Hugh Terry, The Digital Insurer Insurance Industry Asia 2015 –Strategic Priorities for Profitable Growth 2 nd December 2014, Ritz Carlton Hotel, Hong Kong DIGITAL THINKING TO TRANSFORM FACE-TO-FACE INSURANCE IN ASIA

Transcript

Hugh Terry, The Digital Insurer

Insurance Industry Asia 2015 – Strategic Priorities for Profitable Growth

2nd December 2014, Ritz Carlton Hotel, Hong Kong

DIGITAL THINKING TO TRANSFORM FACE-TO-FACE

INSURANCE IN ASIA

Discussion agenda

1Digital trends & the case for change

2 The Digital Advisor – transforming face-to-

face insurance

3Emerging success stories

2

Presentation can be found in the articles/conferences @www.the-digitial-insurer.com

Digital trends and the case for change

3

InsuranceCom Conference: Insurance Industry Asia 2015 – Strategic Priorities for Profitable Growth: 2nd December 2014,

1

The Digital Revolution: “It will not be televised”

DIGITAL

CONVENIENCE

DIGITAL

CONNECTIVITY

DIGITAL

EXPECTATIONS

Always on

Always there

Universal

Almost free

Access to information

(Google)

Access to each other

(Facebook)

Access through

devices (Apple)

Location-agnostic

(cloud services)

Data “on demand”

Desire for clarity

& simplicity

Dialogue not

monologue

Easy to promote a

product .. And

complain

4

Change, Change, Change….

