Page 1

1

OKAFOR, CHINEDU MARTIN

PG/M.Eng/12/62783

DESIGN OF TWO-FACTOR AUTHENTICATION (PIN AND SMS

PASSWORD) FOR AN AUTOMATED TELLER MACHINE (ATM).

FACULTY OF ENGINEERING

DEPARTMENT OF ELECTRONIC ENGINEERING

Ebere Omeje Digitally Signed by: Content manager’s Name

DN : CN = Webmaster’s name

O= University of Nigeria, Nsukka

OU = Innovation Centre

Page 2

2

DESIGN OF TWO-FACTOR AUTHENTICATION (PIN AND SMS

PASSWORD) FOR AN AUTOMATED TELLER MACHINE (ATM).

BY

OKAFOR, CHINEDU MARTIN

PG/M.Eng/12/62783

DEPARTMENT OF ELECTRONIC ENGINEERING,

UNIVERSITY OF NIGERIA, NSUKKA.

SUPERVISOR: DR. O. N. ILOANUSI

AUGUST, 2015.

Page 3

3

DESIGN OF TWO-FACTOR AUTHENTICATION (PIN AND SMS

PASSWORD) FOR AN AUTOMATED TELLER MACHINE (ATM).

BY

OKAFOR, CHINEDU MARTIN

PG/M.Eng/12/62783

DEPARTMENT OF ELECTRONIC ENGINEERING,

UNIVERSITY OF NIGERIA, NSUKKA.

AUGUST, 2015.

Page 4

4

TITLE PAGE

DESIGN OF TWO-FACTOR AUTHENTICATION (PIN AND SMS

PASSWORD) FOR AN AUTOMATED TELLER MACHINE (ATM).

BY

OKAFOR, CHINEDU MARTIN

PG/M.Eng/12/62783

DEPARTMENT OF ELECTRONIC ENGINEERING,

UNIVERSITY OF NIGERIA, NSUKKA.

Page 5

5

APPROVAL PAGE

DESIGN OF TWO-FACTOR AUTHENTICATION (PIN AND SMS PASSWORD) FOR

AN AUTOMATED TELLER MACHINE (ATM).

BY

OKAFOR, CHINEDU MARTIN

(PG/M.Eng/12/62783)

A THESIS SUBMITTED IN PARTIAL FULFILLMENT OF THE REQUIREMENTS FOR

THE AWARD OF MASTER OF ELECTRONIC ENGINEERING (DIGITAL

ELECTRONICS AND COMPUTERS OPTION) IN THE DEPARTMENT OF

ELECTRONIC ENGINEERING, UNIVERSITY OF NIGERIA, NSUKKA.

OKAFOR, CHINEDU MARTIN

(STUDENT)

SIGNATURE: ………….......... DATE: ………..........

DR. O. N. ILOANUSI

(SUPERVISOR)

SIGNATURE: ………….......... DATE: ………..........

EXTERNAL EXAMINER

SIGNATURE: ………….......... DATE: ………..........

PROF. C.I. ANI

(HEAD OF DEPARTMENT)

SIGNATURE: ………….......... DATE: ………..........

PROF. E.S. OBE

(CHAIRMAN, FACULTY

POSGRADUATE COMMITTEE)

SIGNATURE: ………….......... DATE: ………..........

Page 6

6

CERTIFICATION

Okafor, Chinedu Martin, a master’s degree postgraduate student in the

Department of Electronic Engineering and with registration number

PG/M.Eng/12/62783 has satisfactorily completed the requirements for the

award of Master of Engineering (M.Eng) in Electronic Engineering.

______________________ _____________________ Dr. O.N. Iloanusi Prof. C. I. Ani Supervisor H.O.D.

_____________________________________________

PROF. E.S. OBE

(CHAIRMAN, FACULTY POSTGRADUATE COMMITTEE)

Page 7

7

DECLARATION

I, Okafor Chinedu Martin, a postgraduate student of the Department of

Electronic Engineering, University of Nigeria, Nsukka declare that the work

embodied in this thesis is original and has not been submitted by me in part or

in full for any other diploma or degree of this or any other University.

___________________________

OKAFOR, CHINEDU MARTIN

PG/M.Eng/12/62783

__________________

DATE

Page 8

8

DEDICATION

This research work is dedicated to God Almighty for his mercy. Also to my

family, for all the support towards achieving my career goals.

Page 9

9

ACKNOWLEDGEMENTS

My profound thanks go to my supervisor, Dr. O.N. Iloanusi for her accessibility,

encouragement and constructive criticism that geared me towards working

hard to achieve this work. My unalloyed thanks go to Prof. C.C. Osuagwu, Prof.

C.I. Ani and the rest of the staff of the department for their co-operation

within the time of this work.

A number of personal friends and professional colleagues, especially Engr.

Ahamdi Abarikwu and Engr. Uche Nwali, provided valuable help in the course

of this research. I wish to use this opportunity to thank them all.

My regards go to my family for the moral support throughout this programme.

Finally, I wish to acknowledge all the authors whose materials are referenced

in this research work.

Okafor, Chinedu Martin

Page 10

10

ABSTRACT

Most ATMs employ one means of authentication (single factor authentication) by using the PIN. These kinds of ATMs are vulnerable to ATM frauds like Card Skimming: where a device placed at the slot for the ATM Card copies all the information stored in ATM cards including the PINs and then copies of the original cards will be made, afterwards money will be stolen from the accounts concerned. This work presents the design of ATM software that employs a two factor authentication method that utilises the PIN and a One Time Password (OTP) which will be sent to the client’s mobile phone through SMS. This process will be initiated by the ATM as soon as the user slots his ATM card and the system accepts it. By employing this technology, a fraudster who has access to someone’s ATM Card and PIN will still not gain access to their bank account if he has no access to the SMS containing the One Time Password. This work employed Object Oriented Analysis and Design (OOAD) as its methodology and this includes the use of the Unified Modelling Language (UML). In order to realise the system using the OOAD approach, C#, an oriented programming language was used. The result obtained at the end of this project is the prototype of ATM software that employs two factor authentication. Finally, the performance of the system while it was being tested shows that the objective of providing additional security using two factor authentication was achieved to a large extent.

