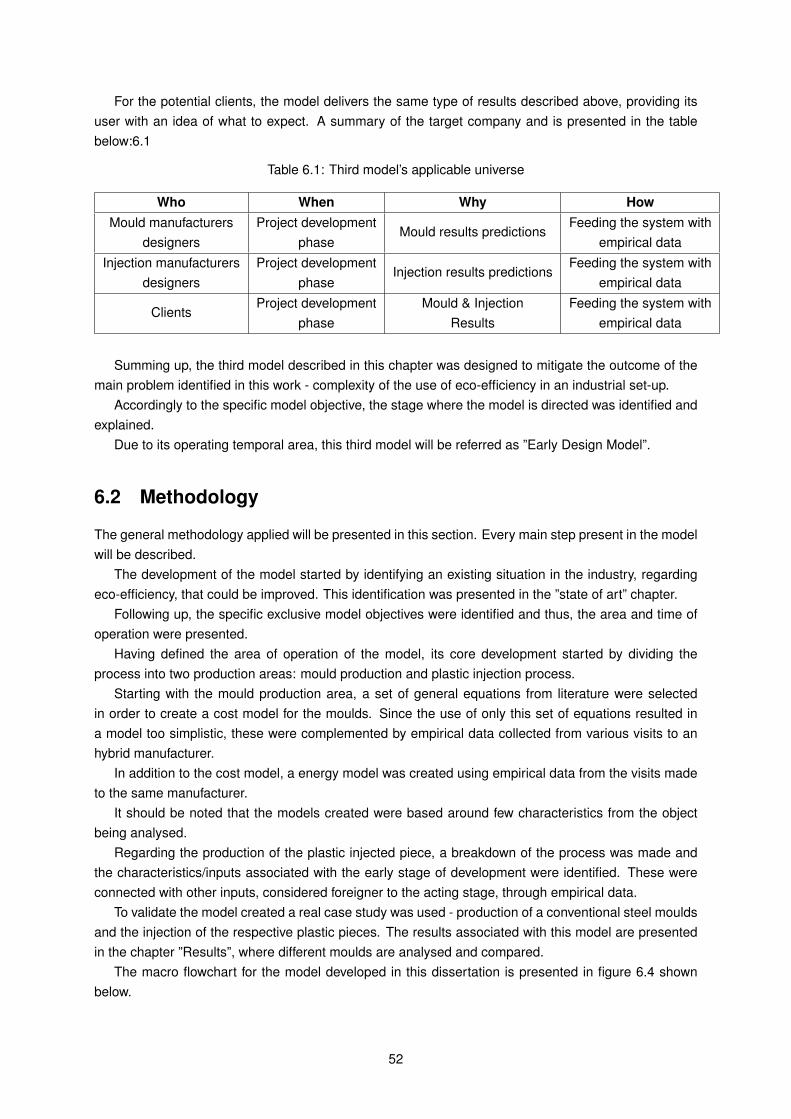

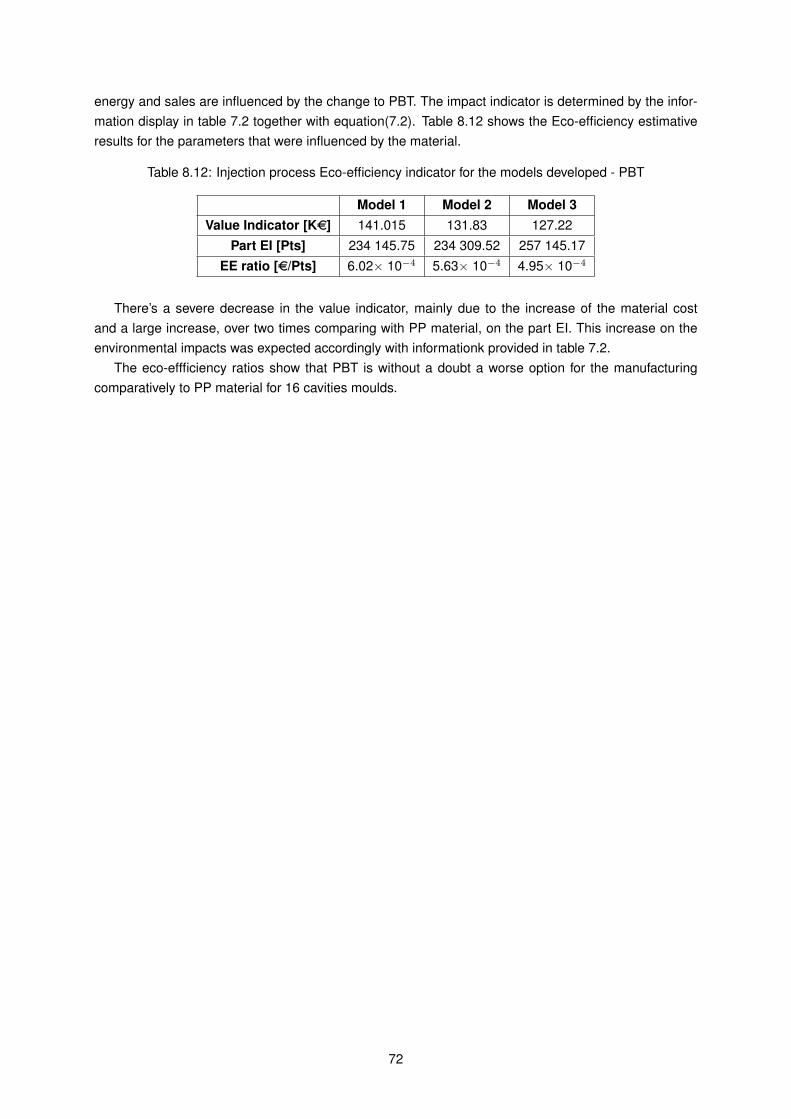

Development of models for operationalisation of eco-efficiency indicators: Application to mould design and plastic injection processes Rafael Nuno Coutinho Ferreira Thesis to obtain the Master of Science Degree in Mechanical Engineering Supervisors: Prof. Paulo Miguel Nogueira Pec ¸as Prof. Inˆ es Esteves Ribeiro Examination Committee Chairperson: Prof. Rui Manuel dos Santos Oliveira Baptista Supervisor: Prof. Paulo Miguel Nogueira Pec ¸as Members of the Committee: Prof. Elsa Maria Pires Henriques Eng. Eduardo Jo ˜ ao de Almeida e Silva June 2017

Transcript

Development of models for operationalisation ofeco-efficiency indicators: Application to mould design

and plastic injection processes

Rafael Nuno Coutinho Ferreira

Thesis to obtain the Master of Science Degree in

Mechanical Engineering

Supervisors: Prof. Paulo Miguel Nogueira PecasProf. Ines Esteves Ribeiro

Examination Committee

Chairperson: Prof. Rui Manuel dos Santos Oliveira Baptista

Supervisor: Prof. Paulo Miguel Nogueira Pecas

Members of the Committee: Prof. Elsa Maria Pires HenriquesEng. Eduardo Joao de Almeida e Silva

June 2017

Acknowledgments

There are a number of people without whom this dissertation might not have been completed and towhom i am immeasurably indebted.

To my parents and brother, who have been a continuous source of assistance and inspiration to methrough the time of writing. And also for the countless ways in which they have supported me in findingstrength to complete this work.

To my grandparents, who represent to me the proof of our ability to redefine our lives through deter-mination.

I am also very grateful to Prof. Paulo Pecas and Prof. Ines Ribeiro, for providing me the necessaryguidance, patience and support during this campaign.

Also, to Ana, Goncalo, Joao, Miguel, Diogo, Ze and Maria for their camaraderie during the lastmonths.

I would also like to thank R. Ursılio, C. Salvador, T. Pinto, D. Rato, F.Rei e P.Fernandes for theirfriendship for so many years.

i

Resumo

Com a crescente preocupacao ambiental por parte da sociedade, a importancia da implementacao defilosofias ambientais nas empresas e inegavel. A eco-eficiencia, faz a ponte entre economia e ambienterelacionando, atraves de racios de eco-eficiencia, o valor do produto/servico com o impacte ambiental,tentando maximizar o valor do produto e minimizar o impacto ambiental associado.

A presente dissertacao tem o objectivo de tornar o uso da filosofia da eco-eficiencia operacionalatraves do desenvolvimento de modelos simplificados para o calculo de indicadores de eco-eficiencia,esperando-se que a existencia de modelos simplificados, contribua para o uso mais generalizado daeco-eficiencia no mundo empresarial.

Para que o trabalho tivesse uma maior abrangencia, foram identificados tres cenarios diferentesdentro do processo productivo das empresas de moldes e injeccao de plastico e para cada uma delasum modelo simplificado de previsao economica, ambiental e eco-eficiencia foi desenvolvido.

Os resultados dos modelos sao apresentados de um modo comparativo entre os tres modelos de-senvolvidos e exibem analises para diferentes tipos de materiais plasticos, e para diferentes cavidades.Os resultados sao apresentados sobre a forma de tabelas e graficos.

A analise realizada sobre os resultados permitiu retirar conclusoes sobre a capacidade dos modelosactuarem com precisao na industria e sobre semelhancas e diferencas entre eles.

Following society’s growing awareness about environmental aspects, the importance of implementingenvironmental philosophies within companies is undeniable. Eco-efficiency serves as a bridge betweeneconomy and environment relating, through eco-efficiency ratios, the value of the product/service withits environmental impact, trying to maximise product value and minimise the associated environmentalimpact.

The present dissertation has as goal of making eco-efficiency philosophy operational through thedevelopment of simplified models for the calculation of indicators of eco-efficiency, hoping that the ex-istence of simplified models contributes for a more generalise use of eco-efficiency within corporatesphere.

With the intent of making this work’s area of action broader, three different scenarios within theproduction process of mould and plastic injection companies were identified and for each one of them asimplified model that estimates economic, environmental and eco-efficiency results was developed.

The results are presented in the form of comparison between the three models developed and offeranalysis for different types of plastic materials, and for a different number of cavities.

The analysis performed over the results allowed to reach some conclusions about the capacity ofmodels to act with precision in the industry and about similarities and differences between them.

ISO International Organization for Standardization

IST Instituto Superior Tecnico

MRR Material removal rate

OECD Organization for economic Co-operation and Development

WBCSD World Business Council for Sustainable Development

xix

Chapter 1

Introduction

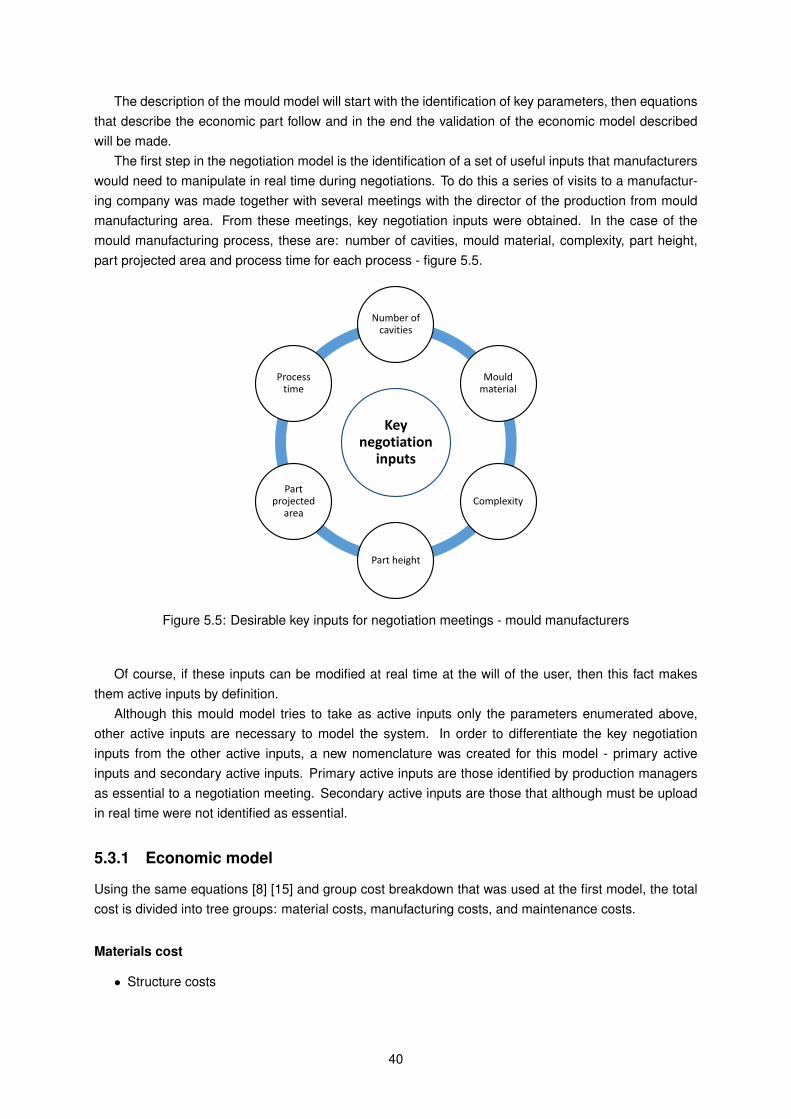

In recent years the level of awareness about natural environmental protection has picked up momentum.This increase in awareness is reflected in both governments and ordinary people, who demand stricterregulations that reflect the importance of environmental performance in diverse areas of society. In thecase of costumers, this is echoed within companies who turn to more environmentally-friendly products.