Two digital “Mega” trends: forces beyond our control

Changing consumer behaviour –

they are more demanding and

looking for a different experience

2

Technology is cheaper and easier to

implement than ever – it is the fulcrum

to meet consumer needs, reduce

operating costs and to change your

culture

1

5

66

A different world

A real-time and rapid

fundamental change in the

way we live

Our Digital World in 2014: every 60 seconds we…

Source: blog.Qmee.com

777

3. Less Trust in Financial

Services brands

2. Multi-channel service

1 Research on-line and purchase

anywhere

3 changes in customer behaviour: Transforming our industry

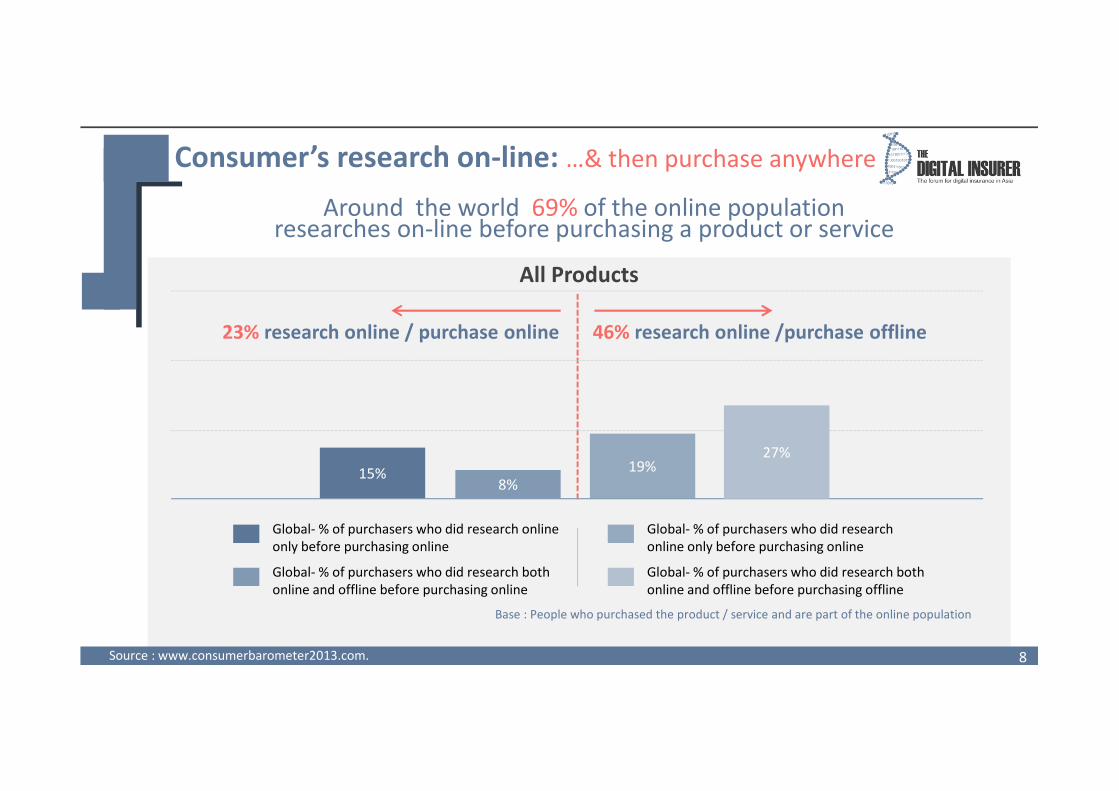

Around the world 69% of the online population researches on-line before purchasing a product or service

15%8%

19%27%

23% research online / purchase online 46% research online /purchase offline

Global- % of purchasers who did research online

only before purchasing online

Global- % of purchasers who did research both

online and offline before purchasing online

Base : People who purchased the product / service and are part of the online population

Global- % of purchasers who did research

online only before purchasing online

Global- % of purchasers who did research both

online and offline before purchasing offline

Consumer’s research on-line: …& then purchase anywhere

All Products

Source : www.consumerbarometer2013.com. 8

9

Welcome to digital customers: “they are multi-channel”

9

Myth #1: Digital is a new distribution channelReality : Digital enables customer (& distributor) engagement

Online

Face To Face

Phone

The multi-channel customer is…

Better informed

More demanding

Uses multiple customer touch

points for both sales & services

Will jump channels at any point –

catch them if you can!

Source : Edelman 2014 Trust barometer

71% would rather go to the dentist than listen to what their banks are saying to them

Source: survey by Viacom

We have a Trust

Challenge

10

Trust is at the heart of financial services: and…

78%69% 67% 64% 64% 61% 59%

55% 55% 52% 49% 48% 48%

32%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

Tech Co.1 Pharma

Co.1

Tech Co.2 Food &

Bev Co.1

Food &

Bev Co.2

Energy

Co.1

Energy

Co.2

Food &

Bev Co.3

Pharma

Co.2

Tech Co.3 Food &

Bev Co.4

Pharma

Co.3

Financial

services

industry

Pharma

Co.4

48%

52% 52%

47%46%

42%

44%

46%

48%

50%

52%

54%

Financial services industry Banks Credit/Payments Insurance Financial advisory/asset

management

3 core strategies

Transform existing face-to-face models

2

Create or participate in new models

3

Manage existing models for profit

1

11

The Digital Advisor: transforming face-to-face selling

12

2

InsuranceCom Conference: Insurance Industry Asia 2015 – Strategic Priorities for Profitable Growth: 2nd December 2014,

Trust is at the

heart of

insurance

Rely on agent relationships

Insurance brand is a hygiene

factor in the sales process

As customer research on-line trust

will need to be developed and

leveraged on-line

Trust must be earned & reinforced at

every interaction/touch point

Great insurance

advisors - always

in demand

Lack of standardization in training, performance management & coachingResult : variable quality of advice and low productivity resulting in high agent turnover, low policy persistency

When customers research online they will research their advisors as well….Less time face-to-face – but no less important (probably more so)Insurance advisors need to be more mobile (digitally & physically)Digital will transform & standardize key management processes

Customer

service matters

Nearly 100% reliant on the

advisor

Back office is … back office

Mobile technology provides

opportunities for cost effective

customer service differentiation

Push based communications can be

used to reconnect with customers

Myth #2: Digital changes the way insurance is soldReality: Digital strategies must incorporate the fundamentals

Current agency paradigm Digital impacts

Back to basics: Digital Advisor strategies need to leverageinsurance fundamentals

13

Customer Portal / App

Policy Systems

Advisor Portal

Lead/Prospect Management

Sales

Opportunities

The Digital Advisor Business Model

Tablet

14

Digital Transformation of face-to face

Digital Opportunities

1. More Leads

2. Better service

3. Better selling

Customer Portal / App

Policy Systems

Advisor Portal

Lead/Prospect Management

Sales

Opportunities

Tablet

Improved selling

3. “connecting the eco system”

15

3

Present credentials (materials)

Identify needs

Produce quotes and help to close

Easy proposal submission

Tablet Functionality: Should be focused on the customer

Must be designed for advisors to connect with

customers

Easy to use with a “wow” factor that encourages

use with clients

Great usability is critical: engage/delight customers

& advisors

Usability is the Key Success Factor

POS Tablet sales toolkits:“business as usual” in most markets within 53 years?

