36

McDermott DLV2000 Press Event April 13, 2016 Singapore

| Date post: | 19-Feb-2017 |

| Category: |

Documents |

| Upload: | rick-goins |

| View: | 72 times |

| Download: | 2 times |

McDermott DLV2000 Press Event

April 13, 2016Singapore

Forward-Looking Statements

In accordance with the Safe Harbor provisions of the Private Securities Litigation Reform Act of 1995, McDermott cautions that statements in this presentation which are forward-looking, and provide other than historical information, involve risks, contingencies and uncertainties that may impact McDermott’s actual performance and results of operations. The forward-looking statements in this presentation include, but are not limited to, statements about backlog, opportunity pipeline and revenue pipeline and the anticipated breakdown and timing of award of the associated contracts and expected backlog roll-off, to the extent these may be viewed as indicators of future revenues or profitability, market trends and overall expected market size, the expected specifications of and operations related to the DLV 2000, expected benefits from our joint ventures and alliances, the expected scope, execution, timing and value of projects discussed herein, expected benefits and savings resulting from our cost saving initiatives and McDermott’s earnings and other guidance for 2016. Although we believe that the expectations reflected in those forward-looking statements are reasonable, we can give no assurance that those expectations will prove to have been correct. Those statements are made by using various underlying assumptions and are subject to numerous risks, contingencies and uncertainties, including, among others: adverse changes in the markets in which we operate or credit markets, our inability to successfully execute on contracts in backlog, changes in project design or schedules, the availability of qualified personnel, changes in the scope, terms or timing of contracts, contract cancellations, change orders and other modifications and actions by our customers and business partners, difficulties executing on the project, changes in industry norms and adverse outcomes in legal and other dispute resolution proceedings. If one or more of these risks materialize, or if underlying assumptions prove incorrect, actual results may vary materially from those expected. You should not place undue reliance on forward-looking statements. For a more complete discussion of these and other risk factors, please see McDermott’s annual and quarterly filings with the Securities and Exchange Commission, including its annual report on Form 10-K for the year ended December 31, 2015. This presentation reflects management’s views as of the date hereof. Except to the extent required by applicable law, McDermott undertakes no obligation to update or revise any forward-looking statement.

|2

Today’s Agenda

|3

• Welcome

• Introduction of McDermott’s Leadership Team

− David Dickson, President and CEO

− Stuart Spence, Executive Vice President and CFO

− Hugh Cuthbertson, Vice President, Asia

− Jonathan Kennefick, Senior Vice President, Project Execution & Delivery

− John Macpherson, DLV2000 Project Manager

• McDermott Overview

− David Dickson, Stuart Spence, Hugh Cuthbertson

• Focus on the Derrick Lay Vessel DLV2000

− Jonathan Kennefick

• Question & Answer Session

• Your Tour of the DLV 2000

− John Macpherson

• Lunch and Additional 1-on-1 Opportunities

McDermott today

|4

•A vertically integrated offshore and subsea engineering, procurement, installation and construction company

• In-market fabrication yards and a versatile marine fleet

• Focus on long-term relationships with leading energy customers, building strong core capabilities and deepening talent

Today, we will focus on positioning for the future

Maximize Profitable Wins

Capture Value Through Integrated Capabilities

Deliver Value Through Execution

Strategic Themes in Action

Perspective on the Future

QHSES

People & Project

Management

Partnerships

Market Trends

Geographic Outlook

Alignment, Engagement & Solutions

In-market Capabilities

2016 OutlookEngineering

Procurement

Construction

OffshoreInstallation

|5

Priorities

Maximize Profitable WinsMarket Trends

Geographic Outlook

Short-term perspective:

Market Trends

|7

• Sharp decline in existing production could be amplified due to lack of investment

• Sustained low oil price creating a lower for longer environment

Long-term perspective:

1) Source: EIA Spot Brent Price

$/B

arre

l

2-Year Look Ahead:

• Offshore is most significant market segment

Offshore48%

Subsea33%

Fab Only19%

Overall Market Size ~$96BGlobal Oil Supply by Type

1) Source: Exxon Dec 2015

$20

$30

$40

$50

$60

$70

$80

$90

$100

$110

$120

Jan

14

Mar

14

May

14

Jul 1

4Se

p 1

4N

ov

14

Jan

15

Mar

15

May

15

Jul 1

5Se

p 1

5N

ov

15

Jan

16

Mar

16

May

16

Jul 1

6Se

p 1

6N

ov

16

Jan

17

Mar

17

May

17

Jul 1

7Se

p 1

7N

ov

17

Actuals Rolling Average Forecast

Brent Outlook to 20181

Geographic diversity provides through cycle opportunities

|8

Clie

nt

Typ

es

Pro

ject

Typ

es

Americas, Europe, Africa$18B

Middle East$10B

Asia$7B

Middle East NOCs and Brownfield Projects Generate Confidence to Maximize Profitable WinsNOC = National Oil Company; IOC = International Oil Company; Note: IOCs include supermajors and all other non-NOCs1) There is no assurance that projects in the bid pipeline (targets and backups) will be awarded to McDermott2) As of September 30, 2015

