CA Ashutosh Pandey Membership No. 427484 Forex and Treasury Management Batch No 38, Mumbai Derivatives markets in Interest Rate and Exchange Rates, and their utility for exporters and importers in mitigating forex risk.

Transcript

CA Ashutosh PandeyMembership No. 427484Forex and Treasury Management Batch No 38, Mumbai

Derivatives markets in Interest Rate and Exchange Rates, and their utility for exporters and importers in mitigating forex risk.

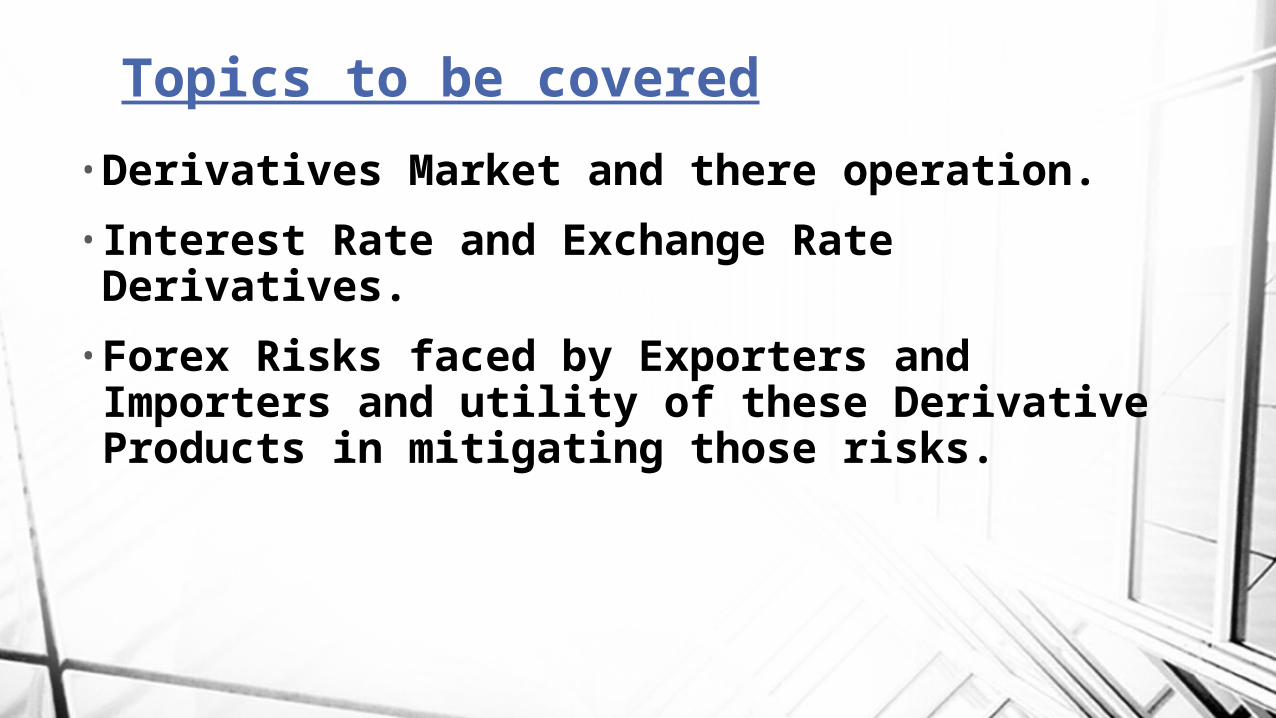

• Derivatives Market and there operation.• Interest Rate and Exchange Rate Derivatives.• Forex Risks faced by Exporters and Importers and utility of

these Derivative Products in mitigating those risks.

Topics to be covered

• A Place where Derivative Products are bought and sold. We have 2 platforms for purchase and sale of such securities:• Over The Counter Where 2 parties meet an agrees to buy and sale as per there

customized agreement. There is always a risk of counterparty default inherent in these transactions known as Default Risk.

