Page 1

Fachbereich Agrarwirtschaft und Lebensmittelwissenschaften

Fachgebiet Landwirtschaftliche Betriebslehre

Prof. Dr. Clemens Fuchs

Master-Thesis

Determinants of Financial Literacy in Rural Areas of Kazakhstan

von

Sholpan Gaisina

Neubrandenburg

März 2016

URN:nbn:de:gbv:519-thesis 2016-0021-5

Page 2

Sholpan Gaisina – Master thesis

Abstract

Much of financial literacy studies is limited to developed economies, there are few

studies considering financial literacy and financial behavior of people in developing

and transition economies. Financial literacy is a crucial problem in both high-income

and poorer countries. Following experiences of rich countries governments in

emerging and developing economies started to pay more attention to this issue.

A main contribution of this study is to extend the literature on financial literacy in

developing and transition countries in a direction which is not yet widely covered,

namely, the rural population financial literacy. This study studied the relation between

financial literacy of rural population in Kazakhstan and determinants, such as

financial experience, presence of financial institutions in the rural areas, socio-

demographic characteristics.

Since the subsistent majority of rural population in Kazakhstan depends heavily on

income from their small subsidiary households the issue of access to formal financial

services becomes of a significant importance. Along with a number of reasons of

being underbanked, a problem of low financial literacy among rural dwellers is one of

the keenest.

Despite some activities undertaken recently by the Kazakhstani government, rural

people still have very limited access to financial education programs; suffer from the

lack of financial experience due to the insufficient presence of financial institutions in

rural areas; have low level of income which is one of the most important impediments

in having access to financial services.

I

Page 3

Sholpan Gaisina – Master thesis

Table of content

Abstract ....................................................................................................................... I

Table of content.......................................................................................................... II

List of figures ............................................................................................................. III

List of tables .............................................................................................................. IV

Abbreviations.............................................................................................................. V

1 Introduction.............................................................................................................. 1

2 Literature review ...................................................................................................... 3

2.1 Definitions of financial literacy........................................................................... 3

2.2 Determinants of financial literacy ...................................................................... 5

3 Country context ....................................................................................................... 8

4 Financial education in Kazakhstan ........................................................................ 10

5 Development of advising centers in rural areas of Kazakhstan ............................. 14

6 Data source and description of variables............................................................... 18

6.1 Data set........................................................................................................... 18

6.2 Sample description.......................................................................................... 20

7 Methodology .......................................................................................................... 28

7.1 Dependent variable ......................................................................................... 29

7.2 Explanatory variables...................................................................................... 30

8 Empirical Results................................................................................................... 32

8.1 Factors affecting financial literacy level........................................................... 32

8.2 Factors affecting credit behavior ..................................................................... 37

8.3 Factors affecting saving rates ......................................................................... 39

9 Discussions ........................................................................................................... 43

10 References .......................................................................................................... 47

II

Page 4

Sholpan Gaisina – Master thesis

List of figures

Figure 1: Number of CKD participants by regions .................................................... 14

Figure 2: Structure of teaching methods at Centers for Knowledge

Dissemination, 2011 ................................................................................................. 15

Figure 3: Structure of CKDs participants, 2012 ........................................................ 16

Figure 4: Distribution of the correct answers among respondents............................ 19

Figure 5: Consumer credit in Kazakhstan................................................................. 27

Figure 6: Distribution of respondents according to the level of savings .................... 40

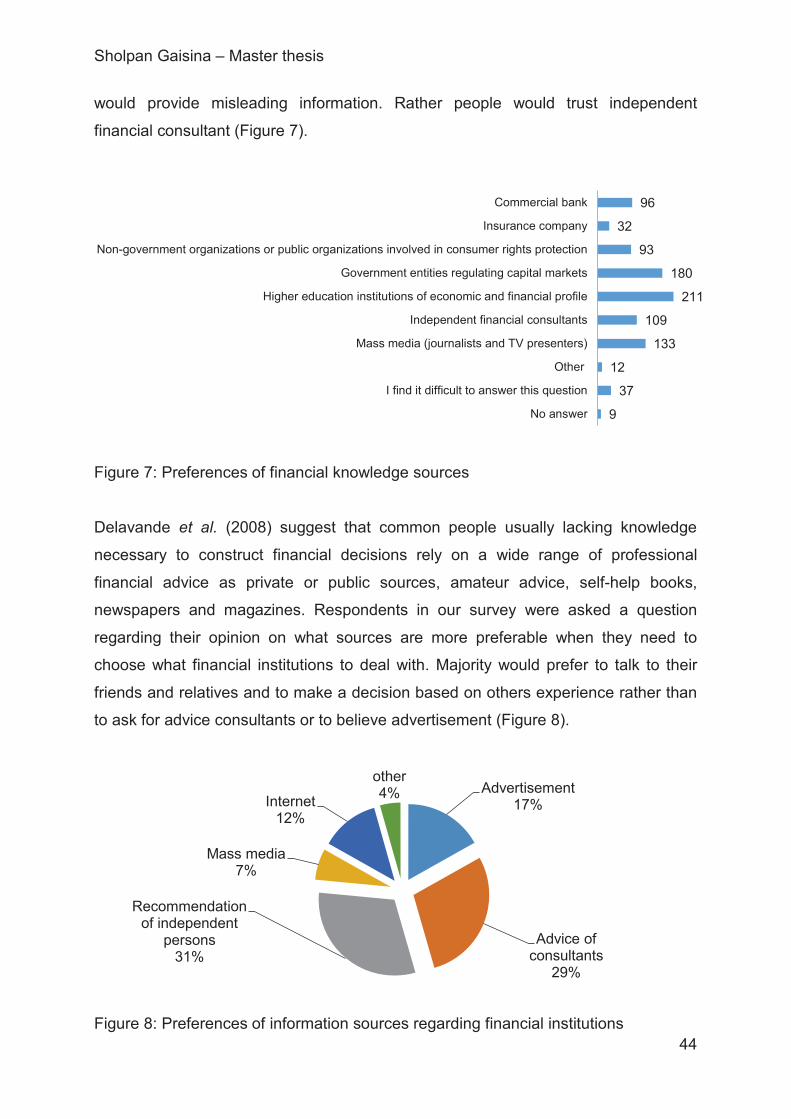

Figure 7: Preferences of financial knowledge sources ............................................. 44

Figure 8: Preferences of information sources regarding financial institutions........... 44

Figure 9: Preference criteria in choosing a financial institution................................. 45

III

Page 5

Sholpan Gaisina – Master thesis

List of tables

Table 1: Stages of institutional formation of consumer protection in financial services

in Kazakhstan ........................................................................................................... 10

Table 2: Results of surveys, in % ............................................................................. 13

Table 3: Self-estimation of financial literacy.............................................................. 21

Table 4: Correlation between objective and subjective literacy level ........................ 21

Table 5: Composition of financial literacy level by gender ........................................ 22

Table 6: Composition of financial literacy level by age groups ................................. 22

Table 7: Composition of financial literacy level by education level ........................... 22

Table 8: Composition of financial literacy level by education level ........................... 23

Table 9: Composition of financial literacy level by education level ........................... 23

Table 10: Composition of sources of financial knowledge by education groups....... 24

Table 11: Composition of sources of financial knowledge by financial literacy

measurement results ................................................................................................ 25

Table 12: Correlation between objective literacy level and financial activity ............. 25

Table 13: Correlation between objective literacy level and financial experience ...... 26

Table 14: Correlation between objective literacy level and number of financial

institutions in the area............................................................................................... 26

Table 15: Ordered probit model results of financial literacy measurement ............... 32

Table 16: Predicted outcomes of correct answers under the variable CREDIT........ 34

Table 17: Predicted outcomes of answers under the variable NUMBERFI .............. 35

Table 18: Predicted outcomes of answers under the variable EMPLOYMENT ........ 36

Table 19: Ordered probit model results of financial behavior towards formal credit . 37

Table 20: Predicted probabilities .............................................................................. 38

Table 21: Ordered probit model results of financial behavior towards savings ......... 40

Table 22: Composition of correct answers on specific questions by gender groups. 43

IV

Page 6

Sholpan Gaisina – Master thesis

Abbreviations

OECD Organization for Economic Co-operation and Development

IMF International Monetary Fund

RFCA Regional Financial Center Almaty

RIOEAReport on CKDs, Research Institute of Organizational and Economics of

Agriculture

CKD Centers for knowledge dissemination

V

Page 7

Sholpan Gaisina – Master thesis

1 Introduction

Financial literacy problem has received rising interest over the past two decades in

both high-income countries and poorer parts of the world (Holzmann, 2010).

