1 4 4 Determining your 2017 stock plan tax requirements — a step-by-step guide Incentive Stock Option (ISO) plans can provide you with the benefit of favorable capital gains, but can be complicated with respect to tax. To determine your tax-reporting requirements, follow the steps outlined in this document. If you are unsure if your plan is an ISO, you can easily determine this by looking up your grant type on NetBenefits ® , under your Plan Summary page. Incentive Stock Option Plan INSIDE How to use the Supplemental Form to avoid overpaying taxes Alert: The tax-reform legislation adopted in December 2017 does not affect the 2017 tax year or the federal tax return for 2017 that you file in 2018.

Transcript

14

4

Determining your 2017stock plan tax requirements— a step-by-step guide

Incentive Stock Option (ISO) plans can provide you

with the benefit of favorable capital gains, but can be

complicated with respect to tax. To determine your

tax-reporting requirements, follow the steps outlined in

this document. If you are unsure if your plan is an ISO,

you can easily determine this by looking up your grant

type on NetBenefits®, under your Plan Summary page.

Incentive Stock Option Plan

INSIDEHow to use the

Supplemental Form to avoid

overpaying taxes

Alert: The tax-reform legislation adopted in December 2017 does not affect the 2017 tax year or the federal tax return for 2017 that you file in 2018.

* Fidelity is not involved in the preparation of the content supplied at the third-party unaffiliated website and does not guarantee or assume any responsibility for its content.

* This is important tax information and is being furnished to the Internal Revenue Service. If you are required to file a return, a negligence penalty or other sanction may be imposed on youif this income is taxable and the IRS determines that it has not been reported.

2017 TAX REPORTING STATEMENT

10/12/2017 9001029539 Pages 4 of 8

Customer Service:Account No.MASKED NAME***-**-8644 Payer's Fed ID Number:

800-544-6666Recipient ID No. 04-3523567

X27-495794

0 0 0

FORM 1099-B* 2017 Proceeds from Broker and Barter Exchange Transactions Copy B for Recipient OMB No. XXXX-XXXX

Short-term transactions for which basis is reported to the IRS --report on Form 8949 with Box A checked and/or Schedule D, Part IProceeds are reported as gross proceeds unless otherwise indicated (a).(This Label is a Substitute for Boxes 2, 3, 5 & 6)

(IRS Form 1099-B box numbers are shown below in bold type)

1a Description of property, Stock or Other Symbol, CUSIP

TOTALS 42,500.73 31,904.53 0.00 0.00 0.00Box A Short-Term Realized Gain 10,596.20Box A Short-Term Realized Loss 0.00

For any transaction listed on Form 1099-B in a section indicating that "basis is reported to the IRS", we are reporting to the IRS: 1a Description of Property, 2 type of gain or loss (i.e. short-term orlong-term), 3 basis reported to IRS, 6 Gross or Net Proceeds, and columns 1b, 1c, 1d, 1e, 1f, 1g, 4, 7, 14, 15 and 16. We are not reporting to the IRS: the Action, the Gain/Loss, and all subtotals andtotals.

For any section 1256 option contracts we are reporting to the IRS: 1a Description of Property and totals for boxes 8, 9, 10 and 11.

For any transaction listed on Form 1099-B in a section indicating that "basis is not reported to the IRS", we are reporting to the IRS: 1a Description of Property, 5 Noncovered security, 6 Gross or NetProceeds, and columns 1c, 1d, 4, 14, 15 and 16. We are not reporting to the IRS: 2 type of gain or loss (i.e. short-term or long-term), the Action, the Gain/Loss, columns 1b, 1e, 1f, 1g, 2, 3 and 7 and allsubtotals and totals.

Although Fidelity makes every effort to provide accurate information, please bear in mind that you, the taxpayer, are ultimately responsible for the accuracy of your tax returns.

(b) Cost or other basis provided may include adjustments including, but not limited to, dividend reinvestment, return of capital/principal, wash sale loss disallowed, amortization, accretion, acquisitionpremium, bond premium, market discount, market premium, and option premium.

(e) Your 1099-B reflects shares disposed of that were acquired through your employers stock plan. Cost basis associated with these shares may not have been adjusted for any compensation incomethat was associated with those shares in the year of acquisition or disposal. Please consult a tax advisor for the rules specific to your grant and plan. Refer to the Supplemental Stock Plan ServiceLot Detail section of this form for additional detail.

Amortization, accretion, and similar adjustments to cost basis are not provided for short-term instruments, unit investment trusts, or securities of foreign issuers.

Account No. XXX-XXXXXX Customer Service: XXX-XXX-XXXXRecipient ID No. XXX-XX-XXXX Payer’s Fed ID Number: XX-XXXXXXX

Form 1099-B

Note: This information is not reported to the IRS. It may assist you in tax return preparation.