2 Y

ear

Op

po

rtu

nit

y P

ipe

line

1,2

NOC16%

IOC84%

NOC100%

NOC21%

IOC79%

Greenfield67%

Brownfield33%

Greenfield4%

Brownfield96%

Greenfield86%

Brownfield14%

Capture Value Through Integrated Capabilities

Engineering

Procurement

Construction

OffshoreInstallation

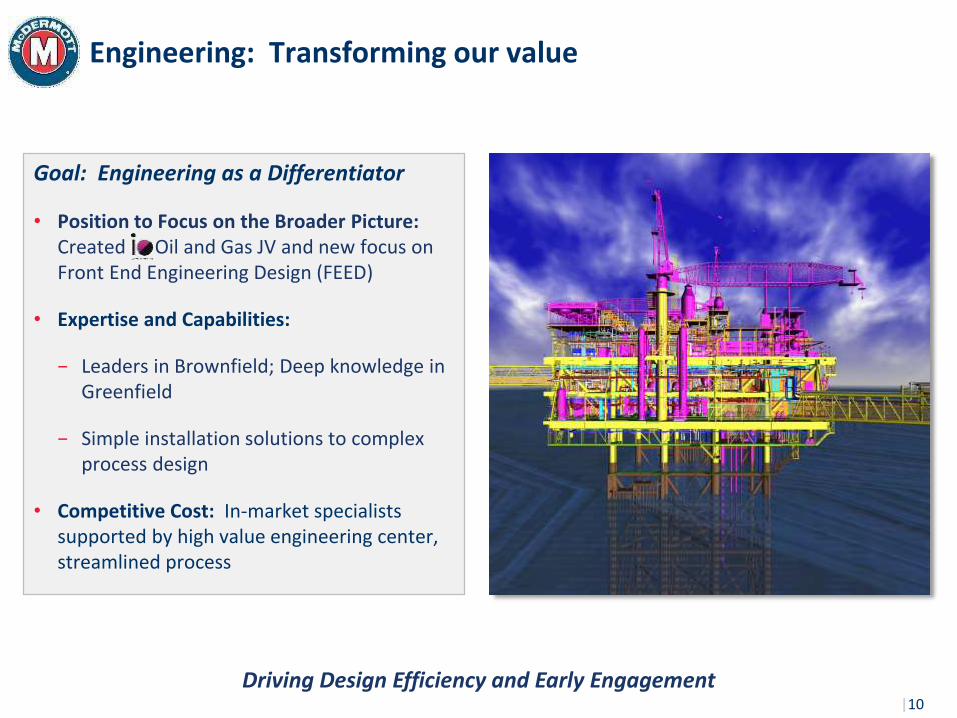

Engineering: Transforming our value

|10

Goal: Engineering as a Differentiator

• Position to Focus on the Broader Picture: Created Oil and Gas JV and new focus on Front End Engineering Design (FEED)

• Expertise and Capabilities:

− Leaders in Brownfield; Deep knowledge in Greenfield

− Simple installation solutions to complex process design

• Competitive Cost: In-market specialists supported by high value engineering center, streamlined process