Page 11

11

TABLE OF CONTENT

Title page - - - - - - - - - - i

Approval page - - - - - - - - - ii

Certification - - - - - - - - - - iii

Declaration - - - - - - - - - - iv

Dedication - - - - - - - - - - v

Acknowledgements - - - - - - - - - vi

Abstract - - - - - - - - - - vii

Table of Content - - - - - - - - - viii

List of Figures - - - - - - - - - xi

List of Tables - - - - - - - - - xiv

CHAPTER ONE: INTRODUCTION

1.1 Background to the study - - - - - - - 1

1.2 Statement of the Problem - - - - - - - 7

1.3 Objectives - - - - - - - - - 8

1.4 Scope of Study - - - - - - - - - 8

1.5 Significance of Study - - - - - - - - 9

1.6 Proposed Methodology - - - - - - - 9

1.7 Organization of Thesis - - - - - - - 10

CHAPTER TWO: LITERATURE REVIEW

2.1 Review of the Related Works - - - - - - 12

2.2 Review of the Technologies involved in the proposed Design - 17

2.2.1 Authentication Mechanisms used in electronic banking - 17

2.2.2 The ATM System Technology - - - - - 20

2.2.2.1 The ATM Hardware - - - - - 24

2.2.2.2 The ATM Software - - - - - 25

Page 12

12

2.2.3 Short Message Service (SMS) - - - - - 32

2.2.3.1 Bulk SMS Service - - - - - 33

2.2.4 Mechanism employed in this work for sending

the One Time Password (OTP) - - - - - 34

CHAPTER THREE: RESEARCH METHODOLOGY

3.1 Methods Adopted for this Work - - - - - - 35

3.1.1 Object Oriented Analysis and Design (OOAD)- - - 35

3.1.1.1 The Waterfall Model Software Development

Life Cycle - - - - - - - 40

3.1.2 Modelling and Simulation - - - - - - 45

CHAPTER FOUR: SYSTEM ANALYSIS AND DESIGN

4.1 System Specification - - - - - - - - 53

4.1.1 Requirements Definition - - - - - - 53

4.1.2 UML Modelling of the System - - - - - 55

4.1.3 Main Menu Specification - - - - - - 65

4.1.4 Input Specification - - - - - - - 65

4.1.5 Output Specification - - - - - - 66

4.1.6 Database Specification - - - - - - 68

4.1.7 Hardware and Software Requirements - - - - 69

4.2 System Design - - - - - - - - 70

4.2.1 Main Menu Design - - - - - - - 70

4.2.2 Input Design - - - - - - - - 76

4.2.3 Output Design - - - - - - - 77

4.2.4 Database Design - - - - - - - 79

CHAPTER FIVE: SYSTEM IMPLEMENTATION, TESTING AND SIMULATION

5.1 System Implementation - - - - - - - 82

5.1.1 Main Menu Implementation - - - - - 84

Page 13

13

5.1.2 Input Implementation - - - - - - 85

5.1.3 Output Implementation - - - - - - 87

5.1.4 Choice of Programming Language - - - - 88

5.2 System Integration - - - - - - - 94

5.3 System Testing - - - - - - - - 95

5.3.1 Cash Withdrawal Testing - - - - - - 102

5.3.2: Change Security PIN Testing - - - - - 105

5.3.3 Balance Inquiry Testing - - - - - - 108

5.4 Debugging - - - - - - - - - 110

CHAPTER SIX: CONCLUSION

6.1 Summary - - - - - - - - - 112

6.2 Contribution of the proposed model to the Body of Knowledge - 113

6.3 Recommendations - - - - - - - - 113

References - - - - - - - - - - 115

Appendix A - - - - - - - - - - 119

Appendix B - - - - - - - - - - 126

Appendix C - - - - - - - - - - 152

Page 14

14

LIST OF FIGURES

Fig. 1.1: A Classical ATM Machine - - - - - - 2

Fig. 1.2: Schematic diagram for the ATM - - - - - 2

Fig. 1.3: Typical Skimming Device - - - - - - 4

Fig. 1.4: A typical Card Trapping device - - - - - 5

Fig. 1.5: Card Trapping Device being placed on genuine card slot - 5

Fig. 1.6: A typical Pin Pad Overlay - - - - - - 6

Fig. 2.1: A Typical ATM Machine - - - - - - 21

Fig. 2.2: Diagram for the ATM Connected to a Network - - - 21

Fig. 2.3: Block diagram for the ATM - - - - - - 24

Fig. 2.4: Xpeak architecture - - - - - - - 30

Fig. 2.5: SMS network architecture - - - - - - 32

Fig. 2.6: Mechanism for sending the One Time Password - - - 34

Fig. 3.1: Typical diagram of a class - - - - - - 37

Fig. 3.2: Encapsulation hides the class’ state and implementation

from the (client) - - - - - - - - 38

Fig 3.3: Withdrawal class, Deposit class and Transfer class inherit

from Transaction class as shown with a small triangle

pointing to the superclass - - - - - - 39

Fig. 3.4: The Waterfall Model (with interstage feedback) - - - 42

Fig. 3.5: A typical Use Case Diagram - - - - - - 46

Fig. 3.6: A typical Class Diagram - - - - - - - 47

Fig. 3.7: A typical Sequence Diagram - - - - - - 48

Fig. 3.8: A typical Activity Diagram - - - - - - 50

Page 15

15

Fig. 3.9: A typical Deployment Diagram - - - - - 51

Fig. 4.1: Sequence diagram of the system - - - - - 56

Fig. 4.2: Activity Diagram for the System - - - - - 58

Fig. 4.3: ATM Use Case diagram - - - - - - - 60

Fig. 4.4: Class diagram of Banking and ATM classes - - - - 62

Fig. 4.5: Deployment diagram of the system - - - - - 64

Fig. 4.6: System Block Diagram - - - - - - - 70

Fig. 4.7: Operation of One Time Password verification - - - 71

Fig. 4.8: System flowchart - - - - - - - 72

Fig. 4.9: ATM Keypad - - - - - - - - 77

Fig. 4.10: Output Design of ATM - - - - - - 78

Fig. 4.11: ATM machine input and output design - - - - 78

Fig. 5.1: The Simulated ATM system - - - - - - 84

Fig. 5.2: Transaction Menu Screenshot - - - - - 86

Fig. 5.3: ATM Welcome screen - - - - - - - 96

Fig. 5.4: ATM cards form - - - - - - - - 97

Fig. 5.5: Input Security PIN screen - - - - - - 98

Fig. 5.6: Invalid PIN screenshot - - - - - - - 99

Fig. 5.7: Account blocked screenshot - - - - - - 99

Fig. 5.8: One Time Password (OTP) verification screen - - - 100

Fig. 5.9: Invalid OTP screenshot - - - - - - - 101

Fig. 5.10: ATM machine showing transaction main menu - - - 101

Fig. 5.11: Select Account Type Screenshot - - - - - 102

Fig. 5.12: Select amount to withdraw Screenshot - - - - 103

Fig. 5.13: Input amount to withdraw Screenshot - - - - 103

Fig. 5.14: Cash withdrawal screenshot - - - - - - 104

Fig. 5.15: Cash Withdrawal Statement - - - - - - 105

Page 16

16

Fig. 5.16: Input old PIN Screenshot - - - - - - 106

Fig. 5.17: Enter new PIN Screenshot - - - - - - 106

Fig. 5.18: Re-enter new PIN Screenshot - - - - - 107

Fig. 5.19: PIN changed successfully Screenshot - - - - 107

Fig. 5.20: Balance Inquiry Screenshot - - - - - - 108

Fig. 5.21: Perform another operation Screenshot - - - - 109

Fig. 5.22: Transaction Termination message - - - - - 109

Page 17

17

LIST OF TABLES

Table 2.1: Comparison Table for the related works - - - - 17

Table 2.2: Windows XP System Requirements - - - - 27

Table 4.1: Input and Output Specifications - - - - - 68

Table 4.2: List of tables in ATM database - - - - - 68

Table 4.3: atm_cards– stores ATM card information - - - 79

Table 4.4: atm_cash_withdrawal– stores predefined ATM withdrawal

amount - - - - - - - - - 79

Table 4.5: atm_otp– stores one time password - - - - 80

Table 4.6: bank_account– stores customers account balance - - 80

Table 4.7: bank_minbalance– stores the bank mini balance that cannot be

withdrawn - - - - - - - - 80

Table 4.8: bank_transactions– stores contacts and inquiries - - 80

Table 4.9: customers– stores customers’ personal details - - - 81

Table 5.1: List of output screen user controls - - - - 88

Table 5.2: Comparison of C# and Java based on data type - - - 90

Table 5.3: Comparison of C# and Java based on reference type - - 91

Table 5.4: Comparison of C# and Java based on arrays and collections - 92

Table 5.5: Comparison of C# and Java based on object orientation - 94

Table 5.6: Pre-stored ATM cards - - - - - - 95

Page 18

18

CHAPTER ONE

INTRODUCTION

1.1 Background to the Study

Brief History of the ATM

The concept of self-service in retail banking has evolved through various

stages. These stages include cash machines developed in the early 1960s

through independent and simultaneous efforts of engineers in Britain, Sweden

and Japan. The first of such commercial cash machines was put into use in the

UK on the 27th of June 1967 by the Barclays Bank. These and other

developments (which were championed by efforts in Asia, Europe and

America) gave rise to the automated (automatic) teller machine (ATM). The

first modern ATM came into use in December 1972 and was designed by IBM

for Lloyd Banks. The machine was called the IBM 2984 and popularly known as

the CIT: Cash Issuing Terminal. The CIT was considered the first true cash point

and is similar to what we have nowadays [1].

The ATM is a networked computer terminal that provides Bank clients with

access to financial transactions from a public space without the need for one

to visit the bank branch. Figure 1.1 shows a classical ATM Machine and figure

1.2 shows the schematic diagram for the ATM. The ATM is considered a

networked computer terminal because it is basically a computer that must be

connected to a bank server or/and network of computers such as the internet

in order to achieve its purpose (see fig. 2.1). Using the ATM, customers can

access their bank accounts in order to make cash withdrawals or check their

account balances as well as paying their bills [2].

Page 19

19

Fig. 1.1: A Classical ATM Machine (Source: elprocus.com).

Fig. 1.2: Schematic diagram for the ATM.

