Restricted UNDP/NIW75/113 Terminal Report NIGERIA ... Deve I o p m e n t of Professional Accountancy Courses (Bendel) Project Findings and Recommendations Serial No. FMWED/OPS/84/263 (UNDP) United Nations Educational , Scientific and Cultural Development Organization Programme United Nations Paris, 1984

Transcript

Restricted UNDP/NIW75/113 Terminal Report NIGERIA

...

Deve I o p m e n t of Professional Accountancy Courses (Bendel)

Project Findings and Recommendations

Serial No. FMWED/OPS/84/263 (UNDP)

United Nations Educational , Scientific and Cultural Development Organization Programme

United Nations

Paris, 1984

I.

GLOSSARY

INTRODUCTION

TABLE OF CONTENTS

I1 . PROJECT OBJECTIVES

I11 . ACTIVITIES AND OUTPUTS

IV MATTERS INCIDENTAL TO THE IMPLEMENTATION OF THE PROJECT OBJECTIVES

V. ACHIEVEMENTS OF THE OBJECTIVES

VI. FINDINGS AND CONCLUSION

VI1 . RECOMMENDATIONS

APPENDICES

A. List of International Staff

B. Counterpart Staff: National Staff and Expatriate (Non-Nigerian) Staff

C.

D.

E.

F.

” -U - H.

I.

J,

Unesco Fellowships

Student Enrolment and Graduate Output

Programme of Study

Institute of Chartered Accountants of Nigeria The New Training Scheme - Some Salient Features of the Scheme

The QEB System - Question/Exercise ITandov:? Bank

Practical Workbooks in Accounting

Recommendation concerning the Purchhse of Audio-visual Equipment

The Proposed ND/HND Programmes in Banking and Insurance

(ii)

Paragraph No.

( 1- 5)

( 6- 9)

( 10-42)

(43-47 1 (48-49 1

(50-54 1 (55)

Page No.

21

22-23

24

25

26-27 .

28-30

31-32

33

34

35-36

GLOSSA.RY

CDC

FMNP

HND

ICAN

NBTE

ND

NND

OND

PE I

PE I1

RTC

TMMQ

UNDP

Unesco

Curriculum Development Committee

Federal Ministry of National Planning

Higher National Diplona

Institute of Chartered Accountants of Nigeria

National Board for Technical Education

National Diploma

Nigerian National Digloma (now defunct)

Ordinary National Diploma (now defunct)

Professional Examination I

Professional Examination I1

Recognized Training Centre in relation to the new ICAN scheme "Education and Accelerated Training for Chartered Accountants in Nigeria"

Teaching Methods/Materials Questionnaire

United Nations Development Programme

United Nations Educational, Scientific and Cultural Organization

UNDP/NIR/75/113 - Development of Professional Accountancy Courses (Bendel)

TERMINAL REPORT

I. INTRODUCTION

I. of the Second National Development Plan 1970/75 were being collated and

National Development Plan, 1975/80. The latter plan was considered monumental in the sense that the capital outlay of N33 billion, envisaged for the Third Plan Period, was ten times higher than that invested during the Second Plan Period. In appraising the results of the Second Development Plan, national consensus was reached on one point; that the shortfalls of the Second Plan Period were mainly attributable to a lack of executive capacity, a phenomenon further aggravated by the justifiable demands of the newly enacted Nigerian Enterprises Promotion Decree, 1973. Taking full cognizance of this flaw in the national strategy for manpower development the Third National Development Plan emphatically sought to rectify this managerial bottleneck by placing proper emphasis on maqower development and on the training needs of the nation's economy. Consequently, a major share of the development funds was allocated to the education and manpower development sector of the plan.

The project NIR/75/113 was conceived at a time when the results

ir national attention was focused on finalizing the blue prints of the Third

2. The acute shortage of accounting personnel at all levels of training, both in the public and private sectors of the economy, was considered a major constraint to the timely and effective implementation of the Third National Development Plan. Institute of Chartered Accountants of Nigeria (ICAN), the sole body responsible for regulating the accounting profession in Nigeria, put the number of qualified accountants in the country at less than 900, a ratio of one qualified accountant to every 100,000 Nigerians, as compared to one to 600 in the U.K., one to 1,400 in the USA and one to 5,000 in India. An enquiry conducted midway through the Third National Development Plan by the National Manpower Secretariat to take stock of manpower as relating to Federal ministries, showed that the vacancy rate for accountants and auditors was one of the highest at 59.2 per cent (Second Progress Report on Third National Development Plan 1975/80, page 28, Table 3.2). This acute shortage was even more pronounced in the State Government Ministries which were hard put to comply with the decisions reached at the Annual Conferences of the Accountants General of Nigeria which included:

A survey conducted in 1974 by the

(i)

(ii) installing an internal audit unit at each minis:ry;

(iii)

(iv) the computerization of the Treasury accounting

simplifying and decentralising the accounting systems ;

adopting the new budgetary techniques such as the Project Performance Budgeting System (PPBS); and

systems, etc.

- 2 -

3- The rapid pace of industrialization generated by the oil boom and the introduction of the Nigerian Enterprises Promotion Decree, 1973 (as amended) had, to some extent, exacerbated the shortage of accounting personnel in the private sector as well, In Bendel State alone, where, like everywhere else, the expansion of light and medium industries was being vigorously encouraged, the number of qualified accountants was put at less than 50. Consequently, banks, manufacturing and other commercial companies were known to experience difficulties in expanding the scope of their operations and services.

4. students taking diploma and degree level courses in Accounting at the various universities and polytechnics in Nigeria. In order to increase student intake and accelerate the pace of training of professionally qualified accountants, the Institute of Chartered Accountants of Nigeria was encouraging the introduction of common curricula and a unified system of training at the universities and polytechnics which wanted to join the new education and training scheme, It was proposed in this context that the Ordinary National Diploma (Om) course in Accounting being offered at Auchi Polytechnic be upgraded to a Higher National DiFloma (HND) and aligned with the training needs and examination requirements of the Institute of Chartered Accountants of Nigeria. It was in pursuit of this major objective that the project NIR/75/113 was proposed under the UNDP Country Funding Programme,with technical assistance to be provided by Unesco. The project was finally approved in June 1978 for immediate implementation,

5. came formally into operation when the first Unesco ExFert assigned to the project took up his duties at Auchi Polytechnic in October 1978. However, being a one-man project, it suffered a serious setback with the expert's unscheduled departure in May 1980 after spending 20 months on the job, new expert assigned to the project began work in March 1981, With only 16 months of the project life to run, an appraisal of the situation showed that this short period was totally inadequate to bring the project to a successful completion. Because of the timely initiative of the Polytechnic authorities and the full cooperation and understanding of the Federal Ministry and National Planning ( F W ) and UNDP, the life of the project, albeit in stages, was extended to 31 July 1984,

In April 1975 a total of 432 persons were enrolled as full-time

The project, which was initially designed for a period of 36 months,

The

I1 . PROJECT OBJECTIVES

6, The project objectives, as defined in the project document, were as follows:

Development Objective (Long-term Objective)

7- The Government's sectoral development objective is to eliminate the existing serious shortfall in the supply of middle-level managerial and technical personnel. It is proposed in the Third National Development Plan that the total student enrolment in post-secondary technical institutions should increase from about 8,850 in 1975/76 to about 36,450 in 1980/81. Eleven per cent (N277 million) of the total capital allocation for the

- 3 -

Education Sector is reserved for post-secondary technical institutions.

Immediate Ob j e c t ive -..

t 8. The project's immediate objective is the implementation of a Higher National Diploma course in Accounting at Auchi Polytechnic, Bendel. This will entail the preparation of course materials relevant to the Nigeria1 situation. The introduction and, where necessary, the revision of the course, the expansion of the present staff development programme to cover the new course and the introduction of practical student attachment training, in cooperation with employers of accountants in the Government, industry and commerce.

