Derivative Trading and Structural Changes in Volatility K. N. Badhani 1 Harish Bisht 2 Ajay Kumar Chauhan 3 Abstract: It is believed that the derivatives contribute in efficient price discovery of underlying assets and reduce the volatility in their prices. This hypothesis has been tested by many researchers for Indian stock market and most of them conclude that the volatility of stock prices has come down after the introduction of derivative trading in the market. However, use of a dummy variable as additional regressor with GARCH specification of conditional volatility is not capable to isolate the effect of derivative trading from the impact of other market reforms on the volatility of stock prices. In this paper we identify the dates of structural breaks in volatility of twenty-one stocks using CUSUM estimator and compare these dates with the dates of introduction of derivative trading in respective stocks. We do not find any conclusive evidence suggesting that the introduction of derivative trading has caused a reduction in the volatility of the prices of underlying stocks. Key Words: Structural Changes, Volatility, CUSUM, Derivative Trading JEL Classification: C22, G12 1. Reader, DSB Campus, Kumaun University, Nainital-263002, Uttarakhand, E-Mail- [email protected]. Mobile- 919412908097. 2. Research Scholar, DSB Campus, Kumaun University, Nainital 3. Faculty, Finance Area, Apeejay Institute of Management, Dwarka, Delhi.

Transcript

Derivative Trading and Structural Changes in

VolatilityK. N. Badhani1

Harish Bisht2

Ajay Kumar Chauhan3

Abstract:It is believed that the derivatives contribute in efficient price discovery of

underlying assets and reduce the volatility in their prices. This hypothesis has been tested

by many researchers for Indian stock market and most of them conclude that the volatility

of stock prices has come down after the introduction of derivative trading in the market.

However, use of a dummy variable as additional regressor with GARCH specification of

conditional volatility is not capable to isolate the effect of derivative trading from the

impact of other market reforms on the volatility of stock prices. In this paper we identify

the dates of structural breaks in volatility of twenty-one stocks using CUSUM estimator

and compare these dates with the dates of introduction of derivative trading in respective

stocks. We do not find any conclusive evidence suggesting that the introduction of

derivative trading has caused a reduction in the volatility of the prices of underlying

RIL Yes Decreased Increased DecreasedSAIL NoSBIN Yes Decreased Increased IncreasedTata Power Yes Increased Increased DecreasedTata Moters NoTotal Yes= 13

No= 8Increased= 7Decreased=6

Increased= 8Decreased=5

Increased= 4Decreased= 9

17

4. Results and Discussion:The stock-options on ACC stock were introduced on July 02, 2001 but the trading

of stock-futures started on November 9, 2001, which has been used as the effective date

of introduction of derivative trading on this stock. A volatility break on this stock is

observed on March 5, 2002, which is within six months’ period from the date of

introduction of stock futures on ACC. Data presented in Panel: 1 of the Annexure show

that during the period following this break the volatility persistence has increased, while

the unconditional volatility and the rate of adjustment to news ( ) have decreased.

In Case of Ambuja Cement, no volatility break is detected around the date of

introduction of derivative trading.

A structural break is found in volatility of Bajaj Auto on August 13, 2001, which

is within the stipulated time period in proximity of the introduction of derivative trading

on this stock. The results presented in Panel: 3 of the Annexure show that the rate of

adjustment in volatility has increased while the volatility persistence and the measure of

unconditional volatility have decreased during the period following this break. However,

these changes in the volatility dynamics are not of permanent nature as another break in

volatility takes place after a period of about four years and the situation inverts. The

similar phenomenon is observed in other stocks also.

The trading of stock-futures started in BHEL stock on November 9, 2001 and we

detect a structural break in volatility of returns on this stock on March 07, 2002. The

result shows that the unconditional volatility has decreased but its persistence as well as

the rate of adjustment towards new information has increased after this structural break.

In BPCL a structural break in volatility is observed on the April 19, 2001. During

the period subsequent to this break the volatility persistence and unconditional volatility

come down but the rate of adjustment increases (Panel: 5). Similar results are obtained

for Cipla (Panel: 6). However, no structural break is fond in proximity of the introduction

of derivatives trading on Dr. Reddy’s Lab (Pane: 7), Glexo (Panel: 8) and HPCL (Panel:

10).

Panel: 9 presents the results of the analysis of volatility breaks in Grasim. The

trading of futures started on this stock on November 9, 2001 and a structural break is

detected in volatility of the stock price on December 31, 2001. The results show that the

18

rate of adjustment towards new information has decreased and unconditional volatility

and the total persistence have increased after the introduction of derivative trading. These

results are just opposite of the observations that we had made in case of BPCL and Bajaj

Auto.

