25

NYSE: TEN Detroit, MI January 17, 2018 Deutsche Bank Global Auto Industry Conference

NYSE: TENDetroit, MI

January 17, 2018

Deutsche Bank Global Auto Industry Conference

This presentation contains forward-looking statements that involve risks and uncertainties which could cause the company’s plans, actions and results to differ materially from its

current expectations. The words “expect,” “estimate,” “will,” and similar expressions identify certain of these forward-looking statements. The company cautions that actual results

may differ materially from those projected or implied in forward-looking statements due to a variety of factors including, but not limited to, the following: (i) general economic,

business and market conditions; (ii) the company’s ability to source needed goods and services in accordance with customer demand and at competitive prices; (iii) the cost and

outcome of claims, legal proceedings or investigations, including, but not limited to, those arising in connection with the ongoing global antitrust investigation, product safety or

intellectual property rights; (iv) the impact of the changing laws and regulations to which we are subject, including environmental laws and regulations, pensions or other regulated

activities; (v) the ability of the company to access capital markets on commercially reasonable terms; (vi) changes in consumer demand; (vii) changes in vehicle manufacturers’

production rates and their requirements for the company’s products, including with respect to any delays in the adoption of the current mandated timelines for worldwide

emissions regulations; (viii) the overall highly competitive nature of the automobile and commercial vehicle parts industry, and any resultant inability to realize the sales

represented by the company’s awarded book of business which is based on anticipated pricing for the applicable program over its life; (ix) the loss of any of our large original

equipment manufacturer (“OEM”) customers, or the loss of market shares by these customers if we are unable to achieve increased sales to other OEMs; (x) the company’s

continued success in cost reduction and cash management programs; (xi) economic, exchange rate and political conditions in the countries where we operate or sell our products;

(xii) workforce factors such as strikes or labor interruptions; (xiii) increases in the costs of raw materials; (xiv) the negative impact of fuel price volatility on logistics costs and

discretionary purchases of vehicles or aftermarket products, and demand for off-highway equipment; (xv) the cyclical nature of the global vehicular industry, including the

performance of the global aftermarket sector and longer product lives of automobile parts; (xvi) product warranty costs; (xvii) material developments relating to our intellectual

property or the failure or breach of our IT systems; (xviii) the company’s ability to develop and profitably commercialize new products and technologies; (xix) governmental actions,

including the ability to receive regulatory approvals and the timing of such approvals; and (xx) the timing and occurrence (or non-occurrence) of transactions and events which may

be subject to circumstances beyond the control of the company. Additional information regarding these and other risk factors and uncertainties is detailed from time to time in the

company’s SEC filings, including but not limited to its annual report on Form 10-K/A. Unless otherwise indicated in this presentation, the forward-looking statements in this

presentation are made as of the date hereof, and the company does not undertake any obligation to publicly disclose revisions or updates to any forward-looking statements.

Safe Harbor

2

Positioned to drive long-term shareholder value

Why Invest in Tenneco

3

Focused Priorities

Outpace industry production

Invest in new technologies and markets

Margin expansion and improved cash flow

Built to Outperform

Diversified business profile

Proven track record of growth

Leading ROIC performance

N Y S ETEN

Accelerating Core Growth

Technology-driven growth

New market growth

Content growth

Market expansion growth

Accelerating Core Growth

Transformation in the Auto Space

Tenneco is well-positioned to benefit from industry trends

4

Electrification / HybridizationAutonomous Driving Mobility Emissions Regulations

Accelerating Core Growth

Multiple growth drivers further diversify the business profile

5

Long-term Growth Drivers

Technology-driven Growth • Monroe® Intelligent Suspension

• Noise Vibration and Harshness (NVH) Solutions

New Market Growth • China aftermarket opportunity

• Opportunity to add new aftermarket product category

Content Growth • Light vehicle hybridization of the fleet

• Tightening emissions regulations globally

Market Expansion Growth • Increasing number of commercial truck and off-highway

powertrains under regulation

45%

23%

20%

12%

49%

22%

18%

11%

2017Q3 YTD

Product ApplicationsVA Revenue

2020 Projection

Clean Air Light Vehicle

Ride Performance Light Vehicle

Aftermarket

Commercial Truck and Off-Highway

Accelerating Core Growth – Technology-driven

Monroe® Intelligent Suspension

Increasing demand for advanced suspension technologies to differentiate ride

6Source: IHS database and Tenneco analysis

• Expect advanced suspension to grow from 2% to more than 15% of LV production by 2025, representing >40% of available market in 2025