2017 SUPPLEMENTAL INFORMATION

10/12/2017 9001029539 Pages 7 of 8

Customer Service:Account No.MASKED NAME***-**-8644 Payer's Fed ID Number:

800-544-6666Recipient ID No. 04-3523567

X27-495794

0

Detail Information Supplemental Stock Plan Lot DetailBased on the disposal method you have selected, the lots that appear on your 1099 Supplemental may differ from the lots on the 1099-B.Short-Term TransactionsDescription of Property, Stock or Other Symbol, Cusip

Totals 42,500.73 42,541.56Short-Term Adjusted Realized Gain 0.00Short-Term Adjusted Realized Loss -40.83Wash Sale Loss Disallowed 0.00

(w) Grant Type describes the equity award source of the lot you sold this tax year. Please see the Grant Type table for additional description.xxxxxx

Grant Type Equity Award Type Acquisition date represents:DO Deposit Only Shares Deposit DateNQSOP Non Qualified Stock Option Shares Exercise DateNQSP Non Qualified ESPP Shares Purchase DateNSR Non-Incentive SAR (NSR) Exercise DateQSOP Qualified Stock Option Shares Exercise DateQSP Qualified ESPP Shares Purchase DateRSA Restricted Awards Vesting DateRSU Restricted Units Distribution DateRSU Performance Units Distribution DateRSU Total Shareholder Return Units Distribution DateSAR Stock Appreciation Rights Exercise Datexxxxxxxxxxxx

(x) Date of Acquisition is the date that shares were acquired from your Equity Plan and deposited into your brokerage account.

Account No. XXX-XXXXXX Customer Service: XXX-XXX-XXXXRecipient ID No. XXX-XX-XXXX Payer’s Fed ID Number: XX-XXXXXXX

Form 1099-Supplemental

Participant uses these Fidelity forms…

to complete…

Rolls up

into

Rolls up

into

Form 8949Department of the Treasury Internal Revenue Service

Sales and Other Dispositions of Capital Assets▶ Go to www.irs.gov/Form8949 for instructions and the latest information.

▶ File with your Schedule D to list your transactions for lines 1b, 2, 3, 8b, 9, and 10 of Schedule D.

OMB No. 1545-0074

2017Attachment Sequence No. 12A

Name(s) shown on return Social security number or taxpayer identification number

Before you check Box A, B, or C below, see whether you received any Form(s) 1099-B or substitute statement(s) from your broker. A substitute statement will have the same information as Form 1099-B. Either will show whether your basis (usually your cost) was reported to the IRS by your broker and may even tell you which box to check.

Part I Short-Term. Transactions involving capital assets you held 1 year or less are short term. For long-term transactions, see page 2. Note: You may aggregate all short-term transactions reported on Form(s) 1099-B showing basis was reported to the IRS and for which no adjustments or codes are required. Enter the totals directly on Schedule D, line 1a; you aren't required to report these transactions on Form 8949 (see instructions).

You must check Box A, B, or C below. Check only one box. If more than one box applies for your short-term transactions, complete a separate Form 8949, page 1, for each applicable box. If you have more short-term transactions than will fit on this page for one or more of the boxes, complete as many forms with the same box checked as you need.

(A) Short-term transactions reported on Form(s) 1099-B showing basis was reported to the IRS (see Note above)(B) Short-term transactions reported on Form(s) 1099-B showing basis wasn't reported to the IRS(C) Short-term transactions not reported to you on Form 1099-B

1

(a) Description of property

(Example: 100 sh. XYZ Co.)

(b) Date acquired (Mo., day, yr.)

(c) Date sold or disposed of

(Mo., day, yr.)

(d) Proceeds

(sales price) (see instructions)

(e) Cost or other basis. See the Note below and see Column (e)

in the separate instructions

Adjustment, if any, to gain or loss. If you enter an amount in column (g),

enter a code in column (f). See the separate instructions.

(f) Code(s) from instructions

(g) Amount of adjustment

(h) Gain or (loss).

Subtract column (e) from column (d) and combine the result

with column (g)

2 Totals. Add the amounts in columns (d), (e), (g), and (h) (subtract negative amounts). Enter each total here and include on your Schedule D, line 1b (if Box A above is checked), line 2 (if Box B above is checked), or line 3 (if Box C above is checked) ▶

Note: If you checked Box A above but the basis reported to the IRS was incorrect, enter in column (e) the basis as reported to the IRS, and enter an adjustment in column (g) to correct the basis. See Column (g) in the separate instructions for how to figure the amount of the adjustment.

For Paperwork Reduction Act Notice, see your tax return instructions. Cat. No. 37768Z Form 8949 (2017)

SCHEDULE D (Form 1040)

Department of the Treasury Internal Revenue Service (99)

Capital Gains and Losses▶ Attach to Form 1040 or Form 1040NR.

▶ Go to www.irs.gov/ScheduleD for instructions and the latest information. ▶ Use Form 8949 to list your transactions for lines 1b, 2, 3, 8b, 9, and 10.

OMB No. 1545-0074

2017Attachment Sequence No. 12

Name(s) shown on return Your social security number

Part I Short-Term Capital Gains and Losses—Assets Held One Year or Less

See instructions for how to figure the amounts to enter on the lines below. This form may be easier to complete if you round off cents to whole dollars.

(d) Proceeds

(sales price)

(e) Cost

(or other basis)

(g) Adjustments

to gain or loss from Form(s) 8949, Part I,

line 2, column (g)

(h) Gain or (loss) Subtract column (e) from column (d) and

combine the result with column (g)

1a Totals for all short-term transactions reported on Form 1099-B for which basis was reported to the IRS and for which you have no adjustments (see instructions). However, if you choose to report all these transactions on Form 8949, leave this line blank and go to line 1b .

