Departement SAEMQ, University of Bergamo February-March 2015 International Monetary Economics course (taught by Riccardo Bellofiore, Stefano Lucarelli and Jan Toporowski) JAN TOPOROWSKI LECTURES transcript by Lecture 1: Michela Locatelli, Silvia Maggi, Diana Brambilla, Chiara Carissimi. Lecture 2: Ilaria Brivio, Sophie Ciacciarelli, Marco Fassina, Federica Tarantino, Sara Tinelli Lecture 3: Brando Viganò, Claudio Iacopino, Simone Perego, Michael Ravelli Lecture4: Sara Brevi, Roberto Moroni, Federica Rota, Niccolo’ Suardi, Rudy Zanoli Lecture 5: Invernici Elena and Vailati Valeria Lecture 6: Antonella Cordaro, Laura Birbes, Mattia Ferrarin, Silvia Bacis, Souad El Khadir Lecture 7: Polina Vasileva, Salam Aslam and Alina Giachin revised by Patrizio Lainà, Ph.D. University of Helsinki, Visiting Scholar at Department SAEMQ, University of Bergamo 1 1. TOPOROWSKI LECTURE TRANSCRIPTION 1 st LECTURE – University of Bergamo, Friday 20 th February 2015 Performed by Michela Locatelli, Silvia Maggi, Diana Brambilla, Chiara Carissimi. Introduction : These lectures have been a great stimulus to my own thinking and to my own research because they have challenged me to think what is international money really about, what is the connection between international money and macro economy. In particular, how it is connected to the problems of the Eurozone. Money credit concept I’ll give you an Outline of the rest of the course at the end of this lecture. These lectures are new, there is not a textbook about this, I refer to some literature, but there is not one book or one paper where you can find all of this. It’s a synthetic discussion of money and the macro economy and how macroeconomic imbalances fit into international money. - Introduction of Theories of International Money - Credit and Finance: usually in the text books credit and finance are treated as savings and very usually divided, I want to treat them more specifically from an historical perspective. - Varieties of International monetary circulation: how money circulates in the modern globalised economy - Overview of the whole course in one table which shows the whole course. That’s what you have to remember to fit the other lectures in. 1.Introduction of Theories of International Money Essentially, what I’m looking at is a macro economic theory of money, in other words, an explanation of what money does in any economy, and its role in economic crisis. This has to be understood, without it, it is not possible to understand the role of money. As we will see later on, there are theories of explanations of money which talk about how useful it is in exchange; these kinds of explanations that’s not all the money does in the modern economy. We need to know the traditional ones. Let’s consider the theories that explain the functions of essential properties of money. If you look at a standard textbook of money, it would tell you that money has to be scarce, divisible, quotable, essential features. The functions of money: mean of exchange, unit of account, store of value. These are all features of money, but they don’t tell you what money does in a modern international economy. Those kind of definitions we had had since the XIX century, money has changed very much since the XIX century. Theory of money has an explanation of what money does in an economy and its role in economic crisis, this requires an explanation of the economy in which money functions. This is why you can’t understand money by looking at its functions or its properties. Nor we understand money by knowing that once it was gold, or that money is what the government says it’s money or money is what we use to pay taxes. We need to understand how money functions in an economy, so we need to understand the economy in which it works. This was done by Joseph Schumpeter who distinguished between, first of all, commodity theories of money in which money is related to some commodity (ex. gold) and therefore to obtain it through exchange. Because a commodity is what you exchange. That’s a relatively simple first type of money. Money which comes from trade or money which is used to trade. Schumpeter distinguished that this is one money but nowadays we use credit. What is credit? Well, you have monetary theories of credit where money that is obtained through exchange is deposited into a 2

Transcript

Departement SAEMQ, University of Bergamo

February-March 2015

International Monetary Economics course

(taught by Riccardo Bellofiore, Stefano Lucarelli and Jan Toporowski)

Lecture 2: Ilaria Brivio, Sophie Ciacciarelli, Marco Fassina, Federica Tarantino, Sara TinelliLecture 3: Brando Viganò, Claudio Iacopino, Simone Perego, Michael RavelliLecture4: Sara Brevi, Roberto Moroni, Federica Rota, Niccolo’ Suardi, Rudy Zanoli Lecture 5: Invernici Elena and Vailati ValeriaLecture 6: Antonella Cordaro, Laura Birbes, Mattia Ferrarin, Silvia Bacis, Souad El Khadir Lecture 7: Polina Vasileva, Salam Aslam and Alina Giachin

revised by Patrizio Lainà,

Ph.D. University of Helsinki, Visiting Scholar at Department SAEMQ, University of Bergamo

1

1. TOPOROWSKI LECTURE TRANSCRIPTION

1st LECTURE – University of Bergamo, Friday 20th February 2015

Performed by Michela Locatelli, Silvia Maggi, Diana Brambilla, Chiara Carissimi.

Introduction:These lectures have been a great stimulus to my own thinking and to my own research because theyhave challenged me to think what is international money really about, what is the connection betweeninternational money and macro economy. In particular, how it is connected to the problems of theEurozone. Money credit conceptI’ll give you an Outline of the rest of the course at the end of this lecture.These lectures are new, there is not a textbook about this, I refer to some literature, but there is not onebook or one paper where you can find all of this. It’s a synthetic discussion of money and the macroeconomy and how macroeconomic imbalances fit into international money.

- Introduction of Theories of International Money

- Credit and Finance: usually in the text books credit and finance are treated as savings and very

usually divided, I want to treat them more specifically from an historical perspective.

- Varieties of International monetary circulation: how money circulates in the modern globalised

economy

- Overview of the whole course in one table which shows the whole course. That’s what you

have to remember to fit the other lectures in.

1.Introduction of Theories of International MoneyEssentially, what I’m looking at is a macro economic theory of money, in other words, an explanationof what money does in any economy, and its role in economic crisis. This has to be understood,without it, it is not possible to understand the role of money. As we will see later on, there are theoriesof explanations of money which talk about how useful it is in exchange; these kinds of explanationsthat’s not all the money does in the modern economy. We need to know the traditional ones.Let’s consider the theories that explain the functions of essential properties of money. If you look at astandard textbook of money, it would tell you that money has to be scarce, divisible, quotable, essentialfeatures. The functions of money: mean of exchange, unit of account, store of value. These are allfeatures of money, but they don’t tell you what money does in a modern international economy. Thosekind of definitions we had had since the XIX century, money has changed very much since the XIXcentury.Theory of money has an explanation of what money does in an economy and its role in economiccrisis, this requires an explanation of the economy in which money functions. This is why you can’tunderstand money by looking at its functions or its properties. Nor we understand money by knowingthat once it was gold, or that money is what the government says it’s money or money is what we useto pay taxes. We need to understand how money functions in an economy, so we need to understandthe economy in which it works. This was done by Joseph Schumpeter who distinguished between, first of all, commodity theories ofmoney in which money is related to some commodity (ex. gold) and therefore to obtain it throughexchange. Because a commodity is what you exchange. That’s a relatively simple first type of money.Money which comes from trade or money which is used to trade. Schumpeter distinguished that this is one money but nowadays we use credit. What is credit? Well, youhave monetary theories of credit where money that is obtained through exchange is deposited into a

