28

DNO INTERNATIONAL ASA PRESENTATION FIRST QUARTER 2009

DNO INterNatIONal aSa

Presentation First Quarter 2009

Agenda Introduction & Operational Review • Ivar Brandvold, COO

Financial Review • Haakon Sandborg, CFO

Q&A

First Quarter 2009 | 2

Making positive change Strategy • During the last years DNO’s strategy has been focused on low cost projects in high potential areas -

avoiding long term capital commitments • This strategy made the company well prepared to adapt to recent oil price levels

Shift in focus • Shift in focus to production and near term developments, with exploration activity to be undertaken on a

more selective basis • This will reduce the overall investment level for this year significantly compared to 2008

Ready for full scale production • Tie-in of the Tawke pipeline to Iraq’s Northern pipeline system was completed by the end of Q1’09 • On 10 May, DNO received formal notice by KRG to commence crude oil export from the Tawke field

First Quarter 2009 | 3

Initiation of crude oil export from Kurdistan Start of export on 1 June, 2009

Marketed by SOMO

Confirmation received • DNO is instructed by KRG to

complete any outstanding work and undertake all necessary preparations

• Ensure safe and smooth operation on the commencement date

First Quarter 2009 | 4

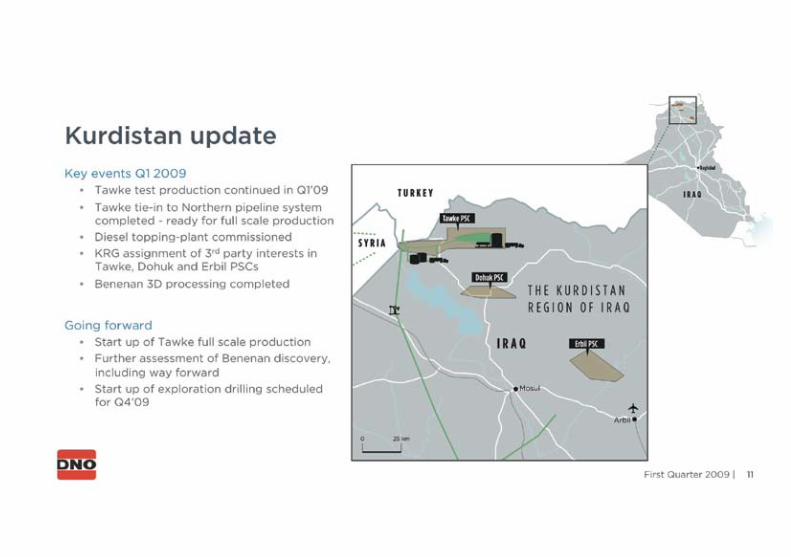

Key events in the First Quarter 2009 • The tie-in of the Tawke pipeline to Iraq’s Northern pipeline system was completed by the

end of first quarter 2009

• The Annual Statement of Reserves shows an increase to 163 mboe (P50)

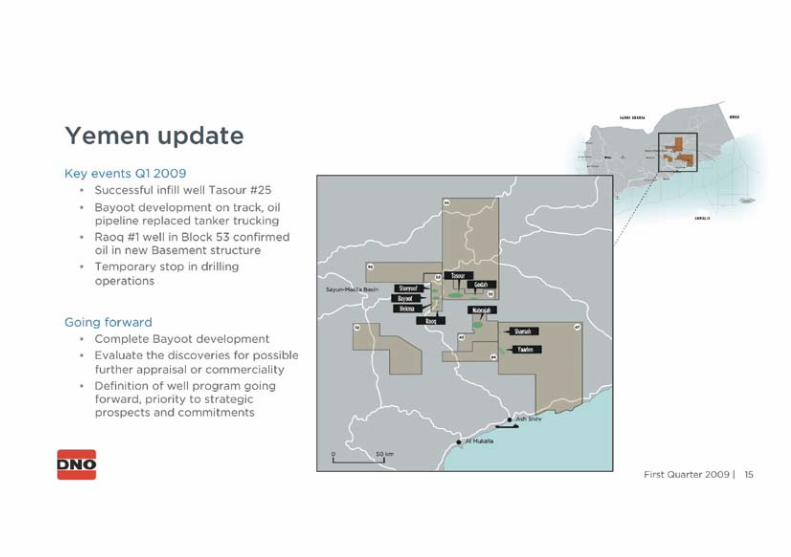

• Exploration drilling has temporarily been suspended in Yemen and Kurdistan with prospects being matured to define the drilling program going forward

