Page 1

Document of

The World Bank

FOR OFFICIAL USE ONLY

Report No. 62013-UG

INTERNATIONAL DEVELOPMENT ASSOCIATION

PROGRAM DOCUMENT

FOR FINANCIALSECTOR DEVELOPMENT POLICY CREDIT

IN THE AMOUNT OF SDR 30.9 MILLION

(US$50 MILLION EQUIVALENT)

TO

THE REPUBLIC OF UGANDA

May 31, 2011

Finance and Private Sector Development

Africa Region

This document has a restricted distribution and may be used by recipients only in the

performance of their official duties. Its contents may not otherwise be disclosed without World

Bank authorization.

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Page 2

i

UGANDA – GOVERNMENT FISCAL YEAR

July 1 – June 30

CURRENCY EQUIVALENTS

(Exchange Rate Effective as of May 27, 2011)

Currency Unit Uganda Shillings

US$1.00 = 2,387 UGS

Weights and Measures Metric System

ABBREVIATION AND ACRONYMS

ACGC Audit Committee and Governance Committee

AG Auditor General

AGO Accountant General‘s Office

BoU Bank of Uganda

CAS Country Assistance Strategy

CFAA Country Financial Accountability Assessment

CMA Capital Market Authority

CPAR Country Procurement Assessment Report

CPI Consumer Price Index

CRB Credit Reference Bureau

CSD Central Securities Depository

DFID Department for International Development (UK)

DPC Development Policy Credit

EAC East African Community

EFT Electronic Fund Transfer

FIA Financial Institutions Act

FMDP Financial Market Development Plan

FSAP Financial Sector Assessment Program

GDP Gross Domestic Product

GNI Gross National Income

GoU Government of Uganda

GIZ Gesellschaft für Internationale Zusammenarbeit

HIPC Heavily Indebted Poor Countries

IDA International Development Association

IFAD International Fund for Agricultural Development

IFRS International Financial Reporting Standards

IMF International Monetary Fund

IPSAS International Public Sector Accounting Standards

JAF Joint Assessment Framework

JBS Joint Budget Support

JSAN Joint Staff Assessment Note

KfW Kreditanstalt fur Wiederaufbau

LIS Land Information System

M&E Monitoring and Evaluation

MDIs Micro Deposit Institutions

Page 3

ii

MFI Micro Finance Institutions

MoFPED Ministry of Finance, Planning and Economic Development

MoPS Ministry of Public Service

MoTTI Ministry of Tourism, Trade and Industry

MSCL Microfinance Support Center Limited

MTEF Medium Term Expenditure Framework

NDP National Development Plan

NGO Non-Governmental Organization

NIMES National Integrated Monitoring and Evaluation Strategy

NPS National Payment System

NSSF National Social Security Fund

OAG Office of Auditor General

OPM Office of the Prime Minister

PCC Policy Coordination Committee

PEAP Poverty Eradication Action Plan

PERD Public Enterprise Reform and Divestiture

PFM Public Financial Management

PPDA Public Procurement and Disposal of Public Assets Act

PPP Public Private Partnership

PROST Pension Reform Operational Strategies and Tools

PRSC Poverty Reduction Support Credit

PRSP Poverty Reduction Strategy Paper

PSI Policy Support Instrument

PSIA Poverty and Social Impact Assessment

PSPF Public Service Pension Fund

PUSRP Privatization and Utility Sector Reform Program

RFSS Rural Financial Services Strategy

ROC Regional Operations Committee

RTGS Real Time Gross Settlement

SACCOs Savings and Credit Associations

SCP Small Claims Procedure

UBOS Uganda Bureau of Statistics

UCSCU Uganda Credit and Savings Cooperative Union

UPSPS United Public Sector Pension Scheme

URA Uganda Revenue Authority

Vice President:

Country Director:

Acting Sector Manager:

Task Team Leader:

Obiageli Katryn Ezekwesili

John Murray McIntire

Michael Fuchs

Javier Suarez

Page 5

THE REPUBLIC OF UGANDA

FINANCIAL SECTOR DEVELOPMENT POLICY CREDIT

TABLE OF CONTENTS

CREDIT AND PROGRAM SUMMARY ...................................................................................... 1 I. INTRODUCTION ............................................................................................................... 3 II. COUNTRY CONTEXT ...................................................................................................... 3

RECENT ECONOMIC DEVELOPMENTS IN UGANDA .................................... 3 MACROECONOMIC OUTLOOK AND DEBT SUSTAINABILITY ................... 6

III. THE GOVERNMENT’S PROGRAM AND PARTICIPATORY PROCESSES .......... 8 IV. BANK SUPPORT TO THE GOVERNMENT’S PROGRAM ....................................... 9

LINK TO CAS AND NEW AFRICA STRATEGY ................................................ 9 COLLABORATION WITH THE IMF AND OTHER DONORS .......................... 10 RELATIONSHIP TO OTHER BANK OPERATIONS ........................................... 10 LESSONS LEARNED ............................................................................................. 11 ANALYTICAL UNDERPINNINGS ....................................................................... 12

V. THE PROPOSED FINANCIAL SECTOR DEVELOPMENT POLICY CREDIT ..... 12 OPERATION DESCRIPTION ................................................................................ 12 POLICY AREAS ..................................................................................................... 12

VI. OPERATION IMPLEMENTATION ............................................................................... 30 POVERTY AND SOCIAL IMPACTS .................................................................... 30 ENVIRONMENTAL ASPECTS ............................................................................. 30 IMPLEMENTATION, MONITORING AND EVALUATION ........................ 30 FIDUCIARY ASPECTS .......................................................................................... 31 DISBURSEMENT AND AUDITING ..................................................................... 33 RISKS AND RISK MITIGATION .......................................................................... 34

ANNEXES ANNEX 1: LETTER OF DEVELOPMENT POLICY ................................................................................ 36 ANNEX 2: FINANCIAL SECTOR DEVELOPMENT POLICY MATRIX ............................................. 61 ANNEX 3: FUND ASSESMENT LETTER .................................................................................................. 63 ANNEX 4: UGANDA AT A GLANCE ......................................................................................................... 66 ANNEX 5: MAP UGA33504 .......................................................................................................................... 69

TABLES

Table 1: Selected Macro Indicators 2008/09-2013/14 ........................................................................ 5

Table 2: Ugandan Pension Schemes ................................................................................................. 14

Table 3: Sequencing of actions for pension reform ........................................................................ 17

Box 1: Prior Actions for Uganda First Financial Sector Development Credit ............................ 28 Box 2: Good Practice Principles for Conditionality ....................................................................... 31

This operation was prepared by an IDA team consisting of Javier Suarez (Task Team Leader) and Moses

Kibirige (AFTFE); Manush A. Hristov ( LEGAF); Antony Randle and Simon Walley (GCMNB); Rachel

Sebbudde and Jos Verbeek (AFTP2); Rajiv Sondhi (CTRFC); Howard Centenary (AFTPC); and Paul

Kamuchwezi (AFTFM). The team benefited from extensive preparatory work done by Ravi Ruparel (AFTFE).

Peer reviewers were Dino Merotto (ECSP3) and Heinz Rudolph (GCMNB).

