23

Design of competitive electricity market in India NCAER

| Date post: | 01-Jan-2016 |

| Category: |

Documents |

| Upload: | reginald-griffith |

| View: | 217 times |

| Download: | 0 times |

Design of competitive electricity market in India

NCAER

Pre-reform structure

Vertical integrated utility (State Electricity Boards)

Regional Load Despatch centres, Transmission utilities (Power grid corporation)

Problems relating to governanceUnder priced supply of electricity to rural areas

Theft and losses prevalent in urban areas

Post reform structure

Separation of generation, transmission and retail businessElectricity Act 2003 enacted

Reforms with a focus on governance

Need for reforms

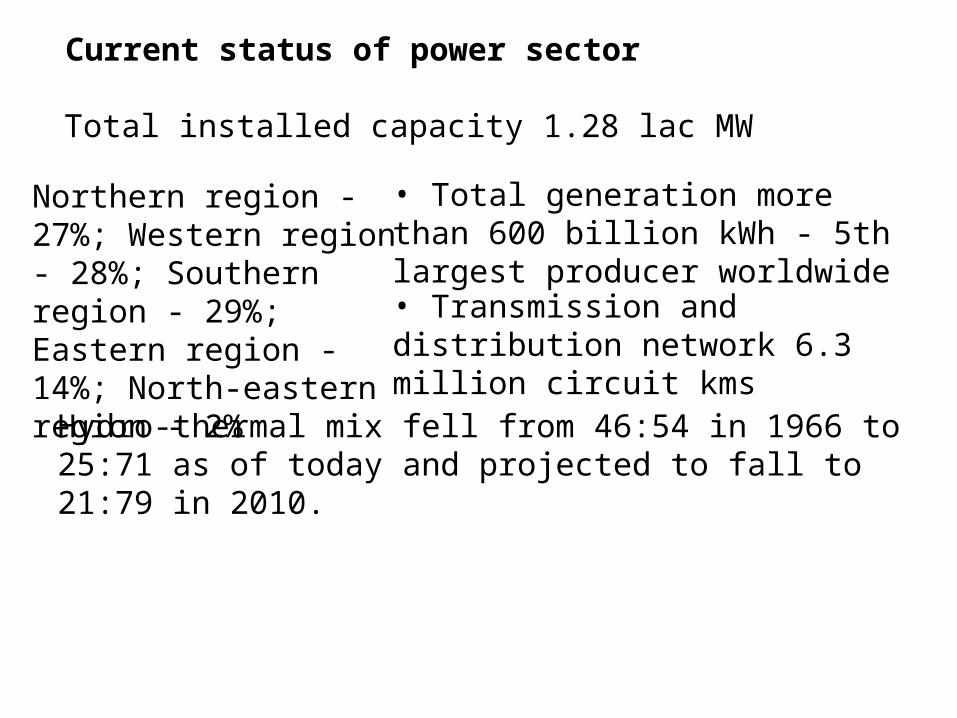

Total installed capacity 1.28 lac MW

• Total generation more than 600 billion kWh - 5th largest producer worldwide

Northern region - 27%; Western region - 28%; Southern region - 29%; Eastern region - 14%; North-eastern region - 2%

• Transmission and distribution network 6.3 million circuit kms

Hydro-thermal mix fell from 46:54 in 1966 to 25:71 as of today and projected to fall to 21:79 in 2010.

