loans grew 20 % Y-o-Y and accounted for 49 %of net advances.It saw a corporate credit growth of 0.6% and said that working capital loans grew 21% y-o-y.

� The bank is continuously witnessing a steady improvement in the overall asset quality environment.All key metrics, like new NPA formation,recoveries,credit costs,NPA ratios, continue to see strong improvement.Gross NPA stood at 5.96% as compared to 6.52% in the previous quarter and the Net NPA ratio fell to 2.54% from 3.09% in June. Slippages from standard to bad loans declined 69% Y-O-Y to Rs.2,777 crore, lowest in the last three years. Provisions during the quarter declined to 6.78%.While total deposits grew by 15% over the year, CASA (current account and savings account) deposits grew by 9%, constituting 48% of total deposits with the bank as at the end of September 2018. Moreover, the Bank will not be impacted much by the IL&FS crisis since it has negligible exposure.The Bank’s has a total outstanding of Rs.825 crore which is approximately 10-25 bps of its total loan.

� There is a strong indication of internal cleanup and turnaround.The Board has appointed Amitabh Chaudhry as the Managing Director and later as Chief Executive Officer in place of Shikha Sharma.It has roped in Grish Paranjpe as an additional independent director.

Company Data

Market Cap (cr) 161,326

52 week high (Rs) 677

52 week low (Rs) 481

3m average volume NSE 11,040,840

Beta 1.25

Face value ( RS ) 2

Key Financials

Category FY18 FY17 FY16

Net Sales (Cr) 56747 56233 50359

EBITDA (Cr) 16162 18093 16547

PAT (Cr) 275 3679 8223

Net Profit Margin

(%) 0.6 8.26 20.06

EPS (RS) 1.1 15.4 34.6

Book Value (Rs.) 247 232 223

P/BV(x) 2.1 2.1 2

RoNW(%) 0.43 6.59 15.46

RoCE(%) 6.43 7.66 7.89

Peerless Securities Master Picks

The Bank also stated that its present Deputy Managing Director V.Srinivasan will not seek re-appointment at the end of his current term.This will instill faith among the shareholders regarding the Bank’s credibility, work transparency and management efficiency, and will impact the Bank positively.

� Going forward, the Bank’s balance sheet clean-up is expected to get over and the earnings should return to normalcy in the later half of FY19.The bank is also continuously improving its Provisioning Coverage Ratio(PCR) and a gradual improvement in core operations is expected as credit cost normalized with positive bias on NIMs and improving loan growth.

Technical Outlook � The stock has been in its long time consolidating pattern since May

2016 and in last 2 years it has formed a classical bullish formation of Ascending triangle. Such formation acts strongly when it breaks out and longer time it occurs to form, the more confirmation it takes for breakout confirmation.

� Directional indicator in weekly chart MACD and momentum indicators Stochastic and RSI are showing strength and the direction of the stock is clearly up.

� Recently it broke the upper end of the triangle giving strong bullish

breakout above INR 612. Target of this breakout is around INR 800. However intermediate level of resistance lies around INR 730.

Peerless Securities Master Picks

ACCUMULATE | PERIOD: 12 Months

CMP: Rs.771 | Target: Rs.880

Godrej Consumer Products Limited. Sector: Consumer Staples | NSECODE: GODREJCP Godrej Consumer Products Limited (GCPL) is an Indian consumer goods company based in Mumbai.GCPL is among the largest household insecticide and hair care player in the emerging markets.GCPL's products include soap, hair colourants, toiletries and liquid detergents.The company’s portfolio of brands include Good Knight,Godrej Expert, Cinthol,Godrej No.1,HIT, Protekt, Godrej AER,Ezee, B Blunt, to name a few.GCPL has a wide distribution network across India.It makes sales in both urban and rural markets enabling it to benefit from the opportunities in both segments.