9. When translated into terms of attainable goals, the immediate objective was sub-divided into three sectkons for implementation purposes:

(a) Programme of activities:

i. the introduction of the Higher National Diploma Course in Accounting; evaluating and revising the existing OND course and converting it into an HND programme;

course in Accounting;

training programme.

ii. the development of course materials for the HND

iii. the introduction of a practical student attachment

(b) Physical resources: the development of capacity for the procurement, use and maintenance of audio-visual. and other teaching aids, books and periodicals.

Human resources:

i. the planning of teaching staff trained in appropriate

ii. the strengthening of the teaching staff induction

iii. the strengthening of evaluation of teaching staff

fields for the HND course;

and development programme;

performance.

I11 . ACTIVITIES AND OUTPUTS

General Observation

10 . The project was initially designed for a period of three years but, with periodic extensions, the project actually ran for a total period of five years and one month. During this period two Unesco Experts were involved in its implementation; the first expert for 20 months from October 1978 to Mag 1980 and the second for 41 rconths from March 1981 to

- 4 -

31 July 1984. The life of the project was extended piece-meal three times: for seven ,.mths from June 1982 to 31 December 1982; for twelve months from January 1983 to 31 December 1983; and again for seven months from January 1984 to July 1984. The entire funding was under the UNDP Country Programme with the exception of the seven-month period from 1 June to 31 December 1982 which was financed on a cost-sharing basis, It is to be observed that this piece-meal extension of the life of the project created a sense of suspense and uncertainty, a state of affairs not considered conducive to the smooth implementation of the project objectives.

Objective (a) (i)

Introduction of Higher National Diploma (HND) in Accountina:

11. Just prior to the commencement of the project in October 1978, the Federal ' Government of Nigeria, as a matter of national policy, introduced the three-year, single-tier diploma programme system in all the disciplinary areas of technical education. The new programme9 known as the Nigerian National Diploma (NND), was appasentlyintroduced to cut the training period from four to three years acd thus accelerate the training and production of technically-trained personnel, an area which had been identified as a serious bottleneck to the implementation of the economic development plans. However, owing to lack of public support and persistent agitation by students resulting in the disruptlion of normal academic activity, the

* system was scrapped and replaced by the old two-tier ND and HND system in October 1980. Therefore, the immediate tasks facing the project, in its initial stages of implementation, were the switching over from one system to another and again, after a trial-run of two years, changing back to the two-tier four-year ND and HND system. The revised twin-diploma system, based on the National Board for Technical Education's (LWTE) approved course structure and syllabi was se-introduced as of the 1980/81 academic session.

The Nigerian National Diploma in Accounting - NND Accounting:

12 . The National Board for Technical Education (NBTE): It is pertinent to note at this stage that the award of National and Higher National Diplomas ND and HND, is goveEned and regulated by the National Board for Technical Education (NBTE), an autonomous body comprising leading educationists and practitioners drawn from all walks of national life. the course structure and curricula considered minimal for the award of National and Higher National Diplomas in various fields of technical education By rsriodic visits and through an in-built monitoring system, the Board seeks to ensuie thaL the minimal conditions prescribed in terms of course structure, curricula and contact hours are in fact strictly observed b the institutions of higher education which offer courses leading to the a w c d of Nationa: and Higher National Diplomas.

The Board determines

13 The Institute of Chartered Accountants of Nigeria (ICAN): Founded by an act of Parliament in 1965, the Institute of Chartered Accountants of Nigeria (ICAN) regulates the accountancy profession in the country and conducts professional examinations leading to its membership. Since only ICAN members are entitled to practise the Accountancy Profession in Nigeria, the majority of students, on completing their Higher National Diploma

- 5 -

programme in Accounting, aspire to pass the ICAN Professional Examination I1 (PE iIj to becomefully-flsdg2dChartered Accountants -- a much coveted professional qualification. As a result, the process of association with 'ICAN starts at an early stage of a student's educational career and most

1 - students register with ICAN as student members during the first or second year of their course of study.

14. The Main Project Objective Re-defined:, The main project objective, the "Introduction of a Higher National Diploma in Accounting at Auchi Polytechnic", when viewed in this professional context, and read in conjunction with the project title "Development of Professional Accountancy Courses (Bendel)", acquires a broader but more precise connotation in the sense that the HND course in Accounting must not only accord with the NBTE regulations regarding the award of national diplomas, but it must also have a strong professional bias. In other words, the HND course in Accounting to be introduced under the aegis of the project must be designed to provide an educational and prpfessional framework which not only fulfils the NBTE requirements but also prepares the students for a professional career by enabling them to pass the ICAN final examination, a pre-requisite to admission to full membership of the Institute. It was, therefore, clearly understood by the Unesco Expert and his national counterparts right at the outset that the revised HND course in Accounting had to be designed with these two objectives in mind; the observance of the NBTE regulations, and the provision of an educational and instructional framework which would enable the END graduates to acquire professional status as fully-fledged members of the Institute of Chartered Accountants of Nigeria. The immediate task, therefore, was to revise the ,XBTE-Sased HND course in Accounting to align it with the ICAN exaaination requirements.

15 0 Nodus Operandi: After thorough discussion with the national counterparts and other expatriate staff on the scope of the project and the related- issues, the Expert, soon after the commencement of his mission, designed and issued a questionnaire -- Teaching Methods Materials Questionnaire (TMMQ). The main objective of the exercise was to ascertain staff members' own evaluations of the existing system and course curricula and to make an objective assessment of its relevance to the re-defined project objective as discussed above. Thanks to the full cooperation extended by all staff members, their candid and unreserved comments and suggestions highlighted the anomalies inherent in the course curricula and pin-pointed the short-comings, particulzrly in the areas of staffing and teachjng aic-!s/material resources. The resultjng findings, conclusions and recommendations were made the central prank of the strategy for the implementation of the prime project objective: the introduction of a professionally-oriented HND course in Accounting at Auchi Polytechnic.

16. Findings, Conclusions & Recommendations Arising from the Questionnaire: Staff members' comments and suggestiom arising from the questionnaire, as summarised and collated by the Expert, were discussed at a staff moting and, by general consensus, they were adopted and accepted as a basis for further concerted action in implementing the project objectives. This resulted in the establishment of two departmental committees to implement these recommendations: the Curriculum Development

- 6 -

Committee (CDC) and the Library Development Committee (LDC). the chairmanship of the Unesco Exp.-rL, and keeping within the NBTE framework, has the following specific terms of reference:

The CDC, under

17 - The

removing the duplications/overlappings inter se, discovered as a result of the TMMQ; converting the newly-announced ICAN examination scheme "Education and Accelerated Training of Chartered Accountants in Nigeria" into a teaching programme and aligning it with the ND and HND course structure and syllabi;

incorporating as far as feasible the salient features of the examination requirements of the Association of Certified Accountants (ACCA) and the Institute of Cost and Management Accountants (ICMA) into the new course structure and to:

(i) critically review and, if necessary, revise the course structure for both the ND and HND programmes;

syllabus in each course and present it as a teaching programme, complete with lists of recommended textbooks and further reading lists; and

present the entire package as a comprehensive education and training scheme befitting an HND graduate in terms of a wholesome educational upbringing and professional training.

(ii) revise, amend, add to and up-date the

(iii)

conversion of the ICAN examination curricula into a Teaching - Programme therefore became an integral part of the CDC assignment. This part .of the CDC assignment, however, could not be proceeded with until after the new scheme had been officially adopted by the ICAN Council and ratified by the participating institutions, a lengthy procedure which could not be completed before the second half of 1983 (see paragraph 18 for further elaboration of the ICAN scheme).

18. Joint Consultative Committee on Education and Accelerated Training of Chartered Accountants in Nigeria: The Institute of Chartered Accountants of Nigeria, realixing.+:hat the traditional method of training chartered accountants under the AAticled Clerkship system had not proved as productive as had been expected, and also taking into account the developments which had taken place in the field of Accaunting Education in other parts of the world, finally accepted the fact that the robe of institutions of higher education in the country (the polytechnics and the universities) in imparting formal Accounting Education should be recognized and incorporated in its own training scheme. Consequently, a joint consultative committee, comprising representatives of the various

- 7 -

polytechnics and universities participating in the scheme and practising members from the profession, was appointed in 1978 under the chairmanship of a distinguished Nigerian Chartered Accountant and one-time President of the Institute. The committee, on which the Unesco Expert served both before and after the commencement of his mission, completed and submitted its report in 1982 which was finally adopted by the ICAN Council later that year and subsequently ratified by most of the participating institutions. The new scheme, "Education and Accelerated Training of Chartered Accountants in Nigeria" finally came into force as of November 1983. Accounting graduates of Auchi Polytechnic enjoy automatic exemption from the Foundation and professional Examination I (PE I> of the Institute and proceed direct to the Professional Examination I1 (PE 11) after fulfilling a one-year practical training requirement, to be serve2 at a Recognized Training Centre (RTC). (Some salient features of the new scheme are shown in Appendix F).