Page 7

1

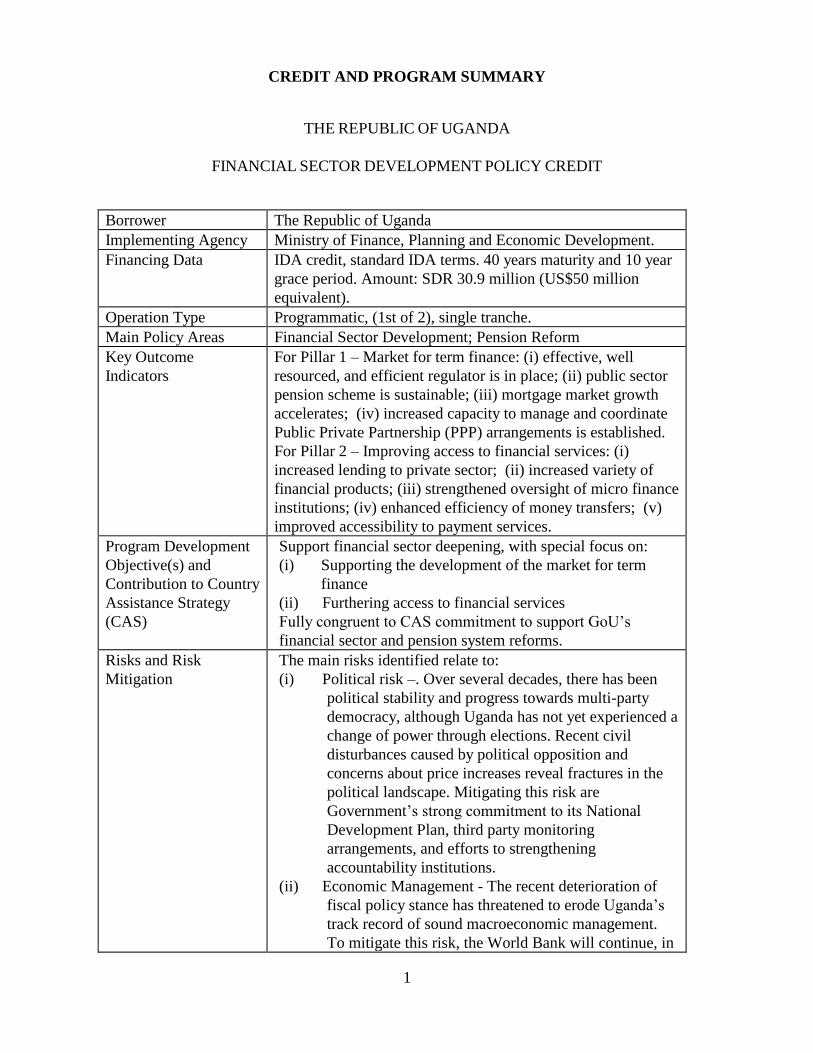

CREDIT AND PROGRAM SUMMARY

THE REPUBLIC OF UGANDA

FINANCIAL SECTOR DEVELOPMENT POLICY CREDIT

Borrower The Republic of Uganda

Implementing Agency Ministry of Finance, Planning and Economic Development.

Financing Data

IDA credit, standard IDA terms. 40 years maturity and 10 year

grace period. Amount: SDR 30.9 million (US$50 million

equivalent).

Operation Type Programmatic, (1st of 2), single tranche.

Main Policy Areas Financial Sector Development; Pension Reform

Key Outcome

Indicators

For Pillar 1 – Market for term finance: (i) effective, well

resourced, and efficient regulator is in place; (ii) public sector

pension scheme is sustainable; (iii) mortgage market growth

accelerates; (iv) increased capacity to manage and coordinate

Public Private Partnership (PPP) arrangements is established.

For Pillar 2 – Improving access to financial services: (i)

increased lending to private sector; (ii) increased variety of

financial products; (iii) strengthened oversight of micro finance

institutions; (iv) enhanced efficiency of money transfers; (v)

improved accessibility to payment services.

Program Development

Objective(s) and

Contribution to Country

Assistance Strategy

(CAS)

Support financial sector deepening, with special focus on:

(i) Supporting the development of the market for term

finance

(ii) Furthering access to financial services

Fully congruent to CAS commitment to support GoU‘s

financial sector and pension system reforms.

Risks and Risk

Mitigation

The main risks identified relate to:

(i) Political risk –. Over several decades, there has been

political stability and progress towards multi-party

democracy, although Uganda has not yet experienced a

change of power through elections. Recent civil

disturbances caused by political opposition and

concerns about price increases reveal fractures in the

political landscape. Mitigating this risk are

Government‘s strong commitment to its National

Development Plan, third party monitoring

arrangements, and efforts to strengthening

accountability institutions.

(ii) Economic Management - The recent deterioration of

fiscal policy stance has threatened to erode Uganda‘s

track record of sound macroeconomic management.

To mitigate this risk, the World Bank will continue, in

Page 8

2

close coordination with the International Monetary

Fund (IMF), its monitoring and policy dialogue on

economic policies.

(iii) Public Financial Management and Procurement –

While Uganda‘s budget is published, the absence of an

integrated accounting to capture projects outside the

consolidated fund, and the variance of actual

expenditure to original budget, undermines budget

transparency. This situation is compounded by

insufficient capacity in the procurement oversight

body and procuring entities and lacking compliance

with procedures in oversight and procurement audit

and effective planning and conducting procurement.

To help mitigate this risk, the World Bank is

supporting efforts to address the weaknesses in the

Public Financial Management (PFM) system. The

World Bank is also engaged in coordination with other

development partners to help strengthen procurement

regulations and procedures.

(iv) Fraud and Corruption - Petty and high-level corruption

is prevalent. The World Bank is working with the

GoU to reinvigorate institutions and accountability

systems, rethinking decentralization policies, and re-

launching stalled public service reform processes.

Operation ID P117979

Page 9

3

IDA PROGRAM DOCUMENT FOR A

PROPOSED FINANCIAL SECTOR DEVELOPMENT POLICY CREDIT

TO THE REPUBLIC OF UGANDA

I. INTRODUCTION

1. This program document presents a proposed Financial Sector Development

Policy Credit to the Republic of Uganda for an amount of SDR 30.9 million (US$50

million equivalent) for the period FY10-FY11. This would be the first in a programmatic

series of two operations supporting Government of Uganda‘s efforts to further financial sector

development. The proposed operation is fully congruent with the National Development Plan

for 2010/2015 and the Financial Markets Development Plan for 2008-2012 which the

authorities have started to implement.

II. COUNTRY CONTEXT

RECENT ECONOMIC DEVELOPMENTS IN UGANDA

2. Over the last two decades, Uganda’s economy has achieved noteworthy growth

supported by a prudent macroeconomic framework and propelled by consistent policy

reforms. Annual growth in real GDP averaged 7.4 percent over the 10 years ending in

2009/10, compared with 6.5 percent recorded in the 1990s. This was achieved in spite of

consecutive exogenous shocks including: oil price shocks; prolonged drought conditions with

adverse effects on energy generation and agricultural production; and volatile and increasing

food prices. The translation into similar gains in per capita income, however, has been less

pronounced due to high population growth. Consequently the gross domestic product (GDP)

per capita grew merely 4.0 percent per year over the last decade.

3. The global economic slowdown has been felt in Uganda, as reflected in the

deceleration of GDP growth, but medium-term growth prospects remain solid. GDP

growth in 2009/10 was 5.2 percent, 2.0 percentage points lower than in 2008/09 (Table 1).

This relatively weaker performance was explained by lower external and domestic demand,

demonstrating itself in particular through a slowdown in the construction sector. Economic

activity has rebounded in 2010/11, supported by a strong recovery in credit to private sector

and faster growth in the services sector, resulting in a projected GDP growth of 6.4 percent.

Fueled by persistent weak current account balances and uncertainty related to Presidential

Elections, the Uganda shilling depreciated significantly in the first half of 2011. Inflation

increased and has reached double digits in March 2011, driven by high food and fuel price

inflation. As of April 2011, consumer price index (CPI) inflation stands at a non-seasonally

adjusted 14.1 percent.

4. Fiscal policy stance deteriorated in the run up to the election of February 2011.

Overall spending is estimated to increase by 3.7 percentage points of GDP this FY10/11,

compared to FY09/10. Of this increase, 1.6 percentage points was above the originally

approved budget by parliament for this FY. The main cause of this increase was unplanned

security related expenditures amounting to 2.6 percent of GDP alone in FY10/11. Even

though revenues performed better than planned, the overall deficit after grants is now

Page 10

4

expected to reach 6.3 percent of GDP for FY10/11, well above the 4.7 percent of GDP last

FY.

