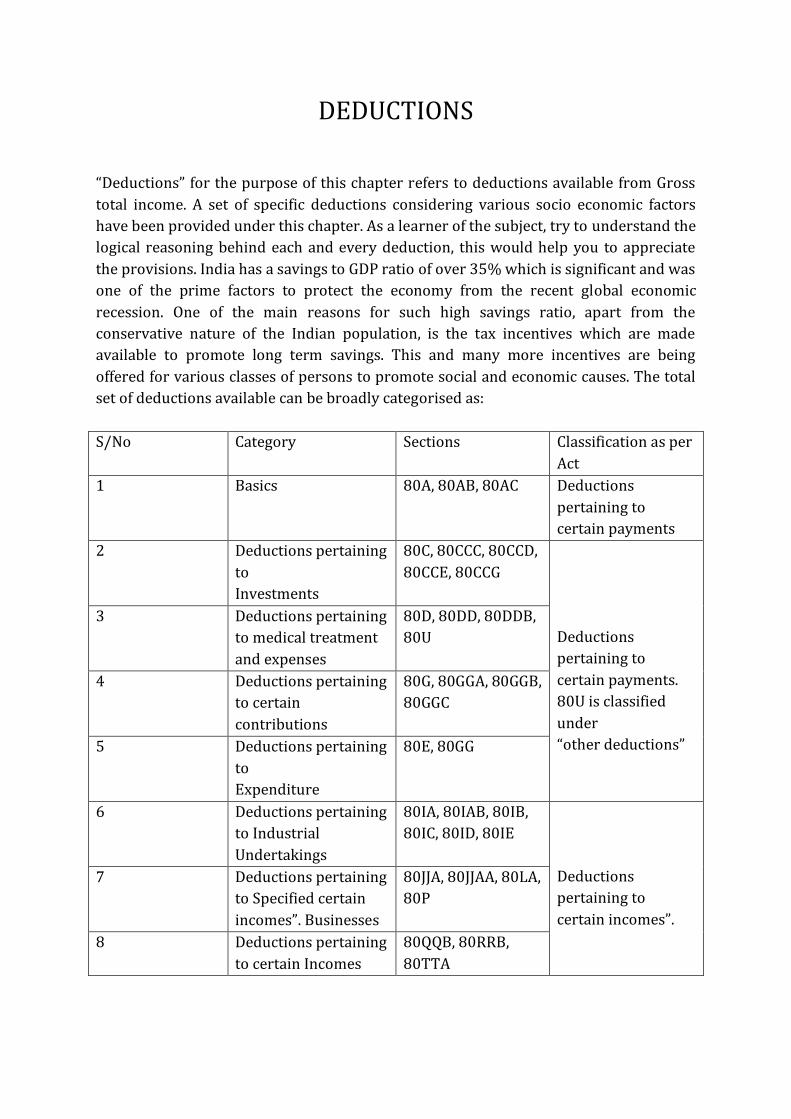

DEDUCTIONS “Deductions” for the purpose of this chapter refers to deductions available from Gross total income. A set of specific deductions considering various socio economic factors have been provided under this chapter. As a learner of the subject, try to understand the logical reasoning behind each and every deduction, this would help you to appreciate the provisions. India has a savings to GDP ratio of over 35% which is significant and was one of the prime factors to protect the economy from the recent global economic recession. One of the main reasons for such high savings ratio, apart from the conservative nature of the Indian population, is the tax incentives which are made available to promote long term savings. This and many more incentives are being offered for various classes of persons to promote social and economic causes. The total set of deductions available can be broadly categorised as: S/No Category Sections Classification as per Act 1 Basics 80A, 80AB, 80AC Deductions pertaining to certain payments 2 Deductions pertaining to Investments 80C, 80CCC, 80CCD, 80CCE, 80CCG Deductions pertaining to certain payments. 80U is classified under “other deductions” 3 Deductions pertaining to medical treatment and expenses 80D, 80DD, 80DDB, 80U 4 Deductions pertaining to certain contributions 80G, 80GGA, 80GGB, 80GGC 5 Deductions pertaining to Expenditure 80E, 80GG 6 Deductions pertaining to Industrial Undertakings 80IA, 80IAB, 80IB, 80IC, 80ID, 80IE Deductions pertaining to certain incomes”. 7 Deductions pertaining to Specified certain incomes”. Businesses 80JJA, 80JJAA, 80LA, 80P 8 Deductions pertaining to certain Incomes 80QQB, 80RRB, 80TTA

Transcript

DEDUCTIONS

“Deductions” for the purpose of this chapter refers to deductions available from Gross

total income. A set of specific deductions considering various socio economic factors

have been provided under this chapter. As a learner of the subject, try to understand the

logical reasoning behind each and every deduction, this would help you to appreciate

the provisions. India has a savings to GDP ratio of over 35% which is significant and was

one of the prime factors to protect the economy from the recent global economic

recession. One of the main reasons for such high savings ratio, apart from the

conservative nature of the Indian population, is the tax incentives which are made

available to promote long term savings. This and many more incentives are being

offered for various classes of persons to promote social and economic causes. The total

set of deductions available can be broadly categorised as:

S/No Category Sections Classification as per

Act

1 Basics 80A, 80AB, 80AC Deductions

pertaining to

certain payments

2 Deductions pertaining

to

Investments

80C, 80CCC, 80CCD,

80CCE, 80CCG

Deductions

pertaining to

certain payments.

80U is classified

under

“other deductions”

3 Deductions pertaining

to medical treatment

and expenses

80D, 80DD, 80DDB,

80U

4 Deductions pertaining

to certain

contributions

80G, 80GGA, 80GGB,

80GGC

5 Deductions pertaining

to

Expenditure

80E, 80GG

6 Deductions pertaining

to Industrial

Undertakings

80IA, 80IAB, 80IB,

80IC, 80ID, 80IE

Deductions

pertaining to

certain incomes”.

7 Deductions pertaining

to Specified certain

incomes”. Businesses

80JJA, 80JJAA, 80LA,

80P

8 Deductions pertaining

to certain Incomes

80QQB, 80RRB,

80TTA

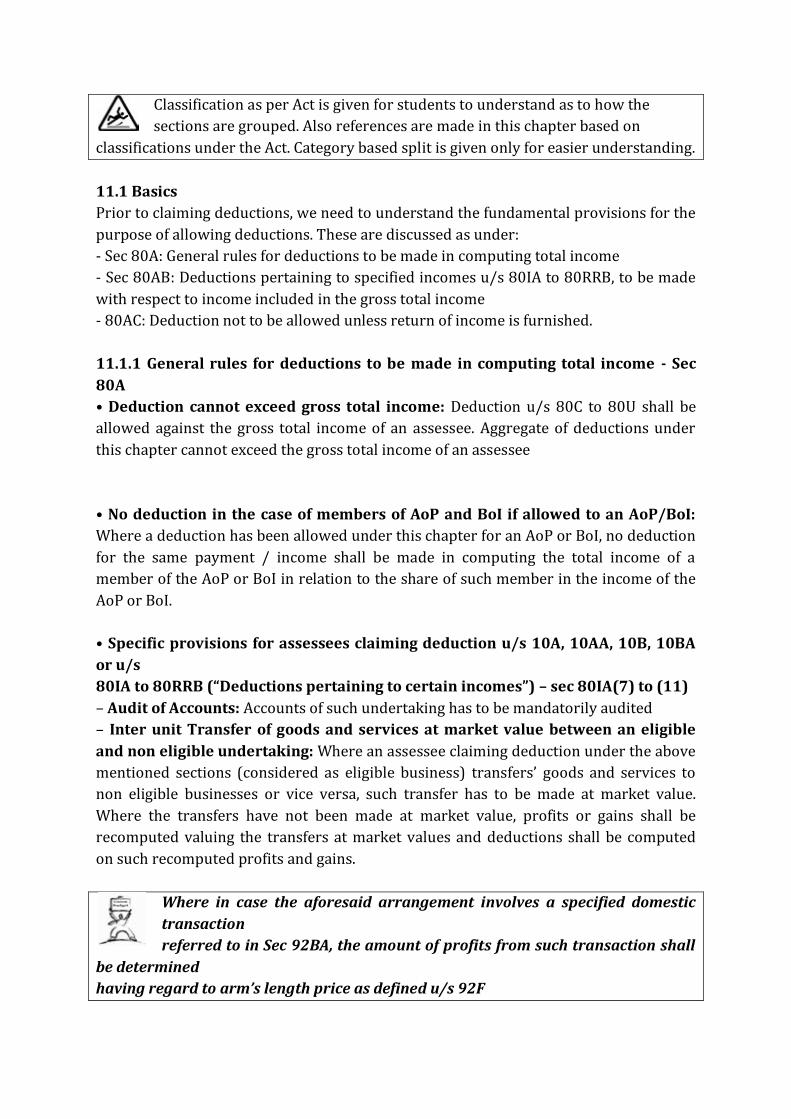

Classification as per Act is given for students to understand as to how the

sections are grouped. Also references are made in this chapter based on

classifications under the Act. Category based split is given only for easier understanding.

11.1 Basics

Prior to claiming deductions, we need to understand the fundamental provisions for the

purpose of allowing deductions. These are discussed as under:

- Sec 80A: General rules for deductions to be made in computing total income

- Sec 80AB: Deductions pertaining to specified incomes u/s 80IA to 80RRB, to be made

with respect to income included in the gross total income

- 80AC: Deduction not to be allowed unless return of income is furnished.

11.1.1 General rules for deductions to be made in computing total income - Sec

80A

• Deduction cannot exceed gross total income: Deduction u/s 80C to 80U shall be

allowed against the gross total income of an assessee. Aggregate of deductions under

this chapter cannot exceed the gross total income of an assessee

• No deduction in the case of members of AoP and BoI if allowed to an AoP/BoI:

Where a deduction has been allowed under this chapter for an AoP or BoI, no deduction

for the same payment / income shall be made in computing the total income of a

member of the AoP or BoI in relation to the share of such member in the income of the

AoP or BoI.

