33

DEVELOPMENT OF COMMON USER INFRASTRUCTURE FACILITIES 23 April 2015

DEVELOPMENT OF COMMON USER INFRASTRUCTURE FACILITIES

23 April 2015

2

Common User Facilities

New Depot at Meramandalli (Odisha)

CUF at Borkhedi(Nagpur)

PNGRB Bid – Ennore-Manali Pipeline

3

POL Infrastructure facilities (Terminal /Depots/LPG Bottling Plant/AFS)forms the backbone of Oil Marketing Companies (OMC’s) energysupply chain

Presently most of POL infrastructure facilities are owned and operatedby OMC’s, typically located in same vicinity and catering to their owndemand

Development of these POL facilities by OMC’s to cater their ownrequirements for the same market leads to duplication of infrastructureand sub-utilization of resources at industry level

To address above, BPCL, HPCL & IOCL (“OMCs” or “Sponsors” )proposes to develop Common User POL Facilities

Common User Facilities (CUF) would primarily be used by OMCs’ &would help in Rationalization of capital requirements at industry level Cost effective and efficient operations due to economies of scale

Background

4

Secretary(PNG) took a meeting of the officials of the public sectorOMCs viz. IOC, BPC and HPC on the issue of Common User facilitieson 07.04.2014.

Following were agreed Centralised planning for infrastructure required for POL and LPG in

the next 10-15 years would be done by PPAC. An SPV, as recommended as the preferred option by the OMCs out

of options recommended by SBICAPS, will be set up to take up common infrastructure projects in future.

OMCs to decide structure of the SPV after due discussions within the next 15 days.

OMCs to decide on list of existing facilities to be handed over to the SPV once formed.

SPV to be formed for implementation of CUF by July, 2014.

Background

5

The OMCs obtained “In principle Approval” from their Board ofDirectors for formation of JV/SPV for developing CUF.

Core Committee formed for finalization of MoU amongst PSUOMCs, members nominated by each OMC.

Background

6

Following constraints noted for operationalising CUF thru JV mode The Company would be treated as a Deemed Govt Company, since

no PSU holds more than 50% shareholding, but CollectiveShareholding of the PSUs would be > 50%.

CVC guidelines, CAG Audit would be applicable. It would fall under purview of RTI Act. Obtaining permission from “Competition Commission of India” for

integrating existing facilities. The JV would be a Related party to all 3 OMCs. Hence, all

procedures wrt Related Party Transactions would have to be followed.Transaction Pricing would have to be maintained on Arms’ Lengthbasis.

Repeated Award of contract to JV on Nomination Basis would not bein line with Vigilance Guidelines.

There would be an operating cost associated with the JV formationand operation.

Constraints in JV formation

7

Economic Advisor and DG(PPAC), vide letter dt 11.07.2014,advised requirement of development of Centralised PlanningModel for Common User Facilities for Petroleum Products forPublic Sector Oil and Gas Marketing Companies.

A steering Committee consisting of DG(PPAC) and 3 EDs from OilCompanies was formed to develop the Centralised PlanningModel.

PPAC study

8

Objectives of the study To formulate a Centralised Planning mechanism for operationalising the

concept of Common User Facility in respect of POL Terminals and LPGBottling Plants of Public Sector of Oil Marketing Companies (OMCs)

To identify tentative locations for future infrastructure which would serveas the basis for the OMC plans and specific initiatives to be undertakenunder the CUF regime for the period upto 2019 in the short term andupto 2029 in the long term.

To highlight challenges and opportunities to OMCs in developing POLterminals / LPG Bottling Plants under the concept of Common UserFacility.

To capture broadly the projected requirements of various modes oftransportation of POL/LPG eventuated from the projected demand ofOMCs

To highlight changes that may be required to be effected at the policylevel to ensure the effective functioning of the CUF arrangement.

PPAC study -Objectives

9

Report presented by PPAC to Secretary, P&NG on 16.12.2014 Following category of locations kept out of purview of CUF

Coastal Refinery Pipeline

It was agreed that “Structure of CUF would have to be jointly decidedby OMCs i.e. JV/SPV/Lead Company Approach or any other hybrid.To be conveyed by 10.01.2015.”

