116

INUED) ANNUAL REPORT 2012

COCA-COLA AMATIL LIMITED ANNUAL REPORT 2012 01

Directors’ report (continueD)COCA-COLA AMATIL LIMITEDFOR THE FINANCIAL YEAR ENDED 31 DECEMBER 2012 annuaL report

2012

co

ca

-co

La

aM

at

iL L

iMit

eD

an

nu

aL

re

po

rt

20

12

Coca-Cola Amatil limitedABN 26 004 139 397www.ccamatil.com

COCA-COLA AMATIL LIMITED ANNUAL REPORT 2012 001

Directors’ report (continueD)COCA-COLA AMATIL LIMITEDFOR THE FINANCIAL YEAR ENDED 31 DECEMBER 2012

contents

Chairman’s Review 1

Managing Director’s Review 2

Financial Commentary 4

Board of Directors 5

Senior Management 7

Corporate Governance Statement 8

Financial and Statutory Reports 15

Directors’ Report 15

Financial Report 45

Income Statement 45

Statement of Comprehensive Income 46

Statement of Financial Position 47

Statement of Cash Flows 48

Statement of Changes in Equity 49

Notes to the Financial Statements 50

1. SummaryofSignificantAccountingPolicies 50

2. Segment Reporting 57

3. Revenue 59

4. Income Statement Disclosures 59

5. Income Tax Expense 61

6. Cash and Cash Equivalents 62

7. Trade and Other Receivables 63

8. Inventories 64

9. Other Financial Assets 64

10. Investment in Joint Venture Entity 65

11. Investments in Bottlers’ Agreements 65

12. Property, Plant and Equipment 66

13. Intangible Assets 67

14. Impairment Testing of Investments in 68 Bottlers’ Agreements and Intangible Assets withIndefiniteLives

15. Trade and Other Payables 70

16. Interest Bearing Liabilities 71

17. Provisions 72

18. Deferred Tax Liabilities 73

19.DefinedBenefitSuperannuationPlans 74

20. Share Capital 77

21. Shares Held by Equity Compensation Plans 77

22. Reserves 78

23. Employee Ownership Plans 79

24. Dividends 82

25. Earnings Per Share (EPS) 82

26. Commitments 83

27. Contingencies 83

28. Auditors’ Remuneration 83

29. Business Combinations 84

30. Key Management Personnel Disclosures 85

31. Derivatives and Net Debt Reconciliation 88

32. Capital and Financial Risk Management 89

33. Related Parties 101

34. CCA Entity Disclosures 102

35. Deed of Cross Guarantee 103

36. Investments in Subsidiaries 104

37. Events After the Balance Date 105

Directors’ Declaration 106

Independent Auditor’s Report 107

Shareholder Information 108

Company Directories 110

Share Registry and Other Enquiries 110

Calendar of Events 2013 111

AnnuAl GEnERAl MEEtInG

the Annual General Meeting will be held on tuesday, 7th May 2013 at 10am in the James Cook Ballroom, InterContinental Sydney, cnr Bridge and Philip Streets, Sydney, nSW.

COCA-COlA AMAtIl lIMItED ABn 26 004 139 397

COCA-COLA AMATIL LIMITED ANNUAL REPORT 20121

chairMan’s review

Coca-Cola Amatil (CCA) reported net profi t after tax of $558.4 million and before signifi cant items, an increase of 5.0% on the 2011 full year result. the increase in earnings and strong cash fl ow generation has once again supported an increase in dividends.

CCA’srecord2012profitresultwasdrivenbystrongperformancesfromthe Indonesian & PNG business and the Australian beverage operations with disappointing performances from New Zealand and SPC Ardmona. The ongoing impact of the high Australian dollar on the competitiveness of SPC Ardmona has led to a write-down of assets and goodwill in the businesswhichwasrecognisedasasignificantitemintheaccounts.

Afterincludingtheimpactofsignificantitems,reportednetprofitaftertaxdeclinedby22.3%,withanetsignificantwrite-downof$98.5millionthisyearcyclinga$59.8millionsignificantgainin2011.

StROnG CASH FlOW & BAlAnCE SHEEt

Cashflowgenerationforthebusinesscontinuestoimprove.Operatingcashflowbeforesignificantitemsincreasedby$128.1millionto$794.3millionandwassufficienttofullyfundCCA’s2012dividendpaymentsandthesignificantinvestmentsmadeinourbusiness during the year. The balance sheet continues to be very strong, with interest cover increasing from 6.8 times to 8.0 times for the year beforesignificantitemswiththerefinancingofallmaturingdebtuptolate 2014 completed by January 2013.

tOtAl DIVIDEnDS uP 13.3% FOR 2012

Solid earnings growth, strengthening of the balance sheet and strong cashflowgenerationhassupportedthe6.7%increaseinfullyearordinarydividends.Thefinaldividendof32.5centsfortheyearwasfranked to 75% and a special unfranked dividend of 3.5 cents per share hasbeendeclaredtobroadlysupplementthefinancialimpactofthelessthan100%frankedfinaldividend,takingfullyeardividendstoshareholders to 59.5 cents per share, an increase of 13.3%.

The dividend payout ratio for full year ordinary dividends has increased from 74.9% to 76.4%. Given the continued strength of the balance sheet andfinancialratios,wewouldexpecttotargetthedividendpayoutratioto the middle of our 70-80% target payout level for 2013.

OuR EMPlOYEES

The 2012 results arose in major part from the quality of our people and their passion for servicing our customers. On behalf of the Board, I congratulate and thank all of CCA’s employees for their special efforts and contributions in 2012.

CORPORAtE GOVERnAnCE

CCA has an ongoing commitment to transparency and best practice corporategovernanceandcontinuestorefineitspracticesinthisarea. The diversity strategy, which is detailed on page 12, centres on attraction, inclusion and retention of a diverse range of talent and has resulted in a marked progress towards achievement of our gender diversity and indigenous employment targets. The belief that a truly diverse culture not only drives better business outcomes but enables innovation and change, is led from the top of the organisation and embraced by all employees.

CCA’S RElAtIOnSHIP WItH tHE COCA-COlA COMPAnYThe CCA Board continues to have a strong and constructive relationship with The Coca-Cola Company (TCCC), both as a shareholder and as the major supplier of ingredients for the majority of our non-alcoholic beverage products. As at 31 December 2012, TCCC held 29.3% of the shares in CCA and nominates two Non-Executive Directors to the current nine-member Board.

In 2012, CCA’s Related Party Committee, comprising the Independent Non-Executive Directors, met on seven occasions and reviewed all material transactions between CCA and TCCC ensuring that they are all at arm’s length. The Related Party Committee remains an important forum for dealing with all related party governance issues.

CORPORAtE SOCIAl RESPOnSIBIlItY

CCA believes in and strongly supports social and environmental activities through its community and environmental programs. These programs help to sustain business performance by strengthening the communities inwhichtheCompanyoperates,improvingbusinessefficiencyand developing strong relationships with stakeholders, ultimately leading to increased shareholder returns. CCA’s sustainability report, “Sustainability@CCA”, measures the Company’s achievements under four pillars – Environment, Marketplace, Workplace and Community.

I encourage you to read this report which is available on our website, www.ccamatil.com.

COnCluSIOn

CCA has delivered another excellent result in what was a challenging year for the business. The Board thanks all of the Group’s stakeholders in assisting CCA in this success.

David M. Gonski, AC Chairman

COCA-COLA AMATIL LIMITED ANNUAL REPORT 2012 2

Managing Director’s review

OVERVIEW

CCA has delivered another excellent result with 5.0% growth in net profitto$558.4million(beforesignificantitems).Thestandoutperformerwas once again Indonesia & PNG with double-digit volume and earnings growth while Australia delivered solid volume and earnings growth and increasedmarketsharedespiteadifficulttradingenvironment.Earningsgrowth was moderated by disappointing performances from New Zealand and SPC Ardmona.

Material progress has been made in developing the alcoholic beverages platform for growth in anticipation of our re-entry into the Australian beer market in December 2013, and with the multi-year investment in developing the manufacturing and technology platform nearing completion,thebusinesshascommencedamajoroperationalefficiencyprogrammetotarget$30-40millionofadditionalannualefficiency gains and cost out initiatives to be delivered progressively over the next three years.

REVIEW OF OPERAtIOnS

Australia

VolumeandEBIT(earningsbeforeinterest,taxandsignificantitems)growth of 3.3% was delivered against the backdrop of a weak consumer spendingenvironmentandverypoorweatherinthefirstquarter.Despite sustained aggressive competitor discounting in the second half, market share increased in sparkling beverages and EBIT margins were maintained above 20%.

Coke Zero was the standout performer with volumes growing by 12%. Mount Franklin grew strongly driven by successful promotional programs supporting the McGrath foundation while the launch of the colourful Jennifer Hawkins’ “Cozi” range grew lightly sparkling volumes by over 50%. The launch of Powerade Zero drove volume growth of around 5% in sports drinks, while the Grinders coffee business also delivered solid volume growth.

new Zealand & Fiji

The New Zealand business delivered a disappointing result with a decline in volume and earnings. The business experienced a very poor start to 2012 as New Zealand recorded one of the coolest and wettest summers onrecordandtheeconomyandconsumerconfidenceremainedverysoftthroughout the year.

The energy category has continued to grow in New Zealand, with Mother growing volumes by over 5.0% driven by the successful “Mother made me do it” campaign and the Grinders coffee business also continued to grow driven by the expansion of its customer base.

Indonesia & PnG

The volume increase of 10.3% and EBIT growth of 16.8% was driven by increased demand for commercial ready-to-drink beverages, brand and package innovation and the continued strong growth of Minute Maid Pulpy juice and sparkling beverages.

