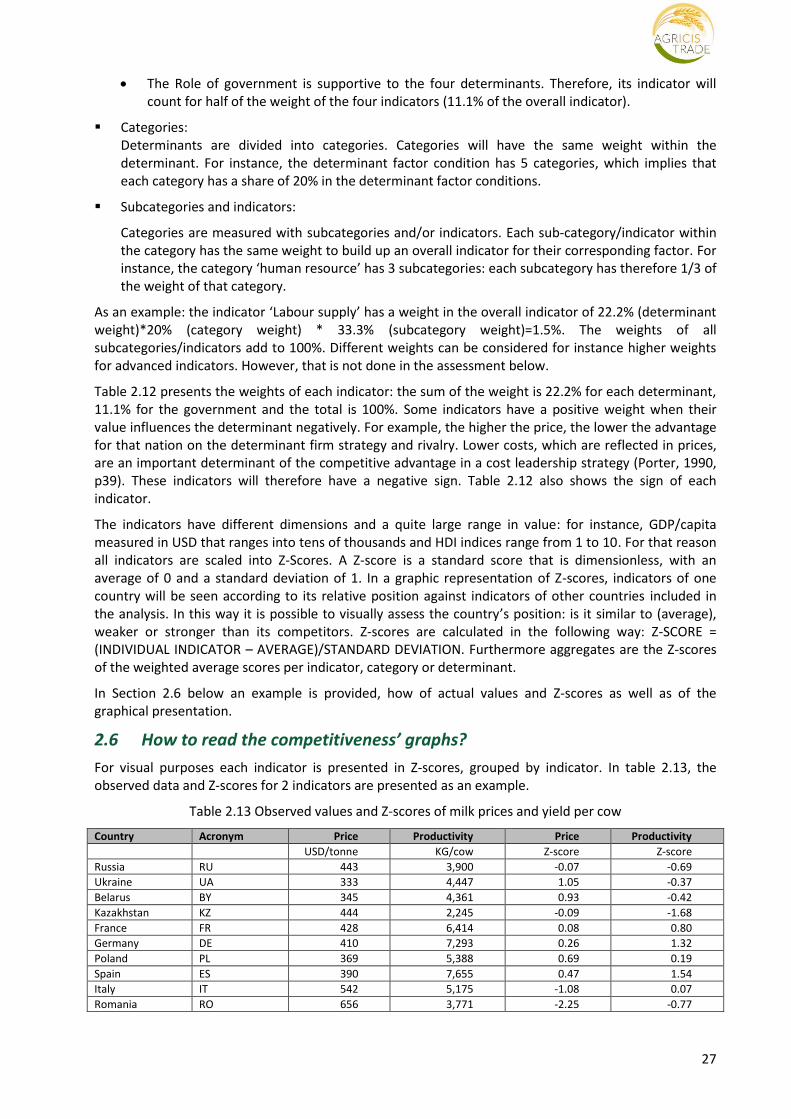

1 Deliverable 4.1: Competitiveness of CIS and EU agrifood chains Quantifying Porter’s diamond Submission date: November 2015 Jo H.M. Wijnands, Siemen van Berkum and David Verhoog LEI Wageningen UR The Hague, The Netherlands This project has received funding from the European Union’s Seventh Framework Programme for Research, Technological Development and Demonstration under Grant Agreement no 612755

Transcript

1

Deliverable 4.1: Competitiveness of CIS and EU agrifood chains Quantifying Porter’s diamond Submission date: November 2015

Jo H.M. Wijnands, Siemen van Berkum and David Verhoog LEI Wageningen UR The Hague, The Netherlands

This project has received funding from the European Union’s Seventh Framework Programme for Research, Technological Development and Demonstration under Grant Agreement no 612755

2

Acknowledgement We gratefully acknowledge the work done by Bibiana M. Armenta Gutiérrez, who made first steps in elaborating the approach of quantifying Porter’s diamond, together with her supervisor Jo Wijnands, when drafting her master thesis (unpublished master thesis, 2011). Next, we like to thank Inna Levkovich and Aaron Grau from IAMO (Germany), and Stephan von Cramon-Taubadel (University of Göttingen) for their constructive comments while reviewing a first draft of this report.

Contents Abbreviations and Acronyms ....................................................................................................................... 4

Abbreviations and Acronyms CIS Commonwealth of Independent States. Member states are:

AM Armenia AZ Azerbaijan BY Belarus GE Georgia KZ Kazakhstan MD Moldova RU Russia UA Ukraine

EU European Union. Member states are: AT Austria

BE Belgium BG Bulgaria HR Croatia CY Cyprus CZ Czech Republic DK Denmark EE Estonia FI Finland FR France DE Germany GR Greece HU Hungary IE Ireland IT Italy LV Latvia LT Lithuania LU Luxembourg MT Malta NL Netherlands PL Poland PT Portugal RO Romania SK Slovak Republic SI Slovenia ES Spain SE Sweden UK United Kingdom

EU-xx Refers to the number of EU member states in order of accession. HDR Human Development Report IDI ICT Development Index LPI Logistics performance index RMA Relative iMport Advantage index RTA Relative Trade Advantage index RXA Relative eXport Advantage index UNDP United Nations Development Programme WDI World Development Indicators WEF Word Economic Forum

5

Executive summary

This study evaluates the competitiveness of the agrifood sectors in CIS countries benchmarked against EU countries, using Porters’ diamond framework of determinants of competitiveness to analyse the competitive strength of agrifood sectors. In the quantification of performance indicators, the study focuses on nine agrifood sectors and the CIS countries Russia, Ukraine, Kazakhstan and Belarus, which together account for over 90% of CIS’ total production value of these agrifood sectors. At EU level, major producers of each agrifood sector are selected for benchmarking.

Conclusions on Porter’s diamond determinants of competitiveness

Competitiveness of the agrifood sectors in the CIS countries is largely based on low prices (based on abundant and hence cheap land and labour). The competitive position of the CIS agrifood sector is weak, as it lacks the presence of strong supplier industries and a government that provides regulatory quality and ensures compliance with rules of society (including formal laws and informal norms). More competitive supplier industries and services enhance efficiency in processing and distributing stages in the agrifood sectors while ‘good governance’ adds to an economically sound and stable business environment. The international competitiveness of the CIS agrifood sectors, therefore, would benefit from strengthening the agrifood supplying industries and from government policies that create an enabling business environment which is more supportive to the agrifood sectors’ development.

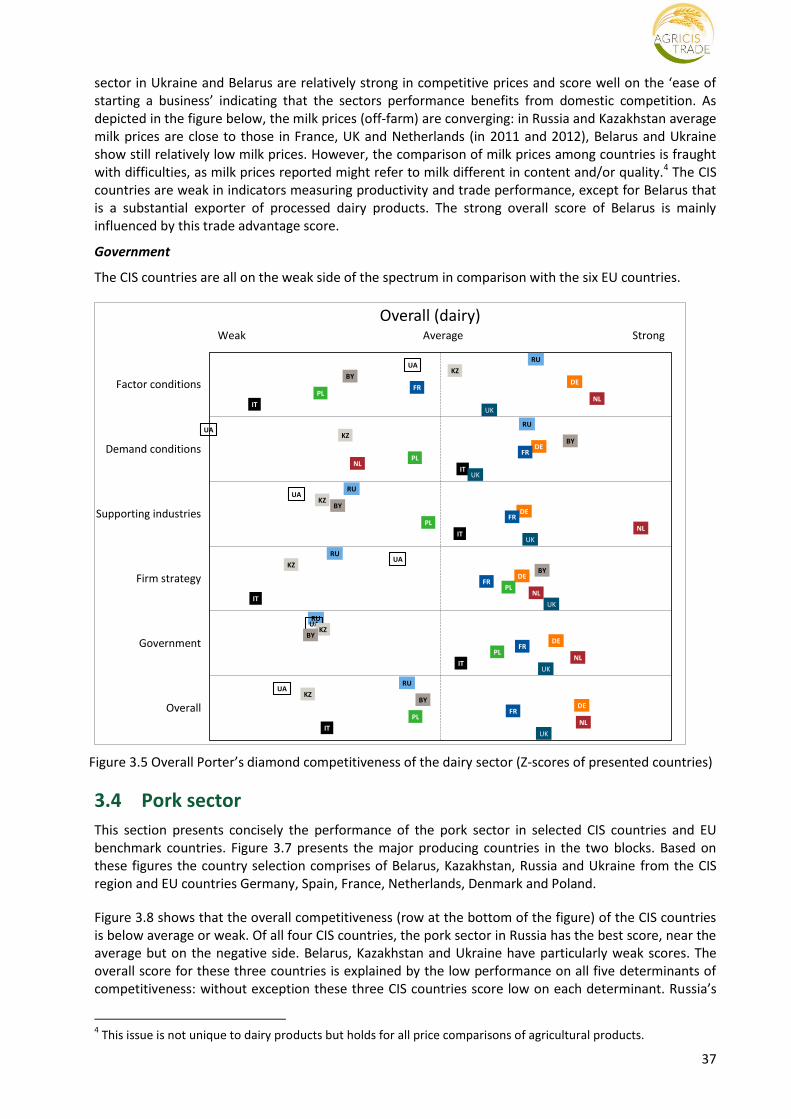

Figure S1 Scores on Porter’s diamond determinants for all food sectors (Z-scores of presented countries) See Section 2.6 on how to interpret the figure.

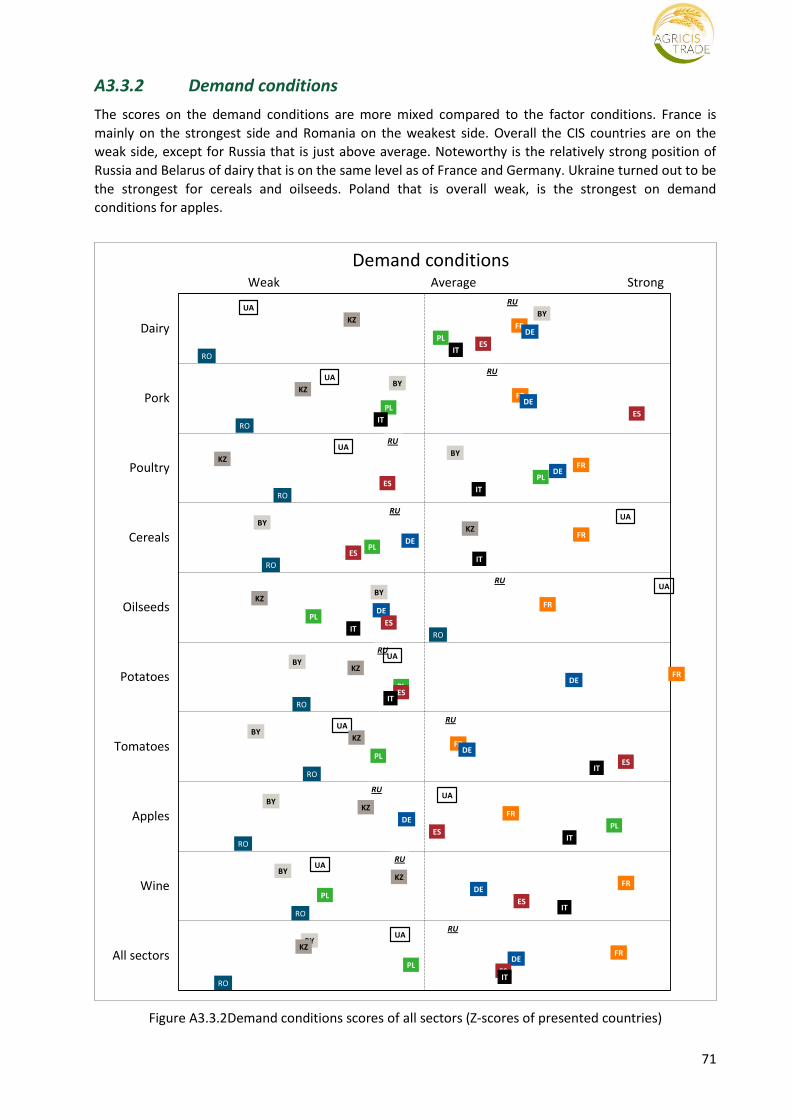

The four largest CIS countries (see figure S1: Russia RU, Belarus BY, Ukraine UA, Kazakhstan KZ) show the highest scores on the Factor Conditions and Demand Conditions determinants, indicating that the food sectors’ strength is mainly in cheap labour and land, and the home country orientation (although all of these countries also export agricultural commodities in significant volumes). All CIS countries are

