29

March 22, 2016 NYSE: GLT Deutsche Bank Basic Materials One-on-One Day John P. Jacunski, EVP & CFO

| Date post: | 06-Apr-2018 |

| Category: |

Documents |

| Upload: | trankhuong |

| View: | 215 times |

| Download: | 0 times |

March 22, 2016

NYSE: GLT

Deutsche Bank Basic Materials

One-on-One Day

John P. Jacunski, EVP & CFO

Any statements included in this presentation which pertain to future financial and business matters are

“forward-looking statements” within the meaning of the safe harbor provisions of the United States Private

Securities Litigation Reform Act of 1995. The Company uses words such as “anticipates”, “believes”,

“expects”, “future”, “intends” and similar expressions to identify forward-looking statements. Any such

statements are based on management’s current expectations and are subject to numerous risks,

uncertainties and other unpredictable or uncontrollable factors that could cause future results to differ

materially from those expressed in the forward-looking statements including, but not limited to: changes in

industry, business, market, political and economic conditions in the U.S. and other countries in which the

Company does business, demand for or pricing of its products, changes in tax legislation, governmental

laws, regulations and policies, initiatives of regulatory authorities, technological changes and innovations,

market growth rates, and cost reduction initiatives. In light of these risks, uncertainties and other factors,

the forward-looking matters discussed in this presentation may not occur and readers are cautioned not to

place undue reliance on these forward-looking statements. The forward-looking statements speak only as

of the date of this presentation and Glatfelter undertakes no obligation, and does not intend, to update

these forward-looking statements to reflect events or circumstances occurring after the date of this

presentation. More information about these factors is contained in Glatfelter’s filings with the U.S.

Securities and Exchange Commission, which are available at www.glatfelter.com.

During the course of this presentation, certain non-U.S. GAAP financial measures will be presented. A

reconciliation of these measures to U.S. GAAP financial measures is included in the appendix of this

presentation.

Forward-Looking Statements and Use of Non-GAAP Financial Measures

2

Agenda

• Business Overview

• Financial Overview

3

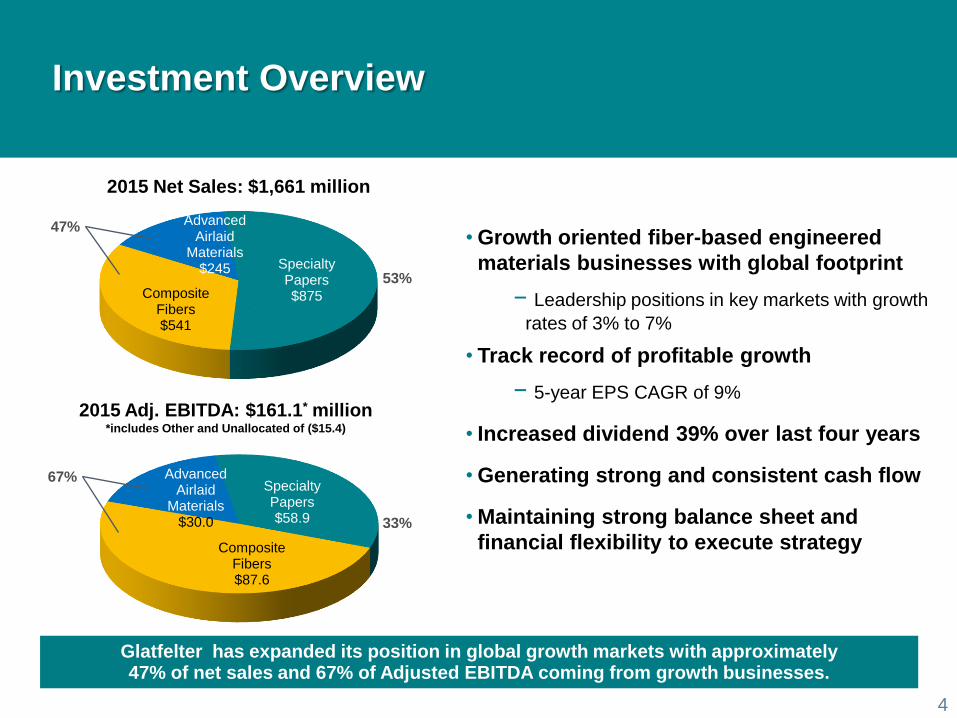

Glatfelter has expanded its position in global growth markets with approximately 47% of net sales and 67% of Adjusted EBITDA coming from growth businesses.