2

bank which lends the money out. So here we have this idea that there is credit, but credit operates aspurely as intermediation. Banking and finance it is pure intermediation: it’s taking the money that Idon’t want to use today and lending it to someone else who wants to use it today. Commodity or fiatmoney, just simply put into a bank and then lend it out today. What I want to argue is that this explainshow money operates in an exchange economy or in a merchant capitalist economy. I buy goods, I haveto pay money for them, I take them to the market, I sell them for more money and in exchange formoney. I may finance this by borrowing money from a bank; that is a relatively simple economy andeven if you do have a credit it’s a relatively simple credit.What we need to distinguish here is a different type of money which is a pure credit money or Credittheories of money. These are the theories that you can find in Keynes, Wicksell and Schumpeter. I willdiscuss this more in the coming lectures because they actually changed the way in which the economyworks and I’ll explain this later on. Let me just say what Schumpeter had to say about these theories. Ifyou read a text book, they would tell you: yes, money was notes and coins, then there were bank notesand now we use bank deposits, but it’s the same thing. It is not the same thing, although the text bookstell you it is, it isn’t. Schumpeter when considering these views, he explained the situation as follows, and this is one of hismost important quotations: “…logically it is by no means clear that the most useful method (in the analysis of money) is to startfrom the coin (i.e. metallic money) – even if, making a concession to realism, we add inconvertiblegovernment paper (i.e. paper money or government bonds) – in order to proceed to the credittransactions of reality. It may be more useful to start from these (credit transactions) in the first place,to look upon capitalist finance as a clearing system that cancels claims and debts and carriesforward the differences … In other words, practically and analytically, a credit theory of money ispossibly preferable to a monetary theory of credit.’(Schumpeter 1954 p. 717) The monetary theory of credit was the stereo credit in which money is put into a bank end the banklends the money out. The other system, which Schumpeter was referring, is capitalist finance as aclearing system that cancels claims and debts and carries forward the differences. Here Schumpeter waslooking at the practice how banks operate when clearing payments. When payments are cleared, if youpay with a debit card in a shop, what the shop gets it’s a record of your payment and it gives that to itsbanker and the shop’s banker takes it to your banker and says: please, pay this from this person’saccount. In average, yesterday they would have made each payment like this. What they do today is thatthe shop’s banker will take the instructions to pay to your bank, your bank will show the shop’s bank allthe payment instructions that it has from the shop’s bank, they will add all these up and they will makea payment for just a difference. Ex. If my bank owes to your bank 200€ and your bank owes my bank150€, then they will simply cancel all the payments through my bank paying 50€ to your bank. This iscalled clearer, system of clearing. Banks do this every day. Years ago, when everything was based onpaper, they did this every two weeks, but nowadays they just do it every day. Schumpeter was pointingout that you can go even further of this; my bank says to your bank: I owe you 50€, I won’t pay todaybut I will add the 50€ to what I will owe you tomorrow. So in a fact you have clearing, but nopayments. In a pure credit economy this what happens, payments cancel out over time. It means youdon’t need to have reserves for making credit transactions, you have a pure credit economy betweenbanks.In the international context this does affect the theory of exchange rates and the macro economicadjustments. The traditional theory of exchange rate is that when two countries trade, they havepayments, currency going one way and currency going other way with export and imports. Actuallywhat happens is that those payments cancel out. It’s just a transfer. I’m introducing to you a firstcomplication in the theory of money, which is the idea that, in pure credit, credit transactions don’trequire any payments, they cancel out over time. The second complication that I want to introducewhen credit and finance come into the analysis.2.Credit and finance.

3

Coming to the analysis, in the second half of the XIX century with the Companies acts at the age of70s, this allowed companies with limited liabilities to be established. Why is this important? It meantthat companies could be financed with long term debt and equity=share capital of the company. The1870s acts started in North America and in Great Britain and developed in Europe in a different way.They changed finance with 2 very important effects:

2.1- This new system of financing enterprises changed the nature of capitalistic crisis.

If you consider the traditional economic analysis, this analysis envisages a capitalist or classic

capitalist who financed its business out of its own pocket/money or with short term bank loans or

with bills. Bills are like a commitment to pay in 3 months’ time and you use this time to buy goods,

especially those guaranteed. The consequence of financing in this way was that the classic

capitalists were permanently and chronically short of money. Because if you finance your business

enterprise with short term money, let’s say with 3 months loans and every 3 moths you have to

renew the loan, if you have equipment like machinery which lasts 30/40/50 years, over those

30/40/50 years, if it’s financed this way, you have to keep renewing loans.

They were permanently short of money and that lead to a classic 19th century capitalist crisis which

was essentially a bank crisis.

An economic boom usually means that bank notes and coins would circulate out of the bank andwould be circulating in the economy. The bank would be running short of notes and coins and withtherefore stop lending; if a bank is running short of reserves it stops lending and arises interestrates. When banks did this in the 19th century this would cause a credit squeeze and all theseclassic capitalists who had long term assets which they were financing with short term loans, theywould find themselves obliged to repay their debts, but unable borrow more. So they had to repaytheir debts out of their own money, but they didn’t have much of this. So they would stopproducing materials, stop paying their workers in order to repay the debts. It was, in classic words, acommercial crisis and trade crisis, it took Hawtrey saying that was the kind of crisis that wouldaffect capitalism. With long term finance this changes.After the 1870s, what capitalism could do it was matching financing to the duration of the capitalistequipment, this is what used to be called funding. It is the standard way, that Keynes describes intohis Treaties of money, in which a firm even today finances its long term assets; instead of using itsown money, it borrows money from a bank, it buys the assets and then it issues a long term bondof approximately the length of the life time of the assets. Ex. Airlines: an airline which is buying aircraft, a long term asset which will last 20 or 30 years. Anairline, when it is buying an aircraft will use its own money or borrow money to buy that aircraft,and then, as soon as it can, it will replace that money by issuing a long term bond, put money intoreserves and use that money for the bond to put money back into its savings and reserves and repayback the bank loan. Why? Because the finance it’s cheaper, it’s long term, the financing is fixed andfinancing costs are fixed. The airline does not have to worry about this anymore, unlike theprevious case when it had to keep refinancing with short term loans.

The other thing that happened was the internationalisation of crisis. Old bank crisis with localcrisis. What happened with in new kind of crisis is that the new crisis would be a stock market crisis,and stock market when it crash it would affect shareholders and other markets elsewhere.

- One of the earliest and most important ones was the Vienna stock market crisis of 1873 which

affected the whole of Europe, in particular central Europe.

- A second big important crisis was in 1893, Bearings Crisis (Bearings was a bank in London).

That was interesting because the reason why the bank went into trouble was the bank had been

issuing bonds for the Argentine government and the Argentine government run out of gold to

make the payments of the bonds. And Bearings had guaranteed the bonds, so Bearings started

4

to run out of gold. The Bearings crisis caused such a collapse in London and such a shortage of

gold that the Bank of England nearly survived. Payments had to be made in gold, they had to

obtain gold from somewhere else. So London was draining gold, taking gold from Paris, and

eventually advocate the crisis.

- The biggest one of the period of the Gold Standard was the Knickerbocker Trust Crisis in

New York in 1907. Knickerbocker Trust was a major bank in New York, it suspended

payments to other banks in New York, but also in Chicago, because it didn’t have enough gold.

Those banks didn’t receive gold from Knickerbocker Trust, so they couldn’t make their own

payments and in this way the crisis spread internationally. All the way through to affecting Italy

as well. The core feature of the crisis was that Knickerbocker was operating in the capital and

stock market, that was why it brought into difficulties other banks. So you have a changed

nature of capitalist crisis. It changed the structure and possibly even the nature of capitalism.

2.2 Change of structure or nature of capitalismIf a company was financed with long term capital, it then becomes possible, by issuing long termbonds or long term capital, to take over another company; you can do much as an acquisition.In the previous system where companies where operating with short term loans, they barely hadenough money to finance production and their business investment; there wasn’t finance formergers and takeovers, you didn’t have mergers and takeovers. You had occasionally companiesjoining together, but they didn’t buy each other out. With the purchase or the refinancing ofcompany stock what you get is the rise of monopoly corporations or monopoly finance capital.All I want to emphasise is that it’s at this point that academic economics started to go wrong andstarted to lose touch on with was actually happening. If you look on text books under monopoly,what they are really talking about is the idea of Monopoly. Alfred Marshall, a 19th century economist,talked about monopoly in terms of unnatural monopoly. Ex. If I control a natural spring I can sellwater and decide the price. State Monopoly: if a government gives a company a monopoly for tradeor a monopoly over a road infrastructure or railway. For Marshall if there were increasing returns forscale, especially in manufacturing industry, large companies could have lower average costs andtherefore they could get to dominate in position and eliminate competition because their costs werelower. What the monopoly and finance capital, it’s nothing to do with competition. It is notcorporations which are good at competition, they became big through operations like mergers andacquisitions. Ex. Back to the Case of airlines: Ryanair makes a great pretence that it’s very bigbecause it competes with other airlines, but it’s a minor part of the story; it’s big because it took overother smaller airlines through mergers and acquisitions. General Motors is a very large corporationcar producer, not because it is so competitive, but because it took over other companies.

