17

DEPARTMENT OF TRADE AND INDUSTRY DEPARTMENT OF TRADE AND INDUSTRY INCREASING ACCESS TO FINANCE

| Date post: | 31-Dec-2015 |

| Category: |

Documents |

| Upload: | fiorello-lappin |

| View: | 45 times |

| Download: | 0 times |

DEPARTMENT OF TRADE AND DEPARTMENT OF TRADE AND INDUSTRYINDUSTRY

INCREASING ACCESS TO FINANCE

Table of contents

• Strategic approach

• SME support since 1994

• SMME contribution to GDP

• SME finance initiatives

• Finance products for SMEs

• Finance needs of SMEs

• SME growth strategy

• Conclusion

2

3

Strategic approach

• Create an enabling legal framework;

• Streamlining of regulatory conditions;

• Facilitating access to information and advice;

• Facilitating access to marketing and procurement;

• Facilitating access to finance;

• Providing training in entrepreneurship & management

skills; and

• Facilitating access to appropriate technology.

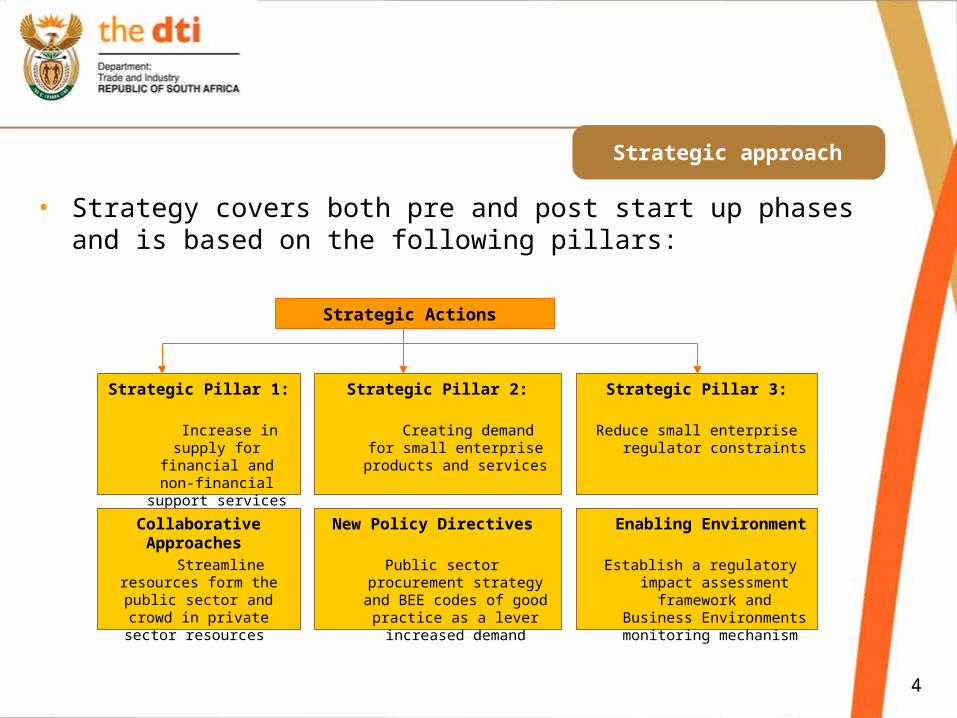

Strategic approach

Strategic Actions

4

Strategic Pillar 1:

Increase in supply for financial and

non-financial support services

Strategic Pillar 2:

Creating demand for small enterprise products

and services

Strategic Pillar 3:

Reduce small enterprise regulator constraints

• Strategy covers both pre and post start up phases and is based on the following pillars:

Collaborative Approaches

Streamline resources form the public sector and crowd in private

sector resources

New Policy Directives

Public sector procurement strategy and BEE codes

of good practice as a lever increased demand

Enabling Environment

Establish a regulatory impact assessment framework

and Business Environments monitoring

mechanism

SME support since 1994

• Easing the regulatory compliance burden on SMEs;

• Access to finance;

• Business development services;

• Youth enterprise development;

• Support for women owned enterprises;

• Incubation and technology acquisition and transfer of services;

• Productivity enhancement measures and support;

• Sector-focused support measures; and

• Skills development measures.