Under this scheme

19 The first batch of Auchi Polytechnic HND graduates eligible to sit the PE I1 examination will do so in November 1984 after having fulfilled the mandatory one-year practical training requirement under the National Youth Service Corps (NYSC) scheme. The Institute and the Polytechnic have worked out a special arrangement with the NYSC Secretariat whereby the HND graduates in Accounting are, as a matter of policy, deployed during their NYSC service- year at a Recognized Training Centre, enabling them to satisfy the ICAN one-year macdatory practical training requirement, a pre-condition to sitting the PE I1 examination.

Objective (a> (ii)

The Development of Course Materials for the HND Course

20. Being an applied discipline, Accounting cannot be effectively taught merely by the classroom lecture/discussion method, The classroom effort has to be supplemented by a pre-planned tutorial/seminar system and followed up with graded practice exercises and life-like case studies. This aspect of instruction becomes even more imperative when coupled with textbook shortages. Therefore, the development of course materials in the form of handouts, practice exercises and case studies, etc., must be an integral part of instructional input. An in-house study conducted by the Expert had clearly shown that the department had hitherto followed no particular system for the development of course materials and lectureTs were mainly left to their own devicas. There was complete unanimity among staff members that a uniform system of developing course materials sh,ruld be designed and introduced into the department.

21. The Question/Exerci;o Bank - The QEB System: It is an esta'liished practice that during the course of teachinz a lecturer prepares teaching materials in the form of illustrations, examples, case studies, practice exercises and assignments to be done at home, etc. If these materials are properly catalogued, filed and indexed, they can, in the course of time, build up into a sizeable body of teaching materials easily available for future teaching and reference purposes. It was in pursuit of this objective that the Expert designed and introduced the QUESTION EXERCISE HANDOUT BANK (Appendix G) into each course unit. Under the system staff members are

- 8 -

required to code number, according to the prescribed indexing system, each and every item of teaching material issued to students, tnsee copies of which are to be placed on the files under the departmental QEB filing system. The system was introduced in early 1982 and has been widely adopted by all staff members.

22. The Purpose and Objectives of the QEB System: The purpose and objectives of the QEB system, as defined in the original document, may be summed up as follows:

to build up a permanent body of teaching materials in each course which should be readily available to other staff members who may be assigned to teach that course in future;

to provide for a system of cataloguing and filing of these materials on a scientific and orderly basis; to help the course lecturer monitor to some extent his/her own teaching input in the course; to afford thehad of Department/Course Coordinator an opportunity to indirectly monitor a lecturer's progress in a particular course, both in terms of quality and quantity, as related to the handout input vis-a-vis the lecturing/teaching plan, referred to in paragraph 42.

23 The Accounting Student and the Practical Exposure Handicap: Based on his personal expertise, wide-ranging discussions with the national counterparts, consultations with Chartered Accountants in public practice and employers of accounting graduates, the Expert fully realized that Accounting students generally suffer from a serious handicap in the sense that, during their student days, they get very little exposure to the practical applications of the discipline. students, they have no laboratory facilities where they can test for themselves the efficiency of the theoretical knowledge they have gained in the classroom. Some of tham do manage to find suitable openings during the long vacation periods, but the majority of them go through school without ever having seen the inside of a ledger or a cash book or having tackled a real-life accounting or business problem, Educationists appr?ciate the 3

importance of this exposure and unanimously advocate practical industrial attachment as an integral part of the training programme, However, in real life, the inadequacy of infrastructural facilities tends to militate against the full implementation of this objective, at least durir,.; the initial stages of a student's course of study when he is not considered to be of much practical value by the prospective short-term employer. This Pack of practical exposure, therefore, seldom allows the najority of students to consolidate their grasp of the basic accounting concepts and technircles on the anvil of practical work experience.

unlike the Science and Engineering

- 9 -

24. Practical Workbooks in Accounting: Sincerely believing that the drawback could,to some extent, be mitigated by making the student tackle simulated case studies and practice exercises, the Expert, soon after the commencement of his mission, initiated the development of PRACTICAL WORKBOOKS IN ACCOUNTING. They are similar to laboratory books, generally used by Science and Engineering students in their practical experiments in the Laboratory. Preceded by step-by-step explanations of the concepts and techniques and adequately illustrated, they seek to introduce the student, topic by topic, to life-like accounting problems and to provide him with a series of graded exercises on which to consolidate his grasp of the conceptual situations and perfect his mastery of the practical techniques. The Expert sincerely believes that, used judiciously in connexion with a tutorial system under the supervision and guidance of a tutor, or attempted independently by the student, they can go a long way to helping him master the theory and technique of the double-entry system of book-keeping, the bedrock on which the philosophies and practices of the accounting discipline are founded.

,

25 Four books in the series planned to cover the entire spectrum of the Foundation Course in Accounting, and consisting of over 200 pages each, have been developed and are ready for publication. students may benefit from the introduction of this new approach to teaching this applied discipline, the Expert strongly recommends that arrangements should be made to publish these PRACTICAL WORKBOOKS IN ACCOUNTING on a priority basis and they should be made available to all students, not only in institutions of higher education in Nigeria but all over Africa and beyond.

In order that accounting

(For fuller details see Appendix HI,

Objective (a> (iii)

The Introduction of a Practical Student Attachment Training programme

26. Industrial practical training is an integral part of the NBTE .

curricula-based ND and HND programmes in all fields of technical education and a pre-condition to the award of the National and Higher National Diplomas in Nigeria. Auchi Polytechnic follows a well coordinated policy in this regard. A special cell in the Principal's office, headed by a senior-level Industrial Placement Officer, arranges and coordinates the placement of all Polytechnic students in industrial establishments, generally during the long vacation periods. This tri-partite arrangement of industrial training between the Industrial Training Fund (ITF), the Industrial Establishment and the Polytechnic requires the student to go through a pre-determined training programme. The student's progress under the industrial training scheme is closely monitored by the Polytechnic Industrial Placement Section and the department to which the student belongs. At the completion of his training, the student has to complete and file a report signed by his industrial supervisor, detailing various aspects of practical training he has received during the attachment period. This is a well-established system at Auchi Polytechnic and the Department of Accountancy fully participates in this programme.

- 10 - 27 Accountinp; Student and the Recognized Training Centre: The introduc:.lon of the new ICAN scheme "Education and Accelerated Training of Chartered Accountants in Nigeria" has added a new angle to the industrial. attachment programme as far as zccounting students are concerned, The scheme lays down that a student must have completed a 12-month practical training programme at a Recognized Training Centre (RTC) before he is eligible to sit the ICAN Final PE I1 Examination, This pre-condition of attachment to an RTC has the following important features:

(i> the examinee must be a registered student-member of

(ii) he must have completed a 12-month practical training the Institute;

period at an RTC prior to sitting the ICAN Final PE I1 Examination;

a Chartered Accountant firm in public practice in Nigeria or an industrial establishment/edueatisnal institution where an ICAN member, a Chartered Accountant, is employed in a managerial/senior executive capacity;

ICAN format, must be drawn up between the student and the Chartered Accountant, hereinafter called the Principal, and registered with the ICAN Secretariat;

(VI the Principal must put the student through the ICAN approved training schedule and make periodic reports to the Education and Training Department of ICAN to that effect;

no Principal is allowed to have more than six trainee-students at any given time and there is provision for the transfer of a trainee-student from one RTC to another to give him an opportunity to gain a different type of professional experience,

(iii) an RTC is defined as an establishment which is either

(iv) a formal contract of training, based on the official

(vi)

28. It is, therefore, clear that industrial practical training attachment in the case of accounting students following the ICAN programme, does not merely mean attachment to any industrial establishment. It must be at a Recognized Training Centre satisfying the aforementioned requirements and approved by ICAN.