16

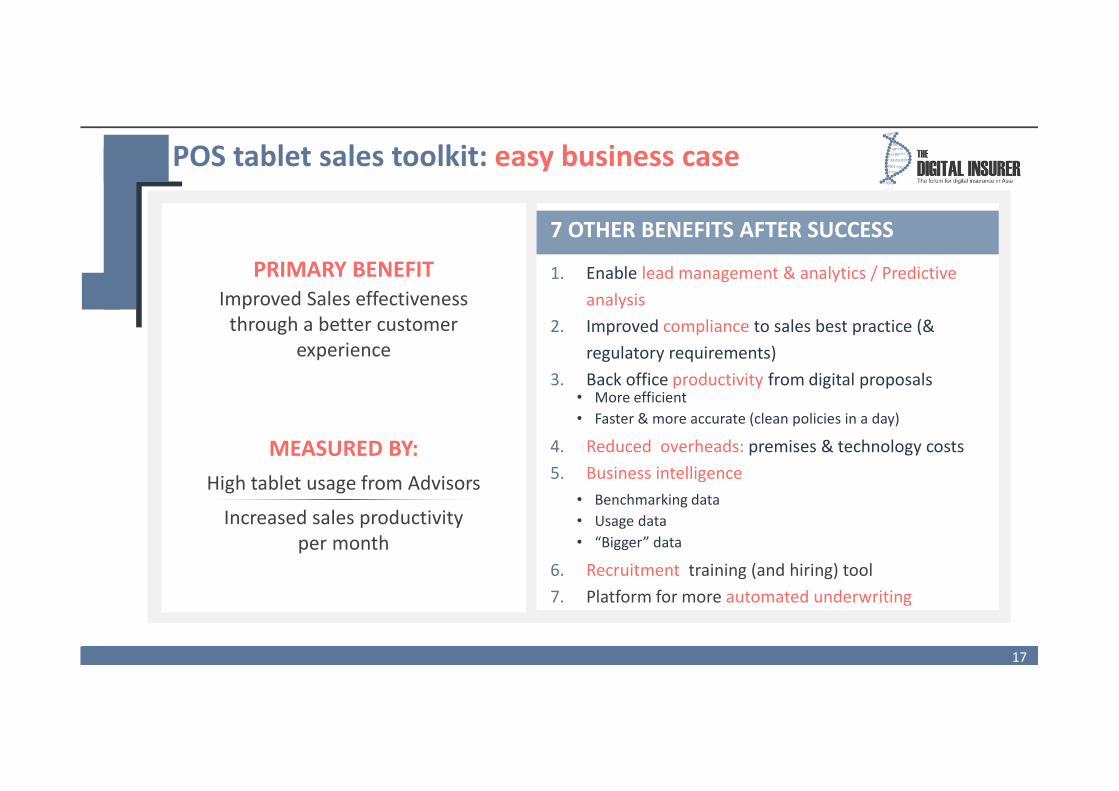

1. Enable lead management & analytics / Predictive

analysis

2. Improved compliance to sales best practice (&

regulatory requirements)

3. Back office productivity from digital proposals

7 OTHER BENEFITS AFTER SUCCESS

POS tablet sales toolkit: easy business case

PRIMARY BENEFIT

Improved Sales effectiveness

through a better customer

experience

MEASURED BY:

High tablet usage from Advisors

Increased sales productivity

per month

• More efficient

• Faster & more accurate (clean policies in a day)

4. Reduced overheads: premises & technology costs

5. Business intelligence

6. Recruitment training (and hiring) tool

7. Platform for more automated underwriting

• Benchmarking data

• Usage data

• “Bigger” data

17

Emerging Success Stories

18

InsuranceCom Conference: Insurance Industry Asia 2015 – Strategic Priorities for Profitable Growth: 2nd December 2014,