2015 Net Sales: $1,661 million

2015 Adj. EBITDA: $161.1* million *includes Other and Unallocated of ($15.4)

Specialty Papers $863

Advanced Airlaid Materials

$239

Composite Fibers $447

Specialty Papers $58.9

Composite Fibers $87.6

Advanced Airlaid

Materials $30.0

Specialty Papers $875 Composite

Fibers $541

Advanced Airlaid

Materials $245

67%

33%

53%

Investment Overview

• Growth oriented fiber-based engineered

materials businesses with global footprint

− Leadership positions in key markets with growth

rates of 3% to 7%

• Track record of profitable growth

− 5-year EPS CAGR of 9%

• Increased dividend 39% over last four years

• Generating strong and consistent cash flow

• Maintaining strong balance sheet and

financial flexibility to execute strategy

47%

4

Composite Fibers Business Unit

Food & Beverage

51%

Nonwoven

Wallcovering 17% Metallized

Products 13%

Technical Specialties

13%

Composite Laminates

6%

• Leading market positions driving growth

• 2015 revenue flat in constant currency

– Food & beverage volume +5%

– Wallcover volume down 20% due to situation in Russia &

Ukraine

• Attractive long term growth rates

– Global tea and coffee markets ~ 3%

– Nonwoven wallcover market ~ 5%

– Electrical market ~ 7%

• Broadened electrical product portfolio with 2014

acquisition

2015 Key Product Sales Mix

5

Revenue & Shipment Trends

$419 $476 $437

$566 $618

$541

90,350 93,317 90,300

133,570

157,336 153,767

2010 2011 2012 2013 2014 2015

Revenue Tons Sold

• Tea Bags #1

• Single-Serve Coffee #1

• Nonwoven Wallcovering #1

Market Positions (Worldwide, Pro-Forma)