5. Two supplemental budgets had to be issued amounting to 4.6 percent of GDP, up

from an already large 2.8 percent of GDP in FY09/10, and below 1 percent the year

before. This was to allow for the unplanned security related expenditures and the re-

composition of expenditures to accommodate un-programmed election related outlays. As not

all of the supplemental authorization has led to increased spending, this has led to an

adjustment in the composition of expenditures. The priority sectors, health education, water,

and works and roads, have also been affected. Their releases are down by 0.5 percent of GDP

for the first three quarters of this FY. The main priority sector affected has been ‗works and

roads‘ which has received only 66 percent of its original allocation.

6. The IMF Executive Board decided in February 2011 not to complete the first

review of the Policy Support Instrument (PSI) program due to the first supplementary

budget passed in early January which put the PSI program objectives at risk. However,

since then the IMF mission, who visited Uganda in March/April this year and the authorities,

reached an understanding on macroeconomic and structural policies that are consistent with

the objectives of the PSI. The agreed stance of fiscal policies aims to bring the budget, in

particular for FY11/12, back in line with the original PSI. The program focuses on rebuilding

the cushions in fiscal balances and international reserves of which the latter had declined

significantly to allow for the security related expenditures. Foreign reserves are projected to

fall to 3.4 months of imports by end of FY10/11, down from a comfortable 4.7 in FY09/10.

On the basis of the understanding reached during the discussion with the authorities, the IMF

mission is recommending to its management to complete the second review of the PSI by the

end of June 2011.

7. Uganda’s banking sector remains sound and well-capitalized despite the

international financial crisis. In Uganda, there were two main channels through which the

global financial crisis could have impacted the financial sector: through direct contagion and

through the indirect impact of global downturn on domestic economic activity. Ugandan

financial sector was relatively immune from direct contagion given the minimal exposure of

banks to toxic assets. Banks‘ holdings in foreign assets amounted to only 12 percent of total

assets at the end of 2008, and most of these assets were deposits in correspondent banks which

remained in sound conditions. Moreover, Ugandan banks‘ reliance on short term finance from

foreign institutions to fund their asset portfolio is limited; at the end of 2008, liabilities to

foreign institutions stood at about 4 percent of total liabilities. Ugandan banks were,

therefore, largely immune from losses of liquidity when global credit crunch triggered a

reversal of financial flows to emerging markets. Nonetheless, the economic slowdown had,

and is still having, an impact in the financial sector, though. The rapid growth in assets and

profitability which characterized the banking sector in 2007 and 2008 slowed markedly in

2009. Growth in total assets fell from 35 in 2008 to 16 percent in 2009, and the share of

nonperforming loans almost doubled, reaching 4.4 percent at the end of 2009. The

profitability of the banking system, as measured by the average return on assets, fell from 3.5

percent in 2008 to 3 percent in 2009. The banking system remained profitable on aggregate

and generated sufficient profits to maintain its core capital to risk weighted asset ratio at close

to 19 percent. Preliminary figures for 2010 show an improvement of performance indicators

Page 11

5

with share of nonperforming loans back to 2.1 percent. Overall profitability remained low, at

about 2.7 percent, partly explained by new bank entries.

Table 1: Selected Macro Indicators 2008/09-2013/14

Indicators

2008/091 2009/10

1 2010/11

2 2011/12

2 2012/13

2 2013/14

2

(Annual percentage change)

Domestic prices

Headline inflation 14.2 9.4 6.4 12.5 6.4 5.2

National income accounts

Agriculture 2.9 1.8 2.7 3.0 3.0 3.8

Manufacturing 10.0 7.4 5.8 5.7 7.0 7.0

Services 8.8 6.6 7.3 7.6 7.0 7.8

Total GDP at market prices 7.2 5.2 6.4 6.6 6.8 7.0

GDP per capita 3.9 1.9 3.1 3.3 3.7 3.7

(As percentage of GDP at market prices)

Real Sector

Gross domestic investment 23.5 24.3 25.4 27.9 29.4 28.5

Public investment 5.4 6.6 7.8 10.3 11.6 10.4

Private investment 18.0 17.7 17.6 17.6 17.8 18.0

Gross domestic savings (excl. grants) 13.1 13.1 12.5 15.5 18.0 17.4

Public 0.6 -0.8 -2.9 2.6 3.2 3.5

Private 12.5 13.9 15.4 12.9 14.8 13.9

External Sector

Current account balance (incl. grants) -7.8 -8.8 -4.3 -9.9 -9.3 -9.2

Current account balance (excl. grants) -10.4 -11.3 -12.9 -12.4 -11.4 -11.0

Exports of goods & nonfactor

services

19.6 20.3 22.2 21.3 21.8 22.4

Imports of goods & nonfactor

services

34.1 33.7 38.3 36.6 36.2 36.5

External Debt to GDP ratio 19.6 20.1 23.3 25.7 26.3 26.4

Debt service to exports ratio 3.5 4.4 6.1 6.6 7.6 8.2

Public debt service to exports ratio 0.7 1.6 1.5 1.7 2.0 2.1

Foreign reserves (in months of imports) 5.1 4.7 3.4 3.1 3.3 3.5

Government Finance

Domestic Revenue 12.5 12.4 13.2 13.8 14.0 14.2

Total expenditure and net lending 17.3 19.8 23.9 21.4 22.4 21.1

Overall balance (excl. grants) -4.8 -7.4 -10.7 -7.7 -8.4 -6.9

Overall balance (incl. grants) -3.1 -4.7 -6.3 -3.5 -4.6 -3.3

Domestic borrowing 0.2 2.2 -0.5 2.1 1.8 1.4

Net Foreign financing 2.0 2.2 2.5 3.1 4.5 3.6

Notes: 1. Estimate.

2. Projection.

Sources: Ugandan Authorities; and staff estimates and projections.

8. A large portion of the Ugandan population does not have access to any kind of

financial services. Despite considerable progress in the expansion of Uganda‘s financial

services, 28 percent of Ugandans (18 years old and above) remain unserved by any kind of

financial institution, formal or informal. The proportion of the population served by formal

Page 12

6

institutions is only 28 percent.1 Uganda suffers from a low savings rate, low levels of lending,

and high intermediation costs and margins. While liquidity within the system is considerable,

banks prefer to invest in treasury securities rather than servicing a broader segment of the

enterprise sector.

9. The local market for term finance remains underdeveloped. The financial system

is able to provide bank financing for segments of the enterprise sector, however financing for

maturities longer than seven years is largely unavailable. This is a major constraint to the

financing of much-needed infrastructure investment and severely curtails the development of

finance for the housing market. The dearth of investment in infrastructure has repeatedly been

identified as a major constraint to economic development. Despite the increase in private

sector activity over the last decade, few private sector companies have accessed the capital

markets in Uganda to meet their term financing needs. The majority of businesses in Uganda

rely on internal funds to meet their term financing needs. The bond market is dominated by

the Government. There are currently 21 government bonds on the market for a total value of

UGX 984 billion, while the five corporate bonds represent about UGX 100 billion. The

average maturity for government bonds is 3.8 years, while corporate bonds have a longer

average maturity – 8.2 years.

MACROECONOMIC OUTLOOK AND DEBT SUSTAINABILITY

10. Uganda’s macroeconomic framework is deemed appropriate to support the

proposed operation. The authorities are committed to return to prudent fiscal management

and to ensure budget allocations are in line with National Development Plan (NDP) priorities.