• 25% revenue CAGR opportunity for advanced suspension growth through 2025

• Autonomous trend drives additional opportunities

RID

E P

ER

FO

RM

AN

CE

More than6x

AC TIVE SUSPENSION

Average4xSEMI-ACTIVE SUSPENSION

$50-$60CON VENTIONAL SUSPENSION

A segment F segment

Content per Vehicle

• China car parc grows and ages over the next decade

• #1 market position in Americas and Europe

• Market-leading aftermarket capabilities

• New mobility models create demand for replacement parts

• Countercyclical business with strong margins and cash flow

Accelerating Core Growth – New Markets

Significant Aftermarket Opportunities

Bringing market-leading capabilities to new, high-growth markets

7Source: IHS database and Tenneco analysis

Investing for Growth in China

• Brand building

• Product coverage

• Distributor Development

• Supply Chain Footprint

1950 1960 1970 1980 1990 2000 2010 2020 2025 2030

Aftermarket Car Parc Growth

Unprecedented growth over next 15 years led by China

Global Vehicles in Operation

Source: OCIA, Frost & Sullivan

Hybrid production grows at a 32%* CAGR through 2025

• Hybrids forecasted to be almost 90%* of electrified production in 2025

• EU6 Hybrid value-add CPV expected to increase 30% - 40%** by 2025; at par with ICE CPV

• Plug-in hybrids offer additionalcontent opportunity; packaging, engineering, acoustics and thermal management

Accelerating Core Growth – Content

Hybridization Driving Clean Air Growth

Strong TEN content growth on hybrid powertrains

8

Electrification of Light Vehicles

* Source: IHS Automotive October 2017 global production forecast ** Tenneco estimates

(millions) 2016 2020 2025

BEV/FC 0.5 2.2 4.6

Hybrid 2.7 12.0 33.3

Total build 93 102 110

BEV/FCCAGR 28%

HybridCAGR 32%

Accelerating Core Growth – Market Expansion

Tightening Emissions Regulations

CTOH market expands with increasing number of vehicles under regulation

9

Regulatory-driven growth accelerates through the next decade

Source: PSR production forecast and Tenneco estimates

CTOH – Growth of Vehicles Under Regulation

(millions) 2016 2020 2025

CT: Euro VI (equivalent) 1.1 2.2 3.2

Regulated Off-Hwy 1.1 2.1 4.3

Total 2.2 4.3 7.5

** Tenneco estimates

• Commercial Truck– 2020-21 / 2023 – China CN VIa/VIb**

– 2020 – India BS VI (skipping BS V)

– 2023-2027 – CARB & EPA Low NOx

• Off-Highway– 2019 – EU Stage V & China CN IV**

– 2020 – Brazil Stage 3B**

– 2020/2023 – India BS IV**/India BS V**

• Light Vehicle– 2017-2025 – US Tier 3

– 2017-2021 – Euro 6c/6d Real Driving Emissions

– 2020-2023 – China CN 6a/6b

– 2020 – India BS 6 (skipping BS 5)

CAGR

13%

16%

15%

Accelerating Core Growth – Clean Air

Clean Air Outpaces Industry Growth

Clean Air growth projected to outpace industry production through 2030

10

$ billions

*Source: IHS Automotive forecast and Tenneco estimates

CLEAN AIR VA REVENUE VA MARKET SIZE

Total Clean Air

LightVehicle

CTrk & Off-Hwy

LightVehicle

CTrk & Off-Hwy

2016 $3.7 $3.3 $0.5 $12.6 $5.4

2030 Projections*:

@16% LV full BEV penetration

$7.0 $5.1 $1.9 $17.0 $9.2

@25% LV full BEV penetration

$6.4 $4.5 $1.9 $15.1 $9.24.0% CAGR

4.7% CAGR

$ billions

@ 16%

@ 25%

TEN Clean Air 2030 VA Revenue Growth Projection

LV BEV PENETRATION

Tenneco Clean Air VA Revenue

Global LV Build (Industry)*

4.7% CAGR

4.0% CAGR

1.7% CAGR

1.7% CAGR

• Boston Consulting Group 14%• Bloomberg New Energy Finance 14%• Morgan Stanley 16%• Roland Berger 20%

Industry forecasts for 2030 BEV penetration average 16% Assumptions:

• CPV held at 2025 levels

• Market share (2016/2030)

- CTOH 9% / 20%- LV 26% / 30%

IHS Automotive 6%

HeadquartersClean Air ManufacturingRide Performance ManufacturingEngineering

Built to Outperform

Diversified Profile

Diversified business profile enables long-term growth

11

Product lines Ride Performance and Clean Air

Product applications Light vehicle, commercial truck, off-highway and aftermarket

Customers623 OE and AM customers

Platforms435 OE platforms; enabling aftermarket growth

Global footprint 91 manufacturing facilities, 15 engineering centers

Built to Outperform

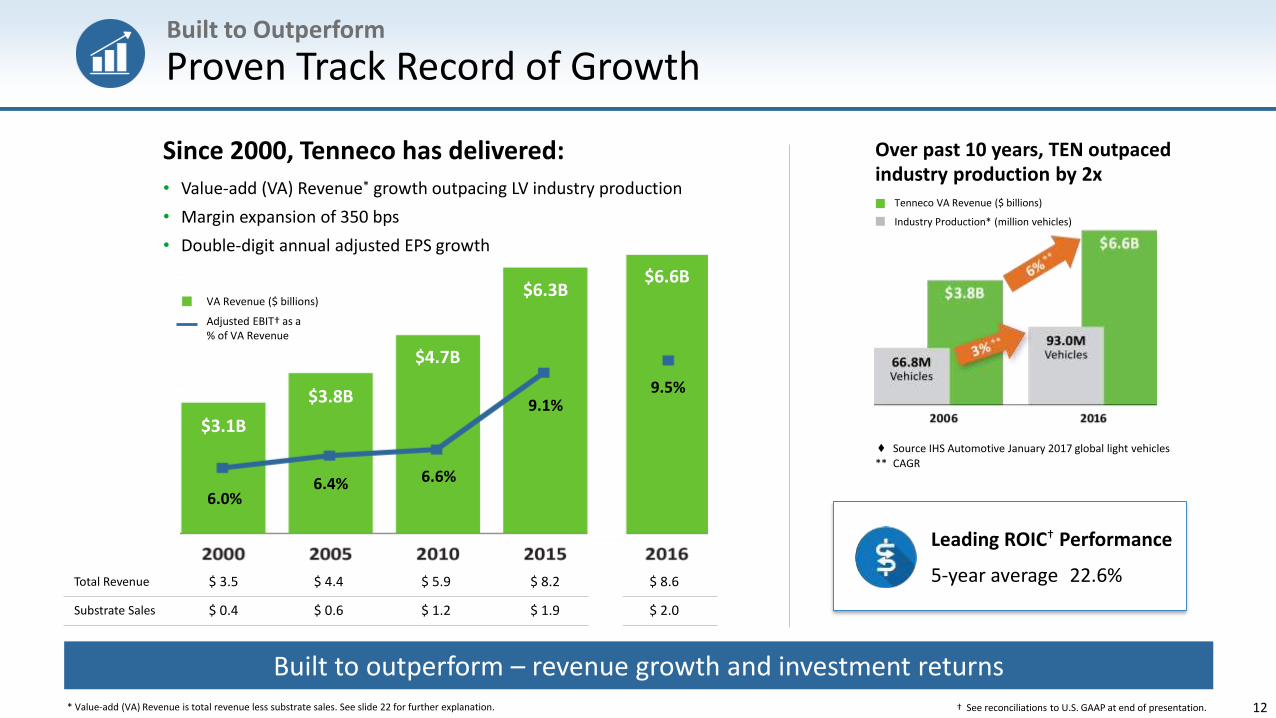

Proven Track Record of Growth

Built to outperform – revenue growth and investment returns

12

Since 2000, Tenneco has delivered:

• Value-add (VA) Revenue* growth outpacing LV industry production

• Margin expansion of 350 bps

• Double-digit annual adjusted EPS growth

Total Revenue $ 3.5 $ 4.4 $ 5.9 $ 8.2 $ 8.6

Substrate Sales $ 0.4 $ 0.6 $ 1.2 $ 1.9 $ 2.0

VA Revenue ($ billions)

Adjusted EBIT† as a % of VA Revenue

Leading ROIC† Performance

5-year average 22.6%

Over past 10 years, TEN outpaced industry production by 2x

Tenneco VA Revenue ($ billions)

Industry Production* (million vehicles)

♦ Source IHS Automotive January 2017 global light vehicles

** CAGR

$6.6B$6.3B

$4.7B

$3.8B

$3.1B

9.5%9.1%

6.6%6.4%6.0%

* Value-add (VA) Revenue is total revenue less substrate sales. See slide 22 for further explanation. † See reconciliations to U.S. GAAP at end of presentation.

