Nevada–Voluntary Loss Costs and Rating Values and Assigned Risk Rates and RatingValues to Be Effective March 1, 2010

ACTIONNEEDED

Please review this circular, which contains information on the approval of Nevada voluntaryloss costs and rating values, and assigned risk rates and rating values, effective March 1, 2010for new and renewal policies.

BACKGROUND This approval circular is a supplement to Filing Circulars NV200911 and NV200912 andState Information Circular NV200913, released in November 2009.

IMPACT The Nevada Division of Insurance has approved an overall voluntary loss cost level decrease of7.6% for industrial classifications and an overall voluntary loss cost level increase of 5.9% forFclassifications. The Division has also approved an overall assigned risk rate level decreaseof 3.7% for industrial classifications and an overall assigned risk rate level increase of 10.4%for Fclassifications.

Important: Each insurer must adopt the revised voluntary loss costs effective March1, 2010 for all new and renewal business.

The anniversary rating date rule (Rule 3A2 in the Basic Manual) applies.

Insurers do not need to make a filing to the Division of Insurance unless they are changingtheir loss cost multipliers or other rating parameters in association with their adoption of thenew loss costs.

NCCI ACTION Revised manual pages will be mailed shortly to subscribers of NCCI’s Basic Manual andExperience Rating Plan Manual. If you would like to subscribe to any of our manuals, pleasecontact NCCI’s Customer Service Center at 800NCCI123.

NCCI has posted this approval circular to ncci.com.

PERSON TOCONTACT

If you have any questions, please contact: Technical contact:

Maggie Karpuk Ia HauckState Relations Executive Director and ActuaryNCCI, Inc. NCCI, Inc.30501 Agoura Road, Suite 201 901 Peninsula Corporate CircleAgoura Hills, CA 91301 Boca Raton, FL 3348713628187078374 561893[email protected][email protected]

30501 Agoura Road, Suite 201, Agoura Hills, California 91301 Phone: (818)-707-8374 Fax: (818)-707-8387 Email: [email protected]

Magda (Maggie) Karpuk State Relations Executive Regulatory Services Division November 18, 2009 Honorable Scott Kipper Commissioner of Insurance State of Nevada Department of Business and Industry Insurance Division 788 Fairview Drive, Suite 300 Carson City, NV 89701-5453 RE: Workers Compensation Assigned Risk Rates and Rating Values Nevada Assigned Risk Market - Effective March 1, 2010 Dear Commissioner Kipper: In accordance with the applicable statutes and regulations of the state of Nevada, we are filing for your consideration and approval revised rates and rating values for the Nevada assigned risk market. This filing proposes an overall average decrease of 3.7% in assigned risk rates from the current rate levels approved effective March 1, 2009. These changes are applicable to new and renewal business only. The components of the proposed changes are listed in the enclosed summary. The following class codes are of special note as a result of item filings approved in Nevada:

1. As a result of Item B-1399A, effective 7/1/2006, the loss cost for class code 7425 was updated by the average overall change in loss cost for Industry Group 5 (Miscellaneous). This will be the last year code 7425 will need special handling as it will have a full year of data in the 3/1/3011 filing.

2. As a result of Item B-1406, effective 3/1/2010, the following changes were made:

• Class code 0100 was discontinued and class code 0005 was payroll weighted to reflect the combined experience of 0005 and 0100.

• Class code 0094 was discontinued and class code 0016 was payroll weighted to reflect the combined experience of 0016 and 0094.

• Class code 0092 was discontinued.

3. As a result of Item B-1408, effective 3/1/2010, the following changes were made:

• New class codes 8602, 8603 and 8725 were established in this filing.

• Class codes 8869 and 9059 were combined in this filing to reflect the first year of a two‐year transition program. At the end of the two‐year transition, code 9059 will be discontinued.

4. As a result of Item B-1418, effective 1/1/2010, class code 7402 was established.

5. As a result of Item 02-NV-2009, effective 3/1/2010, class code 9429 was discontinued.

6. As a result of Item 02-NV-2008, effective 3/1/2009, the following changes were made:

• Class codes 0010, 0058, 0083, 0091, and 0101 were payroll weighted to reflect the second year of a three-year transition program. At the end of the three-year transition, codes 0010, 0058, 0091, and 0101 will be discontinued.

• Class codes 0107 and 8288 were payroll weighted to reflect the second year of a three-year transition program. At the end of the three-year transition, code 0107 will be discontinued.

• Class codes 8867 and 8688 were payroll weighted to reflect the second year of a three-year transition program. At the end of the three-year transition, code 8867 will be discontinued.

This filing is made exclusively on behalf of the companies that have given valid consideration for the express purpose of fulfilling regulatory rate or loss cost filing requirements and other private use of this information. In the enclosed appendix is a list of companies, sorted by group, which as of the time this filing is submitted, are eligible to reference this information. The inclusion of a company on this list merely indicates that the company, or the group to which it belongs, is affiliated with NCCI in this state, or has licensed this information as a non-affiliate, and is not intended to indicate whether the company is currently writing business or is even licensed to write business in this state. Please contact me at (818) 707-8374 or Ia Hauck at (561) 893-3104 if you have any questions or need any further information. Respectfully submitted, NATIONAL COUNCIL ON COMPENSATION INSURANCE, INC.

Actuarial Certification The information contained in this filing has been prepared under the direction of the undersigned actuary in accordance with applicable Actuarial Standards of Practice as promulgated by the Actuarial Standards Board. The Actuarial Standards Board is vested by the U.S.-based actuarial organizations with the responsibility for promulgating Actuarial Standards of Practice for actuaries providing professional services in the United States. Each of these organizations requires its members, through its Code of Professional Conduct, to observe the Actuarial Standards of Practice when practicing in the United States. Filing prepared by:

Ia Hauck, ACAS, MAAA Director and Actuary Actuarial and Economic Services

NCCI MAKES NO REPRESENTATIONS OR WARRANTIES RELATING TO THESE MATERIALS, INCLUDING ANY EXPRESS, STATUTORY OR IMPLIED WARRANTIES INCLUDING THE IMPLIED WARRANTY OF MERCHANTABILITY AND FITNESS FOR A PARTICULAR PURPOSE. ADDITIONALLY, AUTHORIZED END USERS ASSUME RESPONSIBILITY FOR THE USE OF, AND FOR ANY AND ALL RESULTS DERIVED OR OBTAINED THROUGH THE USE OF SUCH MATERIALS.