Current status of power sector

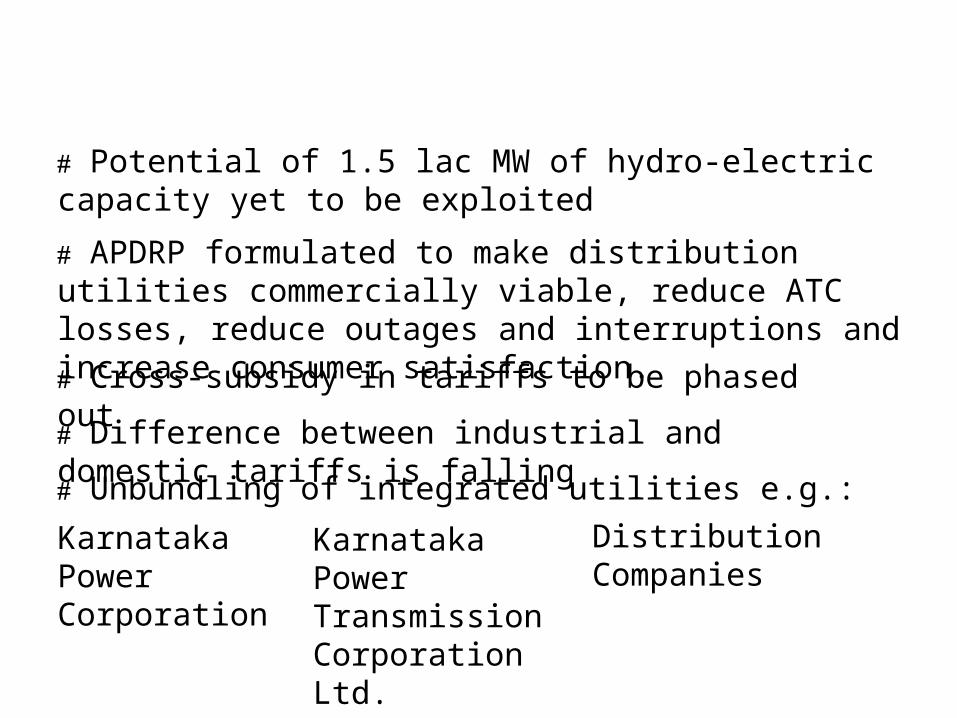

Potential of 1.5 lac MW of hydro-electric capacity yet to be exploited

Cross-subsidy in tariffs to be phased out

Difference between industrial and domestic tariffs is falling

Unbundling of integrated utilities e.g.:

Karnataka Power Corporation

Karnataka Power Transmission Corporation Ltd.

Distribution Companies

APDRP formulated to make distribution utilities commercially viable, reduce ATC losses, reduce outages and interruptions and increase consumer satisfaction.

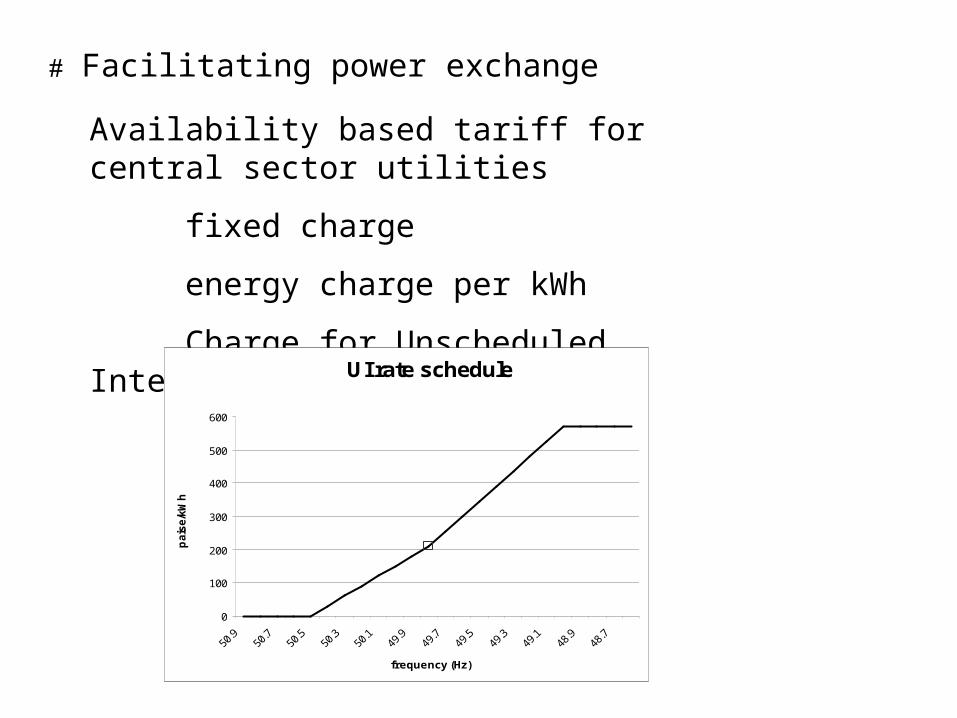

Facilitating power exchange

Availability based tariff for central sector utilities

fixed charge

energy charge per kWh

Charge for Unscheduled Intercharge (UI)