RU

RU

RU

RU

RU

RU

UA

UA

UA

UA

UA

UA

BY

BY

BY

BY

BY

BY

KZ

KZ

KZ

KZ

KZ

KZ

FR

FR

FR

FR

FR

FR

DE

DE

DE

DE

DE

DE

PL

PL

PL

PL

PL

PL

ES

ES

ES

ES

ES

ES

IT

IT

IT

IT

IT

IT

RO

RO

RO

RO

RO

RO

Factor conditions

Demand conditions

Supporting industries

Firm strategy

Government

Overall

All sectors

Weak Average Strong

6

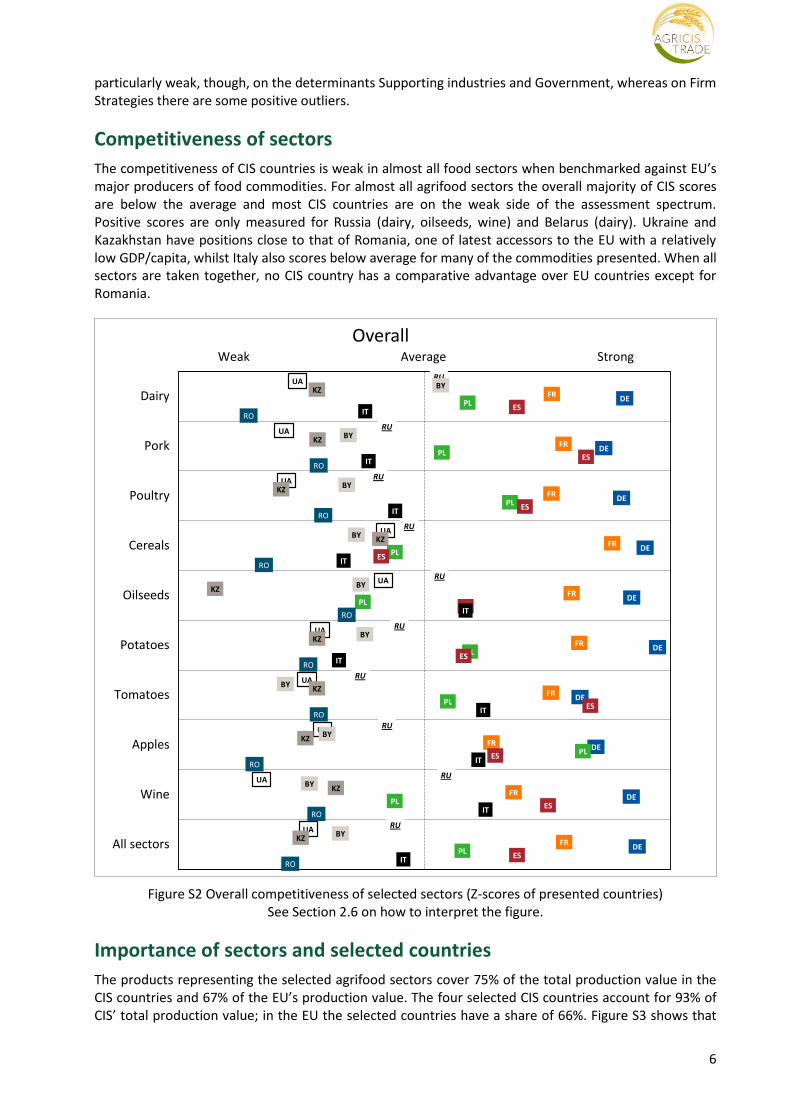

particularly weak, though, on the determinants Supporting industries and Government, whereas on Firm Strategies there are some positive outliers.

Competitiveness of sectors

The competitiveness of CIS countries is weak in almost all food sectors when benchmarked against EU’s major producers of food commodities. For almost all agrifood sectors the overall majority of CIS scores are below the average and most CIS countries are on the weak side of the assessment spectrum. Positive scores are only measured for Russia (dairy, oilseeds, wine) and Belarus (dairy). Ukraine and Kazakhstan have positions close to that of Romania, one of latest accessors to the EU with a relatively low GDP/capita, whilst Italy also scores below average for many of the commodities presented. When all sectors are taken together, no CIS country has a comparative advantage over EU countries except for Romania.

Figure S2 Overall competitiveness of selected sectors (Z-scores of presented countries) See Section 2.6 on how to interpret the figure.

Importance of sectors and selected countries

The products representing the selected agrifood sectors cover 75% of the total production value in the CIS countries and 67% of the EU’s production value. The four selected CIS countries account for 93% of CIS’ total production value; in the EU the selected countries have a share of 66%. Figure S3 shows that

RU

RU

RU

RU

RU

RU

RU

RU

RU

RU

UA

UA

UA

UA

UA

UA

UA

UA

UA

UA

BY

BY

BY

BY

BY

BY

BY

BY

BY

BY

KZ

KZ

KZ

KZ

KZ

KZ

KZ

KZ

KZ

KZ

FR

FR

FR

FR

FR

FR

FR

FR

FR

FR

DE

DE

DE

DE

DE

DE

DE

DE

DE

DE

PL

PL

PL

PL

PL

PL

PL

PL

PL

PL

ES

ES

ES

ES

ES

ES

ES

ES

ES

ES

IT

IT

IT

IT

IT

IT

IT

IT

IT

IT

RO

RO

RO

RO

RO

RO

RO

RO

RO

RO

Dairy

Pork

Poultry

Cereals

Oilseeds

Potatoes

Tomatoes

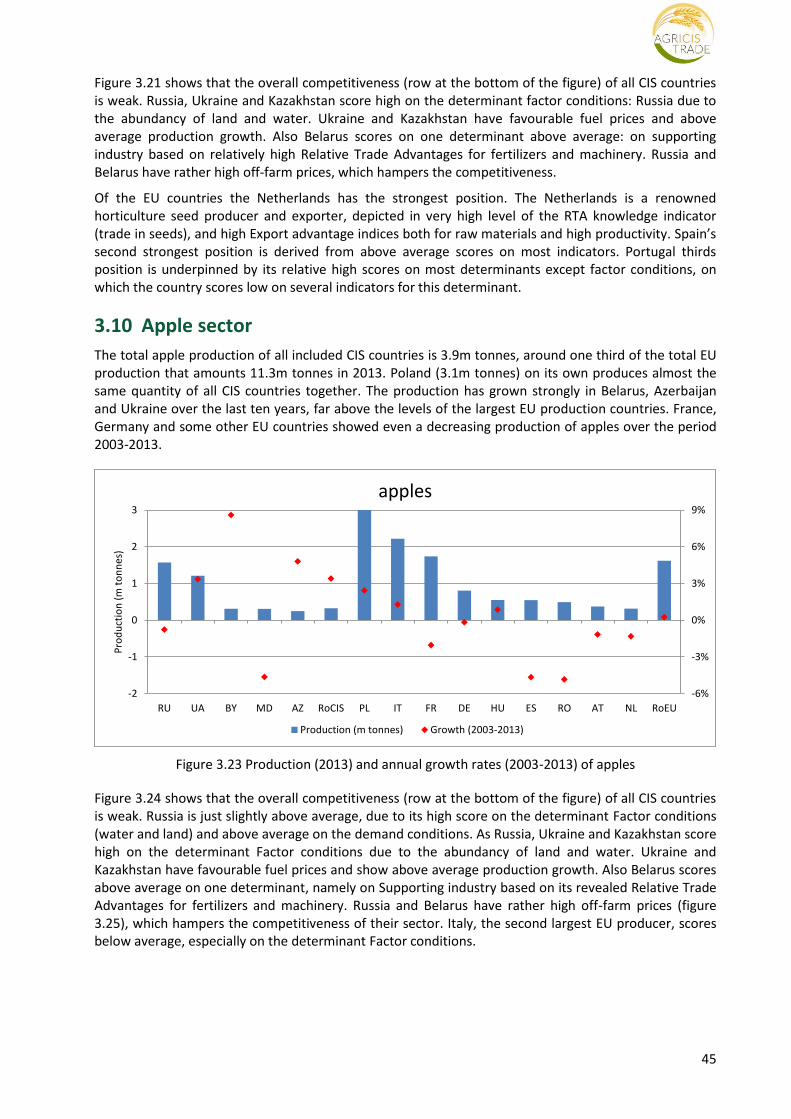

Apples

Wine

All sectors

OverallWeak Average Strong

7

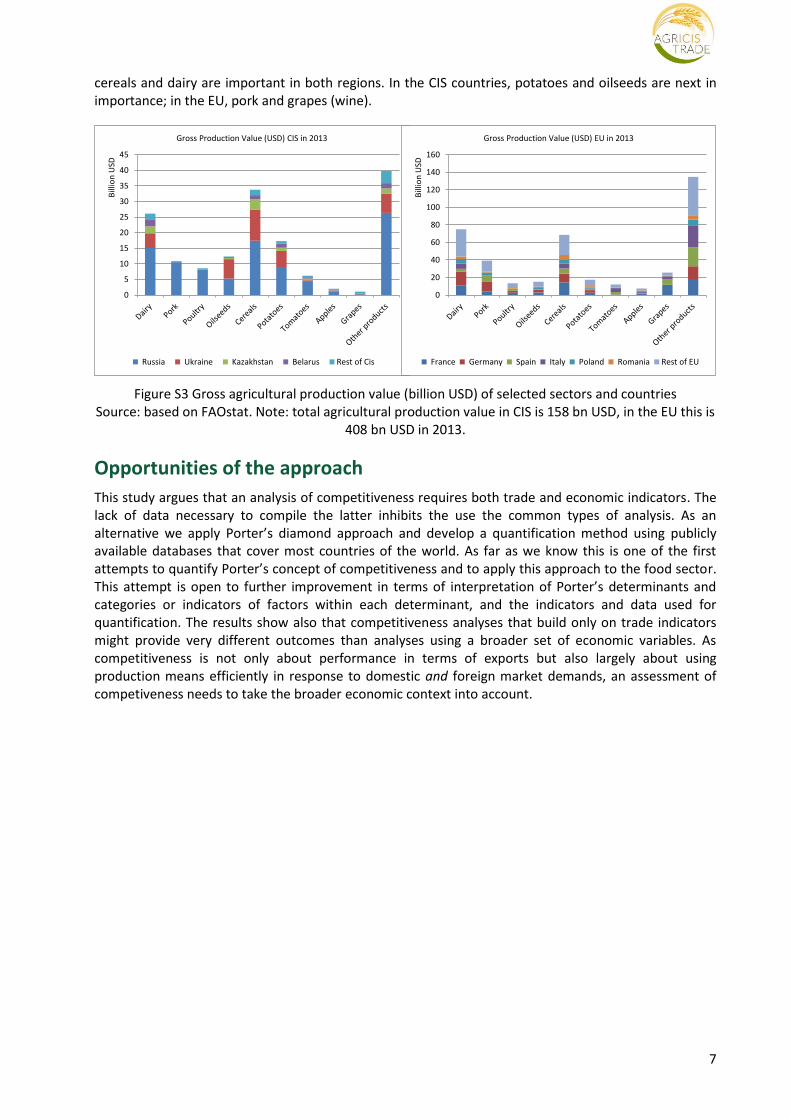

cereals and dairy are important in both regions. In the CIS countries, potatoes and oilseeds are next in importance; in the EU, pork and grapes (wine).

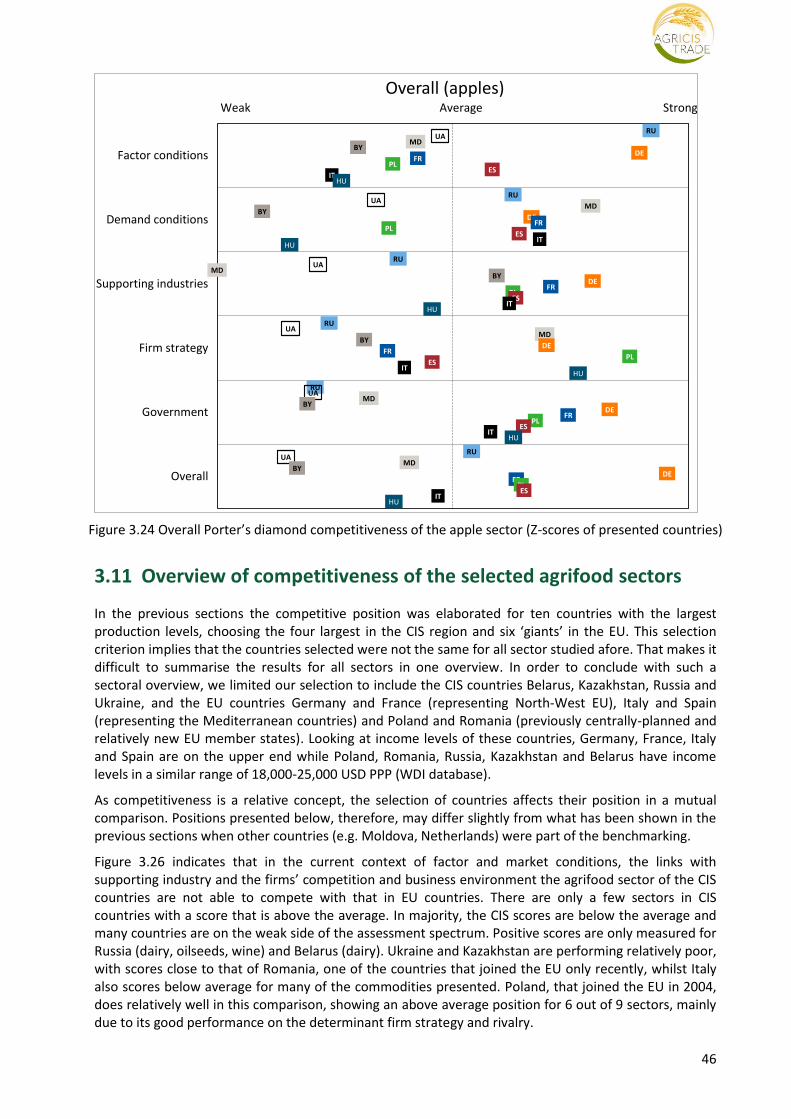

Figure S3 Gross agricultural production value (billion USD) of selected sectors and countries Source: based on FAOstat. Note: total agricultural production value in CIS is 158 bn USD, in the EU this is

408 bn USD in 2013.

