Department of Education and Training Financial Statements For the Year Ended 30 June 2017 Statement of Comprehensive Income TABLE OF CONTENTS Financial Statements Page 3 Page 4 Page 5 Page 6 Page 7 Pages 8 and 9 Page 10 Page 10 Page 10 Page 10 Page 10 Page 11 Page 11 Page 12 Page 12 Page 13 Page 13 Page 14 Page 15 Page 15 Page 15 Page 16 Page 16 Page 16 Page 18 Page 18 Page 19 Page 20 Page 20 Page 21 Page 22 Page 22 Page 24 Page 24 Page 25 Page 26 Page 27 Page 28 Page 28 Page 28 Page 28 Page 29 Page 30 Page 30 Page 31 Statement of Comprehensive Income by Major Departmental Service Statement of Financial Position Statement of Assets and Liabilities by Major Departmental Service Statement of Changes in Equity Statement of Cash Flows (including Notes to Statement of Cash Flows) Notes to the Financial Statements Section 1 About the Department and this Financial Report A1. Basis of Financial Statement Preparation A1-1 General Information A1-4 Authorisation of Financial Statements for Issue B1. Revenue A1-2 Compliance with Prescribed Requirements A1-5 Basis of Measurement B1-1 Appropriation Revenue A1-3 Presentation Details Section 2 Notes about our Financial Performance A1-6 The Reporting Entity A2. Departmental Objectives A3. Machinery of Government Changes A4. Controlled Entities A4-1 Disclosures about wholly-owned controlled entities A4-2 Disclosures about non wholly-owned controlled entities B1-2 User Charges and Fees B1-3 Grants and Contributions B2. Expenses B2-1 Employee Expenses B2-2 Supplies and Services B2-3 Grants and Subsidies B2-4 Other Expenses Section 3 Notes about our Financial Position C1. Cash and Cash Equivalents C2-1 Impairment of Receivables C6-1 Borrowings C2. Receivables C3. Property, Plant, Equipment and Depreciation Expense C3-1 Closing Balances and Reconciliation of Carrying Amount C3-2 Recognition and Acquisition C3-3 Measurement using Cost C3-4 Measurement using Fair Value C3-5 Depreciation Expense C3-6 Impairment C4. Intangibles and Amortisation Expense C4-1 Closing Balances and Reconciliation of Carrying Amount C4-2 Recognition and Measurement C4-3 Amortisation Expense C4-4 Impairment C5. Payables C6. Interest Bearing Liabilities Page I of 58

Transcript

Department of Education and Training Financial StatementsFor the Year Ended 30 June 2017

Statement of Comprehensive Income

TABLE OF CONTENTSFinancialStatements

Page 3

Page 4

Page 5

Page 6

Page 7

Pages 8 and 9

Page 10

Page 10

Page 10

Page 10

Page 10

Page 11

Page 11

Page 12

Page 12

Page 13

Page 13

Page 14

Page 15

Page 15

Page 15

Page 16

Page 16

Page 16

Page 18

Page 18

Page 19

Page 20

Page 20

Page 21

Page 22

Page 22

Page 24

Page 24

Page 25

Page 26

Page 27

Page 28

Page 28

Page 28

Page 28

Page 29

Page 30

Page 30

Page 31

Statement of Comprehensive Income by Major Departmental Service

Statement of Financial Position

Statement of Assets and Liabilities by Major Departmental Service

Statement of Changes in Equity

Statement of Cash Flows (including Notes to Statement of Cash Flows)

Notes to theFinancialStatements

Section 1

About the Department

and this Financial

Report

A1. Basis of Financial Statement Preparation

A1-1 General Information

A1-4 Authorisation of Financial Statements for Issue

B1. Revenue

A1-2 Compliance with Prescribed Requirements

A1-5 Basis of Measurement

B1-1 Appropriation Revenue

A1-3 Presentation Details

Section 2

Notes about our

Financial Performance

A1-6 The Reporting Entity

A2. Departmental Objectives

A3. Machinery of Government Changes

A4. Controlled Entities

A4-1 Disclosures about wholly-owned controlled entities

A4-2 Disclosures about non wholly-owned controlled entities

B1-2 User Charges and Fees

B1-3 Grants and Contributions

B2. Expenses

B2-1 Employee Expenses

B2-2 Supplies and Services

B2-3 Grants and Subsidies

B2-4 Other Expenses

Section 3

Notes about our

Financial Position

C1. Cash and Cash Equivalents

C2-1 Impairment of Receivables

C6-1 Borrowings

C2. Receivables

C3. Property, Plant, Equipment and Depreciation Expense

C3-1 Closing Balances and Reconciliation of Carrying Amount

C3-2 Recognition and Acquisition

C3-3 Measurement using Cost

C3-4 Measurement using Fair Value

C3-5 Depreciation Expense

C3-6 Impairment

C4. Intangibles and Amortisation Expense

C4-1 Closing Balances and Reconciliation of Carrying Amount

C4-2 Recognition and Measurement

C4-3 Amortisation Expense

C4-4 Impairment

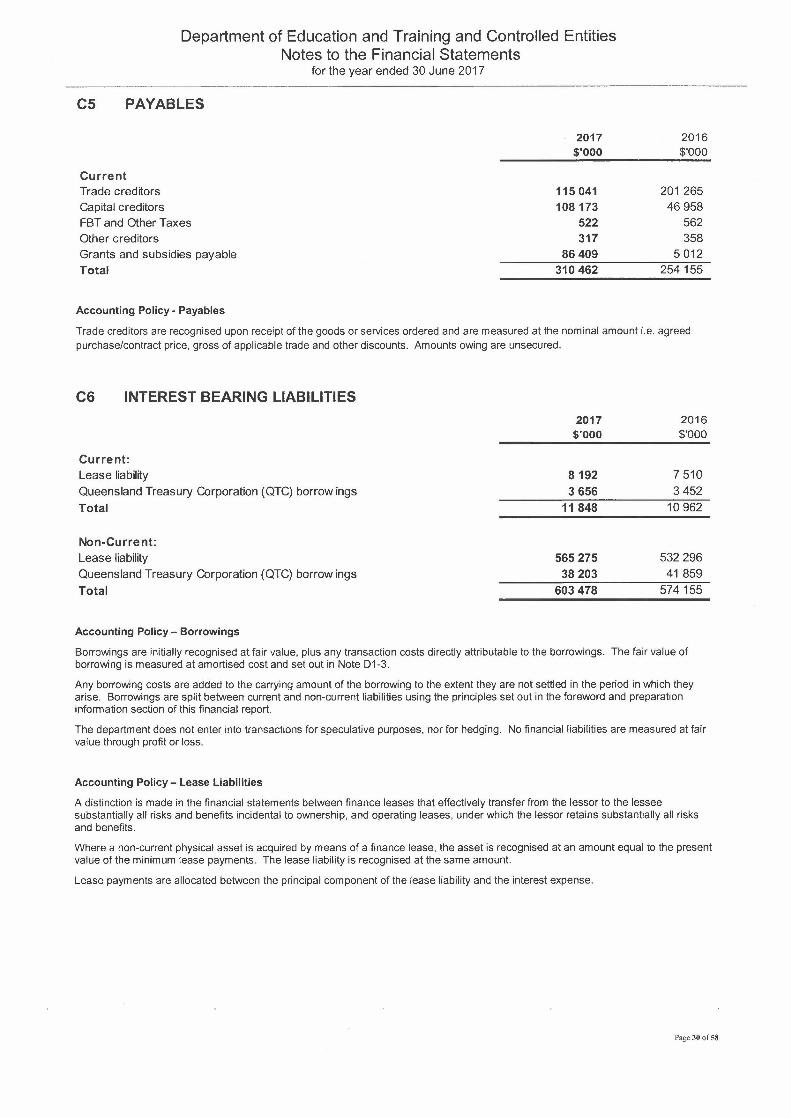

C5. Payables

C6. Interest Bearing Liabilities

Page I of 58

Department of Education and Training Financial StatementsFor the Year Ended 30 June 2017

TABLE OF CONTENTS (continued)Notes to the Section 3 C6. Interest Bearing Liabilities (continued) Page 31

Financial Notes about our C6-2 Finance Lease Liabilities and Commitments Page 31Statements Financial Position C6-3 Disclosures about Sensitivity to Movements in Interest Rates Page 31(continued) (continued) C7. Accrued Employee Benefits Page 32

C8. Provisions Page 32

C9. Equity Page 33

C9-1 Contributed Equity Page 33

C9-2 Appropriations Recognised in Equity Page 33

C9-3 Asset Revaluation Surplus by Asset Class Page 33

Section 4 D1. Fair Value Measurement Page 34

Notes about Risks and D1-1 Accounting Policies and Inputs for Fair Value Page 34Other Accounting D1-2 Basis for Fair Values of Assets and Liabilities Page 34Uncertainties D1-3 Fair Value Disclosures for Financial Liabilities Measured at Page 36

