l-' \JI EF-T .E;: 6S= o :- * 3..S *r''*Sl +j s 1.E- FF- ;s i'. E s EF iü e.X ¡J :o6¡ -e F9 ¡s <6 ii o <5aS - ? si¡ Eg :.E -wóx= xg S* 6 *E < *i e ;.F o =^ 6s U S. R. \ G s \ rJ a 1-- R. ñ ft\ \>\ ; s\ G o \ s í*lÉli$ril*ÉlÉiEii gÉgllglIiÉlíaíÉlig glÉilIgÉíggíÉErggg - I tr , P N : i] o = S s@ - H ó < tFf+€5i*írí3*igFF# #H f f g 1s 3F n';+alo -j - 3=?8.-¡;: 6= H -El5o.djÉ I= ñ EFe*i== 7A F E*qEd;K *ij I =S.gábgñ. {rn ; =*ñ- a?ir= ¿i< 2 teá€;ñg á,t ñ iñ P: F? *- ¡r/'\ O Éñá=É_cr= vi; ;r '.+< -.5-.X ¿'' 9ea:E+3 Ée : d51F@É"c ]: É ñ 38"; fs'E é: z Ég:5:*'g s= ü x1d3f ó' iÉ 3 d 9.c 5.Tq,9 i< o ó tFgáaiE 8 : ¡ xa¡; =s 7 i'E'Éa-*E { ? <: c *5 (D O .5: @ !3iÉ.=.q = q ! 6I +; s ó g -'-9I Q-éoq'=- { ^oTI-3 ¡ :;(joieo ,=p=x* x o == Y o N' w á# da: F 5 --"'¡xY- as á9 '5 .i 847;Sr i 996oHo ==^xx< ooñXoi- (,r r FD @¡X 5 s A ---=ooUtt tr) V) =1 ¡r Y( 3Se illt il U) ,i-¡ z) "=( "o 9{ - *i v ililil : "** jjj 8 j j '88 iíggd= - ¿'E¿*, Fl á aÍf se3.> lll ; g 3 *eE E F 55*FáE íi S.++H+ , x 5 ='.3 o :j @ @ @ .i o fá;:?i g 3r s lE ?aFe*¡ ¿ O3$tÜ iHg;Ée $Éii É .! t*iiE;1 gS3: e *rrsiFí íEÉ ; ü EHHi$;' +l.s á e ¡3gÉsa +li g ñsqÉri iEg € E',fr¡Eü0 d? ¡¡ F "sB'[E? r:E á. 9?6e; ; "-' *o ¡ p. c F 1 S ?r*HÉ E á f aC6<Í= eriñ? ;. € + .t aai o I =. *iÉñ* : e =' q o x j6r X - 1^:I-i.i"=' E3¡l'á 8- i -99'fió t o<;írr! o + lt + + \ú + I \ ¡l ¡ ?- + -t ó Tt t + + + ol FI ál l l l l ot .¡ E E F' P g.l É' á s. o 3l o o o I gl r ¡ I d ol o o x r il ; Z á F ñl E g E 6 pl @ o @ Q 2l É D ? =. ;l llH B il @ o t - qi r g * ñ gl E3cs rl m 5 " e ól ^ 6 c r *l +o á i =i 5 = - E él o X *.8' Nl E - r oq *l I F 6 = Ei á 'o d él ^ O +l É- o Ffd NI G <t YI dl X -l :l xt sl EI rl ot

Transcript

l-' \JI

EF

-T

.E;:

6S=

o :-

* 3

..S*r

''*S

l+

j s

1.E

-F

F-

;si'.

E

sE

F iü

e.X

¡J

:o6¡

-e

F9

¡s<

6 ii

o<

5aS

- ?

si¡

Eg

:.E-w

óx=

xg S

*6

*E<

*i

e ;.F

o =

^6s

U S.

R. \ G s \ rJ a 1--

R. ñ ft\ \>\ ; s\ G o \ s

í*lÉ

li$ril

*ÉlÉ

iEii

gÉgl

lglIi

Élía

íÉlig

glÉ

ilIgÉ

íggí

ÉE

rggg

- I

tr

, P

N

:

i] o

=

S

s@

- H

ó

<

tFf+

€5i*

írí3

*igF

F#

#H f

f g 1s

3F

n';+

alo

-j -

3=?8

.-¡;

: 6=

H

-El5

o.dj

É

I=

ñ

EF

e*i=

= 7

A F

E*q

Ed;

K

*ij

I=

S.g

ábgñ

. {r

n ;

=*ñ

- a?

ir=

¿i<

2

teá€

;ñg

á,t

ñiñ

P

: F

? *-

¡r

/'\

OÉ

ñá=

É_c

r=

vi;

;r'.+

<

-.5-

.X

¿''

9ea:

E+

3 É

e :

d51F

@É

"c

]: É

ñ 38

"; fs

'E é

: z

Ég:

5:*'

g s=

üx1

d3f

ó'

iÉ

3d

9.c

5.T

q,9

i< o

ó

tFgá

aiE

8

:¡ xa

¡; =

s 7

i'E'É

a-*E

{

? <

: c

*5(D

O

.5:

@!3

iÉ.=

.q

=q

! 6I

+;

só

g -'-

9IQ

-éoq

'=-

{

^oT

I-3

¡:;(

joie

o,=

p=x*

x

o =

=

Y

o N

' w

á# d

a: F

5

--"'¡

xY-

as

á9

'5

.i84

7;S

r i

996o

Ho

==

^xx<

ooñX

oi-

(,r

r F

D @

¡X 5

s

A--

-=oo

Utt

tr)

V)

=1

¡r Y

(3S

eill

t il

U)

,i-¡

z)"=

( "o

9{

- *iv

ililil : "*

*jjj 8

j j

'88

iíggd

= -

¿'E

¿*,

Fl á

aÍf

se3.

> ll

l ;

g 3

*eE

E F

55*F

áE

íi S

.++

H+

, x

5 =

'.3

o :j

@ @

@ .

i o

fá;:?

i g 3

r s

lE?a

Fe*

¡ ¿

O

3$tÜ

iHg;

Ée $É

ii É

.!t*

iiE;1

gS

3:

e

*rrs

iFí í

EÉ

; ü

EH

Hi$

;' +

l.s á

e¡3

gÉsa

+li

g

ñsqÉ

ri iE

g €

E',f

r¡E

ü0

d? ¡

¡ F

"sB

'[E?

r:E

á.

9?6e

; ;

"-'

*o

¡ p.

c

F 1

S

?r*H

É E

á f

aC6<

Í=er

iñ?

;. €

+.t

aai

o I

=.

*iÉ

ñ*

: e

='

q o

x j6

r X

-

1^:I-

i.i"=

'E

3¡l'á

8-

i

-99'

fió

to<

;írr!

o

+ lt

+ + \ú + I \

¡l ¡

?-

+-t

ó

Tt

t +

+ +

ol FI ál

l l

l l

ot.¡

E

E

F

' P

g.l

É' á

s.

o3l

o

o o

Igl

r

¡ I

dol

o

o x

ril

; Z

á F

ñl

E g

E 6

pl

@ o

@

Q2l

É

D

?

=.

