Page 11 International Journal of Accounting & Business Management www.ftms.edu.my/journals/index.php/journals/ijabm Vol. 3 (No.2), November , 2015 ISSN: 2289-4519 DOI: 10.24924/ijabm/2015.11/v3.iss2/11.28 This work is licensed under a Creative Commons Attribution 4.0 International License. Research Paper DETERMINANTS OF FINANCIAL WELL-BEING FOR GENERATION Y IN MALAYSIA Sing Chie Tie, FTMS Alumni, FTMS Global Cyberjaya Master of Business Administration Email: [email protected]Dr. Ismail Nizam, Head of MBA Programs, School of Accounting and Business Management, FTMS Global Malaysia, Cyberjaya Email: [email protected]Abstract The purpose of this study is to identify the determinants that influence the state of financial well- being of Gen-Y in Malaysia. This study is done in response to a recent study by Asia Institute of Finance (2015) that discovers Gen-Y Malaysians have a mediocre financial literacy score. This study begins by understanding what the Asia Institute of Finance (2015) study discovers and who the Gen-Ys are. As there has not been a defining approach to determine financial well-being, this study adopts the measure of financial satisfaction as a proxy to it. Once the independent variable financial satisfaction and its independent variables; financial knowledge, financial management, financial planning, financial situation and financial status are being put into context, a survey consisting of Likert scale question on the aforementioned independent and dependent variables are sent to 206 Gen-Ys across Malaysia. The regression result concludes that financial knowledge and financial planning are two determinants that influence the financial satisfaction of Gen-Y Malaysians. There is no significant influence of financial management, financial situation and financial status on financial satisfaction. This study contributes to the bodies of research which have determined financial literacy, which both financial knowledge and financial planning is part of, to have an impact on an individual’s financial satisfaction. Key Terms: Financial Well-being, Financial Satisfaction, Financial Knowledge, Financial Management, Money Management, Financial Planning, Financial Situation, Financial Problem, Financial Status, Financial Habits, Financial Attitudes, Financial Behaviours, Financial Literacy, Millennials, Generation-Y, Malaysia 1. Introduction There has been a growing interest in the world in exploring how financial well-being contributes to a fulfilling life (Hira & Mugenda, 1998; Xiao, et al., 2008; Robb & Woodyard, 2011; Ali, et al., 2015; Taft, et al., 2013). In Malaysia alone, numerous studies by academia (Loke, 2015; Taft, et al., 2013; Ali, et al., 2015) and trade publications (Asian Institute of Finance, 2015;

Transcript

Page 11

International Journal of Accounting & Business Management

Abstract The purpose of this study is to identify the determinants that influence the state of financial well-being of Gen-Y in Malaysia. This study is done in response to a recent study by Asia Institute of Finance (2015) that discovers Gen-Y Malaysians have a mediocre financial literacy score. This study begins by understanding what the Asia Institute of Finance (2015) study discovers and who the Gen-Ys are. As there has not been a defining approach to determine financial well-being, this study adopts the measure of financial satisfaction as a proxy to it. Once the independent variable financial satisfaction and its independent variables; financial knowledge, financial management, financial planning, financial situation and financial status are being put into context, a survey consisting of Likert scale question on the aforementioned independent and dependent variables are sent to 206 Gen-Ys across Malaysia. The regression result concludes that financial knowledge and financial planning are two determinants that influence the financial satisfaction of Gen-Y Malaysians. There is no significant influence of financial management, financial situation and financial status on financial satisfaction. This study contributes to the bodies of research which have determined financial literacy, which both financial knowledge and financial planning is part of, to have an impact on an individual’s financial satisfaction.

1. Introduction There has been a growing interest in the world in exploring how financial well-being contributes to a fulfilling life (Hira & Mugenda, 1998; Xiao, et al., 2008; Robb & Woodyard, 2011; Ali, et al., 2015; Taft, et al., 2013). In Malaysia alone, numerous studies by academia (Loke, 2015; Taft, et al., 2013; Ali, et al., 2015) and trade publications (Asian Institute of Finance, 2015;

Price WaterhouseCoopers, 2015) have been done to explore the extent and influence of financial literacy on the Gen-Y in the country. It has been a subject of much conversation in the media and the nation’s policy has been structured in no small part to influence a positive growth on the national’s level of financial literacy (Bank Negara Malaysia, 2011). The Gen-Y – a cohort of people born between the years 1977 – 1998 is a huge population worldwide. The Department of Statistics Malaysia (2015) forecasts based on the 2010 national census, that the Gen-Y population in Malaysia will amount to 13 million which is about 44% of the total population with Price Waterhouse Coopers (2009) estimating that Gen-Y constitutes of about 62% of Malaysia’s workforce. However, the Gen-Y in Malaysia is not in a financially good shape. A recent survey by Asian Institute of Finance (AIF) (2015) on over 1,000 Gen-Y in Malaysia revealed that the cohort have a poor level of financial literacy. The report shows that 58% of them rate themselves as having average financial knowledge with 28% saying that they are confident in handling daily money management activities. An article from the local newspaper – The Star (2015) supports the statement stating that Gen-Y in Malaysia are being declared bankrupt due to inability to pay their loans. The Credit Counselling and Debt Management Agency (AKPK) is asking credit card and education loan defaulters to approach them for loans payments restructuring (Credit Counselling and Debt Management Agency, 2015a). AKPK also reports (2015b) that year-on-year, the number of Malaysians having borrowing repayment issues have increased by 11% in 2015. This study acknowledges that there are much efforts needed to be done in the field of enhancing financial literacy of Gen-Y in Malaysia and shifts the focus to determining how the Gen-Y are coping with their current financial affairs; their financial well-being. This study sets out to 1) understand how financial literacy affects the financial well-being of Gen-Y in Malaysia, 2) discover if current financial status has any impact on financial well-being and 3) how the current financial situation that they are facing with today affects them. This study begins with a review on extant literature on the field of financial literacy, the components that affect financial well-being and who the Gen-Y are. A conceptual framework will be proposed with the research designs and methodology used to explore the questions that this study seeks out to answer. Finally, the results of this study will be analysed and discussed. This study will conclude with some proposals and enhancements we can take to enhance our understanding on financial well-being. 2. Literature Review A well-being in a person’s life is subjective. However, it is positively related to how an individual copes with its mental and physical health, his job performance (or business ventures), his personal relationship with the people around him as well as his marital status (Sirgy, et al., 2006). This study narrows down this broad topic of life well-being to explore just one component of it – the financial well-being. Sufficient studies and extant literature have shown that financial well-being has an effect on a person’s life well-being (Hira & Mugenda, 1998; Xiao, et al., 2008; Robb & Woodyard, 2011; Ali, et al., 2015; Taft, et al., 2013). However, these studies have not been conclusive on a single agreed approach to measure financial well-being of an individual (Joo & Grable, 2004; Robb & Woodyard, 2011; Gerrans, et al., 2014). All these studies concur that financial well-being is subjective and it is dependent on contexts and circumstances as perceived by the individual to bring a certain level of satisfaction. Financial well-being, or its proxy term – financial satisfaction, is also fluid and it is, at its best, a snapshot of an individual’s perception on the subject matter as time goes by. These contexts and circumstances are dependent on demographic and socio-economic factors as well as the components of financial literacy. It is well established that the components of financial well-being are interdependent (Joo & Grable, 2004; Huston, 2010; Robb & Woodyard, 2011; Taft, et al., 2013; Ali, et al., 2015).