Investment Theme � The homegrown FMCG major GCPL posted a steady quarter.It

posted a net profit of 59.61% Y-O-Y jump in consolidated net profit at Rs 577.73 crore.Consolidated total revenue from operations increased by 6.09%,driven by healthy growth of 10% in domestic business (branded volume growth stood at 5%).However, the consolidated EBITDA contracted by 7.7% while EBITDA margins contracted 273bps YoY.The margins contracted mainly due to the raw material inflation and rise in advertisement cost.GCPL had a mixed performance in Q2 FY19.The Indian business delivered double-digit sales growth and strong profit growth. However, the performance was impacted by poor performance from its international business(1% reported growth, 6% constant currency growth). Indonesia continued its strong recovery, while Africa and Latin America recorded relatively weaker performances due to adverse macroeconomic conditions.

� The company is relentlessly focussing on becoming more agile and

increasing the pace of innovation.Launched liquid handwash (opportunity size of Rs8,000cr in handwash category) at disruptive price point of Rs15 for 200ml refill and Rs35 for combi-pack (with dispenser).Entered into male grooming category (opportunity size of Rs3,500cr) and launched After shave, Shave + Face wash, Beard range, hair cream and body wash under the brand Cinthol. The company forayed in herbal based powder (HBP) hair colours (opportunity size of Rs1,000cr) and the product is made available in 3 shades at disruptive price point of Rs10 pack under brand Godrej Nupur.Introduced new paper based mosquito repellent in Indonesian market.

Company Data

Market Cap (cr) 79322

52 week high (Rs) 978

52 week low (Rs) 637

3m average volume NSE 1044868

Beta 1.15

Face value ( RS ) 1

Key Financials

Category FY18 FY17 FY16

Net Sales (Cr) 9950 9343 8507

EBITDA (Cr) 2174 1973 1635

PAT (Cr) 1633 1307 830

Net Profit

Margin (%) 16.59 14.1 9.85

EPS (RS) 24 19 24

Book Value (Rs.) 91.9 155.7 125.6

P/BV(X) 11.9 10.7 11

RoNW(%) 26.11 24.59 19.39

RoCE(%) 16.67 13.45 19.39

Peerless Securities Master Picks

� Across the board, the company is eyeing a rise in the company’s

rural growth, which has been doing nearly 2X of urban growth. MSPs increases, the government's stimulus and various social programmes have helped the to see healthy momentum.

� Led by demand uptick and company led initiatives towards

constant focus on product innovation, increasing penetration & distribution reach and sustained brand building efforts, we estimate GCPL’s consolidated Revenue and PAT to grow by 12.5% & 16% CAGR respectively.Volume offtake in the domestic business is likely to remain healthy with meaningful contribution expected from new products. While the market environment remains challenging for the international operations, especially in Indonesia and South Africa, it is expected to revive gradually going forward on the back of innovative launches and effective marketing initiatives.The overall margin trajectory for GCPL is expected to improve in the coming quarters on the back of improved profitability from the overseas business (especially Africa & Latin America), improving mix and cost cost efficiency measures.

Technical Outlook � The stock has been in classical uptrend making higher top higher

bottom formation since last many years. In last 3 years, the stock has continuously started it upmove whenever it comes to 100wema(Weekly exponential moving average) and moves above it. Thus it provides good opportunity to enter the stock as it has taken support and moved above 100wema.

� The support of the stock also was at its weekly Donchian channel

and historically whenever it comes around its support lies the stock after taking support starts its upmove.

� Trix indicator also has come to its oversold zone and this is the

third occasion in last 3 years where it came and such levels always has given start of rally in medium to long term.

� The stock is in its fresh leg of its upmove and we expect price

target of INR 880 in time frame of around 12 months.

Peerless Securities Master Picks

Infosys Limited. Sector: IT|NSECODE: INFY

Infosys Limited, based in Bengaluru,is the second largest Indian IT company.Infosys Limited is engaged in consulting,information technology, outsourcing and next-generation services.It provides software development, maintenance and independent validation services to companies in finance, insurance, manufacturing and other domains.One of its known products is Finacle which is a universal banking solution with various modules for retail & corporate banking.Its key products and services are:NIA - Next Generation Integrated AI Platform,Infosys Consulting - a global management consulting service,Infosys Information Platform (IIP)- Analytics platform, EdgeVerve Systems which includes Finacle, a global banking platform,Panaya Cloud Suite,Skava.