Amortised Costs

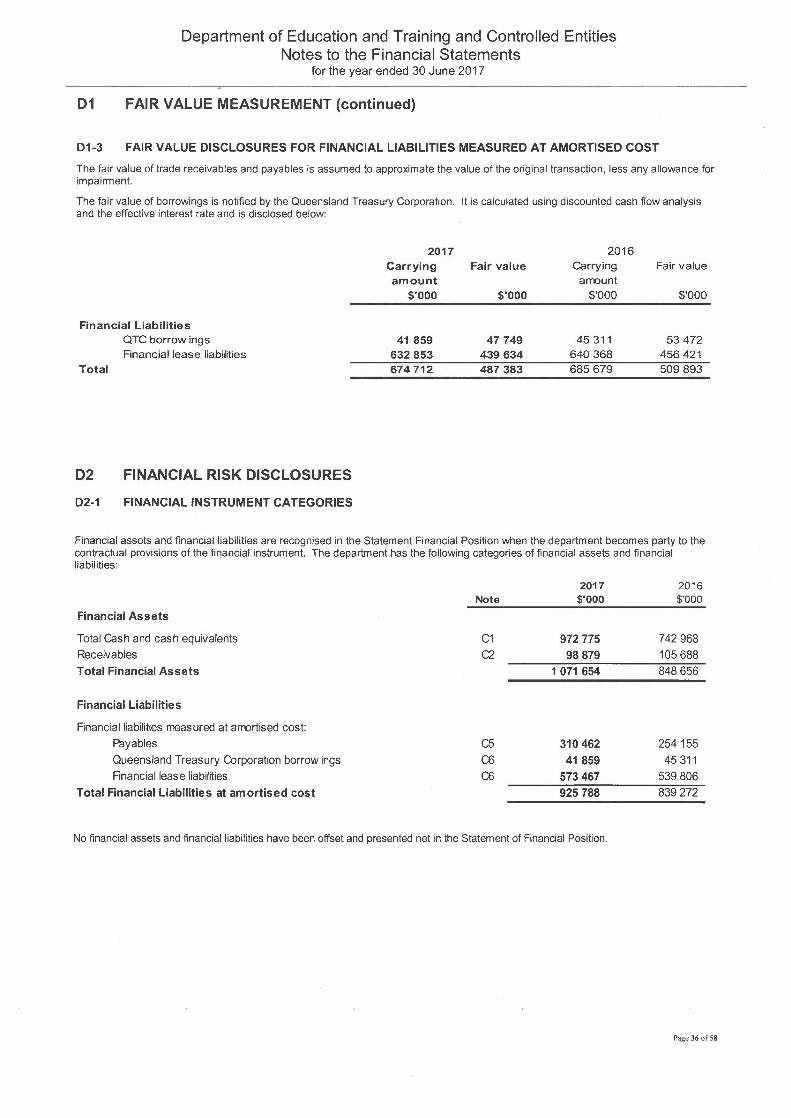

D2. Financial Risk Disclosures Page 36

D2-1 Financial Instrument Categories Page 36

D2-2 Financial Risk Management Page 37

D2-3 Maximum Credit Risk Exposure Where Carrying Amounts Do Page 37Not Egual Contractual Amounts

Notes about our E1-1 Explanation of Major Variances - Statement of Page 43Performance compared Comprehensive Incometo Budget E1-2 Explanation of Major Variances - Statement of Financial Page 43

Position

E1-3 Explanation of Major Variances - Statement of Cash Flows Page 43

Section 6 F1. Administered Activities Page 45

What we look after on F1-1 Schedule of Administered Income and Expenditure Page 45behalf of whole-of- F1-2 Reconciliation of Payments from Consolidated Fund to Page 46Government and third Administered Incomeparties F1-3 Schedule of Administered Assets and Liabilities Page 46

F1-4 Administered Activities - Budget to Actual Comparison and Page 47Variance Analysis

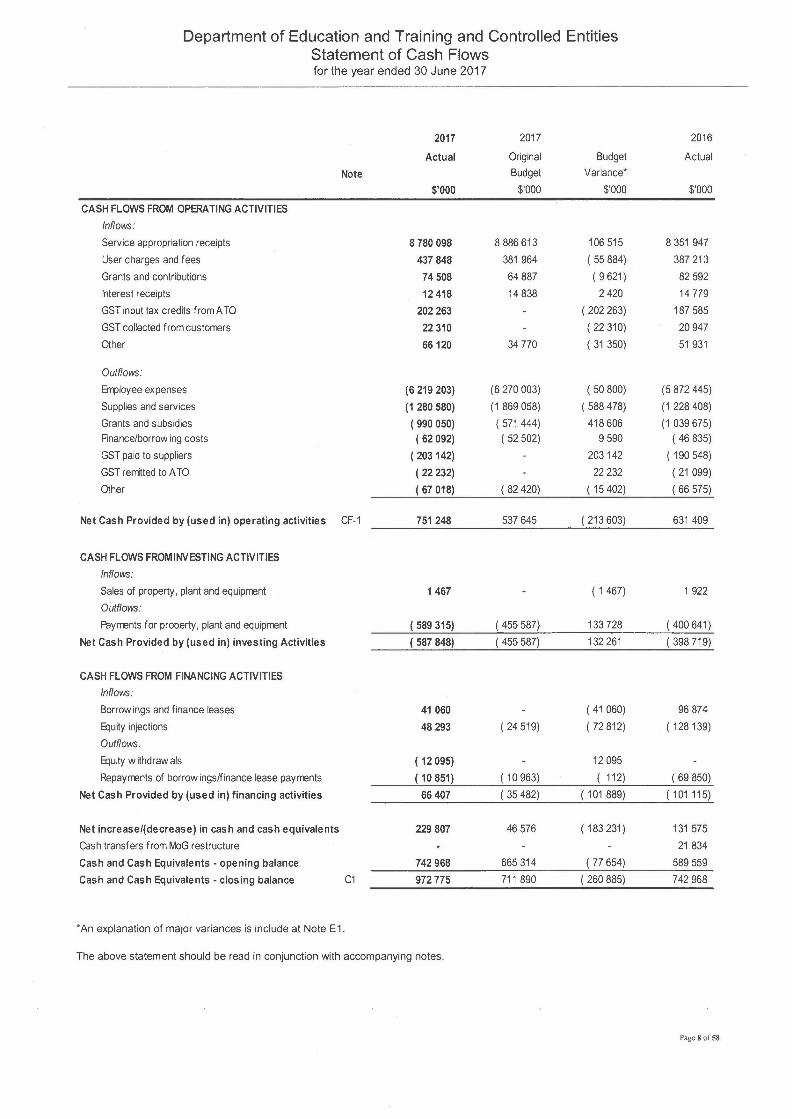

*An explanation of major variances is include at Note E1.

The above statement should be read in conjunction with accompanying notes.

Page 8 of 58

Department of Education and Training and Controlled EntitiesStatement of Cash Flowsfor the year ended 30 June 2017

NOTES TO THE STATEMENT OF CASH FLOW

CF-1 Reconciliation of Operating Result to Net Cash Provided by Operating Activities2017 2016$'000 $'000

Operating surplus/(deficit) 28817 36541

Depreciationand amortisationexpense 522309 507760Net gains on disposal of property, plant and equipment 2729 3034Donatedassets received (4238) (11713)Bad debts and impairmentlosses 7313 2222

Change in assets/liabilities (net of MaGtransfers):(Increase)/decrease in GST input tax credits receivable ( 903) ( 3 118)(Increase)/decrease in net operating receivables 7610 ( 8673)(Increase)/decrease in inventories 389 4(Increase )/decrease in other current assets 52718 ( 12663)Increase/(decrease) in other current liabilities 48610 ( 163)Increasel (decrease) in GSTpayable 102 3Increase/(decrease) in payabies 56308 17907Increase/(decrease) in accrued errployee benefits 29484 100268

Net cash provided by Operating Activities 751248 631409

Page 9 of 58

Department of Education and Training and Controlled EntitiesNotes to the Financial Statements

for the year ended 30 June 2017

SECTION 1ABOUT THE DEPARTMENT AND THIS FINANCIAL REPORT

A1 BASIS OF FINANCIAL STATEMENT PREPARATION

A1-1 GENERAL INFORMATIONThe Department of Education and Training ("the department") is a Queensland Government department established under the PublicService Act 2008 and controlled by the State of Queensland, which is the ultimate parent.

The head office and principal place of business of the department is:

Education House30 Mary StreetBrisbane QLD 4000

A1-2 COMPLIANCEWITH PRESCRIBEDREQUIREMENTSThe department has prepared these financial statements in compliance with section 42 of the Financial and Performance ManagementStandard 2009. These financial statements comply with Queensland Treasury's Minimum Reporting Requirements for reporting periodsbeginning on or after 1 July 2016.

The department is a not-for-profit entity and these general purpose financial statements are prepared on an accrual basis (except for theStatement of Cash Flowwhich is prepared on a cash basis) in accordance with Australian Accounting Standards and Interpretationsapplicable to not-for-profit entities.

New accounting standards early adopted andl or applied for the first time in these financial statements are outlined in Note G4.

A1-3 PRESENTATIONCurrency and Rounding

Amounts included in the financial statements are in Australian dollars and rounded to the nearest $1,000 or, where that amount is $500or less, to zero unless disclosure of the full amount is specifically required. Sub-totals and totals may not add due to rounding, but theoverall discrepancy is not greater than two thousand.

Comparatives

Comparative information reflects the audited 2015-16 financial statements.

CurrenU Non-current Classification

Assets and liabilities are classified as either 'current' or 'non-current' in the Statement of Financial Position and associated notes.

Assets are classified as 'current' where their carrying amount is expected to be realised within 12 months after the reporting date.Liabilities are classified as 'current' when they are due to be settled within 12 months after the report date, or the department does nothave an unconditional right to defer settlement to beyond 12 months after the reporting date.

All other assets and liabilities are classified as non-current.

A1-4 AUTHORISATIONOF FINANCIALSTATEMENTSFORISSUEThe financial statements are authorised for issue by the Director-General and Chief Finance Officer at the date of signing theManagement Certificate.

