70

DELIVERING CARE DELIVERING RESULTS Annual Report 2010

DELIVERINGCAREDELIVERINGREsults

Annual Report 2010

CoRpoRAtE pRofilE

Medical Facilities Corporation (“Medical Facilities” or “MFC”) owns majority interests

in four specialty surgical hospitals (“SSHs”) located in South Dakota and Oklahoma,

as well as a majority interest in one ambulatory surgery center (“ASC”) in California.

Medical Facilities’ SSHs focus on a limited number of high-volume, non-emergency

procedures, and diagnostic and imaging services, which are delivered on both an

inpatient and outpatient basis. The ASC is a specialized surgical center that performs

planned, non-emergency procedures on an outpatient basis.

The majority of free cash flows from operations of Medical Facilities is distributed

to holders of its Income Participating Securities (“IPSs” or “IPS units”) in the form

of interest and dividend on the subordinated debt and common share components,

respectively, of the IPS. The IPS units of the company are publicly traded on the

Toronto Stock Exchange under the symbol “DR.UN”.

Medical Facilities has a Distribution Reinvestment and Unit Purchase Plan, which

allows unitholders resident in Canada to automatically reinvest in a cost-effective

manner the monthly cash distributions on their IPS units in additional IPS units.

This Plan is administered by Computershare Investor Services Inc.

spECiAltY suRGiCAl HospitAls

Black Hills Surgical Hospital Rapid City, South Dakota

Dakota Plains Surgical Center Aberdeen, South Dakota

Oklahoma Spine Hospital Oklahoma City, Oklahoma

Sioux Falls Surgical Hospital Sioux Falls, South Dakota

AMBulAtoRY suRGERY CENtER

The Surgery Center of Newport Coast Newport Beach, California

Annual Report 2010

1

2010 — Year in Review

HIGHLIGHTS

• In a year marked by uncertainties created by healthcare reform, high

unemployment, and continued economic weakness, we recorded:

• Revenue of US$217.9 million, representing a four-year CAGR* of 10.1%

• Strong operating margin of 37.4%

• Robust cash generation, with cash available for distribution of

US$36.7 million, representing a four-year CAGR of 3.6%

• Comfortable payout ratio of 82.6%

• Completed organic expansions started in 2009 at our specialty surgical hospitals,

adding a total of 36 overnight stay rooms that increased our overnight stay

capacity by 55.4%

• Repurchased 107,200 units at an average price of C$9.24 per unit

• IPS unit price increased by 18.8% during the year to C$10.74 per unit

• Including distributions, our IPS units delivered a total return of 31.0% in 2010

FINANCIAL HIGHLIGHTS In US$ millions, unless otherwise noted

2010 2009 2008 2007 2006

Revenue $217.9 $207.4 $199.4 $168.8 $148.5

Operating income $81.4 $77.0 $80.7 $67.5 $60.1

Operating margin (%) 37.4% 37.1% 40.5% 40.0% 40.5%

Net income (loss) $(0.6) $(0.7) $19.6 $(17.6) $2.0

Cash available for distribution

$36.7 $33.1 $37.7 $34.2 $31.8

Cash available for distribution (C$ millions)

$37.8 $37.8 $40.2 $36.8 $36.0

Payout ratio 82.6% 82.6% 79.3% 84.6% 85.5%

Unit Price High (C$) Low (C$)

$11.11 $8.39

$9.12 $6.49

$11.99 $5.50

$12.85 $9.00

$12.00 $8.20

*Compound annual growth rate

Medical Facilities Corporation

2

It is with great pleasure that we report on our achievements in 2010. Despite a challenging

environment and weakness in the first two quarters of the year, we achieved the highest level of

revenue and operating income in our history. Our consolidated revenue for 2010 grew by 5.1% to

US$217.9 million and our consolidated operating income increased by 5.7% to US$81.4 million,

reflecting a strong increase in orthopedic and neurosurgical revenues. We saw both an increase

in the number of these cases and the average revenue generated by each case. As a result of

strong overall operations, our cash available for distribution increased by 10.7% in U.S.-dollar

terms, but was only in line with the previous year’s level in Canadian-dollar terms due to the

strength of the Canadian dollar.

This level of performance was made possible, at least in part, by our expansion projects which

began in 2009, which saw our overnight room capacity increase by 55.4% at our specialty

surgical hospitals. We have begun to see the positive impact of increased capacity in the form of

higher case volumes and an 11.0% increase in inpatient cases. We are pleased to have completed

these strategic projects in light of restrictions introduced with the Patient Protection and

Affordable Care Act (PPACA). This legislation prohibits future expansions of physician-owned

hospitals that treat Medicare patients. In addition, the legislation also prohibits these hospitals

from increasing the percentage owned by physicians. We would note, however, that while we

cannot increase this percentage, Medical Facilities can still add new physician-owners especially if

the economics are favorable to existing physician-owners. The status of the PPACA continues to

be uncertain given various judicial and legislative challenges facing it. Accordingly, it is impossible

to predict the impact, if any, that healthcare reform will have on the Medical Facilities’ operations.

As a result of the recession, over the past year, we have seen the percentage of services paid for

by governmental plans such as Medicare and Medicaid increase above historical norms. While

management expects this increased level of activity with the lower-paying governmental payors

to continue in the short term, we are especially pleased to observe favorable changes in our

payor mix in the fourth quarter, which, combined with impressive revenue growth during the

quarter, drove our operating margin up to 41.3%, the highest level in two years, and only slightly

below the level recorded in the fourth quarter of 2008. It is encouraging to see this improvement

in payor mix following two years during which we and many of our peers have reported

recession-induced reductions in the proportion of revenues coming from higher-reimbursing

non-governmental payors. However, it is also difficult to assess the sustainability of this recent

improvement, because although the U.S. economy has exhibited occasional positive signs on

certain economic indicators, many factors and events, both within the U.S. and globally, can

impact U.S. economic recovery.

Notwithstanding the general state of the U.S. economy, South Dakota and Oklahoma continue

to be among the states with lower unemployment and residential foreclosure rates, and provide

over 95% of Medical Facilities’ revenues. As for our California ASC, while the recession has

impacted the performance of Newport Coast, management is confident in the long-term outlook

for Newport Coast and the ambulatory surgery center (ASC) market in general.

Dear Unitholders,

Annual Report 2010

3

As we enter 2011, we expect to continue with the strategic initiatives we undertook in 2010 —

namely, cost control and physician recruitment. In addition, we are monitoring the market for

potential accretive acquisition opportunities while continuing to leverage our recent capacity

expansions to drive organic growth. Combined with growth in the areas serviced by our facilities,

we expect revenue to grow as case volumes increase and as case mix continues to shift to utilize

the expanded facilities at our SSHs and unused capacity at our ASC.

Over the longer term, our operating results will be affected by demographic and healthcare

spending trends. As the U.S. population increases and as the baby boomers continue to grow as

a proportion of total U.S. population over the next two decades, we expect that the demand for

healthcare services will also continue to increase.

Our balance sheet remains strong, giving us the financial flexibility to pursue strategic

opportunities as they arise, and to continue building value for our stakeholders. We are confident

that we will continue to produce cash available for distribution that is more than adequate to

continue paying the current level of distributions to our unitholders.

Sincerely,

Dr. Donald Schellpfeffer

Chief Executive Officer

TOTAL RETURN IN 2010

31.0%

Medical Facilities Corporation

4

HiGHlY EffiCiENt WoRK ENViRoNMENt

DEliVERiNG

MODERNBryan Den Hartog, M.D., orthopedic surgeonFoot and Ankle Specialist at Black Hills Surgical Hospital’s Orthopedic and Spine Center

Dr. Bryan Den Hartog joined Black Hills Surgical Hospital as a physician-owner in 1999,

after having previously worked in over a dozen hospitals. “It’s really the doctors that

run the hospital… administration is very responsive to our suggestions and to improving

quality of care, and the resulting efficiencies are staggering,” says Dr. Den Hartog, as he

highlights what differentiates Black Hills from other hospitals where he has practiced.

As a foot and ankle surgeon, his cases are higher-volume, shorter procedures. At Black

Hills, he can finish 10 to 12 cases a day and leave by 5:00 p.m. — more cases in less time

than a traditional hospital — due to the fast operating room turnaround time and a highly

skilled surgical team. Working at Black Hills has provided a significant balance in his life,

allowing him to spend quality time with family and pursue other interests. “This is as

perfect as I’ve seen it for hospital environments,” he adds.

CARE

Dr. Den Hartog and his sons were in Haiti as volunteers for Mission to Haiti when the devastating earthquake struck in January 2010. His team performed emergency surgical procedures on earthquake victims.

Annual Report 2010

5

World-class Surgical Teams in Leading-edge Facilities

At Medical Facilities, we recognize the importance of professionals who

provide high-quality care for our patients. Our facilities attract the best

surgeons and specialists in their respective areas of specialization because

of our focus on process efficiency and physician productivity. Our surgeons,

both owners and non-owners alike, are directly involved in establishing

operational processes and the resulting efficiencies. These efficiencies are

evident in our operating room turnaround time, which ranges between 5 and

22 minutes on average across our facilities, and in some cases, is almost

negligible as surgeons may be given two rooms in which to operate, allowing

them to move quickly from one procedure to another. Our surgeons are ably

supported by well-trained and highly skilled physician assistants (typically

employed by the surgeons in their practices) and nurses, whose value is

never overlooked. The support staff is a critical element of our success.

The objective of management of our facilities is to select the best nursing,

patient care, and support staff, provide continuous training, and foster a

collaborative, enthusiastic, team-oriented environment. This allows our

surgical teams to function harmoniously in providing quality care.

Donna Skinner, Chief Nursing Officer, Black Hills Surgical Hospital

“ We are successful not only because of our skilled

surgeons, but because of the very hardworking, dedicated,

caring, and professional staff throughout the hospital.

I am privileged to be a part of this organization.”

Medical Facilities Corporation

6

An Enhanced Care Environment

In addition to providing the highest quality treatment and care, we also

offer a superior patient experience comparable with the finest hospitality

service. Our focus is on our patients and the quality of their stay in our

hospitals. Fresh flowers, luxurious robes, digital media entertainment,

aromatherapy, specially catered meals, wireless internet access, and laptop

computers — these are just some of the amenities that are included in the

patient- and guest-friendly environment at our facilities as we deliver

a more personal approach to patient care. We strongly believe that

recovery is made easier by the presence of a patient’s family and friends.

Our hospitals have guest facilities to make their visits more comfortable

and allow them to spend more time with the patient.

First-rate surgical treatment, advanced medical equipment, enhanced patient care. We understand what our patients value.

Sioux Falls Surgical Hospital patient

“ I have used your hospital three times for different

surgeries in the last year — hip surgery, bladder surgery,

and now knee scope. There is nothing I can think of that

could be changed to make it better.”