Opportunities of the approach

This study argues that an analysis of competitiveness requires both trade and economic indicators. The lack of data necessary to compile the latter inhibits the use the common types of analysis. As an alternative we apply Porter’s diamond approach and develop a quantification method using publicly available databases that cover most countries of the world. As far as we know this is one of the first attempts to quantify Porter’s concept of competitiveness and to apply this approach to the food sector. This attempt is open to further improvement in terms of interpretation of Porter’s determinants and categories or indicators of factors within each determinant, and the indicators and data used for quantification. The results show also that competitiveness analyses that build only on trade indicators might provide very different outcomes than analyses using a broader set of economic variables. As competitiveness is not only about performance in terms of exports but also largely about using production means efficiently in response to domestic and foreign market demands, an assessment of competiveness needs to take the broader economic context into account.

0

5

10

15

20

25

30

35

40

45

Bill

ion

USD

Gross Production Value (USD) CIS in 2013

Russia Ukraine Kazakhstan Belarus Rest of Cis

0

20

40

60

80

100

120

140

160

Bill

ion

USD

Gross Production Value (USD) EU in 2013

France Germany Spain Italy Poland Romania Rest of EU

8

1. Introduction

1.1 Background: contribution to the AGRICISTRADE project

AGRICISTRADE aims at analysing the current and potential developments for agricultural and biomass trade between the EU and eight of its eastern neighbour countries, also known as the CIS countries (http://www.agricistrade.eu). AGRICISTRADE is structured around four research objectives:

Understanding the agrifood sector performance in the CIS countries in the context of policies;

Understanding the causes of untapped agricultural production potentials in CIS countries and suggest pathways for enhancing yields, land use and competitive performances;

Exploring current and future developments in agricultural supply chains in CIS countries;

Enhancing the analytical framework for scenarios of developments of the agrifood potentials in CIS countries and consequences for trade between the CIS and EU.

This study relates to the third objective of the project, which is ‘to explore developments in agricultural supply chains’ in CIS countries. This report contributes to the work package that evaluates the performances of selected supply chains in these countries, identifies institutional factors that constrain their economic performance and makes suggestions how policies could enhance supply chain performance. More specifically, this report looks into performance indicators of selected agrifood sectors in EU’s eastern neighbours to assess their relative competitive position against EU agrifood sectors. We use the term ‘agrifood sectors’ that also includes other terms such as ‘agricultural value chains’, ‘agricultural supply or demand chains’. An agrifood sector includes all activities from suppliers of (advanced) inputs to the demand by the final users, including the supporting and enabling industries. Some of these activities are performed by industries, such as the food processing or manufacturing industries or the input (e.g. machinery or seeds) supplying industries.

1.2 Approach and structure of the study

Competitiveness is a broad, complex concept embracing many issues of (the availability, quality and use of) resource endowment and is often heavily affected by policy interventions. There is no general agreement on how to define and measure competitiveness precisely. Studies often adopt own definitions and choose a specific measurement method that fits the entity level of analysis, which can be at country, sector or firm level (Sagheer et al., 2009). There is, however, more or less consensus on which measures could be used to assess competitiveness, namely measures that focus on trade success (exports and import indices) and measures that place emphasis on the firm’s structure and strategy (cost leadership, productivity, efficiency indicators, and non-price supremacy) (see Latruffe, 2010, for an overview of methods and indicators used).

In assessing the food processing industry’s competitiveness, performance indices such as the development in production value, value added, profits, productivity, export market shares and Revealed Comparative Advantage (RCA) indicators are generally used (Wijnands et al., 2015; Ecorys, 2015 (forthcoming); Wijnands et al., 2008)). Trade data used to calculate export market shares or compile RCA indicators1 are available for all countries in the world via the UNCOMTRADE database. Other economic data such as on production value, value added and profits have to come from national statistics on the economic activities of the food industry. For the EU countries, for instance, a major source of relevant data is Eurostat’s Structural Business Statistics (SBS) that presents economic activities according to the NACE activity classification for the industry and distributive trade, yet not for (primary) agriculture. The SBS describes the structure, conduct and performance of businesses across the EU: data are available for the EU-27/28 and for the individual Member States. A subset of the SBS information is also available according to the size of enterprises.

1 Appendix 1 provides the specification of these trade-based indicators

9

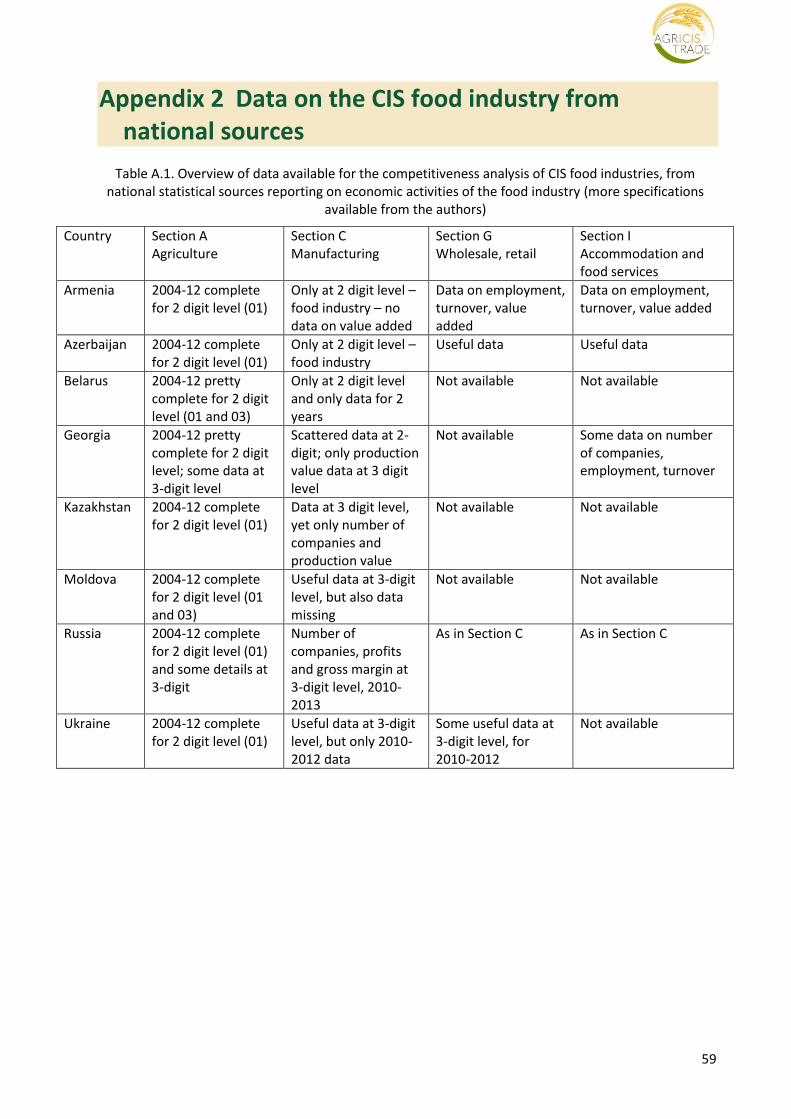

Our survey exploring the national statistical sources of the eight CIS countries, however, did not provide the details necessary for a food industry analyses that differentiates among subsectors within the food industry in detail. Appendix 2 provides an overview of data available in each of the countries, indicating that for Armenia, Azerbaijan, Belarus and Georgia, some data at the level of the total food industry (at 2-digit NACE level) is available but not the full set we are looking for. Next, where countries have information on specific sectors in the food industries, data are scattered. Hence, although trade data are available to compile relevant trade indicators, data to build the economic indicators of performance of the food industry in CIS countries are too incomplete for making a useful country comparison with the aim to evaluating competiveness. Therefore, in this study we explored an alternative approach for assessing the competitiveness of agrifood sectors in CIS countries.

This paper presents an alternative approach that is based on Michael Porter’s study (1990) on the international competitive advantage of nations. This approach includes several indicators that cover trade, structure and strategy as well as institutions. We will use Porter’s diamond approach to compile a national indicator of advantage, based on a country’s score on 1) factor conditions; 2) demand conditions; 3) firm strategy, structure and rivalry; 4) related and supporting industries. Most of these indicators are of a general nature, that is, they refer to macroeconomic variables related to sectors, while others are or can be interpreted as agrifood sector (commodity) specific. Porter’s framework has, however, a highly qualitative and abstract nature and lacks a methodology for measuring competitiveness (e.g (Rugman and Verbeke, 1993)). We couldn’t retrieve literature that operationalises and quantifies the determinants and the underlying categories of Porter’s Diamond. In this paper we consistently follow Porter’s argument and assign a quantitative indicator to each aspect, and by this build a composite index for each determinant and finally for Porter’s full set of determinants of competitiveness. This quantification adds a new dimension to the extensive literature on Porter’s diamond.

This report, therefore, contributes to the literature in two ways: it proposes a quantitative measurement of competitiveness based on the determinants of a nation’s competitiveness according to Porter’s theoretical framework, and applies this quantitative approach to assessing the competitive position of CIS food industries benchmarked against EU countries, something which to the authors’ knowledge has not been done in a similar structured way.

To that end we carried out the following activities:

1. Identifying indicators for measuring Porter’s diamond determinants. We briefly summarise Porter’s diamond approach and the determinants of competitiveness identified in that concept. Next, we present an overview of competitiveness’ indicators that we identified as appropriate proxies to measure the factors that are important in determining competitiveness according to Porter’s approach. These indicators can have a general and a sector specific nature. The selection of indicators and the methodology of quantifying these indicators are presented in Chapter 2.

2. Selecting agrifood sectors. The selection is based on the production value at primary producer level and covers the full agricultural sector: livestock, arable crops, horticulture and perennial crops. Our analysis focuses on the following selected agrifood sectors: dairy, pork, poultry, cereals, oilseeds, wine, potatoes, tomatoes and apples. These are the most important agricultural products of the agrifood sector in the CIS countries. This means they are not all equally important in all countries, but each product is important to the agricultural sector in at least several countries. The overview of the sectors included in this study is provided in Chapter 3.

3. Assessing the competitiveness of the selected agrifood sectors by applying our operationalisation of Porter’s determinants. These results are the topic of Chapter 3.

The three steps of activities are reported in the next two chapters. Chapter 4 concludes with discussing some issues that put our results in perspective and a brief list of major findings.

10

2. Methodology and indicators

This chapter presents the methodology and data sources used to operationalise our approach. In the first section we illustrate the many aspects associated with the concept of competitiveness. In the next section, we clarify Porter’s approaches of explaining competitiveness and motivate the choice for using Porter’s diamond as a base for our analyses of competitiveness of CIS agrifood sectors. The third section briefly presents the attributes of Porter’s diamond and explains the operationalizing of the determinants of competitiveness and specifies data sources that will be used for quantification. As our application of Porter’s diamond model entails quite a number of indicators, Section 4 wraps up the indicators and presents the scoring methodology. Finally, Section 5 clarifies how the scores will graphically be presented.

2.1 Competitiveness: a relative and multidimensional concept

Although competitiveness is not precisely defined in economic theory, it is generally understood as the ability to successfully face competition. Competitiveness would then be the ability to sell products that meet demand requirements (price, quality, quantity) and, at the same time, ensure profits over time that enable the firm to thrive. However, there is an extensive library of literature on the determinants of competitiveness and how it is (or should be) measured (e.g Crouch and Ritchie, 1999; Krugman, 1994; Metcalfe et al., 1992; Gorton et al., 2013; Latruffe, 2010; Buckley et al., 1988). Spence and Hazard (1998) illustrate the complexity of the concept as follows (on (p. xvii):

“The problem of international competitiveness has been defined in highly diverse ways. These definitions (and the proposed solutions to the problem) are partially inconsistent, and thoroughly confusing to most academics, politicians, policy-makers, and business managers. There is good reason for this confusion. The collection of problems alluded to as “competitiveness” is genuinely complex. Disagreements frequently occur not only at the level of empirical effects and of policies, but also in the very definition of the problem. Well-intentioned and reasonable people find themselves talking at cross purposes; sometimes it almost seems they are addressing different subjects.”