In case of HUL (previously, HLL), we observe that a structural break in volatility

takes place on October, 2001 (Panel: 11). During the period subsequent to this break the

persistence of the volatility increases; while, the adjustment coefficient and unconditional

volatility decrease. On the other hand we observe just opposite impact of derivative

trading on the volatility of L&T stock (Panel: 12), where the persistence of the volatility

decreases; while, the adjustment coefficient and unconditional volatility increases during

the period subsequent to the introduction of derivative trading.

The results of analysis of the volatility breaks in ITC stock are also similar to the

results of BPCL and Bajaj Auto. We observe an increased value of adjustment

coefficient, , and reduction in the volatility persistence and the unconditional volatility

of this stock for the period subsequent to introduction of derivative trading (Panel: 12).

On the other hand, the stocks of L&T and Reliance Energy show just opposite results

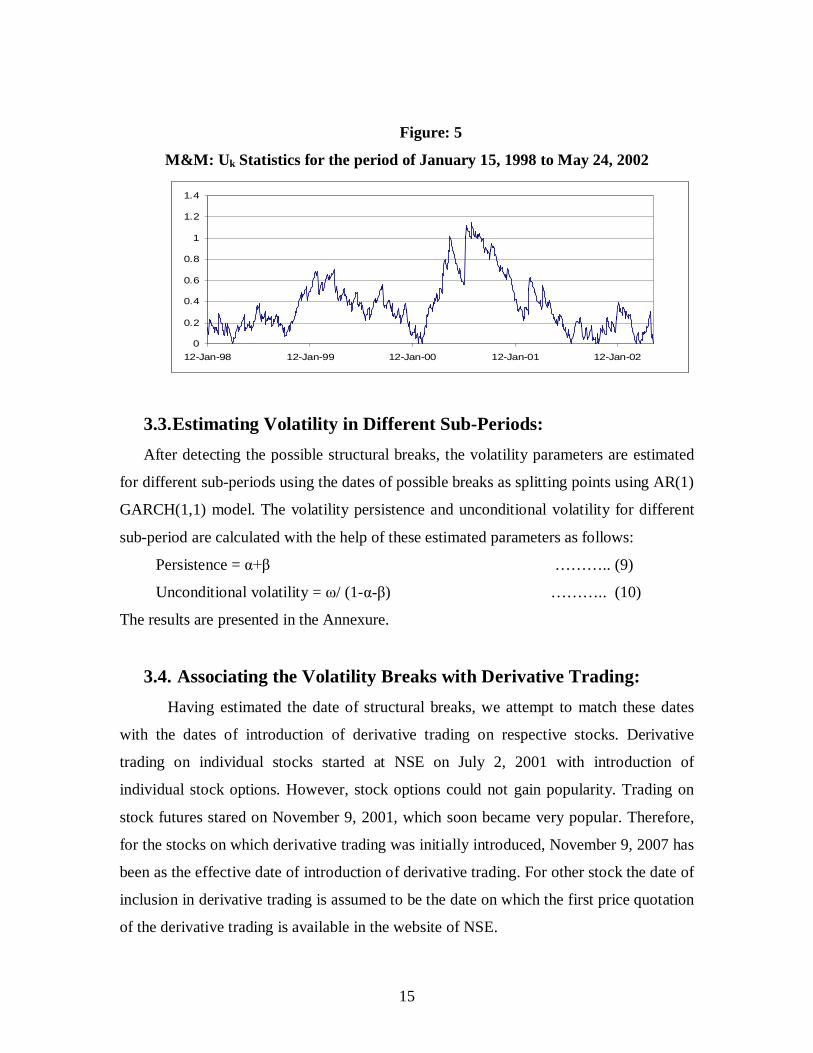

(Panel: 13 and 16). The stocks of M&M (Panel: 14) and SAIL (Panel: 18) do not show

any structural break in proximity of the date of introduction of derivative trading. The

stocks of MTNL (Panel: 15) and Tata Motors (Table: 20) do not show any structural

break in volatility at all during the period covered in this study. Stock of RIL, alike to

ITC, shows a decreased level of volatility persistence and unconditional volatility but an

increased level of adjustment coefficient after the introduction of derivative trading

(Panel: 17). In case of State Bank of India (SBI) the adjustment coefficient of the

volatility and unconditional volatility increase and persistence of volatility decreases after

the introduction of the derivative trading (Panel: 19); while in case of Tata Power (Panel:

21) the unconditional volatility decreases and the volatility persistence as well as the

speed of adjustment of volatility to new information increases.