;l llH

B

il @

o

t -

qi r

g *

ñgl

E3c

srl

m

5 "

eól

^

6 c

r*l

+

o á

i=

i 5

=

- E

él

o X

*.8

'N

l E

-

r oq

*l

I F

6

=E

i á

'o d

él

^ O

+l

É-

oF

fdN

I G

<t

YI

dl

X

-l :l xt sl EI rl ot

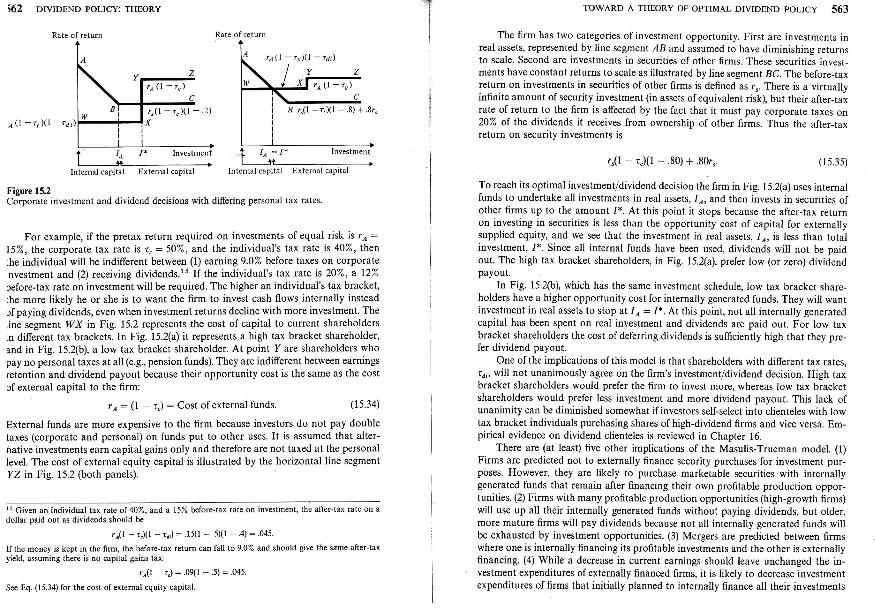

546 DTvTDEND PoLIcY: THEoRY

If the numerator and denominator of (15.1) are multiplied by the current number of

shares outstanding, ndr), then by rearranging terms, we have

Div,(¿+1)+nl¿)Pf¿+1) (rs.2)vt(t): l+p(¿+1)

where

Div,(t + 1) = total dollar dividend payment : nl|divl¿ + 1)'

l4(¡) : the market value of the firm : n¡(t)Pt(t).

Hence the value of the firm is seen to be equal to the discounted sum of two cash

flows: any dividends paid out, Div,(l * 1), and the end-of-period value of the firm'

To show that the present value of the firm is independent of dividend payout, we

shall examine the sources and uses of funds for the two firms in order to rewrite

(15.2) in a way that is independent of dividends.

2. Sources and Uses of Funds

There are two majoJ sources of funds for an all-equity firm. First, it receives

cash from operations, ÑdÍ¡r + 1). Second, it may choose to issue new shares,

m,(t + \F,( + l¡, *h"tt mt(t + l) is the number of new shares' There are also two

.uior utti of funds: dividends paid out, bivt(r + 1), and planned cash outlays for

inv;stment, I-r(¡ + l).2 By definition, sources and uses must be equal' Therefore we

*n,i, nrf¡Ánt assuntes, for thc sake of convenience, tl¡at sources and uses of funds from balance sheet

THE IRRELEVANCE OF DIVIDEND POLICY IN A WORLD WITHOUT TAXES 541

wherc V,1t + l): n.(¡ + l)Fr(r * 1). Therefore the valuation equation (15.2) may berewritten

(15.8)

3. V¡luation and the Irrelevancy of Dividend Payout

It is no accident that dividends do not appear in the valuation equation (15.g).Given that there are no taxes, the firm can choose any dividend policy whatsoeverwithout affecting the stream of cash flows ¡eceived by shareholders. It could, e.g., electto pay dividends in excess of cash flows from operations and still be able to unáertakeany planned investment. The extra funds needed are supplied by issuing new equity.on the other hand, it could decide to pay dividends less than the amount of cashleft over from operations after making investments. The excess cash would be usedto repurchase shares. It is the availability of external financing in a world withoutinformation asymmetry or transactions costs that makes the value of the firm inde-pendent of dividend policy.

we can use Eq. (15.8) to prove that two firms that are identical in every respectexcept for their current dividend payout must have the same value. The equation hasfour terms. First, the market+equired rate of return, p, must be the same because bothfirms have identical risk, ÑdÍr14 : ÑdÍrp¡, for all ¿. Second, currenr cash flows fromoperations and current investment outlays for the two firms have been assumed to beidentical:

ño*r,1r¡ : ñdr,1r¡, i¡r¡: i,1t¡.Finally, the end-of-period values of the two firms depend only on future investments,dividends, and cash flows from operations, which also have been assumed to beidentical. Therefore the end-of-period values of the two firms must be the same:

t,,o¡: 7,tt¡consequently, the present values of the two firms must be identical regardless of theircurrent dividend.payout. Dividend policy is irrelevant because it has no effect onshareholde¡s' wealth in a world without taxes, information asymmetry, or transac-tions costs.

Note that the proof of the irrelevancy of dividend policy was made using a multi_period model whose returns were unce¡tain. Therefore it is an extremely genéral argu-ment. In addition to providing insight into what does not affect the value of the fiim,it provides conside¡able insight into whaf does affect value. The value of the firmdepends only on the distribution of future cash flows provided by investment deci-sions. The key to the Miller-Modigliani argument is that investment decisions a¡ecompletely independent of dividend policy. The fi¡m can pay any level ofdividends itwishes without affecting investment decisions. If dividends plus desired investmentoutlays use more cash flow than is provided from operations, the firm should seekextefnal financing (e.g., equitv). The desire rn nreintoi- q la',-l ^r a:-.:)-'- )-

548 DIVIDEND POLICY: TI{EORY

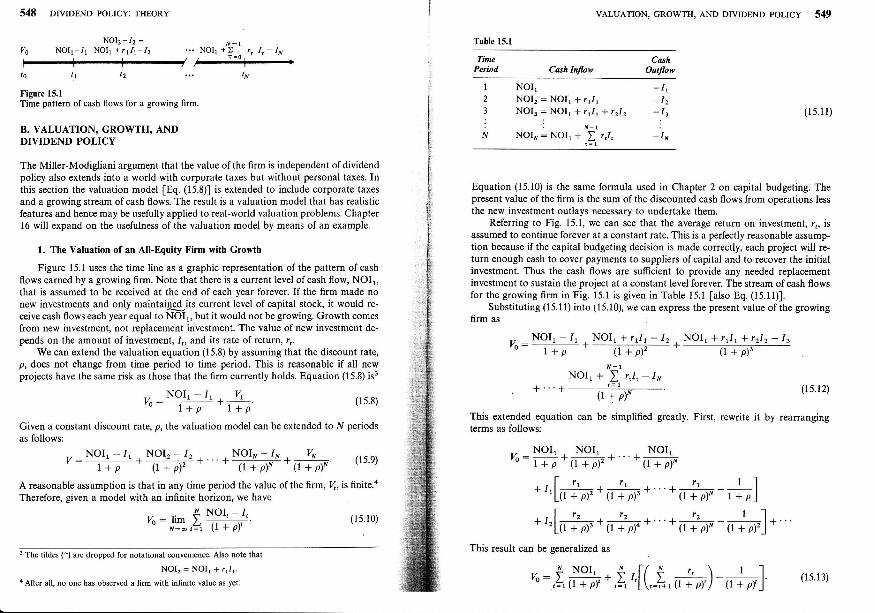

NOlz- 12 =NOIl-/1 NOll +r¡Iy-12 X-l...

.NOtr + !_o

.\ 4 - IN

NOL - r. v.l/ t'u l+p l+p

g NoI. - I,h:JT,!, 0+py

VALUATION, GROWTH, AND DIVIDEND POLICY 549

CuhOutfo,

Table 15.1Vs

Figure l5.lTime pattern ofcash flows for a growing firm.

B. VALUATION, GROWTH, ANDDIYIDEND POLICY

The Mille¡-Modigliani argument that the value of the firm is independent of dividendpolicy also extends into a world with corporate taxes but without personal taxes. Inthis section the valuation model [Eq. (15.8)] is extended to include corporate taxesand a growing stream ofcash flows. The result is a valuation model that has realisticfeatures and hence may be usefully applied to real-world valuation problems. Chapter16 will expand on the usefulness ofthe valuation model by means ofan example.

1. The Valuation of an All-Equity Firm with Growth

Figure 15.1 uses the time line as a graphic representation of the pattern of cashflows earned by a growing firm. Note that there is a current level of cash flow, NOI',that is assumed to be received at the end of each year forever. If the firm made nonew investments and only maintai4ed its cu¡rent level of capital stock, it would re-ceive cash flows each yearequal to Ñdlr, but it t"ould not be growing. Growth comesfrom new investment, not replacement investment- The value of new investment de-pends on the amount of investment, 1,, and its rate of return, r,.

