14

Disability Income Insurance Catastrophic Disability Benefit Rider (CAT) (Available at an Additional Cost) For Producer Use Only. Not For Use with The Public. C:57865

| Date post: | 24-Dec-2015 |

| Category: |

Documents |

| Upload: | neal-maximilian-walton |

| View: | 214 times |

| Download: | 0 times |

Disability Income Insurance

Catastrophic Disability Benefit Rider (CAT)(Available at an Additional Cost)

For Producer Use Only. Not For Use with The Public.

C:57865

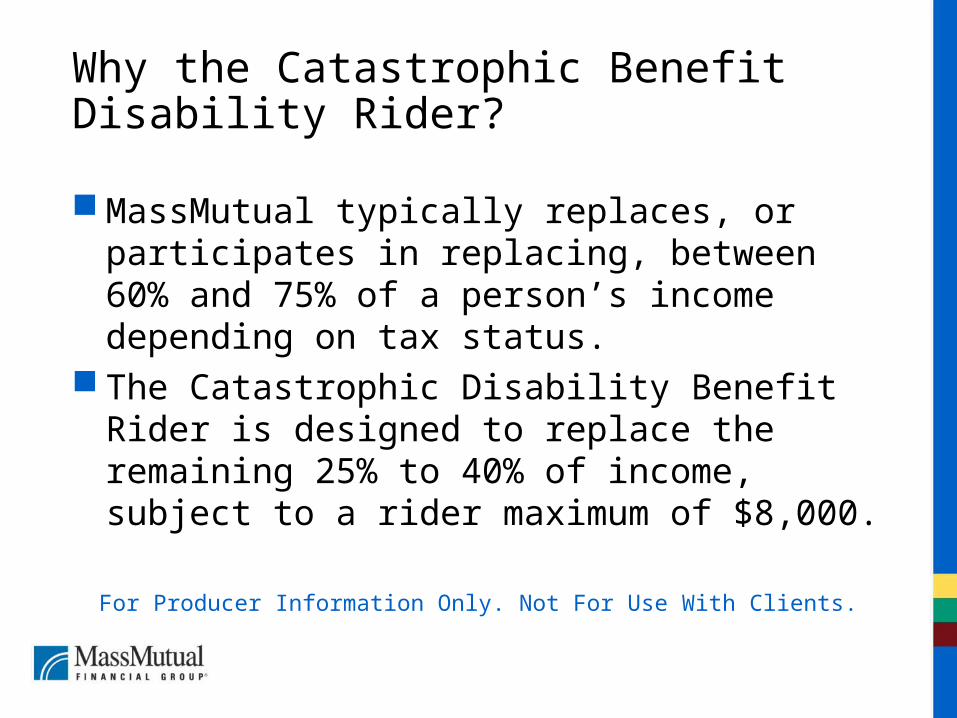

Why the Catastrophic Benefit Disability Rider?

MassMutual typically replaces, or participates in replacing, between 60% and 75% of a person’s income depending on tax status.

The Catastrophic Disability Benefit Rider is designed to replace the remaining 25% to 40% of income, subject to a rider maximum of $8,000.

For Producer Information Only. Not For Use With Clients.

What Does It Cover?

Presumptive Disability - covered by both the base contract and the rider

Severe Cognitive Impairment (Alzheimer’s, dementia, etc.) plus the definition of Total Disability on the base contract

Cannot perform 2 out of 6 Activities of Daily Living (ADLs – bathing, continence, dressing, eating, toileting, transferring ) plus the definition of Total Disability on the base contract.

For Producer Information Only. Not For Use With Clients.

Plan Design & Underwriting

Insures up to 100% of income (at time of original policy issue), subject to a maximum of $8,000

Available under all base benefit periods (base can be less than, greater than or equal to the CAT benefit period subject to underwriting approval)

Waiting period must match base Can increase CAT rider with full underwriting

can use Right to Apply cannot use FIO/AABI

For Producer Information Only. Not For Use With Clients.

Plan Design & Underwriting Cannot be added to a RetireGuard Stand Alone

policy Is available with the following new policies:

Radius® 04 Series MaxElect FlexElect Multi-Life FlexElect Individual

Can be added to the following in force policies: Radius 01Series Radius 98 Series FlexElect Multi-life FlexElect Individual

For Producer Information Only. Not For Use With Clients.