The workers compensation benefit system in Nevada is designed to cover medical costs associated with workplace injuries, as well as provide wage replacement (indemnity) benefits to injured workers for lost work time. The National Council on Compensation Insurance, Inc. (NCCI) collects an extensive amount of information regarding the workers compensation system in Nevada, and submits proposed assigned risk rates for review and approval by the Nevada Department of Insurance. These prospective assigned risk rates are intended to cover the indemnity and medical benefits provided under the system, the expenses associated with providing these benefits (loss adjustment expenses), and any other costs associated with providing workers compensation insurance (such as commissions, taxes, etc.). Employers unable to secure coverage in the voluntary market can apply for such coverage in the assigned risk market. In this filing, NCCI is proposing that the Nevada Department of Insurance approve a 3.7% overall average decrease to the current assigned risk rate level (which went into effect on March 1, 2009), and that the new rates become effective on March 1, 2010 for new and renewal policies. This document will explain why this decrease is necessary. NCCI separately determines rates for each workers compensation classification. In this filing, the actual change from the current rates is different depending on the classification. A brief discussion of key components of the proposed rate change follows this page.

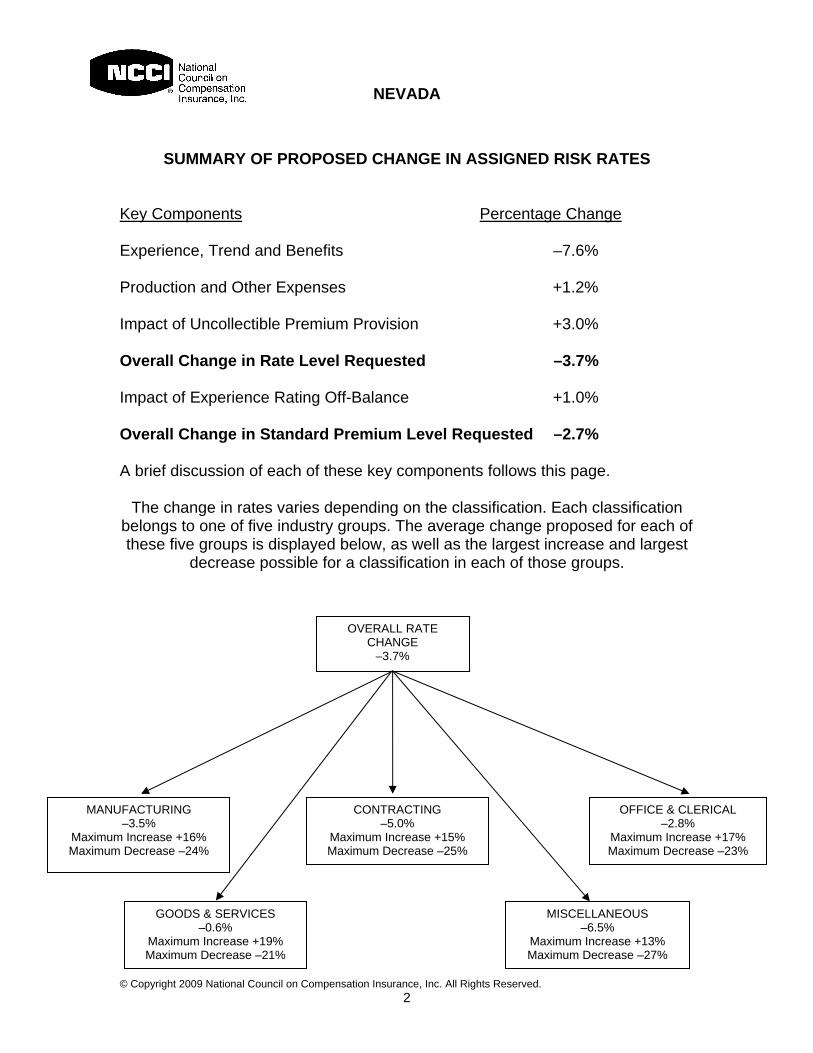

SUMMARY OF PROPOSED CHANGE IN ASSIGNED RISK RATES Key Components Percentage Change Experience, Trend and Benefits –7.6% Production and Other Expenses +1.2% Impact of Uncollectible Premium Provision +3.0% Overall Change in Rate Level Requested –3.7% Impact of Experience Rating Off-Balance +1.0% Overall Change in Standard Premium Level Requested –2.7% A brief discussion of each of these key components follows this page.

The change in rates varies depending on the classification. Each classification belongs to one of five industry groups. The average change proposed for each of these five groups is displayed below, as well as the largest increase and largest

decrease possible for a classification in each of those groups.

KEY COMPONENT – EXPERIENCE, TREND AND BENEFITS This key component has three main parts. EXPERIENCE NCCI reviewed the emerging experience of Nevada workers compensation policies in recent years. The primary focus of our review was on financial call data premiums and losses from policy years 2006 and 2007, evaluated as of December 31, 2008. Policy year data captures the premiums and losses from the block of policies that have effective dates during a given year. Consistent with last year’s filing, in addition to the financial call data, we used historical data obtained from Employers Insurance Group (formerly known as the State Industrial Insurance System). Calendar-Accident Year 2008 experience was also examined for the purposes of this filing. A calendar-accident year captures the premiums earned during a given year, together with the losses associated with workplace accidents taking place during the same year. This information is useful in analyzing whether the pattern observed in recent years can be expected to continue in the future. It should be noted that NCCI adjusts the historical policy and calendar-accident year experience to reflect both loss cost and rate changes approved and statutory benefit changes implemented since that time period. The specific loss experience used by NCCI in this filing is paid losses, which are the benefit amounts already paid by insurers on reported claims. The use of paid loss experience is consistent with NCCI’s prior Nevada rate and loss cost filings. In this filing NCCI relies on an average change in paid losses over the last two or three years. Adjustment for Enacted Assembly Bill 438 Assembly Bill 438 incorporates a cost of living adjustment (COLA) for workers entitled to receive compensation under permanent total disability from which the accident causing such injury occurred on or after January 1, 2004. The annual COLA is set at 2.3%. The experience period for this filing includes any permanent total disability claims incurred during policy years 2006 and 2007, which are subject to AB 438. However, because the COLA on these claims is minimal as of December 31, 2008, the reported paid losses do not reflect the impact of AB 438. Since the future emergence of the COLA is also not fully reflected in the paid loss

development pattern, an adjustment to the reported paid losses is necessary. Going forward, the impact of this adjustment will diminish over time as the reported paid loss data includes claims subject to the COLA.