The results obtained in this study show a mixed picture. Out of the 21 stocks, in

eight stocks no structural break was found within the stipulated time period. Out of

remaining thirteen stocks, which show structural break during the period in proximity of

introduction of derivative trading, the unconditional volatility has decreased in nine

19

stocks while in four stocks it has increased. The volatility persistence has increased in

seven stocks and decreased in six stocks. The rate of adjustment of volatility to new

information has increased in eight stocks, while it has decreased in five stocks. Therefore,

no generalisation can be made about the impact of derivative trading on volatility.

5. Conclusion:In this paper we have made an attempt to identify the structural breaks in the

volatility dynamics of twenty-one stocks using the cumulative-sum-of-squares (CUSUM)

procedure. These dates are compared with the date of introduction of derivative trading in

respective stocks to examine if any structural break is induced by the derivative trading.

If a break is observed in proximity of introduction of derivative trading, the nature of

changes in volatility persistence, rate of adjustment in volatility to news and

unconditional volatility have been analysed. We do not observe any consistent pattern in

the reaction of volatility dynamics towards introduction of derivative trading. Therefore,

it can be concluded on the basis of the results of this study that the introduction of

derivative trading has no definite implication for the volatility of underlying stocks.

Reference:Afsal E. M. and Mallikarjunappa, T. (2007), “Impact of Stock Futures on the Stock

Market Volatility”, The ICFAI Journal of Applied Finance, Vol. 13 No.9, pp.54-75.

Aggarwal, R.; Inclan, C., and Leal, R. (1999), “Volatility in Emerging Stock Markets”,Journal of Financial and Quantitative Analysis, Vol.34, No.1, pp. 33-55.

Aitken, M; Frino, A. and Jarnecic, E. (1994), “Option Listings and the Behaviour ofUnderlying Securities: Australian Evidence”, Securities Industry Research Centreof Asia-Pacific (SIRCA) Working Paper, Vol. 3, pp. 72-76.

Alexakis, P. (2007), “On the Effect of Index Futures Trading on Stock MarketVolatility”, International Research Journal of Finance and Economics, Vol. 11, 7-20.

Andreou, E. and Ghysels, E. (2002), “Detecting Multiple Breaks in Financial MarketVolatility Dynamics”, Journal of Applied Econometrics, Vol.17, No.5, pp. 579-600.

Antoniou, A. and Holmes, P. (1995), “Futures Trading, Information and Spot PriceVolatility: Evidence for the FTSE-100 Stock Index Futures Contract usingGARCH”, Journal of Banking and Finance, Vol. 19(2), pp. 117-129.

20

Bacmann, J. and M. Dubois (2002), "Volatility in Emerging Stock Markets Revisited."http://www.ssrn.com/abstract=313932.

Baillie, R. T.; Bollerslev, T. and Mikkelsen, H. O. (1996), “Fractionally IntegratedGeneralised Autoregressive Conditional Heteroskedasticity”, Journal ofEconometrics, Vol.74, No.1, pp 3-30.

Bandivadekar, S. and Ghosh, S. (2003), “Derivatives and Volatility in Indian StockMarkets”, Reserve Bank of India Occasional Papers, Vol. 24(3), pp. 187-201.

Basal, V. K.; Pruitt, S. W. and Wei, K. C. J. (1989), “An Empirical Re-examination ofthe Impact of COBE Option Initiation on the Volatility and Trading Volume ofUnderlying Equities: 1973-1986”, Financial Review, Vol. 24, pp. 19-29.

Bauer, L. (2006), “Regime Dependent Conditional Volatility in the US Equity Market”,http://papers.ssrn.com/sol3/papers.cfm?abstract_id=927044.

Bessembinder H. and Seguin, P. J. (1992), Futures Trading Activity and Stock PriceVolatility, Journal of Finance, Vol. 47, pp. 2015-2034.

Bollen, N. P.B. (1998), “A Note of the Impact of Options on Stock Return Volatility”,Journal of Banking and Finance, Vol. 22, pp. 1181-1191.

Bollerslev, T.; and Engle, R. F. (1986), “Modelling the Persistence of ConditionalVariance”, Econometric Review, Vol.5, No.1, pp 1-50.