Focused Priorities

Revenue Outlook

Strong organic revenue growth outpacing industry production

13

Organic Growth 5%

2018 Revenue Outlook (in 2017 constant currency)

Expecting organic growth of 5%, outpacing industry production by 3% driven by content growth in light and commercial vehicles and continued recovery in regulated off-highway regions

* IHS Automotive December 2017 global light vehicle production and Tenneco estimates.

** Power Systems Research (PSR) January 2018 global commercial truck and bus production and Tenneco estimates.

*** Customer schedules and Tenneco estimates for off-highway engine production in North America and Europe.

See slide 18 for further key assumptions related to our revenue projections.

Impact vs. 2017 Euro/USD RMB/USD Real/USD

+ 2.5% 1.20 0.156 0.328

- 1.14 0.149 0.313

- 2.5% 1.08 0.141 0.297

2018 Assumptions

• Global light vehicle production +2%*

• Global commercial truck production about flat**

• Off-highway engine production for regulated regions expected up low double-digits***

• Organic growth is net of OE price downs

• Substrates estimated at 24% - 25% of total revenue

2018 Currency Sensitivity

Mid-term Revenue Outlook

Expect to outperform industry production by:

• 4% - 6% in 2019

• 3% - 5% in 2020

Focused Priorities

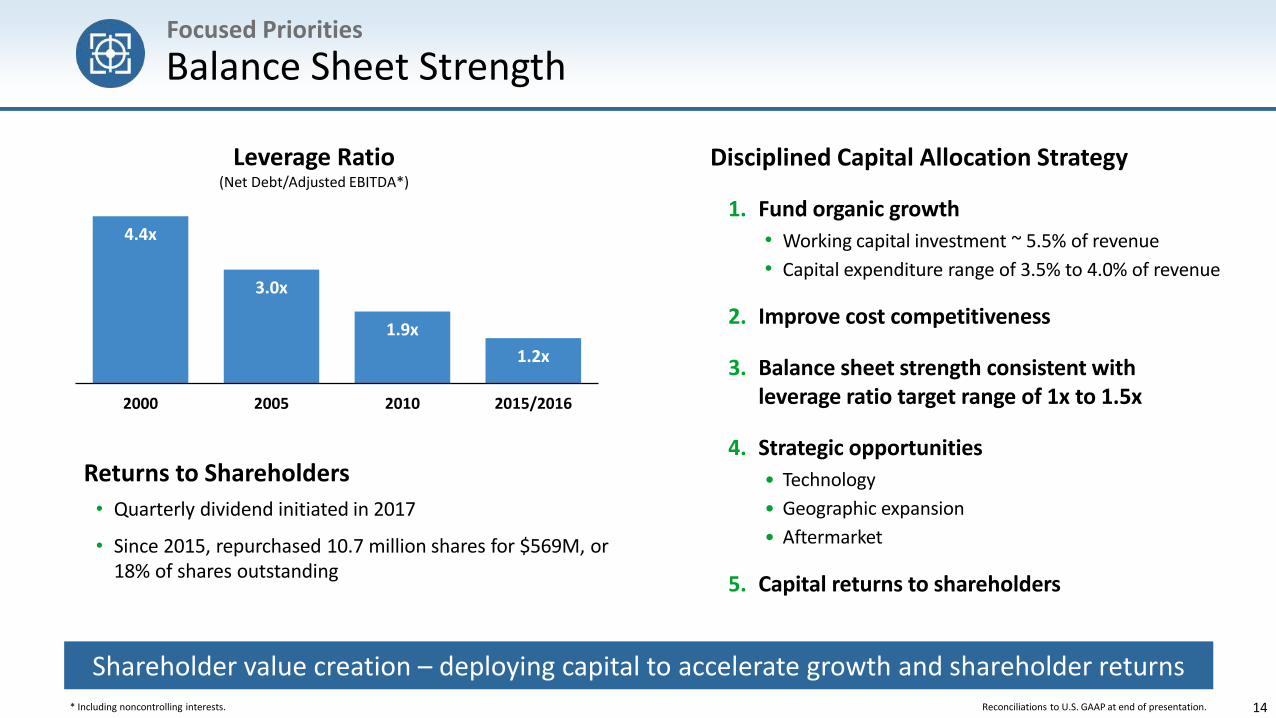

Balance Sheet Strength

Shareholder value creation – deploying capital to accelerate growth and shareholder returns

14

Returns to Shareholders

• Quarterly dividend initiated in 2017

• Since 2015, repurchased 10.7 million shares for $569M, or 18% of shares outstanding

Reconciliations to U.S. GAAP at end of presentation. * Including noncontrolling interests.

