90

| Date post: | 15-Jul-2015 |

| Category: |

Education |

| Upload: | gouravsoni |

| View: | 307 times |

| Download: | 0 times |

Derivatives

Discussion Points What are Derivatives: An Introduction

Global growth of Derivatives

Domestic Derivatives Market

Overview of different types of derivatives Forwards Futures Options

Derivatives Defined An instrument whose value is derived from

another security or any other variable

Is has no independent value

The underlying could be financial instruments, metals, agri products, oil etc.

Example

Dependence on other variables and pre-defined nature of contract make it an excellent vehicle for managing risk

In the preceding example: Wheat was the underlying asset

The predefined contract provides certainty to both the farmer and the baker about the future proceeds and help them mitigate risk associated with uncertainty

Development and Growth of Derivatives Market Increase in Macroeconomic instability during the crisis of

1970s

Oil crisis of 1970s exposed the financial systems to the risk inherent in commodities

Collapse of Bretton Woods system that led to most currencies adopting free-float exchange rate

Increased currency risk

Increased Globalization of Business Activities resulting in higher foreign trade and a need for managing FX exposure

First Option Pricing formula was given by Black Scholes in 1970

Markets were flooded with various refined and sophisticated and complex derivative pricing models

Advanced computation facilities

Derivatives Contract

Primarily of 2 kinds

Traded on Exchange (organized derivatives trading)

Traded on OTC (unorganized trading)

OTC is a generic term used for the market outside the exchange

Derivatives in India Exchange Traded Equity Derivatives (derivatives

whose value is dependent on equities / stocks) – Launched in year 2000

Index Derivatives (underlying is an Index like Nifty or Sensex) – Launched in year 2001

The most preferred products Single stock futures account for about 55% of total

volume Nifty Futures account for about 35% of total volume

Commodity Derivatives Commodity Derivatives are contracts where the

underlying asset is a commodity like oil, gold, metals etc.

FCRA – Forward Contract Regulation Act governs Commodity Derivatives in India

Two nationwide online commodity exchanges NCDEX – National Commodity and Derivatives

exchange (mostly agri products are traded)

MCX – Multi Commodity Exchange (trading mostly bullion, metals and energy products)

Currency Derivatives Underlying asset is currency of a country

Recently launched in India

OTC currency derivative market large and active

Participation is mainly by Banks who trade on behalf of their clients (mostly companies)

Interest Rate Derivatives Value is derived from future interest rates

Underlying instrument is Interest Rate

Might be launched in India in coming years

Active in OTC market

Need for Derivative Products

Need for products which can be used to mitigate risk exposure

To guard against uncertainties arising out of fluctuations in asset prices

Products that work in both domestic as well as in the global markets

Types of derivatives Derivative Products Case Studies on application of derivatives Forwards Contracts Disadvantages and Advantages Futures Contract Forwards versus Futures: Comparison

Chart

Types of Derivatives

Forward Contract

Futures Contract

Option Contract

Derivatives Products

Products UnderlyingEquity Derivative StocksCommodity Derivative Metals, Bullion, OilExchange Rate Derivative Exchange RateInterest rate Derivative Interest RatesIndex Derivative Market Index (e.g. Nifty)

Illustrations Example 1.

Scenario - Tata Steel plans to obtain bank loan of INR 500 crores two months from now

Risk – Interest Rate uncertainty

If interest rate climbs by 1% Tata Steel will have to pay additional INR 5 crores for the loan (1% on 500 crores)

Solution: The company would like to lock in the prevailing interest rate for obtaining the loan using an interest rate derivative contract and hedge the risk exposure

Example 2.

Scenario – An investor expects a cash outflow of INR 50 thousand one month from now

To meet the cash requirement she has to sell a part of her portfolio (say shares of Stock X)

Stock X is currently trading at INR 1000 (she is required to sell 50 stocks to make the payment)

Risk – Asset price (Stock Volatility) uncertainty

If price of the stock falls to INR 900 after one month she will have to sell 56 shares resulting in further liquidation of her portfolio

Solution – She would like to lock in the prevailing market price using a equity derivative contract and hedge the risk exposure today rather than wait for one month and suffer loss from adverse price movements

Example 3.

Scenario – A company providing IT services (mainly exporting to US) would sell product worth USD 50 million in 3 months from now. Prevailing exchange rate is INR 50 per USD.