PPAC Report – Presentation to Secy P&NG

10

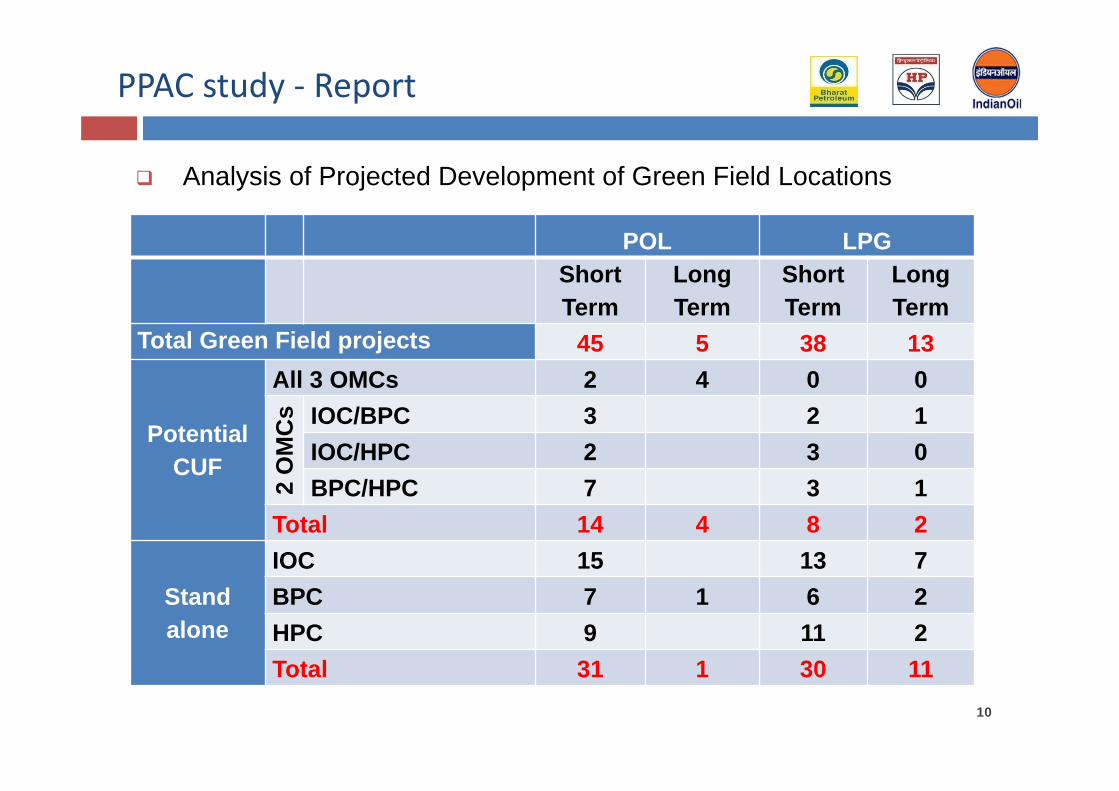

Analysis of Projected Development of Green Field Locations

PPAC study - Report

POL LPGShort Term

Long Term

Short Term

Long Term

Total Green Field projects 45 5 38 13

Potential CUF

All 3 OMCs 2 4 0 0

2 O

MC

s IOC/BPC 3 2 1IOC/HPC 2 3 0BPC/HPC 7 3 1

Total 14 4 8 2

Stand alone

IOC 15 13 7BPC 7 1 6 2HPC 9 11 2Total 31 1 30 11

11

Considering constraints in formation of JV, following models identifiedfor implementation of CUF Nodal Company Concept amongst OMCs with CAPEX sharing. Development of infrastructure through a private operator on BOO/BOOT

basis.

Lead Company Concept amongst OMCs. Project-wise implementation models and status was communicated to

MoPNG on 09.01.2015. Thereafter, status updates are being provided to PPAC, who are

monitoring implementation of CUF. Monitoring Mechanism

Project Management Groups for LPG and POL to meet on monthly basis. To be reviewed by a Committee of Dir(M)’s of the OMCs on quarterly

basis. Report to be submitted to PPAC on monthly basis.

Models Identified for CUF implementation

12

As per MoM of the meeting All CMDs were of the view that the JV route was the preferred

mode for implementation of CUF. Accordingly, PPAC would drawup a plan in consultation with OMCs

Issue Whether we should proceed with the current process

or proceed with JV formation. In case if JV route is to be adopted, individual OMC should obtain

permission from Board for placement of Work Orders on JV, onnomination basis, for development of CUF at identified locations.

MoP&NG meeting dt 21st March 2015

13

POL– Short Term – Action Plan

Sr Identified Locations

CUF-OMCs Proposed Model Nodal

Co. Remarks

1 Raipur IOC/BPCDevelopment through a private operator on BOO/BOOT

Construction by IOT.Work in progress. Expected

Commissioning –June/July 2015

2 Borkhedi(Nagpur) IOC/HPC

Development through a private operator on BOO/BOOT

Discussions in progress with IOT. Expected

Commissioning –March 2018

3 Tatanagar BPC/HPCDevelopment through a private operator on BOO/BOOT

Land purchased by IOT.EC obtained.Commercial offer

from IOT awaited.

14

POL– Short Term – Action Plan

Sr Identified Locations

CUF-OMCs Proposed Model Nodal

Co. Remarks

4 Bhopal IOC/HPC Nodal Company with Capex Sharing IOC

Land identified. Follow up being made with

State Govt for revalidating demand note.Railway Siding feasibility

established.

5 Sambalpur BPC/HPC Nodal Company with Capex Sharing BPC

Land identification completed. Application for Land Acq can

be submitted after Notification of LARR 2013.

6 Gulbarga/Bellary BPC/HPC Nodal Company with

Capex Sharing HPC

To be developed as Industry CUF at Chitradurga.Land identified. Application to be submitted to

KIADB for acquisition.