1b Totals for all transactions reported on Form(s) 8949 with Box A checked . . . . . . . . . . . . .

2

Totals for all transactions reported on Form(s) 8949 with Box B checked . . . . . . . . . . . . .

3

Totals for all transactions reported on Form(s) 8949 with Box C checked . . . . . . . . . . . . .

4 Short-term gain from Form 6252 and short-term gain or (loss) from Forms 4684, 6781, and 8824 . 4 5

Net short-term gain or (loss) from partnerships, S corporations, estates, and trusts from Schedule(s) K-1 . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5

6

Short-term capital loss carryover. Enter the amount, if any, from line 8 of your Capital Loss Carryover Worksheet in the instructions . . . . . . . . . . . . . . . . . . . . . . . 6 ( )

7 Net short-term capital gain or (loss). Combine lines 1a through 6 in column (h). If you have any long-term capital gains or losses, go to Part II below. Otherwise, go to Part III on the back . . . . . 7

Part II Long-Term Capital Gains and Losses—Assets Held More Than One Year

See instructions for how to figure the amounts to enter on the lines below. This form may be easier to complete if you round off cents to whole dollars.

(d) Proceeds

(sales price)

(e) Cost

(or other basis)

(g) Adjustments

to gain or loss from Form(s) 8949, Part II,

line 2, column (g)

(h) Gain or (loss) Subtract column (e) from column (d) and

combine the result with column (g)

8a Totals for all long-term transactions reported on Form 1099-B for which basis was reported to the IRS and for which you have no adjustments (see instructions). However, if you choose to report all these transactions on Form 8949, leave this line blank and go to line 8b .

8b Totals for all transactions reported on Form(s) 8949 with Box D checked . . . . . . . . . . . . .

9

Totals for all transactions reported on Form(s) 8949 with Box E checked . . . . . . . . . . . . .

10

Totals for all transactions reported on Form(s) 8949 with Box F checked. . . . . . . . . . . . . .

11

Gain from Form 4797, Part I; long-term gain from Forms 2439 and 6252; and long-term gain or (loss) from Forms 4684, 6781, and 8824 . . . . . . . . . . . . . . . . . . . . . . 11

12 Net long-term gain or (loss) from partnerships, S corporations, estates, and trusts from Schedule(s) K-1 12

13 Capital gain distributions. See the instructions . . . . . . . . . . . . . . . . . . 13 14

Long-term capital loss carryover. Enter the amount, if any, from line 13 of your Capital Loss Carryover Worksheet in the instructions . . . . . . . . . . . . . . . . . . . . . . . 14 ( )

15

Net long-term capital gain or (loss). Combine lines 8a through 14 in column (h). Then go to Part III onthe back . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 15

For Paperwork Reduction Act Notice, see your tax return instructions. Cat. No. 11338H Schedule D (Form 1040) 2017

Form 8949

Form 1040 Department of the Treasury—Internal Revenue Service (99)

U.S. Individual Income Tax Return 2016 OMB No. 1545-0074 IRS Use Only—Do not write or staple in this space.

For the year Jan. 1–Dec. 31, 2016, or other tax year beginning , 2016, ending , 20 See separate instructions.Your first name and initial Last name Your social security number

If a joint return, spouse’s first name and initial Last name Spouse’s social security number

▲ Make sure the SSN(s) above and on line 6c are correct.

Home address (number and street). If you have a P.O. box, see instructions. Apt. no.

City, town or post office, state, and ZIP code. If you have a foreign address, also complete spaces below (see instructions).

Foreign country name Foreign province/state/county Foreign postal code

Presidential Election Campaign

Check here if you, or your spouse if filing jointly, want $3 to go to this fund. Checking a box below will not change your tax or refund. You Spouse

Filing Status

Check only one box.

1 Single

2 Married filing jointly (even if only one had income)

3 Married filing separately. Enter spouse’s SSN above and full name here. ▶

4 Head of household (with qualifying person). (See instructions.) If

the qualifying person is a child but not your dependent, enter this

child’s name here. ▶

5 Qualifying widow(er) with dependent child

Exemptions 6a Yourself. If someone can claim you as a dependent, do not check box 6a . . . . .

34 Tuition and fees. Attach Form 8917 . . . . . . . 34

35 Domestic production activities deduction. Attach Form 8903 35

36 Add lines 23 through 35 . . . . . . . . . . . . . . . . . . . 36 37 Subtract line 36 from line 22. This is your adjusted gross income . . . . . ▶ 37

For Disclosure, Privacy Act, and Paperwork Reduction Act Notice, see separate instructions. Cat. No. 11320B Form 1040 (2016)

17

Form 1040Schedule D

Form W-2 This form will be provided by your company.Your company’s payroll department

IRS Form 1040 (the full 1040, not the 1040EZ or the 1040A), including Schedule D Capital Gains and Losses

Forms are available online at www.irs.gov,* by calling 800.TAX.FORM (800.829.3676), or by visiting your local IRS office.

Your local IRS office or your tax advisor

IRS Form 8949 This form is available online at www.irs.gov,* by calling 800.TAX.FORM (800.829.3676), or by visiting your local IRS office.

Your local IRS office or your tax advisor

Form 1099-B

You can access the form online at Fidelity.com/taxforms at the end of January. In addition, a form will be mailed to you no later than mid-February, if applicable.