Following experiences of rich countries in the development of national financial

literacy policies, governments in emerging and developing economies started their

activities in this area. Much of financial literacy study is limited to developed

economies, there are few studies considering financial literacy and financial behavior

of people from developing and transition economies.

Financial education is beginning to be interested and cared in Kazakhstani society as

a whole. The necessity and importance to be financial literate for Kazakhstani people

have increased significantly due to a number of reasons, among them are those

which were formulated by the Organization for Economic Co-operation and

Development (OECD). OECD emphasizes the emergence of new more complicated

financial products in modern financial markets, significantly increased quantity of

financial products, and specific knowledge required in finance are most important

barriers of making effective decisions making (OECD, 2005), as well as the financial

market being more globalized became increasingly risky for financial decisions

(Lusardi et al., 2011).

Some governmental initiatives in the area of financial education have been launched

recently in Kazakhstan. They include creating a national fund supporting the

promotion of financial education among citizens, funding specifically designed

educational programs for both urban and rural population, and supporting non-

government organizations working in this area. All these activities started very

recently and are on their first stage. Currently in Kazakhstan, a variety of financial

educational programs are offered and different educational materials are available in

many forms. However, most of those programs and material are designed without

considering needs of specific groups of Kazakhstani population.

In Kazakhstan according to the World Bank data, in 2014 some 8.1 million or about

46.7% of the population lived in rural areas and a significant part of the rural

population is officially employed in the agricultural sector, about 36.4% (World Bank,

2015). At the same time agriculture production is a main source of income for the

majority of rural population, for more than 6.5 million rural dwellers. There is a

1

Page 8

Sholpan Gaisina – Master thesis

substantial population of rural unemployed and rural poor whose economic prospects

depend heavily on a reversal in the fortunes of the sector.

Rural households, semi-commercial agricultural entities not legally registered,

produce a large part of agricultural products for the domestic market in Kazakhstan.

Vegetables and fruits (about 80%), meat and dairy production (about 90%) are

dominated by rural households. However, as legally unregistered physical persons,

rural households are excluded from all state supported programs and preferential

state credit lines. On the other hand, the unregistered rural households in many

cases are large enough to be considered as family farms, but they are not motivated

to register and change their status. Nevertheless, these agricultural entities need to

have access to formal financial services to be able to maintain their wellbeing as well

as to increase their productivity and quality. However, as in many other developing

and transition economies, rural population find themselves excluded or dissuaded

from the formal financial sector (Nguyen, 2007).

It is well known that different types of customers have different levels of access to

certain types of financial services and certain types of financial institutions (Hoff et al.,

1990). The problem of limited access to formal financial services by the rural

population is crucial for most developing and transition economies. On the one hand,

formal financial institutions in these economies tend to restrict access to their

products for marginal clientele (in most cases small-scale farmers) (Gonzalez-Vega,

1982). On the other hand, rural population, possessing a low level of basic financial

literacy, is generally unable to demand financial services to suit their needs, or to

take proper advantage of those services that already exist (GIZ, 2014). It is obvious

that people with low financial literacy are more likely to face financial problems

(Lusardi et al., 2010)

A main contribution of this study is to extend the literature on financial literacy in

developing and transition countries in a direction which is not yet widely covered,

namely, the rural population financial literacy. This study studied the relation between

a level of financial literacy of rural population in Kazakhstan and a number of

determinants, such as financial experience, presence of financial institutions in the

rural areas, socio-demographic characteristics.

2

Page 9

Sholpan Gaisina – Master thesis

2 Literature review

2.1 Definitions of financial literacy

Financial markets become more sophisticated consisting of a range of new types of

entities as on-line banks and brokerage firms and constantly offering new financial

products and instruments (OECD, 2005). People must be prepared to make well-

informed financial decision in an increasingly risky and globalized marketplace; it is

true for both developed economies and emerging economies (Lusardi et al., 2011).

Even in developed countries the level of financial literacy of population is reported as

poor and not corresponding to innovative financial products emerging worldwide; a

lack of basic economic and financial knowledge is an important impediment in

effective financial decision-making (Gaurav et al., 2012). Conclusions based on

financial literacy surveys in OECD countries show that understanding financial issues

among people is low, in particular among specific groups, such as less educated and

having low levels of income (OECD, 2006).

Xiao considers financial behavior as human behavior related to money management

which includes budgeting, spending, borrowing, saving and investing, and risk

managing (Xiao, 2008). Individuals who are more financially literal tend to make

fewer mistakes in financial decisions and as a result are in better financial conditions

(Meier et al., 2008).

Hira (2012) believes that financial behavior should be aimed to achieve financial

sustainability when personal and household resources are managed in a manner that

ensures sufficient funds to meet personal financial obligations including dealing with

formal financial institutions and making decisions regarding savings. The financial

behavior is affected by both external and internal factors. Among external factors the

author considers those over which people do not have any direct control, as for the

internal factors, most people have some control over them. Among internal factors

one can consider education, financial skills, income level, and a family size.

There are different definitions of financial literacy presented in literature. According to

Orton (2007) financial literacy is the ability to understand and distinguish financial

options, feel comfortable talking on personal finance topics, make decisions

protecting against future insecurities as well as be prepared to solve every day

financial problems effectively. PRI (2005) considers financial literacy as a concept

3

Page 10

Sholpan Gaisina – Master thesis

that “emphasizes objective knowledge on specific topics related to money,

economics, or financial matters, and subjective measures of self-reported

confidence”. Financial literacy could be also defined as an ability of a person to

understand and process information to be able to make a proper financial decision

(Gaurav et al., 2012). Financial literacy is very often associated with knowledge on

saving and borrowing, which means in turn possessing sound financial management

skills and habits (Hogarth et al., 2002).

When talking about financial literacy, one should keep in mind that it is not about just

individual retirement security, but indeed about the stability of the global financial

system (Lusardi et al., 2011). The financial decisions could range from simple

everyday spending to making choices regarding banking products, investments, and

saving ways (PRI, 2005). It is believed that financial literacy affects financial security,

well-being, and prosperity of people (PRI, 2005). Financial literacy could be

considered from two points of view, the first one is related to the financial knowledge

which includes such things as understanding the concept of interest rate, inflation

rate, different types of loans etc.; the second point related to a confidence component

such as self-estimated level of financial knowledge and self-reported abilities to make

effective financial decisions (PRI, 2004).

There exist very few studies investigating financial literacy and factors affecting the

level of financial literacy in rural areas of transition economies. Most researches are

aimed at the national level without focusing on rural population. Many studies show

that household’s financial behavior is determined significantly by financial literacy

(Lusardi et al., 2013). At the same time being more financially experienced can be a

source of getting financial knowledge and improving financial literacy. Those who

report keeping day-to-day management over their finance and being involved in

some formal financial operations such as formal credit or a deposit account indicate

that this experience is the most important source of financial knowledge (Monticone

et al., 2010).

Even people with limited resources, in particular from rural areas, who would never

afford to have a mortgage or own a big amount of money, need to be able to perform

some financial calculations because their incomes are highly vulnerable and difficult

to be predicted. Such low-income population needs to be financial literate to be able

to make decisions without the expertise of paid consultants (Willis, 2008).

4

Page 11

Sholpan Gaisina – Master thesis

It is generally assumed that financial literacy could change people’s behavior towards

financial services and products, however, as West emphasizes financial literacy does

not provide sustained changes in and optimal of financial behavior (West, 2012).

According to Hogarth (2006) financial education is considered differently by different

people. Some people would esteem themselves as financial educated if they

possess quite broad range of financial knowledge as understanding complicated

macroeconomic issues and their effect of everyday household financial decisions. At

the same time others would focus exclusively on basic routine money management.

However, apparently financial education covers both macro and narrow ranged

topics.

Financially literate people according to Bhushan and Medury (2013) are “… able to

sail through tough financial times” because financial literacy is directly correlated with

positive financial behavior.

2.2 Determinants of financial literacy

Klapper, Lusardi, and Panos (2013) surveyed 160 individuals from seven federal

regions in Russia in 2008 and 2009. A questionnaire included four financial literacy

questions covering interest rate, interest compounding, inflation, and sales discount.

