ABSTRACT. Within discourse theory, language isseen as constitutive of reality. Furthermore, facts andvalues are viewed as inseparable. This has conse-quences for business ethics. In this paper the rela-tionship between discourse theory and business ethicsis discussed. Both the descriptive and prescriptiveaspects of business ethics are taken into account.Furthermore, an example of an empirical study ispresented. A discourse analysis is concluded to answerthe questions of how bankers in Holland concep-tualize and thus treat their customers and whetherthere are differences between the largest three banks.The article contains the description of five differentdiscourses on customers within the banks.

Within business ethics, discourse theory is mostlydisregarded. Yet, discourse analysis can be veryinsightful when describing the normative side ofa company. In this article I will first discussseveral possibilities that can be used to describeand compare the way Dutch bankers treat theircustomers. I will conclude that discourse theoryis very promising for that purpose. Then I willdiscuss some of the effects discourse theory canhave on (descriptive) business ethics and whatapplied ethics (prescription) would look likewithin discourse theory. After that I will give anexample of an empirical study of Dutch bankers,

using discourse analysis. When confronted withquestions of how to describe the normative sideof banks, and how to compare the ways they treattheir customers, discourse theory turns out to bevery helpful.

Describing the normative side of banks

In Holland the three largest banks dealing withprivate businesses are ING, ABN-Amro andRabobank. In my research project I asked myselfthe following questions: how do the three largestbanks in Holland treat their customers? And: arethere differences in the way they treat theircustomers?2 The answers to these questions arenot only relevant from an ethicist’s point of view,but the banks themselves are also very interestedin the answer.

As far as the differences between the banksare concerned, each of the three banks wouldargue that yes, they differ from each other. Thisis because all three have their own image andsee themselves as clearly different from theircompetitors. Rabobank for example is a co-operative company, not listed on any stockexchange. Therefore it doesn’t have to satisfyshareholders and according to Rabobank thismeans more than just a different legal way ofdoing business. Rabobank claims that (partly)because they don’t have to make a profit to satisfyshareholders, they treat their clients differently.

Before answering the two research-questions,I must first answer another question: what is thebest way to describe and compare the way inwhich the Rabobank, ING and ABN-Amro treattheir customers? This question, with a clearnormative side, is partly one of descriptive ethics.

Discourse Theory and BusinessEthics. The Case of Bankers’Conceptualizations of Customers1

Writing his Ph.D.-thesis, Gjalt de Graaf works at theFaculteit der Bedrijfskunde/Rotterdam School ofManagement of the Erasmus University Rotterdam.

In the business ethics literature, little atten-tion is paid to the way in which the morallyrelevant aspects of a company can be describedand analyzed (Kaptein, 1998, p. 5). In order togive an ethical judgement though (and prescrip-tion), the ethical issues must first be identified(description).

One way of describing and comparing com-panies in an ethical sense is looking at thecompany as a moral entity and studying theircodes of conduct. ABN-Amro recently declaredfour basic values in their code of conduct:respect, professionalism, integrity and teamwork.Rabobank on the other hand announced thesethree core values to the world: respect, expertiseand integrity. There is a striking similarity. Yet Iam not sure my research questions are answeredwith the conclusion that both banks treat theircustomers in the same way. Codes of conduct arethe result of lengthy consultations at the top-levelof how management should act. But of coursewhen formulating them, not only the real situ-ation, also the image of the company plays a bigrole. And even when the difference betweenthese is acknowledged and something is doneabout it, the results are far from certain. Recentresearch concludes that “the use of codes ofconduct alone in defining conduct, culture andperformance in the private sector may be lesseffective than their proponents think, and of lessimpact on managers and employees, customersand stakeholders than they would wish” (Doigand Wilson, 1998, p. 148). This conclusion is notsurprising. Morals and values must somehow liedeeper than something you can easily influencetop-bottom with some statements (Warren,1993). So if codes of conduct don’t tell the wholestory, what other ways are there to describe andcompare companies in the way they treat theircustomers?

Another possibility is looking at the moralagent. In the association model, the ethical sideof a company is reviewed by examining theemployees. The company is reduced to being thesum of individual actions. Employees can bescreened, for example, on the way they deal withthings such as their personal responsibilitytowards stakeholders, their own tasks and thecompany’s assets. The question then always

remains though, what this says about the orga-nization at large. What would happen if aresearcher would individually screen theemployees of an army (or a drug cartel) in thisway? Surely this wouldn’t reveal most (at least notthe most important) ethical questions about suchan organization.

I suggest an additional method for describingnormative issues of companies is looking at theway they talk about and view reality. Instead oflooking at the moral agents or the company as amoral entity, one can study a company’s internaldiscourse. With a discourse defined as “a lin-guistic practice that puts into play sets of rulesand procedures for the formation of objects,speakers, and thematics” (Shapiro, 1992, p. 108).In discourse theory, language is seen as consti-tutive of reality. With this viewpoint discoursetheory can have a very valuable contribution inbusiness ethics, because it means that studyingdiscursive practices within companies becomesvery insightful and revealing for business ethicists.Discourses produce organizations and the otherway around. Therefore, if the Rabobank, forexample, really treats their customers differentlycompared to their competitors, a researcher mustbe able to find more than some official statementswhich say they do (or hear from individualemployees that they “always put the customerfirst”). In that case, the Rabobank must alsoconceptualize “a customer” differently, the word“customer” must function differently in theirinternal discourse. In the next two paragraphs Iwish to discuss discourse theory in more detail.First I will discuss the impact discourse theorycan have on description within business ethics,then I will do the same for applied ethics, pre-scription.

Business ethics and discourse theory,description

Discussions on the nature of truth have affectedsocial research in a profound way during the lastdecades. Instead of assuming a given world outthere that is waiting to be discovered, attentionis drawn by many to processes and ways throughwhich the world is represented in language.

300 Gjalt de Graaf

Discourses are constitutive of reality. By lookingat what people say and write, we can learn howthey construct their world. In poststructuralismfor example, language is not looked upon as aneutral means of communication, but as a processthat forms the objects and subjects of which wespeak: conversations always take place in a pre-constituted meaning and value system (Shapiro,1992, p. 10). For business studies this means thatlanguage is not just seen as reflective of what goeson in an organization; discourses and organiza-tions are one in the same. “That is, organizingbecomes communicating through the intersec-tion of discourse and text” (Putnam, 2000, p.225).

This development is very important forbusiness ethics, since discourses necessarilycontain both facts and values. A different lookat the truth-untruth dichotomy also means adifferent idea about the fact-value dichotomy. Tobe more precise: the strict dichotomy ceases toexist. The way one looks at the world, the wayone perceives the facts, necessarily determines theway one values it. Not only meaning, but alsovalues are immanent features of discourse. Assoon as managers of soccer clubs start to talk,for whatever reasons, about soccer as a “product”(a relatively new development), a whole newworld opens up around the same old game withnew opportunities, new managerial problems andnew ethical issues (Hawkes, 1998).

The “is” and “ought” influence each other incountless ways. Without the subjects of a dis-course being aware of it, values, causal assump-tions and problem perceptions affect each other.In our daily lives we jump so often between nor-mative and factual statements, that we don’trealize how much our views of facts determinewhether we see problems in the first place. Butwhen we study our discussions more carefully, wecan see that the “is” and “ought” are in veryclose conjunction. The problem definition andthe possible solutions are inseparable. Or asRandels recently put it: “worldview narrativesnot only describe particular understandings ofbusiness, but have important normative consid-erations. They are not merely stories, butconstrue how we do, can, or should view theworld, and how business people and corporations

act, can act and should act” (1998, p. 1299). Thethesis that meaning is constructed by and throughdiscourse has also implications for the notion ofethics itself. It is, as Hackley (1999b, p. 38) notes,“inseparable from ways of talking about anddoing ethics and ethical things”.

When facts and values are thus viewed asinseparable, this has an effect on business ethics:3

the object of the study changes. Not only purelynormative aspects are relevant, as seen bymanagers, but facts are important as well. Theobject of study becomes all discursive practices.It is through studying these discursive practices,combined with the different status discoursetheory attributes to them, that discourse theoryadds a new way of describing the normative sideof a company.

