86

644031-4 Demand forecast for Annual Security Assessment (from 2010) Prepared by Electricity Commission 26 October 2010

| Date post: | 24-Jun-2018 |

| Category: |

Documents |

| Upload: | vuongthuan |

| View: | 220 times |

| Download: | 0 times |

644031-4

Demand forecast for Annual Security Assessment (from 2010)

Prepared by Electricity Commission

26 October 2010

Demand forecast for Annual Security Assessment (from 2010)

644031-4 C

Executive summary

This document presents demand forecasts prepared for use in the 2010 Annual Security

Assessment (ASA).

Transpower must prepare and publish the 2010 ASA. As part of the transition of Security of

Supply monitoring and forecasting responsibilities, it has been agreed that the Commission

will provide a demand forecast for use in this assessment. Transpower will be responsible for

preparing forecasts for future assessments.

The report includes five-year forecasts of total annual energy demand (GWh), annual peak

demand (MW), and (new this year) the mean of the 200 highest half-hourly peaks.

Forecasts are provided for New Zealand as a whole, the North and South Islands, and the

four half-islands (Upper North, Lower North, Upper South, Lower South).

The forecasting methodology is essentially the same as that used in the 2007 and 2008

demand forecasts. It is based on:

stakeholder expert knowledge about specific existing and new loads; and

statistical extrapolation of other demand.

For 2011, the national energy forecasts are 40,466 GWh (expected, P50) and 41,798 GWh

(prudent, P95). These forecasts represent annual growth of 1.6% or 2.4% since 2007, in

which the energy demand was 38,034 GWh.

The expected rate of energy growth from 2011 to 2015 is 2.1%.

For 2011, the national half-hourly peak forecasts are 6,676 MW (expected, P50) and 6,931

MW (prudent, P95). These forecasts represent annual growth of 1.0% (expected) or 2.0%

(prudent) since 2007, in which the half-hourly peak was 6,405 MW.

The expected rate of peak growth from 2011 to 2015 is 2.0%.

Energy growth is predicted to be very similar across the two islands. Peak growth is

expected to be higher in the North Island (2.2%) than the South Island (1.7%).

The report discusses some unusual features of recent demand:

both peak and energy demand were low in 2009 and 2010, even allowing for reduced

demand at the Tiwai smelter; and

organic energy demand growth in the North Island has been low since 2006.

A low growth ("hockey stick") sensitivity scenario is included.

Demand forecast for Annual Security Assessment (from 2010)

D 644031-4

Glossary of abbreviations and terms

5% POE Forecast with 5% probability of exceedence, i.e. there is intended to

be a 5% chance that actual demand will be higher than forecast in

any given year. Also referred to as 'prudent forecast' and P95

50% POE Forecast with 50% probability of exceedence. Also referred to as

'expected forecast' and P50

Embedded

generator

Generator connected to a distribution network (as opposed to: grid-

connected generator)

Energy Used here in the sense of total electrical energy, denominated in

GWh. Energy forecast is used in the calculation of Winter Energy

Margin

Expected forecast See '50% POE'

Forecast Prediction of the future (c.f. 'projection', which is used in this

document to indicate a single possible sequence of future values -

many projections are combined to produce a single forecast)

Generation

component of

demand

Reduction in total demand (energy or peak) stemming from the

netted-off generators listed in Table 1 - always expressed as a

negative number (see also: industrial component of demand, residual

component of demand)

GPA Grid Planning Assumptions, as published in the Statement of

Opportunities

Grid-connected

generator

Generator connected directly to the national grid (as opposed to:

embedded generator)

GXP Grid Exit Point

Half-hourly peak Maximum half-hourly demand in a given time period, where half-

hourly demand is defined as the mean electricity demand in each

trading period and denominated in MW. C.f. instantaneous peak

Half-island One of the Upper North Island, Lower North Island, Upper South

Island and Lower South Island regions (see Section 1.5)

Industrial

component of

demand

Portion of total demand (energy or peak) stemming from the direct-

connect customers listed in Table 2 (see also: generation component

of demand, residual component of demand)

Instantaneous

peak

Maximum demand in a given period, where demand is measured at a

high frequency (e.g. every 10 seconds) and denominated in MW. C.f.

half-hourly peak

LNI, LSI Lower North Island and Lower South Island (see Section 1.5)

Demand forecast for Annual Security Assessment (from 2010)

644031-4 E

Netted-off

generation

Generation whose total output has been subtracted from the demand

forecast. Should not be modelled on the supply side (this would be

double counting).

NIPS North Island Public Supply (i.e. total electricity supplied by

generators)

P50, P95 See '50% POE' and ‘5% POE’

Projection In this document, used interchangeably with 'trajectory' to indicate a

single possible sequence of future values - a 'forecast' is calculated

as a summary of a set of projections

Prudent forecast See '5% POE'

RENA Reserve Energy Needs Assessment – older name for Annual Security

Assessment

Residual

component of

demand

Portion of total demand (energy or peak) that is left over after

'generation component' and 'industrial component' have been

subtracted

Short-term

variation factor

Factor applied to half-hourly peak demand forecasts to produce

instantaneous peak forecasts, reflecting the influence of within-half-

hour variation in demand

SIPS South Island Public Supply (i.e. total electricity supplied by

generators)

SOO Statement of Opportunities (contains Grid Planning Assumptions)

SSF Transpower's System Security Forecast

Temperature

correction factor

Factor measuring the effect of temperature on the residual

component of peak (or top200) demand. A high factor (substantially

over 1) means that cold winter temperatures led to high demand

Temperature-

corrected residual

demand

Residual component of peak (or top200) demand divided by the

temperature correction factor. Indicates the estimated value that

residual peak demand would have taken in a given year if

temperatures had been average

Top200 Mean of the highest 200 half-hourly peaks in a given year.

Denominated in MW. Used in the calculation of Winter Capacity

Margin

Trajectory Used interchangeably with 'projection'

UNI, USI Upper North Island, Upper South Island (see Section 1.5)

Winter Capacity

Margin, Winter

Energy Margin

Metrics used in the Annual Security Assessment

Demand forecast for Annual Security Assessment (from 2010)

F 644031-4

Demand forecast for Annual Security Assessment (from 2010)

644031-4 G

Contents

Executive summary C

Glossary of abbreviations and terms D

1. Introduction 1

1.1 Background 1

1.2 Scope of the forecast 2

1.3 Reactive demand growth - out of scope 3

1.4 Treatment of netted-off generation 4

1.5 Region definitions 7

2. Methodology 8

2.1 Overview 8

2.2 Data preparation – historical demand 11

2.3 Collection of information from stakeholders 12

2.4 Temperature vs peak demand modelling 13

2.5 Statistical analysis of residual demand 15

2.6 Assembling the forecasts 16

2.7 Instantaneous peak forecasts 18

3. Results 19

3.1 Historical demand data 19

3.2 Demand questionnaire findings 25

3.3 Temperature vs peak demand – results 27

3.4 Forecasts 32

3.5 Instantaneous peak forecasts 40

3.6 Changes since 2008 41

3.7 Caveats 44

4. Validation 45

4.1 Introduction 45

4.2 Validation of the predictions for 2009 and 2010 46

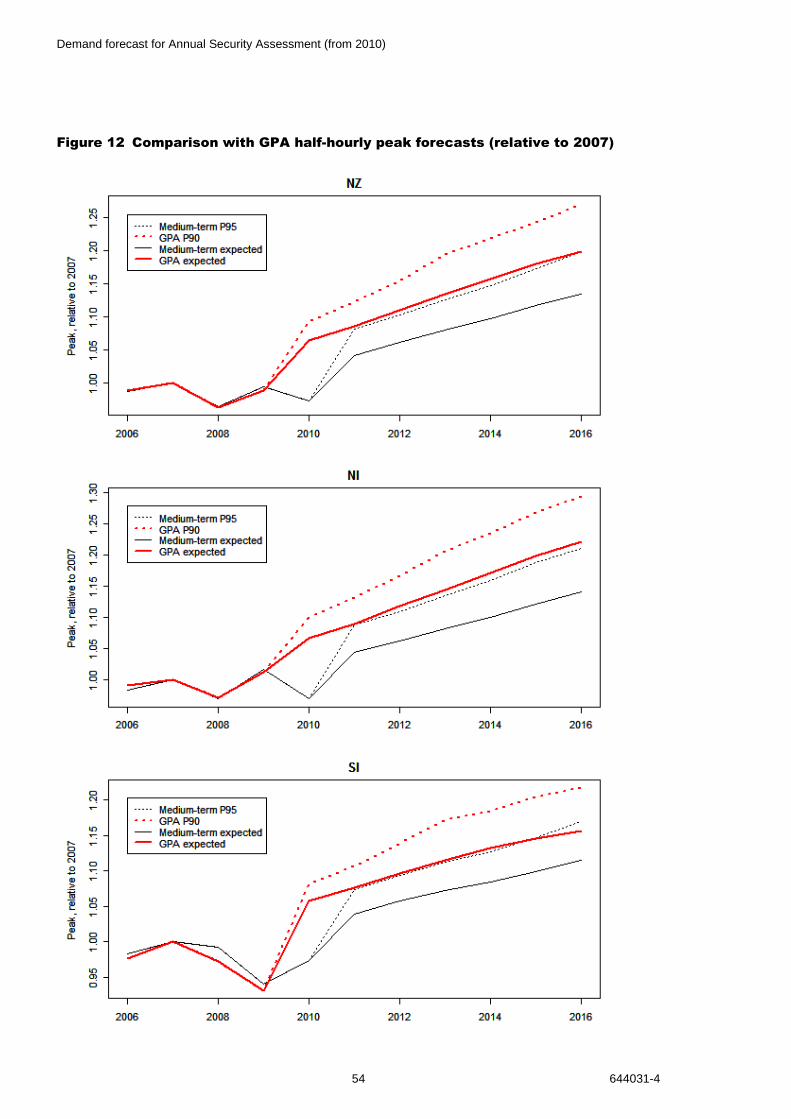

5. Comparisons with other published forecasts 51

Demand forecast for Annual Security Assessment (from 2010)

H 644031-4

5.1 Introduction 51

5.2 The 2010 GPA forecasts 51

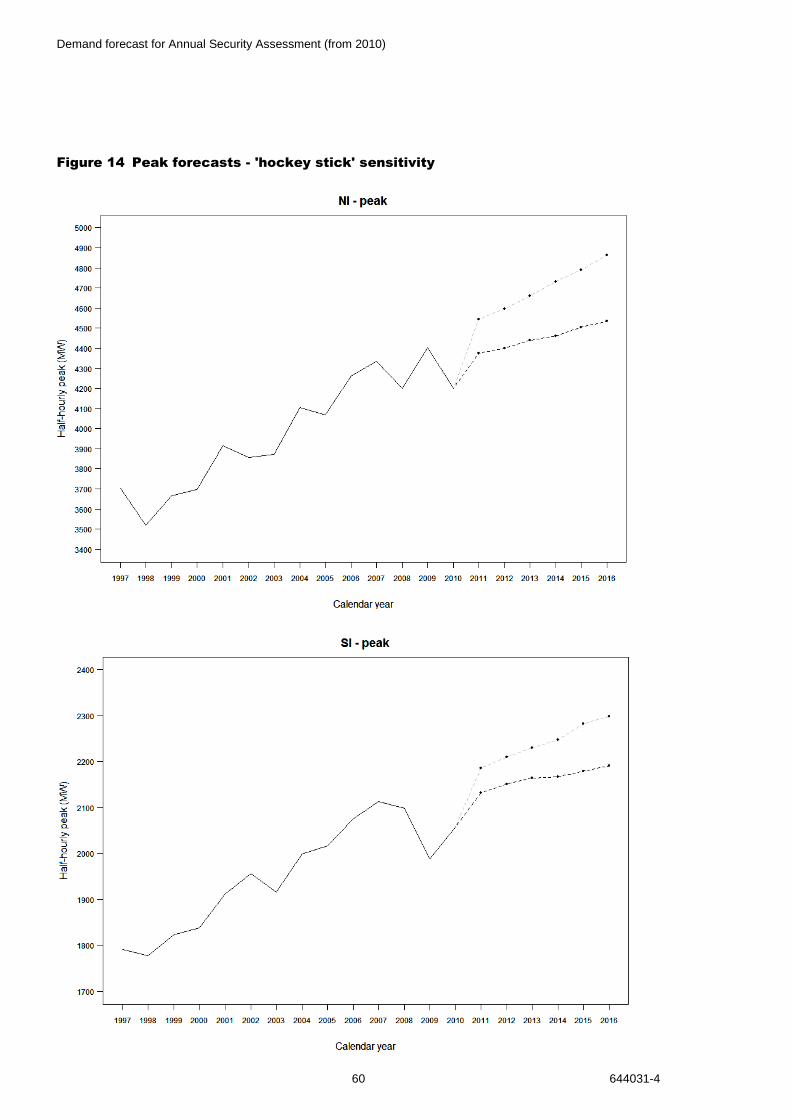

6. Low growth ('hockey stick') sensitivity 56

6.1 Rationale 56

6.2 Assumptions 56

6.3 Results 56

Appendix 1 Gnash script used to produce the half-hourly demand

dataset 63

Appendix 2 Demand and embedded generation survey 66

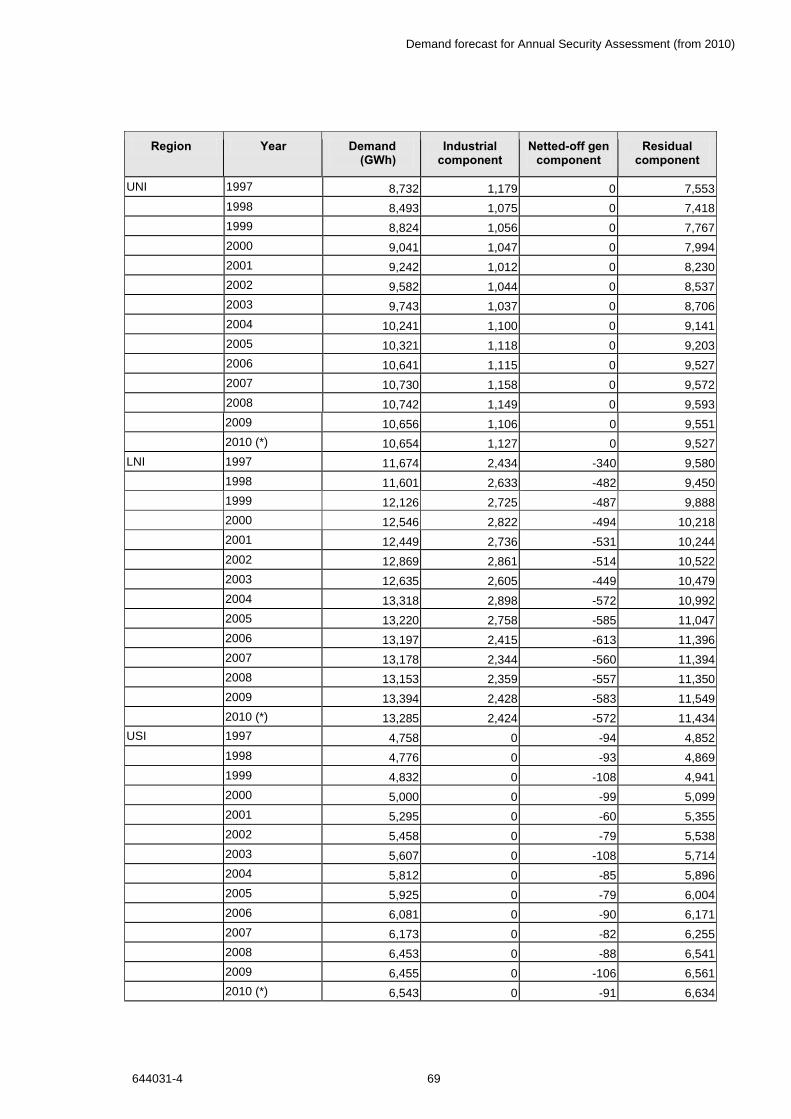

Appendix 3 Historical demand data 68

Tables

Table 1 Netted-off generators 5

Table 2 Existing direct-connect customers in the industrial component 10

Table 3 Existing netted-off generators in the generation component 10

Table 4 Comparison of recent energy demand growth rates (excluding industrial and embedded generation components) 24