The questionnaire was similar to ones used in studies investigating financial literacy

in the USA and Great Britain. Their findings indicate a significantly positive effect of

financial literacy on the probability of the respondents to have a bank account and to

have formal credit. At the same time financial literacy is negatively correlated to

getting credit from informal sources. This study shows that respondents with higher

financial literacy are more resistant to income shocks and have higher spending

capacity levels.

Rooij et al. (2011) used data from the 2005 De Nederlandsche Bank’s Household

Survey (DHS) containing over 2,000 households. Their questionnaire included two

sets of questions aimed to assess financial literacy of the respondents. The first set

was designed to estimate basic financial literacy and the second one had a goal to

assess more advanced financial knowledge. The results show that lack of literacy

prevents households from participating in the stock market.

Meier and Sprenger (2008) showed that financial knowledge is positively related to

the income level. Monticone (2010) studied 3,992 households using data of a survey

5

Page 12

Sholpan Gaisina – Master thesis

conducted by the Bank of Italy in 2006. The respondents were given questions

regarding financial literacy; results of the analysis indicate that financially wealthy

respondents and those having greater education show higher levels of financial

literacy. In general, the study concluded that the Italian population’s average financial

literacy is quite low compared with the United States and other European countries.

Willis (2008) claims that people’s financial literacy self-assessments measure the

confidence, and apparently overconfidence; however do not provide a robust

measure of actual financial literacy. She says that those individuals who believe in

the effectiveness of their own financial decision making must be able to prove it by

making decisions at hand. Mistaken financial decisions could happen due to both

overconfidence and underconfidence, when people either do not ask for help or to

shy away from engaging in the information search literacy (Willis, 2008). OECD

(2005) reports that respondents in the United States, the United Kingdom, and

Australia often feel that they possess enough financial knowledge than is actually the

case.

According to Lusardi and Mitchell (2011) there is a significant difference in the level

of financial literacy between male and female respondents as well as between

younger/older and middle-aged ones. They showed that respondents with higher

level of education are more financially knowledgeable. Monticone (2010) showed that

there is some evidence of an inverse U-shaped age profile of financial knowledge,

when middle-aged respondents reported higher scores than younger and older

counterparts and also positively related financial experience and the level of financial

literacy; she reports that the respondents consider financial experience as their most

important source of financial knowledge (Monticone, 2010).

Availability of financial services is determined by the availability of financial

institutions in the area. Berry says that the scarcity of bank branches in low-income

and minority neighborhoods prevent some households from being allowed to have an

account (Berry, 2004) and as a result become less financially experience and

knowledgeable. Such so-called “under-banked” or “under-served” people who are

little engaged in the conventional banking system, whose access to information on

even basic financial goods and services is limited (Orton, 2007) have potentially little

financial experience and consequently are less financially educated. Studies show

that in Russia financially literal people are more likely to borrow from formal banking

rather than from informal financial institutions. The authors worn that the rapid growth

6

Page 13

Sholpan Gaisina – Master thesis

of consumer loans in Russia over past several years combined with low financial

literacy of population could lead to the dangerous consequence (Klapper et al.,

2013).

Hogarth et al. (2005) using data from Survey of Consumer Finances for a number of

years conclude that the households’ ability to manage and understand financial

products is an impediment to having bank accounts (Hogarth et al., 2005). They also

indicated that those who lack knowledge regarding the use of specific devices such

as ATMs, personal computers, and mobile phones for banking transactions would

prefer likely informal financial institutions over formal ones (Hogarth et al., 2005).

Studies show that financial literacy is affected by financial behavior and financial

experience emphasizing that the latter can be a source of learning (Monticone,

2010). Monticone also refers to the Michigan Survey of Consumers in 2001

describing a positive influence of personal financial experience on financial

knowledge of respondents, as well as she refers to the study of credit literacy of

Lyons, Rachlis, and Scherpf (Lyons et al., 2007), who found that reported financial

experience had a positive effect on knowledge about credit reports.

Lusardi et al. (2010), using the National Longitudinal Survey of Youth fielded in 2007-

2008, analyzed relationship among financial literacy and a set of socio-demographic

factors, family and peer characteristics. They found that female respondents are less

likely to give correct answers, to the identical results Lusardi and Tufano (2009)

came, studying 1000 respondents in the USA (the survey was fielded by the staff of

Taylor Nelson Sofres Global). This research reports that there is a significant

difference between male and female debt literacy levels. For all the questions in

survey related to financial literacy women gave less correct answers than their male

counterparts (Lusardi et al., 2009).

Christelis et al. (2010) found that individuals with higher education are more

financially sophisticated, as well as the financially wealth respondents are more likely

to become stockholders (Christelis et al., 2010). According to Hogarth (2006) more

educated people could create so-called “economic ripples” making better financial

decision not only for themselves but also for their families (Hogarth, 2006). Calvet et

al (2009) used the Swedish panel covering four years (1999-2002) to investigate

three types of investment mistakes; according to the results respondents with higher

education make smaller investment mistakes (Calvet et al., 2009).

7

Page 14

Sholpan Gaisina – Master thesis

3 Country context

Kazakhstan belongs to a group of upper-middle-income economies with per capita

GDP of about US$ 13000 and with a GDP growth rate of 6% in 2013 which

decreased to 3.9% in 2014 due to recent changes in the world oil market and

economic sanctions in Russia. Poverty in Kazakhstan was estimated to be about 3%

in 2013, as measured by the national poverty line, and about 4% in 2009, as

measured by the PPP approach US$2.5 per capita per day (World Bank, 2015).

Currently agriculture is no longer a leading contributor to the Kazakhstani economy.

Agricultural sector accounts for about 5% of GDP (Ministry of national economy of

the republic of Kazakhstan committee on statistics). The agricultural sector of

Kazakhstan experienced a steep decline in the period since the collapse of the

former Soviet Union. Various agrarian reforms caused a dramatic production

recession in the middle of the 1990s, while further reforms at the beginning of the

2000s became factors of growth. The most important reforms, which have affected

agricultural development, are price liberalization, reorganization of state corporate

farms, mass privatization, and land reforms.

In Soviet times, agriculture in Kazakhstan used to be a sector which received

particular state support. The state provided agricultural producers with fuel, elite

seeds and fertilizers at prices much lower than world market prices. This situation

which was based on absolute state support and artificially set prices and interest

rates has certainly changed during the transition to a market economy.

In 2010 about 2% of rural settlements in Kazakhstan were not provided with electric

power, because of remoteness and low technical conditions, over 11% of settlements

have no automobile communications. The great bulk of agricultural population lives

with limited access to information or in total isolation, 37% of all settlements are not

provided with telecommunication. More than 57% of rural settlements use drink water

from decentralized sources where the quality of water is often not appropriate to

normative parameters. At the lowest level are qualified health services, medicinal

drugs provision, and education. In 2010 medical institutions provided only 83.6% of

rural settlements and only 76.5% of rural settlements had schools. The maintenance

of the agricultural population with communal services lags behind cities: supply with

gas is 25 m3 per capita per month, whereas in cities it is 116.2 m3; daily average

supply with water accordingly 83 and 239 liters (OECD, 2013). Rural poverty dropped

8

Page 15

Sholpan Gaisina – Master thesis

from 59% to 6% for the same period, while urban poverty fell from 36% to 2% (IMF,

2014)

According to official statistics in the mid-1990s each fifth able-bodied agricultural

worker was unemployed, in 2013 the rural unemployed population accounted for

about 42% of total unemployed population in Kazakhstan (the total unemployment

rate in 2013 was 5.2%, in agriculture it was about 21%). Official rural labor statistics

in Kazakhstan is not reliable due to ambiguous treatment of self-employment: a

substantial portion of the rural labor force is recorded as self-employed (IMF, 2014).

Underemployment in agriculture, which was called by statistical agencies as “self-

employment”, reached at that period a rate of close to 70% in rural areas and over

60% in agriculture (Rukowski, 2011). Additionally, low wages in agriculture mean that

being employed does not necessarily protect from poverty. Rural poverty is almost

three times as high as urban, 5% and 1.3% respectively in 2013 (IMF, 2014).

The literacy rate in Kazakhstan is among highest in the world accounting for about

99.8% in 2009 (UNESCO, 2009). According to the Education for All (EFA) 2013-14

Global Monitoring Report, Kazakhstan’ policies in education are aimed at further

strengthening of formal education (UNESCO, 2014). Access to primary and

secondary education is very high and accounts for 91% of net enrolment rate with the

net attendance ration of 98% (UNICEF, 2015).

