Page 1

1

Dividend Policy in Turkey: Survey Evidence from Borsa Istanbul Firms

H. Kent Baker*

American University

Kogod School of Business

Department of Finance and Real Estate

4400 Massachusetts Avenue, NW.

Washington, DC, 20016 USA

[email protected]

Erhan Kilincarslan

Birkbeck University of London

School of Business, Economics and Informatics

Department of Management

Malet Street, WC1E 7HX

London, UK

[email protected]

Alper Haktan Arsal

Yildiz Technical University

Graduate School of Social Sciences

Business Administration

Barbaros Bulvari, 34349 Yildiz

Istanbul, Turkey

[email protected]

*Corresponding author

H. Kent Baker

Page 2

2

Dividend Policy in Turkey: Survey Evidence from Borsa Istanbul Firms

Abstract

This study investigates the views of managers of firms listed on the Borsa Istanbul (BIST) on

dividend policy. The survey evidence provides general support for Lintner’s partial

adjustment model, signaling theory, catering, firm life cycle, and bird-in-the-hand hypotheses

for explaining cash dividends. The results do not support the agency cost theory, substitution

model of dividends, tax-related explanations, transaction cost theory, and residual dividend

policy. The findings suggest that after implementing major economic and structural reforms

and abolishing a mandatory dividend payment requirement, BIST managers follow similar

dividend policy factors and patterns of dividend policy as managers in more developed

countries

1. Introduction

Dividend policy is a highly researched topic in corporate finance. Miller and

Modigliani (1961) demonstrate that dividend payments have no effect on firm value and no

dividend policy is superior to another under perfect capital market assumptions. Yet, in the

real world where market frictions exist such as differential tax rates, information

asymmetries, agency problems, and transaction costs, their argument becomes highly

debatable. In this respect, financial scholars have focused on various market frictions and

proposed many competing theories about why companies pay, or do not pay, dividends

(Lease et al., 2000; Baker, 2009). Hence, the dividend policy literature is vast and contains

numerous theories, hypotheses, and explanations for dividends. Despite voluminous

theorizing, empirical research, and extensive debate, no consensus exists on the actual

motivation for paying dividends.

According to Baker et al. (2006, 2008), two main reasons may lead to this lack of

consensus. First, financial economists typically focus on trying to develop a universal or

“one-size-fits-all” explanation. This tendency exists despite the well-known reality that

corporate dividend decisions are sensitive to various factors, such as firm characteristics,

corporate governance, and legal environments. Second, the proposed explanations largely

rely on economic modeling instead of obtaining direct evidence from actual policy makers.

Unfortunately, economic modeling cannot measure motivation. Given that no single theory

solves the dividend puzzle, Baker et al. (2002) and Chiang et al. (2006) state that one way to

improve our understanding of corporate dividend policy is to investigate the views of

managers who are responsible for making such decisions based on the combination of various

dividend theories, factors, and issues.

Historically, dividend studies primarily focused on developed markets but some

attention has shifted to emerging markets. The evidence generally indicates major differences

in dividend policy behavior between developed and emerging economies. Such differences

stem from such factors as political and social instability, a lack of adequate disclosure, poor

Page 3

3

laws and regulations, weaker corporate governance, and different ownership structures

(Aivazian et al., 2003a, 2003b; Faccio et al., 2001; Glen et al., 1995; La Porta et al., 2000).

Yet, researchers still tend to rely on economic modeling approaches instead of obtaining

insights directly from corporate managers (Baker and Kapoor, 2015; Baker and Powell,

2012).

The purpose of this paper is to extend previous survey-based research on dividends

into an emerging market and to contribute new evidence to the literature. In particular, we

focus on Turkey, which is one of the most important emerging economies. Turkey is

strategically located between Europe and Middle-East and is a candidate member of the

European Union (EU). More importantly, Turkey implemented major reforms starting with

the fiscal year 2003 in compliance with the International Monetary Fund (IMF) stand-by

agreement, the EU directives, and best-practice international standards for a better working of

the market economy, outward-orientation, and globalization. Also, Turkish regulators made

major changes in the regulatory framework of cash dividend policy rules during this period.

Therefore, this paper differs from past survey research in two respects. First, it studies firms

in an emerging market that has undergone major changes to integrate with world markets.

Second, the study attempts to provide insights of what perceptions these managers have about

dividend policy after such developments. Accordingly, we survey corporate managers of

dividend-paying companies listed on the Borsa Istanbul (BIST) – formerly known as the

Istanbul Stock Exchange. We study their views about various theories and explanations for

paying cash dividends, and the most important factors affecting their dividend policy

decisions.

Although survey research is by no means the standard academic approach in finance,

it can provide data unavailable from other sources, which can help bridge the gap between

theory and practice. To the best of our knowledge, this research provides the first

comprehensive study in the Turkish market using survey-based evidence from corporate

managers of dividend-paying firms listed on the BIST. The study also complements previous

empirical research on dividend policy and confirms earlier findings while exploring specific

nuances of the Turkish market. In conducting empirical research, Bruner (2002, p. 50) notes,

“The task must be to look for patterns of conformation across approaches and studies much

like one sees an image in a mosaic of stones.” As discussed later, we intentionally use the

same survey design and questionnaire as several other researchers to enable direct

comparisons. Hence, this study provides insights about dividend policy involving Turkish

firms unavailable in previous research.

The remainder of this paper has the following organization. Sections 2 and 3 review

the theoretical background and selective surveys on dividend policy, respectively. Section 4

provides an overview of the research context in Turkey and develops research hypotheses.

Section 5 discusses our research methodology. Section 6 reports and discusses the survey

results, and Section 7 concludes the paper.

Page 4

4

2. Main dividend policy theories and explanations

Although researchers have contributed numerous theories, explanations, and models

to the dividend policy literature, some have been widely discussed and extensively tested in

the hope of solving the dividend puzzle. In this section, we briefly summarize 10 theoretical

arguments some of which might be important in describing dividend decisions in the

emerging Turkish market. However, this is not the full set of possible explanations for paying

dividends.

Bird-in-the-hand theory: One of the earliest explanations in favor of dividends is that

more certainty is attached to dividend payments received today, against dividend

retention for reinvestment in projects whose future earnings are uncertain.

Signaling theory: A firm’s management has a better understanding of the firm’s

intrinsic value than outside shareholders and investors, who only have access to

public information. Because information asymmetry exists between insiders and

outsiders, managers may use dividends as a device to signal their superior information

about a firm’s future prospects to outsiders.

Agency cost theory: This theory derives from problems associated with the separation

of management and ownership, and the differences in managerial and shareholder

priorities. It further contends that dividend payments help to control these agency

problems by reducing the free cash from the managers’ control and paying it to

shareholders.

Tax-preference theory: Investors who receive favorable tax treatment on capital gains

may prefer shares with none or low dividend payouts because higher dividend

payments increase shareholders’ tax burden.

Tax clientele effect: Each investor has his own implied calculations of choosing

between high or low cash dividends and selecting dividend policies according to his

tax category circumstances. This situation leads to different clienteles for both high

and low dividend yields depending on tax positions.

Transaction cost theory: Using low cost and easily accessible internal funds to pay

dividends instead of retaining them for possible investment projects might result in

additional costs to firms because they may have to raise costly external funds to meet

their investment requirements after paying dividends.

Catering theory: Investor preferences for dividends may change over time. Therefore,

managers may recognize and cater to shifts in investor demand by distributing

dividends when investors put a premium on such stocks. Correspondingly, managers

may omit dividends when investors prefer firms that do not pay dividends.

Residual dividend theory: Firms should pay dividends only when their internally

generated earnings are not fully exhausted for investment projects. Thus, dividend

payments should ideally be the residuals of cash produced by a firm’s operations after

undertaking all positive net present value (NPV) investments.

Maturity (firm life cycle) theory: Higher dividend increases are a sign of change in a

firm’s life cycle. A firm is likely to pay higher dividends as it transits from a growth

to a more mature phase. This change occurs because a firm’s investment opportunities

Page 5

5

decrease and growth rates decline, and the firm starts generating larger amounts of

free cash flow.

Substitute model of dividends: This model posits that dividends are substitutes for

legal protection in countries with poor shareholders’ protection. Companies in such

countries need to establish a reputation treating minority investors fairly. Hence,

paying dividends helps to establish a reputation for preventing expropriation of wealth

from minority shareholders.

3. Survey-based evidence on dividend policy

Given that Baker et al. (2011) provide a detailed review of dividend surveys in both

developed and emerging markets, we focus on two recent surveys. Baker and Powell (2012)

survey dividend-paying firms listed on the Indonesian Stock Exchange (IDX). They find that

Indonesian managers perceive dividend policy as affecting firm value. These managers also

view the level of current and expected future earnings and the stability of earnings are the

most influential determinants of dividend decisions. The survey evidence reveals that

managers view the effects of dividends on share prices and the needs of current shareholders

as important. Additionally, Indonesian executives agree that the signaling, catering, and life

cycle theories primarily help to explain why their firms distribute dividends.

In a recent study, Baker and Kapoor (2015) survey managers of National Stock

Exchange (NSE) firms in India. They report that the most important factors of dividends

relate to earnings (i.e., the level of current and expected future earnings as well as the

stability of earnings) and the pattern of lagged dividends. Their evidence also shows that

Indian managers rank the dividend factors in a significantly positive way along with their

Indonesian, Canadian, and U.S. counterparts. Further, respondents from NSE firms think that

dividend policy affects firm value and view maintaining an uninterrupted record of dividend

payments as important. Finally, Indian managers highly support the signaling, firm life cycle,

and catering theories for paying cash dividends.

Overall, survey evidence shows that no single theory explains the dividend puzzle. In

fact, multiple factors, arguments, and theories exist for paying cash dividends. Nevertheless,

this study aims to extend survey-based research on dividends into the emerging Turkish

market and contribute new evidence to the literature.