15

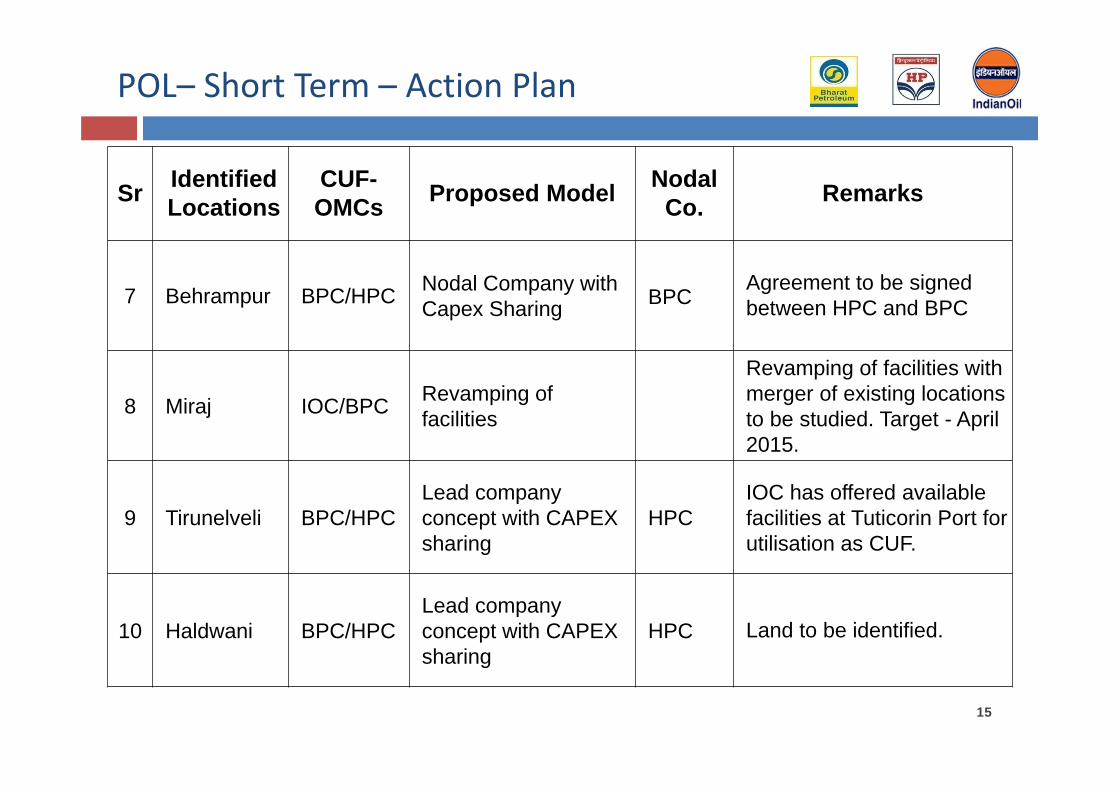

POL– Short Term – Action Plan

Sr Identified Locations

CUF-OMCs Proposed Model Nodal

Co. Remarks

7 Behrampur BPC/HPC Nodal Company with Capex Sharing BPC

Agreement to be signed between HPC and BPC

8 Miraj IOC/BPC Revamping of facilities

Revamping of facilities with merger of existing locations to be studied. Target - April2015.

9 Tirunelveli BPC/HPCLead company concept with CAPEX sharing

HPCIOC has offered available facilities at Tuticorin Port for utilisation as CUF.

10 Haldwani BPC/HPCLead company concept with CAPEX sharing

HPC Land to be identified.