Page 10 of 58

Department of Education and Training and Controlled EntitiesNotes to the Financial Statements

for the year ended 30 June 2017

A1 BASIS OF FINANCIAL STATEMENT PREPARATION (continued)A1-5 BASISOF MEASUREMENTHistorical cost is used as the measurement basis in this financial report except for the following:

• Land, buildings, infrastructure, heritage and cultural assets which are measured at fair value;• Inventories, which are measured at the lower of cost and net realisable value.

Historical Costs

Under historical cost, assets are recorded at the amount of cash or cash equivalents paid or the fair value of the consideration given toacquire assets at the time of their acquisition. Liabilities are recorded at the amount of proceeds received in exchange for the obligationor at the amounts of cash or cash equivalents expected to be paid to satisfy the liability in the normal course of business.

Fair Value

Fair value is the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between marketparticipants at the measurement date under current market conditions (i.e. an exit price) regardless of whether that price is directlyderived from observable inputs or estimated using another valuation technique. Fair value is determined using one of the followingthree approaches:

The market approach uses prices and other relevant information generated by market transactions involving identical or comparable(i.e. similar) assets, liabilities or a group of assets and liabilities, such as a business.

• The cost approach reflects the amount that would be required currently to replace the service capacity of an asset. This methodincludes the current replacement cost methodology.

• The income approach converts multiple future cash flows amounts to a single current (i.e. discounted) amount. When the incomeapproach is used, the fair value measurement reflects current market expectations about those future amounts.

Where fair value is used, the fair value approach is disclosed.

Present Value

Present value represents the present discounted value of the future net cash inflows that the item is expected to generate (in respect ofassets) or the present discounted value of the future net cash outflows expected to settle (in respect of liabilities) in the normal course ofbusiness.

Net Realisable Value

Net realisable value represents the amount of cash or cash equivalents that could currently be obtained by selling an asset in an orderlydisposal.

A1-6 THE REPORTINGENTITYThe consolidated financial statements include all income, expenses, assets, liabilities and equity of the 'economic entity' comprising thedepartment and the entities it controls where these entities are material (refer to Note A4). All transactions and balances internal to theeconomic entity have been eliminated in full.

Page II 0[58

Department of Education and Training and Controlled EntitiesNotes to the Financial Statements

for the year ended 30 June 2017

A2 DEPARTMENTAL OBJECTIVES

The Department of Education and Training is creating opportunities for the success of Queenslanders through high quality learning andskilling services focused on preparing Queenslanders with the knowledge, skills and confidence to successfully participate in thecommunity and the economy.

Through the delivery of learning and skilling services across Queensland the department is contributing to the QueenslandGovernment's objectives for the community of:

• Creating jobs and a diverse economy (through training and skills)• Delivering quality frontline services• Building safe, caring and connected communities.

The department is funded for the departmental services it delivers principally by parliamentary appropriations.

A key focus of the department in contributing to these objectives is the shared responsibility, across service delivery areas, for thecreation of connected and accessible pathways for children, young people and students. Supporting this commitment of workingtogether to lift learning and skilling outcomes are the strategic outcomes for each service delivery area:

Early childhood education and care

Children engaged in quality early years programs that support learning and development and making successful transitions to school.

School Education

Students engaged in learning, achieving and successfully transitioning to further education, training and work.

Training and Skills

Queenslanders skilled to participate in the economy and the broader community.

A3 MACHINERY-OF-GOVERNMENT CHANGES

Transfers out - Controlled Activities

Details of Transfer: Non-reciprocal transfer of training assets (plant and equipment and portable and attractive items) from Departmentof Education and Training to TAFE Queensland.

Basis of Transfer: Ministerial approval dated 5 March 2017

Date of Transfer: Effective from 31 March 2017

The assets transferred as a result of this change were as follows:

The decrease in assets of $1.301 million has been accounted for as a decrease in contributed equity as disclosed in the Statement ofChanges in Equity.

No budgeted appropriation revenue was reallocated from the department to TAFE Queensland as part of the machinery-of-Governmentchanges.

Details of Transfer: Government Employee Centralisation Project - Phase 2.

Basis of Transfer: CBRC 44 dated 30 June 2015

Date ofTransfer: Effective from 1 July 2016

The assets transferred as a result of this change were as follows:

The decrease in assets of $19.398 million has been accounted for as a decrease in contributed equity as disclosed in the Statement ofChanges in Equity.

No budgeted appropriation revenue was reallocated from the department to the Department of Housing and Public Works as part of themachinery-of-Government changes.

Page 12of 58

Department of Education and Training and Controlled EntitiesNotes to the Financial Statements

for the year ended 30 June 2017

A4 CONTROLLED ENTITIES

The following entities are controlled entities of the department:

Directly Controlled

Aviation Australia Pty Ltd

Support the development and growth of aviation and aerospace industries both in Australianand International markets.

% Interest in Entity & Basis for Control: 100% owned by the Department of Education and Training.

Name:

Purpose and Principal Activities:

Total Assets:

Total Liabilities:

$18.423 million

$ 6.654 million

Total Revenue:

Total Operating Result:

$16.386 million

$ (1.360) million

(Unaudited amounts for financial year 2016-17 are provided.)

The BCITF (Qld) Limited

Assist in the acquisition and enhancement of the knowledge, skills, training and education ofworkers in the building and construction industry. BCITF (QLD) Limited does not trade.

% Interest in Entity & Basis for Control: 100% owned by the Department of Education and Training

Name:

Purpose and Principal Activities:

Name: Queensland Education Leadership Institute

Provide a range of professional learning services to school leaders.Purpose and Principal Activities:

% Interest in Entity & Basis for Control: 100% membership of company's constitution controlled by Minister for Education and theDirector-General, Education and Training.

Total Assets:

Total Liabilities:

$11.558 million

$ 9.358 million

Total Revenue:

Total Operating Result:

$ 6.908 million

$ 0.288 million

(Unaudited amounts for financial year 2016-17 are provided.)

Australian Music Examinations Board - Queensland Advisory Committee

Provides a graded system of examinations in music, speech and drama by offering syllabuses,educative services and publications.

% Interest in Entity & Basis for Control: The Committee is selected by the Minister for Education with changes and recommendationsrequiring the Minister's approval.

Name:

Purpose and Principal Activities:

Total Revenue: $ 1.853 million

$ 0.032 millionTotal Operating Result:

Indirectly Controlled

The department has no indirectly controlled entities.

A4-1 DISCLOSURE ABOUT WHOLLY-OWNED CONTROLLED ENTITIESAviation Australia

In October 2001, Aviation Australia Pty Ltd was formed to provide aviation training. Aviation Australia Pty Ltd prepares and publishesseparate financial statements, which are audited by the Auditor-General of Queensland.

Given the activities of the company, no dividends or other financial returns are received by the department. There are no significantrestrictions on the department's ability to access the company's assets or settle its liabilities.

The assets, liabilities, revenues and expenses of the entity listed above have not been consolidated in these financial statements asthey would not materially affect the reported financial position and operating revenue and expenses.

Page 13 of 58

Department of Education and Training and Controlled EntitiesNotes to the Financial Statements

for the year ended 30 June 2017

A4 CONTROLLEDENTITIES(continued)A4-1 DISCLOSURE ABOUT WHOLLY-OWNED CONTROLLED ENTITIES (continued)

Building ConstructionIndustry TrainingFund

The BCITF (Qld) Limited ('the Company') was established on 1 January 1999 to assist in the acquisition and enhancement of theknowledge, skills, training and education of workers in the building and construction industry. The Company is established as a publiccompany, limited by guarantee, and the Minister is the sole shareholder. The Company is controlled by the department, and is auditedby the Auditor-General of Queensland.

The assets, liabilities, revenues and expenses of the entity listed above have not been consolidated in these financial statements asthey would not materially affect the reported financial position and operating revenue and expenses.

The Company is the sole trustee of the Building and Construction Industry Training Fund ('the Trust'). The Trust is established toadvance the education and skills of persons and organisations involved in the building and construction industry, and is audited by theAuditor-General of Queensland. The Trust is not controlled by the department.

Queensland Education Leadership Institute

The Queensland Education Leadership Institute (QELi) was established on 1 June 2010 to provide a range of professional learningservices to school leaders. QELi was established as a not-for-profit public company, limited by guarantee, jointly owned by the Ministerfor Education, the Department of Education and Training, Queensland Catholic Education Commission (QCEC) and IndependentSchools Queensland (ISQ). Effective from 31 October 2016, QCEC and ISQ withdrew from membership of QELi. The company isaudited by Grant Thornton Australia Pty Ltd.

Given the.activities of the company, no dividends or other financial returns are received by the department. There are no significantrestrictions on the department's ability to access the company's assets or settle its liabilities.

The assets, liabilities, revenues and expenses of the entity listed above have not been consolidated in these financial statements asthey would not materially affect the reported financial position and operating revenue and expenses.

A4-2 DISCLOSURE ABOUT NONWHOLLY-OWNED CONTROLLED ENTITIESAustralian Music Examinations Board

The Australian Music Examinations Board (AMEB) was constituted by agreement between the Ministers for Education of the states ofQueensland, New South Wales and Tasmania and the Universities of Melbourne, Adelaide andWestern Australia. The AMEB exists toprovide a graded system of examinations in music, speech and drama, by offering high quality syllabuses, educative services to ourteachers, examiners and candidates, and quality publications to the highest editorial standard. The Queensland Advisory Committee isselected by the Minister for Education with changes and recommendations requiring the Minister's approval. The financial activities ofAMEB (Queensland) have been incorporated into the financial transactions of the department.

