CONFIDENTIAL FOR INTERNAL USE PUBLIC UPON APPROVAL DOCUMENT OF THE INTER-AMERICAN BANK MULTILATERAL INVESTMENT FUND SAINT LUCIA PROADAPT PPCR SUPPORTING CLIMATE RESILIENT INVESTMENTS IN THE AGRICULTURAL SECTOR IN ST. LUCIA (RG-T2935) DONORS MEMORANDUM This document was prepared by the project team comprised of: Lorena Mejicanos Rios (MIF/CSA), Vashtie Dookiesingh (MIF/CTT) and Gerard Alleng (CSD/CCS) as team leaders, María Victoria Sáenz (MIF/CSA), Sara Valero Freitag (CSD/CCS) and Anna Copplind (GCL/GCL). This document contains confidential information relating to one or more of the ten exceptions of the Access to Information Policy and will be initially treated as confidential and made available only to Bank employees. The document will be disclosed and made available to the public upon approval.

Transcript

CONFIDENTIAL

FOR INTERNAL USE PUBLIC UPON APPROVAL

DOCUMENT OF THE INTER-AMERICAN BANK MULTILATERAL INVESTMENT FUND

SAINT LUCIA

PROADAPT PPCR

SUPPORTING CLIMATE RESILIENT INVESTMENTS IN THE AGRICULTURAL SECTOR IN ST. LUCIA

(RG-T2935)

DONORS MEMORANDUM

This document was prepared by the project team comprised of: Lorena Mejicanos Rios (MIF/CSA), Vashtie Dookiesingh (MIF/CTT) and Gerard Alleng (CSD/CCS) as team leaders, María Victoria Sáenz (MIF/CSA), Sara Valero Freitag (CSD/CCS) and Anna Copplind (GCL/GCL).

This document contains confidential information relating to one or more of the ten exceptions of the Access to Information Policy and will be initially treated as confidential and made available only to Bank employees. The document will be disclosed and made available to the public upon approval.

-i-

CONTENTS PROJECT INFORMATION

I. THE PROBLEM ................................................................................................. 1

A. Problem Description ............................................................................. 1

II. THE INNOVATION PROPOSAL ............................................................................. 3

A. Project Description ................................................................................ 3 B. Project Results, Measurement, Monitoring and EvaluationError! Bookmark not defined

III. ALIGNMENT WITH IDB GROUP, SCALABILITY, AND RISKS ................................... 10

A. Alignment with IDB Group .................................................................. 10 B. Scalability............................................................................................ 11 C. Project and Institutional Risks ............................................................. 11

IV. INSTRUMENT AND BUDGET PROPOSAL ............................................................. 12

V. EXECUTING AGENCY (EA) AND IMPLEMENTATION STRUCTURE ........................... 13

A. Executing Agency(s) Description ........................................................ 13 B. Implementation Structure and Mechanism ......................................... 14

VI. COMPLIANCE WITH MILESTONES AND SPECIAL FIDUCIARY ARRANGEMENTS ........ 15

VII. INFORMATION DISCLOSURE AND INTELLECTUAL PROPERTY** ............................. 15

-ii-

PROJECT SUMMARY

ST. LUCIA SUPPORTING CLIMATE RESILIENT INVESTMENTS IN THE AGRICULTURAL SECTOR IN

ST. LUCIA

RG-T2935

The island of St. Lucia, located in the Windward island chain of the Caribbean, has traditionally depended heavily on bananas production as a driver of exports and GDP. However, the combination of loss of access to preferential EU markets and an accelerated impact of climate change, specifically increased temperatures and changes in rainfall patterns1 has resulted in a significant decline in the island’s agricultural sector and fish catch negatively impacting both livelihoods of rural populations and heightened exposure to food security issues. To enhance the productivity and sustainability of livelihoods in local agro production, particularly in the context of climate change, two parallel but inter related changes are needed in the sector. First, a recent study illustrates that there is a need for training and technical support for producers in the adoption of more climate resilient technologies and practices to increase both productivity and quality of output. Second, as demonstrated in the Caribbean region, small scale producers that dominate the regional agricultural sector require an incentive in the form of greater access to higher value markets if they are to invest time and finances in the adoption of new ways of farming. The main objective of the project is to strengthen the viability of agri-business operators in the southern region of St. Lucia within the context of climate change. The proposed project is highly innovative as it will deliver blended financial support for the adoption of climate resilient practices and improved livelihoods for small producers in St. Lucia. The model that has been developed to achieve this objective includes three inter-related elements, specifically: (1) support for capacity building and financing of climate resilient practices by small producers in the targeted region; (2) development and leverage of new, more sustainable and profitable market channels in the island’s tourism and retail sectors; and, (3) strengthening of cooperative structures to organize independent small producers and ensure that quality, pricing and quantities required for transactions with larger scale buyers are achieved and maintained. This model explicitly addresses the fact that changes in traditional practices must be accompanied by new market opportunities, and such market opportunities are most efficiently and effectively accessed through participation in a producer centered, reliable organization that can effectively function as an intermediary between large numbers of independent small scale producers and commercial buyers. Expected results of the intervention include: (i) 154 producers’ access financing to implement climate resilient technologies and practices, (ii) sales volume of farmers output increase of 100% and (iii) 85 hectares of farmlands are cultivated using sustainable practices. In addition, a reduction in GHG emissions is expected, although specific targets will be set based on the types of technologies implemented. The proposed project is directly aligned with IDBG objectives in the context of the emphasis on climate adaptation, improving productivity and improving livelihoods of small and vulnerable populations. The program is consistent with the Update to the Institutional Strategy 2010-2020 (GN-2788-5) which identifies climate change and adaptation and mitigation as one of the two cross-cutting issues. According to the joint MDB approach on climate finance tracking, 100% of total IDB funding for this project will be invested in climate change adaptation activities. This contributes to the IDBG’s climate finance goal of 30% of combined IDB and IIC operational 1 UN ECLAC, 2011.An assessment of the economic impact of climate change on the agricultural sector in St. Lucia October 2011.

approvals by year’s end 2020. To ensure technical and strategic alignment the project team includes members from the IDBG’s Climate Change and Sustainability Division.

iv

ANNEXES

ANNEX I Results Matrix

ANNEX II Budget Summary

APPENDICES

Draft Resolution

AVAILABLE IN THE TECHNICAL DOCUMENTS SECTION OF MIF PROJECT INFORMATION SYSTEM

ANNEX III Detailed Budget

ANNEX IV Diagnostic of Needs of the Executing Agency (DNA) (includes Integrity Due Diligence Analysis)

ANNEX V Reporting Requirements, Compliance with Milestones and Fiduciary Arrangements

ANNEX VI Procurement Plan

ANNEX VII Historical Financial Statements

ANNEX VIII Project’s Financial Projections (Only PPCR Loan)

ANNEX IX Financial Projections LCCU + PPCR Loan

-v-

vi

ACRONYMS AND ABBREVIATIONS

BBFC Black Bay Small farmer cooperative limited

CDB Caribbean Development Bank

CO2e Carbon Dioxide Equivalent

CSA Climate Smart Agriculture

DNA Diagnostic of Executing Agency Needs

EC$ Eastern Caribbean Dollar

EU European Union

FPA Financial Procedures Agreement

GDP Gross Domestic Product

GHG Greenhouse Gas

IDB Inter-American Development Bank

IDBG Inter-American Development Bank Group

IIC Inter-American Investment Corporation

LCCU Laborie Co-operative Credit Union Limited

LFCC Laborie fishers and consumers cooperative

MDB Multilateral Development Bank

MIF Multilateral Investment Fund

MSME Micro, Small and Medium Enterprise

NDF Nordic Development Fund

PPCR Pilot Program for Climate Resilience

SCX Strategic Climate Fund

vii

PROJECT INFORMATION SAINT LUCIA

SUPPORTING CLIMATE RESILIENT INVESTMENTS IN THE AGRICULTURAL SECTOR IN ST. LUCIA

(RG-T2935) Country and Geographic Location:

Saint Lucia, in the rural communities of Laborie and Environs located in the southern part of the island

Executing Agency and borrower:

Laborie Co-operative Credit Union Ltd. (LCCU)

Focus Area: Climate Smart Agriculture

Coordination with Other Donors/Bank Operations:

Climate Change Division of IDB (CSD/CCS) and the Caribbean Development Bank (CDB)

Saint Lucia eligibility In accordance with Article III, Section 3(a) of the MIF II Agreement, all regional developing member countries of the Bank and the CDB are potentially eligible recipients of financing from the Fund to the extent that they are eligible beneficiaries of financing from the Bank. Furthermore, financing in the territories of the countries which are member of the CDB, but not the Bank as in the case of Saint Lucia, shall be conducted in consultation and agreement with, or through the CDB and under such conditions, consistent with the principles for MIF Principles for Fund Operations set forth in Article III thereof, as the Donors Committee shall decide. Therefore, as part of the project design and in compliance with Article III, Sec. 3(d), information on the project has been shared and agreed upon with the Caribbean Development Bank (CDB). The CDB could also potentially assist in scaling the project approach within the Caribbean region.

