POINTE COUPEE PARISH. LOUISIANA POLICE JURY (PRIMARY GOVERNMENT) ANNUAL FINANCIAL STATEMENTS WITH SUPPLEMENTAL INFORMATION SCHEDULES AS OF DECEMBER 31,2004 AND FOR THE YEAR THEN ENDED Under provisions of state law, this report is a public document. A copy of the report has been submitted to the entity and other appropriate public officials. The report is available for public inspection at the Baton Rouge office of the Legislative Auditor and, where appropriate, at the office of the parish clerk of court. Release Date O

AS OF DECEMBER 31,2004 AND FOR THE YEAR THEN ENDED

Under provisions of state law, this report is a publicdocument. A copy of the report has been submitted tothe entity and other appropriate public officials. Thereport is available for public inspection at the BatonRouge office of the Legislative Auditor and, whereappropriate, at the office of the parish clerk of court.

Owen J. Bello, PresidentMelanie Bueche, Vice President

Gerry BattleyJoseph Bergeron, Sr,

Albert DukesClement GuidrozDudley JarreauClifford Nelson

John R. PourciauMix F. VosburgJuliet WilliamsRussell Young

SECRETARY-TREASURERDavid Cifreo

MEETING DATES

2nd and 4th Tuesday of Every Month5:00 PM - Police Jury Office

TABLE OF CONTENTS

Independent Auditor's Report 1

Required Supplemental Information (Part I)

Management's Discussion and Analysis (omitted)

Basic Financial Statements:

Government-Wide Financial Statements -

Statement of Net Assets 5Statement of Activities 6

Fund Financial Statements -

Governmental Funds -

Balance Sheet 9

Statement of Revenues, Expenditures, and Changes in Fund Balances , 10

Proprietary Funds -

Statement of Net Assets 12

Statement of Revenues, Expenses and Changes in Fund Net Assets 14

Statement of Cash Flows 16

Fiduciary Funds -

Statement of Fiduciary Net Assets 20

Notes to the Financial Statements 21

Required Supplemental Information (Part II)

Budget Comparison Schedule 43

Other Supplemental Schedule

Schedule of Expenditures of Federal Awards 44

Other Reports

Independent Auditor's Report on Compliance and Internal Control Over Financial Reporting

Based on an Audit of Financial Statements Performed in Accordance with Governmental

Auditing Standards 47

Independent Auditor's Report on Compliance with Requirements Applicable to Each Major

Program and Internal Control Over Compliance in Accordance with OMB Circular A-133 49

Schedule of Findings and Questioned Costs 51

Status of Prior Year Audit Findings 53

Management's Corrective Action Plan 54

<jr.CERTIFIED PUBLIC ACCOUNTANT

(A Professional Corporation)Practice Limited to Governmental Accounting, Auditing and Financial Reporting

Phone Office MemberOFFICE (225) 937-9735 7663 ANCHOR DRIVE AMERICAN INSTITUTE OF CPAs

FAX (225) 638-3669 VENTRESS, IA 70783-4120 LOUISIANA SOCIETY OF CPAsE-mail [email protected] GOVERNMENT FINANCE

OFFICERS ASSOCIATION

INDEPENDENT AUDITOR'S REPORT

Members of the Police JuryPointe Coupee Parish, Louisiana

I have audited the accompanying primary government financial statements of POINTE COUPEE PARISH, LOUISI-ANA, Louisiana, as of and for the year ended December 31, 2004, as listed in the Table of Contents. Thesefinancial statements are the responsibility of the Pointe Coupee Parish Police Jury's management. My responsibil-ity is to express an opinion on these primary government financial statements based on my audit.

I conducted my audit in accordance with auditing standards generally accepted in the United States of Americaand the standards applicable to financial audits contained in Government Auditing Standards, issued by theComptroller General of the United States; the provisions of Office of Management and Budget Circular A-133,Audits of States, Local Governments, and Non-Profit Organizations; and with provisions of Louisiana RevisedStatute 24:513 and the provisions of the Louisiana Governmental Audit Guide, published jointly by the Society ofLouisiana Certified Public Accountants and the Louisiana Legislative Auditor. Those standards, OMB Circular A-133, and the Guide require that I plan and perform the audit to obtain reasonable assurance about whether thefinancial statements are free of material misstatement. An audit includes examining, on a test basis, evidencesupporting the amounts and disclosures in the financial statements. An audit also includes assessing the account-ing principles used and significant estimates made by management, as well as evaluating the overall financialstatement presentation. I believe that my audit provides a reasonable basis for my opinion.

The primary government financial statements referred to above do not include depreciation expense for itsgovernmental activities, which should be included to conform with generally accepted accounting principles. Anestimate of the effect on assets, net assets, and expenses can not be reasonably estimated.

A primary government is a legal entity or body politic and includes all funds, organizations, institutions, agencies,departments, and offices that are not legally separate. Such legally separate entities are referred to as componentunits. In my opinion, the primary government financial statements present fairly, in all material respects, thefinancial position of the primary government of Pointe Coupee Parish, Louisiana, as of December 31, 2004, andthe results of its operations and cash flows of its proprietary fund types for the year then ended in conformity withaccounting principles generally accepted in the United States of America.

However, the primary government financial statements, because they do not include the financial data of compo-nent units of Pointe Coupee Parish, Louisiana, do not purport to, and do not, present fairly the financial positionof Pointe Coupee Parish, Louisiana, as of December 31, 2004, and the results of its operations and cash flows ofits proprietary funds for the year then ended in conformity with accounting principles generally accepted in theUnited States of America.

In my opinion, except for the omission of depreciation expense for governmental activities that cannot bereasonably estimated, the primary government financial statements referred to in the first paragraph present fairly,in all material respects, the financial position of Pointe Coupee Parish, Louisiana as of December 31, 2004, and

the results of its operations and the cash flows of its proprietary funds for the year then ended in conformity withaccounting principles generally accepted in the United States of America.

Management failed to provide "Management's Discussion and Analysis" which is required supplemental informat-ion under GASB 34.

My audit was performed for the purpose of forming an opinion on the primary government financial statementstaken as a whole. The accompanying schedule of expenditures of federal awards on page 49 is presented forpurposes of additional analysis as required by U.S. Office of Management and Budget Circular A-133, Audits ofStates, Local Governments, and Non-Profit Organizations, and the other supplemental information listed in thetable of contents are not a required part of the primary government financial statements of the Pointe CoupeeParish Police Jury, Louisiana. Such information has been subjected to the auditing procedures applied in theaudit of the primary government financial statements and, in my opinion, is fairly stated, in all material respects,in relation to the primary government financial statements taken as a whole.

In accordance with Government Auditing Standards, I have also issued my report dated June 29, 2005, on myconsideration of Pointe Coupee Parish Police Jury's internal control over financial reporting and my tests of itscompliance with certain laws, regulations, contracts and grants. That report is an integral part of an auditperformed in accordance with Government Auditing Standards and should be read in conjunction with thisreport in considering the results of my audit.

June 29, 2005

Basic Financial Statements

The basic financial statements include integrated sets of financial statements as required by the Govern-mental Accounting Standards Board (GASB). The sets of statements include:

• Government-wide financial statements

• Fund financial statements

- Governmental funds

- Proprietary (enterprise) fund

- Fiduciary funds

In addition, the notes to the financial statements are included to provide information that is essential to auser's understanding of the basic financial statements.

THIS PAGE INTENTIONALLY LEFT BLANK

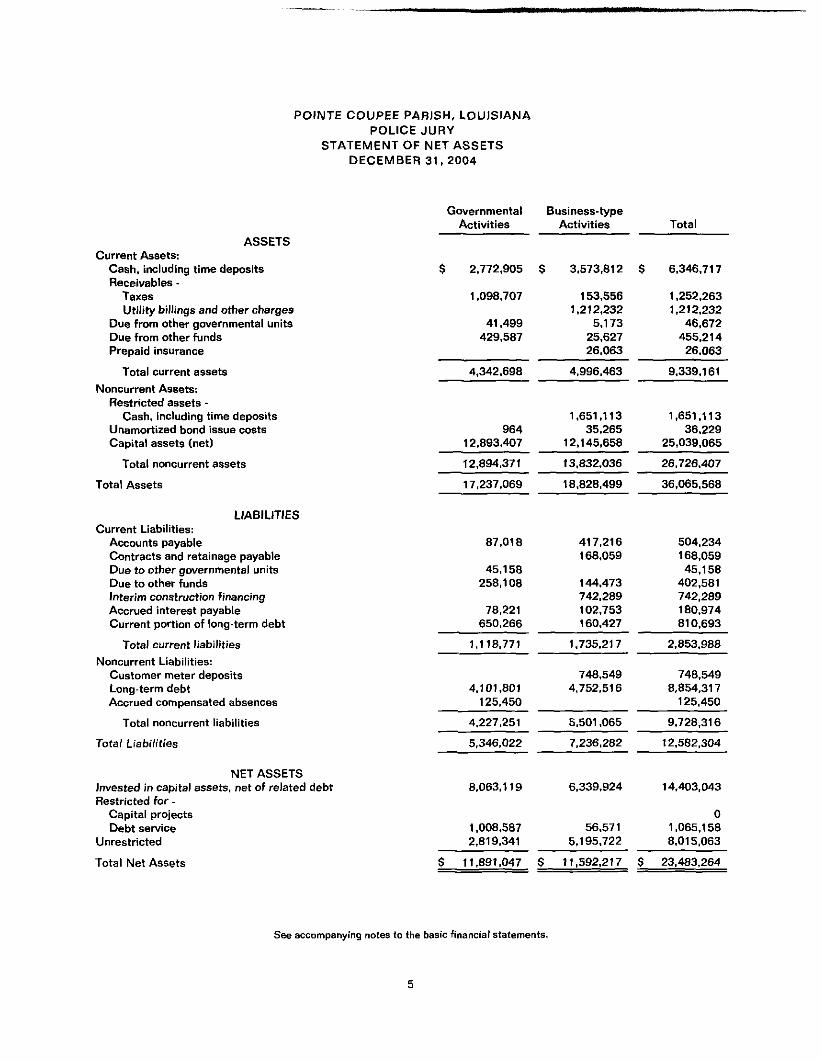

POINTE COUPEE PARISH, LOUISIANAPOLICE JURY

STATEMENT OF NET ASSETSDECEMBER 31,2004

ASSETSCurrent Assets:

Cash, including time depositsReceivables -

TaxesUtility billings and other charges

Due from other governmental unitsDue from other fundsPrepaid insurance

Total current assetsNoncurrent Assets:

Restricted assets -Cash, including time deposits

Unamortized bond issue costsCapital assets (net)

Total noncurrent assets

Total Assets

LIABILITIESCurrent Liabilities:

Accounts payableContracts and retainage payableDue to other governmental unitsDue to other fundsInterim construction financingAccrued interest payableCurrent portion of long-term debt

Total current liabilitiesNoncurrent Liabilities:

Customer meter depositsLong-term debtAccrued compensated absences

Total noncurrent liabilities

Total Liabilities

NET ASSETSInvested in capital assets, net of related debtRestricted for -

Capital projectsDebt service

Unrestricted

Total Net Assets

GovernmentalActivities

$ 2,772,905

1 ,098,707

41 ,499429,587

4,342,698

96412,893,407

12,894,371

17,237.069

87,018

45,158258,108

78,221650,266

1,118,771

4,101,8011 25,450

4,227,251

5,346,022

8,063,119

1,008,5872,819,341

$ 11,891.047

Business-typeActivities

$ 3,573,812 $

153,5561,212,232

5,17325,62726,063

4,996,463

1,651,11335,265

12,145,658

13,832,036

18,828,499

417,216168,059

144,473742,289102,753160,427

1,735,217

748,5494,752,516

5,501 .065

7,236,282

6,339,924

56.5715,195,722

$ 11,592,217 $

Total

6,346,71 7

1 .252,2631,212.232

46,672455,21426.063

9.339.1 61

1,651,11336,229

25,039.065

26,726.407

36,065,568

504,234168,05945,158

402,581742,289180,97481 0,693

2,853,988

748,5498,854,317

125,450

9,728,316

12,582,304

14,403,043

01 ,065,1 588,015,063

23,483,264

See accompanying notes to the basic financial statements.