Bollerslev, T.; Chou, R. Y. and Kroner, K. F. (1992), “ARCH Modelling in Finance: AReview of Theory and Empirical Evidence”, Journal of Econometrics, Vol.52, No.(1, 2), pp 5-59.

Brown, R. L., Durbin, J., and Evans, J. M. (1975), “Techniques for Testing the Constancy ofRegression Relationships over Time”, Journal of the Royal Statistical Society, Ser. B,Vol.37, pp 149-163.

Chou, R.Y. (1988), “Volatility Persistence and Stock Valuations: Some EmpiricalEvidence using GARCH”, Journal of Applied Econometrics, Vol.3, No.4, pp 279-294.

Conrad, J. (1989), “The Price Effect of Option Introduction”, Journal of Finance, Vo. 44,pp. 487-498.

Cox, C. C. (1976), “Futures Trading and Market Information”, Journal of PoliticalEconomy, Vol. 84, pp. 1215-37.

Danthine, J. (1978), “Information, Futures Prices and Stabilizing Speculation”, Journal ofEconomic Theory, Vol. 17, pp. 79-98.

21

Darrat, A.F., and Rahman, S. (1995), “Has Futures Trading Activity Caused Stock PriceVolatility?” Journal of Futures Markets, Vol. 15, pp. 537 – 557.

den Haan, W. J. and Levin, A. (1997), “A Practitioner’s Guide to Robust CovarianceMatrices Estimation”, in Handbook of Statistics, Vol. 15, Rao, C. R. and Maddala,G. S. (eds.), 291-341.

Diebold, F. X. (1986), “Modelling the Persistence of Conditional Variances: AComment”, Economic Review, Vol.5, No.1, pp 51-56.

Diedold, F. X. and Inoue, A. (2001), “Long Memory and Structural Change”, Journal ofEconometrics, Vol. 105, pp. 131-159.

Dueker, M. J. (1997), “Market Switching in GARCH Process and Mean Reverting StockMarket Volatility”, Journal of Business and Economic Statistics, Vol.15, No.1,pp26-34.

Edwards, Franklin R., (1988), “Does Futures Trading Increase Stock Market Volatility?”Financial Analyst Journal, Vol. 44, pp. 63-69.

Engle, R. (1982), “Autoregressive Conditional Heteroskedasticity with Estimates of theVariance of UK Inflation”, Econometrica, Vol.50, No.4, pp 987-1008.

Engle R. and Lee, G. J. (1999) “A Permanent and Transitory Component Model of StockReturn Volatility”, in R. Engle and H. White (eds.), Cointegration, Causality, andForecasting: A Festschrift in Honour of Clive W.J. Granger, Oxford UniversityPress, pp 475-497.

French, K. R; Schwert, G. W. and Stambaugh, R. F. (1987), “Expected Stock Returns andVolatility”, Journal of Financial Economics, Vol.19, pp 3-30.

Freund, S. P.; McCann, D. and Webb, G. P. (1994), “A Regression Analysis of the Effectof Option Introduction on Stock Variance”, Journal of Derivatives, Vol. 6, pp. 25-38.

Granger, C.W.J. and Hyung, N. (1999), “Occasional Structural Breaks and LongMemory”, Discussion Paper 99-14, Department of Economics, University ofCalifornia, San Diego.

Gray, S. F. (1996), “Modelling the Conditional Distribution of Interest Rates as RegimeSwitching Process”, Journal of Financial Economics, Vol.42, No.1, pp 27-62.

Gupta O.P., (2002), “Effects of Introduction of Index Futures on Stock Market Volatility:The Indian Evidence“, paper presented at Sixth Capital Market Conference, UTICapital Market, Mumbai.

22

Gulen, H. and Mayhew, S. (2000), “Stock Index Futures Trading and Volatility inInternational Equity Market”, Journal of Futures Markets, Vol. 20, pp. 661-685.

Hamilton, J. D. (1988), “Rational Expectations Econometric Analysis of Changes inRegime: An Investigation of the Term Structure of Interest Rates”, Journal ofEconomic Dynamics and Control, Vol.12 No. (2-3), pp 385-423.

Hamiltom, J. D. and Susmel, R. (1994), “Autoregressive Conditional Heteroskedasticityand Changes in Regime”, Journal of Econometrics, Vol.64, No.12, pp 307-333.

Harries, L.H. (1989), “The October 1987 S&P 500 Stock-Futures Basis”, Journal ofFinance, Vol. 1 (1), pp. 77-99.