In Indonesia, all of our major brands performed well, with highlights including the strong growth in trademark Coca-Cola brands (Coke, Sprite and Fanta) and Frestea. There were a number of new product launches including Minute Maid Pulpy Lemon and Burn Energy Drink, as well as new packaging launches in the fast-growing tea and juice categories.

In2012,thebusinessmadesignificantinvestmentsinproductioncapacityto support the ongoing growth of the business and in anticipation of a substantial new product and package pipeline for 2013.

COCA-COLA AMATIL LIMITED ANNUAL REPORT 20123

Alcohol, Food & Services

Alcohol,Food&Servicesearningsincreasedby2.0%beforesignificantitems, due to a solid result from spirits and alcoholic ready-to-drink beverages, partly offset by a decline in SPC Ardmona (SPCA) earnings.

Beam earnings were driven by the success of Canadian Club, the introductionofnewflavourextensionsintheBeamrange(JimBeamHoney, Black Cherry and Devil’s Cut), with Beam’s value share of the Spirits category increasing by close to one percentage point.

The ongoing impact of the high Australian dollar on the competitiveness oftheSPCAbusiness,thesignificantdeflationoffreshfruitpricesand the growth of imported grocery private label packaged fruit and vegetableshasnecessitatedasecondhalfsignificantwrite-downinSPCA assets and goodwill.

Material progress made in positioning the alcoholic beverages platform for growth

CCA is the leading non-alcoholic beverages and spirits partner for thelicencedtradeinAustralia.Significantprogresswasmadeinstrengthening its brand portfolio including an agreement to form a beer manufacturing joint venture with Casella commencing December 2013, and a long-term exclusive agreement to distribute Rekorderlig cider in Australia from January 2014.

Internationally, CCA acquired the Foster’s Fiji brewery and distillery and the commenced distribution of premium beer for Grupo Modelo, Carlsberg andMolsonCoorsinFiji,PapuaNewGuineaandthePacificIslands.

Commencement of major operational effi ciency programme

As the investment in the technology platform and the self-manufacture of PET bottles nears completion, the next phase of Project Zero initiatives will extend into driving productivity gains across the business.

We will seek to fully leverage the functionality of the new manufacturing and technology platforms which have been installed across the business over the past three years.

Atthisstagewearetargeting$30-40millionofannualefficiencygains and cost out initiatives to be delivered progressively over the next three years, with a particular focus on further reducing the cost base of the under-performing SPC Ardmona business and the New Zealand beverage operations.

PRIORItIES & OutlOOk FOR 2013

trading outlook

The Australian business expects to again deliver revenue and earnings growthin2013.Inaddition,webelieveproductivityandefficiencygains from the Project Zero investment programme will make a good contribution to earnings growth. We do however remain concerned by the generally weak consumer spending environment which has persisted for the last two years.

The strong momentum in Indonesia & PNG is expected to continue. The outlook for growth continues to be positive with revenue expected toexceed$1billionforthefirsttimein2013.Thesuccessfulcompletionof a number of large investments in manufacturing and distribution has materially increased our production capacity and will support the ongoing growth of the business and the strong pipeline of new products and packs that will be launched in 2013.

Medium term capital spend to reduce to $350-420 million pa

Based on current forecasts, capital expenditure is expected to reduce fromthe2012peaklevelstoanaverageof$350-420millionperannumover the next three years, with 2013 capex expected to be around $420million.

The delivery of consistently strong results from Indonesia & PNG will drive a shift in the weighting of capex to this region. For 2013 we expect capitalexpenditureinthisregiontoincreasetoaround$200million,which we expect will deliver a 45% increase in our one-way-pack production capacity in Indonesia and the placement of around 55,000 new cold drink cooler doors, representing a 20% increase in cooler doors in Indonesia by the end of the year.

terry DavisGroup Managing Director

COCA-COLA AMATIL LIMITED ANNUAL REPORT 2012 4

FinanciaL coMMentarY

The following commentary summarises the Company’s performance regardingcapitalemployed,cashflow,netdebtandinterestcoverposition,capitalexpenditureandsignificantitems.

CAPItAl EMPlOYED

Capitalemployeddecreasedby$66.1millionto$3.71billionwithGroupROIC(beforesignificantitems)remainingverystrongat17.1%.Property,plant&equipmentincreasedby$221.7million,aresultofCCA’sup-weighted Project Zero capital investment program and accelerated investment in Indonesia & PNG. The increase in IBAs and intangible assetsof$26.7millionismainlyduetothecontinuingdevelopmentandroll-out of the OAisys platform across the Group and goodwill arising from acquisitions less the write-down of goodwill in the SPCA business. Non-debtderivativeassetsdeclinedby$18.6millionreflectingyear-endmarket valuations of commodity contracts, foreign exchange contracts and the interest rate portion of cross currency swaps. Other net liabilities increasedby$278.0million,reflectingthesaleofCCA’s50%jointventureinterestinPacificBeveragestoSABMillerinDecember2011for$288.6million.

CASH FlOW

CCAgeneratedastrongcashflowof$629.6million,anincreaseof$345.4million,whichincludesnetproceedsfromthesaleofCCA’sjointventureinterestinPacificBeverages.Operatingcashflow,beforesignificantitems,increasedby$128.1millionto$794.3millionprimarilydue to improvements in earnings, working capital as well as lower interest and tax payments. Capital expenditure increased by $103.6millionreflectingtheaccelerationofhigh-returningProjectZeroinvestments and accelerated investment in manufacturing capacity and cold drink coolers in the fast-growing Indonesia & PNG business. The$6.0millionnetcashinflowfromsignificantitemscomprises $34.2millioninaftertaxproceedsreceivedfromSABMillerfornotproceeding with the acquisition of the Foster’s Australian spirits business,netof$28.2millioninnetcashcostsrelatingtocurrent andprioryearsignificantitems.

nEt DEBt & IntERESt COVER

The balance sheet remains in a very strong position with net debt reducingby$110.4millionto$1.63billionandEBITinterestcoverincreasingstrongly,from6.8xto8.0x,beforesignificantitems.Netcashonhandandondepositincreased$663.1millionwithCCAholdingfundson deposit with major Australian banks from the pre-funding of all debt maturing until late 2014 with deposit margins exceeding the cost of funds.

CCAhadtotalavailabledebtfacilitiesofapproximately$3.0billionwithan average maturity of 4.1 years as at 31 December 2012. During 2012, CCAraised$580millionindomesticandoffshoredebttoprefund2014debtmaturities.InJanuary2013,anadditional$100millionwasraisedinthe Euro Medium Term Note market to prefund 2014 debt maturities. As a result, 2014 debt maturities have been fully funded to November 2014.

$A million 2012 2011 $ChangeWorking capital1 842.7 856.7 (14.0)Property, plant & equipment 1,993.8 1,772.1 221.7IBAs & intangible assets 1,533.9 1,507.2 26.7Deferred tax liabilities (157.7) (153.8) (3.9)Derivatives – non-debt (63.9) (45.3) (18.6)Other net assets/(liabilities) (437.7) (159.7) (278.0)Capital employed 3,711.1 3,777.2 (66.1)ROIC2 % 17.1% 17.1% 0.0 pts

$A million 2012 2011 $ChangeEBIT(beforesignificantitems) 895.5 868.9 26.6Depreciation & amortisation 233.4 205.2 28.2Change in working capital 33.2 (36.7) 69.9Net interest paid (104.0) (118.4) 14.4Taxation paid (167.0) (206.2) 39.2Other (96.8) (46.6) (50.2)Operating cash flow (beforesignificantitems) 794.3 666.2 128.1Capital expenditure (464.8) (361.2) (103.6)Cashimpactofsignificantitems 6.0 (24.4) 30.4Other 5.5 3.6 1.9Free cash flow 341.0 284.2 56.8Net proceeds from sale of JV interest 288.6 – 288.6Cash flow 629.6 284.2 345.4

$A million 2012 2011

$ ChangeNet Debt

Interest bearing liabilities 2,787.2 2,309.2 478.0Debt related derivatives – liabilities 173.3 123.1 50.2Long-term deposits (150.0) – (150.0)Trade & other receivables* – (24.5) 24.5Less: Cash assets (1,178.0) (664.9) (513.1)

net Debt 1,632.5 1,742.9 (110.4)EBIT interest cover (beforesignificantitems) 8.0x 6.8x 1.2x

1.2011workingcapitalexcludes$24.5millionloantoPacificBeverages.2.Beforesignificantitems.

*LoantoPacificBeverages

COCA-COLA AMATIL LIMITED ANNUAL REPORT 20125

CAPItAl EXPEnDItuRE

Capitalexpenditureincreasedby$103.6millionto$464.8million. The major areas of capital expenditure included Project Zero initiatives across the Group, an acceleration of high-returning PET bottle self-manufacture investments in Australia, manufacturing capacity expansion and cold drink cooler investment in Indonesia & PNG and the continued rollout of cold drink coolers.

ProjectZerocontinuestodeliverefficiencygainswithexpenditureonProjectZeroinitiativesexceeding$270million.TheinvestmentinPETbottleself-manufacturelinesacrosstheGroupcontinuedwithfiveproduction lines completed in Australia, two in New Zealand and three lines in Indonesia. In addition, the business commissioned a PET bottle preform and bottle closure injection moulding plant at the Eastern Creek facility in NSW.

$120millionwasinvestedincolddrinkequipmentacrosstheGroup.CCA’s cooler investment continues to be an important driver of cold drink market share gains in Australia with up-weighted investment in Indonesia&PNGsignificantlyincreasingthepenetrationofcoolers in these countries.

