43

Deep Dive: 08 Retail and Wholesale Distribution Date: September 2016 FINAL REPORT

Deep Dive: 08 Retail and Wholesale Distribution

Date: September 2016

FINAL REPORT

September 2016 2

Contents Executive Summary .............................................................................................................. 3

1 Introduction ............................................................................................................... 6

2 Definitions ................................................................................................................. 7

3 Significance ............................................................................................................... 8

4 Businesses and Employment .................................................................................. 10

5 Skills ........................................................................................................................ 29

6 Key Assets .............................................................................................................. 32

7 Growth Potential ...................................................................................................... 36

8 Spatial Considerations ............................................................................................. 41

September 2016 3

Executive Summary Context

British Retail and Wholesaling is a success story that is continually evolving and

incorporating new forms of shopping. Amid the talk of the decline of the retail sector the

evidence in this Deep Dive highlights the fact that the retail sector as a whole is buoyant,

with growing opportunities. It is also an important source of employment for around 4.5m

people across the UK. The sector has seen substantial transformation, as consumers

have increasingly combined different channels of shopping, both online and in-store,

which has had a significant impact on the nature of work, as well as on the supply chains

of retailers, wholesalers and distribution businesses.

The sector is a significant employer in Greater Manchester (GM), with almost 200,000 jobs

(16.5% of total employment in GM) and over 20,000 companies. By subsector, Retail

accounts for the majority of employment (123,000 jobs) many of which are part time.

Wholesale is also a significant source of work, employing an estimated 58,000 people. In

terms of economic output, the Retail and Wholesaling sector generates £6.7bn annually,

equivalent to 12.7% of total Gross Value Added (GVA) in GM.

Across GM, the retail market is becoming increasingly polarised between a handful of

large corporate chains, and a long-tail of small independent retailers. While independent

retailing has been in decline for several years (in terms of number and market share),

major chains have grown substantially – including their diversification into multi-channel

retail. There is a clear hierarchy of retail centres in GM, led by Manchester city centre and

the Trafford Centre, with other concentrations in GM’s eight principal town centres.

The Growth Opportunity

The baseline forecast for GM suggests an extra 17,600 jobs by 2035, and an average

employment growth rate of 0.4% per annum. This equates to an additional £4.3bn in GM’s

economy each year by 2035. However, the central Accelerated Growth Scenario suggests

the number of additional jobs could be higher, growing by 26,300 employees from 2014 to

2035, this would equal a further £4.9bn GVA per annum in GM’s economy by 2035. Over

half of this growth will be within the wholesale sub-sector. There will also be significant

demand to replace the existing workforce leaving the sector due to retirement.

Replacement demand forecasts suggest this equates to 27,000 jobs per annum up to

2035.

In recent years, technological change, social media and increased consumer expectations

have all contributed to a change in consumption patterns. This has already caused a

fundamental change in the retail and distribution industries, as well as manufacturers and

logistics businesses. Furthermore, the change in consumer behaviour is linked to

changing leisure preferences and, going forward, some places will have the opportunity to

re-define the role of town centres to provide a balance of retail, food and drink and leisure

to address the challenges of reducing footfall.

September 2016 4

The growth of online shopping and growth in multi-channel shopping will continue and

while much of the impact will be in changing how people shop, it will also enable some

producers and retailers to both reach a larger, and sometimes a different, market, as well

as increase their market share. In addition, there will also be more opportunities available

to new entrants and niche producers to enter the market. It will also have a significant

influence on the future of customer fulfilment and distribution companies.

E-Commerce and customer expectations of speed in delivery will boost the wholesale and

distribution sector over the next twenty years which will impact on town centres. Research

from the Javelin Group forecast that by 2020 there will be 31% fewer non-food stores in

the UK, and 21% less floor-space than at present. Growth in e-commerce will increase the

need for regional and local distribution centres, as well as centres for sales returns; and

the introduction of new pick-up points in existing retail centres. Larger multiple retailers

throughout GM will need to consider how their high street locations could change or be

enhanced to facilitate a greater level of click and collect sales, acting as a point for

collection and returns of online purchases. The presence of Click and Collect is seen as a

positive approach for most retailers, as it reduces costs of delivering to multiple homes

and means people spend more in store when they come to collect the item that they

ordered, providing this is supported at a town centre scale.

GM already benefits from strong existing distribution sites. MDS Transmodal have

highlighted opportunities for expansion of Regional and Urban Distribution Centres (RDCs

and UDCs) and potentially National Distribution Centres in GM, which have the potential to

offer significant employment growth, in particular in locations near centres of population

growth. 1

Key Challenges

There is a major challenge in updating the role and purpose of town centres, particularly

the eight principal centres. In particular, this will be promoting them as locations that

provide choice for retail consumers, alongside other reasons to visit. Increasingly, the

leisure offer2 of town centres will be important in complementing and strengthening their

retail role, helping to attract and maintain larger multiple retail brands alongside their other

uses such as housing, civic space and public realm.

There is a degree of uncertainty about how people will shop in the multi-channel era.

There may well be a changing role for physical stores as more people shop online. ‘Click

& Collect’ could become key to physical stores remaining competitive in the market for

consumers’ convenience. Businesses will also have to look to provide a customer

‘experience’ in order to retain footfall.

There will be significant demand within the sector to replace the existing workforce, many

of whom are ageing. Replacement demand figures suggest that there could be up to

1 MDS Transmodal, September 2014, Greater Manchester Logistics Study

2 Detail of GM’s leisure offer is not contained in this report but in the Hospitality, Tourism and Sport Deep Dive

September 2016 5

27,000 leavers from the sector per annum (mostly retirements) and there will be a

requirement to fill many of these roles, potentially leading to recruitment difficulties.

The use of new technologies is leading to greater skills requirements, particularly in IT,

while increased automation, such as self-checkouts, will reduce some roles but create

new ones in technical support. New technology is also pervasive across Wholesale and

Distribution industries3. As a result, the wider sector will see a marked increase in staff

requiring IT-related qualifications and skills.

Spatial Considerations

While changes to consumer behaviour towards online retail will adversely impact high

streets, the net impact of these changes in the larger context of change across GM

remains unclear. Both population growth and the expansion of key growth sectors will lead

to rising numbers of consumers and purchasing power. This suggests town centres, in

particular those with concentrations of employment in sectors other than retail and those

with higher residential populations, will see increased footfall and thus correspondingly

growth in the retail sector. Given their existing strengths, Manchester city centre and the

Trafford Centre would be expected to remain as the prime GM retailing locations.

Demand from the consumer for out-of-town Retail is likely to remain strong, mostly due to

ease of access from the consumer perspective and the flexibility offered around floor

space configurations for occupiers. It is likely that existing out-of-town locations such as

Middlebrook retail park in Bolton or the Lowry Outlet Centre in Salford Quays will continue

to perform well, and older facilities will be renovated to secure trading positions. At a larger

scale, the Trafford Centre has developed to become the second most significant retail

centre in GM (after the city centre), with a retail and leisure offer that attracts visitors from

within and far beyond GM.

Online retail continues to be a significant growth area nationally and for GM. This presents

opportunities for digital businesses that will cluster in areas where there are existing sector

strengths. The growth of online retail will also drive increasing need for major logistics

sites, alongside many new smaller distribution hubs that are close to customers to enable

retailers to meet demanding delivery timescales.

GM already benefits from strong existing retailer distribution sites, for example ASDA has

a distribution site at Kingsway Business Park in Rochdale and the Heywood Distribution

Park site, as well as strong road and rail links across the UK. GM is also home to National

Distribution Centres, including the 100,000sqm Shop Direct national distribution centre in

Shaw Oldham. MDS Transmodal4 have highlighted opportunities for expansion of Regional

and Urban Distribution Centres (RDCs and UDCs) as well as potentially National

Distribution Centres in GM, which could help stimulate growth opportunities for the Retail,

Wholesale Distribution.

3 Wholesale Distribution Industries largely focus on the sale of goods. Logistics (for which there is a separate deep dive report)

largely focuses on transport. 4 MDS Transmodal, September 2014, Greater Manchester Logistics Study

September 2016 6

1 Introduction 1.1 This report is one of a series of sector ‘Deep Dive’ reports. It was commissioned by the

Greater Manchester Combined Authority (GMCA) as part of Greater Manchester’s

economic evidence base, and in particular, to inform the development of the Greater

Manchester Spatial Framework (GMSF). The report is part of a wide ranging analysis of

the economic issues and opportunities across GM. The evidence is at a greater degree

of granularity than has ever been done before for any industry sector in GM.

1.2 The Deep Dive research comprises the following reports:

Part 1: Research summary: Providing an overview of the key issues affecting

productivity and participation in GM, including demographic structures and labour market

profiles. It also includes an assessment of the key factors that are expected to drive

economic change in the global, UK and GM economies in the coming decades. It

summarises the key findings from each of the sector chapters.

Part 2: Sector Deep Dive reports: Covering the following key sectors: Manufacturing;

Business, Finance and Professional Services; Digital & Creative; Health/Social Care and

Health Innovation; Low Carbon and Environmental Goods and Services; Logistics; Retail

and Wholesale Distribution; Hospitality, Tourism and Sport; and Construction.

1.3 For each sector, the analysis covers:

Current make-up of the sector, covering the size, scale and its relative importance to GM

and geographic footprint, not constrained to administrative boundaries5;

Recent growth rates and growth potential (using forecasts by Oxford Economics);

The location of critical assets and institutions across GM;

Market opportunities and threats for the sector, including long-term trends which will shape

the future scale, needs and location of the sector; and

The spatial considerations of accelerated levels of growth in the sector.

1.4 The Deep Dive research has been produced by New Economy, with Deloitte supporting

at the scoping stage and Ekosgen reviewing the outputs and providing independent

quality assurance. The work has been developed drawing on input from both the public

and the private sectors. Workshops have been held with Chief Executives and local

authority officers in each GM district to check and challenge the evidence presented; to

assess how it fits with local plans and to draw out the GM wide implications of the

research. Consultation has also been undertaken with experts from a wide range of

public and private partners including the Manchester Growth Company, GM’s

universities, TfGM, GM Chamber, pro-Manchester, Manchester Airport, NHS North West

and LEP and Business Leadership Council members to provide further input and

challenge to the evidence presented. The work also draws upon and feeds into the

findings of the Northern Powerhouse Independent Economic Review.

5 The data provided in the sector deep dive series of reports is used to support the understanding of the major trends within the

sector and to set the context of the sector against the wider economy and UK.

September 2016 7

2 Definitions 2.1 Retail and Wholesale comprises all units whose principal economic activity involves

purchasing transportable goods and reselling them and/or acting as an agent between

sellers and buyers of goods. Such goods are subject only to handling and packaging; they

are not transformed in any substantial way. The broad sector comprises not only direct

trading between two parties but also that arranged on behalf of one or more third parties.

2.2 The three primary sub-sectors reviewed in this report are:

Retail: The Retail economic activity consists primarily of a business selling goods on its

own account, or on behalf of a third party, predominantly to households. Retail trade is

mostly carried out in premises accessible to anyone. There are, however, other forms of

Retail activity such as mail, telephone or internet selling. Examples of retail firms in GM

include: J D Sports, N Brown Group Plc (incorporating J D Williams), Co-operative Group

Ltd, Bestway National Chemists Ltd and Bestway Panacea Healthcare Ltd (operating Well

pharmacies, formerly Co-op Pharmacy), Timpson, Findel Plc (incorporating Express Gifts

Ltd), Adidas, AO World Plc, Boohoo.com, Missguided, Entertainment Magpie Ltd and

Dabs.com.