To follow the emergence of this new environmental aspect, and following the pragmatism that char-acterises the industrial sector, a rather new management philosophy that combined economic growthand environmental protection start being used - Eco-efficiency (EE). Eco-efficiency is a method thatinstigates the search for environmental improvements that yield economic benefits alongside [4].

Manufacturing sector contributes significantly to the damage of the environment, they are indeed thekey player in the management of resources in modern society, and as such ought to take responsibilityfor their preservation. This responsibility can take form in the insertion of environment aspect at decisiontime, namely in the choice of processes employed by manufacturers and also at product design. Thesedecisions control not only the impacts of manufacturing products but also the impact these have on theirlife cycle [12].

The situation described was the drive of studies whose goal was directed towards an improvementof the environmental characteristics within the manufacturing industrial sector, thus cracking the factorsthat largely influence it.

The present work aims to assist in decision-making processes regarding Eco-efficiency’s improve-ment.

1.1 Motivation

Although practical measures are necessary to introduce Eco-efficiency within policies of organisationsand companies, the environmental and economic scope affected objectivity and led to different inter-pretations. Thus the necessity of developing general metrics to enable decision makers to base theirdecisions was paramount [13].

The World Business Council for Sustainable Development (WBCSD) suggested an appropriate plat-form or assessment method which agrees with the original definition of Eco-efficiency: create more valuewith fewer impacts [14].By following WBCSD guidelines, Eco-efficiency can be achieved by consideringa set of Eco-efficiency indicators meticulously chosen, that can be analysed by using different designconfigurations.

This work of interpreting eco-efficiency results to select the best design configuration for a certainobjective has been a subject of previous studies within Instituto Superior Tecnico (IST) work groups,

1

often targeting the design phase of mould and injection industries [8], [15], [16].One thing common to these works is the fact that the characterization of the industrial systems,

needed in the use of eco-efficiency, is complex and high time-consuming. Thus a question arises: ’Isthis complexity, reflected into high characterization times, an obstacle to a more generalized use of eco-efficiency within industries?’. This work offers a possible solution to those entities that answer positivelyto the previous question. It is assumed that this complexity is an important drawback to the generalizeduse of eco-efficiency in an industrial scenario and, therefore, finding a way to operationalise EE, i.e. turnthe formulation of EE and its indicators simple enough to be used commonly, would be tremendouslyuseful to either companies or any other entity that works at macro level.

To sum up, the proposed work has one major target within the manufacturing industries: operational-isation of eco-efficiency models, i.e. development of simplified models that target a specific scenariowithin the industry. Practical models, whose regular use is not as time-consuming as the existing mod-els.

1.2 Contributions

In the studies aforementioned about determining EE within mould manufacturing and injection mouldingindustries, the strategy to calculate it was standard - first, the model of the entire system was constructedand then, different eco-efficiency indicators were analysed considering distinct design parameters. Thedesign combinations that originated the highest indicators ratios were chosen as the most suitable forthe manufacturing, [8], [15]. The construction of the model phase is high time-consuming and it is thischaracteristic that this work tries to improve.

So the main contributions of this work comprehend:

• Development of simplified models, representing different scenarios within the mould and injectionindustries, that mitigate the high characterization times needed when using EE in a regular way.

• Developed models are able to support mould design and injection moulding process alternativesselection through the understanding of the influence of design and process alternatives in eco-efficiency.

It’s understandable that there must be a trade-off between model simplification and accuracy. Othercontribution can be seen a better understanding of how the level of simplification influences the accuracyof a model.

1.3 Overview

A brief description of the developed work follows. Firstly, some research was made to gather informationabout the mould manufacturing and injection moulding industry fields. After recognising some drawbacksin Eco-efficiency’s assessment, simplified models were developed to counter those drawbacks. Alongwith their application, follows the results and conclusions.

• Chapter 1 - Introduction. The introductory chapter offers a view over the need of manufacturingindustries combining their economic goal with environmental improvements, in the form of a newmanagement philosophy – Eco-efficiency. It includes the motivation and this work contributions.

• Chapter 2 - State of the Art. In this chapter is explained what eco-efficiency is, several definitionsare shown and a comparison between them are made. Eco-efficiency indicators are highlightedand previous simplified works are mentioned.

2

A brief overview on mould manufacturing and injection processes is made.

• Chapter 3 - Operationalization of Eco-efficiency models. This chapter presents the basesneeded for understanding the three models developed. Several concepts are defined and ex-plained, including types of inputs and exclusive model objectives.

• Chapter 4 - Operationalization model: Process selection model. In this chapter the first sim-plified model developed is presented. Starting by its context, followed by model itself and finally itsvalidation.

• Chapter 5 - Operationalization model: Negotiation phase. In this chapter the second simplifiedmodel is presented. Starting by its context, followed by model itself and finally its validation.

• Chapter 6 - Operationalization model: Early design. In this chapter the third simplified modelis presented. Starting by its context, followed by model itself and finally its validation.

• Chapter 7 - Environmental models. In this chapter the environmental part of the three models arepresented. This includes equations that describe the model together with simplifications proposed.

• Chapter 8 - Results. In this chapter individual results of each model are compared with one an-other. A assessment about if simplification was achieved is made together with its cost to accuracy.An analysis of the influence of few design aspects have over results is made.

• Chapter 9 - Conclusions and Future work. A final statement is made regarding the develop-ment of the proposed models and their results and some suggestions about this work’s futuredevelopments are offered.

3

4

Chapter 2

State of the Art

2.1 Eco-efficiency

2.1.1 Philosophy and principles behind eco-efficiency

Since the beginning of the industrial era, the corporate sphere has had an immense impact on theenvironment. In the 20th century, environmental movements started pointing out that there were en-vironmental costs associated with the manufacturing industries and in the at the end of the century,environmental problems became global in scale. An increasing global awareness of the threat posed byignoring environmental impacts gave birth to a new paradigm, which brought to centre stage the pursuitof a common ideal. In the industrial field, this new paradigm brought the appearance of a new philoso-phy where not only economic indicators were used to assess a business model but also environmentalindicators.

The first notion of eco-efficiency can be traced back to AM Freeman III and RH Haveman in the 70sas the concept of “environmental efficiency” [17].

In the 1990s, Schaltegger and Sturm [18] introduced eco-efficiency as a “business link to sus-tainable development”. In 1992, the concept of eco-efficiency was widely popularised in ChangingCourse (Schmidheiny 1992), a publication of the World Business Council for Sustainable Development(WBCSD) [19].

Since then, eco-efficiency has been accepted as a philosophy that intends to help businesses under-stand how the search for environmental improvements can yield economic benefits, thus showing howachieving both environmental and business goals can be compatible.

Being a relatively new concept, a standard definition of eco-efficiency does not exist, but several def-initions were proposed (see table 2.1) and although there are some differences between the definitionsshown, it’s possible to draw some similarities, they all address the need of creating more value and lessimpact. Thus, eco-efficiency can be seen as a broader manifestation of the concept of resource effi-ciency – minimising the resources used in the production of a unit of output – and resource productivity– the efficiency of economic actions in creating added value for the use of resources.

5

Table 2.1: Several definitions of eco-efficiency.[1][2][3]

Entity responsible for the definition EE definitionOrganisation for Economic Cooperation and Development (OECD) ”the efficiency with which ecological resources are used to meet human needs”

ISO/DIS 14045”quantitative management tool that enables the consideration of life cycleenvironmental impacts of a product system alongside its product system valueto a stakeholder”

European Environment Agency (EEA)

”A concept and strategy enabling sufficient delinking of the ‘use of nature’from economic activity needed to meet human needs (welfare) to allow itto remain within carrying capacities, and to permit equitable access anduse of the environment by current and future generations”

From the various definitions that appeared the one provided by WBCSD is often referred in worksrelated to eco-efficiency, and it will be the one used in this work also. According to WBCSD, “eco-efficiency is achieved by the delivery of competitively-priced goods and services that satisfy humanneeds and bring quality of life, while progressively reducing ecological impacts and resource intensitythroughout the life-cycle, to a level at least in line with the Earth’s estimated carrying capacity” [20].Eco-efficiency can be calculated using equation 2.1 [21].

(2.1)Eco− efficiency =Production or service value

Environmental Influence

In the business sphere, WBCSD affirms that to become more eco-efficient, a company should focuson well-known methods and strategies and as such, to help companies achieve a better eco-efficiency,proposed seven elements which may lead to improved eco-efficiency in business [20], [21], [5]. Theseseven principles are presented in table 2.2 where they were grouped accordingly with their function.

Table 2.2: Seven principles of eco-efficiency as stated by WBCSD.[4]

Function of the principle Eco-efficiency principle

Resource optimizationReduce material requirements

Reduce energy intensityReduce toxic dispersion

Increase of valueEnhance material recyclability

Maximize use of renewable resources

Reduction of environmental impactsExtend product durabilityIncrease service intensity

Even though the seven principles show in table 2.2 were proposed by WBCSD, they can be insertedin any of the definitions presented previously. They work on what is similar between them - the possibilityof obtaining more value using less material and energy inputs with the emissions reduction, and theyshow that eco-efficiency can be an integral part of the strategy that any organisation has [20].

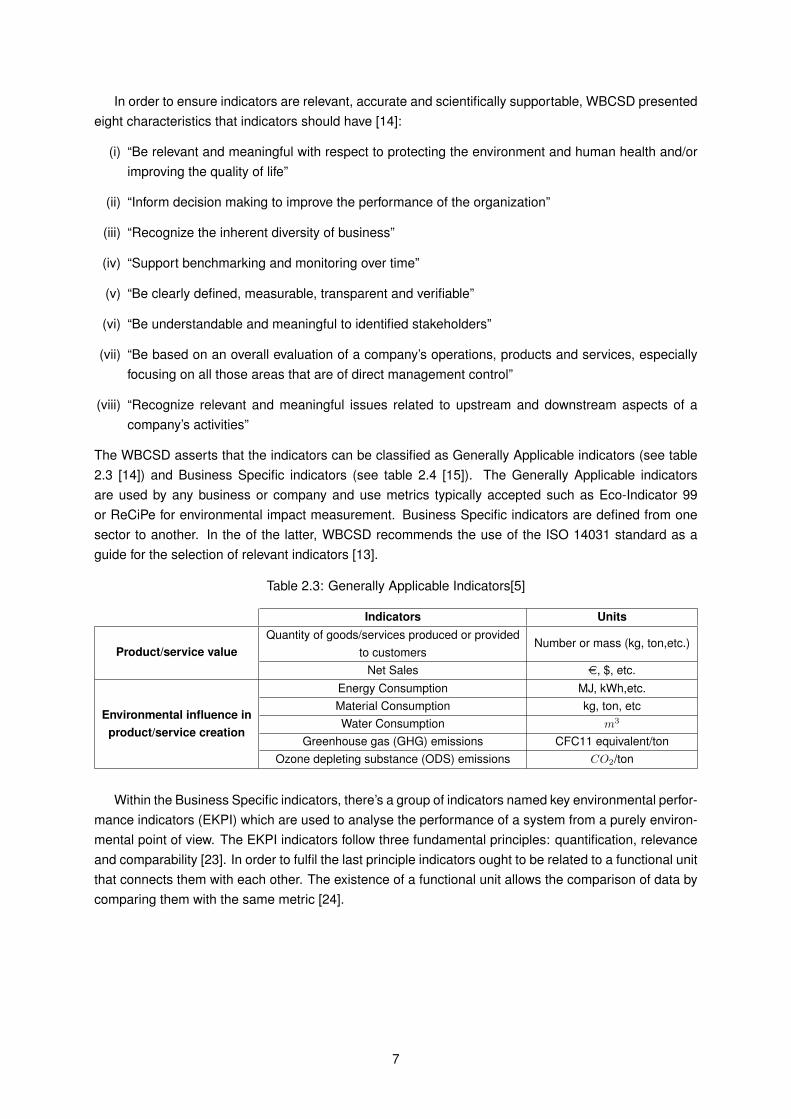

2.1.2 Eco-efficiency indicators

Taking into consideration the vast number of definitions for eco-efficiency and the fact that they sharethe same core ideas, we can affirm that eco-efficiency concept is well-established. Nonetheless, lookingat the equation that quantifies eco-efficiency we notice that the concepts of value and environmental aregeneric and vague, leading to the possibility of different interpretations. Thus the necessity of havingappropriate metrics that allow a better orientation is essential [22].

The necessity of quantifying eco-efficiency in order to gather quantitative and qualitative informationfor making decisions gave birth to EE indicators. Indicators are defined as parameter or reference for aparameter and serve the purpose of assessing the progress of a company [13].