• Specific provisions for assessees claiming deduction u/s 10A, 10AA, 10B, 10BA

or u/s

80IA to 80RRB (“Deductions pertaining to certain incomes”) – sec 80IA(7) to (11)

– Audit of Accounts: Accounts of such undertaking has to be mandatorily audited

– Inter unit Transfer of goods and services at market value between an eligible

and non eligible undertaking: Where an assessee claiming deduction under the above

mentioned sections (considered as eligible business) transfers’ goods and services to

non eligible businesses or vice versa, such transfer has to be made at market value.

Where the transfers have not been made at market value, profits or gains shall be

recomputed valuing the transfers at market values and deductions shall be computed

on such recomputed profits and gains.

Where in case the aforesaid arrangement involves a specified domestic

transaction

referred to in Sec 92BA, the amount of profits from such transaction shall

be determined

having regard to arm’s length price as defined u/s 92F

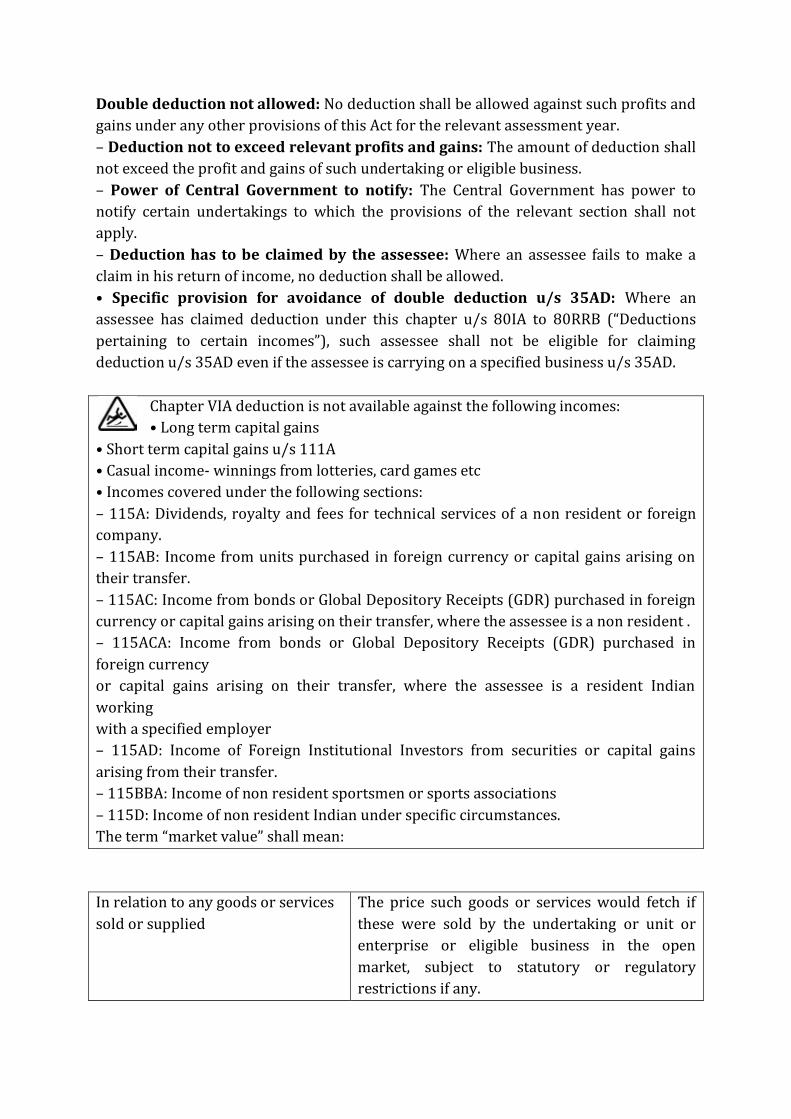

Double deduction not allowed: No deduction shall be allowed against such profits and

gains under any other provisions of this Act for the relevant assessment year.

– Deduction not to exceed relevant profits and gains: The amount of deduction shall

not exceed the profit and gains of such undertaking or eligible business.

– Power of Central Government to notify: The Central Government has power to

notify certain undertakings to which the provisions of the relevant section shall not

apply.

– Deduction has to be claimed by the assessee: Where an assessee fails to make a

claim in his return of income, no deduction shall be allowed.

• Specific provision for avoidance of double deduction u/s 35AD: Where an

assessee has claimed deduction under this chapter u/s 80IA to 80RRB (“Deductions

pertaining to certain incomes”), such assessee shall not be eligible for claiming

deduction u/s 35AD even if the assessee is carrying on a specified business u/s 35AD.

Chapter VIA deduction is not available against the following incomes:

• Long term capital gains

• Short term capital gains u/s 111A

• Casual income- winnings from lotteries, card games etc

• Incomes covered under the following sections:

– 115A: Dividends, royalty and fees for technical services of a non resident or foreign

company.

– 115AB: Income from units purchased in foreign currency or capital gains arising on

their transfer.

– 115AC: Income from bonds or Global Depository Receipts (GDR) purchased in foreign

currency or capital gains arising on their transfer, where the assessee is a non resident .

– 115ACA: Income from bonds or Global Depository Receipts (GDR) purchased in

foreign currency

or capital gains arising on their transfer, where the assessee is a resident Indian

working

with a specified employer

– 115AD: Income of Foreign Institutional Investors from securities or capital gains

arising from their transfer.

– 115BBA: Income of non resident sportsmen or sports associations

– 115D: Income of non resident Indian under specific circumstances.

The term “market value” shall mean:

In relation to any goods or services

sold or supplied

The price such goods or services would fetch if

these were sold by the undertaking or unit or

enterprise or eligible business in the open

market, subject to statutory or regulatory

restrictions if any.

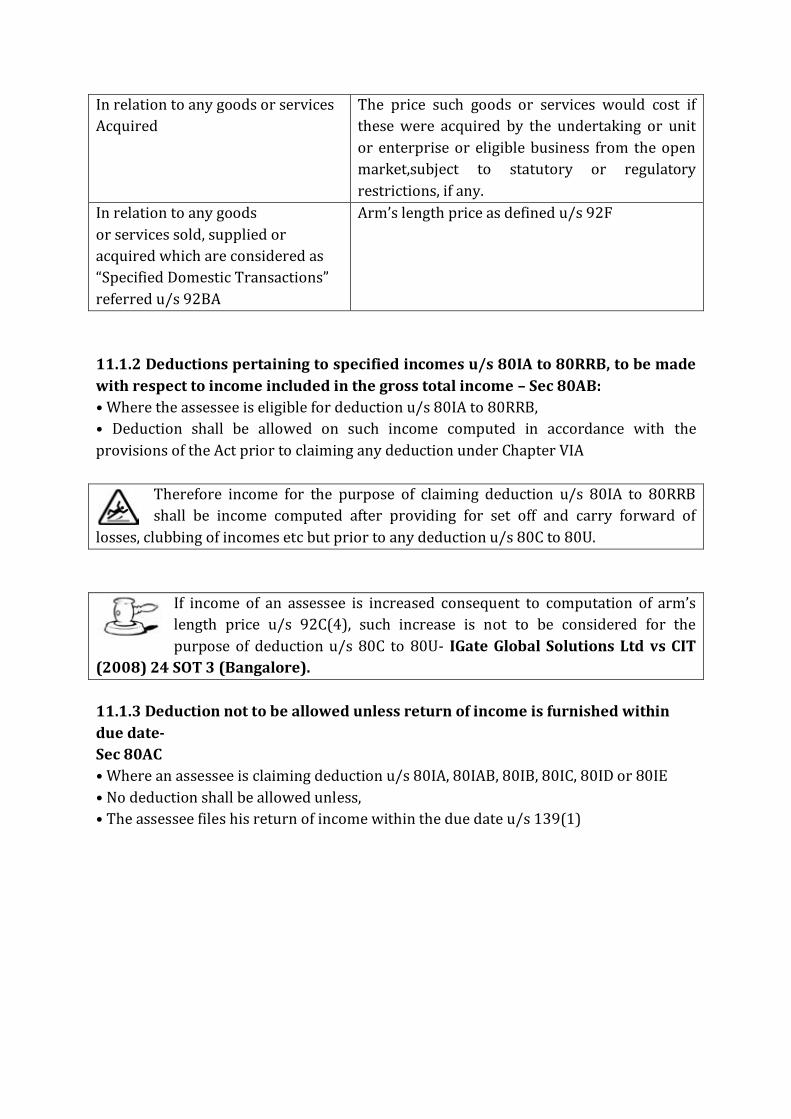

In relation to any goods or services

Acquired

The price such goods or services would cost if

these were acquired by the undertaking or unit

or enterprise or eligible business from the open

market,subject to statutory or regulatory

restrictions, if any.

In relation to any goods

or services sold, supplied or

acquired which are considered as

“Specified Domestic Transactions”

referred u/s 92BA

Arm’s length price as defined u/s 92F

11.1.2 Deductions pertaining to specified incomes u/s 80IA to 80RRB, to be made

with respect to income included in the gross total income – Sec 80AB:

• Where the assessee is eligible for deduction u/s 80IA to 80RRB,

• Deduction shall be allowed on such income computed in accordance with the

provisions of the Act prior to claiming any deduction under Chapter VIA

Therefore income for the purpose of claiming deduction u/s 80IA to 80RRB

shall be income computed after providing for set off and carry forward of

losses, clubbing of incomes etc but prior to any deduction u/s 80C to 80U.

If income of an assessee is increased consequent to computation of arm’s

length price u/s 92C(4), such increase is not to be considered for the

purpose of deduction u/s 80C to 80U- IGate Global Solutions Ltd vs CIT

(2008) 24 SOT 3 (Bangalore).