Wholesale: The Wholesale (or Distribution) trade groups comprise all units whose

economic activity consists primarily in reselling merchandise in their own name to retailers,

industrial, commercial, institutional or professional users or to other wholesalers, such as

wholesale of household goods, machinery, equipment and suppliers, food, beverages and

tobacco. Examples of wholesale firms in GM include 6: Brother, BASF Plc, AG Parfett &

Sons, Burdens, Brammer, Mawdsley Brooks & Co Ltd, Visage Group, Danish Crown,

Yearsley Food, Spectrum Brands Ltd, LWC Drinks, Kingsland Drinks, J P McDougall & Co.

Motor Trade: Motor Trade activity is made up of various subsectors such as motor vehicle

and parts dealers, sale of new motor vehicles, sale of used motor vehicles, retail sale of

fuel. Examples of motor trade firms in GM include: Lookers Motor Group, Marubeni Auto

Investment UK, Williams Group, RRG Group, Tetrosyl. OMC Motor Group, National Tyre

Service Ltd, West Pennine Trucks.

2.3 The table below displays the specific SIC codes used in this report.

SIC Code(s) Description Retail

47 Retail trade, except of motor vehicles and motorcycles

Wholesale

46 Wholesale trade, except of motor vehicles and motorcycles

Motor Trades

45 Wholesale and retail trade and repair of motor vehicles and motorcycles

6 There is a separate Deep Dive on Logistics which includes logistics firms which serve major retailers.

September 2016 8

3 Significance 3.1 Retailing is one of the UK’s top service industries and is strongly connected to many

other areas of the economy, in particular the Logistics, Business, Financial &

Professional Services, Agriculture, Digital and Creative and Manufacturing sectors.

Retail is also employment intensive with nearly one-in-six jobs in the UK being in the

sector. Within GM, Retail provides the second highest employment of any sector in the

conurbation and counts for 16.5% of total employment.

3.2 The sector contributes a significant amount to both employment and GVA. Indeed, the

sector provides the second highest output of any sector nationally, only behind

Business, Financial & Professional Services. In GM the sector produced £6.7bn of

output in 2013, or 12.7% of the total GM economy. The retail sector is also the third

fastest growing sector in GM.

3.3 The market is becoming increasingly polarised between the numerically dominant

independent retailers and a handful of large corporate chains. Independent retailing has

been declining for several years (in terms of number and market share), while major

chains have been growing substantially – including their diversification to multi-channel

retail. Within GM the Retail sector is large, diverse and especially prominent in scale

and growth within Manchester city centre and Trafford Centre.

3.4 The parameters of UK retail are changing at an ever-increasing rate. The growth and

adoption of digital and mobile technologies has brought about structural change in

people’s everyday lives, which has transformed the retail landscape. Retail has changed

more in the last five years than in the previous twenty. An informed and ever-connected

consumer can now shop at any time of the day or night, from anywhere, post reviews

instantly and share their experiences with their friends and online communities across

the world.

3.5 A range of factors drive growth and change across the industry, these include:

The speed of change in the retail market.

Structural change in the market.

The impact of technology in the sector.

Sustainability of destinations, operations and trading formats.

How global trends affect local markets.

Delivering new floor space.

How capital flows affect the retail market.

The relationship of in and out-of-town retail.

Re-allocating redundant space.

3.6 While some of the variables aren’t new, for example, ageing population, globalisation

and resource scarcity, the impact on retail is still profound. Moreover, the impact of

technology and consumer attitudes has proved to be an additional challenge. Shoppers

continue to want products to be available faster and more easily. They also want to shop

at their convenience for authentic products with proven provenance. They also look for

September 2016 9

personalised customer experiences. These conditions have led to unprecedented levels

of creativity in the sector, facilitated by the extending influence of the digital and mobile

era. Today’s consumers expect a seamless, multi-channel experience that goes beyond

traditional retail formats. They browse a wide range of products instore or online (by PC,

mobile or tablet), arrange next-day delivery to their nearest pick-up point and have the

option of returning it to a store on their way to a high street restaurant – all in an

uncomplicated way.

3.7 During the last 10 years there has been a significant shift in the shopping channels used

by consumers. In 2004, 47% of total retail sales occurred in town centres. This is

estimated to have fallen to 39% in 2014. While the proportion of spend in out-of-town

and neighbourhood venues has remained relatively flat, the growth of non-store (online,

mail order and TV) spend has come at the expense of town centres.7 This has impacted

all parts of the retail sector, but is particularly evident in terms of clothing and, with the

ever advancing development of Click and Collect this will continue to impact on high

street retailing.

3.8 The ever-connected consumer has transparency of pricing, quality and service at their

disposal at all times. They are increasingly searching for an online shopping experience,

with similar touchpoints in the physical high street environment. The use of technology

in stores and on high streets to support the multichannel proposition provides

consumers with the opportunity to make experiential purchases – in both goods and

services. This seamless experience will increasingly derive much greater satisfaction for

customers and create much deeper social engagement. The future high street

experience will therefore become more than a retail channel. Instead retailers and high

streets could partner to provide a one-stop for consumer interaction. New services will

create a seamless physical retail experience, responding to factors such as digital and

mobile technologies and social interaction.

3.9 The push toward consumer-focused integrated mobile platforms, paired with collective

marketing, has important ramifications for the high street. Just as online has affected

store sales, the reverse is also true, with evidence suggesting the presence of a

physical high street store can also drive a “halo effect” of online sales within close

proximity. This can be especially powerful for smaller retailers establishing their brand.

3.10 The logistics and distribution industries have also changed radically in the last five years

in response to changing consumer behaviours, with next-day and same-day delivery

becoming increasingly commonplace, and significant growth in local distribution jobs.

This has led to the development of ‘Fourth Party Logistics Firms’, businesses that act as

a supply chain manager which assembles the resources, capabilities, and technology of

its own organisation (which may also include major national and regional logistics

activity) with those of complementary service/distribution providers to deliver a

comprehensive supply chain solution from national to local level. This is driving

increases in localised delivery activity, alongside new local employment.

7 British Retail Consortium (2015): The changing Face of Retail

September 2016 10

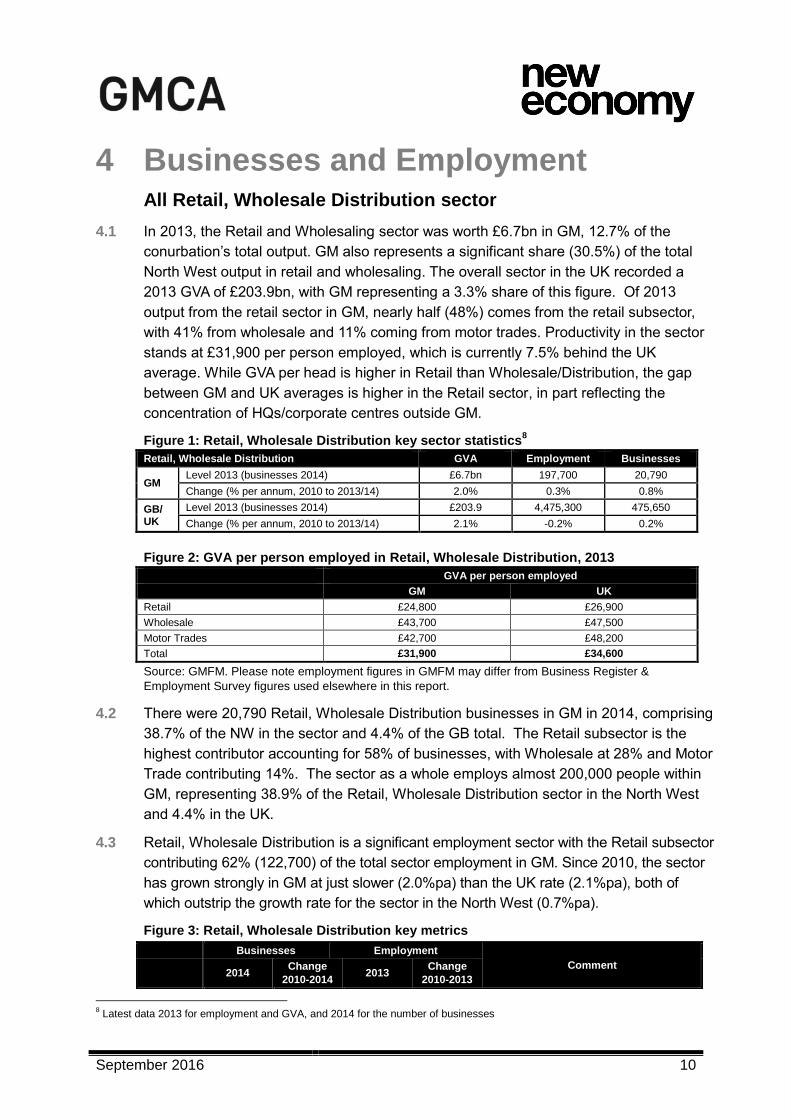

4 Businesses and Employment All Retail, Wholesale Distribution sector

4.1 In 2013, the Retail and Wholesaling sector was worth £6.7bn in GM, 12.7% of the

conurbation’s total output. GM also represents a significant share (30.5%) of the total

North West output in retail and wholesaling. The overall sector in the UK recorded a

2013 GVA of £203.9bn, with GM representing a 3.3% share of this figure. Of 2013

output from the retail sector in GM, nearly half (48%) comes from the retail subsector,

with 41% from wholesale and 11% coming from motor trades. Productivity in the sector

stands at £31,900 per person employed, which is currently 7.5% behind the UK

average. While GVA per head is higher in Retail than Wholesale/Distribution, the gap

between GM and UK averages is higher in the Retail sector, in part reflecting the

concentration of HQs/corporate centres outside GM.

Figure 1: Retail, Wholesale Distribution key sector statistics8

Retail, Wholesale Distribution GVA Employment Businesses

GM Level 2013 (businesses 2014) £6.7bn 197,700 20,790

Change (% per annum, 2010 to 2013/14) 2.0% 0.3% 0.8%

GB/ UK

Level 2013 (businesses 2014) £203.9 4,475,300 475,650

Change (% per annum, 2010 to 2013/14) 2.1% -0.2% 0.2%

Figure 2: GVA per person employed in Retail, Wholesale Distribution, 2013

GVA per person employed

GM UK

Retail £24,800 £26,900

Wholesale £43,700 £47,500

Motor Trades £42,700 £48,200

Total £31,900 £34,600

Source: GMFM. Please note employment figures in GMFM may differ from Business Register &

Employment Survey figures used elsewhere in this report.

4.2 There were 20,790 Retail, Wholesale Distribution businesses in GM in 2014, comprising

38.7% of the NW in the sector and 4.4% of the GB total. The Retail subsector is the

highest contributor accounting for 58% of businesses, with Wholesale at 28% and Motor

Trade contributing 14%. The sector as a whole employs almost 200,000 people within

GM, representing 38.9% of the Retail, Wholesale Distribution sector in the North West

and 4.4% in the UK.

4.3 Retail, Wholesale Distribution is a significant employment sector with the Retail subsector

contributing 62% (122,700) of the total sector employment in GM. Since 2010, the sector

has grown strongly in GM at just slower (2.0%pa) than the UK rate (2.1%pa), both of

which outstrip the growth rate for the sector in the North West (0.7%pa).