Page 13

2.1 Financial Satisfaction Hira & Mugenda (1998) frames financial satisfaction as an individual’s perception of happiness and contentment that are derived from effective practices of financial skills to achieve one’s financial goal through the right attitudes and behaviours. It is referred to as financial distress by Joo & Grable (2008) when it is observed from a different perspective. Taft, et al. (2014) calls it financial concerns. Regardless, all three terms point to a similar definition. Extent studies on the subject matter is usually conducted with surveys focusing on financial attitudes and behaviours (Xiao, et al., 2008; Ali, et al., 2015; Duh, 2016). 2.2 Financial Literacy Financial literacy is perhaps one of the most studies subject in the field of personal finance. Many attempts by extent literature and studies to define the term but none has been universally accepted as definitive. Huston’s (2010) extensive attempt to review key publications on financial literacy have enabled her to summarises financial literacy as having multiple common terms such as financial knowledge and financial education. This study will subscribe to the term financial literacy as a measure of the level of an individual’s understanding and the articulation of key financial concepts and can be objectively explained in two distinct components: i) conceptually and ii) operationally (Remund, 2010). The concept of financial literacy is a measure of the level of an individual’s understanding and the articulation of key financial concepts (Remund, 2010). Huston (2010) considers this knowledge dimension as financial knowledge. Financial literacy is achieved operationally through four broad financial activities – saving, borrowing, investing and budgeting which Atkinson and Messy (2011) refers to as the application of financial knowledge and skill. This can be further categorised into financial management and financial planning skills (Muske & Winter, 1998; Reasie, et al., 2001). The component that integrates both the conceptual and operation aspects of financial literacy is the attitude and behaviour of the individual towards financial matters (Huston, 2010; Remund, 2010; Atkinson & Messy, 2011). High financial literacy score have a positive impact towards an individual’s financial well-being (Loke, 2015; Taft, et al., 2013; Ali, et al., 2015). However, Schmeiser and Seligman (2013) posit that a financial literacy score do not have any influences over an individual’s financial well-being in the long term since the score is a snapshot of an individual’s level of financial literacy during the time of assessment. They suggest that longitudinal data on the respondents of the financial literacy survey is a better predictor of individual’s financial well-being. 2.2.1 Financial Knowledge This study adopts Huston’s (2010) definition of financial knowledge as the knowledge dimension of financial literacy. These include the concept of money, debt management, interest compounding and rates, inflation, investment strategies and financial products or tools. Individuals who are financially knowledgeable tend to be more financially responsible (Hilgert, et al., 2003; Monticone, 2010; Robb & Woodyard, 2011; Joo & Grable, 2004). The sources of financial knowledge include formal education, such as primary, secondary school or college courses, seminars and training classes as well as from informal education such as the influence from parents, friends and work. In addition to that, individuals also gain financial knowledge through personal experiences either through observation or active participation in financial activities (Hoch & Ha, 1986). 2.2.2 Financial Management and Financial Planning Good financial management contributes to financial well-being (O’Neill, et al., 2000; Albeerdy & Ghareghi, 2015). Financial management relates to managing cash flow, borrowing,

Page 14

saving and the balance between them. Individuals who have good financial management habit are more prudent in their spending, invest better and can manage their financial well (Rooij, et al., 2011a). Financial management skill will be most effective with proper financial planning. Malaysia Financial Planning Council (2004) defines financial planning as the utilisation of savings for wealth accumulation, followed by the preservation of such wealth against value depreciation, losses and finally distribution of wealth during the final stages of life. It is through effective financial planning with an adequate mastery of financial management skill that an individual can reach financial well-being (Ali, et al., 2015). Good financial management and financial planning are also subject to and influenced by an individual’s financial attitude and behaviour (Huston, 2010; Remund, 2010; Atkinson & Messy, 2011). 2.2.3 Financial Attitude and Behaviour An individual’s financial knowledge and attitudes determine an individual’s financial behaviours (Perry & Morris, 2005; Britt, et al., 2013; Lusardi & Mitchell, 2014). Vice versa is also true as attitudes and behaviours also empower individuals to seek more financial knowledge and skills. Individuals with adequate financial knowledge are also more self-directed and make conscious financial decisions on their own (Perry & Morris, 2005; Joo & Grable, 2004). Robb & Woodyard’s (2011) study concludes that financial attitudes and behaviour are both more correlated to the income level of individuals than by financial knowledge. Studies have also discovered that individuals from households with large financial assets are more receptive towards increasing their financial knowledge (Monticone, 2010; Robb & Woodyard, 2011; Luksander, et al., 2014). The perception of current financial situation of individuals also has a correlation to how one behaves (Hira & Mugenda, 1998; Joo & Grable, 2004; Wiener & Doescher, 2008). 2.3 The Gen-Y As this study focuses on the Gen-Y, it is crucial the cohort’s identity and characteristics are understood so that the results can be interpreted accurately. The definition on when the Gen-Y begins and ends has not been agreed upon by academia. FINRA (2014) and Broadbridge, et al. (2007) consider those born between the years 1978 to 1994 as Gen-Y while Kumar & Lim (2008) categorises those born in between 1980 to 1994. The Council of Economic Advisers of United States (2014) puts those born in between 1980 to 2004 as Gen-Y instead. This study will adopt the age range of between the years 1977 – 1998 as proposed by Cudmore, et al. (2010 cited in Harland Clarke, 2008). The cohort is also given other alternative names. USA Today (2005) calls them Generation Y but majority of publications (Deal, et al., 2010; Cudmore, et al., 2010; The Council of Economic Advisers of United States, 2014; Smith & Nichols, 2015; Asian Institute of Finance, 2015; PriceWaterhouseCoopers, 2015) refer them as the Millennials. Table 1: Generational Cohort Demographic of Malaysia based on Cudmore, et al. (2010)

Demographic Born Current (in 2015)