The literature referenced above singles out different aspects and dimensions of competitiveness. From that we learn that competitiveness (Wijnands and Verhoog, 2015 (forthcoming)):

is a relative concept. Latruffe (2010: 50) states that “competitiveness should be measured with

respect to a benchmark.” Competitiveness is a comparison of their ability to face competition and

sell products between entities, such as firms, industries or nations (Siggel, 2006). The outcome

depends on who is compared with whom: being successful in competition with one specific entity

does not mean that you are also successful in competing with other entities. Hence,

competitiveness will differ with the selection of entities.

can be expressed at different aggregation levels, such as at goods or services, people, firms,

industries or countries.

has multi-dimensional features. The World Economic Forum, for instance, distinguishes over 100

indicators divided into 12 pillars to assess the global competitiveness of countries (Schwab, 2014).

Several authors stress that competitiveness is not measured by a singly indicator (Sagheer et al.,

2009, Metcalfe et al., 1992). Porter argues that five forces determine the long run competition,

whether on the international or domestic market, of any industry. Each force is measured by several

indicators (Porter, 1980b). Porter’s diamond model for analysing competition between nations

distinguishes four determinants, each with several sub-determinants for determining the

competitiveness between nations (Porter, 1990). Buckley et al. (1988) also propose several

indicators, depending on the (aggregation) level of analysis and time horizon. Siggel (2006) as well as

Latruffe (2010) underline the need to include not only economic (costs, productivity, value added)

and trade indicators (unit values, export indicators) but also institutional factors such as

infrastructure or government policies. The dimensions depend on the aim of the study. Krugman

11

(1994), for example, argues that it makes little sense to measure an industry’s competitiveness on

the export market if it is (almost) fully focused on the domestic market. The dimensions or

indicators also depend on the focus of the study. Argote and Ingram stress that competitive

advantage of firms is based on the creation and transfer of knowledge (Argote and Ingram, 2000),

highlighting innovation and knowledge as determinants of competitive potential.

is measured in many different ways. Several theories or schools of thought defining and analysing

competitiveness point at different indicators to measure it. From a strategic management

perspective, competitiveness refers to the conduct of companies in shaping organizational

advantages (Thompson and Strickland, 2003, Wright et al., 1998) and/or market advantages (Hamel

and Prahalad, 1994). Financial ratios (profit margin, current ratio, return on assets, debtor and

collector period) are the metrics in accounting (Fleisher and Bensoussan, 2003). Measuring

competitiveness with international economic indicators has its roots in Adam Smith’s trade theory,

which explains differences in competitiveness by way of absolute cost differences between

countries. However, the application of new trade theories entails incorporating a wider array of

aspects in the analysis such as product differentiation, innovation, economies of scale and

productivity (Van Berkum and Van Meijl, 2000). O'Mahoney and Van Ark focus on productivity,

explaining that productivity differences explain largely differences in competitiveness (O'Mahoney

and Van Ark, 2003).

may point at time horizons (Siggel, 2006). Several authors use sustainable gain in e.g. market share:

hence a comparison between two periods. According to Porter (1980, 1990) sustainable competitive

advantage is the fundamental source for above-average performance in the long run. Buckley et al.

(1988) also introduce the dynamic aspect in the measurement of competitiveness by three

characteristics: competitive performance (what it is), potential (what can be) and process (how to

reach potential), each with different indicators.

often has ambiguous linkages with policies. In her overview of studies on competitiveness in the

agricultural and agrifood sectors, Latruffe (2010) points to several authors indicating that the

measurements of competitiveness have to be interpreted with care as they may be distorted by

policy measures. Latruffe therefore argues that that competitiveness research should give more

attention to potential effects of agricultural policies and should investigate whether government

funds used to protect a country’s agriculture or agrifood sector and to support its competitiveness

could generate greater social welfare if they were used differently, either in other policies or in

other sectors of the economy. For instance, public investments in innovation, education or

infrastructure, or tax or labour policies may be more effective in enhancing competitiveness of the

agrifood sector than price support to the sector.

The previously presented considerations on the complexity of the concept of competitiveness would indeed suggest that it is impossible to define competitiveness. Still, we try and use a definition that combines several of the aspects mentioned above in the following: “Competitiveness of the agrifood (sub)sector in a CIS country is the sustained ability of that (sub)sector to achieve profitable gain and market share in domestic and export markets in which the industry is active, benchmarked against agrifood (sub)sectors in EU countries and over a period 2004-2012.” The wording “sustained ability” includes aspects of (ex-post) competitive performance as well as future potential, hence of what can be given the factor resources available and technology (investments) to use them efficiently. We will argue below that by applying Porter’s approach, we will capture these aspects. These aspects are also nicely structured in the framework developed by Buckley et al. (1988) and we will show how these two approaches are related in Chapter 4.

2.2 Porter’s models

Michael Porter, specialist in business strategy and industrial economics, developed several frameworks to analyse competitiveness. The industry and the firm are the principle units of analysis in his earlier work, and the nation plays a larger role in his later publications. In his book Competitive Strategy

12

(1980a) Porter analyses the competitiveness of an industry and develops a theoretical framework in which five forces are recognised as defining the nature and degree of competition in an industry. This approach constitutes an analytical framework to understand industries and competitors. Later on, in Competitive Advantage (1985) Porter focuses on competition of firms. In this book he introduces the concept of a value chain and elaborates principles of corporate competitive advantage based on the concepts of cost advantage, product differentiation and technology. Finally, in his book The Competitive Advantage of Nations, Porter’s focus is on national competitive advantage (Porter, 1990). In this book, he explains why some nations achieve disproportionate worldwide success in particular industries; apparently some national environments seem more stimulating to advancement and progress than others. Porter claims that, basically, four factors determine the competitive strength of a nation’s particular industry. The graphical arrangement of these factors as four points of a diamond gave the name to the model: Porter’s diamond. The diamond has been recognised as a breakthrough in the analysis of competitiveness (Tong-sŏng Cho, 2000). Porter’s key developed models are listed in Table 2.1.

Table 2.1 Porter’s main theories and approaches

Book Model Approach Level of analysis

Competitive Strategy (1980a)

Five forces framework

Five forces shape an industry structure. These determine industry attractiveness and profitability

Industry

Competitive Advantage (1985)

Generic strategies

Three strategies for achieving sustainable competitive advantage: differentiation, cost leadership and focus

Firm

Value chain framework

The firm is divided into the discrete activities it performs. These value chain activities are the building blocks of competitive advantage

Firm

The Competitive Advantage of Nations (1990)

The diamond

Competitive advantage of nations are influenced by four attributes that shape the environment in which firms compete

Nation

In principle, both of Porter’s theoretical frameworks - the five forces and the diamond - would suit the present research because they permit to examine competitiveness of industries. However, Porter’s two theories differ in scope. The five forces (industry competitors, substitutes, potential entrants, suppliers and buyers) present a comprehensive framework to help a firm analyse its industry as a whole and forecast that industry’s future evolution, to understand its competitors and its own position, and to translate this analysis into a competitive firm strategy. This framework is used to assess how firms achieve superior profitability, how they can best position themselves in order to maintain competitive in the long run, and how to respond to rivals’ actions (Porter, 1980a). Porter’s framework of five forces, however, has received criticism. Grundy (2006), for instance, lists a number of drawbacks to the five forces framework, such as being (too) abstract and rigid, highly analytical and prescriptive. Moreover, Porter’s framework does not stipulate a methodology for measuring competitiveness; it is qualitative rather than quantitative, which would imply a need for further thinking how to effectively operationalise the framework. A more operationalised framework would be very useful for firms to assess their position in an industry. However, we also need a broader focus, as we want to examine the world market and government policies as the arena in which agrifood sectors compete.

The diamond model has this broader view. The diamond model examines industries as well, but at the same time defines four broad attributes of a nation that shape the environment in which industries compete and that promote or impede the creation of their competitive advantage. The framework allows the assessment of why some companies based in some nations innovate more than others, and why some nations’ environments enable companies to improve and innovate faster than foreign rivals (Porter, 1990). As Grundy (2006) summarises: the diamond works on a macro level while the five forces framework is formulated in microeconomic language. For our purposes, the diamond model is better suited as an analytical framework for assessing the competitive positions of food industries among competing countries.

13

2.3 Porter’s diamond approach and operationalisation

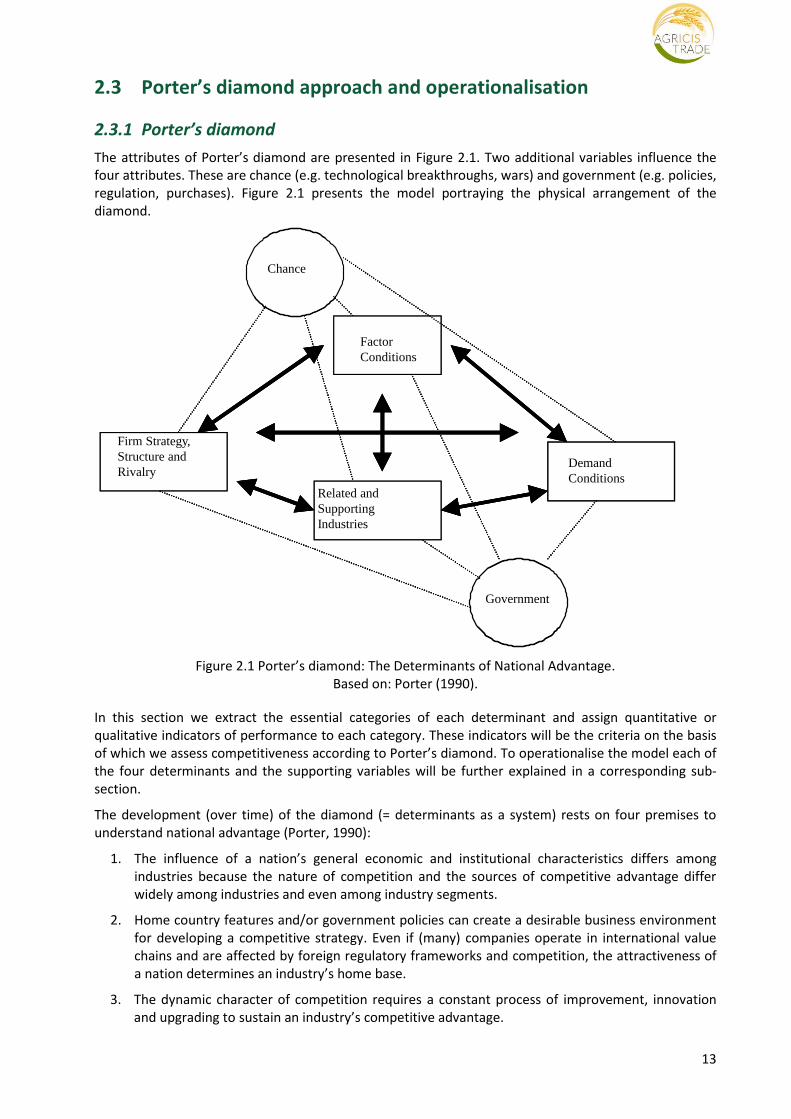

2.3.1 Porter’s diamond

The attributes of Porter’s diamond are presented in Figure 2.1. Two additional variables influence the four attributes. These are chance (e.g. technological breakthroughs, wars) and government (e.g. policies, regulation, purchases). Figure 2.1 presents the model portraying the physical arrangement of the diamond.

Figure 2.1 Porter’s diamond: The Determinants of National Advantage. Based on: Porter (1990).

In this section we extract the essential categories of each determinant and assign quantitative or qualitative indicators of performance to each category. These indicators will be the criteria on the basis of which we assess competitiveness according to Porter’s diamond. To operationalise the model each of the four determinants and the supporting variables will be further explained in a corresponding sub-section.

The development (over time) of the diamond (= determinants as a system) rests on four premises to understand national advantage (Porter, 1990):

1. The influence of a nation’s general economic and institutional characteristics differs among industries because the nature of competition and the sources of competitive advantage differ widely among industries and even among industry segments.

2. Home country features and/or government policies can create a desirable business environment for developing a competitive strategy. Even if (many) companies operate in international value chains and are affected by foreign regulatory frameworks and competition, the attractiveness of a nation determines an industry’s home base.

3. The dynamic character of competition requires a constant process of improvement, innovation and upgrading to sustain an industry’s competitive advantage.

binnenlandse

vraag

aanbod

netwerk

bedrijvenstructuur

en strategie

kansen

overheid

Demand

Conditions

Factor

Conditions

Related and

Supporting

Industries

Firm Strategy,

Structure and

Rivalry

Chance

Government

14

4. Firms with an international competitive advantage are often those that innovate and/or invest in market opportunities.

In next subsections we will use the following terminology:

1. Determinants are the four attributes of Porters’ diamond as well as the two additional variables. 2. Categories are elements of the determinants. 3. Sub-categories are more detailed categories, at which level indicators of performance are assigned. 4. Indicators are metrics of these (sub-)categories.