Figure 3: Retail, Wholesale Distribution key metrics

8 Latest data 2013 for employment and GVA, and 2014 for the number of businesses

Businesses Employment

Comment 2014

Change

2010-2014 2013

Change

2010-2013

September 2016 11

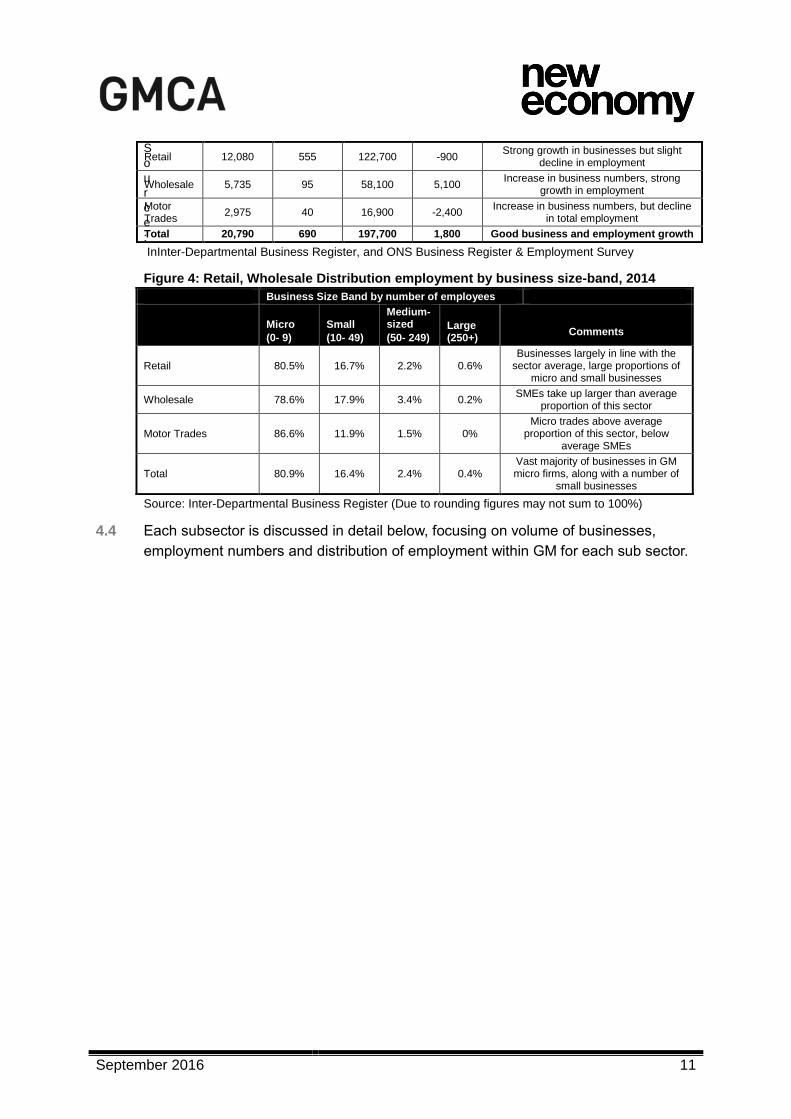

S

o

u

r

c

e

:

InInter-Departmental Business Register, and ONS Business Register & Employment Survey

Figure 4: Retail, Wholesale Distribution employment by business size-band, 2014

Business Size Band by number of employees

Micro

(0- 9)

Small

(10- 49)

Medium- sized

(50- 249) Large (250+)

Comments

Retail 80.5% 16.7% 2.2% 0.6% Businesses largely in line with the

sector average, large proportions of micro and small businesses

Wholesale 78.6% 17.9% 3.4% 0.2% SMEs take up larger than average

proportion of this sector

Motor Trades 86.6% 11.9% 1.5% 0% Micro trades above average

proportion of this sector, below average SMEs

Total 80.9% 16.4% 2.4% 0.4% Vast majority of businesses in GM micro firms, along with a number of

small businesses

Source: Inter-Departmental Business Register (Due to rounding figures may not sum to 100%)

4.4 Each subsector is discussed in detail below, focusing on volume of businesses,

employment numbers and distribution of employment within GM for each sub sector.

Retail 12,080 555 122,700 -900 Strong growth in businesses but slight

decline in employment

Wholesale 5,735 95 58,100 5,100 Increase in business numbers, strong

growth in employment

Motor Trades

2,975 40 16,900 -2,400 Increase in business numbers, but decline

in total employment

Total 20,790 690 197,700 1,800 Good business and employment growth

September 2016 12

Figure 5: Retail, Wholesale Distribution businesses in Greater Manchester, 2014

Figure 5 shows all Retail, Wholesale Distribution businesses in GM. This shows clusters of employment in the regional centre, Ashton-Under-Lyne, Rochdale, Bolton, Bury and Stockport town centres, and to a lesser extent in Oldham and Wigan town centres.

This map also highlights the importance of out-of-town shopping locations, including:

Middlebrook Retail Park (Bolton); West One Retail Park (Eccles); Woodfields Retail Park (Bury); The Trafford Centre; Broadheath Retail Park (Altrincham).

In the regional centre, the Lowry Outlet and Salford Quays and Manchester Fort near Collyhurst also provide alternatives to city centre shopping.

As well as this, there are smaller locations, for example - Ramsbottom and Bramhall which have a high concentration of individual retail businesses, outside of the larger town centres.

Source: Inter-Departmental Business Register:

September 2016 13

Figure 6: Retail, Wholesale Distribution employment in Greater Manchester, 2013

Figure 6 shows the employment in all of the Retail, Wholesale Distribution sector. Clusters of employment are found in Manchester City Centre and the Trafford Park area, as well as Stockport, Bolton and Bury town centres and Middlebrook Retail Park (Bolton).

Source: ONS Business Register & Employment Survey

September 2016 14

Retail

4.5 In 2014 there were 12,080 businesses in GM’s Retail subsector, more than half (58%) of

all businesses in the sector. Between 2010 and 2014, the Retail subsector saw stronger

business growth in GM (4.8%) than Great Britain as a whole (0.5%). This is particularly

impressive in the context of a struggling subsector in the North West, where the Retail

business base shrank by 0.2% from 2010 to 2014. London continues to have strong

performance in this sector, growing by more than double the GM rate (9.7%).

4.6 Employment in the Retail sector contracted by 0.6% (18,000 fewer jobs) nationally

between 2010 and 2013, yet the sector still employed 2,838,700 people in 2013. The fall

across the country was reflected by a fall in the North West of 3.4% (11,200 fewer jobs)

and in GM of 0.7% (900 fewer jobs). In contrast, London created 25,700 new jobs in the

sector at a growth rate of 6.8%, taking employment in the sector above 400,000.

4.7 The location quotient (LQ) – a measure of employment concentration within the local

economy compared with the national average – suggests that GM’s Retail sector is in

line with the GB average.

Figure 7: Location quotient of Retail

SIC Description LQ Employment

47 Retail trade, except of motor vehicles and motorcycles

1.01 122,700

Source: ONS Business Register & Employment Survey

September 2016 15

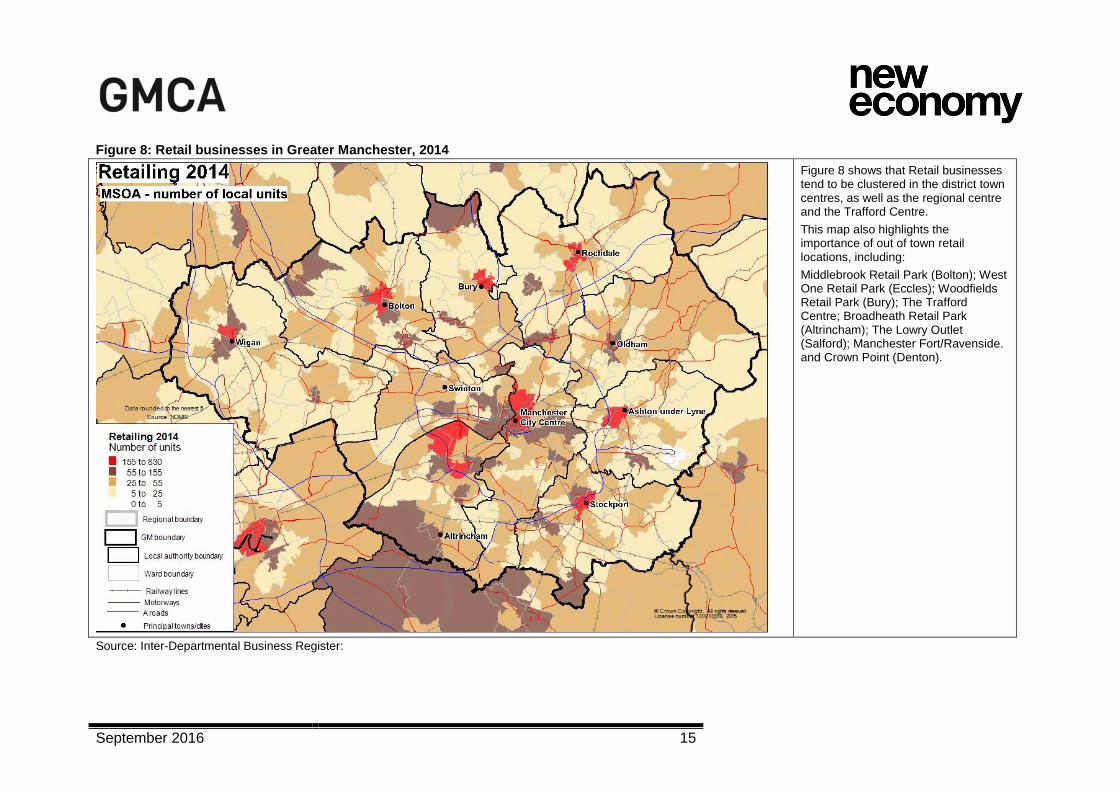

Figure 8: Retail businesses in Greater Manchester, 2014

Figure 8 shows that Retail businesses tend to be clustered in the district town centres, as well as the regional centre and the Trafford Centre.

This map also highlights the importance of out of town retail locations, including:

Middlebrook Retail Park (Bolton); West One Retail Park (Eccles); Woodfields Retail Park (Bury); The Trafford Centre; Broadheath Retail Park (Altrincham); The Lowry Outlet (Salford); Manchester Fort/Ravenside. and Crown Point (Denton).

Source: Inter-Departmental Business Register:

September 2016 16

Figure 9: Retail employment in Greater Manchester, 2013

Figure 9 shows that retail employment is concentrated mainly in the regional centre and around the Trafford centre, with some strong concentrations in other town centres such as Stockport.

When comparing the employment and businesses maps, it is clear that smaller towns and localities such as Bramhall and Ramsbottom host a number of small retailers which don’t employ large numbers of people.

Source: ONS Business Register & Employment Survey

September 2016 17

4.8 Figure 10 shows the main findings of a hierarchy analysis by retail and venue

consultants Javelin, covering town centre and out-of-town locations in 2014. It is based

on the number of major retail multiples and does not reflect the potentially more diverse

offer (other than retail) in centres. However, it can be used to summarise retail assets in

GM, as follows:

Manchester and the Trafford Centre rank the highest classed as a Major City and a Major

Regional centre respectively. Five of GM’s eight principal town centres are classed as

Regional (Bolton, Bury, Oldham, Stockport and Wigan).

Three centres are classed as Sub-regional (Altrincham, Ashton-under-Lyne and

Rochdale). Salford’s main centre –Salford Shopping City – is classified as a Major District

Centre alongside the Lowry Outlet, as is Leigh Town Centre.

4.9 Retail business growth appears to be largely driven by specific retail developments.

Trafford, home to the Trafford Centre, saw a net business increase of 250 (20.0%

growth). In Salford, home to MediaCityUK, this figure was 75 (9.0% growth). Bury, which

opened £350m shopping centre ‘The Rock’ in 2010, saw a net increase of 65

businesses. In Manchester this number also rose by 375 (16.8% growth). Manchester is

home to more than a fifth of Retail subsector businesses (21.6%). In other districts,

such as Tameside, the number of Retail businesses shrank or remained the same. Net

decrease was highest in Bolton which lost 75 businesses, and Stockport which had 65

fewer in 2014 than in 2010.