29 - The Accounting Student and the National Service: Like Iledical graduater who, during the course of their NYSC service,are attached to approved medical establikhments, the ICAN secretariat has worked out a farmal arrangement with the NYSC directorate whereby accounting graduates, following the ICAN course of training, are deployed to RTC during their NYSC service period. This attachment counts towards the or,e-year mandatory training period, a pre-requisite to sitting the ICAN Final PE I1 Examination. By special arrangement with the ICAN Secretariat, the Department of Accountancy at Auchi Polytechnic acts as a mini-secretariat for this purpose. The department stocks relevant ICAN official forms and issLes them to interested students and, early during each academic session, furnishes the

- 11 - ICAN Secretariat with full particulars of the HND graduates, The ICAN Sec-?Lariat in turn P.llocates students to the Recognized Training Centres across the country and arranges with the NYSC directorate for their deployment to these centres. By reason of its special professional nature, this part of the industrial attachment programme operates independently of the Polytechnic Industrial Placement Section and is, by now, a well-established arrangement between the department and the ICAN Secretariat,

Objective (b) b

The Development of Capacity for the Procurement, Use and Maintenance of Audio-visual and Other Teaching Aids, Books and Periodicals

30 Activities relating to the implementation of this objective may be discussed under two headings:

(i)

(ii)

the establishment of an Audio-visual Teaching Aids Centre; and the development of Library Facilities.

31 - The Establishment of an Audio-visual Teaching Aids Centre: Preliminary discussions with regard to the establishment of the proposed Audio-visual Teaching Aids Centre were held with the Polytechnic authorities soon after the commencement of the Expert's mission, It soon became apparent that the authorities were of two minds, whether to establish a centrally-based centre for the entire Polytechnic or whether to let the individual departments and schools have their own separate facilities. Overtaken by other events, the issue has not yet been resolved,

32 Being a Government input, the Polytechnic had to provide the project with two pre-requisites; funds with which to acquire the necessary equipment and suitable accommodation to house the centre. Financial constraints, however, have prevented the project from moving beyond the drawing-board stage. By mutual agreement, the Expert, with the assistance of the Unesco Field Equipment and Subcontracting Division in the Cooperation for Development and External Relations Sector (CPX/PEC) has prepared a list of equipment which can be acquired at a later date as and when the circumstances permit, (See Appendix I),

33 The Develo.?ment of Library Facilities: The staff's response to A* L ~ z T X Q clearly indicated that the library facilities in the Accounting discipline, as they existed, were far from satisfactory, Books being a teaqher's only tool, ,staff members felt greatly frtzstrated by ti?z lack of adequate reference and reading facilities. The department therefore decided to set up a high-powered departmental committee, the Library Development Committee, under the chairmanship of a Senior Principal Lecturer, to take full stock of the situation and to make recommendations for its improvement. The Committee reported that of the titles in Accounting subject areas on the library shelves, the majority of them were not only obsolete, having been published over ten years ago, but also, in terms of sheer numbers, the books

- 12 - were grossly inadequate to meet the growing needs of a rapidly expanding department. from 334 in 1978 to 461 in 1981). and technical journals was equally disheartening. that the on-premises reading facilities (seating accommodation) in the Business School Library were totally inadequate to cater for the needs of a student population of 1,255 in the School of Business (1981 enrolment figures).

34 - ongoing process, the department, based on the Committee's recommendations, set up a permanent departmental committee, the Library Development Committee, which was to liaise with the library authorities with a view to re-furbishing the facilities and making regular recommendations for the acquisition of new titles and updating the subscription lists of professional and technical journals. several recommendations for the acquisition of new books.

(Student enrolment L-ri .tL; department of Accountancy had jumped The situation with regard to professional

The Committee also reported

The development of library and reading raom facilities being an

The Committee has been pursuing the matter actively and has made

Objective (c) (i>

Planning Teaching Staff Trained in Appropriate Fields for the HND Course

35 The Recurrent Staffing Problem: The TP!.!MQ findings clearly showed not only that the department was grossly understaffed, but also that the shortage was more pronounced in the core subject area - Financial Accounting, The immediate recommendation arising from the study was to allocate five of the ten vacant posts to the Financial Accounting specialization and to make an all-out effort to recruit qualified staff from both inside and outside Nigeria. However, over the years the department has registered more losses than gains in this regard.

36 The impact of the acute shortage of qualified accounting personnel, discussed in paragraphs 2-4 of this report, has been more keenly felt by the academic accounting departments in the-country's institutions of higher education than by any other segment of the economy. as a career by qualified accountants has never been one of the higher priorities in their career planning. polytechnics since 1980 has further aggravated the staffing situation since existing staff tend to move from the older institutions to the newer ones in quest of faster personal advancement. Furthermore, the new significantly improved salary scales granted ,y thr: univ-rsities and not yet implemented by the polytechnics have put the latker at a further disadvantage vis-a-vis I

the universities when it comes to staff recruitment. Taking all these factors into account, it was reulized at an aarly stage of the project that the department, while making every effort to recruit qualified staff on the open market, should evolve and introduce its own staff development policy.

The adoption of teaching

The emergence of over twelve new

37 The Staff Development Programme: A comprehensive staff development programme proposed by the Expert, and designed to develop, in the long run, an academically-viable indigenous faculty for the HND course, was accepted by the department and finally approved and adopted by the Polytechnic authorities. It was based on the following features:

- 13 - (a)

(b)

Four areas of sub-specialization were identified and adopted as a basis for tr-2 HND programme:

(i) Financial Accounting - ten core courses; (ii) Professional Accounting - eight courses; (iii)

(iv)

Cost and Management Accounting - six courses; Mechanized Accounting and Quantitative Techniques - six courses.

It was decided that instead of the present two posts, five posts of Senior Principal Lecturers should be created, one reserved for the Head of Department and the remaining four allocated one to each of these areas of sub-specialisation.

A vigorous effort should be made to fill these posts as soon as possible and each specialist should be designated as the course coordinator for his area of specialization,

Five trainee positions in the form of Assistant Lecturers-in- Training should also be created in the departmental budget on an annual basis.

These posts should be filled by the Polytechnic's own promising HND graduates or first degree holders desirous of making a career in teaching,

The Senior Principal Lecturers/Specialists should be assigned as supervisors to these trainee lecturers who should be given light tutorial responsibilities, with major emphasis being placed on assisting and encouraging them to pass the final professional examinations in the shortest possible time; if possible, within a year of their joining the department.

After serving for between two to three years and on gaining their professional qualifications, these young lecturers should be sponsored to read for Master-level qualifications in their area of choice, at a university at home or abroad, with a view to helping them realize their full potential as lecturers in Accounting.

In order to retain their services, the trainees should be made to enter into a bond to serve the Polytechnic for a specified period of time sfter gaining their profez,sional qualifications.

The scheme should be an ongoing process on a rotational basis, providing that there are Zive trainee lecturers working for their professional qualifications at any given point of time.

programme has been only partially implemented owing mainly t o financial and infrastructural constraints.

- 14 - 38 . The Course Coordinator System: In order to acbieve a grsa.ter degree of staff participation in the departmental affairs and to decentralize the departmental administration, the course coordinator system was introduced into the department and based on the following areas of course classifications:

(i) Financial Accounting

(ii) Professional Accounting

(iii) Cost and Managemect Accounting (iv) Mechanized Accounting and

Quantitative Techniques (VI Economic Studies

(vi) Legal Studies

10 courses

8 courses 6 courses

6 courses 6 courses 4 courses

Invariably a specialist in his own area of study, the Course Coordinator is responsible for supervising and guiding all staff members teaching courses in his area of specialization, performance, the initiation and assessment of proposals for updating the course structure and curricula, etc., fall within the bounds of his duties and responsibilities. The system is designed to make the department operate at an optimal level of efficiency both in terms of instructional performance and administrative competence.