The envisaged budget for FY11/12 will figure a significant adjustment, as well as expansion

of infrastructure spending. The overall balance is expected to shrink by close to 3 percent of

GDP (including grants) as exceptional security-related spending winds down. Banking system

financing of the deficit will be limited to drawing down deposits (including from exceptional

oil exploration tax earnings) to finance initiation of a large hydropower project. The proposed

medium term expenditure framework for FY11/12 to FY15/16 appears sound and coherent. It

features moderate fiscal deficits and maintains significant expenditures in infrastructure to

address key biding constrains to growth. The effectiveness and efficiency of the

implementation of government‘s policies will hinge on the quality of Public Financial

Management (PFM) and procurement systems. The authorities are committed to strengthen

accountability and efficiency of these systems and are engaged with donors, including in the

context of general budget support and its related Joint Assessment Framework which details

specific performance indicators.

11. Uganda’s medium term growth prospects remain solid. In the medium term

growth is projected to remain robust, averaging about 7 percent in the next few years. A

critical part of the government‘s economic development strategy is to focus on eliminating

infrastructure constraints and strengthening competitiveness in export markets, in particular

for processed agricultural products as a means to sustain growth. In the short to medium term

Uganda‘s growth is expected to remain robust as agricultural production in the northern

region continues to rebound with the return to peace and as regional demand for Uganda‘s

exports grows. The focus on improving productivity – supported by more effective financial

1 FINSCOPE Uganda 2009, Final Report.

Page 13

7

intermediation - will also be critical to help mitigate the adverse impact of possible real

exchange rate appreciation brought on by oil sector investment and production.

12. In the medium to long term, growth will for a large extent depend on the ability

of the authorities to harness effectively the anticipated resources from oil exploration.

Growth will hinge on prudent macroeconomic management in the presence of oil revenue

inflows, the ability to channel the fiscal resources from oil to the most productive public

investments, the management of the fiscal revenue streams from the oil sector, and the pace of

productivity growth and skills development in the labor force. Related medium term

challenges to be addressed to sustain Uganda‘s economic growth and poverty reduction

include monitoring and if possible addressing Uganda‘s demographic dynamics, addressing

inefficiency in public service delivery, and tackling emerging skills gaps as the economy

continues to transform.

13. Uganda’s oil discoveries promise significant increases in domestic revenues in the

longer-term. Even though production is anticipated to begin in 2013, peak production, which

is likely to be roughly 175,000 barrels per day, is to be reached in 2017. This rate of

exploration could be sustained for 10-20 years. Although oil price volatility makes it difficult

to predict the revenue stream from oil, public revenues are projected to increase by 10

percentage points of GDP at the height of production i.e. in six to ten years. Based on an oil

price of US$80 per barrel, export receipts will reach close to US$4 billion when production

peaks to slowly decline as domestic demand increases and to decline more drastically when

oil exploration declines towards the end of the 2020. Large supportive investments in

infrastructure will be needed between now and 2017 to produce, transport, export and refine

the oil so there remains considerable uncertainty regarding the time frame for reaching peak

oil production and revenue generation.2

14. The Government will continue to require external financing to maintain its fiscal

policy for growth. Domestic revenue mobilization remains low, at 13 percent in FY10/11

and is not expected to increase beyond 15 percent in the medium term. Therefore, further

external financing, concessional as well as non-concessional, will be required to sustain fiscal

policy. The non-concessional borrowing is to mainly address the infrastructural deficit in

roads and energy. These investments will be effective if Government also addresses

absorption capacity and implementation problems in the infrastructure development programs,

particularly in the roads sector. The fiscal deficit (including grants) is projected to decline to

3.3 percent of GDP by FY13/14 through increased tax revenues, partly due to elimination of

various tax exemptions, and containment of recurrent expenditures (see Table 1).

15. The external financing requirements are driven by the needed investments in the

oil sector and in public infrastructure. Imports are projected to increase significantly to

provide for the goods needed to prepare the oil sector for production and for the planned

public investments in energy and roads. The oil sector investments are anticipated to be

financed through direct foreign investments while the imports needed for the public

investments in infrastructure are financed through grants and concessional as well as non-

2 A detailed analysis of impact of oil sector in Uganda is included in the Annex 6 of the Country Assistance

Strategy for Uganda for FY11/15 (World Bank Report No. 54187-UG).

Page 14

8

concessional borrowing. Additional external resources are needed to rebuild Uganda‘s

foreign reserves. Foreign reserves remain relatively low compared to overall imports.

16. Uganda’s risk of debt distress is low as a result of international debt relief and

prudent macro management. The authorities intend to continue to rely on concessional

assistance to finance their public infrastructure investment in the coming years, but increase

gradually their use of non-concessional funds as they build up their debt management

capacity. The preliminary results of the 2011 Joint Debt Sustainability Analysis update

suggest that all parameters for sustainability are within the prescribed thresholds and the risk

of debt distress is low.3 Even as the non-concessional limits are increased to US$800 million,

the debt service ratios remain robust under most of the standard stress tests. The sensitivity of

Uganda‘s debt indicators to a growth shock suggests that careful selection of public

investment projects have a key role to play in the maintenance of debt sustainability over the

near and medium term, requiring continued attention from the Ugandan authorities to

improving investment planning processes and strengthening implementation capacity. As

domestic financial market develops, improved availability and allocation of savings will help

satisfy Uganda‘s investment needs.

III. THE GOVERNMENT’S PROGRAM AND PARTICIPATORY PROCESSES

17. The authorities completed the preparation of the National Development Plan for

2010/11-2014/15 (NDP) in March 2010. The NDP succeeds to the third Poverty Eradication

Action Plan and broadens its strategic focus to structural transformation to raise growth and

living standards sustainably. During implementation of the third PEAP, the government‘s

strategy began to shift towards a greater focus on economic growth and reduction in income

poverty. Building on achievements under the Poverty Eradication Action Plan (PEAP), the

NDP aims at fostering skilled employment growth and a sectoral shift to higher value-added

activities. The NDP identifies four priority targets: (i) human resource development through

health, education and skills building; (ii) boosting up physical infrastructure, particularly in

the energy and transportation areas; (iv) supporting science, technology and innovation; and

(iv) facilitating private access to critical production inputs, particularly in agriculture.

18. The National Development Plan was developed through an extensive and broad-

based country-driven consultative process. Consultations have been held at local and

sector level, and have included representatives from the public sector, private sector and civil

society organizations. They combined a bottom-up and top-down approach through active

consultations with the grass-root stakeholder, including at the local government level. Cabinet

discussions helped build further ownership within Government. The NDP reflects, therefore, a

broad national consensus on country‘s strategy for growth, social progress, and governance.

As part of the NDP monitoring and evaluation strategy, Government is launching sub-county

level barazas - an annual forum for communities to hold public officials to account for public

service delivery. Local governments, civil society and the private sector have broadly

expressed consent and support for the NDP‘s focus on growth-enhancing investments, social

equity and improved governance, while cautioning Government to ensure that the growth

agenda does not compromise goals in the social sectors, particularly health and education.

3 Uganda: Joint IMF/World Bank Debt Sustainability Analysis, 2011.

Page 15

9

19. The NDP identifies three objectives for the financial sector. The first one is to

promote a sound, vibrant and deep financial system. Areas of interventions under this

objective include: strengthening of regulatory environment; strengthening of payment

systems; promoting competition and prudence in the sector; encouraging product innovations;

promoting expansion of banking services to rural areas; strengthening property and land rights

legislation; and strengthening anti-money laundering framework. The second objective is to

increase access to affordable long term finance. Specific areas of intervention are:

strengthening institutional arrangements for mobilizing long-term funds; and reforming the

pension sector and promoting savings mobilization. The third objective is to attain further

integration of financial services within the East African Community (EAC), focusing on the

harmonization on financial sector policies across the Community. The objectives and areas of

interventions outlined in the NDP are fully congruent with the Financial Markets

Development Plan for 2008-2012. Implementation of the Financial Market Development Plan

started in 2008, supported notably by Bank‘s second Private Sector Competitiveness Project.