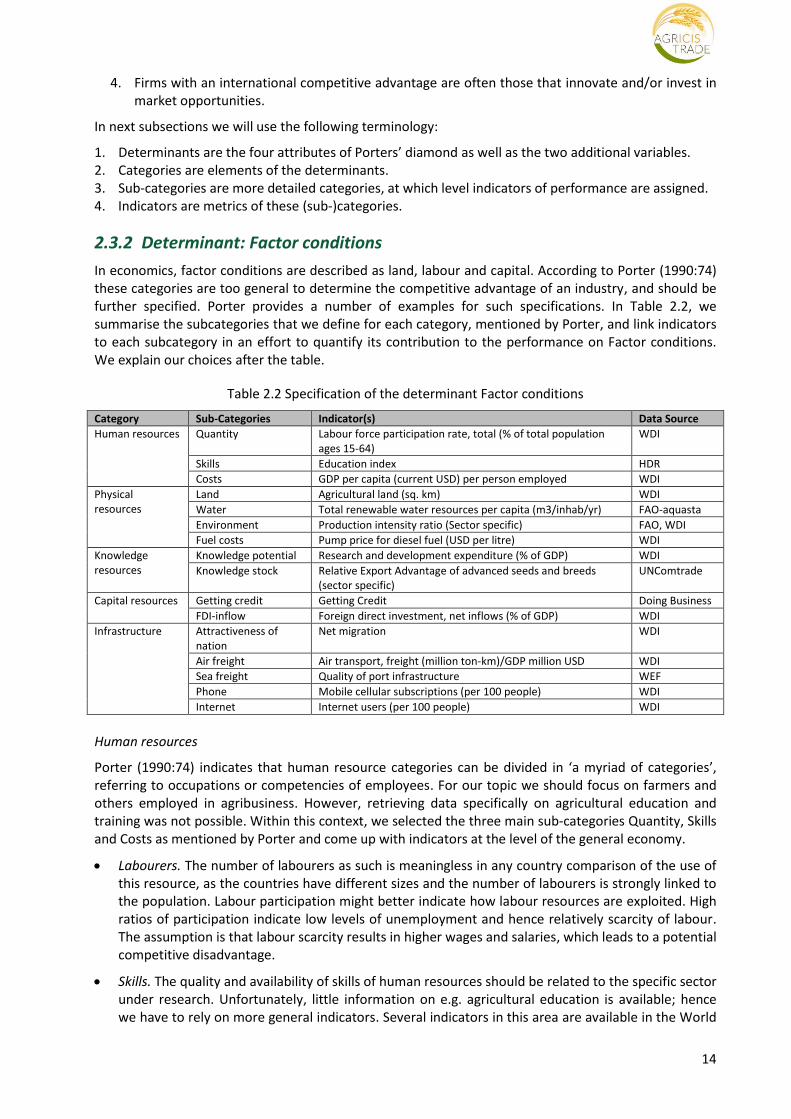

2.3.2 Determinant: Factor conditions

In economics, factor conditions are described as land, labour and capital. According to Porter (1990:74) these categories are too general to determine the competitive advantage of an industry, and should be further specified. Porter provides a number of examples for such specifications. In Table 2.2, we summarise the subcategories that we define for each category, mentioned by Porter, and link indicators to each subcategory in an effort to quantify its contribution to the performance on Factor conditions. We explain our choices after the table.

Table 2.2 Specification of the determinant Factor conditions

Category Sub-Categories Indicator(s) Data Source

Human resources Quantity Labour force participation rate, total (% of total population ages 15-64)

WDI

Skills Education index HDR

Costs GDP per capita (current USD) per person employed WDI

Physical resources

Land Agricultural land (sq. km) WDI

Water Total renewable water resources per capita (m3/inhab/yr) FAO-aquasta

Environment Production intensity ratio (Sector specific) FAO, WDI

Fuel costs Pump price for diesel fuel (USD per litre) WDI

Knowledge resources

Knowledge potential Research and development expenditure (% of GDP) WDI

Knowledge stock Relative Export Advantage of advanced seeds and breeds (sector specific)

UNComtrade

Capital resources Getting credit Getting Credit Doing Business

FDI-inflow Foreign direct investment, net inflows (% of GDP) WDI

Infrastructure Attractiveness of nation

Net migration WDI

Air freight Air transport, freight (million ton-km)/GDP million USD WDI

Sea freight Quality of port infrastructure WEF

Phone Mobile cellular subscriptions (per 100 people) WDI

Internet Internet users (per 100 people) WDI

Human resources

Porter (1990:74) indicates that human resource categories can be divided in ‘a myriad of categories’, referring to occupations or competencies of employees. For our topic we should focus on farmers and others employed in agribusiness. However, retrieving data specifically on agricultural education and training was not possible. Within this context, we selected the three main sub-categories Quantity, Skills and Costs as mentioned by Porter and come up with indicators at the level of the general economy.

Labourers. The number of labourers as such is meaningless in any country comparison of the use of this resource, as the countries have different sizes and the number of labourers is strongly linked to the population. Labour participation might better indicate how labour resources are exploited. High ratios of participation indicate low levels of unemployment and hence relatively scarcity of labour. The assumption is that labour scarcity results in higher wages and salaries, which leads to a potential competitive disadvantage.

Skills. The quality and availability of skills of human resources should be related to the specific sector under research. Unfortunately, little information on e.g. agricultural education is available; hence we have to rely on more general indicators. Several indicators in this area are available in the World

15

Development Indicators (WDI) database of the World Bank, such as literacy or participation in primary education. To limit the number of indicators we will use the Education Index from the Human Development Report (HDR) that includes among others literacy, population with secondary education, gross enrolment ratio, trained teachers or education expenditures ((UNDP, 2014), p192). A high index indicates a high level of skills that contributes to a country’s competitive advantage.

Costs. Little specific information on factor costs is available, such as labour costs for agricultural workers. To include labour costs in our overview we use GDP per person employed as indicator. Generally, wages are linked to the gross domestic products. However, labour costs are the largest item of production costs in agribusiness. To be able to make comparisons between countries a proxy for wages used in this research is the GDP constant in 2,000 USD per person economically active. A high level of GDP/capita (as the interpretation of high wages) indicates a competitive disadvantage.

Physical resources

Physical resources refer to natural resources (agricultural land, water resources), climate but also to a nation’s location, geographical size and other physical traits. Abundance, quality, accessibility and costs determine a nations advantage (Porter (1990),p74).

Land. The availability of agricultural land is an inappropriate indicator for potential production, as quality should be included. However, there is little information on land quality in world covering databases. Therefore, we include the area of agricultural land as the indicator for the potential to increase production. A large agricultural area indicates a country’s competitive advantage in agrifood production. We did not chose countries’ total area surface as mountains, lakes, deserts or urban areas add little to agricultural production potential.

Water. Water availability affects agricultural production importantly: plant growth potentials are seriously limited in arid areas. Total annual renewable water resources per inhabitant measured by the FAO gives a measure of water availability in the country considering its size. A high index is a positive indicator of a country’s availability of renewable water resources, and hence of a competitive advantage in agriculture.

Environment. Favourable growing conditions depend on the requirements of the crops regarding days of sunshine, light intensity, humidity and temperatures. Effects of climate on agricultural production are influenced by several factors such as latitude, altitude, winds, distance from the sea and soil. To classify world’s climates there are several systems, from which the Köppen climate classification is popular (Peel et al., 2007). It is based on native vegetation as expression of the climate of the zone. The largest areas of the CIS countries (Belarus, Russia and Ukraine) as well a part of the EU (Central and East European countries, Scandinavian countries and Eastern part Germany) have a continental climate with warm to cool summers and cold winters. Other countries have mainly a temperate climate with warm and humid summers with mild winters. We will, however, not include a climate classification in our analyses, as the climatic features may not be distinguishing enough for the countries subject to our study. Moreover, the impact of climate can be mitigated by technology, as for instance the examples of Dutch vegetable and floriculture sector show where the ‘inhospitable climate’ resulted in upgrading the cultivation techniques in greenhouses, artificial heating and light.

To recognise the suitability of growing crops or animal husbandry we introduce a production specialisation ratio (table 2.3). The ratio is the harvested area (for crops) and/or stocks of animals per inhabitant. The ratio expresses a degree of specialisation, it recognises a country’s production abilities and is independent of the country or population size. Large ratios point at countries having favourable natural resources or at being able to adapt to unfavourable natural conditions, for instance through greenhouse production and/or irrigation works. The ratio also points to the ability of upgrading the natural resources from basic to advantage production factors as is shown by the abovementioned Dutch example.

16

Table 2.3 Production intensity ratio per sector

Sector Indicator*

Dairy Stocks of live cattle per inhabitant

Pork Stocks of live pigs per inhabitant Poultry Stocks of live chickens per inhabitant Cereals Area harvested cereals total+ (Total per inhabitant

Oilseeds Area harvested oil crops primary+ (Total) per inhabitant Wine Area harvested grapes per inhabitant Potatoes Area harvested potatoes per inhabitant Tomatoes Area harvested tomatoes per inhabitant Apples Area harvested apples per inhabitant

*Databases: FAOstat databases on production and WDI for inhabitants

Fuel costs. The availability of energy resources is important to agriculture as an major input for the logistics of its rather bulky and/differentiated (e.g. cold chain) products, for producing fertilizers and for energy for machinery either for land cultivation or husbandry. As indicator we use the price at the gasoline pump. Higher prices indicate a disadvantage. As a note we acknowledge the strong influence that government policies may have on energy prices (via taxes, subsidies), but assume that differences in the value of the indicator across countries are primarily caused by availability of energy as a natural resource in the country.

Knowledge resources

This category refers to a nation’s stock of scientific, technical and market knowledge on goods and services.

Knowledge potential. A suitable indicator for measuring the level of knowledge would be the Technology achievement index developed for the Human Development Report 2001. That index covers the creation of technology, diffusion of innovation and human skills (Desai et al., 2002). However, that index has not been updated since 1999, so we have to look for an alternative. Data on patents are available, but not on a global scale, nor for all EU and CIS countries subject to this study. Moreover, agribusiness-related patents are not always registered in a way it is clear that they are specifically related to the agribusiness sector. Furthermore, agricultural and food processing have relatively low levels of patents application (Lippoldt, 2015). For that reason, the share of expenditure on research and development in the GDP is taken as a measure of a country’s knowledge base and its potential: assuming that it also affects agrifood sectors. This indicator includes the input for knowledge development. High levels are considered to add to a country’s agrifood sector competitive advantage.

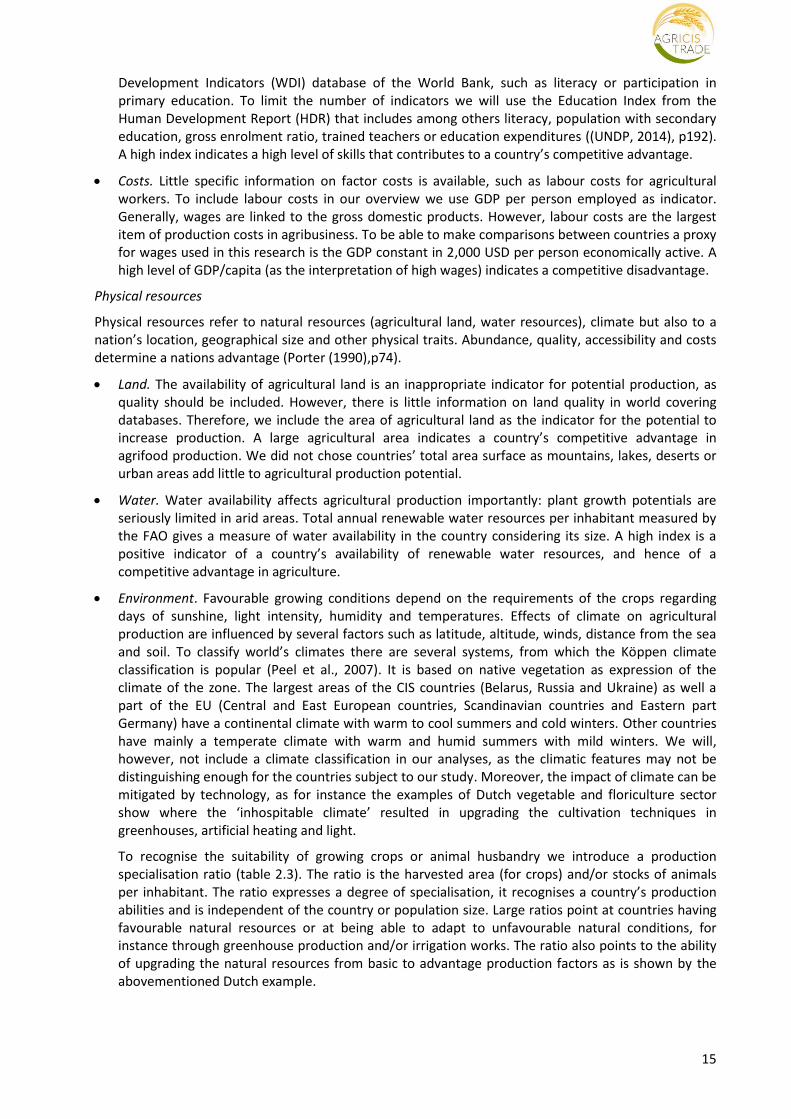

Advanced Knowledge stock. Not all factors contribute to competitive advantage in the same proportion; indicators should measure the performance of factors, according to its relative importance on competitive advantage. Porter distinguishes a hierarchy among factors as follows:

1. Basic versus advanced factors:

a. Basic factors include inhere factors of a country, like natural resources, climate and geographical location. They are important in the primary sector in general. They must be of sufficient quantity and quality to allow the creation of related advanced factors.

b. Advanced factors: are often build on basic factors and the result of large and often sustained investments in human and physical capital. Examples are differentiated products, proprietary production technology, and infrastructure.