The evaluation of staff and student

. The Strengthening of Teaching Staff Induction and the Development Programme

39- Staff Seminar Programme: The staff seminar programme introduced during the 1979/80 session was reactivated in 1981/82 and its scope was widened to include the entire staff of the School of Business Studies. After running successfully for one session,it once again ran into operational difficulties owing mainly to the acute staff shortages in the department during the 1982/83 and 1983/84 sessions and also because of frequent disruption of academic work caused by work stoppages by the Auchi Polytechnic Academic Staff Association (APASA). The basic framework for operating a staff seminar programme, however, has been fully established and it is hoped , that it will be re-activated as soon as the staff shortages becoma a thing of the past.

40- The Staff Manual: In furtherance of the stpff induction objective, the Expert developed a STAFF MANUAL of about 50 page,c which has b:.zn officially adopted by the Polytechnic authorities, In addition t,? giving an introductory account of the department, the manual deals with the duties and responsibilities of staff members at all levels and details the operational framework of the various departmental committees. A section of the manual deals with the examination regulations, duties of external examiners and rules and regulations governing the Gross Points Average (GPA) and Cumulative Points Average (CPA) computations, the points average system being an integral part of the semester system operating in the Polytechnic.

I

- 15 .-

41. Unesco Fellowship Programme: provided for 24 man-months of training, under the Unesco fellowship programme.

The project- document initially from July 1981 to September 1984, Two fGllowshim of

12 months each were provided for. Sponsor'ing staff meibers for short-term training programmes was, however, considered more appropriate to the staff development needs of the department. Five senior staff members benefited under the fellowship scheme. Three of them attended the International Teachers' Programme Summer School run by a consortium of about eight European and U.S. business schools held every two years at a different venue. One fellow attended a training course at the University of Pittsburg, U.S,A,,and the Principal himself was sponsored to undertake a study tour of technical institutions in Brazil, U.S.A., Canada and the U.K. with the sole objective of gaining a deeper insight into the latest curricula plenning and development trends in technical education. Full details of the fellowship programme are shown in Appendix C.

,

Strengthening of Evaluation of Teaching Staff Performance

42 . The Lecturing/Teachina Plan: The department did not appear to have a well-defined policy with regard to a pre-planned approach to teaching. A LecturindTeaching Plan System which requires a course lecturer to prepare a teaching budget, dividing the course syllabus into weekly teaching blocks with adequate reference to textbooks and further reading lists first introduced during the 1981/82 session has now become an established policy in the department. The LecturindTeaching Plan is prepared by the course lecturer prior to the commencement of the semester and photocopied, with three copies being filed on the departmental files and one copy being provided to each student taking that course.

IV. MATTERS INCIDENTAL TO THE IMPLEMENTATION OF THE PROJZCT OBJZCTIVES 43 Teaching Assiqment and Administrative Responsibilities: In addition to performing normal teaching duties, the unscheduled departure of senior staff and the general staff shortages in the department made it necessary for the Expert to assume administrative duties for the department during the 1982/83 and 1983/84 sessions. This constituted a heavy workload in addition to his official duties.

44. The Student Handboz: A 50-page STUDENT HANDBOOK, designec! and developed by the Expert, was issued for the first time to all the students in the department during the 1982/83 session. operational aspects of the departmental set-up &Ad administration, objectives of the academic programmes, method of instruction, operation of the tutorial system and procedures relating to the evaluation of student perfornance and diploma classifications, the booklet aims at a faster integration of freshmen/women students into the Polytechnic Community by briefing students of their own role and ?lace within the academic framework.

Containing details of the

- 16 -

45 The Tutorial System: The tutorial system has come to be accepted as an essential and integral part of academic life in an institution of higher education. The system was introduced into the department during the 1982/83 session and has been operating fairly successfully ever since. Under the tutorial system a cross-section of students from each class are assigned to a lecturer to whom they can turn in the first instance for guidance and counselling on any academic or personal problems encountered by them. Once assigned to a tutorial section, the student stays with that tutor during his entire stay at the campus and knows who to turn to if the need arises. The tutor, in turn, being a guardian of his wards, is supposed to keep an eye on their academic performance and intellectual pursuits. The system seeks to create a family atmosphere between the two sections of the community,

46. The Student Consultative Council: Again with a view to creating an atmosphere of understanding and friendship among staff and students, the concept of regular and formal consultations between staff members and student representatives has become a reality in the department. The committee, called the STUDENT CONSULTATIVE COUNCIL, which formally meets at least twice a semester, under the fatherly chairmanship of the Head of Department, provides a forum where either side can table and discuss any issues of mutual interest and concern. The student side is represented by members of the Professional Accounting Students' Association (PASA) and class representatives. By building a channel of communication between the students and staff, the forum has succeeded in creating a family spirit within the department and has helped to ward off confrontational attitudes and tensions which might otherwise have built up from lack of proper communication.

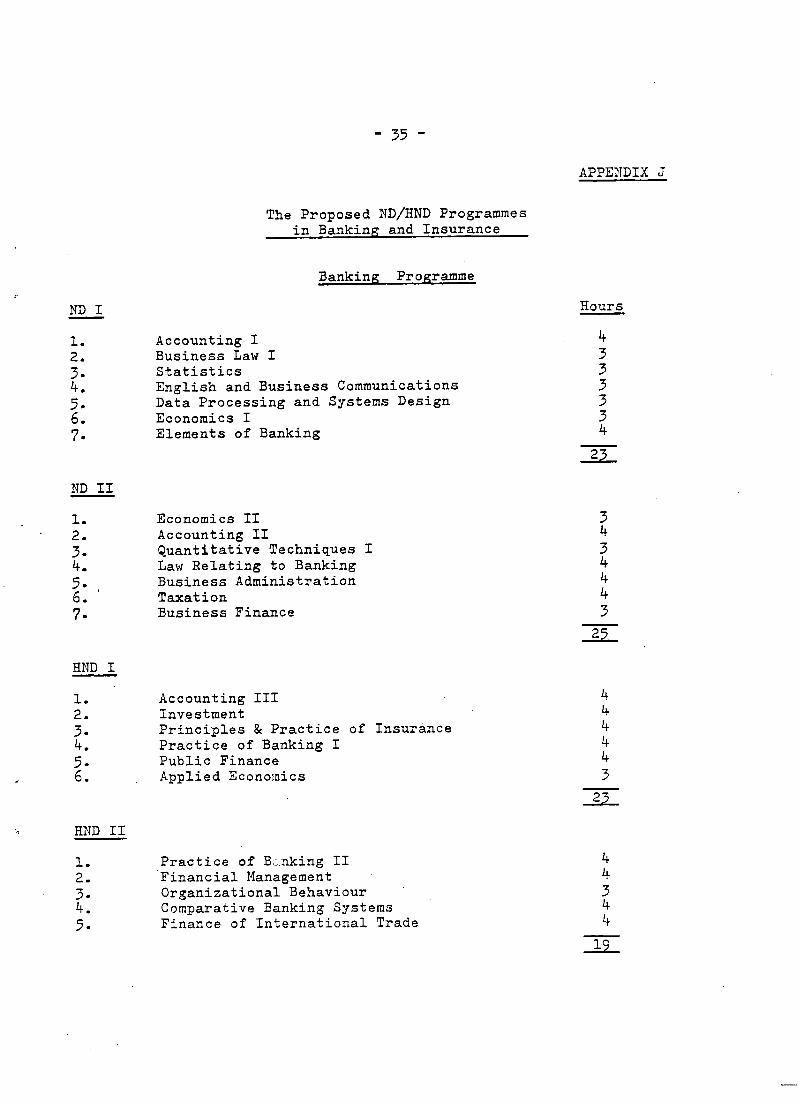

47 - The Proposed ND and HND Diplomas in Finance (Banking and Insurance Options): Notwithstanding the temporary staff shortages in the department, a stage in its academic development has been reached where allied academic programmes in the area of Financial Administration can be viably introduced into the department. In this connection, a programme for offering ND and HND programmes in Finance (Banking and Insurance majors) has been prepared and recommended for adoption by the Polytechnic in the near future (see Appendix J).