We can extend the valuation equation (15.8) by assuming that the discount rate,p, does not change from time period to time period. This is reasonable if all newprojects have the same risk as those that the firm currently holds. Equation (15.8) is3

TimePqiod Crch Inflowtl

1

2

3

:

N

(15.1 1)

Equation (15.10) is the same formula used in Chapter 2 on capital budgeting. Thepresent value of the firm is the sum of the discounted cash flows from operations lessthe new investment outlays necessary to undertake them.

Referring to Fig. 15.1, we can see that the average return on investment, r,, isassumed to continue foreve¡ at a constant rate. This is a perfectly reasonable assump-tion because if the capital budgeting decision is made correctly, each project will re-turn enough cash to cover payments to suppliers ofcapital and to recover the initialinvestment. Thus the cash flows are sufficient to provide any needed replacementinvestment to sustain the project at a constant level forever. The stream of cash flowsfor the growing firm in Fig. 15.1 is given in Table l5.l falso Eq. (15.11)].

Substituting (15.11) into (15.10), we can express the present value ofthe growingfirm as

NOIrNOI, = NgJt .r rt¡tNOI.:¡6¡, +rJr+rzl2

. N- 1

NOI':¡¡91r + | r,l,.= I

-Ir-12-13

-;,

Given a constant discount rate, p, the valuation model can be extended to N periodsas follows:

n:*:'i;".T?#* *ffrl +- -!L ¡5e)

A reasonable assumption is that in any time period the value of the firm, 4, is finite.4Therefore, given a model with an infinite horizon, we have

.r,[u+tF + t+fr+ +(r+;F-#t].This result can be generalized as

(rs.t2)

3 The tild€s (-) are dropped for notational convenienc. Also noto thal

NOIr=N9¡,*"t¡t.4 After all, no one has obse¡ved a fim with infinite value as yet,

(1s.10)

n :,i #h.,i .[(,á, d;) - #r] (15.13)

550 DTVIDEND PoLIcY: THEoRY

We can simplify Eq. (15.13) by recognizing that the-first term is an

with constant payments of NOI, per period' Therefore

.. A NOIr NOI1

;'*,=¿, (1Trl p '

Next, the second term in (15.13) can be simplified as follows:

grrln-trl

.!*'tt * pr: I +e ,4,1+ ü'

infinite annuitY

(1s.14)

(15.1s)

1'-r,lrt(1+pl,l*6;7: $ +dn

Substituting (15.14) and (15.15) back into (15'13), we obtain a simplified expression

lor the present value of the firm:

.. [NoI,, $ ,f/ ', \- t ,l]%:'l'*t o *,=¿,"l\pd+py)- t + il )J. NOI, S l,(r,- Pl .t)-p ',?1 p$+Pl"

: Value of assets in place + value offuture growth' (15'16)

2. Why Darnings per Share Growth Maximization

Is an InaPProPriate Goal

This form of valuation equation provides important insights into the- m^uch

uuur.J ir.* growth stock.The first terÁ in Eq' (15'16) is the present value of a firm

that makes n-o new investments. It is the presént value of an infinite stream of con-

stant cash flows. In other words it is the value of a firm that is not growing' It is

itt" nulu" of assets in place. But what about the fi¡m that makes new investments?

iL prc*r, value of new investment is shown in the second term of Eq' (15'16)' It

i, if,, pr"t"nt value of expected future growth' The tal.ue-of rrew investment depends

on two things: (1) the amount of investáent made and (2) the difference between the

u*.ug. ,ut""of'ráturn on the investment, r', and the market-required rate of return'

p. TltJ uss"t, of a firm may grow, but they do not add anything to value-unless they

earn a rate of return greatei than what tÍre market requires for assets of equivalent

;irk. F"; example, srftposing that the market requires a l0% rate of return (i'e''

p : l}%),.onrid". the ihree situations given in Table 15'2'

Firm 3 has the greatest "growth" ii earnings (ANOI : 5'000)' But which firm

has the greatest incráse in val-ue? Obviously, firm 1 does' The reason is that it is the

lnlynrti that has new investments that eam more than the required market rate.of

..ii.r "f 10%. Therefo¡e the objective of a firm should ¡¡¿u¿r be to simply maximize

gr"*ii it *-ings or cash flows' The objective should be to maximize the market

VALUATION, GROWTH, AND DIVIDEND POLICY 55

Table 15.2

Firm 1 10,000

Firm 2 30,000

Firm 3 100,000

9,090o

-45,454

Another feature of Eq. (15.16) is that it is derived directly from Eq. (15.g), andin both we have the result that dividend policy is irrelevant in a world without taxes,information asymmetry, o¡ transactions costs. All that counts is cash flows frominvestment.

3. The Value of an All-Equity Firm that Growsat a Constant Rate Forever

Equation (15.16) is elegant but somewhat cumbersome to use.s It has two usefulvariations. The first, which is developed below, assumes that the firm experiences aconstant rate of growth forever. we shall call it the infinite constant growth moilel.The second, developed later on, assumes that the firm can maintain a supernormalrate of growth (where r, > p) for a finite period of time, T, and realizes a no¡malrate of growth thereafter. It is called the finite supernormal growth mod.el.

The constant growth model can be derived from Eq. (15.16) if we assume that aconstant fraction, K, of earnings is retained for investment and the average rate ofreturn, r,, on all projects is the same. The fraction of earnings to be retained forinvestment is usually called the retention ratio; however, there is no reason to restrictit to be less than 100% of cash flows from operations. Rather than calling K theretention rate, we shall call ittlte inuestment rate. As was mentioned in the first sec-tion of this chapter, the firm can invest more than cash flow from operations if itprovides for the funds by issuing new equity. If investment is a constant proportionof cash flows, we have

1,: K(NOIJ. (15.17)

And if the rate of return on investment, r,, is the same for every project, then

NOI':NOI'-'+rI'-t: NOI¡_r * TKNOI,_,

: NOI,-r(1 + rK).

By successive substitution, we have

NOI,: ¡9J,11 + rK)'-l (15.18)

5 However, do not unde¡estimate the usefulness of Eq. (15.16). It is the basis for most commonly u;valuation models. ep AIaaD 'l;^L ¡- ^ ----- I

$A t//of

20 2,000

10 3,000

5 5.000

552 DTVTDEND PoLrcY: THEoRY

Note that rK is the same as the rate of growth, g, for cash flows. In other words, NOIin the tth time period is the future value of NOI in the first time period, assumingthat cash flows grow at a constant rate, g:

NOI':N6¡t11 *'Y-t'By substituting (15.17) into (15.16) and maintaining the assumption that r, = ¡, 1rys

have

VALUATION, GROWTH, AND DIVIDEND POLICY 553

Given these facts and the necessary condition that g < p, the infinite growth model,Eq. (15.21), can be rewritten as

,, Div,p-g

/o:NOIt *; KNot'(r -P).Q ' ,?t p(l + p)'

Then by using (15.18) in (15.19) we obtain

n":y*,.,*o,,(ry, ),i(f,#-Y['.+#,i("iÍ)']

lf rK < p, then the last term in (15.20) will have a finite limit:6

;'*,ü(*+)':=t* iff p>rK

y_NoIrfr_K(r-p) l+Krlp l'' t+Kr p-rKf

_ Norl(l - K).p-Kr

Substituting (15.20a) into (15.20) and simplifying, we have an equation for the valueof the firm, assuming infinite growth at a rate less than the market rate of return, p:

(ls.21a)

which is the Gordon growth model.