2. Generalised versus specialized factors:

a. Generalised factors: can be deployed in a wide range of industries.

b. Specialised factors: factors with relevance to a limited range or to just a single industry like narrowly skilled personnel, infrastructure with specific properties, knowledge bases

17

in particular fields. They are scarce because they require focused and often risky private and social investment.

Figure 2.2 shows the interlinkage of basic/advantage factors versus generalised/specialised factors and its impact on a country’s competitive advantage.

Specialised Most significant and

sustainable competitive advantage

Generalised

Basic Advanced

Figure 2.2 Interlinkage of basic/advanced factors versus generalised/specialised factors (Based on Porter, 1990)

Important assets in agriculture are advanced seeds in crop production and advanced breeds in animal husbandry. These products are examples of embedded technology: knowledge that is being put in the development of a product: hence specialised and advanced. International trade statistics provide information on the exports and imports of such advanced inputs. We use export data, based on the Relative Export Advantage (RXA) indicator, as proxy for the availability of such knowledge (Table 2.4).

Table 2.4 Advanced Knowledge stocks, proxied by Relative Export Advantage

Sector Indicator: the export of HS codes available in UNcomtrade

Dairy 0102100 Cattle pure bred & 10221 Cattle: pure bred breeding animals

Pork 010310 Live swine: pure bred breed animals

Poultry 010511 Live fowls (gallus domestic) <185 gr. 040711 Fertilised eggs for incubations.

Cereals 120999 Seeds, nes (for Cereals & oilseeds)

Oilseeds 120999 Seeds, nes (for Cereals & oilseeds)

Wine -

Potatoes 070110 Seed potatoes

Tomatoes 120991 Vegetable seeds, used for sowing

Apples 060210 Unrooted cutting & 060220 Trees shrubs

Capital resources

Availability and costs of capital are of major importance as factors of production. We propose the following indicators to measure them:

The indicator ‘getting credit’ used by the World Bank in it’s Doing Business reports measures the legal rights of borrowers and lenders with respect to secured transactions and the sharing of credit information. The indicator measures whether certain features that facilitate lending exist within the applicable collateral and bankruptcy laws and the coverage, scope and accessibility of credit information ((World Bank, 2014), p125). The indicator provides the ranking of a country: one is the highest rank, hence the lower rank number the higher the competitive advantage.

Foreign Direct Investment (FDI). Attractiveness of a country can result in foreign direct investments which increase the capital resources of a country. Assuming that the capital inflow is not speculative in nature (‘hot money’), a high level of FDI indicates a strong competitiveness. The level of FDI depends, among others, on the size of economy; therefore we use the FDI as percentage of the GDP.

18

Infrastructure

Type, quality and cost of infrastructure affects competitiveness. Infrastructures includes transport systems, communication and mail systems as well cultural institutions that affect quality of life ((Porter, 1990) p.75).

For the quality of cultural institutions we use the net-migration index (published in the World Bank’s WDI) as a proxy to measure the attractiveness to live in a country and to assess the possibility of brain drain. The WDI net-migration index measures the difference between the number of persons leaving and entering a country during the year. A positive index means there is net immigration while negative figures mean there is net emigration. A high index is a positive indicator of a country’s attractiveness to live and to work, although a high positive net-migration does not signal a comparative advantage if it is the result of conflicts, e.g. the high levels of refugees in Turkey and Lebanon in 2015. Such emergency cases did not occur in the period and countries subject to this study.

World Bank’s WDI provides among others indicators for the performance of transport:

Air transport. For air transport, freight (million ton-km) will be used as a performance indicator instead of registered departure of carriers. The latter does not provided information on the quantity, where the former does. The indicator will take into account the size of the economy: we propose to use as indicator freight ton-km /GDP USD. The GDP expresses the level of economic activity of a country which we prefer above freight ton-km /inhabitants. A higher level is seen as being more competitive.

Seaport. For (sea-)port performance indicators several options are available such as container port traffic (performance indicator), Liner shipping connectivity index (based on among others number and size of vessels, number of service and companies) or the quality of port infrastructure assessed by the World Economic Forum (1=extremely underdeveloped to 7=well developed and efficient by international standards). The latter two show a strong correlation and for that reason only one will be selected. The first one - container port traffic - is correlated with the level of economic activity in the country. We prefer the quality of port infrastructure as this indicates the potential of the country and this data is available for most countries.

Roads. World Bank’s WDI used to but no longer provides information on paved roads. Hence we will not use that variable.

Communications infrastructure is related to ICT. We selected two indicators for which high(er) levels (compared to benchmark countries) indicate better competitiveness:

Mobile phones. Phones enable direct communication between people on a long distance. We selected the mobile cellular subscriptions per 100 people instead of fixed lines. The investments for cellular phones networks are lower and cellular phones are widely used as main phone connections.

Internet access. Internet access enables retrieving information (e.g. market prices, documentation) and written communication (e.g. contract) between people. For this purpose we use Internet users per 100 people.

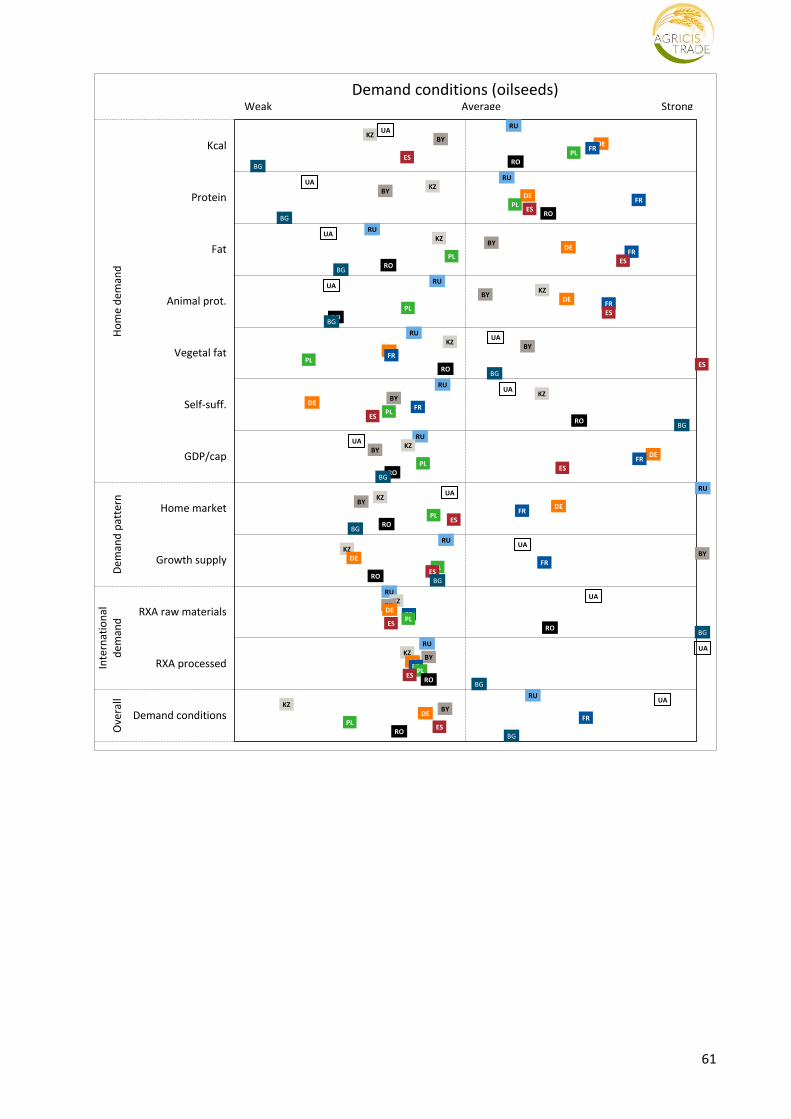

2.3.3 Determinant: Demand conditions

In Porter’s analytical framework (1990:86) home market demand conditions also play an important role in determining competitive advantage of a nation. Home market demand shapes how domestic firms perceive, interpret and respond to buyers’ preferences. The basic hypothesis is that domestic firms understand more quickly changes in these preferences due to cultural nearness of these buyers. Home market demand is also less prone to fluctuations such as those caused on external markets by exchange rate changes or trade policy changes in destination countries. This provides a more dependable base and can reduce risk, thus fostering investment We will discuss below the categories and subcategories Porter distinguishes within this determinant and which indicators can be used to measure the agribusiness’ responsiveness to home market demand developments. However, quantifying indicators

19

of the categories and subcategories that Porter enumerates requires detailed information that is not always easily available in databases covering all countries in the world. Home demand composition

Segment structure of demand. The demand for particular food varieties segments markets. In agribusiness, a wide range of differentiated products can be distinguished. For example, consumers can buy potatoes fresh in bulk, fresh washed and bagged, processed in French fries or in chips, part of ready-to-eat meal or in other forms when eating out-of-home. Detailed information on how much of each differentiated product consumers demand is not available in global databases. The hypothesis is that consumers with high incomes demand quality and differentiated products in line with the pyramid of Maslow's hierarchy of needs. Consumers want products that satisfy basic needs but also contribute to self-actualization and self-fulfilment needs. Indicators that serve our purpose of measuring demand segmentation are derived from FAOstat’s food supply balances. These indicators are levels of protein consumption from animal origin (which are seen as higher valued products), and fat consumption (in many processed and ready-to eat food products, fat is an essential ingredient for sensory and taste aspects of the food). Furthermore, the consumption of vegetable fats are increasing with increasing demand for differentiated products e.g. low levels saturated fatty acids in vegetable oil compared to animal fats or cooking oils with specific tastes (olive oil, sesame oil).

Table 2.5 Specification of the determinant demand conditions

Category Subcategories Indicator(s) Data Source

Home demand composition

Segment structure of demand Food supply (kcal/capita/day)

FAOstat

Protein supply (g/capita/day) FAOstat

Fat supply (g/capita/day) FAOstat

Share animal protein (%) FAOstat

Share vegetable fat (%) FAOstat

Sophisticated and demanding buyers Self-sufficiency (Production/domestic consumption)

FAOstat

GDP/capita WDI

Anticipatory buyer needs None

Demand size and pattern of growth

Size of the home market Population size WDI

Number of independent buyers None

Rate of growth of home demand Annual growth domestic supply (% over 10 years)

Table 2.6

Early home demand None -

Early saturation None -

Internationalisation of domestic demand

Mobile or multinational local buyers Relative Export Advantage (RXA) index Table 2.7

Influences on foreign needs Idem

Sophisticated and demanding buyers.

Porter argues that if domestic buyers are among the most demanding and sophisticated buyers, a nation will gain competitive advantage. At their home market domestic suppliers have a major advantage over foreign suppliers concerning anticipation of buyer needs and proximity to the actual buyer. Little or no public and standardised databases are available that measure these benefits, though. For this reason we use two proxies, one that indicates to what extent domestic production covers domestic demand (self-sufficiency) and one that indicates the extent of sophistication (income per capita).

Self-sufficiency

The self-sufficiency ratio measures the relation between the domestic production and the demand and can serve as a proxy for serving domestic demand. A high(er) level of self-sufficiency (share of domestic demand covered by domestic production) indicates a high(er) performance in meeting the domestic consumer’s requirements. These requirements are not only quantity but also quality oriented. If the quality does not match with the consumer preferences, imports will occur. GDP/capita. GDP/capita works through its effects on the demand for complementary goods and services that go into processing

20

differentiated food products – richer and poorer people do not eat such different amounts of food, but they eat very different types of food. Where GDP/capita is high, people demand a lot of complementary goods and services along with their food, and the agrifood industry can accumulate expertise and experience in adding these goods and services (i.e. producing specialised processed products). Income per capita levels, therefore, could be a proxy for ‘sophisticated and demanding buyers’, and for that reason we include GDP/capita in our set. A higher level of GDP indicates demand for variety, quality and differentiated products. We expect that higher levels of GDP/capita will contribute to exploit competitive advantages.