A discourse analysis can reveal ethical issuesof a company that would remain unrevealed withother methods. Traditional descriptive ethicsdeals with concepts like “normative choices” and“decision-making”. When one adopts the post-structuralist view however, this can be seen asonly part of the picture at best. The traditionalview can easily ignore all the nuances andcountless ways that determine the possible par-ticipants in the process in the first place, as wellas the terms in which things are problematized.The study of discursive practices offers businessethics a possibility to go beyond the typicalpassive grammar (Shapiro, 1992, p. 127) ofmanagers “faced with problems”. It inquires intothe way in which management thinking withincompanies tends to remain within narrow modesof problematization and offers a narrative aboutthe production of problems: why is somethingconsidered a problem (or not a problem), ratherthan just concentrate on answering the problemat hand. If there are many ethical issues that arenot perceived as such, just looking at the nor-mative choices managers say they face, is no morethan a small part of the normative picture. Many(ethical) aspects of society cannot be explainedby fundamental ethical choices. Discourse theorydoesn’t consider concepts like “motivation”,“intention” or “decisions” as the main causalconditions to explain behavior.4 Managers ofcompany A that mainly talk among themselvesabout customers as people out of which their

Discourse Theory and Business Ethics 301

company makes its profit, will ask themselvesdifferent (ethical) questions than managers fromcompany B who view their customers as col-leagues with shared interests. For example,managers of company B might consider it unfairto sell a certain product to a client, knowing thata different, cheaper product would do just aswell. Managers of company A would not see anethical problem here whatsoever. I am not sayingeither view is better in a business sense or in anethical sense, just that a different discourse (orworldview/belief system/frame/paradigm) leadsto different ethical questions.

Prescriptive business ethics and discoursetheory

One of the main points I tried to make duringmy discussion of discourse theory is that whereasin current business ethics facts and values aretreated as ontologically different, discourse theorytreats them as different sides of the same coin.This, of course, also has implications and newpossibilities for prescription in business ethics.

If discourse theory is capable of revealing moreethical issues, and if it brings different ethicalissues to the foreground, then this automaticallyleads to more issues/areas prescriptive ethics canbe applied to. First, one has to identify ethicalissues before one can formulate an opinion on it.Applied ethics can be very helpful at the momentan ethical question is raised. But when everyworldview contains many values, the fact that anethical question arises is as interesting as whatquestion is asked, as is the fact that many ethicalquestions are not asked. Every (non-) decision ofany manager in any company is a social activityand affects people’s lives (Hackley and Kitchen,1999a, p. 23). Therefore, applying ethics toonly obvious ethical questions within a companydeals at best with only a small portion (albeitsometimes a very important one) of the valuequestions involved. A discourse analysis is capableof revealing many different ethical sides andleaves therefore more room for ethics to have asay.

Applied ethics would look differently withindiscourse theory than within philosophical ethics.

It would be more like accommodating a processthan prescribing an outcome based on a philo-sophical ethical theory.5 Prescription withindiscourse theory consists of conflicting existingdiscourses and in that process try to influencethem. Within discourse theory one deals withdiscourses that are always “out there” (containingboth values and facts). Discourses are alwayswithin a context. When an ethicist wants tochange things in reality, discourse theory suggestsit might be more effective to conflict existingdiscourses, with their normative sides, instead ofconfronting managers with philosophical ethics.Roe (1994) and Van Eeten (1998) for examplehave interesting ideas of how to confront existingincommensurable discourses.

As I stated, every issue in daily managementhas its value implications. But this is oftenwithout the managers being aware of it. Thismight be one of the reasons why applied businessethics as a field isn’t as evolved as applied legalor medical ethics. Managers in these last twofields deal daily with issues they perceive as beingethical, so naturally they are more prone to turnfor help from philosophical ethics (Sorell, 1998).But when a discourse doesn’t perceive an issue asbeing ethical, the ethical discourse runs a greatrisk of not being understood. Even whenbusiness people find a certain philosophicaldiscussion interesting, they have a hard timerelating it to their daily problems. The ethics aretoo far removed from daily practice. In otherwords, the discourses are too different, they areincommensurable. When talking about the sameissue, ethicists and business people sometimes usedifferent terms and concepts and talk “past eachother”.6, 7 Within business ethics, philosophicalethics can play a very important role. Butsomehow the philosophical discourse within afield of applied ethics should move closer to daily(business) practices, or it will suffer from whatSorell (1998, p. 17) calls the alienation problem:the problem of the alienation of ethicists frompractitioners.

302 Gjalt de Graaf

An empirical study using discourse analysis

In order to show how discourse theory can beapplied in empirical studies, I will now get backto the study I introduced earlier in this paper.In the rest of this study I will describe andcompare the way Dutch bankers treat theircustomers using discourse analysis. I will showhow discourse analysis can be used as an alter-native way for conducting descriptive ethics.

The way customers are described in thediscourse of the three banks is ethically highlyrelevant. If we can learn something about howthe banks internally make sense of “customers”,it can provide great insight into their moralchoices. According to discourse theory, ifbank-managers speak differently about theircustomers, they will treat them differently. Buthow can a researcher look at the way the word“customer” functions within the internal discur-sive practices of the Rabobank, ING and ABN-Amro?

One of the ways the literature suggests toanalyze discourses is Q-methodology.8 This is themethodology used here. “Q study will generallyprove a genuine representation of that discourseas it exists within a larger population ofpersons . . . To put it another way, our units ofanalysis, when it comes to generalizations are notindividuals, but discourses” (Dryzek andBerejikian, 1993, p. 52). The discourses areexamined without pre-developed categories ofthe researcher. On the contrary, Q-methodologygives researchers the opportunity to reconstructthe discourses, in their own words, using onlythe words spoken by individuals actually involvedin the discourse.

In this article I won’t go into every detail ofQ-research. Only the main steps and relevantinformation for this study are presented.9

First, for Q-research, a concourse had to beconstructed. The concourse is supposed tocontain all the relevant different aspects of all thediscourses. It is up to the researcher to draw arepresentative sample from the concourse athand. In this case it contains statements usedinternally by the banks about the different aspectsof customers. In order to deconstruct the waysbanks talk about their customers, I used the word

customer as an organizing principle. All thestatements that used the word “customer” wereconsidered.

An important first decision is where exactly tolook for the discourses. Because almost allcontact between companies and banks is at a locallevel, I decided to look at the local branches ofthe three different banks for the statements of myconcourse.10 As a representative of each localbank, I took the local bank director. This is theperson in charge who should know how cus-tomers are dealt with within the local bank.Another advantage of local bank directors is thatthey all have considerable personal experiencein dealing with customers.

Ten open interviews were conducted withlocal bank directors (from the three differentbanks). In these interviews the directors wereinvited to talk about as many aspects of cus-tomers11 and dealing with customers as their timewould allow. These interviews were taped. Allliteral statements about customers and dealingwith customers were written down later. To thesestatements I added statements about customersthat I found in written documents producedby the banks. I also looked into the academicliterature on customer views of companies. A fewstatements were added from this source. Afterlooking at these sources, the concourse containedabout 150 statements. All (largely) overlappingstatements were thrown out. Finally, this list wasshown to the three participating banks and a fewcolleagues who are familiar with the bankingbusiness. The question was then asked whetherthe remaining statements contained all relevantissues. After suggestions from a bank and a col-league, a few statements were added. At the endof this stage my concourse was formed: 52 state-ments were gathered (in Q-methodology this iscalled the Q-set).12 I would like to stress thatmost statements are literal statements from bankdirectors. Some statements can be ambiguous tosome people. But that is the nature of language,therefore most statements were not edited.Ambiguity is resolved by each of the Q-sorters,who gave their own interpretation to thestatements (every bank director interpreted thestatements within his own worldview).

The next step was to decide who would be

Discourse Theory and Business Ethics 303

asked their opinion about the Q-set, or, in otherwords, asked to Q-sort the statements. In Q-methodology one has to construct a P-set, theperson samples. The P-set is the set of personswho are relevant to the problem (Brown, 1980,p. 192). Following the same logic of the Q-set,I decided to let local bank directors13 Q-sort the52 statements. These local bank directors wererandomly selected, 10 from each bank.Furthermore, I decided to structure the P-setaccording to the size of the municipality thebanks are located in, ranging from big cities tosmall rural villages.14

The 30 bank directors who were interviewed,were given a deck of 52 cards, containing the52 statements (the Q-set). Then they were askedto arrange the cards according to the degree theyagreed with the statements, with scores rangingfrom –3 to +3. The particular score an isolatedstatement received was not the most importantaspect. More importantly was the placement ofa particular statement among the other 51 state-ments. That’s why the respondents were askedto order the statements according to a fixeddistribution.15 (See Figure 1.)