Investment Theme

� Infosys Limited reported a decent Q2 performance with steady execution, stable execution, stable margin and strong deal wins.However, the overall performance was dragged down by muted revenue and margins.The firm’s net profit rose 13.6 percent sequentially to Rs 4,110 crore in the second quarter.Revenue for the quarter rose 17.30 per cent on a yearly basis to Rs 20,609 crore.Operating profit rose 14.7 percent to Rs 4,894 crore, however the operating margin remained largely flat at 23.7 percent.It maintained revenue guidance for 2018-19 in constant currency at 6-8 percent.

� Large deal wins at over $2 billion during the quarter demonstrate that the firm has increased client relevance and also give us better growth visibility for the near-term.Infosys Consulting Pte Limited, a wholly-owned subsidiary of Infosys, signed an agreement to acquire 60 per cent stake in Trusted Source, a wholly-owned subsidiary of Temasek Management Services), a Singapore-based IT services company, for a total consideration of up to SGD 12 million (about $9 million). That apart, in October, Infosys Consulting acquired 100 per cent of voting interests in Fluido Oy (Fluido), a Nordic-based salesforce advisor and consulting partner in cloud consulting, implementation and training services for a total consideration of up to Euro 65 million (approximately $75 million).

Company Data

Market Cap (cr) 293303

52 week high (Rs) 754

52 week low (Rs) 475

3m average volume NSE 7922502

Beta 0.65

Face value ( RS ) 5

Key Financials

Category FY18 FY17 FY16

Net Sales (Cr) 73715 71564 65564

EBITDA (Cr) 22204 21684 20202

PAT (Cr) 16100 14383 13492

Net Profit

Margin (%) 22.82 21 21.6

EPS (RS) 71.1 62.8 59

Book Value (Rs.) 298.4 301.5 269.9

P/BV(X) 3.8 3.4 4.5

RoNW(%) 24.68 20.8 21.84

RoCE(%) 30.92 20.69 21.71

ACCUMULATE | PERIOD: 12 Months

CMP: Rs670.| Target: Rs.760

Peerless Securities Master Picks

� Infosys is a global leader in next-generation digital services and

consulting ,and continue to strive to maintain its strong valuations in the coming financial years. Infosys is looking to shift focus back to business after being hit by a boardroom coup and a leadership change last year. It's bet for revival is its digital offerings that already contribute slightly over a quarter of the revenue. Its four-pronged strategy includes scaling up digital services, reskilling employees to match the new needs of the industry,hiring more local workers in offshore centres in the U.S. and Europe while also holding its fort in their core business.Now the company has complete brand clarity and stability has been restored.The company has set up three year roadmap to achieve their objectives FY19: Stabilising business, FY20: Build momentum and FY21: Accelarate the business.

Technical Outlook � The stock corrected 50% of the rally from September 2017 and

took support around its 50wema. Thereafter it closed on weekly basis with engulfing bullish candlestick pattern along with strong volumes, suggesting the fall from its top made in September 2018 is over. Donchian channel support also has been taken by this stock.

� Technical indicators Stochastic is in oversold zone and turned up giving positive crossover indicating upmove to continue. William %R and RSI are also above 50 indicating strength to continue in medium term.

� We expect the stock to move up and price target for the stock is likely to be INR 760 in time frame of around next 12 months.

Peerless Securities Master Picks

BUY | PERIOD: 12 Months

CMP: Rs.942 | Target: Rs.1120

Siemens Limited. Sector: Capital Goods |NSECODE: SIEMENS Siemens Limited is the Indian subsidiary of German multinational engineering and electronics conglomerate Siemens that focuses on IT and management services.It is engaged in manufacturing of electric motors, generators, transformers and electricity distribution, and control apparatus; general purpose machinery, and electrical signaling, safety or traffic-control equipment.It segments include Power &Gas, Energy Management, Building Technologies, Mobility, Digital Factory, Process Industries & Drives, Healthcare, Metal Technologies & Others, including services provided to group companies and lease rentals.It is one of the leading producers of technologies for combined cycle turbines for power generation; power transmission and distribution solutions.