CPU

PRINTER

KEYPAD SPEAKER

CARD

READER

DISPLAY

CASH

DISPENSER

COMMUNICATION

INTERFACE

MEMORY

Page 20

20

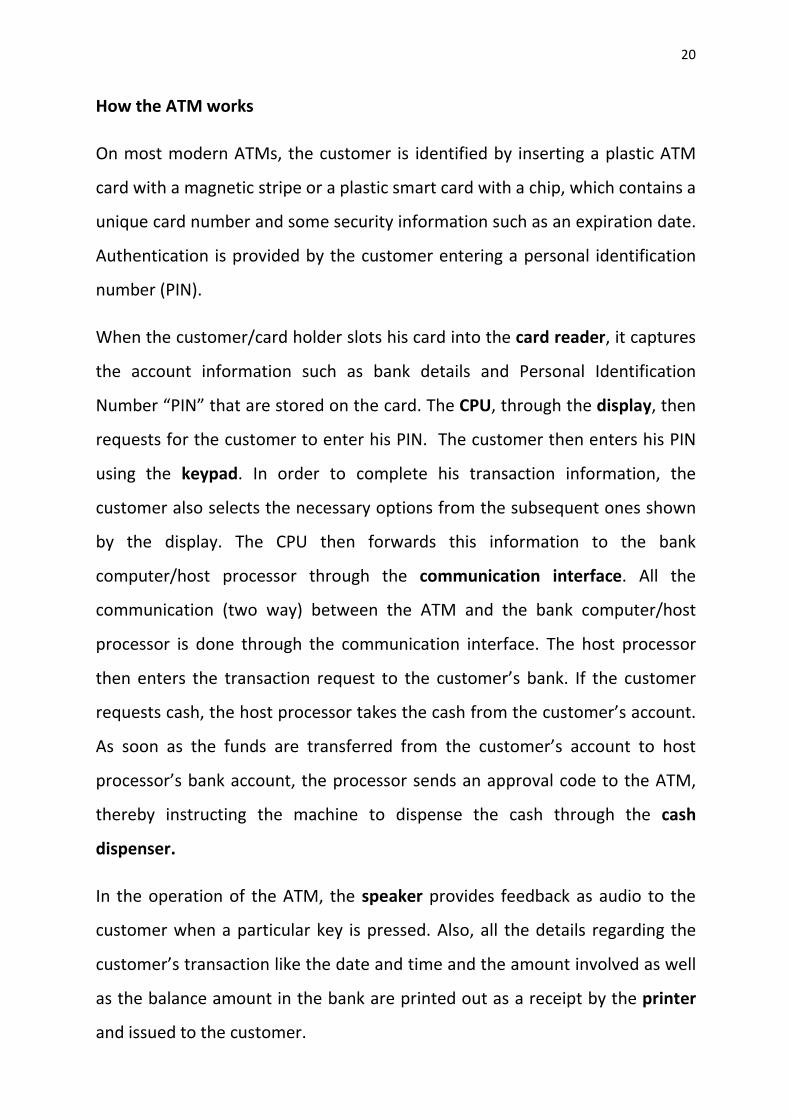

How the ATM works

On most modern ATMs, the customer is identified by inserting a plastic ATM

card with a magnetic stripe or a plastic smart card with a chip, which contains a

unique card number and some security information such as an expiration date.

Authentication is provided by the customer entering a personal identification

number (PIN).

When the customer/card holder slots his card into the card reader, it captures

the account information such as bank details and Personal Identification

Number “PIN” that are stored on the card. The CPU, through the display, then

requests for the customer to enter his PIN. The customer then enters his PIN

using the keypad. In order to complete his transaction information, the

customer also selects the necessary options from the subsequent ones shown

by the display. The CPU then forwards this information to the bank

computer/host processor through the communication interface. All the

communication (two way) between the ATM and the bank computer/host

processor is done through the communication interface. The host processor

then enters the transaction request to the customer’s bank. If the customer

requests cash, the host processor takes the cash from the customer’s account.

As soon as the funds are transferred from the customer’s account to host

processor’s bank account, the processor sends an approval code to the ATM,

thereby instructing the machine to dispense the cash through the cash

dispenser.

In the operation of the ATM, the speaker provides feedback as audio to the

customer when a particular key is pressed. Also, all the details regarding the

customer’s transaction like the date and time and the amount involved as well

as the balance amount in the bank are printed out as a receipt by the printer

and issued to the customer.

Page 21

21

Common ATM Frauds

The evolution of ATMs has resulted in the evolution of ATM Frauds. These

frauds are of various types and employ varying tactics. Amongst these frauds

we have;

Card Skimming: The card details and PIN are captured at the ATM by a device

placed at the card reader and used to produce counterfeit cards for

subsequent fraudulent cash withdrawals. Figure 1.3 shows a typical case of

card skimming.

On the left part of figure 1.3, the skimming device is shown being placed on

top of the card slot/card reader. It looks much like the card reader but it is

fake. The right part of figure 1.3 shows the skimming device fully placed on top

of the card reader. As the card holder slots his card, the skimming device

copies all the information on the card including the PIN and as such copies of

Fig. 1.3: Typical Skimming Device (Source: Google.com).

Genuine Card Slot

Skimming Device

Page 22

22

the card could be made elsewhere and used to withdraw from the same

account. The customer is unaware of the card skimming and sees a normal

transaction and retains the card.

Card Trapping: In this case, the card is physically captured at the ATM by a

device placed at the card slot and the PIN is compromised. Later the card is

retrieved and used to make fraudulent cash withdrawals. The customer loses

the card. Figure 1.4 shows the card trapping device while figure 1.5 shows

how the card trapping device is placed on the card slot.

Fig. 1.4: A typical Card Trapping device (Source: google.com).

Fig. 1.5 Card Trapping Device being placed on genuine card slot (Source:

google.com).

Genuine Card Slot

Card Trapping Device

Page 23

23

Pin Compromise: Here the criminal uses a Pin Pad Overlay to acquire the PIN.

The Pin Pad Overlay is a false PIN pad which is fitted on top of the existing PIN

pad. Most times the Pin Pad Overlay could be a flexible piece of circuit-

embedded plastic that fits perfectly over the ATM's genuine PIN pad. Figure

1.6 shows a pin pad overlay being placed on a genuine keypad.

Sometimes miniature cameras, remotely positioned cameras or video

surveillance could be used to accomplish Pin Compromise.

Fig 1.6: A typical Pin Pad Overlay (Source: google.com).

These frauds necessitate the need for such efforts as Two-Factor

Authentication in other to curb them.

Two-Factor Authentication

This is an authentication mechanism that utilizes a combination of two factors

such as Username and Password, PIN and SMS One Time Password, or

Username and Fingerprint. This method is used by various banks and other

financial institutions for authentication for online banking.

Pin Pad Overlay

Genuine Key Pad

Page 24

24

Most ATMs employ one means of authentication (single factor authentication)

by using the PIN. These kinds of ATMs are vulnerable to ATM frauds like Card

Skimming: where a device placed at the slot for the ATM Card copies all the

information stored in the card including the PIN [3]. Since the PIN is the only

means of authentication (Single Factor Authentication), then the security of

the ATM will be compromised, duplicates of all cards copied will be made and

illegal access to the corresponding bank accounts will be achieved and money

will move to the wrong hands.

This project aims to reduce these ATM frauds by developing the prototype of

the ATM software that will employ a two factor authentication method that

utilises the PIN and a One Time Password (OTP) which will be sent by the ATM,

through SMS, to the client’s mobile phone immediately it accepts his ATM

Card. As this technology is employed, whoever then has access to somebody’s

ATM Card and PIN will fail at any attempt to gain access to their bank account,

unless the fraudulent person has access to the phone (and SMS) which bears

the One Time Password (OTP).

1.2 Statement of the Problem

The need to ensure the security of money while carrying out the automation of

banking services cannot be over-emphasised, i.e. the advantages are

overwhelming. Considering the fact that automation speeds up processes

(most especially the rolling out of services) and the banking sector is at the hub

of economic development, automating retail banking invariably speeds up an

economy and ensures economic growth provided there are means to curb the

resulting frauds.

Page 25

25

1.3 Objectives

The objectives of this project are:

--To develop ATM software that will employ the Two Factor Authentication

process in its operation and thereby achieve the security of funds and the

reduction of ATM frauds.

--This project is aimed at showing that already existing infrastructure for

financial services could be further utilised to enhance the security of financial

transactions and as such save cost of additional hardware needed to achieve

enhanced security.

--To explore the viability of the GSM/SMS technology in enhancing ATM

security.

1.4 Scope of Study

The scope of this work includes the technologies, parameters and processes

that are within this research and they are listed below as follows:

-- Security of ATM transactions and the effect of Two Factor Authentication in

reducing them.

--SMS technology and the Bulk SMS Service: In this work, the SMS technology

is the medium through which the One Time Password is delivered to the

customer.

--Object Oriented Analysis and Design (OOAD): The Software Engineering

involved in this work is firmly rooted in OOAD.

--Unified Modelling Language (UML): The UML is the industry-standard

Modelling language in the field of software engineering. UML is employed in

creating visual models, specifying and constructing software systems and also,

Page 26

26

non-software systems [4]. UML is found to be very useful in carrying out

OOAD.

--Object Oriented Programming (OOP): Usually OOAD gives rise to Object

Oriented Programming. C# is the Object Oriented Programming Language

employed in this research.

1.5 Significance of Study

The significance of this project is that it will provide a viable means of fortifying

the security of money in bank accounts. This project will provide a way of

reducing illegal banking transactions made with the ATM. By employing the

Two Factor Authentication procedure crime will be curtailed and financial

services will be enhanced.

1.6 Proposed Methodology

This work uses the following methodology:

Object Oriented Analysis and Design (OOAD): In this work Object Oriented

Analysis and Design (OOAD) is employed. Using OOAD, Object Oriented

Decomposition is done within the confines of the vocabulary of the problem to

be solved. Object-oriented analysis focuses on the analysis that examines

requirements with respect to the classes and objects found in the description

of the problem domain. By using this methodology requirements will be

organised around objects, which integrate both behaviours (processes) and

states (data) modelled after real world objects that the system interacts with.

Object Oriented Design employs the results obtained through Object-oriented

analysis in order to design the system.

Also, a suitable Software Development Life Cycle (SDLC) is chosen for use in

this work. The choice of the SDLC is the Waterfall Model Software

Page 27

27

Development Life Cycle. At the appropriate stage of this SDLC, OOAD will be

carried out. OOAD also involves the use of graphical modelling and simulation.