Annual Report 2010

7

DEliVERiNG

EXCEPTIONAL

supERioR pAtiENt EXpERiENCE

REsults

Black Hills Surgical Hospital patient

“ I have never been to a more professional facility —

exceptional, first-class service from admissions

through to discharge.”

Medical Facilities Corporation

8

CARENECEssARyDEliVERiNG

A soCiAllY REspoNsiBlE EMploYER

Annual Report 2010

9

An Intrinsic Part of the Local Community

Our hospitals are integral and active members of the communities where

they are located. Aside from providing easy access to superior surgical

services to these communities, they also provide employment and training

to the best talent they can find, thereby helping support the local economy.

Our commitment to our locations is not limited to being employers in these

cities, but it extends to being active participants and sponsors of various

community programs. Black Hills is a major sponsor of the Wellspring

Stampede 10K, which benefits Wellspring Family-based Services. Additionally,

Black Hills sponsors clothing bins around the city to benefit the local rescue

mission. Oklahoma Spine has sponsored the Regional Food Bank, which

collects and distributes food to the needy in the Oklahoma City area, and the

Go Red for Women movement, which helps raise awareness of heart disease

among women. Furthermore, many Oklahoma Spine employees participate

in Hot Dogs for the Homeless, a weekly event where volunteers cook and

distribute hot dogs for homeless people in and around the city. Dakota Plains

offered free bone density testing at the Red Cross Community Fair. These are

just some examples of our hospitals’ involvement in their local communities.

Black Hills is a major sponsor of the Wellspring Stampede 10K,

which benefits Wellspring Family-based Services.

Medical Facilities Corporation

10

REsults

*Gross revenue represents total amounts billed to payors for reimbursement

DEliVERiNG

OPTIMAL

WoRKiNG WitH A BRoAD RANGE of pAYoRs

Our facilities have relationships with an extensive list of payors that represent

major payor groups, including private insurers, Medicare, Medicaid, and Workers’

Compensation. To remain competitive with traditional hospitals, our facilities work

with all of our patients’ healthcare providers and insurers. The goal of every payor is

to obtain the best possible treatment for their health plan members while minimizing

costs. Our objectives are aligned with those of payors, as our facilities and surgical

teams work towards providing best-in-class treatments for patients while operating

within the payors’ guidelines for reimbursement rates for services.

In 2010, private insurance and self-paying patients accounted for 66.7% of gross revenue, but represented 74.9% of net revenue.

18.4%

24.0%

24.3%

27.1%

3.4%

2.8%

Gross Revenue*

(%)

66.7% Other private insurance and self-pay

Workers’ compensation

Blue Cross/Blue Shield

Medicare

Dakotacare

Medicaid

15.0%

34.2%

25.8%

16.7%

6.2%

2.1%

Net Revenue

(%)

74.9% Other private insurance and self-pay

Workers’ compensation

Blue Cross/Blue Shield

Medicare

Dakotacare

Medicaid

Annual Report 2010

11

Healthcare Spending and Population Growth — Our Industry Drivers

0

1000

2000

3000

4000

5000

‘04 ‘05 ‘06 ‘07 ‘08 ‘09 ‘10 ‘11 ‘12 ‘13 ‘14 ‘15 ‘16 ‘17 ‘18 ‘19

National Health Expenditure projections* (us$ billions)

Source: U.S. Census Bureau,

National Population

Projections 2008

Source: Centers for Medicare & Medicaid Services, National

Health Expenditure Projections 2009-2019, September 2010

* 2009-2019 are projections

The U.S. population is expected to grow to 390 million in 2035 from 310 million now. The 45-and-over age group alone is expected to increase by 44 million during this period.

Demand for surgery increases for the higher age groups.

u.s. population projection Distribution (thousands)

0

100,000

200,000

300,000

400,000

500,000

‘10 ‘15 ‘20 ‘25 ‘30 ‘35 ‘40 ‘45 ‘50

65 yrs & over

45-64 yrs

25-44 yrs

18-24 yrs

Under 18

Our long-term operating results will be affected by demographic and healthcare

spending trends. As the U.S. population increases and as the baby boomers continue

to grow as a proportion of total U.S. population over the next two decades, it is

expected that the demand for healthcare services will continue to increase. In its

national population projections, the U.S. Census Bureau expects the over-65 age

group to grow from 13% of total population in 2010 to almost 20% of the population

by 2035. Combined with the 45-to-64 age group, the proportion of 45-and-over

population is expected to increase from 39% of the total population in 2010 to

42% in 2035.

The Centers for Medicare & Medicaid Services projects national health expenditures

to grow at an average annual rate of 6.3% from 2009 to 2019. This estimate, which

reflects the impact of the Patient Protection and Affordable Care Act enacted in

March 2010, is slightly higher than the pre-reform estimate of 6.1%.

Medical Facilities Corporation

12

Our SSHs are located in states that were less affected by the recession that gripped

the U.S. over the last few years. The unemployment rates in 2008 and 2009 in

South Dakota and Oklahoma were significantly lower than the national averages.

In addition, the 65-years-and-over age group represented a higher percentage

of the population compared with the national percentage.

SPeCIALTy SuRGICAL HOSPITALS

Name primary specialties

location size (‘000 sq.ft.)

licensed operating Rooms

licensed overnight Rooms

Black Hills Surgical Hospital Neurosurgery, Orthopaedics

Rapid City, SD 55 11 26

Dakota Plains Surgical Center Orthopaedics Aberdeen, SD 19 3 15

Oklahoma Spine Hospital Neurosurgery, Pain Management

Oklahoma City, OK 61 8 25

Sioux Falls Surgical Hospital Orthopaedics, E.N.T. Sioux Falls, SD 76 13 35

AMBuLATORy SuRGeRy CeNTeRS

Name primary specialties

location size (‘000 sq.ft.)

operating Rooms

overnight Rooms

The Surgery Center of Newport Coast Orthopaedics Newport Beach, CA 7 2 —

‘08 ‘09 ‘09

USA

SOUTHDAKOTA

OKLAHOMA

0

2

4

6

8

10

0

3

6

9

12

15

unemployment Rate (%) 65 & over (% of population)

Source: USDA Economic Research Service, U.S. Census

Bureau State & Country Quick Facts

Black Hills Surgical Hospital

Locations

Annual Report 2010

13

Management’s Discussion & Analysis 14

Management’s Responsibility for Financial Reporting 41

Auditors’ Report to the Shareholders 42

Consolidated Balance Sheets 44

Consolidated Statements of Income and Deficit 45

Consolidated Statements of Cash Flows 46

Notes to Consolidated Financial Statements 47

Corporate Information Inside Back Cover

Table of Contents

Medical Facilities Corporation

14

Management’s Discussion & Analysis Of Consolidated Financial Condition and Results of Operations

For the three-month and twelve-month periods ended December 31, 2010

March 17, 2011

The information in this Management’s Discussion and Analysis (“MD&A”) is supplemental to and should be read in conjunction with the consolidated financial statements of Medical Facilities Corporation (the “Corporation”) for the year ended December 31, 2010 and the notes thereto, which financial statements have been prepared in accordance with Canadian generally accepted accounting principles (“GAAP”). Substantially all of the Corporation’s operating cash flows are in U.S. dollars and all amounts presented in the financial statements and herein are stated in thousands of U.S. dollars, unless indicated otherwise.

This MD&A contains forward-looking statements (including, without limitation, in the section of this MD&A entitled “Outlook”). Such statements involve known and unknown risks, uncertainties and other factors outside of management's control that could cause actual results to differ materially from those described or anticipated in the forward-looking statements. Those risks include the risks identified in the section of this MD&A entitled “Risk Factors” (in particular in this regard, those identified under the subheading “Risks Related to the Business and the Industry of the Corporation”). The Corporation does not assume responsibility for the accuracy and completeness of these forward-looking statements and, except as may be required by law, does not undertake the obligation to publicly revise these forward-looking statements to reflect subsequent events or circumstances.

This discussion also makes reference to certain non-GAAP measures which assist in assessing the Corporation’s financial performance. Non-GAAP measures do not have any standard meaning prescribed by GAAP and are therefore unlikely to be comparable to similar measures presented by other issuers. Non-GAAP measures should not be considered as alternatives to comparable measures determined in accordance with GAAP as indicators of the Corporation’s financial performance, including its liquidity, cash flows and profitability. Reference should be made to the discussion under Section 2 “Non-GAAP Financial Measures – Standardized Distributable Cash and Cash Available for Distribution.”

Additional information about the Corporation and its Annual Information Form are available on SEDAR at www.sedar.com or the Corporation’s website at www.medicalfacilitiescorp.ca.

This MD&A is presented in the following sections:

1. Corporate Overview

2. Non-GAAP Financial Measures – Standardized Distributable Cash and Cash Available for Distribution

3. Condensed Consolidated Financial Highlights

4. Operating and Financial Results

5. Liquidity, Capital Resources and Financial Condition

6. Market Activities of the Corporation’s Securities

7. Financial Instruments

8. Related Party Transactions

9. Critical Accounting Estimates

10. Management’s Responsibility for Financial Reporting and Disclosure Controls

11. Risk Factors

12. Outlook

13. Supplementary Information

Annual Report 2010

15

1. CORPORATE OVERVIEW

The Corporation is a British Columbia corporation and is subject to corporate taxation in both Canada and the United

States. The capital of the Corporation is in the form of Income Participating Securities (“IPS”) units, convertible secured

debentures and other debt facilities at the corporate level. Each IPS unit represents: (a) Cdn$5.90 aggregate principal

amount of 12.5% subordinated notes payable of the Corporation and (b) one common share of the Corporation. In

December 2010, 10,000 IPS units separated into 10,000 common shares and $59,000 aggregate principal amount of

12.5% subordinated notes payable. For the purposes of this MD&A, the term “IPS unit” shall include the common shares

and subordinated notes that separated in December, 2010 and the term “IPS unitholders” shall include the holders of

common shares and subordinated notes payable that have separated.

The Corporation, through its wholly-owned U.S. subsidiary, owns majority interests in, and derives substantially all of its

income from, five limited liability entities (collectively the “Centers”), each of which owns either a specialty surgical

hospital (“SSH”) or an ambulatory surgery center (“ASC”). Three SSHs are located in South Dakota, one SSH is located in

Oklahoma and one ASC is located in California. On August 13, 2010, the holders of the minority interest in Barranca

Surgery Center, LLC (“Barranca”), a second ASC in California, redeemed the Corporation’s indirect 51% interest in

Barranca (see note 5 to the Corporation’s consolidated financial statements for the year ended December 31, 2010). ASCs

are specialized surgical centers that only provide outpatient procedures, whereas SSHs are licensed for both inpatient and

outpatient surgeries. The Centers provide facilities, including staff, surgical materials and supplies, and other support

necessary for scheduled surgical, pain management, imaging, and diagnostic procedures and derive their revenue

primarily from the fees charged for the use of these facilities. The Centers mainly focus on a limited number of clinical

specialties such as orthopaedic, neurosurgery, pain management and other non-emergency elective procedures.