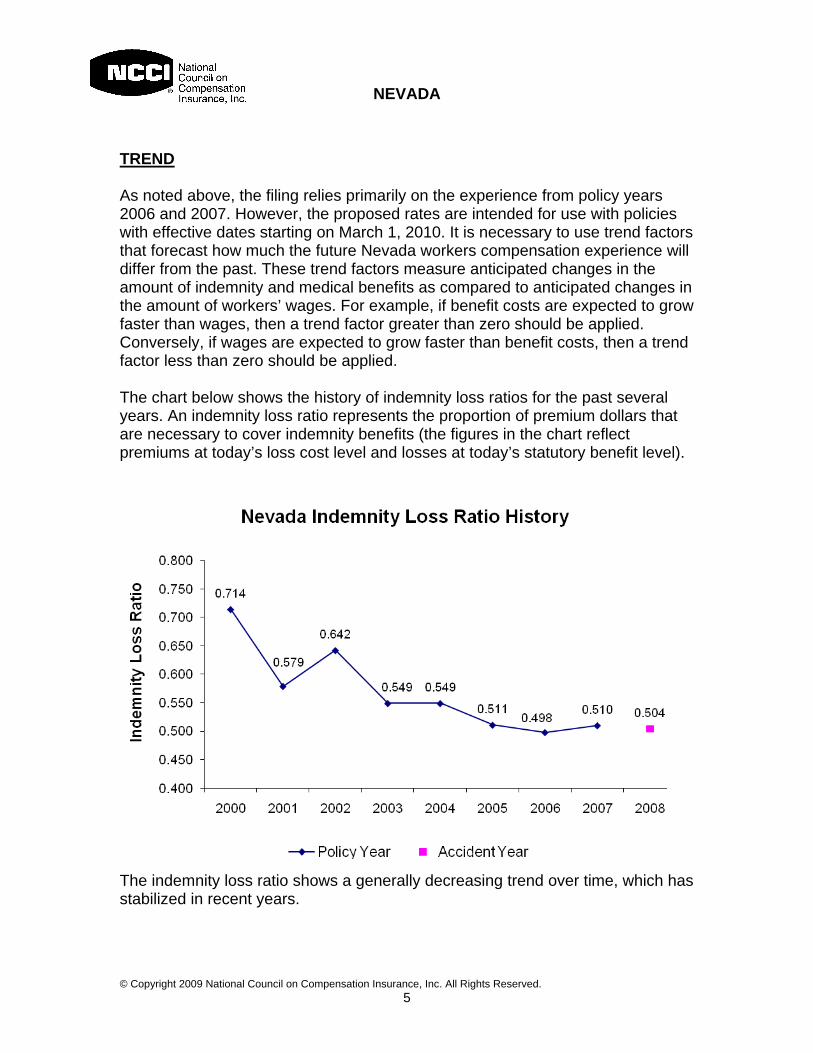

TREND As noted above, the filing relies primarily on the experience from policy years 2006 and 2007. However, the proposed rates are intended for use with policies with effective dates starting on March 1, 2010. It is necessary to use trend factors that forecast how much the future Nevada workers compensation experience will differ from the past. These trend factors measure anticipated changes in the amount of indemnity and medical benefits as compared to anticipated changes in the amount of workers’ wages. For example, if benefit costs are expected to grow faster than wages, then a trend factor greater than zero should be applied. Conversely, if wages are expected to grow faster than benefit costs, then a trend factor less than zero should be applied. The chart below shows the history of indemnity loss ratios for the past several years. An indemnity loss ratio represents the proportion of premium dollars that are necessary to cover indemnity benefits (the figures in the chart reflect premiums at today’s loss cost level and losses at today’s statutory benefit level).

The indemnity loss ratio shows a generally decreasing trend over time, which has stabilized in recent years.

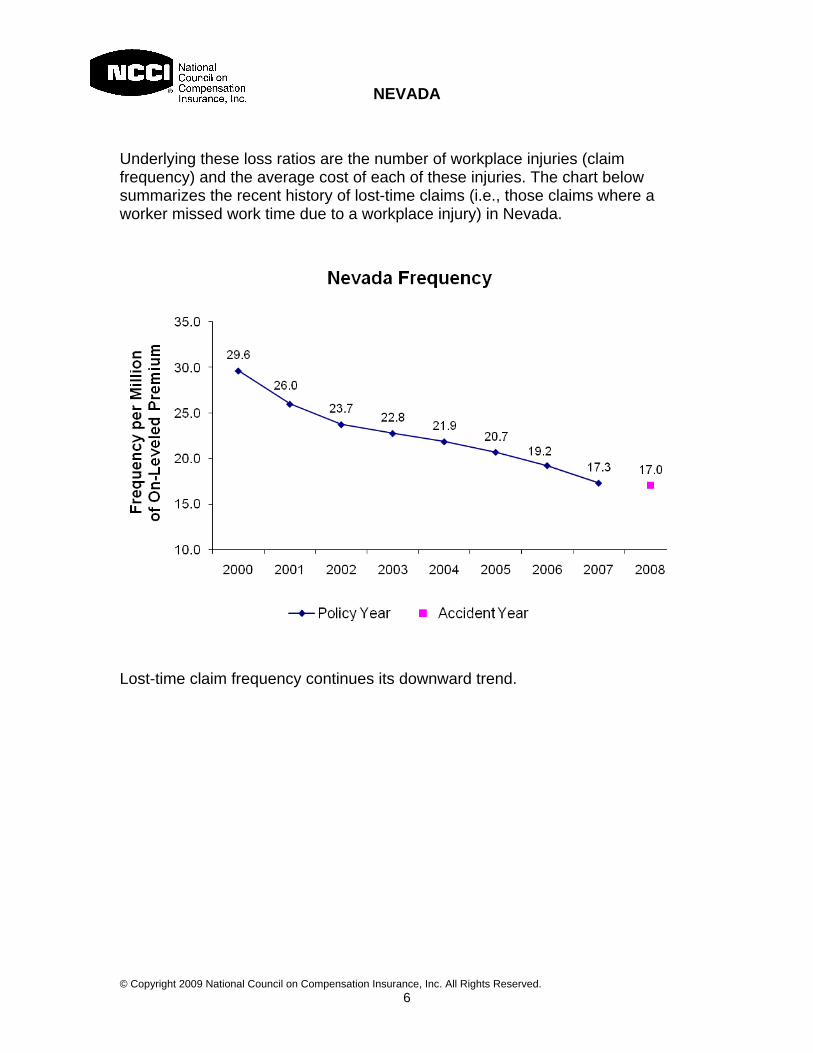

Underlying these loss ratios are the number of workplace injuries (claim frequency) and the average cost of each of these injuries. The chart below summarizes the recent history of lost-time claims (i.e., those claims where a worker missed work time due to a workplace injury) in Nevada.