UI rate schedule

0

100

200

300

400

500

600

frequency (Hz)

pais

e/k

Wh

North

West

South

East

North-East950 MW

1650 MW

3000 MW1000 MW

1200 MW

500 MW

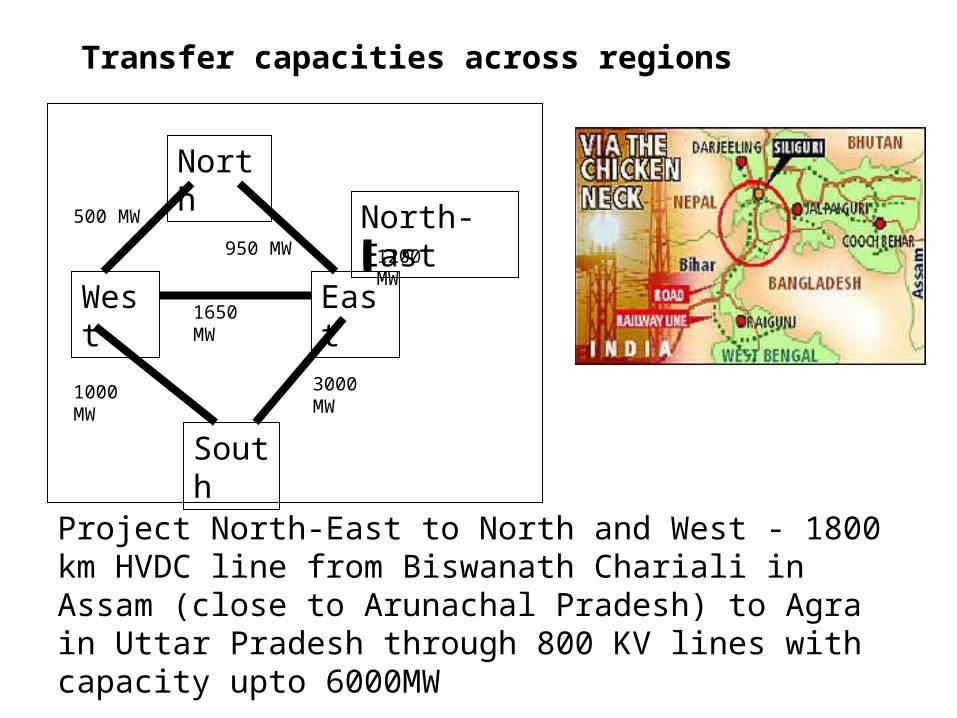

Project North-East to North and West - 1800 km HVDC line from Biswanath Chariali in Assam (close to Arunachal Pradesh) to Agra in Uttar Pradesh through 800 KV lines with capacity upto 6000MW