Facility service revenue of the Centers (“facility service revenue”) for any given period is dependent on the volume of the

procedures performed as well as the acuity and complexity of the procedures (“case mix”) and composition of payors

(“payor mix”) as various payors have different reimbursement rates for the same type of procedures. The volume of

procedures performed at the Centers depends on (among other things): (i) the Centers’ ability to deliver high quality care

and superior services to patients and their family members; (ii) the Centers’ success in encouraging physicians to perform

procedures at the Centers through, among other things, maintenance of an efficient work environment for physicians as

well as availability of facilities; and (iii) established relationships with major third-party payors in the geographic areas

served. The case mix at each Center is a function of the clinical specialties of the physicians and medical staff and is also

dependent on the equipment and infrastructure at each Center.

Minority interests in the Centers are indirectly owned primarily by physicians practicing at the Centers. Upon acquisition

by the Corporation of the SSHs located in South Dakota and Oklahoma, the minority interest owners were granted the

right to exchange up to 14% of the ownership interest in their respective Centers for IPS units of the Corporation. The

minority interest owners of several Centers have exercised portions of their exchangeable interests. In April 2010,

pursuant to the terms of the exchange agreement between the Corporation and Oklahoma Spine Hospital, LLC, the

minority owners of Oklahoma Spine Hospital, LLC, exchanged 0.75% of the ownership in the Center for IPS units of the

Corporation. In connection with this transaction, the Corporation issued 64,443 IPS units.

As of December 31, 2010, the minority interests in the Centers were as follows:

Sioux Falls Surgical Hospital, LLP 49.0%

Dakota Plains Surgical Center, LLP 35.4%

Black Hills Surgical Hospital, LLP 45.8%

Oklahoma Spine Hospital, LLC 43.9%

The Surgery Center of Newport Coast, LLC 49.0%

Medical Facilities Corporation

16

Center Descriptions

Sioux Falls Surgical Hospital, LLP

Sioux Falls Surgical Hospital, LLP (“SFSH”), established in October 1985, is a multi-specialty surgical facility located in

Sioux Falls, South Dakota. SFSH performs orthopaedic, ear, nose and throat, urology, neurosurgery, gynecology, plastic,

gastrointestinal, pain management, general surgery and ophthalmology procedures. The SFSH service area includes Sioux

Falls and the communities east of Chamberlain, north of Yankton and south of Aberdeen in South Dakota, as well as

districts west of Worthington, Minnesota.

Dakota Plains Surgical Center, LLP

Dakota Plains Surgical Center, LLP (“DPSC”) is located in Aberdeen, South Dakota, and is attached to an orthopaedic clinic

that is the primary office of the orthopaedic physicians who account for 92% of the hospital's admissions. DPSC has been

operating as a licensed specialty hospital since 1998 and focuses primarily on orthopaedic procedures. The primary service

area for DPSC is the city of Aberdeen and surrounding townships.

Black Hills Surgical Hospital, LLP

Black Hills Surgical Hospital, LLP (“BHSH”) is located in Rapid City, South Dakota, and has been operating as a licensed

specialty hospital since January, 1997. BHSH is a multi-specialty surgical hospital, which focuses primarily on orthopaedic,

neurosurgical and pain management procedures. Other specialties include ear, nose and throat, general surgery,

gynecology, ophthalmology, podiatry and bariatric surgery. The BHSH service area includes western South Dakota, eastern

Wyoming, northwestern Nebraska and western North Dakota.

Oklahoma Spine Hospital, LLC

Oklahoma Spine Hospital, LLC (“OSH”) is located in Oklahoma City, Oklahoma, and has been operating as a licensed

specialty hospital since December 1999. OSH focuses on a limited number of clinical and surgical specialities, including

neurosurgery, pain management, orthopaedic surgery and podiatry. OSH’s primary service area extends beyond Oklahoma

City, a city with a metropolitan area of over one million people, into central and western Oklahoma. OSH is the only facility

in the Oklahoma City metropolitan area that focuses on the treatment of disorders of the spine.

The Surgery Center of Newport Coast, LLC

The Surgery Center of Newport Coast, LLC (“Newport Coast”) is located in Newport Beach, California. Newport Coast has

been operating since 2004 and is accredited by the AAAHC as a Medicare Deemed Multi-Specialty Facility. Newport Coast

focuses primarily on orthopaedic, gastroenterology, gynecology, cosmetic surgery and pain management procedures.

Table 1: Summary of Center information

SFSH DPSC BHSH OSH Newport Coast

Location Sioux Falls

SD Aberdeen

SD Rapid City

SD Oklahoma City

OK Newport Beach

CA

Size 76,000 sq ft 19,000 sq ft 75,000 sq ft 61,000 sq ft 7,000 sq ft

Operating Rooms 13 3 11 7 2

Overnight Rooms 35 15 26 25 -

Annual Report 2010

17

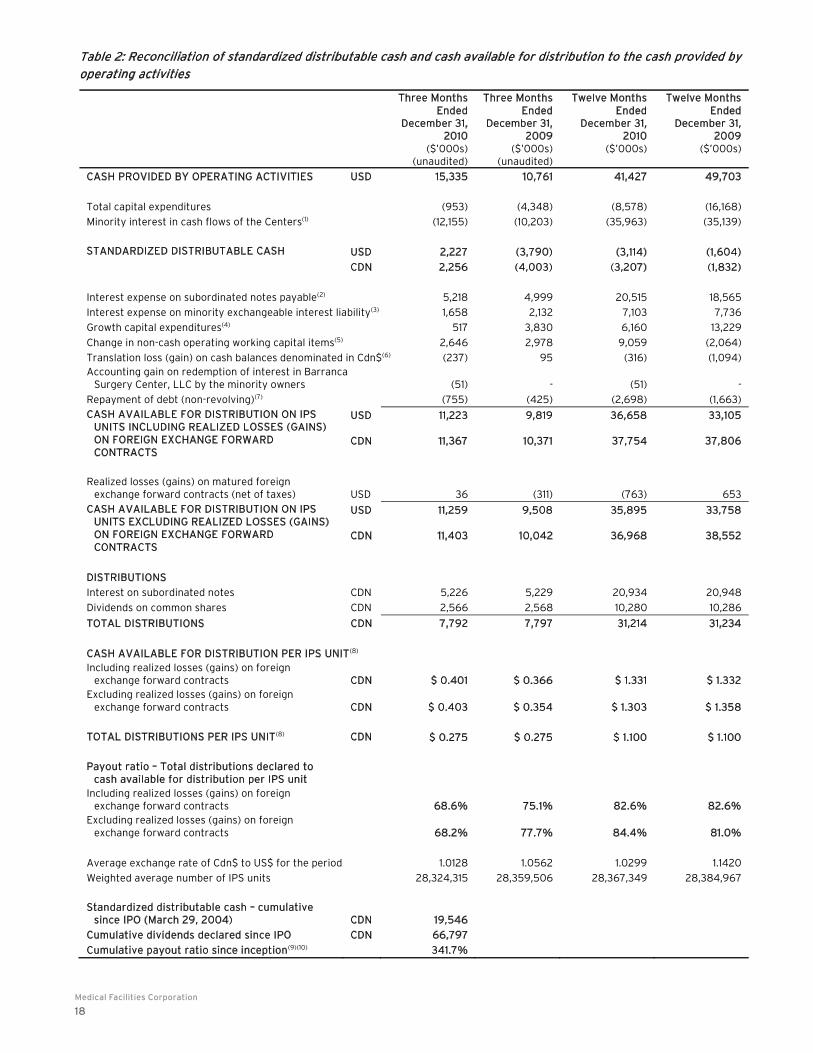

2. NON-GAAP FINANCIAL MEASURES – STANDARDIZED DISTRIBUTABLE CASH AND CASH AVAILABLE FOR DISTRIBUTION

The following is a discussion of two distinct non-GAAP measures: standardized distributable cash and cash available for

distribution.

Standardized Distributable Cash

Standardized distributable cash is a non-GAAP measure, defined in the Canadian Institute of Chartered Accountants

(“CICA”) 2007 interpretive release regarding standardized distributable cash, but it does not have any standardized

meaning within GAAP. While it is intended to provide a consistent and comparable measurement of distributable cash

across entities, standardized distributable cash as presented by the Corporation is unlikely to be comparable to similar

measures presented by other issuers. This measure is applicable primarily to income trusts. While the Corporation

distributes a significant portion of its cash available for distribution on a monthly basis, Medical Facilities Corporation is a

corporation and is not an income trust and some of the recommendations of the CICA’s interpretive release would not be

meaningful when applied to it. Therefore, certain recommendations have not been applied in determining the standardized

distributable cash and related ratios in the accompanying table (see Notes 2 and 9 to Table 2).

According to the CICA’s interpretive release, “standardized distributable cash is defined as the GAAP measure of cash

provided by operating activities after adjusting for capital expenditures, restrictions on distributions arising from

compliance with financial covenants restrictive at the time of reporting, and minority interests.” There are no restrictions

on distributions of the Corporation arising from its financial covenants as at December 31, 2010. Therefore, no adjustment

is made in respect of such restrictions in the calculation of standardized distributable cash.

Cash Available for Distribution

The Corporation distributes the majority of its free cash flows from operations to holders of its IPS units, taking into

account the anticipated working capital and liquidity needs of the Corporation, with a portion of such distributions being

interest payments on its subordinated notes and a portion being dividends on its common shares. The Corporation

believes that cash available for distribution on its IPS units provides a useful measure for evaluation of the Corporation’s

performance as it outlines the net cash flow generated by the Corporation, which is available for distribution in the period.

In particular, the Corporation believes that investors should be able to ascertain the extent to which the distributions are

funded by operations, as discussed below.

Cash available for distribution is a non-GAAP financial measure, does not have any standardized meaning prescribed by

GAAP and is therefore unlikely to be comparable to similar measures presented by other issuers. It is not intended to be

representative of cash flow or results of operations determined in accordance with GAAP. Table 2 below presents the

reconciliation of cash available for distribution to the cash provided by operating activities. The Corporation’s primary

source of cash for distribution is the Centers’ operating activities. Deficiencies arising from short-term working capital

requirements and capital expenditures may be financed with bank indebtedness. Investors are cautioned that cash

available for distribution, as calculated by the Corporation, may not be comparable to similar measures used by other

issuers.