• Regulated Exchange A place where securities are bought and sold with counterparty being the exchange itself, this eliminates the risk of default as exchange acts as a mediator between the parties and daily margins are charged from them based on there exposure.

• There are 3 motives for entering into a Derivative Transactions:• Hedging is mitigating an existing risk. It can be in full hedge or partial hedge against

your exposure.• Arbitrage is making a riskless profit by taking advantage of mispricing of an asset within

a market or across market. It is done by creating a short and long positions at the same point of time.

• Speculation is done on an arbitrary basis with a motive of making high profits with associated risks.

Derivatives Market

• Financial Instrument whose value changes based on movement in underlying interest rates.

• 1) Interest Rate Swap (IRS) A contract where one party agrees to pay fixed rate and receive floating rate at regular intervals over a certain period of time. At initiation a fixed rate is determined known as Swap Rate. In India any Regulated Institutional Entity can trade in interest rate swaps on electronic trading platforms. For Rupee IRS these entities are allowed to enter for the purpose of hedging as well as market making, but corporate customers are only allowed for hedging purposes. For Non Rupee IRS participation is only allowed for hedging an underlying exposure.• Example XYZ has floating rate obligation for 3 years and is worried about

increasing interest rates in future, so they can go for a pay fixed and receive floating IRS wherein they will be able to lock in there interest obligation. This will be a Fixed for Floating IRS.

Interest Rate Derivatives.