Project Beneficiaries: (i) 250 members of the Laborie Co-operative Credit Union Ltd. (LCCU). These members are expected to be farmers of the Black Bay Small Farmer Cooperative Limited (BBFC) or fishermen of the Laborie Fishers and Consumers Cooperative (LFCC);

(ii) the three cooperatives (LCCU, BBFC, LFCC), agro-processors and/or agricultural distributors who are also members of these cooperatives and who incorporate climate resilient agricultural technologies and practices into their operations; and

PPCR (SCX) Reimbursable Loan3 The loan will be a Senior full recourse loan.

US$ 804,000 43%

Counterpart: US$ 691,456 37%

TOTAL PROJECT BUDGET: US$ 1,856,396 100%

2 Transfer from the PROADAPT facility, RG-X1167, approved December 26th, 2012. 3 PPCR resources will be provided to the IDB from the World Bank, in its capacity as trustee of the Strategic Climate Fund (SCX).

2

Execution and Disbursement Period:

The execution period for the blended technical cooperation financing in this project (MIF/MSE and PROADAPT (NDF) will be 36 months, with a 42 month disbursement period.

Disbursements under the Project shall not be made after 18 months of the execution of the Loan Agreement and final transaction documents. Upon such date, the Borrower’s right to request disbursements under the facility shall be cancelled automatically without the need of any action by IDB/MIF. Principal amounts disbursed under the Loan Facility will bear a yearly Base Interest Rate of 5%, applicable to the outstanding principal at the calculation date. A grace period on principal repayments of up to 1.5 years counted as from the date of execution of the loan agreement may be granted. The Loan Facility will be disbursed in up to five (5) drawdowns. The first drawdown will be for an amount of no less than US$100,000 and of no more than US$250,000, or the respective equivalents in East Caribbean Dollars. The following drawdowns (up to four (4)) will be for a maximum amount of the equivalent of US$250,000 each, provided that the total amount disbursed under the facility does not exceed the total loan amount of US$804.000. Disbursements would be limited to one per quarter.

3

Special Contractual Conditions:

Special conditions precedent to the first disbursement are as follows:

i. For the blended Technical Cooperation Financing: Memorandum of Understanding (MOU) between the LCCU and BBFC establishing the roles and responsibilities of each organization in the execution of the project;

ii. MOU between LCCU and LFCC establishing the roles and responsibilities of each organization in the execution of the project;

iii. MOU between the LCCU and the Ministry of Agriculture of Saint Lucia establishing the roles and responsibilities of each organization in the execution of the project;

iv. A project coordinator has been appointed by LCCU; and

v. 2 letters submitted by commercial buyers (e.g. hotels or supermarkets) confirming interest in initiating /expanding purchase of local produce from BBFC.

For the Loan Financing: First Disbursement will be subject to the usual and customary conditions to the Bank’s satisfaction including, without limitation, the following conditions:

i. The Borrower having delivered all organizational documents thereof;

ii. completion of all authorizations, including all Directors’ and Shareholders’ Resolutions of the Borrower;

iii. a certificate of incumbency of the Borrower being delivered;

iv. all transaction documents being unconditional and fully effective;

v. credit regulations have been reviewed by the IDB and the IDB’s non-objection to these regulations has been provided to LCCU.

Further Disbursements under the facility shall be subject to the usual and customary conditions to the Bank’s satisfaction including, without limitation, proof that Borrower has caused that funds disbursed under the facility have been used exclusively to extending credits to Eligible Sub-Borrowers, as well as compliance with all loan conditions and covenants.

Disbursements under the Program shall not be made after 18 months of the execution of the Loan Agreement. Upon such date, the Borrower’s right to request disbursements under the facility shall be cancelled automatically without the need of any action by IDB/MIF.

Risks Exchange risk: the Eastern Caribbean dollar (EC$) has been stable in the last several decades, nonetheless, there´s a minor risk that in case of any eventual adverse move in this currency it could undermine the ability of LCCU to repay the loan. Mitigating measure: the loan would be repayable in EC dollars; and the PPCR will absorb the potential losses related to exchange rate variations. Market risk: small producers face a market risk where a conglomerate owned by local and foreign investors imports produce into St Lucia to supply the local tourism market (hotels and restaurants), making fair competition difficult. Mitigation measure: BBFC is in the process of forging an alliance with this conglomerate so that BBFC can itself

4

become a supplier; moreover, the alliance will include exploring the possibility of supplying produce to other Caribbean countries. In addition, the BBFC is already supplying to the largest supermarket and several tourism operators and this operation creates opportunities for further business expansion. Regulatory risk: Saint Lucia, given its small size and limited food production, has several import food quotas which eventually could affect BBFC and the local producers, since the quota of imports and compete with the local production. Mitigation measure: the project is aligned to the Saint Lucia climate strategic plan that aims to improve the local livelihoods. The government through the ministry of agriculture is an important stakeholder of this initiative, therefore is open to modify the quotas as the project develops and shows the need for such changes. Natural disasters: during the project execution, any natural disaster could occur given St. Lucia’s geographic location and vulnerability. Mitigation measure: the project includes the dissemination and adoption of best practices to increase the resilience of agro producers and of the LCCU as executing agency and as a key financial institution in the southern region. Additionally, parametric agro insurance will be included in each climate resilient loan to support the borrowers in resuming business in case of any major climate event. Currently, LCCU already provides property and life insurance to its customers, and plans to bundle agro parametric insurance with these services to reduce the cost of the premiums to its borrowers and members while reducing their business risk. In addition, LCCU will be strengthened via the development of a climate and enterprise risk assessment and a business continuity plan that will allow it to continue operations in case of any disaster. Low appetite for loans from the producers. Mitigation measure: BBFC will lead the change with the producers by linking adaptation to climate change with access to higher value markets year-round. To support this initiative, BBFC will access a loan to improve its own productive infrastructure (storage, processing and cooling room) and logistics capacity. This improvement is expected to have a trickledown effect on the supply chain, as members will in turn need to access loans to adopt the technology that will allow for climate resilient year-round production (green houses, irrigation and rainwater harvesting systems, solar water pumps and solar chillers).

Environmental and Social Impact Review

This operation was screened and classified as required by the IDB’s safeguard policy (OP-703) March 22, 2017. Given the limited impacts and risks, the proposed category for the project is C.

Unit responsible for disbursements

MIF/CBA

I. The Problem A. Problem Description 1.1. St Lucia is a volcanic and mountainous island in the Windward Island chain of the

Caribbean with a total land area of 616 square kilometers and a population of approximately 187,000. The economy depends primarily on tourism (65 percent of GDP), banana production, and light manufacturing4. Most of the tourism infrastructure and associated economic activities are concentrated in and around the island’s capital city; however, the southern region remains primarily rural with agriculture and fishing as key forms of income generation.