Lost-time claim frequency continues its downward trend.

After removing the impact of the growth in workers’ wages that occurred over this time period, the average indemnity cost per case in excess of wage growth is shown in the following chart.

The indemnity average cost per case in excess of wage growth exhibits an upward trend in recent years, with a sharp increase in the latest policy year.

In last year’s Nevada filing, NCCI proposed an indemnity trend factor of –2.5% per year. Based on our analysis this year, we are proposing no change to the annual indemnity trend factor. This means that indemnity benefits are expected to increase at a slower pace than workers’ wages.

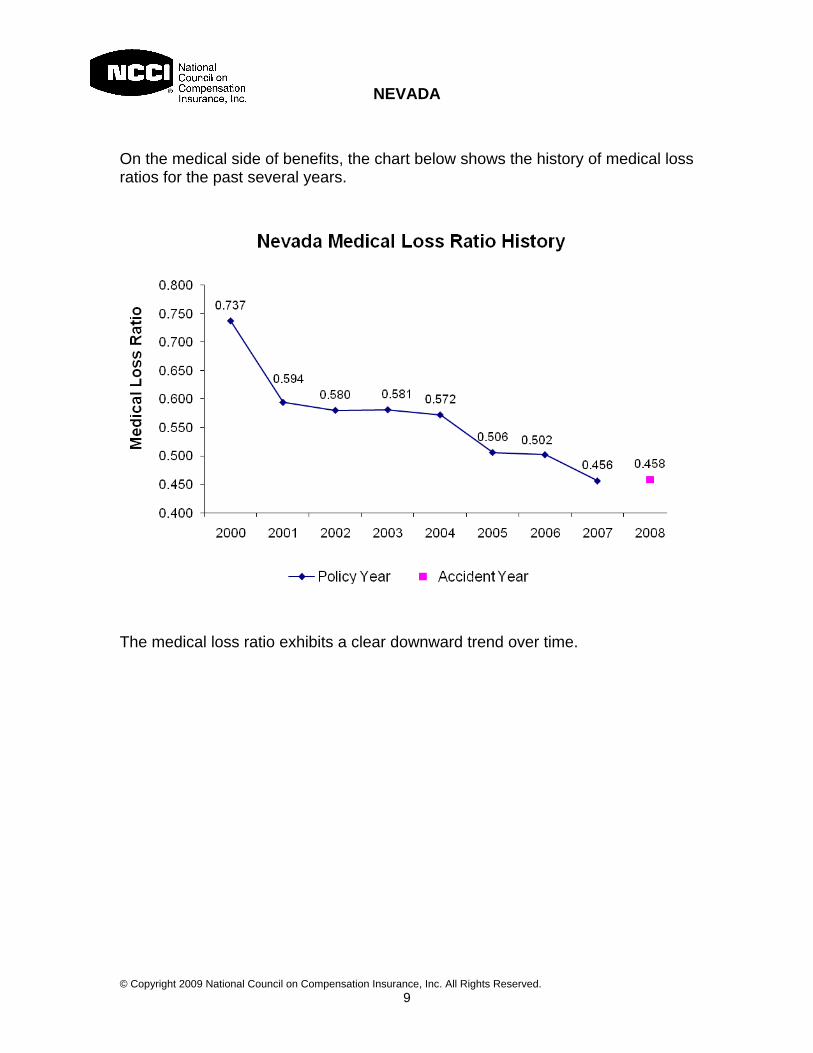

As with indemnity, underlying these loss ratios are the number of workplace injuries (claim frequency) and the average cost of each of these injuries. The frequency chart discussed earlier is also a primary driver of medical costs. For these workplace injuries, the average medical cost over time is tracked in the following chart.

The medical average cost per case has been steadily increasing over time.

After removing the impact of the growth in workers’ wages that occurred over this time period, the average medical cost per case in excess of wage growth is shown in the following chart.

The general pattern of the medical average cost per case in excess of wage inflation is upward over time. In last year’s Nevada filing, NCCI proposed a medical trend factor of 0.0% per year. Based on our analysis this year, we are proposing to decrease the medical trend factor to –2.0% per year. This means that medical benefits are expected to increase at a slower pace than workers’ wages.

BENEFITS Increase in the Maximum Weekly Wage Workers injured in Nevada receive wage replacement (indemnity) benefits at a rate of two-thirds of their pre-injury weekly wage. These benefits are subject to a weekly minimum and maximum. Each July 1, the minimum and maximum weekly benefits are updated based on the most recent average weekly wage in Nevada. Since losses from policy years 2006 and 2007 reflect the indemnity benefits being paid at that time, it is necessary for NCCI to reflect what the level of these benefits will be starting July 1, 2009. Changes in the Medical Fee Schedule The Nevada Medical Fee schedule is based on the Relative Values for Physicians, and is revised annually to reflect updated St. Anthony’s Press Relative Values for Physicians (RVP). In addition, an update to the conversion factors for the current fee schedule, which are used to convert the RVPs to maximum reimbursable amounts, became effective February 1, 2009. NCCI estimates that the combined impact of recent changes to the schedule is an increase of 3.0% on medical costs. The overall system cost impact is an increase of 1.4%.

Enactment of Senate Bill 6 Nevada Senate Bill 6, effective July 1, 2009, removes the age limit for which a volunteer firefighter can make a claim for compensation due to heart disease, and requires that any volunteer firefighter 50 years of age or older submit to a physical examination once a year. NCCI estimates that the impact of Senate Bill 6 on the volunteer firefighter class code is an increase of 15%, and in this filing, the loss cost for class code 7711 has been adjusted to reflect this impact. NCCI estimates that the impact of this legislation on overall system costs is negligible, since the volunteer firefighter class code represents only a small portion of overall system costs. Enactment of Senate Bill 195 Nevada Senate Bill 195 is comprised of several sections that affect the workers compensation system in Nevada, with varying effective dates. Section 9 of Senate Bill 195, effective October 1, 2009, increases the maximum burial expense from $5,000 to $10,000. NCCI estimates that the impact of this change on overall system costs is an increase of 0.1%. Any cost impacts which emerge from other sections of Senate Bill 195 will be realized through future loss experience and reflected in subsequent loss cost filings. Enactment of Senate Bill 363 Nevada Senate Bill 363, effective October 1, 2009 (retroactively to October 1, 2007), extended lifetime benefits to spouses of fatally-injured workers, regardless of remarriage, and eliminated the two-year lump sum award previously provided upon remarriage. NCCI estimates that the impact of this change on overall systems costs is an increase of 0.7%.