Disciplined Capital Allocation Strategy

1. Fund organic growth

• Working capital investment ~ 5.5% of revenue

• Capital expenditure range of 3.5% to 4.0% of revenue

2. Improve cost competitiveness

3. Balance sheet strength consistent with leverage ratio target range of 1x to 1.5x

4. Strategic opportunities

• Technology

• Geographic expansion

• Aftermarket

5. Capital returns to shareholders

4.4x

3.0x

1.9x

1.2x

2000 2005 2010 2015/2016

Leverage Ratio(Net Debt/Adjusted EBITDA*)

Focused Priorities

Strategic Objectives

Diversified portfolio drives organic growth and shareholder value

15

• Continue outpacing industry production by 3% to 5+%

• Drive margin expansion and improve cash flow performance

• Invest to continue diversifying portfolio to capture growth and become more light vehicle powertrain agnostic

• Build financial strength and maximize flexibility

Current Value-add Revenue Long-term Value-add Revenue

Aftermarket

Ride Performance (OE)

Clean Air (OE)

Source: IHS database; Power Systems Research, Tenneco analysis

16

Financial Results Disclaimer

17

Use of Non-GAAP Financial Information

In addition to the results reported in accordance with accounting principles generally accepted in the United States (“GAAP”)

included in this presentation, the company has provided information regarding certain non-GAAP financial measures.

These measures include Earnings Before Interest Expense, Income Taxes, Noncontrolling Interests and Depreciation and

Amortization (“EBITDA*”), Net Debt, Value-Add Revenue, Adjusted EBITDA*, Adjusted Earnings Before Interest Expense,

Income Taxes and Noncontrolling Interests (“Adjusted EBIT”), Adjusted Earnings Per Share, and Return on Invested Capital.

Reconciliations of these non-GAAP financial measures to the comparable GAAP measure are included in this presentation.

* Including noncontrolling interests.

Tenneco Projections

18

In addition to the information set forth on this slide and slide 10 and 13, Tenneco’s revenue projections are based on the type of information set forth

under “Outlook” in Item 7 – “Management’s Discussion and Analysis of Financial Condition and Results of Operations” as set forth in Tenneco’s Annual

Report on Form 10-K/A for the year ended December 31, 2016. Please see that disclosure for further information. Key additional assumptions and

limitations described in that disclosure include:

• Revenue projections are based on original equipment manufacturers’ programs that have been formally awarded to the company; programs

where the company is highly confident that it will be awarded business based on informal customer indications consistent with past practices;

and Tenneco’s status as supplier for the existing program and its relationship with the customer.

• Revenue projections are based on the anticipated pricing of each program over its life.

• Revenue projections assume a fixed foreign currency value. This value is used to translate foreign business to the U.S. dollar.

• Revenue projections are subject to increase or decrease due to changes in customer requirements, customer and consumer preferences, the

number of vehicles actually produced by our customers, and pricing.

• No inflation assumed.

Certain elements of our GAAP revenue cannot be forecasted accurately over long periods of time on account of the variability and volatility of

precious metal pricing in the substrates that we pass through to our customers. In this respect, we are not able to forecast GAAP revenue on a

forward-looking basis for the time periods provided herein on slide 10 without unreasonable efforts.

Tenneco’s revenue projection constitutes a forward-looking statement. We also refer you to the cautionary language regarding our forward-looking

statements set forth in the Safe Harbor statement on slide 2.