So, after three months the company will get a cash inflow of INR 250 crores from selling the product

Risk – Exchange Rate Risk

If after three months the Rupee appreciates to INR 45 / dollar. The company would make a loss of INR 25 crores

Solution – The company would like to lock in the prevailing exchange rate using currency derivative contract and hedge the risk exposure today rather than wait for three month and suffer loss from exchange rate movements

Example 4.

Scenario – A domestic airlines company needs to import 2 million barrels of oil for meeting operational requirements in two months from now.

Oil is trading at $65/bbl in the international market and INR USD exchange rate is INR 45/USD.

Company is required to have approx INR 585 crores to purchase oil

Risk – Oil price risk and exchange rate risk

If after two months Oil prices rise to $75/bbl and exchange rate moves to INR 50/ USD, the company would end up paying INR 750 crores (excess of INR 165 crores) to purchase 2MMbbl oil.

Solution – The company would like to lock in the prevailing spot price of Oil ($65/bbl) in the international markets using commodity derivatives on oil.

Further, the company shall use currency derivatives to sell INR and buy USD two months in future at the prevailing exchange rate of INR45/$.

The strategy will help the company to hedge the risk exposure of the firm from any uncertain movement in asset price or exchange rate.

Three Types of Derivatives

Forward Contract

Futures Contract

Options Contract

Forwards Contracts

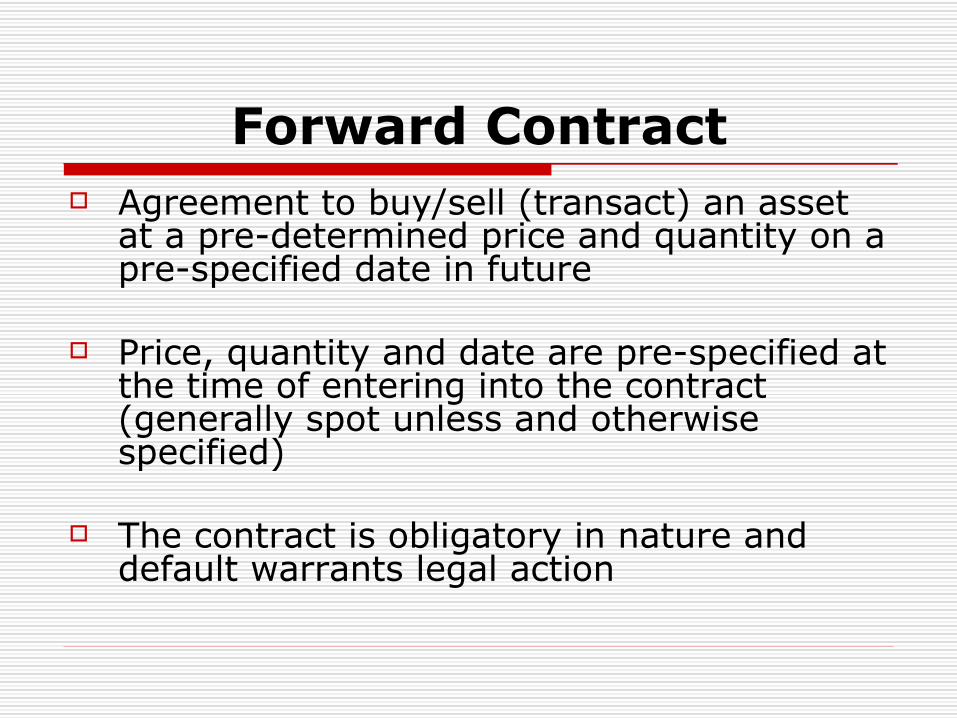

Forward Contract Agreement to buy/sell (transact) an asset

at a pre-determined price and quantity on a pre-specified date in future

Price, quantity and date are pre-specified at the time of entering into the contract (generally spot unless and otherwise specified)

The contract is obligatory in nature and default warrants legal action

Terminologies

Technically speaking:

The party agreeing to buy the asset assumes a Long position

The party agreeing to sell the asset assumes a Short position

Contract is traded off-exchange i.e. in the OTC market and settlement takes place as per mutual agreements (pre-decided terms and conditions)

Customization of contract along with risk hedging makes it an attractive product

No standardization of terms and condition is required for forward contracts

Example (asset/goods)

Party A <<<<<<< Party B Buyer Seller Long Position Short Position

T = After 2 months (specific date)P = @ INR 350/unitQ = 100 units

Contrary to spot contracts T, P and Q are pre-determined. At the time of delivery the goods and cash shall exchange hands.