A Fidelity Stock Plan Services Representative at the number provided on the statement

2017 Supplemental Information (Fidelity is providing you with additional information to supplement your 1099-B due to cost basis regulations that no longer permit brokers to include ordinary income.)

You can access the form online at Fidelity.com/taxforms at the end of January. In addition, a form will be mailed to you no later than mid-February, if applicable.

A Fidelity Stock Plan Services Representative at the number provided on the statement

Generally, you will owe ordinary income tax on shares sold that were acquired from the exercise of an ISO when your stock sale is considered a disqualifying disposition. Note that alternative minimum tax (AMT) may apply when you hold the ISO shares through the calendar year of exercise. You should consult a tax advisor regarding your personal tax situation.

The income earned from the sale of shares acquired from your stock option plan may be taxable in full or in part as ordinary income and reported on your W-2 provided by your company. However, with ISOs, you have no tax withholding and no Social Security or Medicare tax. In addition, you may owe tax on any capital gains resulting from the sale of your stock from the exercise, which is explained in later steps.

Report your ordinary income.2

34

4

The amount of ISO income is included in box 1.†

ISO income is included in boxes 16 and 18 if state and local tax withholding applies.

Your company may voluntarily report the ISO income in box 14.

W-2 income is reported on line 7

of Form 1040.

Example: IRS W-2 for ISO and Form 1040

For illustrative purposes only.

* Fidelity is not involved in the preparation of the content supplied at the third-party unaffiliated website and does not guarantee or assume any responsibility for its content.

† ISOs have no tax withholding and no Social Security or Medicare tax.

For illustrative purposes only.

Incentive Stock Option Plan

a Employee’s social security number

OMB No. 1545-0008

Safe, accurate, FAST! Use

Visit the IRS website at www.irs.gov/efile

b Employer identification number (EIN)

c Employer’s name, address, and ZIP code

d Control number

e Employee’s first name and initial Last name Suff.

f Employee’s address and ZIP code

1 Wages, tips, other compensation 2 Federal income tax withheld

3 Social security wages 4 Social security tax withheld

5 Medicare wages and tips 6 Medicare tax withheld

7 Social security tips 8 Allocated tips

9 10 Dependent care benefits

11 Nonqualified plans 12a See instructions for box 12Co d e

12bCo d e

12cCo d e

12dCo d e

13 Statutory employee

Retirement plan

Third-party sick pay

14 Other

15 State Employer’s state ID number 16 State wages, tips, etc. 17 State income tax 18 Local wages, tips, etc. 19 Local income tax 20 Locality name

Form W-2 Wage and Tax Statement 2015

Department of the Treasury—Internal Revenue Service

Copy B—To Be Filed With Employee’s FEDERAL Tax Return. This information is being furnished to the Internal Revenue Service.

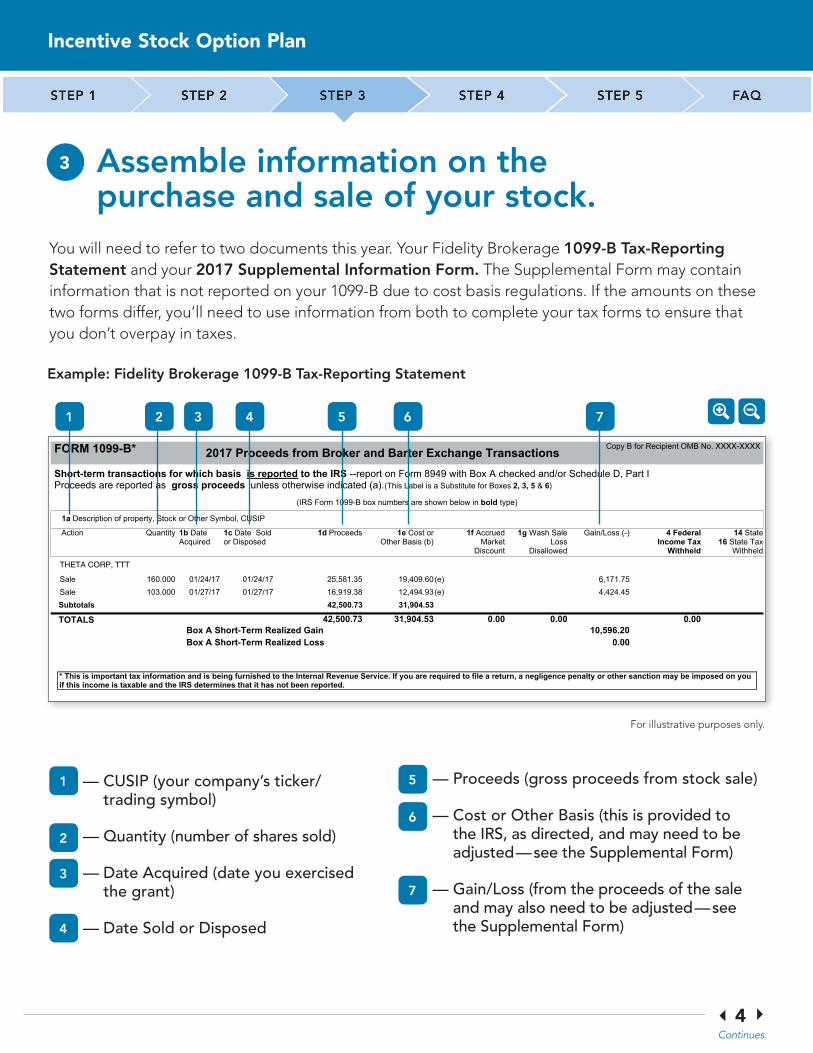

You will need to refer to two documents this year. Your Fidelity Brokerage 1099-B Tax-Reporting Statement and your 2017 Supplemental Information Form. The Supplemental Form may contain information that is not reported on your 1099-B due to cost basis regulations. If the amounts on these two forms differ, you’ll need to use information from both to complete your tax forms to ensure that you don’t overpay in taxes.