V. ACHIEVEMENT OF THE OBJECTIVES

The Primary Objective

48, - The primary objective of the project, the "Implementation of a Higher National Diploma in Accounting" ha% been fully realized. The conversion of the prior three-year NBTE-based NND programme into a full ND and HND four-year programme in October 1980 was the first step towards the realization of this objective. Since the HND course in Accounting is professionally-oriented with a strong link with the Institute of Chartered Accountants of Nigeria, the conversion of the newly-introduced ICAN examination programme "Education and Accelerated Training of Chartered Accountants in Nigeria" into a teaching programme can be said to b e the

- 17 - final step in the implementation of this objective, With the formal adoption- df the revised course structure and syllabi in the 1984/85 academic session the full implementation of this objective will have been achieved.

Other Objectives

49 - Other ancillary objectives: I

(a)

(b) the expansion of the present staff development programme to

(c) the introduction of practical student attachment training,

the preparation of course materials relevant to the Nigerian situation;

cover the new course; and

1

It may be stated that objectives (a> and (b), with the development of four Practical Workbooks in Accounting and the introduction of the new ICAN/NYSC-based scheme for the placement of HND graduates at RTCs during their national service year, have been substantially implemented. As regards objective (c), with the adoption of a practical staff development programme to build up an academically-viable indigenous faculty from its own resources, a firm foundation has been laid, the results of which are bound to be felt in the not-too-distant future.

L

VI . FINDINGS AN D CONCLUSION

Inadequacy of Library and Reading Room Facilities

50 In the course of implementing the project objectives it was discovered that the existing library and reading room facilities were totally inadequate to meet the needs of a fast growing student population, particularly in the School of Business Studies. Most of the titles in Accounting and related subjects were found to be out-of-date by over a decade and no new books had been purchased or made available for over four years. This state of affairs is bound to adversely affect the academic standards of the department. Even the reading room facilities in the existing, make-shift, Business School Library Section are meagre and inadequate. The construction of the proposed Central Library for the entire Polytechnic should be accorded a high priority in the Physical Resource Development Plan of the Polytechnic.

Chronic Staff Shortages

51. It has been observed that the department pereniallg suffers from chronic staff shortages. Qualified Nigerian accountants apFear reluctant to adopt teaching as a career, resulting in a heavy dependence on expatriate qualified staff. This dependence on non-Nigerian staff can create problems if, far any reason, either the source dries up or the existing staff decide to leave en masse. When drawing up staffing plans for the department this potentially dangerous factor should not be ignored.

- 18 - 52 Staff shortages generally lead to the overloading of existing staff members and a 1,eliance on part-time staff whose professional competence and reliability cannot always be guaranteed. With the Polytechnic located in a small township, even opportunities for hiring the services of part-time staff are rather limited, The only conclusion to be drawn, therefore, is that academic standards are bound to-be adversely affected by this academically unhealthy situation.

Support Staff Services.

53. Support staff services is another area which affects the administrative and academic efficiency of the department. The deployment of support staff should be related to the needs of the department in terms of student numbers and staff to be catered for. It has been observed that the inability of the support staff to produce teaching materials, an essential aid to efficient teaching, has at times led to embarrassing situations and affected staff morale, Provision for support staff should be based on the needs of the department rather than the application of the arbitrary rule of one department one typist. Even the quality of support provided needs to be examined closely.

54. It has also been observed that an indiscriminate admissions policy has at times been adopted in total disregard of staffing and physical facilities available in the department. Staff shortages and larger student in-takes do not go hand in hand and can create numerous academic and administrative problems. The department must be commended for strictly observing the minimum entry qualification regulations but a more discriminating admission policy has to be adopted with regard to quality and number of in-take, both at the ND and HND levels, if academic standards are to be maintained and improved upon.

VI1 . RECOMMENDATIONS

55 In order that, in the long run, the department derive full benefit from the substantial investment in this project, the following recommendations, which emerge from the implementation of the project objectives, should be adopted and implemented:

(a> The revised course structure should be adopted and introduced in the 1984/85 academic session. It incorporates the following three iL2ortant features:

(i> it is in full conformity with the NBTE requirements for the award of National, and Higher National Diplomas in Accountancy;

Accelerated Training of Chartered Accountants in Nigeria" and covers the entire syllabus with respect to the Foundation, Professional I and Professional I1 Examinations of the Institute; and

(ii> it is based on the new ICAN scheme, "Education and

- 19 -

(C>

(f)

(h)

(i>

(iii) it is educationally broad-based in the sense that three new courses have been addsd and all anomalies resulting from duplications, gaps and repetition, etc., have been removed,

A serious thought should be given to the publication of the four Practical Workbooks in Accounting developed by the Expert in the course of the implementation of the project's objectives so that they are made available not only to students undergoing Accounting courses at Auchi Polytechnic, but also to all Accounting students in institutions of higher education in Nigeria.

Staff members should be encouraged to develop similar workbooks on topics drawn from the ND and HND courses in Accounting, Costing and Auditing.

Practical industrial attachment arrangements, worked out between the ICAN Secretariat and NYSC directorate, providing for the de2layment of Auchi HND graduates at the ICAN-approved RTCs during the national service year, should be maintained and followed up.

The Head of Department and the course coordinators should ensure that the Question Exercise Bank (QEB) system established in the course of the project is maintained and made use of by all course lecturers.

After a decision has been reached on whether to set up a centrally-based Audio Visual Teaching Aids Centre under the control and supervision of the Polytechnic Librarian or whether departments/schools should be allowad to have their own centres, the possibility of acquiring audio-visual equipment through the CPX/PEC division of Unesco, as suggested by the Expert in his memo of June 1983, should be given serious consideration.

With a view to improving the library facilities, regular recommendations for the acquisition of new titles/editions in all areas of Accounting and related disciplines should be made by the department. Course coordinators should be made responsible for the development of library facilities in their own course areas, The subscription lists for professional and technical journals should also be reviewed on an annual basis.

The depar tment should ensure that the STAFF DEVELOPMENT PROGRAMME linked to the lecturers-in-training scheme, as already introduced, is vigorously pursued with a view to building up the nucleus of an academically-viable indigenous faculty.

In the meantime, no effort should be spared to recruit senior- k,21 &aff fTom national and international sources in order t:, rectify the chronic staff shortages in the department.

- 20 - Since the success of the course coordinator and lecturers-in-training schemes rests on the availability of specialist teachers in core-subject areas, a vigorous effort should be made to recruit specialist lecturers.

The staff seminar system, a firm foundation for which has already been laid in the department, should be resuscitated as and when the staffing situation permits.

The STAFF MANUAL compiled by the Expert should be published and made available to all staff members in the department. After suitable amendments,the possibility of its application in other departments/schools on a Polytechnic-wide basis, should also be exzmined.

The Head of Department/course coordinators should ensure that the LECTDRING/TEACHING PLAN system, already fully accepted and established in the department and linked to the QEB system, is maintained and used by all course lecturers, without exception, as a pre-planned approach to teaching, and the QEB system made an integral part of evaluating staff performance.

Notwithstanding the staffing situation, a stage has been reached1 where the department is in a position to introduce a new ND/HND course in Finance leading to Banking and Insurance majors. It is recommended that the department give serious thought to introducing the new courses as and when the staffing situation permits.

The subject/location-based.open-ended filing system, as already introduced in the department, should be operated and maintained, and, in order to further improve the operational efficiency of the department, the STUDENTS' PERSONAL FILING SYSTEM (SPFS), already designed as an integral past of the departmental filing system, should be fully implemented and maintained.

The STUDENT HANDBOOK,designed by the Expert and first issued during the 1982/83 session, should be produced and issued annually to all freshmen/women students as part of their induction programme.