September 2016 18

Figure 10: Javelin retail / venue ranking, 2014 (*see footnote 9)

Source: Javelin Retail Location Grades 2014

9 Stretford should be listed as being in Trafford and not Manchester as shown in Figure 10, table produced by Javelin

September 2016 19

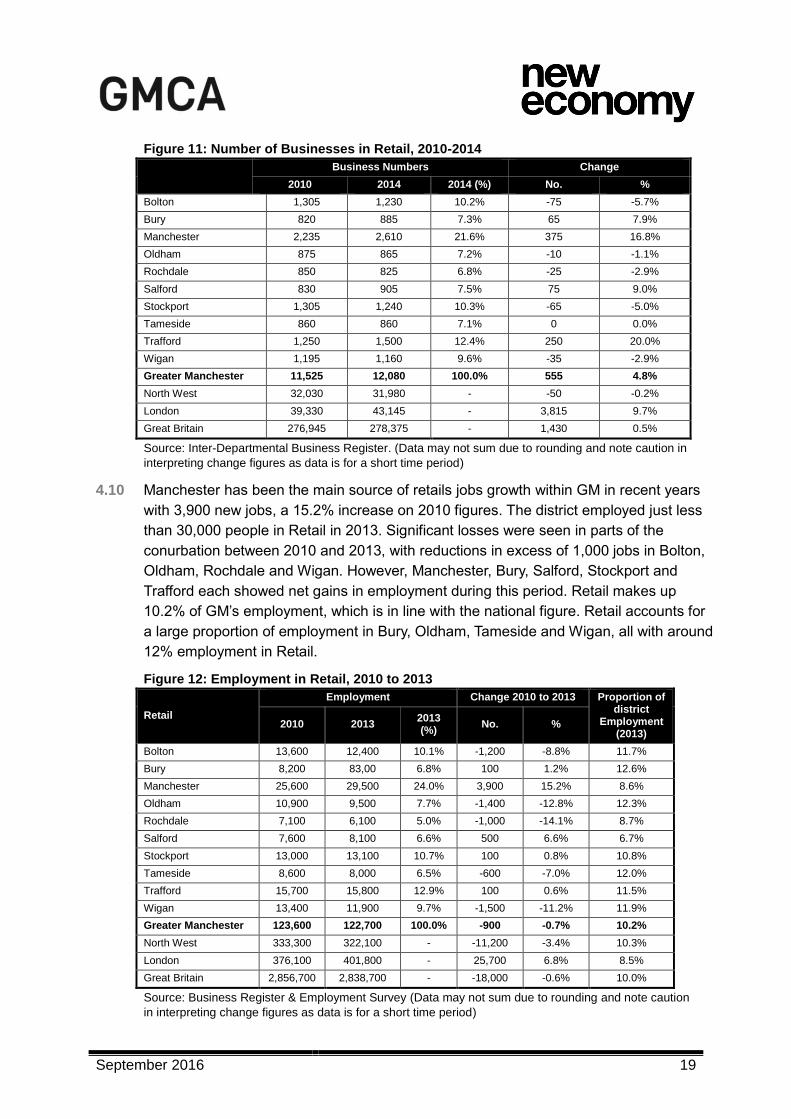

Figure 11: Number of Businesses in Retail, 2010-2014

Business Numbers Change

2010 2014 2014 (%) No. %

Bolton 1,305 1,230 10.2% -75 -5.7%

Bury 820 885 7.3% 65 7.9%

Manchester 2,235 2,610 21.6% 375 16.8%

Oldham 875 865 7.2% -10 -1.1%

Rochdale 850 825 6.8% -25 -2.9%

Salford 830 905 7.5% 75 9.0%

Stockport 1,305 1,240 10.3% -65 -5.0%

Tameside 860 860 7.1% 0 0.0%

Trafford 1,250 1,500 12.4% 250 20.0%

Wigan 1,195 1,160 9.6% -35 -2.9%

Greater Manchester 11,525 12,080 100.0% 555 4.8%

North West 32,030 31,980 - -50 -0.2%

London 39,330 43,145 - 3,815 9.7%

Great Britain 276,945 278,375 - 1,430 0.5%

Source: Inter-Departmental Business Register. (Data may not sum due to rounding and note caution in

interpreting change figures as data is for a short time period)

4.10 Manchester has been the main source of retails jobs growth within GM in recent years

with 3,900 new jobs, a 15.2% increase on 2010 figures. The district employed just less

than 30,000 people in Retail in 2013. Significant losses were seen in parts of the

conurbation between 2010 and 2013, with reductions in excess of 1,000 jobs in Bolton,

Oldham, Rochdale and Wigan. However, Manchester, Bury, Salford, Stockport and

Trafford each showed net gains in employment during this period. Retail makes up

10.2% of GM’s employment, which is in line with the national figure. Retail accounts for

a large proportion of employment in Bury, Oldham, Tameside and Wigan, all with around

12% employment in Retail.

Figure 12: Employment in Retail, 2010 to 2013

Retail

Employment Change 2010 to 2013 Proportion of district

Employment (2013)

2010 2013 2013 (%)

No. %

Bolton 13,600 12,400 10.1% -1,200 -8.8% 11.7%

Bury 8,200 83,00 6.8% 100 1.2% 12.6%

Manchester 25,600 29,500 24.0% 3,900 15.2% 8.6%

Oldham 10,900 9,500 7.7% -1,400 -12.8% 12.3%

Rochdale 7,100 6,100 5.0% -1,000 -14.1% 8.7%

Salford 7,600 8,100 6.6% 500 6.6% 6.7%

Stockport 13,000 13,100 10.7% 100 0.8% 10.8%

Tameside 8,600 8,000 6.5% -600 -7.0% 12.0%

Trafford 15,700 15,800 12.9% 100 0.6% 11.5%

Wigan 13,400 11,900 9.7% -1,500 -11.2% 11.9%

Greater Manchester 123,600 122,700 100.0% -900 -0.7% 10.2%

North West 333,300 322,100 - -11,200 -3.4% 10.3%

London 376,100 401,800 - 25,700 6.8% 8.5%

Great Britain 2,856,700 2,838,700 - -18,000 -0.6% 10.0%

Source: Business Register & Employment Survey (Data may not sum due to rounding and note caution

in interpreting change figures as data is for a short time period)

September 2016 20

Wholesale

4.11 GM is home to nearly 6,000 Wholesale businesses (5,735), with more than a fifth of

these in Manchester (22.8%).

4.12 Despite the number of Wholesale businesses nationally falling by 0.2% in the four years

between 2010 and 2014, GM’s business base grew by 1.7% over the same period. This

is stronger growth than seen in the North West, which remained stagnant (0.0%), but is

weaker than London, where the business base grew by 4.3%. While Wholesale

employment fell nationally between 2010 2013 by 0.8%, GM saw growth in this

subsector of 9.6%, though this ranks below the North West (11.7%) and London

(20.2%).

4.13 The location quotient suggests the GM Wholesale subsector has a higher concentration

in GM compared to nationally.

Figure 13: Location quotient of Wholesale

SIC Description LQ Employment

46 Wholesale trade, except of motor vehicles and motorcycles 1.21 58,100

Source: ONS Business Register & Employment Survey

4.14 Figure 15 shows there are clusters of Wholesale employment throughout GM, in

particular within Trafford Park, Altrincham, Stockport, Ashton-under-Lyne, and near to

Bolton and Bury town centres.

September 2016 21

Figure 14: Wholesale businesses in Greater Manchester, 2014

Figure 14 shows that Wholesale businesses are distributed across GM. There are particular concentrations of businesses in the regional centre, Trafford Park, Altrincham, and in Stockport, Ashton-under-Lyne, Bolton and Bury town centres.

Other town centres such as Rochdale, Oldham and Wigan have slightly less strong clusters of businesses. There are also clusters around areas with good rail and road transport links, such as the Ardwick area of East Manchester, Farnworth and Horwich in Bolton, and the Heywood Distribution Park and Pilsworth Industrial Estate in Rochdale and Bury.

Source: Inter-Departmental Business Register:

September 2016 22

Figure 15: Wholesale employment in Greater Manchester, 2013

Figure 15 displays the Wholesale employment levels in 2013 across GM. This shows heavily concentrated employment in the outskirts of Manchester city centre, Salford and the Trafford Park area, as well as Bredbury near Stockport.

Relatively large pockets of employment within the Wholesale subsector are visible For example Horwich in Bolton. Altrincham and the majority of the rural areas in both north and south GM show very low levels of employment within the Wholesale industry.

In relation to the business map, it is clear that Wholesale businesses in the far North and South of the conurbations are not large employers, but rather SMEs employing few people.

Source: ONS Business Register & Employment Survey

September 2016 23

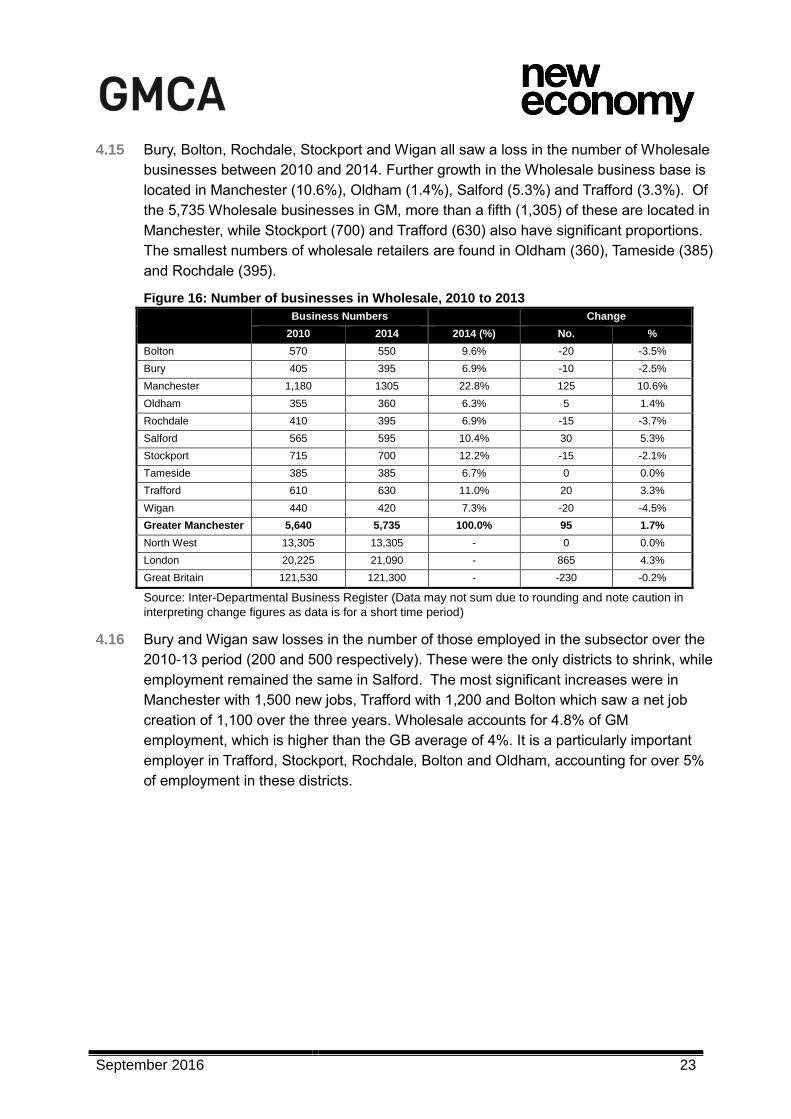

4.15 Bury, Bolton, Rochdale, Stockport and Wigan all saw a loss in the number of Wholesale

businesses between 2010 and 2014. Further growth in the Wholesale business base is

located in Manchester (10.6%), Oldham (1.4%), Salford (5.3%) and Trafford (3.3%). Of

the 5,735 Wholesale businesses in GM, more than a fifth (1,305) of these are located in

Manchester, while Stockport (700) and Trafford (630) also have significant proportions.