Page 14 of 58

Department of Education and Training and Controlled EntitiesNotes to the Financial Statements

for the year ended 30 June 2017

SECTION 2NOTES ABOUT OUR FINANCIAL PERFORMANCE

81 REVENUE

B1-1 APPROPRIATION REVENUEReconciliation of Payments from Consolidated Fund toAppropriated Revenue Recognised in Operating Result

User charges, fees and sales revenue controlled by the department are recognised as revenues when the revenue has been earnedand can be measured reliably with a sufficient degree of certainty. This involves either invoicing for related goods/services and/or therecognition of accrued revenue. Revenue from student fees is recognised as the service is provided. User charges, fees and salesrevenue are controlled by the department where they can be deployed for the achievement of departmental objectives.

Accounting Policy - Property Income

Property income is recognised as revenue when received.

Page 15 of 58

Department of Education and Training and Controlled EntitiesNotes to the Financial Statements

for the year ended 30 June 2017

81 REVENUE(continued)B1-3 GRANTS AND CONTRIBUTIONS

2017 2016$'000 $'000

10331 18749

25856 249134760 3631455 411

34295 397164238 11 714

80935 95866

Comm:mwealthreceiptsSpecific purpose

Contributions received from external partiesGrants from other State Government departmentsGoods and services received below fair valueDonations- cashDonations- other assets (1)

Total

Accounting Policy - Grants, Contributions and Donations

Grants, contributions, donations and gifts are generally non-reciprocal in nature so do not require any goods or services to be providedin return. Corresponding revenue is recognised in the year in which the department obtains control over the grant! contribution/donation (control is generally obtained at the time of receipt). Where grants are received that are reciprocal in nature, revenue isrecognised over the term of the funding arrangements.

Contributed physical assets are recognised at their fair value.

Accounting Policy - Services received below fair value

Contributions of services are recognised only if the services would have been purchased if they had not been donated and their fairvalue can be measured reliably. Where this is the case, an equal amount is recognised as revenue and an expense.

Disclosure about Donations

(1) The department's policy is to only record physical assets with a value of $10 000 or more for buildings and $5 000 for plant andequipment. Plant and equipment contributed by Parents' and Citizens' Associations were recorded on the department's Fixed AssetRegister.

Employee BenefitsTeachers' salaries and allowancesPublicservants' and other salaries and allowancesTeacher aides' salariesCleaners' salaries and allowancesJanitors'/groundstaff salaries and allowances

Employersuperannuation contributionsAnnual leave expensesLong service leave levyRedundancy payments

Employee Related ExpensesFringebenefits taxWorkers' corrpensationStaff transfer costsStaff rental accorrmodationStaff trainingTotal

Department of Education and Training and Controlled EntitiesNotes to the Financial Statements

for the year ended 30 June 2017

82 EXPENSES(continued)

B2-1 EMPLOYEE EXPENSES (continued)

The number of employees as at 30 June, including both full-time employees and part-time employees measured on a full-timeequivalent basis (reflecting Minimum Obligatory Human Resource Information (MOHRI}) is:

2017No.

2016No.

Full-TimeEquivalentErrployees 69356 68103

Accounting Policy - Wages and Salaries

Wages and salaries due but unpaid at reporting date are recognised in the Statement of Financial Position at the current salary rates.As the department expects such liabilities to be wholly settled within 12 months of reporting date, the liabilities are recognised atundiscounted values.

Accounting Policy - Sick Leave

Prior history indicates that on average, sick leave taken each reporting period is less than the entitlement accrued. This is expected tocontinue into future periods. Accordingly, it is unlikely that existing accumulated entitlements will be used by employees and no liabilityfor unused sick leave entitlements is recognised. As sick leave is non-vesting, an expense is recognised for this leave as it is taken.

Accounting Policy - Annual Leave

The entitlement for annual leave includes a component for accrued leave loading for teaching staff working at schools, but does notinclude recreation leave, which is not an entitlement under their award.

The Queensland Government's Annual Leave Central Scheme (ALCS) became operational on 30 June 2008 for departments,commercialised business units and shared service providers. Under this scheme, a levy is made on the department to cover the cost ofemployees' annual leave (including leave loading and on-costs). The levies are expensed in the period in which they are payable.Amounts paid to employees for annual leave are claimed back from the scheme quarterly in arrears.

Accounting Policy - Long Service Leave

Under the Queensland Government's Long Service Leave Central Scheme (LSLCS), a levy is made on the department to cover thecost of employees' long service leave. Levies are expensed in the period in which they are paid or payable. Amounts paid toemployees for long service leave are claimed from the scheme quarterly in arrears.

Accounting Policy - Superannuation

Post-employment benefits for superannuation are provided through defined contributions (accumulations) plans or the QueenslandGovernment's QSuper defined benefit plans as determined by the employee's conditions of employment.

Defined Contribution Plans - Contributions are made to eligible complying superannuation funds based on the rates specified in therelevant EBA or other conditions of employment. Contributions are expensed when they are paid or become payable followingcompletion of the employee's service each pay period.

Defined Benefit Plan - the liability for defined benefits is held on a whole-of-government basis and reported in those financial statementspursuant of AASB 1049 Whole of Government and General Government Sector Financial Reporting. The amount of contributions fordefined benefit plan obligations is based upon the rates determined by the Treasurer on the advice of the State Actuary. Contributionsare paid by the department at the specified rate following completion of the employee's service each pay period. The department'sobligation are limited to those contributions paid.

The department pays premiums to WorkCover Queensland in respect of its obligations for employee compensation. Workers'compensation insurance is a consequence of employing employees, but is not counted in an employees' total remuneration package. Itis not an employee benefit and is recognised separately as employee related expenses.

Key management personnel and remuneration disclosures are detailed in Note G1.

Page 17of 58

Department of Education and Training and Controlled EntitiesNotes to the Financial Statements

Accounting Policy - Distinction between Grants and Procurement

For a transaction to be classified as supplies and services, the value of goods or services received by the department must be ofapproximately equal value to the value of the consideration exchanged for those goods or services. Where this is not the substance ofthe arrangement, the transaction is classified as a grant in Note 82-3.

Accounting Policy - Operating Lease Rentals

Operating lease payments are representative of the pattern of benefits derived from the leased assets and are expensed in the periodsin which they are incurred. Incentives received on entering into operating leases are recognised as liabilities. Lease payments areallocated between rental expense and reduction of the liability.

Disclosure - Operating Lease

Operating leases are entered into as a means of acquiring access to office accommodation. Lease terms extend over a period of 1 to15 years. The department has no option to purchase the leased item at the conclusion of the lease although the lease provides for aright of renewal at which time the lease terms are renegotiated.

Operating lease rental expenses comprise the minimum lease payments payable under operating lease contracts. Lease payments aregenerally fixed, but with inflation escalation clauses on which contingent rentals are determined.

B2-3 GRANTS AND SUBSIDIES2017 2016$'000 $'000

RecurrentState Government

Grants and allowances to external organisations 538730 501 252Trainingand related services 565088 533688

Department of Education and Training and Controlled EntitiesNotes to the Financial Statements

for the year ended 30 June 2017

82 EXPENSES(continued)82-4 OTHEREXPENSES

2017 2016$'000 $'000

27076 27213776 820

2729 3034

41444 331 4

37693 365961427 1494

69747 69608

Insurance - QGIFExternal audit fees (1)

Loss on disposal of property, plant and equipmentSpecial payments: (2)

Ex-gratia payments - payments to former CoreAgreement errployeesEx-gratia payments - generalCourt awarded damages

Paymentsto other Govt Departments (3)

OtherTotal

Audit Fees

(1) The total external audit fees relating to the 2016-17 financial year are estimated to be $0.790 million (2015-16: $0.780 million).There are no non-audit services included in this amount.

Special Payments

(2) Special Payments represent ex gratia expenditure and other expenditure that the department is not contractually or legallyobligated to make to other parties. Special payments during 2016-17 include the following payments over $5,000:

the department made an ex-gratia payment for staff transfer costs on compassionate grounds.

reimbursement for damages caused by students at council premises was made by the department.

compensation was paid by the department to a community centre as a result of delayed building works and the associatedimpact on their business.

Payments to other Government Departments

(3) Payments to other Government Departments are related to School Transport arrangements with Department of Transport andMain Roads.

Losses of Public Money

Certain losses of public property are insured with the Queensland Government Insurance Fund (QGIF). The claims made in respect ofthese losses have yet to be assessed by QGIF and the amount recoverable cannot be estimated reliably at reporting date. Uponnotification by QGIF of the acceptance of the claims, revenue will be recognised for the agreed settlement amount and disclosed as'Other revenue'.

Page 190f58

Department of Education and Training and Controlled EntitiesNotes to the Financial Statements

for the year ended 30 June 2017

SECTION 3NOTES ABOUT OUR FINANCIAL POSITION

C1 CASH AND CASH EQUIVALENTS2017$'000

2016$'000

Gash on handGash at bankTotal

165972610

192742776

972775 742968

Accounting Policy - Cash and Cash Equivalents

For the purposes of the Statement of Financial Position and the Statement of Cash Flows, cash and cash equivalents includes cash onhand, cheques receipted but not banked at 30 June and cash in school and central office bank accounts which are used in the day-today cash management function of the department.

Departmental bank accounts (excluding school bank accounts) are grouped within the whole-of-Government set-off arrangement withthe Queensland Treasury Corporation and do not earn interest on surplus funds. Interest earned on the aggregate set-off arrangementbalance accrues to the Consolidated Fund.