Disadvantages of Forward Contracts

Common concerns while using forward contracts

Two major risks involved in Forward Contracts:

1/ Liquidity

No secondary market

Customization makes it a non-standard product

Trading happens on a one-on-one basis

Non-availability on exchange makes it extremely difficult to locate counterparty for transaction

2/ Default Risk

No exchange driven clearing and settlement procedure

Adverse price movements might tempt either counterparty to dishonor the contract

At any time, only one counter-party has the incentive to default

In the previous example if the spot price after two months rises to INR 400/unit, seller would gain by selling on spot and shall default on the contract

Advantages of Forward Contracts

Advantages of Forward Contracts No listing requirement

Activity is highly customized and negotiable (non-standardized)

Counterparties can mutually decide upon What to trade (asset / product and type) Where to trade (delivery location) How much to trade (quantity) What price to trade (price) When to trade (date)

No transaction cost, taxes etc.

No margin requirement

Futures Contract

Futures Contract

Agreement to buy/sell (transact) an asset at a pre-determined price and quantity on a pre-specified date in future

Price, quantity and date are pre-specified at the time of entering into the contract

The contract is obligatory in nature and default warrants for legal action

Understanding Futures Contract w.r.t. Forward Contracts

Exchange traded forward contracts

Standardized forward contracts

Attractive for large set of market participants

High liquidity

No counter-party risk or default risk as counterparty is the exchange itself

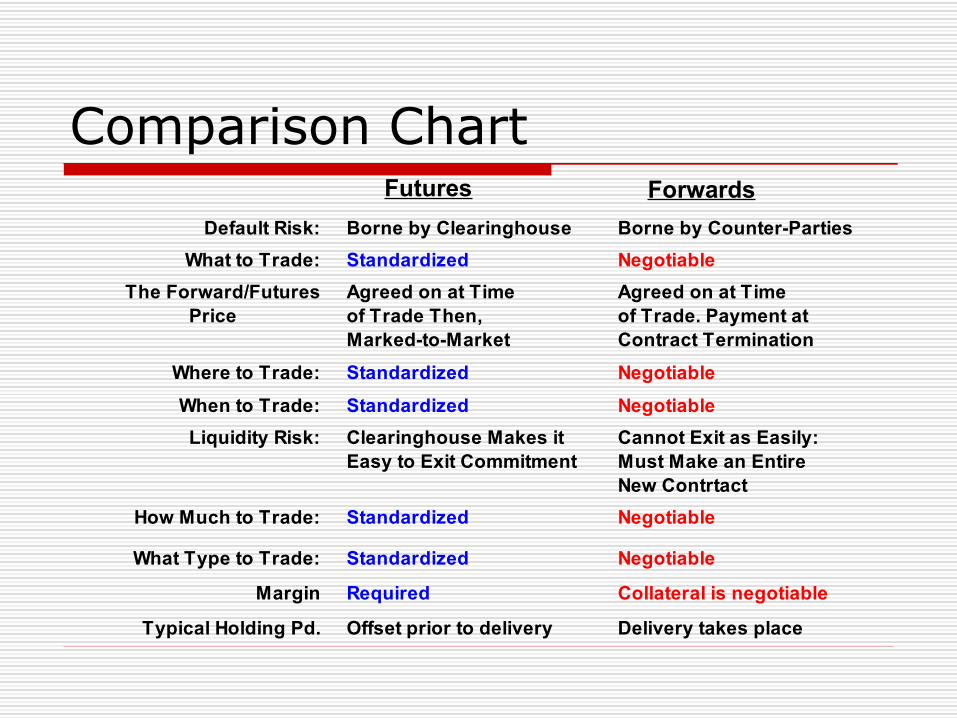

Comparison ChartFutures Forwards

Default Risk: Borne by Clearinghouse Borne by Counter-Parties

What to Trade: Standardized Negotiable

The Forward/Futures Agreed on at Time Agreed on at TimePrice of Trade Then, of Trade. Payment at

Marked-to-Market Contract Termination

Where to Trade: Standardized Negotiable

When to Trade: Standardized Negotiable

Liquidity Risk: Clearinghouse Makes it Cannot Exit as Easily:Easy to Exit Commitment Must Make an Entire