The proposed rates include a provision for servicing carrier allowance (including loss-based expenses, taxes and overhead), commissions, and administrative expenses. The proposed combined expense provision is 31.6 percent. The impact of this change in assigned risk expenses is an increase of 1.2 percent in rates. In the past, NCCI has recognized uncollectible premium implicitly in its Internal Rate of Return (IRR) analysis. For this filing, NCCI is proposing to include an uncollectible premium provision of 3.0% via a separate rate provision. The impact of this change to the uncollectible premium provision is an increase of 3.0 percent in rates. In addition, this filing proposes to increase the current assigned risk market minimum premium multiplier from 175 to 185. The overall premium level impact of this change is 0.0%.

KEY COMPONENT – ASSIGNED RISK PRICING PROGRAMS A number of assigned risk pricing programs have been instituted in Nevada. These programs help to assure that the assigned risk market is self-funding, or that the premium collected is enough to pay the losses and expenses generated by employers in that market. These programs also encourage employers in the assigned risk market to seek coverage in the voluntary market. This filing proposes no changes to these programs. The current assigned risk pricing programs are listed below:

• 30% Assigned Risk Differential • Assigned Risk Adjustment Program (ARAP) with a 25% Cap • Loss Sensitive Rating Program (LSRP)

CONCLUSION This filing document provides a high-level perspective on why Nevada assigned risk rates need to decrease by 3.7%. Following are various exhibits containing other Nevada workers compensation information that may be of interest, as well as the proposed assigned risk rates and rating values by classification.

WORKERS COMPENSATION AND EMPLOYERS LIABILITY NEVADAExhibit III

Page S7Effective March 1, 2010

APPLICABLE TO ASSIGNED RISK POLICIES ONLY

FOOTNOTES

E Rate for classification already includes the specific disease loading shown in the table below.

Code No.Disease Loading Symbol Code No.

Disease Loading Symbol Code No.

Disease Loading Symbol

1164E 0.19 S 1852E 0.10 Asb 5508E 0.07 S1165E 0.15 S 3081E 0.10 S 6251E 0.12 S1624E 0.08 S 3082E 0.20 S 6252E 0.12 S1710E 0.12 S 3085E 0.08 S 6260E 0.24 S1741E 1.78 S 3175E 0.05 S1803E 0.57 S 4024E 0.03 SS=Silica, Asb=Asbestos

F Rate provides for coverage under the United States Longshore and Harbor Workers Compensation Act and itsextensions. Rate includes a provision for USL&HW assessment.

M Risks are subject to Admiralty Law or Federal Employers Liability Act (FELA). However, the published rate is for risks that voluntarily purchase standard workers compensation and employers liability coverage. A provision for the USL&HW assessment is included for those classifications under Program II USL Act. The listed codes of 6702, 6703, 6704, 7151, 7152, 7153, 8734, 8737, 8738, 8805, 8814, and 8815 under the Federal Employers’ Liability Act (FELA) for employees of interstate railroads are not applicable in the residual market.

N This code is part of a ratable / non-ratable group shown below. The statistical non-ratable code and correspondingrate are applied in addition to the basic classification when determining premium.

Class Non-RatableCode Element Code4771 07717405 74457431 7453

P Classification is computed on a per capita basis.

X Refer to special classification phraseology in these pages which is applicable in this state.

* Class Codes with Specific Footnotes

1005 Rate includes a non-ratable disease element of $8.01. (For coverage written separately for federalbenefits only, $3.11. For coverage written separately for state benefits only, $4.90.)

1016 Rate includes a non-ratable disease element of $25.36. (For coverage written separately for federalbenefits only, $9.88. For coverage written separately for state benefits only, $15.48.) It also includesa catastrophe loading of $0.10.

6702 Rate and rating values only appropriate for laying or relaying of tracks or maintenance of way - no work on elevated railroads. Otherwise, assign appropriate construction or erection code rate and elr each x 1.215.

6703 Rate and rating values only appropriate for laying or relaying of tracks or maintenance of way - no work on elevated railroads. Otherwise, assign appropriate construction or erection class rate x 1.675 and elr x 1.631.

6704 Rate and rating values only appropriate for laying or relaying of tracks or maintenance of way - no work onelevated railroads. Otherwise, assign appropriate construction or erection class rate and elr each x 1.35.