The S'UDENT GONSULTATIVE COUNCIL (SCC) , comprising representatives of students and staff, designed to provide a forum where either side csn table and formally discuss issues of mutual concern and interejt should be constituted early every session with a viev to providini a communications channel and thereby creating a friendly and family-like atmosphere in the department,

Senior Principal Lecturer in Accounting and Head of Department Senior Principal Lecturer in Law (Vice Principal) Senior Lecturer in Accounting (transferred as Bursar as of of October 1978) Senior Lecturer in Accounting (left in 1980) Lecturer in Accounting

Senior Lecturer in Law (deceased) Lecturer in Law (resigned Aug 1983) Principal Lecturer in Economics

Qualifications

Lecturer in Economics (transferred to Quantity Surveying in early 1981) Higher Instructor in Data Processing (resigned August 1982)

Senior Principal Lecturer and &ad of Department (Feb 83 - Aug 83) (killed in a road accident) Lecturer in Accounting

Lecturer in Accounting Lecturer in Data Processing

Lecturer in Statistics

Senior Principal Lecturer and'Head of Department (assumed duty July 1984)

HND (Accounts) A.C.C.A., A.C.A. E.Sc, (Accounts) B.Sc. (Econ), 14 . B . A. B.Sc. (Sonp. Science), r.r.C.1. F.C.C.A., A.C.A.

- 23 - APPENDIX 3 (contd)

Expatriate (Non-Nigerian) Staff

Name

MAITIN, T.P. - THANABALASINGHAM , K .

BERI, S.K.

SILVA, D.T.

ATUGODA, M.S.

IDDAMALGODA, R.

SARAVANAPAVAN, T.V,

ANSAH, G.K.

WATTS, K.

Position

Senior Principal Lecturer in Account ing(Dec .77- Dec. 83) Principal Lecturer in Accounting (resigned Aug 1983)

Principal Lecturer

Lecturer in Accounting (resigned July 1982) Lecturer in Accounting (resigned July 1982) Lecturer in Acccunting (resigned September 1983) Lecturer in Accounting

FI.Sc. (I4.I.S. 1 A.C.C.A., C.A. (Ghanz) LL.B. Dip. M .'S c .

- 24 - APPENDIX C

Unesco Fellowships

Field of Place of Period of Study Position on - mama Study Study From - To Re turn - UTOMARILI, S.Q. Accounting Manchester 09.07.81 03.10.81 Senior

L I.T.P. Business Principal International School, Lecturer azd Teachers ' Manchester, Head of Programme U.K. Department

USIDAMA, N.B. F inanc i a1 Stockholm 10.07.82 10.09.82 Senior Administration School of Principal and I.T.P. Economics, Head, School International Sweden of Business Teachers! Studies P r o gramme

IGHARO, P.O. New Trends in Visited 07.11.83 15.12.83 Principal, Curricula Universities/ Auchi Development Polytechnics Polytechnic Planning in in Brazil, Technical U.S.A., E duc a t ion Canada & U.K.

EAZUAYE, E. Personnel/ University 07.05.84 20.06.84 Vice PrinciFal Institutional of Pittsburg and Senior Administration -'Pr i n c i p a 1

Lecturer in Lav

UI(!JUMABUA, G.C. Business London 15.07.84 31.08.84 Principal Management Business Lecturer and I.T.P. School, Head of International London, Department o f Teachers U.K. Business Programme Administration

- 25 - APPENDIX D

Student Enrolment and Graduate Output

Student Enrolment

Academic ND Accounting HND AccountinE Session National Diploma in Higher National Diploma October Accounting (A Two= in Accounting (A Two- to July Year Programme) Year Programme after

the ND Course)