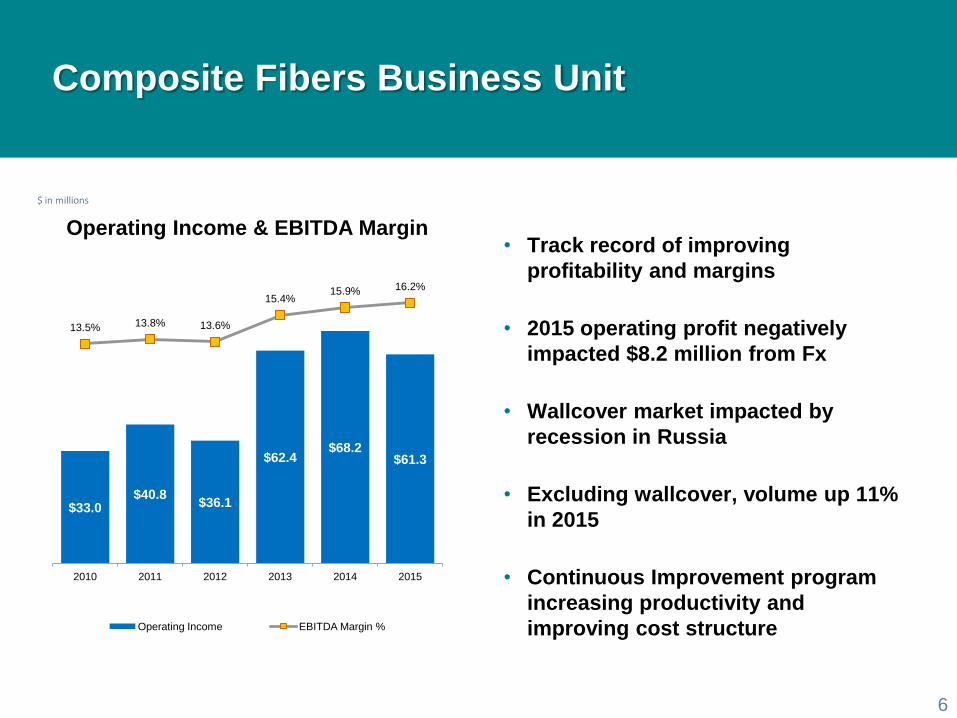

Composite Fibers Business Unit

• Track record of improving

profitability and margins

• 2015 operating profit negatively

impacted $8.2 million from Fx

• Wallcover market impacted by

recession in Russia

• Excluding wallcover, volume up 11%

in 2015

• Continuous Improvement program

increasing productivity and

improving cost structure

$ in millions

Operating Income & EBITDA Margin

6

$33.0 $40.8

$36.1

$62.4 $68.2

$61.3

13.5% 13.8% 13.6%

15.4% 15.9% 16.2%

2010 2011 2012 2013 2014 2015

Operating Income EBITDA Margin %

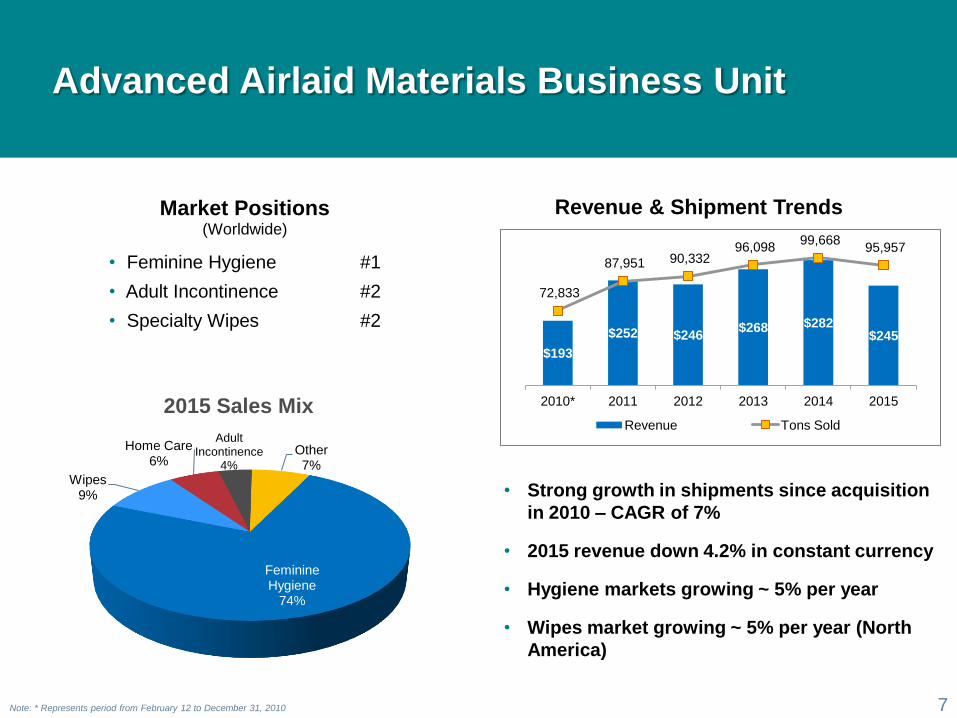

Advanced Airlaid Materials Business Unit

Feminine Hygiene

74%

Wipes 9%

Home Care 6%

Adult Incontinence

4%

Other 7%

2015 Sales Mix

7 Note: * Represents period from February 12 to December 31, 2010

Revenue & Shipment Trends

$193

$252 $246 $268 $282

$245

72,833

87,951 90,332 96,098

99,668 95,957

2010* 2011 2012 2013 2014 2015

Revenue Tons Sold

• Feminine Hygiene #1

• Adult Incontinence #2

• Specialty Wipes #2

Market Positions (Worldwide)

• Strong growth in shipments since acquisition

in 2010 – CAGR of 7%

• 2015 revenue down 4.2% in constant currency

• Hygiene markets growing ~ 5% per year

• Wipes market growing ~ 5% per year (North

America)

Advanced Airlaid Materials Business Unit

• Track record of profit and margin

growth since 2010

– Operating profit impacted by weak

volume in 1H’15

• Leading market positions driving

growth

• Innovation and R&D capability

creating new product opportunities

• Continuous Improvement initiatives

are expanding margins

• ~ 90% of revenue has cost pass-

through arrangements

• Building new facility in U.S. with

start-up expected in late 2017

$ in millions

Operating Income & EBITDA Margin

8

$4.4

$13.4

$18.0 $21.4

$25.3

$21.2

6.0%

8.7%

10.8% 11.3%

12.2% 12.3%

2010* 2011 2012 2013 2014 2015

Operating Income EBITDA Margin %

Note: * Represents period from February 12 to December 31, 2010

Specialty Papers Business Unit

Carbonless & Forms

40%

Engineered Products

22%

Book Publishing

18%

Envelope & Converting

20%

2015 Sales Mix

9

• 11 consecutive years of outperforming

broader market and growing market

share

• Superior customer service

• Intensive focus on new products

Year-Over-Year Change in Shipments

0.0%

-5.0% -8.0%

-16.0%

-2.3% -3.7% -3.4% -2.3%

-8.1%

-1.0%

4.0% 1.6% 2.5%

-0.7%

3.5% 2.0% 1.2% 1.4% 0.3% -0.1%

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

UFS Market Demand for N.A.