Driving Design Efficiency and Early Engagement

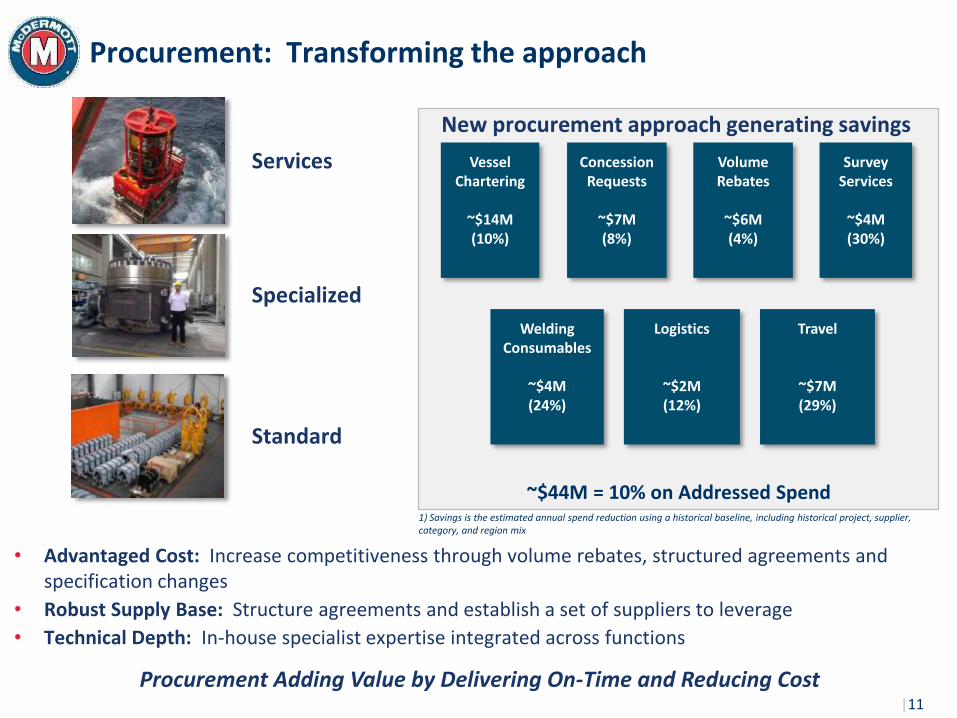

Procurement: Transforming the approach

|11

Services

Specialized

Standard

• Advantaged Cost: Increase competitiveness through volume rebates, structured agreements and specification changes

• Robust Supply Base: Structure agreements and establish a set of suppliers to leverage

• Technical Depth: In-house specialist expertise integrated across functions

Procurement Adding Value by Delivering On-Time and Reducing Cost

~$44M = 10% on Addressed Spend

Vessel Chartering

~$14M(10%)

Concession Requests

~$7M(8%)

Volume Rebates

~$6M(4%)

Welding Consumables

~$4M(24%)

Survey Services

~$4M(30%)

Logistics

~$2M(12%)

Travel

~$7M(29%)

1) Savings is the estimated annual spend reduction using a historical baseline, including historical project, supplier, category, and region mix

New procurement approach generating savings

Construction: Driving to a global standard of efficiency

|12

Jebel Ali / Dammam BatamAltamira

• Global, in-market fabrication facilities with in-house full control of cost, quality and schedule

• Instituted fabrication council to drive global process while streamlining supervision and structure

• Creating the ability to workshare

• Optimized processes and procedures

• JVs providing access to low cost and in-market solutions

• A relentless culture of improvement

China

Malaysia

Control of Fabrication is an EPCI Sustainable Competitive Advantage

Installation: Shallow to deep throughout the lifecycle

|13

Dynamically Positioned Vessel

Anchored Vessel

Hook-up & Commissioning

Versatile Fleet with Broad Capabilities is a Differentiator

• Class 3 dynamically positioned vessel with a 2,200-ton crane & deepwater S-lay pipelay system

• Fast transit speeds make the DLV2000 a global asset

• Scheduled to work in 2016 and 2017 on the INPEX Ichthys and Woodside Greater Western Flank Phase II Projects in Australia

• A full solution of shallow water fleet capabilities with versatile subsea fleet

• Supported by in-market teams

• Expertise in complex brownfield installation, hook up and commissioning

Heavy Lift and High-End Pipelay Vessel

DLV 2000:

Deliver Value Through Execution

QHSESPeople & Project

ManagementPartnerships

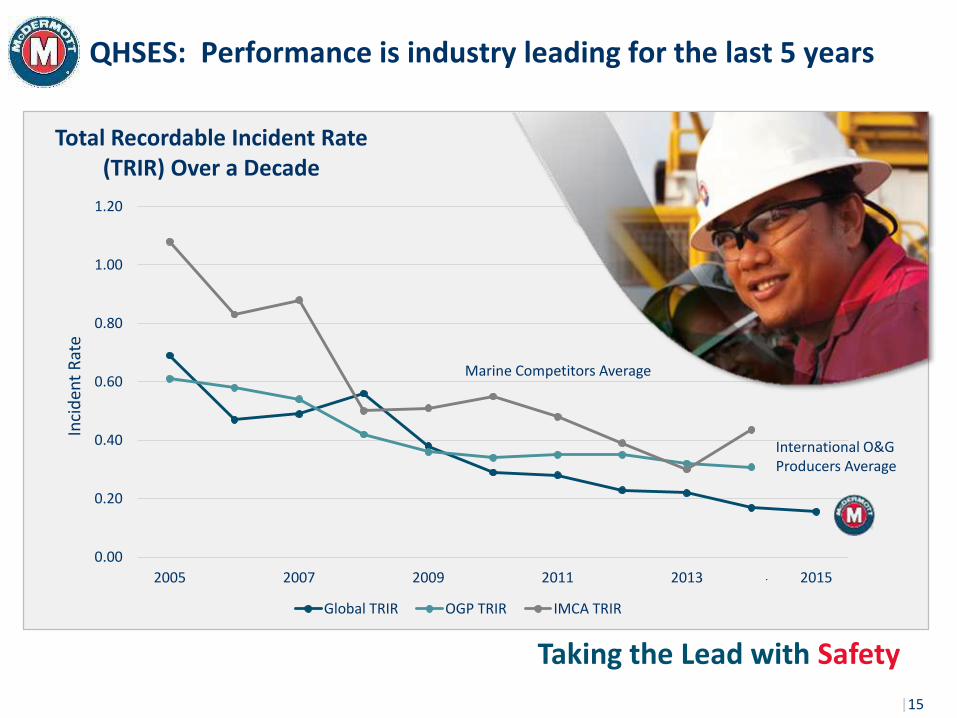

QHSES: Performance is industry leading for the last 5 years

|15

Taking the Lead with Safety

0.00

0.20

0.40

0.60

0.80

1.00

1.20

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Total Recordable Incident Rate (TRIR) Over a Decade