16

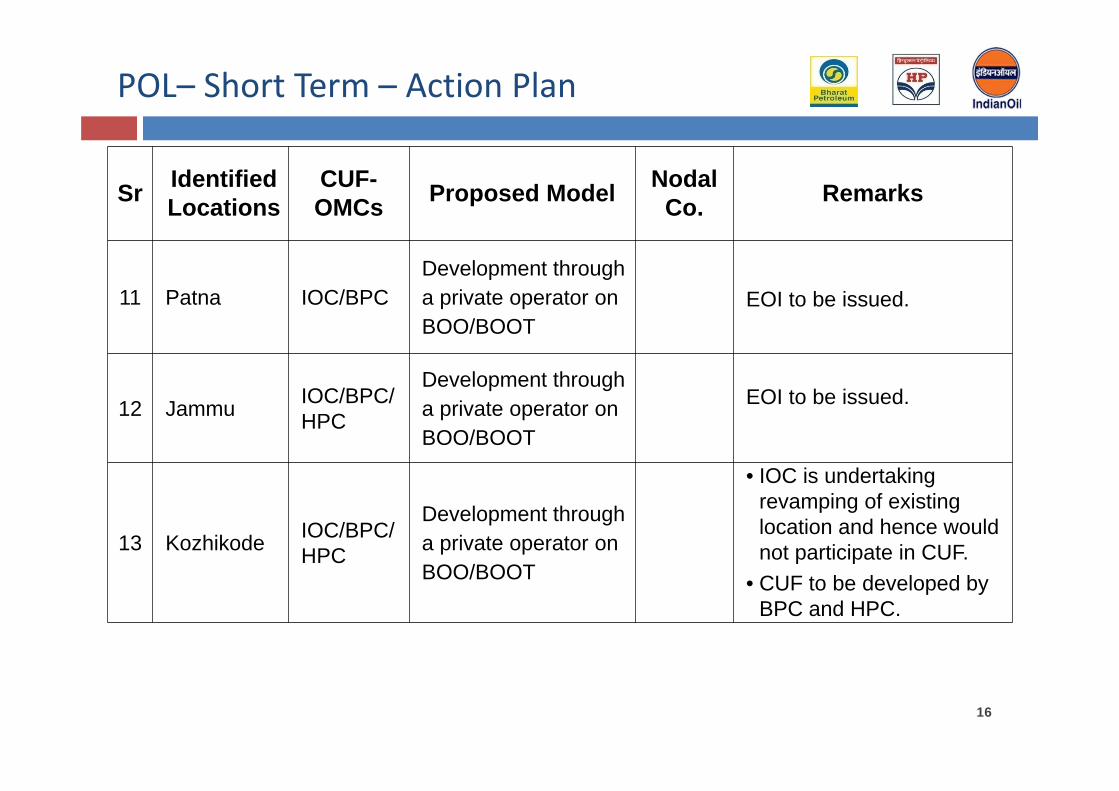

POL– Short Term – Action Plan

Sr Identified Locations

CUF-OMCs Proposed Model Nodal

Co. Remarks

11 Patna IOC/BPCDevelopment through a private operator on BOO/BOOT

EOI to be issued.

12 Jammu IOC/BPC/HPC

Development through a private operator on BOO/BOOT

EOI to be issued.

13 Kozhikode IOC/BPC/HPC

Development through a private operator on BOO/BOOT

• IOC is undertaking revamping of existing location and hence would not participate in CUF.

• CUF to be developed by BPC and HPC.

17

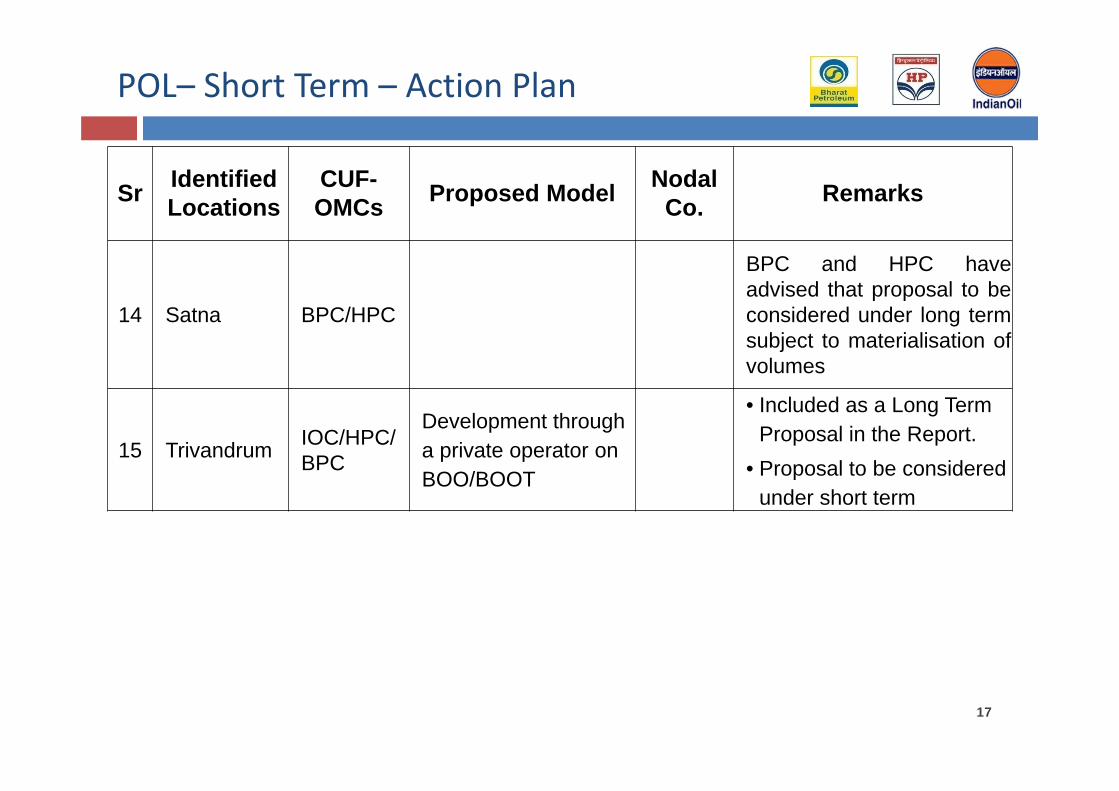

POL– Short Term – Action Plan

Sr Identified Locations

CUF-OMCs Proposed Model Nodal

Co. Remarks

14 Satna BPC/HPC

BPC and HPC haveadvised that proposal to beconsidered under long termsubject to materialisation ofvolumes

15 Trivandrum IOC/HPC/BPC

Development through a private operator on BOO/BOOT

• Included as a Long Term Proposal in the Report.