• DNO divested 11.9 per cent of DETNOR in January, bringing the total ownership to 25 per cent

• Netback in the first quarter was negative with NOK 6 million while the net profit in the first quarter was NOK 138 million due to a partial impairment reversal on the DETNOR investment

First Quarter 2009 | 5

OPERATIONS

Block 32, 43, 44, 47, 52, 53, 72 and 84

Business Overview

First Quarter 2009 | 7

Det norske oljeselskap ASA

PL1067

Tawke Benenan (Hawler)

Dohuk

Sharyoof Tasour Nabrajah

Bayoot

Inhaminga

Block P

HSE summary DNO’s approach

• Based on continuous improvement processes aimed to create and maintain a good environment for employees, contractors and for the communities in which the Company operates

• Application of acknowledged risk reduction principles shall eliminate or minimize any exposure

• Maintain, as far as practically possible, zero discharge of emissions or pollutions to the environment.

• With DNO operating on land, reducing the risk exposure related to driving and logistics is a primary focus to the company

HSE performance trends

First Quarter 2009 | 8

0

1

2

3

4

5

6

7

8

9

Ap

ril 0

8

Mai

08

June

08

July

08

Aug

ust

08

Sep

tem

ber

08

Oct

ob

er 0

8

Nov

emb

er 0

8

Dec

emb

er 0

8

Janu

ary

09

Feb

ruar

y 0

9

Mar

ch 0

9

Fre

que

ncy

YTD Lost Time Incident Frequency

YTD Vehicle Incident Frequency

YTD Total Recordable Incident Frequency

2009 Annual statement of reserves Reserves & resources (1-7)*

0

20

40

60

80

100

120

140

160

180

200

31-12-07 Discoveries Revisions Production 31-12-08

MB

BL

156,8

-5,7

24.3

2.8 178.3

Classification 1-7*

First Quarter 2009 | 9

162.6

2.5 13.1

178.3

0

20

40

60

80

100

120

140

160

180

200

Class 1-3 Class 4 Class 5 Class 7 Class 1-7 M

BB

L

*Does not include associated reserves (P50) and resources in Det norske oljeselskap ASA (36,9%) of 40,1 mbbl

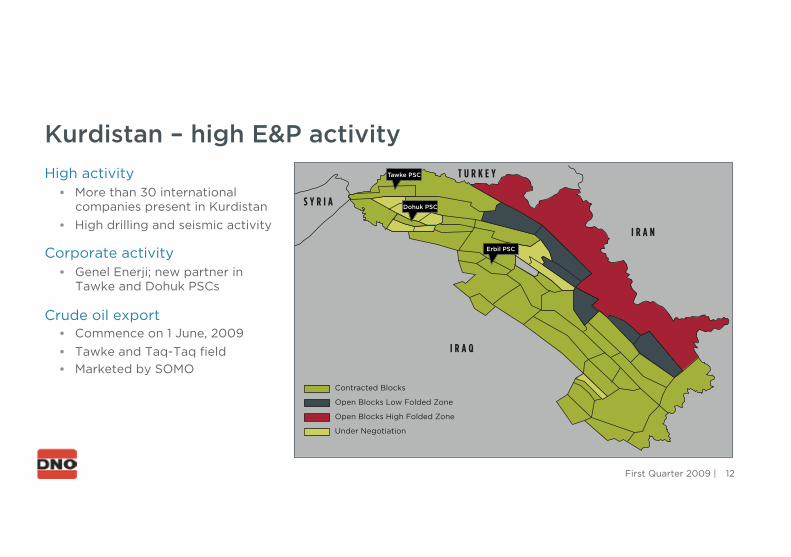

Kurdistan – high E&P activity High activity • More than 30 international

companies present in Kurdistan • High drilling and seismic activity

Corporate activity • Genel Enerji; new partner in

Tawke and Dohuk PSCs

Crude oil export • Commence on 1 June, 2009 • Tawke and Taq-Taq field • Marketed by SOMO