.

Investment Theme

� Siemens Limited reported its best quarterly performance in over

six financial years on higher revenue across all segments, led by building technologies, power and gas, and mobility.The company’s revenue in the July-September period stood at Rs 3,939 crore—the highest since the second quarter of the financial year 2011-12.Siemens’ top line was aided by incentives worth Rs 67 crore under the Merchandise Export from India Scheme.Profit, however, fell 55% over the last year to Rs 279 crore due to an exceptional gain of Rs 560 crore in the base quarter on selling their land at Worli. Adjusted for the exceptional gain, profit grew 39%. The company’s operating income grew 32% that led to a 600-basis-point jump in margin.

� The company’s new orders saw strong growth of 38.1 percent to Rs 3720 crore compared to Rs 2694 crore in the same quarter last year.As per the management order inflows in the business continues to grow and the growth is robust across most of their divisions.At present, for Siemens India orderbook, contribution from the private sector remains stable in the 40% and 60% range.The company sees signs of revival of capital expenditure in India.Recently, it has acquired two large projects of more than Rs.1 billion value, from power and mobility segments.Siemens’ subsidiary company -- Siemens Gamesa Renewable Power has bagged a wind energy order from ReNew Power for construction of 150 MW wind farm located in the Kutch district, in the state of Gujarat.Going forward, the management sees revival signs in these sectors and large project opportunities.

� Siemens continues to gather momentum in

digitalization.Recently, it has launched its digitalization platform Mindsphere in India along with four application centres.Mindsphere is open,cloud- based operating system for the Internet of Things(IoT) that connects products,plants,systems and

Company Data

Market Cap (cr) 33693

52 week high (Rs) 1336

52 week low (Rs) 850

3m average volume NSE 538067

Beta 1.23

Face value ( RS ) 2

Key Financials

Category Sep18 Sep17 Sep16

Net Sales (Cr) 13005 11269 10972

EBITDA (Cr) 1596 1305 1137

PAT (Cr) 893 1133 2888

Net Profit Margin

(%) 10.29 21.71 11.25

EPS (RS) 25 31.8 81.1

Book Value (Rs.) 216 184.9 144

P/BV(X) 5.5 6.7 9.2

RoNW(%) 14.71 43.87 23.08

RoCE(%) 14.23 42.24 21.15

Peerless Securities Master Picks

machines with advanced analytics capabilities.It has also signed a Memorandum of Understanding(MOU) with Bangalore International Airport Limited to jointly drive the digital transformation of Kempegowda Airport.Another step in this regard is its acquisition of U.K. based Lightwork Design to deliver advanced 3D data visualizaton.This will provide customers with enhanced 3D data visualization, high-end rendering and virtual reality(VR) capabilities via its comprehensive suite of 3D product lifecycle management (PLM) applications.

� Going forward,Siemens delivered a strong execution across all

verticles. The company constantly focuses on engineering excellence, innovation, quality and reliability, and is focussing on leveraging the rising digitisation trend. The base business are likely to drive the earnings growth in upward direction as the order inflow in the base business continues to remain strong and is expected to improve as the private sector capital expenditure revives.On the bigger upside, a recovery in growth and improvement in profitability is expected over the next two to three years.The company is focusing in the areas of electrification, automation and digitalization.And with the Indian economy witnessing infrastructural growth the company gains a competitive edge. Given its wide portfolio, the company is best placed to benefit from recovery in capex cycle as and when it happens.