* This is important tax information and is being furnished to the Internal Revenue Service. If you are required to file a return, a negligence penalty or other sanction may be imposed on youif this income is taxable and the IRS determines that it has not been reported.

2017 TAX REPORTING STATEMENT

10/12/2017 9001029539 Pages 4 of 8

Customer Service:Account No.MASKED NAME***-**-8644 Payer's Fed ID Number:

800-544-6666Recipient ID No. 04-3523567

X27-495794

0 0 0

FORM 1099-B* 2017 Proceeds from Broker and Barter Exchange Transactions Copy B for Recipient OMB No. XXXX-XXXX

Short-term transactions for which basis is reported to the IRS --report on Form 8949 with Box A checked and/or Schedule D, Part IProceeds are reported as gross proceeds unless otherwise indicated (a).(This Label is a Substitute for Boxes 2, 3, 5 & 6)

(IRS Form 1099-B box numbers are shown below in bold type)

1a Description of property, Stock or Other Symbol, CUSIP

TOTALS 42,500.73 31,904.53 0.00 0.00 0.00Box A Short-Term Realized Gain 10,596.20Box A Short-Term Realized Loss 0.00

For any transaction listed on Form 1099-B in a section indicating that "basis is reported to the IRS", we are reporting to the IRS: 1a Description of Property, 2 type of gain or loss (i.e. short-term orlong-term), 3 basis reported to IRS, 6 Gross or Net Proceeds, and columns 1b, 1c, 1d, 1e, 1f, 1g, 4, 7, 14, 15 and 16. We are not reporting to the IRS: the Action, the Gain/Loss, and all subtotals andtotals.

For any section 1256 option contracts we are reporting to the IRS: 1a Description of Property and totals for boxes 8, 9, 10 and 11.

For any transaction listed on Form 1099-B in a section indicating that "basis is not reported to the IRS", we are reporting to the IRS: 1a Description of Property, 5 Noncovered security, 6 Gross or NetProceeds, and columns 1c, 1d, 4, 14, 15 and 16. We are not reporting to the IRS: 2 type of gain or loss (i.e. short-term or long-term), the Action, the Gain/Loss, columns 1b, 1e, 1f, 1g, 2, 3 and 7 and allsubtotals and totals.

Although Fidelity makes every effort to provide accurate information, please bear in mind that you, the taxpayer, are ultimately responsible for the accuracy of your tax returns.

(b) Cost or other basis provided may include adjustments including, but not limited to, dividend reinvestment, return of capital/principal, wash sale loss disallowed, amortization, accretion, acquisitionpremium, bond premium, market discount, market premium, and option premium.

(e) Your 1099-B reflects shares disposed of that were acquired through your employers stock plan. Cost basis associated with these shares may not have been adjusted for any compensation incomethat was associated with those shares in the year of acquisition or disposal. Please consult a tax advisor for the rules specific to your grant and plan. Refer to the Supplemental Stock Plan ServiceLot Detail section of this form for additional detail.

Amortization, accretion, and similar adjustments to cost basis are not provided for short-term instruments, unit investment trusts, or securities of foreign issuers.

Account No. XXX-XXXXXX Customer Service: XXX-XXX-XXXXRecipient ID No. XXX-XX-XXXX Payer’s Fed ID Number: XX-XXXXXXX1 32 65 74

Assemble information on the purchase and sale of your stock.

— Cost or Other Basis (this is provided to the IRS, as directed, and may need to be adjusted — see the Supplemental Form)

— Gain/Loss (from the proceeds of the sale and may also need to be adjusted — see the Supplemental Form)

* This is important tax information and is being furnished to the Internal Revenue Service. If you are required to file a return, a negligence penalty or other sanction may be imposed on youif this income is taxable and the IRS determines that it has not been reported.

2017 TAX REPORTING STATEMENT

10/12/2017 9001029539 Pages 4 of 8

Customer Service:Account No.MASKED NAME***-**-8644 Payer's Fed ID Number:

800-544-6666Recipient ID No. 04-3523567

X27-495794

0 0 0

FORM 1099-B* 2017 Proceeds from Broker and Barter Exchange Transactions Copy B for Recipient OMB No. XXXX-XXXX

Short-term transactions for which basis is reported to the IRS --report on Form 8949 with Box A checked and/or Schedule D, Part IProceeds are reported as gross proceeds unless otherwise indicated (a).(This Label is a Substitute for Boxes 2, 3, 5 & 6)

(IRS Form 1099-B box numbers are shown below in bold type)

1a Description of property, Stock or Other Symbol, CUSIP

TOTALS 42,500.73 31,904.53 0.00 0.00 0.00Box A Short-Term Realized Gain 10,596.20Box A Short-Term Realized Loss 0.00

For any transaction listed on Form 1099-B in a section indicating that "basis is reported to the IRS", we are reporting to the IRS: 1a Description of Property, 2 type of gain or loss (i.e. short-term orlong-term), 3 basis reported to IRS, 6 Gross or Net Proceeds, and columns 1b, 1c, 1d, 1e, 1f, 1g, 4, 7, 14, 15 and 16. We are not reporting to the IRS: the Action, the Gain/Loss, and all subtotals andtotals.