12 First Quarter 2009 |

DNO

T U R K E Y

I R A N

S Y R I A

I R A Q

Contracted Blocks

Open Blocks Low Folded Zone

Open Blocks High Folded Zone

Under Negotiation

Tawke PSC

Dohuk PSC

Erbil PSC

Tie-in area completed

First Quarter 2009 | 13

Diesel topping-plant commissioned

First Quarter 2009 | 14

FINANCIALS

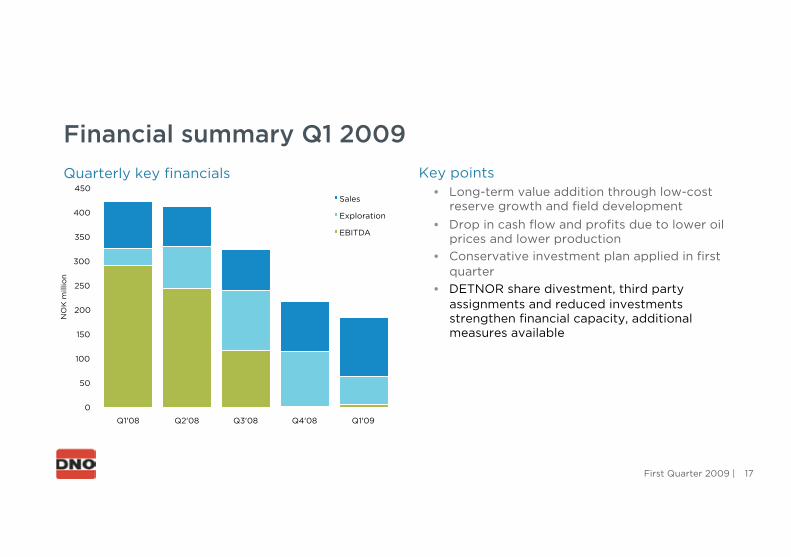

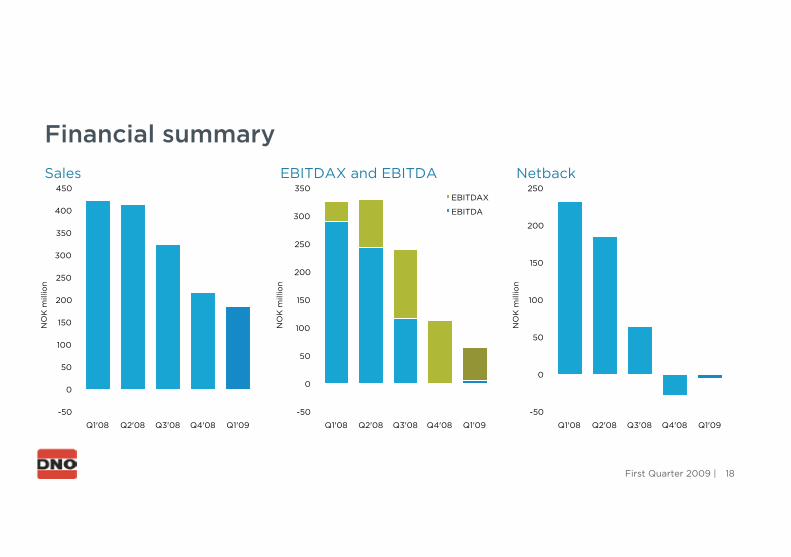

Financial summary Q1 2009 Quarterly key financials Key points

• Long-term value addition through low-cost reserve growth and field development

• Drop in cash flow and profits due to lower oil prices and lower production

• Conservative investment plan applied in first quarter

• DETNOR share divestment, third party assignments and reduced investments strengthen financial capacity, additional measures available