Modelling and Simulation: This software system will be modelled using the

Unified Modelling Language (UML). The UML is found very useful in developing

the visual models of a whole lot of systems.

The coding (in C#) and simulation of this system will be done using Visual

Studio.

1.7 Organization of Thesis

The rest of this Thesis is organised as follows;

Chapter Two: Literature Review- In this chapter, an analytical overview of the

significant literature published on this work is provided and their strengths and

weaknesses are exposed. The reasons for this are to gain insight into the work,

to distinguish what has been done from what needs to be done and to

rationalise the significance of the work.

Also the key concepts involved in this work will be looked into and reviewed.

Chapter Three: Research Methodology- This chapter will deal with the

methods involved in carrying out this work. It aims at showing how they are

organised and structured.

Chapter Four: System Analysis and Design- This chapter provides a practical

application of Object Oriented Analysis and Design along with the Waterfall

Software Development Life Cycle in analysing and designing the system in

question.

Chapter Five: System Implementation, Testing and Simulation- Here the

different modules of the software will be implemented. The implementation

Page 28

28

will be done using an object oriented programming language called C#. Also

this chapter will handle the testing and simulation of the software codes.

Chapter Six: Conclusion- Here the work will be summarised and duly

concluded.

Page 29

29

CHAPTER TWO

LITERATURE REVIEW

2.1 Review of the Related Works

In the following, already existing works concerning the improvement of ATM

and Internet Banking security through various technologies are discussed.

(I) Model for Token Based Secure Transaction in ATM Networks by Sonika

Katta, Dinesh Goyal, Ruchi Dave, Naveen Hemrajani, IJCSET, August 2011,

Vol 1, Issue 7, 395-398.

Here, the authors introduce the hardware Token. The hardware Token or

simply Token is a physical device that performs or aids authentication. This can

be a secure storage device containing passwords, such as a bankcard or smart

card. This can also be an active device that yields One-Time Passcodes, either

time-synchronous (changing in synchrony with a master at the host server) or

challenge–response (responding to a one-time challenge). Token security

defences include tamper-resistant packaging and special hardware that

disables the token if it is tampered with or if the number of failed

authentication attempts exceeds a chosen threshold. The token acts like an

electronic key to access something.

In this model if a user wishes to use the ATM, he would use the Token along

with the PIN for authentication and prove that he is who he claims to be

before making any transaction. The token provides the One Time Passcode

needed for authentication [5].

Page 30

30

(II) Authentication in an Internet Banking Environment by the US Federal

Financial Institutions Examination Council (http://www.ffiec.gov/)

In this work, the USB token device is introduced. This device is typically the size

of a house key. It plugs directly into a computer’s USB port and therefore does

not require the installation of any special hardware on the user’s computer.

Once the USB token (the first authenticating factor) is recognized by a

computer in which it is plugged, the customer is prompted to enter his or her

password (the second authenticating factor) in order to gain access to the

computer system and effect financial transactions.

USB tokens are one-piece, injection-moulded devices. USB tokens are hard to

duplicate and are tamper resistant; thus, they are a relatively secure vehicle for

storing sensitive data and credentials. The device has the ability to store digital

certificates that can be used in a public key infrastructure (PKI) environment.

The USB token is generally considered to be user-friendly. Its small size makes

it easy for the user to carry and, as noted above, it plugs into an existing USB

port; thus the need for additional hardware is eliminated [6].

(III) Enhancing ATM security using fingerprint and GSM technology by Ashish

M. Jaiswal and Mahip Bartere, IJCSMC, Vol. 3, Issue. 4, April 2014, pg.28 – 32.

In this design Bankers will collect the customer’s finger prints and mobile

phone number(s) while opening accounts for them, then afterwards the

customer can access the ATM machine. When the customer uses the ATM:

after inserting the card, he must place his finger on the finger print module, he

then gets automatically generated 4-digit code every time as a message to his

mobile phone through GSM modem connected through a microcontroller to

the ATM. The code received by the customer should be entered by pressing

Page 31

31

the keys on the ATM screen, and only after that will he be able to make

transactions [7].

(IV) Facial Verification Technology for Use in ATM Transactions by Aru,

Okereke Eze, Ihekweaba Gozie, AJER, Vol-2, Issue-5, 2013, pp-188-193.

This paper proposes an automatic teller machine security model that would

combine a physical access card, a PIN, and electronic facial recognition. In this

model, as a user walks to the ATM (its digital camera is on 24hours a day), its

computer will automatically initiate a face recognition procedure. Whenever

the computer detects a human face, its camera obtains a picture of the face,

the computer compares the image of the face to the images of those of

registered customers in its database .If the face (as seen by the ATMs camera)

matches the picture of that in the database, then the user is automatically

recognized by the machine [8].

(V) Designing a Biometric Strategy (Fingerprint) Measure for Enhancing ATM

Security in Indian E-Banking System by Sri Shimal Das, Smt. Jhunu Debbarma,

IJICT, Vol. 1, No. 5, September 2011.

In this paper the authors propose the design of an ATM that uses the ATM card

and the customer’s fingerprint (instead of the PIN) in order to achieve

sufficient ATM security. The proposed system works as follows: at the time of

transaction (i.e., after the machine has read and accepted the ATM card),

customers enrol their fingerprint to a high resolution fingerprint scanner. The

fingerprint image is transmitted via secured channel to the central server

which contains a record of customers’ fingerprints. At the banking terminal the

minutiae extraction and matching are performed in order to verify that the

presented fingerprint image belongs to the claimed user in the bank’s

database. Then authentication is granted if the minutiae matching are

Page 32

32

successful, otherwise authentication is denied. This proposed ATM biometric

authentication system consists of five main components. They are: sensor,

feature extractor, fingerprint/template database, and matcher and decision

module. The function of the sensor is to scan the biometric trait of the user.

The function of the feature extraction module is to extract the feature set from

the scanned biometric trait. This feature set is then stored into the template

database. The matcher module takes two inputs, i.e. features set from the

template database and features set of the user who it wants to authenticate

and compares the similarity between the two sets. The last module, i.e., the

verification module makes the decision about the matching of the two features

sets [9]. By doing all these, this proposed system could achieve sufficient

security for ATMs.

Comparison Table for the related works

Title and Author Strength Limitation

Model for Token Based

Secure Transaction in

ATM Networks by Sonika

Katta, Dinesh Goyal,

Ruchi Dave, Naveen

Hemrajani, 2011.

The use of Tokens is

another means of

achieving secure

transactions as against

the use of human

features in biometrics.

It is costly to implement

because of the

introduction of hardware

token.

Page 33

33

Authentication in an

Internet Banking

Environment by the US

Federal Financial

Institutions Examination

Council.

(http://www.ffiec.gov/)

The USB token is a

relatively secure

vehicle for storing

sensitive data and is

generally considered

to be user-friendly

The introduction of the

USB token still adds to

the cost.

Enhancing ATM security

using fingerprint and

GSM technology by

Ashish M. Jaiswal and

Mahip Bartere, 2014.

Fingerprint biometric is

used along with GSM

technology to enhance

security.

The addition of

biometrics introduces

more complexity in terms

of hardware and

software.

Facial Verification

Technology for Use in

ATM Transactions by

Aru, Okereke Eze,

Ihekweaba Gozie, 2013.

In real time

applications, this

approach gives good

results.

Facial Verification is quite

complex.

Designing a Biometric

Strategy (Fingerprint)

Measure for Enhancing

ATM Security in Indian E-

Banking System by Sri

Shimal Das, Smt. Jhunu

Using fingerprint

biometrics ensures a

high level of ATM

security.

The proposed system is

quite complex: it contains

about five intricate

components.

Page 34

34

Debbarma, IJICT, Vol. 1,

No. 5, September 2011.

Advantages of the proposed two factor authentication: Pin and SMS

Password Model over the Above Compared Models

(1) Cost Effectiveness: the proposed model employs already existing ATM,

Internet and GSM infrastructure without needing additional resources in the

form of hardware and software as is the case with designs that involve

biometrics.

(2) Less Complexity: the proposed model achieves lesser complexity because

of no additional hardware or software resources. Complexity is an obvious

disadvantage of the above compared technologies.

2.2 Review of the Technologies involved in the proposed Design

The proposed system involves various technologies that serve unique purposes

in the operation of the system. These technologies are reviewed from section

2.2.1 to section 2.2.4.

2.2.1 Authentication Mechanisms employed in electronic banking

Authentication is the process of verifying a claim made by a subject that

it should be allowed to act on behalf of a given person, computer,

process, etc. Also, Authentication can be defined as the process of

determining whether someone or something is, in fact, who or what it is

declared to be. Authentication works closely with Identification and

Table 2.1: Comparison Table for the related works

Page 35

35

authorization. Identification can be defined as the process of pinpointing

(identifying) someone or something while Authorization can be defined as the

process of giving someone permission to do or have something.

Authentication can be accomplished with, for instance, a password while

Identification can be accomplished with a username, a smart card, or anything

else that can uniquely identify a subject. Once a user is identified and

authenticated, they can be granted authorization based on their proven

identity [10].