Table 5 Forecasts 32

Table 6 Short-term variation factors, as used to produce instantaneous peak forecasts 40

Table 7 Instantaneous peak forecasts 41

Table 8: Comparison between expected energy demand forecasts 42

Table 9: Comparison between prudent energy demand forecasts 42

Table 10: Comparison between expected halfhourly peak demand forecasts 42

Table 11: Comparison between prudent halfhourly peak demand forecasts 42

Table 12 Predicted 2009 half-hourly peaks vs actual values 46

Table 13 Predicted 2010 half-hourly peaks vs actual values 48

Table 14 Predicted 2009 energy vs actual values 49

Table 15 Energy forecasts - 'hockey stick' sensitivity 57

Table 16 Peak forecasts - 'hockey stick' sensitivity 59

Table 17 Historical energy demand data 68

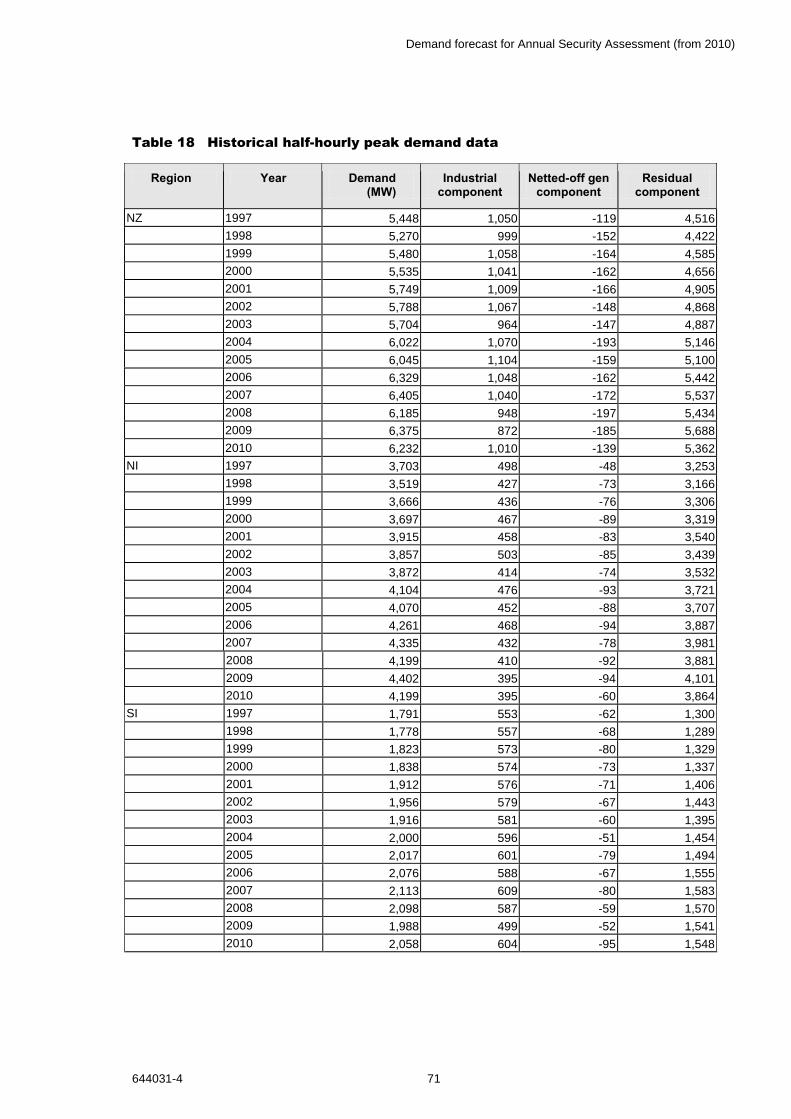

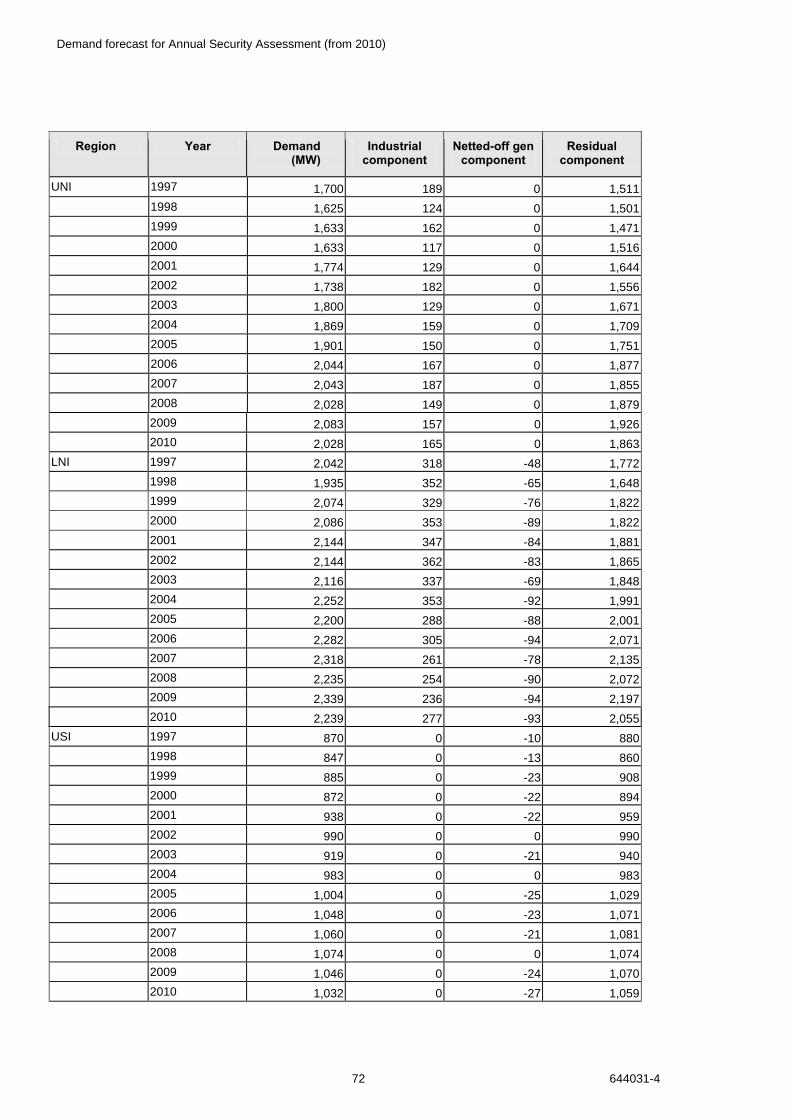

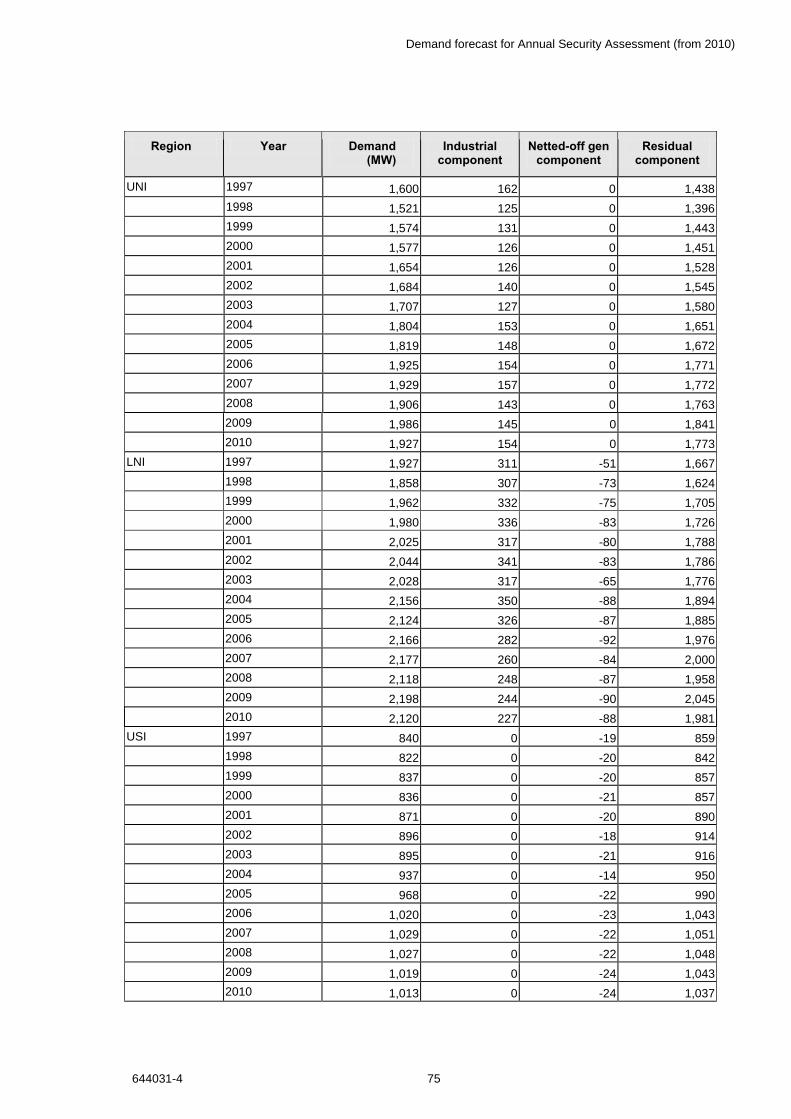

Table 18 Historical half-hourly peak demand data 71

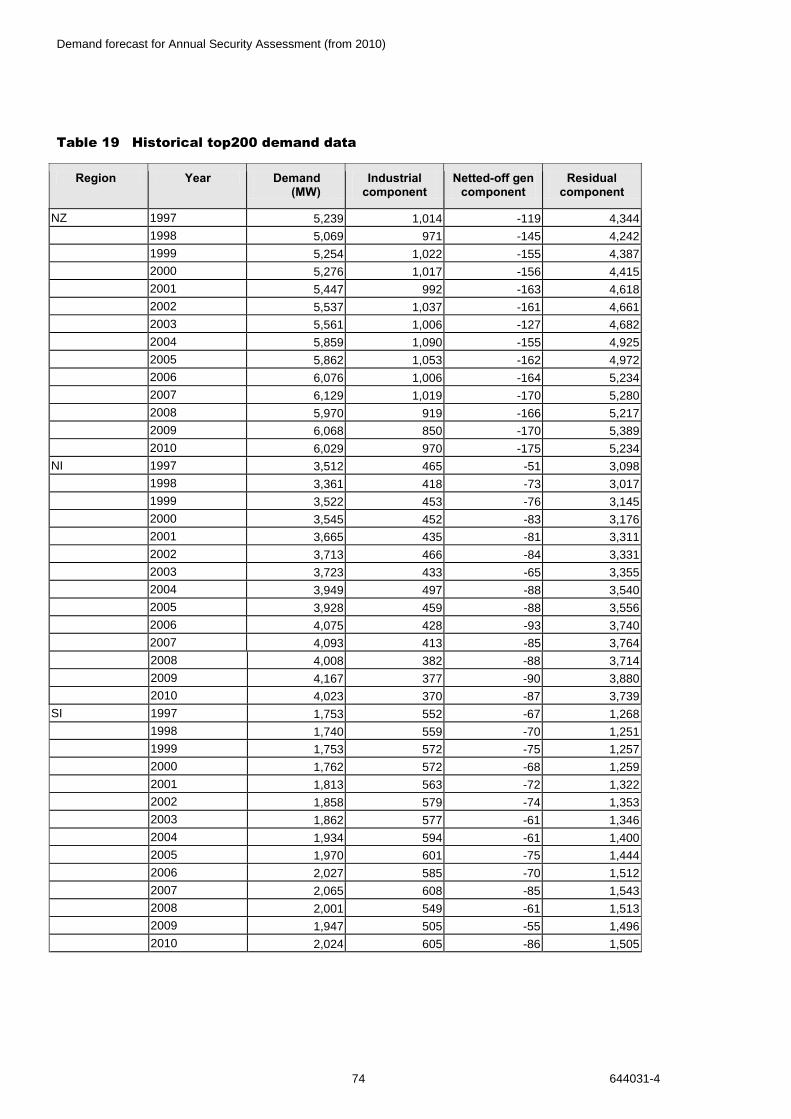

Table 19 Historical top200 demand data 74

Demand forecast for Annual Security Assessment (from 2010)

644031-4 I

Figures

Figure 1: A sample of 20 projections of the residual demand component 16

Figure 2: A sample of 20 projections of half-hourly peak demand 17

Figure 3: Historical demand data used in the forecast 20

Figure 4: Residual component of North Island energy demand 22

Figure 5: Residual component of North Island peak demand 23

Figure 6: Residual component of South Island energy demand 23

Figure 7: Residual demand component averaged over top 200 peaks - actual vs temperature-corrected 28

Figure 8: Residual demand component at half-hourly peak - actual vs temperature-corrected 29

Figure 9: Forecasts 35

Figure 10: Comparison between expected forecasts 43

Figure 11: Comparison with GPA energy forecasts (relative to 2007) 53

Figure 12 Comparison with GPA half-hourly peak forecasts (relative to 2007) 54

Figure 13 Energy forecasts - 'hockey stick' sensitivity 58

Figure 14 Peak forecasts - 'hockey stick' sensitivity 60

Demand forecast for Annual Security Assessment (from 2010)

644031-4 1

1. Introduction

1.1 Background

1.1.1 This document presents the energy and peak demand forecasts prepared for use

in the 2010 Annual Security Assessment (ASA).