9

Page 16

Sholpan Gaisina – Master thesis

4 Financial education in Kazakhstan

Financial education is beginning to be interested and cared by the Kazakhstani

government and Kazakhstani society as a whole. The National Bank of Kazakhstan

starting in 2001 paid attention to the protection of financial services consumers’

rights. A special department established in 2001 has been several times reorganized,

nevertheless keeping its leading role as last resort for protection rights of financial

services consumers in Kazakhstan (Table 1).

Table 1: Stages of institutional formation of consumer protection in financial services

in Kazakhstan

Year State institutionsNon-state

institutions

2001-2004National Bank of Kazakhstan. The department of

financial services surveillance/ The department of

consumer protection in financial services.

No

2004-2011

The Agency of the Republic of Kazakhstan on

financial market and financial organizations

regulation and surveillance.

The department of financial services surveillance/

The department of consumer protection in financial

services.

Insurance

ombudsman

2011-2012The Committee on financial organizations control

and surveillance. The department of consumer

protection in financial services.

Insurance

ombudsman

Bank

ombudsman

29.12.2012The Committee on consumer protection in financial

services.

Insurance

ombudsman

Bank

ombudsman

Source: Chusnutdinova, 2013

In 2011, as a stage of the reforming process in this area and according to the decree

of the President of the Republic of Kazakhstan of December 29, 2012 No. 458 "On 10

Page 17

Sholpan Gaisina – Master thesis

some questions of National Bank of the Republic of Kazakhstan" the Committee on

protection of the rights of financial services’ consumers under the National Bank of

the Republic of Kazakhstan was created. The Committee was designed to secure

proper protection of the rights and interests of financial services consumers and

services of micro-financial entities (Presidential Decree, 2013).

Among other tasks, the Committee is responsible for the development of specific

instruments aimed to improve financial education of Kazakhstani citizens. These

instruments include such activities as carrying out explanatory work by means of

mass media resources, the Committee’s website, holding trainings and meetings with

financial services’ consumers. The Committee publishes articles in the central

republican newspapers, mainly on topics related to collateralized real estate court

sale procedure, mortgage lending, mandatory insurance, consumers and financial

services investors’ protection. Also the Committee representatives are interviewed by

the central republican TV Company on such topics as:

a. Fines and penalties for failure to comply with terms and conditions of a bank

loan agreement (overdue liabilities) and the restriction of interest;

b. Banking commissions under a bank loan agreement;

c. Out of court sale of the collateralized property;

d. Getting pensions and state benefits by plastic cards;

e. How to choose a pension fund?

The Committee’s web-site, www.fingramota.kz (finliteracy), is an informational-

educational web-site, which provides basic knowledge for using financial instruments,

managing personal savings, evaluating risks. The web-site includes such subsections

as “Fundamentals of financial literacy”, “Financial glossary”, “What a customer should

know?”, the information is placed on three languages Kazakh and Russian

(Committee for the Control and Supervision, 2013).

In 2008 “Informational and educational centers” (Centers) for population began to

operate in all regions and cities Astana, Almaty and Semei. Centers provide free of

charge seminars and consulting for population and have covered more than 360,000

people from all over the country, 2.7% of adult population (RFCA, 2015). Additionally,

in 2009, a TV training talk show “Vash vykhod” (Your solution) was launched on a

weekly basis. The Program touches such issues as banking, pension, insurance, and

11

Page 18

Sholpan Gaisina – Master thesis

securities market. Participants of the talk show are people with real stories, experts,

and analysts.

A number of surveys on the national level aimed at measuring financial literacy of

Kazakhstani population were conducted. According to the RFCA (Regional Financial

Center Almaty), survey about 40% of respondents never had any experience dealing

with financial instruments and only 8% reported to have a deposit account in the

bank.

In 2013 the non-governmental fund “International Centre of Economic Literacy”

(ICEL), the first non-governmental organization in Kazakhstan in the sphere of

financial literacy, was founded. The main goal of this NGO is to improve financial

literacy of Kazakhstani people taking into account particularities of social-economic

development of the country as well as to protect rights of consumers of financial

services using mass media means. One of its first projects ICEL was a large-scale

research on the level of financial literacy of Kazakhstan’s population in early 2014.

According to the data based on a survey conducted in all 14 regions of Kazakhstan

as well as in Almaty and Astana cities, around 44% of the Kazakh population prefers

to keep their savings at home; around 38% of respondents do not keep record of

family budget while 43% of the respondents were not aware of deposit insurance

mechanisms. Only 6% of respondents were aware of the maximum value of the

deposits insured and 63% admitted that they usually ran out of money before next

salary payments (Interfax-Kazakhstan, 2015). The results of the survey says that

about 44% indicated their financial literacy level as satisfying to be able to make

decisions related to formal financial services. However, according to the data 67% of

respondents believes that they would not face any punishments if they would fail to

meet the legal obligations of a formal loan and 50% indicated that they do not plan to

pay their loans back (Nuraichan, 2014). The available data on Kazakhstani

population financial literacy and own data based on the survey in Pavlodar region

undertaken in 2014 are summarized in Table 2.

12

Page 19

Sholpan Gaisina – Master thesis

Table 2: Results of surveys, in %

RFCA

survey

ICEL

survey

Pavlodar

region,

rural areas,

own survey

Used any type of financial services 62.5 72

Used any type of formal loans 32 65

Used consumer loans 52

Have a deposit account 8.5 8 3

Keep savings at home 44 21

Save exclusively in livestock 37

Do not keep records on family budget 55 38 37

Self-estimation of financial literacy as

high44 69

Sources of financial knowledge

TV programs 36.9 8

Internet resources 24.3 15

Newspapers 20

Consultancy 23 27

Special training and workshops 17.1 23

Sources: RFCA, NFDFS, Own calculations

In November 2014 the National Fund for the Development of Financial Services

(NFDFS) in Kazakhstan has been founded. The goals of the NFDFS are to help

financial services consumers to realization their rights and legal interests, “… to

monitor quality of services provided by banks and financial organizations, to study

financial services market and to explain legislation related to financial services”

(inform.kz, 2015).

13

Page 20

Sholpan Gaisina – Master thesis

5 Development of advising centers in rural areas of Kazakhstan

According to the National Plan on Realization of "Strategy of Kazakhstan-2050", as a

task of top priority the improvement of knowledge and professional skills of

Kazakhstani people was indicated. This issue is particularly important for rural areas.

The government undertook a number of measures to create an information and

advisory system in rural areas (Agribusiness 2020, 2012).

Since 2009, JSC "Kazagroinnovation” (KAI), entirely state-owned company, aiming to

implement modern achievements in agricultural sector and distribute highly effective

technologies, started a project designed to create a system of knowledge distribution

and transfer. A model called "Extension”, used widely in the USA and other

developed countries, has been used as an example. According to this model,

advising centers initially supported by the state subsequently should become either

entirely or partly independent. Within this pilot project a network of “Centers for

knowledge dissemination” (CKDs) was created. CKDs are attached to research

institutes in each region. The CKDs along educational goals are aimed to be involved

into assessment of specific needs of rural people in order to improve understanding

of rural population demand for extension/training/advisory service (Fileccia et al.,

2010). Currently there are eight centers (RIOEA, 2012) in such regions as Akmola,

Almaty, Kostanay, Southern Kazakhstan, Karaganda and Eastern Kazakhstan

(Figure 1).

Figure 1: Number of CKD participants by regions

Source: RIOEA, 2012

406

80127

5 25 5 84

317

94153

22 1 7 15

252

17

125

5 250

50100150200250300350400450

2009 2010 2011

14

Page 21

Sholpan Gaisina – Master thesis

CKDs conduct training (up to 5 days) on the premises either of research institutes,

agricultural enterprises or using own infrastructure. Major activities of CKDs include:

a. Research based training;

b. Practical instructions;

c. Improvement of existing knowledge;

d. Scientific conferences and workshops.

During 2009 more than 1700 persons engaged in agricultural production were trained

at the CKDs. The major source of funding is a national budget. There are a number

of problems the CKDs faced:

a. Lack of sufficient equipment and teaching technologies for conducting

trainings;

b. Lack of well-developed manuals and training materials;

c. The content of trainings does not always meet the needs of trainees;

d. Underdeveloped monitoring system;

e. Low interest from agricultural producers and their passiveness (Yespolov et

al., 2012).