• Proposal to be considered under short term

18

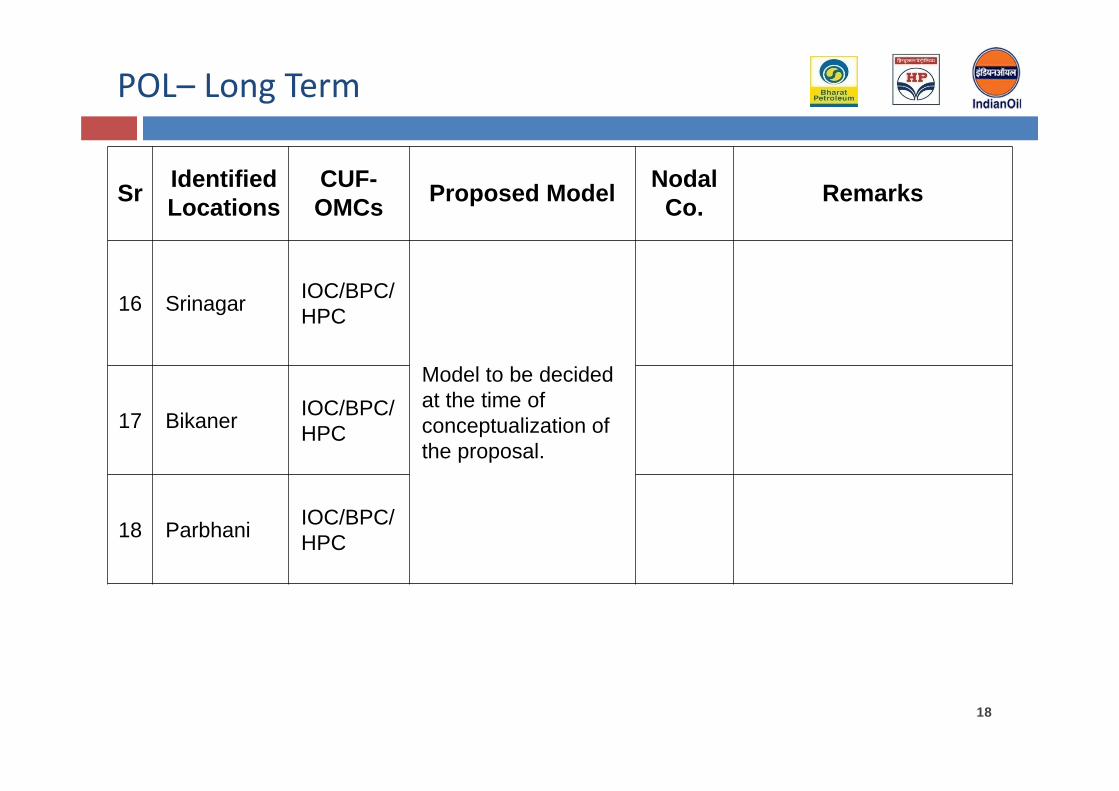

POL– Long Term

Sr Identified Locations

CUF-OMCs Proposed Model Nodal

Co. Remarks

16 Srinagar IOC/BPC/HPC

Model to be decided at the time of conceptualization of the proposal.