Silent Generation Born before 1946 70 years or more

Baby Boomers 1946 – 1964 51 - 69

Generation X 1965 – 1976 39 - 50

Generation Y (Millennials) 1977 – 1998 17 - 38

2.4 Conceptual Framework

Page 15

This study will use the financial literacy model as proposed by Remund (2010) and Huston (2010) and associate it to Joo’s (2008) financial well-being model to form a conceptual framework. This study also acknowledges the dependencies of all the components that affect financial well-being as discussed by Gerrans et al. (2014). Financial satisfaction will be used as a proxy to determine financial well-being (Hira & Mugenda, 1998; Xiao, et al., 2008; Robb & Woodyard, 2011; Ali, et al., 2015; Taft, et al., 2013) as there is no agreed approach towards measuring financial well-being (Joo & Grable, 2004; Robb & Woodyard, 2011; Gerrans, et al., 2014). The focus of the conceptual framework is to determine what affects the financial satisfaction of the Gen-Y in Malaysia. The financial attitude and behaviour of individuals is not observed directly as the conceptual framework takes cues from an individual’s financial attitudes and behaviours to determine financial management, financial planning and financial situation independent variables. The conceptual framework has five hypotheses. Figure 1: Conceptual Framework

2.4.1 Hypotheses Joo’s (2008) model describes financial status as an individual’s income and expense at a point in time that can be quantified in financial figures or ratios. This study hypothesizes that an individual financial status has an influence over financial satisfaction as shown in H1. H1: Financial Status has a positive influence on an individual’s financial satisfaction. Financial knowledge is one of the determinants to any financial literacy measurements (Huston, 2010; Remund, 2010; Atkinson & Messy, 2011; ANZ, 2011). This study hypothesizes that financial knowledge can determine financial satisfaction. H2: Financial Knowledge has a positive influence on an individual’s financial satisfaction.

Page 16

Past studies have posited financial management contribute positively to financial satisfaction (O’Neill, et al., 2000; Albeerdy & Ghareghi, 2015). This study will set to explore this positive correlation. H3: Financial Management has a positive influence on an individual’s financial satisfaction. Many studies have confirmed this positive correlation between financial planning with financial satisfaction (Almenberg & Säve-Söderbergh, 2011; Behrman, et al., 2012; Lusardi & Mitchell, 2014; Ali, et al., 2015). This study is set out to validate that financial planning has a positive influence towards financial satisfaction. H4: Financial Planning has a positive influence on an individual’s financial satisfaction. Financial situation also correlates to how an individual financial habits are (Hira & Mugenda, 1998; Joo & Grable, 2004; Wiener & Doescher, 2008). Hence this study hypothesizes that financial situation is also having a positive influence towards an individual’s financial satisfaction. H5: Financial situation has a positive influence on an individual’s financial satisfaction. 3. Research Design and Methodology This study will take a positivism approach towards exploring the social realities that have causal relationships with the independent variable; financial satisfaction (Johnson & Duberley, 2000; Ponterotto, 2005). This study hypothesise that the determinants that influences financial satisfaction are deterministic in nature and can be proven through empirical evidences as mentioned in extant literature. The positivism approach is also the most parsimonious approach to explain the complex subject of personal finance as explored by Remund (2010), Huston (2010), Joo (2008) and Gerrans et al. (2014). The quantitative method is used to approach the subject matter in a systematic and empirical manner (Crowther & Lancaster, 2012) in the likes of studies on personal finance in extant literature (Mahdzan & Victorian, 2013; Behrman, et al., 2012; Taft, et al., 2013). This study will be conducted through a survey whereby observations will be quantified and the determinants will be identified through mathematical analysis (Crowther & Lancaster, 2012). 3.1 Data Collection and Sampling Methods This study aims to collect 180 samples for analysis in a span of three weeks through a simple random sampling to anyone who wishes to take part in the survey (Donley, 2012). All participants are clearly informed on the purpose, duration and intention of the survey and accepts the terms of the survey prior to attempting it. The survey design will be sourced and structured from various different published extant literature that has been adopted by institutions familiar with the subject matter (ANZ, 2011; OECD, 2011; Australia Unity, 2014) as well as based on studies from prominent subject matter experts on the subject (Lusardi & Mitchell, 2011; Huston, 2010; Atkinson & Messy, 2011; Robb & Woodyard, 2011; Remund, 2010; Yamauchi & Templer, 1982; Albaity & Rahman, 2012; Joo & Grable, 2004; Hira & Mugenda, 1998; Xiao, et al., 2008). The questions will be written to suit the language semantics of Malaysians.

Page 17

Majority of the questions are designed with Likert scale responses with five types of responses ranges between ‘(1) – Strongly Disagree’ to ‘(5) – Strongly Agree’ to observe criteria which are subjective in nature; particularly those that explores perceptions, opinions, attitudes and behaviours of participants (Crowther & Lancaster, 2012). The survey is in English. The survey begins with three filter questions. These questions are designed to filter out unqualified samples from being included into the sample data. This is followed by the questions on socio-demographics. Financial positions portion consist of seven objective questions that focuses on capturing the participant’s level of debt. Financial management consists of twelve five-point Likert scale (1 – “Strongly Disagree to 5 – “Strongly Agree”) questions aim to assess the individual’s financial attitude and behaviour related to financial management to explore the subject matter in detail. Financial planning is explored through seven five-point Likert scale (1 – “Strongly Disagree to 5 – “Strongly Agree”) questions covering general planning activities, retirement, insurance, investing and risk. Financial knowledge questions consist of four objective questions to test the financial knowledge of participants while the next three questions are two five-point Likert scale (1 – “Very Difficult to 5 – “Very Easy”) questions and one five-point Likert scale (1 – “Extremely Uncomfortable to 5 – “Extremely Comfortable”) question based to explore the participants application of financial knowledge; how the participants applies the financial knowledge in day-to-day activities. Finally, the financial satisfaction are measured using seven five-point Likert scale (1 – “Strongly Disagree to 5 – “Strongly Agree”) questions to explore the understanding on an individual’s perception on financial standing based on one’s attitudes and behaviours. 3.2 Analysis Plan The data collected from the survey will be compiled, translated, tabulated and analysed using Microsoft Excel and IBM SSPS Statistical software. The data will undergo a reliability test using Cronbach’s Alpha test and correlation checking as this survey is derived from more than one sources. This is next followed by factor analysis to determine the set of determinants for financial satisfaction. The new set of determinants would undergo a reliability check to ensure the strength of the components that construct the determinants are valid and correlated. Finally, the data set will be descriptively analysed and the final determinants will be examined for correlations to determine the validity of the study’s hypotheses. 4. Results, Analysis and Discussions 4.1 Reliability Analysis The Cronbach’s Alpha test shows a score of 0.825 based on all thirty-three questions in the survey indicates that there is high level of internal consistency for the mesh of questions used for this survey. The Cronbach’s Alpha if Item Deleted also indicates that all thirty-three items registers a score of greater than 0.81 which concludes that removal of questions does not causes the survey to be unreliable.