First Quarter 2009 | 17

0

50

100

150

200

250

300

350

400

450

Q1'08 Q2'08 Q3'08 Q4'08 Q1'09

NO

K m

illio

n

Sales

Exploration

EBITDA

EBITDAX and EBITDA

Financial summary

Sales Netback

First Quarter 2009 | 18

-50

0

50

100

150

200

250

300

350

400

450

Q1'08 Q2'08 Q3'08 Q4'08 Q1'09

NO

K m

illio

n

-50

0

50

100

150

200

250

300

350

Q1'08 Q2'08 Q3'08 Q4'08 Q1'09

NO

K m

illio

n

EBITDAX

EBITDA

-50

0

50

100

150

200

250

Q1'08 Q2'08 Q3'08 Q4'08 Q1'09

NO

K m

illio

n

Condensed income statement NOK Million Q1 2009 Q4 2008 Q1 2008 2008

Sales 183.8 217.3 421.9 1,376.2

Cost of goods sold -190.2 -198.7 -212.8 -745.5

Gross profit -6.4 18.6 209.1 630.7

Dry well cost expensed -8.9 -73,5 -4.1 -158,3

Seismic and other exploration expensed -49.3 -39,3 -30.0 -198,6

Other -12.5 -203,4 -20.9 -265,1

Profit/(loss) from operating activities -77.1 -297,5 154.1 8,8

Share of profit/(loss) associates 1.8 87.0 -3.3 83.3

Net finance 204.5 -702.1 -35.7 -782.0

Profit/(loss) before income tax 129.2 -912,7 115.0 -689,9

Income tax expense 8.7 -64,6 -52.6 -214.0

Net profit/(loss) 137.9 -977,3 62.4 -903,9

First Quarter 2009 | 19

Key points Q1’09 • Gain of NOK 23.8 million from sale of DETNOR shares in January 2009 • NOK 239 million non-cash reversal in Q1’09 of impairment on DETNOR investment • Interest costs down on lower interest rates • Improved FX balance following conversion of bond debt to USD in Q4’08

Net finance

First Quarter 2009 | 20

NOK Million Q1 2009 Q4 2008 Q1 2008 2008

Other financial income 23.8 1.2 - 13.9

Impairment/reversal of impairment of financial assets 229.9 -738.4 - -765.4

Net interest cost -32.4 -52.1 -31.6 -158.3

Exchange rate gain (loss), unrealized items -7.9 65.4 1.4 114.1

Other financial items -7.1 108.9 -8.9 97.1

Net finance 206.3 -615.2 -39.1 -698.6

Exploration expenditure Exploration expensed

-20

0

20

40

60

80

100

120

140

Q1 2008 Q2 2008 Q3 2008 Q4 2008 Q1 2009

NO

K m

illio

n

Yemen

Kurdistan

Africa

Q1 2009 exploration expenses • Reduced exploration activity, maturing of

prospects for later drilling • NOK 58 million in expensed exploration in the

quarter, including NOK 29 million in Yemen seismic survey

First Quarter 2009 | 21

Capital expenditure CAPEX per segment

-50

0

50

100

150

200

250

300

350

400

Q1 2008 Q2 2008 Q3 2008 Q4 2008 Q1 2009

NO

K m

illio

n

Yemen

Kurdistan

Africa

Q1 2009 CAPEX • Overall investment levels significantly down

from previous quarters • NOK 77 million in Capex in the quarter:

• NOK 50 million on pipeline tie-in, diesel-topping plant and other development on the Tawke field