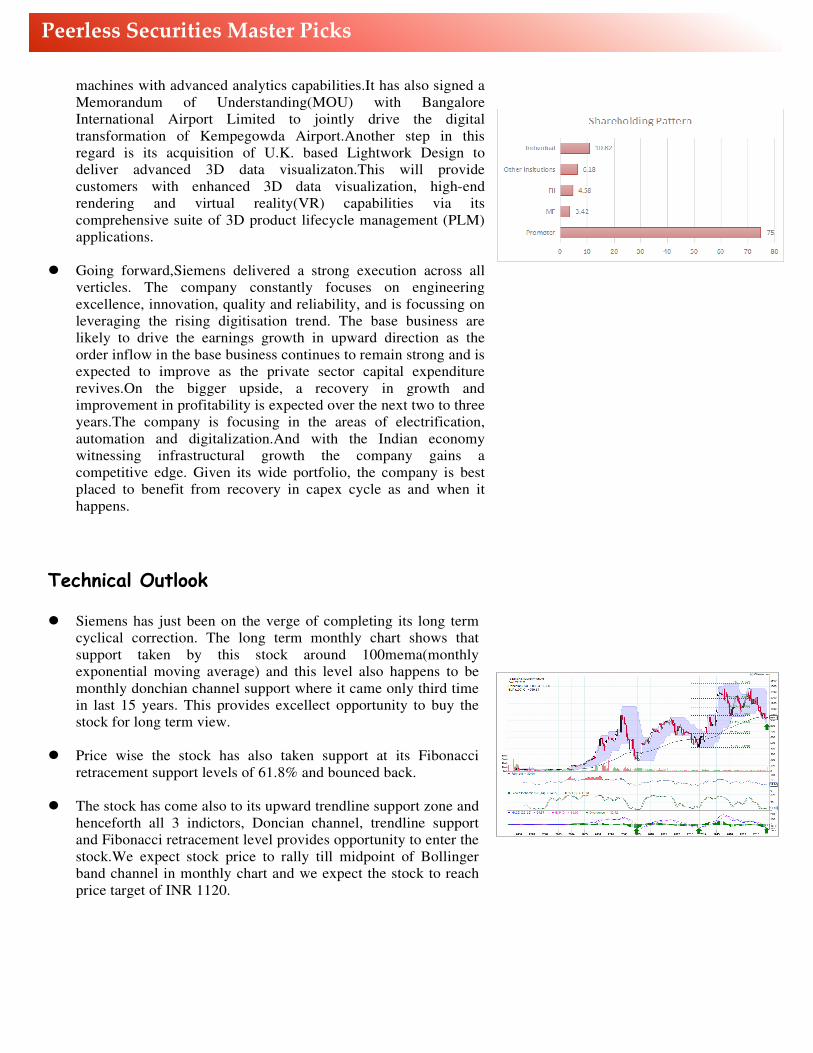

Technical Outlook � Siemens has just been on the verge of completing its long term

cyclical correction. The long term monthly chart shows that support taken by this stock around 100mema(monthly exponential moving average) and this level also happens to be monthly donchian channel support where it came only third time in last 15 years. This provides excellect opportunity to buy the stock for long term view.

� Price wise the stock has also taken support at its Fibonacci

retracement support levels of 61.8% and bounced back. � The stock has come also to its upward trendline support zone and

henceforth all 3 indictors, Doncian channel, trendline support and Fibonacci retracement level provides opportunity to enter the stock.We expect stock price to rally till midpoint of Bollinger band channel in monthly chart and we expect the stock to reach price target of INR 1120.

Peerless Securities Master Picks

ACCUMULATE | PERIOD: 12 Months

CMP: Rs.698 | Target: Rs.800

Godrej Properties Limited. Sector: Realty |NSECODE: GODREJPROP Godrej Properties Limited is a leading real estate company with its head office in Mumbai. A subsidiary of Godrej Industries Limited, the company is operational in twelve major cities across India.The Company is engaged in construction and real estate development.Currently, the business focuses on residential, commercial and township developments. They undertake the projects through in-house teams and by partnering with companies with domestic and international operations.The realty firm has successfully delivered 18 million sq ft of real estate in the past five years. It had about 145 million sq ft of developable area across India.

Investment Theme � The company has reported a multi-fold rise in second quarter

consolidated net profit to Rs 20.6 crore YoY. The growth was largely driven by higher revenue, tax reversal and other income.Consolidated revenue during the quarter grew by 25.6 percent to Rs 393.2 crore compared to year-ago.At operating level,the company witnessed a de-growth in consolidated EBITDA at Rs.11.6 crore due to rising finance cost and cost of sales.