EBITDA* – Reconciliation of Non-GAAP Results

19

EBITDA* represents earnings before interest expense, income taxes, noncontrolling interests and depreciation and amortization. EBITDA* is not a calculation based upon generally accepted accounting principles. The amounts included in the EBITDA* calculation, however, are derived from amounts included in the historical statements of income. In addition, EBITDA* should not be considered as an alternative to net income or operating income as an indicator of the company’s operating performance, or as an alternative to operating cash flows as a measure of liquidity. Tenneco has presented EBITDA* because it regularly reviews EBITDA* as a measure of the company’s performance. In addition, Tenneco believes that its security holders utilize and analyze its EBITDA* for similar purposes. Tenneco also believes EBITDA* assists investors in comparing a company’s performance on a consistent basis without regard to depreciation and amortization, which can vary significantly depending upon many factors. However, the EBITDA* measure presented may not always be comparable to similarly titled measures reported by other companies due to differences in the components of the calculation.

* Including noncontrolling interests.

2016 2015 2010 2005 2000

Net income (loss) attributable to Tenneco Inc. $ 356 $ 241 $ 39 $ 56 $ (41)

Net income attributable to noncontrolling interests 68 54 24 2 2

Income tax expense (benefit) - 146 69 26 (27)

Interest expense (net of interest capitalized) 92 67 149 133 188

EBIT, earnings before interest expense, income taxes & noncontrolling interests (GAAP measure) 516 508 281 217 122

Depreciation & amortization of other intangibles 212 203 216 177 151

EBITDA* $ 728 $ 711 $ 497 $ 394 $ 273

$ Millions, Unaudited

Adjusted EBITDA* – Reconciliation of Non-GAAP Results

20

2016 2015 2010 2005 2000

EBITDA*

Adjustments (reflect non-GAAP(1) measures):

$ 728 $ 711 $ 497 $ 394 $ 273

Restructuring & related expenses 32 59 14 12 61

Pension/post retirement charges 72 4 6 - -

New aftermarket customer changeover costs - - - 10 -

Other non-operational items - - - - 4

Adjusted EBITDA* (non-GAAP financial measure)(2)

$ 832 $ 774 $ 517 $ 416 $ 338

(1) Generally Accepted Accounting Principles

(2) Tenneco presents the above reconciliation of non-GAAP results in order to reflect the results for full years 2000, 2005, 2010, 2015 and 2016 in a manner that allows a better understanding of the results of operational activities separate from the financial impact of decisions made for the long-term benefit of the company. Adjustments similar to the ones reflected above have been recorded in earlier periods, and similar types of adjustments can reasonably be expected to be recorded in future periods. Using only the non-GAAP earnings measure to analyze earnings would have material limitations because its calculation is based on the subjective determinations of management regarding the nature and classification of events and circumstances that investors may find material. Management compensates for these limitations by utilizing both GAAP and non-GAAP earnings measures reflected above to understand and analyze the results of the business. The company believes investors find the non-GAAP information helpful in understanding the ongoing performance of operations separate from items that may have a disproportionate positive or negative impact on the company’s financial results in any particular period.

* Including noncontrolling interests.

$ Millions, Unaudited

Net Debt / Adjusted EBITDA* – Reconciliation of Non-GAAP Results

21

2016 2015 2010 2005 2000

Total debt $ 1,384 $ 1,210 $ 1,223 $ 1,383 $ 1,527

Total cash 349 288 233 141 35

Debt net of cash balances 1,035 922 990 1,242 1,492

Adjusted EBITDA* $ 832 $ 774 $ 517 $ 416 $ 338

Ratio of net debt to adjusted EBITDA* 1.2x 1.2x 1.9x 3.0x 4.4x

Note: We present debt net of cash balances because management believes it is a useful measure of our credit position and progress toward reducing leverage. The calculation is limited in that we may not always be able to use cash to repay debt on a dollar-for-dollar basis.

* Including noncontrolling interests.

$ Millions, Unaudited

Adjusted EBIT as a Percentage of Value-add Revenue –Reconciliation of Non-GAAP Results

22

(1) Tenneco presents the above reconciliation of revenues in order to reflect value-add revenues separately from substrate sales, which include precious metals pricing, which may be volatile. Substrate sales occur when, at the direction

of its OE customers, Tenneco purchases catalytic converters or components thereof from suppliers, uses them in its manufacturing processes and sells them as part of the completed system. While Tenneco original equipment

customers assume the risk of this volatility, it impacts reported revenue. Excluding substrate sales removes this impact. Tenneco uses this information to analyze the trend in revenues before this factor. Tenneco believes investors

find this information useful in understanding period to period comparisons in the company's revenues.