Glatfelter Shipments (adjusted for acquisitions)

• Postal Applications #1

• Playing Cards #1

• Trade Book Publishing #1

• Carbonless Products #2

• Greeting Cards #2

• Envelope #2

Market Positions (North America)

Specialty Papers Business Unit

• Recent results impacted by

following:

– Bottom of cycle pricing

– Pulp production issues

• Customer service and new business

development driving share gains

• Culture of continuous improvement

and aggressive cost control

• Manufacturing flexibility

• Track record of success

Operating Income & EBITDA Margin

$ in millions

10

$58.4 $57.3

$67.3

$39.7 $38.6 $33.0

11.1% 10.7%

11.1%

8.2%

7.6%

6.7%

2010 2011 2012 2013 2014 2015

Operating Income EBITDA Margin %

Agenda

• Business Overview

• Financial Overview

11

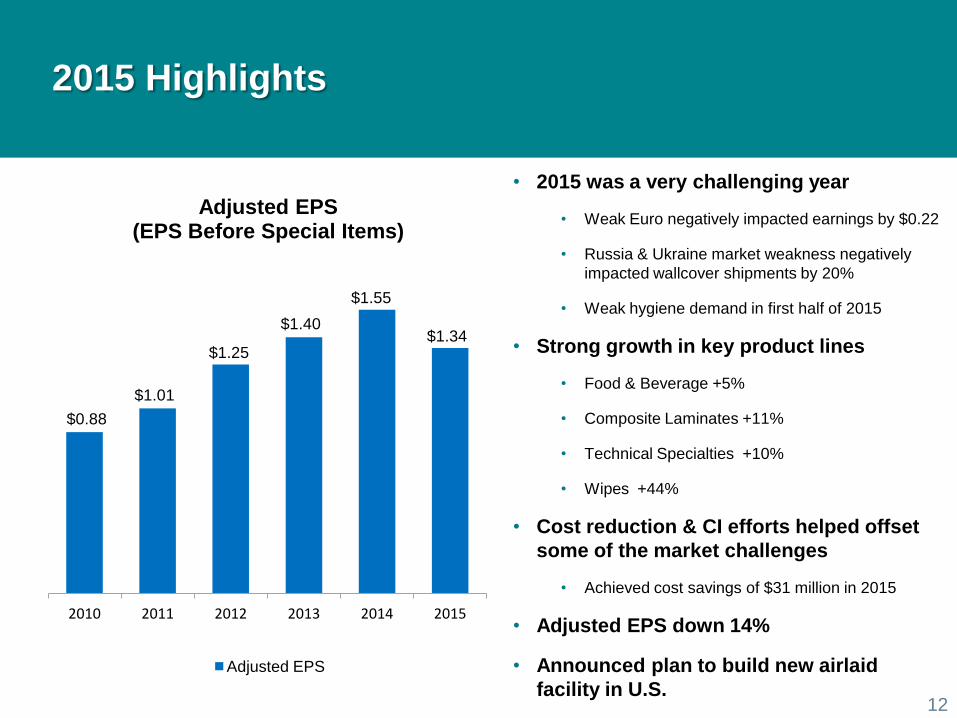

2015 Highlights

• 2015 was a very challenging year

• Weak Euro negatively impacted earnings by $0.22

• Russia & Ukraine market weakness negatively

impacted wallcover shipments by 20%

• Weak hygiene demand in first half of 2015

• Strong growth in key product lines

• Food & Beverage +5%

• Composite Laminates +11%

• Technical Specialties +10%

• Wipes +44%

• Cost reduction & CI efforts helped offset

some of the market challenges

• Achieved cost savings of $31 million in 2015

• Adjusted EPS down 14%

• Announced plan to build new airlaid

facility in U.S.