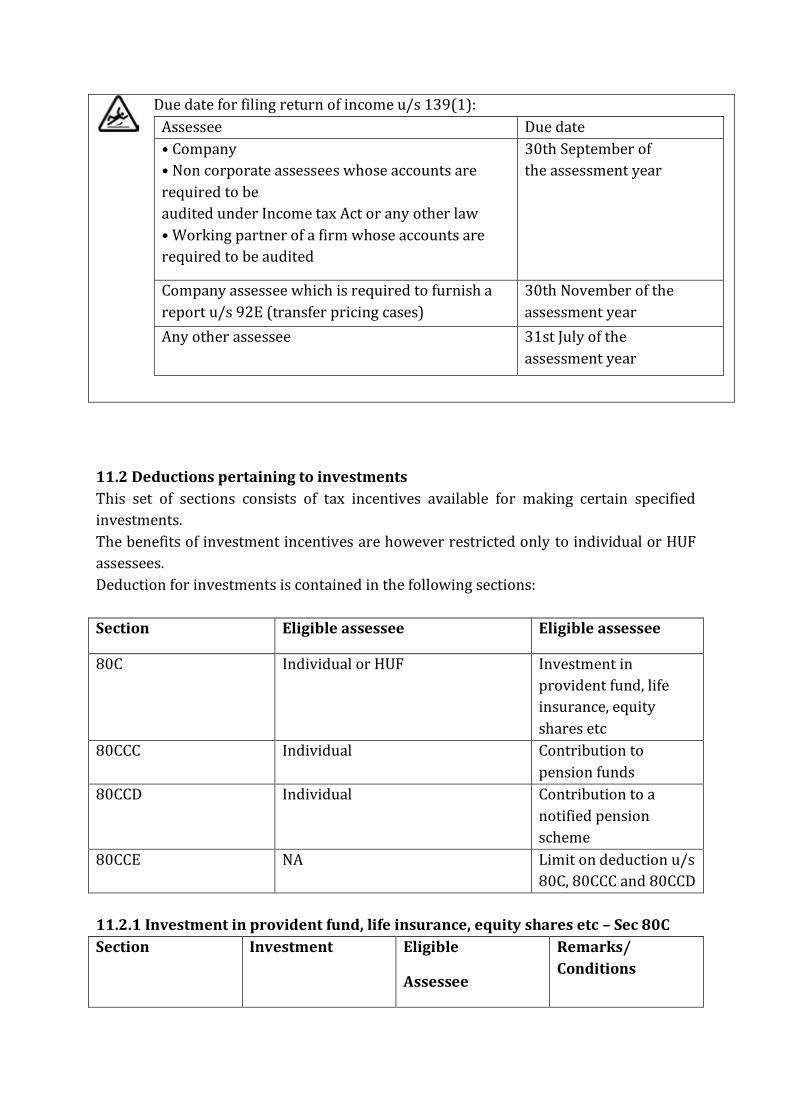

11.1.3 Deduction not to be allowed unless return of income is furnished within

due date-

Sec 80AC

• Where an assessee is claiming deduction u/s 80IA, 80IAB, 80IB, 80IC, 80ID or 80IE

• No deduction shall be allowed unless,

• The assessee files his return of income within the due date u/s 139(1)

Due date for filing return of income u/s 139(1):

Assessee Due date

• Company

• Non corporate assessees whose accounts are

required to be

audited under Income tax Act or any other law

• Working partner of a firm whose accounts are

required to be audited

30th September of

the assessment year

Company assessee which is required to furnish a

report u/s 92E (transfer pricing cases)

30th November of the

assessment year

Any other assessee 31st July of the

assessment year

11.2 Deductions pertaining to investments

This set of sections consists of tax incentives available for making certain specified

investments.

The benefits of investment incentives are however restricted only to individual or HUF

assessees.

Deduction for investments is contained in the following sections:

Section Eligible assessee Eligible assessee

80C Individual or HUF Investment in

provident fund, life

insurance, equity

shares etc

80CCC Individual Contribution to

pension funds

80CCD Individual Contribution to a

notified pension

scheme

80CCE NA Limit on deduction u/s

80C, 80CCC and 80CCD

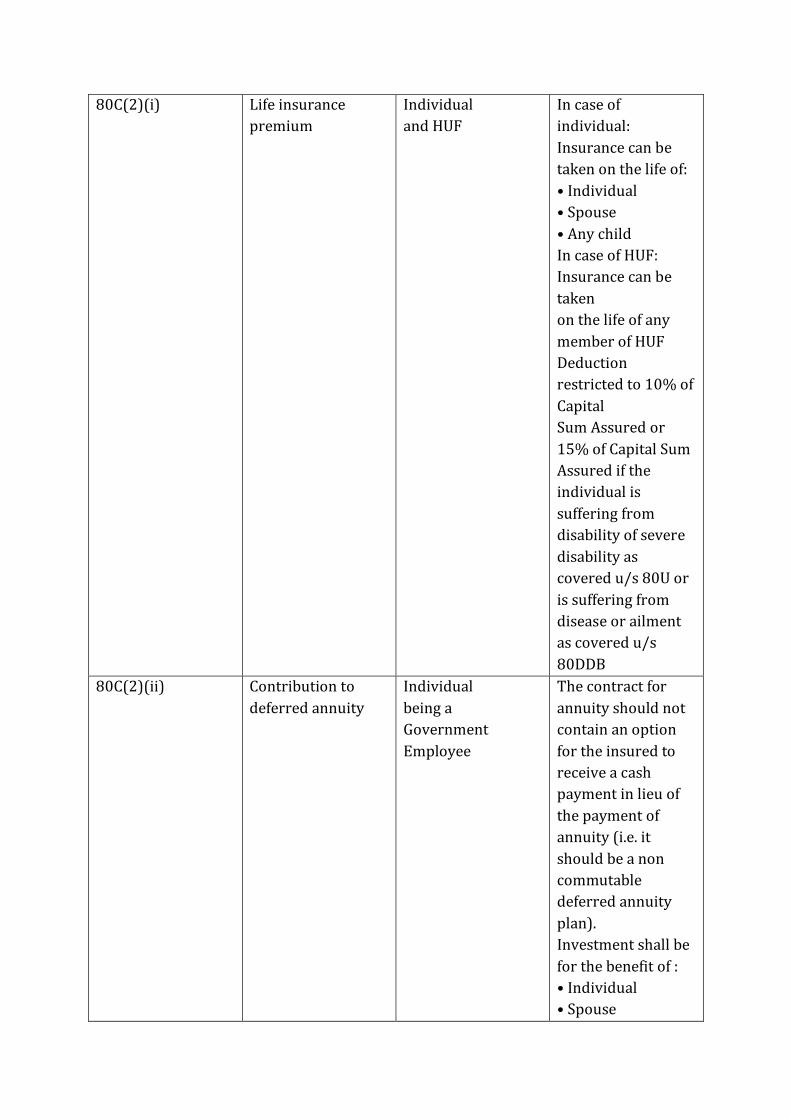

11.2.1 Investment in provident fund, life insurance, equity shares etc – Sec 80C

Section Investment Eligible

Assessee

Remarks/

Conditions

80C(2)(i) Life insurance

premium

Individual

and HUF

In case of

individual:

Insurance can be

taken on the life of:

• Individual

• Spouse

• Any child

In case of HUF:

Insurance can be

taken

on the life of any

member of HUF

Deduction

restricted to 10% of

Capital

Sum Assured or

15% of Capital Sum

Assured if the

individual is

suffering from

disability of severe

disability as

covered u/s 80U or

is suffering from

disease or ailment

as covered u/s

80DDB

80C(2)(ii) Contribution to

deferred annuity

Individual

being a

Government

Employee

The contract for

annuity should not

contain an option

for the insured to

receive a cash

payment in lieu of

the payment of

annuity (i.e. it

should be a non

commutable

deferred annuity

plan).

Investment shall be

for the benefit of :

• Individual

• Spouse

• Any child

80C(2)(iii) Contribution to

deferred annuity

Individual being a

Government

employee

Contribution should

be made as a

deduction from

salary. Sum

deducted shall

not exceed 1/5th of

the salary

Contribution shall

be for the benefit of:

• Individual

• Spouse

• Children

80C(2) (iv) Contribution to a

provident fund to

which Provident

Funds Act 1925

applies

(statutory

provident

fund)

Individual NA

80C(2) (v) Contribution to a

notified provident

fund set up by

Central Government

(15

year public

provident

fund)

Individual

and HUF

In case of

individual:

Investment shall be

in the name of :

• Individual

• Spouse

• Any child

In case of HUF:

Investment shall be

madein the name of

any member of HUF.

Maximum

investment ceiling

as per

Public Provident

Scheme is Rs

1,00,000.

However there is no

ceiling under the

Income Tax Act

80C(2)(vi) Contribution to Individual being an NA

recognised

provident fund

Employee

80C(2)

(vii)

Contribution to an

approved

superannuation

fund

Individual

being an

employee

NA

80C(2)

(viii)

Subscription to a

notified security or

deposit scheme.

Individual

and HUF

Scheme of deposit

or security must be

notified by the

Central Government

in

the Official Gazette

National Savings

Scheme has since

been

Notified

80C(2)

(ix)

Subscription to a

notified

savings certificates

–

National Savings

Certificates

(VIII Issue

Individual

and HUF

Savings certificates

must be notified by

the Central

Government in the

Official

Gazette

Interest accrued on

these certificates is

deemed to be

reinvested and also

qualify for

deduction under

this section.