1st year of study

1978/79 116

1979/80 99 19 8 0/8 1 167 1981/82 143 1982/83 120

1983/84 130

2nd yekc of study

112 106 75 119 118 73

3rd year of study

72 106 116 a2 42 49

4th year of study Total -

34 72 110

117 75 50

334 383 468 461 3.55 302

~~~ ~

To tal 775 603 467 4.58 2 9 303

Graduate Output

19 7 8/7 9 1979/80 1980/8 1 19 81/82 l982/83

109 98 72 116 106

32 68 106 118 61

19 8 3/8 4 71 50 121

Total 5 72 435 1,007

Mote: - 1. The numbei of students on roll does not necessarily agree with that in

the subseqxent year because of weaker students dropsing out or being required to repeat the gear under the Polytechnic examination regulatioEs.

ar.d IIMD levels and MD graduates are not automatically adnitted into t3.e HMD programme, as they are generally reqaired to spend a year o ~ t in industry after completing their ND Frogramme.

3- Students zho complete the ND and HND progrimes successfully ari a:.ra=.ded the ND and €IBD diplozas respectively.

2. Students graduating after completing the two-year programme both at PTD

- 26 - APTENDIX E

3;igramme of Study

Revissd Course Structure Based on the New ICAN Scheme "Education and Accelerated Training of Chartered Accountants in Nigeria"

ND Accountina - National Diploma in Accountinq PTD I - First Year of Study

The New TrainingGcheme - Some Salient Features of the Scheme . 1. Universities and Colleges of Technology will play a more active role in the training of future accountants. To this end, students wishing to become chartered accountants will be encouraged to attend a full-time course in a Polytechnic leading to a higher diploma in accountancy or obtain a degree from a University at present recognized by the Institute of Chartered Accountants of Nigeria. The present system of full-time articleship or approved studentship will also continue.

2. There will be a continuous dialogue between the Institute and the Higher Institutions of Learning with a view to reviewing and agreeing on the syllabuses and the standard expected of the qualifications obtained from these institutions. To this effect, there shall be a joint committee to approve accountancy qualifications in the Righer Institutions of Learning. The committee shall consist of the representatives of the Institute of Chartered Accountants of Nigeria and selected universities and Polytechnics at present recognized br the Institute. The Committee - , - shall examine particular courses of instruction at different Higher Institutions of Learning and approve those meeting the requirement criteria o.f the Institute of Chartered Accountants of Nigeria.

3- The Council of the Institute shall nominate suitably qualified persons for appointment as Reviewers of the professionally-oriented subjects of the examinations conducted by the Higher Institutions of Learning so recognized. The ;erson so norr,inated would moderate the question papers as well as model answers marked by the internal exaniners as would enable him to be satisfied about the contents of the programme and their standards.

4. The rule whereby each Higher Institution of Learning is expected to have on its permanent staff two qualified members of the Institute shall not he mandatory in view of the fewness of qualified accountants in the country. Bigher Institutions of Learning would be encouraged to recruit qualified lecturers including professional accountants. These institutions are required to ensure that professionallg-oriented suSjects are tazght by professionallr-qualified accountants which should be done by the emplogaect of pofessionallg-qualified accountants as part-time lecturers.

5. The Institute, through its District Societies, will conduct a survey of the accl-lunting departments of all establishments in Nigeria and determine where rr,ajor accountancy works are carried out in these departments and. where the department is mar-ned by a member of the Institute; such an organization shall be designated "Recognized Training Centre" (RTC) . Firms of practising accountants shall automatically become RTCs. Every member of the Institute engaged in an RTC shall be eligible to employ six graduates at such RTCs.

6. The Ixstitute shall draw up a training progranme that is expected to be completed by a student attacked to-an RTC. This Frogramre shall be

- 29 - APPENDIX F (contd)

given to the employer of the student who shall ensure strict compliance. The training programme will cover the various aspects of the profession in order to provide the student with experience in different facets of the Nigerian economy.

7. Every student employed in an RTC shall maintain a training record card in a prescribed form. to the Secretariat of the Institute at half-yearly intervals shall show the nature and extent of work done by such a student during the relevant period. It shall be signed by the student and the qualified accountant in the RTC.

This card which must be completed and returned

8, Graduates of Universities and Colleges of Technology shall undergo a two-year training period in an RTC. graduates on the National Youth Service in RTCs so that the one-year service could count as part of the two-year training.

Efforts should be made to place

9. On allocation of a student to an RTC, a training contract shall be entered into between the employer, the student and the Institute so as to ensure involvement of the emplogir in the training of future accountants. There shall be a provision for the transfer &%e cunpletedtraining period where this is necessary.

10. Graduates of other disciplines who may wish to become chartered accountants shall either first obtain the prescribed qualifications from a College of Technology or University recognized by the Institute and then enrol in an RTC or take up articles of clerkship or approved studentship in the traditional manner.

11. The Institute shall conduct three examinations, namely: Foundation Examination, Professional Examinations I and 11. Professional Examination I1 shall be a test of the student's ability to apply theoretical knowledge to solving practical problems. The subjects are as follows:

A.

3.

C.

Foundation Examination: Accounting I Ec onornics Quantitative Analysis Law I Business Management

Professional Examination I: Accounting I1 Cost Accounting Auditing and Information Processing Systems Law I1 Taxation I Professional Examination 11:

12. Graduates from Higher Institutions of Learning who have been admitted into an RTC are eligible to sit for the Professional Examination I1 at the expiration of twelve months'training in the RTC but they will not be eligible for admission to membership of ,the Institute until they have satisfactorily completed their 24 months training in the RTC.

APPENDIX G

The QEE System - Question/Exercise Handout Bank A*1 purposes each staff member is required to strictly follow the - cataloguing/indexing system detailed hereunder:

A.2 Each and every question, practice exercise or other teaching material given out to students as a handout shall be code-numbered as laid down in Section A.3.

In order to build up a Question/Exercise Handolzt Bank for teaching

3

A.3 The code number which shall be cut out on the right-hand top corner of page one of each handout shall consist of four sections:

Section I :

Section I1 :

Section I11 :

Section IV :

to indicate the academic session sag. 82/83 - academic session commenced October 1982; to represent the Course initials/abbreviation and the year of study, e.g.: FA I (Financial Accounting Year 1) MA 4 (Management Accounting Year 4); to represent the course lecturer's initials, e.g.: TPM (T.P. Maitin) VOO (V.0. Osagie); the number allocated to the particular handout, e.g. 7, signifying that six handouts have precalsd this one during this sesston. The .one .

to follow will be numbered 8.

The number will begin with 1 each academic session and number ,1 shall always be given to the Teaching/Lecturing Plan prepared by the Course Lecturer, a copy of which has been supplied to each student taking that course.

Illustration; 82/83/TAX.4/BCN/14 - 82/83 Session, Taxation Pear 4 Mr B.C. Njokwna, handout number 14. 82/83/AUD/TPIiI/lO - 82/83 Session, Auditing Year 2 Dr T.P. Maitin, handout number 10.

A.4 File numbers ACC/E/561 - kCC/E/599 have been al1ocatr.d to the QEB files in the departmental filing index.

A.5 Filinq System:

(i> Each lecturer will indicate the code number on the draft before passing it to the typist for typing/'stencil cutting ;

- 32 - APPENDIX G (contd)

(ii)

(iii

(iv)

(V)

(vi)

(vii)

After the typist has finished typing, he/she shall indicate his/her identity by cutting his/'ner initials on the stencil together with the date on which the job was completed, This will appear on the last page of the handout, a few spaces below the text. If the handout is cut out by the lecturer himself he shall indicate so in like manner; Once the handout has been duplicated, it shall be the responsibility of the lecturer concerned to hand in three copies of the handout to the departmental secretary for filing purposes;

The departmental secretary shall punch the handout and file all three copies on the relevant file strictly in consecutive numerical order. There shall be no gaps between one number and the other;

The first copies each Semester/Session shall be those of the formal lecturing/teaching plan mapping out the teaching of the course during the semester, a copy of which shall have been issued to each student; There shall be a separate file for each course held in two filing cabinets and the keys to the cabinets shall be held by the departmental secretary;

If the handout has been culled out of a textbookijournal or adapted from a past question paper, etc., the fsct shall be so stated on the last page of the transcript.

A.6 Removal of Papers fr0.m the File:

Lecturers may refer to the previous handouts for teaching and examining purposes, but, under no circumstances, should any paper be removed from the file.

A-? PurDose and Objectives of the QEB:

ThP purpose and objectives of the exercise bank may bn summed up as n

follows :

(i 1 To build up a permanent body of teaching materials in the department which should be available for use by other staff members in future years;

these materials on a scientific and orderly basis;

his/her own progress in the course;

indirectly monitor a lecturer's progress in a particular course from both the quantitative and qualitative view-points, particularly in relating the handout ol;tput to the lecturing/teaching plan referred to in Section A.5 (v) of this Appendix.

2,

(ii) To provide for a system of cataloguing aad filing of

(iii) To help the course lecturer monitor, to some extent,

(iv) To afford the Head of Department an opportunity to

- 33 - APPENDIX iI

.

Practical Workbooks in Accounting

L, Practical Workbooks in Accounting

' Basic Accounting Entries Book I

"The Debit and Credit Concept" A manuscript of 236 pages ready for publication.

2. Practical Workbooks in Accounting Book I1 Accounting for Credit Sales and Fixed Assets Provisions,Reserves and Disposals .

A manuscript of 287 pages ready for publication.

3- Practical Workbooks in Accounting Book 111 Preparation of Financial Statement including Non-profit Making Organizations and Incomplete Records A manuscript of 239 pages ready for publication.

4, Practical Workbooks in Accounting Book IV The Partnership and Joint Venture Accounts A manuscript of 262 pages ready for publication.

..

- 34 - APPERDIX I

Recommendation concerning the Purchase of Audio-visual Equipment

The following is a list of Audio-visual equipment recommended to be purchased for the proposed Audio-visual Teaching Aids Centre for the

4 Department of Accountancy,to cater for a student population of 350 to 400:

Song Equipment

L, Overhead projectors

2, Slide projectors

3. 4. 5. 6. 7. a. 9- 10 . 11 . 12 . 13 - 14.

15 16.

Audio cassette player/recorder Video cassette player/recorder

16mm movie projector Phono-disc players Colour T.V. receiver/monitor

Portable T.V. camera Portable lighting Lettering kit

Transparency makers Projection stands/carts

Portable projection screens Video monitors, wallmocnted Photo-copiers Typewriters - English memory

Quanti t j

4 4 6 2 1 4 4 1 1 1 2 2 4 4 1 1

MOTE

(i) Since models and prices keep changing rapidly, they have

- been omitted.

(ii) Two 20' I:. 24' Air conditioned rooms especially wired with adequate number of power socket points and reliable power supply sgstern, suitably furnished with an attached technician's office/ark roon are considered the minimum accommodation re qui r e men t s .

(iii) Overhead projectors can be permanently installed in the classrooms.

- 3s - APPENDIX J

The Proposed ND/HND Programmes in BankinR and Insurance

Banking Programme

ND I - 1. 2. 3. 4.

6. 7.

5.

ND I1 - 1. 2. 3. 4. 5- I 6. 7.

Accounting I Business Law I Statistics English and Business Communications Data Processing and Systems Design Economics I Elements of Banking

Economics I1 Accounting I1 Quantitative Techniques I Law Relating to Banking Business Administration Taxation Business Finance

Hours - 4 3 3 3 3 3 4 zz

3 4

4 4 3 25

HND I - 1. Accounting I11 2. Investment 3. 4. Practice of Banking I S* Public Finance 6. , Applied Economics

Principles & Practice of Insurance

1. Practice of B,:.nking I1 2. Financial Management 3. Organizational Behaviour 4. Comparative Banking Systems /- e; Finance of International Trade

4 4 4 4 4 3 3 -

4 4 3 4 4 19 -

- 36 - APPENDIX J (ccntd)

Year I

1. 2. 3. 4. 5. 6. 7.

Year I1

1. 2, 3. 4. 5- 6.

Year I11

1. 2. 3. 4. S.

Year IV

1. 2. 3. 4. 5.

Insurance Programme

Hours - Economics 3 Accounting I 4 General Principles of Law 3 Quantitative Analysis 4 English Language & Business Communications 3 Data Processing and Systems Design 3 Principles & Practice of Insurance 4

Insurances of the Person Property and Pecuniary Insurance Insurances of Liability Insurances of Transportation Life Assurance Law & Practice Pensions and Related Benefits

Business Management Life Insurance Practice Pension Scheme Design and Administration Marine & Aviation Underwriting and Claims Motor and Liability Insurances

Financial Management Property Insurance Underwri-ing ani Claims Principles & Practice of Be-insurance Risk Management Insurance Broking Management