� Godrej Properties sales performance have been good despite

overall slowdown in the property market and thus has helped the company to achieve a better debt management.The company has reduced its net debt by 51 % in last one year to Rs 1539 crore and net debt-equity ratio has also reduced to 0.6 from 2.08 during the period under review.The average borrowing cost stood at 7.88% as against 8.1% a year-ago. As per the management this year the company witnessed the best ever growth in terms of value and volume of real estate.The company have well diversified portfolio and aided by debt reduction, have ventured into affordable housing where growth is currently the highest.

� The ongoing liquidity crisis in the non-banking finance company

(NBFC) space may have hit the prospects of small realty players, but the bigger entities like Godrej Properties with deep pockets and better cash flows are unfazed. It has in fact opened up a big window of opportunity for them to acquire land parcels aggressively.In a highly competitive real estate business environment the bigger players are better equipped to ride this storm and continue to deliver.The sector will also witness large scale consolidations and will provide the big players with economies of scale.

� In the backdrop of all these developments the company expects a strong financial growth in the coming quarters.The company

Company Data

Market Cap (cr) 15749

52 week high (Rs) 920

52 week low (Rs) 460

3m average volume NSE 171706

Beta 1.2

Face value ( RS ) 5

Key Financials

Category FY18 FY17 FY16

Net Sales (Cr) 2390 1701 2252

EBITDA (Cr) 497 371 266

PAT (Cr) 228 175 143

Net Profit

Margin (%) 12.11 11.06 6.75

EPS (RS) 10.8 9.6 7.5

Book Value (Rs.) 103 92 81

P/BV(X) 7 4.2 3.6

RoNW(%) 10.48 10.32 8.98

RoCE(%) 8.53 8.32 5.4

Peerless Securities Master Picks

expects the pace of project additions to accelerate and with the number of important launches in pipeline the sales will witness strong growth.Its ‘Asset Light Business Model’,where the company generally ties up with land owners to develop projects, helps the company to have a better risk management and enables the company to undertake more projects without having to invest large amount towards additional acquisitions. All these will help the company to scale new heights.

Technical Outlook

� The stock has been in strong up move since Jan 2017 and

thereafter it took sharp downmove. However it took support around INR 500 where double bottom support took place and price recovered strongly .

� The support level around INR 500 also happened to be 200

wema(weekly exponential moving average) and price then broke out of the downward trend line which lasted of around last 4 months. This shows that the stock price has now moved and price is likely to retrace on upside at least till 61.8% Fibonacci up move which happens to be INR 742.

� Stock price has also shown clear positive divergence on RSI in

weekly chart and given MACD crossover indicating continuation of upmove and strength.

� We expect that target price is 71.8% Fibonacci retracement

upmove of weekly high and close of last fall and our price target in 12 months come to INR 800.

Peerless Securities Master Picks

Disclaimer

RATING PARAMETER

BUY We expect the stock to deliver more than 15% returns over the next 12months

ACCUMULATE We expect the stock to deliver 6% - 15% returns over the next 12months

REDUCE We expect the stock to deliver 0% - 5% returns over the next 12months

SELL We expect the stock to deliver negative returns over the next 12months

NOTE: Target prices are for a period of 12-month perspective. Returns stated in the rating parameter are for our internal benchmark.

TECHNICAL CALL RATING PARAMETER

BUY A condition that indicates a good time to buy a stock. The exact circumstances of the signal will be determined by the indicator that an

analyst isusing.

SELL A condition that indicates a good time to sell a stock. The exact circumstances of the signal will be determined by the indicator that an

analyst isusing.An instruction to the broker to buy or sell stock when it trades beyond a specified price. They serve to either protect your

profits or limit your losses.

DISCLOSURE / DISCLAIMER

Peerless Securities Ltd (PSL) e s t a b l i s h e d in 1995, is a subsidiary of Peerless General Finance & Investment Co Ltd. PSL is a corporate trading member of Bombay Stock Exchange Limited (BSE), Metropolitan Stock Exchange of India Limited (MSEI) & National Stock Exchange of India Limited (NSE). Our businesses include stock broking, services rendered in connection with distribution of primary market issues and financial products like mutual funds and fixed deposits, and depositoryservices.

