FINANCIAL INSTITUTIONS CREDIT OPINION 11 February 2019 Update RATINGS Deutsche Bank AG Domicile Frankfurt am Main, Germany Long Term CRR A3 Type LT Counterparty Risk Rating - Fgn Curr Outlook Not Assigned Long Term Debt A3 Type Senior Unsecured - Fgn Curr Outlook Negative Long Term Deposit A3 Type LT Bank Deposits - Fgn Curr Outlook Negative Please see the ratings section at the end of this report for more information. The ratings and outlook shown reflect information as of the publication date. Contacts Michael Rohr +49.69.70730.901 VP-Sr Credit Officer [email protected]Peter E. Nerby, CFA +1.212.553.3782 Senior Vice President [email protected]Yana Ruvinskaya +44.20.7772.1618 Associate Analyst [email protected]Laurie Mayers +44.20.7772.5582 Associate Managing Director [email protected]» Contacts continued on last page Deutsche Bank AG Semiannual update Summary We assign A3 (negative) deposit and senior unsecured debt ratings to Deutsche Bank AG (DB). We also assign Baa3 junior senior unsecured debt ratings and an A3 Counterparty Risk Rating (CRR), as well as a ba1 Baseline Credit Assessment (BCA) and Adjusted BCA to DB. DB's ratings reflect (1) its ba1 BCA and Adjusted BCA; (2) the results of the amended application of our Advanced Loss Given Failure (LGF) analysis, which provides three notches of rating uplift for deposits and senior unsecured debt, as well as one notch for its junior senior unsecured debt; and (3) our assumption of a moderate probability of government support for the bank's deposits and senior unsecured debt ratings, leading to the assignment of one additional notch of rating uplift for these debt classes. DB’s BCA reflects (1) the bank’s challenges in executing on its multi-year restructuring program; and (2) the bank's low profitability, which we only expect to improve gradually from the levels achieved in 2018. The BCA further reflects (1) DB's sound asset quality displaying a moderate volume of problem loans and manageable exposures to highly cyclical lending arrangements; (2) its sound capitalisation displaying a Common Equity Tier 1 (CET1) ratio of 13.6% as of year-end 2018; and (3) its solid liquidity profile supported by a meaningful volume of highly liquid assets offsetting potential strain resulting from the bank's moderate reliance on confidence-sensitive wholesale funding sources. Exhibit 1 Rating Scorecard Deutsche Bank AG - Key financial ratios 2.4% 15.1% 0.0% 33.1% 52.6% 0% 10% 20% 30% 40% 50% 60% 0% 2% 4% 6% 8% 10% 12% 14% 16% Asset Risk: Problem Loans/ Gross Loans Capital: Tangible Common Equity/Risk-Weighted Assets Profitability: Net Income/ Tangible Assets Funding Structure: Market Funds/ Tangible Banking Assets Liquid Resources: Liquid Banking Assets/Tangible Banking Assets Solvency Factors (LHS) Liquidity Factors (RHS) Deutsche Bank (BCA: ba1) Median ba1-rated banks Solvency Factors Liquidity Factors Source: Moody's Investors Service

Transcript

FINANCIAL INSTITUTIONS

CREDIT OPINION11 February 2019

Update

RATINGS

Deutsche Bank AGDomicile Frankfurt am Main,

Germany

Long Term CRR A3

Type LT Counterparty RiskRating - Fgn Curr

Outlook Not Assigned

Long Term Debt A3

Type Senior Unsecured - FgnCurr

Outlook Negative

Long Term Deposit A3

Type LT Bank Deposits - FgnCurr

Outlook Negative

Please see the ratings section at the end of thisreport for more information. The ratings andoutlook shown reflect information as of thepublication date.

SummaryWe assign A3 (negative) deposit and senior unsecured debt ratings to Deutsche Bank AG(DB). We also assign Baa3 junior senior unsecured debt ratings and an A3 Counterparty RiskRating (CRR), as well as a ba1 Baseline Credit Assessment (BCA) and Adjusted BCA to DB.

DB's ratings reflect (1) its ba1 BCA and Adjusted BCA; (2) the results of the amendedapplication of our Advanced Loss Given Failure (LGF) analysis, which provides three notchesof rating uplift for deposits and senior unsecured debt, as well as one notch for its juniorsenior unsecured debt; and (3) our assumption of a moderate probability of governmentsupport for the bank's deposits and senior unsecured debt ratings, leading to the assignmentof one additional notch of rating uplift for these debt classes.

DB’s BCA reflects (1) the bank’s challenges in executing on its multi-year restructuringprogram; and (2) the bank's low profitability, which we only expect to improve gradually fromthe levels achieved in 2018. The BCA further reflects (1) DB's sound asset quality displayinga moderate volume of problem loans and manageable exposures to highly cyclical lendingarrangements; (2) its sound capitalisation displaying a Common Equity Tier 1 (CET1) ratioof 13.6% as of year-end 2018; and (3) its solid liquidity profile supported by a meaningfulvolume of highly liquid assets offsetting potential strain resulting from the bank's moderatereliance on confidence-sensitive wholesale funding sources.

Exhibit 1

Rating Scorecard Deutsche Bank AG - Key financial ratios

Deutsche Bank's BCA is supported by its Weighted Macro Profile of Strong (+)Deutsche Bank's Strong (+) Weighted Macro Profile is mainly driven by its exposure to Germany (Aaa stable) and the United States(Aaa stable), to which we assign a Very Strong (-) Macro Profiles, partly offset by its exposures to other EU countries with a less benignoperating environment, such as Spain (Baa1 stable) and Italy (Baa3 stable).

As the largest private-sector bank in Germany, Deutsche Bank benefits from an environment with very high economic, institutionaland government financial strength and very low susceptibility to event risk. Operating conditions for the German banking system are,however, constrained by overly high cost bases, high fragmentation in an over-saturated market, persistently very low interest rates,modest fee income generation and strong competition for domestic business.

Credit strengths

» Solid capital and improved leverage position help mitigate tail risks

» Strong balance sheet liquidity

Credit challenges

» Significant execution challenges relating to strategic reengineering

» Meaningful ongoing reliance on capital markets activities, despite right-sizing

» Weak efficiency ratios and very modest overall profitability

Rating outlook

» The negative outlook on the bank's senior unsecured and deposit ratings reflects persistently high execution challenges at DB,highlighted by 2018 senior management changes, strategic shifts and ongoing weak financial performance.

