Video Games in the Cloud A disintermediated video game industry M15275IN2A – June 2015 – Report Synopsis Digital Entertainment This document is a part of our "Digital Entertainment" category which includes in 2015: - two datasets in Excel, - a state-of-the-art report in PowerPoint, - four market reports in Word, each with its synopsis in PowerPoint - Privileged access to our lead Media analysts

Transcript

Video Games in the Cloud

A disintermediated video game industry

M15275IN2A – June 2015 – Report Synopsis

Digital Entertainment

This document is a part of our "Digital Entertainment" category which includes in 2015:

- two datasets in Excel,

- a state-of-the-art report in PowerPoint,

- four market reports in Word, each with its synopsis in PowerPoint

Dematerialisation affects all segments of the video game industry.

It affects distribution and in-game consumption patterns.

It has led to disintermediation in the value chain and raises questions over the role of certain stakeholders downstream.

As a result, 'online' has ultimately eroded a silo-based industry structure and allowed practices and cross-platform services to emerge that both benefit

gamers and boost creativity within the sector.

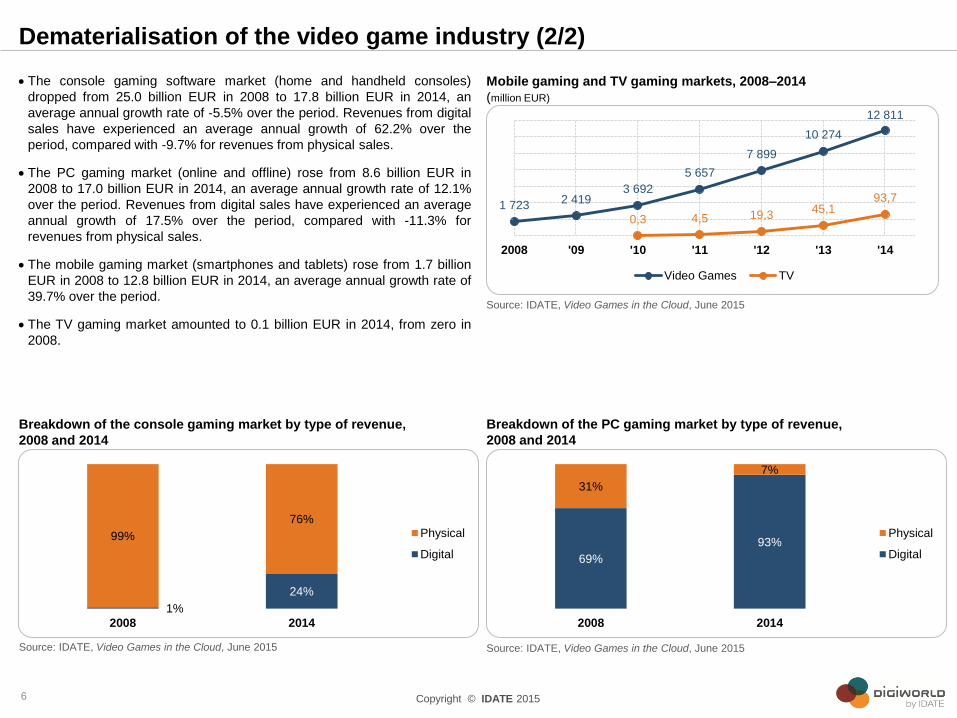

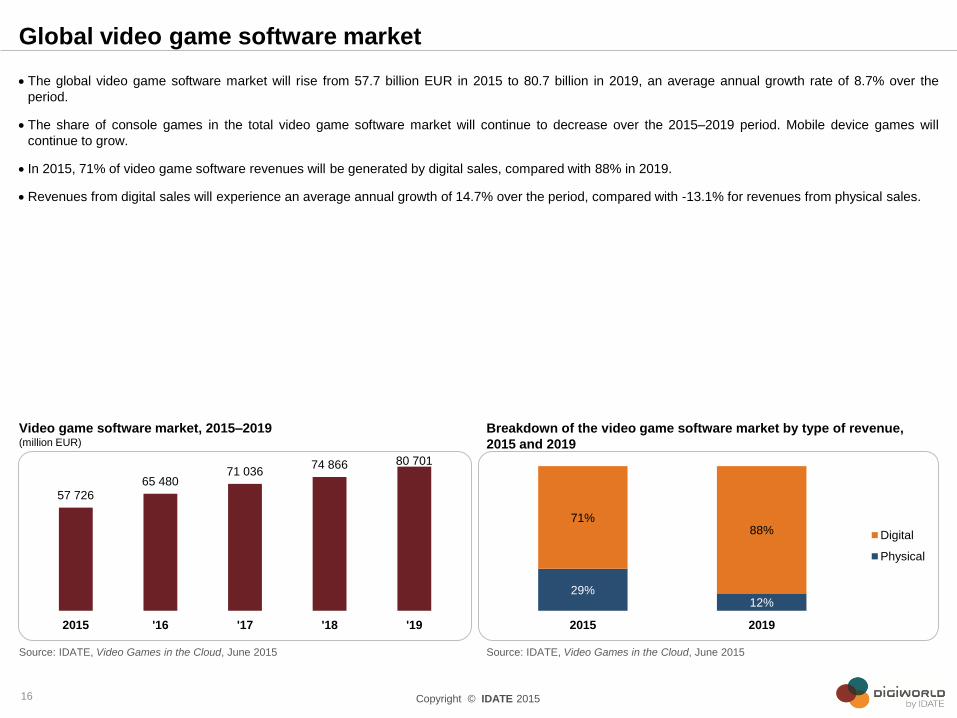