Page 18

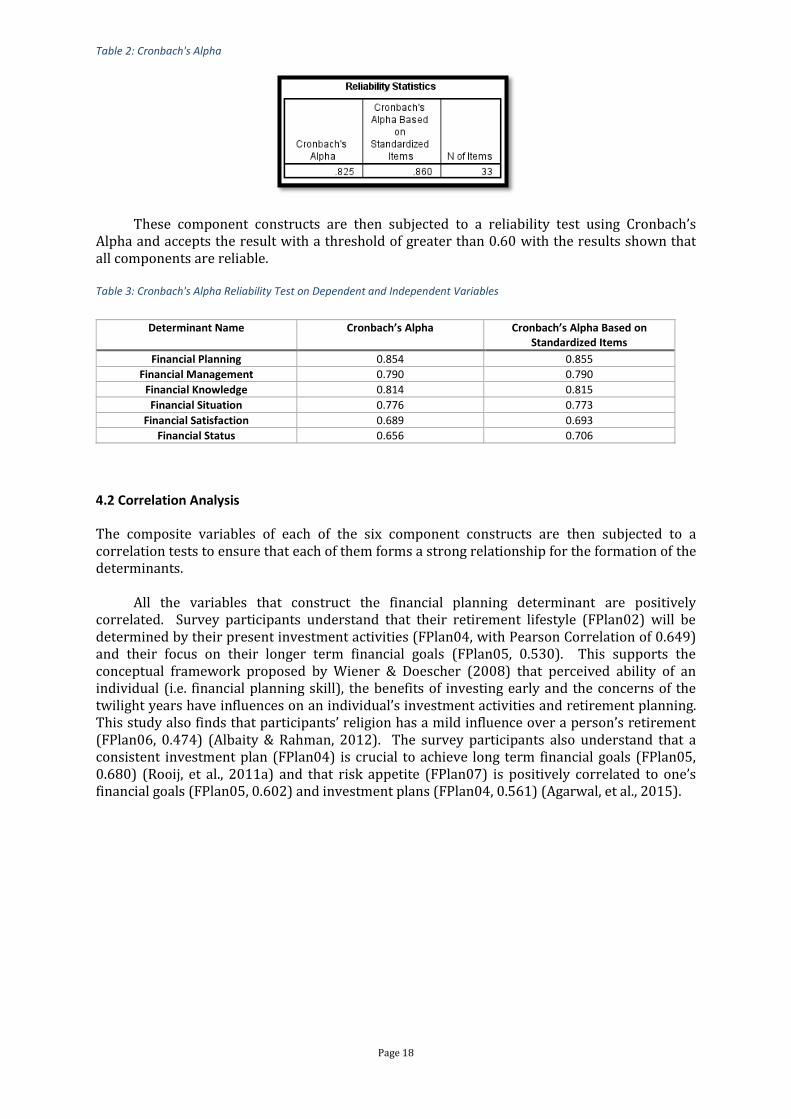

Table 2: Cronbach's Alpha

These component constructs are then subjected to a reliability test using Cronbach’s Alpha and accepts the result with a threshold of greater than 0.60 with the results shown that all components are reliable. Table 3: Cronbach's Alpha Reliability Test on Dependent and Independent Variables