4, Independence between Investment Plans andDividend Payout

This form of the valuation model can be usod to illustrate the relátionship be-tween the result that the value ofthe firm is independent ofdividend policy and theassumption that investment decisions should never be affected by dividend payout.A commonly made error is to impücitly assume that there is some relationshipbetween the amount of cash flow retained and the amount of investment the firmunde¡takes. Suppose we take the partial derivative of Eq. (15.21) with respect tochanges in the investment rate, K:

)Vo NOI,(r - p)

ax: -¡o - ,*y ' u'

This suggests that if the rate of return on investments, r, is greater than the market-required rate of return, p, the value of the firm will increase as more cash flow isretained, and presumably the increased amount of retained cash flow implies lowerdividend payout. This line of reasoning is incorrect for two reasons. First, the amountof cash flow retained has nothing to do with dividend payout. As was shown in thesources and uses offunds, identity (15.3), the firm can arbitrarily set dividend payoutat any level whatsoever, and if the sum of funds used for dividends and investmentis greater than cash flows from operations, the firm will issue new equity. Second,the investment decision that maximizes sha¡eholder wealth depends only on themarket-required rate of return. The amount of cash flow retained could exceed theamorjnt ofinvestment, which would imply that shares would be repurchased. There-fore there is no reiatiooship between the value of the firm and either dividend payoutor cash flow retention.

5. The Bird-in-Hand Fallacy

A more sophisticated argument for a relationship between the value of the firmand dividend payout is that although the dividend decision cannot change thepresent value of cash payments to shareholders, it can affect the temporal patternof payouts. Suppose that investors view distant dividend payments as riskier thancurrent payments, might they not prefer a bird in the hand to two in the bush? Wecan represent this argument mathematically by assuming that higher investmentrates mean lower current dividend payout, more risk, and therefore an increase inthe market rate of return, p, as a function of the investment rate, K. A simple examplewould be to specify the relationship as

(15.1e)

(1s.20)

(15.20a)

( 1 5.21)

Equation (15.21), rewritten in a somewhat different form, is frequently referredto as the Gordon growth model. Nofe that since K is the investment rate (althoughK need not be less than one), the numerator of(15.21) is the same as dividends paidat the end of the first time period:

NOIl(l-K) :Divr.Also, as was shown earlier, the product of the investment rate and the average rate

of return on investment is the same as the growth :c:te, g, in cash flows; therefore

Kr: Q.

s:u+u2+...+Yn.Multiplying this by U and subtracting ihe resuit from the above, we have

s=ul0-q-uN+Ll0-u).The second tem approaches zero in the limit as N approaches infinity. By substituting brck the deflnitionof U, we get (15.20h). p:d+8K2, p>0.

NOI'ffK2 -2PK+ r-a):Q.To see the error in this line of reasoning, we need only to return to our understandingof vah¡ation under uncertainty. The risk of the firm is determined by the riskinessof the bash flows from its projects. An increase in dividend payout today will resultin an equivalent drop in the ex-dividend price of the stock. It will not increase thevalue of the firm by reducing the riskiness of future cash flows.

6. Finite Supernormal Growth Model for anAlFEquity Firm

Perhaps the most useful variation of the valuation equation is one that assumes

that the rate of return on investment is greater than the market-required rate ofreturn for a finite number of years, T, and from then on is equal to the market-required rate of return. In other words the firm experiences supernormal growthfor a short period of time, then settles down and grows at a rate that is equal tothe rate of growth in the economy. Obviously a firm cannot grow faster than theeconomy forever or it would soon be larger than the economy.

To derive the finite growth model we start with Eq. (15.20). Note that the sum-mation is no longer infinite:

(15.20)

Instead, growth lasts for only I years. After year ?, we assume that r: p, whichmeans that the second term adds nothing to the present value of the firm. Whenevera firm is earning a rate of return just equal to its cost of capital, the net presentvalue of investment is zero. The summation term in Eq. (15.20) can be evaluatedas follows. Let

u: [(1 + rK)10 + df.We can then expand the sum:

S:U+U2+"'+Ur.Multiplying thiq by U and subtracting the result, we have

S - US: U - (Jr*1.

Solving for S and substituting back for U, we obtain

[(1 + KrXl + p)] - [(1 + Kr)/(l + p)]rrl

n,:Y['.H,\ (l.Tf)]

. IJ -TJT+I1-U

IF

II

I

Éii

VALUATIoN, GRowTH, AND DIVIDEND PoLIcY 555

Substituting (15.21b) into (15.20) yields

',, : N;I'

{, . #1, _ (+f)J} (ts.22)

As long as Kr is approximately equal to p, and T is small, we can approximate thelast term as?

(+f,)'-1-r(--!!)By substituting the approximation (15.23) into the varuation equation (r5.22), we havean approximate valuation fo¡mula for finite supernormal g.o*th,t

/o: NOI' * K(" =l)r14-lr'\

Not'p p_Kr'\t+p) p

- NoIr * *t¡6¡'¡7[-r:-P 1'p ' Lp1+dl

?_The ¡inomial expansion en be used- to a"tu" th(1 + p; : 1 + A. Then, recalling that Kr = c, we haye

ffi':,' *ar:i ([)or-.a"

:r+? *i,(f)o"'t*ro

A:l+Kt- l=K'-P.

Therebrethecor¡e"tapproximation,r t *o 1 * p

1+rA= r-r(o-:":\.\t+P)

::l::lT_r11,-1P-"jl]igitl 1l:he app¡oximarion, asume that the investmcnl rate, K, is 50%, rhe rate ofrerum on rnyestmcnt' r' is 202. and.the_market-required rare of ¡etu¡n is tsz. Éigir" rs.Á'i, "

piái "il(l + Ktll{.l + p)1. We can see visually that t¡" rinüi up-pñ,i"iüilr.*"onu¡r".

(ff¡'' o

0.9

('#)' ,

(1s.23)

(ls.24)

Solving for A, we have

.9565

.9t49

.8',152

.83'71

.8007

I2345

7. Finite Supernormal Growth Model for a Firmwith Debt ¡nd Taxes

Up to this point, we have maintained the assumption that we are dealing withan all-equity firm in a world without taxes. To extend the above valuation equationinto a world where firms have debt as well as equity and where there are corporate

taxes, we can rely on the results obtained in Chapter 13. The value of a levered firmwith finite supernormal growth can be written as follows:

WACC : weighted average cost of capital : pll - c"B/(B + S)],

B : market value of debt,

K : investment rate,

T : the number of years that r > WACC,

r : the average rate ofreturn on investment,

p : the cost ofequity capital for an all-equity firm.

The first two terms in (15.25) are the value of a levered firm with no growth, i.e., the'?alue of assets in place. They are the same as Eq. (13.3), the Modigliani-Miller result

that assumes that firms pay corporate taxes but are not growing. The third term inEq. (15.25) is the value ofgrowth for the levered firm. It depends on the amount ofinvestment, /, : K(NOIJ, the difference between the expected average rate of returnon investment and the weighted average cost of capital, r - WACC, and the length oftime, T, that the new investment is expected to earn more than the weighted average

cost of capital.Equation (15.25) is used in Chapter 16 as the basis fo¡ the valuation ofBethlehem

Steel. Note, however, that even in this model (which is the most realistic of those

developed so far in this chapter) dividend payout is not relevant for determining the

value of the ñrm.

C. DIVIDEND POLICY IN A WORLD WITHPERSONAL AND CORPORATE TAXES

Up to this point the models of firms that have been introduced assume a world with

only corporate taxes. What happens when personal taxes are considered? In partic-

ular, how is dividend policy affected by the important fact that in the United States

the capital gains tax is less than the personal income tax?e An answer to this question

e The 1986 tax code nominally makes the capital gains rafe equal to the ordinary income rate. However,

capital gains taxos are still lcs than ordinary taxes in effect, because capital gains can be deferred in-

definitely, whereas taxes on ordinary income cannot.

is provided by Farrar and Selwyn [1967] and extended into a market equilibrium

framework bY Brennan [1970]'roFarrar and Selwyn use partial equilibrium analysis and assume that individuals

attempt to maximize their after-tax income. Sha¡eholders have two choices. They can

own shares in an all-equity firm and borrow in order to provide personal leverage,

or they can buy shares in a levered firm. Therefore the first choice is the amount ofpersonal versus corporate leverage that is desired. The second choice is the form ofpaym"nt to be made by the firm. It can pay out earnings as dividends, or it can retain

éarnings and allow shareholders to take their income in the form of capital gains.