C2 RECEIVABLES

2017 2016$'000 $'000

106441 109231(36943) ( 30267)69498 78964

3006 623932 23029( 103) ( 1)2177 399369 291

98879 102688

CurrentDebtors of an operational natureLess: Allowance for impairmentloss

Loans and advancesGST input tax credits receivableGSTpayableOther debtorsEmployeeclaims receivableTotal

Non-CurrentLoans and advances non-currentTotal

30003000

Accounting Policy - Receivables

Receivables are measured at amortised cost which approximates their fair value at reporting date.

Trade debtors are recognised at the amounts due at the time of sale or service delivery i.e. the agreed purchase/contract price.Settlement on trade debtors is required within 30 days from invoice date.

Other debtors generally arise from transactions outside the usual operating activities of the department and are recognised at theirassessed values. Terms are a maximum of three months, no interest is charged and no security is obtained.

Page 20 of 58

Department of Education and Training and Controlled EntitiesNotes to the Financial Statements

for the year ended 30 June 2017

C2 RECEIVABLES (continued)Disclosures - Credit Risk Exposure of Receivables

The maximum exposure to credit risk at balance date for receivables is the gross carrying amount of those assets inclusive of anyprovisions for impairment.

No collateral is held as security and no credit enhancements related to receivables are held by the department. In terms of collectability,receivables will fall into one of the following three categories:

• within terms and expected to be fully collectible• past due but not impaired• past due and impaired

The collectability of receivables is assessed periodically with allowance being made where receivables are impaired. Note C2-1 detailsthe accounting policies for impairment of receivables, including the loss events giving rise to impairment and the movement in theprovision for impairment.

If no loss events have arisen in respect of a particular debtor or group of debtors, no allowance for impairment is made in respect of thatdebt! group of debtors. If the department determines that an amount owing by such a debtor does become uncollectible (afterappropriate range of debt recovery action), that amount is recognised as a Bad Debt expense and written-off directly againstReceivables. In other cases where a debt becomes uncollectible but the uncollectible amount exceeds the amount already allowed forimpairment of that debt, the excess is recognised directly as a Bad Debt expense and written-off directly against Receivables.

All known bad debts were written-off as at 30 June.

All receivables within terms and expected to be fully collectible are considered of good credit quality based on recent collection history.Credit risk management strategies are detailed in Note 02.

C2-1 IMPAIRMENT OF RECEIVABLES

Accounting Policy - Impairment of Receivables

The allowance for impairment reflects the occurrence of loss events. The most readily identifiable loss event is where a debtor isoverdue in paying a debt to the department, according to the due date (normally terms of 30 days). Economic changes impacting thedepartment's debtors, and relevant industry data, also form part of the department's documented risk analysis.

Impairment loss expense for the current year regarding the department's receivables is $7.31 million. This is an increase of $5.09million from 2016, and is mainly due to recognition of corporate receivables unlikely to be recovered.

Disclosure - Movement in Allowance for Impairment for Impaired Receivables

2017$'000

2016$'000

Balance at 1 JulyIncrease/(decrease) in allowance recognised in the operating resultAmounts written off during the yearAmounts recovered during the yearBalance at 30 June

t::: It)00~N'u ~~ :::Ic.."')~~'01;jQ) -1;j t::::i SE E~«u Cl« t:::

';;",_,_111(.)

tiltil tilo til

t5j

r-- CX)..- (O C")L{)"<t(j) aCX) L{)

coCX)

o (j)

a(j)

coN

00

~

"<t C")r-- C")CX) (j)

N (ON (j)L{)

C") (j)CX) r-L{) (j)

CX)

C")cx)NNr::C") a (j) CX) r-C") L{) L{) aL{) CX) (O "<t(j) ..-a ..-

"<tC")C")L{) CX) Na N (OC") "<t C")C") CX)CX) N"<t

(00C") en

o C") It)

NegL{) M~N

NCOr-- ....a MO{o"<I'N~~

~o (O

NN(oOr-- r-- r-- Mo r-- (j) a N

..- 0N

~ ..........

(V)CX)

o "<t

C") L{) It)C")..- N

I co ........ I 0L{) CX) It)"<tC") 0

N "<I'It)

o:Q)ECQ)

c!¥r:::CD>c3""0r:::~rnr:::Q)Q):::la

eg.....oN

rn rnm (Drn '+o rn0.. r:::rn roo~

Department of Education and Training and Controlled EntitiesNotes to the Financial Statements

for the year ended 30 June 2017

C3 PROPERTY, PLANT, EQUIPMENT AND DEPRECIATION EXPENSE (continued)

C3-2 RECOGNITIONANDACQUISITION

Accounting Policy - Recognition

Basis of Capitalisation and Recognition Thresholds

Items of property, plant and equipment with a cost or other value equal to or in excess of the following thresholds are recognised forfinancial reporting purposes in the year of acquisition:

Buildings and land improvementsHeritage and cultural buildingsLandOther (including heritage and cultural assets other than buildings)

$10000$10000

$1$5000

Items with a lesser value are expensed in the year of acquisition.

Expenditure on property, plant and equipment is capitalised where it is probable that the expenditure will produce future servicepotential for the department. Subsequent expenditure is only added to an asset's carrying amount if it increases the service potential oruseful life of that asset. Maintenance expenditure that merely restores original service potential (lost through ordinary wear and tear) isexpensed.

Componentisation of Complex Assets

The department's complex assets are special purpose schools and TAFE buildings.

Complex assets comprise separately identifiable components (or groups of components) of significant value, that require replacementat regular intervals and at different times to other components comprising the complex asset.

On initial recognition, the asset recognition thresholds outlined above apply to the complex asset as a single item. Where the complexasset qualifies for recognition, components are then separately recorded when their value is significant relative to the total cost of thecomplex asset.

When a separately identifiable component (or group of components) of significant value is replaced, the existing component(s) isderecognised. The replacement component(s) are capitalised when it is probable that future economic benefits from the significantcomponent will flow to the department in conjunction with the other components comprising the complex asset and the cost exceeds theasset recognition thresholds specified above. Replacement components that do not meet the asset recognition thresholds forcapitalisation are expensed.

Components are separately recorded and valued on the same basis as the asset class to which they relate. The accounting policy fordepreciation of complex assets, and estimated useful lives, is disclosed in Note C3-5.

Accounting Policy - Cost of Acquisition

Actual cost is used for the initial recording of all non-current physical asset acquisitions. Cost is determined as the value given asconsideration plus costs incidental to the acquisition, including all other costs incurred in getting the assets ready for use, includingarchitects' fees and engineering design fees. However, any training costs are expensed as incurred.

Where assets are received free of charge from another Queensland Government department (whether as a result of a machinery-ofGovernment change or other involuntary transfer), the acquisition cost is recognised as the gross carrying amount in the books of theother entity immediately prior to the transfer together with any accumulated depreciation.

Assets acquired at no cost or for nominal consideration, other than from an involuntary transfer from another Queensland Governmententity, are recognised as assets and revenues at their fair value at the date of acquisition.

C3-3 MEASUREMENTUSINGCOSTAccounting Policy

Plant and equipment is measured at cost in accordance with Non-Current Asset Policies. The carrying amounts for such plant andequipment are not materially different from their fair value.

Page 24 of 58

Department of Education and Training and Controlled EntitiesNotes to the Financial Statements

for the year ended 30 June 2017

C3 PROPERTY, PLANT, EQUIPMENT AND DEPRECIATION EXPENSE (continued)C3-4 MEASUREMENT USING FAIR VALUEAccounting Policy

Land, buildings (including residential buildings and land improvements such as sports facilities), heritage and cultural assets, andbuildings under a finance lease are measured at fair value as required by Queensland Treasury's Non-Current Asset Policies for theQueensland Public Sector. These assets are reported at their revalued amounts, being the fair value at the date of valuation, less anysubsequent accumulated depreciation and impairment losses where applicable (refer also to an explanation later in this note regardingthe impact of different methods of accounting for accumulated depreciation and accumulated impairment losses in conjunction withrevaluations).

The cost of items acquired during the financial year has been judged by management to materially represent their fair value at the endof the reporting period. •

Assets built privately (PPP assets) are tendered out and the fair value is calculated based on construction of the assets in a privatemarket.

Assets under a finance lease that would otherwise have been included in the classes above are also revalued on the same basis as theassets in the class to which they would have belonged had they not been under a finance lease.

Fair value for land is determined by establishing its market value by reference to observable prices in an active market or recent markettransactions. The fair value of buildings and heritage and cultural assets is determined by calculating the current replacement cost ofthe asset.

Use of Specific Appraisals

Land, buildings, heritage and cultural assets are revalued by management each year to ensure that they are reported at fair value.Management valuations incorporate the results from the independent revaluation program, and the indexation of the assets not subjectto independent revaluation each year.

For the purposes of revaluation, the department has divided the state into 25 districts and each year's selection is chosen to ensure thatmajor urban, provincial and rural characteristics were included. Districts independently valued in each year are as follows:

2016-17 2017-18Tablelands-Johnstone TownsvilleMount Isa WarwickThe Downs Moreton EastBrisbane North Brisbane SouthLogan-Albert Beaudesert Sunshine Coast NorthCentral Queensland Wide Bay North

2018-19 2019-20Cairns Coastal Torres Strait and CapeCentral West RomaToowoomba Mackay-WhitsundayBrisbane Central and West MoretonWestGold Coast South East BrisbaneWide Bay West Sunshine Coast South

Wide Bay South

The fair values reported by the department are based on appropriate valuation techniques that maximise the use of available andrelevant observable inputs and minimise the use of unobservable inputs.