The smallest numbers of wholesale retailers are found in Oldham (360), Tameside (385)

and Rochdale (395).

Figure 16: Number of businesses in Wholesale, 2010 to 2013

Business Numbers Change

2010 2014 2014 (%) No. %

Bolton 570 550 9.6% -20 -3.5%

Bury 405 395 6.9% -10 -2.5%

Manchester 1,180 1305 22.8% 125 10.6%

Oldham 355 360 6.3% 5 1.4%

Rochdale 410 395 6.9% -15 -3.7%

Salford 565 595 10.4% 30 5.3%

Stockport 715 700 12.2% -15 -2.1%

Tameside 385 385 6.7% 0 0.0%

Trafford 610 630 11.0% 20 3.3%

Wigan 440 420 7.3% -20 -4.5%

Greater Manchester 5,640 5,735 100.0% 95 1.7%

North West 13,305 13,305 - 0 0.0%

London 20,225 21,090 - 865 4.3%

Great Britain 121,530 121,300 - -230 -0.2%

Source: Inter-Departmental Business Register (Data may not sum due to rounding and note caution in

interpreting change figures as data is for a short time period)

4.16 Bury and Wigan saw losses in the number of those employed in the subsector over the

2010-13 period (200 and 500 respectively). These were the only districts to shrink, while

employment remained the same in Salford. The most significant increases were in

Manchester with 1,500 new jobs, Trafford with 1,200 and Bolton which saw a net job

creation of 1,100 over the three years. Wholesale accounts for 4.8% of GM

employment, which is higher than the GB average of 4%. It is a particularly important

employer in Trafford, Stockport, Rochdale, Bolton and Oldham, accounting for over 5%

of employment in these districts.

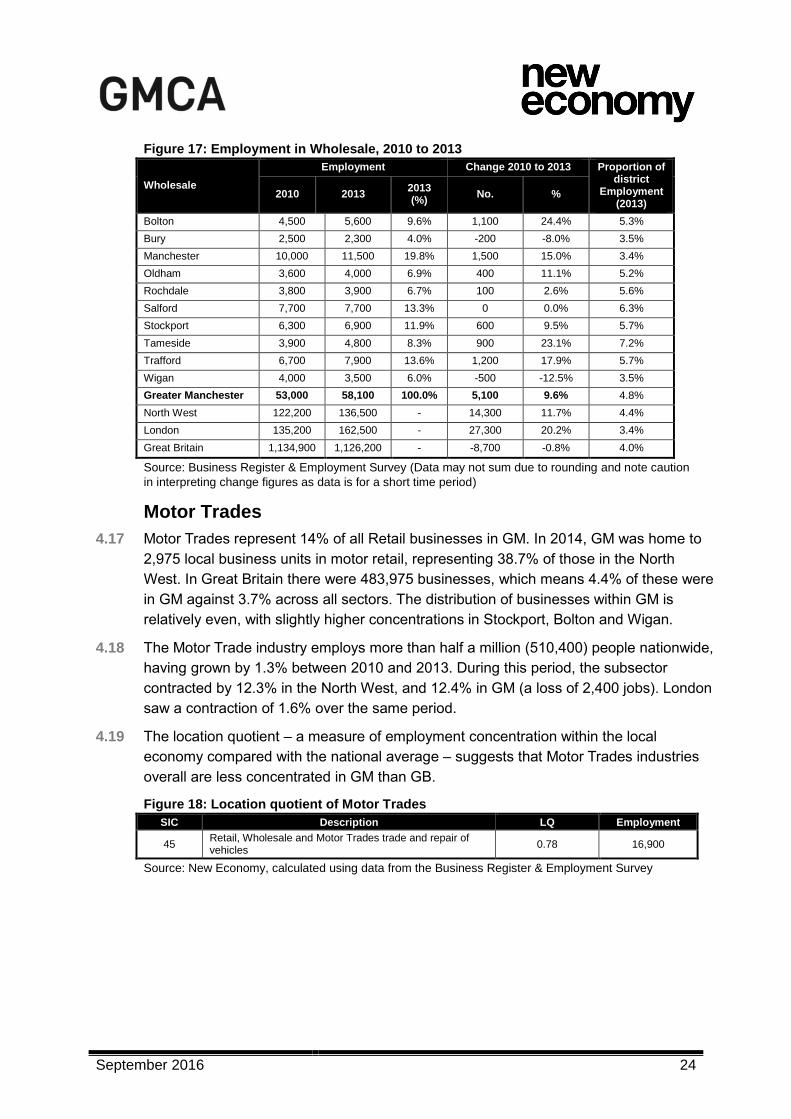

September 2016 24

Figure 17: Employment in Wholesale, 2010 to 2013

Wholesale

Employment Change 2010 to 2013 Proportion of district

Employment (2013)

2010 2013 2013 (%)

No. %

Bolton 4,500 5,600 9.6% 1,100 24.4% 5.3%

Bury 2,500 2,300 4.0% -200 -8.0% 3.5%

Manchester 10,000 11,500 19.8% 1,500 15.0% 3.4%

Oldham 3,600 4,000 6.9% 400 11.1% 5.2%

Rochdale 3,800 3,900 6.7% 100 2.6% 5.6%

Salford 7,700 7,700 13.3% 0 0.0% 6.3%

Stockport 6,300 6,900 11.9% 600 9.5% 5.7%

Tameside 3,900 4,800 8.3% 900 23.1% 7.2%

Trafford 6,700 7,900 13.6% 1,200 17.9% 5.7%

Wigan 4,000 3,500 6.0% -500 -12.5% 3.5%

Greater Manchester 53,000 58,100 100.0% 5,100 9.6% 4.8%

North West 122,200 136,500 - 14,300 11.7% 4.4%

London 135,200 162,500 - 27,300 20.2% 3.4%

Great Britain 1,134,900 1,126,200 - -8,700 -0.8% 4.0%

Source: Business Register & Employment Survey (Data may not sum due to rounding and note caution

in interpreting change figures as data is for a short time period)

Motor Trades

4.17 Motor Trades represent 14% of all Retail businesses in GM. In 2014, GM was home to

2,975 local business units in motor retail, representing 38.7% of those in the North

West. In Great Britain there were 483,975 businesses, which means 4.4% of these were

in GM against 3.7% across all sectors. The distribution of businesses within GM is

relatively even, with slightly higher concentrations in Stockport, Bolton and Wigan.

4.18 The Motor Trade industry employs more than half a million (510,400) people nationwide,

having grown by 1.3% between 2010 and 2013. During this period, the subsector

contracted by 12.3% in the North West, and 12.4% in GM (a loss of 2,400 jobs). London

saw a contraction of 1.6% over the same period.

4.19 The location quotient – a measure of employment concentration within the local

economy compared with the national average – suggests that Motor Trades industries

overall are less concentrated in GM than GB.

Figure 18: Location quotient of Motor Trades

SIC Description LQ Employment

45 Retail, Wholesale and Motor Trades trade and repair of vehicles

0.78 16,900

Source: New Economy, calculated using data from the Business Register & Employment Survey

September 2016 25

Figure 19: Motor Trade businesses in Greater Manchester, 2014

Figure 19 shows Motor Trades businesses are focused in the district town centres, as well as around the Trafford Park and Wharfside areas. There are also smaller concentrations of businesses in several out-of-town sites, such as around Atherton in Wigan, Bredbury in Stockport and around the Pilsworth and Blackrod Bridge area in Bury.

Source: Inter-Departmental Business Register:

September 2016 26

Figure 20: Motor Trade employment in Greater Manchester, 2013

Figure 20 details the employment in the Motor Trades industry. A high concentration is visible around the Trafford Park area, with the outer city centre limits of Salford and Manchester also showing a high concentration.

Wigan and Bolton have notable pockets of employment in this sector in and around the town centres.

Areas in the south of Manchester have a less concentrated workforce within the Motor Trades industry, with Altrincham and Stockport showing lower pockets of employment.

Comparison of the business and employment maps again suggests that a lot of businesses are SMEs, as employment is generally not concentrated in the same areas as businesses.

Source: ONS Business Register & Employment Survey

September 2016 27

4.20 In terms of growth, GM saw a net increase of 40 businesses in the subsector between

2010 and 2014, representing 1.4% growth. GM therefore grew faster than the North

West (1.0%), but slower than London (11.6%) and Great Britain as a whole (3%).

4.21 The number of businesses over this period increased in all districts in GM, with the

exceptions of Trafford, Rochdale and Stockport, which each saw net decrease of 20

businesses or fewer. Tameside saw no change in the number of businesses. Elsewhere,

the strongest growth in business numbers was seen in Bolton, Manchester and Oldham,

and Bury.

Figure 21: Number of businesses in Motor Trades, 2010 to 2014

Business Numbers Change

2010 2014 2014 (%) No. %

Bolton 350 365 12.3% 15 4.3%

Bury 235 255 8.6% 20 8.5%

Manchester 300 315 10.6% 15 5.0%

Oldham 260 275 9.2% 15 5.8%

Rochdale 255 240 8.1% -15 -5.9%

Salford 225 235 7.9% 10 4.4%

Stockport 400 390 13.1% -10 -2.5%

Tameside 245 245 8.2% 0 0.0%

Trafford 280 260 8.7% -20 -7.1%

Wigan 380 390 13.1% 10 2.6%

Greater Manchester 2,935 2,975 100.0% 40 1.4%

North West 8,380 8,460 - 80 1.0%

London 5,785 6,455 - 670 11.6%

Great Britain 73,780 75,975 - 2,195 3.0%

Source: Inter-Departmental Business Register (Data may not sum due to rounding and note caution in

interpreting change figures as data is for a short time period)

4.22 In employment within GM, contractions were seen in all districts except Salford, which

grew by 17.6% (an increase of 300 jobs). Elsewhere, the most significant losses of

employment in terms of numbers were seen in Bolton, Rochdale and Wigan, which each

saw a net loss of 500 jobs respectively. Manchester and Trafford were the joint second

best performing districts over the three years, each losing only 100 employees. Motor

Trades account for 1.4% of GM employment, as opposed to 1.8% of national

employment. In Bolton, Motor Trades accounts for 2% of employment, and 1.9% in

Oldham.

September 2016 28

Figure 22: Employment in Motor Trades, 2013

Motor Trades

Employment Change 2010 to 2013 Proportion of district

Employment (2013)

2010 2013 2013 (%)

No. %

Bolton 2,600 2,100 12.4% -500 -19.2% 2.0%

Bury 1,500 1,200 7.1% -300 -20.0% 1.8%

Manchester 1,700 1,600 9.5% -100 -5.9% 0.5%

Oldham 1,700 1,500 8.9% -200 -11.8% 1.9%

Rochdale 1,700 1,200 7.1% -500 -29.4% 1.7%

Salford 1,700 2,000 11.8% 300 17.6% 1.6%

Stockport 2,400 2,100 12.4% -300 -12.5% 1.7%

Tameside 1,400 1,100 6.5% -300 -21.4% 1.6%

Trafford 2,600 2,500 14.8% -100 -3.8% 1.8%

Wigan 2,100 1,600 9.5% -500 -23.8% 1.6%

Greater Manchester 19,300 16,900 100.0% -2,400 -12.4% 1.4%

North West 57,600 50,500 - -7,100 -12.3% 1.6%

London 37,000 36,400 - -600 -1.6% 0.8%

Great Britain 504,000 510,400 - 6,400 1.3% 1.8%

Source: Business Register & Employment Survey (Data may not sum due to rounding and note caution

in interpreting change figures as data is for a short time period)

September 2016 29

5 Skills 5.1 Despite an improvement in productivity per worker in GM in the sector over the last

decade (from £28,000 in 2003 to £31,900 in 2013), there is still a gap in levels between

GM and the UK average. GM has several retail HQs and regional offices, however the

majority of HQs are located elsewhere in the UK (principally London) and this will, in

part, reflect the productivity differences highlighted in this report. Skills will play a part in

raising performance, however the sector faces several challenges, which are set out in

the following section.