1.1.2 The Commission has undertaken previous Annual Security Assessments (also

referred to as Reserve Energy Needs Assessments, RENA) to assess security of

supply and determine whether there is a need for additional reserve energy.

1.1.3 In 2007, a demand forecasting methodology was developed for use in the Annual

Security Assessment process and published for consultation.1 The new

methodology was implemented to prepare demand forecasts2 that were used in

the 2007 RENA.3

1.1.4 In 2008, the demand forecast was updated4 and used in the 2008 ASA.5

1.1.5 No new demand forecast was prepared for use in the 2009 ASA6, because it was

considered that there was not enough new data to justify the forecasting

exercise. (Data from winter 2008 were considered to be compromised by the dry

winter and public conservation campaign, and data from early-mid 2009 were

suspected to be affected by a short-term 'blip' caused by economic conditions.)

Instead, the assessment used the previous year’s demand forecast, with

modifications based on information collected through a confidential survey.

1.1.6 Transpower must prepare and publish the 2010 ASA, under its Security of Supply

Forecasting and Information Policy (SOSFIP).7 As part of the transition of

Security of Supply monitoring and forecasting responsibilities, it has been agreed

that the Commission will provide a demand forecast for use in this assessment.

1.1.7 Transpower will be responsible for preparing forecasts for future assessments.

1 http://www.ea.govt.nz/our-work/consultations/security-of-supply/demand-forecasting-methodology/

2 http://www.ea.govt.nz/document/11863/download/industry/ec-archive/security-of-supply/asa/archives/

3 http://www.ea.govt.nz/our-work/consultations/security-of-supply/asa-and-reserve-energy-needs-07/

4 http://www.ea.govt.nz/document/11864/download/industry/ec-archive/security-of-supply/asa/

5 http://www.ea.govt.nz/document/2397/download/industry/ec-archive/security-of-supply/asa/

6 http://www.ea.govt.nz/document/4550/download/industry/ec-archive/security-of-supply/asa/

7 http://www.systemoperator.co.nz/sos-policy

Demand forecast for Annual Security Assessment (from 2010)

2 644031-4

1.2 Scope of the forecast

1.2.1 The scope of this work is to produce forecasts of:

(a) energy – total annual energy demand (GWh);

(b) peak – annual half-hourly peak and instantaneous peak (both in MW); and

(c) top200 – the mean of the 200 highest half-hourly peaks in each year (MW).

1.2.2 The energy forecasts are used in the calculation of Winter Energy Margins, and

the top200 forecasts in the calculation of the Winter Capacity Margin.8

1.2.3 The peak forecasts are not strictly required for the Annual Security Assessment,

and are provided for information only.

1.2.4 It has been suggested that an MVA forecast should be included. No such

forecast has been included at this stage, though reactive power issues are

acknowledged as being important (Section 1.3).

1.2.5 Forecasts are presented at national, island and half-island9 levels. Note that peak

demand forecasts refer to national demand at national peak, island demand

at island peak, and half-island demand at half-island peak (rather than, say, half-

island demand at national peak time).

1.2.6 The forecast horizon covers five calendar years (not March years), from 2011 to

2015.

1.2.7 Both expected forecasts and more conservative 'prudent' forecasts have been

prepared.

1.2.8 All forecasts represent demand 'at grid exit point (GXP) level', i.e. inclusive of

distribution losses but exclusive of transmission losses. The output of some

(mostly embedded) generators has been netted off – see Section 1.4.

1.2.9 The aim of this work is to forecast demand in the absence of unusual demand

response. Demand-side response during periods of actual or potential scarcity

should be modelled outside the forecast.

8 http://www.ea.govt.nz/act-code-regs/code-regs/the-code/part-7/

9 I.e. Upper North Island, Lower North Island, Upper South Island and Lower South Island, as defined in Section

1.5.

Demand forecast for Annual Security Assessment (from 2010)

644031-4 3

1.3 Reactive demand growth - out of scope

1.3.1 There is a substantial requirement for reactive power investment in the Upper

North Island and Upper South Island.

1.3.2 In theory, these reactive power needs could be considered in the Annual Security

Assessment - in which case, a forecast of reactive demand would be required.

1.3.3 At this stage, however, it is not felt that it would be useful to do so - these issues

are better canvassed in other contexts. The Commission's recent consultation

paper on Stage 2 of the Transmission Pricing Review discusses the facilitation of

static reactive investment.10

1.3.4 For basic information on reactive growth in the last few years, see the following

IAG presentation: http://www.ea.govt.nz/document/3296/download/our-

work/advisory-working-groups/iag/iag-meeting-11-february-2010/.

1.3.5 In summary, power factors have been generally improving, and are likely to

continue to do so, possibly with additional incentives under a future transmission

pricing methodology or benchmark agreement.

10

http://www.ea.govt.nz/document/9996/download/our-work/consultations/transmission/tpr-stage2options/

Demand forecast for Annual Security Assessment (from 2010)

4 644031-4

1.4 Treatment of netted-off generation

1.4.1 Some generation has been netted off the forecasts – i.e. the predicted future

output of these generators has been subtracted from the demand forecasts.

When using this forecast to carry out security assessments, these generators

should not be modelled on the supply side (this would be double-counting).

On the other hand, any generator that has not been netted off should be

modelled on the supply side.

1.4.2 The generators netted off are listed in Table 1. They include:

(a) most existing embedded generators;

(b) some future embedded generators; and

(c) a small number of grid-connected plants.

1.4.3 By contrast, the Commission's GPA demand forecasts11 are designed to be net

of all embedded generation and gross of all grid-connected generation. So the

two forecasts are not comparable in absolute terms (although it may be

reasonable to compare them in terms of growth rates). For example, the output of

grid-connected cogeneration at Glenbrook has been netted off this forecast but

not the GPA forecast. On the other hand, the output of the embedded parts of

Tararua Wind Farm (stages 1 and 2) has not been netted off this forecast but was

netted off the GPA forecast.

1.4.4 The forecasts in this document are also not comparable in absolute terms with

any historical demand data that do not share the same treatment of netted-off

and grossed-on generation. For ‘apples vs apples’ comparisons of forecast and

historical demand, see:

(a) Section 3.4 of this report; and

(b) monthly reports available on the Commission website12, which discuss

recent demand trends and comment on the accuracy of earlier Security of

Supply demand forecasts.

1.4.5 Any confusion relating to the treatment of netted-off generation is regretted. The

approach used was adopted after some consideration, on the grounds that the

resulting forecast will be the most fit for purpose.

11

http://www.ea.govt.nz/industry/ec-archive/soo/2010-soo/

12 http://www.ea.govt.nz/industry/ec-archive/security-of-supply/short-term-monitoring/demand-archive/

Demand forecast for Annual Security Assessment (from 2010)

644031-4 5

Table 1 Netted-off generators

Generator Netted off Not netted off

Glenbrook –

cogeneration at

NZ Steel mill

All cogeneration is netted off

forecasts (including grid-injected

generation at GLN0332)

Highbank – 'partly

embedded' hydro

generation

All generation is netted off forecasts

(whether embedded or grid-

injected)

Waipori – 'partly

embedded' hydro

generation

All generation, including Deep

Stream, is netted off forecasts

(whether embedded or grid-

injected)

Aniwhenua – 'partly

embedded' hydro

generation

All generation is netted off forecasts

(whether embedded or grid-

injected)

Kawerau (Norske

Skog), Karioi (Winstone

Pulp and Paper), and

Whirinaki (Pan Pac) –

wood processing

cogeneration

Cogeneration is netted off forecasts

Kapuni – CHP

cogeneration

Generation is not netted off

forecasts and should be modelled

on the supply side

Whareroa – dairy

factory cogeneration

Generation is not netted off

forecasts. Net injection should be

modelled on the supply side

Te Rapa – dairy factory

cogeneration

Generation is not netted off

forecasts, even though it is

embedded. Net injection should be

modelled on the supply side

Kinleith - cogeneration Generation is not netted off

forecasts and should be modelled

on the supply side

Demand forecast for Annual Security Assessment (from 2010)

6 644031-4

Generator Netted off Not netted off

Southdown -

cogeneration

Generation is not netted off

forecasts and should be modelled

on the supply side

Tararua Wind Farm –

stages 1-3

Generation is not netted off

forecasts, even though stages 1

and 2 are embedded, and should

be modelled on the supply side

Te Apiti Generation is not netted off

forecasts and should be modelled

on the supply side

White Hill Generation is not netted off

forecasts, even though embedded,

and should be modelled on the

supply side

New wind farms Generation from new wind farms

with capacity under 30 MW is

assumed to be netted off forecasts

Generation from new wind farms

with capacity at least 30 MW is not

netted off forecasts and should be

modelled on the supply side

Other embedded

generators not listed

above, whether existing

or new

Generation is assumed to be netted

off forecasts

Other grid-connected

generators not listed

above, whether existing

or new

Generation is not netted off

forecasts and should be modelled

on the supply side

Demand forecast for Annual Security Assessment (from 2010)

644031-4 7

1.5 Region definitions

1.5.1 In this document, the North Island is divided into the Upper North Island (UNI)

and Lower North Island (LNI), and the South Island is divided into the Upper

South Island (USI) and Lower South Island (LSI).

1.5.2 These 'half-island' labels are used in various other contexts and their meaning

varies between sources. For the avoidance of doubt, the way in which they are

used in this work is defined below.

(a) Upper North Island – all GXPs in the Northland and Auckland 'transmission

regions', including Glenbrook (GLN), Takanini (TAK), Bombay (BOB), Wiri

(WIR) and Meremere (MER) but excluding Huntly (HLY);

(b) Lower North Island – all other North Island GXPs;

(c) Upper South Island – all GXPs in the West Coast, Nelson/Marlborough,

and Canterbury 'transmission regions', and, in the South Canterbury region,

Albury (ABY), Temuka (TMK), Timaru (TIM) and Tekapo (TKA) but not

Twizel (TWZ);

(d) Lower South Island – all other South Island GXPs.

Demand forecast for Annual Security Assessment (from 2010)

8 644031-4

2. Methodology

2.1 Overview

2.1.1 This section describes the methodology used to prepare the forecasts. Results,

including historical demand series and forecasts, are presented in Section 3.

Validation analysis and comparisons with some other forecasts are presented in

Section 4.

2.1.2 The methodology used is essentially the same as that used in the 2007 and

2008 RENA demand forecasts. The only significant difference is that top200

forecasts (i.e. mean of the highest 200 half-hourly peaks in each year) are now

included, for use in calculating the Winter Capacity Margin.

2.1.3 The forecasting methodology is based on:

(a) stakeholder expert knowledge about specific existing and new loads; and

(b) statistical extrapolation of other demand.

2.1.4 The data sources used include:

(a) historical half-hourly demand data covering the period from 1997 to 201013

(Section 2.2);

(b) questionnaires completed by stakeholders, providing information on

expected new loads, changes to existing loads, and changes to embedded

generation (Section 2.3); and

(c) historical air temperature records, used to estimate the impact of weather

conditions on peak and top200 demand (Section 2.4).

2.1.5 Various other sources of data (e.g. econometric projections, appliance use

statistics, etc) have been suggested by stakeholders, and could potentially be

incorporated in future forecasts.

2.1.6 For each year, 'expected' and 'prudent' forecasts were produced. The 'prudent'

forecasts were calculated on a 5% POE basis – i.e. it is intended that there is a

probability of 0.05 that a 'prudent' forecast will be exceeded in any given year.

13

Data for October-December 2010 were not available at the time of writing, but were imputed based on

previous years. This enabled use of January-September 2010 data in the energy forecast.

Demand forecast for Annual Security Assessment (from 2010)

644031-4 9

2.1.7 The process used to prepare the forecasts is described below. This process was

carried out separately for each half-island, for both islands and for New Zealand

as a whole.14

2.1.8 Energy, peak and top200 forecasts were carried out separately - they used

consistent inputs, but were not explicitly linked.15

2.1.9 Energy forecasts were produced by:

(a) using the half-hourly demand data described in Section 2.2 to calculate

annual energy consumption in GWh for 1997-2010, minus the output of

'netted-off generators' (as listed in Section 1.3);

(b) dividing the resulting data series into three components:

(i) industrial – the combined demand of selected direct-connect

customers (Table 2);

(ii) generation – the combined output of selected netted-off generators

(Table 3), expressed as a 'negative demand'; and

(iii) residual – all other demand;

(c) using information from stakeholders (where available, see Section 2.3)

to project the generation and industrial components forwards;

(d) carrying out statistical regression analysis to estimate the trend of the

residual component and extrapolate it forwards, both in terms of expected

value and variability around the mean (see Section 2.5);

(e) producing a set of projections of possible future demand, each generated

by projecting the residual, generation, and industrial components

independently and summing the results (see Section 2.6); and

(f) calculating the 'expected forecast' for each year as the median of the future

demand projections, and the 'prudent forecast' as the 95th percentile of the

future demand projections.

2.1.10 The primary aim of this approach was to separate out the residual component,

which may be somewhat predictable over the medium term using a purely

statistical (time series) approach, from the generation and industrial components,

which are not statistically tractable but can potentially be predicted using expert

knowledge.

14

An alternative would have been to carry out a single national forecast, and then use some form of allocation

technique to break it down by island and region.