8833 The ex-medical rate for this classification is $0.98.

9040 The ex-medical rate for this classification is $1.83.

9662 The ex-medical rate for this classification is $5.18.

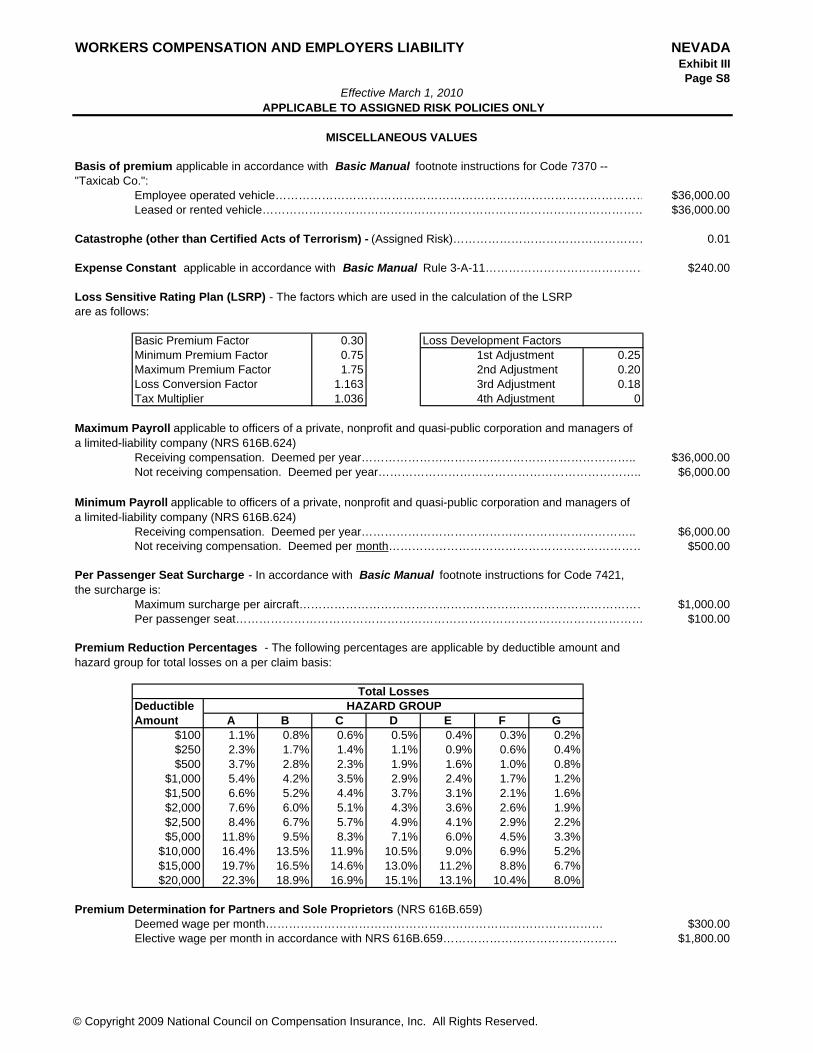

Premium Determination for Partners and Sole Proprietors (NRS 616B.659)Deemed wage per month…………………………………………………………………………… $300.00Elective wage per month in accordance with NRS 616B.659……………………………………… $1,800.00

Maximum Payroll applicable to officers of a private, nonprofit and quasi-public corporation and managers of a limited-liability company (NRS 616B.624)

Minimum Payroll applicable to officers of a private, nonprofit and quasi-public corporation and managers of a limited-liability company (NRS 616B.624)

Per Passenger Seat Surcharge - In accordance with Basic Manual footnote instructions for Code 7421, the surcharge is:

Premium Reduction Percentages - The following percentages are applicable by deductible amount and hazard group for total losses on a per claim basis:

WORKERS COMPENSATION AND EMPLOYERS LIABILITY NEVADAExhibit IIIPage S9

Effective March 1, 2010APPLICABLE TO ASSIGNED RISK POLICIES ONLY

MISCELLANEOUS VALUES (cont.)

Premium Determination for Partners and Sole Proprietors (NRS 616A.210)Licensed as subcontractors and working as a subcontractor under the direction of the principal contractor. Deemed wage per month…………………………………………………………… $500.00

United States Longshore and Harbor Workers' Compensation Coverage Percentage applicableonly in connection with Basic Manual Rule 3-A-4….…..….…..................................................................…….… 29%

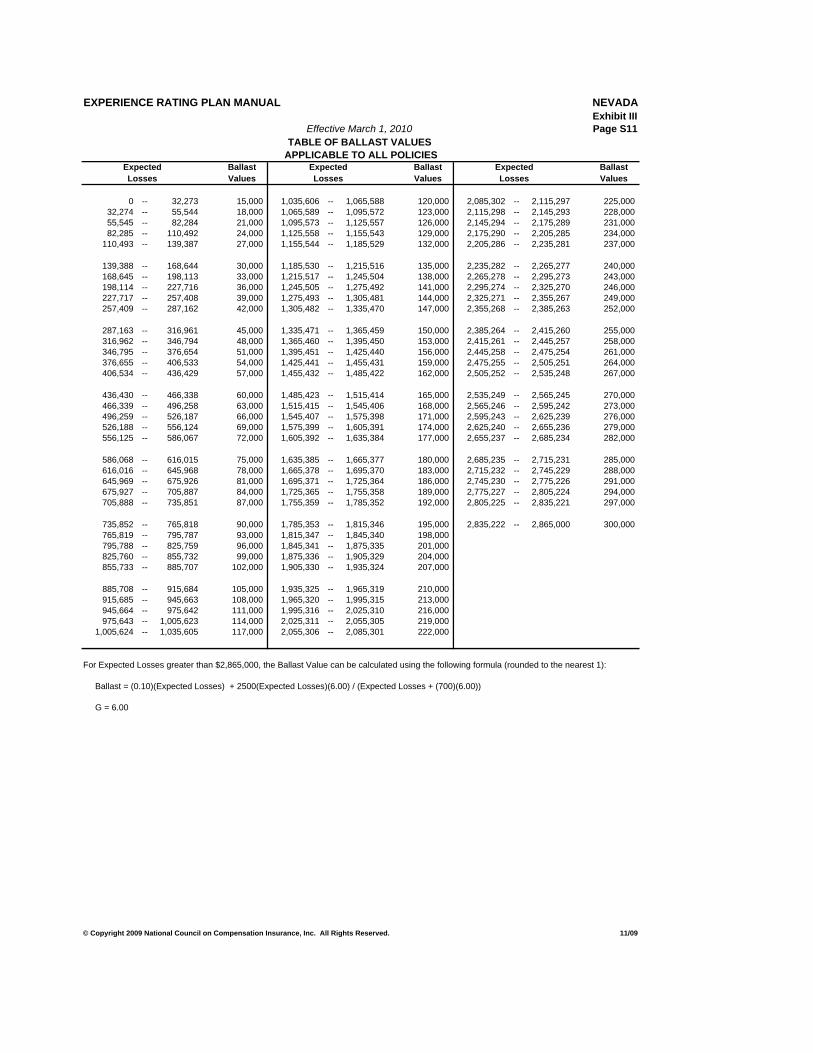

Experience Rating EligibilityA risk is eligible for intrastate experience rating when the payrolls or other exposures developed in the last year or last two years of the experience period produced a premium of at least $6,000. If more than two years, an average annual premium of at least $3,000 is required. Page A-1 of the Experience Rating Plan Manual should be referenced for the latest approved eligibility amounts by state.

(Multiply a Non-F classification rate by a factor of 1.29 to adjust for differences in benefits and loss-based expenses. This factor is the product of the adjustment for differences in benefits (1.21) and the adjustment for differences in loss-based expenses (1.068).)