New Contrtact

How Much to Trade: Standardized Negotiable

What Type to Trade: Standardized Negotiable

Margin Required Collateral is negotiable

Typical Holding Pd. Offset prior to delivery Delivery takes place

One major advantage of Futures contract over Forward contracts

Complication of final settlement if the contract is traded subsequently can be avoided in Futures contract

Futures market would account the net final positions and declare two counterparties thereby facilitating hassle free transaction

Key Terminologies Forward Contract Futures Contract Long Position Short Position Underlying OTC Mark-to-market Hedgers Speculators Arbitragers

Commonly Traded futures contracts

Index Futures

Single stock futures

Interest Rate Futures

Commodity Futures

Futures on Financial Assets At any time three Futures contract trade in the market on

Stock Futures and Index Futures

1 month, 2 months and 3 months

E.g. November Futures, December Futures and January Futures

Futures contract expire on the last Thursday of the month. E.g. Nov Futures contract will expire on Thursday, 20 Nov 08.

On expiry a new 3 month contract is formed, the 2 months contract becomes the 1 month contract and 3 months contract becomes the 2 months contract

Positions Opening a Position

Having a long or short position in a contract. Eg. Mr X shorts 5 Jan Futures contracts on

Infosys

Outstanding or unsettled long or short positions

Closing a Position Buying or selling a contract that results in the

reduction of open positions e.g. Buying or selling two contra futures E.g. Mr X longs 5 Jan Futures contacts on

Infosys

Terminologies Basis – Spot Price minus the Futures Price

Spread – Difference between the prices of two futures contract

Cost of Carry – The cost incurred to finance the trading in derivatives. E.g. transaction cost, opportunity cost (interest lost on the balance in the margin account), storage cost (physical commodities) etc.

Measure of Liquidity

Open Interest

Volume

Open Interest Open Interest: Number of outstanding and unsettled

positions in a contract

Total number of contracts that have not expired or squared-off

Contract specific measure

Total of long position would exactly offset total of short positions and hence only one side of the contract is counted for the purpose of calculating the open interest

Interpretation of Open Interest Indicates level of trading activity in the F&O

segment of the underlying security

E.g. Sudden increase in Open Interest indicates increase in security’s volatility in near term on account of corporate news (insider)

Open Interest indicates that new money is flowing into the marketplace

General Interpretations of OI An increase in Open Interest along with an increase in

price is said to confirm an upward trend (market is strong)

An decrease in Open Interest along with a rise in price is said to confirm (signals) a downward trend

An increase in Open Interest along with decrease in price indicates market is weak

A decrease in both Open interest and Prices indicates market is strengthening

Volume Trading activity in the market with regard

to a specific contract, over a period of time, e.g. a day, a week or the entire life of the contact

Defined in terms of either: Number of contracts traded during a specific

period of time, or

Value of all the contracts traded

Open Interest and Volume Increase in Open Interest along with increase in volume

when prices rise indicates that more traders likely entering long positions

Thumb rules for interpreting changes in volume and open interest in futures market: Rising Vol. and rising OI confirms a trend Rising Vol. and falling OI indicates position

liquidation Falling Vol. and rising OI indicates cautious and

slow accumulation Falling Vol. and falling OI depicts a congestion

phase

Daily Price Movement Limits – Price Band

Daily Price Movement Limits are specified by the exchange for every contract

If the price hits lower limit it is called Limit Down

If the price hits upper limit it is called Limit Up

Normally trading ceases for the day in that contract once the contract is limit up or limit down

Purpose of limits is to prevent large price movements occurring because of speculative excess

What do Futures Prices indicate? Futures are normally traded daily as stocks

and laws of supply and demand apply to arrive at the price of the contract

Assume a Nifty November 2008 Futures Contract is trading at 3123 on 10 Nov 2008. What does that indicate?

As the contract is trading for the settlement on the last Thursday of November 2008, the trading level of 3123 indicates that at the close of market on expiry, the market expects the cash index to settle at 2989

All market participants seek to predict the cash index level at contract maturity

This results in price discovery of the cash index at a specific point

Futures prices are essentially the expected cash prices of the underlying asset at the maturity of the futures contract

Convergence of Futures Price to Spot Price Futures price converge to spot price as the

expiry approaches

On expiry the futures price equals the spot price and all futures contract are settled at the underlying cash market settlement price

Non convergence would result in an arbitrage opportunity

Convergence of Futures Price to Spot Price

Example of an Arbitrage:

Suppose the futures price is above the spot price at expiry. The arbitragers would Short a futures contract Buy the asset Deliver the assets

Margins

Margin Requirement Futures contract settlement on the exchange is the

responsibility of the exchange clearing house

To minimize the default risk on a contract due to unfavorable price movements the exchange mandates the counterparties to deposit a minimum amount as specified by the exchange

The amount is deposited in the margin account

This minimum amount deposited at the time of contract initiation is called the Initial Margin

Margin requirements might vary depending upon the volatility in the markets. Securities can also be deposited in lieu of cash.