Hass, M.; Mittnik, S. and Paolella, M. (2004), “A New Approach to Markov SwitchingGARCH Model”, Journal of Financial Econometrics, Vol.2, No.4, pp 493-530.

Herbst, A. F. and Maberly, E. D. (1992), “The Information Role of End of the DayReturns in Stock Index Futures”, Journal of Futures Markets, Vol. 12, pp. 595-601.

Inclan, C. and Tiao, G. C. (1994), “Use of Cumulative-sum-of-squares for RetrospectiveDetection of Changes of Variance”, Journal of American Statistical Association,Vol.89, No.427, pp 913-923.

Jagadeesh, N. and Subrahmanyam, A. (1993), “Liquidity effect of the Introduction ofS&P 500 Index Futures Contracts on the Underlying Stocks”, Journal of Business,Vol. 66, pp. 171-187.

Kamara, A., Millar, T. and Siegel, A. (1992), “The Effect of Futures Trading on theStability of the S&P 500 Returns”, Journal of Futures Markets, Vol. 12, pp.645-658.

Kim, S.; Cho, S. and Lee, S. (2000), “On the CUSUM Test for Parameter Changes inGARCH (1, 1) Model”, Communications in Statistics: Theory and Methods, Vol.29,No.2, pp 445-462.

Kokoszka, P. and Leipus, R. (2000), “Change-Point Estimation in ARCH Model”,Bernoulli, Vol.6, No.3, pp 513-539.

Kumar, A.; Sarin, A. and Shastri, K. (1995), “The Impact of Listing of Index Options onthe Underlying Stocks”, Pacific-Basin Finance Journal, Vol.3, pp. 303-317.

Lamoureux, C.G. and Lastrapes, W. D. (1990), “Persistence in Variance, StructuralChange and the GARCH Model”, Journal of Business and Economic Statistics,Vol.8, No.2, pp 225-234.

23

Lamoureux, C.G. and Pannikath, S.K. (1994), “Variations in Stock Returns:Asymmetries and Other Patterns”, Working Paper, John M Olin School ofBusiness, St. Louis MO.

Lee, S. and Park, S. (2001), “The CUSUM of Squares Test for Scale Changes in InfiniteOrder Moving Average Process”, Scandinavian Journal of Statistics, Vol.28, No.4,pp 625-644.

Lee, S.; Tokutsu, Y. and Meakawa, K. (), “The Residual Cusum Test for the Consistencyof Parameters in GARCH (1, 1) Models”, Hiroshima University Working Paper.

Ma, C. K. and Rao, R. P. (1988), “Information Asymmetry and Option Trading”,Financial Review, Vol. 23, pp. 39-51.

Mikosch, T. and Starica, C. (2000), “Change in Structure of Financial Time Series, LongRange Dependence and GARCH Model”, Central for Analytical Finance WorkingPaper, University of Aarhus, http://cls.dk/caf/wp/wp-58.pdf.

Narasimhan, J. and Subrahmanyam, A. (1993), “Liquidity Effects of the Introduction ofthe S&P 500 Index Futures and Contracts on the Underlying Stocks”, Journal ofBusiness, Vol. 66, pp. 171-187.

Nath, Golaka C. (2003), “Behaviour of Stock Market Volatility After Derivatives”,NSENEWS, National Stock Exchange of India, November Issue.

Peat, P. and McCorry, M. (1997), “Individual Share Futures Contract: The EconomicImpact of Their Introduction on Underlying Equity Market”, University ofTechnology Sydney, School of Finance and Economics, Working Paper No. 74,http://www.buiness.uts.edu.au./finance/.

Perron, P. (1990), “Testing For Unit Root in a Time Series With a Changing Mean”,Journal of Business and Economic Statistics, 8: pp 153-162.

Poorter M. and Dijk, D. (2004), “Testing for Changes in Volatility in HeteroskedasticityTime Series- A Further Examination”, Economic Institute Report EI 2004-38,Erasmus University Rotterdam.

Raju, M. T. and Karande, K. (2003), “Price Discovery and Volatility on NSE FuturesMarket”, SEBI Bulletin, Vol. 1(3), pp. 5-15.

Robinson, G. (1993), “The Efeect of Futures Trading on Cash Market Volatility”, Bankof England Working Paper No. 19, www.ssrn.com./Abstract id=114759.

Ross, S. A. (1989), “Information and Volatility: The No-Arbitrage Martingale Approachto Timing and Resolution Irrelevancy’, Journal of Finance, Vol. 44, pp. 1-17.