6

In order to ensure indicators are relevant, accurate and scientifically supportable, WBCSD presentedeight characteristics that indicators should have [14]:

(i) “Be relevant and meaningful with respect to protecting the environment and human health and/orimproving the quality of life”

(ii) “Inform decision making to improve the performance of the organization”

(iii) “Recognize the inherent diversity of business”

(iv) “Support benchmarking and monitoring over time”

(v) “Be clearly defined, measurable, transparent and verifiable”

(vi) “Be understandable and meaningful to identified stakeholders”

(vii) “Be based on an overall evaluation of a company’s operations, products and services, especiallyfocusing on all those areas that are of direct management control”

(viii) “Recognize relevant and meaningful issues related to upstream and downstream aspects of acompany’s activities”

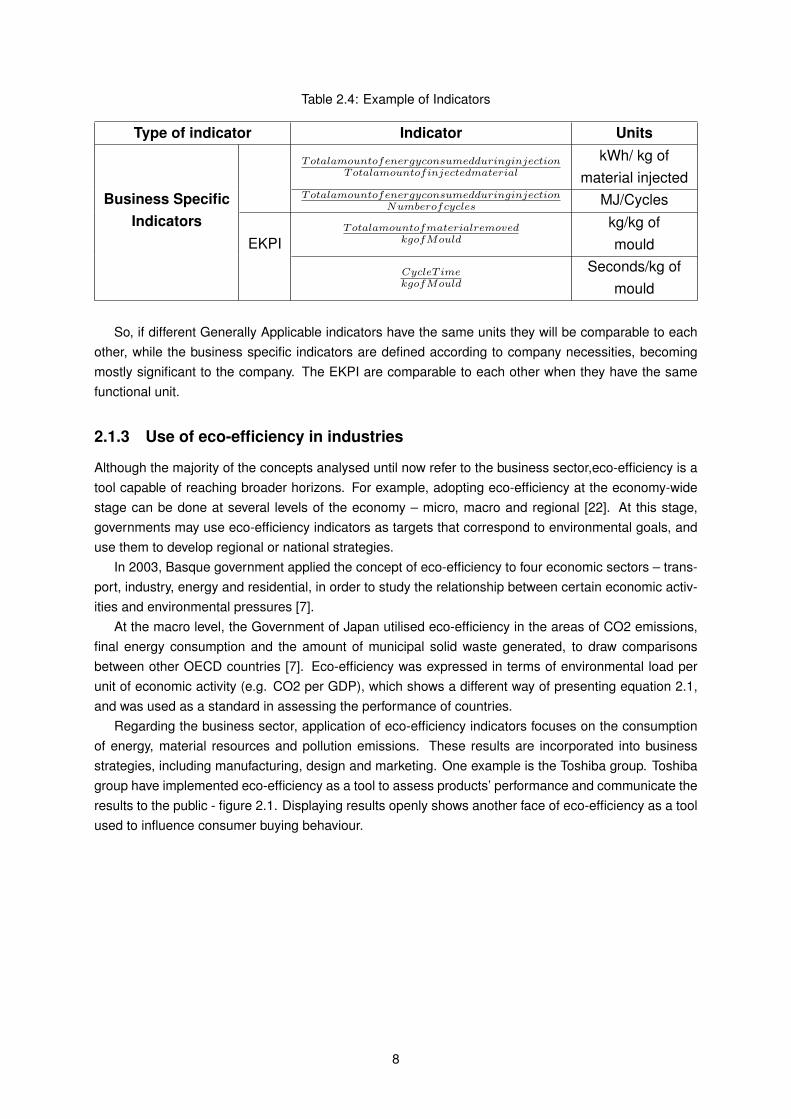

The WBCSD asserts that the indicators can be classified as Generally Applicable indicators (see table2.3 [14]) and Business Specific indicators (see table 2.4 [15]). The Generally Applicable indicatorsare used by any business or company and use metrics typically accepted such as Eco-Indicator 99or ReCiPe for environmental impact measurement. Business Specific indicators are defined from onesector to another. In the of the latter, WBCSD recommends the use of the ISO 14031 standard as aguide for the selection of relevant indicators [13].

Table 2.3: Generally Applicable Indicators[5]

Indicators Units

Product/service valueQuantity of goods/services produced or provided

Within the Business Specific indicators, there’s a group of indicators named key environmental perfor-mance indicators (EKPI) which are used to analyse the performance of a system from a purely environ-mental point of view. The EKPI indicators follow three fundamental principles: quantification, relevanceand comparability [23]. In order to fulfil the last principle indicators ought to be related to a functional unitthat connects them with each other. The existence of a functional unit allows the comparison of data bycomparing them with the same metric [24].

So, if different Generally Applicable indicators have the same units they will be comparable to eachother, while the business specific indicators are defined according to company necessities, becomingmostly significant to the company. The EKPI are comparable to each other when they have the samefunctional unit.

2.1.3 Use of eco-efficiency in industries

Although the majority of the concepts analysed until now refer to the business sector,eco-efficiency is atool capable of reaching broader horizons. For example, adopting eco-efficiency at the economy-widestage can be done at several levels of the economy – micro, macro and regional [22]. At this stage,governments may use eco-efficiency indicators as targets that correspond to environmental goals, anduse them to develop regional or national strategies.

In 2003, Basque government applied the concept of eco-efficiency to four economic sectors – trans-port, industry, energy and residential, in order to study the relationship between certain economic activ-ities and environmental pressures [7].

At the macro level, the Government of Japan utilised eco-efficiency in the areas of CO2 emissions,final energy consumption and the amount of municipal solid waste generated, to draw comparisonsbetween other OECD countries [7]. Eco-efficiency was expressed in terms of environmental load perunit of economic activity (e.g. CO2 per GDP), which shows a different way of presenting equation 2.1,and was used as a standard in assessing the performance of countries.

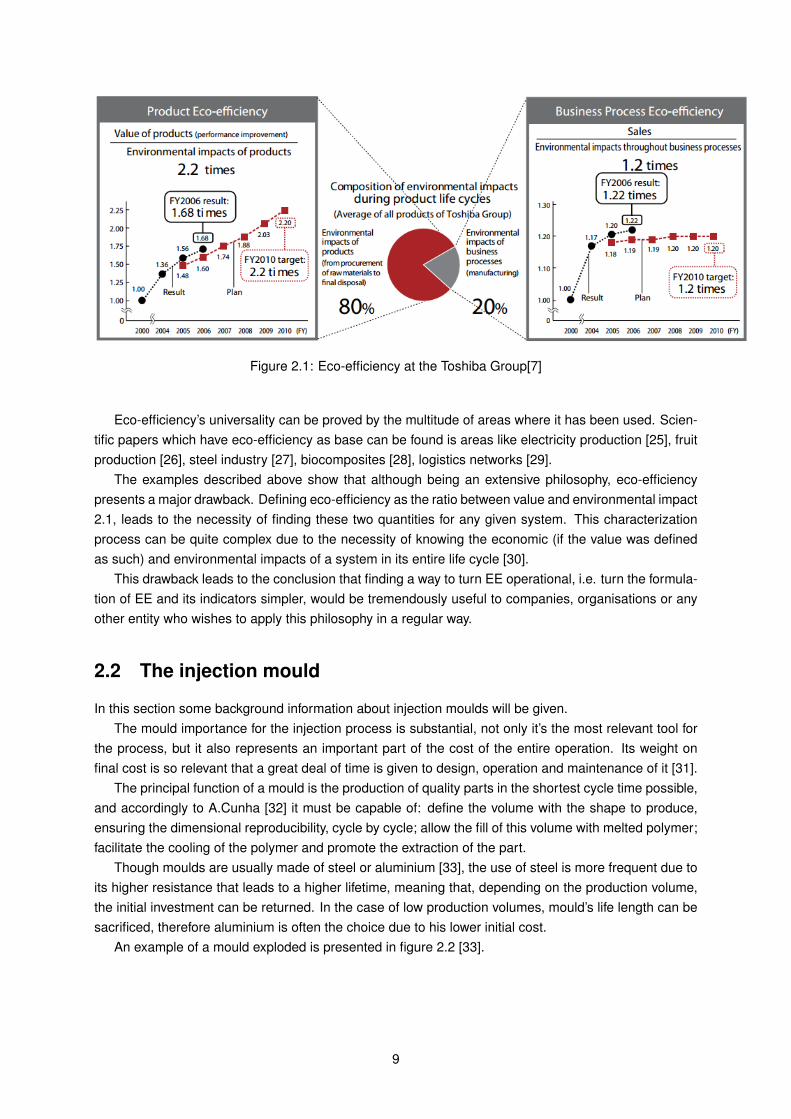

Regarding the business sector, application of eco-efficiency indicators focuses on the consumptionof energy, material resources and pollution emissions. These results are incorporated into businessstrategies, including manufacturing, design and marketing. One example is the Toshiba group. Toshibagroup have implemented eco-efficiency as a tool to assess products’ performance and communicate theresults to the public - figure 2.1. Displaying results openly shows another face of eco-efficiency as a toolused to influence consumer buying behaviour.

8

Figure 2.1: Eco-efficiency at the Toshiba Group[7]

Eco-efficiency’s universality can be proved by the multitude of areas where it has been used. Scien-tific papers which have eco-efficiency as base can be found is areas like electricity production [25], fruitproduction [26], steel industry [27], biocomposites [28], logistics networks [29].

The examples described above show that although being an extensive philosophy, eco-efficiencypresents a major drawback. Defining eco-efficiency as the ratio between value and environmental impact2.1, leads to the necessity of finding these two quantities for any given system. This characterizationprocess can be quite complex due to the necessity of knowing the economic (if the value was definedas such) and environmental impacts of a system in its entire life cycle [30].

This drawback leads to the conclusion that finding a way to turn EE operational, i.e. turn the formula-tion of EE and its indicators simpler, would be tremendously useful to companies, organisations or anyother entity who wishes to apply this philosophy in a regular way.

2.2 The injection mould

In this section some background information about injection moulds will be given.The mould importance for the injection process is substantial, not only it’s the most relevant tool for

the process, but it also represents an important part of the cost of the entire operation. Its weight onfinal cost is so relevant that a great deal of time is given to design, operation and maintenance of it [31].

The principal function of a mould is the production of quality parts in the shortest cycle time possible,and accordingly to A.Cunha [32] it must be capable of: define the volume with the shape to produce,ensuring the dimensional reproducibility, cycle by cycle; allow the fill of this volume with melted polymer;facilitate the cooling of the polymer and promote the extraction of the part.

Though moulds are usually made of steel or aluminium [33], the use of steel is more frequent due toits higher resistance that leads to a higher lifetime, meaning that, depending on the production volume,the initial investment can be returned. In the case of low production volumes, mould’s life length can besacrificed, therefore aluminium is often the choice due to his lower initial cost.

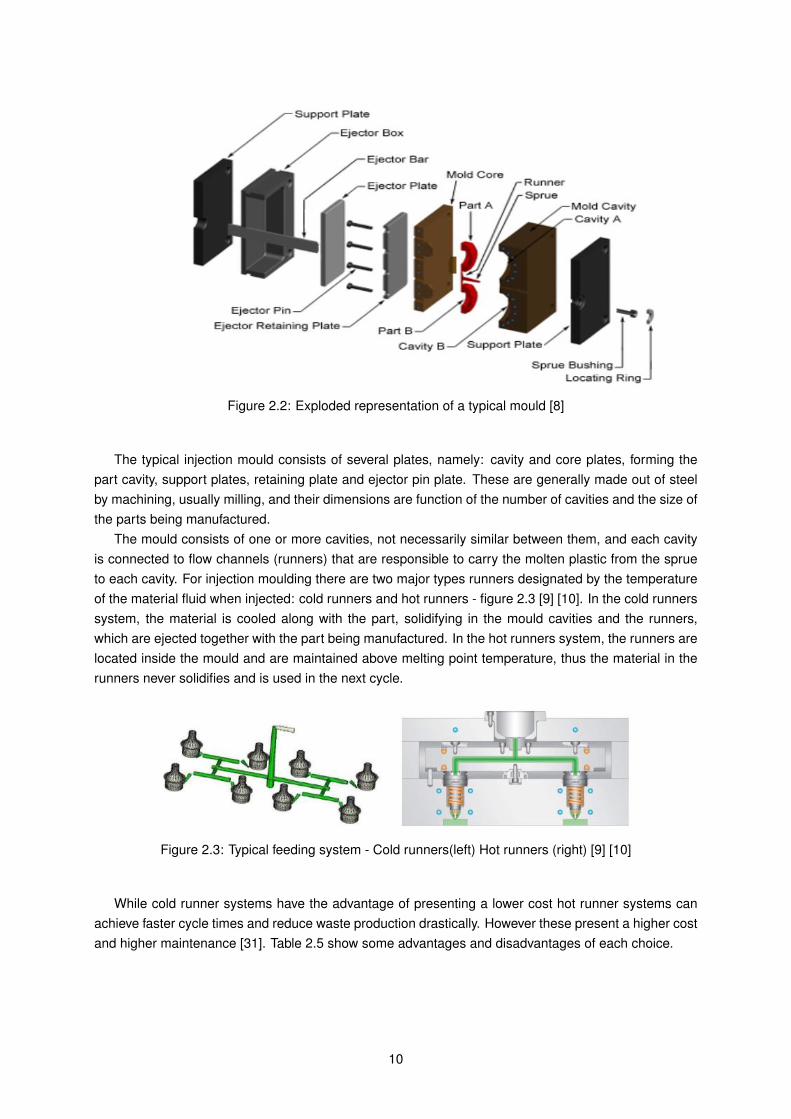

An example of a mould exploded is presented in figure 2.2 [33].

9

Figure 2.2: Exploded representation of a typical mould [8]

The typical injection mould consists of several plates, namely: cavity and core plates, forming thepart cavity, support plates, retaining plate and ejector pin plate. These are generally made out of steelby machining, usually milling, and their dimensions are function of the number of cavities and the size ofthe parts being manufactured.