For any section 1256 option contracts we are reporting to the IRS: 1a Description of Property and totals for boxes 8, 9, 10 and 11.

For any transaction listed on Form 1099-B in a section indicating that "basis is not reported to the IRS", we are reporting to the IRS: 1a Description of Property, 5 Noncovered security, 6 Gross or NetProceeds, and columns 1c, 1d, 4, 14, 15 and 16. We are not reporting to the IRS: 2 type of gain or loss (i.e. short-term or long-term), the Action, the Gain/Loss, columns 1b, 1e, 1f, 1g, 2, 3 and 7 and allsubtotals and totals.

Although Fidelity makes every effort to provide accurate information, please bear in mind that you, the taxpayer, are ultimately responsible for the accuracy of your tax returns.

(b) Cost or other basis provided may include adjustments including, but not limited to, dividend reinvestment, return of capital/principal, wash sale loss disallowed, amortization, accretion, acquisitionpremium, bond premium, market discount, market premium, and option premium.

(e) Your 1099-B reflects shares disposed of that were acquired through your employers stock plan. Cost basis associated with these shares may not have been adjusted for any compensation incomethat was associated with those shares in the year of acquisition or disposal. Please consult a tax advisor for the rules specific to your grant and plan. Refer to the Supplemental Stock Plan ServiceLot Detail section of this form for additional detail.

Amortization, accretion, and similar adjustments to cost basis are not provided for short-term instruments, unit investment trusts, or securities of foreign issuers.

Account No. XXX-XXXXXX Customer Service: XXX-XXX-XXXXRecipient ID No. XXX-XX-XXXX Payer’s Fed ID Number: XX-XXXXXXX

54

4Incentive Stock Option Plan

33 Assemble information on the purchase and sale of your stock.

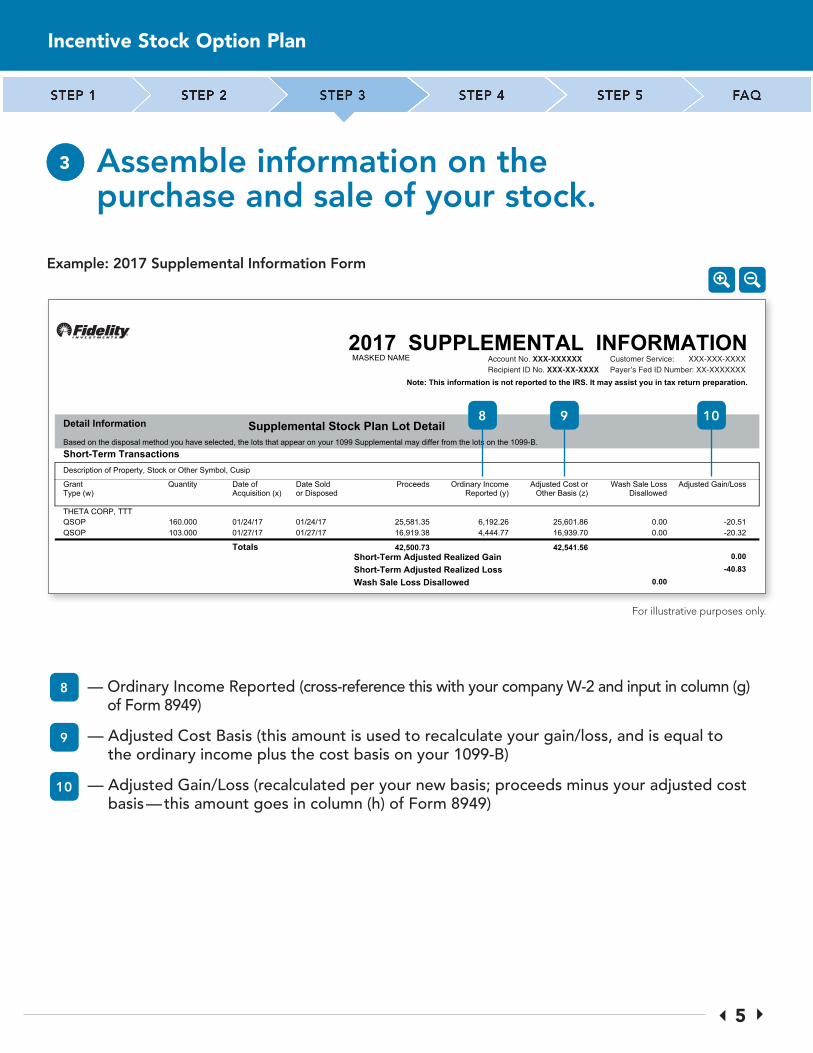

Example: 2017 Supplemental Information Form

For illustrative purposes only.