Anticipatory buyer needs.

Porter argues that a nation’s firms gain advantages if the needs of home buyers anticipate those of other nations, and domestic firms invest and create economies of scale advantages in production of new products or services that will become demanded elsewhere. Stringent home needs benefit competitive advantage only if they anticipate needs elsewhere. If they are idiosyncratic to the nation, they will undermine the competitive advantage of local firms. If home needs are slow to reflect new needs, a nation’s firms are at a disadvantage. A measurement of anticipatory buyer needs is very difficult to determine, a reason why we decided not to include this subcategory into our analyses.

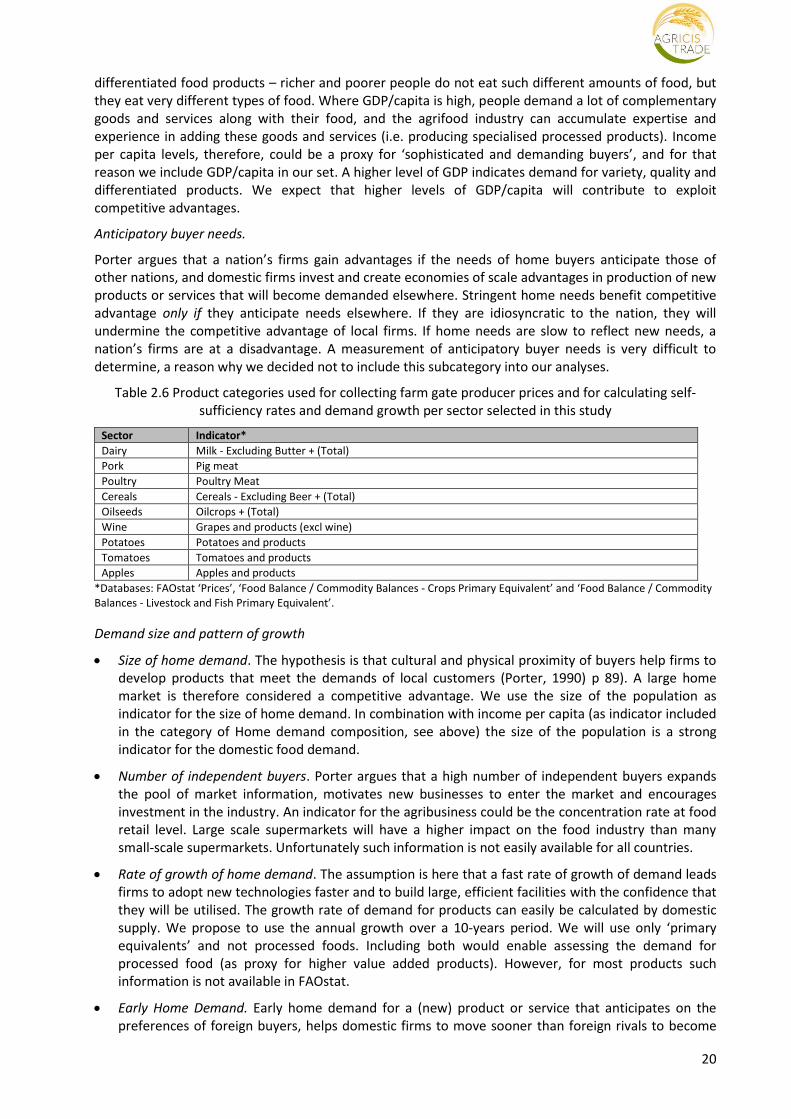

Table 2.6 Product categories used for collecting farm gate producer prices and for calculating self-sufficiency rates and demand growth per sector selected in this study

Sector Indicator*

Dairy Milk - Excluding Butter + (Total)

Pork Pig meat

Poultry Poultry Meat

Cereals Cereals - Excluding Beer + (Total)

Oilseeds Oilcrops + (Total)

Wine Grapes and products (excl wine)

Potatoes Potatoes and products

Tomatoes Tomatoes and products

Apples Apples and products

*Databases: FAOstat ‘Prices’, ‘Food Balance / Commodity Balances - Crops Primary Equivalent’ and ‘Food Balance / Commodity Balances - Livestock and Fish Primary Equivalent’.

Demand size and pattern of growth

Size of home demand. The hypothesis is that cultural and physical proximity of buyers help firms to develop products that meet the demands of local customers (Porter, 1990) p 89). A large home market is therefore considered a competitive advantage. We use the size of the population as indicator for the size of home demand. In combination with income per capita (as indicator included in the category of Home demand composition, see above) the size of the population is a strong indicator for the domestic food demand.

Number of independent buyers. Porter argues that a high number of independent buyers expands the pool of market information, motivates new businesses to enter the market and encourages investment in the industry. An indicator for the agribusiness could be the concentration rate at food retail level. Large scale supermarkets will have a higher impact on the food industry than many small-scale supermarkets. Unfortunately such information is not easily available for all countries.

Rate of growth of home demand. The assumption is here that a fast rate of growth of demand leads firms to adopt new technologies faster and to build large, efficient facilities with the confidence that they will be utilised. The growth rate of demand for products can easily be calculated by domestic supply. We propose to use the annual growth over a 10-years period. We will use only ‘primary equivalents’ and not processed foods. Including both would enable assessing the demand for processed food (as proxy for higher value added products). However, for most products such information is not available in FAOstat.

Early Home Demand. Early home demand for a (new) product or service that anticipates on the preferences of foreign buyers, helps domestic firms to move sooner than foreign rivals to become

21

established in an industry ((Porter, 1990), p95). As we could not find any information on innovative products, we will not include this subcategory.

Early saturation. Saturation forces local firms to continue innovating and upgrading. Saturation escalates local rivalry. It may also give a reason to export, especially when combined with growth of foreign markets. Early saturation is an advantage if home demand composition directs a nation’s firms to products and products features that are desired abroad. Again, no information in publicly available database has been found to measure ‘saturation’ meaningfully.

Internationalisation of domestic demand Mobile or multinational local buyers and Influences on foreign needs.

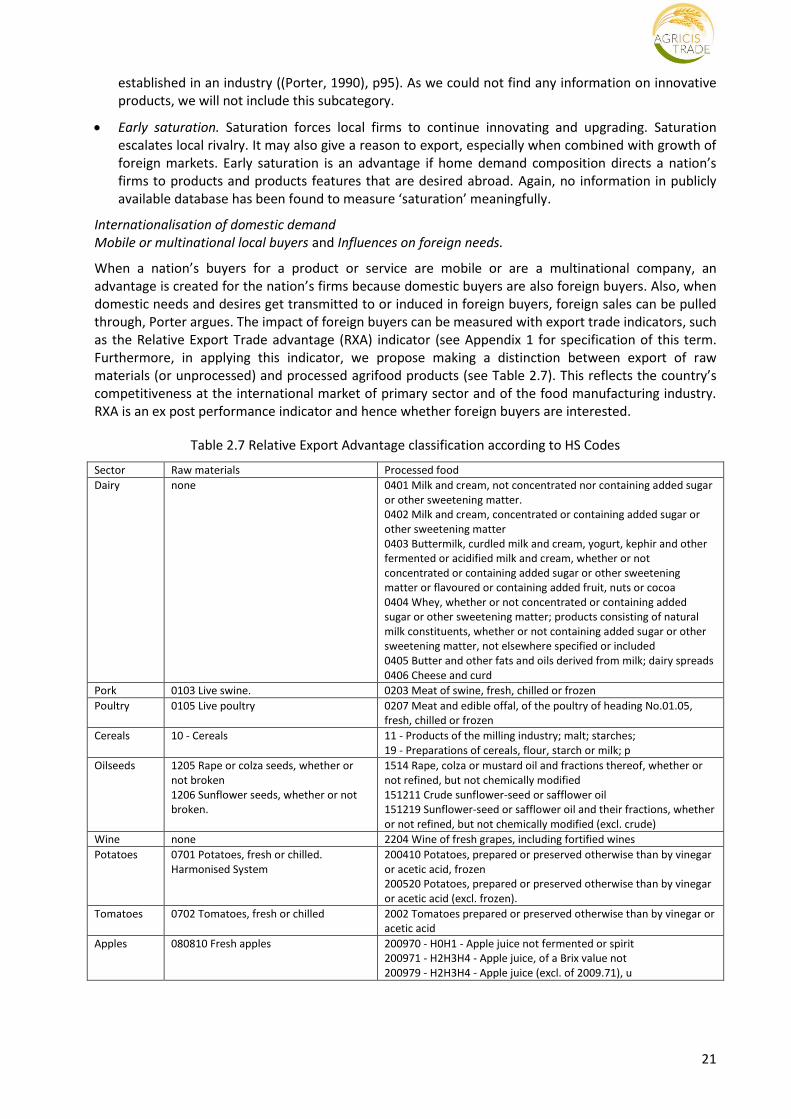

When a nation’s buyers for a product or service are mobile or are a multinational company, an advantage is created for the nation’s firms because domestic buyers are also foreign buyers. Also, when domestic needs and desires get transmitted to or induced in foreign buyers, foreign sales can be pulled through, Porter argues. The impact of foreign buyers can be measured with export trade indicators, such as the Relative Export Trade advantage (RXA) indicator (see Appendix 1 for specification of this term. Furthermore, in applying this indicator, we propose making a distinction between export of raw materials (or unprocessed) and processed agrifood products (see Table 2.7). This reflects the country’s competitiveness at the international market of primary sector and of the food manufacturing industry. RXA is an ex post performance indicator and hence whether foreign buyers are interested.

Table 2.7 Relative Export Advantage classification according to HS Codes

Sector Raw materials Processed food

Dairy none 0401 Milk and cream, not concentrated nor containing added sugar or other sweetening matter. 0402 Milk and cream, concentrated or containing added sugar or other sweetening matter 0403 Buttermilk, curdled milk and cream, yogurt, kephir and other fermented or acidified milk and cream, whether or not concentrated or containing added sugar or other sweetening matter or flavoured or containing added fruit, nuts or cocoa 0404 Whey, whether or not concentrated or containing added sugar or other sweetening matter; products consisting of natural milk constituents, whether or not containing added sugar or other sweetening matter, not elsewhere specified or included 0405 Butter and other fats and oils derived from milk; dairy spreads 0406 Cheese and curd

Pork 0103 Live swine. 0203 Meat of swine, fresh, chilled or frozen

Poultry 0105 Live poultry 0207 Meat and edible offal, of the poultry of heading No.01.05, fresh, chilled or frozen

Cereals 10 - Cereals 11 - Products of the milling industry; malt; starches; 19 - Preparations of cereals, flour, starch or milk; p

Oilseeds 1205 Rape or colza seeds, whether or not broken 1206 Sunflower seeds, whether or not broken.

1514 Rape, colza or mustard oil and fractions thereof, whether or not refined, but not chemically modified 151211 Crude sunflower-seed or safflower oil 151219 Sunflower-seed or safflower oil and their fractions, whether or not refined, but not chemically modified (excl. crude)

Wine none 2204 Wine of fresh grapes, including fortified wines

Potatoes 0701 Potatoes, fresh or chilled. Harmonised System

200410 Potatoes, prepared or preserved otherwise than by vinegar or acetic acid, frozen 200520 Potatoes, prepared or preserved otherwise than by vinegar or acetic acid (excl. frozen).