Shareholders must choose whether they want dividends or capital gains.

If the firm pays out all its cash flows as dividends, the ith shareholder will receive

the following after-tax income, if:ií : ttÑo"r - rD)(r - t") - rD,¡l(r - t ), (15.26)

where

i! : the uncertain income to the ith individual if corporate income is receivedas dividends,

ÑO*I : ttre uncertain cash flows from operations provided by the firm,

r: the borrowing rate, which is assumed to be equal for individuals and firms,

D" : corporate debt,

De¡: personal debt held by the lth individual,

r" = the corporate tax rate,

rri : lbe personal income tax rate of the ith individual.

The first term within the brackets is the after-tax cash flow of the firm, which is

fidÍ - rD)(l - z"). All of this is assumed to be paid out as dividends. The before-tax

income to the shareholder is the dividends received minus the interest on debt used

to buy shares. After subtracting income taxes on this income, we are left with Eq.(ts.26).

Alternatively, the firm can decide to pay no dividends, in which cas€ we assume

that all gains are realized immediately by investors and taxed at the capital gains

rate.rr In this event the after-tax income of a shareholder is

i1 -_ tne uncertain income to the ith individual if corporate income is received as

capital gains,

?ri: the capital gains rate for the ith individual.

r0 More recently Miller and Scholes [1978] have also considered a world with dividends and taxes. Theimplications of this paper are discussed later on in this chapter.rr Obviously there is the third possibility that earnings ¿re translated into capital gains and the capitalgains taxes are defer¡ed to a lat€r date. This possibility is considered in Farrar and Selwyn [1967]; it doesnot change their conclusions.

Now the individual pays a capital gains tax rate on the income from the firm andleducts after-tax interest expenses on personal debt. The corporation can implement.he policy of translating cash flows into capital gains by simply repurchasing its¡hares in the open market.

irom Eqs. (15.26) and (15.28) the advantage to investors of receiving returns in thebrm of capital gains rather than dividends should be obvious. So long as the tax'ate on capital gáins is less than the personal tax rate (rn¡ < toi), individuals will pre-br capital gains to dividends for any positive operating cash flows, rate of interest,md level of debt (personal or corporate). The ratio of the two income streams,

s greater than one if tr¡ 1 xpi. In general the best form of payment is the one thats subject to least taxation. The implication, of course, is that corporations shouldrever pay dividends. Ifpayments are to be made to shareholders, they should alwaysre made via share repurchase. This allows shareholders to avoid paying income tax'ates on dividends. Instead, they receive their payments in the form of capital gainshat are taxed at a lower rate.

What about debt policy? Again the same principle holds. The debt should beteld by the party who can obtain the greatest tax shield from the deductible interest)ayments. This is the party with the greatest marginal tax rate. If the firm pays out¡ll its cash flow in the form of dividends, the favorable tax treatment of capital gainss irrelevant. In this case we have the familiar Modigliani-Miller [1963] ¡esult thathe value of the firm is maximized by taking on the maximum amount of debt (see

Jhapter 13). Proof is obtained by taking the partial derivative of Eq. (15.26) with'espect to personal and corporate debt and comparing the results.

Debt policy becomes more complex when the corporation repurchases shares in-rtead of paying dividends. Taking'the partial derivatives of the capital gains income:quation, (15.27), we obtain

further. He shows that if the borrowing rate on debt is "grossed up" so that theafter-tax rate on debt equals the after-tax rate on other.sources ofcapital, the marginalinvestor will be indifferent between personal and corporate debt.12

Empirical evidence about the existence of debt clienteles is discussed in Chapter1ó. Some clientele efects are obvious. For example, high tax bracket individuals holdtax-free municipal bonds, whereas low tax bracket investors like pension funds (whichpay no taxes) prefer to invest in taxable corporate bonds. A much more subtle ques-tion, however, is whether investors discriminate among various corporate debt issues,

i.e., do high tax bracket investors choose lowleverage firms?Brennan [1970] extends the wo¡k ofFarrar and Selwyn into a general equilibrium

framework where investors are assumed to maximize their expected utility of wealth.Although this framework is more robust, Brennan's conclusions are not much differ-ent from those of Farrar and Selwyn. With regard to dividend payout Brennan con-cludes that "for a given level of risk, investors require a higher total return on asecurity the higher its prospective dividend yield is, because of the higher rate of taxlevied on dividends than on capital gains." As we shall see in the next chapter, thisstatement has empirical implications for the CAPM. It suggests that dividend payoutshould be included as a second factor to explain the equilibrium rate of return onsecurities. If true, the empirical CAPM would become

div¡,fP¡, : the dividend yield of the jth security,

drr : a random erro¡ term,

R¡, : the risk-free rate.

If the dividend yield factor turns out to be statistically significant, then we might con-clude that dividend policy is not irrelevant. Direct empirical tests of the relationshipbetween dividend yield and share value are discussed in Chapter 16.

A paper by Miller and Scholes [1978] shows that even if the tax on ordinarypersonal income is gre¿ter than the capital gains tax, many individuals need not paymore than the capital gains rate on dividends. The implication is that individualswill be indifferent between payments in the form of dividends or capital gains (if thefirm.decides to repurchase shares). Thus the firm's value may be unrelated to its divi-dend policy even in a world with personal and corporate taxes.

r'

I

E,

*ÉF*{i

rf

$g.

.F,

rl

#1l

trtfL

fll

f

Corporate debt: #: -,nt - t")(I - t),

Personal debt: o*: -,r(t - ri.dD pi

(15.30)

(1s.3 1)

.ftheeffective tax rate on capital gains is zero (as Miller [1977] suggests), then per-;onal debt will be preferred to corporate debt by those individuals who are in marlinalax b¡ackets higher than the marginal tax bracket of the ñrm. This result allows thercssibility of clientele effects where low-income investors prefer corporate debt andrigh-income investors prefer personal debt. Miller [1977] takes this argument even 12 The reader is referred to Chapter 13 for a complete discussion of this point.

a o

5N ó^.q = -

xili

e:

¡ H

3I

6 oi

to=

l¿t l^

,lY

ar

F

ulO

É

16ú

lú

616ó

tñ

6t6

ólr

{l{O

t:. 18

ztll

o o

tó

É

FI

{5ló lá

AIN

É

Hlu

6

b\l"o

i^6t

o d

{lO

!

i>-N

t 4

oE

e!4

| ts

= i

éxI

d :.8

!2;

I B

ó-a

oPI

* ó3

lil l^

5r-

I V

F

l-6.j-

-6

t; É

t6

ólÉ

. 31

38 8

t; lr. l¿

3_F

5|

* 59

F

I {

6;

=I

3d&

I A

IN

HI

.519

.j_

-o

I -lu

o

66t

o o

d!to

ó

* E

Bíi_

gí s

¡ ¡,

--,-

sT;:

- É

$#áq

EgE

ái3

sp

i iÉ3É

ElF

É$g

rEiE

[$lE

g E

E E

[EíE

ÉÉ

á1tE

EF

g lg

á[.:t

;=:ix

rr;

i:E

I

É=

l F

E

[* *f

fiág

c il'

Éi 1

t [3

g+lt3

€'á

*ÉE

if fá

iE rE

íi fiÉ

t i u[

É$[

f+sg

Er,

i rÉ

iifiÉ

*iÉ

f ;ái

3a$

;€ iá

Éift

É$i

E€

¿ ti

'si€

;3iE

3

er +

s;r á

i lH

ilET

*.*

'-lñ[

Éi*

Hi E

'' o

ó-¡;

; o

á E

Ff

H á

tÉF

g 3F

IgÉ

irgÉ

iá'$

iHÉ

rlÉiÉ

ÉéF

EÉ

iiiE

r'!

E-<

d

g :.