Minimum initial margins on different positions are prescribed by the clearing house based on specified risk algorithm using Standard Portfolio Analysis of Risk (SPAN)

Maintenance Margin – Minimum margin level to be always maintained in the margin account

MM requirement is lower than the initial margin and it ensures that the margin account never becomes negative

If the margin account falls below the MM, investor receives a margin call and is expected to top up the margin account to the Initial Margin level the next day

The extra funds deposited are known as Variation Margin

Margin account is adjusted at the end of each trading day considering the day’s closing price to reflect the investor’s gain or loss. This practice is referred to as Marking to Market

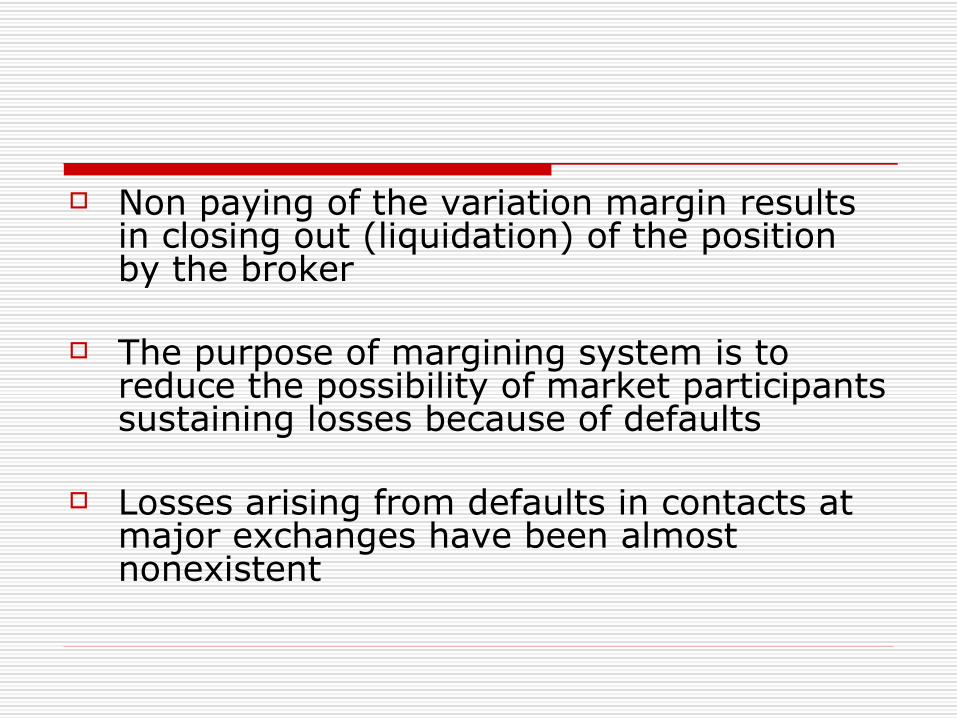

Non paying of the variation margin results in closing out (liquidation) of the position by the broker

The purpose of margining system is to reduce the possibility of market participants sustaining losses because of defaults

Losses arising from defaults in contacts at major exchanges have been almost nonexistent

Using margins the risk is divided into smaller pieces daily

The losses are collected from the losers and given to the gainers

Pay-in and Pay-out happens on T+1 basis

V-a-R model is used to estimate potential losses on any given day using certain confidence interval (probability)

V-a-R also helps deciding the margin limits (SPAN)

Margin Calculation and Margin Call E.g. ICICI Futures – Lot size is 700 shares and

Futures Price is INR 430/ share

Initial Margin (10% of contract value) – INR 30,100/ contract

Let us say; A buys 4 contracts on 07 Nov 2008 B sells 4 contracts on 07 Nov 2008

A and B pay INR 120,400 as Initial Margin

MM is 75% of IM – INR 90,300

IM = INR 120,400MM = INR 90,300

DateFutures Price (INR) Daily Gain(Loss)

Cumulative Gain (Loss)