1.2. Bananas were, prior to the removal of preferential terms of export to the EU, the mainstay of St. Lucia’s agricultural sector, a significant driver of both GDP and exports for the island. A large number of farmers who left the banana industry are now cultivating root crops, citrus and vegetables (cucumbers, green and red pepper, green beans, tomatoes and variety of lettuces, etc.). Although bananas remain St. Lucia’s largest export, agriculture’s contribution to GDP has declined over the past 30 years, falling from 20% in 1986 to 3% in 20105, indicators of significantly reduced participation and productivity of the sector and posing food security issues particularly in light the fact that annual arrivals of visitors in 2014 were roughly double the local population.6.

1.3. As with the majority of islands in the Caribbean, St. Lucia is highly vulnerable to the impacts of climate change as a result of the expected changes in ambient temperatures (projected increase of 1ºC by 2020s with an increase in the frequency of very hot days and nights), changes in rainfall patterns (e.g. median decrease in rainfall of 4-6% by 2030s) and increases in sea surface temperature (up to 2ºC by 2100)7 and sea level rise (global signal of 5 mm yr-1 increase over the next 100 years with regional variations).8 These changes will have profound impacts on socio-economic conditions of the country with the potential of annual losses being of the order of 3-5 percent of total GDP under different climate scenarios (no change to worst case scenario) for 2030.9 At the level of the agricultural sector, these losses will be seen in declining yields particularly for bananas, root crops and fish catch through 2050.10 Cumulative yield losses in bananas are estimated at approximately $165m and between $58-61mfor root crops, with declines in fish catch potential of 10-20% relative to 2005 levels. The implications of climate change suggest worsening soil conditions, soil erosion and land degradation from flooding; and

4 http://www.heritage.org/index/country/saintlucia 2016 Index of Economic Freedom 5 Compete Caribbean Private Sector Assessment Report St Lucia 2014 6 http://data.worldbank.org/indicator/ST.INT.ARVL 7 Government of St. Lucia, 2011. Second National Communication on Climate Change for St. Lucia. Prepared on Behalf of the Government of St. Lucia in fulfillment of its obligations under the United Nations Framework Convention on Climate Change 8 Nurse et al, 2014. Small islands. In: Climate Change 2014: Impacts, Adaptation, and Vulnerability. Part B: Regional Aspects. Contribution of Working Group II to the Fifth Assessment Report of the Intergovernmental Panel on Climate Change. (eds.)]. Cambridge University Press, Cambridge, United Kingdom and New York, NY, USA, pp. 1613-1654. Available: http://www.ipcc.ch/pdf/assessment-report/ar5/wg2/WGIIAR5-Chap29_FINAL.pdf 9 CCRIF, 2010. Enhancing the Climate Risk and Adaptation Fact Base for the Caribbean: Preliminary results of the Economics of Climate Adaptation (ECA) Study. http://www.ccrif.org/sites/default/files/publications/ECABrochureFinalAugust182010.pdf 10 UN ECLAC, 2011. An Assessment of the Economic Impact of Climate Change on the Agricultural Sector in St Lucia October 2011

potentially increased crop loss due to high temperatures and changing rainfall patterns. Uncontrolled agricultural intensification, poor agricultural practices and the current trend of converting prime agricultural lands to other uses, exacerbate the vulnerability of this sector.11

1.4. Thus the agricultural sector in St. Lucia exhibits high sensitivity to climate

change and climate variability. In recent years, high winds and periods of drought with sporadic heavy rains have increased in intensity, together with high sea temperatures and increased SLR12. In 2007, the country was struck by Hurricane Dean (agricultural loses accounted for about US$10 million from direct damages)13 and was followed by Hurricane Tomas in 2010 which resulted in damages of about US$20 million. Overall the total damage caused by the storm accounted for 34% of GDP14. The economy has remained fragile since, with GDP growing by 1.6% in 2012 and falling by 0.5% in 2013 with contractions persisting in 2014.

1.5. The prevalence of small-scale agriculture in St. Lucia and the large number of ex-

banana farmers who have limited experience in viable agricultural diversification hinders national efforts to adapt to environmental and climatic changes. An analysis of climate risk in St. Lucia conducted by CARIBSAVE in 201215 indicates that farmers urgently need to receive training and support in climate resilient practices for sustainability of the sector.

1.6. Policy analysis of initiatives to develop agriculture in St. Lucia indicate that the

major provisions for the sector focus on agricultural diversification, enhancing food security and promoting competitiveness but do not specifically address climate change16.

1.7. In this context, recent experience and lessons learned in MIF project analysis and

implementation in the region17 clearly demonstrates that incentives for farmers to adopt new practices to improve climate resilience, new investment and expanded participation in the sector requires parallel interventions to support access to higher value markets. In St. Lucia, there is an opportunity to expand supply of local agro-products and fish to the island’s hotel and restaurant operations if supply can be guaranteed in terms of quality, availability and pricing, all factors that necessitate the introduction of climate smart agricultural practices and support and support for cooperative structures to organize small scale independent producers in the sector.

11 CARIBSAVE Climate Change Risk Profile for St Lucia March 2012 12 Government of St. Lucia, 2013. The St. Lucia Climate Change Adaptation Policy: Adapting one individual, one

household, one community, one enterprise and one sector at a time. 13 UNECLAC, 2007. St. Lucia macro socio-economic assessment of the damages and losses caused by

Hurricane Dean. http://repositorio.cepal.org/handle/11362/27628 14 UNECLAC, 2011. An Assessment of the Economic Impact of Climate Change on the Agricultural Sector in St

Lucia October 2011 15 ibid 16 ibid 17 For example GY-M1025, BA-M1009, BA-M1011 and TT-T1067 indicate that the adoption of climate smart and good agricultural practices must be linked to access to higher value markets to incentivize farmers and offset required investment costs in implementing changes in crop planning, land preparation, cultivation harvesting and handling/storage outputs.

3

II. The Innovation Proposal A. Project Description 2.1 The main objective of the project is to strengthen the viability of agri-business

operators in the southern region of St. Lucia within the context of climate change. 2.2 The model that has been developed to achieve this objective includes three inter-

related elements, specifically: (1) capacity building for the adoption of climate resilient practices by producers in the targeted region, as well as financing for investment in relevant technologies and the provision of insurance against major climate events; (2) the development and leverage of new, more sustainable and profitable market channels in the island’s tourism and retail sectors for local fruit, produce, ground provisions and fish, based on market analysis and business planning; and (3) strengthening of cooperative structures to organize independent small producers to ensure that quality, pricing and quantities required for transactions with larger scale buyers are achieved and maintained. This model explicitly recognizes and addresses the fact that changes in traditional practices must be accompanied by new market opportunities and that such market opportunities are most efficiently and effectively accessed through participation in a producer centered, reliable collective organization that can function as the trusted intermediary between large numbers of independent small scale producers and commercial buyers.

2.3 Innovation: The project is innovative as it explicitly connects market opportunities, investment capital, capacity building and technical support via a blended financial intervention to support greater climate resilience, environmental and commercial sustainability of small scale agro production and fishing in St. Lucia. The project in this context, offers an integrated solution that is structured to address the market, financial, technical and organizational challenges inherent in successfully supporting the transition of traditional small scale producers to climate smart and climate resilient practices. In addition, the project is innovative as the main partner, Laborie Co-operative Credit Union Ltd (LCCU), acts not just as a provider of financial services to the people of the southern region of St Lucia, but also the organization has reflected in its mandate, board composition and activities over the past 40 years a very strong commitment to building sustainable local economic and community based development. The LCCU in this case functions as both, a trusted and credible change agent as well as financier in the transition of the region’s agricultural and fishing communities. Recognizing the need to strengthen capacity and livelihoods of the farmers, small agro producers and fisherfolk represent the population of Laborie and surrounding communities the LCCU has already forged formal linkages with both the primary agro producers and fishing co-operatives in the region, the BBFC and LFCC. Building on existing technical, organizational and financial linkages between the LCCU and BBFC as well as the LFCC, which has included training of fishermen and farmers, development of market channels for fish and agro production to retail supermarkets, restaurants and smaller visitor accommodation and piloting of desalination, the LCCU is extremely well positioned to facilitate and support the successful implementation of the proposed intervention in climate change adaptation of farmers and fisherfolk.