80C(2)

(x)

Contribution to a

specified

unit linked plan

(ULIP) of UTI

Individual

and HUF

In case of

individual:

Investment shall be

in the name of :

• Individual

• Spouse

• Any child

In case of HUF:

Investment shall be

made in the name of

any member of HUF

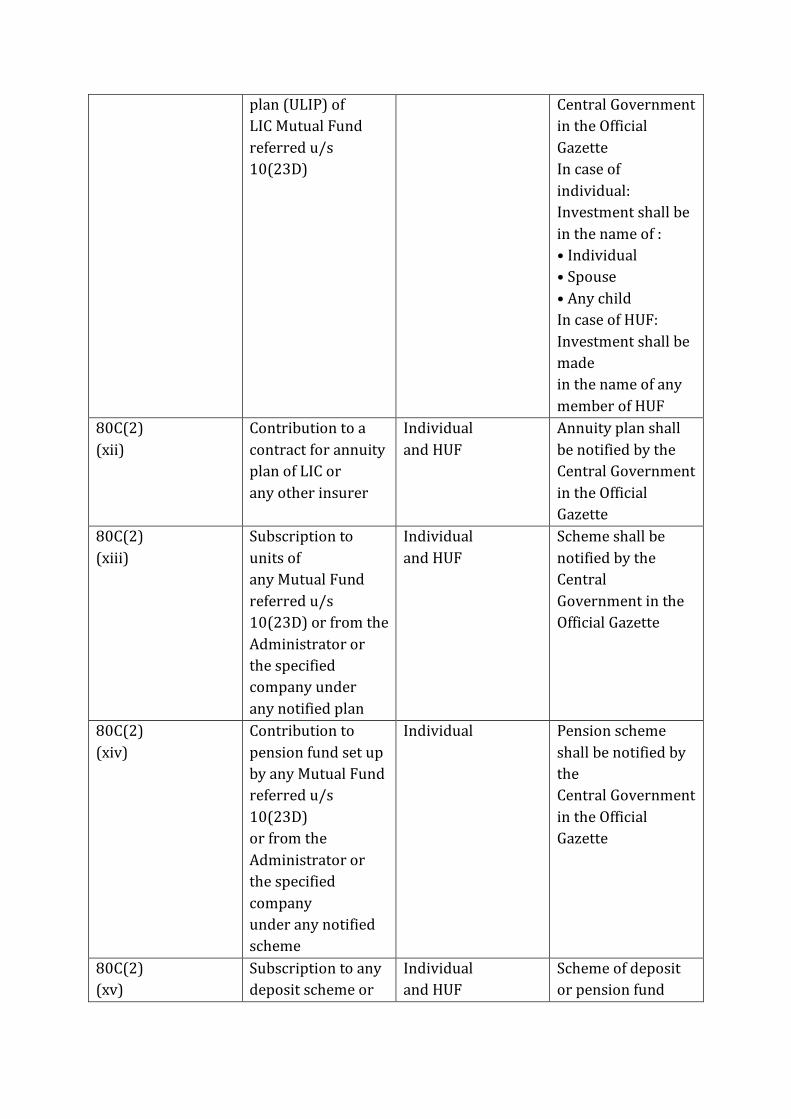

80C(2)

(xi)

Contribution to a

specified unit linked

Individual and HUF Insurance plan shall

be notified by the

plan (ULIP) of

LIC Mutual Fund

referred u/s

10(23D)

Central Government

in the Official

Gazette

In case of

individual:

Investment shall be

in the name of :

• Individual

• Spouse

• Any child

In case of HUF:

Investment shall be

made

in the name of any

member of HUF

80C(2)

(xii)

Contribution to a

contract for annuity

plan of LIC or

any other insurer

Individual

and HUF

Annuity plan shall

be notified by the

Central Government

in the Official

Gazette

80C(2)

(xiii)

Subscription to

units of

any Mutual Fund

referred u/s

10(23D) or from the

Administrator or

the specified

company under

any notified plan

Individual

and HUF

Scheme shall be

notified by the

Central

Government in the

Official Gazette

80C(2)

(xiv)

Contribution to

pension fund set up

by any Mutual Fund

referred u/s

10(23D)

or from the

Administrator or

the specified

company

under any notified

scheme

Individual Pension scheme

shall be notified by

the

Central Government

in the Official

Gazette

80C(2)

(xv)

Subscription to any

deposit scheme or

Individual

and HUF

Scheme of deposit

or pension fund

contribution to a

pension fund set up

by

National Housing

Bank

shall

be notified by the

Central Government

in

the Official Gazette

80C(2)

(xvi)

Subscription to any

such deposit

scheme of:

(a) a public sector

company engaged

in providing long-

term finance for

construction or

purchase

of houses in India

for

residential

purposes; or

(b) any authority

constituted in India

by

or under any law

enacted either for

the purpose of

dealing with

andsatisfying the

need for

housing

accommodation

or for the purpose

of

planning,

development

or improvement of

cities,

towns and villages,

or for

both

Individual

and HUF

Scheme of deposit

shall be notified by

the Central

Government in the

Official

Gazette

80C(2)

(xvii)

Payment of tuition

fees

whether at the time

of

admission or

Individual Tuition fees exclude

any payment

towards

any development

fees or donation or

thereafter:

(a)to any university,

college, school or

other

educational

institution

situated within

India

(b) for the purpose

of fulltime

Education

payment of similar

nature.

Deduction shall be

restricted to any

two

children of an

individual.

80C(2)

(xviii)

Principal

repayment of

housing loan taken

for

the purpose of

acquisition

or construction of

house

property

Individual

and HUF

Repayment of the

amount borrowed

by the

assessee from:

• Central or State

Government

• Any bank

including a

cooperative bank

• LIC

• National Housing

Bank

• Any Indian public

company specified

u/s 36(1)(viii)

• Any company in

which the public are

substantially

interested or any

cooperative

society engaged in

financing

the construction of

houses

• Assessee’s

employer where

such

employer is an

authority or a board

or a corporation or

any other body

established or

constituted under a

Central or State Act,

or

• Assessee’s

employer where

such

employer is a public

company or a

public sector

company or a

university

established by law

or a college

affiliated

to such university

or a local authority

or

a co-operative

society.

80C(2)

(xviii)

Stamp duty,

registration

fee and other

expenses for

the purpose of

transfer of

such house

property to the

assessee

Individual

and HUF

Deduction shall not

be available for

payment towards:

(A) the admission

fee, cost of share

and

initial deposit which

a shareholder of a

company or a

member of a co-

operative

society has to pay

for becoming such

shareholder or

member; or

(B) the cost of any

addition or

alteration

to, or renovation or

repair of, the house

property which is

carried out:

- after the issue of

the completion

certificate or

- after the house

property or any

part thereof has

been occupied.

(C) any expenditure

eligible for

deduction

u/s 24

80C(2)

(xix)

Subscription to

equity

shares or

debentures

forming part of an

eligible

issue of an

approved

public company or

subscription to an

eligible issue of

capital by public

financial institution.

Individual

and HUF

Eligible issue of

capital means an

issue by

a public company

formed and

registered

in India or a public

financial institution

and the entire

proceeds of such

issue are

utilized wholly and

exclusively for the

purpose of business

referred u/s

80IA(4).

80C(2)

(xx)

Subscription to

units of

any mutual funds

referred

u/s 10(23D)

Individual

and HUF

The amount of

subscription to such

units

is subscribed only

in the eligible issue

of

capital of any

company.

Eligible issue of

capital shall have

the

same meaning as

given u/s

80C(2)(xix)

80C(2)

(xxi)

Investment in term

deposit

with a scheduled

Individual

and HUF

Term deposit shall

be for a period of

not

bank less than 5 years

Scheme of deposit

shall be notified by

the

Central Government

in the Official

Gazette

80C(2)

(xxii)

Subscription to

specified

bonds issued by

National

Bank for

Agriculture

and Rural

Development

(NABARD)

Individual

and HUF

Bonds shall be

notified by the

Central

Government in the

Official Gazette

80C(2)

(xxiii)

Contribution under

the

Senior Citizens

Savings

Scheme Rules, 2004

Individual

and HUF

NA

80C(2)

(xxiv)

Contribution to five

year term deposit in

an account under

the Post Office Term

Deposit Rules, 1981.

Individual

and HUF

NA

• Deduction u/s 80C is allowed only on payment basis

• Benefit of deduction under this section is available to a non resident individual

• Deduction u/s 80C towards life insurance premiums shall be restricted to the extent of

least

of the following:

– Actual amount of premium paid

10% of actual capital sum assured (Amendment by Finance Act 2012)

Actual capital sum assured has been defined in relation to a life insurance policy shall

mean the

minimum amount assured under the policy on happening of the insured event at any

time during the term of the policy, not taking into account—

(i) the value of any premium agreed to be returned; or

(ii) any benefit by way of bonus or otherwise over and above the sum actually assured,

which is to be or may be received under the policy by any person.

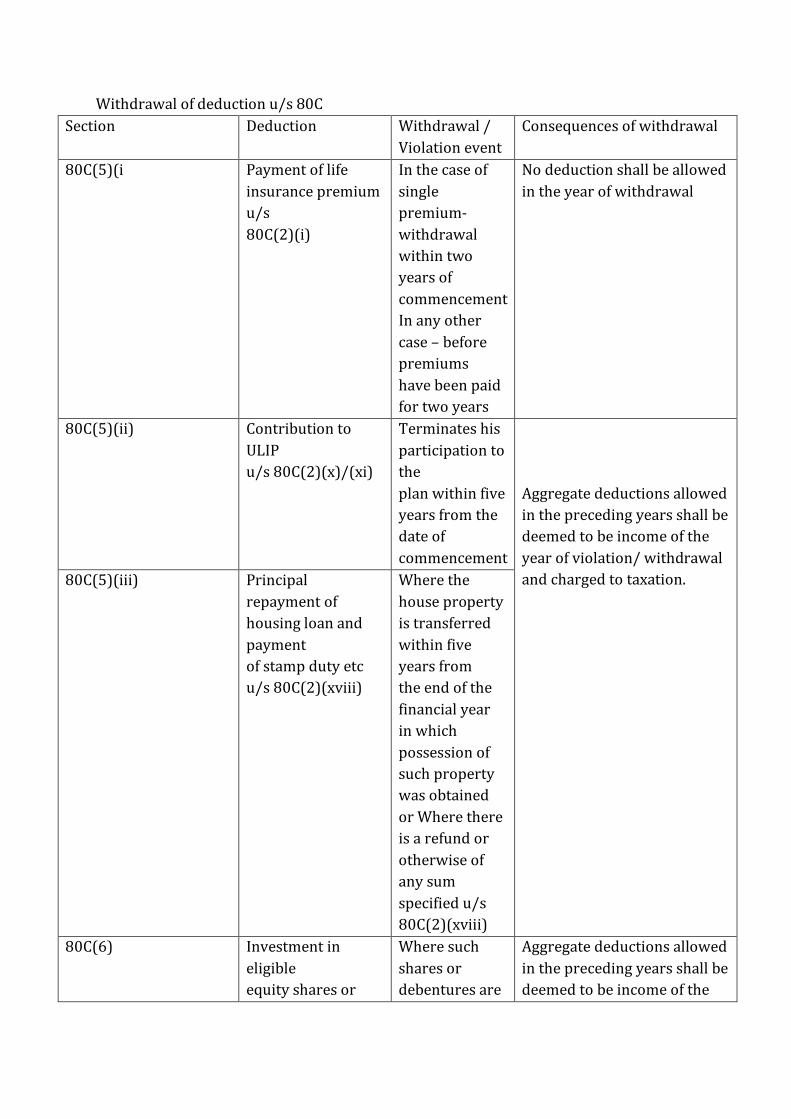

Withdrawal of deduction u/s 80C

Section Deduction Withdrawal /

Violation event

Consequences of withdrawal

80C(5)(i Payment of life

insurance premium

u/s

80C(2)(i)