3

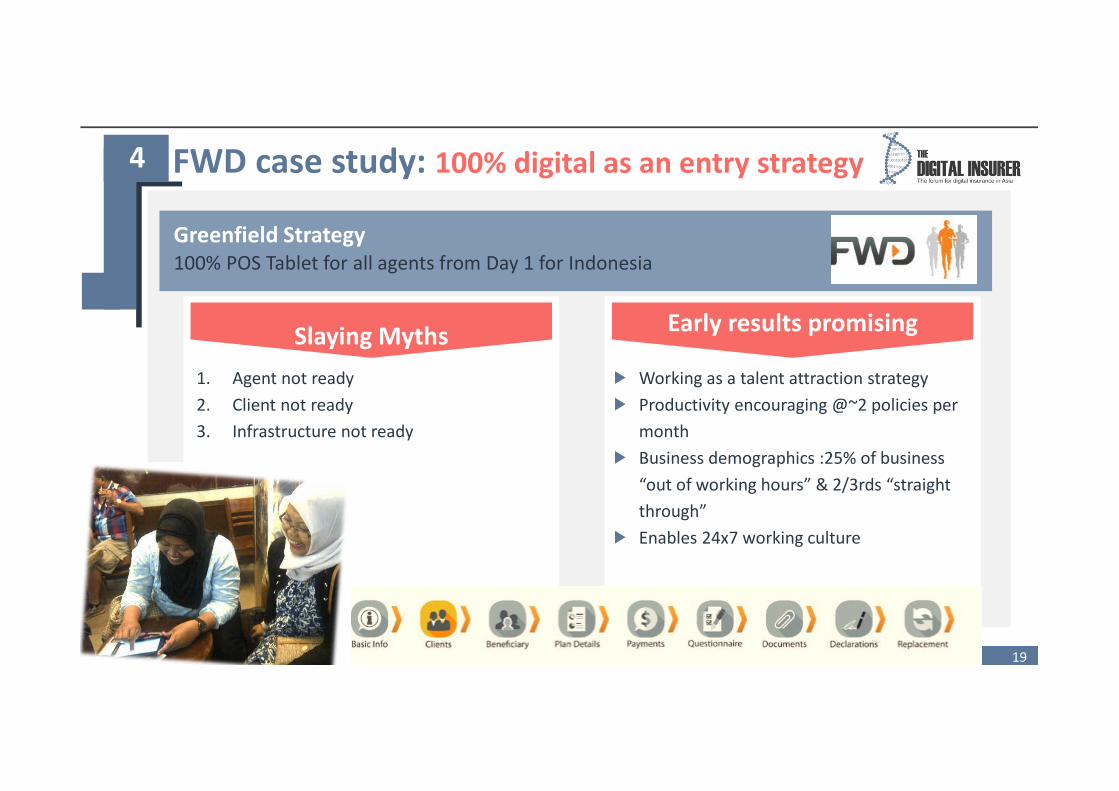

FWD case study: 100% digital as an entry strategy

Slaying Myths

19

4

Early results promising

Greenfield Strategy

100% POS Tablet for all agents from Day 1 for Indonesia

Working as a talent attraction strategy

Productivity encouraging @~2 policies per

month

Business demographics :25% of business

“out of working hours” & 2/3rds “straight

through”

Enables 24x7 working culture

1. Agent not ready

2. Client not ready

3. Infrastructure not ready

2020

FWD case study: a new culture emerges

Real time Training & Supportive Community

On-line Knowledge base with FAQ’s

Support via community forum

“chic, cool and colourful”

AIA case study: iPoS regional digital transformation

21

4 Key differentiators

Off-line model100% availability“Any time, Anywhere”Advisor “digital briefcase”

AIA’s Regional Journey

August 2012: First launch in Singapore Jan 2014: Rollout Across 10 markets completed

2014 first bank partner moves to 100% tablet sales2015 and beyond: Elevate iPoS to a total mobile office

21

3. Interactive, intuitive

2. Native Appon a tablet

� Ease of use

� A new customer experience

� High adoption by advisors

� Independence from internet connection

� Fast and uninterrupted service

� Lightweight device

1. Functionally complete

� Paperless sale, incl. eSignature

� Structured, needs-based sales process

� Straight Through Processing

4. Regionally deployed

� In-house development team in China

� Regional standards with localisation

� Rapid deployment

AIA Case study: Usability = function plus form

22

AIA Case study: benefits

23

Fastturnaround

Agents’productivity

� Complete and pre-validated documentation

� Instant underwriting decision

� Straight Through Processing

� More effective customer meetings,less meetings with one customer

� Enhanced mobility, see more customers� Address multiple needs, higher case size