Medical Facilities Corporation

18

Table 2: Reconciliation of standardized distributable cash and cash available for distribution to the cash provided by operating activities

Three MonthsEnded

December 31,2010

($’000s)(unaudited)

Three MonthsEnded

December 31,2009

($’000s)(unaudited)

Twelve Months Ended

December 31, 2010

($’000s)

Twelve MonthsEnded

December 31,2009

($’000s)

CASH PROVIDED BY OPERATING ACTIVITIES USD 15,335 10,761 41,427 49,703

Total capital expenditures (953) (4,348) (8,578) (16,168)

Minority interest in cash flows of the Centers(1) (12,155) (10,203) (35,963) (35,139)

STANDARDIZED DISTRIBUTABLE CASH USD 2,227 (3,790) (3,114) (1,604)

CDN 2,256 (4,003) (3,207) (1,832)

Interest expense on subordinated notes payable(2) 5,218 4,999 20,515 18,565

Interest expense on minority exchangeable interest liability(3) 1,658 2,132 7,103 7,736

Growth capital expenditures(4) 517 3,830 6,160 13,229

Change in non-cash operating working capital items(5) 2,646 2,978 9,059 (2,064)

Translation loss (gain) on cash balances denominated in Cdn$(6) (237) 95 (316) (1,094) Accounting gain on redemption of interest in Barranca Surgery Center, LLC by the minority owners (51) - (51) -

Repayment of debt (non-revolving)(7) (755) (425) (2,698) (1,663)

CASH AVAILABLE FOR DISTRIBUTION ON IPS UNITS INCLUDING REALIZED LOSSES (GAINS) ON FOREIGN EXCHANGE FORWARD CONTRACTS

USD 11,223 9,819 36,658 33,105

CDN 11,367 10,371 37,754 37,806

Realized losses (gains) on matured foreign exchange forward contracts (net of taxes) USD 36 (311) (763) 653

CASH AVAILABLE FOR DISTRIBUTION ON IPS UNITS EXCLUDING REALIZED LOSSES (GAINS) ON FOREIGN EXCHANGE FORWARD CONTRACTS

USD 11,259 9,508 35,895 33,758

CDN 11,403 10,042 36,968 38,552

DISTRIBUTIONS

Interest on subordinated notes CDN 5,226 5,229 20,934 20,948

Dividends on common shares CDN 2,566 2,568 10,280 10,286

TOTAL DISTRIBUTIONS CDN 7,792 7,797 31,214 31,234

CASH AVAILABLE FOR DISTRIBUTION PER IPS UNIT(8) Including realized losses (gains) on foreign exchange forward contracts CDN $ 0.401 $ 0.366 $ 1.331 $ 1.332 Excluding realized losses (gains) on foreign exchange forward contracts CDN $ 0.403 $ 0.354 $ 1.303 $ 1.358 TOTAL DISTRIBUTIONS PER IPS UNIT(8) CDN $ 0.275 $ 0.275 $ 1.100 $ 1.100

Payout ratio – Total distributions declared to cash available for distribution per IPS unit Including realized losses (gains) on foreign exchange forward contracts 68.6% 75.1% 82.6% 82.6% Excluding realized losses (gains) on foreign exchange forward contracts 68.2% 77.7% 84.4% 81.0%

Average exchange rate of Cdn$ to US$ for the period 1.0128 1.0562 1.0299 1.1420

Weighted average number of IPS units 28,324,315 28,359,506 28,367,349 28,384,967

Standardized distributable cash – cumulative since IPO (March 29, 2004) CDN 19,546

Cumulative dividends declared since IPO CDN 66,797

Cumulative payout ratio since inception(9)(10) 341.7%

Annual Report 2010

19

Note 1: Minority interest in the cash flows of the Centers is deducted in determining standardized distributable cash as distributions from

the Centers to the minority interest holders are required to be made concurrently with distributions from the Centers to the Corporation.

Note 2: Interest expense on the subordinated notes payable is deducted in the determination of net income and cash provided by

operating activities and is added back to determine cash available for distribution as the subordinated notes payable are a component of

the IPS units.

Note 3: Interest expense attributable to the minority exchangeable interest liability represents a notional amount of interest expense

deducted in the determination of net income. It is added back to determine cash available for distribution as it is a non-cash charge and is

not distributable to the holders of the minority interest.

Note 4: Growth capital expenditures relate to the acquisition of capital assets to increase the productive capacity of the Centers beyond

maintaining existing productive capacity. Growth capital expenditures are financed by the Centers through long-term financing

arrangements and the use of general funds. Growth capital expenditures are added back in the determination of cash available for

distribution and the payments associated with these financing arrangements are deducted (see Note 7 below).

Note 5: While changes in non-cash operating working capital are included in the calculation of the cash provided by operating activities

and standardized distributable cash, they are not included in the calculation of the cash available for distribution as they represent only

temporary sources or uses of cash due to the differences in timing of recording facility service revenue and corresponding expenses and

actual receipts and outlays of cash. Such changes in the non-cash operating working capital are financed from the available cash or credit

facilities of the Centers.

Note 6: Unrealized losses (gains) on the translation into US$ of cash balances denominated in Cdn$ are adjusted in the determination of

cash available for distribution as such losses (gains) do not affect the amount of cash available for distribution in Cdn$.

Note 7: Repayment of non-revolving debt at the Centers’ level reflects contractual obligations of the Centers and is deducted in the

calculation of cash available for distribution.

Note 8: Calculated based on the weighted average number of IPS units outstanding.

Note 9: Interest on the subordinated debt portion of IPS units is deducted in the calculation of the cash provided by operating activities

and standardized distributable cash and, therefore, only dividends on the common share portion of IPS units are included in the

calculation of this ratio.

Note 10: The payout ratio of cumulative dividends declared since the IPO to the cumulative standardized distributable cash since IPO

exceeds the ratio of distributions declared to cash available for distribution due to the fact that the standardized cash includes growth

capital expenditures, interest on subordinated notes payable and changes in non-cash operating working capital, while these items are

adjusted in determining the amount of cash available for distribution.

In the three-month period ended December 31, 2010, the Corporation generated cash available for distribution including

realized losses (gains) on foreign exchange forward contracts of Cdn$11.4 million, which exceeded distributions of

Cdn$7.8 million declared in respect of this period by Cdn$3.6 million. On a per IPS unit basis, cash available for distribution

including realized losses (gains) on foreign exchange forward contracts of Cdn$0.401 was Cdn$0.126 or 45.8% higher than

distributions declared of Cdn$0.275, resulting in a payout ratio of 68.6% compared to 75.1% in the same period in 2009.

In the twelve-month period ended December 31, 2010, the Corporation generated cash available for distribution including

realized losses (gains) on foreign exchange forward contracts of Cdn$37.8 million, which exceeded distributions of

Cdn$31.2 million declared in respect of this period by Cdn$6.6 million. On a per IPS unit basis, cash available for

distribution including realized losses (gains) on foreign exchange forward contracts of Cdn$1.331 was Cdn$0.231 or 21.0%

higher than distributions declared of Cdn$1.100, resulting in a payout ratio of 82.6%, which was consistent with the payout

ratio in the same period last year.

Medical Facilities Corporation

20

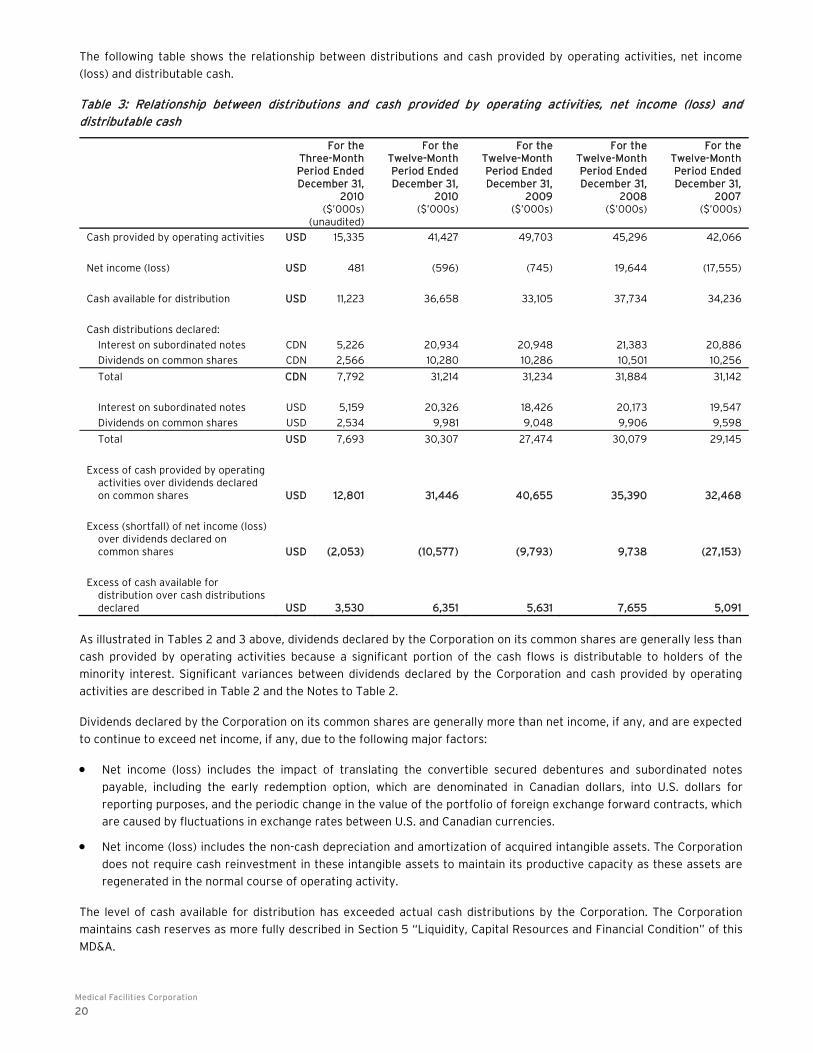

The following table shows the relationship between distributions and cash provided by operating activities, net income

(loss) and distributable cash.

Table 3: Relationship between distributions and cash provided by operating activities, net income (loss) and distributable cash

For the Three-MonthPeriod EndedDecember 31,

2010($’000s)

(unaudited)

For the Twelve-MonthPeriod EndedDecember 31,

2010($’000s)

For the Twelve-MonthPeriod EndedDecember 31,

2009($’000s)

For the Twelve-Month Period Ended December 31,

2008 ($’000s)

For theTwelve-Month Period EndedDecember 31,

2007($’000s)

Cash provided by operating activities USD 15,335 41,427 49,703 45,296 42,066

Net income (loss) USD 481 (596) (745) 19,644 (17,555)

Cash available for distribution USD 11,223 36,658 33,105 37,734 34,236

Cash distributions declared:

Interest on subordinated notes CDN 5,226 20,934 20,948 21,383 20,886

Dividends on common shares CDN 2,566 10,280 10,286 10,501 10,256

Total CDN 7,792 31,214 31,234 31,884 31,142

Interest on subordinated notes USD 5,159 20,326 18,426 20,173 19,547

Dividends on common shares USD 2,534 9,981 9,048 9,906 9,598

Total USD 7,693 30,307 27,474 30,079 29,145

Excess of cash provided by operating activities over dividends declared on common shares USD 12,801 31,446 40,655 35,390 32,468

Excess (shortfall) of net income (loss) over dividends declared on common shares USD (2,053) (10,577) (9,793) 9,738 (27,153)

Excess of cash available for distribution over cash distributions declared USD 3,530 6,351 5,631 7,655 5,091

As illustrated in Tables 2 and 3 above, dividends declared by the Corporation on its common shares are generally less than

cash provided by operating activities because a significant portion of the cash flows is distributable to holders of the

minority interest. Significant variances between dividends declared by the Corporation and cash provided by operating

activities are described in Table 2 and the Notes to Table 2.