Scientific and practical seminars include three components (RIOEA, 2012):

theoretical part, practical part, and demonstration of practical experience (Figure 2).

The topics meet the major needs of agricultural producers and are formulated taking

into account results of special analytical researches.

Figure 2: Structure of teaching methods at Centers for Knowledge Dissemination,

2011

Source: RIOEA, 2012

theoretical49%

practical27%

demonstration24%

15

Page 22

Sholpan Gaisina – Master thesis

During three years since CKDs were created, 259 workshops for agricultural

producers were held. International lecturers/experts from Canada, Germany,

Australia, Syria, and Russia were invited for 25 seminars to teach participants and

promote new ideas. Along with on place trainings, distance consultations via Internet

and call centers started in July, 2010 in eight agricultural research institutes. Since

the beginning of call-centers activity over 2700 phone consultations were made, while

direct consultations are carried out on the basis of applications from agricultural

producers. Direct consultations include individual and group consultations. The

service of the CKD is purposed mainly on farmers and farm staff (RIOEA, 2012),

however, the participation is not limited by agricultural producers, civilian officers from

rural districts and subsidiary small households are also provided with services by

CKDs (Figure 3).

Figure 3: Structure of CKDs participants, 2012

Source: RIOEA, 2012

CKDs consist of three main branches:

a. Administrative

b. Educational

c. Supporting

Administrative staff is responsible for organizing workshops, inviting lecturers,

attracting participants. Educational branch is represented by lecturers, who are

responsible for preparing study programs, handouts, and manuals.

Farmers51%

Farm staff18%

Local authority19%

others12%

16

Page 23

Sholpan Gaisina – Master thesis

The number of consultants annually increases, in 2011, twelve research institutes

and 18 consultants worked in the project. For comparison, in 2010 four institutes and

seven consultants were involved into this activity.

Along with the internal efforts to develop a network of CKDs, there is also an external

support in this activity. "The International German agrarian center", which started

functioning in Kazakhstan in 2011, has as a main goal promoting advanced

European agricultural technologies and equipment in Kazakhstan. The center along

with the main goal attracts attention of foreign companies operating in agriculture to

Kazakhstani "Extension system". The center conducts various trainings for farmers

and demonstrates German agricultural machinery and technologies.

One more state owned company, JSC “Fund of financial support of agriculture”

among other activities undertakes efforts to increase financial literacy of rural

population in Kazakhstan. Through micro-credit organizations created in rural areas

about 100,000 rural people were trained in 2008-2009.

Despite state programs aimed to improve the situation with access to knowledge by

rural people in agriculture of Kazakhstan, a large number of small agricultural

producers, in particular rural households are still underserved, in particular as for

getting financial knowledge. Moreover, the current banking system is not favorable to

a large majority of rural population, specifically to those whose income comes

exclusively from rural households. The lack of basic knowledge in financial area

makes access to formal financial services and financial instruments significantly

difficult. At the same time, better financial literacy of consumers will definitely improve

the performance of financial services providers who “… have a responsibility to

understand their market, and respond with a range of appropriate and affordable

services” (Cohen, 2011).

17

Page 24

Sholpan Gaisina – Master thesis

6 Data source and description of variables

Since the subsistent majority of rural population in Kazakhstan depends heavily on

income from their small subsidiary households, which are mainly producing for

commercial purposes, the issue of access to formal financial services becomes of a

significant importance. Along with a number of reasons of being underbanked, a

problem of low financial literacy among rural dwellers is one of the keenest.

A main objective of our study is to determine and measure factors which affect the

financial literacy level of rural households in Kazakhstan.

6.1 Data set

The sample consists of rural people and therefore it is of particular interest for the

research questions concerning financial literacy, because rural people in Kazakhstan

are in a very vulnerable financial position.

To measure basic financial literacy the questions adopted from the “Supplementary

Questions: Optional Survey Questions for the OECD INFE Financial Literacy Core

Questionnaire” (OECD, 2012) were used. In the questionnaire three questions were

included:

1. Suppose you had USD 100 in a savings account and the interest rate was 2%

per year. After 5 years, how much do you think you would have in the account

if you left the money to grow?

a. More than USD 102

b. Exactly USD 102

c. Less than USD 102

d. no answer

2. Imagine that the interest rate on your savings account was 1% per year and

inflation was 2% per year. After 1 year, how much would you be able to buy

with the money in this account?

a. More than today

b. Exactly the same

c. Less than today

d. no answer

18

Page 25

Sholpan Gaisina – Master thesis

3. A 15-year mortgage typically requires higher monthly payments than a 30-year

mortgage, but the total interest paid over the life of the loan will be less.

a. True

b. False

c. no answer

Those who were not able to give an answer or gave the wrong ones account for 20%

of asked individuals, only 64% demonstrated an understanding of interest rate

concept and only 12% can answer a simple question about inflation. Those who

could give a correct answer on a question regarding mortgage account for 46%. In

general, respondents with one, two, or three correct answers account

correspondently for 42%, 34%, and 4% (Figure 4).

Figure 4: Distribution of the correct answers among respondents

We investigated what and to what extent factors characterizing financial experience,

education, socio-demographic status, and the representativeness of financial

institutions determine the level of financial literacy of respondents. The study is based

on a static model with cross-sectional data for a specific year (2014).

The study uses data from rural areas of Kazakhstan. The study took place in

Pavlodar region of Kazakhstan in spring 2014. Based on the survey we were able to

acquire information for 405 individuals living in villages of four rural districts located in

different distances from the city. The surveys collected information on individual

050

100

150

200

frequ

ency

0 1 2 3

19

Page 26

Sholpan Gaisina – Master thesis

levels of financial literacy (knowledge of interest rate, understanding of inflation, and

understanding of mortgage), as well as information on financial services (the use of

bank accounts and formal credit). The information covers such areas as: whether the

respondent has any experience dealing with formal financial institutions, a measure

of the objective and subjective financial literacy, their income situation. The dataset

provides information on respondents’ socio-demographic characteristics and their

opinion regarding financial education. This survey has questions concerning whether

the individual has got a loan from a formal financial institution for last five years,

information on keeping records of the family budget, as well as a question on the

respondents’ opinion what should be the primary attention when someone compares

the banks in order to choose to take credit from or to make deposit in.

6.2 Sample description

The percentage of female respondents is 52.3%; it corresponds to the national level

of 51.85% in 2013. The average age in the sample is around 40. Households with 3-

4 family members make up 45% and with more than four members is 26.7%. The

percentage of formally employed respondents is around 61%, self-employed

respondents make up about 6.7%, while others including retirees, students and

housewives make up about 30% of all the respondents.

The literacy level of respondents is high enough, 42.96 % have tertiary education and

45.2% have secondary education. According to the World Bank statistics, in

Kazakhstan a secondary education enrollment rate in 2012 was 97.1%, while the

tertiary enrollment rate was 44.53%.

Among respondents with secondary and tertiary education majority of respondents is

formally employed, 56.3% and 71.8% respectively. However, among those who

indicated their status as unemployed the respondents with secondary education

make up the biggest share of 54.6%.

The respondents were asked to provide self-measurements of their financial

knowledge. Most respondents assessed their financial knowledge being above

average: 32.84% of respondents stated their level is 3; 25.93% that their level is 4

and 10.86% that their level is 5. At the same time, only 6.67% reported they do not

have any knowledge in finance. Most importantly, there is no strong correlation

between objective and subjective literacy (Table 3).

20

Page 27

Sholpan Gaisina – Master thesis

Table 3: Self-estimation of financial literacy

FINLITSELF Frequency Percent Cumumulative

0 27 6.67 6.67

1 37 9.14 15.8

2 59 14.57 30.37

3 133 32.84 63.21

4 105 25.93 89.14

On average, 63.95% of respondents correctly answered the question on interest rate;

12.1% correctly answered the question on inflation; and 46.4% correctly answered

the question on mortgage payments. However, 20% of respondents were not able to

provide correct answers.

We can rank respondents who provide correct answers to at least two financial

literacy questions as the ‘‘high’’ financial literacy respondents, a fraction of such

respondents is 34.1%. It was expected that the fraction of those who gave correct

answers to all three questions is small enough, in our survey it is 4.2% of all the

respondents.

We can observe the moderate relationship between measures of financial literacy

and a subjective measure of financial knowledge (Table 4).