Customer experience

� Interactive, progressive buying experience

� Explore more options, deeper conversations

� Enhanced customer engagement

242424

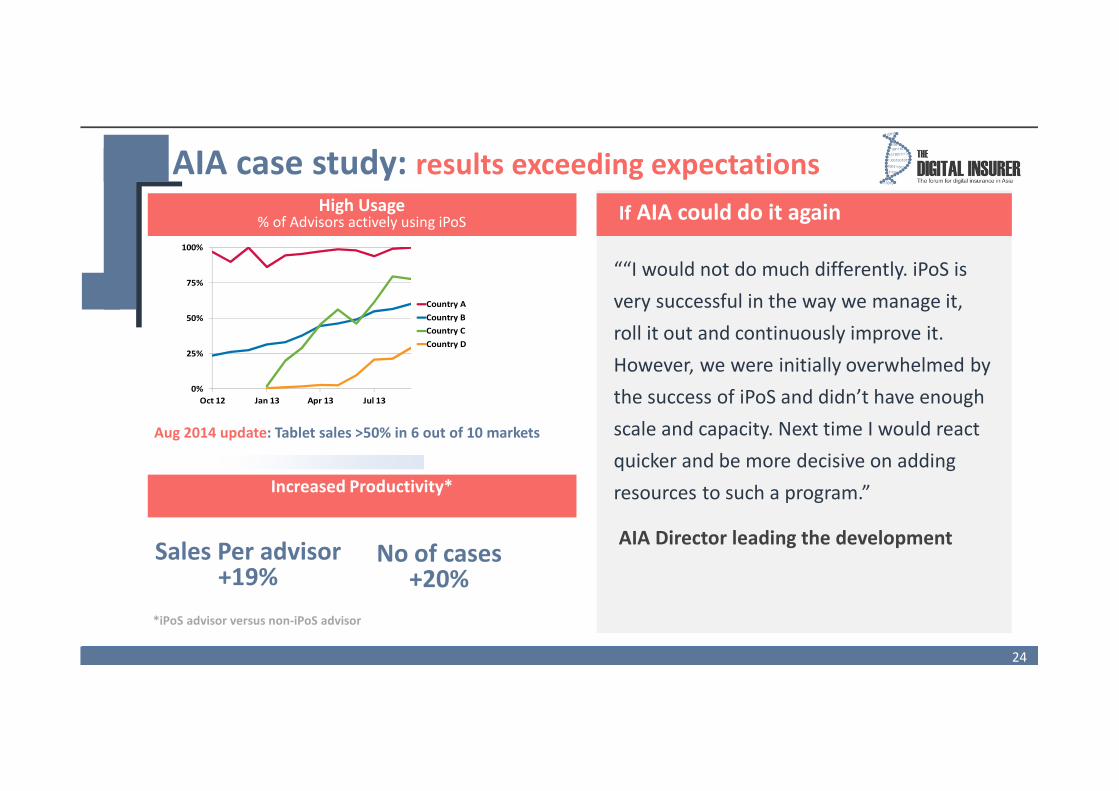

AIA case study: results exceeding expectations

0%

25%

50%

75%

100%

Oct 12 Jan 13 Apr 13 Jul 13

Country A

Country B

Country C

Country D

High Usage% of Advisors actively using iPoS

Increased Productivity*

*iPoS advisor versus non-iPoS advisor

““I would not do much differently. iPoS is

very successful in the way we manage it,

roll it out and continuously improve it.

However, we were initially overwhelmed by

the success of iPoS and didn’t have enough

scale and capacity. Next time I would react

quicker and be more decisive on adding

resources to such a program.”

AIA Director leading the development

If AIA could do it again

Sales Per advisor+19%

No of cases+20%

Aug 2014 update: Tablet sales >50% in 6 out of 10 markets

Leads

50% of leads from digital

engagement activities

Twice as many leads per advisor

Agency KPIs for 2018

The Digital Advisor:where should you be 45 years from now?

Insurance

advisors

At least 2-3 times more

productive

50% fewer advisors

100% tablet usage for all new

advisors – core tool for sales

Customer

service

matters

50% reduction in back office staff

But at least a corresponding

increase in customer facing staff

supporting digital service, sales

and lead processes

Digital will transform

agency operating models

25

26

26

Internal barriers to change ... but the time is now

Source: EY Report - Insurance in a Digital World: the time is now 26

“Digital is a catalyst for dramatic change, one that threatens

rapid transformation of the competitive

landscape and that established insurers are particularly ill-placed to

deal with.”