17 Bikaner IOC/BPC/HPC

18 Parbhani IOC/BPC/HPC

19

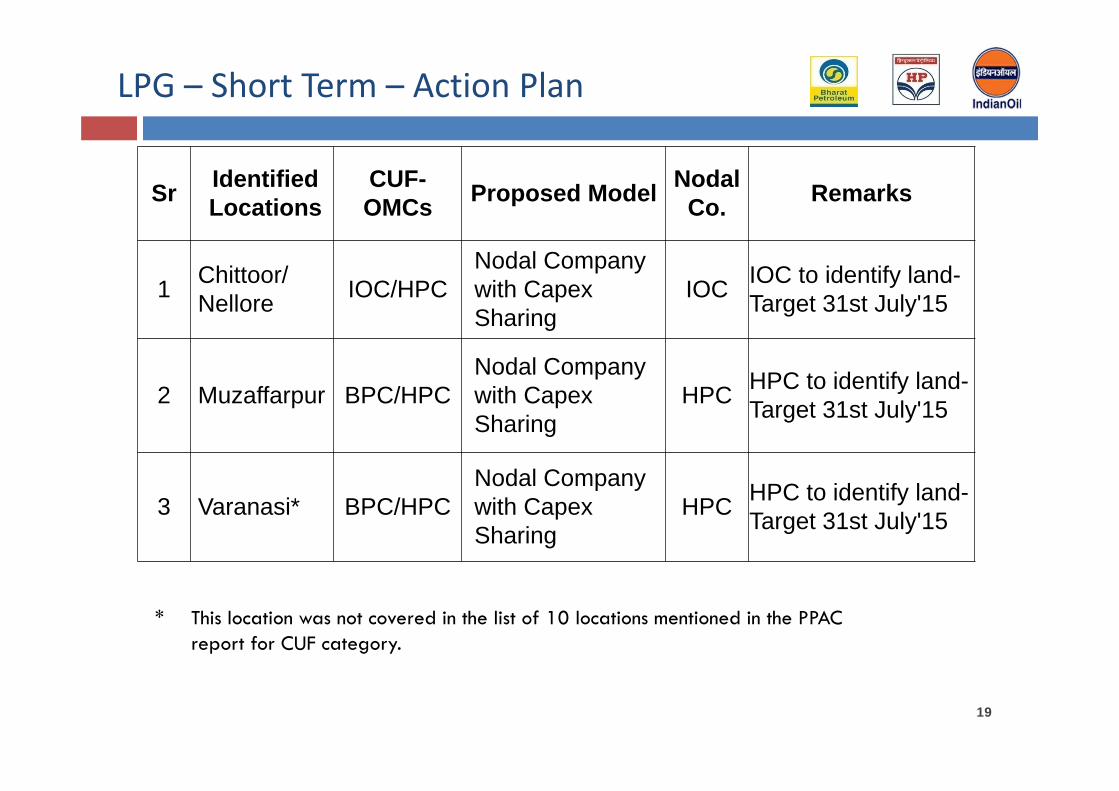

LPG – Short Term – Action Plan

Sr Identified Locations

CUF-OMCs Proposed Model Nodal

Co. Remarks

1 Chittoor/ Nellore IOC/HPC

Nodal Company with CapexSharing

IOC IOC to identify land-Target 31st July'15

2 Muzaffarpur BPC/HPCNodal Company with CapexSharing

HPC HPC to identify land-Target 31st July'15

3 Varanasi* BPC/HPCNodal Company with CapexSharing

HPC HPC to identify land-Target 31st July'15

* This location was not covered in the list of 10 locations mentioned in the PPAC report for CUF category.

20

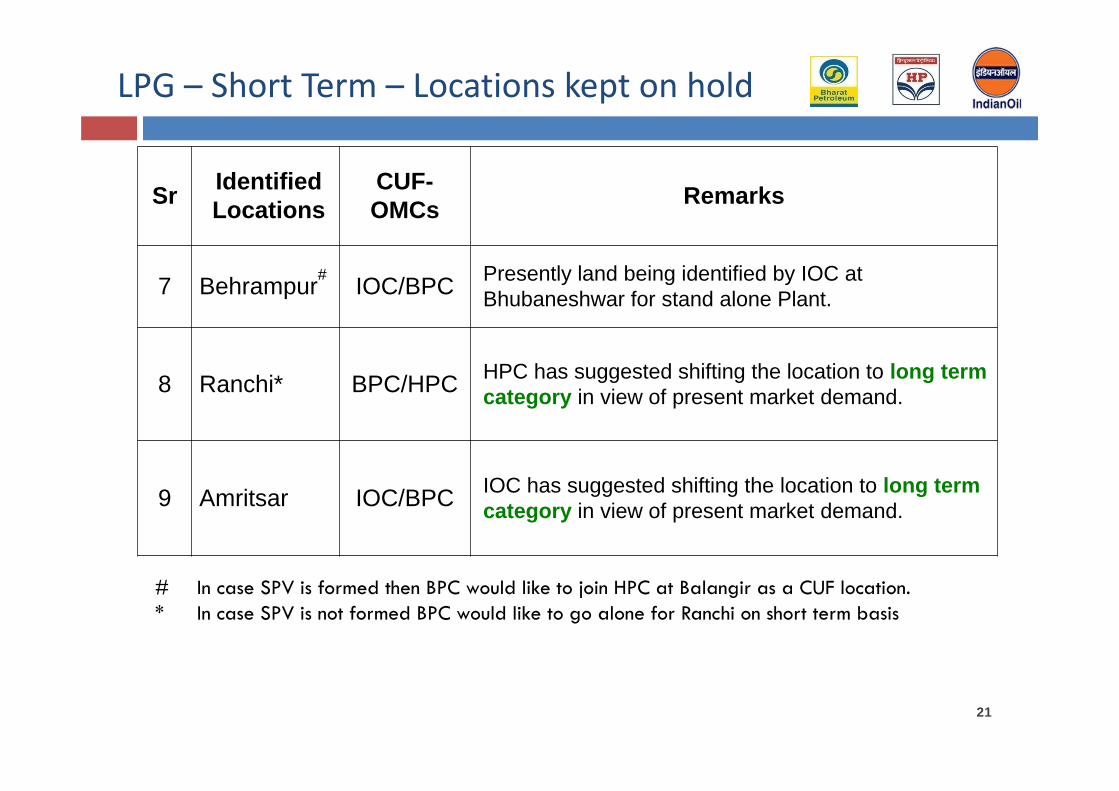

LPG – Short Term – Locations kept on hold

Sr Identified Locations

CUF-OMCs Remarks

4 Udaipur/ Jodhpur IOC/HPC

Existing HPC LPG plant at Jodhpur was to be resited. Hence a CUF location was proposed.Due to non-availability of suitable land, it is now proposed to explore possibility of re-construction of the existing plant at Jodhpur in the same location, meeting OISD 144 standards.

5 Salem HPC/BPCHPC/BPC have expressed interest in sharing of existing/ proposed IOC Plant. New CUF for HPC/BPC to be considered if the above does not materialise.

6 Roorkee IOC/HPCIOC/HPC have expressed interest in sharing of existing/ proposed BPC infrastructure. New CUF for HPC/IOC to be considered if the above does not materialise.