The video game market has risen from 35.3 billion EUR in 2008 to 47.7 billion EUR in 2014.

Dematerialisation has meant an increasing number of consumers can be reached, on any platform equipped with a screen, fixed or mobile, and with

increasingly varied content.

In 2014, 69% of video game software revenues were generated by digital sales and distribution, compared with 22% in 2008.

Source: IDATE, Video Games in the Cloud, June 2015

Breakdown of the video game software market by type of revenue, 2008

and 2014

Dematerialisation of the video game industry (1/2)

5

Source: IDATE, Video Games in the Cloud, June 2015

Video game software market, 2008–2014 (million EUR)

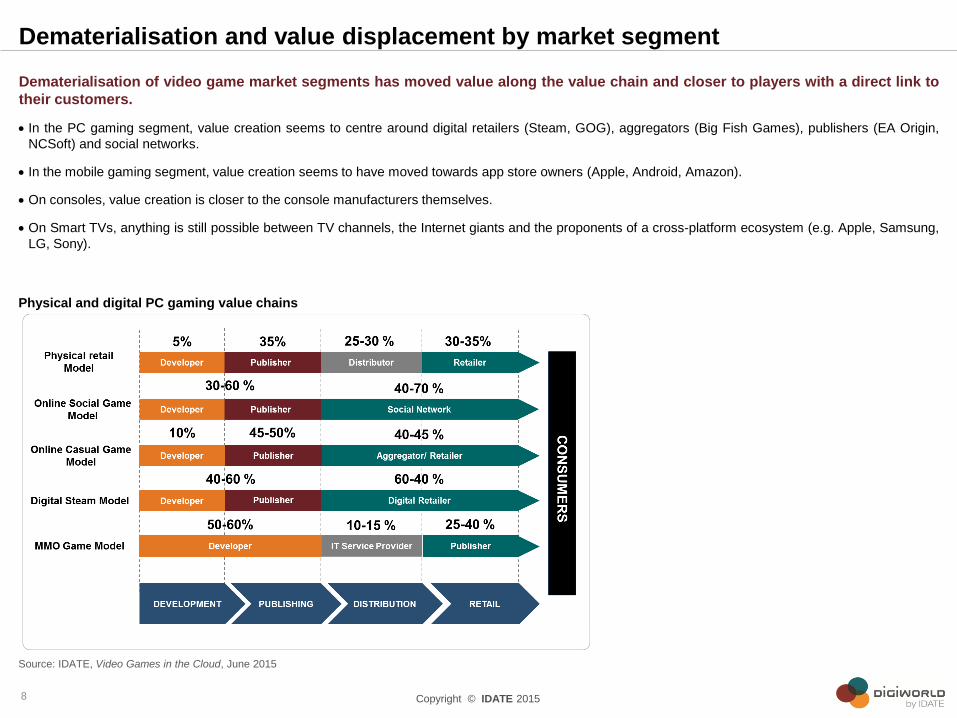

Dematerialisation and value displacement by market segment

Dematerialisation of video game market segments has moved value along the value chain and closer to players with a direct link to

their customers.

In the PC gaming segment, value creation seems to centre around digital retailers (Steam, GOG), aggregators (Big Fish Games), publishers (EA Origin,

NCSoft) and social networks.

In the mobile gaming segment, value creation seems to have moved towards app store owners (Apple, Android, Amazon).

On consoles, value creation is closer to the console manufacturers themselves.