Margin Account Balance Margin Call

430.00 120,40007 Nov 2008 435.00 14,000.00 14,000.00 134,400.0010 Nov 2008 438.00 8,400.00 22,400.00 142,800.0011 Nov 2008 426.00 -33,600.00 -11,200.00 109,200.0012 Nov 2008 420.00 -16,800.00 -28,000.00 92,400.0013 Nov 2008 398.00 -61,600.00 -89,600.00 30,800.00 89,600.0014 Nov 2008 405.00 19,600.00 -70,000.00 140,000.0017 Nov 2008 405.00 0 -70,000.00 140,000.0018 Nov 2008 403.00 -5,600.00 -75,600.00 134,400.0019 Nov 2008 385.00 -50,400.00 -126,000.00 84,000.00 36,400.0020 Nov 2008 398.00 36,400.00 -89,600.00 156,800.00

Margin Calculation for A

Applications of Futures: Valuation and Strategies

Assumptions No transaction costs and taxes

Market participants can borrow money at the same risk-free rate of interest

Borrowing rates equal lending rates

Arbitrage opportunities are exploited as they occur

No income is accrued on the asset like dividend etc.

No storage costs

Forward and futures prices are same

Notations T: time until expiry

S0: Spot price of the underlying asset

F0: Futures / Forward price today

r: Risk free rate of interest per annum, expressed with continuous compounding

Pay-off from Futures Contract

Pay-off is like profit/loss accruing to the investor

Since the contracts are MTM on a daily basis pay-offs are calculated based on the change in the market price of the contract daily

Pay-off from Long Futures: Unlimited gain if the prices rise and huge

losses if prices decline

Pay-off from Short Futures: Huge gains if the prices fall and

unlimited losses if the prices rise

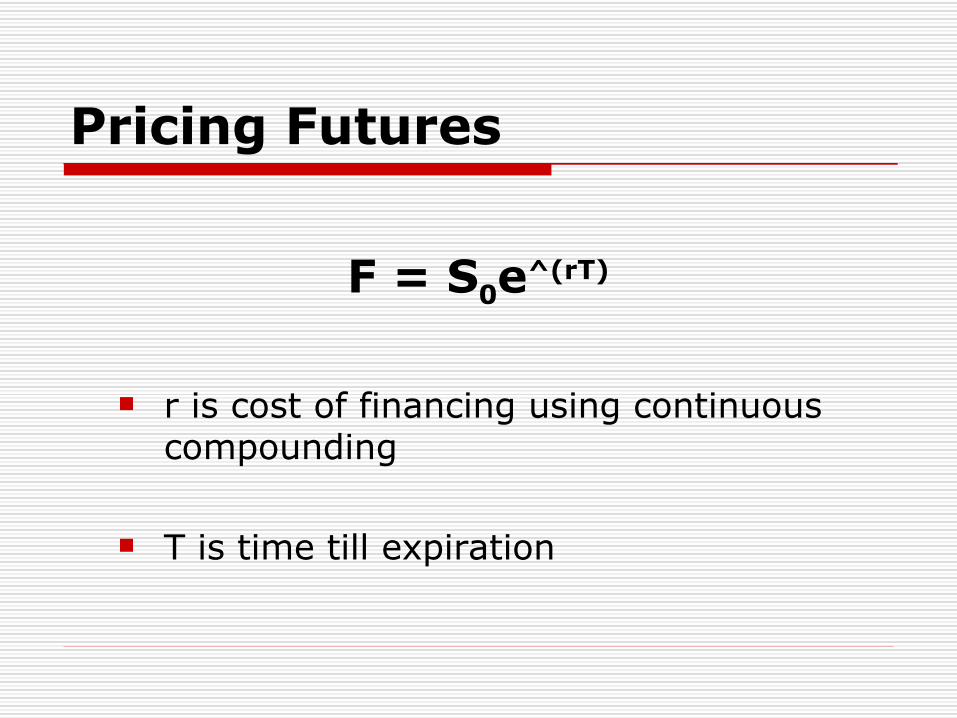

Pricing Futures

F = S0e^(rT)

r is cost of financing using continuous compounding

T is time till expiration

Example:

Security XYZ Ltd trades in the spot market at INR 1150. Assuming risk free rate to be 3% p.a. Calculate the fair value (theoretical value) of the 2 months futures contract (assume the security to be non dividend paying). INR 1156