Dividends declared by the Corporation on its common shares are generally more than net income, if any, and are expected

to continue to exceed net income, if any, due to the following major factors:

Net income (loss) includes the impact of translating the convertible secured debentures and subordinated notes

payable, including the early redemption option, which are denominated in Canadian dollars, into U.S. dollars for

reporting purposes, and the periodic change in the value of the portfolio of foreign exchange forward contracts, which

are caused by fluctuations in exchange rates between U.S. and Canadian currencies.

Net income (loss) includes the non-cash depreciation and amortization of acquired intangible assets. The Corporation

does not require cash reinvestment in these intangible assets to maintain its productive capacity as these assets are

regenerated in the normal course of operating activity.

The level of cash available for distribution has exceeded actual cash distributions by the Corporation. The Corporation

maintains cash reserves as more fully described in Section 5 “Liquidity, Capital Resources and Financial Condition” of this

MD&A.

Annual Report 2010

21

3. CONDENSED CONSOLIDATED FINANCIAL HIGHLIGHTS

Table 4: Condensed consolidated financial highlights

Years Ended December 31,

2010 2009 2008

($’000s, except per share and per IPS unit amounts)

Total assets 391,715 365,708 333,549

Total long-term financial liabilities(1) 243,758 220,044 193,439

Facility service revenue 217,918 207,426 199,375

Net income (loss) (596) (745) 19,644

Basic earnings (loss) per share $ (0.053) $ (0.027) $ 0.683

Fully diluted earnings (loss) per share $ (0.053) $ (0.027) $ 0.637

Cash distributions declared in the respective periods, per IPS unit Cdn$ 1.100 Cdn$ 1.100 Cdn$ 1.100

Note 1: Total long-term financial liabilities consist of long-term debt, convertible secured debentures and subordinated notes payable.

Table 5: Condensed consolidated income statement highlights

4th Q2010

($'000s)(unaudited)

3rd Q2010

($'000s)(unaudited)

2nd Q2010

($'000s)(unaudited)

1st Q2010

($'000s)(unaudited)

Twelve MonthsEnded

2010($'000s)

FACILITY SERVICE REVENUE 64,356 51,016 51,183 51,363 217,918

EXPENSES 37,773 32,073 32,086 34,545 136,478

OTHER INCOME 76 29 15 30 150

DEPRECIATION AND AMORTIZATION 4,978 5,110 4,958 4,830 19,876

INTEREST EXPENSE, NET(1) 6,785 6,667 7,289 5,908 26,647

INTEREST EXPENSE ON MINORITY EXCHANGEABLE INTEREST LIABILITY 1,658 1,808 1,801 1,836 7,103

CHANGE IN FAIR MARKET VALUE OF EARLY REDEMPTION OPTION (1,426) (5,385) 854 (4,382) (10,338)

MINORITY INTEREST 9,269 6,222 6,227 5,632 27,350

NET INCOME (LOSS) BEFORE GAIN (LOSS) ON FOREIGN CURRENCY AND INCOME TAX RECOVERY (EXPENSE) 5,395 4,550 (2,017) 3,024 10,952

GAIN (LOSS) ON FOREIGN CURRENCY(2) (4,282) (3,707) 6,070 (5,306) (7,225)

INCOME TAX RECOVERY (EXPENSE) (632) (2,703) (1,600) 612 (4,323)

NET INCOME (LOSS) FOR THE PERIOD 481 (1,860) 2,453 (1,670) (596)

BASIC AND FULLY DILUTED EARNINGS (LOSS) PER SHARE $ (0.015) $ (0.068) $ 0.085 $ (0.054) $ (0.053)

4th Q

2009($'000s)

(unaudited)

3rd Q2009

($'000s)(unaudited)

2nd Q2009

($'000s)(unaudited)

1st Q2009

($'000s)(unaudited)

Twelve MonthsEnded2009

($'000s)

FACILITY SERVICE REVENUE 58,048 48,960 52,178 48,239 207,426

EXPENSES 36,450 31,564 32,810 29,556 130,381

OTHER INCOME (LOSS) 72 (42) 82 58 169

DEPRECIATION AND AMORTIZATION 4,834 4,930 4,855 4,768 19,387

INTEREST EXPENSE, NET(1) 6,406 5,970 5,724 5,413 23,513

INTEREST EXPENSE ON MINORITY EXCHANGEABLE INTEREST LIABILITY 2,132 1,656 2,207 1,742 7,736

CHANGE IN FAIR MARKET VALUE OF EARLY REDEMPTION OPTION (1,408) (16,793) - - (18,201)

GOODWILL AND OTHER INTANGIBLES IMPAIRMENT - 4,661 - - 4,661

MINORITY INTEREST 7,717 5,961 6,869 6,511 27,058

NET INCOME (LOSS) BEFORE GAIN (LOSS) ON FOREIGN CURRENCY AND INCOME TAX RECOVERY (EXPENSE) 1,989 10,969 (205) 307 13,060

GAIN (LOSS) ON FOREIGN CURRENCY(2) (1,618) (7,161) (6,463) 2,381 (12,862)

INCOME TAX RECOVERY (EXPENSE) (557) (1,510) 2,165 (1,042) (943)

NET INCOME (LOSS) FOR THE PERIOD (186) 2,298 (4,503) 1,646 (745)

BASIC EARNINGS (LOSS) PER SHARE $ (0.009) $ 0.078 $ (0.149) $ 0.053 $ (0.027)

FULLY DILUTED EARNINGS (LOSS) PER SHARE $ (0.009) $ 0.078 $ (0.149) $ 0.050 $ (0.027)

Medical Facilities Corporation

22

Note 1: Interest expense, net, consists primarily of interest expense on the convertible secured debentures, subordinated notes payable

and long-term debt, offset by the interest earned on cash balances held by the Corporation.

Note 2: Gain (loss) on foreign currency is comprised of unrealized gains (losses) resulting from the translation into US$ of cash balances,

convertible secured debentures and subordinated notes payable denominated in Cdn$, changes in the value of the portfolio of foreign

exchange forward contracts held by the Corporation (as described in Section 7 “Financial Instruments” of this MD&A), and realized gains

or losses on the foreign exchange forward contracts matured in the respective periods (see note 19 to the consolidated financial

statements for the year ended December 31, 2010).

Changes in facility service revenue and expenses are discussed in Section 4 “Operating and Financial Results” of this

MD&A. Changes in other items for the three and twelve months ended December 31, 2010 compared to three and twelve

months ended December 31, 2009 are discussed below.

Depreciation and Amortization

Depreciation and amortization expense includes depreciation of property, plant and equipment and amortization of other

intangibles. The increase in depreciation and amortization expense of $0.1 million and $0.5 million for the three and twelve

months ended December 31, 2010, respectively, compared to the same periods last year is attributable to placing in service

and commencing the depreciation of assets constructed at some of the Centers in 2009 and 2010.

Interest Expense

Interest expense, net, consists primarily of interest expense on the convertible secured debentures, subordinated notes

payable (which are all denominated in Canadian dollars) and long-term debt, offset by the interest earned on the cash

balances held by the Corporation. The increase in net interest expense of $0.4 million and $3.1 million for the three and

twelve months ended December 31, 2010, respectively, compared to the same periods in 2009 is mainly attributable to (i)

the impact of a stronger Canadian dollar on the interest on borrowings in Canadian dollars in the three-month and twelve-

month periods ended December 31, 2010 and (ii) the interest on the credit facilities used to finance expansions at some of

the Corporation’s Centers which is no longer capitalized upon completion of the projects in 2009 and 2010.

Interest on Minority Exchangeable Interest Liability

Interest expense on minority exchangeable interest liability is calculated based on the portion of actual distributions from

the Centers to minority interests that is deemed attributable to the exchangeable interest. The change in the interest

expense on the minority exchangeable interest liability during the three-month and twelve-month periods ended

December 31, 2010 compared to the three-month and twelve-month periods ended December 31, 2009 is due to the

changes in the levels of distribution from the Centers in the respective periods.

Early Redemption Option

The Corporation has the right to redeem its subordinated notes payable at various premium rates prior to maturity of the

notes on March 29, 2014. The fair market value of the early redemption option on the Corporation’s subordinated notes

payable is calculated taking into account several factors, including the spread between the redemption strike price and

market yields, volatility of interest rates and the remaining time to maturity of the subordinated notes payable. The

continuing volatility in the credit markets in 2010 has led to substantial changes in the value of the early redemption

option in 2010. This value may fluctuate period by period and will be zero at the scheduled maturity date.

Goodwill and Other Intangibles Impairment

The Corporation performed its annual impairment test for goodwill and other intangibles as at December 31, 2010 and

determined that there was no impairment of goodwill and other intangibles.

Foreign Currency Gains (Losses)

Gains (losses) on foreign currency are comprised of unrealized gains (losses) resulting from the translation into U.S.

dollars of cash balances, convertible secured debentures and subordinated notes payable denominated in Canadian

dollars, changes in the value of the portfolio of foreign exchange forward contracts held by the Corporation (as described

in Section 7 “Financial Instruments” of this MD&A) and realized gains or losses on the foreign exchange forward contracts

matured in the respective periods (see note 19 to the Corporation’s consolidated financial statements for the year ended

Annual Report 2010

23

December 31, 2010). These gains (losses) on foreign currency are mainly attributable to the fluctuations in the exchange

rate between Canadian and U.S. dollars during the respective periods.

Income Tax

Income tax recovery (expense) relates to both current and future tax portions. The current tax portion is driven mostly by

the operating results of the Centers, corporate office expenses and realized gains or losses on the foreign exchange

forward contracts matured in the respective periods, while the future tax portion is driven by the temporary differences

between book and tax values of the reported assets and liabilities. The change in the income tax recovery (expense) for

the three-month and twelve-month periods ended December 31, 2010 compared to the same periods in 2009 is largely

attributable to the impact on future tax of the changes in the value of early redemption option described above and the

impact on current and future taxes of fluctuations in the exchange rate between Canadian and U.S. dollars in relation to:

(i) the fair market value of foreign exchange forward contracts held by the Corporation;

(ii) the translation of the Corporation’s convertible secured debentures and subordinated notes payable; and

(iii) the realized gains or losses on the Corporation’s foreign exchange forward contracts matured in the

respective periods.