It is imperative to understand the difference between authentication,

identification and authorization. Identification occurs when a person claims an

identity (such as with a username) and authentication occurs when a person

proves their identity (such as with a password). Once the person has a proven

identity, authorization techniques can then grant or deny access to services

based on his proven identity [11].

Authorization, involves verifying that an authenticated subject has

permission to perform certain operations or access specific resources.

Authentication procedures are based on three factors related to the user:

i.e. the person who is authenticating, say a transaction in Internet

Banking [12].

They are;

What the user knows: This includes Username, Password, PIN, etc.

What the user possesses: This includes USB token, Smart Card,

SMS/Token, One Time Password (OTP), etc.

What the user is: This refers to features that are peculiar to the user

such as fingerprint, Palm print, IRIS, Retina, Voice, etc.

Page 36

36

There are three kinds of authentication mechanisms, they are;

Single Factor Authentication; this authentication mechanism utilizes only one

of the factors. For example, a Username (User Knows). This is the basic

authentication method [13].

Two Factor Authentication; this authentication mechanism utilizes any two of

the factors. For example, a User using a password as the first factor (User

knows) and a One-Time Password (OTP) as the second factor (User

possesses) to gain access to their account or perform ,for instance, a funds

transfer transaction[13].

Multi Factor Authentication; this authentication mechanism utilizes more than

two of the factors and one of the factors is necessarily a “User is” type. For

example, a large value transaction authorized in a bank by using a combination

of the person’s username, a smart card and his biometric authentication factor

like fingerprint [13].

Multi factor authentication provides users higher levels of protection from

online banking fraud. By employing biometrics (User is) as one factor; Multi

factor authentication improves security for online banking customers and

reduces online fraud. This authentication can be provided for the customers

(corporate or individual customers) who make transactions beyond the

threshold value that was set up by the bank.

Usually, in online Banking a Two Way or Mutual authentication can be

provided between the user and the Organization. It refers to two parties

authenticating each other. When describing online authentication processes,

mutual authentication is referred to as website-to-user authentication. By

means of this authentication, the user knows that they are on the valid

Page 37

37

banking website. Mutual authentication can be implemented by providing

some challenge questions. The customer provides the challenge questions

along with the answers and selects the image (identifiable pictures), image

title and a text phrase (optional) from a collection of images which are

provided in the banking website at the time of enrolment. The customer

can further change this image during his first login. Further when the customer

enters login id and before entering the password, the site asks these

challenge questions and when the user answers them correctly, it displays

the image, title and phrase. A typical example of a challenge question is

“what is your favourite meal?” A typical answer is “Fufu”. If the displayed

image is correct then customer can enter the password and login in. If not

the customer can stop logging in and contact the bank. This makes the

customer to know whether it is a real banking website or fake

website[8]. This facility provides the customer and server the means to

authenticate mutually so that we can reduce Phishing Attacks: this is an

attack aimed at acquiring sensitive information such as usernames, passwords,

or ATM/credit card details by masquerading as a trustworthy person or entity

in an electronic communication[14].

2.2.2 The ATM System Technology

Basically, the ATM is a computer system which grants Bank clients access to

financial transactions from a public space, thereby discarding the need for a

customer to visit any bank’s branch [2]. Figure 2.1 clearly shows a typical ATM

Machine.

Page 38

38

The ATM must be connected to a network in order to achieve its purpose (see

fig. 2.2). With the aid of the ATM, customers would be able make cash

withdrawals, check the balances on their accounts or even pay their bills.

Display Screen

Card Reader

Receipt Printer

Fig. 2.2: Diagram for the ATM Connected to a Network

ATM

ATM

ATM

ACCOUNT

BANK

COMPUTER/HOST -

PROCESSOR

ACCOUNT

ACCOUNT

ACCOUNT

Fig. 2.1: A Typical ATM Machine (Source: circuitstoday.com).

Key Pad

Speaker

Cash Dispenser

Page 39

39

Operation of the ATM Connected to a Network

When a cardholder wants to do an ATM transaction, they provide the

necessary information by slotting their ATM Card into the ATM’s card reader

and when requested, they provide their personal identification number (PIN)

by entering it via the keypad.

The ATM forwards this information to the Bank Computer (also known as host

processor), which routes the transaction request to the cardholder's bank or

the institution that issued the card. If the cardholder is requesting cash, the

host processor causes an electronic funds transfer to take place from the

customer's bank account to the host processor's account.

Once the funds are transferred to the host processor's bank account, the

processor sends an approval code to the ATM authorizing the machine to

dispense the cash [2].

ATMs include many other functions which are not directly related to the

management of one's own bank account, such as the functions below [2]:

• Deposit currency recognition, acceptance, and recycling.

• Paying utility bills, fees, and taxes (utilities, phone bills,

• Printing bank statements.

• Updating passbooks.

• Loading monetary value into stored value cards.

• Purchasing.

• Postage stamps.

• Lottery tickets.

• Train tickets.

• Concert tickets.

• Movie tickets.

Page 40

40

• Shopping mall gift certificates.

• Games and promotional features.

• Donating to charities.

• Cheque Processing Module.

• Adding pre-paid cell phone credit.

An ATM has the following two input devices [2]:

(1) Card reader- The card reader captures the account information stored on

the magnetic stripe on the back of an ATM card. The host processor uses this

information to route the transaction to the cardholder's bank.

(2) keypad/Function buttons - These let the cardholder tell the bank what kind

of transaction is required (cash withdrawal, balance inquiry, etc.) and for what

amount. Also, the bank requires the cardholder's personal identification

number (PIN) for verification.

An ATM has the following four output devices [2]:

(1) Speaker- The speaker provides the cardholder with audio feedback when a

key is pressed.

(2) Display screen- The display screen prompts the cardholder through each

step of the transaction process.

(3) Receipt printer- The receipt printer provides the cardholder with a paper

receipt of the transaction.

(4) Cash dispenser- The heart of an ATM is the safe and cash-dispensing

mechanism. The entire bottom portion of most small ATMs is a safe, because it

contains the cash.

Page 41

41

2.2.2.1 The ATM Hardware

Figure 2.3 shows the block diagram of the ATM and its component devices.

Typically the ATM hardware comprises the following devices [2].

Central Processing Unit (CPU): This is simply a computer system which is used

to control the user interface and all the other devices. Most deployments make

use of the same CPUs found in desktop computers and laptops; CPUs like Intel

Pentium 4, Intel Core i7 and AMD VISION PRO.

Card Reader: The card reader embodies the mechanism that acquires the

account information stored on the chip on the back of an ATM card in order to

identify the customer. The host processor uses this information to route the

transaction to the cardholder's bank.

Encrypting PIN Pad (EPP): This looks much like a calculator keypad. The EPP

contains the security processor, the software function, the encryption keys and

memory to locally perform the PIN-encryption function.

Fig. 2.3: Block diagram for the ATM (Source: Wikipedia.org).

CPU EPP

CARD

READER

CASH CARTRIDGE

CASH CARTRIDGE

CASH CARTRIDGE

CASH CARTRIDGE

HOUSING

VAULT

CASH HANDLING MECHANISM

DISPLAY SCREEN and FUNCTION BUTTONS

Page 42

42

Secure Crypto-Processor: This is a dedicated microprocessor for carrying

out cryptographic (encrypting) operations. It is embedded in a packaging

within a secure enclosure so that it maintains a degree of tamper resistance.

The security of the machine depends heavily on the integrity of the secure

crypto-processor.

Display: This is basically a computer monitor built into the ATM and used by

the customer for performing the transaction.

Function Key Buttons: These buttons are usually located close to the display

and are programmed to perform specific actions like selecting the type of

transaction involved and the amount.

Record Printer: This prints out a record of the customer’s transaction. The

transaction record is normally printed out on a small paper slip.

Vault: This is a secure enclosure that safeguards money and parts of the

machinery that require restricted access. It is intended to protect these from

theft, unauthorized use, fire, natural disasters, and other threats, just like

a safe. Usually, the Vault contains the following Mechanisms: Dispensing

mechanism that provides the cash, Deposit mechanism which allows the

customer to make deposits, Security sensors, Locks that ensure controlled

access to the contents of the vault, Journaling systems like the record printer

or some form of electronic memory that keeps record of transactions, etc [2].

Housing: The housing provides the ATM with the necessary shelter, aesthetics

and physical security.

2.2.2.2 The ATM Software

Standard commercial "off-the-shelf" operating systems and programming

environments can be used inside of ATMs. Typical platforms previously used

Page 43

43

on ATMs include Real time Multitasking Executive (RMX) or Operating

System/2 (OS/2) [1].

Today, most of the ATMs worldwide (over 95%) use Microsoft Windows XP.

Windows XP is a personal computer operating system produced by Microsoft.

The operating system was released to manufacturing on August 24, 2001, and

generally released for retail sale on October 25, 2001.

Windows XP is well known for its security, stability and efficiency due to its use

of Windows NT Kernel. Unlike its predecessors such as Windows 2000 and

Windows ME, it introduced a significantly redesigned graphical user

interface and was the first version of Windows to use product activation in an

effort to reduce software piracy.