Transfer capacities across regions

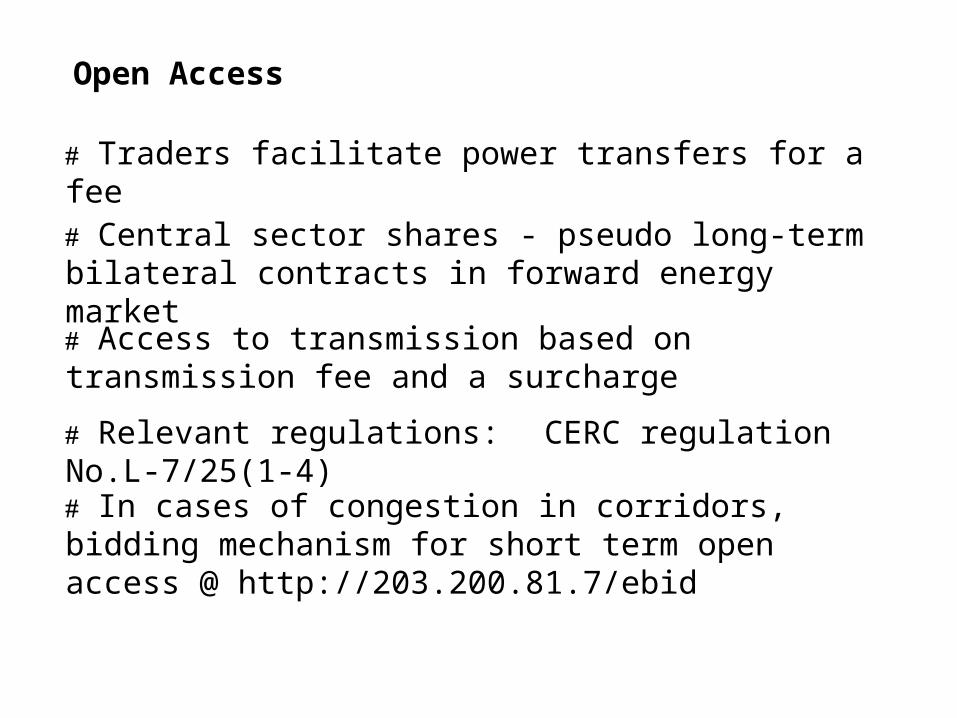

Open Access

Central sector shares - pseudo long-term bilateral contracts in forward energy market

Access to transmission based on transmission fee and a surcharge

Relevant regulations: CERC regulation No.L-7/25(1-4)

In cases of congestion in corridors, bidding mechanism for short term open access @ http://203.200.81.7/ebid

Traders facilitate power transfers for a fee

North-east #

Malda

BongagaonSalakati

Birpara

220 KV 400 KV

DehriMughalsarai

220 KV

SasaramAllahabad

500 MW

Vindhyachal

SingrauliAuraiya

MalanpurKorba

Budhipadar

Rourkela

Raipur

Jeypore

Gazuwaka

Kolar

500 MW

Balimela

Upper Sileru

2000 MW

220 KV

Belgaum

KolhapurChandrapur

Ramagundam

1000 MW

220 KV

400 KV

220 KV

North #

West #

South #

East #

HVDC back-to-back link

HVDC bipole

Existing link

New approved scheme

Legend

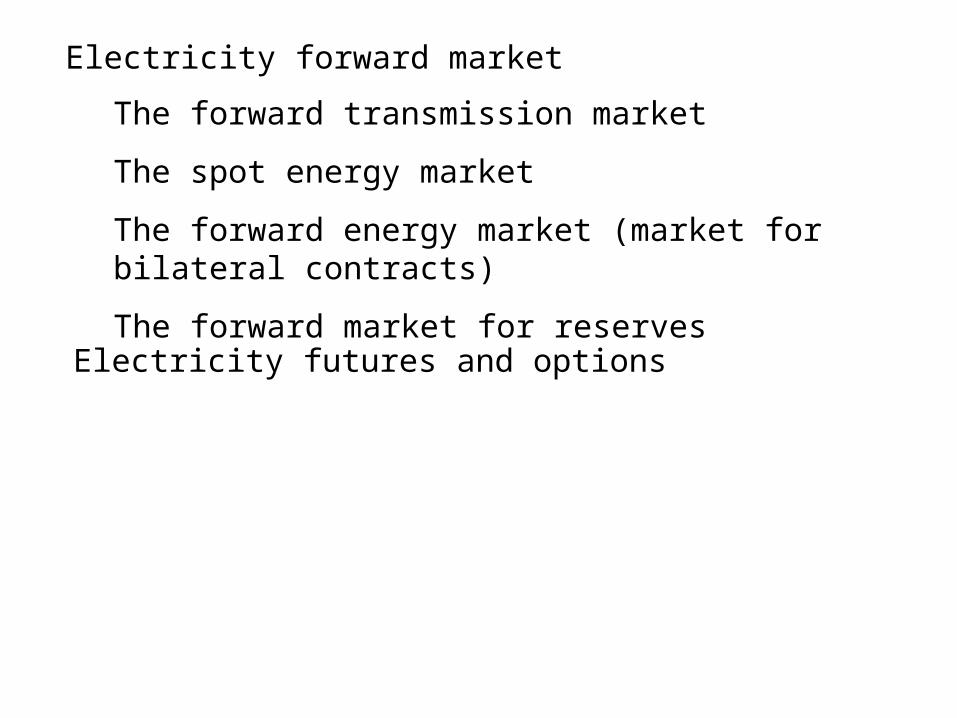

Electricity forward market

The forward transmission market

The spot energy market

The forward energy market (market for bilateral contracts)