4

2.4 To implement the described innovation, the project has two key components. The first component is a technical cooperation facility that will provide required support for LCCU to: (i) define market and business opportunities for agro producers and fisherfolk; (ii) define the most relevant technologies and practices and support farmers in adopting climate resilient practices, in the context of ; (iii) design and promote climate resilient loan product(s) and associated parametric insurance that can be accessed for investment in adoption of climate resilient practices and production by targeted beneficiaries; and, (iii) build institutional capacity and resilience of the LCCU, BBFC and LFCC. The second component of the project will be the extension of PPCR loan financing to LCCU for on lending. to farmers, farmer associations, other small producers, wholesalers, distributors, processing companies and other key actors in the agro production value chain for investment in climate resilient technologies and practices. The second component, specifically the PPCR loan to LCCU, is based on explicit recognition that the tenor and other terms required for such investment differ from LCCU’s existing suite of lending services.

2.5 Beneficiaries: The direct beneficiary of the technical cooperation is the LCCU and the direct beneficiaries of the loan will be: (i) 250 members of LCCU (men and women) whom at the same time can be members of the BBFC or from the LFCC; and (ii) BBFC itself as the organization will benefit from loan financing to improve its productive infrastructure. Targeted farmers are characterized as small scale producers, owners of their land, with limited capacity and access to climate resilient agricultural and other technologies and little or no direct market access. Targeted fisherfolk are highly informal and engaged in subsistence livelihoods.

Component I: Technical Cooperation. The technical cooperation component of the project includes three (3) inter-related sub components as outlined in the following sections. 2.6 Subcomponent 1. Strengthen Market Linkages and Production of producers in

the Black Bay Small Farmers Cooperative Society (BBFC) and Laborie Fishers and Consumers Co-operative (LFCC): (PROADAPT US$130,000, MIF US$95,440, Counterpart US$383,920). This subcomponent will focus on the assessment and climate risk analysis associated with various crops and farming methods, as well as organization and delivery of technical support to small farmers in production planning, adoption of climate resilient land preparation, cultivation and harvesting techniques. A technical study to be conducted to assess current practices and crop selection and associated risks which will be utilized to (I) define the most viable, location specific climate resilient crops and agricultural practices in key locations, (ii) build stakeholder awareness and support for proposed changes and (iii) identify and analyze the most viable/cost effective equipment and technologies that can support climate resilience in the agricultural sector in St Lucia that will be eligible for loan financing. This study will assess current crops, specific soil conditions, climate, topography, water sources, crop varieties, production scale at farmer sites as well as market size. In parallel, under this component specific activities will focus on a market and business plan for establishing new market channels, particularly in the island’s tourism sector and the embedding of required quality, pricing and supply requirements into technical support and investment by farmers and fisherfolk to ensure strong linkages between adoption climate smart practices and market requirements. In addition, the BBFC in particular will receive support to improve the organization of members to supply larger buyers needs via

5

the design of a receiving and packing facility, logistics and communication management, branding and promotion.

2.7 Subcomponent 2: Expanding Access to Climate Resilient Financing (PROADAPT US$20,000, MIF US$20,000, Counterpart US$75,000): This sub component will fund the development and detailed design of climate resilient financing products which will be offered using proceeds of the PPCR loan to LCCU as outlined in Component II. This subcomponent will also support the outreach and marketing activities to engage potential borrowers within the targeted beneficiary group. In addition, this subcomponent will finance the adaptation of a parametric agro insurance service already available on the island to the specific needs of LCCU’s clients. The parametric agro insurance facility will be adapted from a model already developed for St. Lucia by the Munich Climate Insurance Initiative and that will be included in each climate resilient loan. Parametric insurance is payable based on the occurrence of pre-defined triggers, in this case triggers associated with a major climate event that negatively impacts insured agro producers. The purpose of this insurance is to assist borrowing producers to restart business operations in the event of a climate related disaster. Local insurance companies are already providing this service and this project will support LCCU to pilot the adoption of a combined loan product to invest in climate resilience and parametric insurance as a strategy to reduce the premiums to producers.

2.8 Subcomponent 3: Building Institutional Capacity for Climate Resilience (PROADAPT US$45,000, MIF US$22,500, Counterpart US$30,000): An important element of sustaining the results targeted in the project is the institutional capacity of the key organizations that will partner in this initiative to provide a resilience screening/business continuity planning service to its borrowers, specifically the LCCU as change agent and financier, and BBFC and LFCC as the organizations acting as technical and marketing intermediaries between farmers, fishers and larger commercial buyers. In this regard, this component will focus on supporting enterprise and climate risk management, business continuity planning by LCCU as well as business planning, organizational development and human resource capacity building at BBFC and LFCC.

2.9 Component II: Climate Resilient Financing for Climate Adaptation – PPCR LOAN (PPCR: US$804,000)18. The purpose of this component is to provide the LCCU with the necessary resources to create a climate resilient line of financing as a complement to LCCU’s current range of financial services. This credit line

18 The PPCR sub-committee approved the use of PPCR funds as described within the Project. The IDB is an

Implementing Entity of the Strategic Climate Fund (SCX), as outlined in GN-2604. Paragraphs 3.13-3.16 of GN-2604 define the principles of use of SCX funds for NSG operations; Paragraph 3.20 of GN-2604 expressly indicates that all NSG windows of IDB Group will have access to SCX resources. PPCR resources will be provided to the IDB from the World Bank, in its capacity as trustee of the SCX. PPCR resources will be administered by the IDB pursuant to the terms of a Financial Procedures Agreement (FPA) signed between the IDB and the World Bank, as authorized by the Board of Executive Directors in Resolution DE-9/11 (as amended in 2012). The Office of the MIF will be responsible for actively collaborating with other IDB departments (such as ORP/GCM, FIN and LEG) in complying with the fiduciary, reporting, administration and other legal requirements established in the FPA, to ensure that IDB can comply with such obligations on a timely fashion. Furthermore, as stipulated in the FPA, the use of PPCR resources should be consistent with the approvals granted by SCX governing bodies for this project and the applicable policies and guidelines issued by the SCX. Pursuant to such policies and guidelines, PPCR resources include certain fees to assist in the defrayment of project costs for implementation and supervision for an amount in the aggregate of up to US$ 400,000.

6

extended to the LCCU, will be used to finance long term investment loans and working capital to enable its clients to make the necessary investments to adapt to climate change via the adoption of climate resilient practices and technologies that respond to the specific context and conditions in the southern region of St. Lucia. As outlined above, subcomponent II of the complementary technical cooperation will finance the design and targeted promotion of climate resilient financing to direct participants in the project as well as other potential borrowers that may require differentiated financing to enhance climate resilience in both business and residential practices and facilities. The amount of the PPCR loan and the terms under which this loan will be granted to the LCCU are proposed based on the analysis of the LCCU’s historical financial statements and on the results of a model for the projection of the expected results under certain conditions and assumptions.

2.10 The LCCU operates like a commercial bank in terms of lending activities. It offers mainly short term loans with collateral and for those long-term loans, such as housing, the security required is aligned with the term of the loan and therefore mortgages on property, deed or bill of sales are accepted as collateral. In terms of accounting policies, it follows the rules defined in the Cooperative Societies Act. The lending rates on loans range from 7% to 14% with no additional fees or commissions. The Interest paid on deposits to LCCU members varies from 2% to 5% depending on the term.

2.11 The LCCU has demonstrated a solid financial performance, as illustrated in the following table19:

Item 2014 2015 2016 Number of loan clients 3,481 3,959 4,117 Average loan per client 9,235 9,213 9,915 Return on average assets 2.53% 3.03% 3.73% Return on equity 15.4% 16.6% 18.1% Average income rate 9.41% 8.94% 9.41% Cost of funds 4.53% 3.67% 3.33% Net financial margin 50% 58% 64% Operative costs/average portfolio 3% 3% 3% Leverage (Basel is minimum 3%) 12.6% 14.1% 15.8% Default rate n.a. 6.2% 4.4%

2.12 Over the period 2014-2016, the LCCU has steadily increased its client base,

portfolio and profit. The operation generates a financial margin of around 50%, from which operating costs are covered. LCCU’s equity is not affected by the volatility normal in financial cooperatives as its share capital cannot be easily retrieved; instead LCCU promotes savings and offers to its membership different kind of savings products, both withdrawable and fixed. In this context LCCU has funded its growth with equity and shares from members.