Global TRIR OGP TRIR IMCA TRIR

Marine Competitors Average

International O&G Producers Average

Inci

den

t R

ate

People and Project Management

|16Strong Talent and Core Capabilities Integrating All Aspects of the Project Life Cycle

Schedule Assurance

Contract Management

Core Operating Rhythm

StrategicProject

Management

Risk / Opportunity Management

Competency

Cost Optimization

Establishing the “McDermott Way” as the industry benchmark for delivering complex, offshore and subsea capital projects

• Renewed focus on core capabilities and deepening talent sets a strong foundation

― Established workforce of expertise and accountability

― Continued focus on growing, developing and expanding upon revitalized organization and talent

• Created a global project management function to ensure consistent execution and control across areas and projects

• Focus on the key 6 dimensions of project management

― Core operating rhythm based on specific milestones with clear risk mitigation strategies

― Maximize opportunities through contract management

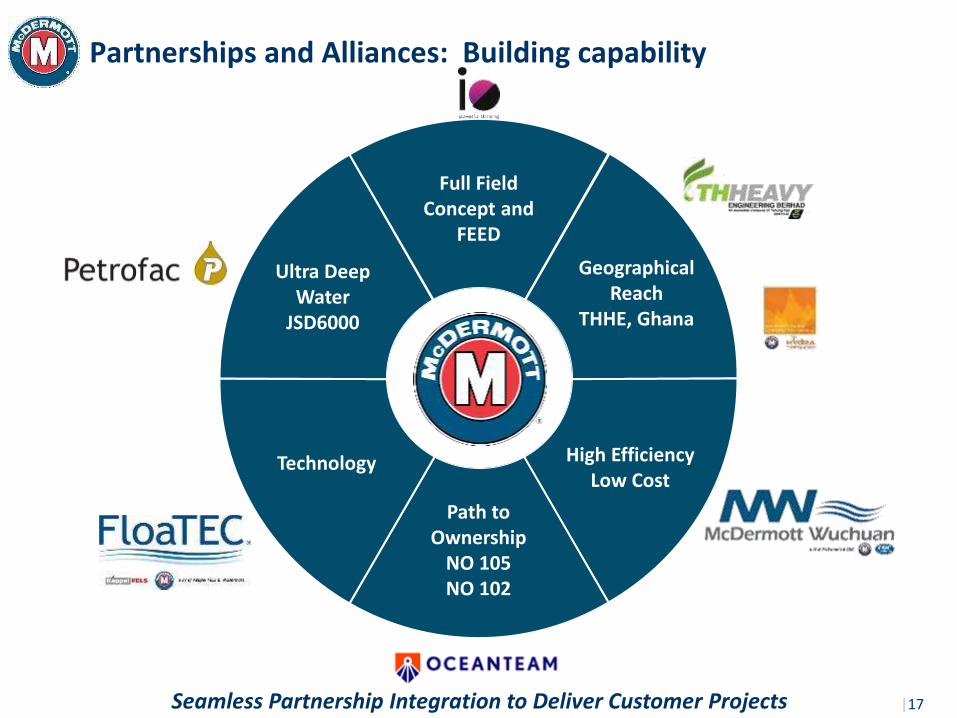

Partnerships and Alliances: Building capability

|17Seamless Partnership Integration to Deliver Customer Projects

High EfficiencyLow Cost

Ultra Deep Water

JSD6000

Full Field Concept and

FEED

Text

Technology

Path to Ownership

NO 105NO 102

Geographical Reach

THHE, Ghana

Strategic Themes in ActionAlignment,

Engagement & Solutions

In-market Capabilities

• Early Engagement: Full field development

− Increased delivery certainty with early de-risking of development concept

− Early engagement provides opportunity to secure EPCI tender following FEED

• Customer Alignment: Saudi Aramco’s Lump Sum award under LTA II

− Largest single award in McDermott’s Middle East history

− Full scale EPCI contract utilizing specialized shallow water installation vessels

• Integrated Solutions: Inpex Ichthys scope of work

− Full engineering to design, with procurement of over $600M of complex and unique components

− Installation of over 85 mile of rigid flowlines, 35 miles of umbilicals and 16 miles of flexible risers procured, installed and tested