The forward market for reserves

Electricity futures and options

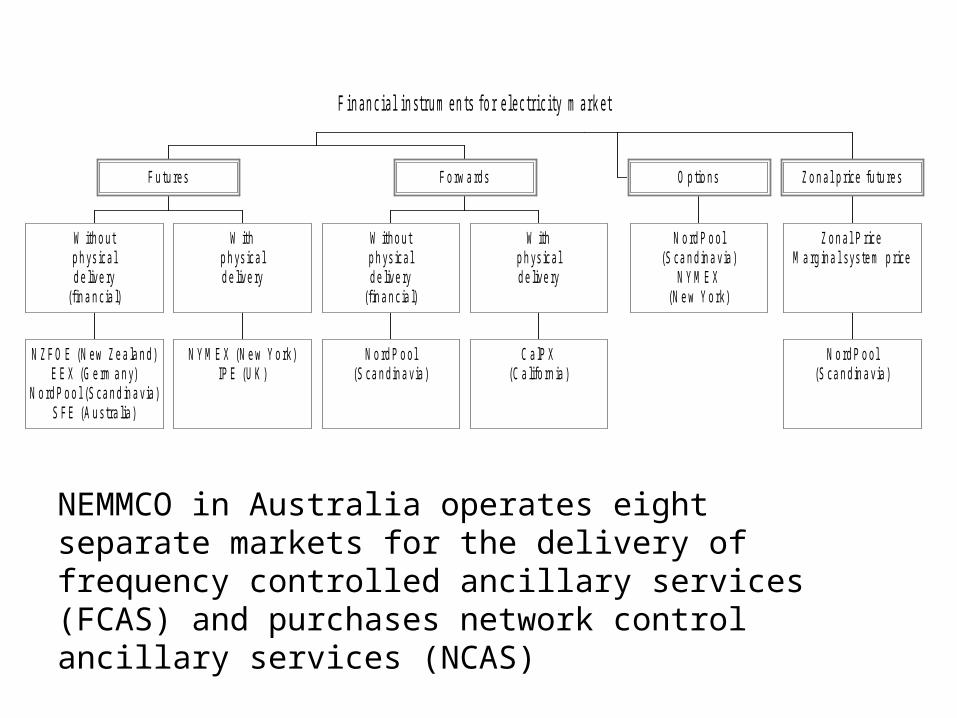

F in a n c ia l in s tru m e n ts fo r e le c tr ic ity m a rk et

N Z F O E (N ew Z e a la n d)E E X (G e rm a n y)

N o rd P o o l (S ca n d in a v ia )S F E (A u s tra lia )

W itho u tp h ys ica ld e live ry

(f in a n c ia l)

N Y M E X (N e w Y o rk )IP E (U K )

W ithp h ys ica ld e live ry

F u tu res

N o rd P o o l(S ca n d in a v ia )

W itho u tp h ys ica ld e live ry

(f in a n c ia l)

C a lP X(C a lifo rn ia )

W ithp h ys ica ld e live ry

F o rw a rds

N o rd P o o l(S ca n d in a v ia )

N Y M E X(N e w Y o rk )

O p tio ns

N o rd P o o l(S ca n d in a v ia )

Z o n a l P riceM a rg ina l s ys tem p rice

Z o n a l p rice fu tu res

NEMMCO in Australia operates eight separate markets for the delivery of frequency controlled ancillary services (FCAS) and purchases network control ancillary services (NCAS)