POINTE COUPEE PARISH, LOUISIANA

POLICE JURYSTATEMENT OF ACTIVITIES

YEAR ENDED DECEMBER 31, 2004

Program Revenues

Functions/Programs

Governmental Activities:General governmentPublic safetyHighways and streetsWelfareCulture and recreationConservationEconomic developmentUnallocated interest & other charges

See accompanying notes to the basic financial statements.

POINTE COUPEE PARISH, LOUISIANAPOLICE JURY

STATEMENT OF ACTIVITIES

YEAR ENDED DECEMBER 31. 2004

Change in Net Assets:

Net (Expense)/Revenue

General revenues:Taxes:

Property taxes, levied for general operationsProperty taxes, levied for debt serviceSales and use taxesFranchise and public service taxesHotel/Motel taxes

IntergovernmentalInvestment incomeMiscellaneous

Transfers

Total General Revenues and Transfers

GovernmentalActivities

Business-typeActivities Total

$ (4,568,605) $ (1,853.459) $ (6,422,064)

2,270,948

1 ,093,475

39,71027,887

1,412,78446,834760,292(195,850)

170,665438,484

48,574

195,850

2,270,948170,665

1,531,95939,71027,887

1,412,78495,408

760,2920

5,456,080 853,573 6,309,653

Change in Net Assets

Net Assets - Beginning

Net Assets - Ending

887,475

11,003,572

(999,886)

12,592,103(112,411)

23,595,675

$ 11,891,047 $ 11,592,217 $ 23,483,264

See accompanying notes to the basic financial statements.

THIS PAGE INTENTIONALLY LEFT BLANK

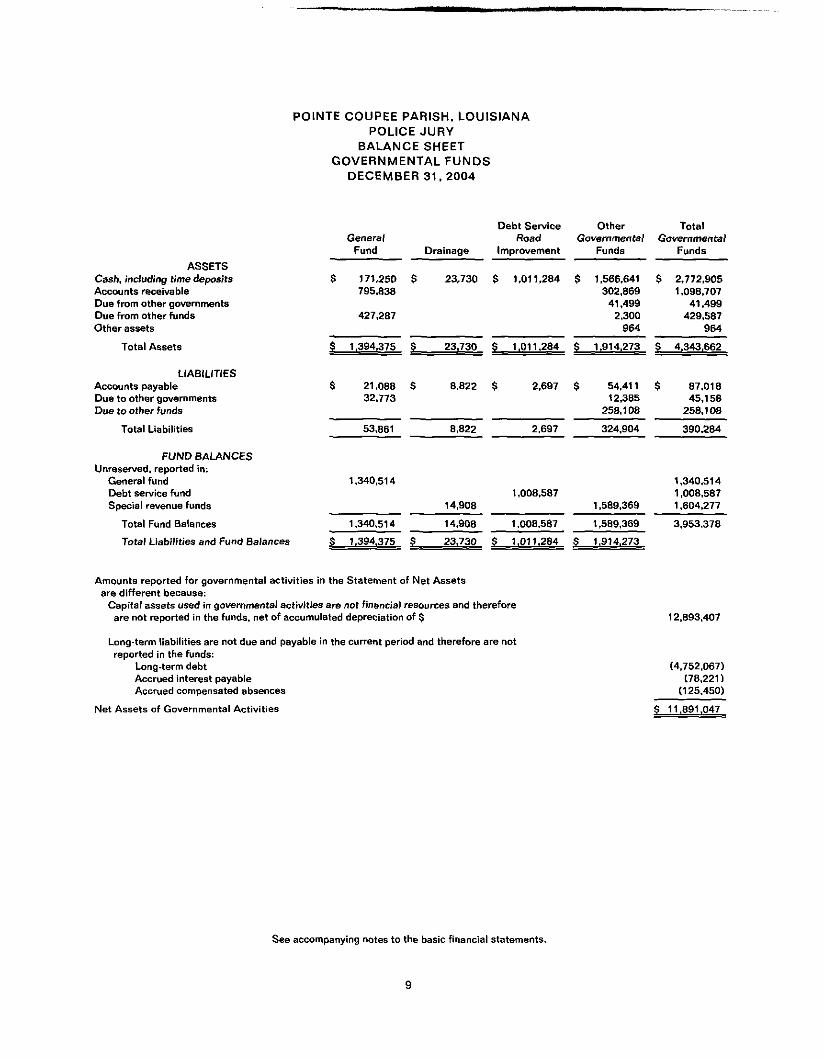

POINTE COUPEE PARISH, LOUISIANAPOLICE JURY

BALANCE SHEETGOVERNMENTAL FUNDS

DECEMBER 31.2004

ASSETSCash, including time depositsAccounts receivableDue from other governmentsDue from other fundsOther assets

Total Assets

LIABILITIESAccounts payableDue to other governmentsDue to other funds

Total Liabilities

FUND BALANCESUnreserved, reported in:

General fundDebt service fundSpecial revenue funds

Total Fund Balances

Total Liabilities and Fund Balances

Debt ServiceGeneral Road

Fund Drainage Improvement

$ 1 71 ,250 $ 23,730 $ 1 ,01 1 ,284795,838

427,287

$ 1.394,375 $ 23,730 $ 1.011,284

$ 21,088 $ 8,822 $ 2,69732,773

53,861 8,822 2,697

1,340,5141,008,587

14,908

1 ,340,514 1 4,908 1 ,008,587

S 1 ,394.375 S 23.730 $ 1 .01 1 .284

OtherGovernmental

Funds

$ 1 ,566,641302,869

41,4992,300

964

$ 1,914,273

$ 54,41 112,385

258,108

324,904

1 ,589,369

1,589,369

$ 1.914.273

Amounts reported for governmental activities in the Statement of Net Assetsare different because:

Capital assets used in governmental activities are not financial resources and thereforeare not reported in the funds, net of accumulated depreciation of $

Long-term liabilities are not due and payable in the current period and therefore are notreported in the funds:

See accompanying notes to the basic financial statements.

POINTE COUPEE PARISH, LOUISIANAPOLICE JURY

STATEMENT OF REVENUES, EXPENDITURES, AND CHANGES IN FUND BALANCESGOVERNMENTAL FUNDS

YEAR ENDED DECEMBER 31, 2004

RevenuesTaxesIntergovernmentalCharges for servicesFines and forfeituresLicenses and permitsInvestment incomeMiscellaneous

Total Revenues

ExpendituresCurrent -

General governmentPublic safetyHighways and streetsWelfareCulture and recreationConservationEconomic development

Debt service -PrincipalInterest and other charges

Capital outlays

Total Expenditures

Excess (Deficiency) of Revenues overExpenditures

Other Financing Sources (Uses)Bond proceedsTransfers inTransfers out

Total Other Financing Sources (Uses)

Net Change in Fund Balances

Fund Balances - Beginning

Fund Balances - Ending

GeneralFund

$ 816,689995,249

22,629

151,91520,821

366,584

2,373,887

1 ,801 ,574

237,878

2,85239,170

57,098

2.138,572

RoadDrainage Improvement

$ 485,989 $ 1,214,97316,951

161 8,877

503,101 1.223,850

979,546

597,191

425,000148,415

83,260

680,451 1,552.961

GovernmentalActivities

$ 914,369503,121

77,228118.030

16,97585,012

1,714,735

25,574594,733578,1221 1 1 ,337

448,847

46,882

96,96419,435

185,503

2,107,397

GovernmentalActivities

$ 3,432,0201,515,321

99,857118,030151.91546.834

451,596

5,815,573

1,827,148832,61 1

1,557,668114,189488,017597,191103,980

521 ,964

167,850268,763

6,479,381

235,315 (177,350) (329,111) (392,662) (663,808)

293,696(992,573)

(698,877)

(463,562)

1 ,804,076

$ 1,340,514 $

1 78,000

178,000

650

14,258

14,908

(50,000)

(50,000)

(379,111)

1 ,387,698

$ 1,008,587 $

293.696823,723

(433,696)

683,723

291.061

1 ,298,308

1,589,369

293,6961,295,419

(1 .476.269)

112,846

(550,962)

4,504,340

$ 3,953,378

See accompanying notes to the basic financial statements.