− Fabrication of 48 structures, total weight >27,000 tons, with In-market execution

Our Strategic Themes in Action

|19

Customer Alignment Combined with Integrated Capabilities Generates Differentiator in Market Solutions

In-market Capabilities: Maintaining the lead in Middle East

|20

The Focus

• Deepen customer alignment and relationships through early engagement and cultural fit

• National oil companies who remain committed to production levels and brownfield and producing basins with lowest production costs

• Invest in new resource skill sets and required assets to address the new customer projects

Unparalleled Company History and Experience in Offshore EPCI

To Deliver

• Trusted brand and strong customer relationships

• Evolving capabilities in a robust market

• Project solutions to maintain customer output

Region Totals514 Structures

1,681 total mi of pipelines

7,500 mi of cable

Qatar

130451 mi

Key Clients

UAE

77422 mi

Key ClientsSaudi Arabia

Key Client

284696 mi

Kuwait & Neutral Zone

23112 mi

Key Client

Engineering Offices in Al Khobar and Dubai

Fabrication Facility in Dubai and Dammam

Experience: Offshore Structures and Pipelines Installed Since 1980

Driving Financial Performance

2015 Full-Year Financial Highlights

|22

• High level of order intake led to largest increase in backlog since 2012

• 2015 Revenue driven primarily by Middle East and Asia

• 2014 Adjusted Operating Income included gains on sale of assets of $46.2M

• $189M of Capex related to DLV2000 deferred from 2015 to 2016

• Adequate coverage on Covenant EBITDA

FY’15 FY’14Year-over-Year

Delta

Orders $3,701 $1,100 $2,601

Backlog $4,231 $3,601 $630

Revenue $3,070 $2,301 $769

Adjusted P&L Metrics1

Gross Profit $396 $188 $208

Gross Profit Margin 12.9% 8.2% 4.7%

Operating Income (OI) $175 $24 $151

OI Margin Percentage 5.7% 1.0% 4.7%

Net Income / (Loss) $66 ($61) $127

Diluted EPS $0.23 ($0.26) $0.49

EBITDA $286 $133 $153

Capex $103 $321 ($218)

Cash $782 $853 ($71)

Covenant EBITDA – TTM2 $338 $143 $195

$ in millions

1) Gross Profit (and margins), Operating Income (and margins), Net Income, Diluted EPS and EBITDA have been adjusted to exclude restructuring charges, mark-to-market pensions adjustments in the fourth quarter of 2014 and 2015 and charges associated with a legal settlement in the third quarter of 2015. The reconciliation of adjusted measures to the nearest GAAP measure are provided in the pages titled “Additional Disclosures”. Also, the number of shares outstanding utilized in determining earnings per share varies based on whether the Company has a Net Income or a Net loss. The appropriate number of shares outstanding is also listed in the pages titled, “Additional Disclosures”.

2) Covenant EBITDA is a Non-GAAP measure and the GAAP reconciliation is provided in the pages titled “Additional Disclosures”.

4Q 2015 Backlog and Roll-off

|23

• 81% of 2016 expected revenue in backlog; driven by Middle East

• Backlog roll-off includes ~$800M from Ichthys in 2016

• Focused on obtaining awards to provide additional coverage in 2017 and beyond

$ in billions

Backlog by SegmentBacklog by Business Line Backlog Roll-Off by Year

Details of $4.2BN Backlog as of December 31, 2015

$2.4

$1.3

$0.5

2016 2017 2018

Offshore$2.969%

Subsea$1.331%

AEA$0.3

7%

MEA$2.662%

ASA$1.331%

Customer Contract Scope

$10.4

$1.6

$7.2

$11.8

$1.7

$6.1

NOC Super Major Independent

$13.1

$0.6

$5.5

$12.4

$0.7

$6.5

EPCI EPC Other

Segment$7.5

$5.7 $6.0

$7.3 $7.1

$5.2

AEA MEA ASA

Greenfield/Brownfield

$8.1

$11.1

$8.6

$11.0

Greenfield Brownfield

Oil/Gas

$13.8

$5.4

$12.9

$6.7

Oil Gas

Business Line

$11.7

$7.5

$14.2

$5.4

Offshore Subsea

Bids Outstanding and Target Projects1

$19.6 billion as of 4Q 2015 compared to $19.2 billion in 3Q 2015

|24

Q3’15

Q4’15

1) Includes change orders. There is no assurance that bids outstanding or target projects will be awarded to McDermott.2) Target projects are those that we believe fit McDermott’s capabilities and are anticipated to be awarded in the market in the next five quarters.3) Other includes T&I, Construction and other types of work.