In the case of

single

premium-

withdrawal

within two

years of

commencement

In any other

case – before

premiums

have been paid

for two years

No deduction shall be allowed

in the year of withdrawal

80C(5)(ii) Contribution to

ULIP

u/s 80C(2)(x)/(xi)

Terminates his

participation to

the

plan within five

years from the

date of

commencement

Aggregate deductions allowed

in the preceding years shall be

deemed to be income of the

year of violation/ withdrawal

and charged to taxation. 80C(5)(iii) Principal

repayment of

housing loan and

payment

of stamp duty etc

u/s 80C(2)(xviii)

Where the

house property

is transferred

within five

years from

the end of the

financial year

in which

possession of

such property

was obtained

or Where there

is a refund or

otherwise of

any sum

specified u/s

80C(2)(xviii)

80C(6) Investment in

eligible

equity shares or

Where such

shares or

debentures are

Aggregate deductions allowed

in the preceding years shall be

deemed to be income of the

debentures u/s

80C(2)

(xix)

transferred

within a period

of three years

from the date of

acquisition.

year of violation/ withdrawal

and charged to taxation.

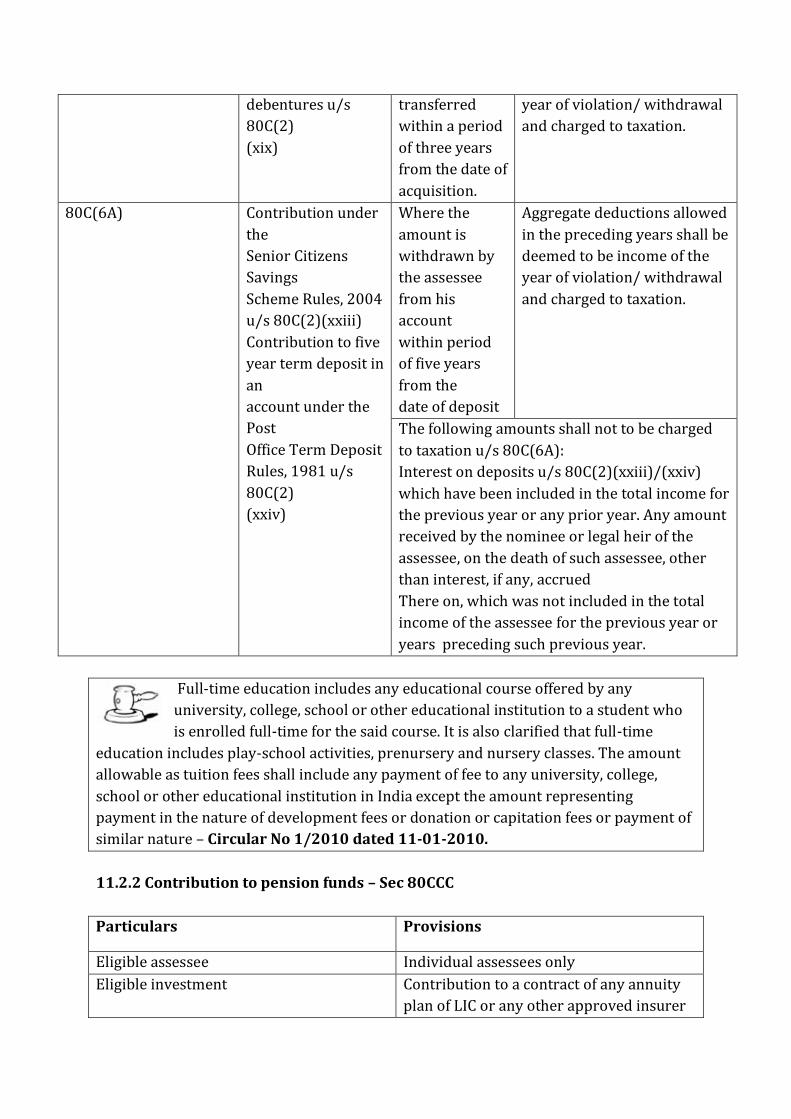

80C(6A) Contribution under

the

Senior Citizens

Savings

Scheme Rules, 2004

u/s 80C(2)(xxiii)

Contribution to five

year term deposit in

an

account under the

Post

Office Term Deposit

Rules, 1981 u/s

80C(2)

(xxiv)

Where the

amount is

withdrawn by

the assessee

from his

account

within period

of five years

from the

date of deposit

Aggregate deductions allowed

in the preceding years shall be

deemed to be income of the

year of violation/ withdrawal

and charged to taxation.

The following amounts shall not to be charged

to taxation u/s 80C(6A):

Interest on deposits u/s 80C(2)(xxiii)/(xxiv)

which have been included in the total income for

the previous year or any prior year. Any amount

received by the nominee or legal heir of the

assessee, on the death of such assessee, other

than interest, if any, accrued

There on, which was not included in the total

income of the assessee for the previous year or

years preceding such previous year.

Full-time education includes any educational course offered by any

university, college, school or other educational institution to a student who

is enrolled full-time for the said course. It is also clarified that full-time

education includes play-school activities, prenursery and nursery classes. The amount

allowable as tuition fees shall include any payment of fee to any university, college,

school or other educational institution in India except the amount representing

payment in the nature of development fees or donation or capitation fees or payment of

similar nature – Circular No 1/2010 dated 11-01-2010.

11.2.2 Contribution to pension funds – Sec 80CCC

Particulars Provisions

Eligible assessee Individual assessees only

Eligible investment Contribution to a contract of any annuity

plan of LIC or any other approved insurer

for receiving pension from a fund set up by

LIC or any other insurer referred u/s

10(23AAB)

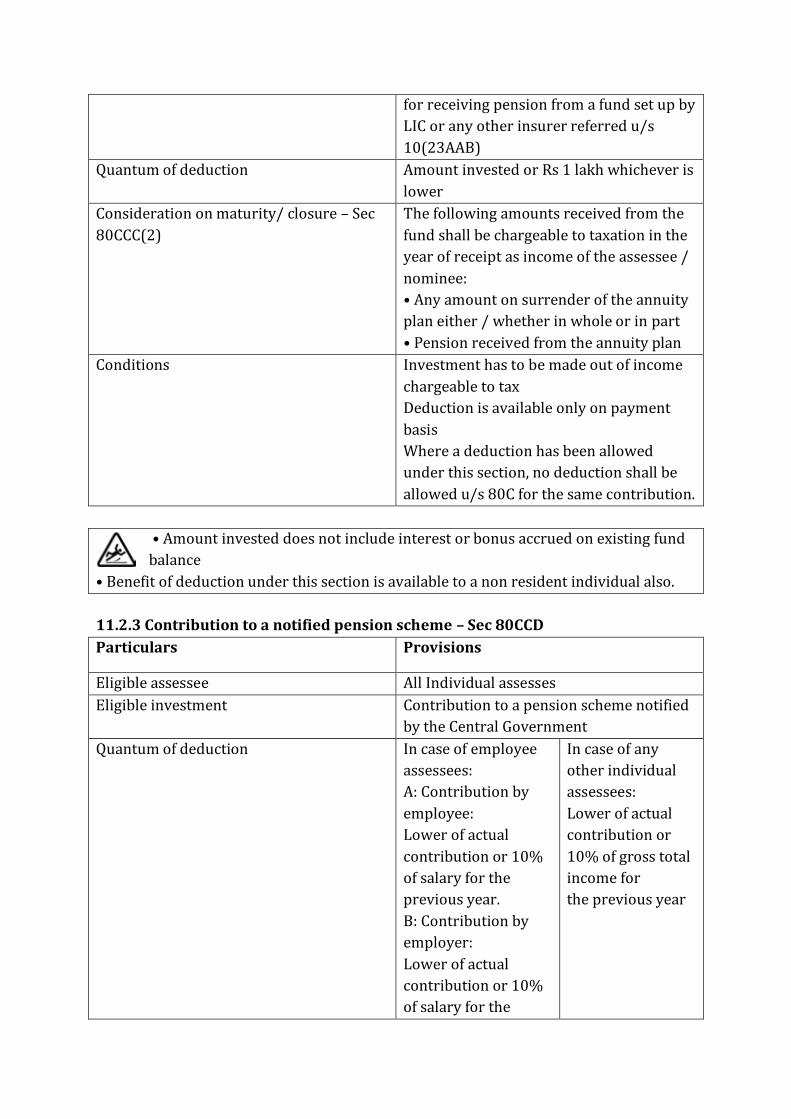

Quantum of deduction Amount invested or Rs 1 lakh whichever is

lower

Consideration on maturity/ closure – Sec

80CCC(2)

The following amounts received from the

fund shall be chargeable to taxation in the

year of receipt as income of the assessee /

nominee:

• Any amount on surrender of the annuity

plan either / whether in whole or in part

• Pension received from the annuity plan

Conditions Investment has to be made out of income

chargeable to tax

Deduction is available only on payment

basis

Where a deduction has been allowed

under this section, no deduction shall be

allowed u/s 80C for the same contribution.