20. Government’s efforts to reform financial sector have made tremendous strides in

establishing a sound, profitable, and growing financial system. Financial sector reform

has been at the core of Government‘s economic reform program since the late 1980s. The first

generation of financial sector economic reforms focused on liberalization of financial markets,

institutional reforms to the prudential regulatory framework, and divestiture of government

owned financial institutions. These reforms were supported, notably, by a Financial Sector

Adjustment Credit which focused on strengthening Bank of Uganda, and the banking system

as a whole, to increase the efficiency of financial intermediation and contribute to sustainable

growth and mobilization of domestic savings over the long term. These reforms have led to a

stronger and more efficient financial sector, which performs relatively well a number of

crucial tasks, such as banking for medium to large corporations and providing payments and

savings services to sizeable segments of the population. Since the removal of the moratorium

on the licensing of new banks in 2007, the sector is also showing signs of increased

competition, notably through marked branch expansion and the introduction of new products

such as mobile phone financial services.4

21. The authorities acknowledge that further efforts are needed to increase

intermediation and savings mobilization in support of higher and more diversified

economic growth and increased poverty reduction. Much needs to be done to improve the

depth and breadth of the financial sector while maintaining stability, and allowing the

financial sector to fully play its role of catalyst for economic growth.

IV. BANK SUPPORT TO THE GOVERNMENT’S PROGRAM

LINK TO CAS AND NEW AFRICA STRATEGY

22. The proposed operation is congruent with the Country Assistance Strategy

(CAS), presented to the Board of Executive Directors in May 2010, and to the new

Africa Strategy. The CAS supports GoU‘s medium-term goals of accelerating economic

growth, transforming the structure of the economy, raising employment and ensuring

prosperity. As underscored in the NDP, the development of a resilient, competitive, and

4 Since 2007, the Bank of Uganda has licensed seven new commercial banks and one credit institution, raising

the number of banks to 21 and credit institutions to 4.

Page 16

10

effective financial system constitutes a critical, though not sufficient, enabling element to

achieve Uganda‘s economic and social development objectives. Countries with higher levels

of financial development experience better resource allocation, higher GDP per capita growth,

and faster rates of poverty reduction. In congruency with the CAS, the proposed operation

would support Government‘s efforts to further financial sector development, including

through pension system reforms. The proposed operation will support pension reform by

improving the regulatory framework and strengthening both public and private pension

schemes; and it will complement current Bank‘s support to the implementation of

government‘s 2008-2012 Financial Market Development Plan (FMDP) to improve access to

financial services and the availability of term finance.5 This operation is fully aligned with the

first pillar of Africa Strategy, namely the competitiveness and employment pillar.

COLLABORATION WITH THE IMF AND OTHER DONORS

23. Collaboration between the Bank and Fund in Uganda is strong. Government‘s

macroeconomic program has been supported in recent years by successive three year IMF

Policy Support Instrument (PSI) arrangements; the current one started in July 2010. The IMF

Executive Board decided in February 2011 not to complete the first review of the PSI due to a

supplementary budget passed in early January which put program objectives at risk. During

subsequent discussions in March 2011 the authorities and the IMF mission reached

understandings ad referendum on macroeconomic and structural policies that are consistent

with the objectives of the PSI. The second review of the program is expected to be presented

for consideration by the IMF Executive Board before the end of June 2011. The Bank and

IMF collaborate on fiscal and financial support issues, including in the follow-up to the 2005

Financial Sector Assessment and the preparation of the planned Financial Sector Assessment

(August, 2011).

24. This operation was prepared in consultation with other Development Partners

active in the financial sector, notably the International Monetary Fund and the German

cooperation agency (Gesellschaft für Internationale Zusammenarbeit - GIZ), and United

Kingdom Department for International Development (DFID).

RELATIONSHIP TO OTHER BANK OPERATIONS

25. World Bank Group engagement is aligned with NDP and covers the main

strategic axes of Uganda’s development strategy. It uses harmonized instruments such as

programmatic development policy lending, investment lending, and joint analytical and

advisory services. The Second Private Sector Competitiveness Project comprised a component

to support financial sector deepening, which enabled targeted activities, including support for

the drafting of commercial and financial legislation and the establishment of the Credit

Reference Bureau. This project directly financed implementation of specific activities of

government‘s FMDP. The proposed Financial Sector Development Policy Credit (DPC)

complements these efforts. Sector-specific development policy operations are useful

instrument to support countries with strong commitment to medium-term reform in a specific

sector which require focused attention. This operation also complements Banks efforts to

5 This operation was discussed during CAS consultations and included in the lending pipeline at the Regional

Operations Committee (ROC) stage of the CAS, albeit it was dropped from the final CAS version at the request

of the authorities during the 2010 Spring Meetings. The authorities reversed their decision subsequently and

requested the Bank to resume the preparation of the operation.

Page 17

11

support the development and integration of financial sector in the EAC, notably the EAC

Financial Sector Development and Regionalization project. Finally the operation will benefit

from parallel targeted TA financed by various trust funds, notably supporting the

establishment of the pension regulator.

26. This operation also complements the PRSC series, the main vehicle for Bank’s

budget support in Uganda. PRSC series focus on Government‘s reforms to improve access

to, and greater value for money in, public services. They are being prepared and monitored

jointly with ten other Joint Budget Support (JBS) donors and Government, and place a strong

emphasis on performance-based management through tools such as output-oriented budgeting

and results oriented management. This joint approach reduces Government transaction costs,

increases the predictability of disbursements, and creates mutual accountability. Financial

sector reforms are not covered under the JBS, as authorities and partners have agreed to

circumscribe the scope of this general budget support to four sectors, namely health,

education, transport and water and sanitation for the time being. The authorities consider that

adding specific sectoral reforms to the JBS framework would introduce unnecessary

complexity and would entail the risk of jeopardizing predictability of disbursements in case

progress in the specific sector is slower than anticipated.

LESSONS LEARNED

27. Strong ownership and strengthened capacity of the institutions involved in the

reform are key factors of success. Ensuring ownership at all levels of government, from the

technical to highest level, is essential for reinforcing commitment to achieving development

objectives and facilitating implementation. Complementary technical assistance and capacity

building activities will also be critical.

28. The political economy of reform needs to be taken into account. In designing a

development policy operation, political factors and the legislative needs of the client need to

be understood and included in the dialogue with the client, particularly if the implementation

of the reform program will involve a future administration. In preparing this operation, the

World Bank understood that some of the policy reforms needed, notably with respect to

pension reform, could not be implemented within the current political cycle. The proposed

programmatic approach combines the discipline of a medium-term framework with triggers

for subsequent operations that offer the flexibility to accommodate the unpredictability and

uncertainty of complex policy reforms. This approach would also strengthen the basis for a

continued policy dialogue with the Ugandan authorities to take office in 2011.

29. Ambitious objectives require a pragmatic approach. The deepening of financial

sector and pension reform is a long-term and ambitious goal that involves difficult decisions.

In designing this operation, the World Bank understood that under current constraints, it is

more realistic to focus on institutional development (improving the legal and regulatory

framework and the capacity of the supervisory agencies), and to leave the restructuring of the

pension schemes for a second stage. This would allow building further momentum for

completion on the reform.

Page 18

12

ANALYTICAL UNDERPINNINGS

30. The design of this operation is underpinned by various diagnostic work

completed in recent years. These include World Bank report on Making Finance Work for

Uganda (2009); a consultant report on Development of PPP frameworks in Uganda (2010);

FINSCOPE survey report (2010); a policy note on Reform Options for the Public Service

Pension Fund in Uganda (2011); a review of National Social Security Fund investment

policies (2011); and the Financial Sector Assessment Program (FSAP) (2001) and its first

update (2005). A new update of the FSAP is scheduled to take place in late August 2011; its

outcomes will inform further authorities‘ financial sector reform program and help refine and

identify specific triggers for the subsequent operation under this programmatic series. This

analytical work was fed into policy dialogue and contributed to Government‘s policy

formulation.