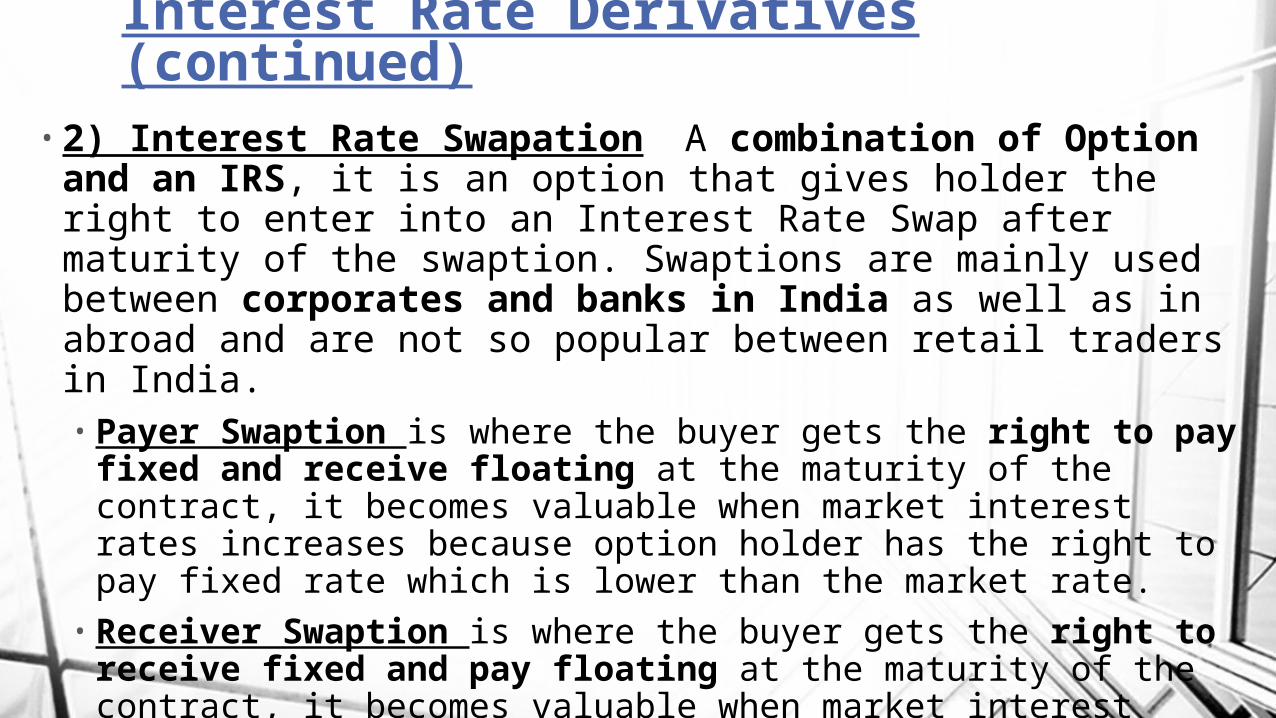

• 2) Interest Rate Swapation A combination of Option and an IRS, it is an option that gives holder the right to enter into an Interest Rate Swap after maturity of the swaption. Swaptions are mainly used between corporates and banks in India as well as in abroad and are not so popular between retail traders in India. • Payer Swaption is where the buyer gets the right to pay fixed and receive

floating at the maturity of the contract, it becomes valuable when market interest rates increases because option holder has the right to pay fixed rate which is lower than the market rate.

• Receiver Swaption is where the buyer gets the right to receive fixed and pay floating at the maturity of the contract, it becomes valuable when market interest rates decreases because the option holder has the right to receive fixed rate which is lower than the market rate.

Interest Rate Derivatives (continued)

• Example XYZ has floating rate obligation for 3 years and is worried about increase in interest rates after 1 year, so they can go for a payer swaption which expires in 1 year and gives right to enter into a 2 year swap, the notation for which will be “1x3 Swaption”.

• 3) Forward Rate Agreement (FRA) A forward contract where 2 parties determine a rate of interest to be paid or received over a period beginning at a future date. It is a customized OTC product.

Interest Rate Derivatives (continued)

Today

1 month30 days

2 months60 days

3 months90 days

FRA initiation Loan

maturity

FRA expiration

30 days loan in 60 days

Loan initiation

“2x3 FRA”

• A 2x3 FRA is a contract that expires in 2 months (60 days), and the underlying loan is settled in 3 months (90 days) for which underlying rate is 1 month (30 days) benchmark rate on a 30 day loan in 60 days.A Long Position in FRA is the party that would borrow money and if the floating rate (benchmark rate) at expiration is above rate specified in agreement the long position has benefited from the specified rate.

• 4) Interest Rate Futures A contract to settle interest rate differential at a future date. In India only Government Bonds and Treasury Bills are allowed as underlying, these are standardized, exchange traded and single settlement derivatives.• Example Buyer of a 3-months IRF contract has a right to

receive fixed interest for 3 months (and pay floating) and seller has the opposite position as an obligation to pay that fixed interest (and receive floating). It generates value based on the fluctuations in underlying interest rate.

Interest Rate Derivatives (continued)