Table 4: Correlation between objective and subjective literacy level

ANSWERS FINLITSELF

ANSWERS 1.0000

FINLITSELF 0.1535 1.0000

Financially literate respondents are more likely to be female, out of those who

provided correct answers on two questions 38.51% are female and 29.53% are male

(Table 5).

21

Page 28

Sholpan Gaisina – Master thesis

Table 5: Composition of financial literacy level by gender

No answerOne correct

answer

Two correct

answers

Three correct

answers

female 17.92 39.15 38.21 4.72

male 22.28 44.56 29.53 3.63

The most financially literate respondents’ age is between 25 and 54 years old (Table

6).

Table 6: Composition of financial literacy level by age groups

No answerOne correct

answer

Two correct

answers

Three correct

answers

16-24 12.35 9.47 7.25 23.53

25-34 14.81 22.49 26.09 17.65

35-44 22.22 33.14 34.78 17.65

45-54 22.22 21.89 26.09 23.53

55-64 23.46 10.65 2.9 17.65

65+ 4.94 2.37 2.9 0

Financially literate respondents are more likely to have secondary/technical

education or tertiary education, respectively, 45.65% and 46.38 of those who gave

correct answers on two questions (Table 7).

Table 7: Composition of financial literacy level by education level

Education No answerOne correct

answer

Two correct

answers

Three correct

answers

Tertiary 39.51 41.42 46.38 47.06

Post secondary/

technical School43.21 45.56 45.65 47.06

22

Page 29

Sholpan Gaisina – Master thesis

Table 7: Composition of financial literacy level by education level (continuous)

High School 14.81 9.47 7.25 5.88

Middle School 2.47 2.37 0.72 0

Primary School 0 1.18 0 0

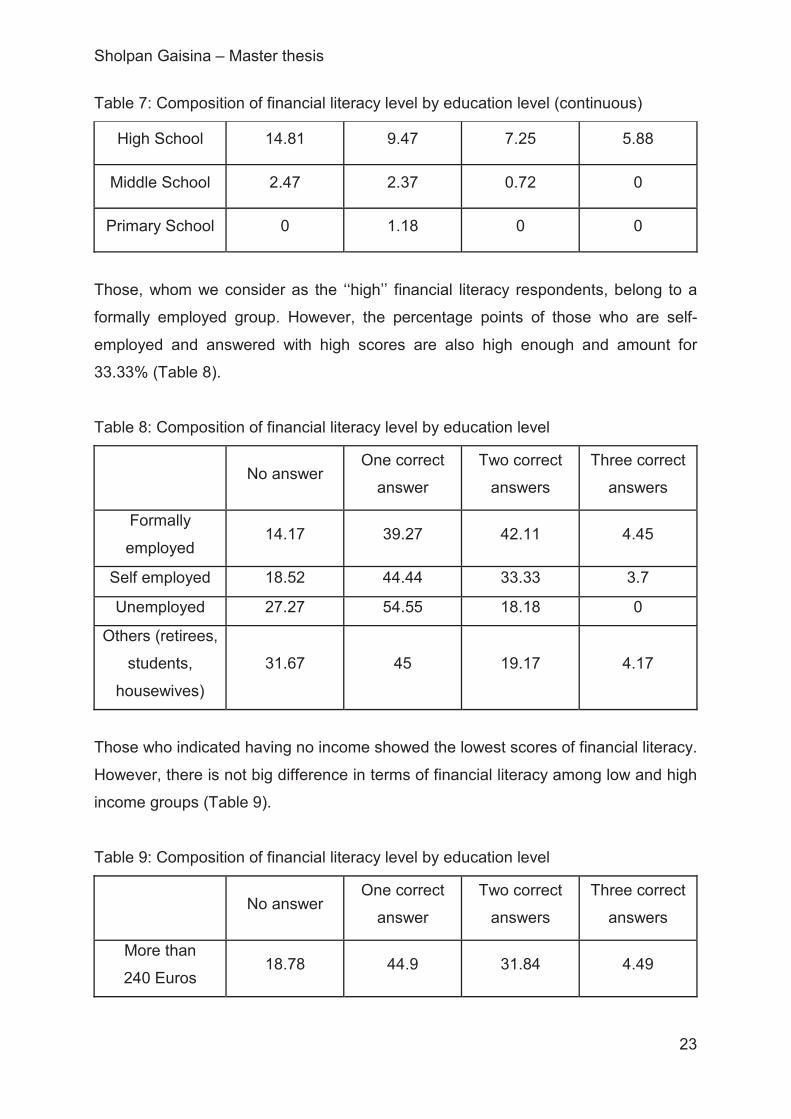

Those, whom we consider as the ‘‘high’’ financial literacy respondents, belong to a

formally employed group. However, the percentage points of those who are self-

employed and answered with high scores are also high enough and amount for

33.33% (Table 8).

Table 8: Composition of financial literacy level by education level

No answerOne correct

answer

Two correct

answers

Three correct

answers

Formally

employed14.17 39.27 42.11 4.45

Self employed 18.52 44.44 33.33 3.7

Unemployed 27.27 54.55 18.18 0

Others (retirees,

students,

housewives)

31.67 45 19.17 4.17

Those who indicated having no income showed the lowest scores of financial literacy.

However, there is not big difference in terms of financial literacy among low and high

income groups (Table 9).

Table 9: Composition of financial literacy level by education level

No answerOne correct

answer

Two correct

answers

Three correct

answers

More than

240 Euros18.78 44.9 31.84 4.49

23

Page 30

Sholpan Gaisina – Master thesis

Table 9: Composition of financial literacy level by education level (continuous)

Less than

240 Euros20.26 37.25 38.56 3.92

No income 57.14 28.57 14.29 0

Respondents with tertiary education indicated that they prefer to use information

obtained from independent sources not affiliated with any financial institution, 43.1%.

At the same time respondents from the group with secondary and high school level

would rely mostly on consultants of the financial institutions. It means respondents

with higher level of education consider this issue as not simple and the wrong

decision would in the future create some troubles and problems. The third group with

lower level of education would make their decision regarding the choice of the

financial institution based on advertising. It could mean that less educated people

from rural areas either possess a deep mistrust of paid advice or consider this

decision as risk-free and not worth to be paid for. For all three groups such sources

of information as press and internet are of low attractiveness (Table 10).

Table 10: Composition of sources of financial knowledge by education groups

Advertise-

ment

Advice of

consultants

Recommen-

dation of

independent

persons

Mass

mediaInternet Other

Tertiary 17.8 32.8 43.1 7.5 17.8 4.0

Post-

secondary/

High

School

19.4 35.6 33.3 8.6 12.6 6.3

Middle

School/

Primary

School

77.8 22.2 0.0 0.0 11.1 0.0

24

Page 31

Sholpan Gaisina – Master thesis

Regardless whether the respondent gave a correct answer and regardless how many

correct answers were given, the majority of respondents would rather follow the

advice provided either by an official consultant or by an independent advisor than rely

on advertisement or mass media and internet. People from rural areas prefer to make

the decision on what financial institution to choose based on a personal talk and

personal advice (Table 11).

Table 11: Composition of sources of financial knowledge by financial literacy

measurement results

Advertise-

ment

Advice of

consultants

Recommen-

dation of

independent

persons

Mass

mediaInternet Other

No correct

answer23.5 25.9 38.3 9.9 13.6 6.2

One correct

answer20.1 33.1 36.1 8.3 16 2.4

Two correct

answers19.6 39.1 35.5 7.2 14.5 8

Three

correct

answers

5.9 41.2 47.1 0 11.8 5.9

Looking at the association between financial literacy and financial activity for last five

years, we observe a moderate positive association (Table 12).

Table 12: Correlation between objective literacy level and financial activity

ANSWERS FINSERV5YEARS

ANSWERS 1.0000

FINSERV5YEARS 0.1452 1.0000

25

Page 32

Sholpan Gaisina – Master thesis

Financial inclusion in our analysis is measured with two variables, the first one is

CREDIT, and this variable indicates whether the respondent used ant type of credit

within last five years (Table 13).

Table 13: Correlation between objective literacy level and financial experience

ANSWERS CREDIT

ANSWERS 1.0000

CREDIT 0.1844 1.0000

We can observe a moderate positive association between financial literacy and a

number of finical institutions operating in the area NUMBERFI, representing a second

variable characterizing financial inclusion. In the questionnaire respondents were

asked to indicate whether they have in their area following financial institutions:

branches of commercial banks, post offices, ATMs, Rural Credit Partnerships, Micro

Credit Organizations, Insurance companies (Table 14).