Use of Indices

Where assets have not been specifically appraised in the reporting period, their previous valuations are materially kept up-to-date viathe application of relevant indices. The department ensures that the application of these indices results in a valid estimation of theasset's fair value at reporting date. The State Valuation Service (SVS) supplies the indices used for various types of assets. Theseindices are derived from market information available to SVS. SVS provides assurance of their robustness, validity and appropriatenessfor application to the relevant assets. The results of interim indexations are compared to the results of the independent revaluationperformed in the year to ensure the results are reasonable. This annual process allows management to assess and confirm therelevance and suitability of indices provided by SVS based on the department's own particular circumstances.

Page 25 of 58

Department of Education and Training and Controlled EntitiesNotes to the Financial Statements

Any revaluation increment arising on the revaluation of an asset is credited to the asset revaluation surplus of the appropriate class,except to the extent it reverses a revaluation decrement for the class previously recognised as an expense. A decrease in the carryingamount on revaluation is charged as an expense, to the extent it exceeds the balance, if any, in the revaluation surplus relating to thatasset class.

On revaluation, accumulated depreciation is restated proportionately with the change in the carrying amount of the asset and anychange in the estimate of remaining useful life. .

Materiality concepts (according to the Framework for the Preparation and Presentation of Financial Statements) are considered indetermining whether any difference between the carrying amount and the fair value of each asset class is material (in which caserevaluation is warranted).

C3-5 DEPRECIATIONEXPENSEAccounting Policy

Land is not depreciated as it has an unlimited useful life.

Property, plant and equipment are depreciated on a straight-line basis so as to allocate the net cost or revalued amount of each asset,less its estimated residual value, progressively over its estimated useful life to the department.

Key Judgement: The estimated useful lives of the assets are reviewed annually and, where necessary, are adjusted to better reflectthe pattern of consumption of the asset. In reviewing the useful life of each asset, factors such as asset usage and the rate of technicaland commercial obsolescence are considered.

Any expenditure that increases the originally assessed capacity or service potential of an asset is capitalised and the new depreciableamount is depreciated over the remaining useful life of the asset to the department.

It has been determined that the department controls buildings that by their nature require componentisation and the assignment ofseparate useful lives to their component parts. The three components of these buildings are: a) Fabric; b) Fit-out; and c) Plant. Theuseful lives for these assets are disclosed in the table below.

Where assets have separately identifiable components that are subject to regular replacement, these are depreciated according touseful lives of each component.

Useful lives for the assets included in the revaluation will be amended progressively as the assets are inspected by the valuers.

The depreciable amount of improvements to or on leasehold land is allocated progressively over the estimated useful life of theimprovements or the unexpired period of the lease, whichever is the shorter. The unexpired period of leases includes any option periodwhere exercise of the option is probable.

Assets under construction (capital work-in-progress) are not depreciated until construction is complete and the asset is first put to useor is installed ready for use in accordance with its intended application. These assets are then reclassified to the relevant classes withinproperty, plant and equipment.

For the department's depreciable assets, the estimated amount to be received on disposal at the end of their useful life (residual value)is determined to be zero.

Page 26 of 58

Department of Education and Training and Controlled EntitiesNotes to the Financial Statements

for the year ended 30 June 2017

C3 PROPERTY, PLANT, EQUIPMENT AND DEPRECIATION EXPENSE (continued)C3-5 DEPRECIATIONEXPENSE(continued)Depreciation Rates

Key Estimates: For each class of depreciable asset the depreciation rates are based on the following useful lives:

Current usefulClass life (years)

Buildings - Fabric 80Buildings - Rt Out 25Buildings - Rant 25Buildings - Demountablebuildings, sheds and covered areasBuildings - Land improvements (including sporting facilities)Heritage and Cultural AssetsRant and equipment - Computer equipmentRant and equipment - Office equipmentRant and equipment - Artefacts and curiosRant and equipment - Musical instruments and craft equipmentRant and equipment - Rant and machineryRant and equipment - Sporting equipmentRant and equipment - Major refurbishments to leasehold adrrinistrative buildingsLeased plant and equipment

4015 - 808055 - 2050 - 100205 - 25102 - 125 - 10

C3-6 IMPAIRMENTAccounting Policy

All non-current physical and intangible assets are assessed for indicators of impairment on an annual basis. If an indicator of possibleimpairment exists, the department determines the asset's recoverable amount.

The asset's recoverable amount is determined as the higher of the asset's fair value less costs to sell and current replacement cost.

An impairment loss is recognised immediately in the Statement of Comprehensive Income, unless the asset is carried at a revaluedamount. When the asset is measured at a revalued amount, the impairment loss is offset against the asset revaluation surplus of therelevant class to the extent available.

Where an impairment loss subsequently reverses, the carrying amount of the asset is increased to the revised estimate of itsrecoverable amount, but so that the increased carrying amount does not exceed the carrying amount that would have been determinedhad no impairment loss been recognised for the asset in prior years. A reversal of an impairment loss is recognised as income, unlessthe asset is carried at a revalued amount, in which case the reversal of the impairment loss is treated as a revaluation increase.

Page 27 of 58

Department of Education and Training and Controlled EntitiesNotes to the Financial Statements

for the year ended30 June2017

C4 INTANGIBLES AND AMORTISATION EXPENSEC4-1 CLOSINGBALANCESAND RECONCILIATIONOFCARRYINGAMOUNT

At cost 12984 12983Less: Accurrulated arrortisation ( 8897) ( 7635)

4087 5348Softw are WIP

At cost 1526 2231526 223

Total intangible assets - net book value 43779 53375

C4-2 RECOGNITIONAND MEASUREMENT

Accounting Policies

Intangible assets of the department comprise purchased software, internally generated software and right of use facilities.

Intangible assets with a cost, or other value, greater than $100 000 are recognised in the financial statements; items with a lesser valueare expensed.

Intangible assets are measured at cost.

It has been determined that there is not an active market for any of the department's intangible assets. As such, the assets arerecognised and carried at cost less accumulated amortisation and accumulated impairment losses.

C4-3 AMORTISATIONEXPENSEAccounting Policy

All intangible assets of the department have finite useful lives and are amortised on a straight line basis over the intangible's useful life.The residual value of all the department's intangible assets is zero.

Useful Life

ClassCurrent usefullife (years)

Intangibles - Softw are purchasedIntangibles - Softw are internally generatedIntangibles- Other (based on contract life)

7 - 107 - 105 - 25

Page 28 of 58

Department of Education and Training and Controlled EntitiesNotes to the Financial Statements

for the year ended 30 June 2017

C4 INTANGIBLES AND AMORTISATION EXPENSE (continued)

C4-4 IMPAIRMENTAccounting Policy

Intangible assets are principally assessed for impairment annually by reference to the actual and expected continuing use of the assetby the department, including discontinuing the use of software or other intangible.

If an indicator of possible impairment exists, the department determines the asset's recoverable amount. Any amount by which theasset's carrying amount exceeds the recoverable amount is recorded as an impairment loss.

Page 29 of 58

Department of Education and Training and Controlled EntitiesNotes to the Financial Statements

Trade creditors are recognised upon receipt of the goods or services ordered and are measured at the nominal amount i.e. agreedpurchase/contract price, gross of applicable trade and other discounts, Amounts owing are unsecured,

Borrowings are initially recognised at fair value, plus any transaction costs directly attributable to the borrowings, The fair value ofborrowing is measured at amortised cost and set out in Note 01-3,

Any borrowing costs are added to the carrying amount of the borrowing to the extent they are not settled in the period in which theyarise, Borrowings are split between current and non-current liabilities using the principles set out in the foreword and preparationinformation section of this financial report,

The department does not enter into transactions for speculative purposes, nor for hedging, No financial liabilities are measured at fairvalue through profit or loss,

Accounting Policy - Lease Liabilities

A distinction is made in the financial statements between finance leases that effectively transfer from the lessor to the lesseesubstantially all risks and benefits incidental to ownership, and operating leases, under which the lessor retains substantially all risksand benefits,

Where a non-current physical asset is acquired by means of a finance lease, the asset is recognised at an amount equal to the presentvalue of the minimum lease payments, The lease liability is recognised at the same amount

Lease payments are allocated between the principal component of the lease liability and the interest expense,

Page 30 of 58

Department of Education and Training and Controlled EntitiesNotes to the Financial Statements

for the year ended 30 June 2017

C6 INTERESTBEARINGLIABILITIES(continued)

C6-1 BORROWINGS

Terms and ConditionsAll borrowings by the department are from the Queensland Treasury Corporation (QTC). The maturity profile is disclosed in Note D2-4.All borrowings are in $A denominated amounts and no interest has been capitalised during the current reporting period. There havebeen no defaults or breaches of the loan agreement during the 2017 or 2016 financial years. No assets have been pledged as securityfor any liabilities.

Interest Rates

The interest rate on borrowings is 5.79% (2015-16: 4.26% to 5.79%).

As it is the intention of the department to hold its borrowings for their full tenm,no fair value adjustment is made to the carrying amountof the borrowings.

Undrawn FacilitiesOn 14 January 2013, an overdraft facility with the Queensland Treasury Corporation was approved on the department's main bankaccount. This facility is limited to $250 million and remains in effect permanently. This facility remained fully undrawn at 30 June 2016and is available for use in the next reporting period. The current overdraft interest rate is 5.00% (2015-16: 5.25%).

Finance Lease Terms and ConditionsThe majority of finance leases relate to the PPP Projects - Southbank Training Precinct, South-East Queensland School - Aspire andQueensland Schools - Plenary. Refer to G3 for details.

Interest RatesInterest on finance leases is recognised as an expense as it accrues. No interest has been capitalised during the current orcomparative reporting period.The implicit interest rate for finance leases range from 2.87% to 15.84 % (2015-16: 2.87% to 13.10%).