One of the consequences of this, is that you have a corporate structure which is divided between largecorporations, which use the capital market, and small medium sized enterprises, on the other hand, thatoperate through competition and survive through competition. The business cycle is in a fact acomplex interaction between corporations and small and medium sized enterprises. Because whenthere is an economic boom the small and medium size enterprises grow, but because the largecorporations have market power, they get the profits. It is a fact.I really want to highlight two aspects of having corporations financed with long term securities. Twoconsequences:

1- Corporations prefer to overcapitalise, they prefer to issue more capital not less. Why? Because it

means they can hold liquid assets in their balance sheet to hedge against their financial liabilities.

So any large corporation (like Ford, Siemens, FIAT), if possible, likes to hold more capital than

it needs, so that it has liquid assets and, the liquid assets it holds, so that it always has money to

be able to make payments on its long term debts. It doesn’t just have to rely only on

production. If it relies on production, then it is vulnerable to the business cycle. Any business if

5

it has a fluctuating market, it tries to keep some savings aside to pay their bills when sales are

produced. This is important because if you don’t pay the bills, that’s the end of the company.

Illiquidity means the end of the company. The company will be taken to court, it will have its

assets taken away. So all the capitalisation becomes important.

2- Liquidity: if a capitalist firm is financed with long term liabilities (bonds or shares), it has to

persuade both the individuals or institutions to hold long term bonds/shares. The condition for

this is that the markets for those bonds or shares are liquid. If they are not liquid markets,

supposing the airline which wants to fund its purchase of an aircraft with a 30 year bond, if

there are not liquid markets, the airline needs to find someone who is willing to hold the bond

for 30 years. Certainly it won’t be an older person, even if most of rich people are actually older,

because he is not going to be alive when the bond has been repaid. On the other hand, an older

person will hold the bond if they knows that they can sell the bond at a good price. To be able

to sell it at a good price you need to have liquid capital markets.

Today this is done through private equity, hedge funds. These institutions which borrow money

short term and use it to buy long term bonds. They operate along the yield curve and borrow

short term to buy long term securities. The important thing about this is that they provide

liquidity with bonds. If I hold a bond or a share, I can go to a bank and I can borrow money

using that as a security, so that I can get cash. If everyone had to wait for 30 years or forever to

get their money back, no one would hold it. For many radical economists, this kind of re-

intermediation, borrowing short term money to buy financial assets, is considered

financialisation or something else like this. It is the liquidity needs of long term assets. Once

you have capitalism operating with long term finance, then it creates additional kinds of credit

in order to make that long term finance liquid.

Rise of multinational corporations:The other fact is that it changes the nature or the type of multinational corporations. Multinationalcorporations are very important, we find them at the heart of the international monetary transactions.How and why they are involved? They’re involved through successive generations.

1st generation of Multinational companies were effectively domestically financed companiestrading companies. They were established in a particular country in order to tradeinternationally. That’s the basis of prosperity of Northern Italy from the Dark Ages over the lastthousand years, in the sense that cities like Venice, Bergamo as well, had international tradingbusinesses financed domestically in their own cities. In modern times, one of the largest is TheBritish East India Company which traded with India, it was established very long time ago. Thenthey gave rise to the second generation2nd generation of multinationals. Domestically financed companies producing abroad. Theoriginal one was the British East India Company which established tea implants in India in the 19th

century to produce tea because English liked to drink tea and tea was very light to carry in ships, sothe value added transport costs were low. But by the end of the 19th century is an industrialcorporation. Producing abroad meant effectively that these companies were exporting capitalequipment. This is what you find in the analysis of the empirics by ? and ?.Ex. General motors: theywere establishing plants which were producing the whole finished goods abroad.3rd generation of multinationals really is what we nowadays associate with multinationals, they aredomestically financed but they are engaged in international production. So you had differentstages of production placed in different countries. Ex. Mexican maquiladora production where thecomponents are produced in Asia, they are assembled in Mexico and exported to Europe. Fordistinternational production: how the car industry is now organised, different components produced in

6

different parts of the world. They produce engines in Germany, body parts elsewhere, theyassemble in a third country and then export.4th generation multinational since the 1980s. This is a multinational corporation that isinternationally financed and operating in different countries. What makes it different to theprevious multinationals is that it doesn’t necessarily come from an advanced industrial country orfrom a trading corporation of an established capitalist country, but in many cases it comes fromother countries, very often third world countries. Ex. Cemex, which is a Mexican corporation. TheMexican stock market is tiny, is not significant; the Cemex became a multinational not throughissuing long term bonds and shares in Mexico, but through borrowing money and then issuing longterm securities in New York, London and other financial centres. So it used the capital markets ofthe main capitalist countries to become an international corporation. Ex. Arcelor-Mittal, the owneris an Indian citizen. The Bombay stock market is a very interesting speculative market, but it’s not amarket from which you could create a multinational corporation. They created Arcelor-Mittalthrough issuing shares in London, New York, Paris, Frankfurt and buying up steel companies; inthis way becoming a multinational corporation. Ex. Tata motors; it was an Indian corporation, butin last 15 years it became a multinational corporation, again, through issuing shares in London. Itnow owns a part of the British car industry. This is a new generation of multinationals because it’susing capital markets in international financial centres to create a large corporation. It’s differentfrom the 3rd generation because with these corporations you now have a cross border structure ofassets and liabilities. That becomes very important for exchange rate theory. It’s a major change inthe way in which capitalised enterprise is organised. This leads on to my third section:

3.Varieties of International monetary circulationIf we want to understand what international money is, we have to understand how money circulates ininternational economy. I’m facing this on the work of a very obscure German monetary theorist HansNeissan and of an Italian monetary theorist Augusto Graziani. You can identify different types ofmonetary circulations.

- Income money. It is money in a circular flow of income between firms and households. Firms

buy facts and services from households, pay them money. Households use their incomes to pay

firms for goods and services they buy from them. Circular flow which takes place through

production. Production creating income, income being used for expenditure, expenditure

creating sales revenue for firms. In monetary economics it is usually where the function of

money finishes, people buy goods and services from each other, households buy goods or

services from firms, firms using money to pay their suppliers through markets for facts and

services.

- Investment money. When firms invest they buy fixed capital equipment and they pay for it

using money. Firms use money to buy facts and services for the production of investment

goods, but the income that workers receive is not spent on buying investment goods because

they don’t use investment goods. So this is a different type of monetary circulation, in

particular, for Kalecki this is the foundation of how money is monetised.

- Portfolio money. Money that financial investors pay each other for financial assets and for

foreign currencies including re-intermediation by banks, hedge funds, private equity in order to

make long term securities bonds and shares more liquid. Once firms started to finance

themselves using long term liabilities (bonds and shares), you have to have a monetary

circulation which will make those long term liabilities/financial obligations liquid. That liquidity

determines the value of those bonds. This 3rd type of monetary circulation is very much

concerned with the liquidity of the capital market. And, because it includes foreign currencies, it

affects the liquidity of markets in other countries. Portfolio money is a very important form of

7

international monetary circulation; it’s not just capital exports or imports and not just countries

which have savings placed abroad, it’s making those financial instruments liquid or less liquid.

- Internal corporate money. These are book keeping transfers between subsidiaries of firms,

especially international firms. 40% of the turnover of foreign trade takes place between

subsidiaries of multinational companies. These are not transactions which take place through

markets, they are administrative payments within the same corporation. Because they don’t go

through a foreign exchange market, the don’t have an effect on exchange rate. But they may

affect the exchange rate. It’s important for transfer pricing within the private sector, this is an

important aspect of corporate financial activity.