4. Research context in Turkey and hypotheses

Turkish authorities strictly regulated their financial markets until the implementation

of a financial liberalization program in 1980. After adopting related regulations enacted and

launched in the subsequent years, the Istanbul Stock Exchange (ISE) emerged in December

1985 and commenced its operations on January 3, 1986 (CMB, 2003). Although the ISE

made rapid progress after being established, especially between 1990 and 2000, the ISE-listed

companies operated under a considerably different regulatory environment compared to

developed markets such as the United States, United Kingdom, Canada, and Australia during

this period. Such differences are due to the nature of Turkey’s legal system that involves the

Page 6

6

poor culture of corporate governance, lack of efficient transparency and disclosure practices,

and inconsistent and unclear accounting and tax regulations (Aksu and Kosedag, 2006; Ararat

and Ugur, 2003; La Porta et al., 1997).

The Turkish capital markets underwent major developments after the November 2002

elections, which resulted in a one-party government. In 2003, the new Turkish government

signed a standby agreement with the IMF and began to implement serious economic

programs and structural reforms for market integration (Adaoglu, 2008; Birol, 2011; CMB,

2003). Turkey’s progress in achieving full membership of the EU in this period provided the

strongest motivation for establishing new reforms, rules, and regulations in line with the EU

directives and best-practice international standards. Joining the EU also provided Turkey with

the impetus to improve corporate governance, transparency, and disclosure practices thus

integrating its economy with Europe and harmonizing its institutions with those of the EU

(Aksu and Kosedag, 2006; IIF, 2005). Accordingly, we advance our research hypotheses in

response to these major developments in the Turkish market.

Prior research reveals highly concentrated corporate ownership in Turkey, mostly

dominated by families who generally owned business groups affiliated with industrial

(businesses and subsidiaries) and financial (banks) companies organized under the legal form

of a “holding company” (Glen et al., 1995; Gursoy and Aydogan, 1999; Yurtoglu, 2003).

Moreover, the Turkish market was characterized by closely-held, bank-financed firms that

were mainly part of those bigger family-owned holding companies (Aivazian et al., 2003a,

2003b; Erturk, 2003). As a result of this infrastructure, families have control over not only

many banks belonging to their business groups but also bank lending decisions. Hence,

business groups used to obtain much of their finance from their own banks (Aksu and

Kosedag, 2006; IIF, 2005).

Until the early 2000s, Turkey experienced a poor culture of corporate governance

coupled with a lack of appropriate transparency and disclosure practices, with very poor

minority shareholders’ protection (Aksu and Kosedag, 2006; IIF, 2005; La Porta et al, 1997).

Also, the controlling families often attempted to use pyramidal corporate structures or even a

more complicated web of inter-corporate equity linkages and dual class shares to further

enhance the control on their companies at the expense of other shareholders, especially

minority owners (IIF, 2005; Yurtoglu, 2003). Hence, the Capital Markets Board (CMB) of

Turkey, as in many other emerging markets, heavily regulated dividend policies of ISE-listed

firms, when it first started to operate in 1986. According to the first regulation, the ISE-listed

firms legally had to pay at least 50% of their distributable income as a cash dividend

(Adaoglu, 1999, 2000; Kirkulak and Kurt, 2010). Thus, ISE managers lacked flexibility in

setting their firms’ dividend policies.

In this context, the nature of the ISE firms’ highly concentrated ownership structures

and their characteristic of bank-oriented financing, specifically owner-bank-firm relations,

lessened the information asymmetry and thus reduced the need to use cash dividends as a

signaling device. Further, the presence of strict mandatory dividend policy regulations also

diminished the role of dividend policy as a signaling tool. In fact, a few studies conducted in

Page 7

7

early periods in Turkey show that firms based cash dividend payments on their current year

earnings, as imposed by regulations (Adaoglu, 2000; Aivazian et al., 2003a).

Nevertheless, the CMB made many amendments to improve the transparency and

quality of the banking sector and adopted related regulations to prevent insider lending (non-

arm’s length transactions) as a source of financing in early 2000s. Since then, ISE managers

have turned to the equity market with a greater incentive for more transparent financing (IIF,

2005), which might possibly affect their financial policies, including corporate dividend

decisions. More strikingly, the CMB granted more flexible policy regulations after

implementing major reforms in 2003. Beginning in fiscal year 2009, the CMB decided not to

determine a minimum payout ratio and abolished mandatory minimum dividend payment

requirements. This action gave ISE corporate managers the freedom to make their own

dividend policy decisions. Accordingly, we conjecture that these recent developments may

affect Turkish managers’ corporate dividend policy decisions. We also expect that they might

then use cash dividends as a credible sign to convey their superior insider information about

their firms to the market. Therefore, we examine the following hypothesis:

H1: Corporate managers of BIST-listed firms now view cash dividends as a signaling

mechanism.

Our second hypothesis concerns the dividend changes relative to earnings. Glen et al.

(1995) observe that managers of firms in emerging markets whose governments dictate

mandatory dividend policy rules generally concentrate on the dividend payout ratio. Because

regulations typically imposed the dividend payout ratio, managers are not worried about

volatility in dividends. Substantial evidence across many countries, especially developed

markets, and different time periods indicates that managers often tend to pursue a traditional

Lintner (1956) style dividend smoothing policy. That is, managers prefer a stable dividend

policy. Because the volatility in dividends reflects the volatility in earnings, managers

perceive that volatile (unstable) dividend payment streams are not good indicators about their

firms’ financial performance to the market.

Applying Lintner’s (1956) model, Adaoglu (2000) and Aivazian et al. (2003a)

conducted studies during early periods in Turkey (i.e., 1985-1997 and 1983-1990,

respectively) demonstrating that ISE firms did not smooth their cash dividends. Thus, Turkish

firms had unstable cash dividend polices. The sole determinant of cash dividends was current

year earnings, as forced by the first dividend rule. The levels of current cash dividends

directly reflect any volatility in earnings of the firms. Nevertheless, Turkey’s serious efforts

to implement various financial and structural reforms to improve its market economy and

converge with the global world-markets in the post-2003 period led its stock market to a

rapid growth in market capitalization and trading volume. Not surprisingly, such changes

attracted a large amount of foreign investment (CMB, 2003, 2014). Thereby, we expect that

Turkish managers are more likely to smooth their dividend payment streams to strengthen the

credibility of stable dividends reflecting their firms’ good financial performance to both

foreign and national investors.

Page 8

8

H2: Corporate managers of BIST-listed firms now follow traditional Lintner style

managed dividend policies.

Moreover, concentrated ownership structures by large controlling shareholders are

still prevalent in Turkey, where especially families and other block holders, such as foreign

and institutional investors and the state, dominate its capital market (Al-Najjar and

Kilincarslan, 2016; Caliskan and Icke, 2011; IIF, 2005; Sevil et al., 2012). Accordingly, our

third hypothesis involves the agency cost argument. Evidence shows that large shareholders

have better incentives and ability to act as an effective monitoring mechanism on

management. Therefore, the existence of such large shareholders can mitigate the free-rider

problem of monitoring managers, which reduces agency conflicts between managers and

shareholders (Demsetz and Lehn, 1985; Grossman and Hart, 1980; Shleifer and Vishny,

1986). Especially, founding families and their direct involvement in the managements of their

firms lead to greater supervision and few owner-manager agency conflicts (La Porta et al.,

1999). Hence, we conjecture that the nature of heavily concentrated ownership structures of

Turkish firms minimizes the traditional agency cost problems (the principal-agent conflict)

and thus reduces, in general, the need for paying cash dividends as an internal disciplinary

device on corporate managers.

On the other hand, numerous studies contend that when large shareholders (especially

families) hold almost full control, they appear to implement policies that generate benefits to

themselves at the expense of minority shareholders due to the absence of efficient monitoring

(Anderson and Reeb, 2003; Johnson et al., 2000; Morck and Yeung, 2003; Shleifer and

Vishny, 1997; Villalonga and Amit, 2006). In these cases, the salient agency problem is

hence expropriation of the wealth of minority investors by the controlling shareholders (so

called the “principal-principal conflict”). Consistent with the substitute model of dividends

purposed by La Porta et al. (2000), paying dividends reduces the possibility of expropriation

of wealth from others and thus establishes good treatment of minority shareholders.

Therefore, we posit that Turkish managers may employ cash dividends as a reputation

mechanism to attract investors.

H3: Corporate managers of BIST-listed firms pay cash dividends to indicate good

treatment of minority shareholders.

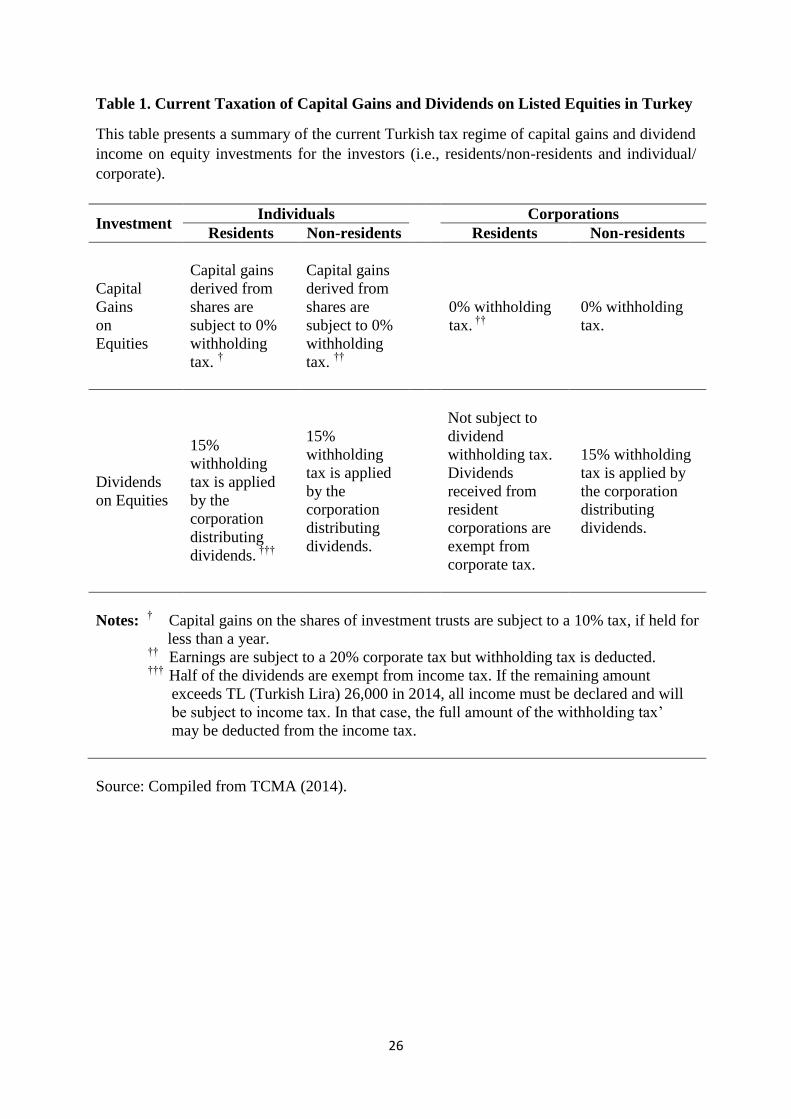

As we present a summary of the current Turkish tax regime on Table 1, differences

exist between the tax rate on capital gains and cash dividends as well as in the taxation of

dividends among investors. Hence, a tax factor may play an important role in dividend payout

decisions in Turkey. Under the current Turkish tax system, capital gains on equities are tax-

free for foreign investors (both individuals and corporations) and domestic individual

investors, whereas they must pay a 15% withholding tax for their cash dividends received on

the shares they hold. Conversely, domestic corporations are not subject to any taxes for either

capital gains or cash dividends that are derived on equities of resident incorporations (TCMA,