Va

F

* r;

sg

E

o. 1

;F

dÉ

EF

ái

t=sE

di¡8

" sg

Ei á

r i

+::

íÉE

i li*

gei$

iÉ1

+{s

itÉiF

¡is

5 i$

$*:F

F*€

r+

;ñiF

Eé'

Er:

r ttF

É;g

.¡;;e

sF¡ia

É;*

Fi;g

9És;

Elir

F;

o o € 6 o A A A a o d

giF

ígíÉ

íggí

árilÉ

lgíg

ÉiF

i$eE

ÉgÉ

iF3E

tfgF

$É

s>l

.:FI rl EI

El ;t cl ;t al al *l sl ;t 3l ;l 1l rl *l nl el =t

-ol

al Fl

ql ¡l 8t +t

#t

oo ¡ b F s V) s

o l. ¡- q

z ló

3 85

.f

-.o

i is

p id

x)¿

da

ooE

Éó

B

e8o

€<50

0á

;o

6"E

l'E -l"

g"g

la hE gd oó d6 -

N

E5 D h il

lN

N

olo

o

s € * = V) s

6írid

!i''li

i+r

; :.r

¡a;i:

iFfii

ÉóR

I I

ql

o\ ¡'¿ U

v= -ñ

o .l ñ o

o

ár*

=l :t el Fb¡ -l il '

:l €t?

al

o*l

i +z

ñggX

g *a

Eái

FS

á$;ir

s ?É

EÍfE

ÉÉ

iEÉ

i:EÉ

iÉig

áEI

íq3i

I =

#X:E

Er"

*:;:=

á; I

'53N

*3

a E

üaT

;9iá

d.S

+

É

Eii

:E3

r f€

.3?É

FE

*3gl

:g :

A;€

.9! l,

+ۃ

ü5;t'

EE

F*É

?eE

[eE

: iá

6;#y

saiE

!;g

g

;ci;.

gE

É;É

3É;tE

ig t

ci9a

l E

xlB

tÉf;ñ

.3gt

s E

:

*i-*

* á

ii3:á

Et€

o'$'

\I 3

:-eE

p ?

gF4_

d*[5

'fr=

3HE

=

=á:

5 e.

s6É

.E:É

1i+

ñóE

- +

i3so

oe

H-$

Ea;

l#l!.

fg

*tti

g H

?$r

r3ü;

Etr

r= ñ

€r;r

I

F.E

EÉ

li:üs

l$ ;

qEtñ

* ñi

r;=

+r:

:q*s

Eó=

=.9

;.9

"!oP

=|io

o-'¿

DiE

il iE

Hse

E*t

X19

s s

iS¡i

H$i

teia

is¡x

a a

rE;E

ü q ifí

3gl H

; -+

BH

P:

_ +

sg+

fE.¡

Sté

-xo.

aiii

s á;

átr#

iFsE

ai

b<=

q-3

E;

C;

H

*ñ

É:1

'i5'

t=

:ábÓ

D

J

s^

cóH

=

:. 9=

@

h 4^

l' +

r u?

- qg

a+

o -=

5D

^ ó'

d-

x -e

óa

g o

o óx

E'

?F 'L

á1

3 q!

o

I *¡

s '

i.F ¡

S

ño

L ;F

=

F

É

-:

* D

c ,

od=

l

x.l.

' A

<

d 'P

-d

üild

ilov

=¿

-X

i l4

q $

IPIH

q=i^

,1.

il-;

.F ü P

s 6

ñl

35e

=o3 *f @

É ;r ñF oo ss 5i eB F6

?o

lg;É

gllÉ

iiÉiíl

Ég+

lgg*

gígs

'gíg

giig

gílíí

gígí

eÉíE

gFE

gígí

ÉF

Frr

ÉE

í íí€

Éi gi

í[iíg

i i[$

Éííí

FE

F

gggr

Éíg

gglg

l¡lrÉ

ííígÉ

Égg

lliiíl

iEiíi

liíííí

ꇃ

e$E

*EgÉ

'=$+

iFF

,$iri

*iui

é*,is

isrÉ

Fig

í;

6

d

-

UI V I'TI TUIIU I: I HbUKY

rather than to make up the shottfall of funds through external financing. (5) Share-holder disagreement over internally financed investment policy will be more likelythe greater the amount ofinternally generated funds relative to the firm's investmentopportunities. In these cases, firms are more likely to experience takeover attempts,proxy fights, and efforts to "go private." Given these tax-induced shareholder con-flicts, diffuse ownership is more likely for externally financed firms than for internallyfinanoed firms.

2. Theories Based on the Informativeness ofDividend Payout

Ross [1977] suggests that implicit in the Miller-Modigliani dividend irrelevancyproposition is the assumption that the market knows the (random) return stream ofthe firm and values this stream to set the value of the firm. What is valued in themarketplace, however,is the perceiu¿d stream of returns for the firm. Putting the issuethis way raises the possibility that changes in the capital structure (or dividend pay-out) may alter the market's perception. In the terminology of Modigliani and Miller,a change in the financial structure (or dividend payout) of the firm alters its perceivedrisk class even though the actual risk class remains unchanged.

Managers, as insiders who have monopolistic access to information about thefirm's expected cash flows, will choose to establish unambiguous signals about thefirm's future if they have the proper incentive to do so. We saw, in Chapter 14, thatchanges in the capital structure of the firm may be used as signals. In particular, Ross

[1977] proved that an increase in the use of debt will represent an unambiguoussignal to the marketplace that the firm's prospects have improved. Empirical evidencese€ms to confirm the theory.

The signaling concept is easily applied to dividend policy as well as to financialstructure. We shall see that a possible benefit of dividends is that they provide valu-able signals. This benefit can be balanced against the costs of paying dividends toestablish a theory of optimal dividend policy.

A firm that increases dividend payout is signaling that it has expected future cashflows that are sufficiently large to meet debt payments and dividend payments with-out increasing the probability of bankruptcy. Therefore we may expect to find em-pirical evidence that shows that the value of the firm inc¡eases because dividends aretaken as signals that the firm is expected to have permanently higher future cashflows. Chapter 1ó reviews the empirical evidence on dividends as signals.

Bhattacharya [1979] develops a model closely related to that of Ross that can beused to explain why firms may pay dividends despite the tax disadvantage of doingso. If investors believe that firms that pay greater dividends per share have highervalues, then an unexpected dividend increase will be taken as a favorable signal. Pre-sumably dividends convey information about the value of the firm that cannot befully communicated by other means such as annual reports, earnings forecasts, orpresentations before security analysts. It is expensive for less successful firms to mimicthe signal because they must incur extra costs associated with raising external funds

TOWARD A THEORY OF OPTIMAL DIVIDEND POLICY 565

in order to pay the cash dividend.l6 Hence the signaling value ofdividends is posi-tive and can be traded ofl against the tax loss associated with dividend income (asopposed to capital gains). Even firms that are closely held would prefer to pay divi-dends because the value induced by the signal is received by current owners onlywhen the dividend message is communicated to outsiders. One of the important im-plications of this signaling argument is that it suggests the possibility of optimal divi-dend policy. The signaling benefits from paying dividends may be traded off againstthe tax disadvantages in order to achieve an optimal payout.

Hakansson [1982] has expanded the understanding ofinformative signaling toshow that in addition to being informative at least one of three sufficient conditionsmust be met. Either investors must have different probability assessments of dividendpayouts, or they must have differing attitudes about how they wish to allocate con-sumption expenditures over time, or the financial markets must be incomplete. Allthree of these effects may operate in a complementary fashion, and all three arereasonable.

Miller and Rock [1985] develop a financial signaling model founded on the con-cept of "net dividends." It is the first theory that explicitly combines dividends andexternal financíng to show that they are merely two sides of the same coin. Theannouncement that "heads is up" also tells us that "tails is down." As was pointedout in the original Miller-Modigliani [1961] article, every firm is subject to a sourcesand uses of funds constraint:

NOI +,nP * AB :1 + Div. (15.36)

Recall that sources of funds are NOI, the firm's net operating income; nP, the pro-ceeds from an issue of external equity (the number of new shares, m, times the priceper share, PI and AB, the proceeds from new debt. Uses of funds are investment, I,and dividends, Div. The sources and uses constraint can be rearranged to have netcash flows from operations on the left-hand side and the firm's "net dividend" on theright-hand side:

NOI-I:Div- A,B-mP. (15.37)

Now imagine a model where time 1 is the present, time 0 is the past, and time 2 isthe future. The present value of the firm, cum dividend, is the value of the currentdividend, Divr, plus the discounted value ofcash flows (discounted at the appropdaterisk-adjusted rate, k):

( 15.38)

16 This suggests that dividend payout and debt level increases are interrelated signals. A firm that simul-taneously pays dividends and borrows nay be giving a diferent signal than if it had made the samedividend payment without borrowing.