10

POINTE COUPEE PARISH, LOUISIANAPOLICE JURY

STATEMENT OF REVENUES, EXPENDITURES, AND CHANGES IN FUND BALANCESGOVERNMENTAL FUNDS

YEAR ENDED DECEMBER 31, 2004

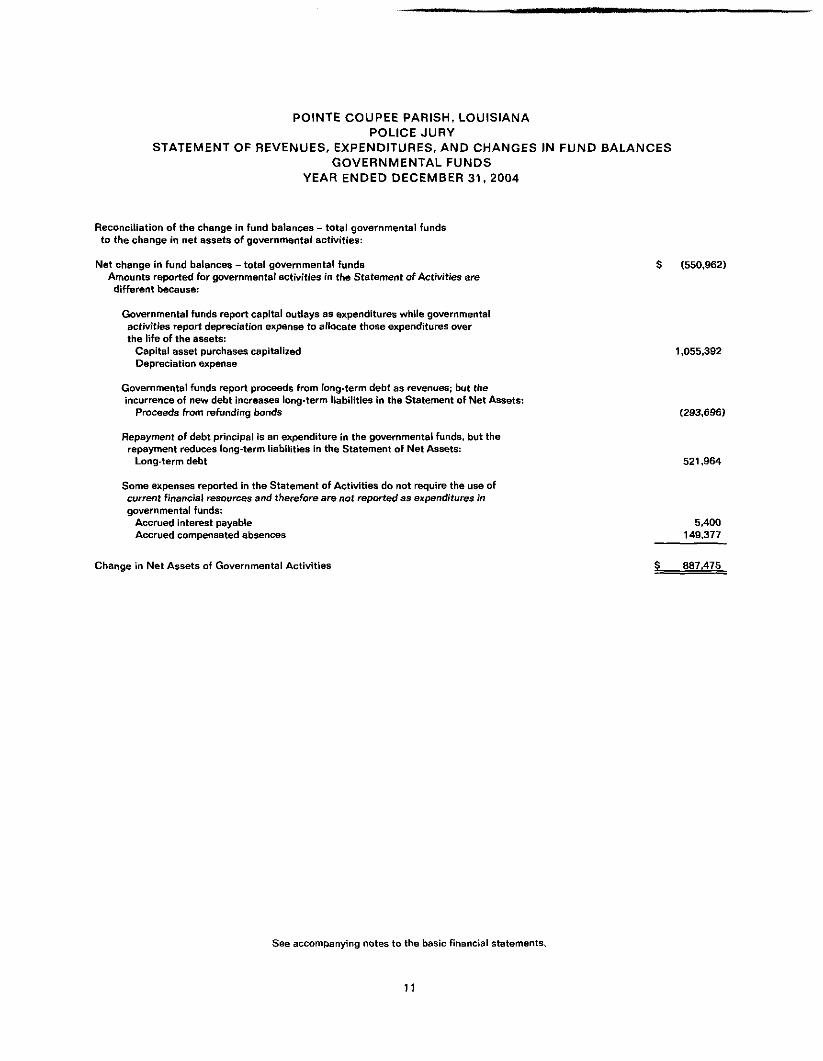

Reconciliation of the change in fund balances - total governmental fundsto the change in net assets of governmental activities:

Net change in fund balances - total governmental funds $ (550,962)Amounts reported for governmental activities in the Statement of Activities aredifferent because:

Governmental funds report capital outlays as expenditures while governmentalactivities report depreciation expense to allocate those expenditures overthe life of the assets:

Capital asset purchases capitalized 1,055,392Depreciation expense

Governmental funds report proceeds from long-term debt as revenues; but theincurrence of new debt increases long-term liabilities in the Statement of Net Assets:

Proceeds from refunding bonds (293,696)

Repayment of debt principal is an expenditure in the governmental funds, but therepayment reduces long-term liabilities in the Statement of Net Assets:

Long-term debt 521,964

Some expenses reported in the Statement of Activities do not require the use ofcurrent financial resources and therefore are not reported as expenditures ingovernmental funds:

Change in Net Assets of Governmental Activities $ 887,475

See accompanying notes to the basic financial statements,

11

POINTE COUPEE PARISH, LOUISIANAPOLICE JURY

STATEMENT OF NET ASSETSPROPRIETARY FUNDSDECEMBER 31, 2004

ASSETSCurrent Assets:

Cash, including time depositsAccounts receivable - taxesAccounts receivable - utility billings and other chargesDue from other governmental unitsDue from other fundsPrepaid insurance

Total Current Assets

Noncurrent Assets:Restricted assets -

Cash, including time depositsUna mortized bond issue costsCapital assets, net

Total Noncurrent Assets

Total Assets

LIABILITIESCurrent Liabilities:

Accounts payableContracts and retainage payableDue to other fundsInterim construction financingAccrued interest payableCurrent portion of long-term debt

Total Current Liabilities

Noncurrent Liabilities:Consumer meter deposits payableLong-term debt

Total Noncurrent Liabilities

Total Liabilities

NET ASSETSInvested in capital assets, net of related debtRestricted for debt serviceUnrestricted

Total Net Assets

Business-type Activities

NaturalGas

System

$ 651 ,896

135,211

2,077

789,184

441,179

885,493

1 ,326,672

2,115,856

125,615

1 2,40449,083

187.102

283,41 7724,654

1,008,071

1,195,173

1 1 1 ,756

808,927

$ 920,683

GasUtility

District 2

$ 1,183,104

224,584

25,6272,271

1 ,435,586

405,494

377,894

783,388

2,218,974

163,490

163,490

310,198

310,198

473,688

377,894

1,367,392

$ 1,745,286

WaterworksDistrict 1

$ 53,49775,42147,836

3,706

180,460

525,31314,931

1 ,282,933

1,823,177

2,003,637

2,084

21 ,54428,842

52,470

101,2191.418,999

1,520,218

1 ,572,688

(164,908)

595,857

$ 430,949

See accompanying notes to the basic financial statements.

12

POINTE COUPEE PARISH, LOUISIANA

POLICE JURY

STATEMENT OF NET ASSETS

PROPRIETARY FUNDS

DECEMBER 31, 2004

Business-type Activities

WaterworksDistrict 2

$ 178,618 $

68,646

3,684

250,948

1 88,42520,334

6,237,773

6,445,932

6,696,880

6,993168,05987,000

742,28922,67041 ,291

1 ,068,302

53,7151 ,331 ,303

1,385,018

2,453,320

3,970,08556,571

216,904

$ 4,243,560 $

SolidWaste

1,063,639

646,81 3

1,710,452

77,132

77,132

t ,787,584

1 1 2,548

15,729

128,277

0

128,277

77,132

1,582,175

1 ,659,307

SewerDistrict 1

$ 120,17975,18752,0365,173

3,160

255,735

55,502

1,184,787

1 ,240,289

1,496,024

2,955

2,300

9,83828,145

43,238

583,970

583,970

627,208

572,673

296,143

$ 868,816

Multi-UseCenter

$ 908

908

35,200

862,61 6

897,816

898,724

619

33,49812,089

46,206

641 ,678

641 ,678

687,884

210,551

289

$ 210,840

NonmajorEnterprise

Funds

$ 321,971 $2,948

37,106

11,165

373,190

1 ,237,630

1,237,630

1,610,820

2,912

39,444

2,799977

46,132

51,912

51,912

98,044

1,184,741

328,035

$ 1,512,776 $

Totals

3,573,8121 53,556

1,212,2325,173

25,62726,063

4,996,463

1,651.11335,265

12,145,658

1 3,832,036

1 8,828,499

417,216168,059144,473742,289102,753160,427

1,735,217

748,5494,752,516

5,501 ,065

7,236,282

6,339,92456,571

5,195,722

11,592,217

See accompanying notes to the basic financial statements.

13

POINTE COUPEE PARISH, LOUISIANAPOLICE JURY

STATEMENT OF REVENUES, EXPENSES. AND CHANGES IN FUND NET ASSETSPROPRIETARY FUNDS

YEAR ENDED DECEMBER 31, 2004

Operating RevenuesCharges for services -

Gas chargesWater chargesSewer chargesSolid waste chargesUser fees and leasesPenalties

Total Operating Revenues

Operating ExpensesSalaries and benefitsAdministrative costsProfessional and technical servicesUtilitiesSolid waste disposal feeNatural gas purchasesInsuranceRepairs, maintenance and suppliesDepreciation

Total Operating Expenses

Operating Income (Loss)

Nonoperating Revenues (Expenses)Ad valorem taxes, net of and revenue sharingSales taxesInvestment incomeGrants receivedUncollectible accountsInterest on long-term debt and other chargesAmortization of bond costs

Total Nonoperating Revenues (Expenses)

Net Income (Loss) Before Contributions and Transfers

Operating transfers in

Net Income (Loss)

Net Assets - Beginning of Year

Net Assets - End of Year

Business-type Activities

NaturalGas

System

$ 841,572 $

31 ,683

873,255

158,184

20,7162,254

526,3331 1 ,030

109.65299,550

927,719

(54,464)

10,496

(393,320)(52,477)

(435,301 )

(489,765)

(489,765)

1,410,448

$ 920,683 $

GasUtility

District 2

1.119,014

42,392

1,161,406

162,2911,825

20,771498

728,5831 1 ,83594,24352,591

1 ,072,637

88,769

1 5,597

(311,042)

(295,445)

(206,676)

50,000

(156,676)

1 ,901 ,962

1 ,745,286

WaterworksDistrict 1

$ 223,316

8,854

232,170

78,6264,2411,9908,869

4,09130,07439,145

1 67,036

65,134

90,402

6,085

(50,147)(101,270)

(686)

(55,616)

9,518

9,518

421,431

$ 430,949

accompanying notes to the basic financial statements.

14

POINTE COUPEE PARISH, LOUISIANAPOLICE JURY

STATEMENT OF REVENUES, EXPENSES, AND CHANGES IN FUND NET ASSETSPROPRIETARY FUNDS

YEAR ENDED DECEMBER 31, 2004

Business-type Activities

WaterworksDistrict 2

$ 301,209

$

11,621

312,830

96,7941 1 ,4064,452

17,039

4,22163,034

1 70,688

367,634

(54,804)

2,565

(87,308)(68,91 6)

(60)

(153,719)

(208,523)

(208,523)

4,452,083

$ 4,243,560 $

SolidWaste

$811,247

33,602

844,849

22,474

1 1 ,391

1,116,594

1 1 1 ,39113,500

1 ,275,350

(430,501)

438,4849,879

(152,054)

296,309

(134,192)

(134,192)

1 ,793,499

1 ,659,307 $

SewerDistrict 1

103,440

$

1 03.440

23,151

1 0,84010,010

5,84446,64739,853

136,345

(32,905)

77,298

1,101

(41 ,460)(30,582)

6,357

(26,548)

(26,548)

895,364

868,816 $

Multi-UseCenter

$

10,641

10,641

44,21 9

1 1 ,334

10,41628,828

94,797

(84,156)

153

(34.370)

(34,217)

(1 1 8,373)

1 1 1 .850

(6,523)

217,363

210,840 $

NonmajorEnterprise

Funds

$

81 ,323

1 04,379

185,702

100,845900

5,39112,244

23,81290,63041,159

274,981

(89,279)

2,965

2,69866,600

(770)(3,391)

68,102

(21,177)

34,000

12,823

1 ,499,953

1,512,776 $

Totals

1 ,960,586524.525184,76381 1 ,2471 1 5,020128,152

3,724,293

686,5841 8,37275,55162,248

1,116,5941,254,916

60,833556,087485,314

4,316,499

(592,206)

1 70,665438,48448,57466,600

(1.036,101)(291,006)

(746)

(603,530)

(1,195,736)

195.850

(999,886)

12,592,103

11.592,217

See accompanying notes to the basic financial statements.