V. THE PROPOSED FINANCIAL SECTOR DEVELOPMENT POLICY CREDIT

OPERATION DESCRIPTION

31. The proposed Development Policy Operation for the sum of US$50 million would

be the first in a series of two programmatic single-tranche operations. The proposed

operation will support the implementation and consolidation of Government‘s financial sector

reforms as outlined in the National Development Plan and the Financial Markets

Development Plan for 2008-2012. The programmatic approach defines the medium-term

framework for policy reform while accommodating the unpredictability and uncertainty of

these complex policy reforms.

32. The overarching development objective of the operation will be to help build a

more efficient, robust and deeper financial sector which can support broad-based

private sector growth. The specific reforms supported by the operation will be organized

around two main objectives: (i) supporting the development of the market for term finance;

and (ii) improving access to financial services. Under the first area, the operation would

support the pension system reform, and the strengthening of institutional arrangements for

mobilizing long-term funds, including through Public Private Partnerships and the

development of the housing finance market. Under the second area, measures supported

would seek in particular to improve the lending environment and strengthen payments and

settlement systems. Proposed prior actions for this operation and their current status are

presented in Box 1 at the end of this section; the expected specific results and proposed

triggers for second operation are contained in the policy matrix in Annex 2.

POLICY AREAS

Pillar 1: Supporting the development of market for term finance

(i) Pension System reform

Overview of the pension sector

33. The Ugandan pension system serves a relatively small portion of the population.

For private sector employees, the mandatory fund is the National Social Security Fund

(NSSF). Many private sector employers have also set up occupational schemes to accumulate

Page 19

13

additional pension benefits for their employees. For public sector employees, the scheme is

the Public Service Pension Fund (PSPF). The armed forces have a specific scheme, the benefit

payments of which are administered through PSPF. Workers in formal firms with less than

five employees, self-employed, and informal workers are not covered. The characteristics of

the major pension schemes in Uganda are described in Table 2.

34. The Public Service Pension Fund covers civil servants in both central government

and local authorities. Pensions for traditional civil servants, primary and secondary school

teachers, police officers, prison officers, doctors and public employees in the judiciary are

provided for under the Pensions Act (Cap 281). The Pensions Act also covers civil servants in

local authorities - until 1994 local authorities had their own provident funds established under

the provisions of the Municipalities and Public Authorities Provident Fund (Cap 291). After

the 1994 amendment to the Pensions Act, all local authorities were required to provide

pensions to their workers under the Pensions Act. The Armed Forces is covered under the

Armed Forces Pension Act, 1939, Cap 295 and is partly administered through PSPF.

35. The PSPF is a generous, non-contributory, defined benefit scheme funded by the

budget. The scheme provides for normal retirement age at 60 years with a benefits vesting

period of ten years. The covered population in this scheme is approximately 260,000 and

currently pensions of approximately 130 billion Ugandan shillings per annum are paid. The

scheme has a generous full pension based on gross salary with an accrual factor of 2.4 percent

multiplied by the number of years in service capped at 87 percent of final gross salary. The

scheme rules allow commutation of up to a third of the pension at commutation factors that

are double what is considered to be actuarially fair. Commuted pensions are restored after 15

years. The unique policy of indexing pensions provides a rate of indexation that is higher than

wage indexation. With regard to survivors‘ pension, the pension payable is 100 percent of the

pension entitlement of the deceased public officer. The guaranteed period for the survivors‘

pension is 15 years. The scheme also provides an array of other gratuities such as contract

gratuities, death gratuities, short term gratuities, and marriage gratuities.

36. The Armed Forces Pension Scheme is also a non-contributory defined benefit

scheme. As noted, the benefits payable by the scheme are administered through PSPF. Data

about the active contributors and pensioners is maintained by the Minister of Defense and are

not publicly available.

37. The National Social Security Fund (NSSF) is the compulsory fund for workers in

the formal sector in enterprises with five or more employees other than those persons

employed as teachers or in the Civil Service and Armed Forces. NSSF is a defined

contribution provident fund which is financed by compulsory contributions of 15 percent of

wages divided between employers and employees in the ratio of 2:1. NSSF operates on a

defined contribution basis, that is, as an investment fund where accrued balances can only be

withdrawn at retirement. As such, its assets and liabilities are by definition matched. The fund

does not guarantee a rate of return on the contributions it collects. While there are no explicit

contingent liabilities that would need to be covered by the scheme sponsors or a pension

administrator, if the fund were to face shortfalls the government would most likely have to

step in. The fund has 450,000 active contributors and its total assets stood at UGX 1.6 trillion

(end of June 2010, unaudited), equivalent to about 5 percent of GDP.

Page 20

14

38. The Board of NSSF has recently approved an investment strategy. There are no

counterparty limits or limits to its exposure to particular industries. Assets are currently

structured as following: 30 percent in fixed interest investments; 30 percent in equities; and

40 percent in real estate. The strategy recently approved by the Board is 40 percent fixed

interest, 30 percent equities (both listed and unlisted) and 30 percent real estate. A more

conventional mix would be: cash and bank deposits in the range of 10 to 15 percent; fixed

interest of 25 to 30 percent; equities of 25 to 30 percent and for real estate, a maximum of 20

percent.

Table 2: Ugandan Pension Schemes

National Social

Security Fund

(NSSF)

Occupational

Provident Schemes

Public Service

Pension Fund (PSPF)

Armed Forces

Pension Scheme

Legal

Framework

NSSF Act 1985 Not regulated Pensions Act (CAP

286)

Armed forces pensions

Act (CAP 295)

Specific

Population

Served

All private sector

employees of formal

sector companies with

more than 5 employees

Employees of private

sector firms that elect

to contribute funds in

addition to NSSF

funds

Civil servants (central

government, police and

prison officers,

judiciary, doctors,

primary and secondary

school teachers

Armed forces

Population

covered

About 450,000

members -

About 50-60 schemes,

number of members

unknown

About 228,000 active

members and 32,000

retirees

N/A

Financing of

Benefits

Mandatory

contribution (15% of

gross salary)

Voluntary (generally

employers‘)

contributions

Non-contributory

(budget-financed)

Noncontributory

(budget-financed)

Scheme design Defined contribution Defined contribution

and defined benefit

Defined benefit Defined benefit

Type of Benefit Lump sums Annuities and lump

sums

Annuities and lump

sums

Annuities and lump

sums

Funding status Funded (about UGX

1.3 billion)

Believed to be funded Unfunded Unfunded

39. There are believed to be more than 50 private sector occupational schemes

established by private sector employers. There is currently no consistent practice or

structured regulation for these schemes. Some take the form of provident funds, others are

pension arrangements based upon the final earnings of members and their length of service.

The estimated total asset value of these funds is UGX 120 billion. Most large employers, such

as the Bank of Uganda and the telecommunications companies, operate such schemes. In

addition to the single-employer schemes, there is also one multi-employer pension fund,

organized and operated by an international company.

Challenges for the pension sector reform

40. Several constraints are hampering the development of a mature and well

functioning pension sector. These can be grouped around three dimensions: (i) the overall

pension regulatory framework; (ii) the private pension schemes; and (iii) the public pension

scheme. The Government has started to take concrete steps to address these challenges.

41. There is no comprehensive regulatory framework for the pension sector,

although steps have been taken to address this. Currently, NSSF and PSPF are regulated

Page 21

15

under separate laws. NSSF is governed by a board and reports to the Minister of Finance,

while PSPF is under the direct control of the Ministry of Public Service. A small number of

occupational pension schemes operating as deposit administration funds are subject to the

Insurance Act. The passage of the URBRA Act in April 2011 has provided for the

establishment of a regulatory authority to supervise the whole pension sector. Additionally,

the Retirement Benefits Sector Liberalisation Bill (the Liberalisation Bill) has been introduced

into Parliament. Under the envisaged new regulatory framework, both NSSF and PSPF are

subject to the supervision of the regulatory authority, which is yet to be appointed.