Factors that could lead to an upgrade

» The negative outlook indicates there is no imminent upward pressure on DB ratings.

» In the longer term, however, upward pressure on the bank's ba1 BCA could emerge if (1) DB substantially completed its strategicplan, resulting in a meaningfully improved and more stable earnings profile; (2) the bank maintained its solid capitalisation andfurther improved its currently sub-par leverage ratio; and (3) DB materially decreased its moderate reliance on wholesale fundingsources, in particular if coupled with the maintenance of a highly liquid balance sheet.

Factors that could Lead to a downgrade

» Downward pressure on the bank's ba1 BCA could be exerted if (1) DB failed to make consistent progress towards the long-termtarget business mix and expense targets; (2) its combined liquidity profile significantly weakened; or (3) its asset quality and capitaladequacy metrics significantly deteriorated. In addition, the ratings could be negatively affected if the bank experienced a materialrisk management failure.

» Moreover, downward rating pressure on the bank's junior senior unsecured ratings could result from a meaningful and sustaineddecrease in the volume of this debt class, leading to a higher loss severity of DB's junior senior unsecured liabilities at failure,potentially resulting in a lower rating uplift as a result of our Advanced LGF analysis (currently one notch).

This publication does not announce a credit rating action. For any credit ratings referenced in this publication, please see the ratings tab on the issuer/entity page onwww.moodys.com for the most updated credit rating action information and rating history.

2 11 February 2019 Deutsche Bank AG: Semiannual update

Gross Loans / Due to Customers (%) 72.1 72.0 79.5 79.8 80.7 76.85

[1] All figures and ratios are adjusted using Moody's standard adjustments. [2] Basel III - fully-loaded or transitional phase-in; IFRS. [3] May include rounding differences due to scaleof reported amounts. [4] Compound Annual Growth Rate (%) based on time period presented for the latest accounting regime. [5] Simple average of periods presented for the latestaccounting regime. [6] Simple average of Basel III periods presented.Source: Moody's Financial Metrics

Detailed credit considerationsOur assigned baa3 Asset Risk score incorporates the execution risks associated with Deutsche Bank's ongoing reengineering program;as well as the market, credit and operational risks and periodic concentration risks inherent to Deutsche Bank's capital market activities.

Significant execution challenges relating to strategic reengineeringDeutsche Bank has been and is still engaged in a multi-year undertaking to simplify its businesses, fortify its controls and stabilizeits earnings. As a result, its earnings volatility has been higher than many of its global investment banking peers, given heightenedrestructuring and litigation costs and the drag of its former non-core legacy portfolio.

The replacement of the CEO, departure of other senior executives and the abrupt change in the direction of the investment bank inearly 2018 highlighted the ongoing strategic turmoil within the bank, exacerbated by weak profitability in 2017 and in 2018. The keychallenge for DB going forward is and remains to successfully reshape and right-size the investment bank1, becoming more focusedon European clients and – at the same time – compete effectively against more diversified global peers, while also earning acceptablereturns over the cycle.

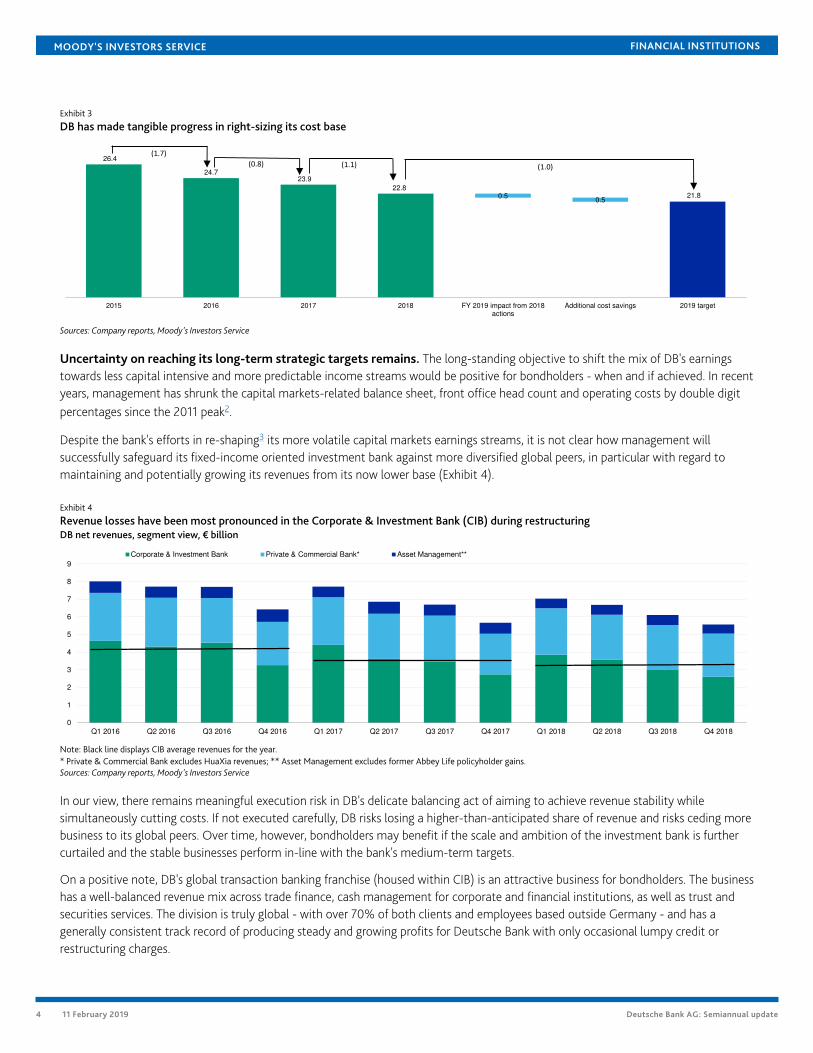

Progress has been made in achieving some of the announced targets. For 2018, DB reported adjusted costs of €22.8 billion,below its initial target of €23 billion (Exhibit 3). The bank further reduced its staff levels to below 91,800 full-time equivalents againstits original target of less than 93,000. This will support the bank's progress on costs and put it in a good position to meet its recentlylowered €21.8 billion adjusted cost target for 2019. DB further reported a CET1 ratio of 13.6% as of year-end 2018, above its 13%medium-term target.