SecurityLease liabilities are effectively secured, as the right to the leased assets revert to the lessor in the event of default.

2017 2016$'000 $'000 $'000 $'000

Minimum Present value Minimum Presentvaluepayments of payments payments of payments

Interest rate sensitivity analysis evaluates the outcome on profit or loss if interest rates would change by +/- 1 per cent from the yearend rates applicable to the department's financial assets and liabilities. With all other variables held constant, the department wouldhave a surplus and equity increase/ (decrease) of $8.821 million (2015-16: $6.486 million).

Page 31 of 57

Department of Education and Training and Controlled EntitiesNotes to the Financial Statements

for the year ended 30 June 2017

C7 ACCRUED EMPLOYEE BENEFITS

2017 2016$'000 $'000

59050 5589927871 26476

113378 883241239 1353

201 538 172 052

Annual leave levy payableLong service leave levy payableWages outstandingPaidparental leaveTotal

Accounting Policy - Accrued Employee Benefits

No provision for annual leave or long service leave is recognised in the department's financial statements as the liability is held on awhole-of-government basis and reported in those financial statements pursuant to AASB 1049 Whole of Government and GeneralGovernment Sector Financial Reporting.

C8 PROVISIONS

2017$'000

2016$'000

Current:TrainingServicesTotal

3437034370

Accounting Policy - Provisions

Provisions are recorded when the department has a present obligation, either legal or constructive as a result of a past event. They arerecognised at the amount expected at reporting date for which the obligation will be settled in a future period.

Key Estimates and Judgements Provisions

Training and Skills Division enters into contractual arrangements with training providers in the contestable training market. Since theintroduction of the contestable market in 2014, the number of providers accessing government funding has grown significantly. Thevaluation is based on the number of students enrolled in a competency at the end of the financial year but not completed. The value for2016-17 has been calculated using 2016-17 activity levels with 2015-16 withdrawal rates.

Due to the complexities in estimating the value of the provisions, it is impractical to retrospectively apply this change and provide acomparative for financial year 2015-16.

Page32 of 58

Department of Education and Training and Controlled EntitiesNotes to the Financial Statements

for the year ended 30 June 2017

C9 EQUITY

C9-1 CONTRIBUTED EQUITY

Interpretation 1038 Contributions by Owners Made to Wholly-Owned Public Sector Entities specifies the principles for recognisingcontributed equity by the department. The following items are recognised as contributed equity by the department during the reportingand comparative years:

Appropriations for equity adjustments (refer Note C9-2); and• Non-reciprocal transfers of assets and liabilities between wholly-owned Queensland State Public Sector entities as a result of

machinery-of-Government changes (refer Note A3).

C9-2 APPROPRIATIONS RECOGNISED IN EQUITY

Reconciliation of Payments from Consolidated Fund to Equity Adjustment

2017 2016$'000 $'000

( 24 519) ( 173491)72812 4535248293 (128139)

Budgeted equity adjustmentappropriationUnforeseen expenditureEquity adjustment recognised in Contributed Equity

C9-3 ASSET REVALUATION SURPLUS BY ASSET CLASS

Accounting Policy

The asset revaluation surplus represents the net effect of upwards and downwards revaluations of assets to fair value.

Heritage and LeasedLand Buildings Cultural Assets Total$'000 $'000 $'000 $'000 $'000

Balance at 1 July 2015 4851290 7457786 17392 2490 12328958

Balance at 30 June 2017 5338845 8886701 19627 54928 14300101

Page 33 of 58

Department of Education and Training and Controlled EntitiesNotes to the Financial Statements

for the year ended 30 June 2017

SECTION 4NOTES ABOUT RISK AND OTHER ACCOUNTING UNCERTAINTIES

01 FAIR VALUE MEASUREMENT

D1-1 ACCOUNTING POLICIES AND INPUTS FOR FAIR VALUESFair Value Measure

Fair value is the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between marketparticipants at the measurement date under current market conditions (i.e. an exit price) regardless of whether that price is directlyderived from observable inputs or estimated using another valuation technique.

Observable inputs are publicly available data that are relevant to the characteristics of the assets/liabilities being valued.

Unobservable inputs are data, assumptions and judgements that are not available publicly, but are relevant characteristics of the .assets/liabilities being valued. Significant unobservable data takes account of the characteristics of the department assets/liabilities,and includes internal records of recent construction costs (and/or estimates of such costs) for assets' characteristics/functionality, andassessments of physical condition and remaining useful life. Unobservable inputs are used to the extent that sufficient relevant andreliable observable inputs are not available for similar assets/liabilities.

A fair value measurement of a non-financial asset takes into account a department's ability to generate economic benefits by using theasset in its highest and best use or by selling it to another market participant that would use the asset in its highest and best use.

Fair Value Measurement Hierarchv

All assets and liabilities of the department for which fair value is measured or disclosed in the financial statements are categorised withthe following fair value hierarchy, based on the data and assumptions used in the most recent specific appraisals:

• level 1 - represents fair value measurements that reflect unadjusted quoted market prices in active markets for identicalassets and liabilities;

• level 2 - represents fair value measurements that are substantially derived from inputs (other than quoted prices included inlevel 1) that are observable, either directly or indirectly; and

• level 3 - represents fair value measurements that are substantially derived from unobservable inputs.

None of the department's valuations of assets or liabilities are eligible for categorisation into level 1 of the fair value hierarchy. Therewere no transfers of assets between fair value hierarchy levels during the period.

D1-2 BASIS FOR FAIR VALUES OF ASSETS AND LIABILITIESLand

Current Year Valuation Activitv:

30 June 2017 by State Valuation Services

Market-based assessment. Fair Value Hierarchy Level 2.

The fair value of land involved physical inspection and reference to publicly availabledata on recent sales of similar land in nearby localities in accordance with Industrystandards.

Approximately one quarter of the department's land was independently valued. Indetermining the values, adjustments were made to the sales data to take into accountthe location of the department's land, its size, street/road frontage and access, andany significant restrictions. The extent of the adjustments made varies in significancefor each parcel of land.

• The remaining three quarters of the land assets, have been indexed to ensure thatvalues reflect fair value as at reporting date. This involved the selection of a randomsample of 208 properties from the 18 districts across the state that were notindependently valued in 2016-17. State Valuation Service then provided indices foreach of these sites based on recent market transactions for local land sales. Theseindices increased the value of land in these districts by 2.86% and have been applied.

Effective Date of Last Specific Appraisal:

Valuation Approach:

Inputs:

Page 34 of 58

Department of Education and Training and Controlled EntitiesNotes to the Financial Statements

for the year ended 30 June 2017

01 FAIRVALUE MEASUREMENT(continued)01-2 BASIS FOR FAIR VALUES OF ASSETS AND LIABILITIES (continued)

Buildings

Effective Date of Last Specific Appraisal:

Valuation Approach:

Current Year ValuationActivitv:

Heritage and Cultural Assets

Effective Date of Last Specific Appraisal:

Valuation Approach:

Current Year Valuation Activitv:

Leased Assets

Effective Date of Last Specific Appraisal:

Valuation Approach:

Current Year ValuationActivitv:

30 June 2017 by State Valuation Services

All purpose-built facilities are valued at current replacement cost in accordance withthe requirements for special purpose assets contained in accounting standard AASB13 Fair Value Measurement, as there is no active market for these facilities.

State Valuation Services conduct physical inspections and applied construction ratesfrom the State School Costing Manual provided by GRC Quantity Surveyors. FairValue Hierarchy Level 3.

Approximately one quarter of the department's buildings were independently valued.The current replacement cost was based on standard school buildings and specialisedfit-out constructed by the department, adjusted for more contemporarydesign/construction approaches. Significant judgement was also used to assess theremaining service potential of these facilities, including the current physical conditionof the facility.

The remaining·three quarters were indexed using the Building Price Index provided byGRC Quantity Surveyors. The change in the Building Price Index (June 2016 to June2017) was a 4.38 percent increase. State Valuation Service have certified that theBuilding Price Index is the most appropriate measure for reflecting price changes inthe department's buildings in the years when an independent valuation is notundertaken. Management is of the opinion that the continuing investment in generaland specific priority maintenance would prevent any abnormal deterioration in assetvalues in the period between independent valuations.

30 June 2017 by State Valuation Services

As there is no active market for these assets, fair value was determined using acurrent replacement cost approach. Fair Value Hierarchy Level 3.

Estimating the cost to reproduce the items with features and materials of the originalitems, with substantial adjustments made to take into account the items heritagerestrictions and characteristics.

Approximately one quarter of the department's heritage and cultural assets wereindependently valued. The remaining three quarters were indexed to ensure thatvalues reflect fair value as at reporting date using the Building Price Index provided byGRC Quantity Surveyors. Management of the department has judged that the abovevaluations continue to materially represent fair value as at 30 June 2017.

30 June 2017 by State Valuation Services

All purpose-built facilities are valued at current replacement cost in accordance withthe requirements for special purpose assets contained in accounting standard AASB13 Fair Value Measurement, as there is no active market for these facilities.

State Valuation Services conduct physical inspections and applied construction ratesfrom the State School Costing Manual provided by GRC Quantity Surveyors. FairValue Hierarchy Level 3.

Leased assets were indexed using the indices provided by State Valuation Service asat 30 June 2017.

Page 3S of 58

Department of Education and Training and Controlled EntitiesNotes to the Financial Statements

for the year ended 30 June 2017

D1 FAIR VALUE MEASUREMENT (continued)

01-3 FAIR VALUE DISCLOSURES FOR FINANCIAL LIABILITIES MEASURED AT AMORTISED COSTThe fair value of trade receivables and payables is assumed to approximate the value of the original transaction, less any allowance forimpairment.