15 An alternative would have been to carry out an energy forecast first, and then base the peak forecast (in whole

or in part) on projected energy growth rates.

Demand forecast for Annual Security Assessment (from 2010)

10 644031-4

Table 2 Existing direct-connect customers in the industrial component

Half-island Sites

UNI Glenbrook – NZ Steel mill

Marsden Point – NZRC oil refinery

Otahuhu – Pacific Steel mill

LNI Kinleith – CHH pulp and paper plant

Kawerau – Norske Skog pulp and paper plant

Whirinaki – Pan Pac mill

Karioi – Winstone pulp mill

Motunui – Methanex methanol plant

USI None

LSI Tiwai – NZAS aluminium smelter

Table 3 Existing netted-off generators in the generation component

Half-island Sites

UNI None

LNI Kaimai - hydro schemes

Rotokawa – embedded geothermal

Aniwhenua – 'partly embedded' hydro

USI Highbank – 'partly embedded' hydro

LSI Waipori – 'partly embedded' hydro

2.1.11 The same method was used to produce half-hourly peak forecasts, except that:

(a) data series and projections were based on the half-hourly peak in each

year, rather than the annual total; and

(b) the effect of temperature on peak demand was incorporated.

2.1.12 Historical temperature records were used to develop a model of the effect of

temperature on annual peaks. This model was then used to strip the effect of

weather conditions out of the residual peak demand series, yielding a

'temperature-corrected' series which could be used to provide better estimates of

underlying trends (Section 2.4). Simulated temperature effects were then

Demand forecast for Annual Security Assessment (from 2010)

644031-4 11

incorporated into future projections, to model the possible future effects of

weather on peak demand (Section 2.6).

2.1.13 Instantaneous peak forecasts were produced by applying a 'short-term variation

factor' to half-hourly peak forecasts, to reflect the effect of within-half-hour

variation. Different factors were used for each region, and for expected and

prudent forecasts. Section 2.7 describes the process used to estimate these

short-term variation factors.

2.1.14 Top200 forecasts were produced in the same way as half-hourly peak forecasts,

except that data series and projections were based on the mean of the top 200

half-hourly peaks in each year, rather than the annual total.

2.2 Data preparation – historical demand

2.2.1 A key input to the analysis was a dataset of historical half-hourly demand data.

This dataset was extracted from the Gnash database published in the

Commission's Centralised Dataset.16

2.2.2 Gnash code is included (Appendix 1). In theory stakeholders could use this code

to reproduce the dataset, but:

(a) Gnash data series labels change without notice, so each published version

of Gnash would require different changes to the code in order for it to run

successfully; and

(b) some data used in the early portion of the dataset were provided by market

participants under confidentiality, and are not included in published

versions of Gnash.

2.2.3 Alternatively, the dataset can be provided on request, minus confidential

information.

2.2.4 Data for October-December 2010 were not available at the time of writing, but

were imputed based on previous years. This enabled use of January-September

2010 data in the energy forecast.

16

http://www.ea.govt.nz/industry/modelling/cds/

Demand forecast for Annual Security Assessment (from 2010)

12 644031-4

2.3 Collection of information from stakeholders

2.3.1 A key component of the forecast was information received from stakeholders

about potential step changes to demand and embedded generation. A

questionnaire was sent to:

(a) distributors;

(b) some major direct-connect customers; and

(c) some industry associations.

2.3.2 The focus of the survey was on step changes in demand and embedded

generation over the next five years. The full questionnaire is reproduced as

Appendix 2.

2.3.3 Individual responses to the questionnaire are covered by commercial confidence,

but some aggregated results are presented in Section 3.1.5.

2.3.4 These responses have been used, along with historical data, to produce demand

projections for each of the direct-connect customers and netted-off generators

listed in Table 2 and Table 3. They have also been used to predict new loads and

embedded generation plants that may be commissioned in the next five years.

2.3.5 When using stakeholder responses relating to new developments, the

Commission has attempted to focus on 'step changes' rather than on 'organic

growth'. The key criteria used were that changes to demand should be

associated with a specific site, should be at least 5 MW (possibly reaching that

level over a period of time rather than in a single step), and should relate to an

industrial or agricultural consumer rather than to residential or commercial

development.

2.3.6 Each step change was assigned a probability by the Commission, based on

indications given by respondents as to the likelihood of it occurring, the time

frame and the current stage of development. These probabilities ranged between

0.5 (credible, but not yet confirmed) and 1 (certain).

2.3.7 Some step changes appear to reflect an acceleration of historical trends, rather

than a genuinely new trend (e.g. increased South Island irrigation and dairy

processing). These types of changes have been derated by 50%, reflecting that

they are not completely additional.

2.3.8 Attempts have been made to avoid double-counting where two or more

stakeholders have commented on the same development.

2.3.9 The Commission thanks all respondents for the information provided. Their

efforts are appreciated; even null responses are useful.

Demand forecast for Annual Security Assessment (from 2010)

644031-4 13

2.4 Temperature vs peak demand modelling

2.4.1 Weather conditions have a significant effect on peak demand. A substantial

proportion of the inter-year variation in annual peak demand is driven by

temperatures. This can obscure the underlying pattern of demand growth.

2.4.2 For example, the 2006 winter peak was very high relative to previous years,

which might have been interpreted as showing an upturn in the rate of demand

growth – but in fact this peak was largely due to cold temperatures in late June.

2.4.3 The methodology used to identify the effect of temperature on historical half-

hourly peak demand is described below. (Air temperature was used as a proxy

for general weather conditions.)

2.4.4 The aim of the analysis was to determine annual 'temperature effects' for each

region, measuring the impact of temperature on the residual component17 of peak

demand in each winter. These temperature effects were expressed as factors,

indicating the amount by which historical peak demands were increased by

temperature effects. For example, a factor of 0.98 for the lower North Island in

2005 would indicate that mild weather had reduced peak demand by 2%.

2.4.5 Historical temperature data were sourced from MetService. A hourly temperature

series covering 1997-2010 was derived for each half-island, as a population-

weighted average of temperature records at population centres within the region.

2.4.6 In brief, the analysis identified the ten days in each winter on which peak demand

was highest, assessed the effect of temperature on each of those days, and

calculated the temperature correction factor as the average of these temperature

effects. Winters where the highest peaks occurred during an unusually severe

cold snap were therefore assigned a high temperature correction factor.

2.4.7 The full process used to produce annual half-island temperature correction

factors was as follows:

(a) identify the 'top ten daily peaks' in each historical winter from 1997 to 2010

– i.e. the ten days on which the highest half-hourly peak demand was

recorded;

(b) create a daily data series of residual demand at evening peak;

(c) build a statistical regression model relating these daily evening peaks to

date, day of week, and temperature variables, including lagged effects

(see Appendix 3 of 2008 RENA demand forecast18 for details);

17

The generation and industrial components of demand were not expected to be strongly temperature-driven.

18 http://www.ea.govt.nz/document/11864/download/industry/ec-archive/security-of-supply/asa/

Demand forecast for Annual Security Assessment (from 2010)

14 644031-4

(d) use the evening peak model to estimate a 'temperature effect on evening

peak' value for each winter day from 1997 to 2010, calculated as the sum of

the temperature-related effects in the model (but excluding other effects like

month or day of week). For example, a cold day might have a temperature

effect of 1.03, meaning that evening peak demand was probably about 3%

higher than it would have been on a day with average temperatures;

(e) repeat steps (b)-(d) for daily morning peaks;

(f) calculate the temperature correction factor for each year as the average

daily temperature effect on the days of the 'top ten daily peaks' (using the

'morning peak effect' from (e) for days when the peak occurred in the

morning, or the 'evening peak effect' from (d) otherwise); and

(g) divide the resulting series of annual temperature correction factors by their

mean, to standardise to a mean of 1 (on the assumption that these ten

years are a representative sample of the historical range of temperatures).

2.4.8 Factors for the North Island, South Island and New Zealand as a whole were

estimated as demand-weighted averages of the respective half-island values.

2.4.9 For each half-island, each island and New Zealand as a whole, the actual annual

peak demands were divided by these temperature correction factors to produce

'temperature-corrected residual peak demand' series. These temperature-

corrected series are shown in Section 3.3.

2.4.10 The analysis was also used to determine a probability distribution for the

'temperature correction factor' applied to each future year when projecting peak

demand forwards (see Section 2.6). For each region, temperature correction

factors were drawn from a normal distribution, with mean of 1 and standard

deviation equal to the standard deviation of the estimated annual temperature

effects in that region over 1997-2010.

2.4.11 The same approach was used to model the effect of temperature on top200

demand, except that the ‘top fifty daily peaks’ were used rather than ‘top ten’.

2.4.12 The implicit assumption is that temperatures over the next five years will be

similar to those experienced over the last decade. This is possibly questionable,

given that the historical record shows some considerably colder winters.

Transpower has suggested that the full recorded range of historical weather

conditions should be taken into account in future analysis. This is a good

suggestion and should be taken up at some point - but to date it has not proved

possible to obtain a significantly longer temperature data series that is consistent

throughout.

Demand forecast for Annual Security Assessment (from 2010)

644031-4 15

2.5 Statistical analysis of residual demand

2.5.1 For each region, for each of energy, top200 and half-hourly peak, the residual

demand component is an annual series covering 1997-2010. Demand from

selected major direct-connect consumers has been subtracted from the total

demand (the industrial component), and the output of selected 'netted-off'

generators has been added back onto the demand series (the generation

component). The resulting residual series comprises residential, commercial and

smaller industrial demands, with only minor embedded generators netted off. For

peak and top200, an attempt has also been made to remove the effect of

temperature (Section 2.4).

2.5.2 As a result, year-to-year changes in the residual demand series should be largely

driven by underlying organic growth plus 'random' variation.

2.5.3 Therefore, these demand series were projected into the future using a 'pure time

series' approach – i.e. using statistical regression models with no exogenous

predictors.

2.5.4 The regression models used an exponential fit, i.e. the logarithm of demand was

regressed against time. This implies a constant underlying growth rate, with log-

normally distributed variation around the trend line.

2.5.5 Data from the 2001, 2003 and 2008 years were excluded from the regression

models19, since demand in these years was reduced by dry-year savings

campaigns, and the goal was to produce a forecast of demand without any

unusual demand response (Section 1.2).

2.5.6 Projections of the residual component into the future were based on

extrapolations of the fitted curve, with three sources of variation incorporated:

(a) uncertainty about the underlying growth rate (based on the standard errors

of the regression coefficients);

(b) year-to-year variation (based on the residual standard deviation of the

model); and

(c) possible future changes in trend, perhaps driven by changes in consumer

behaviour or appliance use. In each projection, the growth rates from 2012

onwards are modified by a random amount, drawn from a normal

distribution with a mean of zero and standard deviation of 0.5%.20

19

An alternative would have been to use a 'savings campaign year' indicator variable in the regression models,

but omitting 2001, 2003 and 2008 data entirely was felt to be a better approach.

20 The same increment is applied to all growth rates from 2012 onwards in a single projection, rather than a

separate increment being randomly drawn for each individual year.

Demand forecast for Annual Security Assessment (from 2010)

16 644031-4

2.5.7 The 'possible future changes in trend' component should be seen as a

precautionary measure. It is intended to allow for unforeseeable changes that

could occur several years from now (affecting energy, or peak, or the relationship

between the two). The effect is to increase prudent forecasts from 2013 onwards

quite significantly, but there is very little effect on expected forecasts. The

assumed date when the changes start to take effect is acknowledged to be

arbitrary, as is the modelled distribution of possible changes.

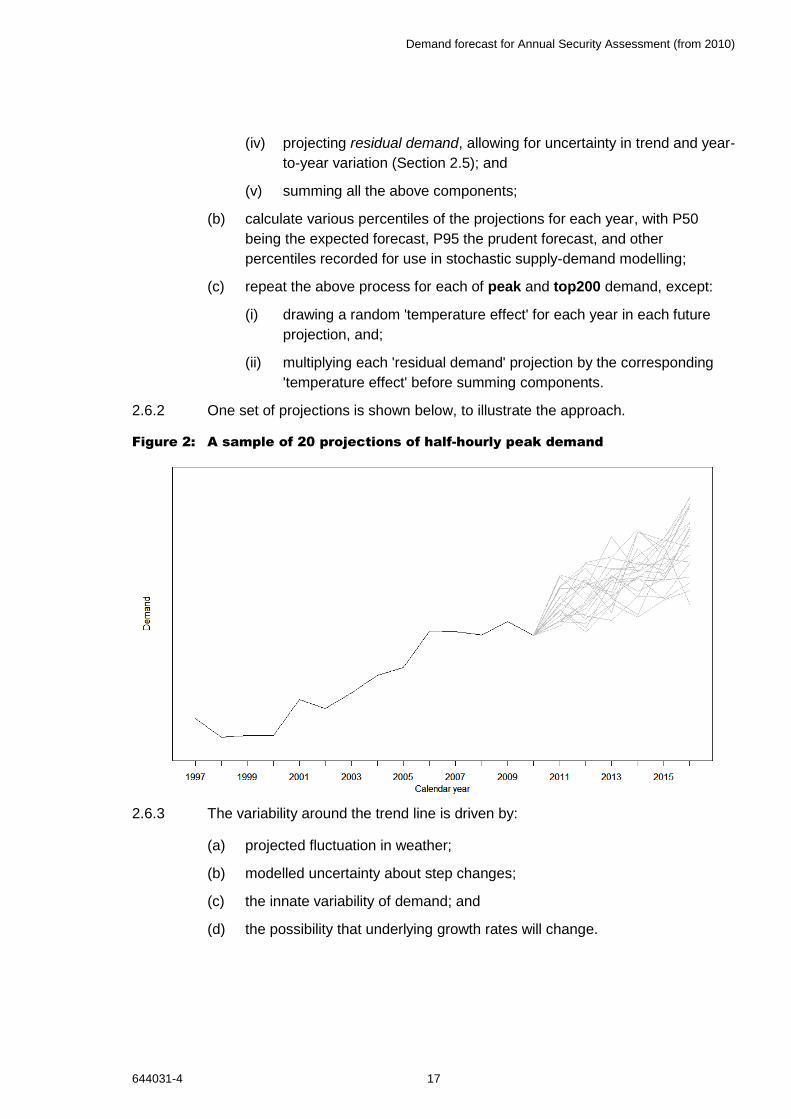

2.5.8 One set of projections is shown below, to illustrate the approach.

Figure 1: A sample of 20 projections of the residual demand component

2.6 Assembling the forecasts

2.6.1 The process used to produce the forecasts was to:

(a) produce many projections of annual energy demand over the 2011-15

period, by:

(i) projecting demand of selected existing direct-connect customers

(listed in Table 2), allowing for uncertainty;

(ii) projecting demand of significant new loads, allowing for uncertainty;

(iii) projecting generation of selected existing netted-off generators (listed

in Table 1) and new netted-off generators, allowing for uncertainty;

Demand forecast for Annual Security Assessment (from 2010)

644031-4 17

(iv) projecting residual demand, allowing for uncertainty in trend and year-

to-year variation (Section 2.5); and

(v) summing all the above components;

(b) calculate various percentiles of the projections for each year, with P50

being the expected forecast, P95 the prudent forecast, and other

percentiles recorded for use in stochastic supply-demand modelling;

(c) repeat the above process for each of peak and top200 demand, except:

(i) drawing a random 'temperature effect' for each year in each future

projection, and;

(ii) multiplying each 'residual demand' projection by the corresponding

'temperature effect' before summing components.