The 2 statements they agreed with most, wereput on the right, the two they disagreed withmost on the left. The statements they felt indif-ferent about (or didn’t understand) were put inthe middle (the 0 category). The final distribu-tion is the Q-sort.16 After the Q-sorting, someopen questions were asked. This was done inorder to check whether the bank directors missedimportant issues, and also to gain more insightinto the discourses by asking about the reasonsbehind the choices they made. This helped mewith the final analysis of the different discourseslater on.

The 30 Q-sorts were analyzed using statisticalmethods. The idea is to look for patterns amongthe Q-sorts. Are there similar ways in which

In parenthesis are the defining variates (loadings !0.43, p < 0.001).The first ten subjects are from the Rabobank, from11 till 20 ABN-Amro and 21 till 30 ING.The first 3 of every bank are located in large cities 4through 7 from medium size communities and thelast 3 from small villages (see footnote 14).

Figure 2. Subjects’ factor loadings.

the 30 different directors have prioritized the 52statements? In this case I used factor-analysis,which is standard in Q-methodology. First acentroid factor analysis produced different factors,which were then rotated according to thevarimax rotation. This analysis led to five dif-ferent factors (an extraction of more than fivefactors, would have lead to statistically insignifi-cant factors). In Figure 2 the loadings of the 30Q-sorts are given on the five different factors.

The five discourses

The five factors form the backbone to recon-struct five discourses, five different ways to con-ceptualize customers. For each factor an idealizedQ-sort is computed (see the appendix). Thisrepresents how a hypothetical bank director witha 100% loading on a factor would have orderedthe 52 statements. Here, I will present the fivediscourses in the form of a label and a narrative(Dryzek and Berejikian, 1993, p. 52). When

reconstructing the discourse, special attention waspaid to the most salient statements and thediscriminating items. So the discourses are notconstructed by simply cutting and pasting state-ments, also taken into account is how thestatements are comparatively placed in the dif-ferent discourses (Dryzek and Berejikian, 1993,p. 52). Furthermore, the interviews after the Q-sorting were used to gain extra insight into thereason why the directors ordered the cards in theway they did. Some relevant statements for adiscourse are presented in smaller print, togetherwith the idealized score of the five discourses.

Similarities between bankers

Before I describe the five discourses, I would liketo stress that I also found many similaritiesbetween all the discourses. Some discourses arehighly correlated. Also, some statements wereordered virtually the same by the bank directors.Here are some noticeable examples:

Discourse Theory and Business Ethics 305

Discourse

A B C D E

36. Financial rates are an important part of doing business. But just as important for customers are good service and image. As a bank you should most of all communicate that you have the knowledge. +3 +3 +2 +3 +3

12. Financial rates are more important to our customers than a sense of involvement from our bank. –2 –1 –1 –2 –2

43. The average customer is someone who puts himself in the center, and in general doesn’t like banks very much. He is mainly focused on making profits. As a bank you feel more as an opponent than as a partner. –2 –3 –2 –3 –2

19. Ethics play a role in our business. This means not facilitating customers with activities that cross our boundaries. These boundaries go clearly further than just legal boundaries. We even ethically reprimand customers sometimes. –0 –0 –0 –0 +1

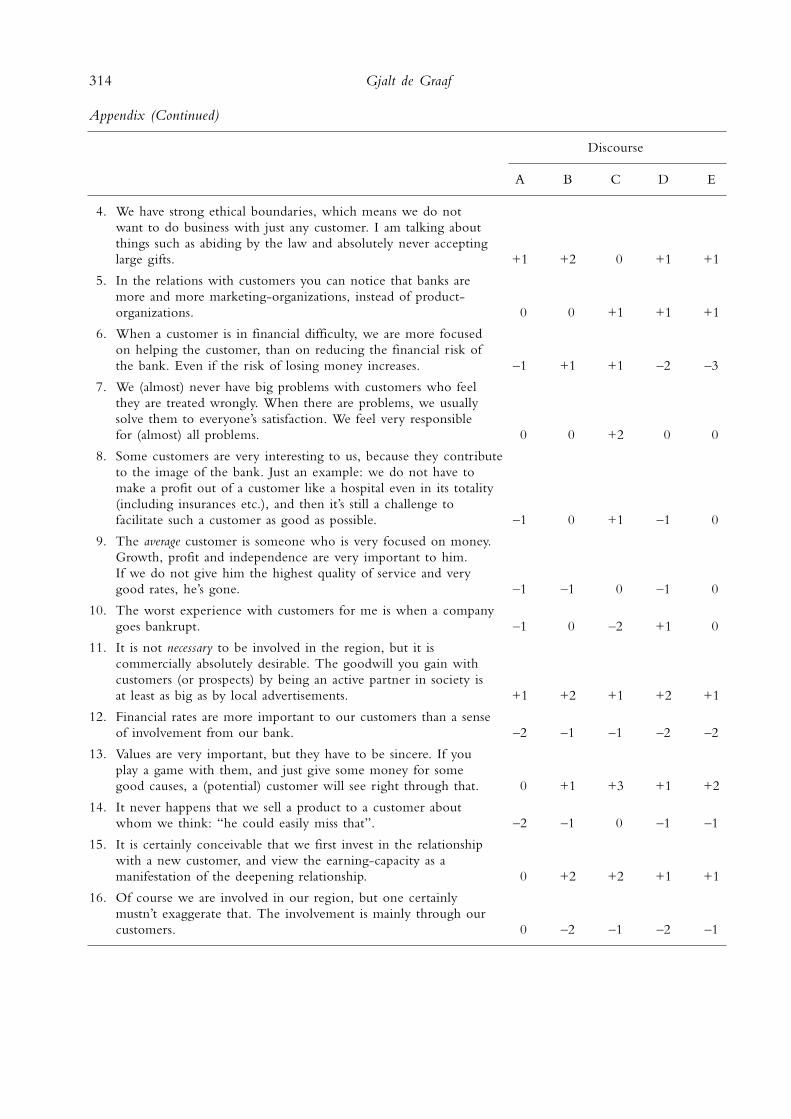

Furthermore, I did not find any bipolarfactors. This suggests the presence of consensuson several issues among the discourses. To anyonefamiliar with the banking business it should comeas no surprise that all the directors stressed in oneway or another that banking is a “peoplebusiness”. For every discourse, money and finan-cial rates certainly aren’t the all-dominatingthemes. Look for example at statement number36: this is a statement with very high agreementwithin all discourses, it certainly doesn’t dis-criminate amongst them.

To all banks, good service and knowledgeabout the business are very important. Earlier Imentioned that every Q-sorter was askedwhether he missed an important issue in thestatements. Even though most of them said no,the issues that were sometimes mentioned werethat professionalism and especially knowledgedidn’t get enough attention given their impor-tance.

Trust is seen as very important by all thebankers. Almost by definition money is abouttrust. When people lend or borrow money, theyonly periodically get to see printed figures on acheap piece of paper. Therefore, they must trustthat their money is in good hands. Also, inWestern society money is a very private business.A bank must first of all be trusted to respect acustomer’s privacy. Therefore, a bank can neverbe a pure opponent of a customer.

As far as the ethical rules within the threelargest banks in Holland are concerned, none ofthe banks go as far as ethically reprimandingcustomers. Furthermore, environmental sustain-ability is not a big issue. The environmental lawsare taken very seriously, but there doesn’t seemto be an active policy that goes any further thanthe legal restrictions of the Netherlands.

There are also very clear differences betweenthe five discourses in the way they conceptualizecustomers. The five discourses now follow.