5

SMME contribution to GDP

6

• 65% of all jobs created in the economy can be attributed to the SMME sector

• Small business contributes between 35% to 50% to the South African GDP

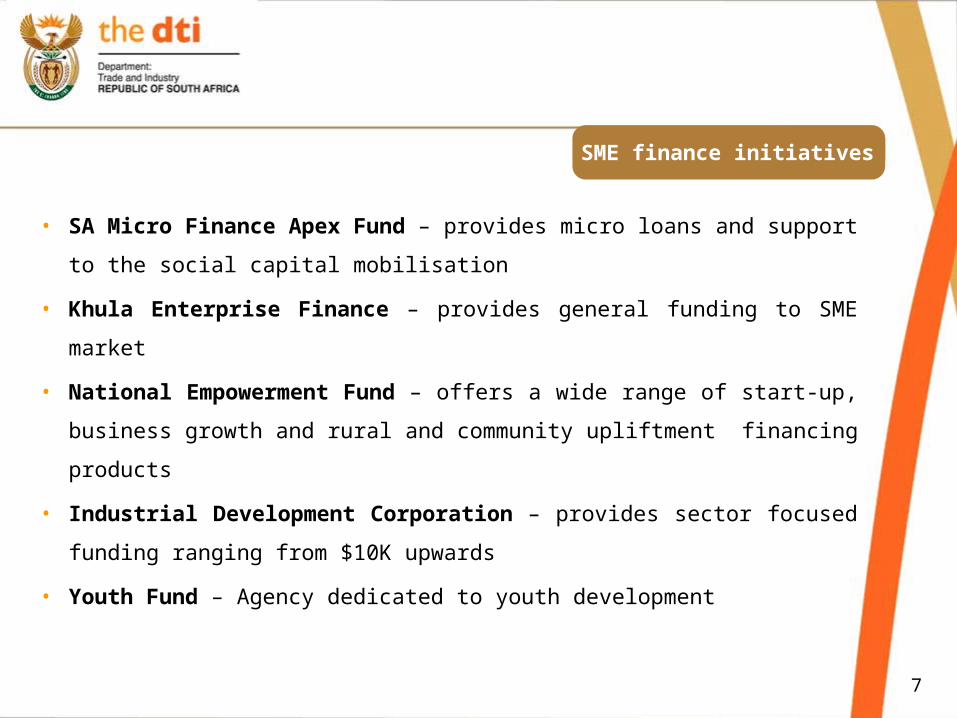

SME finance initiatives

• SA Micro Finance Apex Fund – provides micro loans and support

to the social capital mobilisation

• Khula Enterprise Finance – provides general funding to SME

market

• National Empowerment Fund – offers a wide range of start-up,

business growth and rural and community upliftment financing

products

• Industrial Development Corporation – provides sector focused

funding ranging from $10K upwards

• Youth Fund – Agency dedicated to youth development

7

Finance products for SMEs

• Credit indemnity product – partnerships between Khula and country’s major banks wherein Khula provided indemnity cover to Banks on behalf of qualifying SMEs

• Portfolio indemnity product – partnership between Khula, Dept of Agriculture and major banks wherein banks are covered for providing production inputs and equipment finance to qualifying SME in the agriculture sector

• Business Loans – Khula provides wholesale funding to RFIs for on-lending to qualifying SMEs. Loans range from $1K to $300K.