Windows XP offers Internet features such as Internet Explorer 6, Outlook

Express 6, Windows Messenger and MSN Explorer. New networking features

were also added to XP, including Internet Connection Firewall, Internet

Connection Sharing, Quality of Services features, Internet Protocol version 6

(IPv6), network bridging, peer to peer networking, support for most DSL

modems, IEEE 802.11 (Wi-Fi) connections with auto configuration. Remote

Assistance and Remote Desktop were also added; these two allow users to

connect to a computer running Windows XP from across a network or the

internet and access their applications, files, printers and devices [15]. Table 2.2

below shows the Windows XP System Requirements.

Central Processing Unit (CPU) X86 (Intel Pentium) or compatible

CPUs (e.g. AMD Athlon).

Memory 256 MB.

Hard Drive 1.5 GB.

Page 44

44

Media CD-ROM drive or compatible ones.

Display Super Visual Graphics Adaptor (VGA).

Sound Hardware Sound Card, Speakers and head

phones.

Input Devices Keyboard, mouse, etc.

ATM Vendors and financial institutions have a wide range of Application

Programs to drive their machines. These programs run on the aforementioned

Operating System. The Application Programs are developed using any of these:

Extensions for Financial Services (XFS), Java Extensions for Financial Services

(J/XFS) and XPEAK [1].

(1) Extensions for Financial Services (XFS)

The XFS standard was initiated by Microsoft in the early 90's and it was called

WOSA/XFS. The acronym stands for Windows Open Services

Architecture/Extension for Financial Services. As it became an international

standard adopted by the European Committee for Standardization (CEN), it

then became known as CEN/XFS. The CEN/XFS standard defines a common

language to speak with the hardware components of the Automated Teller

Machine (ATM).

The architecture of CEN/XFS is similar to a client-server model, where the

server knows how to drive a particular ATM hardware component. The server

must publish a standard interface which is common for all similar hardware

components. The client application programm benefits from the services

Table 2.2 Windows XP System Requirements (Source: http://en.wikipedia.org/

wiki/Microsoft_windows_xp).

Page 45

45

provided by the server (also called Service Provider or SP) and uses its

standardized interface to drive hardware components from different

manufacturers with the same set of commands.

This is a huge benefit, because it virtually unifies different ATM platforms, and

creates a common environment for the ATM applications all over the world

[16].

CEN/XFS shares a common conceptual background with Microsoft Windows

device drivers. This common conceptual background with Microsoft Windows

device drivers is hinged on forward compatibility. For instance, Windows

drivers are designed to be forward-compatible such that a Windows driver can

run on a version of Windows newer than what the driver was initially written

for, but doing that would mean that the driver cannot take advantage of any

new features introduced with the new version [17]. In the same way CEN/XFS

ensures that client applications can run on a version of the server that is newer

than what the application was initially written for.

Also Windows drivers are generally not backward-compatible: a Windows

driver is not guaranteed to run on any older version of Windows. For example,

a driver written for Windows 2000 can work on Windows XP (which is higher)

but will not make use of any of the new features that were introduced in

Windows XP. However, a driver written for Windows XP may or may not load

on Windows 2000. In the same manner CEN/XFS allows that client applications

may not run on a version of the server that is older than what the application

was initially written for.

(2) XPEAK

Xpeak aims to become the standard for devices management, not only in the

financial arena, but also for all market types. It is a question of creating a

Page 46

46

standard which is independent of the operating system and the programming

language, as well as of the communications interface (Sockets, Web Services,

USB, etc.) which is used to send messages in XML (Extensible Markup

Language) format.

Xpeak is not an acronym and the name itself is indicative of its main objective:

to communicate with devices (speak) using Xml. It aims to homogenise the

messaging between an application and a device; to communicate

independently of the language used by the application. In fact, it is possible

that it could achieve an architecture in which, to give one example, an

application could be developed in Java and use Xpeak Services from different

suppliers, some implemented in Java, others in C++ and still others in the

device's firmware [18].

For further illustration, the example in fig. 2.4 shows the Xpeak architecture.

The figure shows the ATM application program that communicates (speaks)

with a peripheral device such as the Encrypting Pin Pad (EPP) or Record Printer

using XML Commands like XPEAK_COMMAND_READ (which enables the ATM

to read from the EPP) or XPEAK_COMMAND_PRINT (which enables the ATM

to print from the printer). The ATM application program could be written in

any of the popular programming languages like C++, C#, Java, etc. It does not

matter who the manufacturer of the ATM or the peripheral device is. It also

does not matter the language used to write the ATM application program or

the Xpeak services/drivers that come with the peripheral devices. All that

matters is that the ATM application program sends the XML commands to the

peripheral devices of the ATM [18].

Page 47

47

Fig. 2.4: Xpeak architecture

(3) Java Extensions for Financial Services (J/XFS)

Recognising the advantages of the Java language for developing finance

industry applications, representatives of Diebold, IBM, NCR, Talaris, Wincor

Nixdorf International GmbH and Sun Microsystems, embarked on an effort to

develop a set of standard Java interfaces in support of the unique input and

output peripheral devices used in the finance industry at various access

channels including Branch Teller and Platform, Self-Service and Call Centre.

This new standard is called J/XFSTM (Java eXtensions for Financial Services) for

the JavaTM platform. This initiative has produced a finance industry standard

for financial I/O devices that supports 100% pure Java applications while

leveraging existing standards [19].

Utilizing the Java language, J/XFS provides a standard for a banking device

subsystem with real platform and hardware independence which enables the

access to banking peripherals for new Java banking applications. It also

provides a migration path for current financial I/O subsystems and ensures co-

existence between current Client/Server and new Java banking applications, so

customer investments in banking device infrastructure are protected.

ATM application program

ATM’s peripheral devices

XML

Page 48

48

J/XFS enables full transparency between the application and the device level

[19].

Peripheral Devices supported by the CEN/XFS, J/XFS, XPEAK specifications

The following devices are supported by the CEN/XFS, J/XFS, XPEAK

specifications:

Printers and Scanners

Identification Card Units

Cash Dispensers

Personal Identification Number Keypads

Check Readers and Scanners

Depository Units

Text Terminal Units

Sensors and Indicators Units

Cameras

Alarms

Card Embossing Units

Cash-In Modules

Card Dispensers

Barcode Readers

Item Processing Modules

Page 49

49

2.2.3 Short Message Service (SMS)

Figure 2.5 shows the main components of SMS network architecture.

Fig. 2.5: SMS network architecture

When routing a mobile originated short message service, the Short Message

Service Center (SMSC) forwards the short message to the Short Message

Service Gateway Mobile Services Switching Center (SMS-GMSC). The SMS-

GMSC interrogates the Home Location Register (HLR) for routing information

when the Handset is in the HLR’s geographical area of coverage but when it is

not, the Visitor Location Register (VLR) that covers the geographical area in

question is interrogated for routing information. The SMS-GMSC then sends

the short message to the appropriate Mobile Services Switching Center (MSC).

The MSC delivers the short message to the Handset, otherwise known as the

Mobile Station (MS). On the other hand, when routing a mobile terminated

short message, the MS addresses the required SMSC according to its global

title. If roaming abroad the visited public limited mobile network (PLMN) will

route the short message to the appropriate Short Message Service

Interworking Mobile Services Switching Center (SMS-IWMSC) [20].

The SMSC identifies each short message uniquely by adding a time stamp in

the SMS-DELIVER TP-SCTS field (TP-SCTS: Transfer Protocol Service Center Time

SMSC SMS-GMSC/

SMS-IWMSN MSC MS

HLR VLR

Page 50

50

Stamp). The short message arrival at the SMSC is accurate to the second. It is

the SMSC’s responsibility to assure that if two or more short messages arrive

within the same second their time stamps will be different.

The MS has to be able to receive/submit a short message Transfer Protocol

Data Unit (TPDU), and then return a Delivery report upon successful reception.

It is also responsible for notifying the network when it has memory capacity

available to receive one or more messages, if it had previously rejected a short

message because its memory capacity was exceeded [20].

2.2.3.1 Bulk SMS Service

Sending instant discrete messages is undertaken by SMS while the medium

of Bulk SMS enables an organization or institution to reach the masses with

the same notification at the same time.

There are many advantages of this technology but the most eminent one is its

time saving feature that makes it so much preferred. One can send thousands

of SMS to many people in just a few minutes.

A lot of software that allows the use of Bulk SMS directly from the personal

computer is available on the internet. Also there are numerous bulk SMS web

sites that provide the SMS Gateway for bulk SMS and also provide all the

related services necessary for any type and size of organization. The Bulk SMS

solutions include user-friendly software that makes the task of sending

messages in bulk quite easy [21].

The Bulk SMS Service relies heavily on the SMS GATEWAY. The SMS Gateway is

a service which allows a computer to send or receive SMS to or from a

telecommunications network [22]. Bulk SMS web sites (service providers)

provide the SMS Gateway. For someone to utilise the SMS Gateway, they have

Page 51

51

to open an account with the Bulk SMS Service Provider on their website for a

fee. The SMS Gateway used in this work is provided by “eTextmail”. This

service provider is based in Lagos, Nigeria. Their website is

http://www.etextmail.com.