15

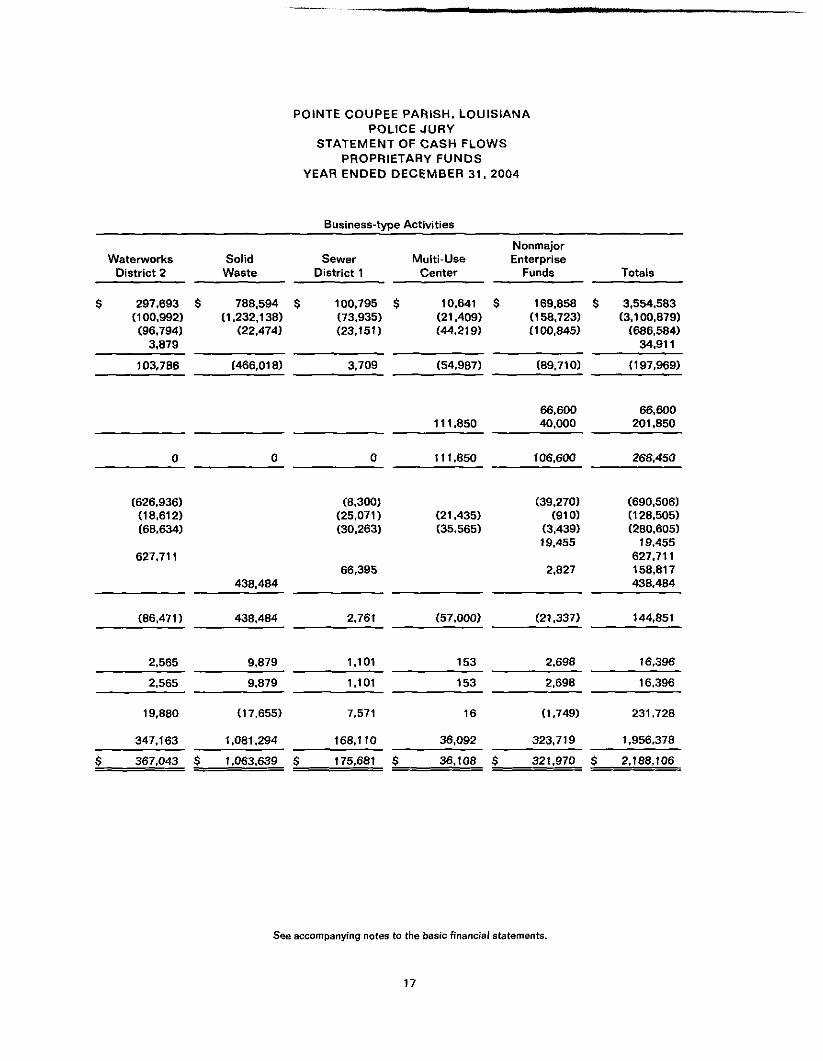

POINTE COUPEE PARISH, LOUISIANAPOLICE JURY

STATEMENT OF CASH FLOWSPROPRIETARY FUNDS

YEAR ENDED DECEMBER 31, 2004

Business-type Activities

Cash Flows from Operating ActivitiesReceipts from customersPayments to suppliersPayments to employees and benefitsReceipts of consumer meter deposits

Net Cash Provided (Used) by Operating Activities

Cash Flows from Noncapital Financing ActivitiesOperating grantsOperating transfers to other funds

Net Cash Provided (Used) by Noncapital FinancingActivities

Cash Flows from Capital and Related Financing ActivitiesAcquisition of capital assetsPrincipal paid on capital debtInterest paid on capital debtProceeds from construction grantsProceeds from construction loansAd valorem and shared taxes received, netSales taxes

Net Cash Provided (Used) by Capital andRelated Financing Activities

Cash Flows from Investing ActivitiesInvestment income

Net Cash Provided (Used) by Investing Activities

Net Increase (Decrease) in Cash and Cash Equivalents

Balances - Beginning of Year

Balances - End of Year

NaturalGas

System

GasUtility

District 2Waterworks

District 1

853,069(635,323)(158,184)

12,781

72,343

(8,000)(30,336)(43,464)

(81,800)

1,107,969(827,657)(162,291)

13,119

131,140

50,000

50,000

(8,000)

(8,000)

225,964(50,702)(78,626)

5,132

101.768

(32,141)(99,240)

89,595

(41,786)

$

1 0.496

10,496

1,039

1 ,092,036

1 ,093,075 $

15,597

15,597

188.737

1 .399,861

1 ,588,598 $

6,085

6,085

66,067

512,742

578,809

See accompanying notes to the basic financial statements.

16

POINTE COUPEE PARISH, LOUISIANAPOLICE JURY

STATEMENT OF CASH FLOWSPROPRIETARY FUNDS

YEAR ENDED DECEMBER 31. 2004

Business-type Activities

WaterworksDistrict 2

$ 297,693 $(100,992)(96,794)

3,879

1 03,786

0

(626,936)(18,612)(68,634)

627.711

(86,471)

Solid SewerWaste District 1

788,594 $ 100,795 $(1,232,138) (73,935)

(22,474) (23,151)

(466,018) 3,709

0 0

(8,300)(25,071)(30,263)

66,395438,484

438,484 2,761

Multi-UseCenter

1 0,641(21 ,409)(44,219)

(54,987)

111,850

1 1 1 ,850

(21 ,435)(35,565)

(57,000)

NonmajorEnterprise

Funds

$ 1 69,858 $(158,723)(100,845)

(89,710)

66,60040,000

106,600

(39,270)(910)

(3,439)19,455

2,827

(21,337)

Totals

3,554,583(3,100,879)

(686,584)34,91 1

(197,969)

66,600201 ,850

268,450

(690,506)(128,505)(280,605)

19,455627,711158,817438,484

144,851

2,565

2.565

19,880

347,163

9,879

9.879

(17,655)

1,081,294

367,043 $ 1.063,639 $

1.101

1.101

7,571

166.1 tO

175.681 $

153

153

16

36,092

36,108 $

2.69S

2.698

(1,749)

323,719

16,396

16.396

231,728

1,956,378

321,970 $ 2,188,106

See accompanying notes to the basic financial statements.

17

POINTE COUPEE PARISH, LOUISIANAPOLICE JURY

STATEMENT OF CASH FLOWSPROPRIETARY FUNDS

YEAR ENDED DECEMBER 31, 2004

Business-type Activities

NaturalGas

System

GasUtility

District 2WaterworksDistrict 1

Reconciliation of Operating Income (Loss) to Net CashProvided (Used) by Operating ActivitiesOperating income (loss)

Adjustments to reconcile operating income to net cashprovided (used) by operating activities -

Cash flows reported in other categories -Depreciation expense

Decrease (increase) in assets -Receivables, netDue from other governmental unitsPrepaid insurance

Increase (decrease) in liabilities -Accounts payableConsumer meter deposits

Balances - End of Year

(54,464) $ 88.769 $ 65,134

$

99,549

(20.186)

354

34,30912,781

72,343 $

52,591

(53,437)

159

29,93913,119

131,140 $

39,145

(6.207)

(2.259)

8235,132

101,768

See accompanying notes to the basic financial statements.

See accompanying notes to the basic financial statements.

19

POINTE COUPEE PARISH, LOUISIANAPOLICE JURY

STATEMENT OF NET ASSETSFIDUCIARY FUNDS

DECEMBER 31, 2004

AgencyFunds

ASSETSCash, including time deposits $ 254,150

Total Assets $ 254.150=======

LIABILITIESTaxes paid under protest $ 10,944Due to other governmental units -

Pointe Coupee Parish School Board 174,161City of New Roads 14,517Town of Livonia 1,466Town of Fordoche 82Village of Morganza 347

Due to other funds -General fund 52,633

Total Liabilities $ 254.150

See accompanying notes to the basic financial statements.