Adjusted EPS (EPS Before Special Items)

12

$0.88

$1.01

$1.25

$1.40

$1.55

$1.34

2010 2011 2012 2013 2014 2015

Adjusted EPS

$1.55

$1.34

$(0.32)

$(0.24)

$0.46

$0.16 $(0.09)$(0.02) $0.06 $(0.22)

2014 Selling

Price

Volume

/Mix (*)

Input

costs

Operations SPBU

expandedoutage

Corporate

Unallocated& Pension

Tax

Rate

FX 2015

Adjusted EPS – 2015 vs. 2014

13 Note: See appendix of this presentation for the reconciliation of adjusted EPS to its nearest GAAP measure.

Food & Beverage +5%

Composite Laminates +11%

Technical Specialties +10%

Wallcover -20%

Feminine Hygiene -6%

Wipes +44%

SPBU -0.1%

Fx ($0.35)

Benefit of Currency Hedges $0.13

Lower input costs and operations improvements were more than offset by the challenging market environment and negative currency headwinds.

Tax rate 17.7% in 2015

versus 21.6% in 2014

* - Volume/mix includes the impact of market related downtime

$1,455 $1,603 $1,578

$1,723 $1,802 $1,661

2010 2011 2012 2013 2014 2015

Net Sales (in millions)

Financial Highlights

$150.9 $164.0

$174.2 $177.2 $183.3 $161.1

10.4% 10.2%

11.0%

10.3% 10.2% 9.7%

2010 2011 2012 2013 2014 2015

Adj. EBITDA / Margin % (in millions)

Adj. EBITDA Adj. EBITDA % of Net Sales

14

Steady growth in Revenue and EBITDA from 2010-2014; 2015 impacted by weak Euro and Russia/Ukraine situation.

Attractive Free Cash Flow Profile

Glatfelter continues to generate strong and consistent cash flow to fund growth initiatives, dividends and share repurchases, and to maintain financial flexibility.

Note: Figures in millions

$168.0

$140.3

$112.8

$173.6

$99.6

$133.7

$76.6 $58.0

$77.3 $94.3

$38.2 $53.9

2010 2011 2012 2013 2014 2015

Cash from Ops. Adjusted FCF (excl. AFM/CBC & Major Capital Projects)

15

Capital Expenditures and Related Cost Estimate

(in millions) 2015A 2016E 2017E

Normal Capital Expenditures $73 $70 - $80 $70 - $80

Major Projects

Boiler Environmental Compliance (SPBU) 27 40 - 45 7 - 17

Capacity expansion (AMBU) - 40 - 45 35 - 40

Total $100 $150 - $170 $112 - $137

• Boiler Environmental Compliance

• Convert/Replace boilers to use natural gas

• Upgrade associated infrastructure including

connecting to gas pipelines

• Total project cost of $85 million to $90 million

• Total spend to date of $33 million

• Total capital expenditures for

Advanced Airlaid Materials capacity

expansion project estimated at $80

million

• Expect start-up in Q4 2017 with

commercial shipments in Q1 2018

(in millions) 2015A 2016E 2017E

Boiler Environmental Compliance (SPBU) - $7 $0

Capacity expansion (AMBU) - $2 $4

Total - $9 $4

Capital Expenditures Estimate

Major Projects One-Time Costs Estimate

• SPBU annual maintenance outages

in Q2 2016 expected to cost $28

million versus $33 million in Q2 2015

16

Improved Returns on Invested Capital

Earnings growth, consistent free cash flow and disciplined capital deployment have significantly improved return on capital, which is above GLT’s weighted average cost of capital.

4.3%

5.6%

6.3%

8.5%

7.6%

8.3% 8.6%

9.3% 8.8%

8.0% 7.7%

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Note: Return on invested capital based on after-tax earnings from operations excluding unusual items. 17

Pension Plan Remains Overfunded

No cash contribution required in 2015 or expected for the foreseeable future. Pension expense

expected to decrease in 2016 primarily driven by higher discount rates.