27

Concluding: “business as usual” is the most dangerous path

Be radical

Now is the time to embrace change and start building digital models.

Be cautious

You don’t need to “bet the bank”. Learn from fast and strategically well thought our pilot

projects. Find people with the skills to transform.

Beware

If you don’t utilise digital thinking, plenty of others will continue to do so.

27

Extra Reading

28

InsuranceCom Conference: Insurance Industry Asia 2015 – Strategic Priorities for Profitable Growth: 2nd December 2014,

29

29Source: Swiss Re Sigma 02/14 29

The cross channel journey ”mono” communication channels going the way of the dinosaur

Online

search

Compare

quotes Browse

reviews

Targeted

advert

Receive quote Check with

friends

Buy online

Text/email

confirmation

Online customer

surveyFill out on-line

claim requestPost rating and

review

Tweet

reviewLike

Renewal

notification

Tweet

review

Referrals to

family/friends

Follow-up call

Buy through

agent

Approach

agent

Product

related call

Request further

information

Report claim

Gather

InformationSeek advise Purchase policy

After sales

serviceMake claim

Internet

Mobile

Social media

Agent/broker

Call center

Retail

branch/bank

Note: The red line shows an example buying journey initiated by a mobile advert, and the blue line a purchase experience via

online search.

30

30

Insurance Consumer trends:

Source: EY Global Customer Insurance Survey 2014 30

Customer centricity as a strategic imperative

31

31

Insurance Consumer trends:

Source: EY Global Customer Insurance Survey 2014 31

trust seems to be a particular issue in Asia

In Asia we see the largest

Trust gap between bank

and insurers (92-70= 22%)

Customer Portal / App

Policy Systems

Advisor Portal

Lead/Prospect Management

Sales

Opportunities

The Digital Advisor Business Model

Tablet

32

Digital Transformation of face-to face

Digital Opportunities

1. More Leads

2. Better service

3. Better selling

Lead/Prospect Management

Sales

Opportunities

More leads

Managing the sales funnel

Co-partnership models for lead generation

Apps to generate leads from the “digital cafes”

Analytics has an enormous role to play

Get the lead to the right person at the right

time

Lead management systems to manage multiple

leads , measure ROI and promote better

practices

Digital Marketing offer engines

Business outcome:• More leads

• Better quality leads

1

33

Better customer service

Customer portal/app: An on-line marketing capability for

customer engagement leading to cross sell / up

sell opportunities

1

Build a digital “eco-system” around legacy policy systems to treat customers like customers

2 Customer experience centre: Multi channel customer

support to connect customer interactions – a digitally

assisted customer service revolution (the engine room for

converting “data into business”)

3 Advisor portal: Customer data and advisor performance

at your finger tips

Business outcome:Building deeper, richer and better relationships with

customers and advisors

Facilitate and co-partners the advisors to better

meet customer needs

Allow “farming” as well as “hunting”

Customer Portal / App

Customer Experience Centre

Policy Systems

Advisor Portal

34

Tablet

2

Customer Portal / App

Policy Systems

Advisor Portal

Lead/Prospect Management

Sales

Opportunities

Tablet

Improved selling

3. “connecting the eco system”

35

3

Digital Advisor model Reprised: designed for the multi-channel customer

Online

Multi-Device

Access

“Digitally enhanced”