• Micro loans – Samaf provides micro loans from $100 to $1K

8

Finance products for SMEs

9

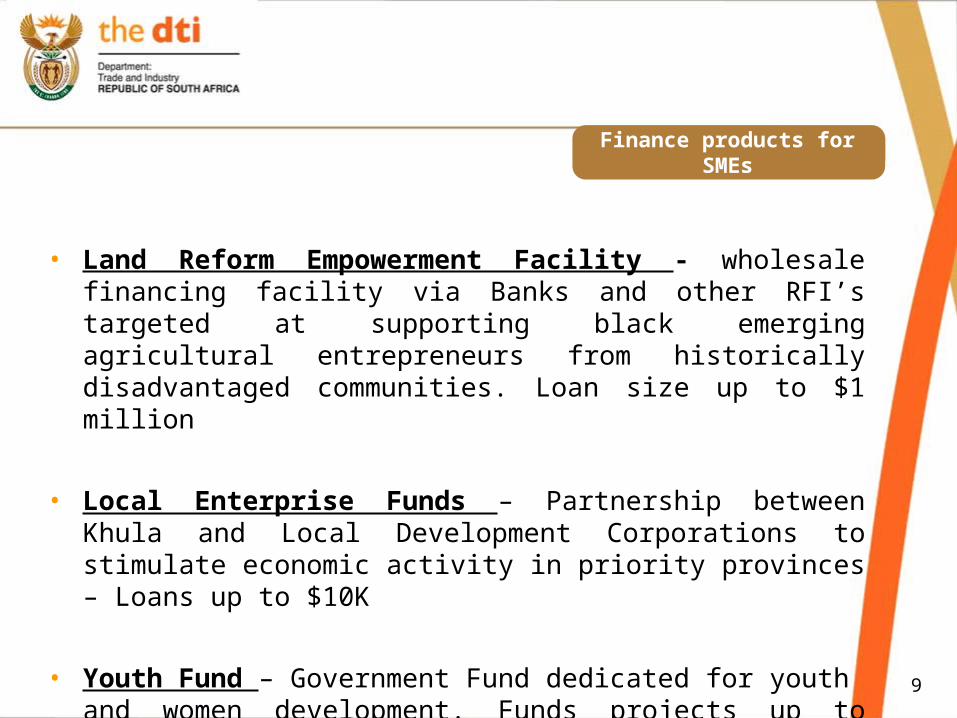

• Land Reform Empowerment Facility - wholesale financing facility via Banks and other RFI’s targeted at supporting black emerging agricultural entrepreneurs from historically disadvantaged communities. Loan size up to $1 million

• Local Enterprise Funds – Partnership between Khula and Local Development Corporations to stimulate economic activity in priority provinces – Loans up to $10K

• Youth Fund – Government Fund dedicated for youth and women development. Funds projects up to $3000K

Finance products for SMEs

• Public Private Partnerships Funds

- Mining Fund ($20m) with Anglo American to fund junior

mining

projects (up to $200K per project)

- Start-Up Fund with Business Partners ($15m). This fund focuses

mainly on start ups and early expansion (up to $30K per project)

- Agriculture Fund ($10m) with second major sugar mill in the

country. (up to $50K per project). Off take agreements in place.

10

Finance products for SMEs

- Enablis Network Funds ($5m) – partnership between Khula and

Enablis Foundation. Two Funds, one focused whilst the other is a

general fund. Entrepreneur to belong to the network and achieve

certain rating before funds can be disbursed.

- Women’s Fund ($20m) – partnership between Old Mutual Asset

Managers and youth fund to finance women owned businesses (up to

$5000K per project).

11

Finance products for SMEs

• Reverse Factoring Product

Partnership between Khula and Regent Factors ($10m) in terms of which Regent provides reverse factoring product to qualifying SMEs.

• Leasing ProductMOU entered into between Khula and private sector entity ($10m) in terms of which computer and office equipment will be leased to qualifying SMEs.

12

Financial needs of SMEs

• Access to finance;

• the ability to make transactions - suitable transactional

banking products;

• Making of investments;

• Insurance and assurance products;

• Brokerage services; and

• Financial advisory services.

These can be made possible by technology

13

Growth strategy

Grow small businesses by addressing access to finance constraints:

– Pursuing innovative ways to increase lending to small businesses;

– Deploying best practice innovation;

– Partnering with local and provincial government, as well as private enterprise; and

– Incubator funding schemes, particularly targeting business development in priority growth sectors.

14

Growth strategy

15

Create business development opportunities:

– Working with government and the private sector, establish a

‘one-stop shop’ solution for small businesses that supports:

• the linking of institutional demand to small business

supply;

• assistance for SMEs with tenders and business acquisition

processes & regulatory services;

• skills development (mentoring);

Growth strategy

• affordable finance provision;

• Invest in rural infrastructure such as information

communication technology, energy and and

transport which would attract funders to locate and

provide financial services to these remote areas;

and

• efficient and convenient basic banking services,

especially in non-urban areas or mobile contexts.

16

Conclusion

17

• Prospects for SME development and growth are good;

• Renewed focus on SMEs by both public and private

sector;

• Scale up of interventions by the DFIs and commercial

banks;

• Better cooperation amongst DFIs; and

• Increased awareness of official programmes by SMEs,

banks, DFIs, and other stakeholders.