• NOK 11 million on Bayoot development • NOK 8 million production wells on Bl 32

First Quarter 2009 | 22

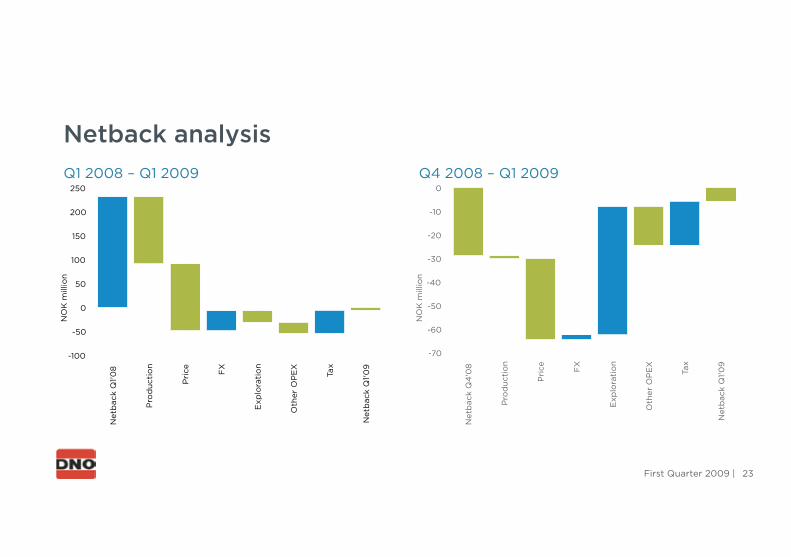

Netback analysis Q1 2008 – Q1 2009 Q4 2008 – Q1 2009

First Quarter 2009 | 23

-70

-60

-50

-40

-30

-20

-10

0

Net

bac

k Q

4'0

8

Pro

duc

tio

n

Pri

ce

FX

Exp

lora

tio

n

Oth

er O

PE

X

Tax

Net

bac

k Q

1'09

NO

K m

illio

n

-100

-50

0

50

100

150

200

250

Net

bac

k Q

1'08

Pro

duc

tio

n

Pri

ce

FX

Exp

lora

tio

n

Oth

er O

PE

X

Tax

Net

bac

k Q

1'09

NO

K m

illio

n

0

50

100

150

200

250

300

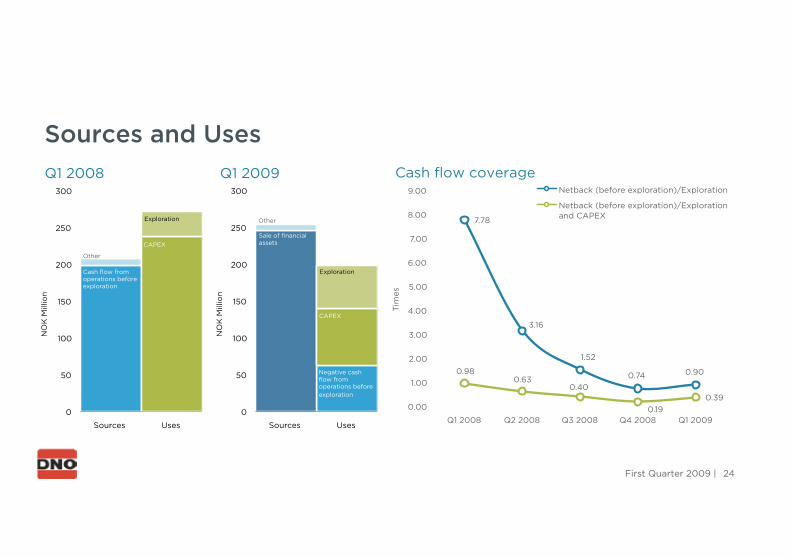

Sources Uses

NO

K M

illio

n

Sources and Uses Q1 2008 Q1 2009

7.78

3.16

1.52

0.74 0.90 0.98 0.63

0.40

0.19 0.39

0.00

1.00

2.00

3.00

4.00

5.00

6.00

7.00

8.00

9.00

Q1 2008 Q2 2008 Q3 2008 Q4 2008 Q1 2009

Tim

es

Netback (before exploration)/Exploration

Netback (before exploration)/Exploration and CAPEX

First Quarter 2009 | 24

Cash flow coverage

0

50

100

150

200

250

300

Sources Uses

NO

K M

illio

n

Cash flow from operations before exploration

Other

CAPEX

Exploration

Negative cash flow from operations before exploration

Sale of financial assets

CAPEX

Exploration

Other

0

1000

2000

3000

4000

5000

6000

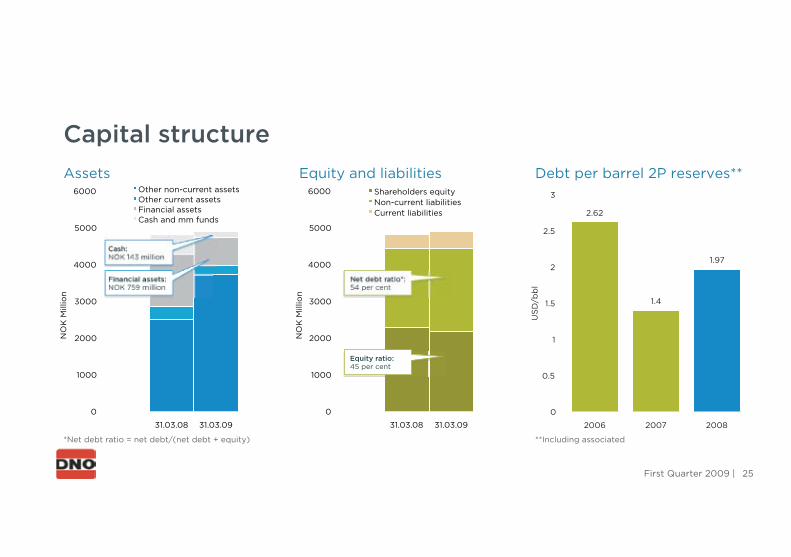

31.03.08 31.03.09

NO

K M

illio

n

Other non-current assets Other current assets Financial assets Cash and mm funds

2.62

1.4

1.97

0

0.5

1

1.5

2

2.5

3

2006 2007 2008

US

D/b

bl

Equity and liabilities

0

1000

2000

3000

4000

5000

6000

31.03.08 31.03.09

NO

K M

illio

n

Shareholders equity Non-current liabilities Current liabilities

Capital structure Assets Debt per barrel 2P reserves**

First Quarter 2009 | 25

Cash: NOK 143 million

Financial assets: NOK 759 million

Net debt ratio*: 54 per cent

Equity ratio: 45 per cent

*Net debt ratio = net debt/(net debt + equity) **Including associated

Summary and closing remarks • Through successful technical completion and pipeline tie-in, the Tawke field is ready for

increased production from a strong proved and developed reserve base

• Preparations for commencement of crude oil export from Tawke on 1 June

• First quarter results affected by lower oil prices and production

• Several measures taken to maintain financial capacity, additional funding options are available