International monetary circulation ideas. The important thing to remember is that: it is much morecomplex than just production and the needs of trade. If someone tells you that the foreign exchangemarket is determined by exports and imports, he’s wrong; it’s all the other complex factors which enterall of which have international aspects. Shareholders of large corporations are often international sopayments on bonds are made cross border. Portfolio transactions, again, take place cross border today.Production may be more or less international. Ex. Car industry or steel industry are veryinternationalised with different stages of production in different countries. That’s a part of the analysis,the other part that must be taken into account is that there are cross boarder assets and liabilities, that iswhat we have to take into account when looking at international money and internationalmacroeconomics.

4.Overview of the whole courseCommodity Money Basic theory of money exchange rate macro adjustments. Money as a medium of exchange, obtainingits value from exchange; commodity money is not necessarily an actual commodity like gold, it may bepaper money, but it obtains its value from exchange with commodities. From this you get a purchasingpower parity theories of exchange rate, in other words, the notion that over time prices adjust indifferent countries to equalise purchasing power. The mechanism of the macro-adjustment is donethrough the Gold standard or movements of gold between countries. Monetary theories of creditTheories of credit in which credit exists, so you have interest rates, but the credit system is a system inwhich money is put into the bank and then lent out today. What you get from this portfolio theory ofthe exchange rate, the exchange rate is no longer just determined by the exchange of commodities, butit’s also determined by the exchange of capital assets/financial obligations. From this, you get notionsof interest rate parity, the exchange rate must somehow gravitate towards an equalisation of the rate ofinterest, so that the return on financial assets in different countries should somehow equalise, orcovered interest parity where changes in the exchange rate should not set differences in interest rates.Theory of monetary hierarchy: notion that different currencies in the world exist within a hierarchywith the ones at the top being the reserve currencies against which all the other currencies areexchanged.Macroeconomic adjustment through Chinese savings glut and shifts of savings around.Credit theories of money They arise out of long term obligations, giving rise to liquidity preference theories of interest of money,as you find in Keynes, but on international scale. Ex. dollar bonds are the most liquid, low rate ofinterest, lower than the interest rate on Greek bonds because they are less liquid. The notion here isthat international credit is backed by debt. There is a problem here, in that, the macroeconomicadjustment that takes place with international credit is not clear. We will try to look at some of theinternational adjustments that take place, but they are much more complex than the other ones. This is

8

one of the reasons why when you’re talked international monetary theories, you are taught either thehistory of the intern monetary arrangements or names and simple versions.

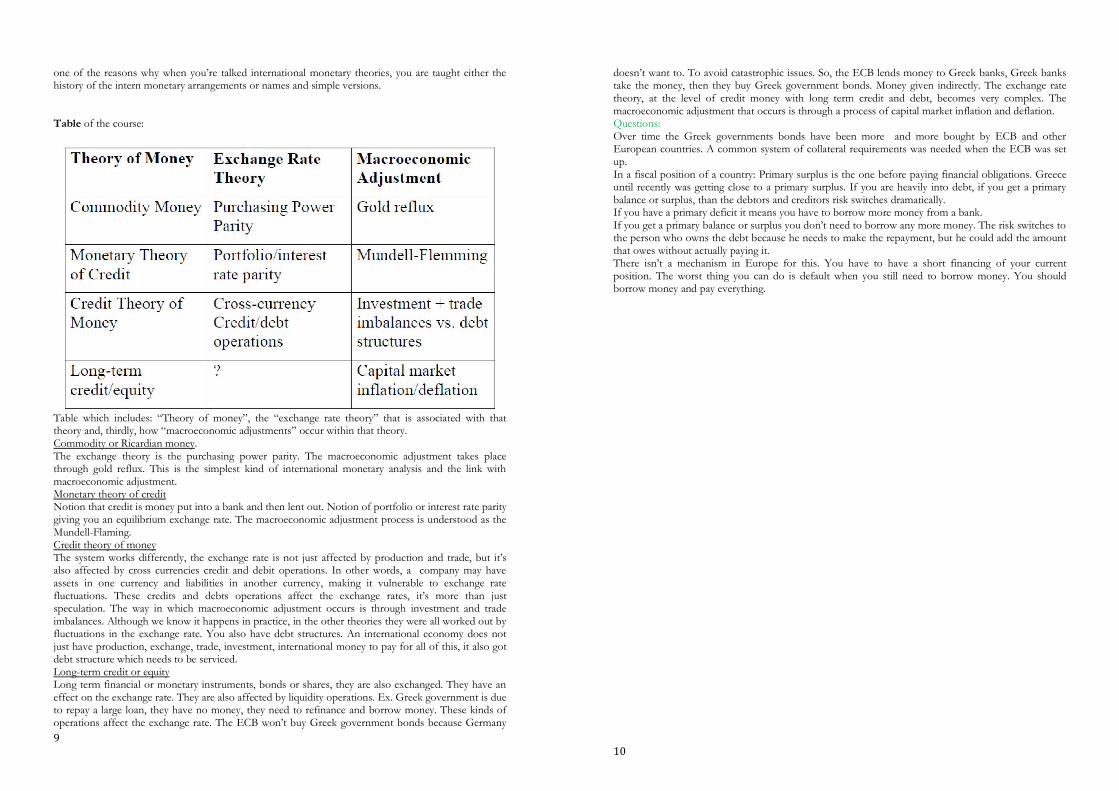

Table of the course:

Table which includes: “Theory of money”, the “exchange rate theory” that is associated with thattheory and, thirdly, how “macroeconomic adjustments” occur within that theory.Commodity or Ricardian money. The exchange theory is the purchasing power parity. The macroeconomic adjustment takes placethrough gold reflux. This is the simplest kind of international monetary analysis and the link withmacroeconomic adjustment.Monetary theory of creditNotion that credit is money put into a bank and then lent out. Notion of portfolio or interest rate paritygiving you an equilibrium exchange rate. The macroeconomic adjustment process is understood as theMundell-Flaming.Credit theory of moneyThe system works differently, the exchange rate is not just affected by production and trade, but it’salso affected by cross currencies credit and debit operations. In other words, a company may haveassets in one currency and liabilities in another currency, making it vulnerable to exchange ratefluctuations. These credits and debts operations affect the exchange rates, it’s more than justspeculation. The way in which macroeconomic adjustment occurs is through investment and tradeimbalances. Although we know it happens in practice, in the other theories they were all worked out byfluctuations in the exchange rate. You also have debt structures. An international economy does notjust have production, exchange, trade, investment, international money to pay for all of this, it also gotdebt structure which needs to be serviced. Long-term credit or equity Long term financial or monetary instruments, bonds or shares, they are also exchanged. They have aneffect on the exchange rate. They are also affected by liquidity operations. Ex. Greek government is dueto repay a large loan, they have no money, they need to refinance and borrow money. These kinds ofoperations affect the exchange rate. The ECB won’t buy Greek government bonds because Germany

9

doesn’t want to. To avoid catastrophic issues. So, the ECB lends money to Greek banks, Greek bankstake the money, then they buy Greek government bonds. Money given indirectly. The exchange ratetheory, at the level of credit money with long term credit and debt, becomes very complex. Themacroeconomic adjustment that occurs is through a process of capital market inflation and deflation.Questions:Over time the Greek governments bonds have been more and more bought by ECB and otherEuropean countries. A common system of collateral requirements was needed when the ECB was setup.In a fiscal position of a country: Primary surplus is the one before paying financial obligations. Greeceuntil recently was getting close to a primary surplus. If you are heavily into debt, if you get a primarybalance or surplus, than the debtors and creditors risk switches dramatically. If you have a primary deficit it means you have to borrow more money from a bank. If you get a primary balance or surplus you don’t need to borrow any more money. The risk switches tothe person who owns the debt because he needs to make the repayment, but he could add the amountthat owes without actually paying it. There isn’t a mechanism in Europe for this. You have to have a short financing of your currentposition. The worst thing you can do is default when you still need to borrow money. You shouldborrow money and pay everything.