20

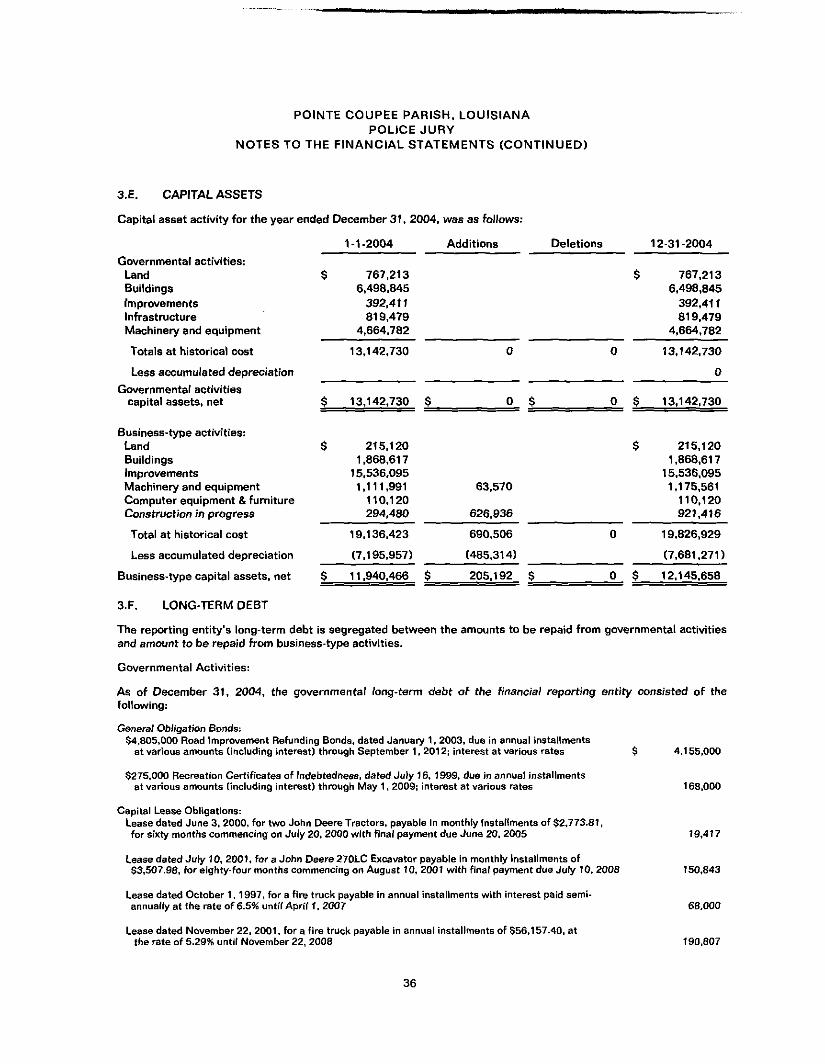

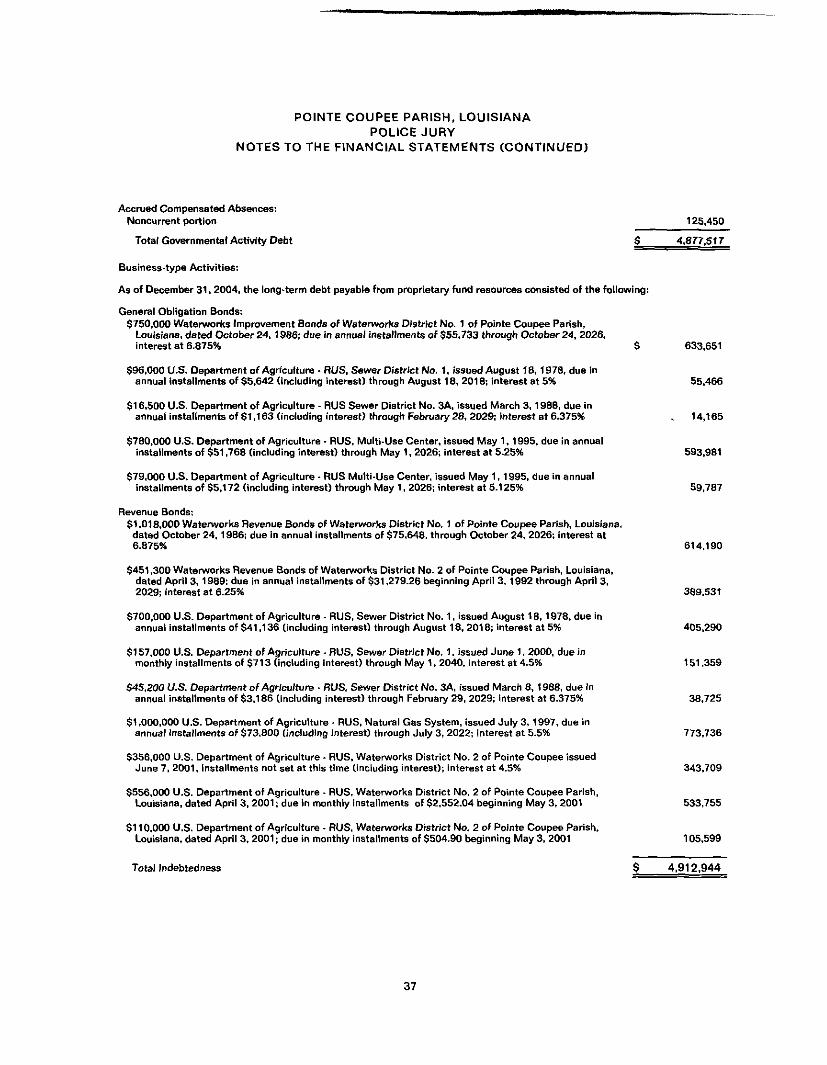

NOTE 1

POINTE COUPEE PARISH, LOUISIANAPOLICE JURY

NOTES TO BASIC FINANCIAL STATEMENTS

INDEX

SUMMARY OF SIGNIFICANT ACCOUNTING POLICIESPage

A. Introduction 22B. Financial Reporting Entity 23C. Basis of Presentation 24D. Measurement Focus and Basis of Accounting 28E. Assets, Liabilities, and Equity 29F. Revenues, Expenditures, and Expenses 31

NOTE 2. STEWARDSHIP, COMPLIANCE, AND ACCOUNTABILITY

A. Fund Accounting Requirements 33B. Deposits and Investments Laws and Regulations 33C. Revenue Restrictions 33D. Debt Restrictions and Covenants 33E. Fund Equity Restrictions 34

NOTE 3. DETAIL NOTES ON TRANSACTION CLASSES/ACCOUNTS

A. Cash and Investments 34B. Restricted Assets 35C. Due From/To Other Governmental Units 35D. Due From/To Other Funds 35

E. Capital Assets 36F. Long-Term Debt 36

NOTE 4. OTHER NOTES

A. Employee Pension and Other Benefit Plans 38B. Post-Retirement Benefits 39C. Risk Management 39D. Estimates 39E. Criminal Court Fund 39F. Utilities Billed By Other Governmental Units 39G. Centralized Collection Agency Agreement 40H. Related Party Transactions 40I. Litigation and Claims 40J. Compensation Paid to Board Members 40

21

POINTE COUPEE PARISH, LOUISIANAPOLICE JURY

NOTES TO THE FINANCIAL STATEMENTS

NOTE 1 - SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

1 .A. INTRODUCTION

The Pointe Coupee Parish Police Jury is the governing authority for Pointe Coupee Parish, Louisiana, and is apolitical subdivision of the State of Louisiana. The Police Jury is governed by twelve jurors representing the variousdistricts within the parish.

The area of Pointe Coupee Parish is 591 square miles and the Police Jury maintains 129 miles of roads. Thepopulation of Pointe Coupee Parish is 22,540 based on the 1990 census and the Police Jury employs approximately70 persons.

The Police Jury, under the provisions of Louisiana Revised Statutes 33:1271-1285, enacts ordinances, sets policyand establishes programs in such fields as social welfare, transportation, drainage, industrial inducement, andhealth services.

Louisiana Revised Statute 33:1236 gives the Police Jury various powers in regulating and directing the affairs ofthe parish and its inhabitants. The more notable of those are the power to make regulations for its own govern-ment; to regulate the construction and maintenance of roads, bridges and drainage; to regulate the sale of alcoholicbeverages; and to provide for the health and welfare of the poor, disadvantaged and unemployed in the parish.Funding to accomplish these tasks is provided by ad valorem taxes, sales taxes, beer and alcoholic beveragepermits, state revenue sharing and various state and federal grants.

In accomplishing its objectives, the Police Jury also has the authority to create special districts (component units)within the parish. The districts perform specialized functions, such as fire protection, library facilities, and healthcare facilities.

The Police Jury complies with generally accepted accounting principles (GAAP). GAAP includes all relevantGovernmental Accounting Standards Board (GASB) pronouncements. In the government-wide financial statementsand the fund financial statements for the proprietary funds. Financial Accounting Standards Board (FASB)pronouncements and Accounting Standards Board (APB) opinions issued on or before November 30, 1989, havebeen applied unless those pronouncements conflict with or contradict GASB pronouncements, in which case, GASBprevails. For enterprise funds, GASB Statement Nos. 20 and 34 provide the Police Jury the option of electing toapply FASB pronouncements issued after November 30, 1989. The Police Jury has elected not to apply thosepronouncements. The accounting and reporting framework and the more significant accounting policies arediscussed in subsequent subsections of this Note.

In June 1999, the Governmental Accounting Standards Board (GASB) unanimously approved Statement No. 34,Basic Financial Statements-and Management's Discussion and Analysis-for State and Local Governments. Certainof the significant changes in the Statement include the following:

• For the first time the financial statements include:

• A Management Discussion and Analysis (MD&A) section providing an analysis of the Police Jury'soverall financial position and results of operations.

• Financial statements prepared using full accrual accounting for all of the Police Jury's activities,including infrastructure (roads, bridges, etc.).

• A change in the fund financial statements to focus on the major funds.

These and other changes are reflected in the accompanying financial statements (including notes to financialstatements). The Police Jury has elected to implement the general provisions of Statements No. 33 and 34 andInterpretation No. 6 in the current year and plans to retroactively report infrastructure (assets acquired prior toJanuary 1, 2002) in the fiscal year ending December 31, 2004.

22

POINTE COUPEE PARISH, LOUISIANAPOLICE JURY

NOTES TO THE FINANCIAL STATEMENTS (CONTINUED)

1 .B. FINANCIAL REPORTING ENTITY

As the governing authority of Pointe Coupee Parish, for reporting purposes, the Pointe Coupee Parish Police Juryis the financial reporting entity for Pointe Coupee Parish. The financial reporting entity consists of [a] the primarygovernment (Police Jury), [b] organizations for which the primary government is financially accountable, and [c]other organizations for which nature and significance of their relationship with the primary government are suchthat exclusion would cause the reporting entity's financial statements to be misleading or incomplete.

GASB Statement No. 14 established criteria for determining the governmental reporting entity and componentunits should be included within the reporting entity. For financial reporting purposes, in conformance with GASBStatement No. 14, the Pointe Coupee Parish Police Jury includes all funds, accounts groups, et cetera, that arewithin the oversight responsibility of the Pointe Coupee Parish Police Jury.

The basic criterion for including a potential component unit within the reporting entity is financial accountability.The GASB has set forth criteria to be considered in determining financial accountability. This criteria includes:

1. Appointing a voting majority of an organization's governing body, and

a. The ability of the Police Jury to impose its will on that organization and/orb. The potential for the organization to provide specific financial benefits to or impose specific

financial burdens on the Police Jury.

2. Organizations for which the Police Jury does not appoint a voting majority but are fiscally dependent onthe Police Jury.

3. Organizations for which the reporting entity financial statements should be misleading if data of theorganization is not included because of the nature or significance of the relationship.

Based on the previous criteria, the Police Jury has determined that the following component units are part of thereporting entity:

Fiscal CriteriaYear End Used

Pointe Coupee Community Advancement, Inc. March 3j 2Pointe Coupee Council on Aging June 30 2Bonne Sante' - Chemical & Well ness Center June 30 1Pointe Coupee Parish Health Service District No. 1 October 31 1Pointe Coupee Parish Nursing Home October 31 1False River Air Park Commission December 31 1False River Recreation Park Commission December 31 1Fire Protection District No. 1 December 31 2Fire Protection District No. 2 December 31 2Fire Protection District No. 3 December 31 2Fire Protection District No. 4 December 31 2Fire Protection District No. 5 December 31 2Pointe Coupee Parish Commission on Tourism December 31 1Pointe Coupee Parish Communication District December 31 1Pointe Coupee Parish Library December 31 1Mosquito Abatement District December 31 1Pointe Coupee Parish Port, Harbor and Terminal District December 31 2Pointe Coupee Parish Poydras Fund December 31 1Pointe Coupee Parish Natural Gas System December 31 1Gas Utility District No. 2 of Pointe Coupee December 31 1Pointe Coupee Parish Waterworks District No. 1 December 31 1Pointe Coupee Parish Waterworks District No. 2 December 31 1Pointe Coupee Parish Sewerage District No. 1 December 31 1Pointe Coupee Parish Sewerage District No. 3A December 31 1

23

POINTE COUPEE PARISH, LOUISIANAPOLICE JURY

NOTES TO THE FINANCIAL STATEMENTS (CONTINUED)

The Police Jury has chosen to issue financial statements of the primary government (Police Jury) only; therefore,have included all funds, account groups, and organizations for which the Police Jury maintains the accountingrecords. Consequently, the following organizations are considered part of the primary government:

False River Recreation Park CommissionFire Protection District No. 1Fire Protection District No. 3

Pointe Coupee Parish Commission on TourismPointe Coupee Parish Communication District

Mosquito Abatement DistrictPointe Coupee Port, Harbor, and Terminal District

Pointe Coupee Parish Natural Gas SystemGas Utility District No. 2 of Pointe Coupee

Pointe Coupee Parish Waterworks District No. 1Pointe Coupee Parish Waterworks District No. 2Pointe Coupee Parish Sewerage District No. 1Pointe Coupee Parish Sewerage District No. 3A

GASB Statement 14 provides for the issuance of primary government financial statements that are separate fromthose of the reporting entity. However, the primary government's (Police Jury) financial statements are not asubstitute for the reporting entity's financial statements. The accompanying primary government financial state-ments have been prepared in conformity with generally accepted accounting principles as applied to governmentalunits. These financial statements are not intended to and do not report on the reporting entity but rather areintended to reflect only the financial statements of the primary government (Police Jury).