8 — Ordinary Income Reported (cross-reference this with your company W-2 and input in column (g) of Form 8949)

— Adjusted Cost Basis (this amount is used to recalculate your gain/loss, and is equal to the ordinary income plus the cost basis on your 1099-B)

— Adjusted Gain/Loss (recalculated per your new basis; proceeds minus your adjusted cost basis — this amount goes in column (h) of Form 8949)

9

10

Note: This information is not reported to the IRS. It may assist you in tax return preparation.

2017 SUPPLEMENTAL INFORMATION

10/12/2017 9001029539 Pages 7 of 8

Customer Service:Account No.MASKED NAME***-**-8644 Payer's Fed ID Number:

800-544-6666Recipient ID No. 04-3523567

X27-495794

0

Detail Information Supplemental Stock Plan Lot DetailBased on the disposal method you have selected, the lots that appear on your 1099 Supplemental may differ from the lots on the 1099-B.Short-Term TransactionsDescription of Property, Stock or Other Symbol, Cusip

Totals 42,500.73 42,541.56Short-Term Adjusted Realized Gain 0.00Short-Term Adjusted Realized Loss -40.83Wash Sale Loss Disallowed 0.00

(w) Grant Type describes the equity award source of the lot you sold this tax year. Please see the Grant Type table for additional description.xxxxxx

Grant Type Equity Award Type Acquisition date represents:DO Deposit Only Shares Deposit DateNQSOP Non Qualified Stock Option Shares Exercise DateNQSP Non Qualified ESPP Shares Purchase DateNSR Non-Incentive SAR (NSR) Exercise DateQSOP Qualified Stock Option Shares Exercise DateQSP Qualified ESPP Shares Purchase DateRSA Restricted Awards Vesting DateRSU Restricted Units Distribution DateRSU Performance Units Distribution DateRSU Total Shareholder Return Units Distribution DateSAR Stock Appreciation Rights Exercise Datexxxxxxxxxxxx

(x) Date of Acquisition is the date that shares were acquired from your Equity Plan and deposited into your brokerage account.

Account No. XXX-XXXXXX Customer Service: XXX-XXX-XXXXRecipient ID No. XXX-XX-XXXX Payer’s Fed ID Number: XX-XXXXXXX

9 108

64

4

Use the forms to calculate your capital gains and/or losses on IRS Form 8949 and Schedule D.

4

Even though the ordinary income may be reported on your W-2, you still need to report the sale of the stock on Form 8949 and carry over the amounts to Schedule D.*

In preparation for completing these forms, consider the following:

1. How long did you hold the shares before you sold them? This determines which section of Form 8949 to complete. Your holding period begins on the day after you exercised your option.

Form 8949 is divided into two parts. Determine which section you will need to complete:

• Part I is for short-term capital gains or losses. Short term is defined as selling the stock less than one year from the date you acquired it.

• Part II is for long-term capital gains and losses. Long term is defined as holding the stock for more than one year from the date you acquired it.

2. Does the cost basis on your 1099-B match the amount on your Supplemental Form? If it doesn’t, you may need to make an adjustment on Form 8949. This is because you may have already paid tax on your ordinary income (as reported on your W-2) and you don’t want to pay taxes twice.

*State and local taxes may also apply and the rules governing such taxes may vary from federal income tax rules. Please consult your tax advisor.

Continues

Incentive Stock Option Plan

For illustrative purposes only.

Use the forms to calculate your capital gains and/or losses on IRS Form 8949.

4

74

4

Example: ISO exercise and subsequent sale within one year as a disqualifying disposition (short term)

Continues

Incentive Stock Option Plan

To complete Form 8949 and Schedule D, you need to know:

• Which shares you sold from which grant

• When you acquired those shares (i.e., the exercise date)

• The fair market value of the stock at exercise

• The date of sale

• The sale price and whether it is net of commission

• Your cost basis

• Amount of ordinary income (from the Supplemental Form)

Use the forms to calculate your capital gains and/or losses on IRS Form 8949.

4

84

4

Continues

Incentive Stock Option Plan

For illustrative purposes only.

To complete Form 8949 and Schedule D, you need to know:

• Which shares you sold from which grant

• When you acquired those shares (i.e., the exercise date)

• The fair market value of the stock at exercise

• The date of sale

• The sale price and whether it is net of commission

• Your cost basis

• Amount of ordinary income (from the Supplemental Form)

Example: ISO exercise and subsequent sale after one year as a disqualifying disposition (long term)

Use the forms to calculate your capital gains and/or losses on IRS Form 8949.

4

94

4Incentive Stock Option Plan

For illustrative purposes only.

To complete Form 8949 and Schedule D, you need to know:

• Which shares you sold from which grant

• When you acquired those shares (i.e., the exercise date)

• The fair market value of the stock at exercise

• The date of sale

• The sale price and whether it is net of commission

• Your cost basis

• Amount of ordinary income (from the Supplemental Form)

Example: ISO exercise and subsequent sale after one year as a qualifying disposition (long term)

Use IRS Form 8949 to calculate your capital gains and/or losses on Schedule D.