2014). Based on the tax-preference theory, investors generally should prefer shares that retain

cash rather than paying dividends in the Turkish market due to the tax advantage of capital

gains over cash dividends. In this scenario, we predict that Turkish managers of dividend-

Page 9

9

paying firms distribute cash dividends because they think different clienteles select dividend

policies according to their tax category circumstances. Accordingly, we hypothesize that:

H4: Corporate managers of BIST-listed firms show strong agreement in favor of the

tax clientele effect explanation.

(Insert Table 1 here)

As previously mentioned, BIST-listed firms have highly concentrated ownership

structures that are dominated by large shareholders, such as families, foreign investors,

financial institutions, and the state. Thus, expecting that the dividend preferences of these

shareholders are homogenous or stay unchanged over time is unrealistic. For instance, a

family-controlled parent company’s attitude toward dividend payments may differ based on

the cash needs of subsidiaries in the business group. Similarly, foreign investors’ sentiment

might change. For example, they may initially seek long-run growth potential, rather than

short-term dividend income. Yet, once they think their direct monitoring exercises on

management are inefficient or too costly, they may require higher cash dividends to augment

better monitoring by the capital markets. Hence, in accordance with the catering theory of

dividends, we formulate the following hypothesis:

H5: Corporate managers of BIST-listed firms base their dividend decisions on their

shareholders’ preferences.

Our sixth hypothesis relates to the transaction costs of dividends. In early periods, the

Turkish market suffered from non-transparent insider lending (non-arm’s length

transactions), especially within business groups. This lack of transparency resulted from

business group companies mostly obtaining much of their funds from their banks.

Nevertheless, after the CMB of Turkey made many amendments to improve the transparency

and quality of the banking sector and adopted related regulations to prevent insider lending as

a source of financing in 2001, listed firms have turned to the capital markets with a greater

incentive for more transparent financing. Thus, we posit that external financing may affect

cash dividend payment decisions of the Turkish managers because the external financing that

they now obtain from arm’s length parties can be more costly.

H6: Corporate managers of BIST-listed firms show strong agreement in favor of the

transaction cost theory.

Emerging markets are generally characterized by higher volatility and greater risk,

compared to the developed markets. Corporations in these markets generally have more

cyclical and impermanent earnings (Adaoglu, 2000; Glen et al. 1995). In this context, the ISE

has been highly representative of a promising but very volatile emerging market, with high

returns in some years and large losses in others (CMB, 2003, 2014; Odabasi et al., 2004).

Accordingly, we conjecture that Turkish managers of dividend-paying firms distribute cash

dividends to their shareholders as more certainty attached to dividend payments against

expected capital gains in the future.

Page 10

10

H7: Corporate managers of BIST-listed firms show strong agreement in favor of the

bird-in-the-hand theory.

Turkey had a very late start in the liberalization of its economy and the establishment

of its stock market (the ISE) whose history only dates back to 1986 (Adaoglu, 2000; Aksu

and Kosedag, 2006). Although the ISE is a relatively young stock market, compared to the

developed stock exchanges with hundreds of years of historical development, corporations

trading in the ISE vary from old and well-established family-controlled business group

companies whose roots can be traced back to the 1920s to large holding companies generally

founded in the 1970s (Bugra, 1994; Yurtoglu, 2003) or even comparatively young and

growing firms that incorporated in the 2000s. This situation implies that the ISE firm’s life

cycles differ dramatically from one another, which could affect how their managers make

corporate dividend policy decisions. Therefore, we hypothesize that:

H8: Corporate managers of BIST-listed firms show strong agreement in favor of the

maturity theory of dividends.

In the presence of real world-market frictions and investors’ preferences, Miller and

Modigliani’s (1961) irrelevance theory becomes highly arguable and dividend policy may

matter. In fact, survey evidence (Baker and Powell, 1999, 2012; Baker and Kapoor, 2015;

Baker et al., 2006; Dhanani, 2005) shows that corporate managers believe that dividend

policy affects firm value and that they tend to follow deliberate dividend policies to maximize

their share price. Accordingly, we hypothesize that, considering the recent developments in

the Turkish market, Turkish managers pay careful attention to making dividend policy

decisions, instead of adopting a residual dividend policy because they consider that their

dividend payment decisions affect common share prices and consequently, shareholder

wealth.

H9: Corporate managers of BIST-listed firms perceive that dividend policy affects

firm value.

Our final hypothesis concerns the most important factors influencing dividend policy

decisions. The ISE-listed firms were subject to mandatory dividend policy regulations in the

early periods. Hence, the compulsory dividend payout ratio imposed by the regulators shaped

dividend payments. Nevertheless, the CMB of Turkey abolished mandatory dividend

payment regulations. Thus, beginning in the fiscal year 2009, ISE corporate managers had the

freedom to make dividend policy decisions. Turkey has also made a serious effort to

implement various major economic and structural reforms to improve its market economy

and integrate with world markets. In this context, we hypothesize that factors similar to those

of their counterparts in developed markets such as the United States, Canada, and European

countries now influence Turkish managers when making their dividend policy decisions.

H10: The most important factors influencing dividend policies of corporate managers

of BIST-listed firms and their peers in other developed markets are similar.

Page 11

11

5. Research methodology

In this section, we discuss the sample, survey design, data collection and response

rate, statistical methods, and limitations of our study.

5.1 Sample

Using the Public Disclosure Platform of Borsa Istanbul (KAP) (2017), we draw our

sample according to the following criteria. First, we consider all firms listed on the BIST-All

Shares Index during 2014. Second, we exclude financial sector companies and utilities as

they are governed by different regulations and follow arguably different investment and

dividend policies. After these exclusions, we select corporations that paid at least one or more

cash dividends to common shareholders between January 1, 2010 and December 31, 2014.

The reason for restricting our sample to dividend-paying BIST-listed firms is because we

focus on why firms pay dividends, consistent with studies such as Baker et al. (2002, 2006,

2008) and Baker and Powell (2012). Finally, these selection criteria result in 126 non-

financial and non-utility dividend-paying firms listed on the BIST.

5.2 Survey design

A survey provides the primary data for this study. We design our questionnaire

mainly after those modeled by Baker and Powell (2000) and Baker et al. (2001, 2002), and

later used by Baker et al. (2006, 2007) and Baker and Powell (2012), and also employ

questions related to dividend policy from Brav et al. (2005). We make minor modifications to

adapt the questionnaire to the Turkish context. Using a similar questionnaire permits

comparing the views of corporate managers of BIST-listed firms with those reported in

previous studies thus finding cross-country differences or similarities involving the

determinants of dividend policy. The survey instrument is available from the authors on

request.

The final version of our survey consists of 55 questions consisting of three different

types. The first type contains seven closed-ended questions about the background information

of managers and their firms. The second type asks managers to express the importance level

of 21 factors that may affect their dividend policy decisions (hereafter we refer to as F1

through F21), using a five-point scale where 0 = none, 1 = low, 2 = moderate, 3 = high, and 4

= very high. The third type asks managers to indicate their level of agreement or

disagreement with each of 27 statements about dividend policy in general (hereafter we refer

to as S1 through S27), using a five-point scale where strongly disagree = −2, disagree = −1,

neutral = 0, agree = +1, and strongly agree = +2. The survey takes about 15 minutes to

complete.

5.3 Data collection and response rate

After obtaining the names, e-mail addresses, and telephone numbers of the financial

officers/directors of our initial sample from the Public Disclosure Platform of Borsa Istanbul

(2017), we emailed a cover letter with the attachment of our questionnaire to the top manager

Page 12

12

of each of these 126 firms in the first week of April 2015. We again emailed our survey to

non-respondents at the beginning of May 2015. Furthermore, we contacted the remaining

non-respondents by telephone and reminded them about our research from mid-June 2015 to

increase the response rate and to reduce potential non-response bias. By early-August 2015,

we had received 57 usable responses (16 responses from the first emailing, 18 responses from

the second emailing, and 23 responses after making telephone reminders) from 126 firms,