2.13 The MIF team in consultation with LCCU’s management created a simple model to project the normal activity of the cooperative and to generate financial statements of the project, considering as such the new loans for the resilience and adaptation to climate change. The main assumptions and results are as follows20:

19 See Annex VII – Historical Financial Statements 20 For detailed information see Annex VIII

7

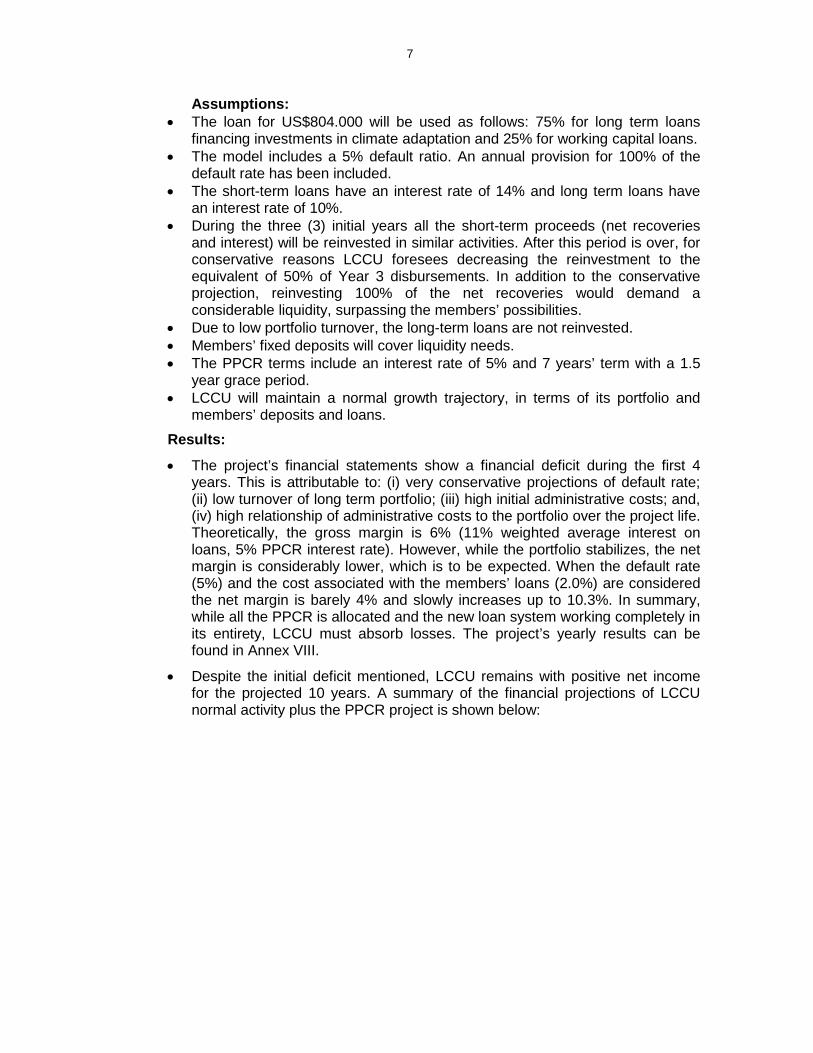

Assumptions: • The loan for US$804.000 will be used as follows: 75% for long term loans

financing investments in climate adaptation and 25% for working capital loans. • The model includes a 5% default ratio. An annual provision for 100% of the

default rate has been included. • The short-term loans have an interest rate of 14% and long term loans have

an interest rate of 10%. • During the three (3) initial years all the short-term proceeds (net recoveries

and interest) will be reinvested in similar activities. After this period is over, for conservative reasons LCCU foresees decreasing the reinvestment to the equivalent of 50% of Year 3 disbursements. In addition to the conservative projection, reinvesting 100% of the net recoveries would demand a considerable liquidity, surpassing the members’ possibilities.

• Due to low portfolio turnover, the long-term loans are not reinvested. • Members’ fixed deposits will cover liquidity needs. • The PPCR terms include an interest rate of 5% and 7 years’ term with a 1.5

year grace period. • LCCU will maintain a normal growth trajectory, in terms of its portfolio and

members’ deposits and loans. Results: • The project’s financial statements show a financial deficit during the first 4

years. This is attributable to: (i) very conservative projections of default rate; (ii) low turnover of long term portfolio; (iii) high initial administrative costs; and, (iv) high relationship of administrative costs to the portfolio over the project life. Theoretically, the gross margin is 6% (11% weighted average interest on loans, 5% PPCR interest rate). However, while the portfolio stabilizes, the net margin is considerably lower, which is to be expected. When the default rate (5%) and the cost associated with the members’ loans (2.0%) are considered the net margin is barely 4% and slowly increases up to 10.3%. In summary, while all the PPCR is allocated and the new loan system working completely in its entirety, LCCU must absorb losses. The project’s yearly results can be found in Annex VIII.

• Despite the initial deficit mentioned, LCCU remains with positive net income for the projected 10 years. A summary of the financial projections of LCCU normal activity plus the PPCR project is shown below:

8

Financial projections of LCCU In US$ Dollars

Year 1 Year 3 Year 5 Year 7 Year 10 FINANCIAL INDICATORS

Total Assets ($000) 56.495.4 63.838.9 72.791.4 83.703.0 106.373.4

Average assets ($000) 54.810.6 61.970.4 70.397.0 80.787.4 102.131.2

Equity ($000) 8.963.8 10.485.9 12.736.2 15.840.5 22.541.7 Average equity ($000) 8.681.0 10.063.0 12.125.6 15.004.9 21.269.1 Market penetration Net portfolio ($000) 46.729.3 54.547.8 63.245.4 73.370.8 91.761.6 Average loan portfolio ($000) 44.849.4 52.548.1 60.987.8 70.743.6 88.455.5 Number of clients 4.326 4.673 5.024 5.433 6.110

Average loan per client 10.367 11.244 12.138 13.021 14.478 Annual loan portfolio growth 10% 8% 8% 8% 8% Total Savings 46.966.8 52.712.9 59.736.7 67.785.2 83.754.3 No. of savings accounts (assume the same as clients) 4.326 4.673 5.024 5.433 6.110

Average savings per client 10.857 11.279 11.889 12.476 13.708 % Women clients 11,7% 12,1% 12,2% 12,3% 12,5% % Rural Clients 100,0% 100,0% 100,0% 100,0% 100,0% Profitability Return on assets 1,52% 2,21% 2,81% 3,39% 4,13% Return on average assets 1,92% 2,68% 3,36% 4,01% 4,96%

• Under normal conditions, LCCU has the capacity to generate enough internal

resources to offset the lack of liquidity generated by the project during the initial years. Indeed, assuming the LCCU will grow conservatively but steadily as compared to the previous 4 years, the cooperative can fundraise from its members a yearly average of more than US$2 million21. The financial projections indicate that the liquidity gap will be close to US$900,000, which is an amount easily offset by LCCU.

• In the following graphic the relationship between the origin of funds can be seen. To grow the portfolio at the low pace the long-term loans demand and cover the very high initial operative costs, it is necessary to cover the gap with member’s deposits:

21 During the past 3 years, the cooperative raised from its membership an average of US$4 million yearly

9

2.14 The previous analysis led the team to propose a loan under the following terms: the tenor will be up to 84 months (7 years) following the date of the first installment of the loan with 1.5 year grace period. The Loan Facility will be disbursed in five drawdowns. The first drawdown will be for an amount of no less than US$100,000 and of no more than US$250,000, or the respective equivalents in EC$. The following drawdowns (up to four (4)) will be for a maximum amount of the equivalent of US$250,000 each, if the total amount disbursed under the facility does not exceed the maximum amount thereof, i.e. US$804.000.