Determinant Name Cronbach’s Alpha Cronbach’s Alpha Based on Standardized Items

Financial Planning 0.854 0.855

Financial Management 0.790 0.790

Financial Knowledge 0.814 0.815

Financial Situation 0.776 0.773

Financial Satisfaction 0.689 0.693

Financial Status 0.656 0.706

4.2 Correlation Analysis

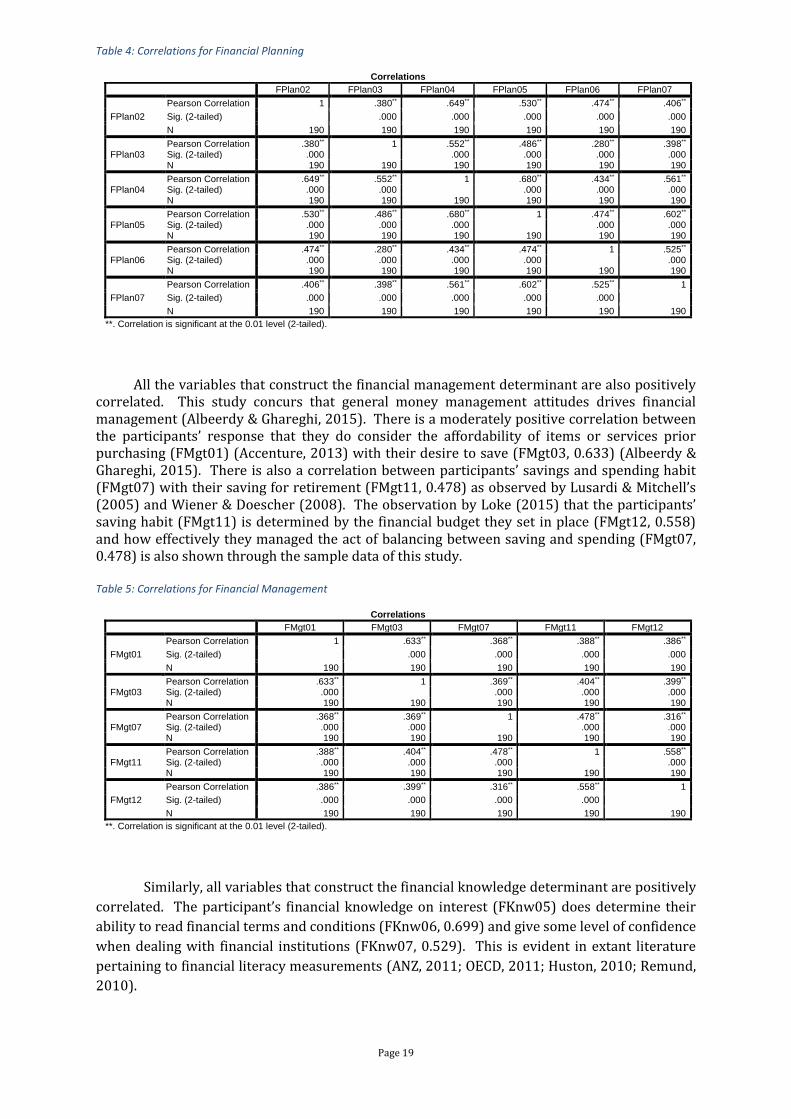

The composite variables of each of the six component constructs are then subjected to a correlation tests to ensure that each of them forms a strong relationship for the formation of the determinants. All the variables that construct the financial planning determinant are positively correlated. Survey participants understand that their retirement lifestyle (FPlan02) will be determined by their present investment activities (FPlan04, with Pearson Correlation of 0.649) and their focus on their longer term financial goals (FPlan05, 0.530). This supports the conceptual framework proposed by Wiener & Doescher (2008) that perceived ability of an individual (i.e. financial planning skill), the benefits of investing early and the concerns of the twilight years have influences on an individual’s investment activities and retirement planning. This study also finds that participants’ religion has a mild influence over a person’s retirement (FPlan06, 0.474) (Albaity & Rahman, 2012). The survey participants also understand that a consistent investment plan (FPlan04) is crucial to achieve long term financial goals (FPlan05, 0.680) (Rooij, et al., 2011a) and that risk appetite (FPlan07) is positively correlated to one’s financial goals (FPlan05, 0.602) and investment plans (FPlan04, 0.561) (Agarwal, et al., 2015).

**. Correlation is significant at the 0.01 level (2-tailed).

All the variables that construct the financial management determinant are also positively correlated. This study concurs that general money management attitudes drives financial management (Albeerdy & Ghareghi, 2015). There is a moderately positive correlation between the participants’ response that they do consider the affordability of items or services prior purchasing (FMgt01) (Accenture, 2013) with their desire to save (FMgt03, 0.633) (Albeerdy & Ghareghi, 2015). There is also a correlation between participants’ savings and spending habit (FMgt07) with their saving for retirement (FMgt11, 0.478) as observed by Lusardi & Mitchell’s (2005) and Wiener & Doescher (2008). The observation by Loke (2015) that the participants’ saving habit (FMgt11) is determined by the financial budget they set in place (FMgt12, 0.558) and how effectively they managed the act of balancing between saving and spending (FMgt07, 0.478) is also shown through the sample data of this study. Table 5: Correlations for Financial Management

Correlations

FMgt01 FMgt03 FMgt07 FMgt11 FMgt12

FMgt01

Pearson Correlation 1 .633** .368** .388** .386**

Sig. (2-tailed) .000 .000 .000 .000

N 190 190 190 190 190

FMgt03 Pearson Correlation .633** 1 .369** .404** .399** Sig. (2-tailed) .000 .000 .000 .000 N 190 190 190 190 190

FMgt07 Pearson Correlation .368** .369** 1 .478** .316** Sig. (2-tailed) .000 .000 .000 .000 N 190 190 190 190 190

FMgt11 Pearson Correlation .388** .404** .478** 1 .558** Sig. (2-tailed) .000 .000 .000 .000 N 190 190 190 190 190

FMgt12

Pearson Correlation .386** .399** .316** .558** 1

Sig. (2-tailed) .000 .000 .000 .000

N 190 190 190 190 190

**. Correlation is significant at the 0.01 level (2-tailed).

Similarly, all variables that construct the financial knowledge determinant are positively

correlated. The participant’s financial knowledge on interest (FKnw05) does determine their

ability to read financial terms and conditions (FKnw06, 0.699) and give some level of confidence

when dealing with financial institutions (FKnw07, 0.529). This is evident in extant literature

FKnw06 Pearson Correlation .699** 1 .556** Sig. (2-tailed) .000 .000 N 190 190 190

FKnw07

Pearson Correlation .529** .556** 1

Sig. (2-tailed) .000 .000

N 190 190 190

**. Correlation is significant at the 0.01 level (2-tailed).

The financial situation constructs are positively correlated too with the one’s

acknowledgement that an out-of-control financial situation (FAB03) has a strong impact on

one’s life (FAB04, 0.821) as posited by Joo & Grable (2004). This study also determines that

person’s level of debt (FAB04) is an indicator of a person’s quality of life as mentioned by (Xiao,

et al., 2008) (FAB02, 0.360).

Table 7: Correlations for Financial Situation

Correlations

FAB02 FAB03 FAB04

FAB02

Pearson Correlation 1 .415** .360**

Sig. (2-tailed) .000 .000

N 190 190 190

FAB03 Pearson Correlation .415** 1 .821** Sig. (2-tailed) .000 .000 N 190 190 190

FAB04

Pearson Correlation .360** .821** 1

Sig. (2-tailed) .000 .000

N 190 190 190

**. Correlation is significant at the 0.01 level (2-tailed).

All the variables that construct financial satisfaction determinant are mildly positively

correlated. The participants’ response that a supportive family towards an individual’s financial

goals (FSat02) do contribute towards an improving financial growth (FSat03, 0.404). This

supports Sabri, et al. (2010) observation that family members has an influence on an

individual’s financial knowledge and behaviour. An individual’s confidence (FAB01) also drives

one’s financial well-being (FSat01, 0.389) either positively or negatively as a result of

overconfidence as evidenced by Albaity & Rahman (2012).

Table 8: Correlations for Financial Satisfaction

Correlations

FAB01 FSat01 FSat02 FSat03

FAB01

Pearson Correlation 1 .389** .327** .312**

Sig. (2-tailed) .000 .000 .000

N 190 190 190 190

FSat01 Pearson Correlation .389** 1 .375** .359** Sig. (2-tailed) .000 .000 .000 N 190 190 190 190

FSat02 Pearson Correlation .327** .375** 1 .404** Sig. (2-tailed) .000 .000 .000 N 190 190 190 190

FSat03

Pearson Correlation .312** .359** .404** 1

Sig. (2-tailed) .000 .000 .000

N 190 190 190 190

**. Correlation is significant at the 0.01 level (2-tailed).

Page 21

Finally, both variables that construct financial status determinant are positively

correlated. It is a known fact that a person’s financial balance from one’s income is termed as

one’s saving.

Table 9: Correlations for Financial Status

Correlations

LN_SavingMonthly LN_IncomeMonthly

LN_SavingMonthly

Pearson Correlation 1 .546**

Sig. (2-tailed) .000

N 190 190

LN_IncomeMonthly

Pearson Correlation .546** 1

Sig. (2-tailed) .000

N 190 190

**. Correlation is significant at the 0.01 level (2-tailed).

4.3 Multiple Regression Analysis

The linear regression used for this study shows that correlation coefficient (multiple R) is at

48.7% with coefficient of determination (R square) at 23.7% and adjusted R Square at 21.3%.