A M C O INSURANCE COMPANY ACCIDENT FUND INS CO OF AMERICA ACCIDENT INSURANCE COMPANY INC ACE AMERICAN INSURANCE COMPANY ACE FIRE UNDERWRITERS INSURANCE COMPANY ACE PROPERTY & CASUALTY INSURANCE COMPANY ACIG INS CO ADVANTAGE WC INSURANCE CO AIG CASUALTY CO AIU INSURANCE CO (AIG CASUALTY CO) AK NATIONAL INS CO ALLIANZ GLOBAL RISKS US INS CO ALLIED PROPERTY AND CASUALTY INS CO AMERICAN ALTERNATIVE INSURANCE CORPORATION AMERICAN AUTOMOBILE INSURANCE CO AMERICAN BUSINESS AND PERSONAL INS MUTUAL INC AMERICAN CASUALTY COMPANY OF READING P A AMERICAN COMPENSATION INS CO AMERICAN ECONOMY INS CO AMERICAN FAMILY HOME INS CO AMERICAN FAMILY MUTUAL INSURANCE CO AMERICAN FIRE AND CASUALTY CO AMERICAN FUJI FIRE AND MARINE INS CO AMERICAN GUARANTEE AND LIABILITY INS CO AMERICAN HARDWARE MUTUAL INS CO AMERICAN HOME ASSURANCE CO AIG CASUALTY CO AMERICAN INS CO AMERICAN INTERNATIONAL PACIFIC INS CO AMERICAN INTERNATIONAL SOUTH INS CO AMERICAN INTERSTATE INS CO AMERICAN MINING INS CO AMERICAN MODERN HOME INS CO AMERICAN STATES INS CO A SAFECO COMPANY AMERICAN STATES INS CO OF TX AMERICAN ZURICH INS CO AMERISURE INS CO

AMERISURE MUTUAL INS CO ARCH INSURANCE COMPANY ARGONAUT GREAT CENTRAL INS CO ARGONAUT INS CO ARGONAUT MIDWEST INS CO ASSOCIATED INDEMNITY CORP ASSURANCE COMPANY OF AMERICA ATHENA ASSURANCE CO ATLANTIC SPECIALTY INS CO (ONEBEACON) BADGER MUTUAL INS CO BANCINSURE INC BANKERS STANDARD FIRE AND MARINE CO BANKERS STANDARD INS CO BENCHMARK INSURANCE COMPANY BERKLEY REGIONAL INS CO BITUMINOUS CASUALTY CORP BITUMINOUS FIRE AND MARINE INS CO BROTHERHOOD MUTUAL INS CO BUILDERS INSURANCE COMPANY INC CALIFORNIA INSURANCE COMPANY CAPITOL INDEMNITY CORP CAROLINA CASUALTY INS CO CENTRE INSURANCE COMPANY CHARTER OAK FIRE INS CO CHEROKEE INS CO CHRYSLER INS CO CHUBB INDEMNITY INS CO CHURCH MUTUAL INS CO CINCINNATI INS CO CLARENDON NATIONAL INS CO CO CASUALTY INS CO COLONIAL AMERICAN CASUALTY & SURETY CO COMMERCE AND INDUSTRY INS CO COMPANION PROPERTY AND CASUALTY INS CO COMPWEST INS CO CONTINENTAL CASUALTY CO

CONTINENTAL INDEMNITY CO CONTINENTAL INS CO CRUM AND FORSTER INDEMNITY CO DALLAS NATIONAL INSURANCE COMPANY DELOS INSURANCE COMPANY DEPOSITORS INS CO DIAMOND STATE INS CO DISCOVER PROPERTY & CASUALTY INS CO ELECTRIC INS CO EMPLOYERS ASSURANCE COMPANY EMPLOYERS COMPENSATION INS CO EMPLOYERS DIRECT INS CO EMPLOYERS FIRE INSURANCE COMPANY EMPLOYERS INS CO OF WAUSAU EMPLOYERS INSURANCE COMPANY OF NEVADA EMPLOYERS MUTUAL CASUALTY CO EMPLOYERS PREFERRED INS CO ESURANCE INSURANCE CO OF NJ EVEREST NATIONAL INS CO EVEREST REINSURANCE CO DIRECT EXPLORER INS CO FAIRFIELD INS CO FAIRMONT SPECIALTY INSURANCE COMPANY FARMERS INS CO OF OR FARMERS INSURANCE EXCHANGE FARMLAND MUTUAL INSURANCE COMPANY FEDERAL INSURANCE COMPANY FEDERATED MUTUAL INS CO FEDERATED RURAL ELECTRIC INS EXCHANGE FEDERATED SERVICE INS CO FIDELITY & DEPOSIT COMPANY OF MARYLAND FIDELITY & GUARANTY INS UNDERWRITERS FIDELITY & GUARANTY INSURANCE CO FIREMANS FUND INDEMNITY CORP FIREMANS FUND INS CO OF GA FIREMANS FUND INS CO OF HI

FIREMANS FUND INS CO OF LA FIREMANS FUND INS CO OF MO FIREMANS FUND INSURANCE CO FIRST LIBERTY INS CORP FIRST NATIONAL INS CO OF AMERICA FIRSTCOMP INSURANCE CO FLORISTS MUTUAL INSURANCE CO GATEWAY INS CO GENERAL CASUALTY COMPANY OF WISCONSIN GENERAL INS CO OF AMERICA GENERAL STAR NATIONAL INS CO GENESIS INS CO GRANITE STATE INSURANCE COMPANY GRAPHIC ARTS MUTUAL INS CO GREAT AMERICAN ALLIANCE INS CO GREAT AMERICAN ASSURANCE COMPANY GREAT AMERICAN INS CO OF NY GREAT AMERICAN INSURANCE COMPANY GREAT AMERICAN SECURITY INS CO GREAT AMERICAN SPIRIT INS CO GREAT DIVIDE INSURANCE COMPANY GREAT NORTHERN INS CO GREAT WEST CASUALTY COMPANY GREENWICH INS CO GUARANTEE INS CO GUIDEONE AMERICA INS CO GUIDEONE ELITE INS CO GUIDEONE MUTUAL INS CO HANOVER INS CO HARTFORD ACCIDENT AND INDEMNITY CO HARTFORD CASUALTY INS CO HARTFORD FIRE INSURANCE CO HARTFORD INS CO OF MIDWEST HARTFORD UNDERWRITERS INS CO HOMELAND INS CO OF NY ILLINOIS NATIONAL INSURANCE COMPANY