• Amount invested does not include interest or bonus accrued on existing fund

balance

• Benefit of deduction under this section is available to a non resident individual also.

11.2.3 Contribution to a notified pension scheme – Sec 80CCD

Particulars Provisions

Eligible assessee All Individual assesses

Eligible investment Contribution to a pension scheme notified

by the Central Government

Quantum of deduction In case of employee

assessees:

A: Contribution by

employee:

Lower of actual

contribution or 10%

of salary for the

previous year.

B: Contribution by

employer:

Lower of actual

contribution or 10%

of salary for the

In case of any

other individual

assessees:

Lower of actual

contribution or

10% of gross total

income for

the previous year

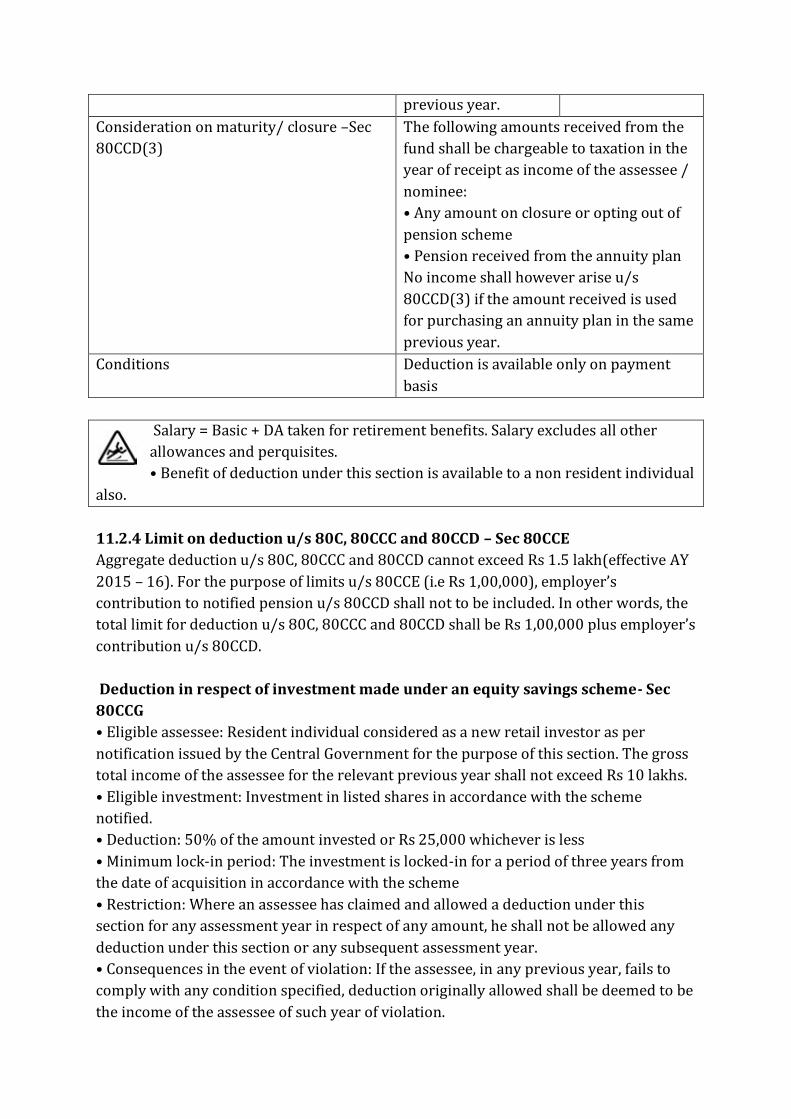

previous year.

Consideration on maturity/ closure –Sec

80CCD(3)

The following amounts received from the

fund shall be chargeable to taxation in the

year of receipt as income of the assessee /

nominee:

• Any amount on closure or opting out of

pension scheme

• Pension received from the annuity plan

No income shall however arise u/s

80CCD(3) if the amount received is used

for purchasing an annuity plan in the same

previous year.

Conditions Deduction is available only on payment

basis

Salary = Basic + DA taken for retirement benefits. Salary excludes all other

allowances and perquisites.

• Benefit of deduction under this section is available to a non resident individual

also.

11.2.4 Limit on deduction u/s 80C, 80CCC and 80CCD – Sec 80CCE

Aggregate deduction u/s 80C, 80CCC and 80CCD cannot exceed Rs 1.5 lakh(effective AY

2015 – 16). For the purpose of limits u/s 80CCE (i.e Rs 1,00,000), employer’s

contribution to notified pension u/s 80CCD shall not to be included. In other words, the

total limit for deduction u/s 80C, 80CCC and 80CCD shall be Rs 1,00,000 plus employer’s

contribution u/s 80CCD.

Deduction in respect of investment made under an equity savings scheme- Sec

80CCG

• Eligible assessee: Resident individual considered as a new retail investor as per

notification issued by the Central Government for the purpose of this section. The gross

total income of the assessee for the relevant previous year shall not exceed Rs 10 lakhs.

• Eligible investment: Investment in listed shares in accordance with the scheme

notified.

• Deduction: 50% of the amount invested or Rs 25,000 whichever is less

• Minimum lock-in period: The investment is locked-in for a period of three years from

the date of acquisition in accordance with the scheme

• Restriction: Where an assessee has claimed and allowed a deduction under this

section for any assessment year in respect of any amount, he shall not be allowed any

deduction under this section or any subsequent assessment year.

• Consequences in the event of violation: If the assessee, in any previous year, fails to

comply with any condition specified, deduction originally allowed shall be deemed to be

the income of the assessee of such year of violation.

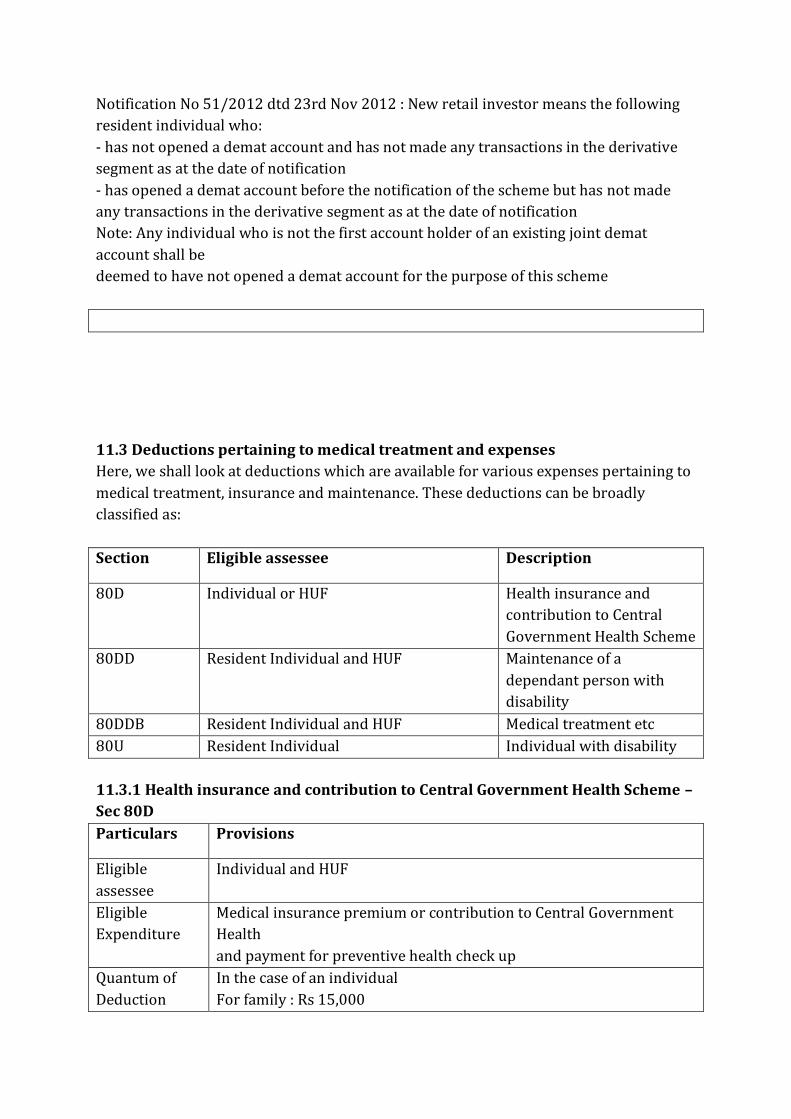

Notification No 51/2012 dtd 23rd Nov 2012 : New retail investor means the following

resident individual who:

- has not opened a demat account and has not made any transactions in the derivative

segment as at the date of notification

- has opened a demat account before the notification of the scheme but has not made

any transactions in the derivative segment as at the date of notification

Note: Any individual who is not the first account holder of an existing joint demat

account shall be

deemed to have not opened a demat account for the purpose of this scheme

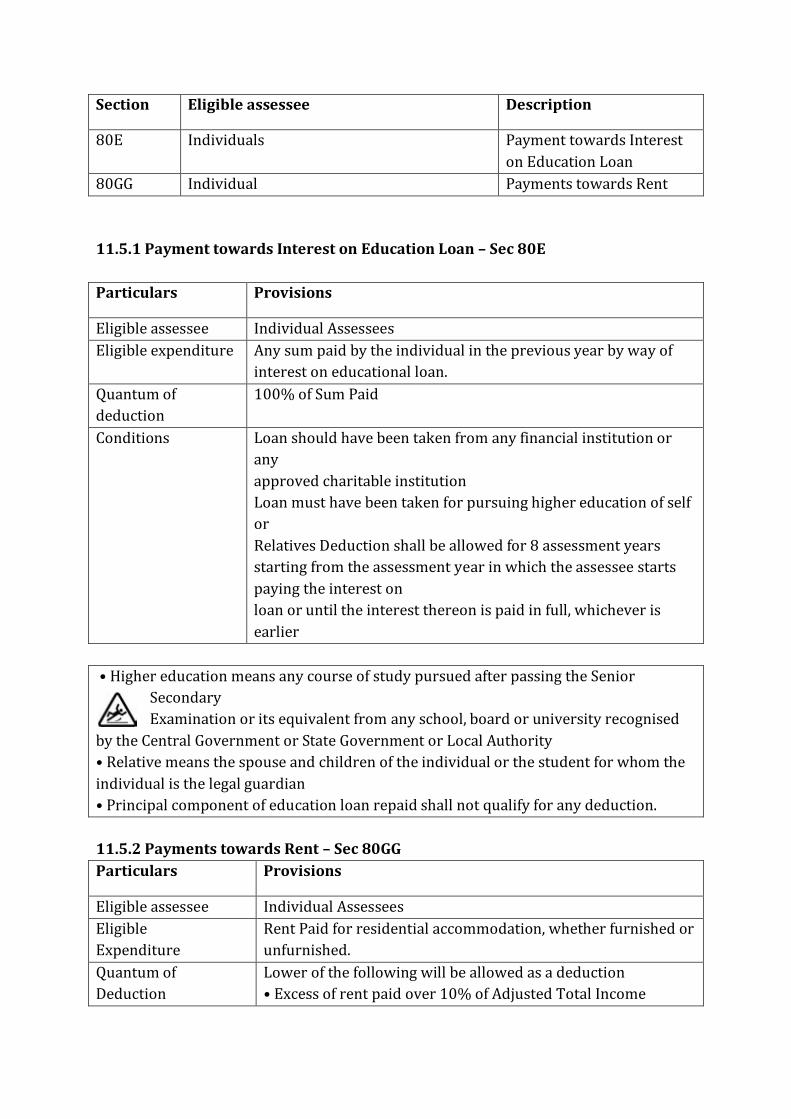

11.3 Deductions pertaining to medical treatment and expenses

Here, we shall look at deductions which are available for various expenses pertaining to

medical treatment, insurance and maintenance. These deductions can be broadly

classified as:

Section Eligible assessee Description

80D Individual or HUF Health insurance and

contribution to Central

Government Health Scheme

80DD Resident Individual and HUF Maintenance of a

dependant person with

disability

80DDB Resident Individual and HUF Medical treatment etc

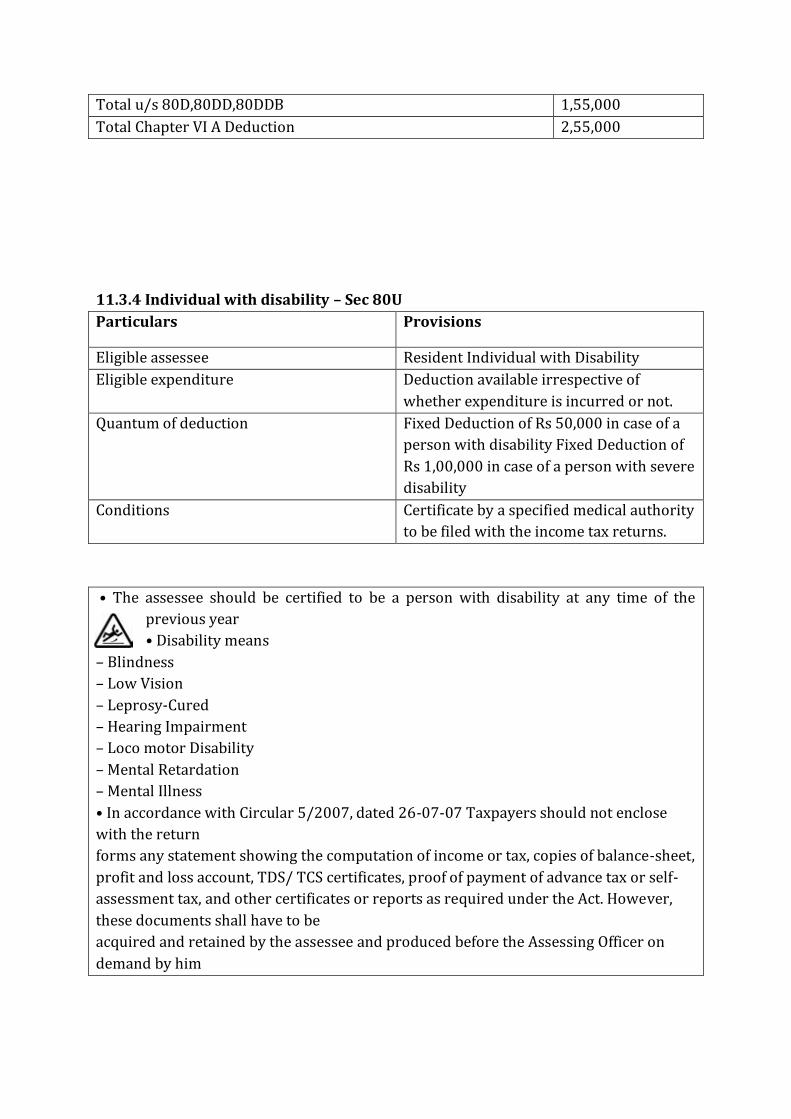

80U Resident Individual Individual with disability

11.3.1 Health insurance and contribution to Central Government Health Scheme –

Sec 80D

Particulars Provisions

Eligible

assessee

Individual and HUF

Eligible

Expenditure

Medical insurance premium or contribution to Central Government

Health

and payment for preventive health check up

Quantum of

Deduction

In the case of an individual

For family : Rs 15,000

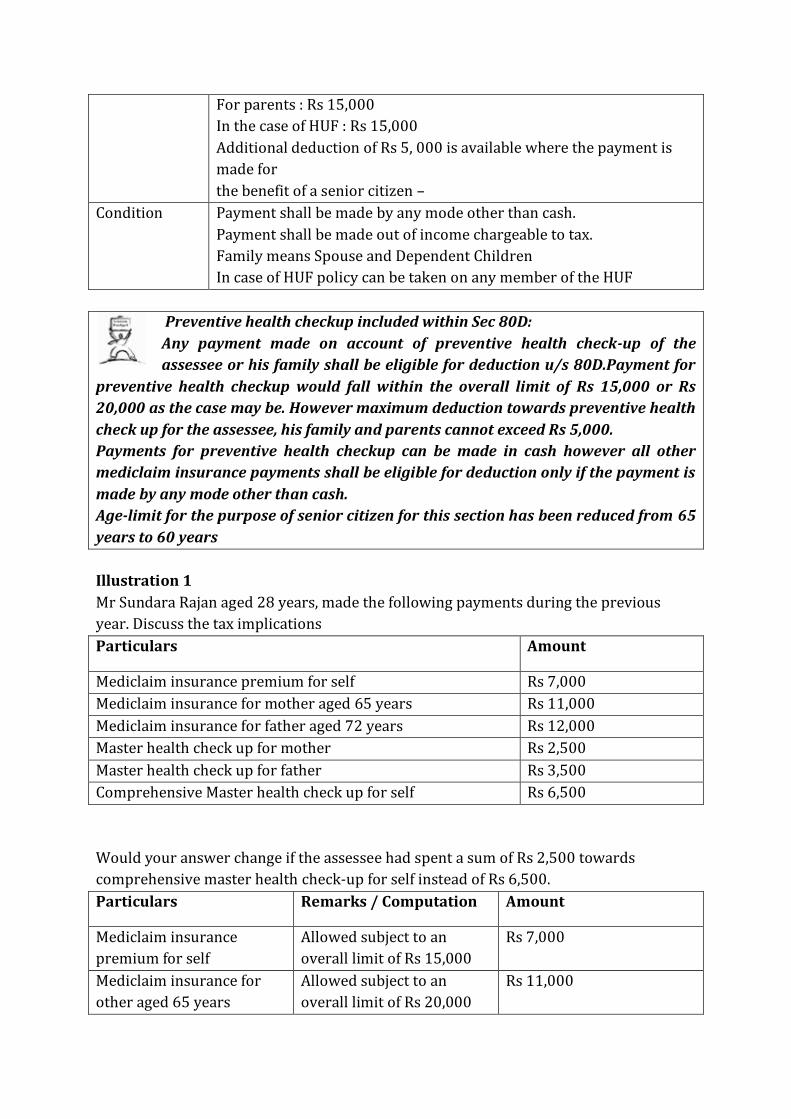

For parents : Rs 15,000

In the case of HUF : Rs 15,000

Additional deduction of Rs 5, 000 is available where the payment is

made for

the benefit of a senior citizen –

Condition Payment shall be made by any mode other than cash.

Payment shall be made out of income chargeable to tax.

Family means Spouse and Dependent Children

In case of HUF policy can be taken on any member of the HUF

Preventive health checkup included within Sec 80D:

Any payment made on account of preventive health check-up of the

assessee or his family shall be eligible for deduction u/s 80D.Payment for

preventive health checkup would fall within the overall limit of Rs 15,000 or Rs

20,000 as the case may be. However maximum deduction towards preventive health

check up for the assessee, his family and parents cannot exceed Rs 5,000.

Payments for preventive health checkup can be made in cash however all other

mediclaim insurance payments shall be eligible for deduction only if the payment is

made by any mode other than cash.

Age-limit for the purpose of senior citizen for this section has been reduced from 65

years to 60 years

Illustration 1

Mr Sundara Rajan aged 28 years, made the following payments during the previous

year. Discuss the tax implications

Particulars Amount

Mediclaim insurance premium for self Rs 7,000

Mediclaim insurance for mother aged 65 years Rs 11,000

Mediclaim insurance for father aged 72 years Rs 12,000

Master health check up for mother Rs 2,500

Master health check up for father Rs 3,500

Comprehensive Master health check up for self Rs 6,500

Would your answer change if the assessee had spent a sum of Rs 2,500 towards

comprehensive master health check-up for self instead of Rs 6,500.