Table 14: Correlation between objective literacy level and number of financial

institutions in the area

ANSWERS NUMBERFI

ANSWERS 1.0000

NUMBERFI 0.1583 1.0000

We did not use in our analysis such a variable as a deposit account, since such a

variable would not show the real inclusion of the respondent into the financial activity.

In Kazakhstan almost all the formally employees are provided by the employer with a

so-called salary account in the assigned bank. This account is used exclusively to

withdraw the salary and cannot be used for other financial activities.

Despite we collected information on a number of credits obtained by the respondents

during the last five years, for analysis we constructed a single variable indicating for

all types of credits. However, it is interesting to notice that about 52% of the

respondents used a consumer credit, which is one of the most popular types of credit

among Kazakhstani population due to the short term nature of such lending. On the

other hand, only 2.5% of respondents reported on the mortgage. This type of credit is

26

Page 33

Sholpan Gaisina – Master thesis

less popular among rural population, since almost all the rural inhabitants possess

own house or apartment (Figure 5).

Figure 5: Consumer credit in Kazakhstan

Source: http://www.tradingeconomics.com/kazakhstan/consumer-credit

27

Page 34

Sholpan Gaisina – Master thesis

7 Methodology

The study tries to answer the following question:

a. What is the relationship between financial literacy and provision of financial

services?

b. What is the relationship between demographic characteristics of age, family

status, education, financial experience and financial literacy?

c. How does financial literacy affect the probability that a respondent receives

credit from the formal financial institution?

d. Whether the financial literacy level affects savings rate of respondents?

Following hypotheses are formulated, based on the questions and objectives of the

research:

H 1. Following Klapper et al. (2013) we assume that financial literacy is positively

related to participation in financial markets.

H 2. Following Lusardi and Mitchell (2011) we suppose that here are significant

differences between men and women in financial literacy.

H 3. Following Monticone (2010) we expect that there is a positive significant

relationship between financial literacy and age.

H 4. Following Christelis et al. (2010) we expect that higher level of education

would lead to higher scores of financial literacy measurements.

H 5. Following Beryy (2004) we expect that the higher representativeness of

financial institutions leads to higher financial literacy.

H 6. Our assumptions that there is a positive relationship between objective and

subjective financial literacy we based partly on conclusions made by Willis

(2008).

H 7. Following Hogarth et al. (2005) we hypothesize that there is a positive

relation between an ability to manage own finance and financial literacy.

H 8. We assume that financial literacy has a significant impact on saving rates, as

financial skills and knowledge enable people to make more substantive

financial plans and wiser allocation of their financial resources (Mahdzan,

2013).

28

Page 35

Sholpan Gaisina – Master thesis

We use ordered probit model to investigate the relationship between financial literacy

and socio-economic factors.

7.1 Dependent variable

To answer above research questions and prove the hypothesis three analyses were

undertaken.

In the first analysis we summarized information about financial literacy resulting from

three questions and used it as a dependent variable coded “ANSWERS” varying from

category “0” meaning that the respondent either did give a correct answer or did not

know the correct answer till a category “3” meaning that the respondent gave corrects

answers on all three questions.

In the second analysis as a dependent variable we used information regarding credit

taken by a respondent for past five years. The variable “CREDIT” is varying as

follows: “0” – no credit, “1” – got credit.

The third analysis considers the dependence of saving rates on some factors

including the level of financial literacy. The respondents were asked to indicate the

savings rate answering a question “What is your average monthly savings (if any) in

percentage to the income?” They had the following options:

a. 0%

b. 1-5%

c. 6-10%

d. 11-15%

e. 16-20%

f. 21-25%

g. above 25%

The variable “SAVINGRATE” was coded as “0” – no savings, “1%-5%” – 1, “6%-10%”

– 2, “11%-15%” – 3, “16%-20%” – 4, “20%-25%” – 5, and “ above 25%” – 6.

29

Page 36

Sholpan Gaisina – Master thesis

7.2 Explanatory variables

A choice of explanatory variables was based on recommendations of Kempson

(2009) as well as studies of Lusardi et al. (2010 and 2011), Klapper et al. (2013).The

explanatory variables include:

a. a set of variables measuring financial inclusion and financial experience of the

respondents: whether the respondent had credit from the formal financial

institution for last five years, whether the respondent has such a habit in

his/her family to keep records on the family budget, and how many formal

financial institutions are available in the area;

b. a set of variables characterizing socio-demographic status of the respondent,

such variables as gender, age, educational level, type of employment, and a

family size;

c. a variable indicating a level of financial literacy based on individual’s self-

estimation

d. and the income level of a respondent (Kempson, 2009).

We used eleven independent variables (predictors) for three regressions:

a. GENDER – a binary variable, where “0” - male and “1” – female.

b. AGE – a discrete variable grouped into six levels: 16-24; 25-34; 35-44; 45-54;

55-64; older than 65

c. EDUCATION – a discrete variable grouped into five levels: Tertiary = 1; Post-

secondary/technical school = 2; High School = 3; Middle School = 4; Primary

School = 5.

d. CREDIT – a binary variable that refers to the respondent’s having or nor

having got a credit for last five years: with credit = 1; without credit = 0.

e. DEPOSIT – a binary variable that refers to the respondent’s having or nor

having a deposit account at the formal financial institution for last five years:

with deposit = 1; without deposit = 0.

f. RECORDS – a binary variable that refers to the respondent’s keeping

regularly records on family budget: yes – 1; no - 0

30

Page 37

Sholpan Gaisina – Master thesis

g. EMPLOYMENT – a discrete variable grouped into five levels: formally

employed – 1; self-employed – 2; unemployed – 3; others (including retirees

and students) – 4.

h. NUMBERFI – a continuous variable that measures the number of financial

institutions available in the area without determining what kind of institution.

i. FINLITSELF – a continuous variable that measures the level of financial

literacy ascending from “0” to “5.”

j. FAMILY – indicates a family size, is a continuous variable that measures the

number of family members

k. INCOME – indicates monthly income per household (including all the

sources), is a discrete variable grouped into five levels: less than 50,000 KZT

– 1, 50,000-70,000 KZT – 2, 71,000-100,000 KZT – 3, 101,000-150,000 KZT –

4, more than 150,000 KZT – 5

l. DISTANCE – a continuous variable that measures the distance from the

settlement to a nearest financial institution, km.

31

Page 38

Sholpan Gaisina – Master thesis

8 Empirical Results

8.1 Factors affecting financial literacy level

We see that all 405 observations in our data set were used in the analysis. The

likelihood ratio chi-square of 55.6 with a p-value of 0.0000 tells us that our model as a

whole is statistically significant, as compared to the zero model with no predictors.

Table 15: Ordered probit model results of financial literacy measurement

ANSWERS Coef Std. Err. p - value

GENDER 0.244** 0.112 0.029

AGE -0.09* 0.046 0.05

EDUCATION

2 0.134 0.122 0.272

3 -0.044 0.208 0.832

4 -0.012 0.439 0.979

5 0.259 0.783 0.741

CREDIT 0.333*** 0.120 0.006

RECORDS 0.289* 0.213 0.175

EMPLOYMENT

2 -0.233 0.223 0.295

3 -0.427 0.351 0.224

4 -0.446*** 0.130 0.001

NUMBERFI 0.181*** 0.063 0.004

FINLITSELF 0.077* 0.042 0.069

Notes: * a significance level of 10%, ** a significance level of 1%, *** a significance

level of 0.5%

Almost all variables are significant at different levels (Table 15). Only one of nine

variables is not significant, however, a sign of this variable meets our expectations. A

variable EDUCATION is not significant. We can explain it by the fact the overall

literacy level in Kazakhstan, including rural areas, is greater than 99%. Moreover, the

literacy level in Kazakhstan does not mean merely an ability to read and to write, but

32

Page 39

Sholpan Gaisina – Master thesis

a particular level of education. Therefore, the education of respondents is not directly

corresponding to the financial literacy. However, the sign of this variable is negative,

which means that the log odds of being in a group with higher answer scores would

decrease as the level of education of the respondent would decrease too.

The variables AGE has a negative sign and a significance level of 10%, it means we

can expect a decrease in the log odds of being in a group with higher answer scores

by 0.08 when the respondent‘s age is increasing.

Being a female increases log odds of being in a group with higher answer scores.