5.2 The analysis below shows the current qualification profile of the resident Retail and

Wholesale workforce based on survey data for the North West of England and UK.

Survey data on specific sectors, jobs and qualifications is not accurate for smaller areas.

The following section then provides skills forecasts produced by Oxford Economics and

indicates the qualification levels the sector will need over the next 20 years.

Current trends

Figure 23: Highest qualification held by people working in Retail and Wholesale, 2015

Level of highest qualification held

NW UK

Level 4+ 22.6% 22.8%

Level 3 19.7% 19.8%

Trade Apprenticeships 5.5% 4.6%

Level 2 21.9% 19.3%

Below Level 2 14.3% 16.2%

Other Qualifications 7.7% 7.7%

No Qualifications 8.4% 9.6%

Source: Quarterly Labour Force Survey, January-March 2015. (Data may not sum due to rounding)

5.3 Figure 23 shows that broadly, the qualification profile in the North West is similar to that

of the UK as a whole. Those qualified to Level 4 and above in the North West

(undergraduate/graduate level) account for just over a fifth (22.6%) of resident

employees, compared to 22.8% on average in the UK. The percentage point gap is

small, but given the sizer of the sector, this still equates to 1,000 additional graduate

level jobs in the region, and potentially around 300 to 400 in GM.

5.4 New Economy has undertaken analysis of the supply and demand relationship for retail

related apprenticeships and there is a mixed picture in terms of supply of retail

apprenticeships. Actual retail apprenticeships are very low (155 at advanced level).

Apprenticeships in areas such as hairdressing and barbering (which indeed have a

higher technical knowledge component) are more numerous at advanced level and

these are included as ‘personal services’ within retail and wholesale. There is a debate

as to the extent to which apprenticeships, dedicated to refining technical knowledge, are

relevant to service sectors in which detailed technical know-how is more limited (such

as retail). Demand is evident from the retail sector and is articulated in this report,

September 2016 30

however it must be noted that many of these jobs are likely to be at lower (Level 2)

skills.

Future trends

5.5 Skills forecasts from Oxford Economics have identified expansion demand (in terms of

new jobs which will be created over the next two decades) and replacement demand

(workforce churn).

5.6 Under the central Accelerated Growth Scenario, the number of new jobs that will be

created in GM in the sector is estimated at 23,400 over the next two decades.10 There

will also be significant demand to replace the existing workforce leaving the sector due

to retirements. Replacement demand forecasts suggest this equates to 27,000 jobs per

annum up to 2035.11

5.7 Oxford Economics have modelled the breakdown of this skills demand and suggest that

by 2035, almost a quarter of workers in the sector are forecast to be qualified at Level 4

and above, and the same proportion at Level 3, indicating an increasing need for highly

skilled workers. However, the sector is forecast to continue to support jobs at all

qualification levels, with 20% of workers forecast to be qualified to Level 2 and 11% with

no qualifications.

Figure 24: Qualification breakdown in the Retail and Wholesale Distribution sector, 2035

Qualification level Proportion of sector

NVQ 4+ 24%

NVQ 3 24%

NVQ 2 20%

NVQ 1 14%

Other 7%

No Qualifications 11%

Source: Oxford Economics (Data may not sum due to rounding)

Skills Challenges

Figure 25: Skills Challenges in the Retail, Wholesale Distribution Sector

Challenge Explanation

Skills shortages Above average number of hard to fill vacancies in the sector

Some applicants lacking technical, sales and entrepreneurial skills

Workforce development and skills gaps

Difficulties for some sole traders and SMEs to access the right training to address workforce skills gaps

Future skills As the sector is changing, retail roles are likely to require more IT and management skills

10

Growth forecast is based on the Greater Manchester Forecasting Model, detailed later in this report 11

See Future Growth section for detailed description of Greater Manchester growth scenarios

September 2016 31

5.8 Skills Shortages: Research covering the UK highlights that the Retail sector has an

above average number of hard-to-fill vacancies, compared with other sectors. Just

under a fifth (17%) of vacancies are considered hard-to-fill because of skill shortages

among applicants.12 The main skills challenges are finding experienced customer

service skills.13 Other challenges include problem handling and customer

management, entrepreneurial skills, commercial acumen/awareness and leadership

skills/vision.

5.9 Workforce development and skills gaps: Retailers, in particular larger firms, are one

of the main of sectors to take up apprenticeships.14 Small and micro-size firms in the

sector are however, much less likely to participate in formal training. Key barriers

include the time and resource to manage trainees, and awareness of what training

programmes include. Employers have also stated that apprenticeships do not fully

provide the skills and training which their new recruits need. In a survey by People 1st,

a third of employers stated that although their staff received training, their performance

had not improved sufficiently. A quarter said that they felt training had not fully

addressed their skills gaps.15

5.10 Future skills: Technological progress, as with all other sectors, is driving significant

change in the skills required by the workforce in both Wholesale and Retail. Many of

these changes are seen in the way retailers manage their supply chains, in a move to

have more product, a quicker turnaround from manufacture to shop and increasingly

internet-based sales. IT skills are a critical and growing part of the industry, alongside

more ‘traditional skills’, for example customer service, product design and

commissioning, buying, merchandising, and marketing and promotion.16

12

UKCES (2012): Employer Skills Survey 2011 13

Skillsmart (2012): Retail UK Sector Skills Assessment 14

Department for Business, Innovation & Skills (2013): A Strategy for Future Retail 15

People 1st (2014): Retail Labour Market Review, Current State of Skills in the Retail Sector

16 Department for Business, Innovation & Skills, October 2013, A Strategy for Future Retail.

September 2016 32

6 Key Assets 6.1 The following section highlights relevant assets for the Retail, Wholesale Distribution

sector. Sector assets have been identified based on their role in supporting jobs and/or

GVA growth for GM now and in the future. Travel to work area maps have been drawn

for two key assets identified by Javelin, Manchester City Centre and the Trafford Centre,

to provide further understanding of their reach. Key assets include:

6.2 Manchester city centre: Javelin Group research ranks the city centre as providing the

third most complete retail offer in the UK behind London West End and Glasgow.17

Having received significant investment in recent years, the retail core is located around

Market Street, King Street, the Arndale Centre, St Ann’s Square, and Exchange Square,

with 2 to 3 million square feet of retail floor space.

6.3 The Trafford Centre: Owned by Intu Properties, The Trafford Centre is a 2 million

square feet retail and leisure space. Situated with easy access from the M60, the centre

attracts 31m customers a year;18 and ranks in the Top 20 Premium Store Rankings

across the UK.19

6.4 Regional, local and district shopping centres: The eight principal town centres are

Bolton, Bury, Rochdale, Oldham, Stockport, Altrincham, Ashton-Under-Lyne and Wigan.

In addition, there are smaller centres such as Farnworth in Bolton, Prestwich in Bury,

Cheadle in Stockport and Sale in Trafford (see figure 10 for full list). Out-of-town

shopping locations include Middlebrook Retail Park (Bolton), West One Retail Park

(Eccles), Woodfields Retail Park (Bury), and Broadheath Retail Park (Altrincham).

17

Javelin Group (2015): Annual Venuescore report, 2014 to 2015 – Top Shopping Venues 18

Intugroup: https://www.intugroup.co.uk/where-we-do-it/our-uk-centres/intu-trafford-centre/key-facts/ 19

Call Credit (2014): Premium Store Rankings

September 2016 33

Figure 26: Retail assets in Greater Manchester

Analysis of Javelin Group’s Venuescore data, which ranks over 20,000 retail locations or ‘venues’ in the UK, shows a clear hierarchy of retail assets in GM. This is led by Manchester city centre and, to a lesser extent, the Trafford Centre.

Behind these nationally and regionally significant assets are the conurbation’s remaining eight principal town centres, including sub-regional town centres like Altrincham, Ashton-under-Lyne and Rochdale, and districts such as Salford Shopping City (major district), Eccles and Swinton.

Source: New Economy

September 2016 34

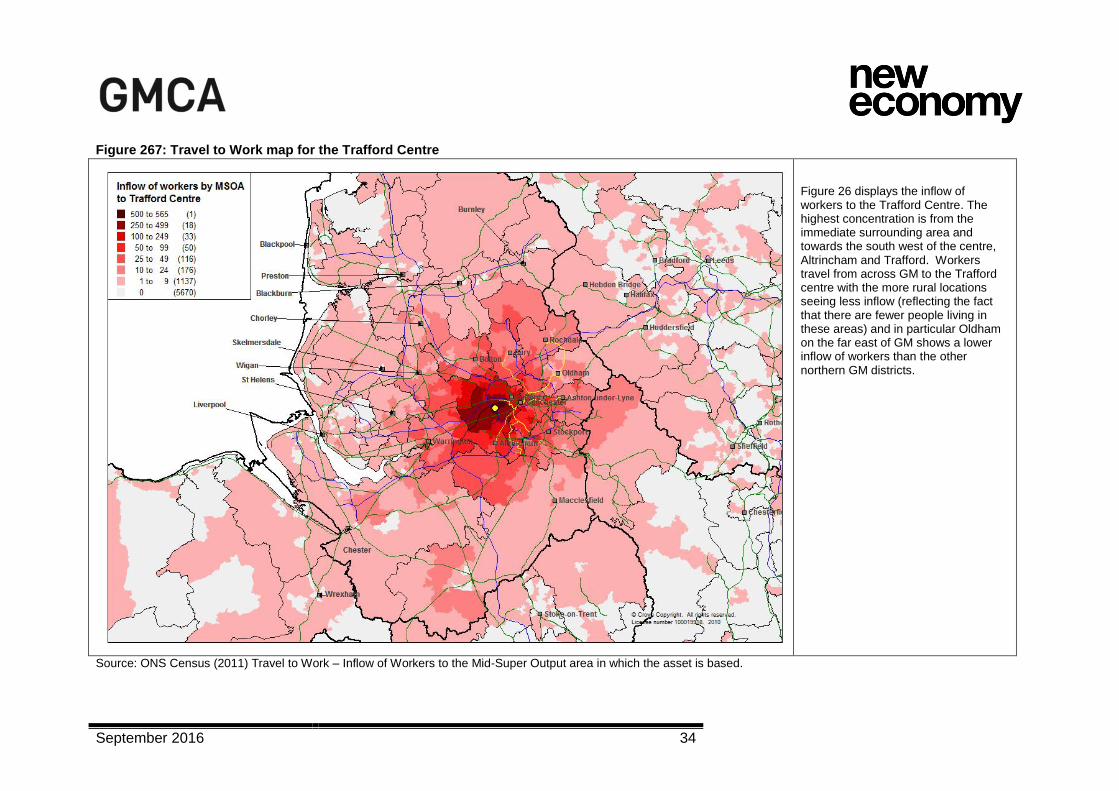

Figure 267: Travel to Work map for the Trafford Centre

Figure 26 displays the inflow of workers to the Trafford Centre. The highest concentration is from the immediate surrounding area and towards the south west of the centre, Altrincham and Trafford. Workers travel from across GM to the Trafford centre with the more rural locations seeing less inflow (reflecting the fact that there are fewer people living in these areas) and in particular Oldham on the far east of GM shows a lower inflow of workers than the other northern GM districts.

Source: ONS Census (2011) Travel to Work – Inflow of Workers to the Mid-Super Output area in which the asset is based.