SIGnIFICAnt ItEMS

CCArecordedanet$98.5millionaftertaxsignificantitemexpense for2012.Significantitemscomprise:

-$34.2millioninaftertaxcashproceedsfromSABMillerfor not proceeding with the acquisition of the Foster’s Australian spirits business;

-$13.3millioninaftertaxcashgainfromTheCoca-ColaCompanyforagreeing to replace the Kirks brand in the licensed channel with the Cascade brand;

- The ongoing impact of the high Australian dollar on the competitiveness oftheSPCAbusiness,thesignificantdeflationoffreshfruitpricesand the growth of imported grocery private label packaged fruit and vegetables has necessitated a non-cash write-down of goodwill in the businessof$48.0million;and

-$98.0millionoflargelynon-cashexpensesrelatingtoinventoryandother asset write-downs and other business restructuring costs primarily associated with the ongoing transformation of SPCA.

$A million 2012 2011 ChangeAustralia* 281.4 229.1 52.3New Zealand & Fiji* 43.0 31.3 11.7Indonesia & PNG* 140.4 100.8 39.6

Capital expenditure 464.8 361.2 103.6Capital expenditure/trading revenue 9.1% 7.5% 1.6 ptsCapital expenditure/depreciation & amortisation 2.0x 1.8x 0.2x

* Geographic breakdown

BoarD oF Directors

DAVID GOnSkI, AC Chairman, non-Executive Director (Independent) – Age 59

Joined the Board in October 1997 – Chairman of the Related Party Committee and Nominations Committee and member of Audit & Risk Committee, Compensation Committee and Compliance & Social Responsibility Committee.

Background:Solicitorfor10yearswiththelawfirmofFreehillsandthereafteracorporateadviserinthefirmofWentworthAssociatescofounded by him, now part of the Investec group. He is presently Chairman of Investec Bank Australia Ltd.

Degrees: B Com; LLB (UNSW); FAICD (Life), FCPA.

Other Listed Company Boards: Director, Singapore Telecommunications Limited (SingTel) (appointed 1 March 2013).

Other Listed Company Directorships held in the last three years: WestfieldGroup(resigned2011);ASXLimited(resignedMarch2012);andSingapore Airlines Limited (resigned August 2012).

Government & Community Involvement: Chancellor of the University of New South Wales; Chairman, the Future Fund, UNSW Foundation Limited, National E-Health Transition Authority and Sydney Theatre Company; Chair of the Federal Government Review of the Funding of Schools in Australia; Director, Infrastructure NSW and the Lowy Institute for International Policy; Member, ASIC External Advisory Panel; and Patron of the Australian Indigenous Education Fund.

tERRY DAVIS Group Managing Director, Executive Director – Age 55

Appointed in November 2001.

Background: Joined CCA in November 2001 as Group Managing Director after 14 years in the global wine industry with most recent appointment as the Managing Director of Beringer Blass (the wine division of Foster’s Group Ltd).

Other Listed Company Boards: Seven Group Holdings Limited, Chairman of SGH Related Party Committee.

Government & Community Involvement: Council Member, University of New South Wales Council (since 2006).

IlAnA AtlAS non-Executive Director (Independent) – Age 58

Joined the Board in February 2011 – Member of the Compensation Committee, Audit & Risk Committee, Related Party Committee and Nominations Committee.

Background: Ms Atlas has extensive experience in business and has held executive and non-executive roles across many industry sectors. From 2003 to 2010 Ms Atlas held senior executive roles within Westpac Banking Corporation. She has been a practising lawyer for 22 years and is a former partner of Mallesons Stephen Jaques.

Degrees: Master of Laws (University of Sydney); Bachelor of Laws (Hons); Bachelor Jurisprudence (Hons) (University of Western Australia).

Other Listed Company Boards:SuncorpGroupLimitedandWestfieldHoldings Limited.

Government & Community Involvement: Chair of the Bell Shakespeare Company, Director of Human Rights Law Centre Limited and Pro-Chancellor of the Australian National University.

COCA-COLA AMATIL LIMITED ANNUAL REPORT 2012 6

BoarD oF Directors (continueD)

CAtHERInE BREnnER non-Executive Director (Independent) – Age 42

Joined the Board in April 2008 – Chair of the Compliance & Social Responsibility Committee and Member of the Compensation Committee, Related Party Committee and Nominations Committee.

Background: Ms Brenner is a former senior investment banker. Prior to this, Ms Brenner was a corporate lawyer.

Degrees: BEc; LLB (Macquarie University); MBA (Australian Graduate School of Management, UNSW).

Other Listed Company Boards: AMP Limited and Boral Limited.

Other Listed Company Directorships held in the last three years: Centennial Coal Company Limited (resigned 2010).

Government & Community Involvement: Trustee of Sydney Opera House Trust, Council Member of Chief Executive Women.

AntHOnY (tOnY) FROGGAtt non-Executive Director (Independent) – Age 64

Joined the Board in December 2010 – Chairman of the Compensation Committee, Member of the Audit & Risk Committee, Related Party Committee and Nominations Committee.

Background: MrFroggattisaformerChiefExecutiveOfficerofScottish& Newcastle plc, a global brewing company based in Edinburgh, UK. Prior to that, he held various senior management positions in Seagram Spirits & Wine Group, Diageo plc, H J Heinz and The Gillette Company. He is experienced in global business and brand development in both mature and developing markets, as well as having extensive marketing and distribution knowledge, particularly in the international food and beverages sector.

Degrees: Bachelor of Laws degree from Queen Mary College, London; MBA from Columbia Business School, New York.

Other Listed Company Boards: Non-Executive Director, Brambles Limited and Billabong International Limited.

Other Listed Company Directorships held in the last three years: AXAAsiaPacificHoldingsLimited(from16April2008toMarch2011).

MARtIn JAnSEn non-Executive Director (nominee of tCCC) – Age 54

Joined the Board in December 2009 – Member of the Audit & Risk Committee.

Background: Martin Jansen is the Regional Director, Bottling Investments Group for China, Singapore and Malaysia and Chief ExecutiveOfficerforCoca-ColaChinaIndustriesLtdand,assuch,isresponsible for The Coca-Cola Company’s Bottling Investment interests in China, Singapore and Malaysia. Mr Jansen joined the Coca-Cola systemin1998whenhewasappointedChiefOperatingOfficerfor Coca-ColaSabco.In2001,hewasappointedChiefExecutiveOfficerleading an anchor bottler with operations in 12 countries in Africa and Asia.

Degree: Bachelor of Commercial Economics (HEAO Groningen, Netherlands); Graduate of the Executive Development Program at Northwestern University Kellogg School of Management.

Other Listed Company Boards: Director, Haad Thip Public Company Limited (Thailand bottling partner).

Government & Community Involvement: Director, The Coca-Cola Company African Foundation.

GEOFFREY kEllY non-Executive Director (nominee of tCCC) – Age 68

Joined the Board in April 2004 – (having previously been a Director between 1996 and 2001). Member of Compensation Committee.

Background: Joined The Coca-Cola Company in 1970 and has held legal positions with TCCC in the US, Asia and Europe. Mr Kelly retired asSeniorVicePresidentandGeneralCounsel,ChiefLegalOfficerofThe Coca-Cola Company on 1 March 2012. He continues to provide consultancy services to that Company.

Degree: LLB (University of Sydney).

Government & Community Involvement: Director, Leadership Council for Legal Diversity and the University of Sydney USA Foundation; Advisory Board Director, YKK Americas; Past Chairman, Japan America Society of Georgia.

WAl kInG, AO non-Executive Director (Independent) – Age 68

Joined the Board in February 2002 – Member of the Related Party Committee, Nominations Committee and Compliance & Social Responsibility Committee.

Background: Mr King has worked in the construction industry for over 40yearsandwasChiefExecutiveOfficerofLeightonHoldingsLimited,a company with substantial operations in Australia, Asia and the Middle East, from 1987 until his retirement on 31 December 2010. He remains as a Consultant.

Degrees: B Eng; M EngSc and Honorary Doctor of Science (UNSW).

Other Listed Company Boards: Ausdrill Limited (Non-Executive Director and Deputy Chairman).

Other Listed Company Directorships held in the last three years: Leighton Holdings Limited (retired 31 December 2010).

Government & Community Involvement: Deputy Chairman, University of New South Wales Foundation Limited; Director, Kimberley Foundation Australia Limited and Garvan Research Foundation and Council Member, University of New South Wales (to June 2012).

DAVID MEIklEJOHn, AM non-Executive Director (Independent) – Age 71

Joined the Board in February 2005 – Chairman of the Audit & Risk Committee, and Member of the Nominations Committee, Related Party Committee and Compliance & Social Responsibility Committee.

Background:StrongexperienceinfinanceandfinancialmanagementandasaCompanyDirector.ChiefFinancialOfficerofAmcorLimitedfor19 years until retirement in June 2000.

Degree: B Com; Dip Ed (University of Queensland); FAIM, FAICD, FCPA.

Other Listed Company Boards: Australia and New Zealand Banking Group Ltd and Mirrabooka Investments Limited.

Other Listed Company Directorships held in the last three years: PaperlinXLimited(retiredAugust2011).

Government & Community Involvement: Chairman of the Board of Governance of the Manningham Aged Care Centre.

GEnERAl COunSEl AnD COMPAnY SECREtARY George Forster – Age 58

Mr Forster joined CCA in April 2005 as General Counsel. He was appointed Company Secretary in February 2007. Mr Forster holds Bachelor of Laws and Bachelor of Commerce degrees from the University of New South Wales and has extensive experience of over thirty years as a corporate and commercial lawyer, including having been a partner of Freehills in Sydney.

COCA-COLA AMATIL LIMITED ANNUAL REPORT 20127

GEORGE ADAMS Managing Director – new Zealand & Fiji – Age 46

Appointed in December 2003 until April 2013

Background: George joined CCA New Zealand on 1 December 2003 and will complete his assignment no later than June 2013. George has 17 years’ experience in the Coca-Cola bottling system having previously spent 10 years with Coca-Cola Hellenic Bottling Company in a number of senior Finance, Commercial and IT roles in Europe.