2.2.4 Mechanism employed in this work for sending the One Time Password

The mechanism that sends the One Time Password comprises the proposed

ATM software, an SMS gateway and SMS Network (GSM) as shown in figure

2.6.

Fig. 2.6: Mechanism for sending the One Time Password

During authentication, the ATM software sends the OTP and the destination

phone number, through the internet, to the SMS Gateway. The SMS Gateway

then sends the OTP and the destination phone number, through the internet,

to the SMS Network. Afterwards, the SMS Network sends the OTP to the

destination phone number, through the Global System for Mobile

Communication (GSM).

The destination phone number is the customer’s phone number, which in this

case is the number of the author of this thesis.

SMS

GATEWAY

SMS NETWORK

(GSM) MOBILE

PHONE

ATM

SOFTWARE

(OTP)

Page 52

52

CHAPTER THREE

RESEARCH METHODOLOGY

3.1 Methods Adopted for this Work

The methodology for this work is Object Oriented Analysis and Design (OOAD)

along with Modelling and Simulation using Unified Modelling Language (UML)

and C# respectively. This chapter elaborately discusses the elements of OOAD

and UML. Here the key elements of OOAD are exposed and illustrated using

the ATM.

3.1.1 Object Oriented Analysis and Design (OOAD)

Object-oriented analysis is a Software Engineering method which focuses on

the analysis that examines requirements with respect to the classes and

objects found in the description of the problem domain. Object-oriented

design refers to the method of Software design which includes the process of

object-oriented decomposition and a notation for portraying the logical and

physical, as well as static and dynamic models of the system being designed. In

object oriented decomposition we identify objects from the vocabulary of

the problem domain and view them as a collection of independent

agents that collaborate to exhibit a certain higher level behaviour [23].

Normally in the design of software systems, using the object oriented

approach, the two methods above are combined; hence we have Object

Oriented Analysis and Design (OOAD). Basically, it is the products of

object oriented analysis that serve as the models from which an object-

oriented design is started; the products of object-oriented design can then be

made use of as blueprints for the complete realisation of a system using

object-oriented programming methods.

Page 53

53

OOAD places data and the operations that are related to them within a single

entity called an object; this approach has eliminated many of the

problems that are associated with the procedural approach to software

development. In OOAD everything is an object and every object has

attributes and actions associated with it. Therefore each object in OOAD

models a certain object in the real world. This approach organizes programs

in a way that so-closely resembles the real world, in which all objects

are associated with both attributes and behaviour. With the use of OOAD

software reusability is very much improved and the development,

improvement and maintenance of software become remarkably easier than it

used to be under the procedural approach [23].

In Object-Oriented Analysis and Design, the following Terms are frequently

employed: Object, Class, Encapsulation, Inheritance, and Polymorphism.

I. Object: In real life, an Object is a visible and tangible thing or entity [24].

For instance, a chair is an object. Likewise a living creature like a dog is

an object. Objects have two characteristics: they

have state and behaviour. For instance, a car has states such as “current

gear, current speed” and it has behaviour such as “changing gear,

applying brakes”.

The ATM has states such as “ATM not servicing a customer, asking for

entry of PIN, displaying menu of transaction types, asking whether

customer wants to perform another transaction” and it has behaviour

such as “ATM system ejects card, system ejects cash, system displays an

error screen”. Identifying the state and behaviour for real-world objects

is a good way to start in carrying out Object Oriented Analysis and

Design.

Page 54

54

II. Class: A class is a family of related objects. In other words an object is

the instance of a class. A class is the template used to create uniform

individual objects [24]. For example, there are different types of cars:

Saloon, Wagon, etc. Though these cars have different qualities and

features, they still belong to that one family of machines called cars. This

family is the class. Thus we can have a Car Class. A class is the blueprint

from which individual objects are created whereas the individual objects

are simply the instances of the class.

In the ATM, there could be many classes such as Account Information,

Banking Class, Transaction Class, ATM Class, etc. Each of these classes is

a family of related instances of the class (objects) along with

properties/attributes and behaviour/methods. For instance, the Account

Information Class could have such objects as, account type, time of last

transaction, minimum balance, date of account opening, along with

methods such as checkbalance(), checkdate() and properties such as

currency, transaction history, etc (see figure 3.1).

Fig. 3.1:

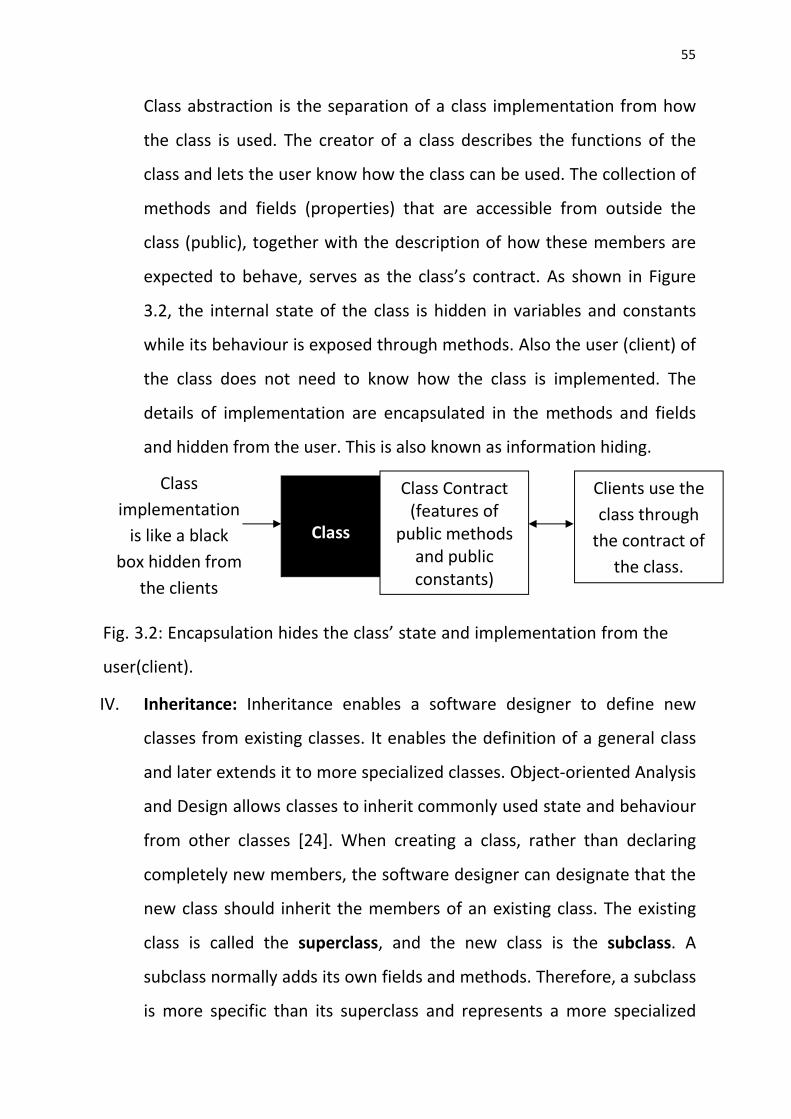

III. Encapsulation: This is an Object Oriented Concept that allows Objects of

a class to hide their internal states in fields or variables but expose their

behaviour through methods or functions [24]. It is also known as class

encapsulation. Class encapsulation is interwoven with class abstraction.

Class Name

Properties (Attributes)

Methods (Behaviour)

Account Information

Currency Transaction History

checkdate() checkbalance()