(in millions) 2010 2011 2012 2013 2014 2015

2016

Estimate

Pension (Income) /

Expense

$9.2 $10.4 $11.6 $14.2 $6.7 $9.1 $4.6

Cash contributions* $0 $0 $0 $0 $0 $0 $0

Funded Status ($ millions)

$92.1

$28.0 $17.3

$113.5

$60.4 $53.0

2010 2011 2012 2013 2014 2015

Funded status ($mm) No cash contributions needed from 2010 through 2015

* Qualified plans only

18

Balance Sheet Metrics

• In 2015, Company completed

sale of 15,628 acres of

timberlands for $25 million

cash and after-tax gain of

approximately $13.2 million

• Leverage at 1.6x as of

December 31, 2015

• Total liquidity of $354 million

• Sufficient financial flexibility

and liquidity to meet near term

investment needs and execute

long term strategy

Notes: *The above calculation is not intended to be used for purposes of calculating debt covenant compliance.

The sum of individual amounts set forth above may not agree to the column totals due to rounding. 19

(in millions) 31-Dec-13 31-Dec-14 31-Dec-15

Cash $122.9 $99.8 $105.3

Debt

Current portion of long term debt - 5.7 7.4

5⅜% Notes, due October 2020 250.0 250.0 250.0

1.55 - 2.4% Term Loans, due June 2022 - 2025 58.8 58.3 47.7

Revolving credit agreement 133.5 90.6 58.8

Total Debt $442.3 $404.6 $363.9

Net Debt $319.4 $304.8 $258.6

Shareholders’ Equity $684.5 $649.1 $663.2

TTM Adj. EBITDA (excl. Pension) $177.2 $183.3 $161.1

Leverage* 1.8 1.7 1.6

Cash available under bank facility $211.3 $246.6 $248.3

Wrap-Up

• Leading positions in key growth markets

• Expansion of growth platforms both organically and through acquisition

• Near term challenges

– Recession in Russia

– Weakened Euro

• Focus Areas

– New product development

– New market opportunities

– Manufacturing execution

– Continuous improvement initiatives

• Track record of profitable growth

• Delivering returns above cost of capital

• Financial strength to fund future growth

20 Profitable Growth • Delivering Returns • Financial Strength

Appendix

21

Adjusted EBITDA– 2015 vs. 2014

22 Note: See appendix of this presentation for the reconciliation of adjusted EBITDA to its nearest GAAP measure.

Lower input costs and operations improvements were more than offset by the challenging market environment and negative currency headwinds.

$183.3

$161.1

$(18.1)

$(13.2)$25.7

$6.7 $(5.2) $1.2 $(17.7)

$(1.6)

2014 Selling

Price

Volume

/Mix (*)

Input

costs

Operations SPBU

expandedoutage

Corporate

Unallocated

FX Net Power

Sales, REC's& Other

2015

Food & Beverage +5%

Composite Laminates +11%

Technical Specialties +10%

Wallcover -20%

Feminine Hygiene -6%

Wipes +44%

SPBU -0.1%

Fx $(24.9)m

Benefit of Currency Hedges $7.2m

* - Volume/mix includes the impact of market related downtime

Flexible Operating Platforms

Strong Global Reach

Fremont, OH

Chillicothe, OH

York, PA

Scaër, France

Lydney, UK

Gernsbach, Germany

Lanao del Norte, Philippines

Falkenhagen, Germany Gatineau, Quebec

Spring Grove, PA

Caerphilly, UK

Atlanta, GA

Moscow, Russia

Suzhou, China

Hong Kong, China

2015 Revenue Breakdown

North America 63% $1.1 billion

Europe 28% $0.5 billion

ROW 9% $0.1 billion

Total 100% $1.7 billion

Corporate Headquarters

Specialty Papers

Composite Fibers

Advanced Airlaid Materials

Sales / Distribution Offices

Glatfelter end-markets

Glatfelter’s strong global production platform in core geographies is enhanced by key sales and distribution operations.