306 Gjalt de Graaf

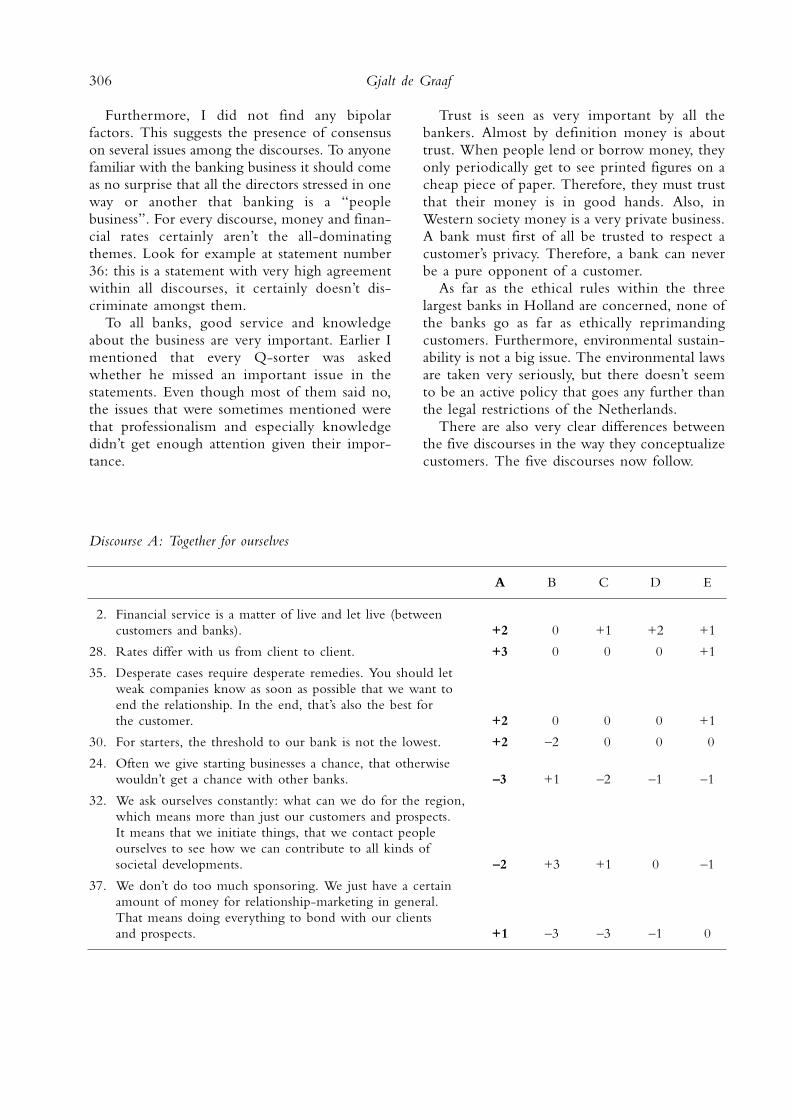

Discourse A: Together for ourselves

A B C D E

–2. Financial service is a matter of live and let live (between customers and banks). +2 –0 +1 +2 +1

28. Rates differ with us from client to client. +3 –0 –0 –0 +1

35. Desperate cases require desperate remedies. You should let weak companies know as soon as possible that we want to end the relationship. In the end, that’s also the best for the customer. +2 –0 –0 –0 +1

30. For starters, the threshold to our bank is not the lowest. +2 –2 –0 –0 –0

24. Often we give starting businesses a chance, that otherwise wouldn’t get a chance with other banks. –3 +1 –2 –1 –1

32. We ask ourselves constantly: what can we do for the region, which means more than just our customers and prospects. It means that we initiate things, that we contact people ourselves to see how we can contribute to all kinds of societal developments. –2 +3 +1 0 –1

37. We don’t do too much sponsoring. We just have a certain amount of money for relationship-marketing in general. That means doing everything to bond with our clients and prospects. +1 –3 –3 –1 0

For the bankers in discourse A, the relation-ship with customers must be mutually benefi-cial. The relationship with the customer is seenas one both have to gain from. The customersare very much seen as partners. Once a rela-tionship is established, the bankers of factor Awant much more out of their customers than justmaking a profit. There is a strong bonding withthe customer. This certainly doesn’t mean thatthe customer is always right. Nothing is done forfree. Financial service is a matter of live and letlive. It is seen as very inefficient to work hard fora customer who doesn’t make you better. Thebankers of discourse A are very focused onmaking both better. They are constantly lookingfor win-win situations while working togetherwith the customer against the rest of the world.Consequently, when the relationship is no longermutually beneficial, these bankers are not themost loyal, considering it best to end the rela-tionship. This is considered to be the most‘honest’ thing to do.

Since the relationship with the customer isvery important, bankers of discourse A havesome demands of their customers. Not justanyone is accepted. Starters for example have themost trouble getting a loan from bankers of factorA. After all, a new business is more risky andthe question is whether you will ever be able tomake a profit out of it. Accepting starters becauseit is good for the region as a whole, is not anissue. The region is of no concern to the banksin discourse A. This also means that sponsoringis not considered important, apart from pro-moting their own name. Customers are purelyjudged on their own merits. They call this being“positively critical”.

Once accepted however, customers get a verypersonal treatment. Bankers of discourse A don’tlook for automatic solutions. And since everycustomer is different, the treatment of eachcustomer is different, thus financial rates differvery strongly from customer to customer.

Discourse Theory and Business Ethics 307

Discourse B: Using the bank to improve the region

A B C D E

50. A customer is someone with whom you have partly common and partly opposing interests. He is a colleague and a competitor in one. –1 –2 +3 –0 –0

–6. When a customer is in financial difficulty, we are more focused on helping the customer, than on reducing the financial risk of the bank. Even if the risk of losing money increases. –1 +1 +1 –2 –3

22. At our bank, every customer pays the same rate for the same service. –3 –1 –3 –3 –3

32. We ask ourselves constantly: what can we do for the region, which means more than just our customers and prospects. It means that we initiate things, that we contact people ourselves to see how we can contribute to all kinds of societal developments. –2 +3 +1 –0 –1

37. We don’t do too much sponsoring. We just have a certain amount of money for relationship-marketing in general. That means doing everything to bond with our clients and prospects. +1 –3 –3 –1 –0

30. For starters, the threshold to our bank is not the lowest. +2 –2 –0 –0 –0–4. We have strong ethical boundaries, which means we do not

want to do business with just any customer. I am talking about things such as abiding by the law and absolutely never accepting large gifts. +1 +2 –0 +1 +1

The correlation between discourses A and Bis the lowest on any of the factors. The onlything they agree on is that the customer is cer-tainly not seen as a competitor. But for the restthe concept “customer” is completely different.For discourse B the main purpose of the rela-tionship is not just to have a win-win situation.Profit is not their main goal. There are otherimportant issues in the world besides each other(more on this later). Money is not so much thegoal, it is more the means to other things.

The broader interest of the customer is veryimportant, not just the direct interests. Withindiscourse A the interest of the customer is theinterest of the bank. In discourse B however, thecustomer is seen within a broader societalcontext. Yet, the direct interests of the customerare also very much in the foreground for bankersin discourse B. This inevitably leads to conflicts.Sometimes the broader context demands some-thing else from a banker than the direct finan-cial interest of a customer (for example how fardo you go with ethically reprimanding acustomer who crosses some ethical boundaries inpolluting the environment, when he doesn’t crossany legal boundaries). This conflict was oftenmentioned and seems to be one of the definingdaily struggles of bankers in discourse B.

When a customer is in trouble, of all thebanks, bankers of discourse B are the most pre-occupied with helping the client, instead ofreducing their own financial risk. Not that thedifferences in this respect are very big, banks willbe banks and all the banks have to keep aconstant strong eye on their own financial situ-ation. They will never go so far as structurallynot making a penny out of a customer. Theycertainly do not see themselves as charity insti-tutions. There is even less understanding,compared to the other discourses, for a customerwho also has a relationship with other banks.

The financial rates are not the same foreveryone, but are certainly more flat than at otherbanks. For customers, negotiating with bankersof factor B is the least useful of all the factors.No two customers are the same, but in principleif two customers are the same, they should paythe same rate for the same service. Just as rela-tionships in life, it is very important for thesebankers that they have “a good feeling” abouttheir customers. They also want customers to“feel at home” in their bank. The client is morelike a partner. You can never have the feeling thata customer is your competitor. Loans are givena little more on intuition than on pure businessplans, compared to the other discourses.

It is considered important to be an active partyin society, especially in one’s own region. Bankersof discourse B do not feel like this because it isgood for business, there is a genuine idealism.Both the bank and the customers are seen as partof the region the bank is located in. Again, thisis very much in contrast with discourse A. A lotof money is spent on sponsoring, because it helpsorganizations in the region, not so much thebank itself. Sponsoring is not just for their ownclients and prospects. Starters are seen as veryimportant to the region, thus they give thesebusinesses many opportunities.

The interests of the customers play a role, butwhen bankers of factor B have to make choices,it’s not that they want to improve the world nomatter what. It is certainly not the case that theyhave very stringent environmental rules for theircustomers. When they say that ethics are impor-tant, they mean respecting the law and neveraccepting a bribe, not in a wider ethical sense:they are not moralists with a clear idea of howto improve the world. They don’t reprimandtheir customers in pure ethical terms.