3 11 February 2019 Deutsche Bank AG: Semiannual update

MOODY'S INVESTORS SERVICE FINANCIAL INSTITUTIONS

Exhibit 3

DB has made tangible progress in right-sizing its cost base

26.4

24.723.9

22.821.80.5

0.5

2015 2016 2017 2018 FY 2019 impact from 2018actions

Additional cost savings 2019 target

(1.0)5

(1.7)5

(1.1)5(0.8)5

Sources: Company reports, Moody's Investors Service

Uncertainty on reaching its long-term strategic targets remains. The long-standing objective to shift the mix of DB's earningstowards less capital intensive and more predictable income streams would be positive for bondholders - when and if achieved. In recentyears, management has shrunk the capital markets-related balance sheet, front office head count and operating costs by double digitpercentages since the 2011 peak2.

Despite the bank's efforts in re-shaping3 its more volatile capital markets earnings streams, it is not clear how management willsuccessfully safeguard its fixed-income oriented investment bank against more diversified global peers, in particular with regard tomaintaining and potentially growing its revenues from its now lower base (Exhibit 4).

Exhibit 4

Revenue losses have been most pronounced in the Corporate & Investment Bank (CIB) during restructuringDB net revenues, segment view, € billion

Corporate & Investment Bank Private & Commercial Bank* Asset Management**

Note: Black line displays CIB average revenues for the year.* Private & Commercial Bank excludes HuaXia revenues; ** Asset Management excludes former Abbey Life policyholder gains.Sources: Company reports, Moody's Investors Service

In our view, there remains meaningful execution risk in DB's delicate balancing act of aiming to achieve revenue stability whilesimultaneously cutting costs. If not executed carefully, DB risks losing a higher-than-anticipated share of revenue and risks ceding morebusiness to its global peers. Over time, however, bondholders may benefit if the scale and ambition of the investment bank is furthercurtailed and the stable businesses perform in-line with the bank's medium-term targets.

On a positive note, DB's global transaction banking franchise (housed within CIB) is an attractive business for bondholders. The businesshas a well-balanced revenue mix across trade finance, cash management for corporate and financial institutions, as well as trust andsecurities services. The division is truly global - with over 70% of both clients and employees based outside Germany - and has agenerally consistent track record of producing steady and growing profits for Deutsche Bank with only occasional lumpy credit orrestructuring charges.

4 11 February 2019 Deutsche Bank AG: Semiannual update

MOODY'S INVESTORS SERVICE FINANCIAL INSTITUTIONS

In addition, the (re-)integration of Deutsche Bank’s German banking operations may eventually bring bondholder benefits in the formof fungible liquidity across the bank, as well as a greater contribution of earnings from German retail banking, bringing more balanceto the business mix. Refocusing the Private and Commercial Banking (PCB) franchise aims to achieve greater profitability through costreduction and product simplification. In 2018, core revenues (excluding one offs and the impact of business disposals) of the divisionwere mostly flat compared with last year. DB's 65% segmental cost-to-income ratio target will nevertheless remain very difficult toachieve: DB reported an 88% cost-to-income ratio for the PCB segment in 2018; this compares with the German banks' average cost-to-income ratio of 76% as of year-end 2017.

Qualitative adjustments capture strategic uncertainties and continued reliance on capital markets activities. Recent seniormanagement changes and strategic shifts highlight the execution challenges and strategic uncertainty facing the bank, and arereflected in a one-notch negative adjustment for 'Corporate Behavior' in our Scorecard.

In addition, DB has a heavy reliance on capital markets activities for income generation: Capital markets revenue accounted forapproximately 40% of Deutsche Bank’s total revenues in 2018. We generally consider capital markets activities to be both opaque andpotentially volatile, posing significant challenges for the management of such activities. These structural challenges continue to resultin a one-notch negative qualitative adjustment to DB's BCA in respect of remaining 'Opacity and Complexity', an adjustment sharedwith all large global investment banks (GIBs) at present.

Solid capital and improved leverage position help mitigate tail risksDB’s substantial progress in running off legacy assets, settling litigation and raising equity has improved the capital position of the bank,although the firm’s relatively weak leverage ratio compared to peers remains an ongoing challenge to capital adequacy. This is reflectedin our five-notch negative adjustment to the bank's initial aa3 Capital score, resulting in an assigned baa2 Capital score.

DB's fully loaded CET1 ratio stood at 13.6% as of the end of 2018 (Exhibit 5). As of the same date, however, and despite havingimproved steadily, the firm's leverage ratio of 4.1% remained at the low end compared to its GIBs peers. DB left unchanged itsmedium-term strategic target of 4.5% for the leverage ratio.

Exhibit 5

Common Equity Tier 1 (CET1) ratio and Tier 1 Leverage Ratio for Moody's-rated GIBs, as of 31 December 2018

17.0%

14.3%13.6%

13.1% 13.2% 13.1% 12.9% 12.9% 12.3%

11.9% 11.7% 11.5% 11.2%

6.5%

5.4%

4.1%

5.2% 4.9%

6.2% 6.4%

5.1%

6.4%6.8%

4.0%

4.4%

4.1%

0.0%

3.0%

6.0%

9.0%

12.0%

15.0%

18.0%

MS HSBC DB UBS* BCS** GS JPM CS* C BAC BNP RBC SG

CET1 ratio Tier 1 Leverage ratio Median CET1 ratio (12.9%) Median leverage ratio (5.2%)

Notes: (1) As of Q4 2018 for Bank of America, Citigroup, Deutsche Bank, Goldman Sachs and JPMorgan and Morgan Stanley which have reported Q4 earnings, and for RBC whose thirdquarter ended in October 2018; Q3 2018 for the rest; (2) Basel III fully phased in advanced approach for all US banks. Citi has only reported CET1 ratio under the standardized approachwhich is the binding constraint. The CET1 ratio under the advanced approach shown in the chart is Moody’s estimate; (3) Tier 1 leverage ratio for US banks is the supplemental leverageratio (SLR).*UBS and CS leverage ratio reflect Common Equity Tier plus Low Trigger Additional Tier 1 and High-Trigger Additional Tier 1 securities.**Barclays leverage is reflective of the spot UK leverage ratio.Sources: Company reports, Moody's Investors Service

As well as raising capital twice in prior years, Deutsche Bank has resolved several litigation proceedings that posed large tail risks forbondholders, thereby meaningfully enhancing its financial flexibility. Most notably, in December 2016, Deutsche Bank settled with theUS Department of Justice (DoJ) regarding residential mortgage backed securities (RMBS). Total litigation reserves stood at €1.2 billionat end-2018 and the amount of reasonably possible contingent liabilities stood at €2.7 billion as of the same date.