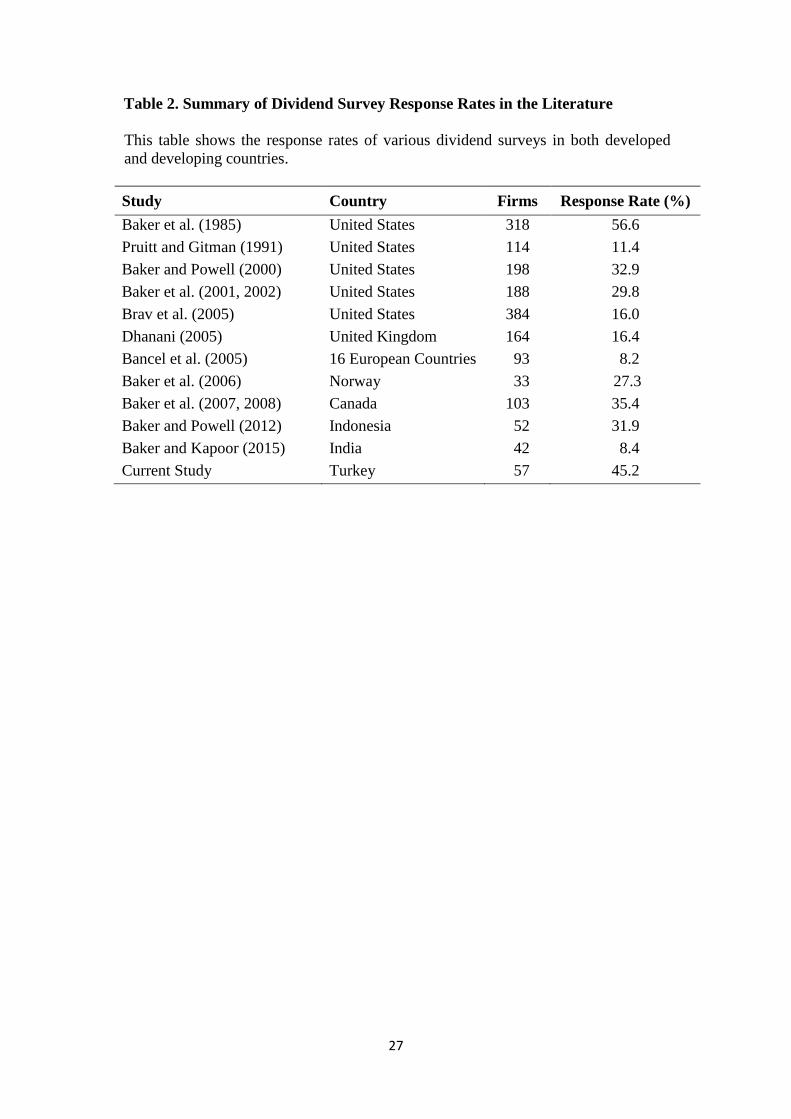

resulting in 45.2% response rate. As Table 2 shows, our response rate is relatively high

compared to rates obtained in similar studies. We also collect the secondary accounting and

financial data for our entire sample (both respondent and non-respondent firms) from

Datastream and Osiris databases to perform supplementary tests.

(Insert Table 2 here)

5.4 Statistical methods

We perform several statistical analyses to test our research hypotheses following prior

studies (Baker et al. 2006, 2008; Baker and Powell, 2012; Baker and Kapoor, 2015). First, we

employ a one-sample t-test for the null hypothesis that the mean response of the level of

agreement/disagreement for each of the 27 statements about dividend policy theories and

explanations equals 0 (neutral) on a five-point scale. Second, we again use a t-test to

determine whether the mean response for each of the 21 factors influencing dividend policy

differs significantly from 0 (no importance). Third, we estimate the Spearman rank

correlation coefficient (rs) to determine whether significant differences exist between the

rankings of these dividend factors by the corporate managers of BIST-listed firms and their

NYSE (New York Stock Exchange), NASDAQ (National Association of Securities Dealers

Automated Quotations), OSE (Oslo Stock Exchange), TSE (Toronto Stock Exchange), IDX,

and NSE counterparts. Lastly, we also conduct additional tests (i.e., Levene’s test, t-tests and

Wilcoxon test) for non-response bias.

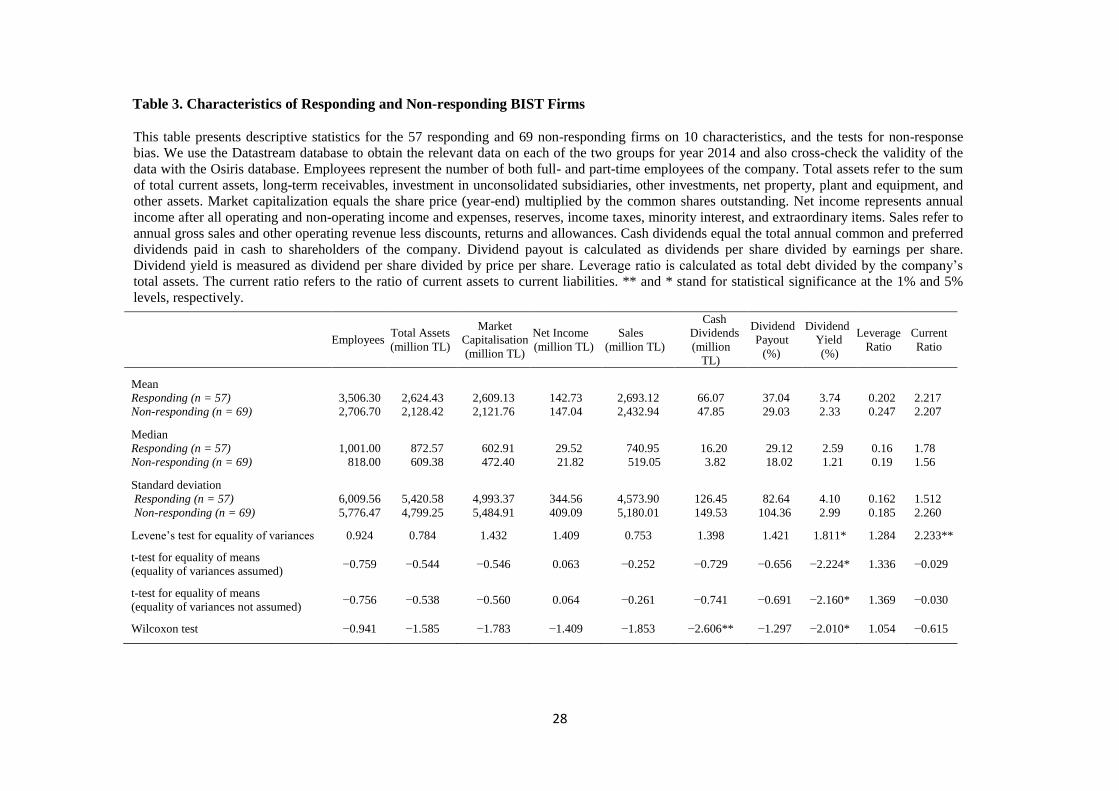

5.5 Limitations

Our study has several possible limitations. First, despite a 45.2% response rate, non-

response bias could be present. Following Baker and Kapoor (2015), we compare

characteristics of the 57 responding firms to those of the 69 non-responding firms applying

Levene’s test for equality of variance, t-tests for equality of means (when equality of variance

is assumed and not assumed) and the non-parametric Wilcoxon test.

(Insert Table 3 here)

As Table 3 displays, we analyze 10 firm characteristics (number of employees, total

assets, market capitalization, net income, sales, cash dividends, dividend payout, dividend

yield, leverage, and current ratios) for responding and non-responding firms based on 2014,

to determine whether the two groups differ significantly on each characteristic. The analyses

reveal that only one of the 10 characteristics, namely dividend yield, differs significantly at

the 5% level for all tests. Specifically, the responding firms have a higher dividend yield than

Page 13

13

the non-responding firms. The Wilcoxon test for cash dividends and the Levene’s test for the

current ratio report a significant difference at the 1% level between the two groups, while

other tests find no significant difference on these characteristics. Nevertheless, the results in

Table 3 show no significant differences exist between the responding and non-responding

firms on any of the remaining seven characteristics at the 5% level. This evidence indicates

that the firm characteristics of the two groups appear statistically similar. Hence, we conclude

that non-response bias does not appear to be a major concern.

Second, we limit our sample to dividend-paying firms because we only focus on why

firms pay dividends. The topic of why companies pay no dividends or how managers of non-

dividend paying firms perceive dividends could be the subject of another research study.

Hence, generalizing our findings to firms whose characteristics differ from those of our

current sample requires caution.

6. Results and discussion

We report our survey results in four sub-sections. The first sub-section presents the

profile information about respondents and their firms. The second sub-section illustrates the

level of support given by the respondents to various theories and explanations involving cash

dividends. The third sub-section examines the importance of factors affecting dividend

policy. The fourth sub-section investigates whether responses to our survey differ based on

different firm characteristics.

6.1 Profile of respondents and firms

Of the 126 surveys, 57 responding firms represent 11 broad industries of which the

most common types are basic resources (19.3%), industrial goods and services (19.3%),

construction and materials (17.5%), and personal households and goods (10.5%), which

constitute almost 67% of all firms. Of the 57 respondents, 84.2% confirm that they are

actively involved in making their companies’ dividend policy decisions. The most common

titles of the respondents are chief financial officer (52.6%), director of finance (26.3%), and

chief executive officer (8.8%), whereas the remaining respondents hold positions such as

director of investor relations, chief accountant, and general manager (finance). Thus, survey

respondents represent top managers of the responding firms who are generally involved in the

dividend policy of their firms.

Of the responding firms, 91.2% only paid dividends during the last five years and

8.8% both paid dividends and repurchased shares. This evidence may reflect that managers of

dividend-paying BIST firms do not view share repurchases as substitutes for dividends,

unlike some U.S. counterparts suggested by Brav et al. (2005). When asked what would be

the most likely alternative use if they had not paid dividends, 52.6% of the respondents

indicated that they would invest more. The second and third most popular answers are to pay

off their own debt (22.8%) and retain the funds as cash (15.8%), followed by using for

mergers/acquisitions and repurchasing shares (5.3% and 3.5%, respectively). Most managers

(82.5%) indicate that they re-examine their firms’ dividend policies annually, compared with

Page 14

14

7.1% that reported every 3 to 5 years, 3.5% that said every six months, and 6.9% stated that

they reconsider their dividend decisions when necessary.

6.2 Theories and explanations involving cash dividends

We test our research hypotheses by investigating the level of support given by

corporate managers of BIST-listed firms to 27 statements based on various theories and

explanations for paying cash dividends. Table 4 presents the survey results from the

respondents, by reporting the descriptive statistics (percentages, mean, and standard

deviation) and t-value for the null hypothesis that mean response equals 0 (neutral) for each

statement.