(2) Generally Accepted Accounting Principles

(3) Tenneco presents the above reconciliation of GAAP to non-GAAP earnings measures primarily to reflect the results in a manner that allows a better understanding of the results of operational activities separate from the financial

impact of decisions made for the long-term benefit of the company and other items impacting comparability between the periods. Adjustments similar to the ones reflected above have been recorded in earlier periods, and similar

types of adjustments can reasonably be expected to be recorded in future periods. Using only the non-GAAP earnings measures to analyze earnings would have material limitations because its calculation is based on the subjective

determinations of management regarding the nature and classification of events and circumstances that investors may find material. Management compensates for these limitations by utilizing both GAAP and non-GAAP earnings

measures reflected above to understand and analyze the results of the business. The company believes investors find the non-GAAP information helpful in understanding the ongoing performance of operations separate from items

that may have a disproportionate positive or negative impact on the company’s financial results in any particular period.

(4) Tenneco presents adjusted EBIT as a percentage of value-add revenue to assist investors in evaluating our company’s operational performance without the impact of substrate sales.

$ Millions 2016 2015 2010 2006 2005 2000

Value-add revenue (1) $ 6,571 $ 6,293 $ 4,653 $ 3,755 $ 3,759 $ 3,127

Clean Air substrate sales $ 2,028 $ 1,888 $ 1,284 $ 927 $ 681 $ 401

Total revenue $ 8,599 $ 8,181 $ 5,937 $ 4,682 $ 4,440 $ 3,528

EBIT $ 516 $ 508 $ 281 $ 196 $ 217 $ 122

Adjustments (reflect non-GAAP (2) measures)

Restructuring and related expenses 36 63 19 27 12 61

Pension / post retirement charges 72 4 6 (7) - -

New aftermarket customer changeover costs - - - 6 10 -

Reserve for receivables from former affiliate - - - 3 - -

Other non-operational items - - - - - 4

Adjusted EBIT (non-GAAP Financial Measures) (3) $ 624 $ 575 $ 306 $ 225 $ 239 $ 187