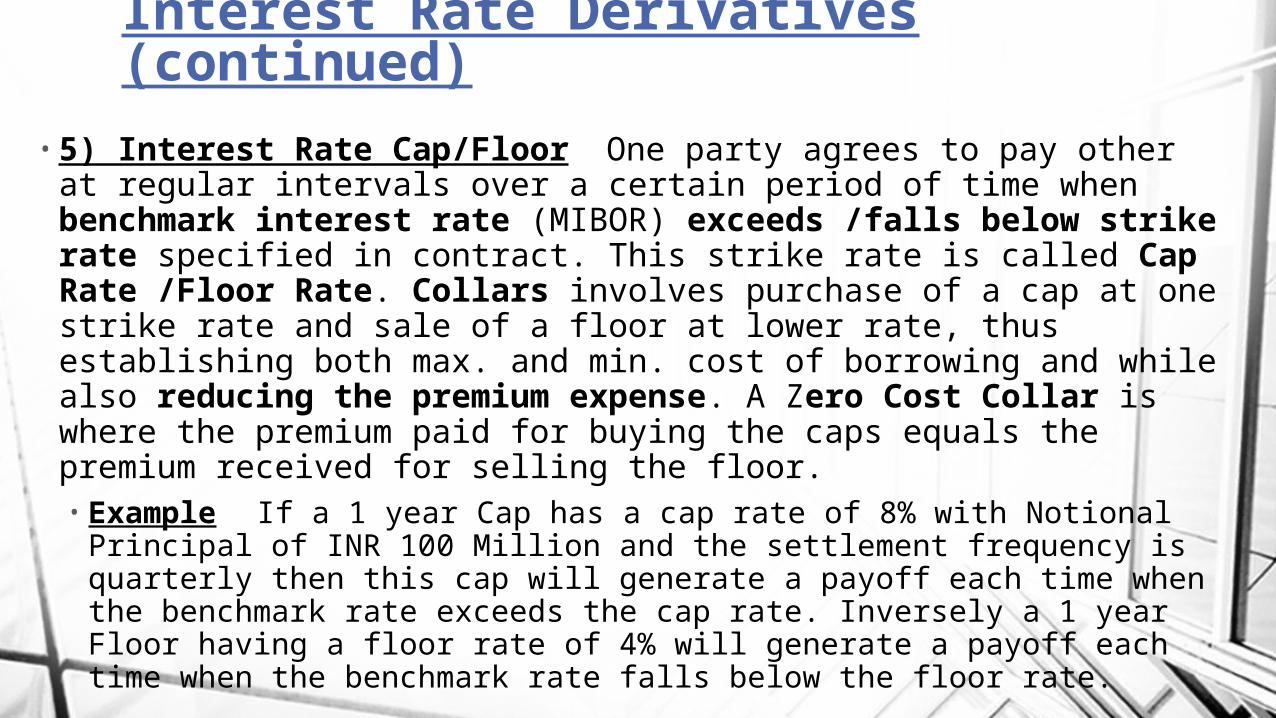

• 5) Interest Rate Cap/Floor One party agrees to pay other at regular intervals over a certain period of time when benchmark interest rate (MIBOR) exceeds /falls below strike rate specified in contract. This strike rate is called Cap Rate /Floor Rate. Collars involves purchase of a cap at one strike rate and sale of a floor at lower rate, thus establishing both max. and min. cost of borrowing and while also reducing the premium expense. A Zero Cost Collar is where the premium paid for buying the caps equals the premium received for selling the floor.• Example If a 1 year Cap has a cap rate of 8% with Notional Principal of

INR 100 Million and the settlement frequency is quarterly then this cap will generate a payoff each time when the benchmark rate exceeds the cap rate. Inversely a 1 year Floor having a floor rate of 4% will generate a payoff each time when the benchmark rate falls below the floor rate.

Interest Rate Derivatives (continued)

• Financial Instrument whose value changes based on movement in underlying exchange rates of 2 or more currencies.

• 1) Currency Forward Agreement between two parties to exchange two designated currencies at a specific time in future at a predetermined exchange rate. It offers protection from exchange rate fluctuations. These are customized OTC products.• Fixed Forward Contract Settlement/Delivery is only allowed at expiry date.• Option Forward Contract Settlement/Delivery is allowed anywhere in between

two dates.• Example XYZ Pvt. Ltd., an exporter, enters into a Forward Currency Contract

with SBI, to sell 5000 USD @ USD/INR 60 at the end of 6 Months from the initiation of the contract. At the date of settlement USD/INR is 58.83, thus XYZ has a gain of INR 5850 from the contract. [(60-58.83)*5000]

Exchange Rate Derivatives.

• 2) Currency Swaps An agreement between two or more parties to exchange interest obligation/receipts for an agreed period between two different currencies. At the start, initial principal is exchanged and at the end of the contract this is re-exchanged, at an exchange rate agreed at the beginning of the contract. This notional principal is used for the calculation of the interest. These are customized OTC products.• Example

Exchange Rate Derivatives (continued)