In addition, the Corporation’s income tax expense in 2010 increased due to the tax effect of the redemption of the

Corporation’s 51% indirect interest in Barranca.

Net Income

The changes in net income for the three-month and twelve-month periods ended December 31, 2010 compared to the same

periods in 2009 are due to a number of off-setting factors, including stronger performance of the Corporation, the

changes in the value of the early redemption option, fluctuations in the exchange rate between Canadian and U.S. dollars

in the respective periods and a provision for goodwill and other intangibles impairment in 2009.

The increase in net income for the three months ended December 31, 2010 compared to the same period in 2009 is

primarily due to the stronger performance of the Centers and the reduced interest expense on minority exchangeable

interest liability, which offset the increase in the consolidated interest expense, an increased loss on foreign currency and

higher income tax expense. The small increase in net income for the twelve months ended December 31, 2010 compared to

the same period in 2009 is primarily due to the stronger performance of the Centers, the reduced interest expense on the

minority exchangeable interest liability, the absence of goodwill impairment in 2010 and a reduced loss on foreign

currency, all of which offset the increase in the consolidated interest expense, an increase in the value of the early

redemption option and higher income tax expense. The impact of operations on net income is discussed in detail in

Section 4 “Operating and Financial Results.”

Medical Facilities Corporation

24

4. OPERATING AND FINANCIAL RESULTS

Three months ended December 31, 2010 compared to three months ended December 31, 2009

Table 6.1: Operating and financial results for the three months ended December 31, 2010 compared to the three months ended December 31, 2009

Three Months Ended

December 31, 2010

Three Months Ended

December 31, 2009

% Change (unaudited) (unaudited)

($'000s)

% of facility service

revenue ($'000s)

% of facility service

revenue

Facility service revenue 64,356 58,048 10.9%

Operating expenses:

Salaries and benefits 14,771 23.0% 13,978 24.1% 5.7%

Drugs and supplies 14,682 22.8% 14,245 24.5% 3.1%

General, administrative and other operating expenses 8,320 12.9% 8,227 14.2% 1.1%

Total operating expenses 37,773 58.7% 36,450 62.8% 3.6%

Income before interest expense, depreciation and amortization, and other expenses (income) 26,583 41.3% 21,598 37.2% 23.1%

Facility service revenue for the three months ended December 31, 2010 of $64.4 million increased by $6.3 million or 10.9%

over the same period in 2009. The increased facility service revenue is primarily a reflection of a favourable case mix at

most of the Centers which resulted in a 9.5% increase in aggregate average revenue per case along with higher pain

management, imaging and anesthesia revenues at some of the Centers. Combined surgical case counts increased

marginally by 1.2% compared to the same period last year while combined pain management procedures increased by

10.6%. The positive impact of the foregoing was partially offset by a continuing trend of a higher proportion of cases

funded by payors with lower reimbursement rates (e.g., Medicare, Medicaid, Workers’ Compensation and private insurers

with fixed reimbursement schedules).

Consolidated expenses, including salaries and benefits, drugs and supplies, and general, administrative and other

operating expenses, for the three months ended December 31, 2010 totaled $37.8 million, an increase of $1.3 million or

3.6% over the same period in 2009. As a percentage of facility service revenue, the consolidated expenses decreased to

58.7% from 62.8% a year earlier.

Salaries and benefits for the three months ended December 31, 2010 increased by $0.8 million or 5.7% compared to the

same period in 2009. Such increase is primarily attributable to the additional staffing requirements to accommodate

increased case load at three out of five Centers which is consistent with the growth in facility service revenue at those

Centers. Annual wage adjustments and changes in employee health insurance costs were additional factors contributing to

the rise in salaries and benefits compared to the same period in 2009. Changes in the value of the Corporation’s Deferred

Share Unit Plan between the reporting periods was the primary cause of an increase in the salaries and benefits at the

corporate level.

Drugs and supplies expenses increased by $0.4 million or 3.1% for the three-month period ended December 31, 2010

compared to the same period in 2009. As a percentage of facility service revenue, the cost of drugs and supplies

decreased to 22.8% from 24.5% a year earlier due to the change in the case mix at all Centers which led to lower cost of

drugs and supplies per case.

General, administrative and other operating expenses for the three months ended December 31, 2010 increased by

$0.1 million or 1.1% compared to the three months ended December 31, 2009, primarily due to increases at BHSH related to

the increased facility service revenue, higher bad debt expense and physician recruiting cost, partially offset by a decline

in general, administrative and other operating expenses at SFSH due to lower bad debt expenses and a reduction in

professional fees and other public company-related costs. Other Centers saw marginal changes in their general,

administrative and other operating expenses.

Annual Report 2010

25

Consolidated income before interest expense, depreciation and amortization, and other expenses (income) of $26.6 million

for the three months ended December 31, 2010 was $5.0 million or 23.1% higher than the consolidated income for the

same period a year earlier, or 41.3% of facility service revenue compared to 37.2% in 2009.

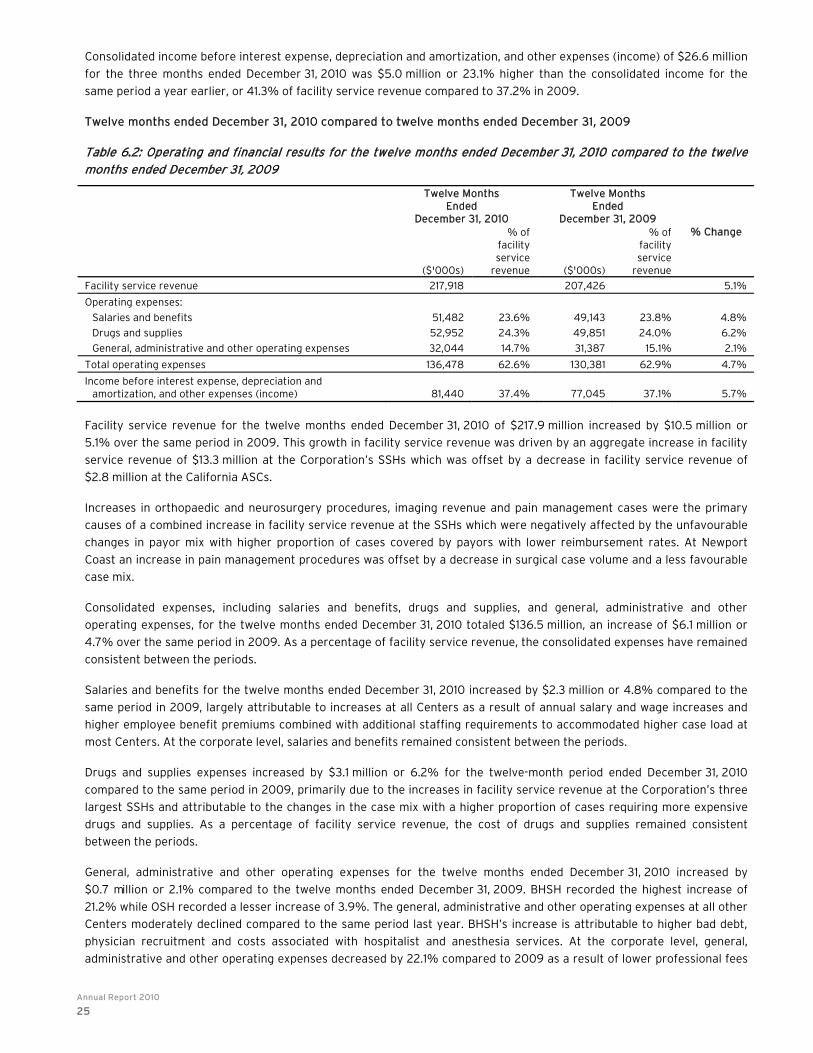

Twelve months ended December 31, 2010 compared to twelve months ended December 31, 2009

Table 6.2: Operating and financial results for the twelve months ended December 31, 2010 compared to the twelve months ended December 31, 2009

Twelve Months Ended

December 31, 2010

Twelve Months Ended

December 31, 2009 % Change

($'000s)

% of facility service

revenue ($'000s)

% of facility service

revenue

Facility service revenue 217,918 207,426 5.1%

Operating expenses:

Salaries and benefits 51,482 23.6% 49,143 23.8% 4.8%

Drugs and supplies 52,952 24.3% 49,851 24.0% 6.2%

General, administrative and other operating expenses 32,044 14.7% 31,387 15.1% 2.1%

Total operating expenses 136,478 62.6% 130,381 62.9% 4.7%

Income before interest expense, depreciation and amortization, and other expenses (income) 81,440 37.4% 77,045 37.1% 5.7%

Facility service revenue for the twelve months ended December 31, 2010 of $217.9 million increased by $10.5 million or

5.1% over the same period in 2009. This growth in facility service revenue was driven by an aggregate increase in facility

service revenue of $13.3 million at the Corporation’s SSHs which was offset by a decrease in facility service revenue of

$2.8 million at the California ASCs.

Increases in orthopaedic and neurosurgery procedures, imaging revenue and pain management cases were the primary

causes of a combined increase in facility service revenue at the SSHs which were negatively affected by the unfavourable

changes in payor mix with higher proportion of cases covered by payors with lower reimbursement rates. At Newport

Coast an increase in pain management procedures was offset by a decrease in surgical case volume and a less favourable

case mix.

Consolidated expenses, including salaries and benefits, drugs and supplies, and general, administrative and other

operating expenses, for the twelve months ended December 31, 2010 totaled $136.5 million, an increase of $6.1 million or

4.7% over the same period in 2009. As a percentage of facility service revenue, the consolidated expenses have remained

consistent between the periods.

Salaries and benefits for the twelve months ended December 31, 2010 increased by $2.3 million or 4.8% compared to the

same period in 2009, largely attributable to increases at all Centers as a result of annual salary and wage increases and

higher employee benefit premiums combined with additional staffing requirements to accommodated higher case load at

most Centers. At the corporate level, salaries and benefits remained consistent between the periods.

Drugs and supplies expenses increased by $3.1 million or 6.2% for the twelve-month period ended December 31, 2010

compared to the same period in 2009, primarily due to the increases in facility service revenue at the Corporation’s three

largest SSHs and attributable to the changes in the case mix with a higher proportion of cases requiring more expensive

drugs and supplies. As a percentage of facility service revenue, the cost of drugs and supplies remained consistent

between the periods.

General, administrative and other operating expenses for the twelve months ended December 31, 2010 increased by

$0.7 million or 2.1% compared to the twelve months ended December 31, 2009. BHSH recorded the highest increase of

21.2% while OSH recorded a lesser increase of 3.9%. The general, administrative and other operating expenses at all other

Centers moderately declined compared to the same period last year. BHSH’s increase is attributable to higher bad debt,

physician recruitment and costs associated with hospitalist and anesthesia services. At the corporate level, general,

administrative and other operating expenses decreased by 22.1% compared to 2009 as a result of lower professional fees

Medical Facilities Corporation

26

and non-recurring expenses incurred in 2009. As a percentage of facility service revenue, general, administrative and

other operating expenses decreased to 14.7% from 15.1% last year.