5

104

4

Gain or loss from the sale of the stock should be reflected on Form 8949 and Schedule D. How this is reflected depends on whether the sale is short term (less than one year from the date the stock was acquired to the date it was sold) or long term (more than one year from the date acquired to the date it was sold).

For illustrative purposes only.

For illustrative purposes only.

Example: Short-Term Gains or Losses

Example: Long-Term Gains or Losses

Incentive Stock Option Plan

Frequently Asked QuestionsQ: Does the tax-reform legislation adopted in December 2017 affect my 2017 taxes?

A: No. The tax-reform legislation adopted in December 2017 does not affect the 2017 tax year or the federal tax return for 2017 that you file in 2018.

Q: How do the tax implications of an ISO differ from those of a nonqualified stock option (NSO)?

A: An ISO can potentially receive beneficial tax treatment. You will not be subject to tax at the time of exercise of an ISO (although the difference between the fair market value of the stock at exercise and the amount you paid for the stock will be treated as taxable income for alternative minimum tax purposes when you hold the shares through the calendar year of the exercise). When you sell shares acquired by exercise of an ISO, your gain (or loss) will be treated as a capital gain (or loss), provided the shares are held for more than one year from the exercise date and two years from the grant date.

When shares are not held long enough, the amount of ordinary income depends on the sale price relative to the market price on the exercise date. If ISO shares exercised are held for the entire holding period, then the entire amount of any gain (or loss) over the exercise price will be treated as a capital gain upon the subsequent sale of those shares (generally, a long-term capital gain, given the holding period requirement for ISOs), and taxed at the favorable rates applicable to capital gains, rather than as ordinary income.*

In contrast, when you exercise an NSO, the difference between the fair market value of the stock at the time of exercise and your exercise cost will be treated as ordinary compensation income, and your employer will generally be required to withhold taxes at the time of your exercise. Upon your sale of the stock (whether at the time of exercise or some later date), your gain or loss (the sale proceeds minus your adjusted basis in the stock) will be subject to tax as a capital gain (or loss).

Q: What is alternative minimum tax or AMT?

A: Congress created the AMT as an alternative form of federal income taxation to ensure that wealthy individuals and corporate taxpayers pay a fair share of federal income taxes. Its reach, however, now sometimes extends beyond the wealthy.

The AMT is a tax system that works in parallel with the regular federal income tax system — while some taxpayers use the regular system, others must use the AMT system. The AMT has its own set of forms, rates, rules, and brackets. It requires taxpayers to calculate their federal income tax using both systems and then pay the higher amount.

114

4*Please see a tax advisor as to your specific tax amounts due.

Continues

Incentive Stock Option Plan

Frequently Asked Questions

124

4

Continues

Incentive Stock Option Plan

Exercising ISOs that are “deep in the money” (on which gain at exercise is usually deferrable and taxed as capital gain income at the time of sale) can potentially subject an individual to AMT. Once you have triggered the AMT for your ISO exercise, you will have an AMT credit and will also need to follow special reporting rules when you sell the ISO stock. You will want to discuss this with a qualified tax advisor to see if this applies to you.

Q: What is a “qualified disposition” and “disqualified disposition,” with respect to an ISO?

A: Your ISO plan qualifies for special tax treatment if you hold your shares for a certain period of time.

Qualified Disposition:

Favorable tax treatment is received when two time periods are met. First, shares you acquired must be sold more than two years from the grant date.† Second, the sale should occur more than one year after the exercise date of the option.

Disqualified Disposition:

This occurs when you sell the shares acquired within the first two years of the grant date† or less than one year from the exercise date.

When did you exercise your options and when did you sell those shares?

For Example: Grant date: 1/1/2015 Date you exercised your options: 2/3/2016Date you sold these shares: 1/2/2017

You have a disqualified disposition because even though you sold two years after the grant date, it was not yet a year after the exercise date.{

† If you are unsure of the grant date, check the NetBenefits website for your grant details.

Year 1 Year 2 Year 3

Disqualified Disposition Qualified Disposition

Purchase DateGrant Date Sold

2/3/20161/1/2015 1/2/2017

Frequently Asked QuestionsQ: Why do my tax forms show a capital loss from my exercise?

A: Generally speaking, a loss on a 1099-B and 8949 is usually a result of any market-related loss on the stock sale and/or any commissions and fees charged.

Q: What is a wash sale?

A: A wash sale occurs when you sell shares at a loss and buy additional shares of the same security within a 61-day period, beginning 30 days before the sale and ending 30 days after the sale, including the date of the sale. If the sale results in a wash sale, generally, you will not be able to deduct the resulting loss. Instead, the loss and the holding period will be carried over to increase the basis of the new shares. Sales of stock received in an ISO exercise raise additional issues under the wash sale rules when the sale price is above the exercise price but below the market price at exercise. For assistance with completing your tax return, please consult your tax advisor.

Q: Will I owe other taxes beyond federal tax when I sell my stock?

A: State and local taxes may also apply, and the rules governing such taxes may vary from federal income tax rules. Please consult your tax advisor for more information.

Go back to the Fidelity SPS Resource Center

Tax laws are complex and subject to change. State and local taxes may also apply, and the rules governing such taxes may vary from federal income tax rules. Your actual income tax consequences depend on your individual circumstances. Therefore, you should always consult a qualified tax advisor regarding your particular tax situation.