2.6.2 One set of projections is shown below, to illustrate the approach.

Figure 2: A sample of 20 projections of half-hourly peak demand

2.6.3 The variability around the trend line is driven by:

(a) projected fluctuation in weather;

(b) modelled uncertainty about step changes;

(c) the innate variability of demand; and

(d) the possibility that underlying growth rates will change.

Demand forecast for Annual Security Assessment (from 2010)

18 644031-4

2.7 Instantaneous peak forecasts

2.7.1 Electricity demand varies within each half-hour period. Published half-hour

demand figures are an average of data sampled at higher frequencies.

Accordingly, the instantaneous peak on any given day is greater than the half-

hourly peak (since the maximal value in the half-hour with highest demand will

always be greater than the average value in that half-hour). In New Zealand, the

difference can be over 100 MW.

2.7.2 For some purposes, half-hourly demand forecasts are adequate; in other

contexts, the instantaneous peak is more relevant. Accordingly, both types of

forecasts are provided in this report.

2.7.3 Instantaneous peak forecasts were derived by applying 'short-term variation

factors' to half-hourly peak forecasts, modelling the effect of within-half-hour

variation. The process used to derive these factors is described in the 2008

RENA demand forecast document.

2.7.4 Typically the process resulted in variation factors of about 1% (for expected

forecasts) or between 1% and 2% (for prudent forecasts). Different factors were

used for each region (NI, SI, and New Zealand overall).

2.7.5 Variation factors and instantaneous peak forecasts are presented in Section 3.5.

Demand forecast for Annual Security Assessment (from 2010)

644031-4 19

3. Results

3.1 Historical demand data

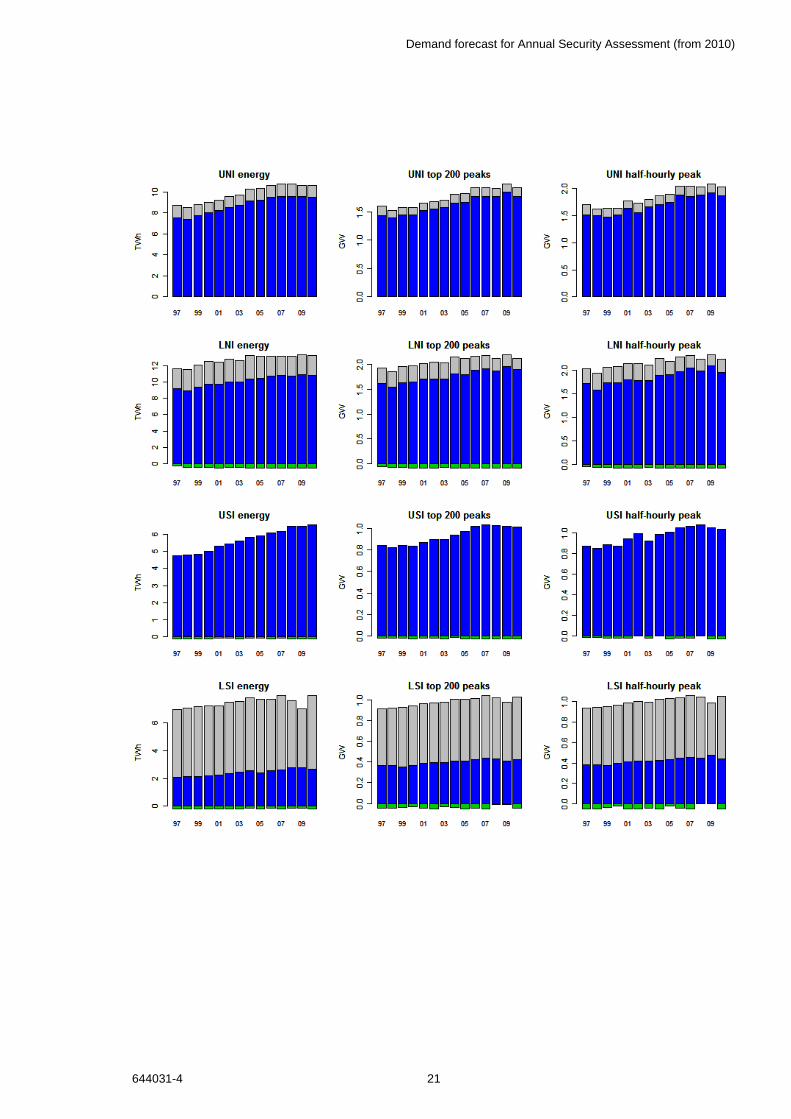

3.1.1 The historical demand data used to prepare the forecast are shown in Appendix

3. These series were derived from augmented Centralised Dataset information,

using the Gnash code in Appendix 1.

3.1.2 It should be expected that these demand figures will not be directly comparable

with those in other publications (such as the 2010 SOO), because of the

treatment of embedded generation, the calendar year (rather than March year)

basis, and some differences in region definitions. Naturally, the half-hourly peak

forecasts are not directly comparable with instantaneous peak forecasts

published elsewhere.

3.1.3 The same data are plotted in Figure 3. A note on interpretation: the position of

the top of each bar indicates the total demand less netted-off generation (this is

the quantity being forecast). The green portion below the y-axis is the embedded

generation component, including the plants listed in Table 3. The grey portion is

the industrial component, made up of the direct-connect customers listed in Table

2. Adding the blue and green portions together would yield the residual

component.

3.1.4 Two features are of particular interest:

(a) both peak and energy demand were low in 2008, 2009 and 2010, due

in part to a combination of:

(i) the 2008 dry winter and public conservation campaign, and

(ii) the 2008-09 demand reduction at the Tiwai smelter (caused by a

transformer failure).

Section 4.2 explores 2009-10 demand in more detail (in the context of

assessing the accuracy of earlier forecasts); and

(b) organic energy (as opposed to peak) growth in the North Island has been

low since 2006. The remainder of this section discusses this trend.

Demand forecast for Annual Security Assessment (from 2010)

20 644031-4

Figure 3: Historical demand data used in the forecast

Demand forecast for Annual Security Assessment (from 2010)

644031-4 21

Demand forecast for Annual Security Assessment (from 2010)

22 644031-4

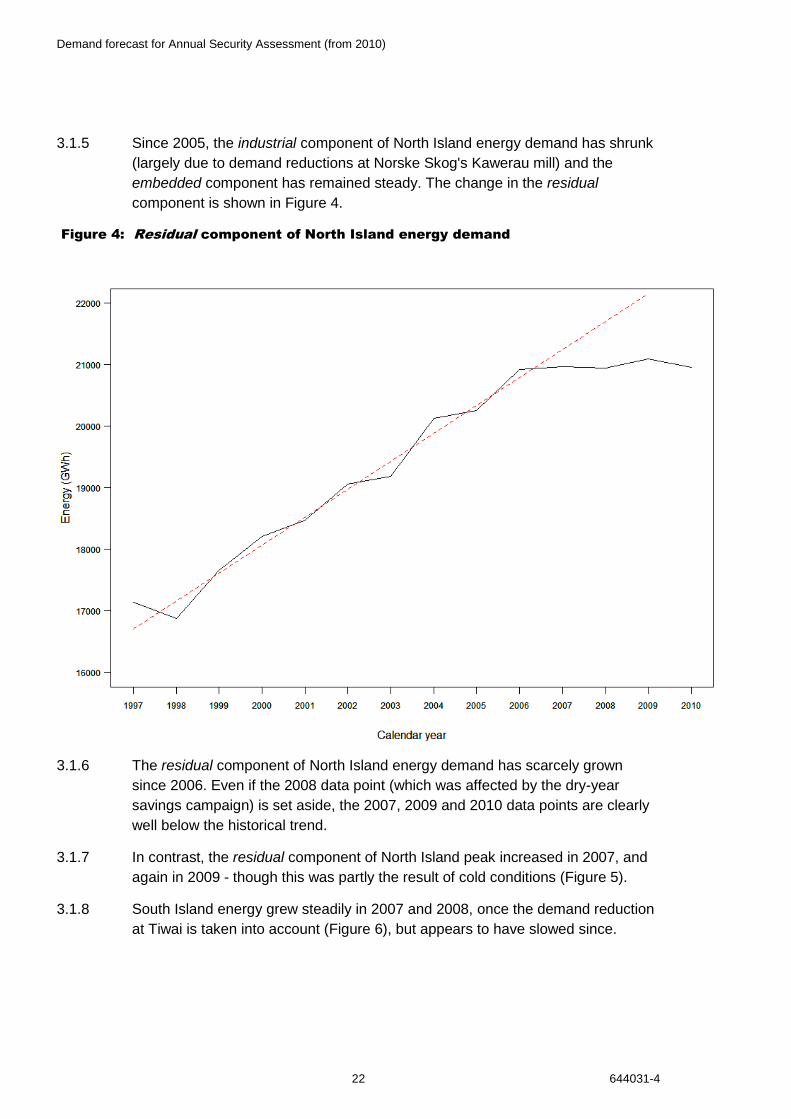

3.1.5 Since 2005, the industrial component of North Island energy demand has shrunk

(largely due to demand reductions at Norske Skog's Kawerau mill) and the

embedded component has remained steady. The change in the residual

component is shown in Figure 4.

Figure 4: Residual component of North Island energy demand

3.1.6 The residual component of North Island energy demand has scarcely grown

since 2006. Even if the 2008 data point (which was affected by the dry-year

savings campaign) is set aside, the 2007, 2009 and 2010 data points are clearly

well below the historical trend.

3.1.7 In contrast, the residual component of North Island peak increased in 2007, and

again in 2009 - though this was partly the result of cold conditions (Figure 5).

3.1.8 South Island energy grew steadily in 2007 and 2008, once the demand reduction

at Tiwai is taken into account (Figure 6), but appears to have slowed since.

Demand forecast for Annual Security Assessment (from 2010)

644031-4 23

Figure 5: Residual component of North Island peak demand

Figure 6: Residual component of South Island energy demand

Excludes Tiwai

2008 - affected by

savings campaign

2010 - mild winter

2009 - cold winter

Demand forecast for Annual Security Assessment (from 2010)

24 644031-4

3.1.9 The reasons why North Island energy growth has slowed since 2006 are not

clear. Some of the reasons could be:

(a) increased electricity efficiency;

(b) consumer response to rising electricity prices; and

(c) economic conditions.

3.1.10 However, at this stage there is no way of determining which of the above factors

has been most important.

3.1.11 The slowdown in demand growth has certainly not affected the whole country.

There have been substantial differences in recent demand growth rates between

regions of New Zealand (Table 4).

Table 4 Comparison of recent energy demand growth rates

(excluding industrial and embedded generation components)

Growth rate Regions

Highest

(over 5% p.a.)

West Coast

High

(2.5-3% p.a.)

Waikato, Bay of Plenty, South Canterbury

Average

(1.5-2% p.a.)

Auckland, Canterbury, Otago/Southland

Low

(less than 1.5%)

Central North Island, Hawkes Bay, Nelson/Marlborough, North

Isthmus/Northland, Taranaki, Wellington

Growth rates shown are based on the increase in demand from 2002-04 to 2007-09.

3.1.12 In some regions, the reasons for the observed trends are clear (e.g. dairy growth

in South Canterbury, dairy and mining on the West Coast). Others are not as

evident.

3.1.13 MED data suggests that the reduction in national energy demand growth rates

has been driven by the residential sector. According to the Energy Datafile21,

there has been substantial growth in commercial and agricultural electricity

demand in the last five years, but minimal growth in the residential sector. It is a

21

Energy Datafile, http://www.med.govt.nz/templates/MultipageDocumentTOC____43905.aspx, Table G.1

Demand forecast for Annual Security Assessment (from 2010)

644031-4 25

little hard to compare the MED figures on an 'apples vs apples' basis with those

presented here, but the result is interesting.

3.1.14 One can speculate about the extent to which electricity efficiency has helped to

restrain demand growth, and will continue to do so. According to EECA (pers.

comm.), some electricity efficiency measures that could have helped slow

demand growth over the last few years are:

(a) increased use of compact fluorescent light bulbs;

(b) replacement of traditional electric heaters with heat pumps;

(c) installation of efficient home appliances (such as whiteware and hot water

cylinders) under minimum energy performance standards (MEPS); and

(d) improvements in the industrial sector (perhaps lighting or motors).

3.1.15 All these measures (and more) will continue over the next few years, and are

expected to yield ongoing efficiency gains.

3.1.16 On the other hand, there are concerns about power-guzzling televisions,

replacement of gas and solid fuel heaters with electric heat pumps, and the

'takeback' effect (i.e. consumers responding to increased efficiency by using their

appliances more often).

3.1.17 The question for the forecaster (and the wider industry) is: will energy growth

over the next few years return to the ten-year trend, or will it continue at the

slower rate that has been seen since 2006? The base case forecasts in this

document effectively assume the former, and predict that electricity consumption

in 2011-15 will be substantially higher than in 2008-10.

3.1.18 A "hockey stick" sensitivity is also included, exploring the effect of a sustained

period of low growth (Section 6).

3.2 Demand questionnaire findings

3.2.1 This section describes the responses to the Commission's questionnaire about

potential step changes in demand and embedded generation (Section 2.3), to the

limited extent that confidentiality requirements allow.