The fair value of borrowings is notified by the Queensland Treasury Corporation. It is calculated using discounted cash flow analysisand the effective interest rate and is disclosed below:

2017 2016Carrying Fair value Carrying Fair valueamount amount

Financial assets and financial liabilities are recognised in the Statement Financial Position when the department becomes party to thecontractual provisions of the financial instrument. The department has the following categories of financial assets and financialliabilities:

Note2017$'000

2016$'000

Financial Assets

Total Cash and cash equivalentsReceivablesTotal Financial Assets

No financial assets and financial liabilities have been offset and presented net in the Statement of FinancialPosition.

Page 36 of 58

Department of Education and Training and Controlled EntitiesNotes to the Financial Statements

for the year ended 30 June 2017

02 FINANCIALRISK DISCLOSURES(continued)

02-2 FINANCIAL RISK MANAGEMENTRisk ExposureFinancial risk management is implemented pursuant to Government policy and seeks to minimise potential adverse effects on thefinancial performance of the department.

The department's activities expose it to a variety of financial risks as set out in the following table:

Risk Exposure Definition ExposureCredit Risk Credit risk exposure refers to the situation where the The maximum exposure to credit risk in respect of

department may incur financial loss as a result of its receivables (Note C2) and the financialanother party to a financial instrument failing to guarantee provided to P&C Association,discharge their obligation. Universities and Grammar Schools (Note 03).

Liquidity Risk Liquidity risk refers to the situation where the The department aims to reduce the exposure todepartment may encounter difficulty in meeting liquidity risk in payables (Note C5) and borrowingobligations associated with financial liabilities that are from Queensland Treasury Corporate (Note C6).settled by delivering cash or another financial asset. The borrowings are based on fixed rate loans.

Market Risk The risk that the fair value or future cash flows of a The department does not trade in foreign currencyfinancial instrument will fluctuate because of changes and is not materially exposed to commodity pricein market prices. Market risk comprises three types changes.of risk: currency risk, interest rate risk and other price The department is exposed to interest rate riskrisk. through its borrowings from Queensland TreasuryInterest rate risk is the risk that the fair value or future Corporation (Note C6) and cash deposited incash flows of a financial instrument will fluctuate interest bearing accounts (Note C1).because of changes in market interest rates.

Risk Measurement and Management Strategies

The department measures risk exposure using a variety of methods as follows:

Risk Exposure Measurement Method Risk Management StrategiesCredit Risk Ageing analysis The department manages credit risk through the use of a credit

management strategy. This strategy aims to reduce the exposure tocredit default by ensuring that the department invests in secure assetsand monitors all funds owed on a timely basis. Exposure to credit riskis monitored on an ongoing basis.

Liquidity Risk Sensitivity analysis The department manages liquidity risk through the use of a liquiditymanagement strategy. This strategy aims to reduce the exposure toliquidity risk by ensuring the department has minimum but sufficientfunds available to meet employee and supplier obligations as they falldue.

This is achieved by ensuring minimal levels of cash are held within thevarious bank accounts so as to match the expected duration of thevarious employee and supplier liabilities.

Market Risk Interest rate sensitivity analysis The department does not undertake any hedging in relation to interestrisk and manages its risk as per the liquidity risk management strategyarticulated in the department's Financial Management PracticesManual.

02-3 MAXIMUM CREDIT RISK EXPOSUREWHERE CARRYING AMOUNTS DO NOT EQUAL CONTRACTUALAMOUNTS

Certain contractual obligations expose the department to credit risk in excess of the carrying amount of any asset or liability recognisedfrom entering the transaction.

The department is exposed to credit risk in respect of the debt guarantee provided to P&C Association; Universities and GrammarSchools. Details of the guarantees and the department's maximum exposure are disclosed in Note 03.

Page37 of 58

Department of Education and Training and Controlled EntitiesNotes to the Financial Statements

for the year ended 30 June 2017

D2 FINANCIAL RISK DISCLOSURES (continued)

02-4 LIQUIDITY RISK - CONTRACTUAL MATURITY OF FINANCIAL LIABILITIES

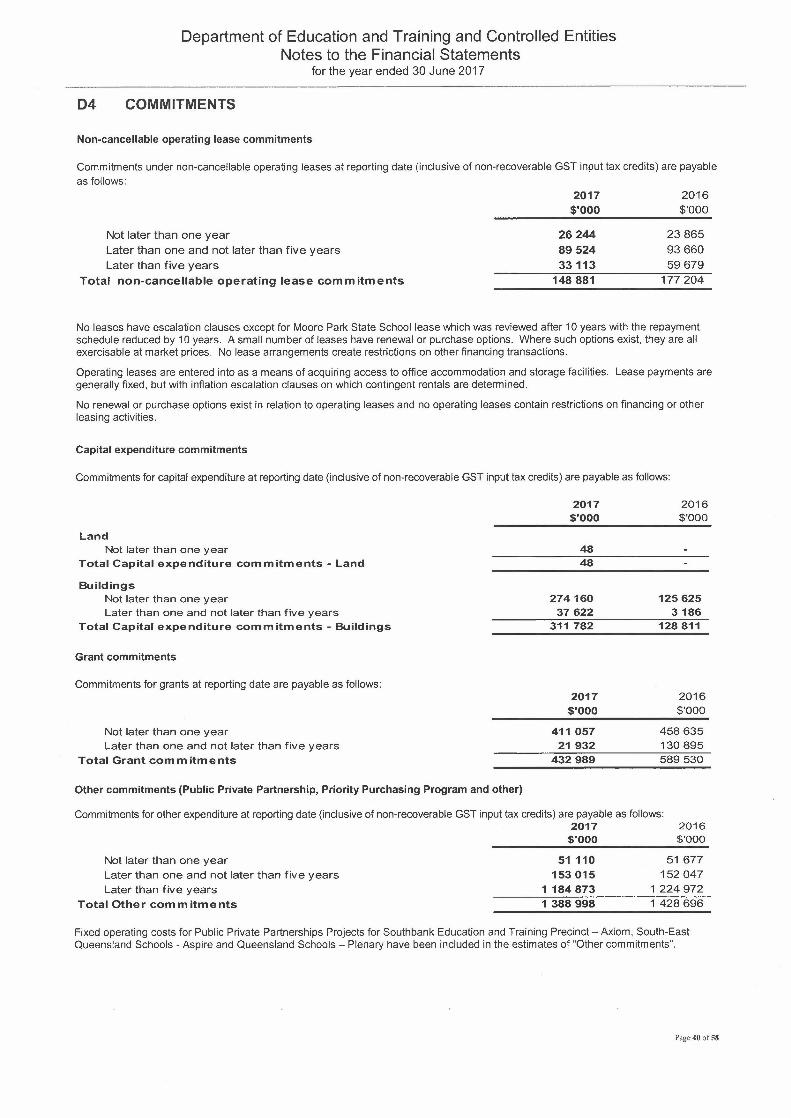

The following tables sets out the liquidity risk of financial liabilities held by the consolidated entity and the department. It represents thecontractual maturity of financial liabilities, calculated based on undiscounted cash flows relating to the liabilities at reporting date.

D3 CONTINGENCIESLitigation in ProgressAt 30 June 2017, the following caseswere filed in the courts naming the State of Queenslandacting through the Department of Educationand Training as defendant:

Litigation in progressAt 30 June 2016, the follow ing cases were before the Courts:

2017No. of cases

2016No. of cases

District Courtfv1agistrates Court

41

The department's legal advisers and management believe that it is not possible to reliably determine the value of payouts in respect ofthis litigation which, in the majority of instances, represent insurable events in terms of the policy held with the Queensland GovernmentInsurance Fund.

The maximum exposure of the department under this policy is $10 000 for each insurable event.

There are currently 132 (2015-16: 129) cases of general liability and 30 (2015-16: 29) WorkCover common law claims being managed bythe department.

., <.-Page 38 of 58

Department of Education and Training and Controlled EntitiesNotes to the Financial Statements

for the year ended 30 June 2017

03 CONTINGENCIES(continued)

Financial Guarantees and Associated Credit RisksThe department has provided 34 (2015-16: 45) financial guarantees to Parents' and Citizens' Associations, 6 (2015-16: 5) guaranteesto Universities, and 7 (2015-16: 7) guarantees to grammar schools for a variety of loans. These guarantees have been provided over aperiod of time and have various maturity dates.

The department also acts as a guarantor for Aviation Australia Pty Ltd in the event of default loan payments owed to Queensland TreasuryCorporation. The guarantee is limited to $1.157 million (2015-16: $1.457 million), which represents 100%of the outstanding loan balanceas at 30 June 2017. No default loan repayments have been recognised since the inception of the loan agreement, and the department'smanagement does not expect that the guarantee will be called upon in the near future.

The department paid a total of $10.65 million to the Construction Industry Skills Centre Pty Ltd (CISC) between 1994 -1998. The amountis only recoverable in circumstances contingent upon the winding up of CISC and the related trust. The department and the QueenslandTraining Construction Fund (QTCF) (a trust) are equal shareholders ($1 share each) in CISC and founders of the fund.

Key Estimate and Judgement: The Department of Education and Training assesses the fair value of financial guarantees annuallyas at 30 June. It has been determined that the fair value of all financial guarantees is nil as at 30 June as no defaults have beenrecognised since the inception of all guarantees, and the department's management does not expect that the guarantees will be calledupon in the near future. As such, the fair value of the guarantees has not been recognised in the Statement of Financial Position.