It was determined that the following governmental entities are not component units of the Pointe Coupee ParishPolice Jury reporting entity because they have separately elected governing bodies, are legally separate, and arefiscally independent of the Pointe Coupee Parish Police Jury.

Pointe Coupee Parish SheriffPointe Coupee Parish Clerk of CourtPointe Coupee Parish Tax AssessorPointe Coupee Parish School Board

District Attorney of the Eighteenth Judicial DistrictVarious municipalities in Pointe Coupee Parish

1 .C. BASIS OF PRESENTATION

The Police Jury's basic financial statements include both government-wide (reporting the Police Jury as a whole)and fund financial statements (reporting the Police Jury's major funds). Both the government-wide and fundfinancial statements categorize primary activities as either governmental or business type.

Government-wide Financial Statements

The Statement of Net Assets and Statement of Activities display information about the reporting government as a.whole. They include all funds of the reporting entity except for fiduciary funds. The statements distinguishbetween governmental and business-type activities. Governmental activities generally are financed through taxes,intergovernmental revenues, and other nonexchange revenues. Business-type activities are financed in whole or inpart by fees charged to external parties for goods or services.

Fund Financial Statements

Fund financial statements of the reporting entity are organized into funds, each of which is considered to beSeparate accounting entitles. Each fund is accounted for by providing a separate set of self-balancing accounts thatconstitute its assets, liabilities, fund equity, revenues, and expenditures/expenses. Funds are organized into threemajor categories: governmental, proprietary, and fiduciary. An emphasis is placed on major funds within the

24

POINTE COUPEE PARISH, LOUISIANAPOLICE JURY

NOTES TO THE FINANCIAL STATEMENTS (CONTINUED)

governmental and proprietary categories. A fund is considered major if it is the primary operating fund of thePolice Jury or meets the following criteria:

a. Total assets, liabilities, revenues, or expenditures/expenses of that individual governmental or enterprisefund are at least 10 percent of the corresponding total for all funds of that category or type; and

b. Total assets, liabilities, revenues, or expenditures/expenses of the individual governmental fund orenterprise fund are at least 5 percent of the corresponding total for all governmental and enterprise fundscombined.

The funds of the financial reporting entity are described below:

Governmental Funds

General Fund -- The General Fund is the primary operating fund of the Police Jury and always classified as a majorfund. It is used to account for all activities except those legally or administratively required to be accounted for inother funds.

Special Revenue Funds -- Special Revenue Funds are used to account for the proceeds of specific revenue sourcesthat are legally restricted to expenditures for certain purposes.

Debt Service Fund — The Debt Service Fund accounts for the accumulation of financial resources for payment ofinterest and principal on the general long-term debt of the Police Jury other than debt service payments made byenterprise funds. Ad valorem and sales and use taxes are used for the payment of principal and interest on thePolice Jury's judgment.

Capital Projects Fund -- The Capital Projects Fund is used to account for resources restricted for the acquisition orconstruction of specific capital projects or items. The reporting entity includes only one Capital Project Fund and itis used to account for the acquisition of capital assets with transfers made from the General Fund.

Proprietary Fund

Enterprise Funds -- Enterprise funds are used to account for business-like activities provided to the general public.These activities are financed primarily by user charges and the measurement of financial activity focuses on netincome measurement similar to the private sector.

Fiduciary Funds (Not included in government-wide statements)

Agency Funds -- Agency funds account for assets held by the Police Jury on behalf of others as their agent.Agency funds are custodial in nature (assets equal liabilities) and do not involve measurement or results ofoperation. The agency funds are as follows:

Sales Tax Escrow accounts for funds from prior sales tax ordinance dedicated for contingencies.

Sales Tax No. 2 accounts for funds received under the central collection agency agreement of the parish.

Major and Nonmajor Funds

The funds are further classified as major or nonmajor as follows:

Major Funds

General Fund (see above for description)

See above for description.

25

PO1NTE COUPEE PARISH, LOUISIANAPOLICE JURY

NOTES TO THE FINANCIAL STATEMENTS (CONTINUED)

Special Revenue Funds

Parishwide Drainage Fund accounts for routine maintenance of parish drainage facilities. Financing isprovided by transfers from the General Fund and proceeds from the State Revenue Sharing Fund.

Debt Service Fund:

Road Improvement Bond Fund accounts for sales taxes used for the payment of interest and principal on$6,600,000 Road Improvement Bonds, dated September 1, 1997 and excess sales tax collected for theconstruction or overlay of parish streets and roads.

Proprietary Fund:

Pointy Coupee Parish Natural Gas System was originally established to provide gas services to residents inthe Sixth, Seventh, and portions of the Fifth, Eight, and Ninth Wards of Pointe Coupee Parish on May 7, 1952.The System is governed by a board consisting of Police Jury members.

Gas Utility Djstrict No. 2 of Pointe Coupee Parish was established on November 10, 1964, to provide gasservices to residents of portions of the parish as designated in the resolution.

Points Coupee Parish Waterworks District No^ 1 was created on March 24, 1981 through an ordinanceadopted by the Pointe Coupee Parish Police Jury. The District was established to provide water service to theresidents of certain parts of Pointe Coupee Parish, as designated in the resolutions and subsequentamendments to the boundaries. The District is governed by a five member Board of Commissioners, appointedby the Pointe Coupee Parish Police Jury.

Waterworks District No. 2 of the Parish of Pointe Coupee. Louisiana was created on August 25, 1987,through an ordinance adopted by the Pointe Coupee Parish Police Jury as authorized by the provisions ofArticle 6, Section 19 of the 1974 Louisiana Constitution and R.S. 33:3811, et seq. The District was establishedto provide water service to the residents of certain parts of Pointe Coupee Parish, Louisiana, as designated inSection 3 of the Ordinance. The District is governed by a five member Board of Commissioners, appointed bythe Pointe Coupee Parish Police Jury.

Pojnte Coupee Parish Sewerage District No. 1 was created by the Pointe Coupee Parish Police Jury onNovember 11, 1969, as authorized by Louisiana Revised Statute 33:3811. The District is responsible for theconstruction, maintenance, and operation of the sewer and sewerage disposal works within the territorial limitsof the District. The District is governed by a Board of Commissioners consisting of three members appointedby the Pointe Coupee Parish Police Jury.

Pojnte^Coupee Parish SoMd Waste Fund was established by the Pointe Coupee Parish Police Jury to providesolid waste disposal for all residents of the parish. It is funded through user charges and a special sales taxlevy for garbage collection and disposal.

Multi-Use Center accounts for the funds generated by the activities of the parish cultural center.

NonrnaJo^Fu nds

Special Revenue Funds

Insurance Loss Fjjnd accounts for funds set aside by the Police Jury for reimbursement of damagesresponsible of the Police Jury because of insurance deductible or damages not covered by insurance.

Building Majntejtance & Replacement Fimd accounts for funds set aside by the Police Jury for themaintenance and replacement of certain government buildings.

Criminal CourtJund accounts for the receipts of court fees and fines and the disbursements of court costs ofthe 18th Judicial District.

26

POINTE COUPEE PARISH, LOUISIANAPOLICE JURY

NOTES TO THE FINANCIAL STATEMENTS (CONTINUED)

Drainage and Road Equipment Fund accounts for set aside revenues and the expenditures to purchaseequipment.

Fire Protection District No. 1 accounts for the levy of a special millage on property assessments to be used toown, maintain, and operate buildings, machinery, and equipment used in providing fire protection to theproperty in the district.

Fire Protection District No. 3 accounts for the levy of a special millage on property assessments to be used toown. maintain, and operate buildings, machinery, and equipment used in providing fire protection to theproperty in the district.

Detention Center accounts For a special tax levy for the construction, maintenance and operations of the parishjail facility.

Parishwjde Recreation Fund accounts for a special tax levy for recreational parks around the pariah.

Emergency Shelter Grant accounts for assistance to indigent individuals.

Nursing Home Capital Outlay accounts for funds set aside for improvements, repairs and maintenance to theparish nursing home.

Roads and Bridges Fund accounts for the construction of new roads and bridges; also, the maintenance ofexisting roads and bridges. The major sources of financing are provided by the State of Louisiana Parish RoadFund, Parish Royalty Fund and grants from the Louisiana Department of Transportation and Development. Useof the funds is restricted by Louisiana Revised Statute 48:753.

Motor Vejijcle Handljng Fund accounts for the expenditure of funds used to maintain the building used for thestate department of motor vehicles.

Sales Tax Special Fund accounts for the surplus funds remaining from the original 1% sales tax ordinance.

Commission on Tourism accounts for the expenditures of funds used to promote the economic developmentand tourism of the parish.

Economic^Deyelopment Fund accounts for the expenditure of funds to promote economic development in theparish.

Weatherization Jund accounts for the revenue and expenditures of a Department of Social Servicesweatherization grant.

Visitor Enterprise accounts for the revenue and expenditures of enterprise funds received from the state.

Scott Civic Center accounts for the revenues and expenditures of the parish civic center.

Mosquito^Abatement District accounts for funds to control mosquitos in the parish.

Capital Projects Funds:

False River Recreation Park^ Construction accounts for funds designated by the Police Jury for the ongoingconstruction and improvements of the False River Recreation Park.

Proprietary Funds:

Pointe Coupee Parish Sewerage District No. 3A was created by the Pointe Coupee Parish Police Jury onMarch 17, 1987, as authorized by Louisiana Revised Statute 33:3811. The District is responsible for theconstruction, maintenance, and operation of the sewer and sewerage disposal works within the territorial limitsof the District. The District is governed by a Board of Commissioners consisting of three members appointedby the Pointe Coupee Parish Police Jury.

27

POINTE COUPEE PARISH, LOUISIANAPOLICE JURY

NOTES TO THE FINANCIAL STATEMENTS (CONTINUED)

Pointy Coupee PgrtLHarbor. and Terminal District was created by Act No. 23 of the 1967 Regular Session ofthe Louisiana Legislature, Louisiana Revised Statutes 34:2451 et seq., as a political subdivision of the statewith full corporate powers. The territorial limits and territorial jurisdiction of said District shall be the territorycomprising and lying within the limits and boundaries of the Parish of Pointe Coupee, Louisiana. The Districtoperates a port, harbor and terminal facility generating funds from loading and unloading charges, dockagecharges, and lease rentals.