3.2.2 Responses were received from a high proportion of questionnaire recipients. The

Commission wishes to thank all respondents.

3.2.3 In some cases the response was a simple 'no step changes expected', or the

step changes predicted did not fit the criteria for inclusion in the forecast, but

these responses were appreciated nonetheless.

Demand forecast for Annual Security Assessment (from 2010)

26 644031-4

3.2.4 Most respondents indicated that they wished the information provided to remain

confidential, and accordingly none of the responses will be published. However,

some qualitative comments about the nature of the responses are made below.

3.2.5 The following types of step changes were not used in the forecast:

(a) changes to generation that is not netted off the forecast, e.g. new wind

farms of at least 30 MW capacity or grid-connected geothermal

developments;

(b) changes of less than 5 MW;

(c) changes taking place after winter 2015;

(d) changes identified by the respondent as having a low probability; and

(e) changes to residential or commercial demand (which are intended to be

incorporated in the 'residual component' of demand, rather than modelled

separately as step changes).

3.2.6 About twenty changes remained after the above filters had been applied. As

noted in Section 2.3, each step change was assigned a probability and some

were derated as not fully additional.

3.2.7 The most significant changes over the period to 2015 relate to (in no particular

order):

(a) expected or potential production increases by major (grid-connected)

industrial consumers;

(b) new generation (small wind and hydro, embedded peakers)

(c) irrigation;

(d) mining; and

(e) new dairy processing facilities.

3.2.8 No single change was expected to have an effect of more than 20 MW.

3.2.9 Results were generally quite consistent with the 2009 survey. The 2008 survey

was more optimistic than either, featuring various new schemes throughout the

country, but economic conditions seem to have damped activity.

Demand forecast for Annual Security Assessment (from 2010)

644031-4 27

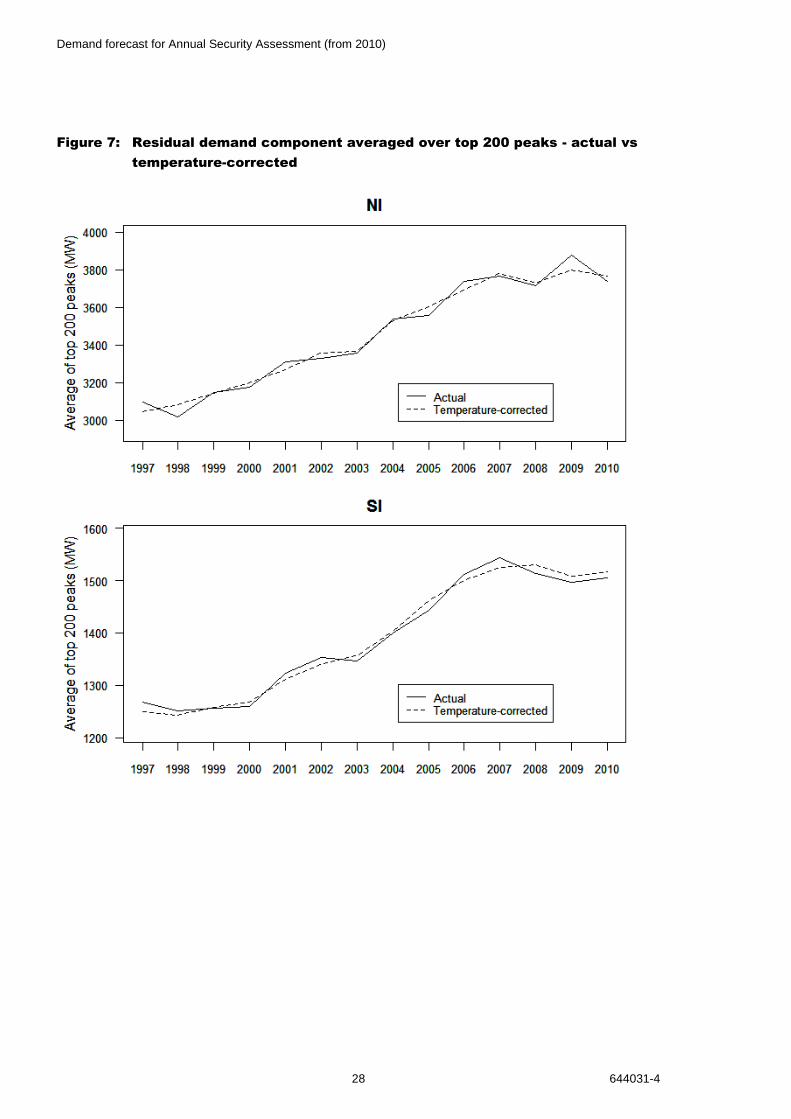

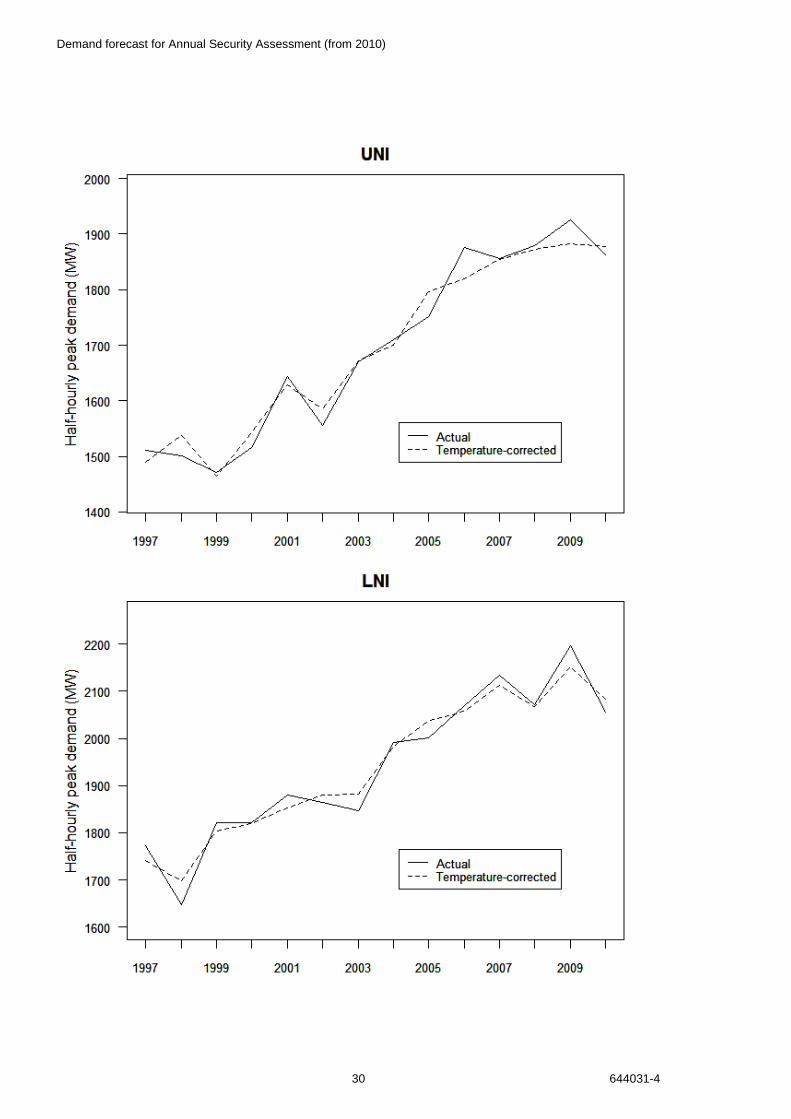

3.3 Temperature vs peak demand – results

3.3.1 The analysis of temperature vs peak demand is described in Section 2.4. This

section presents the 'temperature-corrected peaks' produced for each half-island

for each year from 1997 to 2010.

3.3.2 The analysis applies to the 'residual component' of demand only.

3.3.3 Plots of 'temperature-corrected vs actual' residual demand are shown below, for

each island (peak and top200), and each half-island (peak only). Generally,

accounting for temperature effects reduces the year-to-year variability of demand.

(The dashed series are more linear than the solid series.)

3.3.4 2006 is a good example of a year that was affected by a cold snap (for both

islands, the solid line is higher than the dashed; peak demand would have been

lower if not for cold conditions).

3.3.5 Winter 2008 was mild in the South Island and average in the North.

3.3.6 Winter 2009 was unusually cold in the North Island - with the most severe

temperature effect in the last decade - but average in the Upper South and mild

in the Lower South.

3.3.7 Winter 2010 was mild throughout the country.

Demand forecast for Annual Security Assessment (from 2010)

28 644031-4

Figure 7: Residual demand component averaged over top 200 peaks - actual vs

temperature-corrected

Demand forecast for Annual Security Assessment (from 2010)

644031-4 29

Figure 8: Residual demand component at half-hourly peak - actual vs

temperature-corrected

Demand forecast for Annual Security Assessment (from 2010)

30 644031-4

Demand forecast for Annual Security Assessment (from 2010)

644031-4 31

Demand forecast for Annual Security Assessment (from 2010)

32 644031-4

3.4 Forecasts

3.4.1 This section presents the forecasts of annual energy, half-hourly peak and

top200 (i.e. mean of the 200 highest half-hourly peaks).

3.4.2 As earlier noted, these forecasts are not directly comparable with those in other

publications (such as the 2010 SOO), because of the treatment of embedded

generation, the calendar year (rather than March year) basis, and some

differences in region definitions. Naturally, the half-hourly peak forecasts are not

directly comparable with instantaneous peak forecasts published elsewhere.

3.4.3 2010 energy figures (italic) are partially based on imputed data (since, at time of

writing, the 2010 year is not yet complete).

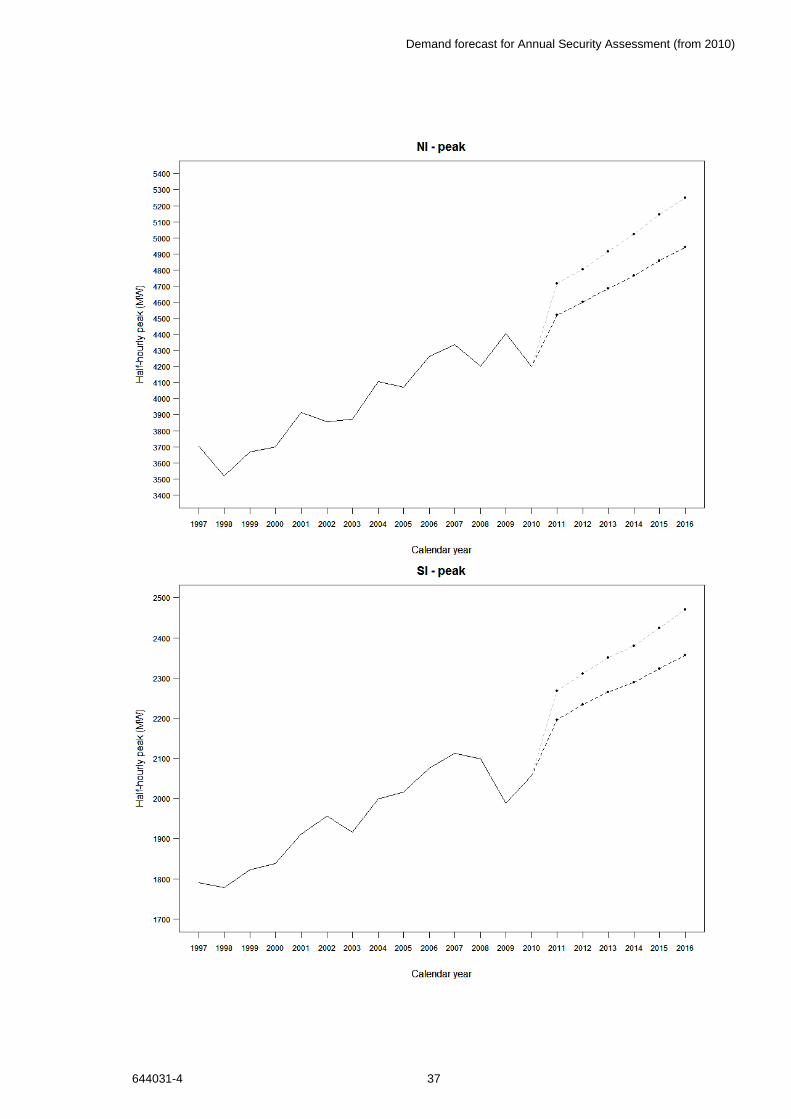

Table 5 Forecasts

Energy (GWh) Half-hourly peak (MW) Top200 (MW)

Region Year Expected Prudent Expected Prudent Expected Prudent

NZ 2004 37,150 6,022 5,859

2005 37,120 6,045 5,862

2006 37,598 6,329 6,076

2007 38,034 6,405 6,129

2008 37,912 6,185 5,970

2009 37,521 6,375 6,068

2010 38,429 6,232 6,029

2011 40,466 41,798 6,676 6,931 6,472 6,698

2012 41,239 42,655 6,800 7,065 6,591 6,827

2013 41,977 43,514 6,921 7,212 6,709 6,973

2014 42,702 44,532 7,027 7,344 6,826 7,115

2015 43,481 45,495 7,154 7,514 6,945 7,277

NI 2004 23,560 4,104 3,949

2005 23,541 4,070 3,928

2006 23,839 4,261 4,075

2007 23,909 4,335 4,093

2008 23,894 4,199 4,008

2009 24,050 4,402 4,167

2010 23,939 4,199 4,023

2011 25,309 26,367 4,520 4,713 4,338 4,511

2012 25,756 26,951 4,600 4,805 4,415 4,594

2013 26,229 27,502 4,685 4,914 4,502 4,695

2014 26,682 28,053 4,766 5,023 4,581 4,801

2015 27,141 28,734 4,855 5,144 4,670 4,913

Demand forecast for Annual Security Assessment (from 2010)

644031-4 33

Energy (GWh) Half-hourly peak (MW) Top200 (MW)