These indicate that the conceptual framework used for this study is weak in predicting financial

satisfaction based its five dependent variable. The Durbin-Watson test for auto-correlation

shows that the value of the model is at 1.655 which is between the values 1.5 to 2.5. This

indicates that there is no first order linear auto-correlation (Hair, et al., 2010; Bakon & Hassan,

2013).

Table 10: Regression Model Summary

The Analysis of Variance (ANOVA) for the regression model indicates the dependent value of financial satisfaction has its error reduced by 23.68% with an F ratio of 9.99 and significance level of 0.00. This indicates that there is a statistical differences among the independent variables. Table 11: ANOVA

Page 22

The regression coefficient model determines that financial planning and financial knowledge are significant predictors for financial satisfaction of Gen-Y based on significance value of below 0.05 for acceptability (Hair, et al., 2010). Among these two independent variable, financial planning has a higher impact (beta = 0.300) than financial knowledge (beta = 0.154). As for multicollinearity checks, the regression model indicates all independent variables have the tolerance value of > 0.1 and Variance Inflation Factor (VIF) < 10 which indicates the multicollinearity has no potential problem (Hair, et al., 2010). This indicates that all five independent variables have a positive impact on the dependent variable. Table 12: Regression Coefficients

This study accepts the hypothesis with significant score (p) of less than 0.05 as showing significant impact on the dependent variable (Hair, et al., 2010). Therefore this study accept that financial planning (H4) and financial knowledge (H2) has a positive influence on an individual’s financial satisfaction with the right degree of confidence. All the independent variable has a positive influence on financial satisfaction with financial planning and financial knowledge showing the acceptable level of confidence. Table 13: Hypothesis Results

Hypothesis Beta Coefficient (β)

Significance (p < 0.05)

Decision

H1: Financial Status has a positive influence on an individual’s financial satisfaction.

0.038 0.622 Reject

H2: Financial Knowledge has a positive influence on an individual’s financial satisfaction.

0.154 0.036 Accept

H3: Financial Management has a positive influence on an individual’s financial satisfaction.

0.121 0.122 Reject

H4: Financial Planning has a positive influence on an individual’s financial satisfaction.

0.300 0.000 Accept

H5: Financial Situation has a positive influence on an individual’s financial satisfaction.

0.092 0.256 Reject

4.2 Discussion and Evaluation The result shows that an individual’s financial knowledge and financial planning capabilities are reliable predictors of one’s financial satisfaction. These two variables are components that make up financial literacy (Remund, 2010; Huston, 2010) and extant literature have confirmed its positive correlation with financial satisfaction (Almenberg & Säve-Söderbergh, 2011; Behrman, et al., 2012; Lusardi & Mitchell, 2014; Ali, et al., 2015). Financial management; though also an aspect of financial literacy (Remund, 2010; Huston, 2010) is shown not to be a factor towards an individual’s financial satisfaction. This can be

Page 23

attributed to that financial management is related to the attitudes and habits of how an individual manages money and that good financial management is the foundation towards good financial planning (Ali, et al., 2015). Thus the outcome of financial management is exemplified, as extant literature posit, in financial planning (Almenberg & Säve-Söderbergh, 2011; Behrman, et al., 2012; Lusardi & Mitchell, 2014; Rooij, et al., 2011b). Financial situation is not a factor to determine financial satisfaction as well. This is in support with extant literature which observe that financial situation is an outcome of an individual’s actions instead of as an independent factor (Hira & Mugenda, 1998; Joo & Grable, 2004; Wiener & Doescher, 2008; Robb & Woodyard, 2011). These extant literature also mentions that financial situation is determined by the way an individual manages one’s money (financial management) and financial planning. Financial status is also not a factor in determining an individual’s financial satisfaction thus not supporting a component of Joo’s (2008) framework that mentions financial status of an individual at a point in time determines a person’s financial satisfaction. 5. Conclusion This study answers the first question by establishing that financial knowledge and financial planning both as determinants of financial literacy, has a positive influence on financial well-being of Gen-Y in Malaysia. The financial literacy model as proposed by Remund (2010) and Huston (2010) has been proven accurate in determining financial satisfaction (Hira & Mugenda, 1998; Joo & Grable, 2004; Taft, et al., 2013). Strong financial knowledge is the precursor to good financial management as it influences an individual’s financial attitude and behaviour (Perry & Morris, 2005; Britt, et al., 2013; Lusardi & Mitchell, 2014). Good financial management is the prerequisite towards a good financial planning as observed by extant literature (O’Neill, et al., 2000; Albeerdy & Ghareghi, 2015; Rooij, et al., 2011a; Ali, et al., 2015). Similarly, this study also establishes that the current financial status of Gen-Y in Malaysia is not a determinant for financial satisfaction as suggested by Joo (2008). An individual’s financial status is a snapshot of an individual’s financial asset and liability at the point in time. This study also concludes that financial situation is not a determinant for financial well-being of Gen-Y in Malaysia. Financial situation is better determined by an individual’s financial attitudes and behaviour (Hira & Mugenda, 1998; Joo & Grable, 2004; Wiener & Doescher, 2008) as evidenced from a weak linkage by the study. This suggests that financial situation is a consequence rather than a determinant for financial satisfaction. In conclusion, financial well-being is subjective and context sensitive with no consensus approach towards accurately measure it (Joo & Grable, 2004; Robb & Woodyard, 2011; Gerrans, et al., 2014). Financial literacy does promote a better financial satisfaction through sound financial knowledge and good financial planning when an individual is engaged in sound financial management attitudes and behaviours as well as the utilisation of financial products. This study is not able to associate financial situation and financial status as a determinant to financial well-being as posited by Joo (2008). 5.1 Implications and Future Directions This is an exploratory study to determine what affects financial well-being of Gen-Y in Malaysia. Knowing that financial literacy or more specifically – financial knowledge and financial planning are strong determinants for financial well-being, the authorities in the field of personal finance can strategize on ways to boost the mediocre financial literacy of Gen-Y in the country. Malaysian should also be made aware that financial planning is not just for those who with strong financial status. Financial planning is for everyone and it is not dependent on financial planners.

Page 24

Extant literature posits that financial literacy is time and context sensitive (Schmeiser & Seligman, 2003). This indicates that the relevance of the financial well-being of Gen-Y in this study will decay in relevance over the passing periods. Such studies should be performed periodically to ensure the outcome of any strategies supports the uptick of financial literacy scores. It is worth noting that this study is conducted in English. In a multi-racial country like Malaysia, this study should also include the survey questions in other languages namely Bahasa Malaysia, Mandarin and Tamil. Moreover, this study is done by survey which restricts the researching on having any interactions with the survey participants. A more effective approach is to conduct selective interviews to gain further insights to the sample participants to explore interesting preliminary findings. The sample size for the study should be significantly large and distributed out to cover all major races and geographies in Malaysia. This study serves as a foundation for future researches on the subject of financial well-being and literacy.