IndiaCounterparty

1

USCounterparty

2

INR 3,000,000

USD 50,0004% intt. on USD

50,000

4% on USD paid to Local Bank

6% intt. on INR 3,000,000

6% on INR paid to Local Bank

Borrow from Local Bank

Borrow from Local Bank

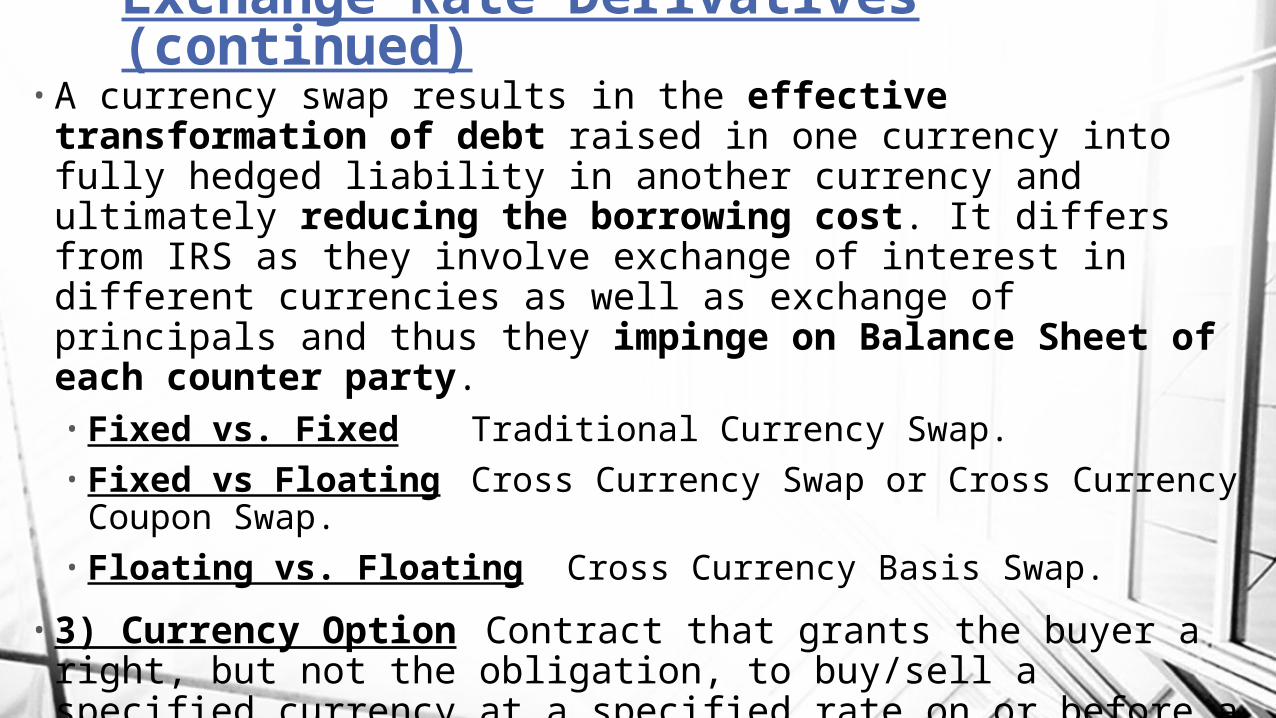

• A currency swap results in the effective transformation of debt raised in one currency into fully hedged liability in another currency and ultimately reducing the borrowing cost. It differs from IRS as they involve exchange of interest in different currencies as well as exchange of principals and thus they impinge on Balance Sheet of each counter party.• Fixed vs. Fixed Traditional Currency Swap.• Fixed vs Floating Cross Currency Swap or Cross Currency Coupon Swap.• Floating vs. Floating Cross Currency Basis Swap.

• 3) Currency Option Contract that grants the buyer a right, but not the obligation, to buy/sell a specified currency at a specified rate on or before a specified date, for which buyer has to pay a premium to the option seller. Currency Call Options gives right to buy and Currency Put Options gives right to sell. In India, SEBI has recently introduced Exchange Traded Currency Options on USD/INR, EUR/INR, GBP/INR and JPY/INR currency pairs.