10

TOPOROWSKI LECTURE TRANSCRIPTION

2nd LECTURE – University of Bergamo, Thursday 18th February 2015

Performed by Brivio Ilaria, Ciacciarelli Sophie, Fassina Marco, Tarantino Federica,Tinelli Sara

1. THE BERNANKE THEORY OF FINANCIAL CRISIS

I am going to talk today about the theory of financial crisis that partially we have already discussedlast week: the “savings glut” theory of financial crisis.This theory was performed by Ben Bernanke as an explanation for the American financial crisis.A couple of words on Ben Bernanke. He was a distinguished American monetary theorist and heworked on monetary theories before becoming a chairman at the general Federal Reserve.He was a provident proponent of what was known as the credit view of money. The prevalent viewat that time was that the most important monetary aggregate was notes and coins, and bank’sreserves in the Federal Reserve.The view of monetarist is the basic money supply determining the price level. Bernanke shouldn’tjust look at what was the monetary base. But, he also had to look on how private commercial bankswere developing credit. This is the background.When he became chairman of the Federal Reserve in 2005, he had to engage with much moreinternational monetary theory .The other background feature of Bernanke was that he spent somestudies about the depression in the 1930s and he had come on the conclusion that the depression hadbeen caused by the fact that so many banks collapsed and he saw banks as the place whereinformation of creditworthiness was concentrated. This information owned by the banks was themost important asset and the destruction of American banks in the 1930s, according to Bernanke,had caused the crisis. Now, I would talk about Ben Bernanke’s pronouncements about the financial crisis. Which is theinternational monetary explanation?It’s the Monetary theory and this of credit leads to a “loanable funds” theory of financial instability.It is associated with the particular view which Keynes had about the Neoclassics.Let me put on the diagram showing where we locate the different monetary theories. Today we aregoing to speak about Monetary theory of credit and Portfolio/interest rate parity. The reason why Idivided these theories into this scheme is due to the fact that each of these theories of credit has itsown logical operations.I will explain the Theory of financial Crisis with a couple of quotations from Ben Bernanke, whenhe was already chairman of the Federal Reserve. This theory became the official view of the federalreserve and due to the fact that federal reserve is the most important central bank in the world itcame to be regarded as the official view of all the central banks. First quotation: global “savingglut” and the US current account deficit.This is Bernanke before the crisis, but he is explaining how international money works and howinternational money is connected with macroeconomic imbalances.He said in 2005 that :“…over the past decade a combination of diverse forces has created asignificant increase in the global supply of saving”.This is a pre-emptive idea that saving is independent of investment.This is what is called “a global saving slut, which helps to explain both the increase in the UScurrent account deficit (we’ll come back on this later on)and the relatively low level of long-termreal interest rates in the world today”.For long-term real interest rate Bernanke was referring to US interest rate.11

The federal US government which was running a very large fiscal deficit (the US government wasin the middle of the war in Iraq, intervention in Iraq and activity to support that).He was saving government bonds but finding that there was a huge demand for US governmentbonds, they could sell US government bonds around 3/4% interest rate at this time, which isextraordinary for a country which had a bigger government debt which was, in relation to GDP, onthe scale of the Greek government debt today. In 2011 he came back to the financial crisis and he pointed out that “In 2007, more than 75% ofinvestment from ‘saving glut’ countries was in AAA rated US assets. An asset class that constitutedonly 36% of total US securities”. There was a reason for this and the main reason was that most ofthe foreign countries reserves were held by central banks and central banks typically were notinvested, they don’t find bonds that are less than AAA rated.“The preference by so many investors for perceived safety created strong incentives for USfinancial engineers to develop investment products that ‘transformed’ risky loans into highly ratedsecurities”This was a reference to the subprime mortgages that were converted into AAA rated mortgagebacked securities. Bernanke said that this, rather than low Fed interest rate, created the crisis.Bernanke was saying this because a number of economists stated that the cause of the crisis was thelow interest rate, determined by Central Banks. Bernanke was saying that crisis really was fault of the countries with the saving gluts, principallyChina.“In analogy to the Asian Crisis, the primary cause of the breakdown was the poor performance ofthe financial system, not the inflows themselves”. It is the fault of a financial system when therewas a demand for AAA rated securities , it manufactures AAA rate securities out off poor qualityloans.Three conclusions we can draw from this:1)first of all the primary cause of the crisis and the macroeconomic imbalances was the excessivethrift of Chinese, too much savings by Chinese. The US financial system was passivelyaccommodating, it was mainly putting the customer first (the customer wanted AAA ratedsecurities, the US financial system gave it).2)Financial globalization is good, or mainly is a passive vehicle for “investors” choices. 3)His final conclusion is a common one at that time which is that “better quality control is needed infinancial services”.

2 – THEORY OF MONEY: COMMODITY OR FIAT MONEY

If you take the standard saving identity from the national income accounts, in an open economysaving is equal to:S = I + (G – T) + (X – M)S = saving I = investments G = government expended sharesT = taxes X = exportsM = importsS – I is equal to the Net Private Sector Acquisition of Financial Assets. (G – T) is equal to the Net Supply of Domestic Financial Assets, the exogenous supply in effect ofgovernment securities. S – I – (G – T) = X – M which is equal to the Net Private Sector Accumulation of Foreign Assets.In effect, what Bernanke said is that in the case of the Chinese (G – T) is very small, while S – I and(X – M) are very big.

12

Now, if your currency or your money is Commodity of Fiat Money, the Foreign Assets are ForeignCurrency. There are not supposed to be more sophisticated flows. So, trade surplus is matched byan inflow currency.Really, the first explanation of macroeconomic adjustment in accordance to this kind of monetaryimbalance was David Hume’s “specie flow” adjustment. David Hume was one of the firstcomponents of the quantity theory of money and this is a commodity theory of money. The idea isthat if you have a trade surplus, these results in money inflows. The money inflow expands themoney supply. In David Hume’s time, this could be in form of crashes methods. As the quantity ofmoney increased, the higher prices will make imports more competitive and it will make exportsless competitive. So, those exports will be reduced and imports will be increased until the tradesurplus will disappear. We have the primitive notion of international money inflows creating anequilibrium in trade balance. This is still the idea at the back of many people’s minds and this iswhy the monetary equilibrium is associated with trade balance. For example, the Greeks could havethe economy and the money supply in equilibrium if they have a trade balance. The way he shiftthis into the monetary theory of credit is evaluated simply a credit based on monetary deposits. Youmake it a little more sophisticated by save the money inflow goes into the credit system and is lentout. So, the credit system acts more or less as pure intermediary. Bernanke had in mind the idea thatthe Chinese banking system accumulates U.S. dollar credits and these are used to buy U.S.securities: the securities prices rise, lowering long – term yields. Bernanke in principle, when hewas in the Federal Reserve, talked about long – term yields. Are you familiar with what long – termyields refer to? The rate of interest obtained on long – term securities. So, this is the Bernanketheory and it is essentially a monetary theory of credit.