Utility Maintenance accounts for the maintenance of False River Water Works Corp. water system.

Legonier Sewer System an extension of Pointe Coupee Parish Sewerage District No. 1 being accounted for ina separate fund.

1 .D. MEASUREMENT FOCUS AND BASIS OF ACCOUNTING

Measurement focus is a term used to describe "which" transactions are recorded within the various financialstatements. Basis of accounting refers to "when" transactions are recorded regardless of the measurement focusapplied.

Measurement Focus

On the government-wide Statement of Assets and the Statement of Activities, both governmental and business-likeactivities are presented using the economic resources measurement focus as defined in item b. below.

In the fund financial statements, the "current financial resources" measurement focus or the "economic resources"measurement focus is used as appropriate:

a. All governmental funds utilize a "current financial resources" measurement focus. Only current assets andliabilities are generally included on their balance sheets. Their operating statements present sources andused of available spendable financial resources during a given period. These funds use fund balance as theirmeasure of available spendable financial resources at the end of the period.

b. The proprietary fund utilizes an "economic resources" measurement focus. The accounting objectives of thismeasurement focus are the determination of operating income, changes in net assets (or cost recovery),financial position, and cash flows. All assets and liabilities (whether current or noncurrent) associated withtheir activities are reported. Proprietary fund equity is classified as net assets.

c. Agency funds are not involved in the measurement of results of operations; therefore, measurement focus isnot applicable to them.

Basis of Accounting

Basis of accounting refers to the point at which revenues or expenditures/expenses are recognized in the accountsand reported in the financial statements. It relates to the timing of the measurements made regardless of themeasurement focus applied. Basis of Accounting is either "accrual" or "modified accrual" depending upon the typeof type of financial statement or funds.

In the government-wide Statement of Net Assets and Statement of Activities, both governmental and business-likeactivities are presented using the accrual basis of accounting. Under the accrual basis of accounting, revenues arerecognized when earned and expenses are recorded when the liability is incurred or economic asset used, Reve-nues, expenses, gains, losses, assets, and liabilities resulting from exchange and exchange-like transactions arerecognized when the exchange takes place.

In the fund financial statements, governmental funds and agency funds are presented on the modified accrual basisof accounting. Under this modified accrual basis of accounting, revenues are recognized when "measurable andavailable." Measurable means knowing or being able to reasonably estimate the amount. Available meanscollectible within the current period or within sixty days after year end. Expenditures (including capital outlay) arerecorded when the related fund liability is incurred, except for general obligation bond principal and interest whichare reported when due.

28

POINTE COUPEE PARISH, LOUISIANAPOLICE JURY

NOTES TO THE FINANCIAL STATEMENTS (CONTINUED)

All proprietary funds utilize the accrual basis of accounting. Under the accrual basis of accounting, revenues arerecognized when earned and expenses are recorded when the liability is incurred or economic asset used.

I.E. ASSETS, LIABILITIES, AND EQUITY

Cash and Investments

For the purpose of the Statements of Net Assets, "cash, including time deposits" includes all demand deposits andpooled cash accounts of the Police Jury. For the purpose of the proprietary fund Statement of Cash Flows, "cashand cash equivalents" include all demand or short-term investments with an original maturity of 90 days or less.

Investments are carried at fair value based on quoted market price. Additional cash and investment disclosures arepresented in Notes 2.C. and 3.A.

Interfund Receivables and Payables

During the course of operations, numerous transactions occur between individual funds that may result in amountsowed between funds. Those related to goods and service type transactions are classified as "due to and from otherothers". Short-term interfund loans are reported as "interfund receivables and payables." Long-term interfundloans (noncurrent portion) are reported as "advances from and to other funds." Interfund receivables and payablesbetween funds within governmental activities are eliminated in the Statement of Net Assets. See Note 3.G. fordetails of interfund transactions, including receivables and payables at year-end.

Receivables

In the government-wide statements, receivables consist of all revenues earned at year-end and not yet received.Allowances for uncollectible accounts receivable are based upon historical trends and the periodic aging ofaccounts receivable. Major receivable balances for the governmental activities include sales and use taxes,franchise taxes, grants, fines, and reimbursements. Business-type activities report utilities and interest earnings asmajor receivables.

In the fund financial statements, material receivables in governmental funds include revenue accruals such as salestax, franchise tax, and grants and other similar intergovernmental revenues since they are usually both measurableand available. Interest and investment earnings are recorded when earned only if paid within 60 days since theywould be considered both measurable and available. Proprietary fund material receivables consist of all revenuesearned at year-end and not yet received. Utility accounts receivable and interest earnings compose the majority ofproprietary fund receivables. Allowances for uncollectible accounts receivable are based upon historical trends andthe periodic aging of accounts receivable.

Inventories

Inventories for supplies are immaterial and are recorded as expenditures/expenses when purchased.

Restricted Assets

Restricted assets include cash and investments of the proprietary fund that are legally restricted as to their use.The primary restricted assets are related to bond accounts and utility meter deposits.

Fixed Assets

The accounting treatment over property, plant, and equipment (fixed assets) depends on whether the assets areused in governmental fund operations or proprietary fund operations and whether they are reported in thegovernment-wide or fund financial statements.

Government-wide Statements

In the government-wide financial statements, fixed assets are accounted for as capital assets. All fixed assets arevalued at historical cost, or estimated historical cost if actual is unavailable, except for donated fixed assets whichare recorded at their estimated fair value at the date of donation.

29

POINTE COUPEE PARISH, LOUISIANAPOLICE JURY

NOTES TO THE FINANCIAL STATEMENTS (CONTINUED)

Prior to January 1, 2002, governmental funds' infrastructure assets were not capitalized. The Police Jury haselected to delay the retroactive recognition of these costs until a later date because of the complexity of estimatingthe historical cost

Depreciation of all exhaustible fixed assets is recorded as an allocated expense in the Statement of Activities, withaccumulated depreciation reflected in the Statement of Net Assets. Depreciation is provided over the assets'estimated useful lives using the straight-line method of depreciation. The range of estimated useful lives by type ofasset is as follows:

Buildings 5 • 50 YearsImprovements other than buildings 20 - 50 YearsMachinery and equipment 3 - 10 YearsComputer equipment 5 YearsVehicles 6 Years

Fund Financial Statements

In the fund financial statements, fixed assets used in governmental fund operations are accounted for as capitaloutlay expenditures of the governmental fund upon acquisition. Fixed assets used in proprietary fund operationsare accounted fro the same as in the government-wide statements.

Amortization of Bond Issuance Costs

The bond issuance costs are amortized on a straight-line basis for a period conforming to the term of the bondsissued.

Long-Term Obligations

The accounting treatment of long-term debt depends on whether the assets are used in governmental fundoperations or proprietary fund operations and whether they are reported in the government-wide or fund financialstatements.

All long-term debt to be repaid from governmental and business-type resources are reported as liabilities in thegovernment-wide statements. The long-term debt consists primarily of bonds payable and accrued compensatedabsences.

Long-term debt for governmental funds is not reported as liabilities in the fund financial statements. The debtproceeds are reported as other financing sources and payment of principal and interest reported as expenditures.The accounting for proprietary fund Is the same in the fund statements as it is in the government-wide statements.

Compensated Absences

The Police Jury's policies regarding vacation time permit employees to accumulate earned but unused vacationleave. The liability for these compensated absences is recorded as long-term debt in the government-widestatements. In the fund financial statements, governmental funds report only the compensated absence liabilitypayable from expendable available financial resources, while the proprietary funds report funds report the liabilityas it is incurred.

Equity Classifications

Government-wide Statements

Equity is classified as net assets and displayed in three components:

a. Invested in capital assets, net of related debt - Consists of capital assets including restricted capital assets,net of accumulated depreciation and reduced by the outstanding balances of any bonds, mortgages, notes,or other borrowings that are attributable to the acquisition, construction, or improvement of those assets.

30

POINTE COUPEE PARISH, LOUISIANAPOLICE JURY

NOTES TO THE FINANCIAL STATEMENTS (CONTINUED)

b. Restricted net assets - Consist of net assets with constraints placed on the use either by (1) external groupssuch as creditors, grantors, contributors, or laws or regulations of other governments; or (2) law throughconstitutional provisions or enabling legislation.

c. Unrestricted net assets - All other net assets that do not meet the definition of "restricted" or "invested incapital assets, net of related debt."

Fund Statements

Governmental fund equity is classified as fund balance. Fund balance is further classified as reserved andunreserved, with unreserved further split between designated and undesignated. Proprietary fund equity isclassified the same as in the government-wide statements. See Note 3.G. for additional disclosures.

1 .F. REVENUES, EXPENDITURES, AND EXPENSES

Property Tax

All taxable property located within the State of Louisiana is subject by law to taxation on the basis of its assessedvaluation. The assessed value is determined by the Parish Assessor, except for public utility property which isassessed by the Louisiana Tax Commission.

The 1974 Louisiana Constitution provided that, beginning in 1978, all land and residential property were to beassessed at 10% of fair market value; agricultural, horticultural, marsh lands, timber lands and certain historicbuildings are to be assessed at 10% of "use" value; and all other property is to be assessed at 15% of fair marketvalue. Fair market values are determined by the elected assessor of the parish and are subject to review and finalcertification by the Louisiana Tax Commission. The Assessor is required to reappraise all property every fouryears.

The Sheriff of Points Coupee Parish, as provided by State Law, is the official tax collector of general property taxeslevied by the Police Jury. By agreement, the Sheriff receives a commission of approximately 3.83%. All taxes aredue by December 31 of the year and are delinquent on January 1 of the next year, which is also the lien date. Statelaw requires the Sheriff to collect property taxes in the calendar year in which the assessment is made. If the taxesare not paid by the due date of December 31st, the taxes bear interest at 1.25% per month until the taxes are paid.After notice is given to the delinquent taxpayers, the Sheriff is required by the Constitution of the State ofLouisiana to sell the least quantity of property necessary to settle the taxes and interest owed. Property taxes arerecognized as revenue in the year for which they are levied and become due. The majority of the year's taxes arecollected from November to February by the Sheriff. Any amounts not collected at December 31st are shown asaccounts receivable. All taxes are considered fully collectible; therefore, no allowance for uncollectible taxes isprovided.

Ad valorem taxes as presented in these financial statements are as follows:

Fund

Expira-tionDate

General Fund •

Parish TaxParish Tax in New RoadsParish Tax in Livonia

Special Revenue -

Fire District No. 1Fire District No. 3

Enterprise Funds -

Water District No. 1Sewer District No. 1Sewer District No. 3A

StatutoryStatutoryStatutory

20102010

202620182029

Mills

3.421.711.71

5.545.97

8.9436.7424.24

PropertyAssessedValuations

Taxes Assessed ForGeneralPurpose

SpecialPurposes

241,628.40331,192,730

5,284.300

20.204,38542,595.738

13,031.7833,926,955

506,500

737,83841,9155,211

$ 96,837196.792

79,47375,1872.948

784,964 $ -451,237

31

POINTE COUPEE PARISH, LOUISIANAPOLICE JURY

NOTES TO THE FINANCIAL STATEMENTS (CONTINUED)

The taxes levied in the enterprise funds are dedicated for debt service.