September 2016 35

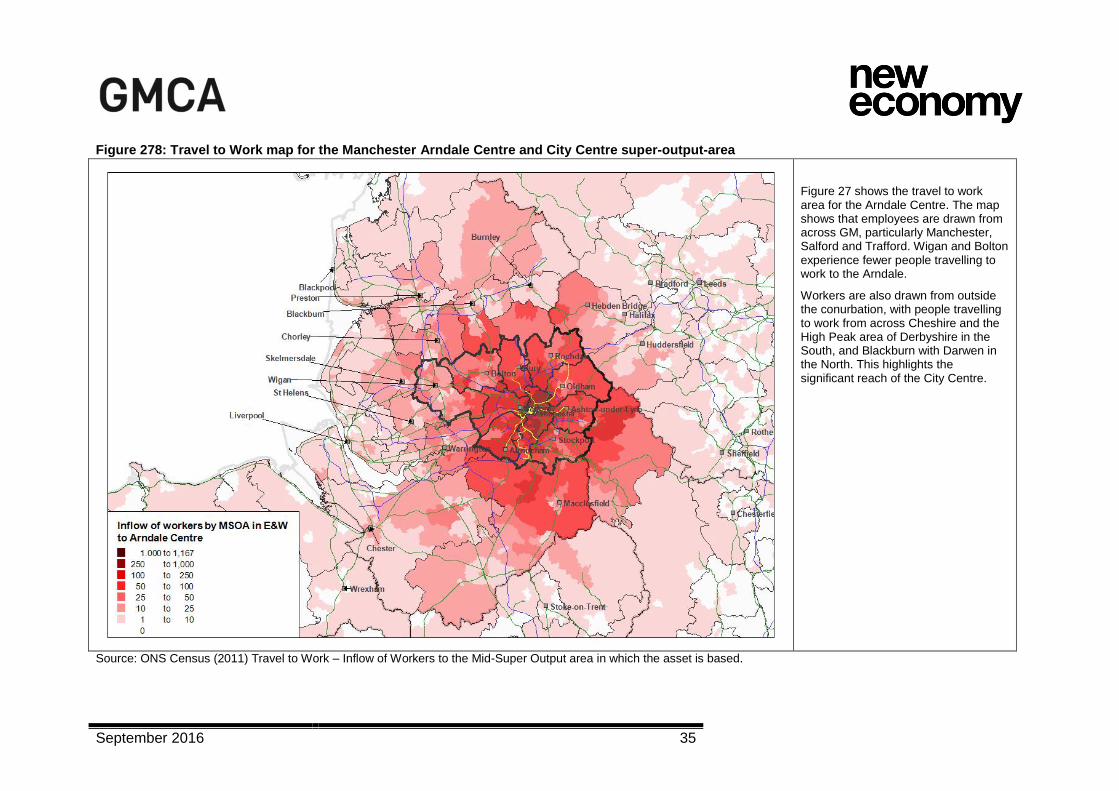

Figure 278: Travel to Work map for the Manchester Arndale Centre and City Centre super-output-area

Figure 27 shows the travel to work area for the Arndale Centre. The map shows that employees are drawn from across GM, particularly Manchester, Salford and Trafford. Wigan and Bolton experience fewer people travelling to work to the Arndale.

Workers are also drawn from outside the conurbation, with people travelling to work from across Cheshire and the High Peak area of Derbyshire in the South, and Blackburn with Darwen in the North. This highlights the significant reach of the City Centre.

Source: ONS Census (2011) Travel to Work – Inflow of Workers to the Mid-Super Output area in which the asset is based.

September 2016 36

7 Growth Potential Forecasts for growth

7.1 A number of economic scenarios have been developed to assess the growth potential of

the sector in GM over the next twenty years. The baseline forecast for GM sets out the

likely growth pattern based on a continuation of past trends and is derived from the

Greater Manchester Forecasting Model (GMFM).20 It is a ‘policy neutral’ forecast as it

assumes that policy will be as effective in the future as it has been in the past. The latest

GMFM baseline (GMFM 2015) is more pessimistic than the previous iteration of GMFM,

reflecting a weaker UK growth profile even before the result of the EU referendum. It

sees GM grow at a faster rate than the NW economy at 2.3% year on year, which is in

line with the UK average.

7.2 To inform the development of the GMSF, an updated Accelerated Growth Scenario

(AGS-2015) has been developed based upon improved sector growth performance

alongside higher population growth. This scenario is predicated upon GM playing a

leading role in the development of the Northern Powerhouse and achieving the

ambitions laid out by the UK Government within its NW Long Term Economic Plan.21

7.3 The baseline forecast for GM suggests an extra 17,600 jobs by 2035, and an average

employment growth rate of 0.4%pa. This is forecast to equate to an additional £4.3bn in

GM’s economy each year by 2035. However, the central Accelerated Growth Scenario

(AGS-2015) suggests that the number of additional jobs could be higher growing by

26,300 employees from 2015 to 2035, and a further £4.9bn GVA per annum in GM’s

economy by 2035.

7.4 Wholesale in particular is predicted to grow substantially over the next two decades.

Under the AGS-2015 this could be as high as 15,100 between 2015 and 2035,

comprising over half of the growth potential for the sector. This is also set in the context

of decline over the previous 20 years (1995 to 2015) of 6,300 in employment further

demonstrating the scale of opportunity that is forecast in this sector.

Figure 28: Retail, Wholesale Distribution - Baseline and accelerated forecast

Net increase

1995 to 2015

GMFM Baseline

2015 to 2035

AGS- 2015

Difference % CAGR Difference % CAGR Difference % CAGR

Jobs 2,400 0.1 17,600 0.4 26,300 0.6

GVA £1.8bn 1.6 £4.3bn 2.5 £4.9 2.8

Source: Oxford Economics and New Economy.

20

Oxford Economics 21

UK Government (2015): Long Term Economic Plan for the North West

September 2016 37

Opportunities

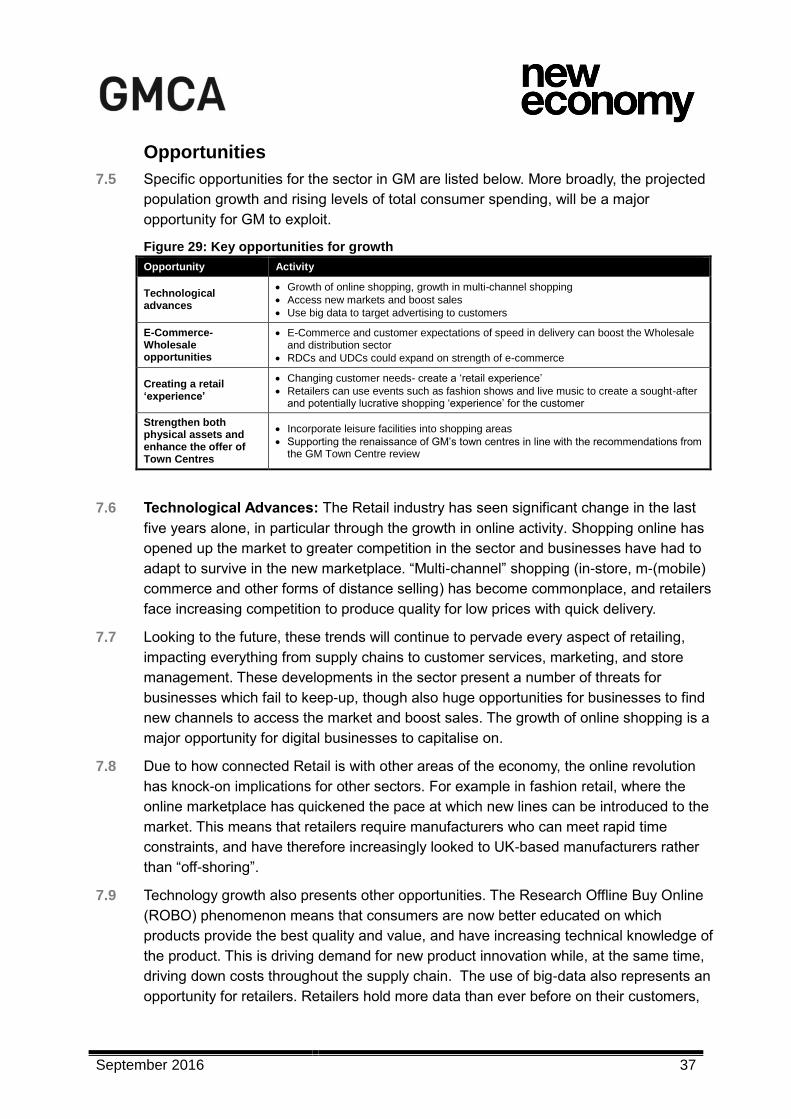

7.5 Specific opportunities for the sector in GM are listed below. More broadly, the projected

population growth and rising levels of total consumer spending, will be a major

opportunity for GM to exploit.

Figure 29: Key opportunities for growth

Opportunity Activity

Technological advances

Growth of online shopping, growth in multi-channel shopping

Access new markets and boost sales

Use big data to target advertising to customers

E-Commerce- Wholesale opportunities

E-Commerce and customer expectations of speed in delivery can boost the Wholesale and distribution sector

RDCs and UDCs could expand on strength of e-commerce

Creating a retail ‘experience’

Changing customer needs- create a ‘retail experience’

Retailers can use events such as fashion shows and live music to create a sought-after and potentially lucrative shopping ‘experience’ for the customer

Strengthen both physical assets and enhance the offer of Town Centres

Incorporate leisure facilities into shopping areas

Supporting the renaissance of GM’s town centres in line with the recommendations from the GM Town Centre review

7.6 Technological Advances: The Retail industry has seen significant change in the last

five years alone, in particular through the growth in online activity. Shopping online has

opened up the market to greater competition in the sector and businesses have had to

adapt to survive in the new marketplace. “Multi-channel” shopping (in-store, m-(mobile)

commerce and other forms of distance selling) has become commonplace, and retailers

face increasing competition to produce quality for low prices with quick delivery.

7.7 Looking to the future, these trends will continue to pervade every aspect of retailing,

impacting everything from supply chains to customer services, marketing, and store

management. These developments in the sector present a number of threats for

businesses which fail to keep-up, though also huge opportunities for businesses to find

new channels to access the market and boost sales. The growth of online shopping is a

major opportunity for digital businesses to capitalise on.

7.8 Due to how connected Retail is with other areas of the economy, the online revolution

has knock-on implications for other sectors. For example in fashion retail, where the

online marketplace has quickened the pace at which new lines can be introduced to the

market. This means that retailers require manufacturers who can meet rapid time

constraints, and have therefore increasingly looked to UK-based manufacturers rather

than “off-shoring”.

7.9 Technology growth also presents other opportunities. The Research Offline Buy Online

(ROBO) phenomenon means that consumers are now better educated on which

products provide the best quality and value, and have increasing technical knowledge of

the product. This is driving demand for new product innovation while, at the same time,

driving down costs throughout the supply chain. The use of big-data also represents an

opportunity for retailers. Retailers hold more data than ever before on their customers,

September 2016 38

opening up potential for targeted advertising and improved use of social media. The

sector has already moved to recruit more personnel with relevant technical and data

expertise for this purpose.

7.10 E-commerce - Wholesale and Distribution opportunities: Home delivery services

from online shopping and ‘Click & Collect’ which is anticipated to grow by 17% in 2015

alone according to the British Retail Consortium22 have had an impact on the

Wholesale and Logistics sectors. The growth of online retail (several major firms are

located in GM including, for example, NBrown Group, Boohoo, and MissGuided) will

drive increasing need for major logistics sites, alongside many new smaller distribution

hubs that are close to customers.