42. The Liberalisation Bill presented to Parliament late April 2011 has significant

gaps. This submission, requested by Parliament to have a broad view of envisaged pension

reform before considering the URBRA, was made before wider consultations had concluded.

The authorities acknowledge that the submitted Liberalisation Bill has significant gaps and

have indicated that these will be addressed at the Parliamentary Committee Stage. The

authorities have requested Bank‘s inputs, as they complete consultations and ensure that gaps

in the Bill are corrected.

43. Government’s commitment to public service and armed forces pension payments

is unsustainable. The government‘s commitment to provide public sector employees pension

benefits through the non-contributory PSPF has resulted in a large contingent liability,

estimated at 63 percent of 2011 GDP at a conservative real discount rate of 5 percent.

Although the Government has embarked on an accelerated amortization of historic arrears,

according to the Ministry of Public Service, new arrears are being accumulated every year due

to under-budgeting of the government's commitments. Data were not provided for members of

the Armed Forces to enable an actuarial evaluation to be undertaken. However, it is certain

that the arrangements for members of the Armed Forces are more unsustainable due to higher

parameters applying to the benefits to these members compared with the Civil Servant and

Teacher groups. The Liberalisation Bill, when passed, will substantially address the issues in

relation to PSPF. Under the proposed Bill, PSPF will become a contributory defined

contribution fund, to which employees in the Civil Service and Teacher groups will contribute

five percent of their wages and the government will contribute 10 percent. The scheme will

be known as the Unified Public Sector Pension Scheme (UPSPS). Existing active members

with fifteen years of service or less will be provided with a redemption bond which is

redeemable at retirement. The current arrangements for active members with more than

fifteen years of service and existing retirees will be grandfathered. The future obligations of

the government will be reduced significantly.

44. Governance issues in National Social Security Fund (NSSF) need to be addressed

durably. Although not directly under government management, the composition, selection,

and rules of accountability of NSSF‘s board make it a de facto publicly managed provident

fund. This kind of structure has often failed in other countries, and NSSF‘s record to date is

certainly less than stellar, with a history of alleged fraud and poor investment decisions related

to shortcomings in its governance structure. The recent independent review of NSSF revealed

a number of issues that need to be resolved, including the valuation practices in relation to

assets for which there is no readily available market price, an inadequate investment strategy

and inequitable practices in crediting scheme earnings to the accounts of individual members.

Further, other available information suggests that there are issues with the internal procedures

of NSSF that have resulted in un-reconciled accounts, lost data and a failure to pay pension

Page 22

16

benefits in a timely fashion. The envisaged new regulatory framework will help address these

issues. The URBRA Act requires that the investment management function needs to be

outsourced to a licensed and qualified investment manager, which cannot be a party related to

the trustees or the administrator of NSSF. The regulator will have the power to set, for all

licensed schemes, regulation and prudential norms, and minimum standards covering

corporate governance, investments, valuation and operations.

45. NSSF’s monopoly over mandatory pensions is hindering the emergence of

alternative schemes. The progressive opening of this market is expected to foster financial

market development, notably with respect to mobilization and allocation of long term fund.

The passage of the Liberalisation Bill will, after a transition period, allow workers to choose

any scheme that is licensed by the regulatory authority in which to make mandatory

contributions. Currently, only a few asset managers have been licensed by the Capital

Markets Authority (CMA) to manage assets of occupational pension schemes. One of these,

African Alliance, has begun to manage and distribute retail investment funds as well. Two

banks (Barclays and Stanbic) provide custody services to these pension funds. The insurance

market, especially life insurance, is also underdeveloped. No annuity products are available

commercially, and the life insurance market consists of group term life policies. There is a

severe shortage of qualified actuaries, which is particularly problematic for the government.

Whereas private sector entities can always find and hire such experts abroad, this constraint is

particularly serious for the Uganda Insurance Commission.

Government’s reform program

46. Pension reform has been at the forefront of public debate and GoU’s agenda for

the past decade. A significant amount of public consultations and analytical work has been

undertaken over that period, ranging from comprehensive approaches embracing broad social

security considerations to more focused analysis for specific schemes. The authorities‘

emerging vision for pension reform emphasizes the capital market development objective,

rather than considerations relating to the provision of adequate, affordable and sustainable

retirement insurance for the Ugandan population.

47. The authorities have adopted a staged approach for pension reform, focusing in

the first steps on the regulatory framework and the two largest pension schemes, NSSF

and PSPF. The passage of the URBRA Act is a major achievement which needs to be

followed by the appointment of the Board and staff to the authority, and activities to make the

authority functional. Trust fund resources have been provided to assist with the set-up of the

authority. The next stage in the reform process is to pass the Liberalisation Bill, which will

ensure that PSPF is made contributory and becomes more financially sustainable and provide

for the progressive introduction of competition in the pension sector. Table 3 presents the

planned sequencing of pension reform; all actions under stage one have been completed.

Specific measures to be undertaken as part of the proposed operation

48. This first operation will support the initial stage of pension reform. The following

prior actions have been agreed with the authorities and have been completed: (i) the conduct

of an independent review of NSSF investment policies and practices; (ii) the conduct of an

Page 23

17

actuarial evaluation and simulation of reform options for the PSPF; (iii) submission of

URBRA Bill to Parliament.

Indicative measures for the preparation of the second operation

49. The second operation would support actions indentified in the second stage of

pension reform sequence. The set of possible triggers for the second operation would

include: address gaps in Liberalisation Bill introduced to Parliament before it is enacted;

appoint URBRA Board and staff; URBRA to adopt regulations, prudential norms and

guidelines; license NSSF; and Cabinet to approve policy paper on PSPF reform.

Expected results

50. The overarching objective of the actions supported in this area is the emergence

of a regulated, competitive and sustainable pension industry catering for both

mandatory and voluntary pension savings. This overall objective will require an effective,

well resourced and efficient regulator, and the transition of the public sector schemes towards

a sustainable scheme.

Table 3: Sequencing of actions for pension reform

Stage Regulatory Authority NSSF PSPF Occupational

Schemes

Other

1 Submit URBRA Bill to

Parliament

Assess NSSF

Investment policies

and Practices

Undertake actuarial

evaluation and

simulation of

reform options

2 Appoint URBRA and

assist in resourcing the

agency

Prepare regulations

prudential standards and

by laws

Adopt internal policies

and procedures

Conduct training

Commence licensing

License NSSF Take Policy

decision on options

for reforms

Appoint trustees to

PSPF

License PSPF

URBRA to review

OPS identified and

license where

warranted

Address gaps

in

Liberalisation

Bill introduced

in Parliament

Enact

Liberalization

Bill

(ii) Developing housing finance market

Overview of housing finance market

51. Uganda mortgage market is relatively small and underdeveloped. Mortgage debt

to GDP stands at some 1 percent (2007). Based on the incomes of 5.2 million households in

the country, only 0.6 percent would theoretically be able to access mortgage loans through

commercial banks, while 19.9 percent of households could access a housing microfinance

Page 24

18

loan through microfinance deposit taking institutions, 7.2 percent could access loans from

microfinance institutions and savings and credit cooperatives, 10.3 percent access loans from

a savings and credit cooperatives only, and 62.3 percent would not have a sufficient level of

income to access any form of housing finance under the current system.

52. The range of mortgage products is varied. They are typically offered for up to 20

years to maturity and at variable rates. Interest rates are still relatively high at between 16 and

18 percent. Loans are available for construction, for house purchase, for incremental

construction (10-year loan only and for shorter term, less than 10 years) and equity release

mortgages. Land loans are also available with a maturity of just four years and a rate of 20

percent. Finally, buy-to-let loans are also available, which allow prospective landlords to

invest in rental properties.

53. Housing demand is growing and a large housing gap exists. Uganda has a very low

level of urbanization of just 13 percent compared to an African average of 40 percent. The

annual housing need is around 200,000 units with 80 percent of this required in rural areas.