PEtER kEllY Managing Director – SPCA – Age 48

Appointed in April 2013

Background: Peter has spent 25 years with the Coca-Cola system, having joined The Coca-Cola Company in 1988 and then CCA in 1993. He has a strong track record of success in a cross section of business functions and has demonstrated breadth and depth of capability having held a number of key positions, including General Manager Grocery and Director of Operations and Logistics in CCA’s Australian business before taking on the role of Regional Director for Asia with accountability for the Indonesian & PNG business units. Since early 2012 he has held the position of Managing Director, Business Services (commercialisation of projects and Mergers & Acquisitions), before being appointed SPCA MD in April 2013.

BARRY O’COnnEll Managing Director – new Zealand & Fiji – Age 46

Appointed in April 2013

Background: Barry has a proven track record of success and joins CCA after 20 years with Coca-Cola Hellenic (CCHBC) where he has held senior positions with increasing responsibility. Having started his career in a marketing role in Ireland, Barry went on to work in the startup of the CCHBC Russian franchise in 1997 before holding sales and marketing director’s roles in both Ireland and Switzerland. He was then appointed to his current role of General Manager for Austria & Slovenia, in 2009. Under Barry’s leadership, the Austrian business has been one of the best performing markets in CCHBC, delivering double digit EBIT growth and significantmarketsharegainsoverthelastthreeyears.

nESSA O’SullIVAn Group Chief Financial Officer – Age 48

Appointed in September 2010

Background: A Fellow of the Institute of Chartered Accountants in Ireland and a graduate of University College Dublin. Nessa joined CCA in May 2005 as CFO for the Australian Beverage business. Prior to joining CCA Nessa held the role of CFO and VP for the Australia/ New Zealand region of Yum! Restaurants International. She spent 12 years with Yum! in senior roles in Finance, Strategic Planning and IT. Nessa holds dual Irish and Australian citizenship and has worked in Europe, the United States and Australia.

senior ManageMent

VInCE PInnERI Managing Director – SPCA – Age 54

Appointed in July 2010 until April 2013

Background: Vince has worked within the Coca-Cola system for over 27 years and has gained great experience across many countries during his time. In 2008 Vince became General Manager Strategy for Non-Alcoholic Beverages and then General Manager of Immediate Consumption and Convenience & Petroleum before becoming Managing Director of SPCA in July 2010.

From April 2013 he has been appointed as Director of New Ventures for CCA Australian Beverages.

ERICH REY President Director – Indonesia – Age 51

Appointed in November 2011

Background:ErichfirstjoinedtheCoca-Colasystemin1996,astheGeneral Manager for one of the bottlers of Panamco Colombia and worked in a variety of roles across Panamco’s Colombia and Latin American operations. He was Femsa’s Director of Operations in 2003 in Nicaragua and was the General Manager for Ecuador Bottling Company prior to joining CCA. Erich was appointed to the position of President Director – Indonesia in November 2011.

WARWICk WHItE Managing Director – Australasia – Age 51

Appointed in November 2002

Background: Warwick has over 31 years in the Coca-Cola System and re-joined Coca-Cola Amatil in November 2002 as the Managing Director for the CCA Australian beverages business.

Prior to that, Warwick held marketing and general management roles within the Coca-Cola System. Immediately prior to joining CCA, Warwick was the Regional Director for Coca-Cola Hellenic Bottling Company with responsibility for Ireland, Poland, Hungary, Czech Republic and Slovakia. This was preceded by 14 years in Great Britain, Europe and Ireland in progressively more senior roles within the Coca-Cola System.

COCA-COLA AMATIL LIMITED ANNUAL REPORT 2012 8

corporate governance stateMent

At Coca-Cola Amatil (CCA), the Board of Directors is committed to achieving the highest standards in the areas of corporate governance and business conduct. This Corporate Governance Statement reports on the corporate governance principles and practices followed by CCA for theperiod1January2012to31December2012asrequiredbytheASXListing Rules.

The Company has followed all of the recommendations established in the ASXCorporateGovernanceCouncil’sPrinciplesandRecommendations,2nd Edition.

The Policies and Board Committee Charters referred to in this Report may be accessed on the Company’s website at www.ccamatil.com.

PRInCIPlE 1 – lAY SOlID FOunDAtIOnS FOR MAnAGEMEnt AnD OVERSIGHt

the Role of the Board

The Board represents shareholders and has the ultimate responsibility for managing CCA’s business and affairs to the highest standards of corporate governance and business conduct. The Board continues to operateontheprinciplethatallsignificantmattersaredealtwithby thefullBoardandhasspecificallyreservedthefollowingmattersfor its decisions:

• the strategic direction of the Company; • approving budgets and other performance indicators,

reviewing performance against them and initiating corrective action when required;

• ensuring that there are adequate structures to provide for compliance with applicable laws;

• ensuring that there are adequate systems and procedures to identify, assess and manage risks;

• ensuring that there are appropriate policies and systems in place to ensure compliance;

• monitoring the Board structure and composition; • appointing the Group Managing Director and evaluating his or her

ongoing performance against predetermined criteria; • approving the remuneration of the Group Managing Director and

remuneration policy and succession plans for the Group Managing Director and senior management;

• ensuring that there is an appropriate focus on the interests of all stakeholders; and

• representing the interests of and being accountable to the Company’s shareholders.

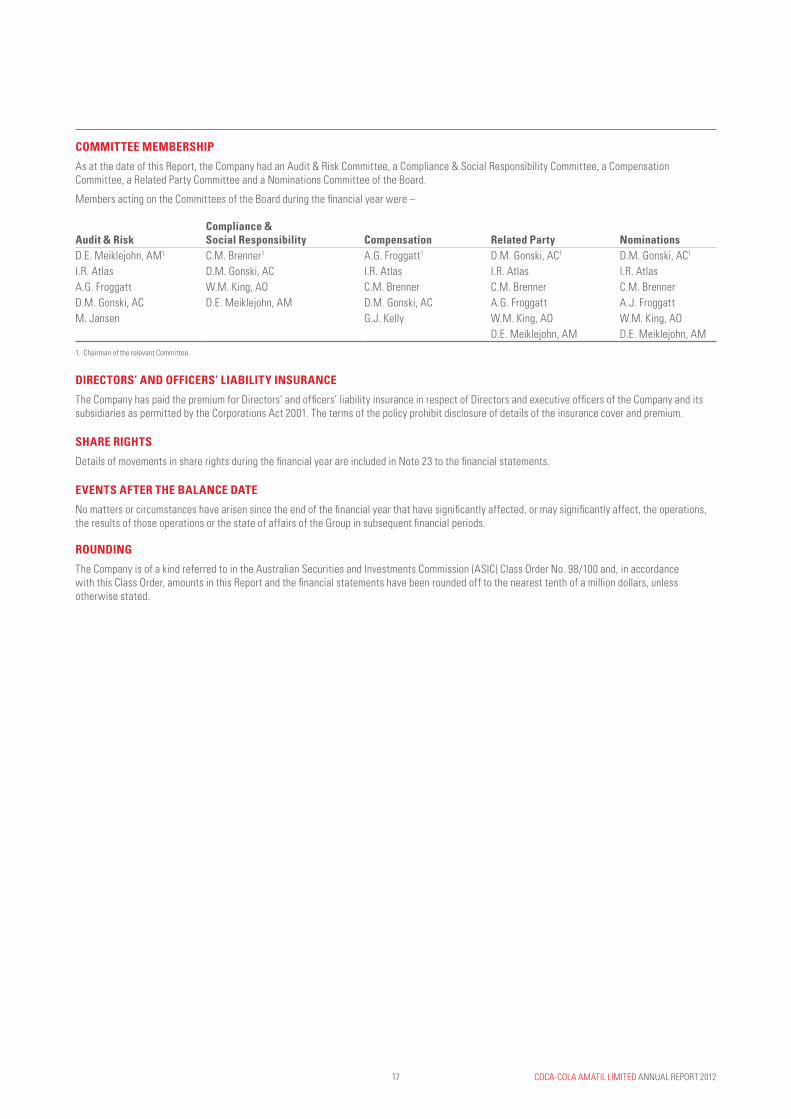

Toassistinitsdeliberations,theBoardhasestablishedfivemaincommittees which, apart from routine matters, act primarily in a review or advisory capacity on the matters set out in their respective Charters. These are the Related Party Committee; Nominations Committee; Compliance & Social Responsibility Committee; Audit & Risk Committee; and Compensation Committee. The Charters of each Committee are summarised in this report. The delegation of responsibilities to these Committeeswillonlyoccurprovidedthatsufficientsystemsareinplaceto ensure that the Board is meeting its responsibilities.

Role of Group Managing Director

The responsibility for implementing the approved business plans and for the day-to-day operations of CCA is delegated to the Group Managing Director who, with the management team, is accountable to the Board. The Board approves the Executive Chart of Authority which sets out the authority limits for the Group Managing Director and senior management.

Senior Executives’ Performance Evaluation Across all of CCA’s Business Units, there is a strong performance management discipline together with competitive reward and incentive programs. The Company’s approach in recent years is to move to have a greater component of at-risk remuneration for senior executives.

Detailed business plans are prepared and approved by the CCA Board prior to the start of the calendar year. The senior executives are then measured against the achievement of these plans during and at the completion of the calendar year, and their annual at-risk remuneration reflectstheirbusinessplanachievements.Anevaluationofperformancehas been undertaken for all senior managers for 2012, and this has been in accordance with the above process.

PRInCIPlE 2 – StRuCtuRE tHE BOARD tO ADD VAluE

Composition of the Board

The composition of the Board is based on the following factors:

• the Chairman is a Non-Executive Director and is independent from The Coca-Cola Company;

• the Group Managing Director is the Executive Director; • The Coca-Cola Company has nominated two Non-Executive Directors

(currently Geoffrey Kelly and Martin Jansen); • the majority of the Non-Executive Directors are independent; • one-third of the Board (other than the Group Managing Director) is

required to retire at each Annual General Meeting and may stand for re-election. The Directors to retire shall be those who have been longestinofficesincetheirlastelection;and

•aDirectorwhohasbeenappointedbytheBoardtofillacasualvacancyis required to be considered for re-election by the shareholders at the next Annual General Meeting.