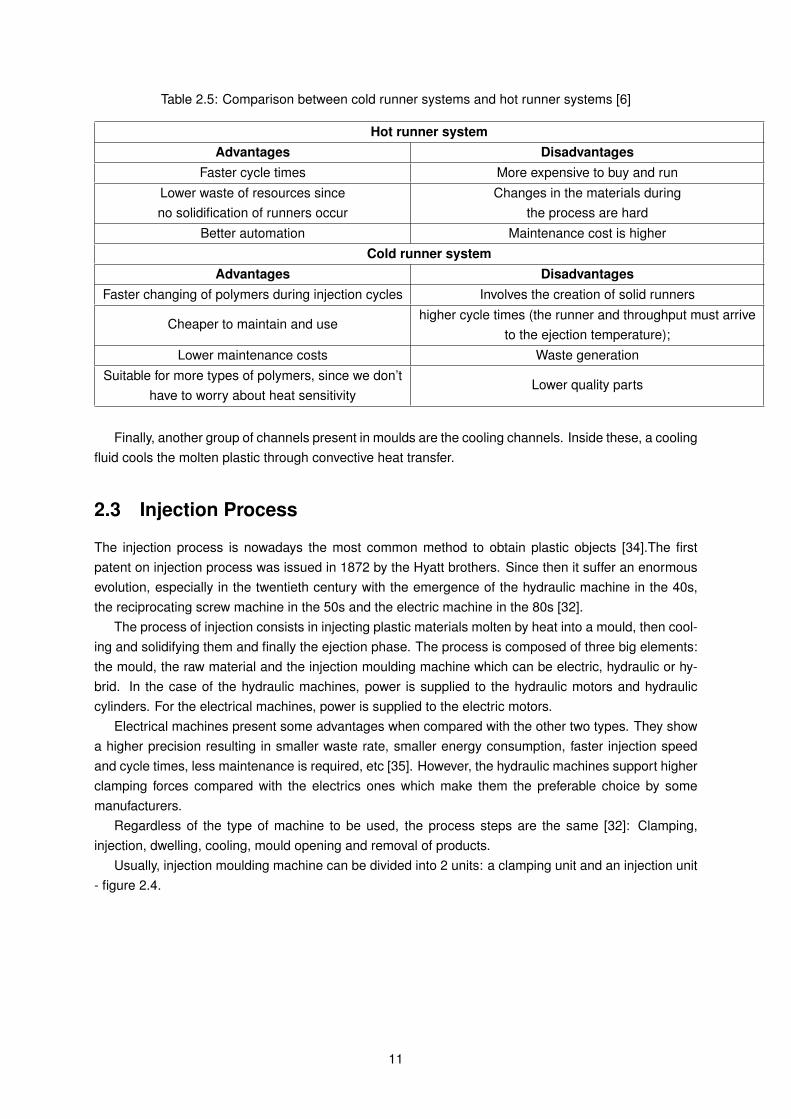

The mould consists of one or more cavities, not necessarily similar between them, and each cavityis connected to flow channels (runners) that are responsible to carry the molten plastic from the sprueto each cavity. For injection moulding there are two major types runners designated by the temperatureof the material fluid when injected: cold runners and hot runners - figure 2.3 [9] [10]. In the cold runnerssystem, the material is cooled along with the part, solidifying in the mould cavities and the runners,which are ejected together with the part being manufactured. In the hot runners system, the runners arelocated inside the mould and are maintained above melting point temperature, thus the material in therunners never solidifies and is used in the next cycle.

Figure 2.3: Typical feeding system - Cold runners(left) Hot runners (right) [9] [10]

While cold runner systems have the advantage of presenting a lower cost hot runner systems canachieve faster cycle times and reduce waste production drastically. However these present a higher costand higher maintenance [31]. Table 2.5 show some advantages and disadvantages of each choice.

10

Table 2.5: Comparison between cold runner systems and hot runner systems [6]

Hot runner systemAdvantages Disadvantages

Faster cycle times More expensive to buy and runLower waste of resources sinceno solidification of runners occur

Changes in the materials duringthe process are hard

Better automation Maintenance cost is higherCold runner system

Advantages DisadvantagesFaster changing of polymers during injection cycles Involves the creation of solid runners

Cheaper to maintain and usehigher cycle times (the runner and throughput must arrive

to the ejection temperature);Lower maintenance costs Waste generation

Suitable for more types of polymers, since we don’thave to worry about heat sensitivity

Lower quality parts

Finally, another group of channels present in moulds are the cooling channels. Inside these, a coolingfluid cools the molten plastic through convective heat transfer.

2.3 Injection Process

The injection process is nowadays the most common method to obtain plastic objects [34].The firstpatent on injection process was issued in 1872 by the Hyatt brothers. Since then it suffer an enormousevolution, especially in the twentieth century with the emergence of the hydraulic machine in the 40s,the reciprocating screw machine in the 50s and the electric machine in the 80s [32].

The process of injection consists in injecting plastic materials molten by heat into a mould, then cool-ing and solidifying them and finally the ejection phase. The process is composed of three big elements:the mould, the raw material and the injection moulding machine which can be electric, hydraulic or hy-brid. In the case of the hydraulic machines, power is supplied to the hydraulic motors and hydrauliccylinders. For the electrical machines, power is supplied to the electric motors.

Electrical machines present some advantages when compared with the other two types. They showa higher precision resulting in smaller waste rate, smaller energy consumption, faster injection speedand cycle times, less maintenance is required, etc [35]. However, the hydraulic machines support higherclamping forces compared with the electrics ones which make them the preferable choice by somemanufacturers.

Regardless of the type of machine to be used, the process steps are the same [32]: Clamping,injection, dwelling, cooling, mould opening and removal of products.

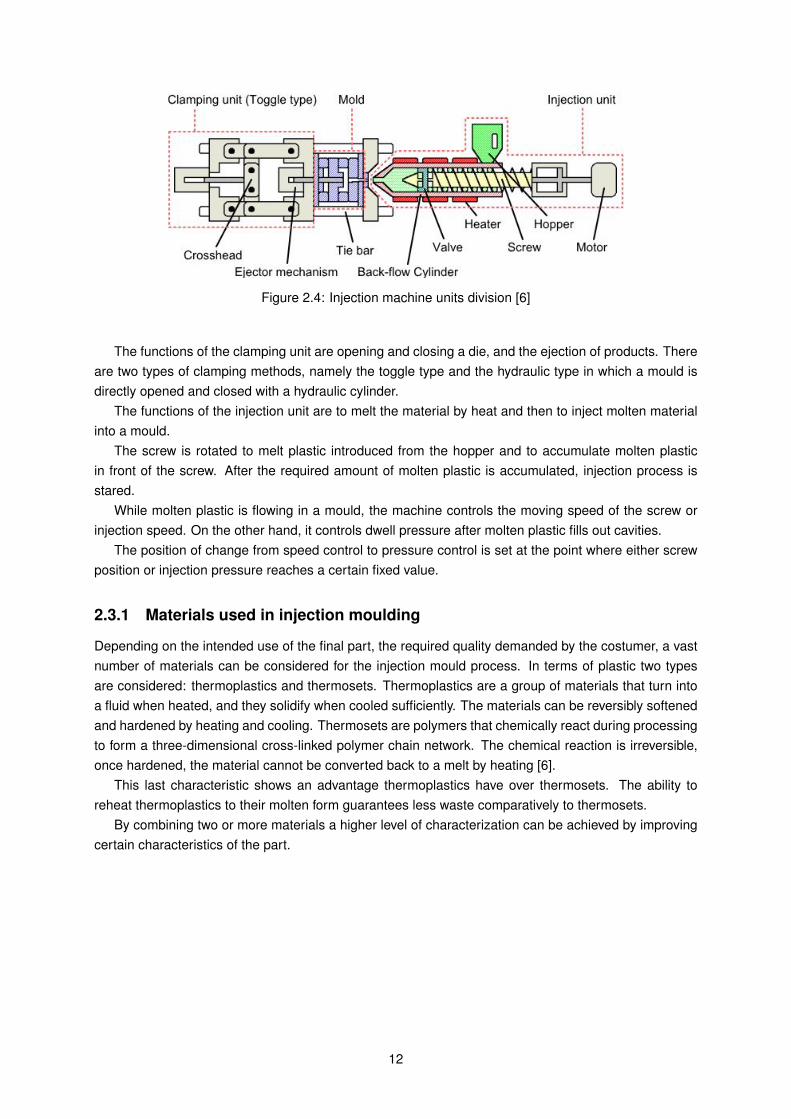

Usually, injection moulding machine can be divided into 2 units: a clamping unit and an injection unit- figure 2.4.

11

Figure 2.4: Injection machine units division [6]

The functions of the clamping unit are opening and closing a die, and the ejection of products. Thereare two types of clamping methods, namely the toggle type and the hydraulic type in which a mould isdirectly opened and closed with a hydraulic cylinder.

The functions of the injection unit are to melt the material by heat and then to inject molten materialinto a mould.

The screw is rotated to melt plastic introduced from the hopper and to accumulate molten plasticin front of the screw. After the required amount of molten plastic is accumulated, injection process isstared.

While molten plastic is flowing in a mould, the machine controls the moving speed of the screw orinjection speed. On the other hand, it controls dwell pressure after molten plastic fills out cavities.

The position of change from speed control to pressure control is set at the point where either screwposition or injection pressure reaches a certain fixed value.

2.3.1 Materials used in injection moulding

Depending on the intended use of the final part, the required quality demanded by the costumer, a vastnumber of materials can be considered for the injection mould process. In terms of plastic two typesare considered: thermoplastics and thermosets. Thermoplastics are a group of materials that turn intoa fluid when heated, and they solidify when cooled sufficiently. The materials can be reversibly softenedand hardened by heating and cooling. Thermosets are polymers that chemically react during processingto form a three-dimensional cross-linked polymer chain network. The chemical reaction is irreversible,once hardened, the material cannot be converted back to a melt by heating [6].

This last characteristic shows an advantage thermoplastics have over thermosets. The ability toreheat thermoplastics to their molten form guarantees less waste comparatively to thermosets.

By combining two or more materials a higher level of characterization can be achieved by improvingcertain characteristics of the part.

12

Chapter 3

Operationalisation of Eco-efficiencyModels

In the last chapter, a brief summary about the state of art of Eco-Efficiency was made. It was shownthat its use goes beyond a mere ”green” ideology but it can bring numerous economic benefits. It wasalso shown that one of the main obstacles to its use resides in the fact that a prior study to the systembeing analysed is indispensable, based on the fact that every characteristic that influences economic orenvironmental impacts must be accounted. The complexity of gathering the necessary data needed forthe use of eco-efficiency varies accordingly to the complexity of the system that we wish to evaluate, butit’s often time-consuming and arduous.

It’s exactly in this time-consuming and arduous work this dissertation will focus. Methods about howto turn the use of Eco-efficiency practical will be proposed together with results that validate the choicesproposed.

3.1 Operationalisation and simplification concepts

Although operationalisation and simplification can be interpreted as similar concepts, they carry differentmeanings in this work.

Operationalisation should be seen as the act of making something practical, of easy usage. On theother hand, the use of simplification should be considered as a mean to reach that operationalisation.

Regarding eco-efficiency, as shown in the previous chapter, its use carries some difficulties, namely,the elevated number of inputs that feed an eco-efficiency model and the arduous work needed to obtainthem. These obstacles, make the use of eco-efficiency non-practical i.e. non-operational for regular use.

This transformation of a non-operational model towards an operational one is the main objective ofthe dissertation and will be accomplished by simplifying methods.

Through expediting calculations and the use of empirical data to turn variable inputs into constants,an practical method can be achieved. These simplifications does not mean lack of rigour but a way tomake the use of Eco-efficiency more practical, i.e. operational.

Summing up, operationalisation should be achieved by means of simplifying processes and choices.This idea of simplification of methods will be shown in this dissertation through three different mod-

els representing three different scenarios connected to distinct moments of the use of eco-efficiencyin mould and injection industries 3.1. These three stages were chosen by identifying key distinct mo-ments within the manufacturing process. And thereafter those stages were validated by interviewing themanufacturing directors of a relevant company.

13

Although each one of these models will be presented individually in the chapters that follow this one,a brief description shall be presented in the next paragraphs so the reader has a succinct idea of thembefore approaching those chapters.

E.E. non operational on regular

basis

Simplification method

Operational E.E. method

Model 1

Model 2

Model 3 Op

era

tio

nal

izat

ion

m

od

els

Figure 3.1: Thesis overview - Problem, method and goal

3.2 Simplification models and exclusive model objectives

Before presenting any type of model a brief explanation about the existing system of the mould andplastic injection industry must be provided. Commonly the group of mould manufacturing and plasticinjection industries can be divided into three types:

• exclusive mould manufacturers - This kind of situation refers to those companies that solelymanufacture moulds for the injection industry. In this type of companies, the plastic injection pro-cesses are non-existent.

• exclusive plastic injection manufacturers - This kind of situation refers to those companies thatsolely act on the plastic injection process. In this type of companies, the mould is acquired from athird party. Mould manufacturing is non-existent.

• hybrid manufacturers - This kind of situation refers to a mix of the previous two types. In this typeof company the majority of the processes are exercised ”indoors”, from the mould creation to thefinal piece obtained from plastic injection.

Along this work only the two first types of manufacturers will be addressed, due to the fact that the lastone - hybrid manufacturers - can be seen as the pairing of the first two entities: mould manufacturerstogether with plastic injection manufacturers, being the characteristics of this last type the sum of thecharacteristics of the first two types.

After having defined the scope of the model (mould manufacturing and plastic injection processes),a more precise location in time for the models is needed.

In order to identify the steps, representing the temporal area of action, necessary to the manufac-turing process several visits to a manufacturing company were done and, together with the productionmanagers, a set of phases were identified. Along with this work, the system in study was defined by aset of phases, namely, ”Project development”, ”Negotiation phase”, ”Start of mould production”, ”End of

14

mould production”, ”Start of injection process”, and finally ”end of injection process”. This temporal flowis represented in figure 3.2.