References

Accenture, 2013. Who are the Millennial shoppers? And what do they really want?. [Online] Available at: https://www.accenture.com/us-en/insight-outlook-who-are-millennial-shoppers-what-do-they-really-want-retail [Accessed 7 August 2016]. Agarwal, S. et al., 2015. Financial literacy and financial planning: Evidence from India. Journal of Housing Economics, Volume 27, pp. 4-21. Albaity, M. & Rahman, M., 2012. Behavioural Finance and Malaysian Culture. International Business Research, 11(5), pp. 65-76. Albeerdy, M. I. & Ghareghi, B., 2015. Determinants of the Financial Literacy among College Students in Malaysia. International Journal of Business Administration, 6(3), pp. 15-24. Ali, A., Rahman, M. S. A. & Bakar, A., 2015. Financial Satisfaction and the Influence of Financial Literacy in Malaysia. Social Indicators Research, 120(1), pp. 137-156. Almenberg, J. & Säve-Söderbergh, J., 2011. Financial Literacy and Retirement Planning in Sweden. Cambridge University Press, 10(4), pp. 585-598. ANZ, 2011. Adult financial literacy in Australia: Full report of the results from the 2011 ANZ survey, s.l.: ANZ. Asian Institute of Finance, 2015. Understanding Gen Y: Bridging the Knowledge Gap of Malaysia's Millennials.[Online] Available at: http://www.aif.org.my/clients/aif_d01/assets/multimediaMS/publication/Finance_Matters_Understanding_Gen_Y_Bridging_the_Knowledge_Gap_of_Malaysias_Millennials.pdf [Accessed 20 October 2015]. Atkinson, A. & Messy, F.-A., 2011. Assessing Financial Literacy in 12 Countries: An OECD Pilot Exercise. Nespar Discussion Paper, Volume 01/2011-014, pp. 1-26. Australia Unity, 2014. Financial Wellbeing Questionnaire - Design and Validation, s.l.: Australia Unity. Bakon, K. A. & Hassan, Z., 2013. Perceived Value of Smartphone and Its Impact on Deviant Behaviour: An Investigation on Higher Education Students in Malaysia. International Journal of Information Systems and Engineering, 2(1), pp. 38-55.

Page 25

Bank Negara Malaysia, 2011. Financial Sector Blueprint 2011-2020. [Online] Available at: http://www.bnm.gov.my/files/publication/fsbp/en/BNM_FSBP_FULL_en.pdf [Accessed 19 October 2015]. Behrman, J. R., Mitchell, O. S., Soo, C. & Bravo, D., 2012. How Financial Literacy Affects Household Wealth Accumulation. American Economic Review, 102(3), pp. 300-304. Britt, S., Cumbie, J. A. & Bell, M. M., 2013. The Influence of Locus of Control on Student Financial Behavior. College Student Journal, 47(1), pp. 178-185. Broadbridge, A. M., Maxwell, G. A. & Ogden, S. M., 2007. Students' Views of Retail Employment - Key Findings from Generation Ys. International Journal of Retail & Distribution Management, 35(12), pp. 982-992. Credit Counselling and Debt Management Agency, 2015a. Gagal Kawal Perbelanjaan Kad Kredit. [Online] Available at: https://www.akpk.org.my/content/858-gagal-kawal-perbelanjaan-kad-kredit?width=100%25&height=460px&inline=true#colorbox-inline-1011609735 [Accessed 18 April 2016]. Credit Counselling and Debt Management Agency, 2015b. Semakin ramai bermasalah kewangan. [Online] Available at: https://www.akpk.org.my/content/721-semakin-ramai-bermasalah-kewangan?width=100%25&height=460px&inline=true#colorbox-inline-1114346637 [Accessed 18 April 2016]. Crowther, D. & Lancaster, G., 2012. Research Methods. 2nd ed. Oxford: Taylor and Francis. Cudmore, B. A., Patton, J., Ng, K. & McClure, C., 2010. The Millennials and Money Management. Journal of Management and Marketing Research, Volume 4, pp. 1-28. Deal, J. J., Altman, D. G. & Rogelberg, S. G., 2010. Millennials at Work: What We Know and What We Need to Do (If Anything). Journal of Business and Psychology, 25(2), pp. 191-199. Department of Statistics Malaysia, 2015. Malaysia Population Projection 2010-2040. [Online] Available at: https://www.statistics.gov.my/index.php?r=column/cdatavisualization&menu_id=WjJMQ1F0N3RXclNGNWpIODBDRmh2UT09&bul_id=aDNJSnBKRTNYSGhvcU5wamlLUFB5UT09 [Accessed 19 October 2015]. Donley, A. M., 2012. Research Methods. 1st ed. New York: Facts on File. Duh, H. I., 2016. Childhood family experiences and young Generation Y money attitudes and materialism. Personality and Individual Differences, Volume 95, pp. 134-139. FINRA Foundation, 2014. The Financial Capabilties of Young Adults - A Generational View. [Online] Available at: https://www.finra.org/sites/default/files/14_0100%201_IEF_Research%20Report_CEA_3%206%2014%20%28FINAL%29_0_0.pdf [Accessed 10 November 2015]. Gerrans, P., Speelman, C. & Campitelli, G., 2014. The Relationship Between Personal Financial Wellness and Financial Wellbeing: A Structural Equation Modelling Approach. Journal of Family and Economic Issues, 35(2), pp. 145-160. Hair, J. F. J., Black, W. C., Babin, B. J. & Anderson, R. E., 2010. Multivariate Data Analysis. 7th ed. New Jersey: Prentice Hall. Harland Clarke, 2008. Closing the Generation Gap. [Online] Available at :http://harlandclarke.com/dv/08Q1/03.php [Accessed 18 April 2016].

