17

Cisco Live Australia’s Demographic Change Predictions and How They Will Affect Business Through the 2020s Bernard Salt 17 March 2015

Cisco LiveAustralia’s Demographic Change

Predictions and How They Will Affect Business Through the 2020s

Bernard Salt

17 March 2015

© 2014 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMGInternational Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

The KPMG name, logo and "cutting through complexity" are registered trademarks or trademarks of KPMG International Cooperative ("KPMG International"). Liability limited by a scheme approved under Professional Standards Legislation.

Disclaimer

These slides are not for commercial use or redistribution. The information contained herein is of a generalnature and is not intended to address the circumstances of any particular individual or entity. No one should acton such information without appropriate professional advice after a thorough examination of the particularsituation. KPMG have indicated within this presentation the sources of the information provided. KPMG has notsought to independently verify those sources unless otherwise noted within the presentation. No relianceshould be placed on additional oral remarks provided during the presentation, unless these are confirmed inwriting by KPMG. KPMG is under no obligation in any circumstance to update this presentation, in either oral orwritten form, for events occurring after the presentation has been issued in final form. The findings in thispresentation have been formed on the above basis.

Forecasts are based on a number of assumptions and estimates and are subject to contingencies anduncertainties. Forecasts should not be regarded as a representation or warranty by or on behalf of KPMG orany other person that such forecasts will be met. Forecasts constitute judgment and are subject to changewithout notice, as are statements about market trends, which are based on current market conditions.

Neither KPMG nor any member or employee of KPMG undertakes responsibility arising in any way fromreliance placed by a third party on this presentation. Any reliance placed is that party’s sole responsibility. Thepresentation (and the accompanying slide pack) is provided solely for the benefit of the conference attendeesand is not to be copied, quoted or referred to in whole or in part without KPMG’s prior written consent. KPMGaccepts no responsibility to anyone other than the conference attendees for the information contained in thispresentation.

Sydney

Melbourne

Hobart

Adelaide

Perth

Darwin

Brisbane

Canberra

Source: Based on Australian Bureau of Statistics data; KPMG Demographics

Australians have always been driven by lifestyle

Areas of high population growth (>2% pa) and loss (<-1% pa) between 1992 and 2013

WINNERS

LOSERS

© 2014 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMGInternational Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

The KPMG name, logo and "cutting through complexity" are registered trademarks or trademarks of KPMG International Cooperative ("KPMG International"). Liability limited by a scheme approved under Professional Standards Legislation.

Strong population growth is driving household formation

Actual and projected net annual population growth for Australia between 1950 and 2050

221,000

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

400,000

450,000

500,000

1950

1952

1954

1956

1958

1960

1962

1964

1966

1968

1970

1972

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

2014

2016

2018

2020

2022

2024

2026

2028

2030

2032

2034

2036

2038

2040

2042

2044

2046

2048

2050

Natural Increase Net Overseas Migration

368,000

354,000

Source: based on medium ABS 2013 NOM projections, ABS 2013 NI projections and ABS Financial Year 2014 actual data projected to Calendar Year 2014

© 2014 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMGInternational Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

The KPMG name, logo and "cutting through complexity" are registered trademarks or trademarks of KPMG International Cooperative ("KPMG International"). Liability limited by a scheme approved under Professional Standards Legislation.

Australia is now an Anglo-Mediterranean-Asian-Indian fusion culture

Source: Based on Australian Bureau of Statistics data; KPMG Demographics

1.2 millionUnited Kingdom1

New Zealand609,0002

China428,0003

India370,0004

Vietnam215,0005

211,000Philippines6

Italy199,0007

South Africa174,0008

Malaysia149,0009

Germany128,00010

Top 10 population by country of birth in Australia 2013

© 2014 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMGInternational Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

The KPMG name, logo and "cutting through complexity" are registered trademarks or trademarks of KPMG International Cooperative ("KPMG International"). Liability limited by a scheme approved under Professional Standards Legislation.