24

Saktival, P. (2007), “The Effect of Futures Trading on the Underlying Volatility:Evidence from the Indian Stock Market”, Paper presented at Fourth NationalConference on Finance & Economics, ICFAI Business School, Bangalore,December 14-15.

Samanta, P. and Samanta, P. K. (2006), “Impact of Index Futures on the Underlying SpotMarket Volatility”, ICFAI Journal of Applied Finance, Vol. 13, No. 10, pp. 52-65.

Sanso, A.; Arago, V. and Carrion, J. L. (2004) ‘Testing for Changes in the UnconditionalVariance of Financial Time Series,’ University of Barcelona Working Paper.

Schwert, G.W. and Seguin, P. J. (1990), “Heteroskedasticity in Stock Returns”, Journalof Finance, Vol.45, No.4, pp 1129-1155.

Shenbagaraman, P. (2003), “Do Futures and Options Trading Increase Stock MarketVolatility”, NSE Research Initiative paper No. 20,http://www.nseindia.com/content/reserch/paper60.pdf.

Spyrou, S. I. (2005), “Index Futures Trading and Spot Price Volatility”, Journal ofEmerging market Finance, Vol. 4, 151-167.

Stein J. C. (1987), “Information Externalities and Welfare Reducing Speculation”,Journal of Political Economy, Vol. 95, pp. 1123-1145.

Thenmozhi, M. (2002), “Futures Trading Information and Spot Price Volatility of NSE -50 Index Futures Contract”, NSE Research Initiative Paper No. 18,http://www.nseindia.com/content/reserch/paper59.pdf.

Thenmozhi, M. and Sony, T. M. (2002), “Impact of Index Derivatives on S&P CNXNifty Volatility: Information Efficiency and Expirations Effects”, ICFAI Journal ofApplied Finance, Vol. 10, pp. 36-55.

Vipul (2006), the Impact of the Introduction of the Derivatives on Underline Volatility:Evidence from India, Applied Financial Economics, Vol. 16, pp.687-694

25

Annexure

1. Volatility Breaks in ACCDate of inclusion in Nifty : before 2002Date of commencement of derivative trading : 02-07-2001

PeriodTotal

Persistence)

UnconditionalVolatility:

/(1- )02-01-1995 to 17-10-1996 2.6722 0.0798 0.7895 0.8692 20.434218-10-1996 to 05-03-2002 5.1401 0.1271 0.7897 0.9168 61.802406-03-2002 to 18-05-2004 2.1123 0.0779 0.8602 0.9381 34.113119-05-2004 to 27-02-2006 0.8276 0.0801 0.8768 0.9569 19.207428-02-2006 to 31-10-2007 3.0037 0.2937 0.5482 0.8419 18.9966

2. Volatility Breaks in Ambuja Cement

3. Volatility Breaks in Bajaj AutoDate of inclusion in Nifty : before 2002Date of commencement of derivative trading : 02-07-2001

4. Volatility Breaks in BHELDate of inclusion in Nifty : before 2002Date of commencement of derivative trading: 02-07-2001

PeriodTotal

Persistence)

UnconditionalVolatility:

/(1- )02-01-1995 to 28-05-1998 3.5799 0.2556 0.5843 0.8399 22.365929-05-1998 to 07-03-2002 9.1327 0.1149 0.6721 0.7871 42.886408-03-2002 to 31-10-2007 2.0388 0.1575 0.7414 0.8989 20.1737

Date of inclusion in Nifty : before 2002Date of commencement of derivative trading : 20-04-2005

PeriodTotal

Persistence)

UnconditionalVolatility:

/(1- )02-01-1995 to 08-01-1998 1.3858 0.1022 0.8510 0.9621 36.563409-01-1998 to 07-05-2001 6.4163 0.1493 0.6133 0.7626 27.027308-05-2001 to 31-10-2007 1.4357 0.0964 0.8558 0.9522 30.0299

26

5. Volatility Breaks in BPCLDate of inclusion in Nifty : before 2002Date of commencement of derivative trading: 02-07-2001

PeriodTotal

Persistence)

UnconditionalVolatility:

/(1- ) 02-01-1995 to 02-04-1998 3.2272 0.1593 0.4942 0.6535 9.3142 03-04-1998 to 19-04-2001 7.0561 0.1146 0.7911 0.9057 74.8180 20-04-2001 to 02-12-2004 5.0257 0.2000 0.5346 0.7346 18.9364 03-12-2004 to 31-10-2007 2.5205 0.0902 0.7976 0.8878 22.4667