5 11 February 2019 Deutsche Bank AG: Semiannual update

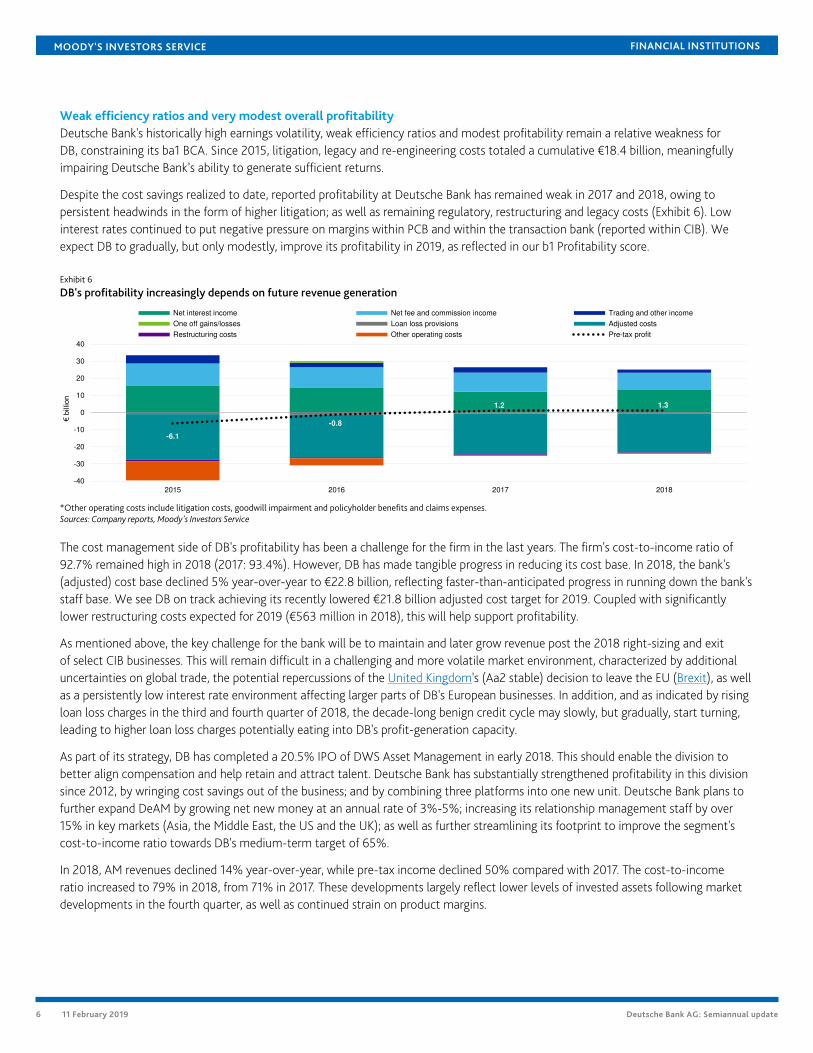

Weak efficiency ratios and very modest overall profitabilityDeutsche Bank's historically high earnings volatility, weak efficiency ratios and modest profitability remain a relative weakness forDB, constraining its ba1 BCA. Since 2015, litigation, legacy and re-engineering costs totaled a cumulative €18.4 billion, meaningfullyimpairing Deutsche Bank’s ability to generate sufficient returns.

Despite the cost savings realized to date, reported profitability at Deutsche Bank has remained weak in 2017 and 2018, owing topersistent headwinds in the form of higher litigation; as well as remaining regulatory, restructuring and legacy costs (Exhibit 6). Lowinterest rates continued to put negative pressure on margins within PCB and within the transaction bank (reported within CIB). Weexpect DB to gradually, but only modestly, improve its profitability in 2019, as reflected in our b1 Profitability score.

Exhibit 6

DB's profitability increasingly depends on future revenue generation

-6.1

-0.8

1.2 1.3

-40

-30

-20

-10

0

10

20

30

40

2015 2016 2017 2018

€ bi

llion

Net interest income Net fee and commission income Trading and other income

One off gains/losses Loan loss provisions Adjusted costs

Restructuring costs Other operating costs Pre-tax profit

*Other operating costs include litigation costs, goodwill impairment and policyholder benefits and claims expenses.Sources: Company reports, Moody's Investors Service

The cost management side of DB's profitability has been a challenge for the firm in the last years. The firm's cost-to-income ratio of92.7% remained high in 2018 (2017: 93.4%). However, DB has made tangible progress in reducing its cost base. In 2018, the bank's(adjusted) cost base declined 5% year-over-year to €22.8 billion, reflecting faster-than-anticipated progress in running down the bank'sstaff base. We see DB on track achieving its recently lowered €21.8 billion adjusted cost target for 2019. Coupled with significantlylower restructuring costs expected for 2019 (€563 million in 2018), this will help support profitability.

As mentioned above, the key challenge for the bank will be to maintain and later grow revenue post the 2018 right-sizing and exitof select CIB businesses. This will remain difficult in a challenging and more volatile market environment, characterized by additionaluncertainties on global trade, the potential repercussions of the United Kingdom's (Aa2 stable) decision to leave the EU (Brexit), as wellas a persistently low interest rate environment affecting larger parts of DB's European businesses. In addition, and as indicated by risingloan loss charges in the third and fourth quarter of 2018, the decade-long benign credit cycle may slowly, but gradually, start turning,leading to higher loan loss charges potentially eating into DB's profit-generation capacity.

As part of its strategy, DB has completed a 20.5% IPO of DWS Asset Management in early 2018. This should enable the division tobetter align compensation and help retain and attract talent. Deutsche Bank has substantially strengthened profitability in this divisionsince 2012, by wringing cost savings out of the business; and by combining three platforms into one new unit. Deutsche Bank plans tofurther expand DeAM by growing net new money at an annual rate of 3%-5%; increasing its relationship management staff by over15% in key markets (Asia, the Middle East, the US and the UK); as well as further streamlining its footprint to improve the segment'scost-to-income ratio towards DB's medium-term target of 65%.