308 Gjalt de Graaf

Discourse C is by far the smallest in myresearch (with only three defining variates, ofwhich one has an even higher loading on anotherfactor). But since it has both clear statistical sig-nificance and a clear view of customers, adescription will follow.

Discourse C is an open business approach. Indiscourse C we see for the first time that acustomer is not only conceptualized as a partner,which is certainly also the case, but also as a com-petitor. This is mainly because, like the twofactors that will follow, making a profit is con-sidered more important than in the previousdiscourses. Surely, there are many common inter-ests with the customer, but there are also clearopposing interests. And the bankers of discourseC are very aware of that. They consider it‘honest’ to admit that. Which also means thatthey think it’s unfair when a banker claims he hasonly common interests with a customer: that issimply not the reality and one should not try toconceal that. That would be ‘insincere’. Typicalis that one of the bankers of this discourse noted

that he missed a few cards about the power gamesin the banking business. They consider it a factthat in the banking business you are in a constantnegotiating position. They never play games withthe customer though.

Money is simply what their business is allabout. Bankers of discourse C want to make abuck and don’t hide that. They also accept thatattitude very easily from their customers. Theyare by far the least prone of all the bankers to calltheir customers materialistic. In that sense theydon’t feel let down by the customer very easily.The relationship with their customers is lesspersonal than in discourse A and B. They are,of all the discourses, also the least upset when acustomer goes bankrupt: that’s all simply part ofthe money game.

Ethically speaking, they don’t have an impulseto improve society. Environmental sustainabilityplays no role. Values are important, of course, butthey don’t take it too far. Also, bankers in dis-course C are very sincere in that sense; theynever try to look better than they are.

Discourse Theory and Business Ethics 309

Discourse C: A customer is a colleague and competitor in one

A B C D E

50. A customer is someone with whom you have partly common and partly opposing interests. He is a colleague and a competitor in one. –1 –2 +3 –0 –0

07. We (almost) never have big problems with customers who feel they are treated wrongly. When there are problems, we usually solve them to everyone’s satisfaction. We feel very responsible for (almost) all problems. 00 00 +2 00 00

13. Values are very important, but they have to be sincere. If you play a game with them, and just give some money for some good causes, a (potential) customer will see right through that. 00 +1 +3 +1 +2

20. When judging a business-plan of a (potential) customer, the concept of sustainability plays a role. We go clearly further than just finding out whether the company has the necessary licenses. +2 +1 –1 00 +1

Discourse D is very marketing oriented. Whennegotiating, bankers of discourse C have a pureand open business approach. Bankers of discourseD are more prone to play games. They look verycarefully at their opponents, like poker players,and try to figure out what the best strategy wouldbe in the negotiations. If a customer doesn’tnegotiate, it will certainly cost him money. Thatis pretty much what characterizes this factor. Likein discourse E (more on that later), bankers ofdiscourse D are very concerned with making aprofit, profits are the bottom-line. The way todo that differs though, in this case it is bylistening to what (potential) customers want.Service is considered very, very important. Likein discourse A, they listen carefully to theircustomers, but in discourse D it is much lesspersonal, it is simply the best way to makemoney. If you keep your customers happy, youkeep yourself happy. It’s the customer who ulti-mately pays the banker’s salary (many of themcommented spontaneously that the client is theirbread and butter). The client is put on a pedestal,because that is the best way to make money. Forexample, when a customer is in trouble, the maingoal is to minimize the bank’s losses. Eventhough this is a very distressing situation, theworst actually that can happen in this kind ofbusiness. (When you do everything to keep your

customer happy, and he fails, then that’s the worstthat can happen.)

The notion that the relationship is less personalmanifests itself in the sense that bankers ofdiscourse D talk more about their clients in termsof categories than in personal terms. They arevery much marketing oriented, they look forproducts to fit their customers, instead of theother way around. They don’t just try to sellexisting products as customers want service madeto measure. That’s not always easy. There are alot of different clients out there.

Since bankers of factor D are by far the mostinterested in what customers think about them,they are most likely to be disappointed by cus-tomers. Many complain that customers are toocritical. When you work your socks off for acustomer, it is not nice when you find out thathe is mainly interested in your financial rates.They view many clients as primarily interestedin money, and are therefore by far the most likely(especially when compared with the other profitoriented factors C and E) to complain aboutcustomers being materialistic.

Bankers of discourse D wouldn’t miss anopportunity to present themselves in the mostfavorable ways, including in an ethical sense.Even if they themselves know the created imageis not completely accurate.

310 Gjalt de Graaf

Discourse D: Marketing: the customer as a buyer of profitable products

A B C D E

45. In our bank, customers are put at the center of attention, because it’s they who have to generate the profits. +1 +1 +1 +3 +3

06. When a customer is in financial difficulty, we are more focused on helping the customer, than on reducing the financial risk of the bank. Even if the risk of losing money increases. –1 +1 +1 –2 –3

10. The worst experience with customers for me is when a company goes bankrupt. –1 00 –2 +1 00

For both discourse D and E, profits are thebottom line. What separates them very clearlythough is that bankers in discourse E are muchless outgoing and much more focused on them-selves. They are very self-assured, also towardstheir customers. Some might call this arrogant.They believe that quality is the name of thegame. If you deliver the best products, the cus-tomers will come automatically, and you willmake the most money. Customers do not decidewhich bank to go to on the basis of “feeling athome” at a bank, they mainly decide on purebusiness calculations. Therefore as a bank youmust make sure you are the best in a businesssense. This certainly doesn’t mean just having thebest financial rates. Also very, very important arequality, good service and professionalism.

As in discourse C, customers and banks do notonly have common interests. A customer is cer-tainly not just a colleague. Both have their ownobligations and tasks. Bankers of discourse E do

recognize themselves in the customers. Abouttheir customers they think in the followingterms: “They are like us. Therefore, they willunderstand if we just try to be the best in every-thing and make a good profit, then the customerwill recognize themselves in us, because they tooare very concerned with the quality of their ownproducts”.

Since the bank is very business oriented, mostdecisions are made on a business basis. When aclient is in trouble, it is simply the duty of thebank to look after their own risks first. Of coursebankers of discourse E want to help, but thereare clear boundaries. Never throw good moneyafter bad. Their own financial risk is number oneon their list of priorities.

Whereas trustworthiness is a great marketingtool, fraud is the worst kind of advertisement.Therefore, in an ethical sense, the worst thingthat can happen, by far, is fraud. Bankers ofdiscourse C are more prone to blame themselves

Discourse Theory and Business Ethics 311

Discourse E: The customer as a commercial relationship

A B C D E

45. In our bank, customers are put at the center of attention, because it’s they who have to generate the profits. +1 +1 +1 +3 +3

06. When a customer is in financial difficulty, we are more focused on helping the customer, than on reducing the financial risk of the bank. Even if the risk of losing money increases. –1 +1 +1 –2 –3

03. A customer is someone you cooperate with, after all we only have common interests. He is like a colleague. 00 +1 00 +1 –1

49. Values are more and more important to us. Because our name has to appear only once in the papers with ‘that bank did something wrong’, and there goes our good name. And that will cost us customers. +1 +1 +1 00 +2

13. Values are very important, but they have to be sincere. If you play a game with them, and just give some money some good causes, a (potential) customer will see right through that. 00 +1 +3 +1 +2

23. The worst experience with customers occurs when one of the many forms of fraud comes to light. 00 00 00 00 +2

38. I wish customers in general wouldn’t be so materialistic. Financial rates are often the only thing that counts when doing business. –1 00 –1 00 –2

for not noticing earlier that something is wrong,not the banker of discourse E. Fraud touches theheart and soul of what they are all about. A clientgoing bankrupt is part of the business banks arein, but fraud can hurt you in many ways. It is notonly bad for the reputation of your bank, it canalso cost you a lot of money. Customers valuequality and a sense of security, and this can behurt badly by bad press. Trust is seen as a crucialpart of providing good service.

The role of the bank in the region is mainlybanking, to provide businesses good service. Soa starter is taken on if his business-plans andapproaches are promising, not to improve thingsin the region.