Peerless Securities Ltd is also a depository participant with National Securities Depository Limited (NSDL) and Central Depository Services (India) Limited (CDSL). We are registered as a Research Analyst under SEBI (Research Analyst) Regulations, 2014.

We hereby declare that our activities were neither suspended nor we have defaulted with any stock exchange authority with whom we are registered in last five years. We have not been debarred from doing business by any Stock Exchange/ SEBI or any other authorities; nor has our certificate of registration been cancelled by SEBI at any point oftime.

We offer our research services to clients as well as our prospects.

This document is not for public distribution and has been furnished to you solely for your information and must not be reproduced or redistributed to any other person. Persons into whose possession this document may come are required to observe these restrictions.

This material is for the personal information of the authorized recipient, and we are not soliciting any action based upon it. This report is not to be construed as an offer to sell or the solicitation of an offer to buy any security in any jurisdiction where such an offer or solicitation would be illegal. It is for the general information of clients of Peerless SecuritiesLtd.Itdoesnotconstituteapersonalrecommendationortakeintoaccounttheparticularinvestmentobjectives, financialsituations,orneedsofindividualclients.

We have reviewed the report, and in so far as it includes current or historical information, it is believed to be reliable though its accuracy or completeness cannot be guaranteed. Neither Peerless Securities Ltd, nor any person connected with it, accepts any liability arising from the use of this document. The recipients of this material should rely on their own investigations and take their own professional advice. Price and value of the investments referred to in this material may go up or down. Past performance is not a guide for futureperformance.

Certain transactions -including those involving futures, options and other derivatives as well as non-investment grade securities - involve substantial risk and are not suitable for all investors. Reports based on technical analysis centres on studying charts of a stock's price movement and trading volume, as opposed to focusing on a company's fundamentals and as such, may not match with a report on a company'sfundamentals.

Opinions expressed are our current opinions as of the date appearing on this material only. While we endeavour to update on a reasonable basis the information discussed in this material, there may be regulatory, compliance or other reasons that prevent us from doing so. Prospective investors and others are cautioned that any forward-looking statements are not predictions and may be subject to change without notice. Our proprietary trading and group company/associate companies may make investment decisions that are inconsistent with the recommendations expressedherein.

PSL shall not be liable for any delay or any other interruption which may occur in presenting the data due to any reason including network (Internet) reasons or snags in the system, break down of the system or any other equipment, server breakdown, maintenance shutdown, breakdown of communication services or inability of the PSL to present the data. In no event shall PSL be liable for any damages, including without limitation direct or indirect, special, incidental, or consequential damages, losses or expenses arising in connection with the data presented by the PSL through thisreport.

We and our affiliates/associates, group companies, officers, directors, and employees, Research Analysts may: (a) from time to time, have long or short positions in, and buy or sell the securities thereof, of company (ies) mentioned herein or (b) be engaged in any other transaction involving such securities and earn brokerage or other compensation or act as a market maker in the financial instruments of the subject company/company (ies) discussed herein or act as advisor or lender / borrower to such company (ies) or have other potential/material conflict of interest with respect to any recommendation and related information and opinions at the time of publication of Research Report or at the time of public appearance. Peerless Securities Ltd (PSL) may have proprietary long/short position in the above mentioned scrip(s) and therefore may be considered as interested. The views provided herein are general in nature and does not consider risk appetite or investment objective of particular investor; readers are requested to take independent professional advice before investing. This should not be construed as invitation or solicitation to do business with PSL. Peerless Securities Ltd does not provide any promise or assurance of favourable view for a particular industry or sector or business group in any manner. The investor is requested to take into consideration all the risk factors including their financial condition, suitability to risk return profile and take professional advice beforeinvesting.

The analyst for this report certifies that all of the views expressed in this report accurately reflect his or her personal views about the subject company or companies and its or their securities, and no part of his or her compensation was, is or will be, directly or indirectly related to specific recommendations or views expressed in thisreport.