Sales and Use Tax

Pointe Coupee has a one per cent sales and use tax approved by the voters on September 19, 1984. The tax, afterall necessary costs for collection and administration, is to be used for the following purposes in the percentagesassigned:

• Not less than 35% is dedicated and used for capital improvements, maintenance, and operation of PointeCoupee Parish Hospital District No. 1, including, but not limited to, the Pointe Coupee General Hospital andother medical complexes adjacent thereto and throughout the Parish;

• Not less than 20% is dedicated and used for the construction, maintenance, and operations of acomprehensive parishwide solid waste and non-hazardous waste disposal program;

• Not less than 20% is dedicated and used for the construction and maintenance of public roads, highways,bridges and drainage facilities throughout the unincorporated areas of the Parish;

• Not less than 14% is dedicated and used for capital improvements, maintenance and operations of aparishwide recreational program, including, but not limited to, a senior citizens and youth services program;

• The remaining 11% shall be appropriated by the Police Jury for lawful Parish purposes, by ordinance orresolution of the Police Jury.

An additional Vfe cent sales and use tax was approved by the voters on May 3, 1997, for 15 years for the purpose ofconstructing, improving and resurfacing the public roads and bridges in the parish.

Operating Revenues and Expenses

Operating revenues and expenses for proprietary funds are those that result from providing services and producingand delivering goods and/or services. It also includes all revenue and expenses not related to capital and relatedfinancing, noncapital financing, or investing activities.

Expenditures/Expenses

In the government-wide financial statements, expenses are classified by function for both governmental andbusiness-type activities.

In the fund financial statements, expenditures are classified as follows:

Governmental Funds - By Character: Current (further classified by function)Debt ServiceCapital Outlay

Proprietary Fund - By Operating and Nonoperating

In the fund financial statements, governmental funds report expenditures of financial resources. Proprietary fundsreport expenses relating to use of economic resources.

Interfund Transfers

Permanent real location of resources between funds of the reporting entity are classified as interfund transfers. Forthe purposes of the Statement of Activities, all interfund transfers between individual governmental funds havebeen eliminated.

NOTE 2. - STEWARDSHIP, COMPLIANCE, AND ACCOUNTABILITY

By its nature as a local government unit, the Police Jury is subject to various federal, state, and local laws andcontractual regulations. An analysis of the Police Jury's compliance with significant laws and regulations anddemonstration of its stewardship over Police Jury resources follows.

32

POINTE COUPEE PARISH, LOUISIANAPOLICE JURY

NOTES TO THE FINANCIAL STATEMENTS (CONTINUED)

2.A. FUND ACCOUNTING REQUIREMENTS

The Police Jury complies with all state and local laws and regulations requiring the use of separate funds,legally required funds used by the Police Jury include the following:

The

FundCriminal Court FundFire Protection District No. 1Fire Protection District No. 2Weatherization FundScott Civic CenterRoad ConstructionPointe Coupee Parish Natural Gas SystemGas Utility District No. 2 of Pointe Coupee ParishPointe Coupee Parish Waterworks District No. 1Waterworks District No. 2 of Pointe Coupee ParishPointe Coupee Parish Sewerage District No. 1Pointe Coupee Parish Sewerage District No. 3AMulti-Use CenterPointe Coupee Port, Harbor, and Terminal District

Required ByState LawState LawState LawGrant AgreementJoint Venture AgreementBond IndentureBond Indenture & Local OrdinanceLocal OrdinanceBond Indenture & Local OrdinanceBond Indenture & Local OrdinanceBond Indenture & Local OrdinanceBond Indenture & Local OrdinanceBond IndentureState Law

2.B. DEPOSITS AND INVESTMENTS LAWS AND REGULATIONS

Under state law, the Police Jury may invest in United States bonds, treasury notes and bills, or certificates or timedeposits os state banks organized under Louisiana law and national banks having principal offices in Louisiana. Inaddition, local governments in Louisiana are authorized to invest in the Louisiana Asset Management Pool Inc.(LAMP), a non-profit corporation formed by an initiative of the State Treasurer and organized under the laws os theState of Louisiana, which operates a local government investment pool. As reflected in Note 3.A., all deposits werefully insured or col lateral ized.

2.C. REVENUE RESTRICTIONS

The Police Jury has various restrictions placed over certain revenue sources from state or local requirements. Theprimary restricted revenue sources include:

Revenue SourceSales TaxGas, Water, and SewerHotel/Motel TaxCDBGAd Valorem Tax

Legal Restrictions on UseSee Note I.E.Debt Service and Utility OperationsConvention and TourismGrant Program ExpendituresDebt Service

For the year ended December 31, 2004, the Police Jury complied, in all material respects, with these revenuerestrictions.

2.D. DEBT RESTRICTIONS AND COVENANTS

General Obligation Debt

Louisiana Revised Statute 39:562, of the Louisiana Constitution, limits the amount of outstanding general obligationbonded debt of the any subdivision for any one of the purposes authorized to 10 percent of the assessed valuationof the taxable property of such subdivision, including both (1) homestead exempt property, which shall be includedon the assessment roll for the purposes of calculating debt limitation and (2) nonexempt property, as ascertainedby the last assessment for parish, municipal, or local purposes prior to delivery of the bonds representing suchindebtedness, regardless of the date of the election at which said bonds were approved. For the year endedDecember 31, 2004, the Police Jury's general obligation debt did not exceed such limitation.

Other Long-Term Debt

Except as noted in the following paragraph, as required by the Louisiana Constitution, the Police Jury may not incurany indebtedness that would require payment from resources beyond the current fiscal year revenue without first

33

POINTE COUPEE PARISH, LOUISIANAPOLICE JURY

NOTES TO THE FINANCIAL STATEMENTS (CONTINUED)

obtaining voter or state bond commission approval. For the year ended December 31, 2004, the Police Juryincurred no such indebtedness.

Bonds Payable

The various bond indentures relating to the bond issues contain some restrictions or covenants that are financialrelated. These include covenants such as debt service coverage requirements and required reserve accountbalances. For the year ended December 31, 2004, requirements of the various bond indentures has been compliedwith.

2.E. FUND EQUITY RESTRICTIONS

Deficit Prohibition

The following individual funds have deficits in unreserved fund balance at December 31, 2004:

DeficitFund Amount

Criminal Court $ 254,073

The Criminal Court deficit has been a problem for the last several years. Until the deficit is corrected, the GeneralFund will advance the necessary funds to cover any deficits. As of December 31, 2004, the General Fund hasadvanced $258,108 to cover accumulated deficits.

NOTE 3. - DETAIL NOTES ON TRANSACTION CLASSES/ACCOUNTS

The following notes present detail information to support the amounts reported in the basic financial statements forits various assets, liabilities, equity, revenues, and expenditures/expenses.

3.A. CASH AND INVESTMENTS

At December 31. 2004, the Police Jury has cash and cash equivalents totaling $7.997,830 in demand depositaccounts and Louisiana Asset Management Pool (LAMP).

These deposits are stated at cost, which approximates market. Under state law, theses deposits must be securedby federal deposit insurance or the pledge of securities owned by the fiscal agent bank. The market value of thepledged securities plus the federal deposit insurance must at all times equal the amount on deposit with the fiscalagent. These securities are held in the name of the pledging fiscal agent bank in a holding or custodial bank that ismutually acceptable to both parties.

At December 31, 2004, the Police Jury has $10,304,555 in demand deposit accounts. These deposits are securedfrom risk by $100,000 of federal deposit insurance and $10,204,555 of pledged securities held by the custodialbank in the name of the fiscal agent bank (GASB Category 3).

Even though the pledged securities are considered uncollateralized (Category 3) under the provisions of GASBStatement No. 3, Louisiana Revised Statute 39:1229 imposes a statutory requirement on the custodial bank toadvertise and sell the pledged securities within 10 days of being notified by the police jury that the fiscal agent hasfailed to pay deposited funds upon demand.

In addition to the demand deposits, the Police Jury has $1,677,524 invested in the Louisiana Asset ManagementPool Inc. (LAMP), a local government investment pool (see Summary of Significant Accounting Policies). Inaccordance with GASB Codification Section 150.165, the investment in LAMP at December 31, 2004, is notcategorized in the three risk categories provided by GASB Codification Section 150.164 because the investment isin the pool of funds and therefore not evidenced by securities that exist in physical or book entry form. LAMP isadministered by LAMP, Inc., a non-profit corporation organized under the laws of the State of Louisiana, which wasformed by an initiative of the State Treasurer, representatives from various organizations of local government, theGovernment Finance Officers Association of Louisiana, and the Society of Louisiana CPA's. Only localgovernments having contracted to participate in LAMP have an investment interest in its pool of assets. The

34

POINTE COUPEE PARISH, LOUISIANAPOLICE JURY

NOTES TO THE FINANCIAL STATEMENTS (CONTINUED)

primary objective of LAMP is to provide a safe environment for the placement of public funds in short-term, high-quality investments. The LAMP portfolio includes only securities and other obligations in which local governmentsin Louisiana are authorized to invest. Accordingly, LAMP investments are restricted to securities issued,guaranteed, or backed by the U.S. Treasury, the U.S. government or one of its agencies, enterprises, orinstrumentalities, as well as repurchase agreements col lateral ized by those securities. The dollar weighted averageportfolio maturity of LAMP assets is restricted to not more than 90 days, and consists of no securities with amaturity in excess of 397 days. LAMP is designed to be highly liquid to give its participants immediate access totheir account balances.

3.B. RESTRICTED ASSETS

The amounts reported as restricted assets are cash, investments, and accrued interest in various accounts requiredby the various bond indentures as described in Note 2.D., and amounts held in trust for customer utility meterdeposits.

The restricted assets as of December 31, 2004, are as follows:

Meter depositsCurrent debt serviceFuture debt serviceDepreciation and contingencyConstruction accounts

Totals

3.C. DUE FROM/TO OTHER GOVERNMENTAL UNITS

A summary of receivables as of December 31, 2004, follows:

StatePointe Coupee Parish SheriffCity of New Roads

A summary of payables as of December 31, 2004, follows:

Pointe Coupee Parish Sheriff

3-D. DUE TO/FROM OTHER FUNDS

As at December 31, 2004, the amounts due to/from other funds is as follows:

1,042,104311,000657,657323,830

10,238

2.344.829

33.7457,7545,173

46,672

45,158

Receivable Fund Payable Fund Amount