Project Development

Negotiation Phase

Start of Mold Production

End of Mold Production

Start of Injection process

End of injection Process

Figure 3.2: Temporal universe of the system

The phases present above are defined as follows:

• Project development - First phase of the process. This is the phase where an idea for a newproject is born. It can be seen as a very early design stage, where the only few aspects aredefined. In this phase, the costumers are the stakeholders, not the company.

• Negotiation Phase - This is the phase where manufacturers negotiate product characteristics(price included) with potential costumers. It’s in this phase, that the final concept for the productbeing manufactured appears and where some manufacturing choices are made due to the client’sdemands. It requires knowledge about capabilities of the manufacturing assets.

• Start of mould production - First phase of the mould manufacturing process. It’s the phase wheredecisions about mould production are made. In this phase the answer to the question ”How will wemanufacture this mould?” is given. Namely, it’s in this stage that machines and other assets areallocated to the project.

• End of mould production - Last phase of the mould manufacturing process. In this phase theproduct manufacturer is able to analyse the project that ended.

• Start of injection process - Similar to the first stage of mould production, in this phase the finaldecisions about injection process are made. In this phase the answer to the question ”How will wemanufacture this product?” is given.

• End of injection process - Last phase of the process. It’s in this last phase that the manufacturercan review all the process and gather information that allows future improvements in the system.

3.2.1 Simplification models - First approach

The definitions presented above help contextualise the simplification models being developed and, al-though each one of them is described in an individual chapter, a brief description of them and thescenario they intend to represent is given:

The first model (model 1) presented in this work, is related to the selection of manufacturing pro-cesses for the mould manufacturing procedure. It arises in order to address the need of studying andpossibly improving the choice of the manufacturing process, and thus, it implies a good precision re-garding the results, meaning low error when comparing to the actual, non-simplified process.

15

The second model (model 2) presented in this work, is related to the negotiation phase of the process.It arises from the need of having real-time estimates of results, namely costs and environmental impacts.It’s expected that the results generated in this model, lack in terms of precision when in comparison withthe previous model.

The third and last model (model 3) presented in this dissertation, is related to an initial design phase.It emerges as a method of providing designers or any other entity that desires it so, a way of estimateresults when little is known about the processes needed to achieve the final product. Thanks to this lackof accurate data about the processes, this third model is expected to present the least accurate results.

3.2.2 Exclusive model objectives

One other aspect common to the three models that is necessary to introduce is the concept of .Recalling that the objective of the thesis is to develop operational models for the use of eco-efficiency,

leads to the conclusion that this also ought to be the main objective for each of the models developed.Although the models have the same main objective, they differ from each other because, as statedbefore, each one of them represents a different scenario. Due to this difference, a new set of objectivesarises, objectives that intend to represent the necessities that each scenario presents. For example,while the second model requires that a certain input should be easily edited by the user that same inputin any other model can be set as a fixed value, outside the immediate control of the user.

Due to this exclusivity of the models regarding some objectives and in order to differentiate themfrom the main one (to develop an operational model for the use of eco-efficiency), it was settled thatthese set of objectives will be known as exclusive model goals.

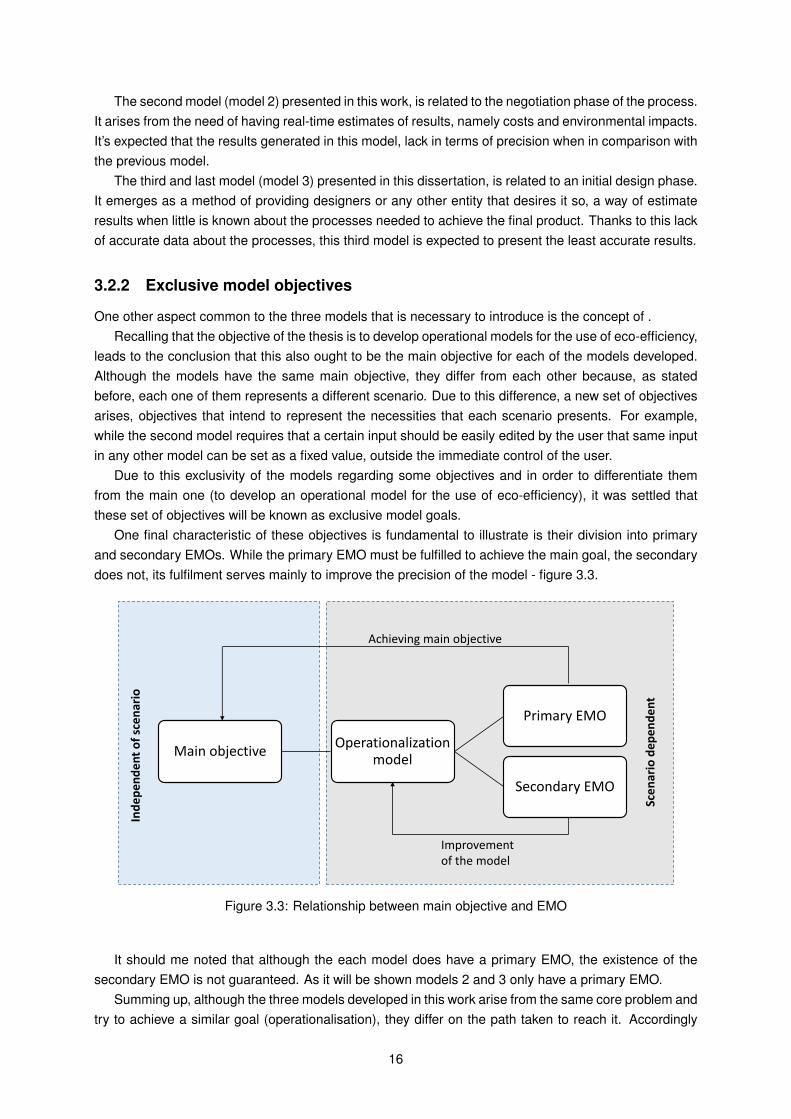

One final characteristic of these objectives is fundamental to illustrate is their division into primaryand secondary EMOs. While the primary EMO must be fulfilled to achieve the main goal, the secondarydoes not, its fulfilment serves mainly to improve the precision of the model - figure 3.3.

Main objectiveOperationalization

model

Primary EMO

Secondary EMO

Sce

nar

io d

epen

den

t

Ind

ep

end

en

t o

f sc

en

ario

Achieving main objective

Improvement of the model

Figure 3.3: Relationship between main objective and EMO

It should me noted that although the each model does have a primary EMO, the existence of thesecondary EMO is not guaranteed. As it will be shown models 2 and 3 only have a primary EMO.

Summing up, although the three models developed in this work arise from the same core problem andtry to achieve a similar goal (operationalisation), they differ on the path taken to reach it. Accordingly

16

to the model’s stage of operation, distinctive mechanisms will be used to simplify the ”real”, originalmodel.3.1

3.2.3 Type of inputs

One last aspect it’s important to explain is the existing division of inputs that feed the models. Theseinputs were divided into two groups: active inputs and inactive inputs. Active inputs are those that mustbe loaded by the user every time the model is used. This gives some degree of freedom to the user.

Inactive inputs are fixed (constant value) inputs. These must be loaded previously to the use of themodel and are used together with active inputs to predict results. Loading the models with inactive inputscan be a time-consuming task, but has the advantage of only being done the first time the model is usedor when something major changes in the manufacturing company - figure 3.4.

Active inputs

Inactive inputs

Model’s equations Model’s output

Inp

uts

div

isio

n

Inputs overview

Pre-fixed values

Variable values

Figure 3.4: Inputs division used in this work

3.2.4 Models Validation

There are 5 moulds available to do the mould model’s validation and the respective 5 parts to do theplastic part’s validation. Moulds are named from Mould A to Mould E and the respective parts, Part A,Part B, etc. In the validation section, one of the moulds will be chosen randomly to perform the validation.

In order to model the system, data was gathered by doing several visits to a mould and injectionmanufacturing site. Thereafter, the model was validated using data from that same company. This canbe seen as an ”overfitting” feature and possible a drawback in the model. Of course, using the samemethodology for different systems should be done carefully, and one should expect larger precisionerrors according to how different that same system is from a mould and injecction system.

Before ending the chapter, one last note should be delivered. It should be pointed out that thesemodels do not intent to be a closed system whose users cannot manipulate. These models should beseen as guidebooks, a set of simplification rules/suggestions created in order to achieve the intendedgoals.

In the next chapter, the first of the three models will be presented in a more detailed way.

17

18

Chapter 4

Operationalisation Model – Processselection model

This chapter will address the first operationalisation model, thus it will be essential to detail it – whatscenario it represents, what its goals are and who will benefit from its use. For a better understanding ofthe model developed, the overall methodology is presented in this chapter, followed by the model itself.

Finally, this operational model must be validated. To do it so, it will be used a real case study from amould manufacturing and plastic injection company.

4.1 Model characterization

Accordingly to what was presented in the previous chapter, the model being described was designed toreduce the problem identified in the introductory chapter - elevated complexity of making eco-efficiencystudies in the mould and plastic injection industries. But, of course, this is true to all three models presentin this thesis. What differentiate them is the scenario they represent.

The first model developed arises from the necessity of having real-time data that would serve as abase to make process decisions allowing the educated choices about what path to take to achieve thedesired results.

In relation to to the different types of industries presented in the previous chapter, it must be notedthat although the model acts in both exclusive mould manufacturers and exclusive plastic injection man-ufacturers its role differs depending on the type of manufacturer.

For exclusive mould manufacturers, and remembering figure 4.2, it can be noted that using the modelat ”Start of Mould Production” gives the manufacturer data that allows selecting the better path for themanufacturing of the mould and using the model in ”Star of Injection Process” provides data aboutinjection process. The usefulness of such data for exclusive mould manufacturers is diverse. It can beseen as adding value to the service provided if we consider that this data can be delivered to clients withthe mould.

Regarding the other type of industry - plastic injection manufacturers - the utility of the model relieson a similar explanation. For exclusive plastic injection manufacturers, the model is able to provide anestimation or more precise data about the injection process if estimation inputs or real ones are used(obtain from a post production stage), respectively.

Using the same model at the end of production, feeding it with real results instead of predicted ones,gives more precise results and therefore can be used to study the processes and gather relevant datato improve the model and future choices.

19

The capabilities described in the last paragraphs can be translated into EMO (see chapter 3.2.2).Accordingly, the primary EMO is the capability of predicting economic, energetic and eco-efficiencyindicators for the moulds to be manufactured and for the plastic injection process. The secondary EMOis the ability to feed a database of characteristics of the processes. This allows a better understandingof the processes by comparing the manufactured mould and plastic piece’s process characteristics withothers previously made, giving the model a continuous improvement capability.

Thus it can be concluded that, and in consequence of the definition of primary and secondary EMO,the completion of the primary EMO is mandatory to achieve the objective of the thesis, since the dis-sertation objective demands a simplified model for eco-efficiency, while the completion of the secondaryEMO is optional. The secondary EMO allows the user to store the results of every mould a plastic pieceproduced allowing a better understanding of the processes by comparing the manufactured mould’s pro-cess characteristics with others previously made, and as such, it provides the model with a continuousimprovement capability. See figure 4.1

Exclusive model

objectives

Dissertation objective

Operationalization

Primary EMO’s

Results prediction

Secondary EMO’s

Results database

Figure 4.1: Main objective and exclusive model objectives

One of the main differences between these two exclusive model objectives resides at the differenttime stage where they act (figure 4.2). While the secondary one, in order to fulfil the requirement ofcreating a database, demands input values with minor errors and therefore known values, which can beobtained in a post-production stage, the first one doesn’t do it so. In order to fulfil this primary objective(capability of predicting economic, energetic and eco-efficiency indicators), predictions about processcharacteristics can be seen as acceptable inputs.