21

LPG – Short Term – Locations kept on hold

Sr Identified Locations

CUF-OMCs Remarks

7 Behrampur# IOC/BPC Presently land being identified by IOC at Bhubaneshwar for stand alone Plant.

8 Ranchi* BPC/HPC HPC has suggested shifting the location to long term category in view of present market demand.

9 Amritsar IOC/BPC IOC has suggested shifting the location to long term category in view of present market demand.

# In case SPV is formed then BPC would like to join HPC at Balangir as a CUF location.* In case SPV is not formed BPC would like to go alone for Ranchi on short term basis

22

LPG – LongTerm

Sr Identified Locations

CUF-OMCs

1 Kota BPC/HPC

2 Siliguri BPC/HPC

23

MoS (I/c), MoPNG during review of Odisha State on 05.09.2014advised“IOC/BPC/HPC jointly to explore for putting up a POL depot (withRail/PPL link) at Meramundli (between Angul and Dhenkanel) whichwill emerge as one of biggest Industrial hub in near future. About100 acre land available near old bus stand –

Distances Jatni - Meramandalli : 112 Km Cuttack – Meramandalli : 85 Km Paradip – Meramandalli : 177 kms

Meramandalli market being fed ex Cuttack, Jatni and Paradip. Considering the short distance, there are minimal savings in secondary

transportation cost even considering positioning of product by Pipeline. Projected Volumes at Meramandalli – 380 TKL with reduction in volumes

at existing locations at Jatni, Cuttack, Paradip and Under ConstructionLocations at Jharsuguda (IOC) and Sambalpur(BPC/HPC)

New Depot at Meramandalli

24

New Depot at Meramandalli

Meramandalli

25

Issue : Requirement of development of CUF at Meramandalli

New Depot at Meramandalli

26

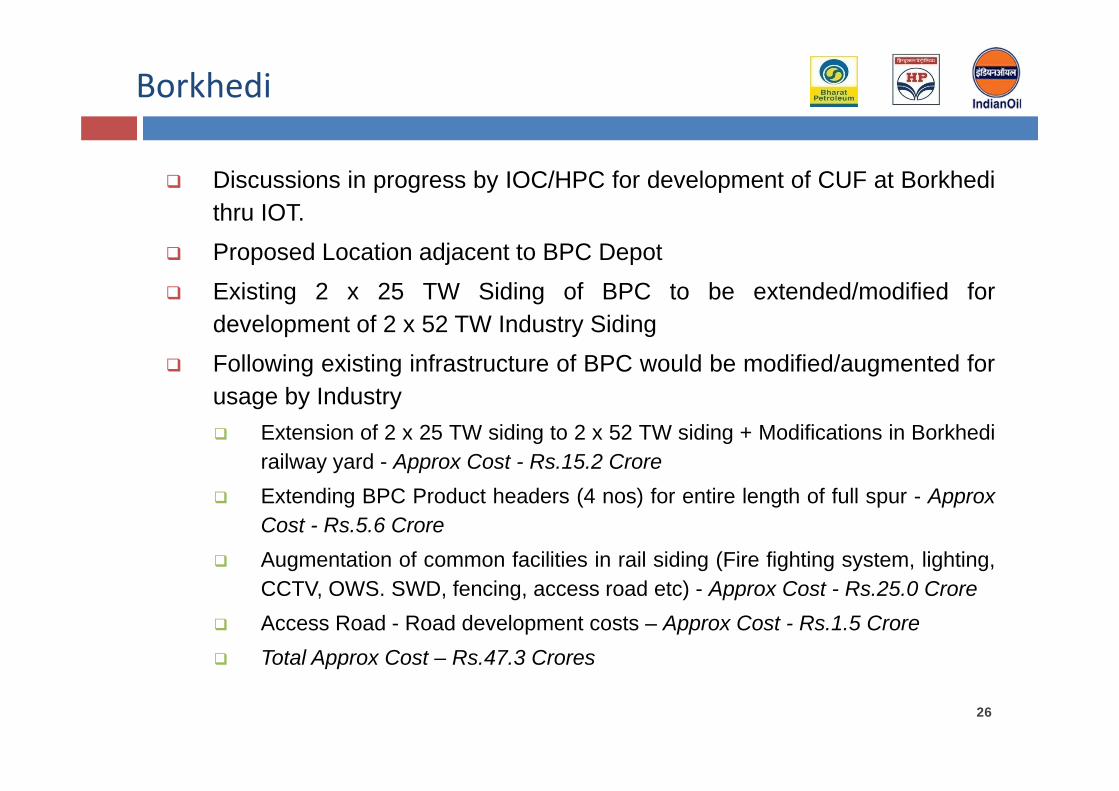

Discussions in progress by IOC/HPC for development of CUF at Borkhedithru IOT.

Proposed Location adjacent to BPC Depot Existing 2 x 25 TW Siding of BPC to be extended/modified for

development of 2 x 52 TW Industry Siding Following existing infrastructure of BPC would be modified/augmented for

usage by Industry Extension of 2 x 25 TW siding to 2 x 52 TW siding + Modifications in Borkhedi

railway yard - Approx Cost - Rs.15.2 Crore Extending BPC Product headers (4 nos) for entire length of full spur - Approx

Cost - Rs.5.6 Crore Augmentation of common facilities in rail siding (Fire fighting system, lighting,

CCTV, OWS. SWD, fencing, access road etc) - Approx Cost - Rs.25.0 Crore Access Road - Road development costs – Approx Cost - Rs.1.5 Crore Total Approx Cost – Rs.47.3 Crores

Borkhedi

27

Permission from BPC for sharing of siding and approaching Railway forextension of siding.