3 – “LOANABLE FUNDS” THEORY

He needs also to take in consideration what happens to this money and what is the circulation of thismoney. The standard explanation is the “loanable funds” theory. Standard because some times agothere was different approaches to the balance of payments. This is very similar to David Hume’sapproach with Fiat currency, but again trade balance is determined by primitive inflation. Thinkingabout the monetary theory of credit, you have that it allows to have a monetary rate of interest. So,you have that it is a standard “real” theory of finance and interest rates. It’s “real” because the rateof interest is supposed to represent not money, but savings. The term that keeps values in thediscussion, Chinese is saving too much. The money earning to American bonds is savings. In theclassical theory, interest is as reward for “abstinence”, or a “postponement of consumption” or“waiting” (Nassau Senior, Mill, Marshall). In the first half of 19th century, the English monetarytheorists Nassau Senior, Mill and Marshall said that the rate of interest is what you get not spendingyour money in assumption. Again, a general discussion of the role of China in the internationalfinancial system notice that Chinese are related to be dealer and postponements of consumption.Chinese living standards lower than Americans. This is a hard documentary because most people indeveloping world have low standards than Americans. In the 30s end of the 19th century, Marxperformed the idea that interest is a claim on “surplus” value produced by labour employed bycapitalists using borrowed money. For Marshall, the interest is payable only on “liquid” capital.“Liquid” capital are the securities that can easy convert into money. Interest is not payable normallyon machinery and so on. As well as now, there is supposed to be a relationship through investmentsand the rate of interest is supposed to be a cost of financing investment. Traditionally, if the rate ofinterest goes up, more would be saved. If the rate of interest goes down, there is a great incentive toborrow money for fixed investment. This leads to the notion of “loanable funds” theory of theeconomics at the beginning at the 20th century (D.H. Robertson; McKinnon & Shaw). This is thenotion that rate of interest equalizes current saving with current investment. AAA savings arerepresenting the capital stock, the accumulated savings in the economy. So, in theory savings are

13

supposed to be brought into the equilibrium of investment, but AAA savings are representing theAAA capital stock in the economy. Investment is a change in the capital stock. So, the rate ofinterest is simply equalizing current saving with current investment. Now, what happens to the restof savings that are not affected by the rate of interest? In this theory, just the new saving that isbought on funds market where it meets business investors with profitable projects and the count ofequilibrium of the rate of interest. This rate of interest really becomes a real rate of interest, whichreally is a concept of commodity money. At the back of it, there is the notion of the commoditymoney. The rate of interest is the word for “postponement of consumption” and it represents theextra consume of goods that you can’t obtain. So, the real rate of interest (RRI) is a concept ofcommodity money. This is different from the Fisher idea of the “real” rate of interest, where RRI isthe inflation – compensated rate of interest. It is closed to the concept of the rate of interest that youfind in the Neoclassical theory, where the rate of interest is simply the rate of discount of futureconsumption or income for current consumption. You have this concept that “Real” Rate of Interestrepresents the commodities from surplus produced in the future. So, the “Real” Rate of Interest isunrelated to money or capital flows. That is what you find in the “loanable funds” theory. Bernanke was unconsciously putting forward the “loanable funds” theory, savings were determinedby the rate of interest, but he also taking on the important notion of the English economist JohnAtkinson Hobson. Hobson was one of the idealist of the international finance and his theory is verysimilar to the Bernanke’s theory of the global savings glut. In the case of Hobson, imperialism iscaused by global savings glut. The global savings glut is not because the Chinese have saving toomuch, but is because of the unequal distribution of income in the capitalist countries, which meansthere are too many rich people that do not spend their own money. So, the savings are settledaround the globe and financing imperialistic advents. In this way, we can see the connection withthe past. In the case of Hobson, there is a much greater emphasis with the principles of economiesand he was arguing that the distribution of income is too unequal, while Bernanke was arguing thatChinese are not consuming there are saving too much. Both Hobson and Bernanke believe that thefundamental course of capitalistic nations is that people do not consume enough.

4. MR KEYNES AND THE “NEO-CLASSICS”

They are not the classics, but the neo-classics.The previous part of the lecture I did talking about the great English physical-economist Hobson,look at his theory of all the savings Hobson was and you could see at his some aspects, Keynes reliable, in one aspect in particular. Hobson and Keynes represented, and always represented, the ideas of the politician of interests, thepolitician at keeping get financial revival Hobson was the opponent of this and argued that the impair was in fact the drain on the finances ofthe British straight. And in the late 1914 and after the Second World War, just at the point it has thateveryone believed that it was with triumph of Keynesianism, he was in fact triumph Hobson. For the rest of this lecture I’m going to talk about some ideas of Keynes, and in particular hiscriticism of neo-classics. All of you I hope are familiar with the criticism that Keynes put forwardthis generally theory of what Keynes called “neo-classics”, the people who believed in free trades,the quantitative theory of money and the tendency of the economy to follow employmentequilibrium; all of which has been denied.Very few people know is that Keynes also used the term neoclassical, and used it in a very veryspecific sense. If you get any edition of Keynes’ general theory and you look in the index you’llfind the nature of neoclassical and you probably find this quotation “Unlike the neo-classicalschool, who believes that saving and investment can actually be unequal, the classical school properhas accepted the view that they are equal”

14

What did Keynes mean by the “neo-classics”? Keynes meant by the neo-classics, people likeWicksell, Hayek, Hawtrey, Robertson and until recently himself. What was the main idea behind the neo-classic theory? The neo-classic theory was that saving wasnot input to investments, but, and this is the important thing for macroeconomics and for thedynamics of the economy, the difference between saving and investment is what createsdisturbances in the economy, cause the economy can have a boom or a recession. At this time theneo-classics like , Robertson, Hayek, Hawtrey and Wicksell, argued that the difference betweensaving and investment is in effect credit creation or credit repayment. They did have this idea thatyou take your saving and you just keep it on deposit; if you did then you will be lent out again forinvestment. Hayek actually had an intermediary position of it, because he argued that this credit creation wouldactually give rise to force saving. If investment was greater than saving, the difference betweenthem would be made up by bank loans and the bank loans would create inflation and the inflationwould cause prices to rise because real wages to fall. So the falling real wages was what Hayekrefers to as forced saving because in effect the economy saves, makes up the difference betweenvoluntary saving and actually investments by the reduction of the living standards or the reductionin consumption of workers. This is Hayek force savings. The origin of this idea really comes from Wicksell. Wicksell, in 1890, argued that credit creation isreally determined by the difference between the money rate of interest and the natural rate ofinterest. The natural rate of interest was a kind of real rate of interest; it’s a marginal return onproductive capital.Wicksell was a neo-classic who believed that capital has a marginal return, that is profits marginalreturn on capital not that profit is the surplus of labor.This natural rate of interest was a money rate of interest . Then entrepreneurs will borrow money toinvest, and this would create an investment, and it will cause the cumulative process of economicexpansion that would gained up boosting the economy and eventually link to inflation. What wouldhappened maybe is that banks in the process of this boom start to losing their reserves, they start tolosing gold, they start to losing coins; the way banks would react it would be by raising interestrates. So eventually this difference will disappear. Similarly and conversely natural rate of interestfell then the natural if fell below the money rate of interest then entrepreneurs will not invest andthe economy will contract. So this was a theory of credit cycles and it could use if it makes up atheory of business cycle. The issue that comes out for this lecture is “why did this low rate ofinterest in the US not simulate an investment boom in America?” It should do that, but it didn’t.There are also several explanations. One of the reasons is that investment is not driven by the rate of interest. If you look at the data ofthe rate of interest and investments you find that both of them are procyclical, variables, they bothrise in a boom and fall in a recession. Wicksell knew this, and that was why he said it was not the rate of interest, that itself determinesthe business cycle, that determines the boom of all the sample and determines the rate ofinvestments, but it’s the difference between the marginal return of capital, the real rate of interest,and the money market rate of interest. And this is, in effect, what happened in Wicksell was thatsaving was catching up with the level of investments, but saving just not equals to investments. Inpractice we know that saving, actually, if you take a closed economy with no government, savingalways equals investments. It’s not just by definition and not because this is a national income,accounting identity, but because there is something else which is disappeared out of the economy,out of economic analysis and that is the circular flows of income. The incomes generated in aconsumption sector represent the consumptions in the economy and the incomes generated in theinvestments sector represent saving.More generally, if you take this, if you accept this national income identity and circular flow ofincome or if you start looking to the schemes of the production in Marx’s Capital, Volume two, you