(Insert Table 4 here)

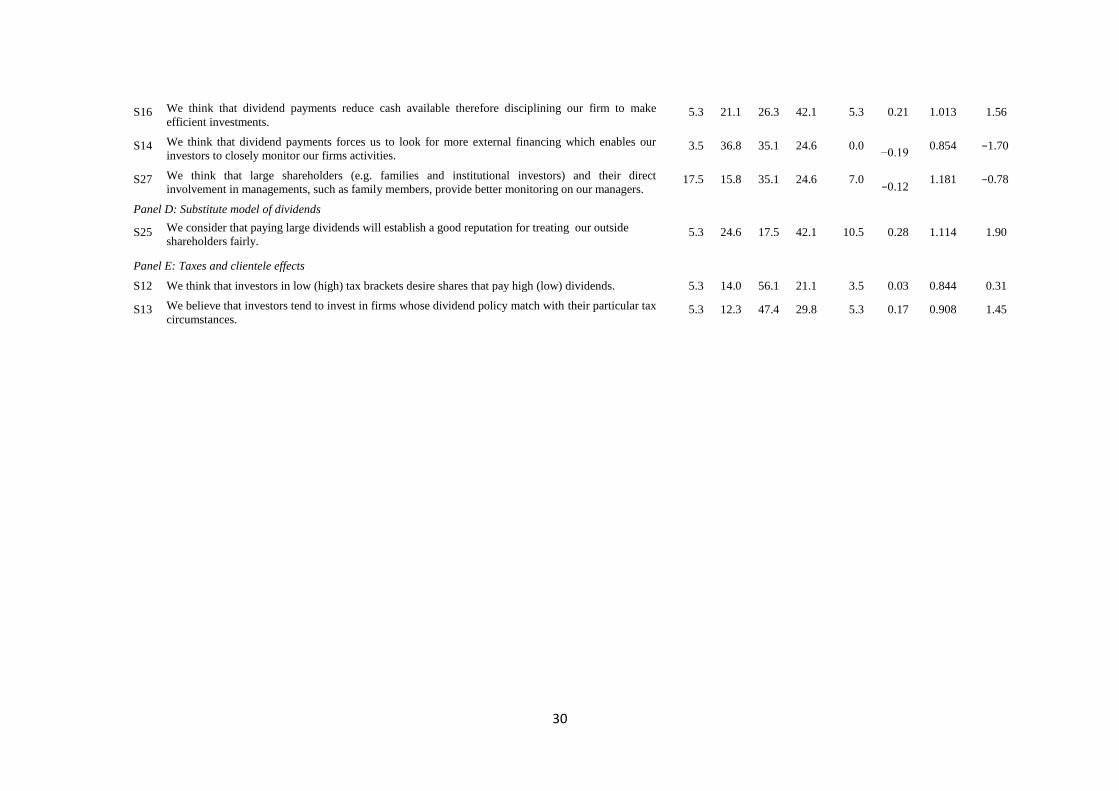

Panel A in Table 4 shows the responses to six statements (S7, S8, S9, S10, S11, and

S26) based on signaling theory. The mean responses of four of these statements are positive

and differ significantly from 0 (neutral) at the 1% level. Of the 57 responding managers, 86%

of them agree that their firms should appropriately inform their investors about the reasons

for changing cash dividends (S11). About 84% of managers consider that their dividend

decisions signal information about their company to investors (S7). Close to 74% of

respondents believe that investors evaluate dividend changes as signals about their firm’s

future performance (S9). Similarly, nearly 60% of managers think that their share price

generally increases (decreases) when their firms increase (decrease) dividend payments (S8).

Consequently, the evidence from these four statements provides support for the signaling

explanation. Moreover, the mean of manager opinions on one of these statements also differs

significantly from 0 at the 1% level but is negative. More than 61% of managers disagree

with the statement that their firms pay higher dividends to signal that their firm is strong

enough to raise costly external capital if needed thereby making them look better than their

competitors (S26). This finding implies that corporate managers of BIST-listed firms are

more concerned with changes in dividends from one period to the next, rather than the

absolute level of dividends. Additionally, the respondents’ views vary about whether

dividend increases are questionable (S10) with a mean value that does not significantly differ

from 0 at the 5% level. In summary, our results suggest that the dividend-paying corporate

managers of BIST-listed firms are aware of signaling and agree with the notion that changes

in dividends have signaling effects. Hence, this evidence lends support to H1.

Panel B in Table 4 reports corporate managers of BIST-listed firms’ views on five

statements (S1, S2, S3, S4, and S5) based on Lintner’s (1956) behavioral model explaining

the corporate dividend setting process and patterns. The mean manager responses to all five

statements are statistically significant from 0 (neutral) at the 1% level. More than 96% of the

managers confirm that they set dividend payments based upon past dividends and current

earnings (S2). About 86% of the managers indicate that they tend to carry on a smooth

dividend payment stream from year to year (S1). Close to 81% of respondents report that they

are reluctant to reduce dividends unless adverse circumstances are likely to persist (S5).

Almost 72% of the respondents state that they only change dividend payout when sustainable

Page 15

15

shifts in earnings occur (S4). About 63% declare that they set a target dividend payout ratio

and make partial adjustments in current payout toward the target (S3). Accordingly, Panel B

shows that dividend-paying BIST-listed firms’ managers set their cash dividends in line with

Lintner’s dividend model. The responding corporate managers of BIST-listed firms make

their dividend decisions conservatively, determining dividend payouts based on sustainable

earnings, and using a target payout ratio. They pursue stable dividend policies and are

reluctant to cut dividends except in extreme cases. Therefore, the survey evidence provides

support for H2.

Panel C in Table 4 presents the results of managers’ responses to four statements

(S14, S15, S16, and S27) involving agency cost theory but none of them is statistically

significant from 0 (neutral). About 35% of the respondents are neutral about whether

dividends force them to look for more external financing, which subjects their firms to

scrutiny by investors (S14), and whether large shareholders and their direct involvement in

management provide better monitoring (S27). On average, they disagree with S14 and S27.

Although almost half of the responding managers think that dividends encourage them to act

in the interest of their outside shareholders (S15) and agree that dividends reduce cash

available hence disciplining them to make efficient investment (S16), the remainder has no

idea or disagree with these two statements. Accordingly, our evidence from corporate

managers of BIST-listed firms does not support the agency cost explanation for paying cash

dividends, which is consistent with previous survey studies such as Baker et al. (2007) in

Canada and Baker and Kapoor (2015) in India. This finding might reflect improvements in

corporate governance and transparency and disclosure practices implemented by the

publication of the CMB of Turkey’s Corporate Governance Principles in 2003 and greater

compliance to these principles by corporate managers of BIST-listed firms in the post-2003

period. However, it may also be the result of refusal to recognize or disclose the existence of

agency conflicts, as Baker and Kapoor (2015) suggest.

Moreover, evidence in Panel D of Table 4 reveals that more than 52% of the

respondents agree with the statement that paying large dividends will establish a good

reputation for treating their outside shareholders fairly (S25). However, the mean response to

this statement does not differ significantly from 0 (neutral) at the 5% level. Hence, the

substitute model of dividends, developed by La Porta et al. (2000), which posits that

dividends are substitutes for legal protection in the countries with poor shareholders’

protection and establish a reputation for good treatment of minority investors, receives

insufficient support in explaining cash dividend decisions of corporate managers of BIST-

listed firms. This finding means that these managers do not appear to use cash dividends as

an internal disciplinary device or as a reputation mechanism. Thus, based on the survey’s

finding, we reject H3.

Panel E in Table 4 shows the responses to two statements (S12 and S13) involving

taxes and clientele effects. The mean responses of both statements do not differ significantly

from 0 (neutral). About 56% of managers are unsure about whether investors in low (high)

tax brackets desire shares that pay high (low) dividends (S12). Almost 48% of them have no

Page 16

16

idea about whether investors tend to invest in firms whose dividend policy matches with their

particular tax circumstances (S13). These findings are consistent with Baker et al. (2002) and

Brav et al. (2005) in the United States, and Baker et al. (2006) in Norway, who report little or

no support for tax-related explanations. Accordingly, although differences exist between the

tax rate on capital gains and cash dividends as well as in the taxation of dividends among

investors in Turkey, our survey results find little evidence that corporate managers of BIST-

listed firms favor the tax-preference or clientele effects for paying dividends. Therefore, this

evidence leads us to reject H4.

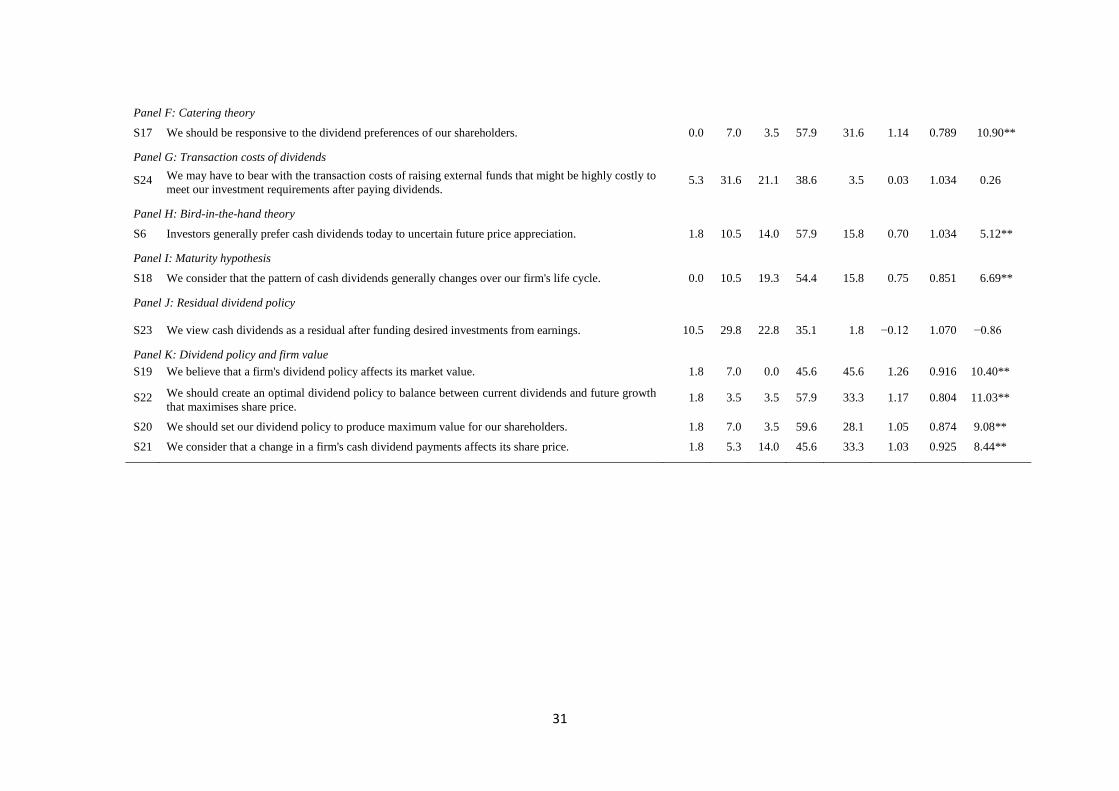

As Panel F in Table 4 presents, about 90% of respondents agree that they should be

responsive to the dividend preferences of their shareholders (S17). In fact, the mean response

is the second highest among 27 statements about theories/explanations for paying dividends

and differs significantly from 0 (neutral) at the 1% level. This evidence is consistent with the

catering theory of dividends and the survey results of Baker and Powell (2012) and Baker and

Kapoor (2015) from Indonesia and India, respectively. Consequently, Baker and Wurgler

(2004a, 2004b) suggest that investor demands determine the managers’ decisions to pay

dividends. Our evidence reveals that corporate managers of BIST-listed firms take their

shareholders’ preferences into consideration while making dividend payment decisions.