20

Project Development

Negotiation Phase

Start of Mold Production

End of Mold Production

Start of Injection process

End of injection Process

Primary Exclusive Model Objectives

Secondary Exclusive Model Objectives

Figure 4.2: EMO’s temporal place

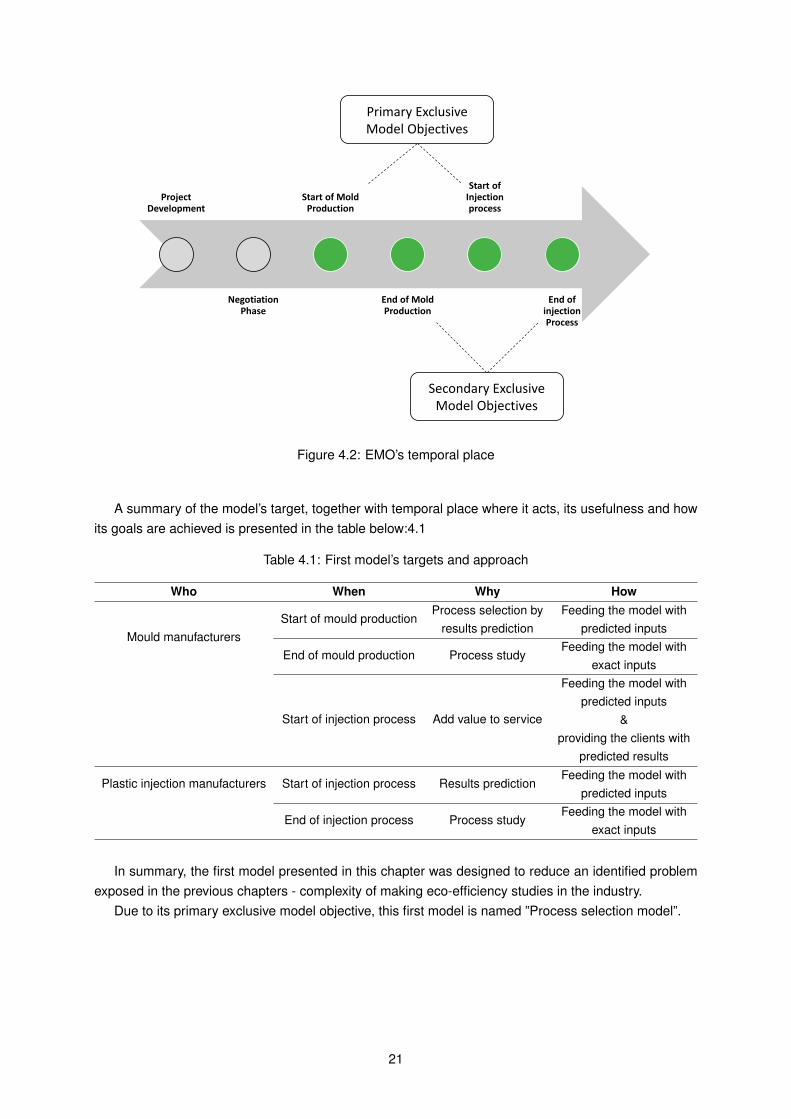

A summary of the model’s target, together with temporal place where it acts, its usefulness and howits goals are achieved is presented in the table below:4.1

Table 4.1: First model’s targets and approach

Who When Why How

Mould manufacturersStart of mould production

Process selection byresults prediction

Feeding the model withpredicted inputs

End of mould production Process studyFeeding the model with

exact inputs

Start of injection process Add value to service

Feeding the model withpredicted inputs

&providing the clients with

predicted results

Plastic injection manufacturers Start of injection process Results predictionFeeding the model with

predicted inputs

End of injection process Process studyFeeding the model with

exact inputs

In summary, the first model presented in this chapter was designed to reduce an identified problemexposed in the previous chapters - complexity of making eco-efficiency studies in the industry.

Due to its primary exclusive model objective, this first model is named ”Process selection model”.

21

4.2 Methodology

The general methodology applied will be presented in this section. Every main step applied in the modelwill be described.

Following the background provided in chapter 1, the first step is recognising and identifying the needto develop a model that fills the existing gap in the mould and injection industries regarding eco-efficiency.Having done this, the time and the model’s scenario of operation was defined. (See figure 4.3)

Project Development

Negotiation Phase

Start of Mould

Production

End of Mould

Production

Start of injection process

End of injection Process

Figure 4.3: First model’s time of operation. Primary EMO in green and secondary EMO in blue

After the goal was defined, the development of the model began with the division of the process intwo major groups: mould production and plastic injection process.

Following the previous step, a breakdown on the first major group started. A study was made todefine what manufacturing sub-groups compose the mould manufacturing process and for each group,what sub-processes are part of them. To achieve this, studies from previous works and several visitsto a hybrid company were done. This information gathering allowed to understand the place of severalvariables and achieve valid simplifications, whose objective is, as stated before, serve as backbone tooperationalisation of the model.

As the sub-processes were defined, the identification of the variables that compose those sub-processes was done, always having in mind the necessity of simplification. Thus variables with lowrelevance to cost or energetic impact were neglected.

Finally, the influence of several components and variables that compose an injection mould weremodelled.

Finished the mould manufacturing part of the model, the injection process part was created.In the same way of the mould creation process, the plastic injection process was considered as a

process composed by sub-processes, thus the first step in the model design was to establish allsub-processes and the inputs variables that are part of them, defining not only the process but also the partto be manufactured in terms of batch, type of machine, etc.

Having established the part dimensions and process data, it was possible to validate the model andpresent the results.

It’s important to notice that the goal of this model, as stated before, is to create a model that iscapable of operating in different companies, as such, two alternatives to inputs were created. The firstset of inputs that feed the model are inputs whose origin can be traced to data from previous studiesand different companies - empirical evidence. The second set of inputs, working as an alternative to thefirst set, are inputs related to the particular company using the model. These inputs need to be insertedin the system beforehand, but bring better precision to results.

Within these two sets of inputs, two subgroups were defined, active inputs and inactive inputs, thuscreating a division between inputs that need constant updates each time a new manufacturing processbegins and those inputs that need only to be changed when the company in question performs somestructural change in the way it performs.

To validate the model created a real case study was used - production of conventional steel mouldsand the injection of the respective plastic pieces. The results associated with this model are presentedin the chapter ”Results”, where different mould alternatives are analysed and compared.

22

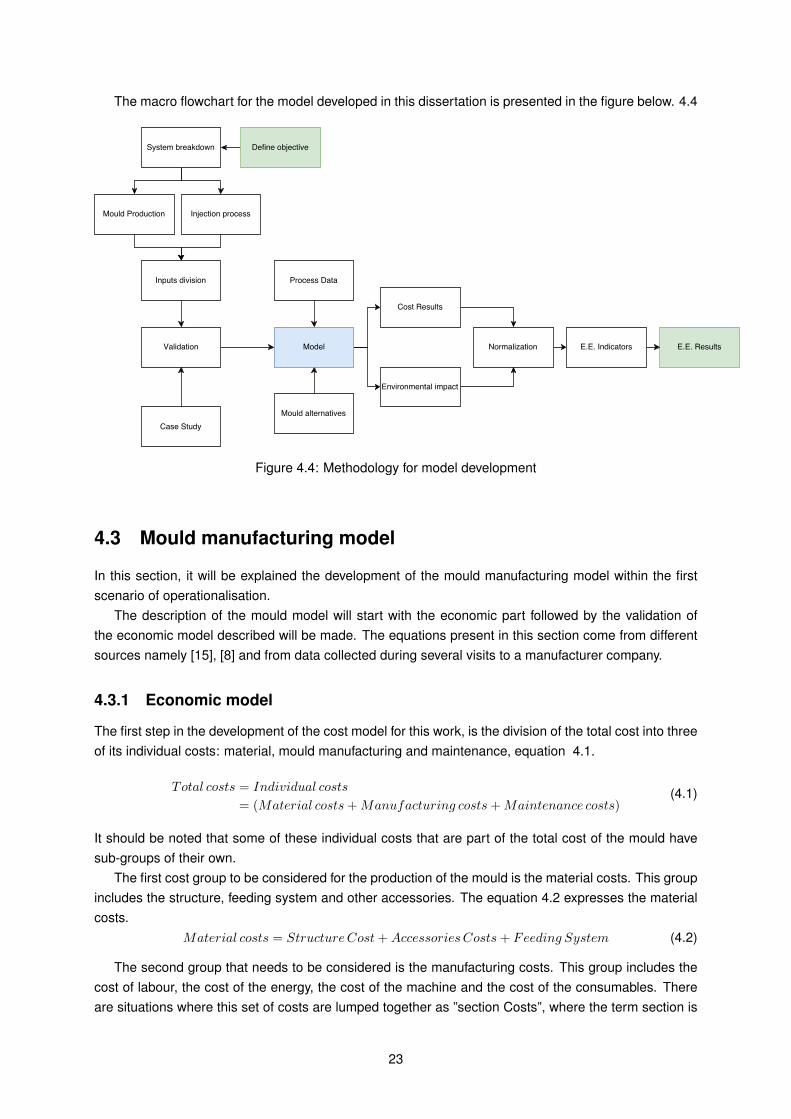

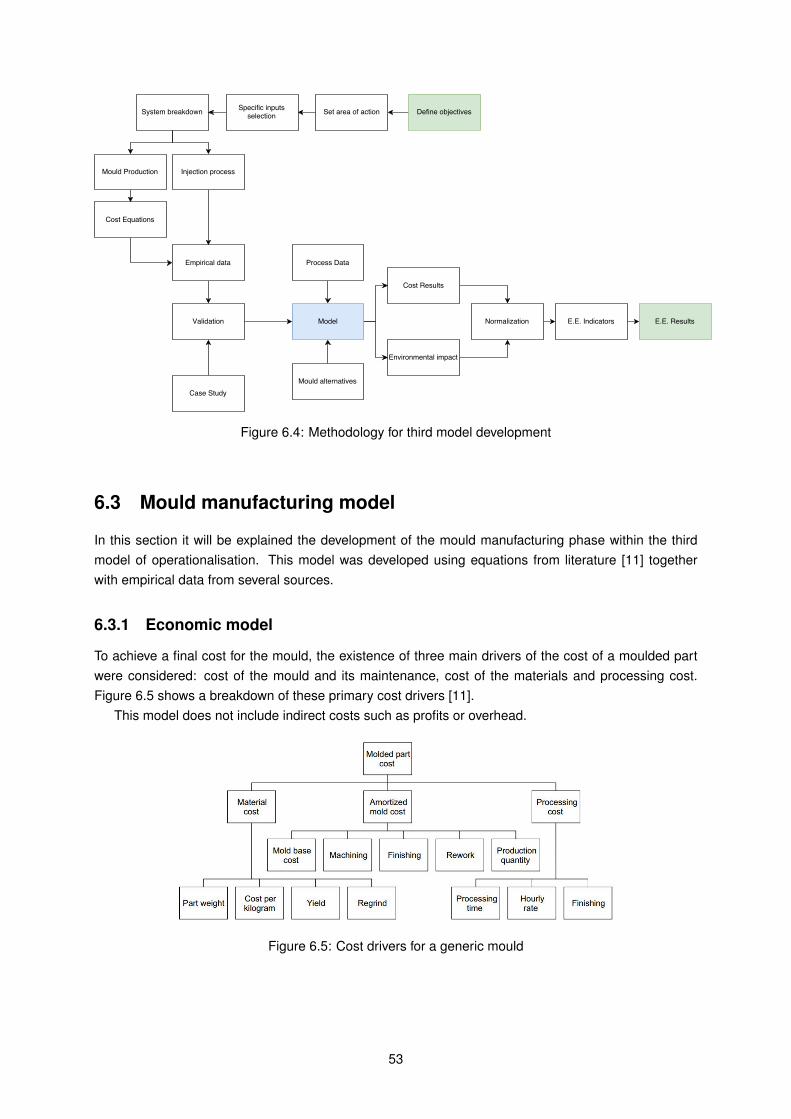

The macro flowchart for the model developed in this dissertation is presented in the figure below. 4.4

Figure 4.4: Methodology for model development

4.3 Mould manufacturing model

In this section, it will be explained the development of the mould manufacturing model within the firstscenario of operationalisation.

The description of the mould model will start with the economic part followed by the validation ofthe economic model described will be made. The equations present in this section come from differentsources namely [15], [8] and from data collected during several visits to a manufacturer company.

4.3.1 Economic model

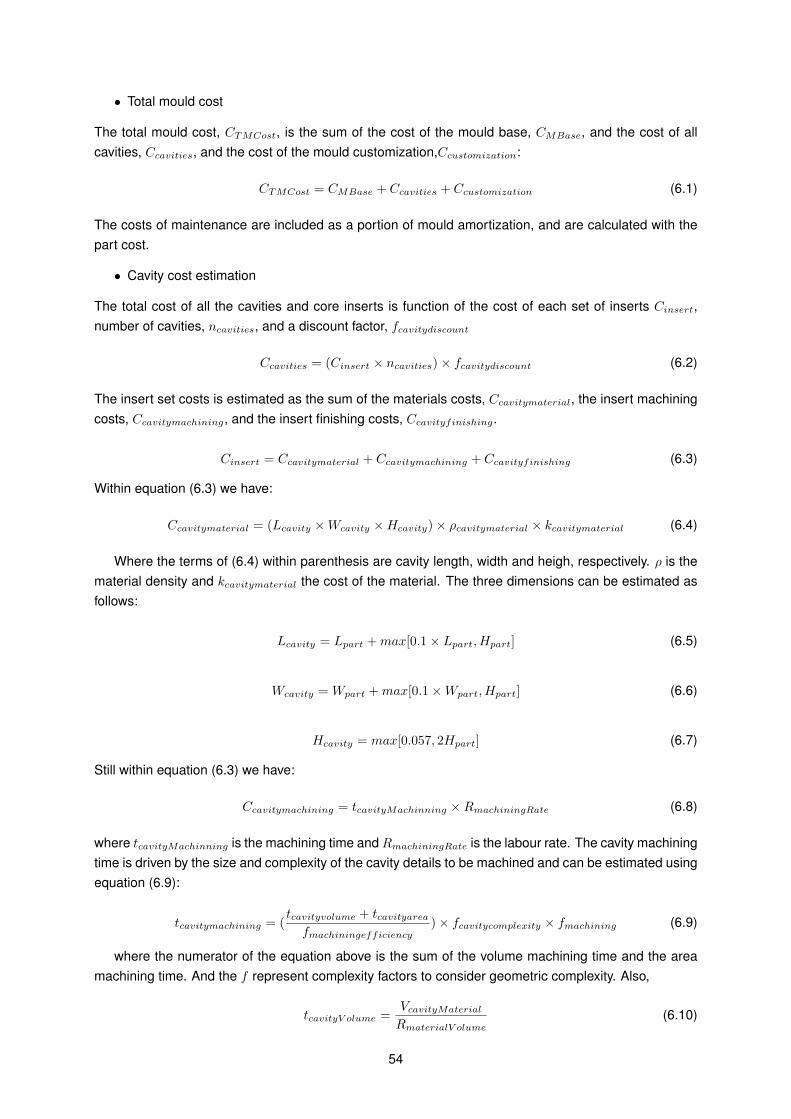

The first step in the development of the cost model for this work, is the division of the total cost into threeof its individual costs: material, mould manufacturing and maintenance, equation 4.1.