Recent migrants are in the household formation stage of the lifecycle

Source: Based on Australian Bureau of Statistics data; KPMG Demographics

Age of population by country of birth 2011

0%

1%

2%

3%

4%

5%

1 3 5 7 9 11 13 15 17 19 21 23 25 27 29 31 33 35 37 39 41 43 45 47 49 51 53 55 57 59 61 63 65 67 69 71 73 75 77 79 81 83 85 87 89 91 93 95 97 99 101

Australia China India England Italy Greece New Zealand

China

India

England

Greece

Italy

NZ

© 2014 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMGInternational Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

The KPMG name, logo and "cutting through complexity" are registered trademarks or trademarks of KPMG International Cooperative ("KPMG International"). Liability limited by a scheme approved under Professional Standards Legislation.

New acronyms for our newest tribes

PUMCINS …→ Professional Urban Middle Class In Nice Suburbs

…NETTELs ←Not Enough Time To Enjoy Life

KIPPERS …→ Kids In Parents Pockets Eroding Retirement Savings

…LOMBARDS←Lots Of Money But A Real Dickhead

Source: KPMG Demographics

© 2014 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMGInternational Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

The KPMG name, logo and "cutting through complexity" are registered trademarks or trademarks of KPMG International Cooperative ("KPMG International"). Liability limited by a scheme approved under Professional Standards Legislation.

Most growth takes place in the middle Australia of middle suburbia

Source: Based on Australian Bureau of Statistics data; KPMG Demographics

Hipster Middle Australia McMansion

<5km 5-15km 15-25km >25km Total Growth

Sydney 8,000 22,500 22,300 28,200 81,000Melbourne 17,300 19,900 28,800 29,500 95,500Brisbane 5,800 10,700 13,400 15,200 45,100Perth 5,100 21,800 18,600 22,000 67,500Adelaide 1,500 6,400 1,100 4,100 13,100

Big Capitals 37,700 81,300 84,200 99,000 302,200Balance - - - - 104,800Total Australia - - - - 407,000• Net population growth in concentric zones around the CBD of our largest cities over the year end June 2013

© 2014 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMGInternational Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

The KPMG name, logo and "cutting through complexity" are registered trademarks or trademarks of KPMG International Cooperative ("KPMG International"). Liability limited by a scheme approved under Professional Standards Legislation.

Net change in Australian population by 5-year age group over 10 years to 2013 and 10 years to 2023Source: Based on Australian Bureau of Statistics data; KPMG Demographics

New business opportunities are being shaped by changes in the Australian demographic profile

-

50,000

100,000

150,000

200,000

250,000

300,000

350,000

400,000

450,000

500,000

0-4 5-9 10-14 15-19 20-24 25-29 30-34 35-39 40-44 45-49 50-54 55-59 60-64 65-69 70-74 75-79 80-84 85+

2003-2013: 3.4 million (19.7m to 23.1m) 2013-2023: 4.2 million (23.1m to 27.3m)

Mature adults

Premium products

Active retirees

Travel & wellness

Kids & teenagers

Suburbia & school

Young adults

Social media & connectivity

© 2014 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMGInternational Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

The KPMG name, logo and "cutting through complexity" are registered trademarks or trademarks of KPMG International Cooperative ("KPMG International"). Liability limited by a scheme approved under Professional Standards Legislation.

Australians are dividing the lifecycle into ‘thirds’

Source: Based on Australian Bureau of Statistics data; KPMG Demographics

0 9010 20 30 40 50 60 70 80

Child Adult Old1934

Child Teen OldAdult1974 71

Child Adolescence Lifestyle OldRetired2014

Adult82

63

Change in life expectancy over 80 years in Australia

© 2014 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMGInternational Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

The KPMG name, logo and "cutting through complexity" are registered trademarks or trademarks of KPMG International Cooperative ("KPMG International"). Liability limited by a scheme approved under Professional Standards Legislation.