Dresden, Germany

23

Dresden, Germany

OberSchmitten, Germany

Cost of Goods Sold Breakdown

Raw Materials

Energy

Labor

Depreciation

Other COGS

― Total Glatfelter ―

46%

8%

23%

4%

19%

― Specialty Papers ―

37%

8% 26%

3%

26%

― Composite Fibers ―

55%

11%

20%

6% 8%

― Advanced Airlaid Materials ―

62%

4%

17%

4%

13%

24

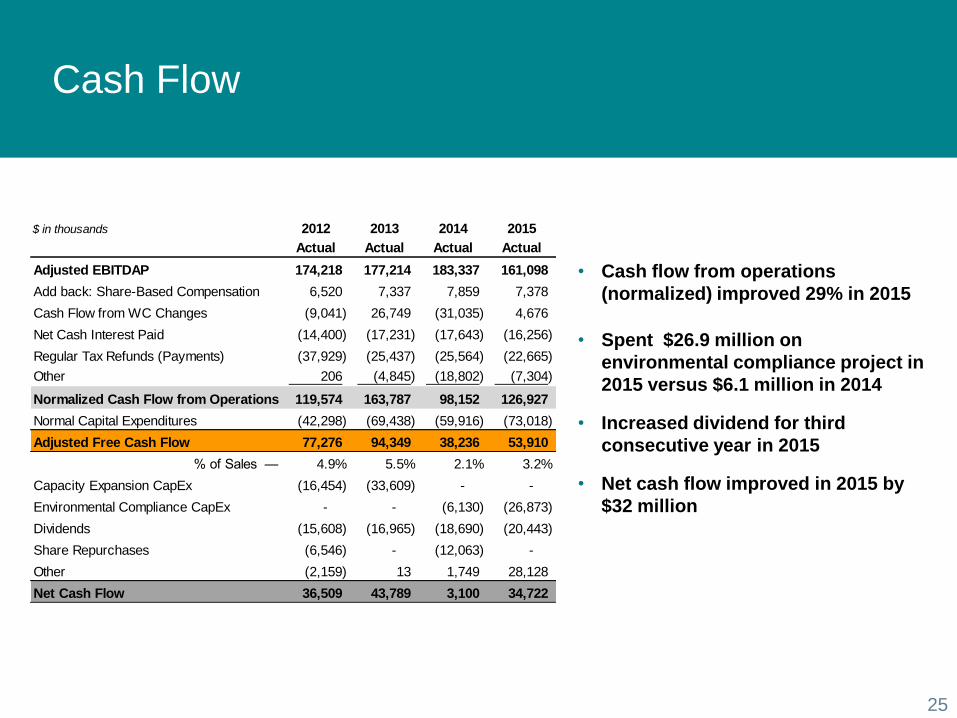

Cash Flow

• Cash flow from operations

(normalized) improved 29% in 2015

• Spent $26.9 million on

environmental compliance project in

2015 versus $6.1 million in 2014

• Increased dividend for third

consecutive year in 2015

• Net cash flow improved in 2015 by

$32 million

$ in thousands 2012 2013 2014 2015

Actual Actual Actual Actual

Adjusted EBITDAP 174,218 177,214 183,337 161,098

Add back: Share-Based Compensation 6,520 7,337 7,859 7,378

Cash Flow from WC Changes (9,041) 26,749 (31,035) 4,676

Net Cash Interest Paid (14,400) (17,231) (17,643) (16,256)

Regular Tax Refunds (Payments) (37,929) (25,437) (25,564) (22,665)

Other 206 (4,845) (18,802) (7,304)

Normalized Cash Flow from Operations 119,574 163,787 98,152 126,927

Normal Capital Expenditures (42,298) (69,438) (59,916) (73,018)

Adjusted Free Cash Flow 77,276 94,349 38,236 53,910

% of Sales — 4.9% 5.5% 2.1% 3.2%

Capacity Expansion CapEx (16,454) (33,609) - -

Environmental Compliance CapEx - - (6,130) (26,873)

Dividends (15,608) (16,965) (18,690) (20,443)

Share Repurchases (6,546) - (12,063) -

Other (2,159) 13 1,749 28,128

Net Cash Flow 36,509 43,789 3,100 34,722

25

Free Cash Flow

Notes: The sum of individual amounts set forth above may not agree to the column totals due to rounding.

Working capital is defined as accounts receivable plus inventories less accounts payable. 26

(in millions) 2011 2012 2013 2014 2015

Adjusted EBITDA $164.0 $174.2 $177.2 $183.3 $161.1

Change in Working Capital 10.1 (9.0) 26.7 (31.0) 4.7

Taxes paid 8.3 (44.7) (15.6) (24.1) (15.8)

Interest Paid (24.2) (14.4) (17.2) (17.6) (16.3)

Other (17.9) 6.7 2.5 (10.9) 0.1

Cash Flow from Operations 140.3 112.8 173.6 99.6 133.7

Less: Capital Expenditures (64.5) (58.8) (103.0) (66.0) (99.9)