We believe that having some experience of dealing with formal financial institutions

as well as keeping records of the households’ income and expenditure could mean

that the respondent has some level of financial literacy. We expected these variables

to be significant. The variable CREDIT is significant at the level of 0.5% and the

variable RECORDS is significant at the level of 10%.

We can observe a link between financial literacy and some type of financial

behaviors. We found a strong dependence of financial literacy on whether the

respondent had any type of credit over past five years. We would say that for a one

unit increase in CREDIT (i.e., going from 0 to 1), we expect a 0.34 increase in the log

odds of being in a higher level of answer scores, given all of the other variables in the

model are held constant. Also, we found that keeping day-to-day financial

management by a household would positively affect financial literacy, with a one unit

increase in RECORDS (i.e., going from 0 to 1), we expect a 0.32 increase in the log

odds of being in a group with higher answer scores.

A variable EMPLOYMENT is significant at the level of 0.5% for a group of retirees,

students and housewives and insignificant for the groups of self-employed and

unemployed. At the same time, the variable has a negative sign for all the groups. It

means being in a group of retirees and students in comparison with formally

employed respondents, will decrease by 0.44 in the log odds of being in a group with

a higher level of answer scores, given that all of the other variables in the model are

held constant. Formally employed respondents in comparison with other employment

groups provide better scores.

The number of financial institutions located in the area is a significant variable at the

level of 0.5% and positively affects the dependent variable. Going towards greater

number of financial institutions would increase the log odds of being in a group with

higher answer scores by 0.18.

33

Page 40

Sholpan Gaisina – Master thesis

The financial literacy self-estimation is significant at the level of 10% and has a

positive sign. For a one unit increase in the financial literacy self-estimations, we

would expect a 0.07 increase in the log odds of being in a higher level of answer

scores, given that all of the other variables in the model are held constant.

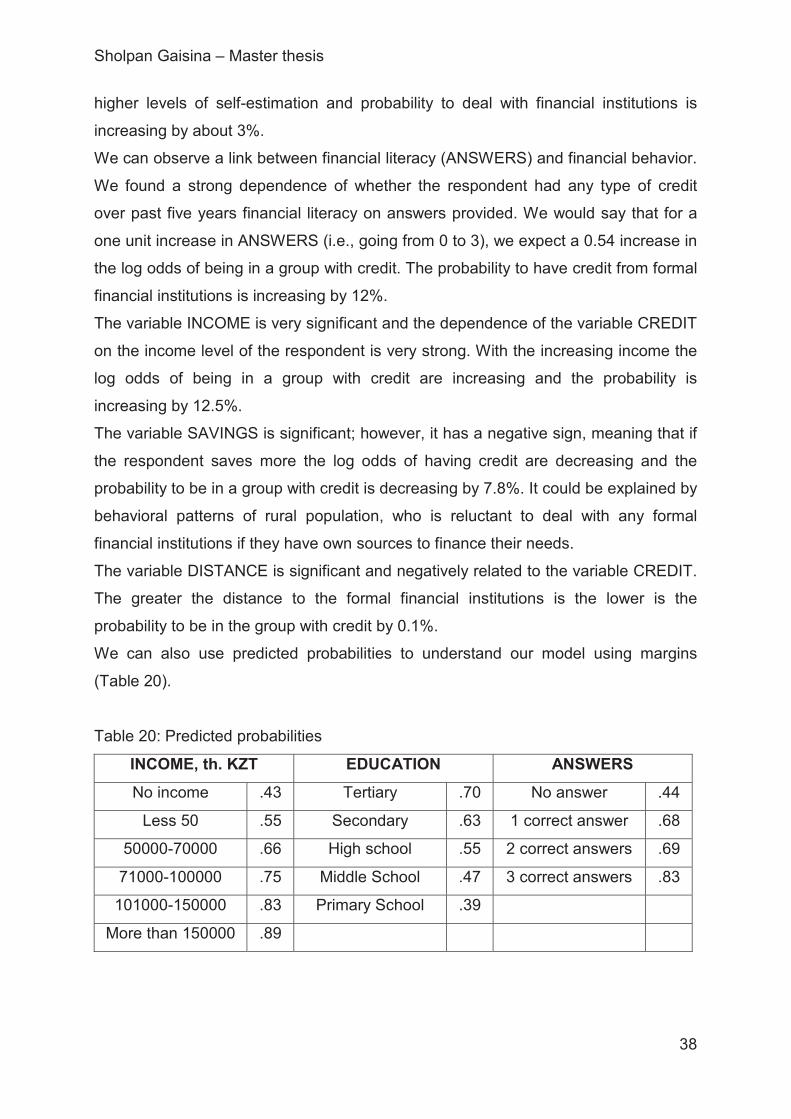

We also obtained predicted probabilities to be able to observe how the probabilities

of belonging to each category of answer scores change as the variable CREDIT is

varied holding the other variables at their means (Table 16).

Table 16: Predicted outcomes of correct answers under the variable CREDIT

CREDIT Margin Std. Err. z p - value

Predicted outcome = 0, not correct answers

1 0.245 0.033 7.410 0.000

2 0.151 0.020 7.350 0.000

Predicted outcome = 1, one correct answer

1 0.466 0.027 17.360 0.000

2 0.433 0.026 16.600 0.000

Predicted outcome = 2, two correct answers

1 0.271 0.032 8.450 0.000

2 0.375 0.028 13.420 0.000

Predicted outcome = 3, three correct answers

1 0.019 0.007 2.840 0.005

2 0.041 0.011 3.840 0.000

As we can see, the predicted probability of being in the category with no correct

answers is 0.25 for the respondent who did not get any type of credit from the formal

financial institutions over past five years and 0.15 if the respondent indicated having

credit. It means those who had some financial experience, the probability to five now

correct answers is lower. For the category of respondents who provided one correct

answer, the predicted probabilities are 0.46 and 0.43, indicating an insignificant

difference between those respondents with and without credit. At the same time, for

the respondents from the group with two correct answers the predicted probabilities

are 0.27 for the respondents without credit and 0.37 for ones who had it. It means

those respondents who dealt with financial institutions during the past five years the

probability to give either two correct answers is higher than for those who did not 34

Page 41

Sholpan Gaisina – Master thesis

have such an experience. Respectively, the predicted probability to provide three

correct answers is greater for those with some financial experience, 0.04 in

comparison to those without any experience, 0.02.

As the variable NUMBERFI (number of financial institutions in the area varying from 1

financial institution to 3 different financial institutions) is varied the predicted

probabilities of being in each category of answer scores is as follows (Table 17).

Table 17: Predicted outcomes of answers under the variable NUMBERFI

NUMBERFI Margin Std. Err. z p - value

Predicted outcome = 0

0 0.250 0.035 7.170 0.000

1 0.196 0.021 9.260 0.000

2 0.150 0.021 7.310 0.000

3 0.112 0.025 4.420 0.000

Predicted outcome = 1

0 0.467 0.027 17.410 0.000

1 0.457 0.026 17.330 0.000

2 0.434 0.026 16.520 0.000

3 0.401 0.033 12.240 0.000

Predicted outcome = 2

0 0.265 0.033 8.070 0.000

1 0.320 0.024 13.160 0.000

2 0.375 0.028 13.220 0.000

3 0.428 0.040 10.630 0.000

Predicted outcome = 3

0 0.018 0.007 2.710 0.007

1 0.027 0.008 3.600 0.000

2 0.041 0.011 3.860 0.000

3 0.060 0.018 3.330 0.001

We can see that the predicted probability increases for the categories of 2-3 answer

scores as number of financial institutions in the area of residence increases. At the

same time the fewer financial institutions in the area the greater the probability of not

providing any correct answers. 35

Page 42

Sholpan Gaisina – Master thesis

As the variable EMPLOYMENT is varied the predicted probabilities of being in each

category of answer scores is as follows (Table 18).

Table 18: Predicted outcomes of answers under the variable EMPLOYMENT

EMPLOYMENTDelta-method

Margin Std. Err. z p - value

Predicted outcome = 0

Formally employed 0.144 0.020 7.120 0.000

Self employed 0.180 0.020 9.190 0.000

Unemployed 0.221 0.025 8.980 0.000

Others (retirees, students,

housewives)0.268 0.036 7.460 0.000

Predicted outcome = 1

Formally employed 0.429 0.026 16.530 0.000

Self employed 0.449 0.026 17.290 0.000