Values are important, but mainly not to lose agood reputation. So the values shouldn’t gofurther than legal boundaries. Improving theworld is not the task of a banker: again, the taskof a banker is to excel in the business of bor-rowing and lending money. One also shouldn’tpresent oneself better in this sense than one is inreality. Besides, there is nothing wrong withbeing a good banker. On the contrary, it is a veryhonorable profession. On the same note, bankersof discourse E expect nothing more from theircustomers, than being good business people.Customers wouldn’t soon be seen as materialistic.Surely most customers are very profit oriented,and that is a good thing.

Different banks and different municipalitysizes

Q-methodology is a form of qualitative research.Therefore, from the numbers I collected I cannotsay, for example, what percentage of big citybanks exactly fall into a specific discourse. Butsince the bankers were selected in a purelyrandom fashion, some conclusions can bedrawn.17

The differences between big cities and smallvillages don’t seem to be very large. The specificbank a banker works for on the other hand doesseem to be important. As can be seen from thesubjects’ factor loadings (Figure 2), seven of theABN-Amro bankers fall into discourse E, whereonly three other defining variates are found in

this factor from the other two banks combined.Discourse E therefore seems to be predominantlyan ABN-Amro factor. Furthermore, discourse Alooks like an ING discourse and discourse BRabobank.

These impressions can be subjected to morerigorous scrutiny (Thomas et al., 1993, p. 707)by treating the loadings on each of the factors asseparate dependent measures18 and analyzingdifferences among these scores in terms of the3

! 3 (Region ! Bank) ANOVA design implicitin the P-set.

The analysis of variance amplified the initialimpressions. The size of the municipality hardlypredicts a factor the banker will fall in to. Onlynoticeable is that small villages have significantlylower loadings on factor E (F = 6.23, p = 0.008).

The impressions of bank-specific factors werealso confirmed. Maybe the most surprising resultfrom the analysis of variance is that the strongestrelation (F = 14.36, p < 0.001) was found withrespect to factor A. At first this didn’t seem tobe the most bank-specific factor, but a secondlook reveals the extremely low score of theRabobank bankers on this factor, resulting in thehigh F score. Factor E also shows significance,Rabobank is very low and ABN-Amro very high(F = 7.26, p = 0.004).

One of the questions I asked myself earlier waswhether the Rabobank is right when it claimsthat it is different from other banks in treatingits customers. Now I can say more about thatquestion: the answer is both a “yes” and a “no”.

Discourse B very clearly seems to be aRabobank discourse. Only one other definingvariate can be found among the other bankdirectors. Furthermore, the loadings among theother bank directors on factor B are very low.So the conclusion is yes: there seems to be aspecific discourse in the Rabobank.

Yet, only five of the ten Rabobank directorsare defined by factor B. And those bankers of theRabobank who are not defined by factor B, haveextreme low loadings on this factor, clearlyindicating they don’t identify themselves ondiscourse B. So even though there is a specificRabobank way to treat their customers, this iscertainly not shared by all of the local Rabobankbankers. Furthermore, in the larger cities no

312 Gjalt de Graaf

Discourse Theory and Business Ethics 313

defining variates were found. A random customergoing to a random Rabobank doesn’t seem tobe able to count on a Rabobank-specific treat-ment, especially in larger cities. This conclusionis not surprising, since the Rabobank is verydecentralized, and every local bank is veryindependent (for example, in contrast to theother banks hiring of personnel is completelydecentralized). Even if they would want to, itwould be very hard to create a shared cultureamong all the local banks throughout theNetherlands.

Concluding remarks

Because of the (different) status discourse theoryattributes to discursive practices, the questionhow bankers treat their customers is answeredby the five discourse-descriptions. The compar-ison between the different bankers has beendiscussed in the previous section.

From the five discourses, it has become veryclear that there are different ways for banks toconceptualize their customers. Furthermore, itpresents further empirical evidence that thefactual images they have of their customers areconnected to different normative questions andpossible solutions to these questions. Forexample, talking about values, bank managersfrom discourse E start to talk immediately aboutfraud and how to prevent it. But also normativeissues like how to treat starters, how to deal withenvironmental issues, how to use the bank to

improve the region the bank is located in, howto deal with sponsor money, how to treat acustomer in financial difficulty, whether to treatclients differently, when to be completely honestto customers, how to negotiate with customers,etcetera, are indissolubly tied to factual images abanker has of his customers. The normativequestions and the factual images are part of thesame discourse. This shows how hard it is to lookat normative issues of companies without takingaccount of factual views. Discourse theory is verywell equipped for studying how facts and valuesinfluence each other. Discourse analysis was veryhelpful in comparing normative sides of differentbanks.

A discursive practice is an act in itself. Forbusiness ethics discourse theory means morestudies of discursive practices instead of behavior.The uniqueness of discourse theory is furtherexpressed by its view of language: language is notjust reflective of what goes on in an organization,it is constitutive of reality. This gives valuationalstatements within discourses a different ontolog-ical status. They are always studied within theircontext.

One way to look at the normative aspects ofthe discursive practices of the three banks, is tostudy their internal discourses. One can also, ashas been done in this study, compare similardiscourses. When showing the discourses next toeach other, by contrast the different normativeand valuational aspects become apparent, whichwould have remained concealed in traditionaldescriptive ethics.

Appendix. Statements and factor scores

Discourse

A B C D E

01. There are no specific sectors of business, which we prefer 00 –1 +2 –1 –1strongly. It doesn’t matter which sector a (potential) client is from.

02. Financial service is a matter of live and let live (between customers and banks). +2 00 +1 +2 +1

03. A customer is someone you cooperate with, after all we only have common interests. He is like a colleague. 00 +1 00 +1 –1

314 Gjalt de Graaf

Appendix (Continued)

Discourse

A B C D E

04. We have strong ethical boundaries, which means we do not want to do business with just any customer. I am talking about things such as abiding by the law and absolutely never accepting large gifts. +1 +2 00 +1 +1

05. In the relations with customers you can notice that banks are more and more marketing-organizations, instead of product-organizations. 00 00 +1 +1 +1

06. When a customer is in financial difficulty, we are more focused on helping the customer, than on reducing the financial risk of the bank. Even if the risk of losing money increases. –1 +1 +1 –2 –3

07. We (almost) never have big problems with customers who feel they are treated wrongly. When there are problems, we usually solve them to everyone’s satisfaction. We feel very responsible for (almost) all problems. 00 00 +2 00 00

08. Some customers are very interesting to us, because they contribute to the image of the bank. Just an example: we do not have to make a profit out of a customer like a hospital even in its totality (including insurances etc.), and then it’s still a challenge to facilitate such a customer as good as possible. –1 00 +1 –1 00

09. The average customer is someone who is very focused on money. Growth, profit and independence are very important to him. If we do not give him the highest quality of service and very good rates, he’s gone. –1 –1 00 –1 00

10. The worst experience with customers for me is when a company goes bankrupt. –1 00 –2 +1 00

11. It is not necessary to be involved in the region, but it is commercially absolutely desirable. The goodwill you gain with customers (or prospects) by being an active partner in society is at least as big as by local advertisements. +1 +2 +1 +2 +1

12. Financial rates are more important to our customers than a sense of involvement from our bank. –2 –1 –1 –2 –2

13. Values are very important, but they have to be sincere. If you play a game with them, and just give some money for some good causes, a (potential) customer will see right through that. 00 +1 +3 +1 +2

14. It never happens that we sell a product to a customer about whom we think: “he could easily miss that”. –2 –1 00 –1 –1

15. It is certainly conceivable that we first invest in the relationship with a new customer, and view the earning-capacity as a manifestation of the deepening relationship. 00 +2 +2 +1 +1

16. Of course we are involved in our region, but one certainly mustn’t exaggerate that. The involvement is mainly through our customers. 00 –2 –1 –2 –1

Discourse Theory and Business Ethics 315

Appendix (Continued)

Discourse

A B C D E

17. Of course it happens that we sell a product to a customer about whom we think: “he could easily miss that”. 00 –2 –1 –2 00

18. I wish that our customers would care a little more for society. You see a lot of superficiality. Customers are very self-occupied. The common interest hardly gets any attention. 00 00 00 00 –1

19. Ethics play a role in our business. This means not facilitating customers with activities that cross our boundaries. These boundaries go clearly further than just legal boundaries. We even ethically reprimand customers sometimes. 00 00 00 00 +1

20. When judging a business-plan of a (potential) customer, the concept of sustainability plays a role. We go clearly further than just finding out whether the company has the necessary licenses. +2 +1 –1 00 +1