2.15 The financial covenants that will be imposed on LCCU are:

Item Year 1 Year 3 Year 5 Year 6 Year 7

Default rate ≤5% ≤5% ≤5% ≤5% ≤5%

PAR30 ≤9.2% ≤8% ≤7% ≤6% ≤6%

Net financial margin (Profits before administrative costs/ revenues) ~45% ~45% ~50% ~50% ~50%

B. Project Results, Measurement, Monitoring and Evaluation 2.16 The project will contribute to the following CRF indicators22: (i) Number of people

(gender disaggregated) who adopt new (climate resilient) practices or technologies (disaggregated by technology) (CRF 210400); (ii) Tons of CO2e in GHG emissions avoided (CRF 340100)23; Number of Hectares of land cultivated sustainably (CRF 240100); BBFC Average annual sales growth by the BBFC (CRF 330101).

22 http://ziglasrl-001-site1.dtempurl.com/?AspxAutoDetectCookieSupport=1 23 This data will be based on technical studies to determine the best technologies and practices in climate resilient

production as outlined in Subcomponent 1, paragraph 2.6.

10

2.17 The project will undergo a midterm evaluation, which will be conducted by an independent consultant either upon reaching 50% of disbursement or at mid-point in the project execution period, whichever comes first. In addition, the achievement of any results or impacts will be assessed and informed by the tracking of the indicators throughout the life of the project. The midterm evaluation will be used primarily for immediate feedback of recommendations and lessons learned to the project team, and will focus primarily on the extent to which the project beneficiaries received the intended results.

2.18 As outlined in Annex V, the LCCU will submit a semiannual report on the achievement of targeted results (as outlined in Annex I, the Results Matrix) through the MIF’s Project Status Report System (PSR). In addition the LCCU on completion of the project will complete a Final Project Status Report (reporting on cumulative achievement of all project objectives and targeted results.

III. Alignment with IDB Group, Scalability, and Risks A. Alignment with IDB Group 3.1 The proposed project will be implemented with resources from the Pilot Program for

Climate Resilience (PPCR) program of the Climate Investment Funds.24 The PPCR was approved in 2008 as one of three programs under the Strategic Climate Fund (SCX), a trust fund under the Climate Investment Funds which is implemented by various Multilateral Development Banks (MDBs). The PPCR is executed globally through a number of regional and national programs and is intended to: (i) pilot approaches for integrating climate risk and resilience into development policies and planning; (ii) strengthen capacities at national levels needed to integrate climate resilience into development planning; (iii) scale up and leverage climate resilient investment, especially by scaling and/or replicating initiatives; (iv) enable learning by doing and lesson sharing at the country, regional and global levels; and to (v) strengthen cooperation and capacity at the regional level for integrating climate resilience in national and regional development planning and processes.

3.2 This operation is linked to the MIF pillar of Climate Smart Agriculture which involves

improving the integration of agricultural development and responsiveness to climate change to achieve food security and poverty reduction, among other development goals, in the face of constant changes in climate and increasing demand for food. This project proposes the use of resources from the MIF PROADAPT Facility, aimed to building climate resilience in MSMEs and accessing business opportunities related to climate resilience. PRODAPT is co-financed by the Nordic Development Fund.

3.3 The project also aligns with Saint Lucia Climate Change Adaptation Policy (CCAP)25, the Strategic Programme for Climate Resilience26 and its Investment

24 The Climate Investment Funds (CIF) are disbursed through Multilateral Development Banks (MDBs) to support effective and flexible implementation of country-led programs and investments. Fourteen contributor countries have pledged a total of US$ 8.1 billion to the CIF, which is expected to leverage an additional US$ 57 billion from other sources. 25 http://www.google.com/url?sa=t&rct=j&q=&esrc=s&source=web&cd=3&cad=rja&uact=8&ved=0ahUKEwjV4on_gOjSAhWIRSYKHV9JBp4QFggsMAI&url=http%3A%2F%2Fdms.caribbeanclimate.bz%2FM-Files%2Fopenfile.aspx%3Fobjtype%3D0%26docid%3D6566&usg=AFQjCNFbP8y6_0AuZy17ZnVeGKvYDaxX6Qhttp

Plan, the PPCR Caribbean Regional Track and St. Lucia’s Intended Nationally Determined Contribution (iNDC) under the United Nations Framework Convention on Climate Change (UNFCCC)27.

3.4 The program is consistent with the Update to the Institutional Strategy 2010-2020 (GN-2788-5) which identifies climate change and adaptation and mitigation as one of the two cross-cutting issues. According to the joint MDB approach on climate finance tracking, 100% of total IDB funding for this project is invested in climate change adaptation activities. This contributes to the IDBG’s climate finance goal of 30% of combined IDB and IIC operational approvals by year’s end 2020.

3.5 This project is led by the MIF and the team includes the Climate Change Division (CSD/CCS) of the IDB. The CSD/CCS Division is responsible for coordinating the implementation of IDB activities and projects related to the Climate Investment Funds, including the PPCR. This operation will share information and lessons with the Caribbean region.

B. Scalability 3.6 This project will help LCCU to develop a sustainable credit and capacity building

model that can be replicated by producers’ members of other cooperatives in St Lucia and in the Caribbean Basin. One of LCCU’s strategies for scalability is investing time and resources in the generation of “success stories”. This will be the way to induce a change in the local producers’ mind set, by showing that it is possible to improve their livelihoods if they comply with the market expectations in time, volume and quality and, on the importance of adopting climate smart agriculture practices to assure stable production year-round. Once the BBFC’s business model demonstrates success for all the stakeholders (markets, primary producers, BBFC and LCCU), LCCU will be able to commit more resources to expand its portfolio to the agricultural sector, which up to date comprises only 1% of its portfolio. Once good results are demonstrated, the Saint Lucia government and LCCU are willing to expand their access to the PPCR and other Climate Change Funds to scale this initiative further in the island’s the southern region and eventually nationwide by transferring LCCU experience to other local credit unions.

3.7 As part of the project design and as the MIF II Agreement references to CDB countries in Article III, Sec. 3(d), information has been shared with the Caribbean Development Bank (CDB)28. The CDB could also potentially assist in scaling the project approach within the Caribbean region.

C. Project and Institutional Risks 3.8 Exchange risk: The Eastern Caribbean Dollar (EC$) has been stable in the last

several decades, nonetheless, there´s a minor risk that in case of any eventual adverse move in this currency it could undermine the ability of LCCU to repay the loan. Mitigating measure: The loan would be repayable in EC dollars; and the PPCR will absorb the potential losses related to exchange rate variations.

3.9 Market risk: small producers face a market risk where a conglomerate owned by local and foreign investors imports produce into St Lucia to supply the local tourism market (hotels and restaurants), making fair competition difficult. Mitigation measure: BBFC is in the process of forging an alliance with this conglomerate so that BBFC can itself become a supplier; moreover, the alliance will include exploring the possibility of supplying produce to other Caribbean countries. In addition, the BBFC is already supplying to the largest supermarket and several tourism operators and this operation creates opportunities for further business expansion.

3.10 Regulatory risk: Saint Lucia, given its small size and limited food production, has several import food quotas which eventually could affect BBFC and the local producers, since the quota of imports and compete with the local production. Mitigation measure: the project is aligned to the Saint Lucia Climate Strategic plan that aims to improve the local livelihoods. The government through the Ministry of Agriculture is an important stakeholder of this initiative, therefore is open to modify the quotas as the project develops and shows the need for such changes.

3.11 Natural Disasters: During the project execution, any natural disaster could occur given St. Lucia’s geographic location and vulnerability. Mitigation measure: the project includes the dissemination and adoption of best practices to increase the resilience of agro producers and of the LCCU as Executing Agency and as a key financial institution in the southern region. Additionally, parametric agro insurance will be included in each climate resilient loan to support the borrowers in resuming business in case of any major climate event. Currently, LCCU already provides property and life insurance to its customers, and plans to bundle agro parametric insurance with these services to reduce the cost of the premiums to its borrowers and members while reducing their business risk. In addition, LCCU will be strengthened via the development of a Climate and Enterprise Risk Assessment and a Business Continuity plan that will allow it to continue operations in case of any disaster.