On Smart TVs, anything is still possible between TV channels, the Internet giants and the proponents of a cross-platform ecosystem (e.g. Apple, Samsung,

LG, Sony).

Source: IDATE, Video Games in the Cloud, June 2015

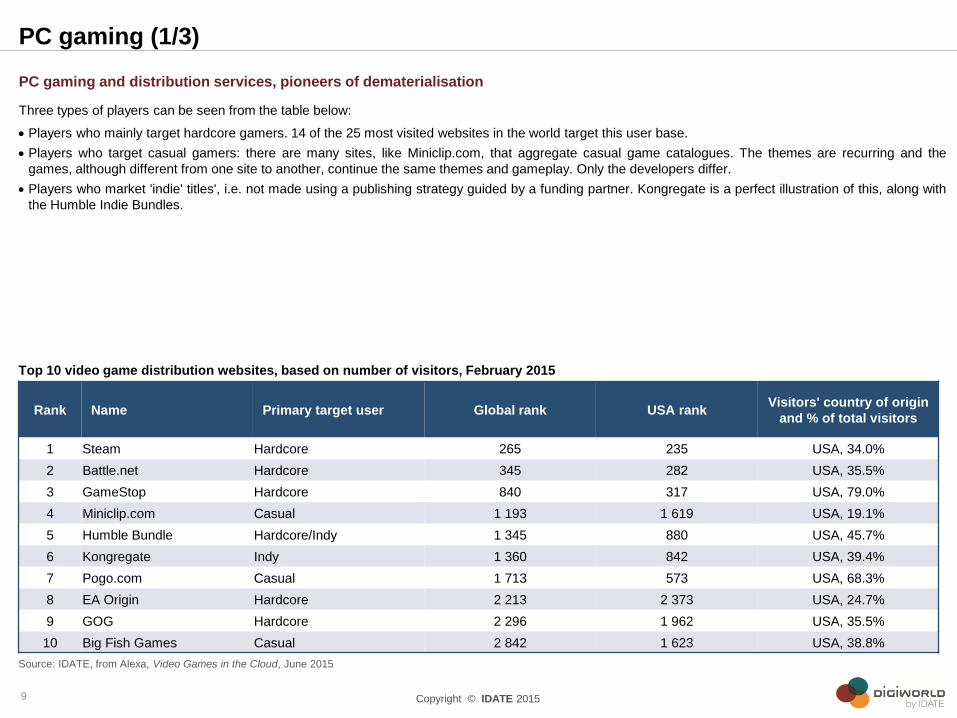

PC gaming and distribution services, pioneers of dematerialisation

Three types of players can be seen from the table below:

Players who mainly target hardcore gamers. 14 of the 25 most visited websites in the world target this user base.

Players who target casual gamers: there are many sites, like Miniclip.com, that aggregate casual game catalogues. The themes are recurring and the

games, although different from one site to another, continue the same themes and gameplay. Only the developers differ.

Players who market 'indie' titles', i.e. not made using a publishing strategy guided by a funding partner. Kongregate is a perfect illustration of this, along with

the Humble Indie Bundles.

Source: IDATE, from Alexa, Video Games in the Cloud, June 2015

Top 10 video game distribution websites, based on number of visitors, February 2015

Rank Name Primary target user Global rank USA rank Visitors' country of origin

and % of total visitors

1 Steam Hardcore 265 235 USA, 34.0%

2 Battle.net Hardcore 345 282 USA, 35.5%

3 GameStop Hardcore 840 317 USA, 79.0%

4 Miniclip.com Casual 1 193 1 619 USA, 19.1%

5 Humble Bundle Hardcore/Indy 1 345 880 USA, 45.7%

Massively multiplayer games (MM) are a very dynamic market segment. According to IDATE, revenues are estimated at nearly 8 billion EUR by late 2015,

45% of the online gaming segment, which itself is composed of social games (38% of online gaming revenue) and casual games (17% of online gaming

revenue).

The MM gaming market segment has seen three major changes in recent years.

- This segment has shifted significantly towards a Free-to-Play model over the last three years In the western hemisphere, World of Warcraft (Activision-

Blizzard) is essentially the only remaining MM game still to be based on a subscription.

- Most MM games use digital distribution. With its flagship title, even Blizzard has switched to this method of distribution.

- MM games have come to mobile platforms.

Asia occupies a unique place in the PC MMO landscape. Seven of the Top 10 games come from Chinese and South Korean companies. As a result, the

Chinese Web giant Tencent has become the world leader in the industry.