In 2018, AM revenues declined 14% year-over-year, while pre-tax income declined 50% compared with 2017. The cost-to-incomeratio increased to 79% in 2018, from 71% in 2017. These developments largely reflect lower levels of invested assets following marketdevelopments in the fourth quarter, as well as continued strain on product margins.

6 11 February 2019 Deutsche Bank AG: Semiannual update

Strong liquidity position and sound funding profileWe assign a ba1 Funding Structure score to DB, in line with the bank's initial score. This captures our expectation that the group'smoderate dependence on market funding will remain unchanged over the next 12-18 months. We view positively DB's sustained andsignificantly diminished refinancing risk compared with the years before its de-risking and restructuring programme, supporting thebuild-up of a more liquid balance sheet (Exhibit 7).

DB's funding largely consists of €565 billion of customer deposits (of which approximately 55% were granular retail deposits),constituting 56% of its net liabilities (including equity) as of 31 December 2018. Debt capital market funds outstanding totaled €166billion, equivalent to around 16% of net liabilities. During 2018, DB issued €20 billion of capital market funding with longer tenors ofslightly above six years on average (equivalent to approximately 1.5% of its average total balance sheet) to fund business growth andreplace maturing senior (mostly non-preferred) debt. The remainder of the funds was sourced in the interbank markets and is mostlyused to finance assets of similar tenors, as well as to support the bank's large trade finance and market making activities.

Exhibit 7

DB's balance sheet is highly liquid, a credit positive

50

405

296

64

166

45

565

76

184 170

Other Assets

Loans to customers

Highly liquid securities

Trading assetsReverse repos and securities borrowed

Cash and equivalents

Deposits

Brokerage paybales

Trading liabilities

Long-term debt

Other liabilities

Equity

Liquidity reserves

77% loan-to-deposit ratio

€1,010 billion €1,010 billion

DerivativesBrokerage recievables

Derivatives

Sources: DB Fixed Income Investor Presentation (4 February 2019), Moody's Investors Service

With a high stock of loss-absorbing debt comfortably exceeding the minimum levels stipulated under the EU's MREL4 by a wide margin(2018 excess: €21 billion), DB may replace some maturing junior senior unsecured debt with less costly preferred senior unsecured debtover time; or simply issue less junior senior unsecured debt. This could potentially lead to a higher loss severity for DB's junior seniorunsecured debt, and – if sustained over the medium-term – the subsequent reduction of the one notch of rating uplift assigned to thisdebt class as a result of our Advanced LGF analysis.

Sound liquidity profileThe aa3 Liquid Resources score we assign to DB is in line with its initial score and captures the bank's generally solid liquidity profile,that has strengthened considerably since management accelerated the pace of balance sheet restructuring in 2015.

Since 2015, DB’s total assets have declined 17%, central bank balances have more than doubled, and the loan-to-deposit ratio(Moody's adjusted) has declined five percentage points to around 71%. As a result, the firm currently maintains significant excess ofshort-term liquidity as required by the LCR5 (2018 excess: €66 billion). Considering its regulatory surplus, management may considerreducing some of this surplus liquidity, to reduce the associated negative carry and strengthen Deutsche Bank’s overall profitability.

The bank held €184 billion of cash reserves on its balance sheet as of 31 December 2018. DB's liquid asset ratio of approximately 45%is further supported by the bank's relatively large portion of highly liquid securities totaling an additional €76 billion as of the samedate.

Overall, we believe DB's funding and liquidity profiles are well balanced because liquid unencumbered assets exceed market funds,supporting our overall baa1 Combined Liquidity score. The score further highlights funding and liquidity as a relative strength for theBCA.

7 11 February 2019 Deutsche Bank AG: Semiannual update

Support and structural considerationsLGF analysisDeutsche Bank is subject to the Bank Recovery and Resolution Directive (BRRD), which we consider an operational resolution regime.We, therefore, apply our Advanced LGF analysis, where we consider the risks faced by the different debt and deposit classes across theliability structure should the bank enter resolution.

Our Advanced LGF analysis follows the insolvency legislation in Germany. Following the change in law in June 2018, the legal hierarchyof bank claims in Germany is now consistent with most other EU countries, where statutes do not provide full preference to depositsover senior unsecured debt. In line with our standard assumptions, we assume a residual TCE of 3%, as well as asset losses of 8% oftangible banking assets in a failure scenario. We also assume a 25% run-off of junior wholesale deposits and a 5% run-off in preferreddeposits. Moreover, we assign a 25% probability to junior deposits being preferred to senior unsecured debt. We apply a standardassumption for European banks that 26% of deposits are junior.

The results of our Advanced LGF analysis are:

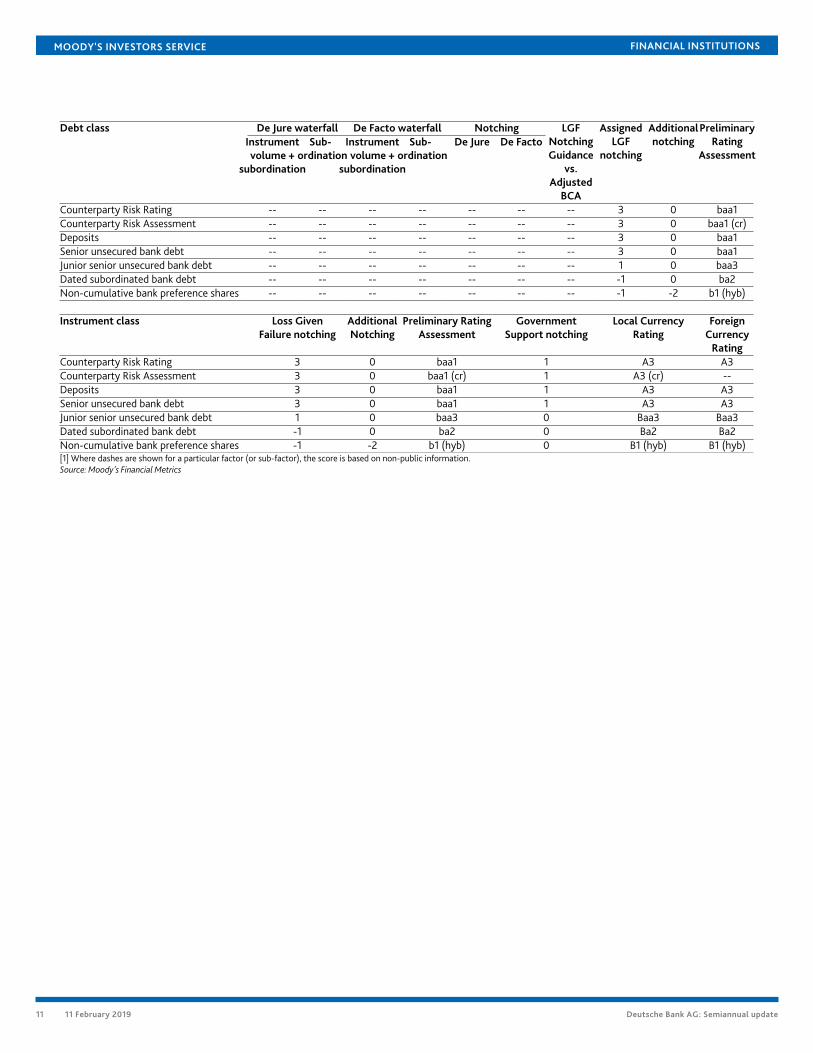

» For deposits and senior unsecured debt, our LGF analysis indicates an extremely low loss given failure, leading to three notches ofrating uplift from the bank's ba1 Adjusted BCA.

» For junior senior unsecured debt, our LGF analysis indicates a low loss given failure, leading to one notch of rating uplift from thebank's ba1 Adjusted BCA.

» For subordinated debt and junior securities issued by Deutsche Bank, our LGF analysis indicates a high loss given failure, giventhe small volume of debt and limited protection from more subordinated instruments and residual equity, leading to a one-notch deduction from the bank's ba1 Adjusted BCA. We also incorporate additional notching from the Adjusted BCA for juniorsubordinated and preference share instruments reflecting the coupon suspension risk ahead of potential failure.

Government supportWe assume a moderate probability of government support for both deposits and senior unsecured debt of Deutsche Bank, which weconsider a domestic systemically important financial institution, resulting in one notch of additional rating uplift. For junior seniorunsecured debt6, subordinated debt and hybrid instruments, we believe the potential for government support is low and these ratings,therefore, do not benefit from any government support uplift.

Counterparty Risk Ratings (CRRs)Our CRRs are opinions of the ability of entities to honour the uncollateralised portion of non-debt counterparty financial liabilities(CRR liabilities) and also reflect the expected financial losses in the event such liabilities are not honoured. Examples of CRR liabilitiesinclude the uncollateralised portion of payables arising from derivatives transactions and the uncollateralised portion of liabilitiesunder sale and repurchase agreements. CRRs are not applicable to funding commitments or other obligations associated with coveredbonds, letters of credit, guarantees, servicer and trustee obligations, and other similar obligations that arise from a bank performing itsessential operating functions.

Deutsche Bank's CRRs are positioned at A3/P-2The bank's CRRs, prior to government support, are positioned three notches above the ba1 Adjusted BCA, reflecting the extremelylow loss given failure from the high volume of instruments, primarily junior senior unsecured debt, which are subordinated to CRRliabilities. DB's CRRs further benefit from one additional notch of rating uplift provided by government support, in line with our supportassumptions on deposits and senior unsecured debt.

Counterparty Risk (CR) AssessmentOur CR Assessment is an opinion of how counterparty obligations are likely to be treated if a bank fails and is distinct from debt anddeposit ratings in that it (1) considers only the risk of default rather than both the likelihood of default and the expected financial losssuffered in the event of default, and (2) applies to counterparty obligations and contractual commitments rather than debt or depositinstruments. The CR Assessment is an opinion of the counterparty risk related to a bank's covered bonds, contractual performanceobligations (servicing), derivatives (for example, swaps), letters of credit, guarantees and liquidity facilities.

8 11 February 2019 Deutsche Bank AG: Semiannual update

Because the CR Assessment captures the probability of default on certain senior operational obligations, rather than expected loss, wefocus purely on subordination and take no account of the volume of the instrument class.

Deutsche Bank's CR Assessment is positioned at A3(cr)/P-2(cr)The bank's CR Assessment, prior to government support, is positioned three notches above the ba1 Adjusted BCA, based on thesubstantial buffer against default provided by more subordinated instruments, primarily junior senior unsecured debt, to the seniorobligations represented by the CR Assessment.

In addition, DB's CR Assessment benefits from one further notch of rating uplift provided by government support.his reflects our viewthat any support provided by governmental authorities to a bank which benefits deposits and senior senior debt is very likely to benefitoperating activities and obligations reflected by the CR Assessment as well, consistent with our belief that governments are likely tomaintain such operations as a going-concern in order to reduce contagion and preserve a bank's critical functions.

Methodology and ScorecardMethodologyThe principal methodology we use in rating Deutsche Bank AG is our Banks rating methodology, published in August 2018.

About Moody's Bank ScorecardOur Bank Scorecard is designed to capture, express and explain in summary form our Rating Committee's judgement. When readin conjunction with our research, a fulsome presentation of our judgement is expressed. As a result, the output of our scorecardmay materially differ from that suggested by raw data alone (though it has been calibrated to avoid the frequent need for strongdivergence). The scorecard output and the individual scores are discussed in rating committees and may be adjusted up or down toreflect conditions specific to each rated entity.

9 11 February 2019 Deutsche Bank AG: Semiannual update

Business Diversification 0Opacity and Complexity -1Corporate Behavior -1

Total Qualitative Adjustments -2Sovereign or Affiliate constraint: AaaScorecard Calculated BCA range ba1-ba3Assigned BCA ba1Affiliate Support notching 0Adjusted BCA ba1

Balance Sheet is not applicable.