Strategies open to an arbitrageur if the futures price is: INR 1175 or, INR 1140

Strategy, if futures price @ INR 1170: Cash and Carry Arbitrage

Step 1/ : Borrow INR 1150 at risk-free rate

Step 2/ : Invest the proceeds to buy the underlying asset at INR 1150

Step 3/ : Short 2 month futures contract to sell the asset for INR 1175

Gain from the strategy: INR 25 is the gain on price differential INR 6 is the interest paid on borrowed amount INR 19 is the overall gain { F - S0e^(rT) }

Strategy, if futures price @ INR 1140: Reverse Cash and Carry Arbitrage

Step 1/ : Sell the security on spotStep 2/ : Invest the proceeds at risk-free rateStep 3/ : Take a long position in a two month

futures contract for INR 1140

Gain from the strategy: INR 6 is the risk-free interest earned Price differential INR(1150-1140) = INR 10 INR 16 is the overall gain { S0e^(rT) - F }

So if;

F > S0e^(rT) {buy the asset and short the forward contract on the asset} – Contango

F < S0e^(rT) {sell the asset and long the forward contract} – Backwardation

The price should be equal to INR 1156 for no arbitrage opportunity to exist

Cash and Carry Arbitrage prevents futures prices from being above the theoretical price

Reverse cash and carry arbitrage prevents prices from dipping below the theoretical price

Example: Non dividend paying stock trading at INR

120

Risk free rate is 5%

Calculate the fair value of 1 year forward contract

Strategy if the forward price is INR 128?

1/ Borrow INR 120 at 5%2/ Invest to buy the stock on spot3/ Sell the one year forward @ INR 128

Gain: Price differential less interest INR (8 – 6) = INR 2 per contract

Application of Futures: Key Strategies Hedging: Long Security, sell futures

Speculation: Bullish security, buy futures

Speculation: Bearish security, sell futures

Arbitrage: Overpriced futures: buy spot, sell futures

Arbitrage: Underpriced futures: buy futures, sell spot

Short Hedging: Long Security, sell futures Investor holding a stock sees the current price falling

from INR 450 to INR 390

In the absence of stock futures he would sell the security (or suffer from hypertension)

Using security futures he can minimize his price risk

Sell a futures contract to off-set the downside risk due to the fall in stock price

Index futures can be effectively used to get rid of the market risk of the portfolio – Long Portfolio + Short Nifty

Speculation: Bullish security, buy futures Futures provide a high leverage on

investment

A speculator is bullish on a stock and decides to buy securities to take the advantage of price rise. Invests INR 100,000 (100 shares * 1000/share)

One month later the price rises to INR 1010, his profit is INR 1,000 on INR 100,000 investment (i.e. return of 6%)

Other speculator takes the same position using one futures contract trading at 1006. Assume contract value is INR 100,600 (100 shares/contract) and approx 20% is the margin i.e. INR 20,000

On expiry the contract closes on INR 1010 (equal to spot price) providing a profit of INR 400 (i.e. annual return of 12% on INR 20,000 invested)

Speculation: Bearish security, sell futures

What if a speculator finds an overvalued stock?

How can he trade based on his opinion?

Sell stock futures

If his prediction is correct the spot price would fall

Arbitragers would ensure that futures price move closely to that of the spot price

If spot prices fall futures are most likely to experience a fall as well

Since the speculator takes a short position he shall benefit from the fall in the futures price

Arbitrage: Overpriced futures: buy spot, sell futures Cost of carry ensures that the futures price

stay in tune with the spot price

If the futures price deviates from the spot arbitrage opportunity arise

E.g. ABC Ltd trading at INR 1000 and ABC Futures trading at INR 1025

Strategies for an arbitrageur ?

Borrow funds at risk free rate and buy the security

Simultaneously, sell the futures at INR 1025

Hold the security till expiry

On expiry the prices will converge

Say on expiry spot price is INR 1015, sell the security. Profit INR 15 from sale in spot position

Futures expire with a profit of INR 10

Overall profit is INR 25 minus the interest cost

Return the borrowed funds

Cost of borrowing must be less than the price differential

What if the futures price is below the spot price?

How would an arbitrager benefit from the opportunity?

Arbitrage: Underpriced futures: buy futures, sell spot

Useful when the Futures are underpriced E.g. ABC Limited trading at INR 1,000.

Near month futures is trading at INR 965.

Strategy: Sell spot Invest in risk free assets Simultaneously, buy futures