6. Volatility Breaks in CiplaDate of inclusion in Nifty : Before 2002Date of commencement of derivative trading: 02-07-2001

PeriodTotal

Persistence)

UnconditionalVolatility:

/(1- )02-01-1995 to 27-02-1996 5.1531 0.2368 0.50063 0.7375 19.627228-02-1996 to 18-12-1998 3.2377 0.2148 0.51033 0.7251 11.777319-12-1998 to 22-10-2001 3.7717 0.0726 0.89078 0.9634 103.024123-10-2001 to 25-04-2003 1.5358 0.1024 0.50407 0.6065 3.902926-04-2003 to 31-10-2007 3.0240 0.1547 0.55661 0.7113 10.4736

7. Volatility Breaks in Dr. Reddy

8. Volatility Breaks in GlaxoDate of inclusion in Nifty : Before 2002Date of commencement of derivative trading: : 01-07-2005

PeriodTotal

Persistence)

UnconditionalVolatility:

/(1- )02-01-1995 to 11-11-1997 2.8904 0.1777 0.1367 0.3143 4.215512-11-1997 to 17-12-1999 6.0813 0.2566 0.1054 0.3621 9.532617-12-1999 to 05-06-2000 12.0360 0.1773 0.2942 0.4715 22.771806-06-2000 to 21-05-2002 3.6969 0.2771 0.3878 0.6649 11.031422-05-2002 to 31-10-2007 1.5725 0.1276 0.7649 0.8925 14.6324

Date of inclusion in Nifty : Before 2002Date of commencement of derivative trading: 02-07-2001

PeriodTotal

Persistence)

UnconditionalVolatility:

/(1- )02-01-1995 to 17-03-1998 2.1294 0.2210 0.6338 0.8548 14.664618-03-1998 to 21-06-2000 6.5563 0.1287 0.7772 0.9059 69.651722-06-2000 to 31-05-2004 5.1207 0.2005 0.0682 0.2687 7.001901-06-2004 to 31-10-2007 0.8829 0.0318 0.9574 0.9892 81.4470

27

9. Volatility Breaks in GrasimDate of inclusion in Nifty : Before 2002Date of commencement of derivative trading : 02-07-2001

PeriodTotal

Persistence)

UnconditionalVolatility:

/(1- )02-01-1995 to 03-02-1998 2.0851 0.1144 0.3234 0.4378 3.708704-02-1998 to 26-05-2000 6.4494 0.0864 0.8591 0.9455 118.229427-05-2000 to 31-12-2001 5.9509 0.3074 0.2615 0.5690 13.806201-01-2002 to 31-10-2007 1.1593 0.1685 0.7733 0.9419 19.9402

10. Volatility Breaks in HPCLDate of inclusion in Nifty : Before 2002Date of commencement of derivative trading : 02-07-2001

PeriodTotal

Persistence)

UnconditionalVolatility:

/(1- )02-01-1995 to 10-05-1995 6.1886 0.0111 0.8245 0.8356 37.643611-05-1995 to 29-05-1998 1.8622 0.1950 0.4607 0.6557 5.409030-05-1998 to12-01-2001 9.4250 0.3387 0.1072 0.4459 17.009613-01-2001 to 06-08-2002 1.9543 0.0891 0.8883 0.9774 86.513907-08-2002 to 31-10-2007 2.3208 0.1089 0.8484 0.9573 54.3013

11. Volatility Breaks in HULDate of inclusion in Nifty : Before 2002Date of commencement of derivative trading : 02-07-2001

PeriodTotal

Persistence)

UnconditionalVolatility:

/(1- )02-01-1995 to 25-04-1997 0.9545 0.1520 0.6730 0.8250 5.452626-04-1997 to 10-10-2001 2.1280 0.1027 0.8372 0.9399 35.389711-10-2001 to 02-07-2003 0.9774 0.0991 0.8447 0.9437 17.366203-07-2003 to 31-10-2007 2.6968 0.1359 0.6235 0.7594 11.2087

12. Volatility Breaks in ITCDate of inclusion in Nifty : Before 2002Date of commencement of derivative trading : 02-07-2001

PeriodTotal

Persistence)

UnconditionalVolatility:

/(1- )02-01-1995 to 02-11-2001 3.4298 0.0689 0.8795 0.9484 66.418103-11-2001 to 02-09-2005 1.6997 0.1810 0.6055 0.7865 7.961703-09-2005 to 31-10-2007 2.2541 0.0878 0.8126 0.9003 22.6129