10 11 February 2019 Deutsche Bank AG: Semiannual update

MOODY'S INVESTORS SERVICE FINANCIAL INSTITUTIONS

De Jure waterfall De Facto waterfall NotchingDebt classInstrumentvolume +

RatingCounterparty Risk Rating 3 0 baa1 1 A3 A3Counterparty Risk Assessment 3 0 baa1 (cr) 1 A3 (cr) --Deposits 3 0 baa1 1 A3 A3Senior unsecured bank debt 3 0 baa1 1 A3 A3Junior senior unsecured bank debt 1 0 baa3 0 Baa3 Baa3Dated subordinated bank debt -1 0 ba2 0 Ba2 Ba2Non-cumulative bank preference shares -1 -2 b1 (hyb) 0 B1 (hyb) B1 (hyb)[1] Where dashes are shown for a particular factor (or sub-factor), the score is based on non-public information.Source: Moody's Financial Metrics

11 11 February 2019 Deutsche Bank AG: Semiannual update

MOODY'S INVESTORS SERVICE FINANCIAL INSTITUTIONS

Endnotes1 In April 2018, the new CEO Christian Sewing announced the broad strokes of a new plan to reshape and right-size the investment bank aiming to achieve

sustainable revenues of approximately 50% from Private & Commercial Bank (PCB) and DWS asset management or 65%, including Global TransactionBanking. PCB intends to focus on growing markets in Italy and Spain, while Wealth Management will focus on Germany and international markets.

2 The firm's management merged the Global Markets unit back into the Corporate and Investment Banking division, creating one division housing all ofthe capital market activities, corporate finance and transactional banking services of the bank. They have also earmarked certain activities including ratesproducts that they wish to discontinue and run off. Management has also shrunk its geographic footprint by exiting 10 local markets, rationalising its clientbase and increasing its focus on corporate clients.

3 The renewed “reshape” of DB's Corporate and Investment Bank (CIB) during 2018 entailed: (1) scaling back in US & Asia in corporate finance with the focuson European clients; (2) reduction of activities in US rates sales and trading as well as repo financing; (3) strategic review of DB's global equities footprintand reduction in Prime Finance; and (4) reduction in risk-weighted assets (RWAs) and leverage exposures.

4 MREL = Minimum Requirement for own funds and Eligible Liabilities.

5 LCR = Liquidity Coverage Ratio.

6 In particular, for junior senior unsecured debt, the 2018 legal changes to Germany's bank insolvency rank order has lowered the likelihood of governmentsupport being available for these instruments, because they legally rank pari passu with most of the outstanding (statutorily subordinated) seniorunsecured instruments issued up until 20 July 2018. This pari passu ranking of new junior senior unsecured debt with legacy (statutorily subordinated)senior unsecured instruments makes it less likely that German authorities would selectively support the legacy instruments (which we reclassified intojunior senior unsecured debt), following clarification that the German authorities expect these liabilities to bear losses in a resolution. As a result, we havereduced our government support assumption for these instruments to 'Low' from 'Moderate.

12 11 February 2019 Deutsche Bank AG: Semiannual update

CREDIT RATINGS ISSUED BY MOODY'S INVESTORS SERVICE, INC. AND ITS RATINGS AFFILIATES (“MIS”) ARE MOODY’S CURRENT OPINIONS OF THE RELATIVE FUTURE CREDITRISK OF ENTITIES, CREDIT COMMITMENTS, OR DEBT OR DEBT-LIKE SECURITIES, AND MOODY’S PUBLICATIONS MAY INCLUDE MOODY’S CURRENT OPINIONS OF THERELATIVE FUTURE CREDIT RISK OF ENTITIES, CREDIT COMMITMENTS, OR DEBT OR DEBT-LIKE SECURITIES. MOODY’S DEFINES CREDIT RISK AS THE RISK THAT AN ENTITYMAY NOT MEET ITS CONTRACTUAL FINANCIAL OBLIGATIONS AS THEY COME DUE AND ANY ESTIMATED FINANCIAL LOSS IN THE EVENT OF DEFAULT OR IMPAIRMENT. SEEMOODY’S RATING SYMBOLS AND DEFINITIONS PUBLICATION FOR INFORMATION ON THE TYPES OF CONTRACTUAL FINANCIAL OBLIGATIONS ADDRESSED BY MOODY’SRATINGS. CREDIT RATINGS DO NOT ADDRESS ANY OTHER RISK, INCLUDING BUT NOT LIMITED TO: LIQUIDITY RISK, MARKET VALUE RISK, OR PRICE VOLATILITY. CREDITRATINGS AND MOODY’S OPINIONS INCLUDED IN MOODY’S PUBLICATIONS ARE NOT STATEMENTS OF CURRENT OR HISTORICAL FACT. MOODY’S PUBLICATIONS MAYALSO INCLUDE QUANTITATIVE MODEL-BASED ESTIMATES OF CREDIT RISK AND RELATED OPINIONS OR COMMENTARY PUBLISHED BY MOODY’S ANALYTICS, INC. CREDITRATINGS AND MOODY’S PUBLICATIONS DO NOT CONSTITUTE OR PROVIDE INVESTMENT OR FINANCIAL ADVICE, AND CREDIT RATINGS AND MOODY’S PUBLICATIONSARE NOT AND DO NOT PROVIDE RECOMMENDATIONS TO PURCHASE, SELL, OR HOLD PARTICULAR SECURITIES. NEITHER CREDIT RATINGS NOR MOODY’S PUBLICATIONSCOMMENT ON THE SUITABILITY OF AN INVESTMENT FOR ANY PARTICULAR INVESTOR. MOODY’S ISSUES ITS CREDIT RATINGS AND PUBLISHES MOODY’S PUBLICATIONSWITH THE EXPECTATION AND UNDERSTANDING THAT EACH INVESTOR WILL, WITH DUE CARE, MAKE ITS OWN STUDY AND EVALUATION OF EACH SECURITY THAT IS UNDERCONSIDERATION FOR PURCHASE, HOLDING, OR SALE.