Consolidated income before interest expense, depreciation and amortization, and other expenses (income) of $81.4 million

for the twelve months ended December 31, 2010 was $4.4 million or 5.7% higher than the consolidated income for the

same period a year earlier, or 37.4% of facility service revenue compared to 37.1% in 2009.

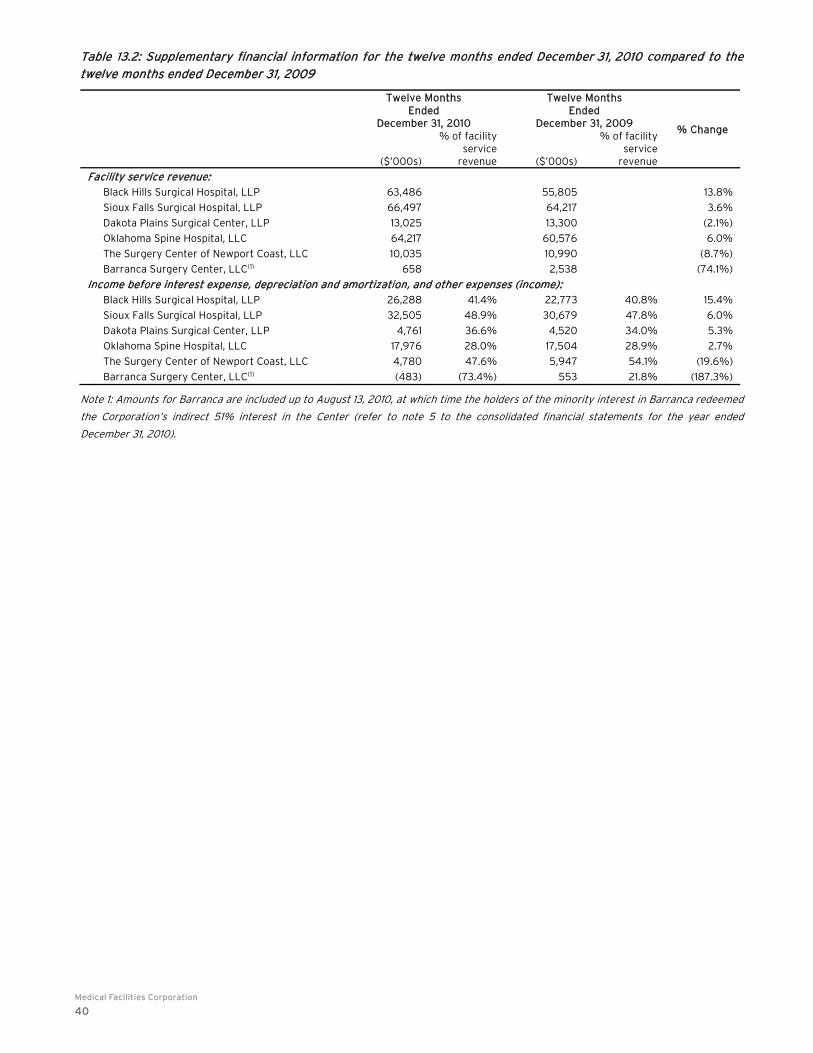

The year-to-date results presented above include results of operations for Barranca through August 13, 2010, at which

time the holders of the minority interest in Barranca redeemed the Corporation’s indirect 51% interest in the Center.

Without including results for Barranca for 2010 and 2009, facility service revenue for the twelve months ended

December 31, 2010 of $217.3 million would have been higher by $12.4 million or 6.0% compared to the same period in 2009

and operating income of $81.9 million would have been higher by $5.4 million or 7.1%.

5. LIQUIDITY, CAPITAL RESOURCES AND FINANCIAL CONDITION

Cash generated from operating activities of the Centers is the source of financing for the Corporation’s operations and for

meeting its contractual obligations. In combination with Table 2 in Section 2 “Non-GAAP Financial Measures –

Standardized Distributable Cash and Cash Available for Distribution,” Table 7 below provides further insight into the

composition of the Corporation’s cash available for distribution.

Table 7: Reconciliation of cash flows from the Centers to cash available for distribution to IPS unitholders

Three MonthsEnded

December 31,2010

($’000s)(unaudited)

Three MonthsEnded

December 31,2009

($’000s)(unaudited)

Twelve Months Ended

December 31, 2010

($’000s)

Twelve MonthsEnded

December 31,2009

($’000s)

Cash flows from the Centers:

Income before interest expense, depreciation and amortization, and other income 28,419 23,424 85,827 81,976

Other income (loss) (6) 72 87 169

Income before interest expense, depreciation and amortization 28,413 23,496 85,914 82,145

Less:

Debt service cost:

Interest (540) (386) (2,062) (1,147)

Repayments (755) (425) (2,698) (1,663)

Maintenance capital expenditures (436) (518) (2,419) (2,940)

Cash available for distribution at Center level 26,682 22,167 78,735 76,395

Less:

Minority interest in cash available for distribution at Center level (12,155) (10,203) (35,963) (35,139)

Corporation's share of the cash available for distribution at Center level 14,527 11,964 42,772 41,256

Less:

Corporate expenses (1,795) (1,816) (4,275) (4,861)

Interest on convertible secured debentures (803) (770) (3,132) (2,836)

Realized gains (losses) on matured foreign exchange forward contracts (61) 527 1,293 (1,106)

Current income taxes (645) (86) - 652

Cash available for distribution to IPS unitholders including realized gains (losses) on foreign exchange forward contracts USD 11,223 9,819 36,658 33,105

Cash available for distribution to IPS unitholders including realized gains (losses) on foreign exchange forward contracts CDN 11,367 10,371 37,754 37,806

Per IPS unit CDN $ 0.401 $ 0.366 $ 1.331 $ 1.332

Average exchange rate of Cdn$ to US$ for the period 1.0128 1.0562 1.0299 1.1420

Annual Report 2010

27

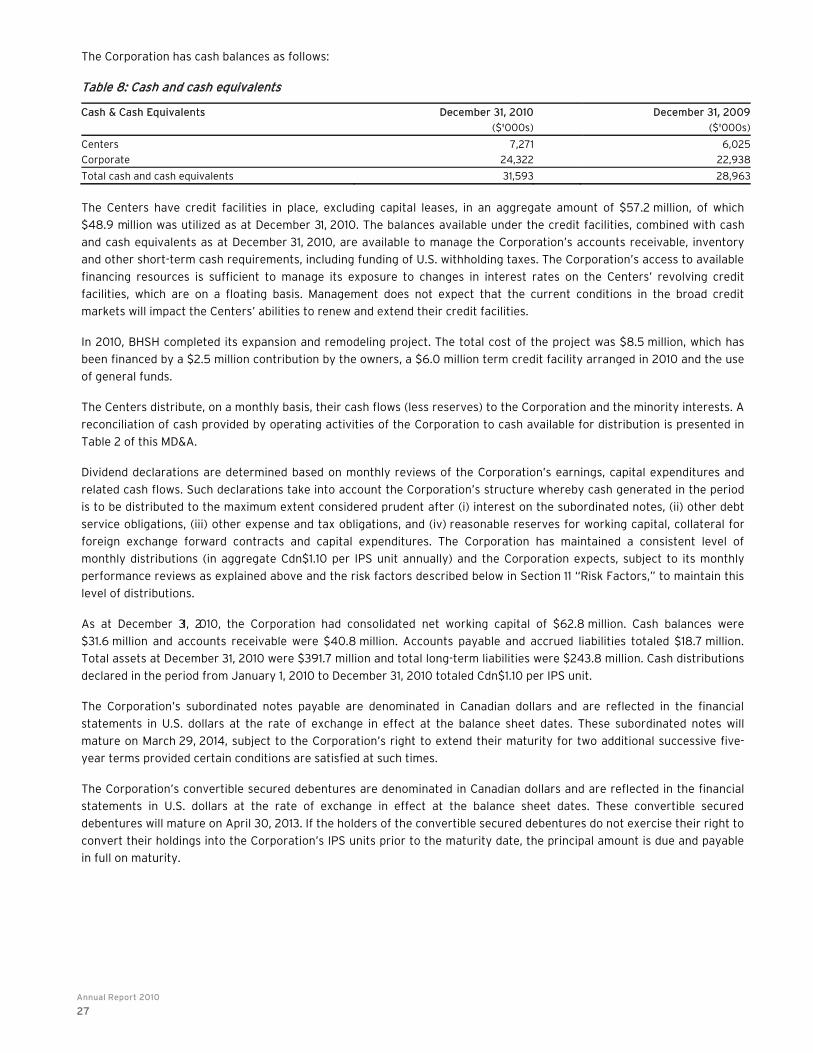

The Corporation has cash balances as follows:

Table 8: Cash and cash equivalents

Cash & Cash Equivalents December 31, 2010 December 31, 2009

($'000s) ($'000s)

Centers 7,271 6,025

Corporate 24,322 22,938

Total cash and cash equivalents 31,593 28,963

The Centers have credit facilities in place, excluding capital leases, in an aggregate amount of $57.2 million, of which

$48.9 million was utilized as at December 31, 2010. The balances available under the credit facilities, combined with cash

and cash equivalents as at December 31, 2010, are available to manage the Corporation’s accounts receivable, inventory

and other short-term cash requirements, including funding of U.S. withholding taxes. The Corporation’s access to available

financing resources is sufficient to manage its exposure to changes in interest rates on the Centers’ revolving credit

facilities, which are on a floating basis. Management does not expect that the current conditions in the broad credit

markets will impact the Centers’ abilities to renew and extend their credit facilities.

In 2010, BHSH completed its expansion and remodeling project. The total cost of the project was $8.5 million, which has

been financed by a $2.5 million contribution by the owners, a $6.0 million term credit facility arranged in 2010 and the use

of general funds.

The Centers distribute, on a monthly basis, their cash flows (less reserves) to the Corporation and the minority interests. A

reconciliation of cash provided by operating activities of the Corporation to cash available for distribution is presented in

Table 2 of this MD&A.

Dividend declarations are determined based on monthly reviews of the Corporation’s earnings, capital expenditures and

related cash flows. Such declarations take into account the Corporation’s structure whereby cash generated in the period

is to be distributed to the maximum extent considered prudent after (i) interest on the subordinated notes, (ii) other debt

service obligations, (iii) other expense and tax obligations, and (iv) reasonable reserves for working capital, collateral for

foreign exchange forward contracts and capital expenditures. The Corporation has maintained a consistent level of

monthly distributions (in aggregate Cdn$1.10 per IPS unit annually) and the Corporation expects, subject to its monthly

performance reviews as explained above and the risk factors described below in Section 11 “Risk Factors,” to maintain this

level of distributions.