The Board is comprised of the following nine members:

name Position Independent Appointed

David Gonski, AC Chairman, Non-Executive Director

Yes 1997

Ilana Atlas Non-Executive Director Yes 2011

Catherine Brenner Non-Executive Director Yes 2008

Anthony (Tony) Froggatt Non-Executive Director Yes 2010

Wal King, AO Non-Executive Director Yes 2002

David Meiklejohn, AM Non-Executive Director Yes 2005

Martin Jansen* Non-Executive Director No 2009

Geoffrey Kelly* Non-Executive Director No 2004

Terry Davis Executive Director and Group Managing Director

No 2001

* Nominated by The Coca-Cola Company

Details of the skills, experience and expertise of each Director are set out on page 6 of this Report. Attendance at Board and Committee meetings and the names of Committee members are included in the Directors’ Report on pages 16 and 17.

COCA-COLA AMATIL LIMITED ANNUAL REPORT 20129

Directors – Independence

The majority of the Board are independent Directors. A Director is considered independent provided he or she is free of any business or other relationship with CCA or a related party which could reasonably be perceived to materially interfere with the exercise of their unfettered and independent judgement. A related party for this purpose would include The Coca-Cola Company.

Whenapotentialconflictofinterestarises,theDirectorconcernedwithdraws from the Board meeting while such matters are considered. Accordingly, the Director concerned neither takes part in discussions nor exercisesanyinfluenceovertheBoardifapotentialconflictofinterestexists. Transactions with The Coca-Cola Company are reviewed by the Related Party Committee. Related party transactions are disclosed in Note33tothefinancialstatements.

Directors – Selection

The Board’s Nominations Committee regularly reviews the composition of the Board to ensure that there is an appropriate mix of abilities, experience and diversity to serve the interests of all shareholders. Any recommendations are presented to the full Board.

The process of appointing a Director is that when a vacancy exists, or isexpected,theNominationsCommitteeidentifiescandidateswiththeappropriate expertise and experience having regard to the skills that the candidate would bring to the Board and the balance of skills that the existing Directors hold. The Board reviews the candidates and the most suitable person is either appointed by the Board and comes up for re-election at the next Annual General Meeting or is recommended to shareholders for election at a shareholders’ meeting.

Related Party Committee

The Related Party Committee is comprised of all the independent Non-Executive Directors (and does not include any Directors who are or have been associated with a related party). The Group ManagingDirectorandtheGroupChiefFinancialOfficerattendmeetings by invitation.

The Committee reviews transactions between CCA and parties who may not be at arm’s length (“related parties”) to ensure that the terms of such transactions are no more favourable than would reasonably be expected of transactions negotiated on an arm’s length basis. It meets prior to each scheduled Board meeting to review all material transactions of CCA in which The Coca-Cola Company, or any other related party, is involved.

Nominations Committee

The Nominations Committee is comprised of all the independent Non-Executive Directors (it does not include any Directors who are or have been associated with a related party).

The Committee reviews the Board’s composition to ensure that it comprises Directors with the right mix of skills, experience, expertise anddiversitytoenableittofulfilitsresponsibilitiestoshareholders.TheCommitteealsoreviewsBoardsuccessionpolicyandidentifiessuitable candidates for appointment to the Board and reviews general matters of corporate governance. The Committee has also been given responsibility for reviewing the Company’s standards of corporate governance.

Directors – Induction and Education

On appointment, each Non-Executive Director is required to acknowledge the terms of appointment as set out in their letter of appointment. The appointment letter covers, inter alia, the term of appointment, duties, remuneration including superannuation and expenses, rights of access to information, other directorships, dealing in CCA’s shares, disclosure of Director’s interests, insurance and indemnity and termination. The Director is provided with the Company’s policies and Board Committee charters and briefed on the content by the Company Secretary.

An induction program is made available to newly appointed Directors covering such topics as the Board’s role, Board composition and conduct, and the risks and responsibilities of company directors, to ensure that they are fully informed on current governance issues. The program also includesbriefingsonthecultureandvaluesoftheCompany,therolesandresponsibilitiesofseniorexecutivesandtheCompany’sfinancial,strategic, operational and risk management position.

Independent Professional Advice

For the purposes of the proper performance of their duties, Directors are entitled to seek independent professional advice at CCA’s expense. Before doing so, a Director must notify the Chairman (or the Group Managing Director in the Chairman’s absence) and must make a copy of the advice available to all Directors.

Directors – Performance Review

A review of the Directors performance is undertaken at least every two years. If a majority of Directors considers a Director’s performance falls below the predetermined criteria required, then the Director has agreed to retire at the next Annual General Meeting and a resolution will be put to shareholders to vote on the re-election of that Director.

The Board has, in late 2012, commissioned an independent external reviewoftheBoardtotakeplaceinthefirsthalfof2013.Thisreview has commenced.

The last external performance review was in 2009. In 2011, the Board resolved that an internal review be undertaken by the Chairman with each Director individually and members of senior management to discuss the operation and composition of the Board. The process of Board performance will remain under continuous review.

Company Secretary

The Company Secretary is appointed by the Board and is accountable to the Board, through the Chairman, on all governance matters.

COCA-COLA AMATIL LIMITED ANNUAL REPORT 2012 10

corporate governance stateMent (continueD)

Compliance & Social Responsibility Committee

The Compliance & Social Responsibility Committee comprises at least three Non-Executive Directors. The Committee regularly reviews and reports to the Board on compliance with laws including occupational health and safety, environmental protection, product safety and trade practices.

TheCommitteealsoreviewspoliciesreflectingontheCompany’sreputation, including quality standards, dealing in the Company’s securities and disclosure. Its responsibilities include – Diversity: recommend to the Board measurable objectives to be set in accordance with the Diversity Policy and review and report to the Board, on an annual basis, on the effectiveness of the Diversity Policy; Social responsibility: review reports and make recommendations to the Board, where appropriate, in respect of political donations, community sponsorship and support and relevant social issues such as obesity, environmentally sustainable initiatives, and CCA’s carbon footprint and other social issues that may be relevant to the Company.

PRInCIPlE 3: PROMOtE EtHICAl AnD RESPOnSIBlE DECISIOn-MAkInG

Code of Business Conduct

The Board recognises the need to observe the highest standards of corporate practice and business conduct. The Code of Business Conduct isreviewedregularlytoensurethatthestandardssetintheCodereflectCCA’s values, acknowledge our responsibilities to our stakeholders and to each other, and ensure that management and employees know what is expected of them and apply high ethical standards in all of CCA’s activities.

The Audit & Risk Committee is responsible for ensuring that effective compliance policies exist to ensure compliance with the requirements established in the Code of Business Conduct. The Code contains procedures for identifying and reporting any departures from the required standards. CCA has also established a system for distribution of the Code at appropriate intervals to employees and for them to acknowledge its receipt.

The Code sets standards of behaviour expected from everyone who performs work for CCA – Directors, employees and individual contractors. It is also expected that CCA’s suppliers will enforce a similar set of standards with their employees. The code is available on our website at www.ccamatil.com.

Interests of Stakeholders

CCA acknowledges the importance of its relationships with its shareholders and other stakeholders including employees, contractors and the wider community. CCA believes that being a good corporate citizen is an essential part of business and pursues this goal in all the markets in which it operates. CCA publishes Sustainability@CCA Reports which focus on four pillars of commitment – Environment, Marketplace, Workplace and Community. These Reports can be viewed on the CCA website at www.ccamatil.com.

The Compliance & Social Responsibility Committee assists the Board in determining whether the systems of control, which management has established, effectively safeguard against contraventions of the Company’s statutory responsibilities and there are policies and controls to protect the Company’s reputation as a responsible corporate citizen.

Share Ownership and Dealings

Details of the shareholdings of Directors in the Company are set out in the Directors’ Report on page 15. The Non-Executive Directors Share Plan was suspended on 1 September 2009 due to the change in taxation arrangements of share plans announced by the Australian Government during 2009.

Non-Executive Directors are encouraged to hold CCA shares, with shareholding guidelines introduced during 2010, based on length of time servedasaCCADirector.SeepageXoftheRemunerationReport for details.

Policy on trading in CCA Shares

Directors are subject to the Corporations Act 2001 which restricts their buying, selling or trading securities in CCA if they are in possession of inside information.

The Board has adopted a formal policy for share dealings by Directors and senior management. Under the policy, trading of CCA shares by Directors and Senior Management is prohibited at all times except for the four weeks commencing on the day after the release of the Half Year and Full Year results and the holding of the Annual General Meeting, unless exceptional circumstances apply. The policy prohibits speculative transactions involving CCA shares, the granting of security over CCA shares or entering into margin lending arrangements involving CCA Shares and reinforces the prohibition on insider trading contained in the Corporations Act 2001.