MOODY’S CREDIT RATINGS AND MOODY’S PUBLICATIONS ARE NOT INTENDED FOR USE BY RETAIL INVESTORS AND IT WOULD BE RECKLESS AND INAPPROPRIATE FORRETAIL INVESTORS TO USE MOODY’S CREDIT RATINGS OR MOODY’S PUBLICATIONS WHEN MAKING AN INVESTMENT DECISION. IF IN DOUBT YOU SHOULD CONTACTYOUR FINANCIAL OR OTHER PROFESSIONAL ADVISER. ALL INFORMATION CONTAINED HEREIN IS PROTECTED BY LAW, INCLUDING BUT NOT LIMITED TO, COPYRIGHT LAW,AND NONE OF SUCH INFORMATION MAY BE COPIED OR OTHERWISE REPRODUCED, REPACKAGED, FURTHER TRANSMITTED, TRANSFERRED, DISSEMINATED, REDISTRIBUTEDOR RESOLD, OR STORED FOR SUBSEQUENT USE FOR ANY SUCH PURPOSE, IN WHOLE OR IN PART, IN ANY FORM OR MANNER OR BY ANY MEANS WHATSOEVER, BY ANYPERSON WITHOUT MOODY’S PRIOR WRITTEN CONSENT.

CREDIT RATINGS AND MOODY’S PUBLICATIONS ARE NOT INTENDED FOR USE BY ANY PERSON AS A BENCHMARK AS THAT TERM IS DEFINED FOR REGULATORY PURPOSESAND MUST NOT BE USED IN ANY WAY THAT COULD RESULT IN THEM BEING CONSIDERED A BENCHMARK.

All information contained herein is obtained by MOODY’S from sources believed by it to be accurate and reliable. Because of the possibility of human or mechanical error as wellas other factors, however, all information contained herein is provided “AS IS” without warranty of any kind. MOODY'S adopts all necessary measures so that the information ituses in assigning a credit rating is of sufficient quality and from sources MOODY'S considers to be reliable including, when appropriate, independent third-party sources. However,MOODY’S is not an auditor and cannot in every instance independently verify or validate information received in the rating process or in preparing the Moody’s publications.

To the extent permitted by law, MOODY’S and its directors, officers, employees, agents, representatives, licensors and suppliers disclaim liability to any person or entity for anyindirect, special, consequential, or incidental losses or damages whatsoever arising from or in connection with the information contained herein or the use of or inability to use anysuch information, even if MOODY’S or any of its directors, officers, employees, agents, representatives, licensors or suppliers is advised in advance of the possibility of such losses ordamages, including but not limited to: (a) any loss of present or prospective profits or (b) any loss or damage arising where the relevant financial instrument is not the subject of aparticular credit rating assigned by MOODY’S.

To the extent permitted by law, MOODY’S and its directors, officers, employees, agents, representatives, licensors and suppliers disclaim liability for any direct or compensatorylosses or damages caused to any person or entity, including but not limited to by any negligence (but excluding fraud, willful misconduct or any other type of liability that, for theavoidance of doubt, by law cannot be excluded) on the part of, or any contingency within or beyond the control of, MOODY’S or any of its directors, officers, employees, agents,representatives, licensors or suppliers, arising from or in connection with the information contained herein or the use of or inability to use any such information.

NO WARRANTY, EXPRESS OR IMPLIED, AS TO THE ACCURACY, TIMELINESS, COMPLETENESS, MERCHANTABILITY OR FITNESS FOR ANY PARTICULAR PURPOSE OF ANY CREDITRATING OR OTHER OPINION OR INFORMATION IS GIVEN OR MADE BY MOODY’S IN ANY FORM OR MANNER WHATSOEVER.

Moody’s Investors Service, Inc., a wholly-owned credit rating agency subsidiary of Moody’s Corporation (“MCO”), hereby discloses that most issuers of debt securities (includingcorporate and municipal bonds, debentures, notes and commercial paper) and preferred stock rated by Moody’s Investors Service, Inc. have, prior to assignment of any rating,agreed to pay to Moody’s Investors Service, Inc. for ratings opinions and services rendered by it fees ranging from $1,000 to approximately $2,700,000. MCO and MIS also maintainpolicies and procedures to address the independence of MIS’s ratings and rating processes. Information regarding certain affiliations that may exist between directors of MCO andrated entities, and between entities who hold ratings from MIS and have also publicly reported to the SEC an ownership interest in MCO of more than 5%, is posted annually atwww.moodys.com under the heading “Investor Relations — Corporate Governance — Director and Shareholder Affiliation Policy.”

Additional terms for Australia only: Any publication into Australia of this document is pursuant to the Australian Financial Services License of MOODY’S affiliate, Moody’s InvestorsService Pty Limited ABN 61 003 399 657AFSL 336969 and/or Moody’s Analytics Australia Pty Ltd ABN 94 105 136 972 AFSL 383569 (as applicable). This document is intendedto be provided only to “wholesale clients” within the meaning of section 761G of the Corporations Act 2001. By continuing to access this document from within Australia, yourepresent to MOODY’S that you are, or are accessing the document as a representative of, a “wholesale client” and that neither you nor the entity you represent will directly orindirectly disseminate this document or its contents to “retail clients” within the meaning of section 761G of the Corporations Act 2001. MOODY’S credit rating is an opinion as tothe creditworthiness of a debt obligation of the issuer, not on the equity securities of the issuer or any form of security that is available to retail investors.

Additional terms for Japan only: Moody's Japan K.K. (“MJKK”) is a wholly-owned credit rating agency subsidiary of Moody's Group Japan G.K., which is wholly-owned by Moody’sOverseas Holdings Inc., a wholly-owned subsidiary of MCO. Moody’s SF Japan K.K. (“MSFJ”) is a wholly-owned credit rating agency subsidiary of MJKK. MSFJ is not a NationallyRecognized Statistical Rating Organization (“NRSRO”). Therefore, credit ratings assigned by MSFJ are Non-NRSRO Credit Ratings. Non-NRSRO Credit Ratings are assigned by anentity that is not a NRSRO and, consequently, the rated obligation will not qualify for certain types of treatment under U.S. laws. MJKK and MSFJ are credit rating agencies registeredwith the Japan Financial Services Agency and their registration numbers are FSA Commissioner (Ratings) No. 2 and 3 respectively.

MJKK or MSFJ (as applicable) hereby disclose that most issuers of debt securities (including corporate and municipal bonds, debentures, notes and commercial paper) and preferredstock rated by MJKK or MSFJ (as applicable) have, prior to assignment of any rating, agreed to pay to MJKK or MSFJ (as applicable) for ratings opinions and services rendered by it feesranging from JPY125,000 to approximately JPY250,000,000.

MJKK and MSFJ also maintain policies and procedures to address Japanese regulatory requirements.

REPORT NUMBER 1159642

13 11 February 2019 Deutsche Bank AG: Semiannual update