IMPERIAL CASUALTY AND INDEMNITY COMPANY INDEMNITY INS CO OF N AMERICA (INA INS) (CT GEN) INS CO OF NORTH AMERICA INS CO OF THE STATE PA INS CO OF THE WEST LIBERTY INS CORP LIBERTY INS UNDERWRITERS INC LIBERTY MUTUAL FIRE INS CO LIBERTY MUTUAL INS CO LM GENERAL INS CO LM INS CORP LM PERSONAL INS CO LM PROPERTY AND CASUALTY INS CO LUMBERMENS UNDERWRITING ALLIANCE MAJESTIC INS CO MANUFACTURERS ALLIANCE INS CO MARYLAND CASUALTY COMPANY MEMIC INDEMNITY CO MID CENTURY INS CO MIDDLESEX INS CO MIDWEST EMPLOYERS CASUALTY CO MIDWEST INS CO MILBANK INSURANCE COMPANY MITSUI SUMITOMO INS CO OF AMERICA MITSUI SUMITOMO INS USA INC NATIONAL AMERICAN INS CO NATIONAL FARMERS UNION PROP AND CAS CO (QBE) NATIONAL FIRE INS CO OF HARTFORD NATIONAL INTERSTATE INS CO NATIONAL SURETY CORP NATIONAL UNION FIRE INS CO OF PITTSBURG NATIONWIDE AGRIBUSINESS INS CO NATIONWIDE MUTUAL FIRE INS CO NATIONWIDE MUTUAL INS CO NETHERLANDS INSURANCE COMPANY NEW HAMPSHIRE INDEMNITY COMPANY

NEW HAMPSHIRE INSURANCE COMPANY NGM INSURANCE COMPANY NIPPONKOA INS CO LIMITED (US BRANCH) NORTH AMERICAN ELITE INSURANCE CO NORTH AMERICAN SPECIALTY INS CO NORTH RIVER INS CO NORTHERN ASSURANCE CO OF AMERICA NORTHERN INSURANCE CO OF N Y NOVA CASUALTY COMPANY OH CASUALTY INS CO OHIO SECURITY INS CO OLD REPUBLIC GENERAL INSURANCE CORPORATION OLD REPUBLIC INS CO ONEBEACON AMERICA INS CO ONEBEACON INSURANCE COMPANY PA GENERAL INS CO PA MANUFACTURERS ASSN INS CO PA MANUFACTURERS INDEMNITY CO PACIFIC EMPLOYERS INS CO PACIFIC INDEMNITY CO PARAMOUNT INS CO PENN AMERICA INSURANCE COMPANY PETROLEUM CASUALTY CO PHARMACISTS MUTUAL INS CO PHOENIX INS CO PIONEER SPECIALTY INSURANCE COMPANY PRAETORIAN INSURANCE COMPANY PREFERRED PROFESSIONAL INSURANCE COMPANY PROPERTY AND CASUALTY INS CO OF HARTFORD PROTECTIVE INS CO PUBLIC SERVICE MUTUAL INS QBE INSURANCE CORPORATION REDLAND INS CO QBE REDWOOD FIRE & CASUALTY COMPANY REGENT INSURANCE COMPANY REINSURANCE CO OF AMERICA INC

REPUBLIC INDEMNITY CO OF CA REPUBLIC INDEMNITY COMPANY OF AMERICA RIVERPORT INSURANCE COMPANY ROCKWOOD CASUALTY INS CO SAFECO INS CO OF AMERICA SAFETY FIRST INS CO SAFETY NATIONAL CASUALTY CORP SCF ARIZONA SEABRIGHT INSURANCE CO SELECTIVE INSURANCE COMPANY OF AMERICA SENECA INSURANCE CO SENTINEL INS CO SENTRY CASUALTY CO SENTRY INSURANCE A MUTUAL CO SENTRY SELECT INSURANCE COMPANY SEQUOIA INDEMNITY COMPANY SEQUOIA INSURANCE CO SFM MUTUAL INS CO SOMPO JAPAN INSURANCE CO OF AMERICA SOUTHERN INS CO SPARTA INSURANCE COMPANY SPRINGFIELD INS CO ST PAUL FIRE AND MARINE INS CO ST PAUL GUARDIAN INS CO ST PAUL MEDICAL LIABILITY INS CO ST PAUL MERCURY INS CO ST PAUL PROTECTIVE INS CO STANDARD FIRE INSURANCE COMPANY STAR INS CO STARNET INSURANCE COMPANY STATE AUTO PROPERTY AND CASUALTY INS CO STATE AUTOMOBILE MUTUAL INS CO STATE FARM FIRE AND CASUALTY CO STATE NATIONAL INSURANCE COMPANY SUA INSURANCE COMPANY T H E INSURANCE COMPANY

TECHNOLOGY INSURANCE CO TM CASUALTY INS CO TNUS INSURANCE CO TOKIO MARINE AND NICHIDO FIRE INS CO LTD US BRANCH TOWER INS CO OF NY TOWER NATIONAL INS CO TRANS PACIFIC INS CO TRANSGUARD INS CO OF AMERICA INC TRANSPORTATION INS CO TRAVCO INS CO TRAVELERS CASUALTY AND SURETY CO TRAVELERS HOME AND MARINE INS CO TRAVELERS INDEMNITY CO TRAVELERS INDEMNITY CO OF AMERICA TRAVELERS INDEMNITY CO OF CT TRAVELERS PROPERTY CASUALTY CO OF AMERICA TRUCK INSURANCE EXCHANGE TRUMBULL INS CO TWIN CITY FIRE INS CO ULLICO CASUALTY CO UNIGARD INDEMNITY CO UNIGARD INS CO UNION INSURANCE COMPANY UNITED NATIONAL CASUALTY INS CO UNITED NATIONAL SPECIALTY INS CO UNITED STATES FIDELITY AND GUARANTY CO UNIVERSAL UNDERWRITERS INS CO US FIRE INS CO UTICA MUTUAL INS CO VALLEY FORGE INS CO VANLINER INS CO VIGILANT INS CO WAUSAU BUSINESS INSURANCE COMPANY WAUSAU UNDERWRITERS INSURANCE COMPANY WESTERN NATIONAL ASSURANCE CO

WESTFIELD INS CO WESTPORT INSURANCE CORPORATION WILLIAMSBURG NATIONAL INS CO WORK FIRST CASUALTY CO XL INSURANCE AMERICA INC XL SPECIALTY INS CO ZENITH INS CO ZURICH AMERICAN INS CO ZURICH AMERICAN INS CO OF IL