COCA-COLA AMATIL LIMITED ANNUAL REPORT 201211

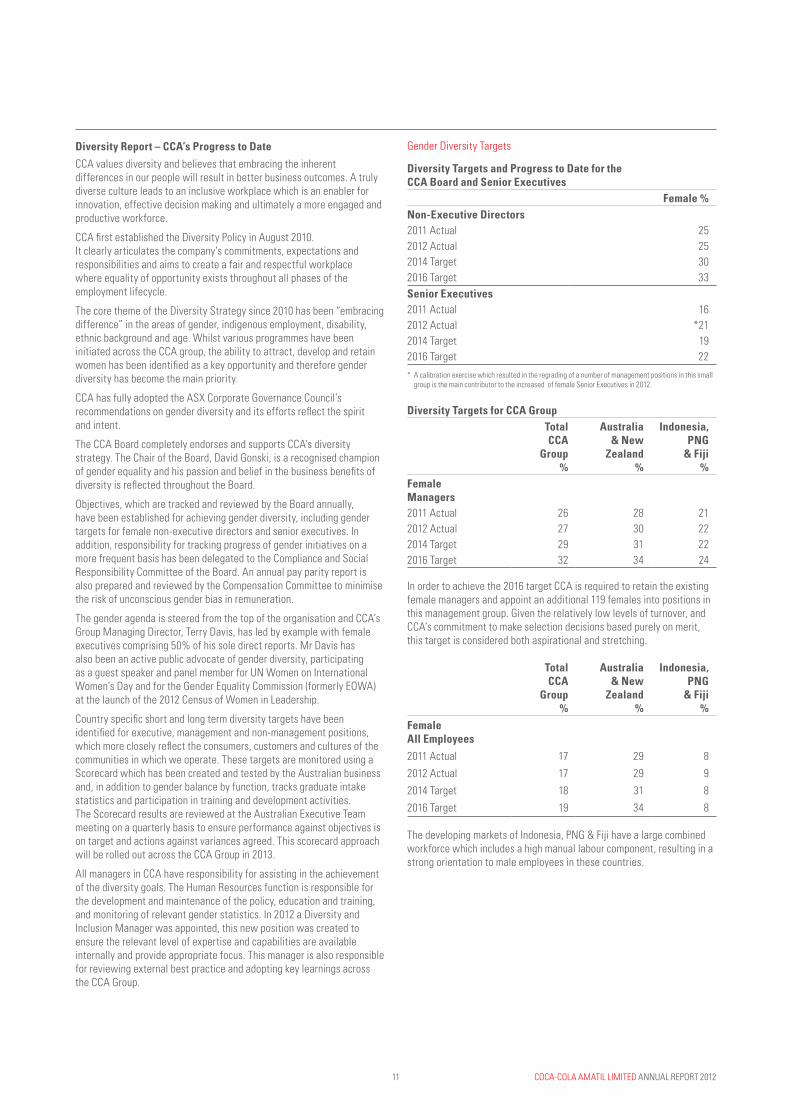

Diversity Report – CCA’s Progress to Date

CCA values diversity and believes that embracing the inherent differences in our people will result in better business outcomes. A truly diverse culture leads to an inclusive workplace which is an enabler for innovation, effective decision making and ultimately a more engaged and productive workforce.

CCAfirstestablishedtheDiversityPolicyinAugust2010. It clearly articulates the company’s commitments, expectations and responsibilities and aims to create a fair and respectful workplace where equality of opportunity exists throughout all phases of the employment lifecycle.

The core theme of the Diversity Strategy since 2010 has been “embracing difference” in the areas of gender, indigenous employment, disability, ethnic background and age. Whilst various programmes have been initiated across the CCA group, the ability to attract, develop and retain womenhasbeenidentifiedasakeyopportunityandthereforegenderdiversity has become the main priority.

CCAhasfullyadoptedtheASXCorporateGovernanceCouncil’srecommendationsongenderdiversityanditseffortsreflectthespirit and intent.

The CCA Board completely endorses and supports CCA’s diversity strategy. The Chair of the Board, David Gonski, is a recognised champion ofgenderequalityandhispassionandbeliefinthebusinessbenefitsofdiversityisreflectedthroughouttheBoard.

Objectives, which are tracked and reviewed by the Board annually, have been established for achieving gender diversity, including gender targets for female non-executive directors and senior executives. In addition, responsibility for tracking progress of gender initiatives on a more frequent basis has been delegated to the Compliance and Social Responsibility Committee of the Board. An annual pay parity report is also prepared and reviewed by the Compensation Committee to minimise the risk of unconscious gender bias in remuneration.

The gender agenda is steered from the top of the organisation and CCA’s Group Managing Director, Terry Davis, has led by example with female executives comprising 50% of his sole direct reports. Mr Davis has also been an active public advocate of gender diversity, participating as a guest speaker and panel member for UN Women on International Women’s Day and for the Gender Equality Commission (formerly EOWA) at the launch of the 2012 Census of Women in Leadership.

Countryspecificshortandlongtermdiversitytargetshavebeenidentifiedforexecutive,managementandnon-managementpositions,whichmorecloselyreflecttheconsumers,customersandculturesofthecommunities in which we operate. These targets are monitored using a Scorecard which has been created and tested by the Australian business and, in addition to gender balance by function, tracks graduate intake statistics and participation in training and development activities. The Scorecard results are reviewed at the Australian Executive Team meeting on a quarterly basis to ensure performance against objectives is on target and actions against variances agreed. This scorecard approach will be rolled out across the CCA Group in 2013.

All managers in CCA have responsibility for assisting in the achievement of the diversity goals. The Human Resources function is responsible for the development and maintenance of the policy, education and training, and monitoring of relevant gender statistics. In 2012 a Diversity and Inclusion Manager was appointed, this new position was created to ensure the relevant level of expertise and capabilities are available internally and provide appropriate focus. This manager is also responsible for reviewing external best practice and adopting key learnings across the CCA Group.

Gender Diversity Targets

Diversity targets and Progress to Date for the CCA Board and Senior Executives

Female % non-Executive Directors2011 Actual 252012 Actual 252014 Target 302016 Target 33Senior Executives2011 Actual 162012 Actual *212014 Target 192016 Target 22

Diversity targets for CCA GrouptotalCCA

Group %

Australia & new

Zealand%

Indonesia, PnG

& Fiji %

Female Managers2011 Actual 26 28 212012 Actual 27 30 222014 Target 29 31 222016 Target 32 34 24

totalCCA

Group %

Australia & new

Zealand%

Indonesia, PnG

& Fiji %

Female All Employees

2011 Actual 17 29 8

2012 Actual 17 29 9

2014 Target 18 31 8

2016 Target 19 34 8

* A calibration exercise which resulted in the regrading of a number of management positions in this small group is the main contributor to the increased of female Senior Executives in 2012.

In order to achieve the 2016 target CCA is required to retain the existing female managers and appoint an additional 119 females into positions in this management group. Given the relatively low levels of turnover, and CCA’s commitment to make selection decisions based purely on merit, this target is considered both aspirational and stretching.

The developing markets of Indonesia, PNG & Fiji have a large combined workforce which includes a high manual labour component, resulting in a strong orientation to male employees in these countries.

COCA-COLA AMATIL LIMITED ANNUAL REPORT 2012 12

corporate governance stateMent (continueD)

The CCA Diversity Strategy

The CCA Diversity Strategy, originally developed in Australia, has been appropriately adopted across the Group. The strategy is based around threecorepillars,detailedbelow,andcountryspecificinitiativeshavebeen designed and implemented locally.

1. Sourcing – Attracting and actively searching for the best and most diverse range of talent in the market.

2. Inclusion – Creating an environment that recognises and celebrates difference, a viable CCA community.

3. Retention – Doing the right and fair thing, retaining our best talent, becoming an Employer of Choice.

Sourcing:

Various initiatives have been adopted which focus on sourcing talent for roles at all levels of the organisation. Recruitment processes have been reviewed and updated where necessary to eliminate bias and ensure the criteria for selection are based purely on suitability to perform the role. Some examples of progress include:

-InAustralia,CCA’sonlinerecruitmentprocesswasrefinedin2012,including the introduction of four voluntary diversity questions to the online application process. As a result of this change, CCA can now monitor online application rates by four demographic categories including gender and indigenous cultural identity. A baseline has been established from the 2012 data which will be monitored to maintain CCA’s focus on achieving high quality and diverse recruitment shortlists.

- Performance measures for all recruitment specialists in Australia were introduced to ensure that gender diverse shortlists are generated for vacancies. In addition, approximately 60 Human Resources and recruitment specialists attended “unconscious bias and equitable recruitment” training and are responsible for supporting line managers in making objective hiring decisions. In 2012, approximately 42% of all external hires were female, a 9% increase on the previous year.

- Graduate programmes have been a very successful vehicle for attracting high potential female employees to the organisation. Since 2010, Indonesia has recruited 219 graduates into the Trainee Programme, 54% of which have been female. In New Zealand, 66% of the most recent graduate intake was female and the NZ team have successfully supported females in securing permanent positions and pursuing CCA careers in traditionally male oriented roles on completion of the graduate trainee programme.

- CCA New Zealand is a long standing sponsor of the First Foundation Scholarship, a charitable programme which awards scholarships to high potential students from the Polynesian and Maori communities. ThesupporttakestheformoffinancialassistancetowardsUniversityfees, paid work experience and access to mentoring throughout the scholars’ time at University. The two most recent students awarded the scholarship by CCA New Zealand are both female.

Inclusion:

In 2012, CCA continued to invest in diversity education programmes. Diversity awareness is included in management induction programmes and initiatives have been targeted at creating an environment which encourages all employees to provide feedback to the business and participate in development activities.

- The “Women’s Mentoring Program” in CCA Australia, which is aimed at strengthening the pipeline of future female leaders, was extended, with 77 females participating in the program nationally. A complementary male program “Mastering Gender Leadership” was piloted in Victoria with 24 male managers, and feedback from the both the Women’s Mentoring Program and Mastering Gender Leadership programs will be used to develop new customised CCA training material in 2013.

- CCA Australia also implemented gender leadership and unconscious bias training to approximately 95 Sales and Customer Service managers. This function was prioritised because it had historically experienced lower levels of female participation and results are already evident with the highest annual increase in female participation being recorded in 2012. The training will continue to be rolled out to other areas of the business during 2013.