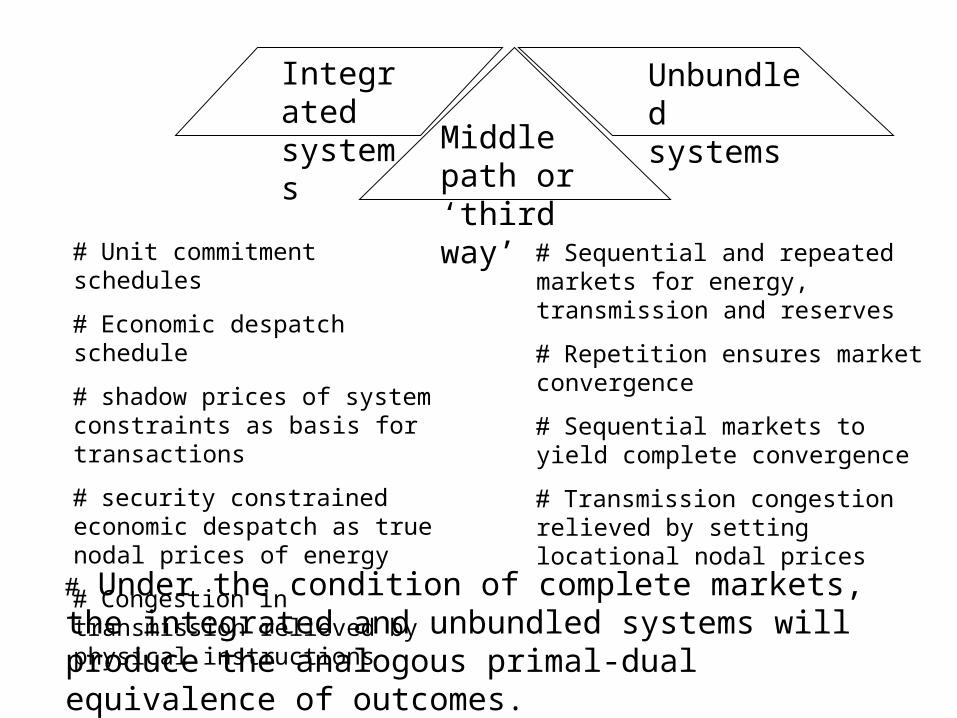

Integrated systems

Unbundled systems

Middle path or ‘third way’

Unit commitment schedules

Economic despatch schedule

shadow prices of system constraints as basis for transactions

security constrained economic despatch as true nodal prices of energy

Congestion in transmission relieved by physical instructions

Sequential and repeated markets for energy, transmission and reserves

Repetition ensures market convergence

Sequential markets to yield complete convergence

Transmission congestion relieved by setting locational nodal prices

Under the condition of complete markets, the integrated and unbundled systems will produce the analogous primal-dual equivalence of outcomes.

Unit Commitment schedule

start up and shut down conditions

spinning reserve

ramp up limits

Power dispatch schedule

real power balance

reactive power balance

Voltage limits

Transmission limits

Energy constraints on hydro plants

Energy markets

Transmission markets

Ancillary markets

“smart” market Decentralised operations

Auctions

First price sealed bid auction Vs Ascending auction

If bidder’s information is independent then all auctions are equally good

Ascending auctions more profitable than standard (first price) sealed bid auctions in expectations if the information is afflicted

Designs should facilitate entry and discourage collusion

Transmission utility pricing and rights

Financial transmission rights (FTRs) or flowgate rights (FGRs) in US as derivatives with values for network transmission capacity in power flow models

FTR holder gets a share of the congestion payment surplus that is received by the ISO when a transmission constraint is binding.

Flowgate rights are linked based transmission rights for hedging transmission risks - settled at the prevailing shadow prices of a security constrained economic despatch model.