From Boomers to Xers and Ys … and finally to Zeds

Source: KPMG Demographics

Forgotten generationWrong place … wrong timeNo workplace guiltAngsty about Ys

XGENERATION

■ Born 1965 – 1982■ Today 32 – 49

HierarchicalIndulged their kidsDepression era parentsSandwich generation

BABYBOOMERS

■ Born 1946 – 1964■ Today 50 – 68

YGENERATION

Special … bubble-wrapChaotic connectionEntrepreneurialsDisappointed generation?

■ Born 1983 – 2000■ Today 14 – 31

Parents results-orientedYouth in straitened timesHighly educated, globalPragmatists … fixers

ZGENERATION

■ Born 2001 – 2019■ Today 0 – 13

© 2014 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMGInternational Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

The KPMG name, logo and "cutting through complexity" are registered trademarks or trademarks of KPMG International Cooperative ("KPMG International"). Liability limited by a scheme approved under Professional Standards Legislation.

2014-20153.0%4.6%0.7%3.4%7.4%-3.3%0.1%8.6%11.6%6.3%

13.6%1.4%

-12.7%4.0%

Sometimes business just isn’t fair … who’s doing well and who isn’t?

Per cent change in retail sales in Australia for 13 categories over ten and five years and over 12 months to Jan-2015

Source: Based on Australian Bureau of Statistics data; KPMG Demographics

2010-201521.1%49.9%26.8%24.5%16.9%16.1%21.1%36.6%4.0%

16.7%8.2%0.1%

-26.3%20.5%

2005-2015121.0%100.7%89.6%75.8%73.2%50.9%47.1%44.4%39.1%37.3%31.1%18.0%-23.5%58.3%

IndustryLiquorCafes, restaurants & catering Pharmaceutical, cosmetic & toiletriesSupermarket & grocery storesTakeaway foodRecreational goodsClothingHardware, building & garden suppliesElectrical & electronic goodsFurniture, floor coverings, housewares, textilesFootwear & other personal accessoriesDepartment storesNewspapers & booksTotal (incl other)

© 2014 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMGInternational Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

The KPMG name, logo and "cutting through complexity" are registered trademarks or trademarks of KPMG International Cooperative ("KPMG International"). Liability limited by a scheme approved under Professional Standards Legislation.

There has been a shift in the Australian economy towards knowledge workers

Hea

lthca

re&

Soc

ial A

ssis

t.

Prof

essi

onal

/Sc

ient

ific/

Tech

.

Publ

ic A

dmin

&

Saf

ety

Adm

in &

Sup

port

Acco

m &

Foo

d

Ret

ail T

rade

Con

stru

ctio

n

Educ

atio

n &

Trai

ning

Arts

& R

ecre

atio

n

Fina

ncia

l &In

sura

nce

Min

ing

Oth

er s

ervi

ces

Who

lesa

le T

rade

Ren

tal/h

iring

&R

eal E

stat

e

Info

Med

ia &

Te

leco

ms

Man

ufac

turin

g

6 years November 2008 – up 1.5m (9.3m – 10.8m)

Source: Based on Australian Bureau of Statistics data; KPMG Demographics

Elec

tric

ity/G

as/

Wat

er &

Was

te

Agric

ultu

re/F

ores

try

& F

ishi

ng

Tran

spor

t/Pos

tal/

War

ehou

se

-100,000

-50,000

0

50,000

100,000

150,000

200,000

250,000

300,000 6 years November 2014 – up 0.9m (10.8m – 11.6m)Healthcare &

Social Assistance

Professionals & Sciences

EducationAccommodation& Food

© 2014 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMGInternational Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

The KPMG name, logo and "cutting through complexity" are registered trademarks or trademarks of KPMG International Cooperative ("KPMG International"). Liability limited by a scheme approved under Professional Standards Legislation.