Adjusted EBIT as a % of value-add revenue (4) 9.5% 9.1% 6.6% 6.0% 6.4% 6.0%

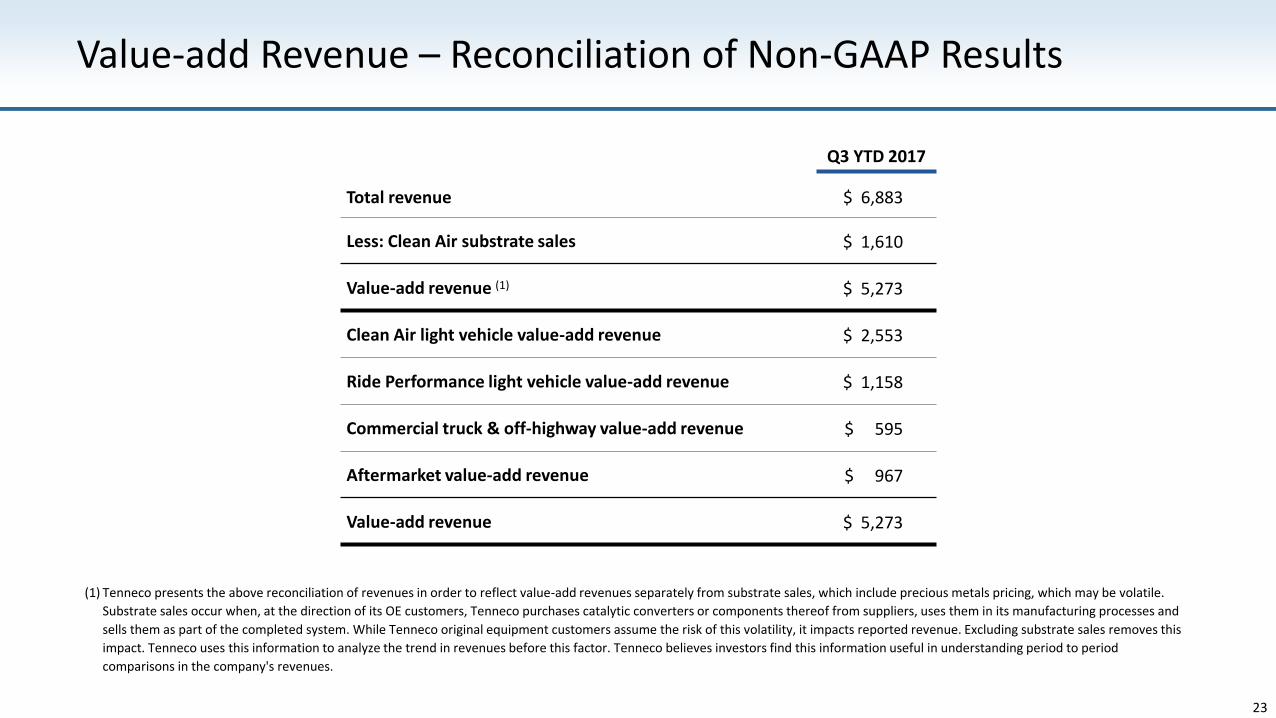

Value-add Revenue – Reconciliation of Non-GAAP Results

23

Q3 YTD 2017

Total revenue $ 6,883

Less: Clean Air substrate sales $ 1,610

Value-add revenue (1) $ 5,273

Clean Air light vehicle value-add revenue $ 2,553

Ride Performance light vehicle value-add revenue $ 1,158

Commercial truck & off-highway value-add revenue $ 595

Aftermarket value-add revenue $ 967

Value-add revenue $ 5,273

(1) Tenneco presents the above reconciliation of revenues in order to reflect value-add revenues separately from substrate sales, which include precious metals pricing, which may be volatile.

Substrate sales occur when, at the direction of its OE customers, Tenneco purchases catalytic converters or components thereof from suppliers, uses them in its manufacturing processes and

sells them as part of the completed system. While Tenneco original equipment customers assume the risk of this volatility, it impacts reported revenue. Excluding substrate sales removes this

impact. Tenneco uses this information to analyze the trend in revenues before this factor. Tenneco believes investors find this information useful in understanding period to period

comparisons in the company's revenues.

Adjusted Earnings Per Share – Reconciliation of Non-GAAP Results

24

2016 2000

Earnings Per Share $ 6.31 $ (1.18)

Adjustments (reflect non-GAAP measures):

Restructuring and related expenses 0.57 1.21

Pension / post retirement charges 0.83 -

Costs related to refinancing 0.27 -

Net tax adjustments (1.96) -

Other non-operational items - 0.07

Adjusted Earnings Per Share $ 6.02 $ 0.10

Return on Invested Capital – Reconciliation of Non-GAAP Results

25

2011Dec 31

2012Dec 31

2013Dec 31

2014Dec 31

2015Dec 31

2016Dec 31

Short-term Debt $ 66 $ 113 $ 83 $ 60 $ 86 $ 90

Long-term Debt 1,138 1,052 1,006 1,055 1,124 1,294

Redeemable Noncontrolling Interests 12 15 20 34 41 40

Tenneco Inc. Shareholders' Equity - 246 432 495 425 573

Noncontrolling Interests 43 45 39 40 39 47

Invested Capital $ 1,259 $ 1,471 $ 1,580 $ 1,684 $ 1,715 $ 2,044

Average Invested Capital $ 1,365 $ 1,526 $ 1,632 $ 1,700 $ 1,880

EBIT $ 428 $ 422 $ 489 $ 508 $ 516

Adjustments (reflect non-GAAP (1) measures)(2)

Restructuring and related expenses 13 78 49 63 36

Pullman recoveries (5) - - - -

Asset impairment charge 7 - - - -

Bad debt charge - - 4 - -

Pension / post retirement charges - - 32 4 72

Adjusted EBIT (non-GAAP financial measure)(2) 443 500 574 575 624

Effective Tax Rate 34.8% 35.7% 33.7% 32.9% 26.6%

Tax effected Adjusted EBIT $ 289 $ 321 $ 381 $ 386 $ 458

Return on Invested Capital (ROIC)(3)

(non-GAAP financial measure)(2)21.1% 21.1% 23.3% 22.7% 24.4%

5 year Average Invested Capital $ 1,626

5 years Average tax effected Adjusted EBIT 367

5 year Average ROIC 22.6%

(1) Generally accepted Accounting Principles

(2) Tenneco presents the above reconciliation of non-GAAP results in order to allow a better understanding of our performance.

(3) We consider Return on Invested Capital (ROIC) to be a meaningful indicator of our operating performance, and we evaluate ROIC because it measures how effectively we use the capital we invest in our operations. Tenneco defines ROIC as tax effected Adjusted EBIT divided by Average Invested Capital, which is the beginning and ending balances of debt, equity and noncontrolling interests. See the tabular calculation above.

$ Millions, Unaudited