Permission from BPC for undertaking the activities and cost sharingmechanism.

Borkhedi - Issues

28

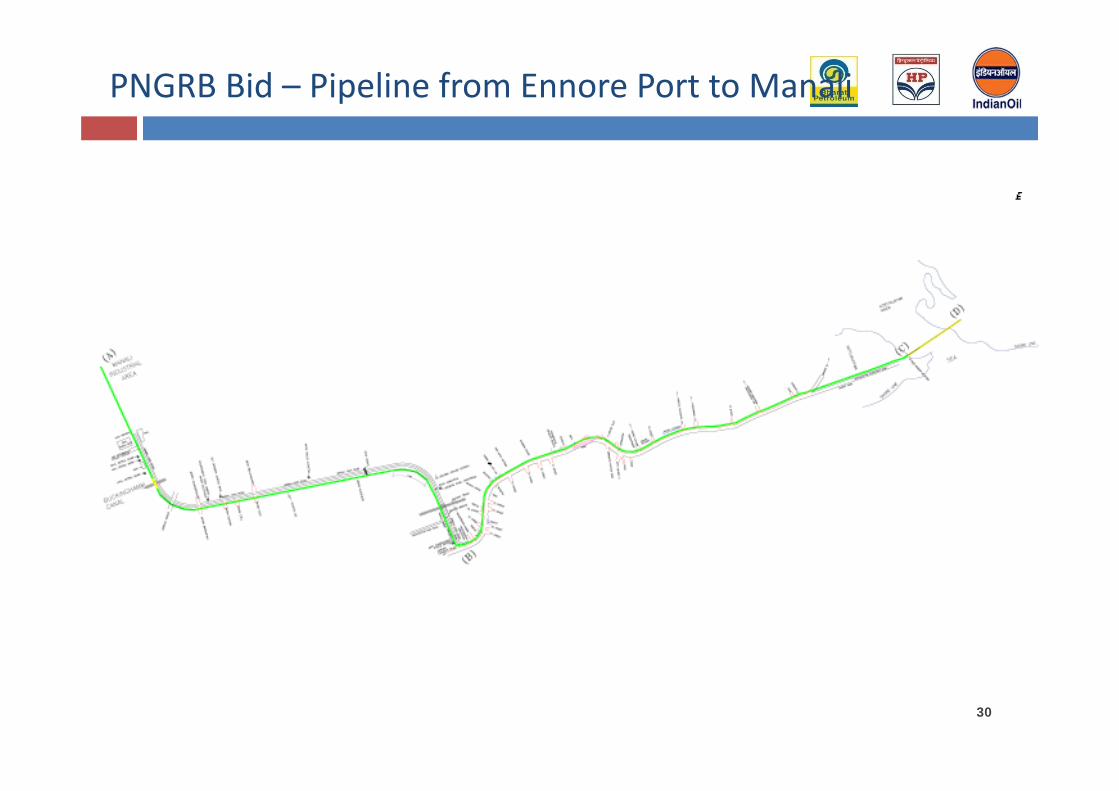

PNGRB has invited bids for laying of 14 kms petroleum product pipelinefrom Ennore Port to Manali Industrial area

Petroleum Products to be transported : At least two grades of MS/HSD(EURO-III, EURO-IV and any other higher quality grade that may bespecified or mandated to be supplied in future), Naptha, Furnace Oil,Vacuum Gas Oil (VGO) and any other petroleum. SAMPLE

Route of the Pipeline (tentative): Ennore Port (Chennai, Tamil Nadu) -Manali Industrial Area (Chennai, Tamil Nadu).

System Capacity: At least 1.0 MMTPA (including common carrier capacityavailable for any third party on open access and non-discriminatory basis.

Approx Volumes White Oil – 0.5 MMTPA Black Oil – 0.5 MMTPA

Pre Bid Meeting : 18.05.2015 Bid Closing Date : 27.07.2015

PNGRB Bid – Pipeline from Ennore Port to Manali

29

Industry Meeting held – 17.04.2015 The proposed pipeline will be useful to Industry if –

Originating point can be accessed directly by IOCL, HPCL, BPCL at theirrespective manifolds in Ennore Port without necessarily having to go throughETTPL Terminal or manifold

Bi-directional pumping is allowed. Ennore to CPCL and CPCL to Ennore asand when required.

In this bid PNGRB permits us to use the route considered by IOC for Pipelineproposed to be laid by IOCL connecting CPCL refinery and Ennore Industryterminals

No limitations on Entry and Exit pressures as specified in 17.4.2

PNGRB Bid – Pipeline from Ennore Port to Manali

30

PNGRB Bid – Pipeline from Ennore Port to Manali

31

PNGRB Bid – Pipeline from Ennore Port to Manali

PNGRB Bid Pipeline

Proposed Common Corridor Pipeline

32

Whether to Bid? Whether to Bid on single company basis or as a Consortium Route to be followed

PNGRB Bid – Issues

33

THANK YOU