- Addressing cultural attitudes to women in the workplace has also been area of focus within the inclusion pillar of the strategy. A large range of initiatives have been executed, including establishment of an Internal Women’s Empowerment Committee in New Zealand, chaired by a recently appointed female member of the Executive Team. This committee’s work is supported by an Intranet Networking Group. In Fiji, a senior female executive hosts a series of focus groups within the business to gather feedback and suggestions from female employees on how to improve the Fiji business as a great place to work for women. The outcomes are shared with the Human Resources Manager and form the basis of the local diversity initiatives.

Retention:

Retaining female employees is a critical factor in ensuring the business benefitsofgenderdiversityareachieved.Opportunitiesforcareerdevelopment and training are available to all employees and progress is monitored through the Organisation Capability Review (OCR). This process is core to CCA’s talent management practices and ensures that internal promotions are based on merit and objective assessment is used in succession planning.

- The OCR process enables local teams to track statistics of high potential employees and ensures programs are put in place to improve and maintain diversity in leadership. This enables CCA to predict futuresuccessbyensuringsuccessionpoolsaccuratelyreflect diversity targets.

- Throughout 2012 CCA Australia’s national Embracing Difference Council continued to guide the execution of the diversity strategy, and in recognition of the importance of diversity to CCA’s progress, the council will be chaired in 2013 by CCA’s Australian Beverages Managing Director.

- CCA Indonesia have focused on retention of employees recruited through the Graduate Trainee Programme and have succeeded in retaining 88% of females graduates from intakes over the last three years. This compares to a retention rate of 79% of male graduates for the same period.

-Onekeythemeidentifiedfromemployeefeedbackwasadesiretobalance work and family commitments, as well as tailoring employee benefits.Asaresultofthisfeedback,CCAAustraliaundertookareviewofemployeebenefitsandinlate2012introducedanewCorporate Family Programme. This includes two online information portals; one aimed at supporting new parents and parents with childcare responsibilities, and the other focussed on providing support to employees who are considering retirement or have caring responsibilities for elderly family members. The utilisation of these andotherbenefitswillbemonitoredthroughout2013,andfurtherrefinementsmaybemadetoensurethatCCAcontinuestoprovidemeaningfulandattractiveemployeebenefitswhichfitwiththeoverallDiversity Strategy.

COCA-COLA AMATIL LIMITED ANNUAL REPORT 201213

Indigenous Employment Program

In 2011 CCA joined the Australian Employment Covenant and committed to place 150 Aborigines into jobs. As part of that ongoing commitment, in March 2012 CCA engaged former Wallaby rugby star Glen Ella in the newly created position of National Indigenous ProgramManager.MrEllaisresponsibleforraisingtheprofileof CCA’s Indigenous Program as well as strengthening ties with communities and indigenous organisations.

Under the Program, four new traineeship positions across CCA’s Human Resources and Finance departments were introduced; CCA advertised job vacancies on the Australian Employment Covenant website and established a national network of indigenous employment partners. CCA also further developed relationships with indigenous organisations and schools.

In total 29 new Indigenous employees commenced work with CCA in 2012.

For more information on CCA’s full Indigenous strategy which includes the Coca-Cola Australia Foundation’s partnerships with indigenous education organisations and CCA’s Remote Communities Strategy, a sales program aimed at increasing the take up of low or no sugar beverages and spring water in Indigenous communities, can be found in CCA’s corporate responsibility report, Sustainability@CCA on the company website.

Audit & Risk Committee

The Audit & Risk Committee comprises at least three Non-Executive Directors, the majority of whom are Independent. The Group ManagingDirectorandGroupChiefFinancialOfficerattendmeetingsby invitation.

The key responsibilities of the Committee are: Financial Reporting – review Financial Statements to ensure the appropriateness of accounting policies, and compliance with accounting policies and standards, compliance with statutory requirements and the adequacy of disclosure; Risk Management – ensure CCA has effective policies in place covering key risks including, but not limited to, overall business risk in CCA’s operations, treasury risk (including currency and borrowing risk), procurement, insurance, taxation and litigation; Audit – review of the auditor’s performance, the professional independence of the auditor, audit policies, procedures and reports, as a direct link between the Board and the auditor.

The Committee approves the policies, processes and framework for identifying, analysing and addressing complaints (including whistleblowing) and reviews material complaints and their resolution.

PRInCIPlE 4: SAFEGuARD IntEGRItY In FInAnCIAl REPORtInG

The Board has an Audit & Risk Committee which meets four times a year and reports to the Board on any matters relevant to the Committee’s role and responsibilities. A summary of the Committee’s formal Charter is set out below.

PRInCIPlE 5: MAkE tIMElY AnD BAlAnCED DISClOSuRE

CCA has a Disclosure & Communication Policy which includes the following principles, consistent with the continuous disclosure obligationsunderASXListingRulesthatgovernCCA’scommunication:

•CCAwill,inaccordancewithASXListingRules,immediatelyissuetoASXanyinformationthatareasonablepersonwouldexpecttohaveamaterial effect on the price or value of CCA’s securities;

• CCA’s Disclosure Committee manages the day-to-day continuous disclosureissuesandoperatesflexiblyandinformally.Itisresponsiblefor compliance, coordinating disclosure and educating employees about CCA’s communication policy; and

•allmaterialinformationissuedtotheASX,theAnnualReports,fullyear and half year results and presentation material given to analysts, is published on CCA’s website (www.ccamatil.com). Any person wishingtoreceiveadvicebyemailofCCA’sASXannouncementscanregister at www.ccamatil.com.

The Company Secretary is the primary person responsible for communicationwithASX.IntheabsenceoftheCompanySecretary,the Investor Relations Manager is the contact. Only authorised spokespersons can communicate on behalf of the Company with shareholders, the media or the investment community.

PRInCIPlE 6: RESPECt tHE RIGHtS OF SHAREHOlDERS

The rights of CCA’s shareholders are detailed in CCA’s Constitution. Those rights include electing the members of the Board. In addition, shareholders have the right to vote on important matters which have an impact on CCA. To allow shareholders to effectively exercise these rights, the Board is committed to improving the communication to shareholders of high quality, relevant and useful information in a timely manner.

CCA’s Disclosure & Communication Policy requires that shareholders be informed about strategic objectives and major developments. CCA is committed to keeping shareholders informed and improving accessibility to shareholders through:

•AustralianSecuritiesExchange(ASX)announcements;• company publications (including the Annual Report and

Shareholder News); •webcastinganalystandmediabriefings;• the Annual General Meeting; • the Company website (www.ccamatil.com); • the investor relations contact number (61 2 9259 6159); and • a suggestion box on the website.

CCA’s shareholders are encouraged to make their views known to the Company and to directly raise matters of concern. From time to time, CCA requests meetings with its shareholders and shareholder interest groups to share views on matters of interest. The views of those parties are shared with the Board on a regular basis, both by the Chairman and management.

Shareholders are encouraged to attend CCA’s Annual General Meeting and use this opportunity to ask questions. The Annual General Meeting will remain the main opportunity each year for the majority of shareholders to comment and to question CCA’s Board and management. The external auditor attends the Annual General Meeting and is available to answer shareholder questions about the conduct of the audit and the preparation and content of the auditor’s report.

COCA-COLA AMATIL LIMITED ANNUAL REPORT 2012 14

corporate governance stateMent (continueD)

PRInCIPlE 7: RECOGnISE AnD MAnAGE RISk

The Board has established a Risk Management Policy which formalises CCA’s approach to the oversight and management of material business risks. The policy is implemented through a top down and bottom up approach to identifying, assessing, monitoring and managing key risks across CCA’s business units. Risks, and the effectiveness of their management, are reviewed and reported regularly to relevant management, the Audit & Risk Committee and the Board. Management has reported to the Board that the Company’s risk management and internalcomplianceandcontrolsystemisoperatingefficientlyandeffectively in all material respects.

The Board is responsible for ensuring that there are adequate systems and procedures in place to identify, assess, monitor and manage risks. CCA’s Audit & Risk Committee reviews reports by members of the management team (and independent advisers, where appropriate) during the year and, where appropriate, makes recommendations to the Board in respect of:

• overall business risk in CCA’s countries of operation; • treasury risk (including currency and borrowing risks); • procurement; • insurance; • taxation; • litigation; • fraud and code of conduct violations; and• other matters as it deems appropriate.

The internal and external audit functions, which are separate and independent of each other, also review CCA’s risk assessment and risk management.

In addition to the risk management duties of the Audit & Risk Committee, the Board has retained responsibility for approving the strategic direction of CCA and ensuring the maintenance of the highest standards of quality. This extends beyond product quality to encompass all ways in which CCA’s reputation and its products are measured. The Board monitors this responsibility through the receipt of regular risk reports and management presentations.

Financial Reporting

In accordance with section 295A of the Corporations Act 2001, the Group ManagingDirectorandChiefFinancialOfficerhaveprovidedawrittenCertificatetotheBoardthattheStatutoryAccountsoftheCompanycomply with the relevant Accounting Standards and other mandatory reporting requirements in all material respects, that they give a true andfairview,inallmaterialrespects,ofthefinancialpositionandperformance of the Company, and that management’s risk management andinternalcontrolsoverfinancialreporting,whichimplementthepolicies and procedures adopted by the Board, are operating effectively andefficiently,inallmaterialrespects.

PRInCIPlE 8: REMunERAtE FAIRlY AnD RESPOnSIBlY

On an annual basis, the Compensation Committee reviews the nature and amount of the remuneration of the Group Managing Director and senior management and, where appropriate, makes recommendations to the Board. As noted in the Remuneration Report on page 36, the Committee draws on a range of services from external consultants to provide information, data and advice where appropriate in relation to remuneration quantum & structure and market practice. Where a consultant is providing a recommendation in accordance with the Corporations Act 2001, CCA has developed practices to select and engage a consultant -

• on how CCA is to receive the advice;• on how to ensure independence from management; and • on how the consultant interacts with management.

CCA recognises the importance of ensuring that any recommendations given in relation to the remuneration of KMP provided by remuneration consultants are provided independently of those to whom the recommendations relate.