Tomatoes 0702 Tomatoes, fresh or chilled 2002 Tomatoes prepared or preserved otherwise than by vinegar or acetic acid

Apples 080810 Fresh apples 200970 - H0H1 - Apple juice not fermented or spirit 200971 - H2H3H4 - Apple juice, of a Brix value not 200979 - H2H3H4 - Apple juice (excl. of 2009.71), u

22

2.3.3 Determinant: Related and supporting industries

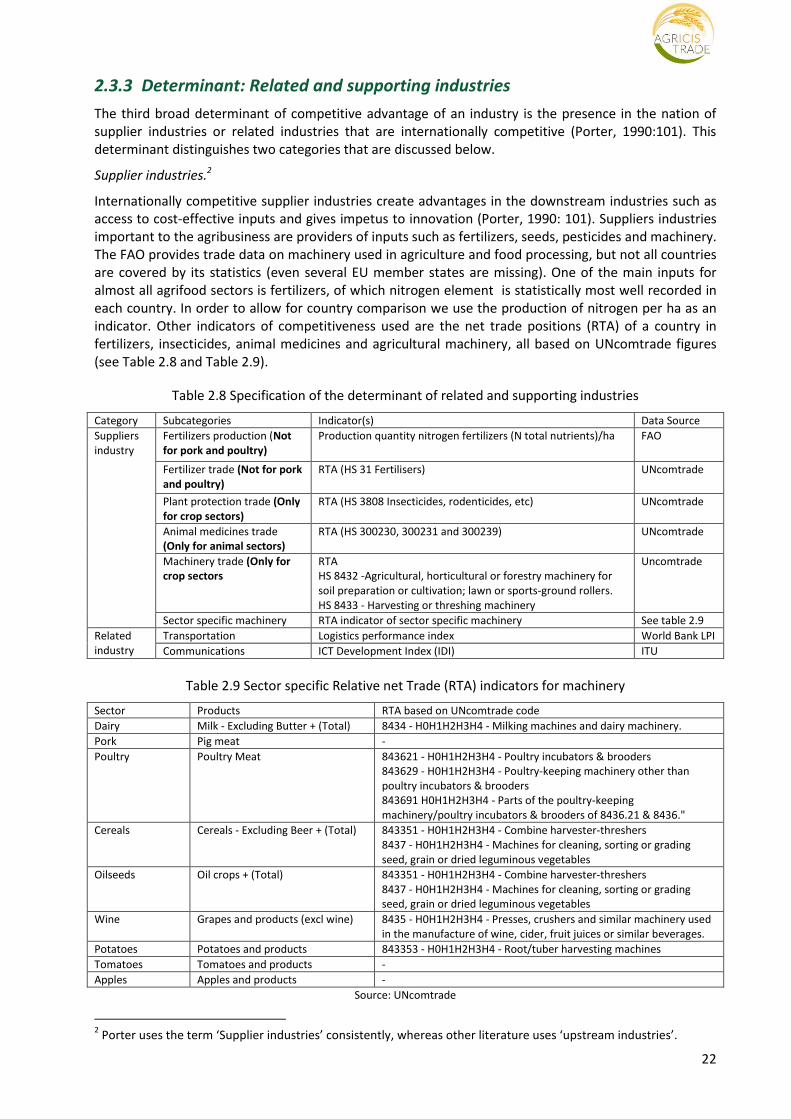

The third broad determinant of competitive advantage of an industry is the presence in the nation of supplier industries or related industries that are internationally competitive (Porter, 1990:101). This determinant distinguishes two categories that are discussed below.

Supplier industries.2

Internationally competitive supplier industries create advantages in the downstream industries such as access to cost-effective inputs and gives impetus to innovation (Porter, 1990: 101). Suppliers industries important to the agribusiness are providers of inputs such as fertilizers, seeds, pesticides and machinery. The FAO provides trade data on machinery used in agriculture and food processing, but not all countries are covered by its statistics (even several EU member states are missing). One of the main inputs for almost all agrifood sectors is fertilizers, of which nitrogen element is statistically most well recorded in each country. In order to allow for country comparison we use the production of nitrogen per ha as an indicator. Other indicators of competitiveness used are the net trade positions (RTA) of a country in fertilizers, insecticides, animal medicines and agricultural machinery, all based on UNcomtrade figures (see Table 2.8 and Table 2.9).

Table 2.8 Specification of the determinant of related and supporting industries

Category Subcategories Indicator(s) Data Source

Suppliers industry

Fertilizers production (Not for pork and poultry)

Production quantity nitrogen fertilizers (N total nutrients)/ha FAO

RTA HS 8432 -Agricultural, horticultural or forestry machinery for soil preparation or cultivation; lawn or sports-ground rollers. HS 8433 - Harvesting or threshing machinery

Uncomtrade

Sector specific machinery RTA indicator of sector specific machinery See table 2.9

Related industry

Transportation Logistics performance index World Bank LPI

Communications ICT Development Index (IDI) ITU

Table 2.9 Sector specific Relative net Trade (RTA) indicators for machinery

Poultry Poultry Meat 843621 - H0H1H2H3H4 - Poultry incubators & brooders 843629 - H0H1H2H3H4 - Poultry-keeping machinery other than poultry incubators & brooders 843691 H0H1H2H3H4 - Parts of the poultry-keeping machinery/poultry incubators & brooders of 8436.21 & 8436."

Cereals Cereals - Excluding Beer + (Total) 843351 - H0H1H2H3H4 - Combine harvester-threshers 8437 - H0H1H2H3H4 - Machines for cleaning, sorting or grading seed, grain or dried leguminous vegetables

Oilseeds Oil crops + (Total) 843351 - H0H1H2H3H4 - Combine harvester-threshers 8437 - H0H1H2H3H4 - Machines for cleaning, sorting or grading seed, grain or dried leguminous vegetables

Wine Grapes and products (excl wine) 8435 - H0H1H2H3H4 - Presses, crushers and similar machinery used in the manufacture of wine, cider, fruit juices or similar beverages.

2 Porter uses the term ‘Supplier industries’ consistently, whereas other literature uses ‘upstream industries’.

23

Related industries.

Related industries that are internationally competitive may strengthen the position of the agrifood sector when activities such as technology development, manufacturing, distribution and marketing are being shared or when there are opportunities to benefit from information flows (Porter, 1990:100). To some extent the topic of related industries is already included in the categories describing the factor conditions of a country, discussed above. Infrastructure and communications are discussed too, but pointing mainly at the physical existence of transport and communication systems. Here, in the vein of Porter’s argumentation, we add performance indicators that indicate institutional strengths of logistic and communicational aspects. Logistics is important for agricultural products that are bulky with a relative low value per tonne. Information and communication technology enhance the information transparency in the value chains such as price information. For that reason we include two indicators for this category:

• Logistics performance index (LPI). The index, compiled by the World Bank, is a benchmarking tool on trade logistics allowing for comparisons across 160 countries (LPI.worldbank.org). The score ranges between 1 (the lowest score, competitive disadvantage) and 5 (the highest score), and is a weighted average of the country scores on six dimensions, such as the

- efficiency of the clearance process (i.e., speed, simplicity and predictability of formalities) by border control agencies, including customs, the quality of trade and transport related infrastructure (e.g., ports, railroads, roads, information technology); and, the

- competence and quality of logistics services (e.g., transport operators, customs brokers);

In 2014, Ukraine ranked number 61 and highest among the CIS subject in this study. All EU member states had a higher LPI score than Ukraine (http://lpi.worldbank.org/international/global/2014)

• ICT Development Index (IDI) from the International Telecommunication Union. IDI is an overall indicator on the measurement of availability of ICT infrastructure and individual’s access to basic ICTs. Data are available for the CIS and EU countries ((ITU, 2014:95-101). A high index is a positive indicator of a country’s availability of ICT (competitive advantage). The index is based on 11 indicators grouped in 3 sub-indices: a) ICT infrastructure and access indicators; b) ICT use indicators and c) ICT skills indicators. The last one shows some overlap with the education index mentioned under the category human resources. The weighting of this ICT skills indicator is 20% in the IDI, compared to 40% each for the other 2.

The food retail sector is an important related sector to the food sector - in many cases it is considered as part of the food supply chain. Ideally some indicators of the development of the food retail sector should have been included in this analysis. However, the lack of consistent and comparable data, for instance on turnover, on this sector made inclusion of such an indicator not useful.

2.3.4 Determinant: Firm strategy, structure and rivalry

This fourth determinant addresses the context in which firms are ‘created, organised as well as the nature of domestic rivalry’ (Porter, 1990:107).The categories are:

Strategy and structure of domestic firms.

The national context of resource endowments and policy environment determines critically the way firms are managed and compete for production means and markets. Nations will tend to succeed in industries in which the management practices and modes of organization favoured by the national business environment are well suited to the industries’ sources of competitive advantage.

Distinctive management practices of the agribusiness are world-wide sparsely available and make assessment difficult. A wider assessment of country conditions for governance of firms is the Ease of

24

Doing Business ranking from The World Bank Group. This indicator measures the favourability of the business environment in a country to run a firm. The ranking benchmarks 181 countries on 10 topics i.e.: starting a business, dealing with construction permits, employing workers, registering property, getting credit, protecting investors, paying taxes, trading across borders, enforcing contracts and closing a business. Because a low ranking indicates a good business environment the indicator will have a negative sign.

Goals.

Nations will succeed in industries where their goals are aligned with the determinants of competitive advantage. Nations will succeed in industries where the goals of owners and managers match the needs of the industry. This factor requires an in-depth study on needs of the industry, goals of companies and of individuals, and alignment of all of them. Such an assessment is beyond the scope of this study and will not be included.

Table 2.10 Specification of the determinant firm strategy, structure and rivalry

Category Subcategories Indicator(s) Data Source

Strategy and structure of domestic firms

-

Ease of doing business World Bank, Doing business

Goals Company goals None

Goals of individuals None

The influence of national prestige/priority of goals

None

Importance of sustained commitment None

Domestic rivalry Domestic competition Price of products FAO (see Table 2.6 for definition of products

Productivity Yield per ha or animal FAO

New business formation Starting a business World Bank, Doing business

Geographic concentration Area of crops/agricultural land Heads of animals/agricultural land

FAO

Foreign suppliers Relative Net Trade Advantage index FAO, see Table 2.7

Domestic rivalry.

Rivalry sharpens advantages at home and stimulates domestic firms to sell abroad in order to grow. It creates pressure on firms to improve and innovate. It can also upgrade the competitive advantage of a nation’s firms by nullifying the advantages that come from only being in the nation.

Domestic competition results first in higher efficiency and lower prices. As indicator we use the price of the products mentioned in Table 2.6.

Productivity. Competition creates pressure to improve and to innovate. This results in a better performance for the industry. For example: the yield of tomatoes per ha indicates the technology used in the sector, such as around 5 kg/sqm is mainly open air production, between 9 and 20 in protected cultivation conditions and above 40 kg in high-tech greenhouses. For the agribusiness we will use yields as proxy for this (sub) category (e.g. yield per ha, milk production per cow). Unfortunately we have no indicator for poultry and pigs. The metrics would be the feed-conversion into meat.

New business formation means new competitors in the industry which will bring new approaches and will drive upgrading of competitive advantage. We use the indicator ‘Starting a business’, an element of the Doing business indicator to measure the ease to create a new business in a country. The main issues addressed for this indicator refer to the number of all procedures required to register a firm, the average time spent during each procedure, the official cost of each procedure, and the minimum capital required as a percentage of income per capita. Although part of the Ease of Doing Business indicator already used in ranking countries in the ‘strategy’

25

category, we use this specific indicator to highlight the importance of market entry possibilities for exploiting comparative advantage.

Geographic concentration. According to Porter (1990, p120), this category reflects and magnifies the power of domestic rivalry. An evaluation of the concentration ratio for regions where firms are located in each country is, however, unfeasible for the number of countries included in this research. We use as proxy the production intensity ratio: the relative importance of each agrifood sector on the total available agricultural land. The assumption is that higher ratios imply higher concentrations and create a competitive advantage. The ratios are evaluated against those of other countries.

Foreign competitors. Porter (1990) does not include foreign competition based on imports from other countries. If a country has a relatively high import level of some products, the domestic performance is considered weak. However, an intensive Intra Industry Trade may exist, based on specialisation or on the advantage to produce a differentiated product. To show this aspect of specialisation, we use the Relative Net Trade Advantage(RTA) indicator, of which a high number shows a strong competitiveness performance. The Grubel-Lloyd index (Grubel and Lloyd, 1971) has been considered as indicator, however this indicator is less suitable for this study as it based on trade between two specific countries, whereas our approach is based on benchmarking several countries.

2.3.5 The role of government

Government influences each of the four determinants above, with an either positive or negative effect on the competitive advantage. Governments shape the playing field for the business community by, for instance, changing the regulatory framework, providing subsidies or taxing activities. On the other hand, government policies might also by influenced by stakeholders that have an interest in changing the performance of a determinant of competitive advantage to their benefit (Porter, 1990:126-128). The latter may result, for instance, in agricultural policies that provide subsidies to inputs used or to exports, protect the domestic market by import tariffs, or reduce taxes to encourage investments in the agrifood sector. In this study we do not address these policies as separate factors affecting the competitive position of the CIS food sectors, but assume that the impacts of these policies are embodied in the performances measured by the indicators of each of the determinants of competitiveness. We will measure the impact of the government on competitive advantage by taking a broad and general scope of the government’s role on the economy by selecting a number of Worldwide Governance Indicators (WGIs), provide by World Bank (see Table 2.11).

Table 2.11 Specification of the determinant role of government

Category Subcategories Indicator(s) Data Source

The role of government - Voice and Accountability www.govindicators.org

- Political Stability and Absence of Violence

www.govindicators.org

- Government Effectiveness www.govindicators.org

- Regulatory Quality www.govindicators.org

- Rule of Law www.govindicators.org

- Control of Corruption www.govindicators.org

www.govindicators.org

World Bank’s Worldwide Governance Indicators measure six dimensions of governance for 212 countries. The dimensions measured are (info.worldbank.org):

• Voice and Accountability measures the extent to which citizens are free to select their government. Also measures freedom of expression, of association and of media.

• Political Stability and Absence of Violence measures the perceptions of likelihood of political stability.

• Government Effectiveness measures the quality of public and civil services, of policy formulation and implementation, their independence from political pressures and the commitment of government to these issues.

• Regulatory Quality measures government capacity to establish policies that promote private sector development.

• Rule of Law measures confidence and obedience to rules of society i.e. contract enforcement, police, and courts. It also measures likelihood of crime and violence.