Plan Design & Underwriting

The CAT rider will not be offered to those clients who are currently over insured based on income.

We will, however, issue the CAT rider to those clients who are over our maximum I&P limits, not to exceed $8,000 per month.

Let’s look at a few examples!

For Producer Information Only. Not For Use With Clients.

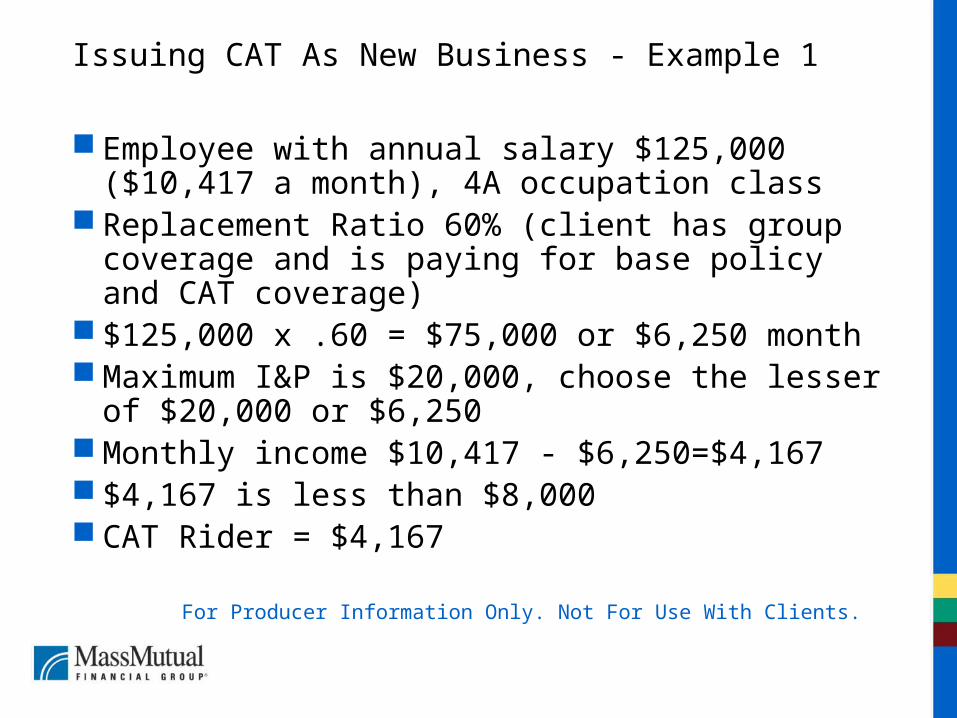

Issuing CAT As New Business - Example 1

Employee with annual salary $125,000 ($10,417 a month), 4A occupation class

Replacement Ratio 60% (client has group coverage and is paying for base policy and CAT coverage)

$125,000 x .60 = $75,000 or $6,250 month Maximum I&P is $20,000, choose the lesser of

$20,000 or $6,250 Monthly income $10,417 - $6,250=$4,167 $4,167 is less than $8,000 CAT Rider = $4,167

For Producer Information Only. Not For Use With Clients.

Issuing CAT As New Business – Example 2

Business owner annual earned income of $80,000 or $6,667 month, 3A occupation

No group LTD and client is paying for base and CAT so we will use “Non-Taxable Issue Limit Chart-No Group”

Table Issue Limit is $4,000 Maximum Issue Limit is $10,000, choose lesser so

we will use $4,000 $6,667 - $4,000 = $2,667 $2,667 is less than $8,000 CAT Rider = $2,667

For Producer Information Only. Not For Use With Clients.

Adding CAT to In Force Business

1. Determine client’s monthly earned income2. Determine total in force coverage from all sources (MM and non-MM)3. Is client over insured based on income?

If Yes – CAT is not available If No – Continue

4. Determine if client’s total in force coverage exceeds our Maximum I&P limits

If No – Continue to Step 6 If Yes – new CAT maximum established (step 5)

5. New CAT Maximum = $8,000 minus amount over Maximum I&P6. CAT = Monthly Income minus greater of:

Maximum coverage available based Maximum I&P, or Total in force coverage subject to CAT maximum (lesser of $8,000 or

new CAT maximum)

For Producer Information Only. Not For Use With Clients.