This does not take account of the housing backlog which has accumulated over the years. The

pattern of housing demand is expected to shift gradually as urbanization accelerates. The

formal housing construction sector could contribute significantly to closing this gap if it were

able to better service groups further down the income distribution scale. Housing supply is

increasing but still lags behind demand. The growing urbanization and rising cost of land has

resulted in a drop of owner occupancy rate. In rural areas, however, the home ownership rate

is still around 90 percent.

54. The market is responding to this growing demand. New real estate developers have

entered the market, including some developers backed by foreign capital. These developers

vary in size and are mainly focused on the high end spectrum of the market, but are expected

to enter the other segments as the market expands. The banks are also responding and getting

involved in mortgage business. Some banks, including the Housing Finance Bank have issued

corporate bonds to finance their mortgage activities. Finally, the supply response also comes

from microfinance institutions, with the introduction of new housing microfinance products

(e.g. small loans targeted at incremental construction without the need for collateral), albeit

further development is constrained by BoU regulations limiting the lending tenure to five

years.

Challenges

55. Obstacles for housing finance development are present at every stage of the

lending process, from obtaining collateral, registration process, obtaining long-term funding,

assessing credit risk, and foreclosure process.

56. There are some legal and regulatory constraints related to the implementation of

the new Mortgage Act and uncertainties regarding the Land Act Amendment Bill. The

implementation of the Mortgage Act is pending the adoption of regulations. Discussions about

the Land Act Amendment Bill are highly sensitive and it is critical that the outcome is reached

by high level of consensus and establishes transparent and fair processes to resolve claims.

Page 25

19

57. There are also important information constraints, notably slow and unreliable

property registration, and difficulties to assess credit risk.

58. Finally there are a set of constraints on the housing supply side, with high cost of

infrastructure for development, few credible developers and builders, and limited large-scale

development.

Government actions

59. Government has acknowledged these constraints and taken action to start

addressing them. The first important step was the enactment of the Mortgage Act in October

2009, which consolidates the laws relating to mortgages, revamps the mortgage industry and

harmonizes it with the Land Act. The regulations to facilitate implementation of the Mortgage

Act have being prepared and are ready for signature. To increase the flow of investment into

housing and encourage development of large scale, well planned residential areas, the

Government has decided to provide fiscal incentives and reduced the Value Added Tax rate

charged on housing from 18 percent to 5 percent. Government has also started addressing the

information constraints, notably through the implementation of the Land Information System

(LIS), and the Rehabilitation and re-opening of the Survey School in Entebbe. The LIS will

help speed up and secure property title registration. The establishment of the Credit Reference

Bureau will also contribute to improve information gaps.

60. The Government is committed to further actions in the housing sector. At the

policy level, the immediate priority areas of reform include: resolving issues associated with

the Land Amendment Act to clarify ownership issues with a view to facilitating land

development in general and housing finance in particular; and strengthening consumer

protection rules. At institutional level, the reforms will focus on: strengthening the capacity

of the Chief Government Valuer; improving knowledge and information flow about mortgage

lending including in the Judiciary; supporting the development of professional bodies in the

sector; and strengthening the technical capacity of housing lending institutions.

Specific measures supported under this operation

61. This operation will support government’s effort to implement the Mortgage Act.

The Act consolidates the laws relating to mortgages and will be instrumental in revamping the

mortgage industry. The act addresses key uncertainties which were hampering further

resources commitments in mortgage products. Most notably, it addresses clauses that could

give courts unilateral rights to change mortgage contract terms for a borrower in default. With

respect to the length of mortgage foreclosure process, until the new law is tested through the

courts, it is difficult to fully know the impact on the time and cost of foreclosing on a

property. The Act as passed will double the time between serving a notice of default and being

able to take further action (from 21 to 45 days), however, the Act provides for a strong power

of sale mechanism which should make foreclosure a straightforward process. The key priority

now, to be supported under this operation, is to prepare the necessary regulations for the act

and to begin implementation. The prior action retained for this operation is to put in force the

Mortgage Act regulations.

Page 26

20

Indicative measures for the preparation of the second operation

62. The set of possible triggers for the second operation under this area could

include: the revision of valuation policy and procedures; establish a Mortgage Market

Development Committee tasked with the setting up of a liquidity facility; and further

issuance of long term bonds. The current difficulties and delays in property registration are

largely attributed to the requirement that every transaction needs to be independently valued

by the Government Value‘s Office for the purposes of levying stamp duty. The authorities

could consider the introduction of the transactional value for tax purposes, with adequate

safeguards to prevent under declaration of value. The introduction of a liquidity facility would

allow banks to overcome some of the maturity issues and provide investors – including

pension funds – with a supply of simple bonds yielding a better return than treasury bills

without a significant increase in risk. This ―liquidity safety net‖ for banks would allow lenders

to engage in higher levels of maturity transformation. Finally, the introduction of longer term

Government bonds would help build sufficient liquidity in long–term debt to get pricing

points for a long term yield curve, hence providing the market with a price for longer term

funds.

Expected results

63. The measures under this area will contribute are expected to improve confidence

in the mortgage market and foster mortgage market growth.

(iii) Developing Public Private Partnership framework for infrastructure financing

Overview

64. Uganda has had a generally positive experience with PPPs. They have been used

to manage existing Government assets and provide infrastructure services as part of Uganda‘s

Privatization and Utility Sector Reform Program (PUSRP), a program supporting the

implementation of the Public Enterprise Reform and Divestiture (PERD) policy and Act.

These PPPs, such as the electricity distribution and railway concessions, were implemented

under a relatively well-defined institutional structure and set of rules. The Government has

also used PPPs to develop new assets, particularly in the energy sector. These have been more

ad hoc, and in some cases driven by unsolicited bids.

Challenges

65. The framework under which these projects have been developed does not apply

to the majority of the potential PPP pipeline. The poorly-defined current PPP framework is

likely to restrict further development of the PPP pipeline for providing new assets and

services. Without a coherent policy structure, line ministries and entities not already familiar

with the PPP concept—which includes much of Government—lack both the understanding of

PPP and the mandate to pursue PPP in their infrastructure development planning. In turn,

developing and transacting projects is slow and inefficient without a basic level of in-house

capacity in structuring deals, and defined responsibilities and procedures to coordinate the

process. Integrating PPP development and assessment with existing public financial

management processes will be important, to ensure the use of PPP does not create a route

around the budget process, debt or fiscal targets.

Page 27

21

Government’s reform program

66. The GoU recognizes that PPP can make an important contribution to the

development of infrastructure facilities and services in Uganda and is committed to

promoting its use. In March 2010, the GoU approved PPP framework which defines the

extent, objectives, and guiding principles of its PPP program. The key objectives of the policy

are: to establish an enabling environment that will foster investment in public infrastructure

and related services; to encourage private sector investment and participation in public

infrastructure and related services; to streamline PPP procurement process; and to articulate

accountability of outcomes. The adopted PPP policy is based on the following core principles:

(i) value for money; (ii) public interest; (iii) risk sharing; (iv) output oriented; (v)

transparency; (vi) accountability; and (vii) competitive bidding process.

67. The GoU has developed a detailed road map to implement Cabinet decision. Key

milestones ahead include: the drafting of PPP Bill and submission to Cabinet; the

establishment of PPP unit (on a non statutory basis until PPP Bill is enacted) with core staff

already familiar with PPP policy; and the preparation and adoption regulations and procedures

for developing and implementing PPPs in congruency with the PPP Bill. The draft Bill was

submitted to Cabinet, albeit it has been returned for revision and will be resubmitted. The

successful implementation of this PPP framework will also hinge on the identification and

selection of pipeline of viable projects. The authorities have started developing a pipeline of

priority projects with support from donors, including through the Public Private Infrastructure

Advisory Facility.

Specific measures supported under this operation

68. This operation will support the adoption of PPP policy, the establishment of the