4=Divr.ffi

566 DTVTDEND pol-rcy: THEoRy

original shareholders'wealth is the value ofthe firm minus the market value ofdebtand new equity issued:

St : Vt -AB, : ¡¡u, . ffi - LB, - mPr.

Using the sources and uses constraint, Eq. (15.37), we have

sr:Norr-r,*ul\oi,,.

(15.39)

(1s.40)

(1s.41)

Without any information asymmetry, this is just the original Miller-Modigliani prop-osition that dividends are irrelevant. All tlrat counts is the investment decision.

If there is information asymmetry, Eq. (15.40) must be rewritten to show howmarket expectations are formed. If future earnings depend on current investment,then we can write that net operating income is a function of the amount of investmentplus a random error term,

NOI, :/(10) + e,,

NOI, =/(11) + er,

where e , and e, are random error terms with zero mean, i.e., E(er) : E(eJ : 0. Wealso adopt the special assumption that the expectation of e, given e, is not necessarilyzefo'.

E(erlet) : yer.

If 7 is interpreted as a persistence coefficient, 0 < I < l, the market is assumed toonly partially adjust to new information (the first-period error). If we use the notationEo to remind us that the current value of the firm is based on preannoutrcementinformation, then the current expected value of shareholders' wealth is

E(s,¡: ¿o¡¡6¡r) - Eo(I,) - YP:f(to)_rr*H.

The corresponding postannouncement value of the firm is

Sr:NOIr -1, +ffi= f(to) + e, - 11 * N##: f(I¡ + e, - 1, * t!## (ts.42)

TOWARD A THEORY OF OPTIMAL DIVIDEND POLICY 567

Subtracting (15.41) from (15.42) gives the announcement efect

s,-E(sl)=r,[t.#]

: [Norl - EoNor,)][l . #] (15.43)

Equation (15.43) says that the announcement effect on shareholders'wealth will de-

pend on the "earnings surprise." Thus we would expect that unexpected changes inearnings will be correlated with share price changes on the announcement date.

Miller and Rock go on to show that the earnings, dividend, and financing an-

nouncements are closely related. Assuming that the expected and actual investment

decisions are at an optimum level, and are therefore equal, then the difference between

Thus the earnings surprise and the net dividend surprise can convey the same in-formation. The financing announcement efect is merely the dividend announcement

effect, but with the sign reversed. An unexpected increase in dividends will increase

shareholders' wealth, and an unexpected issue of new equity or debt will be inter-preted as bad news about the future prospects of the firm'

The Miller-Rock signaling approach shows that announcement effects (including

earnings surprises, unexpected dividend changes, and unexpected external financing)

emerge naturally as implications of the basic valuation model rather than as ad hoc

appendages.One problem that the above theories have in common is that although they

explain how an optimal dividend policy may arise, none of them can successfully

.*plain c.orr-rectional differences in dividend payouts across firms.l7

3. Agency Costs, External Financing, and

Optimal Dividend Payout

Rozeff [1982] suggests that optimal dividend policy may exist even though we

ignore tax considerations. He suggests that c¡oss-sectional regularities in corporate

dividend payout ratiosrs may be explained by a trade-off betw€en the flotation costs

of raising external capital and the benefit of reduced agency costs when the firm in-

creases its dividend payout. It is not hard to understand that owners prefer to avoid

paying the transactions costs associated with external financing.As discussed earlier (Chapter 14, section B.4), there are agency costs that arise

when owner-managers sell portions of their stockholdings to so-called outside equity

r? A posible exaption is the work of Miller and Rock [1985], which suggsts that the oext theory shows

better promis in this regard.r8 The payout ratio is the tatio of dividends to net income.

568 DTvTDEND por,rcy: THEoRy

owners. The outsiders *t|l,*lrr" e,x ante, for the potential problem that owner_managers may increase their personar weartñ at the ex'pense ofoutsiders by means ofmore perquisites or shirking. To decrease ne ", oni[ "narg", "*"..-n,"i",Tjil,ifind it in their own interest to agree to incu¡ monito¡ing or bonding costs if suchcosts a¡€ less than the ex ante charge that ou,rl¿.rr^*áulA b. f"r;i;;;;;;;:Th-us a wealth-maximizing firm wifl

"¿.pi "" "piirn"i.",m¡nrmrzes agency cosrs. tttonngAol-iile nglicr rhatDividend payments may well se¡ve as a means of moniroringro, uo¡áingii'":aagement performance. Although greater dividenJ puyou, i_pti". costly external fi_nancing, the very fact that the firm mur, eo ,o ih. ;;ü mu.k"t, implies that it willcome under greater scrutiny. For exampri u"rt, *iiirio"r.

" ""r"¡;i;;;ü;; ;i;;creditworrhiness of rhe fir;' r"¿ ,tr. í*"t¡,r'*;l';;h"rg, commission w'r re-quire prospectus filings for new equity irru.r. ffrrs *irlde suppliers of capital helpto monitor the owner-manag"r on tenarrof ou,rt¿..q"¡-,y "*"ers.

of course, auditedfinancial statements are a substitute_means for rupplyi'g the same information, butthey may.not be a perfect substitute for tt. "aau"rJu'.y; .llationship between the firmand suppliers of new capital. --'v¡vq¡r r!¡

Because of the t¡ansactions costs of external financing Rozeff arso argues thatthe variabilitv of a firm's cash_flows rill "Á."il,r'JJiá"nd payout. consider rwofirms with the same averase cash flows across tlrnl Uui á-if.r"nt variability. The firmwith g¡eater voratility *iñ borrow in bad years un;-;üy in good. It wi, need tonnance externarry more often. consequentíy, i, *iii,."'J," have a lower dividendpayout ratio.

Rozetr [19821 selected a sample of 1000 nonregulated firms in 64 different in-dustries and examined their averáge_diuid"nd put;;t-;;;ios during the 1974_1980interval' Five proxy variables were chosen ," téri'rtirii.".y. The results a¡e shownin Table r5'4: The independenr variables cnowi ""á'óRow2 are an artempt tomeasure the effect of costlv external ñnancing. fi..r-tn1t grow faster can reducetheir need ro use exremal fiíancing by payin;l&;;;d.rds. GRoWI measures thegrowth rate in ¡evenues between tglc in¿-tg¡g, rt.;;;; cRow2 is varue Line,sfo¡ecast of the growth of sales revenue over the five-year period 1979-19g4. Bothvariables are negativerv related-to di"id.J p;;;;i';;;.. statistically significanr..The variables INS and STOCK ur. pro*i.ri;;;;lgJn;; relationship. rNS is rhepercenrage of the firm held by insiders. Dividend o^tJ i; negativery related to thepercentage of insiders because given

" l"y:.¡;;;;'g;f,riutsi¿ers there is less needto pay dividends to reduce agency costs.re ó" tt..it", ¡"nd, ifthe distribution ofoutsider holdings is diffuse' rh.o ug.n.y costs will be higher; hence one wourd expectsrocK' the number or.."trtoii..r.'," l" p"rrí".iy"'.'Jt'u,"0 ,o dividend payout.Both INS and STOCK are statistically ,igninJu't uni'oiir,. pr.oi"t.a sign. Finally,the variable BETA measures ttt" ,irLin.r,

-oiiÁ. ñ.* Trtáor"¿iction thar riskier firmshave lower dividend payout is *rin"Juy ir," .";;;:.;;;.t"

tn tntt r"t",tonrntOprcler to rake rheir rerurn in rhe form of

t-statisti6 are shown in parentheses under estimated values of the regression coemcients. R2 is adjusted

for degres of freedom. D.W. is Durbin-Watson statistic.