3.12 Low appetite for loans from the producers. Mitigation measure: BBFC will lead the change with the producers by linking adaptation to climate change with access to higher value markets year round. To support this initiative, BBFC will access a loan to improve its own productive infrastructure (storage, processing and cooling room) and logistics capacity. This improvement is expected to have a trickledown effect on the supply chain, as members will in turn need to access loans to adopt the technology that will allow for climate resilient year-round production (green houses, irrigation and rainwater harvesting systems, solar water pumps and solar chillers).

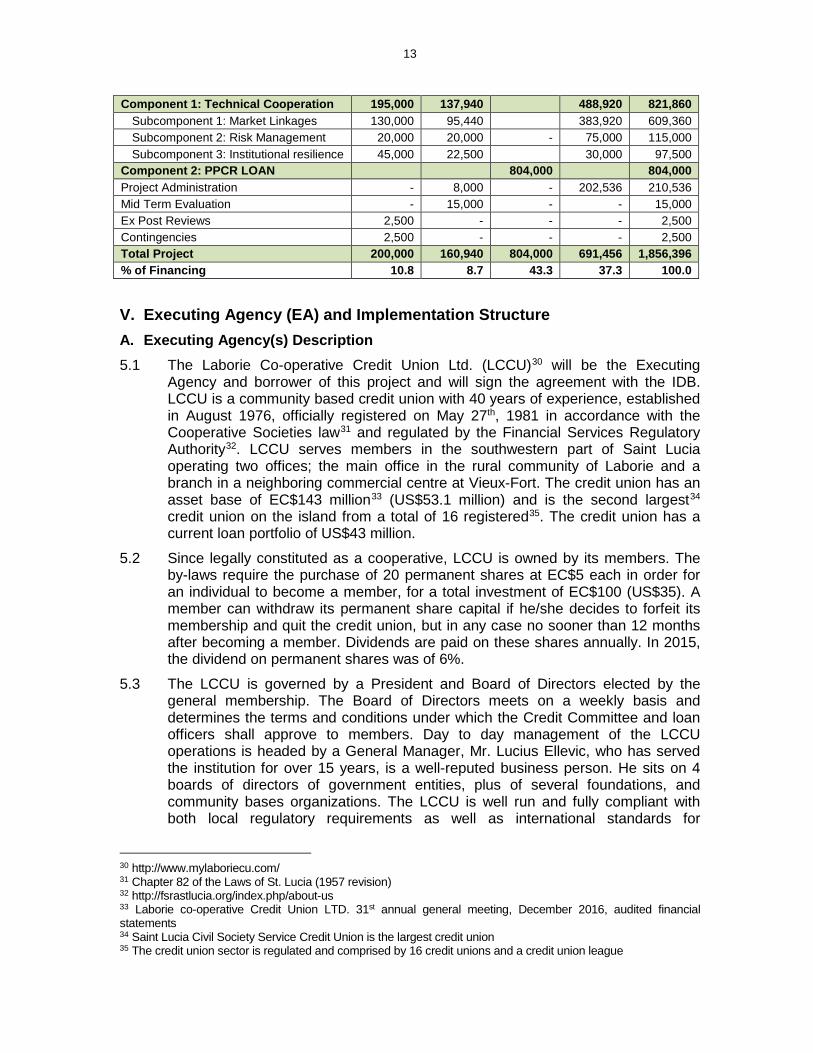

IV. Instrument and Budget Proposal 4.1 The project has a total cost of US$1,856,396, of which US$160,940 (9%) will be

provided by the MIF, US$804,000 (43.3%) by the PPCR as a loan, US$200,000 (11%) as a technical assistance non-reimbursable contribution from NDF from the PROADAPT facility and US$691,456 (37.3%) as counterpart from LCCU.

Project Categories PROADAPT (NDF -US$) MIF (US$)

PPCR (SCX -US$)

Counterpart29 (US$)

Total (US$)

29 Most of the counterpart resources is the time allocated by LCCU executives and credit officers to comply with the project activities and deliverables.

Component 2: PPCR LOAN 804,000 804,000 Project Administration - 8,000 - 202,536 210,536 Mid Term Evaluation - 15,000 - - 15,000 Ex Post Reviews 2,500 - - - 2,500 Contingencies 2,500 - - - 2,500 Total Project 200,000 160,940 804,000 691,456 1,856,396 % of Financing 10.8 8.7 43.3 37.3 100.0

V. Executing Agency (EA) and Implementation Structure A. Executing Agency(s) Description 5.1 The Laborie Co-operative Credit Union Ltd. (LCCU)30 will be the Executing

Agency and borrower of this project and will sign the agreement with the IDB. LCCU is a community based credit union with 40 years of experience, established in August 1976, officially registered on May 27th, 1981 in accordance with the Cooperative Societies law31 and regulated by the Financial Services Regulatory Authority32. LCCU serves members in the southwestern part of Saint Lucia operating two offices; the main office in the rural community of Laborie and a branch in a neighboring commercial centre at Vieux-Fort. The credit union has an asset base of EC$143 million33 (US$53.1 million) and is the second largest34 credit union on the island from a total of 16 registered35. The credit union has a current loan portfolio of US$43 million.

5.2 Since legally constituted as a cooperative, LCCU is owned by its members. The by-laws require the purchase of 20 permanent shares at EC$5 each in order for an individual to become a member, for a total investment of EC$100 (US$35). A member can withdraw its permanent share capital if he/she decides to forfeit its membership and quit the credit union, but in any case no sooner than 12 months after becoming a member. Dividends are paid on these shares annually. In 2015, the dividend on permanent shares was of 6%.

5.3 The LCCU is governed by a President and Board of Directors elected by the general membership. The Board of Directors meets on a weekly basis and determines the terms and conditions under which the Credit Committee and loan officers shall approve to members. Day to day management of the LCCU operations is headed by a General Manager, Mr. Lucius Ellevic, who has served the institution for over 15 years, is a well-reputed business person. He sits on 4 boards of directors of government entities, plus of several foundations, and community bases organizations. The LCCU is well run and fully compliant with both local regulatory requirements as well as international standards for

30 http://www.mylaboriecu.com/ 31 Chapter 82 of the Laws of St. Lucia (1957 revision) 32 http://fsrastlucia.org/index.php/about-us 33 Laborie co-operative Credit Union LTD. 31st annual general meeting, December 2016, audited financial statements 34 Saint Lucia Civil Society Service Credit Union is the largest credit union 35 The credit union sector is regulated and comprised by 16 credit unions and a credit union league

14

community based cooperatives. LCCU has a staff of 35 persons, including 10 tellers and 5 loan officers. No integrity issues were found.

5.4 Based on the last audited statements, LLCU had an outstanding portfolio of loans extended to related parties. The Cooperative Societies Act states that related party transactions are acceptable if: (i) they are deliberated in a joint session of governance bodies (the Board, the Supervisory Committee and the Credit Committee); and (ii) loans and other services are provided at the same conditions, with no special treatments.

5.5 In addition, LCCU has established a strategic alliance and cooperative union with BBFC and LFCC via the formation of the Laborie Co-operative Union. Representing the 3 key member based financial and producer organizations in the Laborie community, this union was established with the specific commitment to develop more sustainable livelihoods in the region. The proposed project will build on an existing practice of cooperation and support that exists between LCCU, BBFC and LFCC, a key factor that will mitigate common issues and challenges inherent in projects requiring a high level of inter organizational coordination.

B. Implementation Structure and Mechanism 5.6 LCCU will establish an executing unit and the necessary structure to execute

project activities and manage project resources effectively and efficiently. LCCU will also be responsible for providing progress reports on project implementation. LCCU will appoint a project coordinator that will be located at the BBFC’s office. This project coordinator will report directly to the LCCU General Manager and will responsible for managing the consultants working on the project, coordinating activities and reporting.

5.7 The Ministry of Agriculture will be a key stakeholder and beneficiary of the project, assigning 4 extension officers in the field to support producers. These extension officers who are already assigned by the Ministry of Agriculture to the Laborie region, will receive training in climate smart agriculture (CSA) and climate resilience practices supported by financing of the technical co-operation. On completion of this training, the agricultural officers, working closely with technical leads at the LCCU will provide ongoing support and advice to farmers in the adoption of climate resilient practices and implementation of new technologies. This arrangement will be confirmed by a Memorandum of Understanding that will be signed between the Ministry of Agriculture and the LCCU as a condition precedent for the first disbursement of the TC.