Zonal prices in Europe under market splitting mechanism

Power Exchange

Independent System Operator

Day Ahead Market

Real Time Market

Generators Transmission Traders Retailers Distribution

companies

Large consumers

Regulated consumers

Bids

Contracts

Transmission

PE-ISO - A possible structure

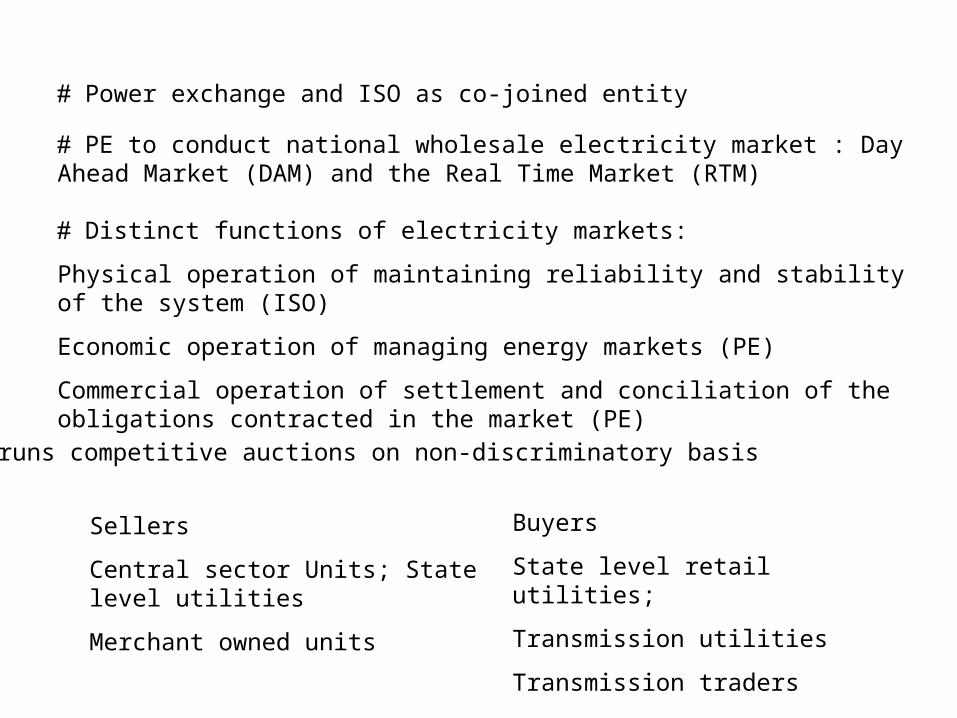

Power exchange and ISO as co-joined entity

PE to conduct national wholesale electricity market : Day Ahead Market (DAM) and the Real Time Market (RTM)

Distinct functions of electricity markets:

Physical operation of maintaining reliability and stability of the system (ISO)

Economic operation of managing energy markets (PE)

Commercial operation of settlement and conciliation of the obligations contracted in the market (PE)

PE runs competitive auctions on non-discriminatory basis

Sellers

Central sector Units; State level utilities

Merchant owned units

Buyers

State level retail utilities;

Transmission utilities

Transmission traders

In event of congestion in transmission corridors, auctions will be held to determine the rights of way

Long term bulk contracts finalised by utilities using multi round auction to get the best deal from wholesale sellers.

Central Transmission Utility as nodal ISO along with five regional transmission

utilities as associate ISOs responsible for regional balancing

At retail level, mostly levelised rate under regulation for core customers

Demand side bidding by load serving utilities in the RTM markets

Bundled generating units precludes any need for state level exchange

Coordination by state transco under the supervision of regional transco

Electricity futures and other derivatives can be developed in conjunction with commodities exchanges in India

Regulation through performance based incentives for generators and transmission traders and levelised tariffs with scope for profits for distribution companies

Constant monitoring of electric market imperfections and inadequacies through appropriate metrics on capacity additions, transmission congestions, etc

Structured tolling contracts as upfront premium paid to plant owner for ability to schedule the operation of the plant

Interruptible load programs

Hedging instruments as insurance schemes for risk management policies

Electricity derivatives

Financial contracts- Contracts for differences in UK and Australian power markets

Physical contracts - Contracts with short maturity period; the PJM power pool market and the energy balancing market operated by CAISO in the US.Electricity futures were first traded on the NYMEX in March 1996Mostly traded in traditional exchangesElectric swaps as financial contracts for fixed price

Electric locational basis swaps

Electricity options and swaps

Plain vanilla electricity call and put options

Options based on attributes like volume, delivery location and timing, quality, and fuel type

Exchange traded energy futures or physical transactions at major power transmission inter ties.

Spark spread options as non-standard cross-commodity electricity options with payment as the difference between the price of electricity sold by generators and the price of the fuels used to generate it

Callable and putable forwards to mimic interruptible supply contracts and the dispatchable independent power producer contracts

Operational details of electricity futures How will it work?

How does the ebid system in the Powergrid website works?