From M. Rozeff, "Crowth, Beta, and Agency Costs as Deteminants of Dividend Payout Ratios," Jo&rru¡

of Financial Research,Fall 1982,249-259. Reprinted with permission

The best regression in Table 15.4 explains 48% ofthe cross-sectional variabilityin dividend payout across individual firms. Although the results cannot be used to

distinguish among various theories of optimal dividend policy, they are consistent

with Rozeff's predictions. Furthermore, the very existence of strong cross-sectional

regularities suggests that there is an optimal dividend policy.

E. OTHER DTVIDEND POLICY ISSUES

1. Dividends, Shares Repurchase, and Spinoffs

from the Bondholders' Point of View

Debt contracts, particularly when long-term debt is involved, frequently restrict

a firm's ability to pay cash dividends. Such restrictions usually state that (1) future

dividends can be paid only out of earnings generated after the signing of the loan

agreement (i.e., future dividends cannot be paid out of past retained earnings) and

(2) dividends cannot be paid when net working capital (current assets minus current

liabilities) is below a prespecified amount.One need not restrict the argument to only dividend payout. When any of the

assets ofa corporation are paid out to shareholders in any type ofcapital distribution,the effect is to "steal away" a portion ofthe bondholders'collateral. In effect, some

of the assets that bondholders could claim, in the event that shareholders decide to

default, are paid out to shareholders. This diminishes the value ofdebt and increases

the wealth of shareholders.Of course, the most common type of capital dist¡ibution is a dividend payment.

A portion of the firm's assets is paid out in the form of cash dividends to share-

holders. The most extreme example of defrauding bondholders would be to simply

liquidate the assets of the firm and pay out a single, final dividend to shareholders,

-0.526 -26.543(-6.43) (-17.05)

-0.758(-8.28)

-0.603 -25.409(-6.94) (- 15.35)

- 33.506(-21.28)

0.48 1.88

0.33 1.79

0.4r 1.88

0.39 1.80

o.t2 1.60

2.584(7.73\

2.517

,u:,

3.15 1

(8.82)

3.429(7.97)

185.47

t23.23

231.46

218.10

69_33

570 DTVTDEND por.rcy: THEoRy

thereby leaving bondholders with a claim to nothing. For this very reason, most bondindentures explicitly restrict the dividend policy of shareholders. usually dividenáscannot exceed the current earnings of the firm, and they cannot be paid oui ofretaineJearnings.

other types of capital distributions are share repurchase and spinoffs. share re-purchase has exactly the same effect as dividend payment except that the form ofpayment is capital gains instead ofdividend income. The conventional procedure fora spinoff is to take a portion of a firm's assets, often a division relativily un."lat"áto the rest of the firm, and c¡eate an independent firm with these assets. ih. i.npo.-tant fact is that the shares of the new entity are distríbuted solely to the sharehoídersof the parent corporation. Therefore, like dividend payment o. ,hur" repurchase, thismay be used as a technique for taking collateral from bondholders. Émpiricaí evi-dence on the effects ofrepurchases and spinoffs is covered in Chapter 16.

It is an interesting empirical question whether or not any diviáend payment, nomatter how large it is, will affect the ma¡ket value of bonds. one would eipect ihatthe ma¡ket price of bonds would reflect the risk that future dividend paymenis wouldlower the asset base that secures debt.2. However, as changes in the dividend pay-ments are actually realtzed, there may be changes in the expectations of the báná-holde¡s, which in tu¡n would be reflected in the market price of bonds. All otherthings being equal, we may expect that higher dividend payments or share repurchaseswill be associated with a decline in the market value of debt. However, ,u."ly do ,.have a situation where all other things are equal. For example, if announcementsabout dividend changes are interpreted as information about iuture cash flows, thena dividend increase means that current debt will be more secure because of the antic-ipated higher cash flows, and we would observe dividend increases to be positivelycorrelated with inc¡eases in the market value of debt.

2. Stock Dividends and Share Repurchase

Stock dividends are often mentioned as part of the dividend policy of the firm.However, a stock dividend is nothing more than a small stock split. it simply in-creases the number of shares outstanding without changing any of th. underiyingrisk or ¡eturn characteristics of the firm. Therefore we mighl exiect that ¡t ¡as iittlior no effect on shareholders'wealth except for the losses associated with the clericaland transactions costs that accompany the stock dividend. Recall, however, that theempirical evidence in chapter 11 indicated that stock dividend announcements arein fact accompanied by statistically significant abnormal returns on the announce-ment date. So far, no adequate explanation has been provided for this fact, althoughBrennan and copeland [1987] suggest that stock dividends may be used to force tieearly conversion of convertible debt, convertible preferred, or warrants, because thesesecurities are frequently not protected against stock dividends.

2oDividendpaymentsdonotnecessarily"h"ng"th"".,"t"ffia1e rgduce!. in order to pay dividends, the¡e is an asset efect. However, it is not ¡ecessary. oi"¡¿""¿,

"""aho be,paid by issuing new debt or equity. In this case, ass€ts remain uíaffected, a¡a tne áini¿ena áecision

Another question that often arises is whether share repurchase is preferable to

dividend payment as a means of distributing cash to shareholde¡s. Share repurchase

allows shareholders to receive the cash payment as a capital gain rather than as

dividend income. Any shareholder who pays a higher tax rate on income than on

capital gains would prefer share repurchase to dividend payment. But not all classes

ofihareholders have this preference. Some, like tax-free university endowment funds,

are indifferent to income versus capital gains, whereas others, such aS corporations

with their dividend exclusions, would actually prefer dividends.

To see that share repurchase can result in the same benefit per share, consider

the following example. The Universal Sourgum Company earns $4.4 million in 1981

and decidesio pay out 50%, or $2.2 million, either as dividends or repurchase. The

company tras 1,IOO,OOO shares outstanding with a market value of $22 per share' Itcan pay dividends of s2 per share or repurchase shares at $22 each. We know that

the maiket price for repurchase is $22 rather than $20 because $22 will be the price

per share afier repurchase. To demonstrate this statement, we know that the current

value of the (all-equity) firm is $24.2 million. For $2.2 million in cash it can repurchase

100,000 shares. Therefore after the repurchase the value of the firm falls to $24.2 -2.2:$22 million, and with 1,000,000 shares outstanding the price per share is $22'

Thus, in theory, there is no price effect from repurchase.

A comparison of shareholders' wealth before taxes shows that it is the same with

either payment technique. If dividends are paid, each shareholder receives a $2 divi-

dend, áná the ex-dividend price per sha¡e is $20 ($22 million -: 1.1 million shares).

Alternately, as shown above, each share is worth $22 under repurchase, and a share-

holder who needs cash can sell off a portion of his or her shares. The preferred form

of payment (dividends versus repurchase) wili depend on shareholders' tax rates.-

In the example shown above there is no price effect from share repurchase. How-

ever, recent emplrical studies of repurchases via tender offers have found a positive

announcement effect. These studies are discussed in detail in Chapter 16'

SUMMARY 57I

STII\4MARY

Several valuation models with or without growth and with or without corporate taxes

have been developed. Dividend policy is ir¡elevant in all instances. It has no effect

on shareholders'wealth. When personal taxes are introduced we have a result where

dividends matter. For shareholders who pay higher taxes on dividends than on capital

gains, the preferred dividend payout is zero; they would rather have the company

áistribute óash payments via the share fepurchasó mechanism. Yet corporations do

pay dividends. The Rozeff [1982] paper suggests that there appear to be strong cross-

iectionai regularities in dividend payout. Thus there may be optimal dividend policies

that result fiom a trade-off between the costs and benefits of paying dividends. The

list of possible costs includes (1) tax disadvantages of receiving income in the form

of diviáends rather than capital gains, (2) the cost of raising external capital if divi-

dends are paid out, and (3) ihe foregone use of funds for productive investment. The

possible benefits of dividend payout are (1) higher perceived corporate value becauseis purely frnancial in nature.