7.11 GM already benefits from strong existing distribution sites, for example ASDA has a

distribution site at Kingsway Business Park in Rochdale, as well as strong road and rail

links across the UK. MDS Transmodal have highlighted opportunities for expansion of

Regional and Urban Distribution Centres (RDCs and UDCs) and potentially National

Distribution Centres in GM should sites be made available, which could help stimulate

growth opportunities for the Retail, Wholesale Distribution sector.23

7.12 Creating a ‘retail experience’: Retailers are facing increasing demand to create a

Retail “experience”, be that in a physical store or online. Deloitte cites retailers

incorporating events such as fashion shows and music festivals, as well as interactive

displays and marketing on mobile phones and tablets into in-store shopping

environments.24 GM retailers can capitalise on this trend to make shopping more of an

experience for consumers and thereby increase footfall through their doors.

7.13 Strengthen Town Centres: Alongside these key technology and data drivers in the

sector, opportunities also exist to strengthen physical retail assets in GM. Town and city

centre retail schemes are increasingly looking to incorporate leisure activities, housing

and civic functions, which are likely to become key occupiers alongside larger Retail

brands, with several GM retail centres, including Bury, Bolton, Oldham, Wigan and

Stockport, already looking to incorporate new in-town cinemas and associated food

offers. In particular, increased leisure activities also serve to improve the sector’s

offering to, and integration with, the evening economy.

7.14 Specific challenges are faced by different town centres. The following actions were

recommended within the GM Town Centres25 report to capitalise on the opportunities,

and combat the challenges, identified (note this has been updated where relevant to

reflect current priorities).

22

British Retail Consortium Business Information Services, 2015, The Changing Face of British Retail 23

MDS Transmodal, September 2014, Greater Manchester Logistics Study 24

Deloitte, 2015. Global Powers of Retailing 2015, Embracing Innovation 25

GMCA, March 2013, GM Town Centres Project: Concluding Report.

http://www.agma.gov.uk/cms_media/files/12_gm_town_centres_project.pdf%3Fstatic%3D1

September 2016 39

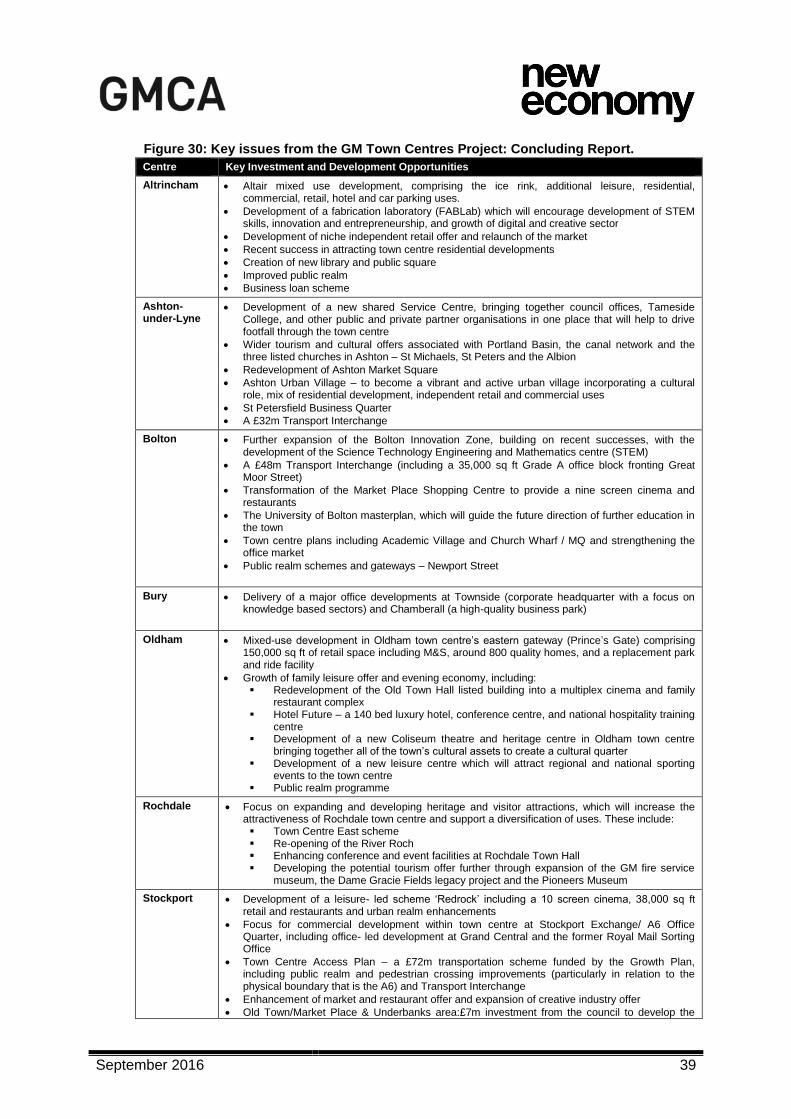

Figure 30: Key issues from the GM Town Centres Project: Concluding Report.

Centre Key Investment and Development Opportunities

Altrincham Altair mixed use development, comprising the ice rink, additional leisure, residential, commercial, retail, hotel and car parking uses.

Development of a fabrication laboratory (FABLab) which will encourage development of STEM skills, innovation and entrepreneurship, and growth of digital and creative sector

Development of niche independent retail offer and relaunch of the market

Recent success in attracting town centre residential developments

Creation of new library and public square

Improved public realm

Business loan scheme

Ashton-under-Lyne

Development of a new shared Service Centre, bringing together council offices, Tameside College, and other public and private partner organisations in one place that will help to drive footfall through the town centre

Wider tourism and cultural offers associated with Portland Basin, the canal network and the three listed churches in Ashton – St Michaels, St Peters and the Albion

Redevelopment of Ashton Market Square

Ashton Urban Village – to become a vibrant and active urban village incorporating a cultural role, mix of residential development, independent retail and commercial uses

St Petersfield Business Quarter

A £32m Transport Interchange

Bolton Further expansion of the Bolton Innovation Zone, building on recent successes, with the development of the Science Technology Engineering and Mathematics centre (STEM)

A £48m Transport Interchange (including a 35,000 sq ft Grade A office block fronting Great Moor Street)

Transformation of the Market Place Shopping Centre to provide a nine screen cinema and restaurants

The University of Bolton masterplan, which will guide the future direction of further education in the town

Town centre plans including Academic Village and Church Wharf / MQ and strengthening the office market

Public realm schemes and gateways – Newport Street

Bury Delivery of a major office developments at Townside (corporate headquarter with a focus on knowledge based sectors) and Chamberall (a high-quality business park)

Oldham Mixed-use development in Oldham town centre’s eastern gateway (Prince’s Gate) comprising 150,000 sq ft of retail space including M&S, around 800 quality homes, and a replacement park and ride facility

Growth of family leisure offer and evening economy, including: Redevelopment of the Old Town Hall listed building into a multiplex cinema and family

restaurant complex Hotel Future – a 140 bed luxury hotel, conference centre, and national hospitality training

centre Development of a new Coliseum theatre and heritage centre in Oldham town centre

bringing together all of the town’s cultural assets to create a cultural quarter Development of a new leisure centre which will attract regional and national sporting

events to the town centre Public realm programme

Rochdale Focus on expanding and developing heritage and visitor attractions, which will increase the attractiveness of Rochdale town centre and support a diversification of uses. These include: Town Centre East scheme Re-opening of the River Roch Enhancing conference and event facilities at Rochdale Town Hall Developing the potential tourism offer further through expansion of the GM fire service

museum, the Dame Gracie Fields legacy project and the Pioneers Museum

Stockport Development of a leisure- led scheme ‘Redrock’ including a 10 screen cinema, 38,000 sq ft retail and restaurants and urban realm enhancements

Focus for commercial development within town centre at Stockport Exchange/ A6 Office Quarter, including office- led development at Grand Central and the former Royal Mail Sorting Office

Town Centre Access Plan – a £72m transportation scheme funded by the Growth Plan, including public realm and pedestrian crossing improvements (particularly in relation to the physical boundary that is the A6) and Transport Interchange

Enhancement of market and restaurant offer and expansion of creative industry offer

Old Town/Market Place & Underbanks area:£7m investment from the council to develop the

September 2016 40

Centre Key Investment and Development Opportunities

historic core as a focus for markets, specialist retail, food & drink and creative industries, building on existing conservation-led regeneration of the area and Portas Pilot status

Residential development currently being delivered

Long-term opportunities relating to transport provision include implications of HS2 for Stockport Rail Station and the opportunity for a tram train network to be developed

Wigan Planned investment / development opportunities include: New Cinema and leisure offer in the town centre New 1100 seat conference and theatre centre Wigan Transport Hub and potential to benefit from HS2/West Coast Mainline Public realm improvements

Threats

7.15 Specific threats facing the sector in GM are listed below. However, as noted above

some of the areas identified as opportunities may present a threat to the sector if they

are not maximised.

Figure 31: Key threats facing the future of the Retail, Wholesale Distribution

Threat Activity

Individual Stores Multi-channel shopping may present difficulties for individual stores as it is unclear how

consumers will choose to shop in the future

7.16 Individual Stores: There is a degree of uncertainty about how people will shop in the

multi-channel era. Research suggests that nationally more than 70% of retailers are

looking to either reduce space, share use of space or close stores altogether in 2015.26

In contrast, 69% were looking to invest in their websites and mobile sites over the

coming year, as opposed to only 28% looking to invest in staff training. There may well

be a changing role for physical stores. ‘Click & Collect’, which is anticipated to grow by

17% in 2015 alone, could become key to physical stores remaining competitive in the

market for consumers’ convenience. Businesses will also have to look to provide a

customer ‘experience’ in order to retain footfall. In town centres, this can also be done in

collaboration with local authorities to improve shopping spaces.

26

TLT Solicitors (2015): Retail Growth Strategies for 2015

September 2016 41

8 Spatial Considerations 8.1 Based upon the evidence presented, there are spatial implications for the online, high

street and out of town markets. As a result the Retail sector will continue to change

significantly in the coming years. The following changes are expected to be observed in

GM, each with its own implications for spatial development.

8.2 Online Retail: Online Retail continues to be a significant growth area nationally and for

GM. This presents opportunities for digital businesses that will cluster in areas where

there are existing sector strengths. The growth of online retail will also drive increasing

need for major wholesale and logistics sites, alongside many new smaller distribution

hubs that are close to customers to enable retailers to meet demanding delivery

timescales.

8.3 GM already benefits from strong existing wholesale and logistics distribution sites, as

well as strong road and rail links across the UK. GM is also home to National

Distribution Centres, including the 100,000sqm Shop Direct national distribution centre

in Shaw Oldham. MDS Transmodal have highlighted opportunities for expansion of

Regional and Urban Distribution Centres (RDCs and UDCs) as well as National

Distribution Centres in GM, which could help stimulate growth opportunities for the

Retail, Wholesale Distribution sector.27

8.4 If GM is to attract further growth in online retailers, the conurbation must continue to

offer high quality accommodation to suit both office and storage/distribution facilities

preferably in adjacent locations. In addition, businesses need an accessible location,

with sufficient space, that is also close to transport routes. This is particularly significant

in attracting headquarters, alongside a highly skilled and digitally savvy resident

workforce from which the company can draw.

8.5 High street Retail (including Manchester City Centre): Growth in online retail,

alongside other factors is having an impact on the high street. Research from the

Javelin Group forecasts that, by 2020, there will be 31% fewer non-food stores in the

UK, and 21% less floor space than at present.28 How this equates into a net gain or net

loss for different individual retail centres across GM requires further analysis through a

Retail capacity study/ies. Given its existing strength, Manchester city centre would be

expected to remain as the prime GM high street retail location.

8.6 There will continue to need be a focus on supporting sustainable town centres across