Adding CAT to In Force Business-Example 1

Earned income annual salary $360,000, $30,000 a month, 3P occupation class

Total in force coverage is $12,000 Client is NOT over insured based on income (60%

Replacement Ratio = $18,000) Client IS over Maximum I&P of $10,000 ($2,000 over

insured) New CAT Maximum ($8,000-$2,000)=$6,000 $30,000 -$12,000 = $18,000, subject to $6,000 new

CAT maximum CAT Rider = $6,000

For Producer Information Only. Not For Use With Clients.

Adding CAT to In Force Business – Example 2

Insured’s earned annual income is $120,000, $10,000 a month, 4A occupation class

Total in force coverage is $5,000 Client is NOT over insured based on income

($5,640 available - No Group, Non-Taxable Table) Client is NOT over Maximum I&P Limit ($15,000

limit) $10,000 - $5,640 = $4,360 CAT Rider = $4,360

For Producer Information Only. Not For Use With Clients.

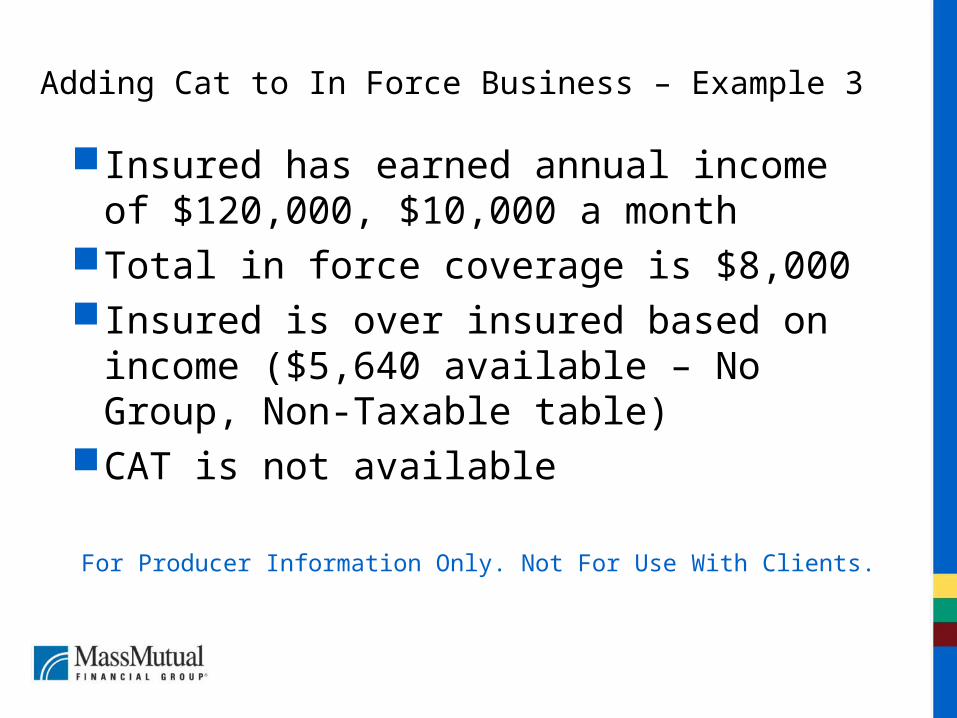

Adding Cat to In Force Business – Example 3

Insured has earned annual income of $120,000, $10,000 a month

Total in force coverage is $8,000Insured is over insured based on income

($5,640 available – No Group, Non-Taxable table)

CAT is not available

For Producer Information Only. Not For Use With Clients.

Positioning CAT in the Market

Aligns with consumer perception of being irreversibly incapacitated and in need of catastrophic coverage

For certain critical disabilities, enables a higher income replacement when most needed

Catastrophic Rider costs, on average, about 8-10% of the base “total disability only” premium.

Presumptive disability covered through both base and CAT rider.

This rider should be quoted on all new business!!!!

For Producer Information Only. Not For Use With Clients.

Massachusetts Mutual Life Insurance Company and affiliates, Springfield, MA 01111-0001 • www.massmutual.comMassMutual Financial Group is a marketing designation (or fleet name) for Massachusetts Mutual Life Insurance Company (MassMutual) and its affiliates.