It should be noted that some of these individual costs that are part of the total cost of the mould havesub-groups of their own.

The first cost group to be considered for the production of the mould is the material costs. This groupincludes the structure, feeding system and other accessories. The equation 4.2 expresses the materialcosts.

Material costs = StructureCost+AccessoriesCosts+ Feeding System (4.2)

The second group that needs to be considered is the manufacturing costs. This group includes thecost of labour, the cost of the energy, the cost of the machine and the cost of the consumables. Thereare situations where this set of costs are lumped together as ”section Costs”, where the term section is

23

connected to the type of manufacturing process being used. Equation 4.3 translates the manufacturingcosts.

Manufacturing costs = Labour cost+ Energy cost+Machine cost+ consumable costs (4.3)

The last element that integrates cost of producing a mould is maintenance cost of the machines andit’s calculated using equation 4.4

Maintenance costs = maintenance allocated%×∑

(Mainmachine cost+ tool cost) (4.4)

An overview of the model is show in figure 4.5:

Materials & Accessories

Structure

Accessories

Feeding system

Manufacturing

Labour

Energy

Machine & Consumables

Maintenance

Investment

Main machine

Cost

Tool Costs

Figure 4.5: Economic model major groups overview

Remembering that the model presented in this work is connected with the idea of simplificationof methods, a detailed analysis of each sub-group, where the simplifications made are explained, isnecessary.

Materials cost

• Structure costs

Starting with the analysis of structure costs, the first step and simplification is to identify the relevantelements that make the structure. These are: clamp plates, mould plates, ejector plates, and ejector set.The next simplification made in ”structure costs” is the transformation of the costs of each component,where common heat treatments and polishing process are included, listed before from active inputs toinactive inputs. To do this, a table relating the dimensions of mould plates (height, width, thickness) andthe cost of those components should be created beforehand and fed to the model, this gives the user allstructure costs from only 3 active inputs for plate. The creation of this table can be done using data frommoulds already built. Although this can be a time-consuming work, it only has to be done once, savingtime in the long run.

In the situation where the desired dimensions are not present in this cost table, the desired cost canbe calculated using the set equation shown in table 4.2 where h,w,t represent respectively height, width

24

and thickness expressed in millimetres. These equations were determined applying a fuzzy algorithm todata from previously made moulds and it was considered that the structure is made from a generic steelwhose cost is around 4.5e per kg. In a very simple way, fuzzy is a logical method that finds approximaterelations between inputs and respective outputs [36].

Table 4.2: Cost [euros] equations, deduced using a fuzzy algorithm

Structure Element Cost EquationClamp Plates 0.733h× 0.113w × 0.154t

Mould Plates 0.631h× 0.201w × 0.168t

Ejector Plates 0.722h× 0.107w × 0.171t

Ejector Set 0.801h× 0.098w × 0.101t

• Accessories

Regarding the accessories costs, the users have two options to enter them into the model, the first one isby direct input and the second one is by selecting from a predefined list of the most common accessoriesand respective costs, the ones that are part of the mould being manufactured. This second option arisesfrom the fact that it may be difficult to introduce specific values for the accessories. Therefore, constantcost values are suggested. These come from average values from empirical data. Table 4.3 shows thesuggested accessories cost values.

Table 4.3: Suggested cost per accessory for common accessories

Finally, the user must provide dimensions for cavity inserts and the material price they are made of.In the case, the user doesn’t provide the material, this is assumed as a martensitic stainless steel with afixed cost of 7.9e/kg. In case this information is uploaded in the model it must be inserted together withthe material density [kg/mm3] and its price [e/kg].

• Feeding System

In this case, there are some options the user must define to calculate the cost: number of nozzles,existence or not of hot runners, type of manifold bloc and cost of the injection controller - equation 4.5.

(4.5)Feeding system costs=Number of nozzles×nozzle cost+Distribution bloc cost+controller cost

The cost of the nozzles should be inserted in the model as an inactive input, by studying the company’sroutines and fixing an average value in the model. The same situation for the controller. In the case ofthe cost of the manifold bloc, it depends greatly on the type of bloc used, so a list of common types usedby the company must be fed to the model, together with their cost, as a set of inactive inputs.

Manufacturing costs

The determination of manufacturing costs starts by defining what processes are part of a mould man-ufacturing process. These are: milling (conventional and CNC), wire and penetration EDM, grinding,laser, turning (conventional + CNC) , CAD, CAM and small manual processes.

• Labour Costs

25

Labour costs are define as the sum of cost of labour internal to the company with the subcontractsmade.

Labour costs associated with a specific process is given by equation 4.6 :

(4.6)Labour costsinternal =Man/hour cost× process time

And the cost of worker per hour is given by equation 4.7:

(4.7)Man/hour cost =Monthly wage× shifts× 14× taxesnumber days year ∗ working hours day

To simplify the calculation of labour costs a few assumptions were made, these are consideredinactive inputs. First of all, the worker’s occupation rate is considered 100%, taxes over wages of 23%,the number of working days in a year is considered to be 240 and a working day is considered to have8 hours. Regarding the cost of the subcontracts, this input is asked to the user as a percentage of theinternal labour cost, thus being an active input.

The default value is 10% of the total production cost, this was suggested by the engineer responsiblefor the mould production.

• Energetic Costs

The energetic cost depends on several factors namely, on the machine, on the processing time and onenergy cost. This relationship between factors is translated by equation 4.8

(4.8)Energy cost[e] = Energy unit cost[e/kWh]× Energy[kWh]

There are two ways to introduce the energy variable into the model, the first is to previously take severalmeasurements directly from the machines and use the average energetic value from those measure-ments, the second one is by using the 60% of the apparent power of the connected machine. Thissecond option can be justified by the analysis of the energetic map of several moulds, where the ma-chine works on average at 60% of its apparent power. Both of these options are fed by inactive inputs,in the first case the energy consumed by the machine and in the second case the apparent power of themachine.

The energy unity cost input, since it is tabled by EDP for industries - Energias de Portugal and majorchanges occur seldom, it’s considered an inactive input and its value was fixed at 0.062 [e/kWh] [37].

• Machine Costs

The cost of the machine is dependent on the machine cost per hour and on the processing time. Thecost is given by equation 4.9

(4.9)Machine cost =Machine cost per hour [e/h]× Processing time [h]

The machine cost per hour can be determined by using equation 4.10, where I is the acquisition cost ofthe equipment, r is the fixed interest rate, that was fixed as 10% and n is the depreciation time.

(4.10)Machine cost per hour[e] = I×(1−(1+r)−n)r × 1

working days per year×working hours per day

The acquisition time is considered an inactive input, therefore it is necessary to create a databasecontaining the acquisition cost for each machine before the use of the model.

In order to simplify the entry of inputs, the depreciation time n was considered to be 8 years [38].

• Consumables Costs

26

The consumable group is composed of the machine’s tools used in the manufacturing of the mould andby the cutting fluids that are needed for some processes. Starting by the cutting fluids, the cost of thefluid is given by equation 4.11

(4.11)Ccf = Ptime × CFcons × CFc

where Ccf represents the cost of cutting fluid (e), Ptime represents the process time (h), CFcons thecutting fluid consumption (dm3/h) and CFc the cutting fluid cost (e/dm3). To simplify the model thecutting fluid consumption and cutting fluid cost were set as constant value (inactive input). Althoughthe cutting fluid consumption parameter changes accordingly with machining characteristics [39], it wasobserved that the difference between processes was negligible, thus this value was set as 0.0012dm3/h.The fluid cost was set as 8 e/h. One final thing that should be noted in regards to cutting fluid costs isthat in the case of the EDM processes, the costs associated with the fluid are inserted in the tool costgroup.

Finally, respecting the tools costs, equation 4.12 is used to determine the cost:

simplification is rather difficult since each machine uses different types of tools and each tool presentsdifferences in the wear rate. It is suitable to emphasize that the mould material has an important effecton the tool’s life and only steel moulds were studied, thus to reach a conclusion about tooling costs twocompanies were analysed - table 4.4

Table 4.4: Tooling cost from 2 different companies for steel moulds

Company Anual Cost of tools [e] Hours/year machines e/hCompany 1 94866 32712 2.9Company 2 74750 28750 2.6

To simplify the tooling cost an average value was chosen, therefore the tooling cost per hour was setas 2.75 e/h.

Maintenance costs

In the case of the maintenance costs, the main machine cost and consumables costs subgroups wereaddressed in the previous subsection and the maintenance investment is an active input of the model.

Complexity factor

After putting all the previous costs together it was noted that there was a gap between real cost andthe costs presented by the model. This was due to the fact that the complexity of the mould was notbeen taken into account. In order to solve this, a new active input was developed - complexity input, thatrepresents a constant value used to multiply by equation (4.1) giving the final cost of the mould.

Still regarding the complexity input, the model demands that the user selects one of three levels ofcomplexity for the mould being developed. The first level represents the simplest mould possible, whereneither the object being produced has a complex geometry nor the mould need to have some complexcinematic, like for example rotation. The second level represents a mould more complex than a com-plexity 1 mould, and is related to the manufacturing of objects with complex geometry, but where themould has simple linear movements. The third complexity level represents a mould developed to man-ufacture objects with complex geometries and non-linear movements. This non-linearity of movements

27

requires the existence of non-ordinary accessories in the mould, increasing its cost. Table 4.5 shows themultiplying factors for each complexity level. These were obtained together with the production managerof a company, by first defining the complexity of several moulds and then finding an average value foreach complexity level that reduced the gap between the model’s results and real results.

Table 4.5: Complexity Cost factors

Complexity Level 1 2 3Cost factor 1.00 1.05 1.10

4.3.2 Model Validation

In order to validate the simplified cost model, a real case study was used. This case study, and in orderto validate the complexity input, is composed by 2 different moulds. In order to fulfil the non-disclosureagreement, images of the mould will not be shown and the manufacturing company identity will not berevealed.

Table 4.6 presents the principal dimensions of the moulds used to validate the model.

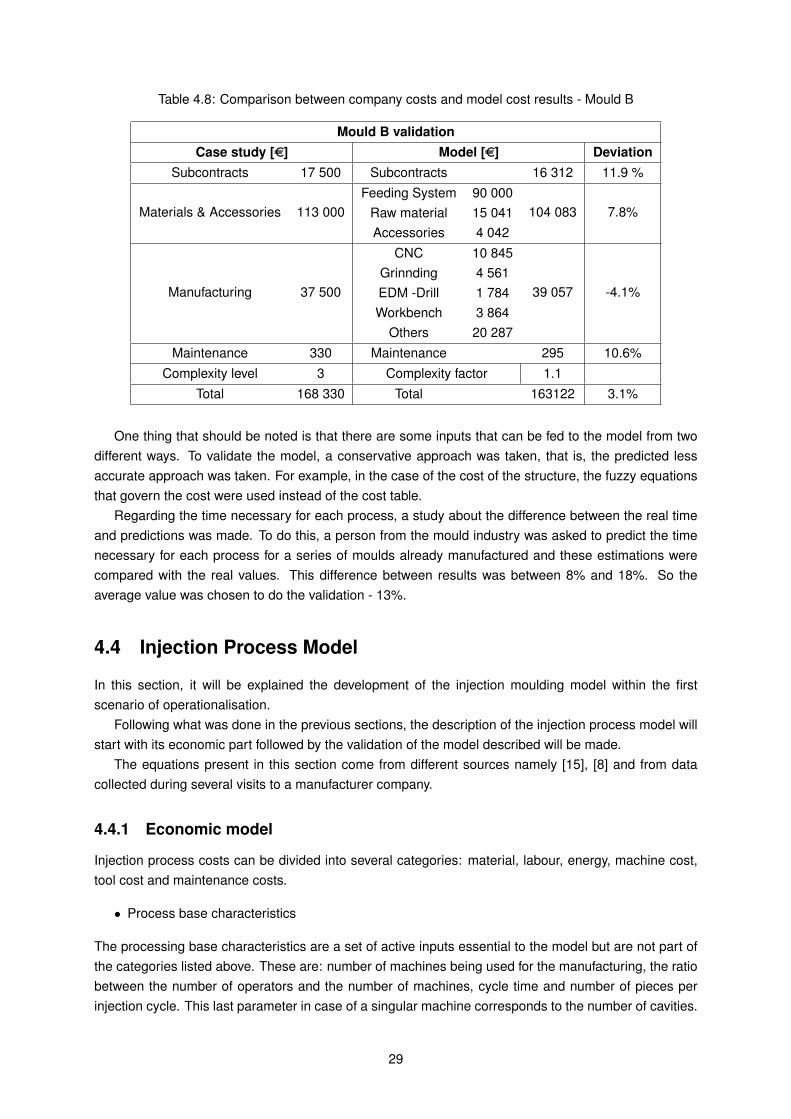

Tables 4.7 and 4.8 present the cost results for the case studies and the current model. A comparisonbetween both is also shown through the deviation between costs.

For mould E of complexity level 1, the deviation between the model and the case study is around2.3%. For mould B the deviation lies at 3.1%.

For each case presented, although the major deviation occurs in the subcontract values, the mostsignificant deviation takes place in the manufacturing group.

Table 4.7: Comparison between company costs and model cost results - Mould E

Mould E validationCase study [e] Model [e] Deviation

One thing that should be noted is that there are some inputs that can be fed to the model from twodifferent ways. To validate the model, a conservative approach was taken, that is, the predicted lessaccurate approach was taken. For example, in the case of the cost of the structure, the fuzzy equationsthat govern the cost were used instead of the cost table.