As at December 31, 2010, the Corporation had consolidated net working capital of $62.8 million. Cash balances were

$31.6 million and accounts receivable were $40.8 million. Accounts payable and accrued liabilities totaled $18.7 million.

Total assets at December 31, 2010 were $391.7 million and total long-term liabilities were $243.8 million. Cash distributions

declared in the period from January 1, 2010 to December 31, 2010 totaled Cdn$1.10 per IPS unit.

The Corporation’s subordinated notes payable are denominated in Canadian dollars and are reflected in the financial

statements in U.S. dollars at the rate of exchange in effect at the balance sheet dates. These subordinated notes will

mature on March 29, 2014, subject to the Corporation’s right to extend their maturity for two additional successive five-

year terms provided certain conditions are satisfied at such times.

The Corporation’s convertible secured debentures are denominated in Canadian dollars and are reflected in the financial

statements in U.S. dollars at the rate of exchange in effect at the balance sheet dates. These convertible secured

debentures will mature on April 30, 2013. If the holders of the convertible secured debentures do not exercise their right to

convert their holdings into the Corporation’s IPS units prior to the maturity date, the principal amount is due and payable

in full on maturity.

Medical Facilities Corporation

28

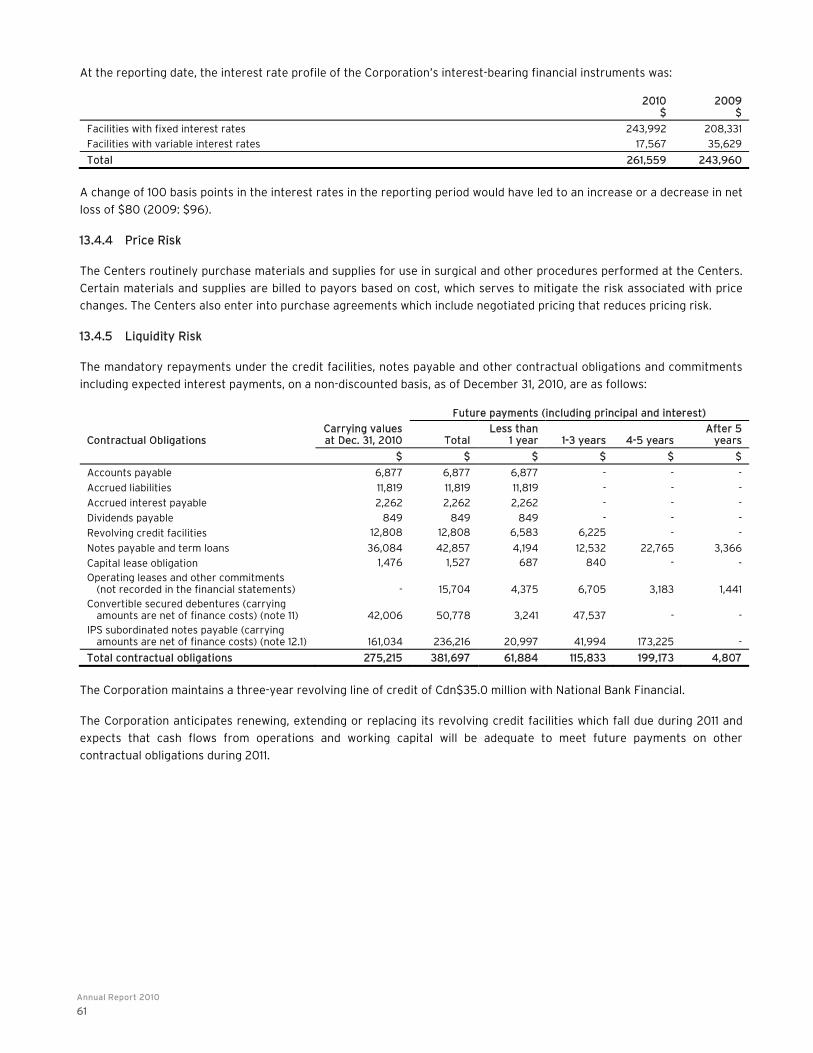

The mandatory repayments under the credit facilities, notes payable and other contractual obligations and commitments

including expected interest payments, on a non-discounted basis, as of December 31, 2010, are as follows:

Table 9: Mandatory repayments under credit facilities, notes payable and other contractual obligations and commitments

Future payments (including principal and interest)

Contractual Obligations

Carrying values at Dec. 31, 2010

($’000s) Total

($’000s)

Less than1 year

($’000s) 1-3 years ($’000s)

4-5 years($’000s)

Thereafter($’000s)

Accounts payable 6,877 6,877 6,877 - - -

Accrued liabilities 11,819 11,819 11,819 - - -

Accrued interest payable 2,262 2,262 2,262 - - -

Dividends payable 849 849 849 - - -

Revolving credit facilities 12,808 12,808 6,583 6,225 - -

Notes payable and term loans 36,084 42,857 4,194 12,532 22,765 3,366

Capital lease obligation 1,476 1,527 687 840 - -

Operating leases and other commitments (not recorded in the financial statements) - 15,704 4,375 6,705 3,183 1,441

Convertible secured debentures (carrying amounts are net of finance costs)(1) 42,006 50,778 3,241 47,537 - -

IPS subordinated notes payable (carrying amounts are net of finance costs)(1) 161,034 236,216 20,997 41,994 173,225 -

Total contractual obligations 275,215 381,697 61,884 115,833 199,173 4,807

Note 1: Finance costs are amortized using the effective interest method and the current amortization expense is included in the interest

expense for the respective periods.

The Corporation maintains a three-year revolving line of credit of Cdn$35.0 million with National Bank Financial.

The Corporation anticipates renewing, extending or replacing its revolving credit facilities which fall due during 2011 and

expects, subject to the risk factors described below in Section 11 “Risk Factors,” that cash flows from operations and

working capital will be adequate to meet future payments on other contractual obligations over the next twelve months.

The Centers derive revenues, incur expenses and make distributions to their owners, including the Corporation, in U.S.

dollars. The Corporation makes distributions to IPS unitholders and incurs a portion of its expenses in Canadian dollars.

The amounts of distributions from the Centers to their owners, including the Corporation and minority interests, are

dependent on the results of the operations and cash flow generated by the Centers in any particular period.

The strengthening of the Canadian dollar against the U.S. dollar negatively impacts currency translation differences with

respect to the Corporation’s Canadian dollar denominated distributions, convertible secured debentures and subordinated

notes payable. A weakening Canadian currency in relation to U.S. currency has the opposite effect.

Since the Corporation’s formation in March 2004, the value of the Canadian dollar has fluctuated from Cdn$1.31 = US$1.00

on March 29, 2004 to Cdn$1.08 = US$1.00 on February 28, 2011, reaching a high of Cdn$0.93 = US$1.00 and a low of

Cdn$1.40 = US$1.00 between these dates.

Annual Report 2010

29

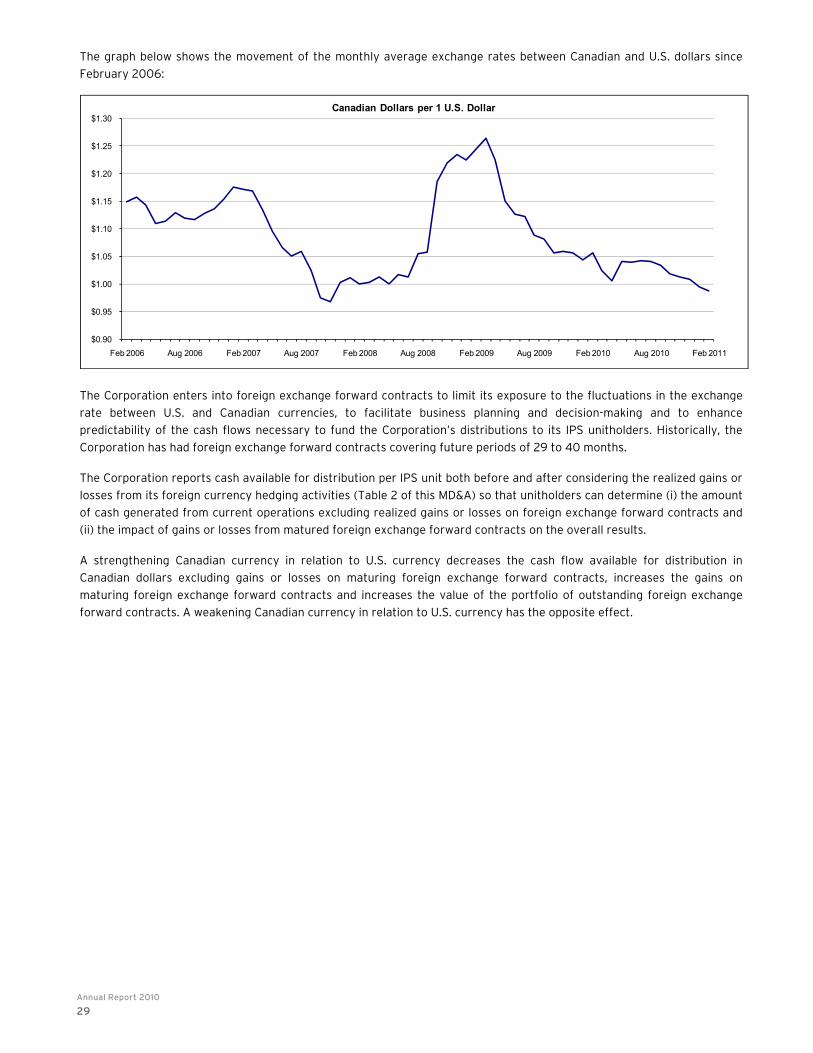

The graph below shows the movement of the monthly average exchange rates between Canadian and U.S. dollars since

February 2006:

$0.90

$0.95

$1.00

$1.05

$1.10

$1.15

$1.20

$1.25

$1.30

Feb 2006 Aug 2006 Feb 2007 Aug 2007 Feb 2008 Aug 2008 Feb 2009 Aug 2009 Feb 2010 Aug 2010 Feb 2011

Canadian Dollars per 1 U.S. Dollar

The Corporation enters into foreign exchange forward contracts to limit its exposure to the fluctuations in the exchange

rate between U.S. and Canadian currencies, to facilitate business planning and decision-making and to enhance

predictability of the cash flows necessary to fund the Corporation’s distributions to its IPS unitholders. Historically, the

Corporation has had foreign exchange forward contracts covering future periods of 29 to 40 months.

The Corporation reports cash available for distribution per IPS unit both before and after considering the realized gains or

losses from its foreign currency hedging activities (Table 2 of this MD&A) so that unitholders can determine (i) the amount

of cash generated from current operations excluding realized gains or losses on foreign exchange forward contracts and

(ii) the impact of gains or losses from matured foreign exchange forward contracts on the overall results.

A strengthening Canadian currency in relation to U.S. currency decreases the cash flow available for distribution in