Insurance

Advisors

Customer Experience

Centre

Face

To

Face

Phone

DIG

ITA

L C

US

TO

ME

R

EN

GA

GE

ME

NT

Customer Portal/App

Self - Service

Referrals

Corporate Website

Direct purchase

Support Requests

Digital eco-system

Engaging content

Research tools

DIG

ITA

L

AD

VIS

OR

S

Customer Facing : Tablet POS Toolkit

Sales Intro & Fact Find

Quote & application

Internal : Advisor Portal

Performance & compensation

Customer data & e-comms

DIG

ITA

L

CU

ST

OM

ER

SE

RV

ICE

Multi-access customer experience centre

Voice/chat/text queries & escalation

Direct Sales : content & calls

Analytics engine room

Lead engine roomSales / Service

Opportunities

36

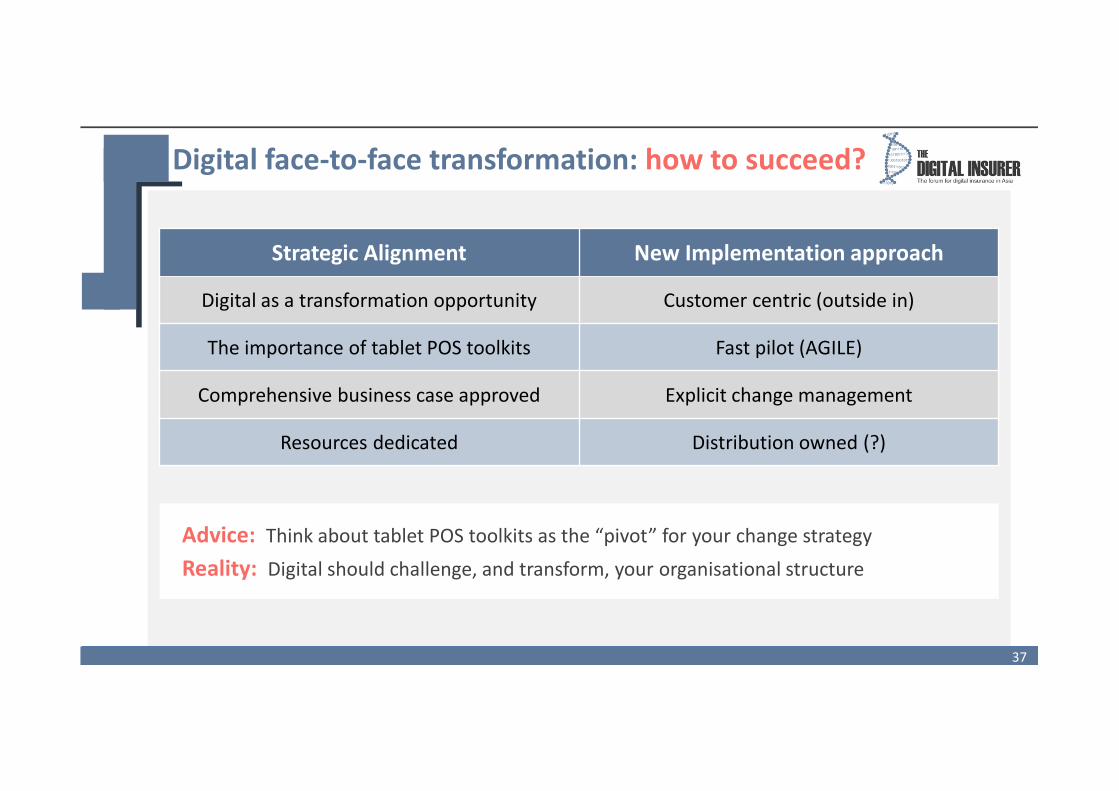

Digital face-to-face transformation: how to succeed?

Strategic Alignment New Implementation approach

Digital as a transformation opportunity Customer centric (outside in)

The importance of tablet POS toolkits Fast pilot (AGILE)

Comprehensive business case approved Explicit change management

Resources dedicated Distribution owned (?)

Advice: Think about tablet POS toolkits as the “pivot” for your change strategy

Reality: Digital should challenge, and transform, your organisational structure

37

Would a new insurer establish a distribution centric model?

Agency Channel

Incumbents have scale

Operations are complex and inefficient

Models don’t deliver value to the consumer on the investment component

Part-time sellers – very hard to manage

Low productivity

Product range is too narrow

BancassuranceHas a lot of advantages but….

Banks have consistently chosen $$ over customer centricity

Lacks the personal touch on servicing

Technology hard to deploy in banking environment

Agency is a cash cow that needs renewal

Bancassurance is an increasingly expensive game – and banking is going digital

Existing models are ripe for disruption:

A personal view for life insurance industry In Asia

38

There are untapped opportunities

Seriously shopped but didn’t buy life

insurance (10%)

Didn't shop for life insurance (78%)

Seriously shopped and bought life insurance

(12%)

Figure 6

Buyers and non-buyers of life insurance, US households(%), 2011

Can digital Strategies change the paradigm that “life

insurance is sold not bought”?