Hence, the survey evidence provides support for H5.

Panel G in Table 4 provides the responses to a statement related to the transaction

costs of dividends (S24). The survey asks corporate managers of BIST-listed firms to express

their agreement on whether they have to bear the transaction costs of raising external funds

that might be highly costly to meet their investment requirements after paying dividends. The

mean responses to this statement do not differ significantly from 0 (neutral) at the 5% level.

About 21% of the responding managers are neutral and almost 37% of them do not agree,

whereas the remaining 42% of respondents agree with the statement. Hence, our evidence

indicates that responding managers generally do not consider transaction costs of dividends

as a troubling issue when making dividend payment decisions. Therefore, we reject H6.

Panel H in Table 4 presents the managers’ responses to a statement of the bird-in-the-

hand theory (S6). These positive mean responses differ significantly from 0 (neutral) at the

1% level. Consistent with the bird-in-the-hand theory, almost 74% of the responding

managers think that investors generally prefer cash dividends today to uncertain future price

appreciation. Our evidence is contrary to the findings of surveys of Baker and Powell (2000)

and Baker et al. (2001) who report no support for this explanation for paying dividends from

NYSE and NASDAQ managers. Further, studies of Indian (Baker and Kapoor, 2015) and

Indonesian (Baker and Powell, 2012) firms find inconclusive evidence about how managers

perceive the bird-in-the-hand theory. In this respect, our survey reveals that our respondents

consider that their shareholders/investors are more conservative than their colleagues in those

markets and hence they favor the bird-in-the-hand theory. Thus, our survey evidence lends

support to H7.

Panel I in Table 4 shows mangers’ opinions about the maturity (firm life cycle) theory

of dividends. About 70% of managers state that the pattern of cash dividends generally

Page 17

17

changes over their firm’s life cycle (S18), with the mean response that is positive and

significantly different from 0 (neutral) at the 1% level. Therefore, corporate managers of

BIST-listed firms generally express agreement with the maturity theory of dividends

consistent with NSE, IDX, TSX, NASDAQ, and NYSE managers as reported by previously

mentioned surveys. This evidence provides support for H8.

Panel K in Table 4 displays the responses of corporate managers of BIST-listed firms

to four statements (S19, S20, S21, and S22) about dividend policy and firm value. The mean

responses to all four statements differ significantly from 0 (neutral) at the 1% level. The

evidence reveals that about 91% of managers believe that a firm’s dividend policy affects its

market value (S19) and they should create an optimal dividend policy to balance between

current dividends and future growth that maximizes share price (S22). Almost 88% of

managers think that they should set their dividend policy to produce maximum value for their

shareholders (S20). Close to 79% of managers express their agreement that a change in a

firm’s cash dividend payments affects its share price (S21). Subsequently, the results shown

in Panel K reveal that the responding managers perceive that dividend policy matters and

affects firm value in contrast to Miller and Modigliani’s (1961) dividend irrelevance theory.

This finding is not surprising given the perfect market conditions assumed by Miller and

Modigliani.

Panel J in Table 4 provides the managers’ responses to a statement about residual

dividend policy (S23). Around 40% of managers do not view cash dividends as a residual

after funding desired investments from earnings, whereas 23% of them are neutral about this

statement. Given that the mean responses to S23 do not differ significantly from 0 (neutral),

this means that the responding managers generally do not support a residual dividend policy.

As previously mentioned, our survey results suggest that respondents believe that dividend

policy matters and affects firm value and therefore shareholder wealth. These managers

typically attempt to follow managed dividend policies with a specific pattern of dividend

payments that involves dividend smoothing, instead of simply paying out whatever remains

after funding investments from internally generated cash flows. Thus, our survey evidence

provides support for H9.

In summary, our survey evidence from managers of dividend-paying BIST firms

provides general support for the signaling theory, Lintner’s (1956) partial adjustment model,

catering, maturity (firm life cycle), and bird-in-the-hand hypotheses for explaining cash

dividends. However, the results do not support the agency cost theory, substitution model of

dividends, tax-related explanations, transaction cost theory, and residual dividend policy.

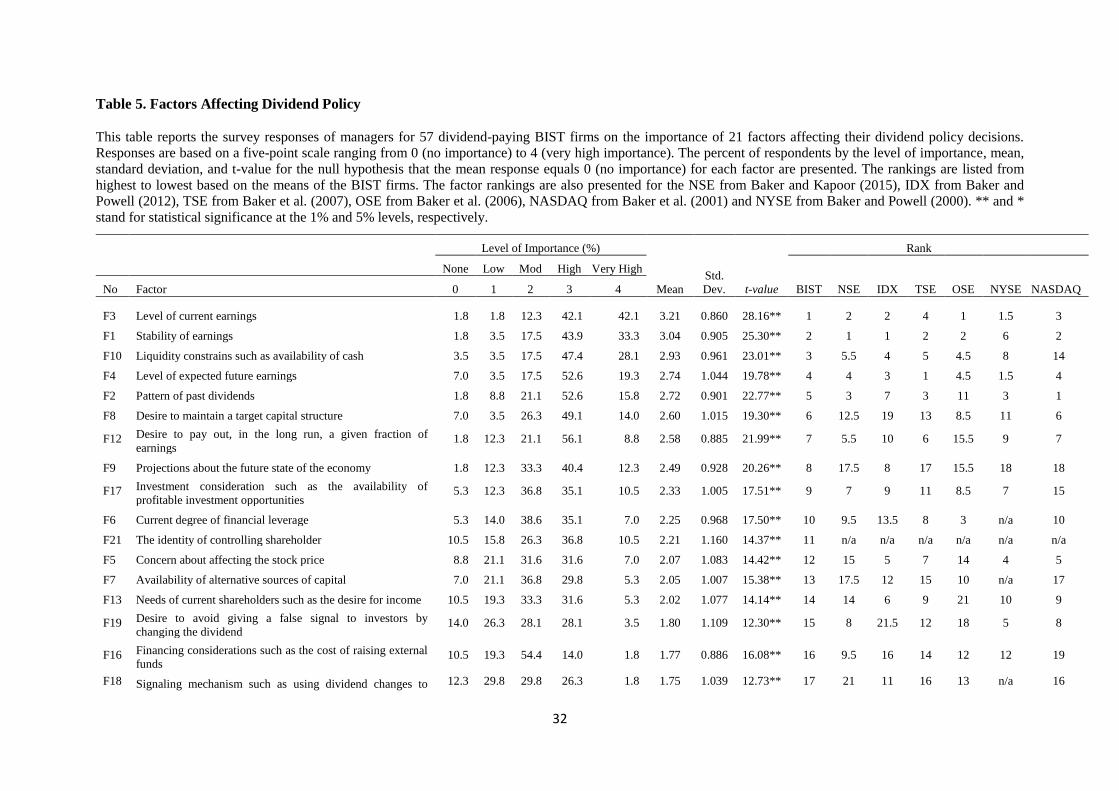

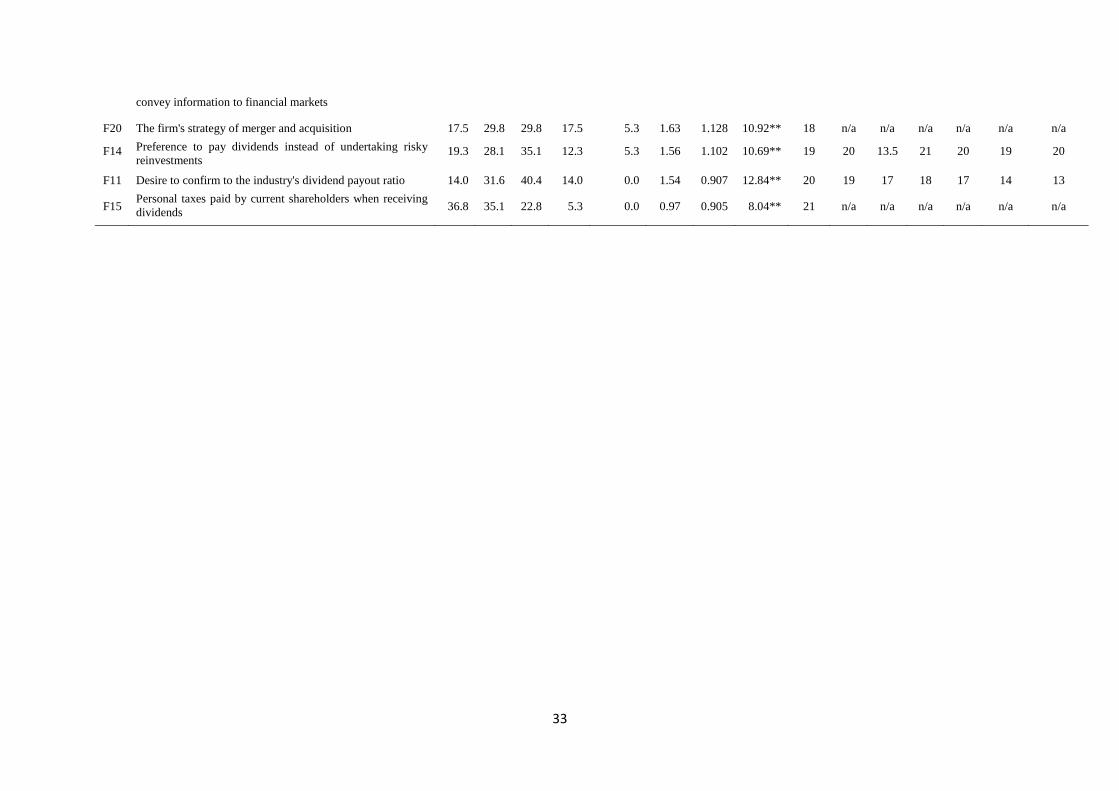

6.3 Factors affecting dividend policy

Our final hypothesis relates to the most important factors affecting dividend policy

decisions of corporate managers of BIST-listed firms. This hypothesis tests whether these

managers give similar or different overall importance to factors influencing dividend policy

compared to managers from developed markets. Table 5 shows the level of importance of 21

potential factors of the dividend policies of the responding companies, by reporting the

Page 18

18

descriptive statistics and the results for each of the 21 factors ranked by their mean score

along with their corresponding t-statistic for the null hypothesis that the mean response

equals 0 (no importance).