28

13. Volatility Breaks in L&TDate of inclusion in Nifty : Before 2002Date of commencement of derivative trading : 02-07-2001

PeriodTotal

Persistence)

UnconditionalVolatility:

/(1- )02-01-1995 to 30-04-1998 2.4064 0.1320 0.7277 0.8597 17.154501-05-1998 to 25-07-2000 7.3246 0.0824 0.8334 0.9159 87.052526-07-2000 to 09-11-2001 5.9836 0.1232 0.6126 0.7358 22.648010-11-2001 to 23-05-2003 0.7583 0.0186 0.9670 0.9856 52.659224-05-2003 to 31-10-2007 1.8871 0.1601 0.7634 0.9235 24.6802

14. Volatility Breaks in M&MDate of inclusion in Nifty : Before 2002Date of commencement of derivative trading : 02-07-2001

PeriodTotal

Persistence)

UnconditionalVolatility:

/(1- )02-01-1995 to 14-01-1998 3.5084 0.1041 0.6018 0.7059 11.928715-01-1998 to 24-05-2002 6.0605 0.1324 0.7527 0.8851 52.736325-05-2002 to 31-10-2007 1.6448 0.0871 0.8717 0.9588 39.9231

15. Volatility Breaks in MTNLDate of inclusion in Nifty : Before 2002Date of commencement of derivative trading : 02-07-2001No structural break in volatility is detected

16. Volatility Breaks in Reliance EnergyDate of inclusion in Nifty : before 2002Date of commencement of derivative trading : 12-03-2004

PeriodTotal

Persistence)

UnconditionalVolatility:

/(1- )02-01-1995 to 01-04-1999 4.6660 0.1367 0.6092 0.7459 18.360802-04-1999 to 30-05-2001 6.3253 0.1646 0.6722 0.8368 38.764931-05-2001 to 06-06-2003 2.0174 0.1347 0.6117 0.7464 7.954707-06-2003 to 18-05-2004 5.9502 0.5140 0.0655 0.4485 10.790019-05-2004 to 31-10-2007 2.1141 0.2109 0.6901 0.9010 21.3477

29

17. Volatility Breaks in RILDate of inclusion in Nifty : before 2002Date of commencement of derivative trading : 29-11-2001

PeriodTotal

Persistence)

UnconditionalVolatility:

/(1- )02-01-1995 to 20-11-2001 3.6022 0.2186 0.6355 0.8541 24.689621-11-2001 to 31-10-2007 2.1473 0.2527 0.4844 0.7371 8.1664

18. Volatility Breaks in SAILDate of inclusion in Nifty : 04-08-2003Date of commencement of derivative trading: 15-09-2006

PeriodTotal

Persistence)

UnconditionalVolatility:

/(1- )02-01-1995 to 24-11-1997 4.2023 0.2113 0.6260 0.8374 5.018625-11-1997 to 05-04-2000 20.2690 0.4358 0.0237 0.4595 35.500506-04-2000 to 09-07-2004 3.2230 0.2363 0.7418 0.9780 3.295510-07-2004 to 31-10-2007 3.1393 0.1815 0.7367 0.9182 3.4191

19. Volatility Breaks in SBIDate of inclusion in Nifty: Before 2002Date of commencement of derivative trading: 02-07-2001

PeriodTotal

Persistence)

UnconditionalVolatility:

/(1- )02-01-1995 to 28-02-2002 0.8837 0.0667 0.8999 0.9666 26.425101-03-2002 to 19-12-2003 2.9875 0.1090 0.8261 0.9351 45.997020-12-2003 to 19-05-2004 6.0329 0.3889 0.2063 0.5952 14.902020-05-2004 to 31-10-2007 1.8995 0.0495 0.9143 0.9637 52.3412

20. Volatility Breaks in Tata MotersDate of inclusion in Nifty : before 2002Date of commencement of derivative trading : 26-12-2003No structural break in volatility is detected

21. Volatility Breaks in Tata PowerDate of inclusion in Nifty : before 2002Date of commencement of derivative trading : 02-07-2001

PeriodTotal

Persistence)

UnconditionalVolatility:

/(1- )02-01-1995 to 26-03-1999 4.1018 0.2074 0.1945 0.4019 6.857927-03-1999 to 04-03-20002 6.9024 0.1175 0.7107 0.8282 40.176905-03-2002 to 31-10-2007 1.4513 0.1572 0.7841 0.9413 24.7026