Regarding the time necessary for each process, a study about the difference between the real timeand predictions was made. To do this, a person from the mould industry was asked to predict the timenecessary for each process for a series of moulds already manufactured and these estimations werecompared with the real values. This difference between results was between 8% and 18%. So theaverage value was chosen to do the validation - 13%.

4.4 Injection Process Model

In this section, it will be explained the development of the injection moulding model within the firstscenario of operationalisation.

Following what was done in the previous sections, the description of the injection process model willstart with its economic part followed by the validation of the model described will be made.

The equations present in this section come from different sources namely [15], [8] and from datacollected during several visits to a manufacturer company.

4.4.1 Economic model

Injection process costs can be divided into several categories: material, labour, energy, machine cost,tool cost and maintenance costs.

• Process base characteristics

The processing base characteristics are a set of active inputs essential to the model but are not part ofthe categories listed above. These are: number of machines being used for the manufacturing, the ratiobetween the number of operators and the number of machines, cycle time and number of pieces perinjection cycle. This last parameter in case of a singular machine corresponds to the number of cavities.

29

In the case of multiple machines, if the cycle time is the same (as in the case of matching machines),this parameter corresponds to the sum of the cavities in all the machines. Finally, in the case of multipledifferent machines being used this parameter corresponds to the number of parts manufactured fromthe moment the first parts are done until the last machine finishes the first set of parts.

Table below shows how to get a set of needed parameters from the base characteristics:

Table 4.9: Set of parameters needed to characterize the injection process

Process characteristic EquationParts/machine Safety Batch/Number of machines

Production rate [parts/unit time/machine] Number of parts per cycle/cycle time

Production time Parts permachine/Production rate

• Material

The cost of the material is determined using equation (4.13), an variation of an equation from [40], wherethe plastic material cost represents the cost of the piece material, safety batch represents represents thedesired batch plus the number of rejected pieces and the setup scrap represents the quantity of materialused during the machine setup.

The part weigh must be uploaded into the model by the user, therefore being an active input. The safetybatch is given by equation (4.14):

(4.14)Safety batch [pieces] = (1 +batch [pieces]

100)× rejected [%]

In the case of the setup scrap, it is difficult to predict it directly. So, an equation that estimates thenecessary quantity of material needed during the setup was created - equation (4.15).

SetupScrap [kg] = partweight [kg/piece]× Total number of cavities× number of cycles for setup(4.15)

Looking at the equation above, we conclude that the number of cycles for setup is another active input,easier to estimate than the quantity of material necessary to setup. Regarding the plastic material cost,this is an inactive input, the company must beforehand create a material database where the cost of thematerials used within the company is present. In the cases where this database in non-existent, genericcosts for pellets of the most common materials are suggested - table 4.10 [41]. In both situations, theonly active input will be the type of material used in the process.

Table 4.10: Average price of plastic pellets from the last 12 months

Material PP PBT PET ABS PS PA 6 POMCost e\kg 1.3 2.7 1.8 1.4 1.0 1.6 2.1

• Energy

The calculation for the energetic cost starts by choosing the machines necessary to the process. To doit so, the user must choose from a list of available machines the desired machine from a selected clampforce range and material being used. The elevated variance in power when different materials are usedeven with the same machine is the reason for which it’s important to select the material [42].

30

This machine list, that must be created beforehand accordingly with the company assets, includesfour types of entries per material: Identification of the machine, clamping force, average energy con-sumption, type (electric, hydraulic or hybrid).

The creation of this list is a time-consuming work since entails a series of measurements for eachmachine and for each material since material does influence the energetic input.

Table 4.11 shows an example of a generic machine table.

Table 4.11: Machine example list for POM plastic pellets

Machine ID ... 5445Clamping Force [ton] ... 50

Average measured power [kW] ... 6.0Type of machine ... Electric

In case such table does not exist average energetic values are offered to the user, accordingly tomeasurements made by Goncalo Cardeal in [42]. for electrical machines.

Besides the type of material, the user must choose from four ranges of clamp forces: [0-60],[60-120], [120-180] and [180-240] all in tonnes. The creation of these four groups comes from the factthat, accordingly to the analysis made from empirical data, the average energetic power does not varysignificantly within each group, but varies from group to group. For hydraulic machines, data from thecompany shows that, in average, they consume about 30% more than electrical machines.

Table 4.12: Average measured energetic values for electric injection machines

The user should have in consideration that energetic estimations are hard to make and unreliable,so the use of the suggested values for energy may bring elevated errors to the energetic cost. Finally,using equation (4.16) we can determine the energetic cost:

(4.16)Energetic cost = energy cost× process time×machine average power

The process time (sum of time each machine spends working to achieve desired batch) is determinedusing the equation (4.17):

(4.17)Process time =safety batch× cycle timeNumber of parts per cycle

In the case of several machines are being used a new active input rises. The user must estimate thewhat percentage of the process time is given to each machine.

• Labour

Labour cost are given by equation (4.18) shown below:

(4.18)Labour Cost =ManhourWage× Production time×Operators permachine

• Maintenance

31

Equation (4.19) is used to calculate the maintenance costs needed to produce the batch of parts for theclient:

(4.19)MaintenanceCost = Cost per intervention× number of interventions needed

(4.20)Number of interventions needed =Number of cycles to produce batch

Number of cycles between interventions

The number or cycles between interventions is defined by the company, therefore it’s considered aninactive input.

Of course, if the number of cycles needed to fulfil the batch requirement is lower that the number ofcycles between interventions the cost is zero.

• Tool

The mould is the main tool used in injection moulding process.The tooling cost is calculated thoughequation (4.9) and (4.10) where I in this case represents the total mould cost, r is the interest rate and nis the number of years defined to pay the investment.

Both interest rate and depreciation time were set as inactive inputs using the constants 10% and 10years respectively.

• Machine cost

To determine the machine cost an identical approach to what was described in the mould productionphase was followed. Equations 4.9 and 4.10 were used. Both interest rate and depreciation time wereset as inactive inputs using the constants 10% and 10 years respectively.

• Complexity factor

Similarly to the mould production phase, a complexity factor is needed to achieve better accuracy on theresults. It corresponds to a factor that will be used to multiply the final cost with it.

The complexity factor tries to fill gaps in the cost models created by complex part geometries. In thesame way, a three level complexity factor was introduced in mould manufacturing phase, an identicalthree level system is part of the injection process cost model.

Each level of complexity translates more complex part geometries, being level 1 associated withparts with simpler geometries and level 3 with parts with complex geometries.

The correct complexity level selection depends on the user’s skill and experience.With the help of an injection production manager, it was possible to analyse several injected parts

costs ans it was possible to create a table that presents the relation between complexity level andcomplexity factors - table 4.13.

Table 4.13: Complexity Cost factors for injection process

Complexity Level 1 2 3Cost factor 1.00 1.1 1.15

4.4.2 Model Validation

In the same way. it was done in the validation of the economic model of the mould manufacturingprocess, the validation presented next will be done resorting to two case studies. The use of two casestudies instead of one will allow assessing the validity of the complexity factor, for that one plastic partof complexity level 1 and another of complexity level 3 will be used.

32

For confidentiality reasons a total breakdown of the injection costs cannot be presented, but only thefinal cost per sector.

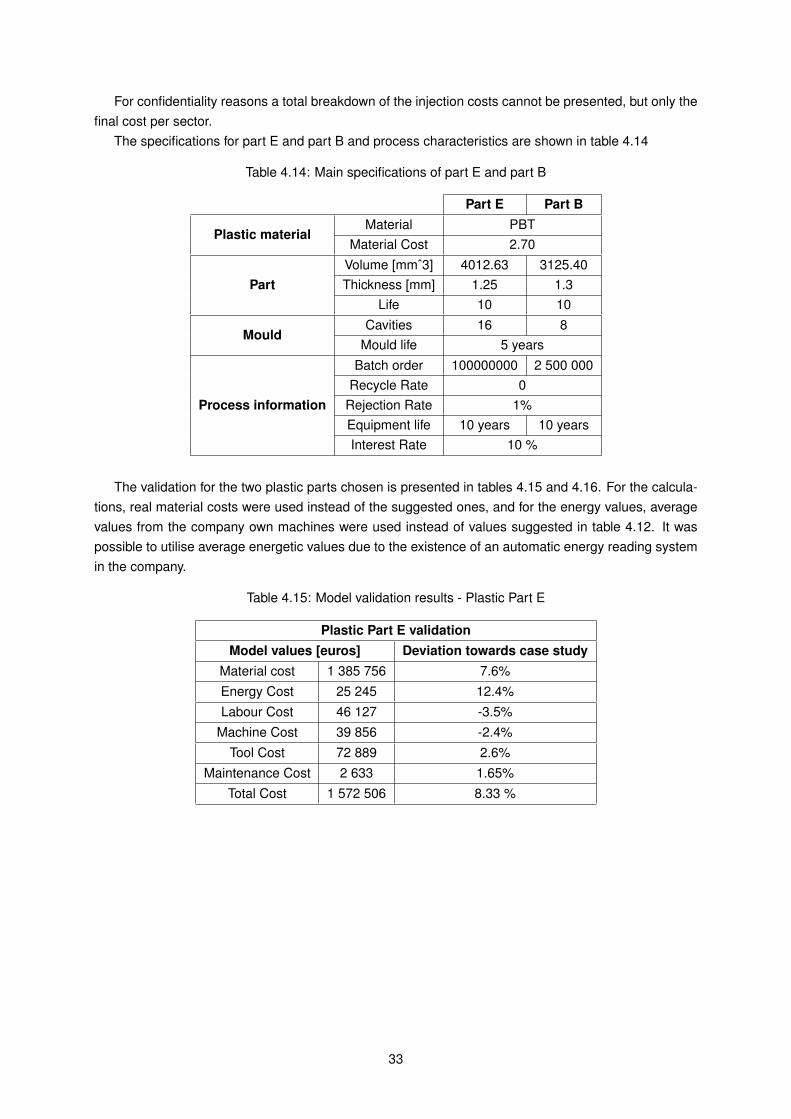

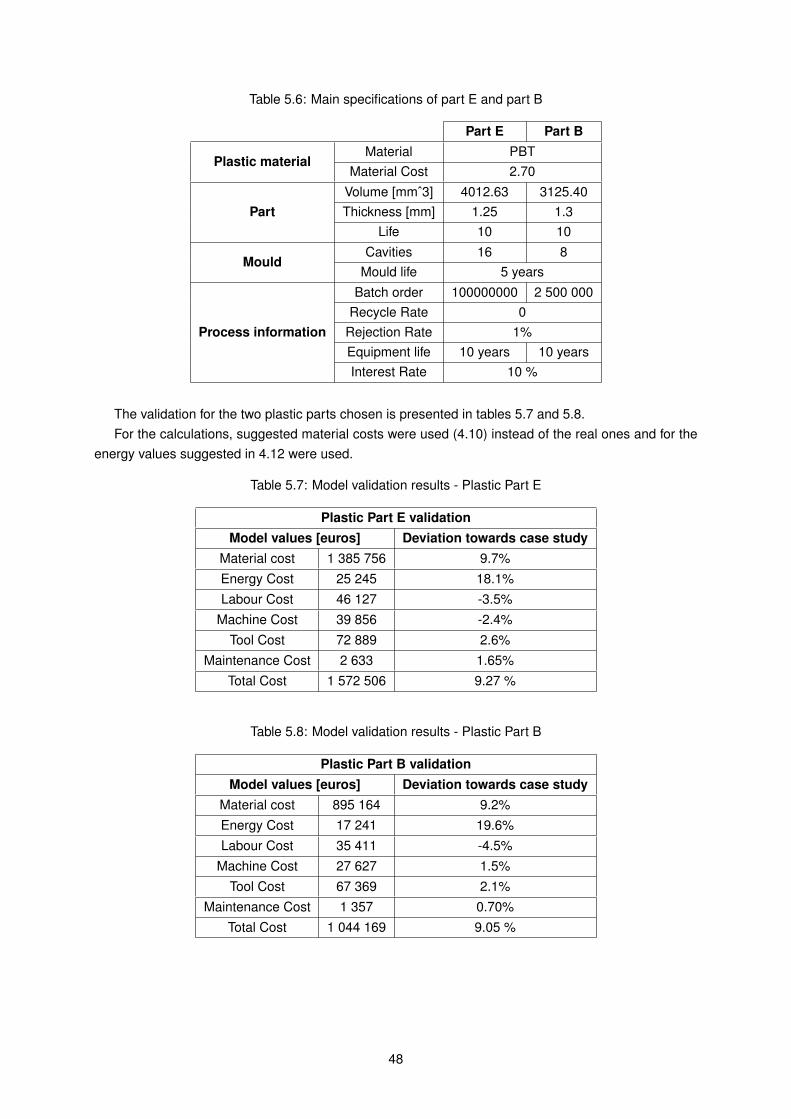

The specifications for part E and part B and process characteristics are shown in table 4.14

Table 4.14: Main specifications of part E and part B

Rejection Rate 1%Equipment life 10 years 10 yearsInterest Rate 10 %

The validation for the two plastic parts chosen is presented in tables 4.15 and 4.16. For the calcula-tions, real material costs were used instead of the suggested ones, and for the energy values, averagevalues from the company own machines were used instead of values suggested in table 4.12. It waspossible to utilise average energetic values due to the existence of an automatic energy reading systemin the company.

Table 4.15: Model validation results - Plastic Part E

Plastic Part E validationModel values [euros] Deviation towards case study

In the last chapter, it was presented the first of the three models covered in this dissertation. This chapterwill address the second model of operationalisation.