$ in billions

3

Perspective on the Future

2016 Outlook Priorities

2016 Outlook

1) Items are adjusted for restructuring costs. All reconciliations to GAAP figures are provided in the pages titled “Additional Disclosures”2) Net Interest Expense has been reduced by ~$10M for capitalized interest included in Capex3) EBITDA, Covenant EBITDA - TTM and Free Cash Flow reconciliations to the nearest GAAP measure are provided in the pages titled “Additional Disclosures”4) The Company has a minimum required Covenant EBITDA – TTM of $251 million, before use of available add back of $28 million

Revenues ~$2.9B

Adjusted Operating Income1 ~$115

Net Interest Expense2 ~$64

Income Tax Expense ~$55

Adjusted Net Income1 ~$0

Adjusted Diluted EPS1 ~$0.00

Adjusted EBITDA1,3 ~$240

Restructuring Expense ~$10

Cash Interest / DIC Amortization Interest ~$60 / ~$14

Covenant EBITDA – TTM3,4 ~$285

Capex2 ~$260

Ending Cash and Restricted Cash ~$580

Ending Gross Debt ~$840

Free Cash Flow3 ~($160)

|26

$ in millions, except per share amounts,

or as indicated

• 81% of 2016 outlook revenue in December 2015 backlog

• Continued focus on highest value proposition opportunities, executing well our existing backlog, customer alignment and asset utilization

• Restructuring expense comprised of McDermott Profitability Initiative (“MPI”) and Additional Overhead Reduction (“AOR”)

• Actively managing our cost and liquidity structure

• Given macro commodity environment, may see pressure from potential customer capex spending delays and stronger competitive pricing pressure

Driving Results Through Cycle

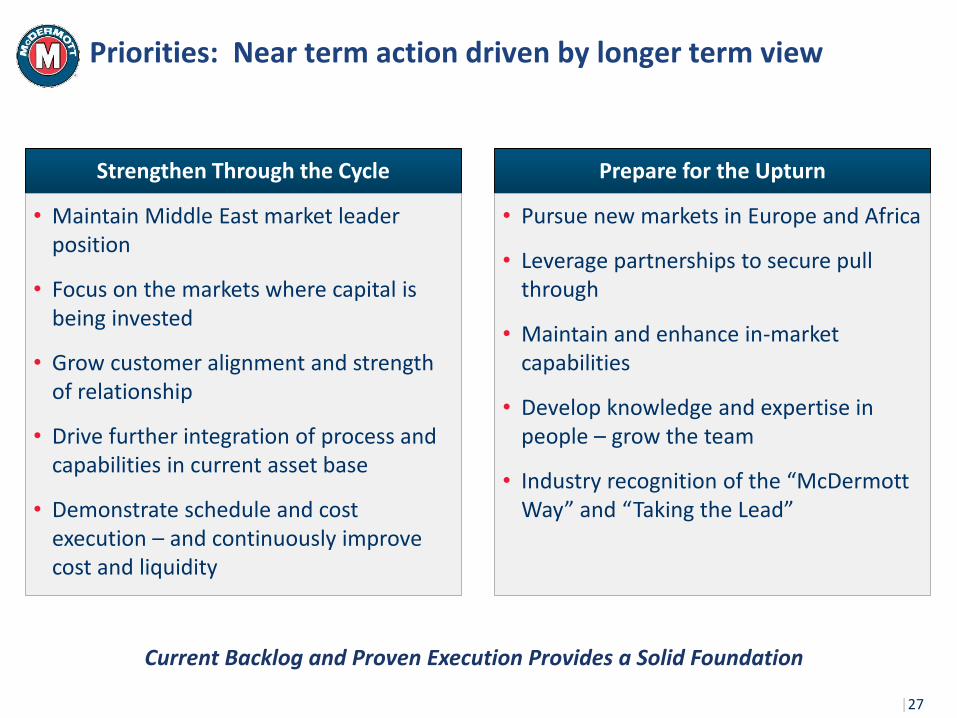

Priorities: Near term action driven by longer term view

Current Backlog and Proven Execution Provides a Solid Foundation

Strengthen Through the Cycle

• Maintain Middle East market leader position

• Focus on the markets where capital is being invested

• Grow customer alignment and strength of relationship

• Drive further integration of process and capabilities in current asset base

• Demonstrate schedule and cost execution – and continuously improve cost and liquidity

Prepare for the Upturn

• Pursue new markets in Europe and Africa

• Leverage partnerships to secure pull through

• Maintain and enhance in-market capabilities

• Develop knowledge and expertise in people – grow the team

• Industry recognition of the “McDermott Way” and “Taking the Lead”

|27

Your QuestionsMcDermott DLV2000 Press Event

April 13, 2016Singapore

The DLV2000 and McDermott

The DLV2000: A Critical Tool in a Specialized Marine Fleet

Thirteen Vessels for Offshore, Subsea and Deepwater Projects

|30

CSV 108

NO 102

Rigid Reel Lay Heavy Lift/Pipelay (S-Lay/J-Lay)Flex Lay

Launch Barges

Agile

Emerald Sea

NO 105

Intermac 600 Intermac 650

Thebaud Sea

Construction Support Vessels DLV2000

(2016 Delivery)DB50 DB32

DB30 DB27

The DLV2000 At A Glance

|31

• Heavy lift pipe-lay vessel

• 2,000 MT crane

− Auxiliary 600 MT

− Whips: 250 MT

• Dynamic Positioning Class 3

• Deepwater S-Lay capability: 4.5 to 60 inches

• Pipe-lay equipment

− Tension capacity: 450 MT (3@150 MT)