(Insert Table 5 here)

As Table 5 shows, the positive t-values for all 21 factors are statistically significant at

the 1% level, indicating that the mean importance level of each of these factors is

significantly greater than 0. This means that corporate managers of BIST-listed firms view all

21 factors as important to some degree in making their dividend policy decisions. The

following discussion focuses on the highest ranked factors.

The results reveal that at least half of the responding managers identify eight factors

as being of high/very high importance (F1, F2, F3, F4, F8, F9, F10, and F12). The three most

highly ranked factors are the level of current earnings (F3), the stability of earnings (F1), and

liquidity constrains such as availability of cash (F10) (84.2%, 77.2%, and 75.5%,

respectively). The fourth highest ranked factor is the level of expected future earnings (F4)

(71.9%). Given that three of four highest ranked factors relate to earnings, this implies that

respondents place high importance on earnings. A likely justification for this ranking is

because earnings are closely associated with cash flows and cash generally serves as the basis

for paying dividends. One of these four most highly ranked factors concerns the availability

of cash in terms of liquidity constraints (F10), suggesting that the availability of cash affects a

firm’s ability to distribute cash dividends. Furthermore, the pattern of past dividends (F2)

ranks as the fifth highest factor by about 68% of respondents. Hence, our results provide

strong evidence that managers of the dividend-paying BIST firms set their dividend policies

(1956) suggested more than 60 years ago. This evidence is also consistent with the responses

illustrated in Panel B of Table 4, which show that respondents report following a traditional

Lintner-style managed dividend policy. Other factors having at least half of the responding

managers view as important are the desire to maintain a target capital structure (F8), the

desire to pay out, in the long run, a given fraction of earnings (F12), and projections about the

future state of the economy (F9) (63.1%, 64.9%, and 52.7%, respectively).

The Spearman rank order correlation coefficient (rs) is the measure used to determine

whether a significant association exists between the rankings of the dividend factors given by

managers of the BIST and managers from developed markets, such as the NYSE and

NASDAQ (United States), TSE (Canada), and OSE (Norway). We also calculate the

Spearman rank correlation coefficients for NSE (Indian) and IDX (Indonesian) managers to

identify if corporate managers of BIST-listed firms give similar or different overall

importance to factors influencing dividend policy compared to their counterparts in different

emerging markets. Table 5 shows the rankings, which are provided from a number of prior

studies. More precisely, we obtain the rankings for the NSE from Baker and Kapoor (2015),

IDX from Baker and Powell (2012), TSE from Baker et al. (2007), OSE from Baker et al.

(2006), NASDAQ from Baker et al. (2001), and NYSE from Baker and Powell (2000). The

related correlation coefficients are as follows; 0.823 for BIST-NSE, 0.698 for BIST-IDX,

Page 19

19

0.810 for BIST-TSE, 0.740 for BIST-OSE, 0.653 for BIST-NASDAQ (all significant at the

1% level) and 0.620 for BIST-NYSE (significant at the 5% level). As hypothesized, these

results reveal that corporate managers of BIST-listed firms rank the factors affecting their

dividend policy decisions in a significantly positive way along with their peers of these

developed (TSE, OSE, NYSE, and NASDAQ) markets. Therefore, these results lend support

to H10. Likewise, our results indicate that respondents also rank the dividend factors

similarly to their counterparts in other emerging (NSE and IDX) markets. Finally, although

characteristics of both these firms and markets differ in many aspects (e.g. adequate

disclosure, laws and regulations, institutional environment, corporate governance practices

and ownership structures, political, social and financial stability), the rankings reveal that the

factors related to earnings (F1, F2, F3, and F4) are always among the most highly ranked by

managers of firms listed on all seven markets. Specifically, stability of earnings (F1), the

level of current and expected future earnings (F3 and F4), and the pattern of past dividends

(F2) appear to be the most important factors in making corporate dividend policy decisions.

This finding is consistent with the pioneering study of Lintner (1956) and surveys conducted

decades ago by Baker et al. (1985) and Pruitt and Gitman (1991).

6.4 Firm characteristics and survey responses

In this sub-section, we perform additional tests to investigate whether managerial

responses to our survey differ based on various firm characteristics. We also provide further

information about the distribution of our survey responses. Accordingly, we start by

partitioning our sample into (1) firms with low and high dividend distribution frequency, (2)

low and high payout firms, (3) small- and large-size firms, (4) low and high growth firms, (5)

low and high profitability firms, (6) low and high levered firms, and (7) family-controlled

firms. Following previous studies (Dhanani, 2005; Baker et al., 2012), we use Wilcoxon

rank-sum tests to identify if the responses from each pair in the sub-sample of a firm’s

characteristics differ on each of the 27 statements and 21 factors. Due to space limitations, we

summarize the results of these tests, which are available from the authors on request.

The results of the Wilcoxon rank-sum tests involving the managerial responses on the

agreement of 27 statements related to various theories and explanations of dividend policy

are generally similar across the seven sub-samples. Overall, different firm characteristics do

not change the levels of statistical significance of our research hypotheses and thus do not

affect our major findings. However, a few significant differences occur in the agreement

levels of different sub-samples’ managers. Among the explanations receiving support from

our study, we test the signaling theory using six statements (S7, S8, S9, S10, S11 and S26).

Of the seven sub-samples, only managers in the profitability group exhibit significantly

different mean responses at the 5% level for just one statement (S8). Specifically, managers

of low profitability firms express more agreement with the notion that their share price

generally increases (decreases) when their firms increase (decrease) dividend payments.

Regarding Lintner’s (1956) partial adjustment model, only managers of the leverage group

have significantly different mean responses at the 5% level for one (S2) of the five statements

(S1, S2, S3, S4, and S5). That is, managers of low-levered firms indicate more agreement

Page 20

20

with the statement that they set dividend payments based on past dividends and current

earnings.

Considering the other arguments supported by our survey findings, managers’

responses to the statements relating to catering theory (S17) and the maturity hypothesis

(S18) show no significant differences between any pairs of these seven sub-samples. By

contrast, managers in the dividend payout ratio, leverage, and family-controlled groups

display significantly different responses at the 5% level to the statement of the bird-in-the-

hand theory (S6). Specifically, managers of high payout and high levered family-controlled

companies give more weight to the idea that investors generally prefer cash dividends today

to uncertain future price appreciation, compared to the managers of low-payout and low-

levered non-family companies. Additionally, only managers of family-controlled firms

exhibit significantly different mean responses at the 5% level to two (S19 and S22) of the

four statements (S19, S20, S21, and S22) in relation to dividend policy and firm value. More

specifically, managers of family firms express higher levels of agreement with statements

that dividend policy affects market value and that they should create an optimal dividend

policy to balance current dividends and future growth to maximize share price.

The test results on firm characteristics’ sub-samples do not support the agency cost

and transaction cost theories, substitute model of dividends, tax-related and residual dividend

policy explanations, which are consistent with our main findings. Mean responses to the

statements about the substitute model (S25), transaction cost theory (S24), and residual

dividend policy (S23) provide no significant differences across any pairs of all sub-groups.

Although the results do not support the agency cost theory and tax-related explanations,

managers of high payout and smaller size firms exhibit more agreement to the idea that

dividend payments reduce excess cash and hence discipline firms to make efficient

investments (S16). Managers of non-family firms strongly disagree with the argument that

large shareholders and their direct involvement in management provide better monitoring

(S27). Additionally, managers of low-payout firms agree more strongly with the statement

that investors in low (high) tax brackets desire shares that pay high (low) dividends (S12).

Finally, we analyze the results of the Wilcoxon rank-sum tests for the managerial

responses on the importance of 21 factors affecting dividend policy based on seven different

firm-characteristic sub-samples. The evidence reveals only a few significant differences

about the perceptions of managers involving the seven groups toward these factors. For

instance, of the eight most highly ranked factors based on importance (F1, F2, F3, F4, F8, F9,

F10, and F12), only two factors (F2 and F10) have significantly different responses at the 1%

level and 5% level, respectively. Each factor differs based on only one group (i.e., the

profitability and growth sub-samples, respectively). In particular, managers of high

profitability firms attach greater importance to the pattern of past dividends (F2), whereas

managers of high growth firms exhibit more concern about liquidity constraints such as

availability of cash (F10). Although a few more significant differences exist involving other

factors, the results generally suggest that different firm characteristics are not related to

noteworthy differences in the distribution of our survey responses.

Page 21

21

7. Conclusions

This study provides new survey-based evidence on how managers of dividend-paying

BIST-listed firms view various theories/explanations for paying cash dividends and the most

important factors affecting their dividend policy decisions. This survey evidence is important

because it investigates the perceptions of managers of an emerging market after receiving

greater flexibility in making dividend payment decisions. Previously, Turkish firms had strict

mandatory dividend policy rules, which changed after Turkish authorities implemented major

economic and structural reforms for market integration and abolished the compulsory

dividend payout regulatory framework. The findings of this study lead to several conclusions

about dividend policy.