Exchange Rate Derivatives (continued)

• 4) Currency Futures It is a standardized form of a forward contract that is traded on an exchange. It's an agreement to buy or sell a specified quantity of an underlying currency on a specified date at a specified price. In India, currently four currency pairs are traded USD/INR, EUR/INR, GBP/INR and JPY/INR with a lot size of 1000 units of the base currency, except JPY where the lot size is 100,000. Settlement for the customer is, however, done in Rupee terms and not in the foreign currency, submitting proof on underlying is not a precondition. Cross Currency Futures has also been recently introduced by SEBI, where one of the common currencies is not INR, they are EUR/USD, GBP/USD and USD/JPY.• Example For example, if Rupee(USD/INR),one month is trading at Rs.47

and if one feels that Rupee would depreciate to Rs.49, he can enter into a 'long' position, by 'buying' a currency futures contract. If USD/INR for the same maturity period goes to Rs.49, he makes a gain of Rs.2 per dollar. So on a single contract of 1000$, he makes a gain of Rs.2000.

• Source: SBI https://corp.onlinesbi.com/corporate/sbi/corp_fx_trade_faq.html and SEBI Circular

• Exporter An exporter is engaged in sell of goods and services abroad for which he will be receiving payment in foreign currency, also they take foreign currency loans for conducting there foreign operations, thus they have a very high exposure to forex movements which can turn there high profits into huge loses just because of a sudden appreciation or depreciation of the currencies they are involved in. To mitigate these high risk exposures and to have a consistent financials, which is unaffected by shocks in forex market, an exporter should go for appropriate hedging products as per there risk exposures.• Examples• 1) If an Indian exporter is to receive a payment of USD 5000 in 3 Months and wants to

hedge his position against the volatility in the USD/INR, he can go for a Currency Forward wherein he can lock in his 3 Months USD/INR Rate for USD 5000. Currency Futures and Currency Options can also be looked upon as an alternative hedging tools, if there is an cost advantage on them.

Forex Risks faced by Exporters and Importers.

• 2) If an Indian exporter wants a USD Loan to enhance it’s operations in overseas, and the rate of borrowing for foreign borrowers is 8% in US but the same is 5% for local borrowers, he can go for a Currency Swap wherein he can exchange his debt obligation with any local borrower in US who needs an INR Loan but is facing the same problem of high rates in India for foreign borrowers.

• 3) Inflation Derivatives and Interest Derivatives are also used for Forex hedging, as they both play an inherent part in appreciation and depreciation of a currency.

Forex Risks faced by Exporters and Importers.

• Importer An importer is engaged in purchase of goods and services from abroad for which he will have to make a payment in foreign currency, and they also take foreign currency loans for conducting there foreign operations, thus they have a very high exposure to forex movements which can turn there high profits into huge loses just because of a sudden appreciation or depreciation of the currencies they are involved in. To mitigate these high risk exposures and to have a consistent financials, which is unaffected by shocks in forex market, an exporter should go for appropriate hedging products as per there risk exposures. • Examples• 1) If an Indian importer is to make a payment of USD 7000 in 6 Months and wants to

hedge his position from the volatility in the USD/INR, he can go for a Currency Forward wherein he can lock in his 6 Months USD/INR Rate for USD 7000. Currency Futures and Currency Options can also be looked upon as an alternative hedging tools, if there is an cost advantage on them.

Forex Risks faced by Exporters and Importers.

• 2) If an Indian importer wants a USD Loan to enhance it’s operations overseas, and the rate of borrowing for foreign borrowers is 8% in US but the same is 5% for local borrowers, he can go for a Currency Swap wherein he can exchange his debt obligation with any local borrower in US who needs an INR Loan but is facing the same problem of high rates in India for foreign borrowers.

• 3) Inflation Derivatives and Interest Derivatives are also used for Forex hedging, as they both play an inherent part in appreciation and depreciation of a currency.

• CONCLUSION Understanding and Mitigating Forex Risk is a very crucial task for the survival of an organization in an International Globalized Market. Organizations need to understand there exposures and accordingly use the hedging products amongst the various derivative products available, one error and the mitigation strategy can itself create exposure to a huge loss.