OtHER BOARD COMMIttEES

To assist in its deliberations, the Board has established a further two committees, the Administration Committee and the Securities Committee. These Committees are comprised of any two Directors or aDirectorandtheGroupChiefFinancialOfficerandmeetasrequired.The Administration Committee‘s powers, while not limited, will generally be applied to matters of administration on behalf of the Board, including the execution of documents in the normal course of business. The Securities Committee attends to routine matters relating to the allotment of securities.

Compensation Committee

The Compensation Committee comprises at least three Non-Executive Directors, the majority of whom are independent Directors. The Group Managing Director attends by invitation. Appropriate periods of time are set aside for only Committee members to be in attendance.

The Committee reviews matters relating to the remuneration of the Executive Director, senior management and Non-Executive Directors. It also reviews senior management succession planning, country retirement plans and remuneration by gender and considers diversity in the context of succession planning. The Committee obtains advice from external remuneration consultants to ensure that CCA’s remuneration practices are in line with market conditions. On at least an annual basis, the Committee reviews the succession plans for the Group Managing Director and senior executives.

COCA-COLA AMATIL LIMITED ANNUAL REPORT 201215

Directors’ reportCOCA-COLA AMATIL LIMITEDFOR THE FINANCIAL YEAR ENDED 31 DECEMBER 2012

TheDirectorssubmithereundertheirReportforthefinancialyearended31December2012.

nAMES AnD PARtICulARS OF DIRECtORS

ThenamesoftheDirectorsofCoca-ColaAmatilLimited(Company,CCAorCCAEntity)inofficeduringthefinancialyearanduntilthedateofthisReportand each Director’s holdings of shares and share rights in the Company are detailed below –

Particularsofthequalifications,otherdirectorships,experienceandspecialresponsibilitiesofeachDirectoraresetoutonpages5and6ofthe Annual Report.

DIVIDEnDS

OrdinaryShares

no.

long term IncentiveShare Rights Plan (ltISRP)

share rights1

no.David Michael Gonski, AC 393,380 –Ilana Rachel Atlas 5,000 –Catherine Michelle Brenner 14,083 –Terry James Davis 524,071 613,785Anthony Grant Froggatt 38,928 –Martin Jansen 10,173 –Geoffrey James Kelly 22,460 –Wallace Macarthur King, AO 55,516 –David Edward Meiklejohn, AM 25,497 –

Rate per share ¢

Amount $M

Date paid or payable

Dividends declared on ordinary shares for 2012 (not recognised as liabilities) –Final dividend (franked to 75%) 32.0 243.9 2 April 2013Special dividend (unfranked) 3.5 26.7 2 April 2013

Dividendspaidonordinarysharesinthefinancialyear–Final dividend for 2011 (franked to 100%) 30.5 231.7 3 April 2012Interim dividend for 2012 (franked to 100%) 24.0 182.7 2 October 2012

1. Consists of vested share rights for the 2010-2012 plan plus the maximum number of unvested share rights in the 2011-2013 and 2012-2014 plans.

OPERAtInG AnD FInAnCIAl REVIEW

Principal activities and operations

TheprincipalactivitiesofCoca-ColaAmatilLimitedanditssubsidiaries(GrouporCCAGroup)duringthefinancialyearended31December2012were–

• the manufacture, distribution and marketing of carbonated soft drinks, still and mineral waters, fruit juices, coffee and other alcohol free beverages;• the processing and marketing of fruits, vegetables and other food products; and• the manufacture and distribution of alcohol ready-to-drink products, and the distribution of premium spirits and beer brands.

The Group’s principal operations were in Australia, New Zealand, Fiji, Indonesia and Papua New Guinea (PNG).

Financial results

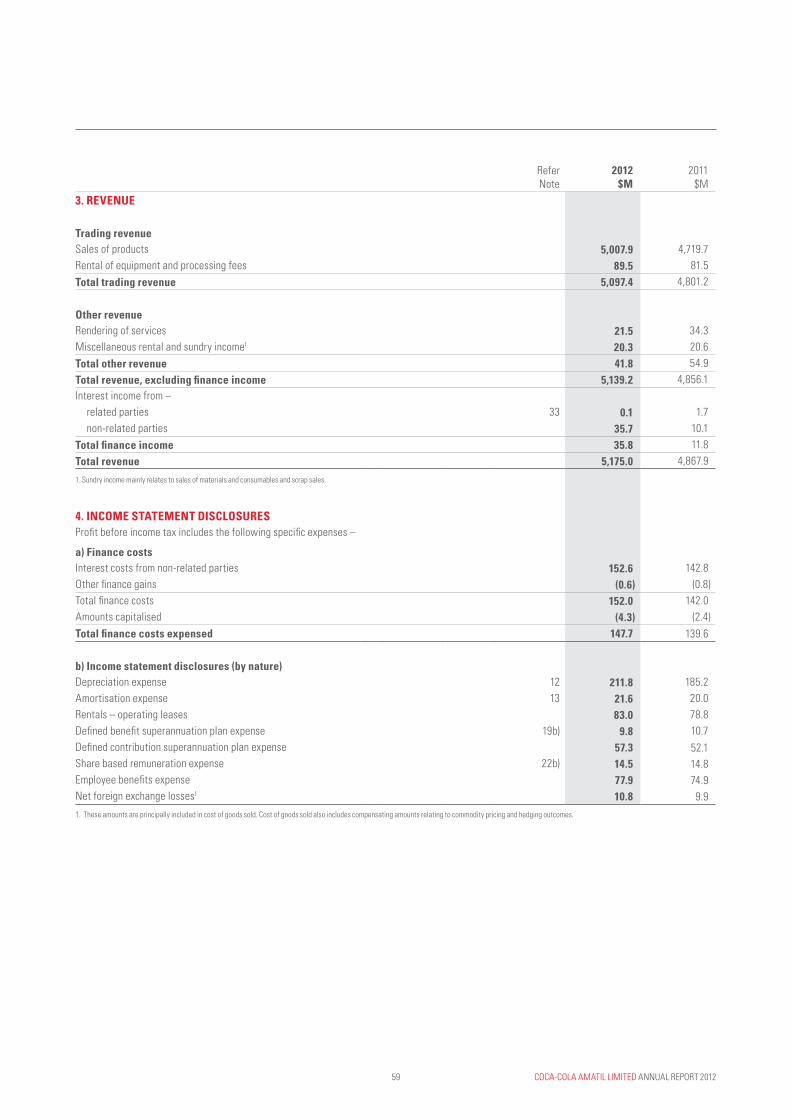

TheGroup’snetprofitattributabletomembersoftheCompanywas$459.9million,comparedwith$591.8millionin2011.Thenetprofitattributabletomembersincludesanetsignificantitemlossof$98.5millionafterincometax,relatingtoagainondiscontinuationofabusinessacquisition,gainon Cascade related transactions and restructuring expenses attributable to the alcohol strategy and ongoing restructure of the SPC Ardmona (SPCA) business.Thecorrespondingperiodin2011includesanetsignificantitemgainof$59.8millionafterincometax,relatingtoarevaluationgaintofairvalueofCCA’s50%interestinPacificBeveragesPtyLtd(PacificBeverages)andcertainexpensesthataredirectlyattributabletothesale,theseparationofthePacificBeveragesbusinessfromCCAandtheresultingstrategicrestructureofCCA,andexpensesarisingfromtheSPCAbusinessrestructure.RefertoNotes4c)and5tothefinancialstatementsforfurtherdetails.

TheGroup’stradingrevenueforthefinancialyearincreasedby6.2%to$5,097.4million,comparedwith$4,801.2millionfor2011.TheGroup’searningsbeforeinterestandtax(EBIT)andsignificantitemsforthefinancialyearincreasedby3.1%to$895.5million,comparedwith$868.9millionfor2011.

Operatingcashflowincreasedby15.6%to$741.9million,comparedwith$641.8millionin2011.

COCA-COLA AMATIL LIMITED ANNUAL REPORT 2012 16

Directors’ report (continueD)COCA-COLA AMATIL LIMITEDFOR THE FINANCIAL YEAR ENDED 31 DECEMBER 2012

OPERAtInG AnD FInAnCIAl REVIEW (CONTINuED)

Review of operations

Segmentresult(definedasearningsbeforeinterest,taxandsignificantitems)foreachoperatingsegmentwasasfollows–

• Non-Alcohol Beverage business – Australiaincreasedby3.3%to$627.4million,comparedwith$607.2millionin2011; NewZealand&Fijiwas$70.1million,comparedwith$79.5millionin2011; Indonesia&PNGincreasedby16.8%to$102.9million,comparedwith$88.1millionin2011;and

•Alcohol,Food&Servicesbusinessincreasedby2.0%to$95.1million,comparedwith$93.2millionin2011.

FurtherdetailsoftheoperationsoftheGroupduringthefinancialyeararesetoutonpages1to5oftheAnnualReport.

Significant changes in the state of affairs

InAugust2012,CCAlent$24.4milliontotheAustralianBeerCompany,partoftheCasellagroup.TheloanwillconvertintoanequityinterestintheAustralian Beer Company after the expiration of CCA’s restraint on selling beer in Australia on 16 December 2013.

InSeptember2012,CCAacquiredan89.6%shareholdingofParadiseBeverages(Fiji)Ltd(formerlyknownasFoster’sGroupPacificLimited)forapurchaseconsiderationofapproximately$59.7million.

Duringthefinancialyear,CCAalsoacquiredvariousindividuallyimmaterialbusinesseswithinthebeverageindustry.

IntheopinionoftheDirectors,therehavebeennoothersignificantchangesintheGroup’sstateofaffairsorprincipalactivitiesduringthe12months to 31 December 2012.

Future developments

Information on the future developments of the Group and its business strategies are included in the front section of the Annual Report.