First, several studies conducted in early periods in Turkey report that Turkish-listed

firms generally concentrated on the mandatory dividend payout ratio imposed by the

regulations (Adaoglu, 2000; Aivazian et al., 2003a). Hence, managers based their cash

dividend payments on the firm’s current year earnings and the level of cash dividends

reflected any variability in earnings. Consequently, dividend smoothing or stability was not a

major consideration. Currently, however, managers of dividend-paying BIST-listed firms

appear to follow managed dividend policies with a specific pattern of dividend payments that

involves dividend smoothing. Consistent with Lintner (1956), they are conservative in

making their dividend decisions, determining dividend payouts based on sustainable earnings,

using a target payout ratio, and making partial adjustments in current payout toward the

target. Hence, these firms pursue stable dividend policies. These managers tend to cut

dividends in extreme cases.

The results further show that respondents perceive that dividend policy affects firm

value and changes in dividends influence share prices and thus shareholder wealth.

Accordingly, these managers believe that they should set their firm’s dividend policies to

maximize shareholder wealth by formulating an optimal dividend policy that balances

between current dividends and future growth. Respondents express strong support for the

signaling, catering, maturity (firm life cycle) and bird-in-the-hand theories. However, the

evidence offers little or no support for agency cost theory, substitute model of dividends, tax-

related explanations, transaction cost theory, and residual dividend policy. The survey

evidence supports multiple theories for paying cash dividends in the Turkish market, which is

inconsistent with a universal or “one-size-fits-all” explanation for paying dividends.

The survey evidence also shows that the most important factors affecting the dividend

policy of BIST-listed firms relate to earnings, specifically, the level of current and expected

future earnings as well as the stability of earnings. Liquidity constraints such as availability

of cash and the pattern of past dividends are other important factors identified by the

responding managers. Comparisons between the views of managers of BIST-listed firms and

their peers in other developed (TSE, OSE, NYSE, and NASDAQ) and emerging (NSE and

IDX) markets on the dividend factors reveal statistically significant positive correlations. This

finding suggests that after implementing major economic and structural reforms and

abolishing mandatory dividend payment requirements, corporate managers of BIST-listed

Page 22

22

firms follow similar dividend policy factors and patterns of dividend policy as managers in

more developed countries.

The factors related to earnings and past dividends appear to be the most highly ranked

determinants for all seven markets, despite differing characteristics among these markets.

These results lead to the conclusion that some factors are typically more important than

others without claiming that they are a universal set of determinants applicable equally to all

firms. However, our evidence reveals that different firm characteristics reflect few

statistically significant differences in the distribution of our survey responses.

References

Adaoglu, C. (1999). Regulation influence on the dividend policy of the Istanbul Stock

Exchange (ISE) corporations. The Istanbul Stock Exchange (ISE) Review – Quarterly

Economics and Finance Review, 3 (11), 1‒19.

Adaoglu, C. (2000). Instability in the dividend policy of the Istanbul Stock Exchange (ISE)

Corporations: Evidence from an emerging market. Emerging Markets Review, 1 (3), 252‒

270.

Adaoglu, C. (2008). Dividend policy of the ISE industrial corporations: The evidence

revisited (1986‒2007). Journal of BRSA Banking and Financial Markets, 2 (2), 113‒135.

Aivazian, V., Booth, L., & Cleary, S. (2003a). Dividend policy and the organisation of capital

markets. Journal of Multinational Financial Management, 13 (2), 101‒121.

Aivazian, V., Booth, L., & Cleary, S. (2003b). Do emerging market firms follow different

dividend policies from US firms? Journal of Financial Research, 26 (3), 371‒387.

Aksu, M., & Kosedag, A. (2006). Transparency and disclosure scores and their determinants

in the Istanbul Stock Exchange. Corporate Governance, 14 (4), 277‒296.

Al-Najjar, B., & Kilincarslan, E. (2016). The effect of ownership structure on dividend

policy: Evidence from Turkey. Corporate Governance: The International Journal of

Business in Society, 16 (1), 135‒161.

Anderson, R. C., & Reeb, D. (2003). Founding-family ownership and firm performance:

Evidence from the S&P 500. Journal of Finance, 58 (3), 301‒1328.

Ararat, M., & Ugur, M. (2003). Corporate governance in Turkey: An overview and some

policy recommendations. Corporate Governance, 3(1), 58‒75.

Baker, H. K. (ed.). (2009). Dividends and Dividend Policy. Hoboken, NJ: John Wiley & Sons

Inc.

Baker, H. K., Chang, B., Dutta, S. & Saadi, S. (2012). Why companies do not pay dividends:

The Canadian experience. Journal of Business Finance & Accounting, 39 (9-10), 1330-1356.

Page 23

23

Baker, H. K., Dutta, S., & Saadi, S. (2008). Impact of financial and multinational operations

on manager perceptions of dividends. Global Finance Journal, 19 ( 2), 171‒186.

Baker, H. K., Farrelly, G. E., & Edelman, R. B. (1985). A survey of management views on

dividend policy. Financial Management, 14 (3), 78‒84.

Baker, H. K., & Kapoor, S. (2015). Dividend policy in India: New survey evidence.

Managerial Finance, 41 (2), 182‒204.

Baker, H. K., Mukherjee, T. K., & Paskelian, O. G. (2006). How Norwegian managers view

dividend policy. Global Finance Journal, 17 (1), 155‒176.

Baker, H. K., & Powell, G. E. (1999). How corporate managers view dividend policy.

Quarterly Journal of Business and Economics, 38 (2), 17‒35.

Baker, H. K., & Powell, G. E. (2000). Determinants of corporate dividend policy: A survey

of NYSE firms. Financial Practice and Education, 10 (1), 29‒40.

Baker, H. K., & Powell, G. E. (2012). Dividend policy in Indonesia: Survey evidence from

executives. Journal of Asia Business Studies, 6 (1), 79‒92.

Baker, H. K., Powell, G. E., & Veit, E. T. (2002). Revisiting managerial perspectives on

dividend policy. Journal of Economics and Finance, 26 (2), 267‒283.

Baker, H. K., Saadi, S., Dutta, S., & Gandhi, D. (2007). The perception of dividends by

Canadian managers: New survey evidence. International Journal of Managerial Finance, 3

(1), 70‒91.

Baker, H. K., Singleton, J. C., & Veit, E. T. (2011). Survey Research in Corporate Finance:

Bridging the Gap between Theory and Practice. New York: Oxford University Press.

Baker, H. K., Veit, E. T., & Powell, G. E. (2001). Factors influencing dividend policy

decisions of Nasdaq firms. Finance Review, 38 (3), 19‒38.

Baker, M., & Wurgler, J. (2004a). A catering theory of dividends. Journal of Finance, 59 (3),

1125‒1165.

Baker, M., & Wurgler, J. (2004b). Appearing and disappearing dividends: The link to

catering incentives. Journal of Financial Economics. 73 (2), 271‒288.

Bancel, F., Bhattacharyya, N., and Mittoo, U. R. (2005). Cross-country Determinants of

Payout Policy: A Survey of European Firms. SSRN Working Paper, available at

http://papers.ssrn.com/sol3/papers.cfm?abstract_id=683111.

Birol, O. H. (2011). The effects of the global economic crisis on Turkey’s economy and the

recent tilt in her international relations. International Journal of Business and Management

Studies, 3(2), 227‒236.

Brav, A., Graham, J. R., Harvey, C. R., & Michaely, R. (2005). Payout policy in the 21st

century. Journal of Financial Economics, 77 (3), 483‒527.

Page 24

24

Bruner, R. E. (2001). Does M&A pay? A survey of evidence from the decision-maker.

Journal of Applied Finance, 12 (1), 48‒68.

Bugra, A. (1994). State and Business in Modern Turkey: A Comparative Study. Albany, NY:

State University of New York.

Caliskan, N., & Icke, T. (2011). Turkish corporate governance principles and its implications

for ISE corporate governance index companies. Journal of Accounting and Finance, 11(1),

60‒75.

Chiang, K., Frankfurter, G. M., Kosedag, A., & Wood, B. G. Jr. (2006). The perception of

dividends by professional investors. Managerial Finance, 32 (1), 60‒81.

CMB (2003). Annual Report 2003. Ankara: Capital Markets Board of Turkey.

CMB (2014). Annual Report 2014. Ankara: Capital Markets Board of Turkey.

Demsetz, H., & Lehn, K. (1985). The structure of corporate ownership: Causes and

consequences. Journal of Political Economy, 93 (6), 1155‒1177.

Dhanani, A. (2005). Corporate dividend policy: The views of British financial managers.

Journal of Business Finance & Accounting, 32 (7), 1625‒1672.

Erturk, I. (2003). Governance or financialisation: The Turkish case. Competition and Change,

7 (4), 185‒204.

Faccio, M., Lang, L. H. P., & Young, L. (2001). Dividends and expropriation. American

Economic Review, 91 (1), 54‒78.

Glen, J. D., Karmokolias, Y., Miller, R. R., & Shah, S. (1995). Dividend policy and

behaviour in emerging markets: To pay or not to pay. IFC Discussion Paper, 26.

Washington, DC: International Finance Corporation.

Grossman, S. J., & Hart, O. D. (1980). Takeover bids, the free-rider problem, and the theory

of the corporation. Bell Journal of Economics, 11 (1), 42‒64.

Grullon, G., Michaely, R., & Swaminathan, B. (2002). Are dividend changes a sing of firm

maturity. Journal of Business, 75 (3), 387‒424.

Gursoy, G., & Aydogan, K. (1999). Equity ownership structure, risk-taking and performance:

An empirical investigation in Turkish companies. Paper presented at the ERC/METU

International Conference in Economics in Ankara.

IIF. (2005). Corporate Governance in Turkey – An Investor Perspective. Task Force Report.

Washington, DC: Institute of International Finance, Inc.

Johnson, S., La Porta, R., Lopez-de-Silanes, F., & Shleifer, A. (2000). Tunnelling, American

Economic Review, 90 (1), 20‒27.

Page 25

25

Kirkulak, B., & Kurt, G. (2010). Are dividends disappearing or shrinking? Evidence from the

Istanbul Stock Exchange. Emerging Markets Finance and Trade, 46 (2), 38‒52.

La Porta, R., Lopez-de-Silanes, F., & Shleifer, A. (1999). Corporate ownership around the

world. Journal of Finance, 54 (2), 471‒517.