• Ideal for installation, maintenance and decommissioning projects

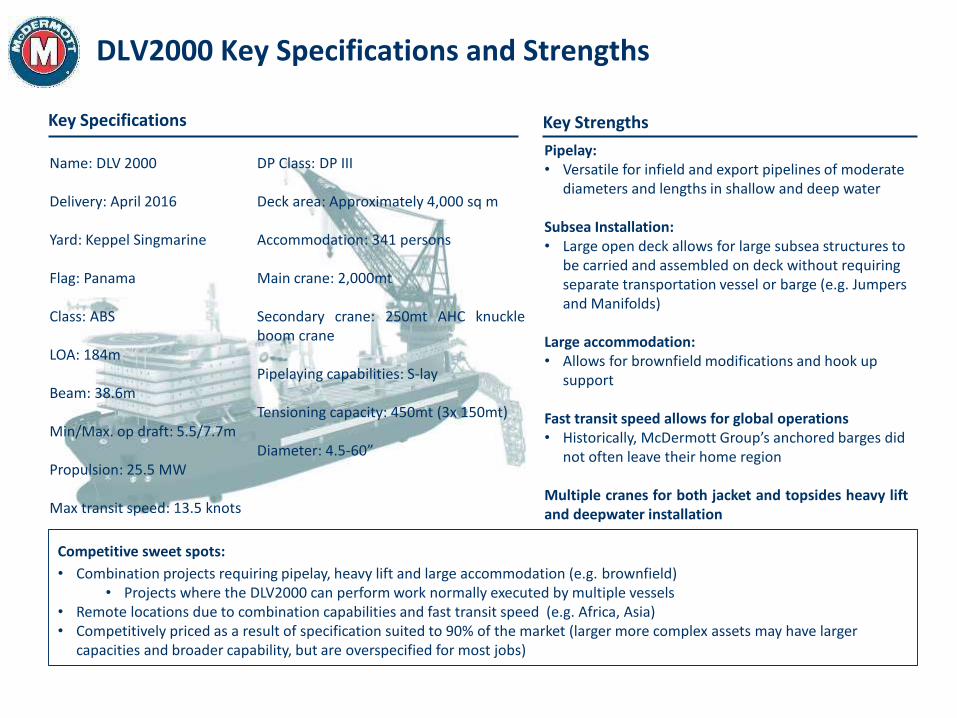

DLV2000 Key Specifications and Strengths

Name: DLV 2000

Delivery: April 2016

Yard: Keppel Singmarine

Flag: Panama

Class: ABS

LOA: 184m

Beam: 38.6m

Min/Max. op draft: 5.5/7.7m

Propulsion: 25.5 MW

Max transit speed: 13.5 knots

DP Class: DP III

Deck area: Approximately 4,000 sq m

Accommodation: 341 persons

Main crane: 2,000mt

Secondary crane: 250mt AHC knuckleboom crane

Pipelaying capabilities: S-lay

Tensioning capacity: 450mt (3x 150mt)

Diameter: 4.5-60”

Key Specifications Key Strengths

Pipelay:• Versatile for infield and export pipelines of moderate

diameters and lengths in shallow and deep water

Subsea Installation:• Large open deck allows for large subsea structures to

be carried and assembled on deck without requiring separate transportation vessel or barge (e.g. Jumpers and Manifolds)

Large accommodation:• Allows for brownfield modifications and hook up

support

Fast transit speed allows for global operations • Historically, McDermott Group’s anchored barges did

not often leave their home region

Multiple cranes for both jacket and topsides heavy liftand deepwater installation

Competitive sweet spots:

• Combination projects requiring pipelay, heavy lift and large accommodation (e.g. brownfield)• Projects where the DLV2000 can perform work normally executed by multiple vessels

• Remote locations due to combination capabilities and fast transit speed (e.g. Africa, Asia)• Competitively priced as a result of specification suited to 90% of the market (larger more complex assets may have larger

capacities and broader capability, but are overspecified for most jobs)