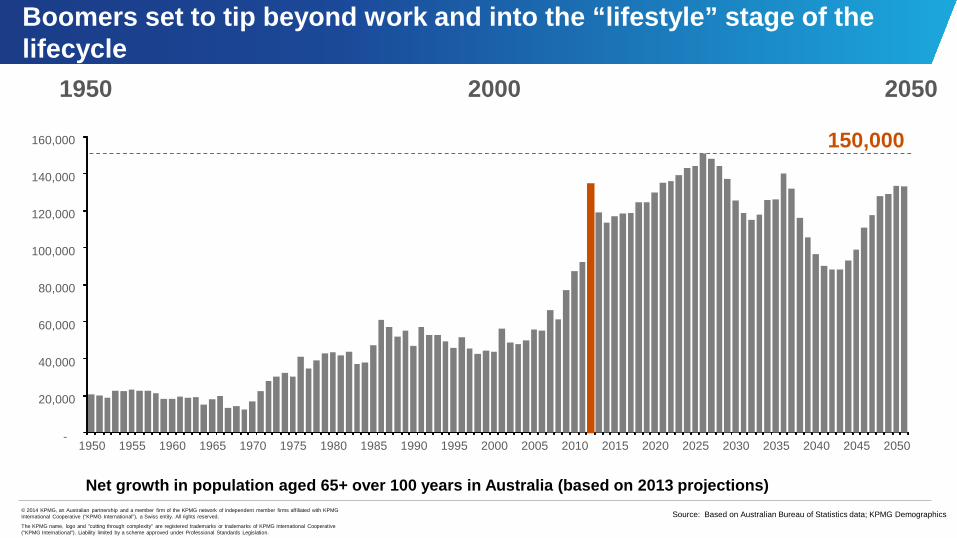

Boomers set to tip beyond work and into the “lifestyle” stage of the lifecycle

Net growth in population aged 65+ over 100 years in Australia (based on 2013 projections)

150,000

1950 20502000

Source: Based on Australian Bureau of Statistics data; KPMG Demographics

-

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

1950 1955 1960 1965 1970 1975 1980 1985 1990 1995 2000 2005 2010 2015 2020 2025 2030 2035 2040 2045 2050

© 2014 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMGInternational Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

The KPMG name, logo and "cutting through complexity" are registered trademarks or trademarks of KPMG International Cooperative ("KPMG International"). Liability limited by a scheme approved under Professional Standards Legislation.

Source: KPMG Demographics

Where are the opportunities in 2015

Population growth at close to record levels … business opportunities in household formation and infrastructure means tradies doing well

The consumer and lifestyle models are changing … new retail and housing formats evolving and especially in the inner city

Reasons to be positive … low interest rates, low dollar, low petrol prices, no natural disasters … time to move on from the GFC

Specific opportunities in healthcare, education, building & construction, retirement financial planning and succession planning services

Cultural shifts in Australia are resulting in an Anglo-Mediterranean-Asian fusion culture … look to more Asian influences in the future especially China

Australians are optimistic about the future … but they will want to protect wealthand mitigate risk

© 2014 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMGInternational Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

The KPMG name, logo and "cutting through complexity" are registered trademarks or trademarks of KPMG International Cooperative ("KPMG International"). Liability limited by a scheme approved under Professional Standards Legislation.

Introducing Melbourne’s bachelor hotspot …

Source: Based on Australian Bureau of Statistics data; KPMG Demographics

Hotspot suburbs for single men and women aged 25-34 at the 2011 Census

“Racecourse of Love”Flemington Racecourse

West Footscray2.08:1

Flemington1.41:1

© 2014 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMGInternational Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

The KPMG name, logo and "cutting through complexity" are registered trademarks or trademarks of KPMG International Cooperative ("KPMG International"). Liability limited by a scheme approved under Professional Standards Legislation.

@bernardsalt

Bernard Salt Demographer

linkedin.com/in/bernardsalt

+61 3 9288 5047

www.bernardsalt.com.au

@bernardsalt

Connect

![FY16 Presentation FINAL (002) [Read-Only]presentation. Such forecasts, prospects, statement or returns are by their nature subject to significant uncertainties and contingencies. Actual](https://static.documents.pub/doc/80x56/5f238304d4d9a60b02570ce8/fy16-presentation-final-002-read-only-presentation-such-forecasts-prospects.jpg)