Free Cash Flow 75.8 54.1 70.6 33.5 33.9

Adjustment for major capital projects 0.0 16.5 33.6 6.1 26.9

Exclude: CBC/AFM Credit (17.8) 6.7 (9.8) (1.4) (6.8)

Adjusted Free Cash Flow $58.0 $77.3 $94.3 $38.2 $53.9

Reconciliation of Non-GAAP

Measures Adjusted EPS

Note: The sum of individual amounts set forth above may not agree to the column totals due to rounding. 27

2009 2010 2011 2012 2013 2014 2015

Net income (loss) $2.70 $1.17 $0.93 $1.36 $1.52 $1.57 $1.47

Charge for workforce efficiencies - - 0.01 - - 0.01 0.03

Cellulosic bio-fuel and alternative fuel mixture credits (2.09) (0.50) - (0.09) (0.23) (0.02) -

Gains from sales of timberland and related transaction

costs(0.00) (0.02) (0.10) (0.12) (0.04) (0.06) (0.33)

Asset impairment charge - - - - - 0.05 0.02

Shutdown and restructuring charges - - - - - - -

Acquisition and integration related costs 0.04 0.20 0.02 - 0.13 0.01 -

International legal entity restructuring - - - - 0.01 - -

Fox River environmental matter - - - - - - 0.14

Debt redemption costs - - 0.14 0.11 - - -

Reserves for environmental matters - - - - - - -

Adjusted earnings (loss) $0.64 $0.88 $1.01 $1.25 $1.40 $1.55 $1.34

Pension Impact on Adjusted EPS 0.10 0.12 0.14 0.17 0.20 0.09 0.13

Adjusted earnings (loss) excl. pension $0.74 $1.00 $1.16 $1.42 $1.59 $1.65 $1.47

Reconciliation of Non-GAAP Measures Adjusted EBITDA, Excluding Pension

Note: The sum of individual amounts set forth above may not agree to the column totals due to rounding. 28

2009 2010 2011 2012 2013 2014 2015

In millions

Net Income 123.4$ 54.4$ 42.7$ 59.4$ 67.2$ 69.2$ 64.6$

Taxes 19.7 (20.9) 8.2 19.6 2.0 18.1 14.0

Net Pension Expenses 7.0 9.2 10.4 11.6 14.2 6.7 9.1

Depreciation and Amortization 61.3 65.8 69.3 69.5 68.2 70.6 63.2

Net Interest Expense 17.3 24.7 31.1 18.2 17.7 18.8 17.2

EBITDA, excluding Pension 228.8$ 133.4$ 161.7$ 178.3$ 169.3$ 183.4$ 168.1$

Adjustments / exclusions:

Gains on Timberland Sales and Transaction Related Costs (0.5) (0.4) (3.4) (9.2) (1.4) (4.9) (20.9)

Asset impairment charge - - - - - 3.3 1.2

Debt Redemption Costs - - 3.6 5.1 - - -

Cellulosic Bio-fuel and Alternative Fuel Mixture Credits (105.5) 0.1 - - - - -

Acquisition and Integration Related Costs 3.5 11.9 1.1 - 6.5 1.1 0.2

Workforce Efficiency Charge - - 1.0 - - 0.5 2.5

International legal entity Restructuring - - - - 2.8 - -

Write-off of Concert Indemnification Receivable - 2.5 - - - - -

Foreign Currency Hedge on Acquisition Price - 3.4 - - - - -

AMBU capacity expansion - - - - - - 0.0

Fox River Environmental matter - - - - - - 10.0

Adjusted EBITDA, excluding pension 126.2$ 150.9$ 164.0$ 174.2$ 177.2$ 183.3$ 161.1$

Reconciliation of Non-GAAP Measures Net Debt and Leverage

* - The above calculation is not intended to be used for purposes of calculating debt covenant compliance. 29

Net debt & Leverage December 31 December 31 December 31

In millions 2013 2014 2015

Current Portion of Long-Term Debt $0.0 $5.7 $7.4

Long-Term Debt 442.3 398.9 356.5

Total Debt 442.3 404.6 363.9

Less: Cash (122.9) (99.8) (105.3)

Net Debt $319.4 $304.8 $258.6

Net Debt $319.4 $304.8 $258.6

Divided by: TTM Adjusted EBITDA 177.2 183.3 161.1

Leverage* 1.8x 1.7x 1.6x