Breakdown of online video game revenues by type of game, 2015

Source: IDATE, Video Games in the Cloud, June 2015

12%

33%

17%

38%

Online… Premium Massively Multiplayer Free Massively Multiplayer Casual Social … Video Game Market

Most of the games available on social platforms are also available on smartphones and tablets.

Mobile gaming and social networks complement each other well. This can be explained by three common elements which, when combined, produce a viral

effect not seen in other market segments in this sector:

- Platform virality: app stores are as viral as Facebook.

- The sheer number of potential users: there are hundreds of millions of users that can be quickly mobilised and can converge on the same app in a very

short space of time.

- The lightning speed of information: with so many users, information is transmitted extremely quickly.

Top 10 Facebook games based on million MAU (Monthly Average Users), April 2015

* only Facebook page

Source: IDATE, from Appdata, Video Games in the Cloud, June 2015

Rank Game Platform Publisher Nb. Active gamers/ month

The spread of smartphones has reduced the importance of telecom operators and content aggregators in the distribution of games.

Phone manufacturers' app stores have become an essential intermediary between the game developer/publisher and the consumer.

Mobile operators are trying to preserve their market share in games distribution, but seem to be refocusing on their core business, i.e. providing the 'pipes'

to deliver content.

Manufacturers' app stores also fulfil publishing and marketing roles. A developer is now able to directly access the market without going through a

publisher. However, the traditional developer–publisher model still remains.

Revenue distribution has been dictated by Apple's strategy of attracting content creators to create a large and varied catalogue of titles. 70% of revenues

are captured by the developers and publishers, and 30% to the app store.

Source: IDATE, Video Games in the Cloud, June 2015

Mobile gaming revenue distribution, 2008 and 2015 (%)

Mobile gaming (1/2)

13

Source: IDATE, Video Games in the Cloud, June 2015

An underlying trend, the huge popularity of Free-to-Play

According to Statista, 92% of iOS games were Free-to-Play in 2014.

According to Distimo, in January 2014, revenues generated by Free-to-Play apps accounted for 79% of revenues generated on the Apple Store, compared

with 46% two years earlier.

Increasing number of ubiquitous games

Most successful mobile games in the Top 20 in 2014 were ubiquitous between the tablet and smartphone. Lower barriers to entry in the mobile gaming

segment has led to a very large supply of games on the market. Both Apple's App Store and Google Play have some 200,000 game titles available. Ubiquity

is certainly a differentiating factor.

The mobile gaming segment was behind a massive and unprecedented phenomenon driven by hugely successful games from

SuperCell, GungHo Online Entertainment, King.com and Kabam.

For example, Puzzle and Dragons from GungHo Online Entertainment generated 4.5 million USD per day during the first nine months of 2014, with an ARPU

greater than 10 USD.

Increased competition from smartphones and tablets is seriously harming the handheld console gaming business. Three elements

could change this situation:

developing the stand-alone connection of handheld consoles

enhancing the online features of these devices, which are now below the expectations of users compared with what smartphones and tablets offer

incorporating Free-to-Play games on handheld consoles

Global mobile gaming sector revenue growth, 2000–2014 (billion EUR)

Source: IDATE, Video Games in the Cloud, June 2015

From global video game market values, we can recreate revenues along the value chain year by year, from the developer and retailer to the various

intermediaries, according to the market segment.

With increasing rates of dematerialisation, which affects each link in the chain positively or negatively, we see that the benefits of this value redistribution

are felt higher up the chain, mainly by developers. Over the 2008–2019 period, this share will gain more than 20 points, from 5% to 26%.

The other link in the value chain to benefit from dematerialisation is retail sales. However, the players have changed. In 2008, retail sales consisted of

physical retailers. These days, although these same retailers have sometimes ridden the wave of dematerialisation by offering digital distribution (e.g.

Gamestop), the retail role is now dominated by digital distribution pure players, such as Apple, Amazon, Google and Steam.

Although the publishing link still captures the largest share of the sector's revenues over the period, retailers will catch up to it in terms of value and relative

share in 2019 as they increasingly benefit from the direct relationship with gamers/customers.

Publishers benefit from cyclical growth in the market, but their share of total revenues in the sector will gradually be reduced as developers take over more

publishing tasks.

Source: IDATE, Video Games in the Cloud, June 2015

Revenues earned by the various links in the video game market value

chain (%)

Impact of dematerialisation on value distribution

17

Source: IDATE, Video Games in the Cloud, June 2015

Revenues earned by the various links in the video game market value