Region Year Expected Prudent Expected Prudent Expected Prudent

SI 2004 13,590 2,000 1,934

2005 13,579 2,017 1,970

2006 13,759 2,076 2,027

2007 14,125 2,113 2,065

2008 14,017 2,098 2,001

2009 13,471 1,988 1,947

2010 14,489 2,058 2,024

2011 15,145 15,444 2,195 2,267 2,150 2,227

2012 15,468 15,816 2,234 2,310 2,190 2,273

2013 15,739 16,131 2,264 2,350 2,224 2,314

2014 16,023 16,494 2,290 2,380 2,253 2,354

2015 16,321 16,874 2,322 2,424 2,287 2,402

UNI 2004 10,241 1,869 1,804

2005 10,321 1,901 1,819

2006 10,641 2,044 1,925

2007 10,730 2,043 1,929

2008 10,742 2,028 1,906

2009 10,656 2,083 1,986

2010 10,654 2,028 1,927

2011 11,418 12,058 2,145 2,270 2,046 2,133

2012 11,644 12,297 2,186 2,316 2,084 2,177

2013 11,860 12,615 2,229 2,368 2,123 2,227

2014 12,105 12,920 2,274 2,424 2,163 2,279

2015 12,369 13,222 2,321 2,487 2,210 2,335

LNI 2004 13,318 2,252 2,156

2005 13,220 2,200 2,124

2006 13,197 2,282 2,166

2007 13,178 2,318 2,177

2008 13,153 2,235 2,118

2009 13,394 2,339 2,198

2010 13,285 2,239 2,120

2011 13,909 14,382 2,416 2,537 2,302 2,394

2012 14,114 14,629 2,459 2,588 2,342 2,436

2013 14,385 14,956 2,508 2,646 2,389 2,495

2014 14,575 15,232 2,550 2,701 2,428 2,545

2015 14,782 15,542 2,592 2,759 2,470 2,600

Demand forecast for Annual Security Assessment (from 2010)

34 644031-4

Energy (GWh) Half-hourly peak (MW) Top200 (MW)

Region Year Expected Prudent Expected Prudent Expected Prudent

USI 2004 5,812 983 937

2005 5,925 1,004 968

2006 6,081 1,048 1,020

2007 6,173 1,060 1,029

2008 6,453 1,074 1,027

2009 6,455 1,046 1,019

2010 6,543 1,032 1,013

2011 6,899 7,126 1,109 1,170 1,083 1,138

2012 7,108 7,335 1,132 1,194 1,108 1,166

2013 7,311 7,582 1,154 1,225 1,130 1,192

2014 7,506 7,833 1,169 1,246 1,150 1,221

2015 7,720 8,109 1,192 1,276 1,176 1,254

LSI 2004 7,779 1,023 1,006

2005 7,654 1,030 1,008

2006 7,678 1,036 1,015

2007 7,952 1,061 1,045

2008 7,565 1,046 1,021

2009 7,015 985 976

2010 7,946 1,054 1,028

2011 8,249 8,376 1,103 1,153 1,063 1,115

2012 8,365 8,505 1,120 1,169 1,076 1,132

2013 8,442 8,602 1,130 1,182 1,086 1,142

2014 8,527 8,706 1,140 1,193 1,093 1,152

2015 8,615 8,815 1,153 1,207 1,102 1,166

Demand forecast for Annual Security Assessment (from 2010)

644031-4 35

Figure 9: Forecasts

Demand forecast for Annual Security Assessment (from 2010)

36 644031-4

Demand forecast for Annual Security Assessment (from 2010)

644031-4 37

Demand forecast for Annual Security Assessment (from 2010)

38 644031-4

Demand forecast for Annual Security Assessment (from 2010)

644031-4 39

3.4.4 For 2011, the national energy forecasts are 40,466 GWh (expected, P50) and

41,798 GWh (prudent, P95). These forecasts represent annual growth of 1.6% or

2.4% since 2007, in which the energy demand was 38,034 GWh.

3.4.5 The expected rate of energy growth from 2011 to 2015 is 2.1%.

3.4.6 For 2011, the national half-hourly peak forecasts are 6,676 MW (expected, P50)

and 6,931 MW (prudent, P95). These forecasts represent annual growth of 1.0%

(expected) or 2.0% (prudent) since 2007, in which the half-hourly peak was

6,405 MW.

3.4.7 The expected rate of peak growth from 2011 to 2015 is 2.0%.

3.4.8 Expected national energy and peak growth rates are quite similar (2.1% vs 2.0%

after 2011).

3.4.9 Energy growth is predicted to be very similar across the two islands. Peak growth

is expected to be higher in the North Island (2.2%) than the South Island (1.7%).

Demand forecast for Annual Security Assessment (from 2010)

40 644031-4

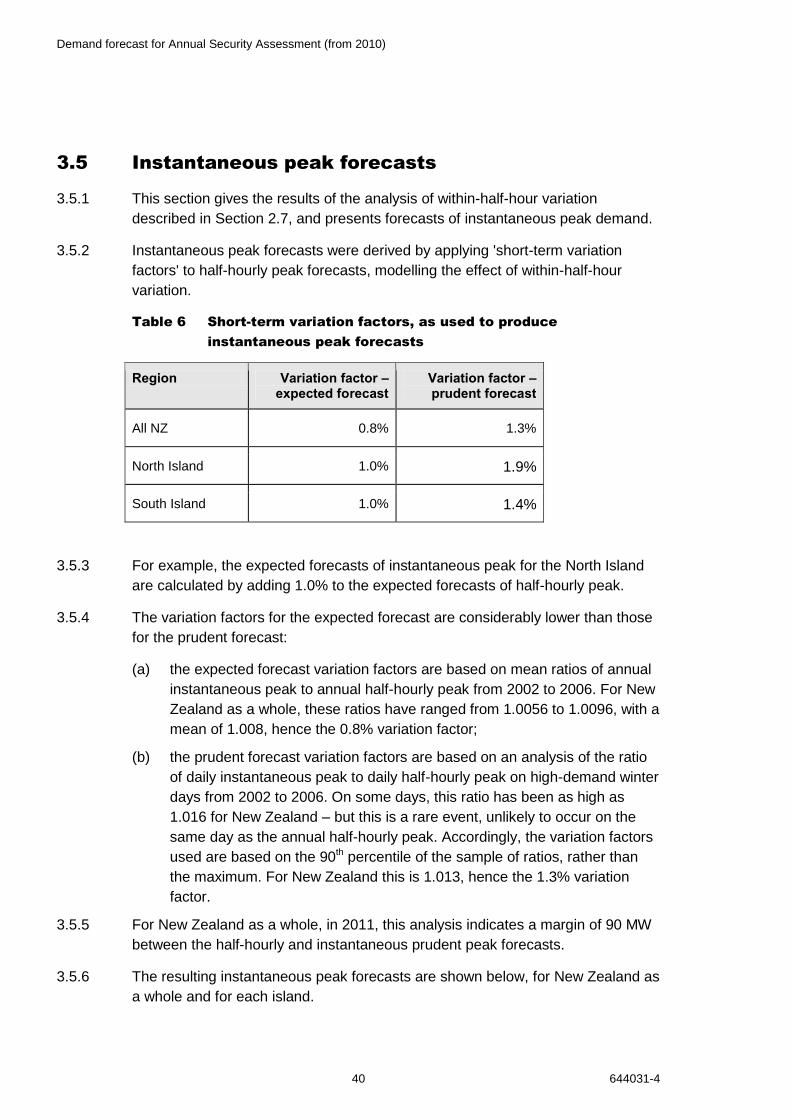

3.5 Instantaneous peak forecasts

3.5.1 This section gives the results of the analysis of within-half-hour variation

described in Section 2.7, and presents forecasts of instantaneous peak demand.

3.5.2 Instantaneous peak forecasts were derived by applying 'short-term variation

factors' to half-hourly peak forecasts, modelling the effect of within-half-hour

variation.

Table 6 Short-term variation factors, as used to produce

instantaneous peak forecasts

Region Variation factor – expected forecast

Variation factor – prudent forecast

All NZ 0.8% 1.3%

North Island 1.0% 1.9%

South Island 1.0% 1.4%

3.5.3 For example, the expected forecasts of instantaneous peak for the North Island

are calculated by adding 1.0% to the expected forecasts of half-hourly peak.

3.5.4 The variation factors for the expected forecast are considerably lower than those

for the prudent forecast:

(a) the expected forecast variation factors are based on mean ratios of annual

instantaneous peak to annual half-hourly peak from 2002 to 2006. For New

Zealand as a whole, these ratios have ranged from 1.0056 to 1.0096, with a

mean of 1.008, hence the 0.8% variation factor;

(b) the prudent forecast variation factors are based on an analysis of the ratio

of daily instantaneous peak to daily half-hourly peak on high-demand winter

days from 2002 to 2006. On some days, this ratio has been as high as

1.016 for New Zealand – but this is a rare event, unlikely to occur on the

same day as the annual half-hourly peak. Accordingly, the variation factors

used are based on the 90th percentile of the sample of ratios, rather than

the maximum. For New Zealand this is 1.013, hence the 1.3% variation

factor.

3.5.5 For New Zealand as a whole, in 2011, this analysis indicates a margin of 90 MW

between the half-hourly and instantaneous prudent peak forecasts.

3.5.6 The resulting instantaneous peak forecasts are shown below, for New Zealand as

a whole and for each island.

Demand forecast for Annual Security Assessment (from 2010)

644031-4 41

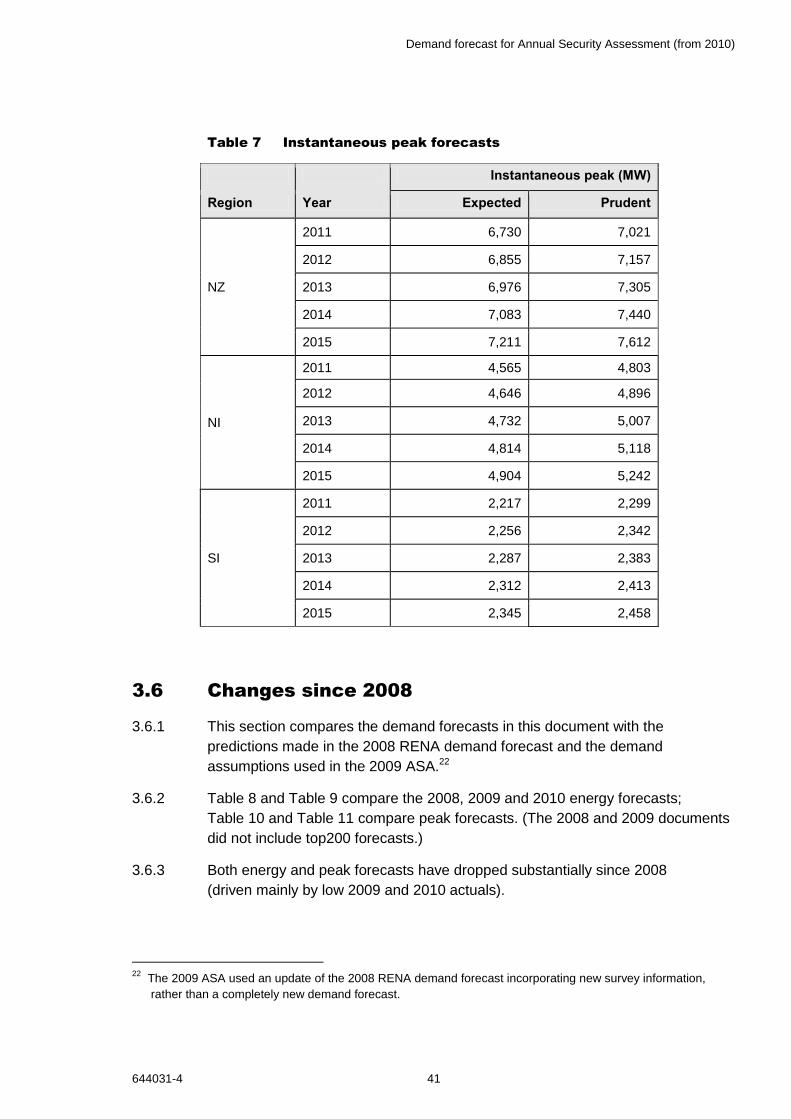

Table 7 Instantaneous peak forecasts

Instantaneous peak (MW)

Region Year Expected Prudent

NZ

2011 6,730 7,021

2012 6,855 7,157

2013 6,976 7,305

2014 7,083 7,440

2015 7,211 7,612

NI

2011 4,565 4,803

2012 4,646 4,896

2013 4,732 5,007

2014 4,814 5,118

2015 4,904 5,242

SI

2011 2,217 2,299

2012 2,256 2,342

2013 2,287 2,383

2014 2,312 2,413

2015 2,345 2,458

3.6 Changes since 2008

3.6.1 This section compares the demand forecasts in this document with the

predictions made in the 2008 RENA demand forecast and the demand

assumptions used in the 2009 ASA.22

3.6.2 Table 8 and Table 9 compare the 2008, 2009 and 2010 energy forecasts;

Table 10 and Table 11 compare peak forecasts. (The 2008 and 2009 documents

did not include top200 forecasts.)

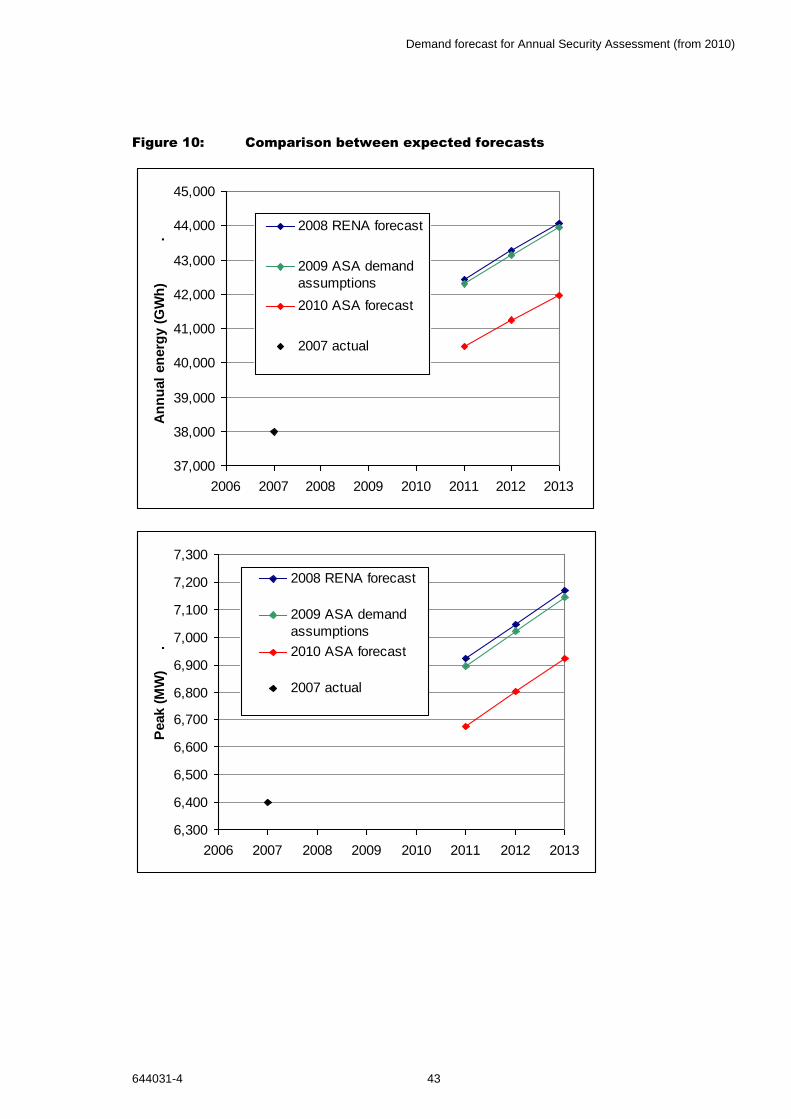

3.6.3 Both energy and peak forecasts have dropped substantially since 2008

(driven mainly by low 2009 and 2010 actuals).