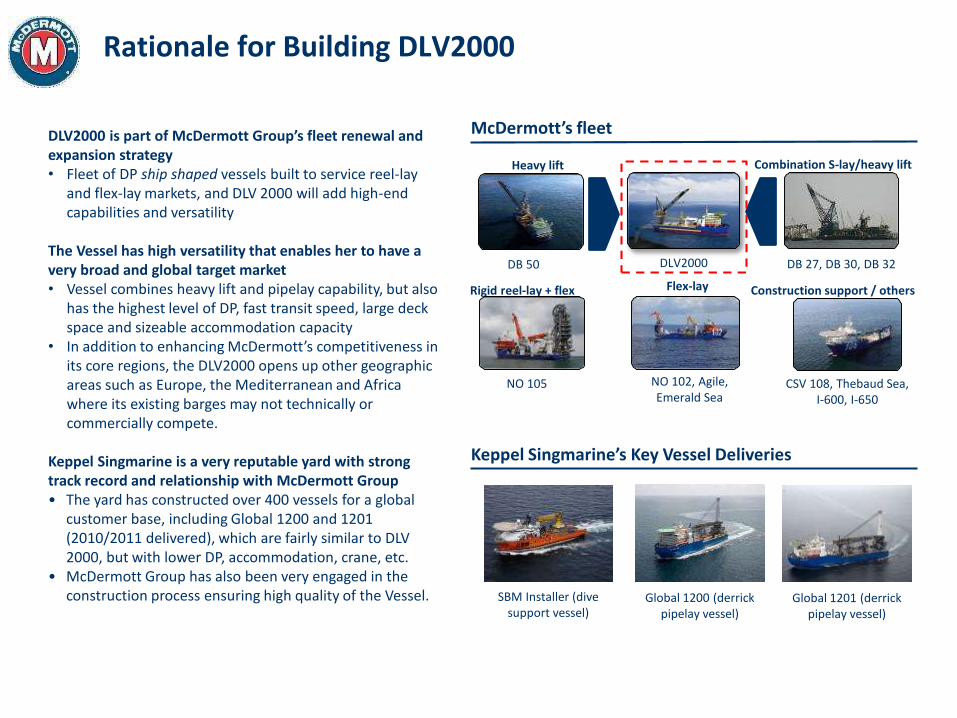

Rationale for Building DLV2000

McDermott’s fleetDLV2000 is part of McDermott Group’s fleet renewal and expansion strategy• Fleet of DP ship shaped vessels built to service reel-lay

and flex-lay markets, and DLV 2000 will add high-end capabilities and versatility

The Vessel has high versatility that enables her to have a very broad and global target market• Vessel combines heavy lift and pipelay capability, but also

has the highest level of DP, fast transit speed, large deck space and sizeable accommodation capacity

• In addition to enhancing McDermott’s competitiveness in its core regions, the DLV2000 opens up other geographic areas such as Europe, the Mediterranean and Africa where its existing barges may not technically or commercially compete.

Keppel Singmarine is a very reputable yard with strong track record and relationship with McDermott Group• The yard has constructed over 400 vessels for a global

customer base, including Global 1200 and 1201 (2010/2011 delivered), which are fairly similar to DLV 2000, but with lower DP, accommodation, crane, etc.

• McDermott Group has also been very engaged in the construction process ensuring high quality of the Vessel.

Combination S-lay/heavy lift

Flex-lay Construction support / others

DB 50

Rigid reel-lay + flex

DB 27, DB 30, DB 32

NO 105 NO 102, Agile, Emerald Sea

CSV 108, Thebaud Sea, I-600, I-650

Heavy lift

DLV2000

Keppel Singmarine’s Key Vessel Deliveries

Global 1200 (derrick pipelay vessel)

SBM Installer (dive support vessel)

Global 1201 (derrick pipelay vessel)

Installation: Shallow to deep throughout the lifecycle

|34

Dynamically Positioned Vessel

Anchored Vessel

Hook-up & Commissioning

Versatile Fleet with Broad Capabilities is a Differentiator

• Class 3 dynamically positioned vessel combining a 2,200-ton crane and deepwater S-lay pipelay system

• Fast transit speeds make the DLV2000 a global asset

• The DLV2000 is scheduled to work in 2016 and 2017 on the INPEX Ichthys and Woodside Greater Western Flank Phase 2 Projects in Australia

• A full solution of shallow water fleet capabilities targeted for the local Middle East and Asian markets

• Versatile subsea fleet

• Expertise in complex brownfield installation, hook up and commissioning

Heavy Lift and High-End Pipelay Vessel

DLV2000:

DLV2000 Media Conference and Tour Map

35

Press Conference Building

Naming Platform

Tentage

VIP Carpark

Touring the DLV2000: Tour Route

• Tour starts and boards the vessel to vessel to Main Deck• Route will follow the Main Deck, including three cranes and Stinger Winch

Systems• Tour will continue below deck and then to the Bridge• Lunch will follow tour’s end• Your questions are WELCOME!

Probable entry points to Main Deck

Limited Access Tented Area for guests with blowers and

ushers to describe the vessel features

Entry point for all other guests Entry point for VIP tour guests

Entry and Exit point to Freeboard Deck

P1

Safety First! Selfie Stop on Bridge Only