15

find that saving is equal to total investments + fiscal deficit + trade surplus , what I showed youbefore. We can use this to examine, to understand the great Chinese saving glut. In China there is a veryvery high level of investments even today, but let’s say in the 1990s and the first decade of thiscentury, it was something like 40% - 45% of GDP put into fixed capital investments?In practice China has a very small fiscal deficit and it has a very small trades surplus (possibly nowa deficit). It’s more or less balanced. In effect it’s this free high level of investment which means that total saving in the Chineseeconomy is extremely high, it gives you very very high saving rate. In the US the situation is much reversed. In US total saving, as a proportion of GDP, is around15%, that is remarkably low. There’s a very large fiscal deficit and there’s similarly large tradedeficit both of 5-6 % of GDP. So the trade deficit offsets the fiscal deficit and this is a negativeeffect for US. Likely China it is at first investment that determine saving, and precisely becauseinvestment is so low, it appears that the US is saving very little. Instead in the case of China itappears as if china is saving a huge amount. But Chinese saving is not the postponed consumptionof Chinese population, it’s not the fact that living’s standards in china is so lower compared to US.In fact most saving in China appears as saving, not of households, but of firms. And you can findthat the big accumulation of savings in china is in Chinese firms and in particular private sectorfirms. So at this point the theory starts to fall apart: it’s not Chinese consumers that are postponingconsumption and investing and buying American government bonds until the moment when theywill be consuming in the future; it’s, on the contrary, Chinese firms that are investing massively(particularly the state corporation) and the result is an accumulation of savings in firms and inparticular in private sector firms. One other thing that comes out, what Keynes call neoclassicalposition, is that in confusing savings with credit, it assumes that all banks do is take saving andpass it onto someone else, and let’s say the case of Chinese saving are passed as loans to USgovernment. It not only confuses saving with credit but it also confuses saving with savings. Thiswas something which Keynes pointing out in his treaty on money and there is an important differentbetween them. Saving, as are saved before, is current income that is not consumed; it’s a flow ofincome over a particular period of time, and this flow is an addition to financial assets. Instead,savings themselves are another flow that are the total stock of financial asset, which if you like ismade up of the cumulating saving of the past. What Keynes is pointing out on his treaty of money isthat the relationship between them is very important, and very unlike what the loanable funds theorysuggests, because if you look at the financial market, the market for security is divided up in two:the primary market (new sec issued) and the secondary market (already issued securitysubsequently bought and sold). Now, why is this distinction important? Because the secondarymarket, according to Keynes, was the market in which the rate of interest is set. So it is not set inthe market of new securities, and the buying and selling assets and liabilities traded in secondarymarket they don’t just cancel out. If we go back, I said that savings minus investments is the netaccumulation of financial assets, and it was the addition to savings of the private sector, but thisdoesn’t mean that the rest of the savings are totally inactive; they’re not inactive, because peoplemove their portfolio around and change them, and it’s in changing their portfolio around that, asKeynes argued, that is where the rate of interest is determined. So, in terms of the financial system, but also the international financial system, this intermediatesnot only current savings, but also provides liquidity against total savings. The reason why you havea secondary market is in order to provide liquidity for existing savings: so I can take a long-termbond and sell it. It also accommodates shifts between assets and liabilities, and these shifts typicallyoccur as quite frequently in balance sheets. In particular in private sector corporations you havefirms borrowing short-terms to pay long-term debts, or they re-issue shares to repay short-termdebts; they may sell long-term assets to build up liquid or short-term assets. It’s common forexample for corporations to sell, let’s say an office building in which they have headquarters, it’scommon to sell the office building and then lease back the office building, so they stay in the office

16

building; the money that they get for selling the office building, they put into a bank deposit, so thebalance sheet becomes much much more liquid.In private sector finance, everyone understands this; unfortunately, the people who owe Greece’sgovernment debt don’t understand this. I think that they have their debts, they must pay them ontime, but no one pays them on time. In the private sector, no one pays, free rate debts are paid ontime. Typically they’re refinanced earlier, they get an opportunity to refinance earlier.It’s the shifts that arise in the markets and become very very important indicators for economicactivity; and use money, as I said in the last week’s lecture, there is a surplus of money going on,and it’s what, if I go back to my diagram, it’s why in the end this monetary theory of credit isunsatisfactory, it doesn’t explain what happens in the financial market, it’s an oversimplificationthat secondary market, if we start looking at it, start on act in it, to see what’s happening there,that’s what takes you down to long-term credit and the operations of credit markets.When Keynes was writing his “Treatise on money”, he was looking at it purely, or largely, assomething that’s domestic at the internal financial markets. I think we have to go beyond this, now,and say that there is an international financial system which is in many respects integrated andwhich allows this kind of shift in assets and liabilities to occur not just between short and long term,but also between currencies. That’s what we will be doing ready in the later lectures.But I now really come to my conclusion. The essence of the Bernanke “Savings glut” theory is thatis essentially a monetary theory of credit, based on a distinction between saving and investment thatreally takes us back to the theories of Hobson and early Keynes. In the case of Hobson, the notionthat these excessive savings are the foundation, are founded on an unequal distribution of incomeand on the foundation of imperialism, which today we consider, you know, it’s not a diplomaticterm. Bernanke would not accuse the Chinese of being imperialistic, but he’s happy, or theAmericans are happy for the Chinese to hold the American government debt, possibly for the samereason that the Greeks are also happy for the Germans and everyone else to hold Greek governmentdebt, because it means that everyone else has an interest in the survival and the financial viability ofthe Greek government. I think in the case of Hobson was a particularly…you know…political-economic interpretation,distinction between saving and investment: in case if Keynes and Wicksell, Hawtrey and all theother economists at the early part of the twentieth century, for them this was the distinction betweensaving and investment with the foundation of the business cycle, and created instability.From a more modern perspective, we can say that what’s wrong with these theories is that theyconfuse “saving” with “savings”. There is a constant shift between saving and savings, there’s alack of understanding that where the saving come from; it’s not due to under-consumption, orpostponed consumption in the case of Chinese, but it is due to their high level of investment.It confuses saving with credit, because credit is supposed to be the same as saving. The financialsystem is reduced to being just a pure intermediary with people who have savings, or who aresaving, putting their money into this intermediary, and the intermediary lending it to someone else.And that actually is the standard feature of the American finance theory, and either the Diamondand Dybvig model of banking, even the Diamond and Dybvig model of maturity transformation it’ssupposed to explain financial instability, but it essentially just presupposes that there’s an agent whoacts as a pure intermediary.So this confusion between saving and credit, I think my fundamental objection to this kind ofanalysis is that it doesn’t explain debt structures. Debt structures are washed out into just simplyborrowing or lending, and differences between short-term and long-term disappear in all of these.What I’m going to do in the remaining lectures is that I will look, I think I will first of all examinesome more of the macroeconomic adjustment, that arises from this kind of theory, which isMundell-Fleming interest rate equalization theory. But I will then, what I will do afterwards, I willstart to fill up what I believe that is blank spaces around here ready that haven’t been developed, butyou won’t find on textbooks, because no one talks about a pure credit of theory of internationalfinance and its macroeconomic implications, all of this is supposed to be, all of this is reduced to a

17

very simple case of pure intermediation of savings, and this is not thoroughly inaccurate, but itgives strong explanation of where credit flows come from, and the relationship to stocks andsavings, the relationship between different rates of interest, and in particular their relationship to theexchange rate which we haven’t dealt with today.So this concludes my first lecture, I hope you have questions on this.

18

TOPOROWSKI LECTURE TRANSCRIPTION

3rd LECTURE – University of Bergamo, Friday 19th February 2015

Performed by Brando Viganò, Claudio Iacopino, Simone Perego, Michael Ravelli

Today I’m going to talk about the global macroeconomic imbalances and neomercantilism.

This what I’m doing is continuing what I did yesterday which was related to talk about thegold influx today I will say something about Mundell-Fleming really looking more at thismonetary theory of credit.

The logic that all the working out monetary have using is a monetary theory credit tounderstand the international monetary system.

Now the monetary theory of credit as I keep seeing it in the last two lectures is really routedin the idea that foreign currencies are accumulated through trade imbalances so we will talkabout macroeconomic imbalances which really mean as trade imbalances and in this a keyrole is played by a so called neomercantilism.