21. The average customer is someone who doesn’t see money as a goal in itself, but more as a means to express a certain achievement. We, as a bank, are sort of a partner with whom he maintains a personal relationship. As soon as he feels he is treated unfairly, you run the risk he will go to a competitor. 00 +1 00 00 +1

22. At our bank, every customer pays the same rate for the same service. –3 –1 –3 –3 –3

23. The worst experience with customers occurs when one of the many forms of fraud comes to light. 00 00 00 00 +2

24. Often we give starting businesses a chance, that otherwise wouldn’t get a chance with other banks. –3 +1 –2 –1 –1

25. The most important reason for a customer to choose us is “the impression we have of each other”, that customers feel comfortable with us, that they feel at home. +1 +2 +2 +1 00

26. We are now certainly more customer-oriented and less product-oriented than we used to be. We used to have products, which we tried to sell to a customer. Nowadays we investigate more in the market what customers want and adapt our products accordingly. +2 +2 00 +2 +1

27. When we notice at a certain point that a customer is not remunerative, it matters to us whether he is a starter just beginning or has been remunerative for years, or that the whole sector is going through a rough period, or that there are signals that point downwards for a longer period. +1 +1 00 +1 00

28. Rates differ with us from client to client. +3 00 00 00 +1

29. When a customer is in financial difficulty, we are strongly focused on helping the customer. But most of our attention is of course on reducing the financial risk of the bank. The risk of losing money may not increase. 00 00 +1 +2 +2

316 Gjalt de Graaf

Appendix (Continued)

Discourse

A B C D E

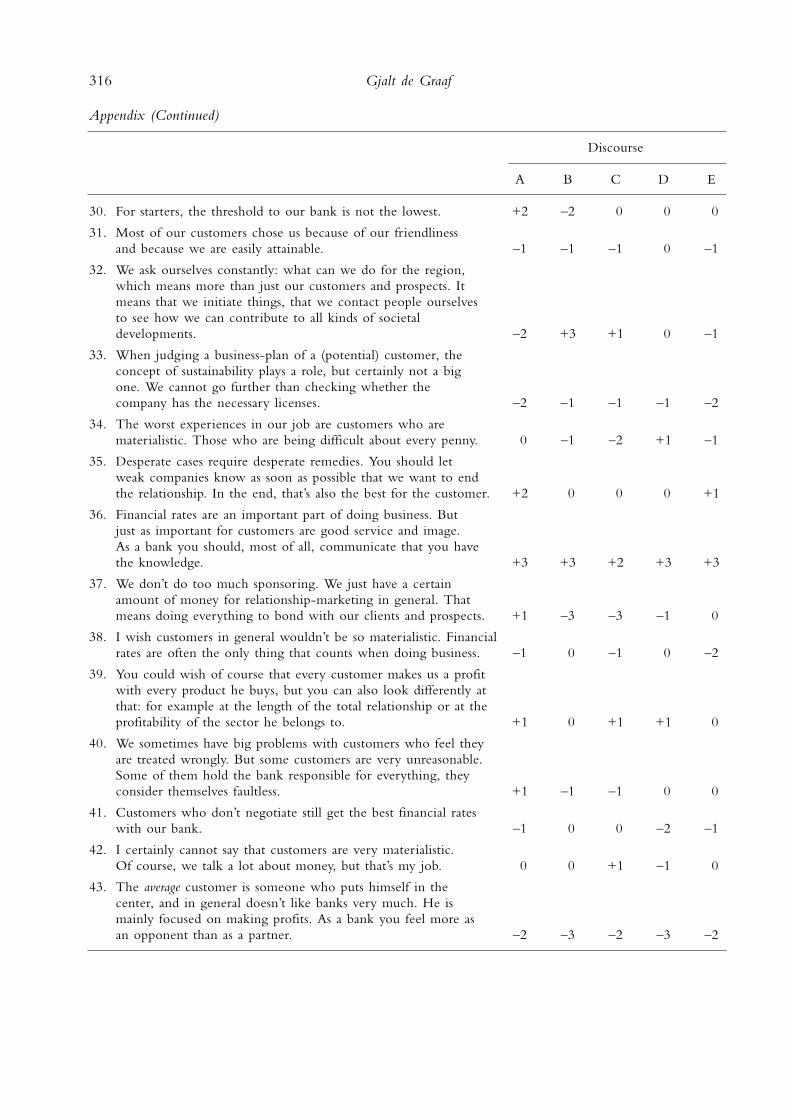

30. For starters, the threshold to our bank is not the lowest. +2 –2 00 00 00

31. Most of our customers chose us because of our friendliness and because we are easily attainable. –1 –1 –1 00 –1

32. We ask ourselves constantly: what can we do for the region, which means more than just our customers and prospects. It means that we initiate things, that we contact people ourselves to see how we can contribute to all kinds of societal developments. –2 +3 +1 00 –1

33. When judging a business-plan of a (potential) customer, the concept of sustainability plays a role, but certainly not a big one. We cannot go further than checking whether the company has the necessary licenses. –2 –1 –1 –1 –2

34. The worst experiences in our job are customers who are materialistic. Those who are being difficult about every penny. 00 –1 –2 +1 –1

35. Desperate cases require desperate remedies. You should let weak companies know as soon as possible that we want to end the relationship. In the end, that’s also the best for the customer. +2 00 00 00 +1

36. Financial rates are an important part of doing business. But just as important for customers are good service and image. As a bank you should, most of all, communicate that you have the knowledge. +3 +3 +2 +3 +3

37. We don’t do too much sponsoring. We just have a certain amount of money for relationship-marketing in general. That means doing everything to bond with our clients and prospects. +1 –3 –3 –1 00

38. I wish customers in general wouldn’t be so materialistic. Financial rates are often the only thing that counts when doing business. –1 00 –1 00 –2

39. You could wish of course that every customer makes us a profit with every product he buys, but you can also look differently at that: for example at the length of the total relationship or at the profitability of the sector he belongs to. +1 00 +1 +1 00

40. We sometimes have big problems with customers who feel they are treated wrongly. But some customers are very unreasonable. Some of them hold the bank responsible for everything, they consider themselves faultless. +1 –1 –1 00 00

41. Customers who don’t negotiate still get the best financial rates with our bank. –1 00 00 –2 –1

42. I certainly cannot say that customers are very materialistic. Of course, we talk a lot about money, but that’s my job. 00 00 +1 –1 00

43. The average customer is someone who puts himself in the center, and in general doesn’t like banks very much. He is mainly focused on making profits. As a bank you feel more as an opponent than as a partner. –2 –3 –2 –3 –2

Discourse Theory and Business Ethics 317

Appendix (Continued)

Discourse

A B C D E

44. With starters, we run more of a risk on purpose, because they are very important to the region. 00 +1 0 +1 –1

45. In our bank, customers are put at the center of attention, because it’s they who have to generate the profits. +1 +1 +1 +3 +3

46. I think it is very wise of customers if they don’t want to be dependent on just one bank for their financial services. –1 –2 –1 –1 00

47. It is very unwise of a customer not to negotiate with us about our financial rates. That would certainly cost them money. –1 –1 –2 –1 00

48. Some customers are very interesting to us. The interest we have in a customer is the total revenue. We don’t have to make a profit out of a loan to a hospital, if we can also do the insurance, pensions, etc. +1 +1 00 +2 +2

49. Values are more and more important to us. Because our name has to appear only once in the papers with “that bank did something wrong”, and there goes our good name. And that will cost us customers. +1 +1 +1 00 +2

50. A customer is someone with whom you have partly common and partly opposing interests. He is a colleague and a competitor in one. –1 –2 +3 00 00

51. We don’t want to have anything to do with illegal business, very clearly, but we aren’t moralists either. If someone in society finds something indecent, it’s not a reason for us not to do business with a customer. Then the fences are down. +1 0 –1 00 00

52. With a starting business we only look at the business-plan. Then we are very critical, because it’s no use throwing good money after bad. That’s for neither a good situation. –1 –1 –1 –1 –2

Notes

1 Great appreciation goes to the numerous colleagueswho helped me with my research. I would likeespecially to thank Prof. dr. F. Leijnse and Prof. dr.Th. Van Willigenburg who commented extensivelyon earlier versions of this paper.2 And whether there are differences among the dif-ferent banks or among the municipality sizes thebanks are in.3 Also the status of the field (business ethics) as awhole changes. The descriptive ethics of theresearcher itself must now also comprise a normativecomponent. Descriptive ethics contains values itselfand doesn’t just mirror reality (Willmott, 1998, p. 80).