Particulars Remarks / Computation Amount

Mediclaim insurance

premium for self

Allowed subject to an

overall limit of Rs 15,000

Rs 7,000

Mediclaim insurance for

other aged 65 years

Allowed subject to an

overall limit of Rs 20,000

Rs 11,000

Mediclaim insurance for

father aged 72 years

Allowed subject to an

overall limit of Rs 20,000

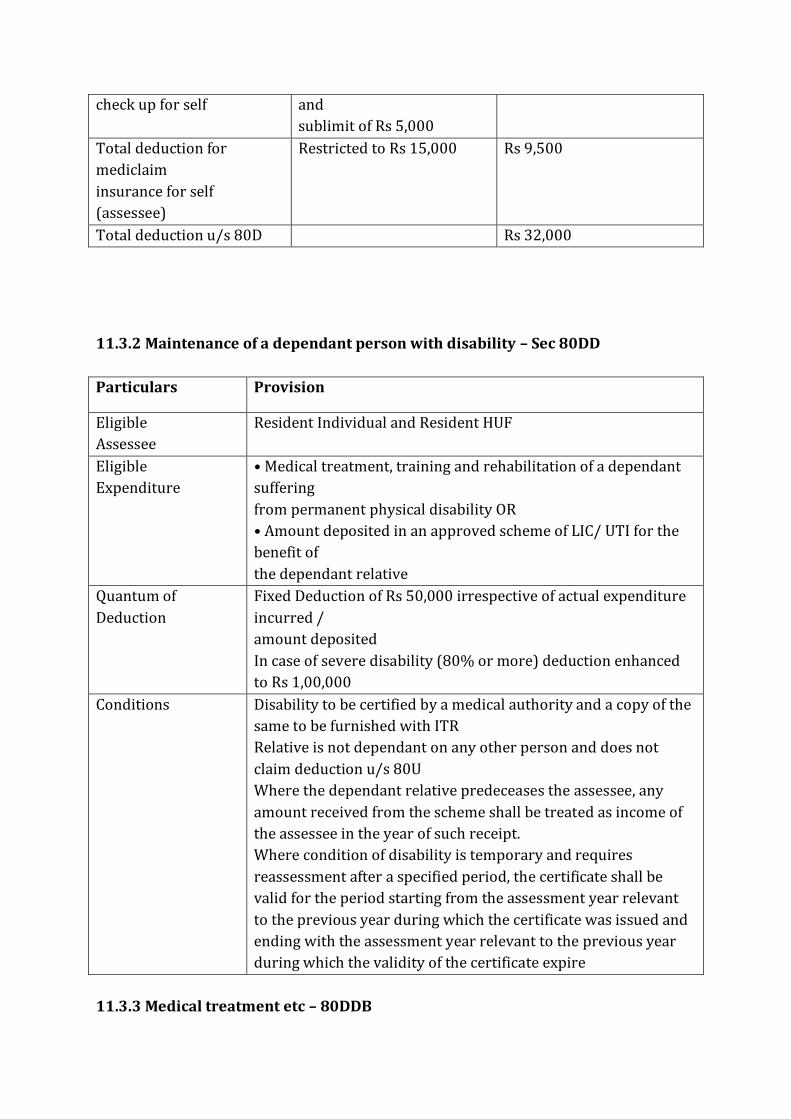

Rs 12,000

Total deduction for

mediclaim

Insurance

Restricted to Rs 7,000 for

the assessee and Rs 20,000

for the parents

Rs 27,000

Master health check up for

mother

Rs 2,500

Master health check up for

father

Rs 3,500

Comprehensive Master

health check up for self

Rs 6,500

Total preventive

expenditure

Rs 12,500

Maximum preventive

expenditure allowed as a

deduction u/s 80D

Rs 5,000 (this is the

aggregate limit for the

assessee, family and

parents)

Rs 5,000

Total deduction u/s 80D Rs 32,000

Particulars Remarks / Computation Amount

Mediclaim insurance for

mother aged 65 years

Allowed subject to an

overall

limit of Rs 20,000

Rs 11,000

Mediclaim insurance for

father aged 72 years

Rs 12,000

Master health check up for

Mother

Allowed subject to the

overall limit of Rs 20,000

and

sublimit of Rs 5,000

Rs 2,500

Master health check up for

father

Rs 3,500

Total deduction for

mediclaim

insurance for parents

Restricted to Rs 20,000 for

the parents

Rs 20,000

Since the mediclaim insurance premium paid for parents exceeds Rs 20,000, there

seems to be

no surplus limits available for claiming preventive health check up expenditure

incurred for parents of the assessee

Mediclaim insurance

premium for self

Allowed subject to an

overall

limit of Rs 15,000

Rs 7,000

Comprehensive Master

health

Allowed subject to the

overall limit of Rs 15,000

Rs 2,500

check up for self and

sublimit of Rs 5,000

Total deduction for

mediclaim

insurance for self

(assessee)

Restricted to Rs 15,000 Rs 9,500

Total deduction u/s 80D Rs 32,000

11.3.2 Maintenance of a dependant person with disability – Sec 80DD

Particulars Provision

Eligible

Assessee

Resident Individual and Resident HUF

Eligible

Expenditure

• Medical treatment, training and rehabilitation of a dependant

suffering

from permanent physical disability OR

• Amount deposited in an approved scheme of LIC/ UTI for the

benefit of

the dependant relative

Quantum of

Deduction

Fixed Deduction of Rs 50,000 irrespective of actual expenditure

incurred /

amount deposited

In case of severe disability (80% or more) deduction enhanced

to Rs 1,00,000

Conditions Disability to be certified by a medical authority and a copy of the

same to be furnished with ITR

Relative is not dependant on any other person and does not

claim deduction u/s 80U

Where the dependant relative predeceases the assessee, any

amount received from the scheme shall be treated as income of

the assessee in the year of such receipt.

Where condition of disability is temporary and requires

reassessment after a specified period, the certificate shall be

valid for the period starting from the assessment year relevant

to the previous year during which the certificate was issued and

ending with the assessment year relevant to the previous year

during which the validity of the certificate expire

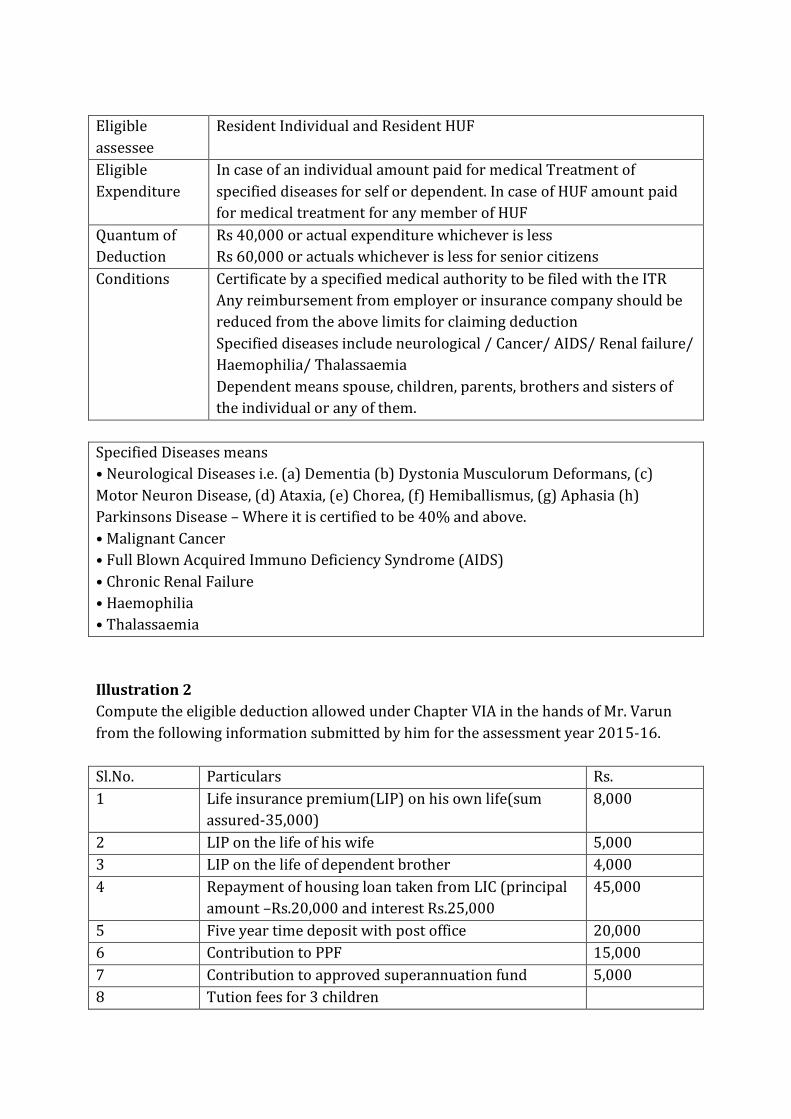

11.3.3 Medical treatment etc – 80DDB

Eligible

assessee

Resident Individual and Resident HUF

Eligible

Expenditure

In case of an individual amount paid for medical Treatment of

specified diseases for self or dependent. In case of HUF amount paid

for medical treatment for any member of HUF

Quantum of

Deduction

Rs 40,000 or actual expenditure whichever is less

Rs 60,000 or actuals whichever is less for senior citizens

Conditions Certificate by a specified medical authority to be filed with the ITR

Any reimbursement from employer or insurance company should be

reduced from the above limits for claiming deduction

Specified diseases include neurological / Cancer/ AIDS/ Renal failure/

Haemophilia/ Thalassaemia

Dependent means spouse, children, parents, brothers and sisters of