• Limited long-term capital commitments, significantly lower investment levels in 2009

First Quarter 2009 | 26

DISCLAIMER This Presentation includes and is based, inter alia, on forward-looking information and statements that are subject to risks and uncertainties that could cause actual results to differ. These statements and this Presentation are based on current expectations, estimates and projections about global economic conditions, the economic conditions of the regions and industries that are major markets for DNO International ASA and DNO International ASA’s (including subsidiaries and affiliates) lines of business. These expectations, estimates and projections are generally identifiable by statements containing words such as ”expects”, ”believes”, ”estimates” or similar expressions. Important factors that could cause actual results to differ materially from those expectations include, among others, economic and market conditions in the geographic areas and industries that are or will be major markets for DNO’s businesses, oil prices, market acceptance of new products and services, changes in governmental regulations, interest rates, fluctuations in currency exchange rates and such other factors as may be discussed from time to time in the Presentation. Although DNO International ASA believes that its expectations and the Presentation are based upon reasonable assumptions, it can give no assurance that those expectations will be achieved or that the actual results will be as set out in the Presentation. DNO International ASA is making no representation or warranty, expressed or implied, as to the accuracy, reliability or completeness of the Presentation, and neither DNO International ASA nor any of its directors, officers or employees will have any liability to you or any other persons resulting from your use.

This presentation was prepared for the presentation at the First Quarter 2009 results presentation, May 13, 2009. Information contained within will not be updated. The following slides should be read and considered in connection with the information given orally during the presentation.

First Quarter 2009 | 28

SeCOND QUarter 2009: 19 aUGUSt 2009

WeLCoMe BaCK

Dno internationaL asa, stranDen 1, aKer Brygge, 0250 osLo, norWay, Phone: (+47) 23 23 84 80, Fax: (+47) 23 23 84 81