In this article I will not pursue this point any furtherhowever.4 What I describe here is also called: the decenteringof the subject. Also the subject is formed in discur-sive practices.5 Because meaning and value are immanent featuresof whatever discourse we are referring to, and becausethey are complexly interwoven, traditional ethicalthinking as an autonomous form of reasoning is nowcalled into question (Shapiro, p. 9). A valuationaldiscourse can never be wholly autonomous.6 A term from Sabatier.7 This point is also very important in relation tostakeholder theory. Even if you have all the relevantrepresentatives of all the relevant stakes around a table,

the question is whether they perceive and are willingto talk about the same problems, let alone the samesolutions. “This does not mean that facts don’t enterthe discussion. Ironically, participants seem exclusivelypreoccupied with getting the facts straight. Theyaccuse each other of misinterpreting or simplyignoring crucial evidence. Many authors contend thatthese disagreements about facts actually mask aconflict underlying ‘belief systems’. These are “sets ofcausal and normative assumptions about reality”(Eeten, 1998, p. 6). Both discourses have valid argu-ments within their own rules, but somehow theydiffer fundamentally.8 Named as a possible method to deconstruct dis-course in Dryzek (1990, p. 187). Examples of suc-cessful discourse analyses include Van Eeten (1999),Dryzek and Berejikian (1993) and Thomas et al.(1993).9 The main source for Q-methodology in general isStephenson (1953). Within the social sciences, Brown(1980) is a classic. 10 In case of the ING and ABN-Amro I decided tolook at the level of “rayon-kantoren”. Rayons are themain areas in which they have divided Holland.Rabobank doesn’t have such an intermediate level.11 Banks usually divide their customers in two cate-gories: business clients and private clients. I instructedthe directors to talk about their business customers.Because of the automation processes, most privateclients hardly ever personally interact with their banks.Therefore this category was less interesting to me thanthe business clients, who always have a personalcontact with the bank. Nowadays, a discourse aboutprivate customers hardly exists within banks: acomputer ‘handles’ most contacts.12 During the many interviews that followed, everyinterviewee was asked whether the 52 statements con-tained all the relevant aspects of customers and dealingwith customers. In almost every instant, this was con-firmed.13 For ABN-Amro and ING only “rayon-directeuren” were considered. There are about 200 ofthem within Holland. Rabobank doesn’t have rayon-directeuren, only local bank directors, about 470.14 For this I used the ‘mate van stedelijkheid’(measure of urbanization) of the Centraal Bureau voorde Statistiek. This measure goes for every municipalityfrom 1 (totally urbanized) to 5 (not urbanized). Foreach bank I took 3 branches that were in category 1or 2, 4 which were in category 3 and 3 that were inthe highest two categories. 15 In this case standard Q-sort procedure wasfollowed, and a quasi-normal distribution was chosen.

16 Even though a forced distribution was used, somedeviations were tolerated. If the Q-sorter found theforced distribution too much unlike his own position,he was allowed to have a few more or less statementsin one category than he was “supposed to”. 17 There is a small literature on the translation of Q-technique results into questionnaire items for admin-istration to larger audiences. A list of literature on thissubject was given on the Q-method discussion list ofKent State University, on March 5th 1999, by StevenR. Brown. On generalization in Q methodology ingeneral, see Thomas and Baas (1992).18 After an email suggestion by Steven R. Brown, theloadings were first transformed into Fisher’s Z.

References

Brown, S. R.: 1980, Political Subjectivity (New Haven,London).

Centraal Bureau voor de Statistiek: 1998, Gebieden inNederland, 1998 (Voorburg/Heerlen).

Combes, Cherry, David Grant, Tom Keenoy and CliffOswick (editors): 2000, Organizational Discourse:Word-views, Work-views and World-views (KMPC,London).

Cowton, C. and R. Crisp: 1998 (Oxford UniversityPress, Oxford).

Dalen, A. A. and C. J. van Gelderen: 1998, In haarmaatschappelijk functioneren is de Rabobank anders!Wens of werkelijkheid? (internal publication).

Doig, A. and J. Wilson: 1998, ‘The Effectiveness OfCodes Of Conduct’, Business Ethics: A EuropeanReview 7, 140–149.

Dryzek, J. S. and M. L. Clark and G. McKenzie:1989, ‘Subject and System in InternationalInteraction’, International Organization 43, 475–505.

Dryzek, J. S.: 1990, Discursive Democracy: Politics, Policyand Political Science (Cambridge University Press,Cambridge).

Dryzek J. S. and J. Berejikian: 1993, ‘ReconstructiveDemocratic Theory’, American Political ScienceReview 87, 48–88

Durning D. and W. Osuna: 1994, ‘Policy Analysts’Orientations: An Empirical Investigation Using QMethodology’, Journal of Policy Analysis andManagement 13, 629–657.

van Eeten, M. J. G.: 1998, Dialogues of the Deaf:Defining New Agendas for Environmental Deadlocks(Eburon, Delft).

Foucault, M., edited by P. Rabinow: 1984, TheFoucault Reader (Penguin Books, London).

Hackley C. E. and Ph. J. Kitchen: 1999a, ‘Ethical

318 Gjalt de Graaf

Perspectives on the Postmodern CommunicationsLeviathan’, Journal of Business Ethics 20, 15–26.

Hackley, C. E.: 1999b, ‘The Meaning of Ethics in andof Advertising’, Business Ethics: A European Review1, 37–42.

Hawkes, T.: 1998, ‘Scoring an own Goal? EthicalIssues in the U.K. Professional Soccer Business’,Business Ethics: A European Review 1, 37–47.

Liljander, V. and T. Stranvik, 1995, ‘The Nature ofCustomer Relationships in Services’, Advances inServices Marketing and Management 4, 141–167.

Putnam, L.: 2000, ‘Work-Views and Work-Views:Building Theory About Discourse andOrganizations’, in C. Combes et al. (ed.),Organizational Discourse: Word-views, Work-views andWorld-views (KMPC, London), p. 255.

Parker, M. (ed.): 1998, Ethics and Organizations (SagePublications, London).

Felkins, P. K. and I. Goldman: 1993, ‘Political Mythas Subjective: Some Interpretations andUnderstandings of John F. Kennedy’, PoliticalPsychology 14, 447–467.

Randels, G. D. Jr.: 1998, ‘The Contingency ofBusiness: Narrative, Metaphor, and Ethics’, Journalof Business Ethics 17, 1299–1310.

Roe, E.: 1994, Narrative Policy Analysis: Theory andPractice (Duke University Press, Durham NC).

Sabatier, P. A.: 1988, ‘An Advocacy CoalitionFramework Of Policy Change and the Role ofPolicy-oriented Learning Therein’, Policy Sciences21, 129–168.

Schneider, B. and J. J. Parkington and V. M. Buxton:1980, ‘Employee and Customer Perceptions ofService in Banks’, Administrative Science Quarterly25, 252–267.

Shapiro, M. J.: 1988, The Politics of Representation(University of Wisconsin Press, Madison).

Shapiro, M. J.: 1992, Reading the Postmodern Polity(University of Minnesota Press, Minneapolis).

Sorell, T.: 1998, ‘Beyond the Fringe? The StrangeState of Business Ethics’, in M. Parker (ed.), Ethicsand Organizations (Sage Publications, London), pp.15–29.

Stephenson, W.: 1953, The Study of Behaviour: Q-technique and Its Methodology (University of ChicagoPress, Chicago).

Thomas, D. B. and L. R. Baas: 1992, ‘The Issue ofGeneralization in Q Methodology: “ReliableSchematics” Revisisted’, Operant Subjectivity 16,18–36.

Thomas, D. and C. McCoy and A. McBride: 1993,‘Deconstructing the Political Spectacle: Sex, Raceand Subjectivity in Public Response to theClarence Thomas/Anita Hill “Sexual Harassment”Hearings’, American Journal of Political Science 37,699–720.

Warren, C.: 1993, ‘Codes of Ethics: Bricks withoutStraw’, Business Ethics: A European Review 4,185–191.

Willmott, H.: 1998, ‘Towards a New Ethics/TheContributions of Poststructuralism andPosthumanism’, in M. Parker (ed.), Ethics andOrganizations (Sage Publications, London), pp.76–121.

Erasmus University Rotterdam,Faculteit der Bedrijfskunde/