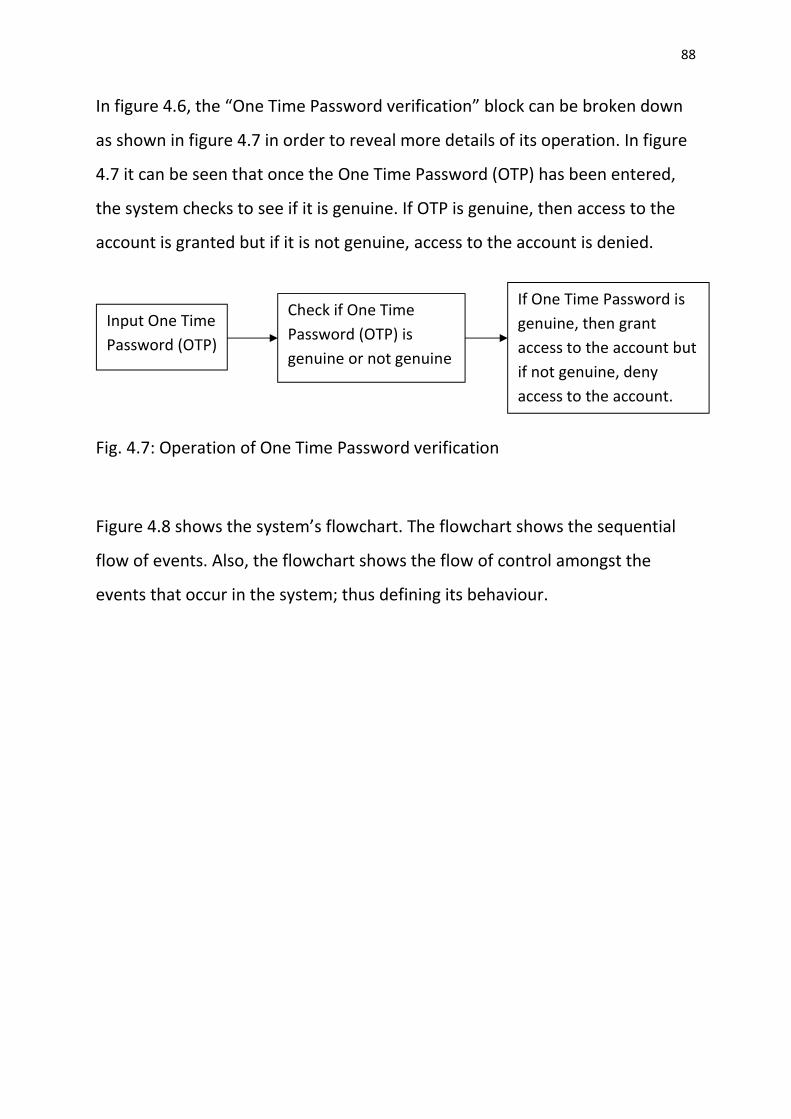

Fig. 3.1: Typical diagram of a class

Page 55

55

Class abstraction is the separation of a class implementation from how

the class is used. The creator of a class describes the functions of the

class and lets the user know how the class can be used. The collection of

methods and fields (properties) that are accessible from outside the

class (public), together with the description of how these members are

expected to behave, serves as the class’s contract. As shown in Figure

3.2, the internal state of the class is hidden in variables and constants

while its behaviour is exposed through methods. Also the user (client) of

the class does not need to know how the class is implemented. The

details of implementation are encapsulated in the methods and fields

and hidden from the user. This is also known as information hiding.

IV. Inheritance: Inheritance enables a software designer to define new

classes from existing classes. It enables the definition of a general class

and later extends it to more specialized classes. Object-oriented Analysis

and Design allows classes to inherit commonly used state and behaviour

from other classes [24]. When creating a class, rather than declaring

completely new members, the software designer can designate that the

new class should inherit the members of an existing class. The existing

class is called the superclass, and the new class is the subclass. A

subclass normally adds its own fields and methods. Therefore, a subclass

is more specific than its superclass and represents a more specialized

Fig. 3.2: Encapsulation hides the class’ state and implementation from the

user(client).

Class

implementation

is like a black

box hidden from

the clients

Class

Class Contract (features of

public methods and public constants)

Clients use the

class through

the contract of

the class.

Page 56

56

group of objects. Typically, the subclass exhibits the behaviours of its

superclass and additional behaviours that are specific to the subclass.

The ATM software could have such classes as “Withdrawal Class, Deposit

Class and transfer class”. These classes have some qualities in common

with each other. One common quality amongst them is that each one of

them is a type of transaction. In this case they would be subclasses that

inherit the features of a superclass that contains the qualities that they

have in common (see figure 3.3). Such a superclass could be named

“Transaction Class”. An arrow headed line points to the superclass.

V. Polymorphism: Polymorphism enables the development of software

that process objects that share the same superclass in a class hierarchy

as if they are all objects of the superclass. It is the provision of a single

interface (method) to entities (objects) of different types [24]. With

polymorphism, the same method name and signature can be used to

cause different actions to occur, depending on the type of object on

which the method is invoked. Polymorphism means “many forms”.

Fig 3.3: Withdrawal class, Deposit class and Transfer class inherit from

Transaction class as shown with a small triangle pointing to the superclass.

Deposit Class

Shared Properties

Shared Methods

Withdrawal Class

Shared Properties

Shared Methods

Transfer Class

Shared Properties

Shared Methods

Transaction Class

Shared Properties

Shared Methods

Page 57

57

Consider the following example of polymorphism. In the illustration in

figure 3.3, “withdrawal class, deposit class and transfer class” are

subclasses of the superclass “transaction class”. Transaction class

contains a method “execute” which carries out a transaction. Each

subclass implements the “execute” method. When the program sends

the same message (execute) to objects of these classes, each class will

respond to the “execute” message in a unique way: withdrawal will

release money to a customer, deposit will accept money from a

customer while transfer will send money to a different account

somewhere else. Relying on each object to know how to "do the right

thing" (i.e., do what is appropriate for that type of object) in response to

the same method call is the key concept of polymorphism. The same

message (in this case, execute) sent to a variety of objects has "many

forms" of results, hence the term polymorphism.

In this chosen methodology, Software Engineering principles are employed in

analysing and designing the system in question. Basically, this involves the use

of Object Oriented Analysis and Design (OOAD) along with a suitable Software

Development Life Cycle (SDLC). The Waterfall Model is the Software

Development Life Cycle of choice in this work.

In applying the Waterfall Life Cycle to this design, Object Oriented Analysis and

Design (OOAD) is employed at the appropriate stages of the Life Cycle.

3.1.1.1 The Waterfall Model Software Development Life Cycle

Software in its nature is intangible, time consuming and requires a lot of

resources. Because of this nature of software, a haphazard approach towards

the development of software has to be avoided and a disciplined process

adopted. This process otherwise known as Software Development Life Cycle

Page 58

58

(SDLC) is a collection of defined activities, actions and tasks that are performed

when software is to be created.

The Waterfall Model is the “SDLC” of choice in this project. Waterfall approach

was the first Process Model to be introduced and followed widely in Software

Engineering. In this project the Waterfall Model is preferred for the following

reasons;

Easy to understand: The stages and activities of the waterfall model are

well defined and therefore easy to comprehend·

It is widely used and known such that resources on it are readily and

easily available.

Being a linear model and progressing sequentially from one stage to the

next, it is very simple to implement.

It’s a good model to start with for someone with limited software design

experience.

Phases are processed and completed one at a time and not overlapped

with one another.

The amount of resources required to implement this model is minimal.

It ensures that all requirements and features are defined before design

and coding.

Generally, this model leads to a project being delivered on time because

each phase has already been planned in detail.

In "The Waterfall" approach, the whole process of software development is

divided into separate process phases.

The phases in Waterfall model are: Requirements Definition phase, Software

Design, Implementation, Integration and Testing, Operation and Maintenance.

All these phases are cascaded to each other so that second phase is started as

Page 59

59

and when defined set of goals are achieved for first phase and it is signed off,

so the name "Waterfall Model" [24]. All the methods and processes

undertaken in Waterfall Model are more visible. Figure 3.1 clearly shows the

Waterfall model and its stages. In this figure each later stage has a bold arrow

headed dashed line that points upwards to the immediate earlier stage and

that is called interstage feedback. The interstage feedback implies that a stage

preceding an ongoing stage could be revisited for any necessary revision. The

interstage feedback is a modification on the original waterfall model which has

no feedback.

Operation and

Maintenance

Integration and

System Testing

Implementation

and Unit Testing

System and

Software Design

Requirements

Analysis and

Definition

Fig. 3.4: The Waterfall Model (with interstage feedback)

Page 60

60

The stages of "The Waterfall Model" are:

Requirements Analysis & Definition: All possible requirements of the system

to be developed are captured in this phase. Requirements are set of

functionalities and constraints that the end-user (who will be using the system)

expects from the system. The requirements are gathered from the end-user by

consultation, these requirements are analysed for their validity and the

possibility of incorporating the requirements in the system to be developed is

also studied. Finally, a Requirement Specification document is created which

serves the purpose of guideline for the next phase of the model.

System & Software Design: At this stage Object Oriented Analysis and Design

(OOAD) is done. Before starting the actual coding, it is highly important to

understand what we are going to create and what it should look like. The

requirement specifications from first phase are studied in this phase and

system design is prepared. System Design helps in specifying Hardware and

Software systems requirements and also helps in defining overall system

architecture. The system design specifications serve as input for the next phase

of the model.

Implementation & Unit Testing: On receiving system design documents, the

work is divided in modules/units and the actual coding is started. At this stage

Object Oriented Programming (OOP) is done. The system is first developed in

small programs called units, which are integrated in the next phase. Each unit

is developed and tested for its functionality; this is referred to as Unit Testing.

Unit testing mainly verifies if the modules/units meet their specifications.

Integration & System Testing: As specified above, the system is first divided in

units which are developed and tested for their functionalities. These units are

Page 61

61

integrated into a complete system during Integration phase and tested to

check if all modules/units work well with each other and if the system as a

whole behaves as per the specifications. After successfully testing the

software, it is delivered to the customer.

Operations & Maintenance: This phase of "The Waterfall Model" is virtually a

never ending phase (Very long). Generally, problems with the system

developed (which are not found during the development life cycle) come up

during operations, so the issues related to the system are solved after

deployment of the system. Not all the problems appear initially but they arise