22

The 2009 ASA used an update of the 2008 RENA demand forecast incorporating new survey information,

rather than a completely new demand forecast.

Demand forecast for Annual Security Assessment (from 2010)

42 644031-4

Table 8: Comparison between expected energy demand forecasts

Year 2008 RENA forecast

2009 ASA demand assumptions

2010 ASA forecast

2011 42,415 42,315 40,466

2012 43,249 43,149 41,238

2013 44,058 43,958 41,976

Table 9: Comparison between prudent energy demand forecasts

Year 2008 RENA forecast

2009 ASA demand assumptions

2010 ASA forecast

2011 43,496 43,396 41,798

2012 44,571 44,471 42,655

2013 45,602 45,502 43,514

Table 10: Comparison between expected halfhourly peak demand forecasts

Year 2008 RENA forecast

2009 ASA demand assumptions

2010 ASA forecast

2011 6,920 6,895 6,676

2012 7,047 7,022 6,800

2013 7,169 7,144 6,920

Table 11: Comparison between prudent halfhourly peak demand forecasts

Year 2008 RENA forecast

2009 ASA demand assumptions

2010 ASA forecast

2011 7,103 7,078 6,931

2012 7,266 7,241 7,065

2013 7,435 7,410 7,211

Demand forecast for Annual Security Assessment (from 2010)

644031-4 43

Figure 10: Comparison between expected forecasts

37,000

38,000

39,000

40,000

41,000

42,000

43,000

44,000

45,000

2006 2007 2008 2009 2010 2011 2012 2013

An

nu

al

en

erg

y (

GW

h)

.

2008 RENA forecast

2009 ASA demand

assumptions

2010 ASA forecast

2007 actual

6,300

6,400

6,500

6,600

6,700

6,800

6,900

7,000

7,100

7,200

7,300

2006 2007 2008 2009 2010 2011 2012 2013

Peak (

MW

)

.

2008 RENA forecast

2009 ASA demand

assumptions

2010 ASA forecast

2007 actual

Demand forecast for Annual Security Assessment (from 2010)

44 644031-4

3.7 Caveats

3.7.1 This section lists some concerns about the forecasts.

3.7.2 The forecasts do not include econometric predictors. It is fairly clear that the state

of the economy has slowed demand growth since 2008 (see sections 3.1, 4.2).

There is further economic trouble ahead - NZIER, for instance, predicts a

"slowing recovery" with "a weak patch in late 2010 and early 2011" and warns of

impending collapse in the non-residential construction sector.23 An implication is

that electricity demand growth may be lower than forecast.

3.7.3 It would be possible to model this dynamic by adding econometric predictors to

future forecasts, but this would only be useful to the extent that the state of the

economy can be predicted years in advance - a notoriously difficult problem.

3.7.4 The forecasts do not consider technological or market step changes that may

occur in future. An example would be the introduction of critical peak pricing

tariffs for residential consumers with smart meters, which would have the

potential to slow peak growth. It has also been suggested that the introduction of

plug-in electric vehicles may increase demand, but it is very unlikely that there

will be significant uptake before 2015.

3.7.5 The forecasts do not specifically model increases in electricity efficiency or an

increased focus on conservation among residential customers. These effects

have slowed demand growth in recent years (Section 3.1) and will continue to do

so - but it is not clear to what extent.

3.7.6 It may be possible to add statistics on efficient appliance sales (heat pumps,

CFLs, whiteware) to future forecasts, though obtaining the relevant data is not

straightforward.

3.7.7 The forecasts do not consider changes in how load control is used. The South

Island load controller has helped to manage peak in the winters of 2009 and

2010 (Section 4.2) and there are opportunities for future cooperation of this sort.

3.7.8 On the other hand, some parties have suggested that the use of load control to

manage peaks may decline in future (because there may not be appropriate

incentives for distributors to do so, or because the load may be controlled for

other purposes e.g. by retailers via smart meters, or because ageing ripple

control systems are not being maintained).

3.7.9 Some of these uncertainties can, perhaps, be addressed by improving the

forecasting methodology; others will only be resolved by the passage of time.

23

http://www.nzier.org.nz/Site/News/media_releases/media_releases_list.aspx

Demand forecast for Annual Security Assessment (from 2010)

644031-4 45

4. Validation

4.1 Introduction

4.1.1 This section describes the analysis carried out to validate the forecasts in this

document.

4.1.2 There are three main approaches to validation:

(a) comparing predicted demand to recent historical demand;

(b) comparing predicted demand to actual demand, once the actual demand

data become available; and

(c) out of sample forecasting – carrying out forecasts for years that have

already occurred, based on the information that would have been available

in advance, and comparing these 'out of sample forecasts' with actual

demand.

4.1.3 On (a), the near-future growth rates predicted in the 'expected' forecasts are

broadly consistent with growth rates in the last decade.

4.1.4 On (b), comparisons of predictions for 2009-10 in the 2008 RENA demand

forecast with actual 2009-10 demand are provided in Section 4.2.

4.1.5 In theory, predictions for 2008 could also be compared with actual 2008 demand.

However, electricity demand in 2008 was depressed by the dry year and resulting

public conservation campaign, so this has not been done.

4.1.6 On (c), an out of sample analysis was carried out as part of the 2007 RENA

demand forecast and has not been repeated this year.

Demand forecast for Annual Security Assessment (from 2010)

46 644031-4

4.2 Validation of the predictions for 2009 and 2010

4.2.1 Actual energy and peak demand figures for 2009, and peak demand figures for

2010, are now available. In this section, these actuals are compared with the

predictions for 2009 in the 2008 RENA demand forecast.

4.2.2 The aim of the analysis is to gain information about the performance of the

demand forecasting methodology over very short time scales.

4.2.3 We first consider half-hourly peak predictions for 2009.

Table 12 Predicted 2009 half-hourly peaks vs actual values

Region Actual peak (MW)

Expected forecast (MW)

Prudent forecast (MW)

Actual minus expected (MW, %)

NZ (*) 6,374 6,646 6,791 -272 (-4.1%)

NI 4,402 4,494 4,626 -92 (- 2.0%)

SI (*) 1,988 2,211 2,270 -223 (-10.0%)

UNI 2,082 2,111 2,235 -29 (-1.4%)

LNI 2,338 2,412 2,505 -74 (-3.1%)

USI 1,045 1,131 1,180 -86 (-7.6%)

LSI (*) 984 1,096 1,135 -112 (-10.2%)

(*) - Affected by reduction in Tiwai consumption following transformer failure in 2008

Figures shown will not correspond exactly to figures published elsewhere, due to different

treatment of netted-off generation.

4.2.4 All peak demand forecasts for 2009 in the 2008 RENA forecast were too high.

4.2.5 New Zealand peak demand was 270 MW (4%) below the expected forecast.

In part this was a consequence of unexpectedly low demand at the NZAS

aluminium smelter (following a transformer failure in 2008), which led to Lower

South Island peak being 110 MW (10%) below forecast.

4.2.6 However, peak forecasts were also too high for regions that do not include the

Tiwai smelter.

Demand forecast for Annual Security Assessment (from 2010)

644031-4 47

4.2.7 North Island peak demand was 90 MW (2%) below the expected forecast, largely

due to reductions in the industrial component of peak - the residual and

embedded components were accurately predicted. This result should be taken in

context of a cold North Island winter (Section 3.3) - had temperatures been

milder, the gap between actual and expected demand would have been higher.

4.2.8 Upper South Island peak demand was 86 MW (7.6%) below the expected

forecast, despite average weather in mid-late winter.24 We believe this was a

result of several factors, including:

(a) the introduction of the Upper South Island load controller in March 200925,

which has been estimated to have reduced peak load by 30 MW over the

winter26;

(b) the economic downturn; and

(c) energy efficiency and fuel switching.

24

South Island weather was unusually cold in early winter, but this period did not set the annual island peak

because Tiwai demand was still low.

25 http://www.oriongroup.co.nz/load-management/Upper-south-island-load-management.aspx

26 http://www.oriongroup.co.nz/downloads/USI_Load_Management_annual_progress_reportFeb10.pdf

Demand forecast for Annual Security Assessment (from 2010)

48 644031-4

4.2.9 We next consider half-hourly peak predictions for 2010.

Table 13 Predicted 2010 half-hourly peaks vs actual values

Region Actual peak (MW)

Expected forecast (MW)

Prudent forecast (MW)

Actual minus expected (MW, %)

NZ 6,232 6,796 6,954 -564 (-8.3%)

NI 4,199 4,607 4,751 -408 (-8.9%)

SI 2,058 2,248 2,309 -190 (-8.5%)

UNI 2,028 2,182 2,309 -154 (-7.1%)

LNI 2,239 2,457 2,555 -218 (-8.9%)

USI 1,032 1,154 1,205 -122 (-10.6%)

LSI 1,054 1,111 1,153 -57 (-5.1%)

(*) - Slightly affected by reduction in Tiwai consumption

Figures shown will not correspond exactly to figures published elsewhere, due to different

treatment of netted-off generation.

4.2.10 All peak demand forecasts for 2010 in the 2008 RENA forecast were much too

high.

4.2.11 We attribute this to a combination of several factors, including:

(a) a mild winter;

(b) Tiwai demand still being slightly below normal;

(c) reduced demand by North Island industrial consumers at peak times;

(d) the effect of the Upper South Island load controller;

(e) the economic downturn; and

(f) energy efficiency and fuel switching.

Demand forecast for Annual Security Assessment (from 2010)

644031-4 49

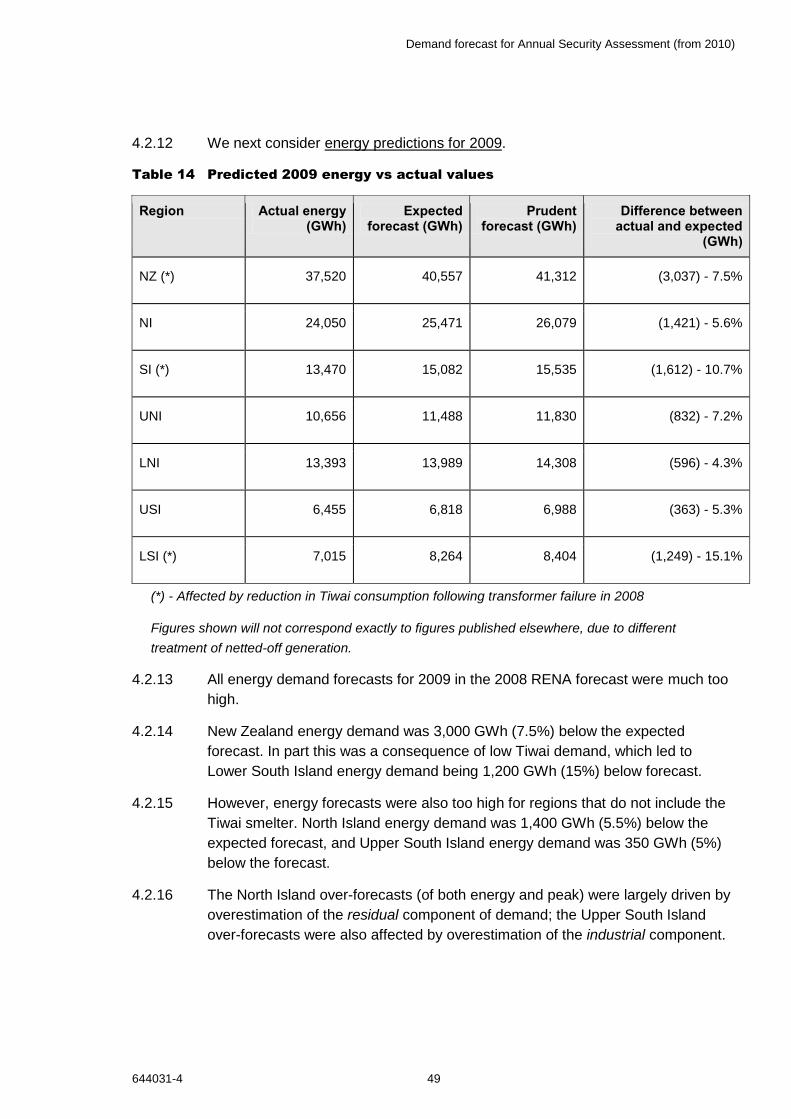

4.2.12 We next consider energy predictions for 2009.

Table 14 Predicted 2009 energy vs actual values

Region Actual energy (GWh)

Expected forecast (GWh)

Prudent forecast (GWh)

Difference between actual and expected

(GWh)

NZ (*) 37,520 40,557 41,312 (3,037) - 7.5%

NI 24,050 25,471 26,079 (1,421) - 5.6%

SI (*) 13,470 15,082 15,535 (1,612) - 10.7%

UNI 10,656 11,488 11,830 (832) - 7.2%

LNI 13,393 13,989 14,308 (596) - 4.3%

USI 6,455 6,818 6,988 (363) - 5.3%

LSI (*) 7,015 8,264 8,404 (1,249) - 15.1%