5.8 A Steering Committee will be established to oversee the project implementation. The membership and structure of the Steering Committee will include the following: (i) General Manager Laborie Credit Union or his designate (Chair); (ii) 1 additional representative from the Laborie Credit Union; (iii) 1 representative from BBFC; (iv) 1 representative from LFCC; (v) 1 representative from the Ministry of Agriculture; (vi) the project coordinator, who will act as the Steering Committee secretariat; and (vii) 1 MIF representative as an observer. During the first year of the project, the Steering Committee will meet at least every month thereafter at least every quarter.

15

VI. Compliance with Milestones and Special Fiduciary Arrangements 6.1 Disbursement by Results, Fiduciary Arrangements. The Executing Agency

will adhere to the standard MIF disbursement by results, IDB’s procurement policy36 and financial management37 arrangements as specified in Annex V.

VII. Information Disclosure and Intellectual Property 7.1 Information Disclosure. Project information is confidential in accordance with the

IDB’s Access to Information Policy. 7.2 Intellectual Property. The IDB will own relevant IP rights related to the project.

36 Link to the Policy: Procurement of Works and Goods Policy 37 Link to the document Financial Management Operational Guidelines

ANNEX I: RESULTS MATRIX PPCR SAINT LUCIA: DEVELOPING AND FINANCING A CLIMATE-SMART AGRICULTURE BUSINESS MODEL

RG-T2935

38 To be defined

Project Objective

The main objective of the project is to strengthen the viability of agri-business operators in the southern region of St. Lucia within the context of climate change.

Results Indicators Baseline Year 1 Year 2 Year 3 Target Notes

Number of people who adopt new ( climate resilient) practices or technologies (CRF 210400)(disaggregated by technology)

0 44 105 147 147 LCCU Green Finance Portfolio registry

Markets that emerged with MIF support (CRF 450600) 0 6 10 13 13 Contracts subscribed by BBFC

Tons of CO2e in GHG emissions avoided (CRF 340100)

0 tbd38 tbd tbd tbd LCCU controls by green product financed

Number of Hectares of land treated sustainably (CRF 240100) 0 35 65 85 85 LCCU green finance

Productivity gain per hectare (measured as total yield per hectare of beneficiaries who adopt new technologies) 0 15 25 30 40%

Baseline report; Monitoring system reports

Component 1: Technical Cooperation Subcomponent 1: Strengthen Market Linkages and Production of producers in the BBFC and LFCC Baseline Year 1 Year 2 Year 3 Target Notes

Number of members at the BBFC cooperative (disaggregated by gender)

32 men 5 Women

72m 25w

102m 40w

142m 50w

142m 50w

BBFC membership registry

Number of people trained (CRF 110100) (disaggregated by gender)

32m 5w

82m 30w

112m 45w

152m 55w

152m 55w

Training sessions controls

Subcomponent 2: Expanding Access to Climate Resilient Baseline Year 1 Year 2 Year 3 Target Notes

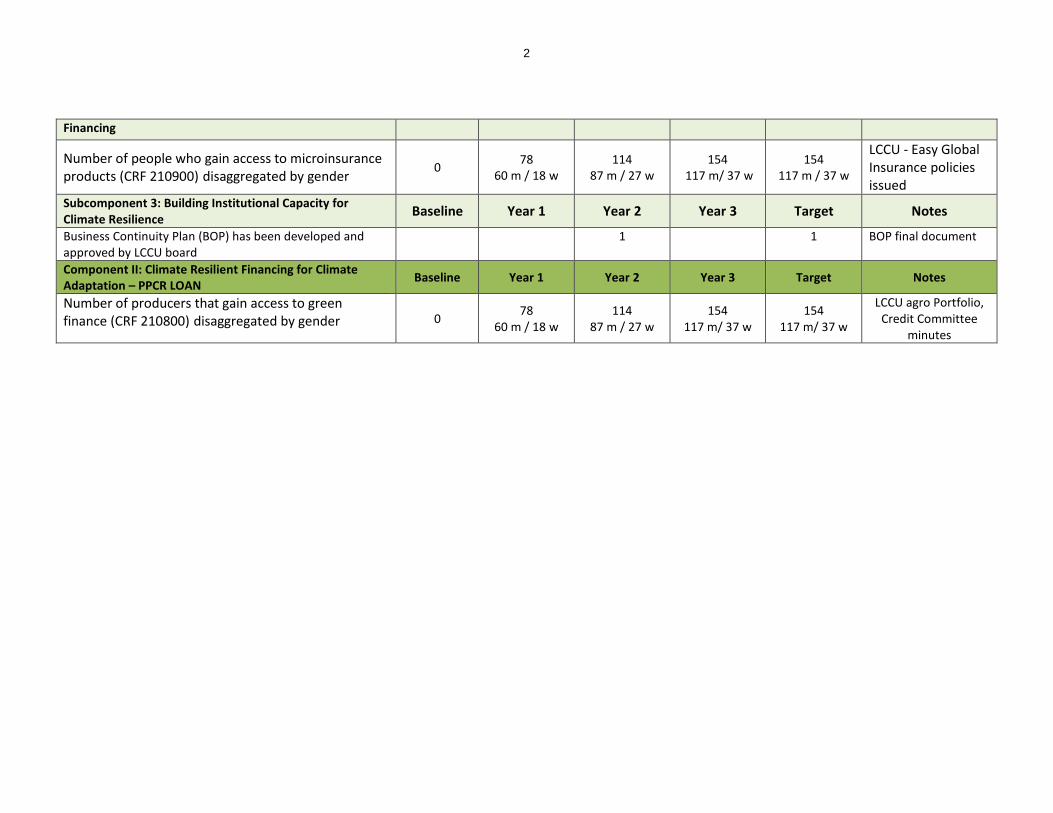

Number of people who gain access to microinsurance products (CRF 210900) disaggregated by gender 0 78

60 m / 18 w 114

87 m / 27 w 154

117 m/ 37 w 154

117 m / 37 w

LCCU - Easy Global Insurance policies issued

Subcomponent 3: Building Institutional Capacity for Climate Resilience Baseline Year 1 Year 2 Year 3 Target Notes

Business Continuity Plan (BOP) has been developed and approved by LCCU board

1 1 BOP final document

Component II: Climate Resilient Financing for Climate Adaptation – PPCR LOAN Baseline Year 1 Year 2 Year 3 Target Notes

Number of producers that gain access to green finance (CRF 210800) disaggregated by gender 0 78

60 m / 18 w 114

87 m / 27 w 154

117 m/ 37 w 154

117 m/ 37 w

LCCU agro Portfolio, Credit Committee

minutes

ANNEX II BUDGET SUMMARY RG-T1235 Developing and Financing A Climate-Smart Agriculture Business Model

In Saint Lucia PROADAPT MIF PPCR Counterpart Contribution TOTAL

COMPONENT 1: TECHNICAL COOPERATION

Subcomponent I: Strengthen Market Linkages and Production for BBFC Membership & LFCC

$ 130,000.00

$ 95,440.00

$ -

$ 383,920.00

$ 609,360.00

1.1 Business Development Consultant (Needs assessment, baseline study of producers, analysis of purchasing patterns of targeted customers, organizational development strategy and proposed structure, strategic and business plan)

$ 30,000.00 $

- $ 30,000.00

1.2 Workshops / meeting logistics $ 10,000.00 $

- $ 10,000.00

1.3 Production Consultancy $ 72,000.00 $

36,000.00 $ 108,000.00

1.4 Agricultural Field Officers (field visits and travel) $ 13,440.00 $

6,720.00 $ 20,160.00

1.5 Training of agricultural field officers $ 25,000.00 $

- $ 25,000.00

1.6 Agricultural Officer $ 259,200.00

$ 259,200.00

1.7 ITC Platform $ 10,000.00 $

- $ 10,000.00

1.8 Climate Resilient / Agricultural Specialist (climate adaptation practices existing and new, research technology)