Source : To Buy not to buy life insurance, LIMRA 2011

Extracted from Swiss Re Sigma 06/13

39

78%

12%

10%

7 operating models for Asia: breaking down the value chain

40

Acquire New Customers Selling to Customers Servicing Customers Taking Product Risk

2. Bancassurance InsurerBank

1. Traditional Agency Insurer

3. Digital / Direct Insurer

4. Digital Managing Agents Single Insurer

5. Price Comparison Sites Multiple Insurers

6. Digital IFA Multiple Insurers

7. Digital Affinity Marketing Co. OR

Brand Financial Service Co e.g. TESCO BankMultiple ProvidersAffinity Partner

NO

WE

ME

RG

ING

IN

AS

IA

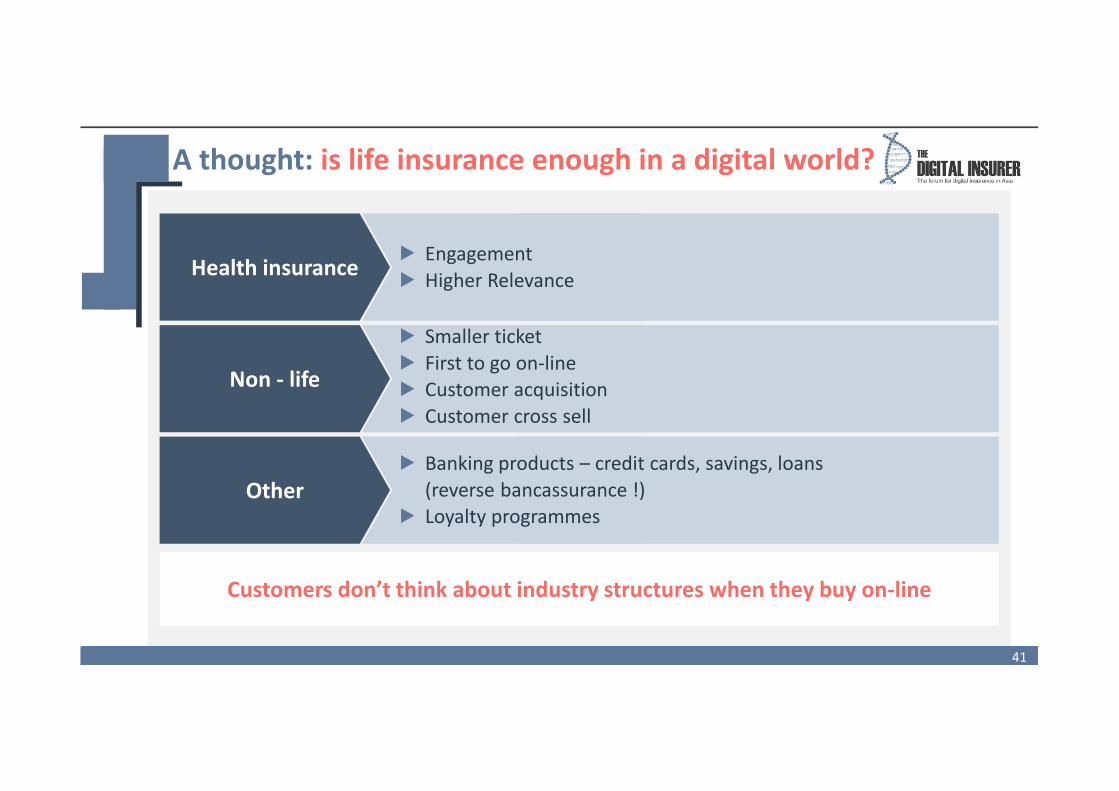

Health insuranceEngagement

Higher Relevance

A thought: is life insurance enough in a digital world?

Non - life

Smaller ticket

First to go on-line

Customer acquisition

Customer cross sell

Other

Banking products – credit cards, savings, loans

(reverse bancassurance !)

Loyalty programmes

Customers don’t think about industry structures when they buy on-line

41

The trend to

choice

Digital = customer centricity

The educated consumer

The world of “more perfect” information

How can insurers

react?

Be the best choice

Buy choice based models

Manage choice

Defend existing models

Do we think we can deny customer choice ?

Do we think we can deliver poor value products?

42

Another thought: embrace customer choice or baton down the hatches?

![Origins of Life Biblical and Evolutionary models face off ... · 2000), 91.] [Hugh Ross. Origins of Life: Biblical and Evolutionary Models Face Off (Kindle Locations 401-405). RTB](https://static.documents.pub/doc/80x56/600c8ae16bf0ec3f4024c5d8/origins-of-life-biblical-and-evolutionary-models-face-off-2000-91-hugh.jpg)