Details of Associates and group companies are available on our website i.e. www.peerlesssec.co.in

Research Analyst has served as an officer, director or employee of subject company(ies): No

Peerless Securities Master Picks

Research Analyst’s financial interest in the subject company(ies): No

Peerless Securities Limited has financial interest in the subject company (ies): No

Research Analyst has actual/beneficial ownership of 1% or more securities of the subject company(ies) at the end of the month immediately preceding the date of publication of Research Report: No

Peerless Securities Ltd has actual/beneficial ownership of 1% or more securities of the subject company (ies) at the end of the month immediately preceding the date of publication of Research Report: No

We or our associates may have received compensation from the subject company (ies) in the past 12 months. We or our associates may have received compensation for investment banking or merchant banking or brokerage services from the subject company(ies) in the past 12 months. We or our associates may have received any compensation for products or services other than investment banking or merchant banking or brokerage services from the subject company(ies) in the past 12 months. We or our associates may have received compensation or other benefits from the subject company (ies) or third party in connection with the research report. Our associates may have financial interest in the subject company(ies).

Our associates/Group Companies may have actual/beneficial ownership of 1% or more securities of the subject company(ies) at the end of the month immediately preceding the date of publication of ResearchReport.

Subject company (ies) may have been client during twelve months preceding the date of distribution of the research report.

"A graph of daily closing prices of securities is available at www.nseindia.com(Choose a company from the list on the browser and select the "three years" icon in the price chart)."

Analyst Certification

I/We, author/s (Research Team) and the name/s subscribed to this report, hereby certify that all of the views expressed in this research report accurately reflect my/our views about the subject issuer(s) or securities. I/we (Research Analyst) also certify that no part of my/our compensation was, is, or will be directly or indirectly related to the specific recommendation(s) or view(s) in this report. I/we or my/our relative or PSL may have financial interest in the subject company. Also I/we or my/our relative or PSL or its associates does not have beneficial ownership of 1% or more in the subject company at the end of the month immediately preceding the date of publication of the research report. Since associates/group of PSL is engaged in various financial service businesses, they might have financial interests or beneficial ownership in various companies including the subject company/s mentioned in this report. I/we have not served as officer/director etc in the subject company.

Name E-mail

Amartya Ray [email protected] Sayantina Mallick Chowdhury [email protected]

Peerless Securities Limited: Registered Office: Peerless Mansion, 1 Chowringhee Square, 2nd Floor, Kolkata 700069.

Telephone No.: 033 4050 2700, Fax No.: 033 2243 6941. Website: www.peerlesssec.co.in

SEBIRegistrationNo.: NSE INB/INE/INF 230821137, BSE INB010821131, BSE Currency- SEBI registered; AMFI ARN 2103, NSDL: IN-DP-NSDL-96-99, DP ID: IN300958; CDSL: IN-DP-CDSL-505-2009; Research Analyst INH300002365, CIN:U67120WB1995PLC067616

Our research should not be considered as an advertisement or advice, professional or otherwise. The investor is requested to take into consideration all the risk factors including their financial condition, suitability to risk return profile and the like and take professional advice before investing. Investments in securities are subject to market risk, please read all the related documents carefully before investing. Please read the SEBI prescribed Combined Risk Disclosure Document (refer to SEBI website) prior to investing. Derivatives are a sophisticated investment device. The investor is requested to take into consideration all the risk factors before actually trading in derivative contracts.

Compliance Officer: Mr. Raj Kumar Mukherjee. Call: 033-4050-2700, Email: [email protected]

Peerless Securities Limited Registered Office:

1, Chowringhee Square, 2nd Floor, Kolkata- 700 069

Phone: +91-33-4050-2700/6450-2002/2243-5942, Fax: +91-33-2243 6941

Institutional Office:

11-A, Mittal Towers, 1st floor, Nariman Point, Mumbai – 400 021

Phone: +91-22-2284 1411, 22-6630 3810, Fax: +91-22-2284 1316

SEBI REGN. NO. NSE: INB/INF 230821137, BSE: INB 010821131, NSDL: IN-DP-NSDL-96-99, CDSL: IN-DP-CDSL-505-2009, ARN - 2103