So I will explain today some more about neomercantilism and in specific domestic saving andthen what the connections between them then look at even comprise that and examine wherefirms’ saving comes into analysis and then this leads beyond to the limits to neomercantilism.

And we will get on to the more interesting topic which looks forward to credit approach thatis international monetary integration.

Before we can finish with monetary theory of credit or monetary approach to credit we needto conclude with the Ricardian approach to international money related to which this is thefoundation of the optimal currency area theory of Mundell-Fleming which postulates aparticular type of macroeconomic adjustment with commodity money then I will give myexplanation of critique of international commodity money and end up with internationalmonetary endogeneity .

So in this lecture like in the other lectures we are looking at the standard textbook approacheswithin a resolution in monetary theory of credit and then trying to move beyond those intocredit approaches to international money.

“Neo-mercantilism”

Neomercantilism is well known concept nowadays it’s a trade and industrial policy ofmaintaining trade surpluses as part of export led growth, it’s a school of thought based on theidea you can obtain growth through having a trade surplus which is necessary to have growth.

19

The other traditional reason for having an export surplus was to accumulate foreign exchangeand the gold reflux principles of I talked about yesterday of debit due this was in fact acritique of mercantilism debit due was an effect arguing that you cannot accumulate moregold without affecting your price level in the idea would if affect your price level it cannotaffect your level of output in such a way of getting growth.

The mercantilist theory is based on the principle that money accumulation stimulates growthas I said, Hume has criticized this because He argued that eventually it leads you to loseinternational competitiveness.

Export led growth experienced a renewed of interest in the work of Nicholas Kaldor in a lot ofhis development economics hicks where he explicated export led growth a particular becauseof the post war experience and Japan since the 1980s Germany since 2000 and some peoplesay that it’s true also for China.

I mentioned this examples because it is forgotten nowadays that the japan traditionally in thepast was not an exponent of export led growth, in post war period in 1950s 1960s and in themost of 1970s Japan periodically hit an export sealing and it’s development was frustrated bybalance of payments deficits

Most countries as their economy expand their imports rise their exports rise at the same time,so typically the foreign trade balance is a bottom neck for growing economies and this indeedwas the case in Japan and also the case in the post war Germany and I think we will see is alsothe case in China.

Nevertheless the economists like Kaldor believe that you could get an export surplus as asustainable position, similarly the IMF and the world banks base their policies on the idea thatcountries can obtain export surpluses.

Neo-mercantilism and domestic saving

So now let’s go to neomercantilism and domestic saving so let’s go back on the nationalincome identity account that incoming be equal to consumption plus investment plus thefiscal deficit plus the trade surplus, this is what I did yesterday so I didn’t go into it today.

Y = C + I + (G – T) + (X – M)

S – I = (G – T) + (X – M)

You get from this I can rearrange this so you can end up with three balances:

The private sector balance (S – I)

The government sector balance (G – T)

The foreign trade surplus (X – M)

20

So that you have from this private sector balance a net financial accumulation so they say NETfinancial accumulation it means the financial accumulation net taking away financial assets orclaims against other sections of the private sector.

Net in this sense because in actual fact private sector accumulation of financial assets will nobe really much much bigger than this but this is taking out or cancelling all the borrowing andlending in the private sector.

So the private sector net financial accumulation is equal to the fiscal deficit plus the tradesurplus.

This leads to what has been advanced by the Levy Institute as it’s sometimes referred to thethree balances approach of Wynne Godley and Randall Wray.

In other words the idea that is necessary to have a fiscal deficit plus some kind of tradesurplus neomercantilism in order to maintain financial accumulation and to give you aneconomic boom.

Godley himself attended to be a little bit sceptical of when you could get this kind of privatesector financial accumulation in particular because he believed that if you expanded the fiscaldeficit too much you tend to reduce the trade surplus and in fact the one offset the other onewhich in the time he was writing actively during the 1980s, it was the case of UK and US, ifyou look at the size of their fiscal deficit it’s more or less equivalent to the trade surplus so theone cancel the other.

So Godley was a little bit sceptical on neomercantilism but on the whole he was close toKaldor and very much abdicated this idea that a trade surplus is a desirable thing because itleads to an economic boom.

Why I think this is need to be unpacked, because it’s only one part of the picture in fact theprivate sector it’s not just one sector, there are number of interesting things about thisapproach, it’s good we have now figured the flow of funds accounts which support this kind ofthree balances analysis, but it misses out some fundamental complexity in the model, inparticular it misses out the fact that the private sector is not one homogeneous agent but itconsists of different classes and even as economic agents it consists of two particular classesof agents, households and firms so that strictly speaking in the flow of funds this will bedistinguished.

Now If you do this you can divide up saving in to saving of households and saving of firms sothat can be total saving equal to saving of households and saving of firms which is equal toinvestment plus the fiscal deficit plus the trade surplus.

S = SH

+ SF

= I + (G – T) + (X – M)

If you move this (Sh) around you get really the most interesting equation which is that thesaving of firm is equal to investment of firms minus households saving plus the fiscal deficitplus the trade surplus and this is the most important distinction.

21

SF

= I - SH

+ (G – T) + (X – M)

The significance of firms’ saving

This is why the distinction is to be made in this kind of analysis, because what you have now isa relationship between saving of firms which is net financial accumulation and the saving ofhouseholds and it’s not the case that the saving of households actually improves and helps theeconomy because it gives money to firm and we know that more savings means moreinvestment, in actual fact if households save more than it means that firms will save less.

The original idea of this goes back belonging to Karl Marx, who argued that holding of moneycould have two effects in the economy. Holding of money can be that on one hand it givesfirms the money to invest or the finance or the liquidity to invest and to expand the economicactivity, but in the same time holding of money can also congest the economy meaning it canstop circulation in the economy, because if households save money than it means that theyhave received income from their employers which employers do not receive back again assales revenue. If a car worker is paid wages and saves some of those wages it means that hisemployer and all the other employers in the economy don’t receive back all the money theypaid to workers as wages and they don’t receive back as sales revenue.

So this is a very very important distinction.

Let me expand on this even further and look at what is the significance of saving of firms.

The saving of firms is the net financial accumulation or the net cash flow of all non-financialfirms or businesses after payment of interest and dividends.

The saving of firms is the way in which firms accumulate money and that saving is thefoundation for the future growth and this financial accumulation may be added to thereserves of firms in order to finance investment or to repay their debts. It’s the source offirms’ liquidity; it gives them bank credit without indebtedness.

Nowadays we are in a credit economy in monetary theory of credit, the financial accumulationof firms’ saving is money that is added to their bank account without them having to borrowenough money. They can use it to finance investment and to repay debt as well. It facilitatesinvestment, investment being the process of circulating liquidity around other firms. If a firminvests using its own reserves, it’s taking those reserves and circulates them around otherfirms. The reserves leave the account, leave the balance sheet of that firm and spread aroundthe balance sheets of other firms.

This is in contrast to households saving where households’ saving is as I said a deduction fromfirms’ cash flow.

The relationship between them is fairly straightforward.

You can put a 45 degree line that suppose that the level of households’ saving is this amountS0, it has negative sign because it’s a deduction from households’ saving.

22

If firms’ investment where 0, then firms would have a cash flow deficit of the amount ofhouseholds’ saving. So at 0 investment, firms’ businesses lose in every period.

Limits to “neo-mercantilism”

What firms need to do is to invest at least as much as household saving if they want theiroverall balance to be balanced. The more firms invest the more money they will receive. Whyis this important? Because this is a domestic business consideration. It’s important because inmost countries this relationship between investments minus households saving is moreimportant and significant than the fiscal deficit and the trade surplus. So this is why theincouragment to save is not desirable. And this is why the encouragment to run a tradesurplus is maybe necessary for exchange rate reasons, and is something like Bretton-Woods,but otherwise it is not essential for a country.