Page 26

Hilgert, M. A., Hogarth, J. M. & Beverly, S. G., 2003. Household financial management: The connection between knowledge and behavior. Federal Reserve Bulletin, 89(7), pp. 309-322. Hira, T. K. & Mugenda, O. M., 1998. Predictors Of Financial Satisfaction: Differences Between Retirees And Non-retirees. Financial Counseling and Planning, 9(2), pp. 75-85. Hoch, S. J. & Ha, Y.-W., 1986. Consumer Learning: Advertising and the Ambiguity of Product Experience. Journal of Consumer Research, 13(2), pp. 221-233. Huston, S. J., 2010. Measuring Financial Literacy. Journal of Consumer Affairs, 44(2), pp. 296-316. Johnson, P. & Duberley, J., 2000. Understanding Management Research : An Introduction to Epistemology. 1st ed. London: SAGE Publications Ltd. Joo, S.-h. & Grable, J. E., 2004. An Exploratory Framework of the Determinants of Financial Satisfaction. Journal of Family and Economic Issues, 25(1), pp. 25-50. Kumar, A. & Lim, H., 2008. Age Differences in Mobile Service Perceptions: Comparison of Generation Y and Baby Boomers. Journal of Services Marketing, 22(7), pp. 568-577. Loke, Y. J., 2015. Financial Knowledge and Behaviour of Working Adults in Malaysia. The Journal of Applied Economic Research, 9(1), pp. 18-38. Luksander, A., Béres, D., Huzdik, K. & Németh, E., 2014. Analysis of the Factors that Influence the Financial Literacy of Young People Studying in Higher Education. Public Finance Quarterly, 29(2), pp. 220-241. Lusardi, A. & Mitchell, O. S., 2005. Financial Literacy and Planning: Implications for Retirement Wellbeing. IDEAS Working Paper Series from RePEc. Lusardi, A. & Mitchell, O. S., 2011. Financial literacy around the world: an overview. Journal of Pension Economics & Finance, 10(4), pp. 497-508. Lusardi, A. & Mitchell, O. S., 2014. The Economic Importance of Financial Literacy. Journal of Economic Literature, 52(1), pp. 5-44. Mahdzan, N. S. & Victorian, S. M. P., 2013. The Determinants of Life Insurance Demand: A Focus on Saving Motives and Financial Literacy. Asian Social Science, 9(5), pp. 274-284. Monticone, C., 2010. How Much Does Wealth Matter in Acquisition of Financial Literacy?. The Journal of Consumer Affairs, 44(2), pp. 403-422. Muske, G. & Winter, M., 1998. Real world financial management tools and practices. Consumer Interests Annual, Volume 44, pp. 19-24. O’Neill, B. et al., 2000. Successful financial goal attainment: Perceived resources and obstacles. Financial Counseling and Planning, 11(1), pp. 1-12. OECD, 2011. Measuring Financial Literacy: Questionnaire and Guide Notes for Conducting an Internationally Comparable Survey of Financial Literacy. [Online] Available at: https://www.google.com/url?sa=t&rct=j&q=&esrc=s&source=web&cd=1&cad=rja&uact=8&ved=0CCIQFjAAahUKEwjOuobQzZLJAhWKC44KHUu0CUs&url=http%3A%2F%2Fwww.oecd.org%2Ffinance%2Ffinancial-education%2F49319977.pdf&usg=AFQjCNE-uiWqExvF4c3F296Fz9AgyfG0VA&sig2=us_ROGoURS [Accessed 14 November 2015].

Page 27

Perry, V. G. & Morris, M. D., 2005. Who Is in Control? The Role of Self-Perception, Knowledge, and Income in Explaining Consumer Financial Behaviour. The Journal of Consumer Affairs, 39(2), pp. 299-313. Ponterotto, J. G., 2005. Qualitative research in counseling psychology: A primer on research paradigms and philosophy of science. Journal of Counseling Psychology, 52(2), pp. 126-136. PriceWaterhouse Coopers, 2009. Malaysia's Gen Y Unplugged. [Online] Available at: http://www.geniustribes.com/resources/gen-yMal.pdf [Accessed 10 November 2015]. PriceWaterhouseCoopers, 2015. Millennials & Financial Literacy - The Struggle with Personal Finance, Virginia: PriceWaterhouseCoopers. Reasie, H. A., Weber, J. G. & Yarbrough, D., 2001. Money Management Practices of College Students. College Student Journal, 35(2), pp. 244-249. Remund, D. L., 2010. Financial Literacy Explicated: The Case for a Clearer Definition in an Increasingly Complex Economy. The Journal of Consumer Affairs, 44(2), pp. 276-295. Robb, C. A. & Woodyard, A. S., 2011. Financial knowledge and ‘best practice’ behavior. Journal of Financial Counseling and Planning, 22(1), pp. 36-46. Rooij, M. v., Lusardi, A. & Alessie, R., 2011b. Financial literacy and stock market participation. Journal of Financial Economics, 101(2), pp. 449-472. Rooij, M. v., Lusardi, A. & Alessie, R. J., 2011a. Financial Literacy and Retirement Planning in the Netherlands. Journal of Economic Psychology, 32(4), pp. 493-608. Sabri, M. F. & Juen, T. T., 2014. The Effects of Financial Literacy, Financial Management and Saving Motives on Financial Well-being among Working Women. Journal of Wealth Management & Financial Planning, Volume 1, pp. 20-32. Schmeiser, M. D. & Seligman, J. S., 2003. Using the Right Yardstick: Assessing Financial Literacy Measures by Way of Financial Well-Being. The Journal of Consumer Affairs,, 47(2), pp. 243-262. Sirgy, M. J. et al., 2006. The quality-of-life (QOL) research movement: Past, present, and future. Social Indicators Research, Volume 76, pp. 343-466. Smith, T. J. & Nichols, T., 2015. Understanding the Millennial Generation. Journal of Business Diversity, 15(1), pp. 39-47. Taft, M. K., Hosein, Z. Z., Mehrizi, S. M. T. & Roshan, A., 2013. The Relation between Financial Literacy, Financial Wellbeing and Financial Concerns. International Journal of Business and Management, 8(11), pp. 63-75. The Council of Economic Advisers of United States, 2014. 15 Economic Facts about Millennials, Washington D.C.: The White House. The Star Newspaper, 2015. Becoming bankrupt before 35. [Online] Available at: http://www.thestar.com.my/News/Nation/2015/06/22/Becoming-bankrupt-before-35-Worrying-trend-of-about-25000-Gen-Y-Msians-in-debt-over-the-last-five-ye/ [Accessed 4 November 2015]. USA Today, 2005. Generation Y: They've arrived at work with a new attitude. [Online] Available at: http://usatoday30.usatoday.com/money/workplace/2005-11-06-gen-y_x.htm [Accessed 10 November 2015].

Page 28

Wiener, J. & Doescher, T., 2008. A Framework for Promoting Retirement Savings. Journal of Consumer Affairs, 42(2), pp. 137-164. Xiao, J. J., Tang, C. & Shim, S., 2008. Acting for Happiness: Financial Behavior and Life Satisfaction of College Students. Social Indicators Research, 92(1), pp. 53-68. Yamauchi, K. T. & Templer, D. I., 1982. Money Attitude Scale. Journal of Personality Assessment, 46(5), pp. 522-528.